emerging trends in real estate 2014 highly regarded and widely read 35th annual outlook based on...

TRANSCRIPT

Emerging Trends in Real Estate 2014

• Highly regarded and widely read

• 35th annual outlook

• Based on over 1,000 interviews and surveys of industry leaders

• Sponsored by PwC and the Urban Land Institute

• Investment and development trends

• Capital markets

• Metro areas

• Property sectors

Fundamentals continue to improve…slowly… across all property groups and property markets

Development is back, and 2014 will likely be the last year when minimal new supply is delivered

Reaching an inflection point where valuations will be driven by fundamentals, not capital markets

Interest rates anticipated to increase; it’s the pace and magnitude of the increase that is uncertain

Capital goes wide, in more markets and taking on more risk

Gaining Momentum

Investment Prospects by Asset Class

Investment-grade bonds

Commercial mortgage backed securities

Publicly listed equities

Publicly listed property companies or REITS

Publicly listed homebuilders

Private direct real estate investments

1 2 3 4 5 6 7 8 9

4.62

4.96

5.49

5.57

5.78

6.43

2014 2013 2012 2011

Source: Emerging Trends in Real Estate surveys

Abysmal Fair Excellent

2005 2006 2007 2008 2009 2010 2011 2012 2013 20140

1

2

3

4

5

6

7

8

9

5.05.4 5.4 5.3

4.74.3

4.6

5.35.6 5.8

Investment Prospects: Average Market ScoreInvestment Prospects

Excellent

Fair

Poor

Source: Emerging Trends in Real Estate surveys

Issues of importance for real estateEconomic/Financial Issues

none moderate great

Source: Emerging Trends in Real Estate 2014 surveyNote: Based on US respondents only

Federal fiscal deficits/imbalances

Global economic growth

Tax policies

Inflation

Income and wage growth

Interest rates

Job growth

0 1 2 3 4 5

3.50

3.60

3.61

3.68

4.11

4.46

4.63

Issues of importance for real estateReal Estate/Development Issues

none moderate great

Source: Emerging Trends in Real Estate 2014 surveyNote: Based on US respondents only

Infrastructure funding/development

Future home prices

Refinancing

Land costs

Vacancy Rates

Construction costs

0 1 2 3 4 5

3.58

3.58

3.59

3.85

3.99

4.03

“2014 should be a year when we see real estate fundamentals improve in sectors beyond the very healthy multifamily sector—and in a number of markets—to a point where we could see above-inflation-rate rental growth”

A “stubbornly high” unemployment rate

Uncertainty over government regulation and fiscal policy

Likely increase in the cost of both equity and debt capital

Economic uncertainty in the Euro-zone

China’s moderating economic growth

Headwinds Facing the Real Estate Industry

“Good if not great” job growth in industries with high real estate utilization including: energy, technology, health care, medical research, education, and financial services

Increasing corporate profits

Continuing recovery in the single-family housing industry

Historically low interest rates currently

Tailwinds Benefiting the Real Estate Industry

Industry profitability expected to continue to improve

Interest rates anticipated to increase

Dependence on cap rate compression to drive value to be replaced by rent growth and vacancy declines

Markets are expected to be “well supplied” with both equity and debt capital

Emerging Trends: Key Trends/Drivers for 2014

Opportunities to develop property finally appear in sectors other than multifamily

Industry begins to understand changing needs of both Gen Y and the baby boomers

Needs of end users of commercial space continue to evolve

The single family housing market continues to make a positive contribution to the overall economy

Emerging Trends: Key Trends/Drivers for 2014

Prospects for profitability by percentage of respondents

2010 2011 2012 2013 20140%

10%

20%

30%

40%

50%

60%

70%

80%

Abysmal to Poor

Modestly Poor to Modestly Good

Good to Excellent

Source: Emerging Trends in Real Estate surveysNote: Based on US respondents only

Capital markets

Prospects by Investment Category/Strategy

Distressed Debt

Distressed Properties

Core Investments

Core-plus Investments

Opportunistic Investments

Development

Value-added Investments

0 1 2 3 4 5 6 7 8 9

4.80

4.99

5.53

5.95

6.13

6.15

6.32

Abysmal Fair ExcellentSource: Emerging Trends in Real Estate 2014 survey

Note: Based on US respondents only

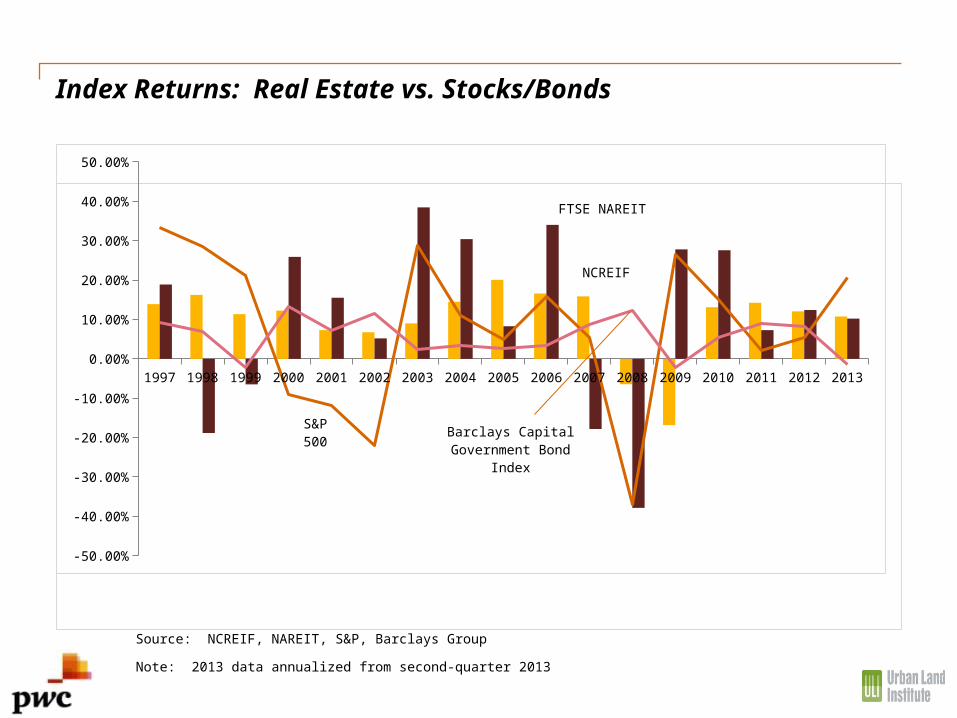

Index Returns: Real Estate vs. Stocks/Bonds

1997 1998 1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013

-50.00%

-40.00%

-30.00%

-20.00%

-10.00%

0.00%

10.00%

20.00%

30.00%

40.00%

50.00%

FTSE NAREIT

NCREIF

S&P 500 Barclays Capital Gov-

ernment Bond Index

Source: NCREIF, NAREIT, S&P, Barclays Group

Note: 2013 data annualized from second-quarter 2013

NCREIF Cap Rates vs. U.S. Ten-Year Treasury Yields

Source: NCREIF, Moody’s Analytics, Federal Reserve Board

*Ten-year Treasury yields based on average of the quarter, 2013Q2 average is as of July 2013

Note: Cap rate based on four-quarter moving average of current-value cap rate

1990

Q1

1990

Q4

1991

Q3

1992

Q2

1993

Q1

1993

Q4

1994

Q3

1995

Q2

1996

Q1

1996

Q4

1997

Q3

1998

Q2

1999

Q1

1999

Q4

2000

Q3

2001

Q2

2002

Q1

2002

Q4

2003

Q3

2004

Q2

2005

Q1

2005

Q4

2006

Q3

2007

Q2

2008

Q1

2008

Q4

2009

Q3

2010

Q2

2011

Q1

2011

Q4

2012

Q3

2013

Q2

-4.00%

-2.00%

0.00%

2.00%

4.00%

6.00%

8.00%

10.00%

12.00%

Cap Rate

10-Year Treasury*

Spread

Equity and Debt Capital Balance Outlook

Substantially undersupplied

Moderately undersupplied

In balance

Modestly oversupplied

Substantially oversupplied

4.4%

26.0%

43.4%

23.5%

2.7%

1.8%

17.1%

26.9%

40.5%

13.7%

Equity capital for investing Debt capital for acquisitionsSource: Emerging Trends in Real Estate 2014 surveyNote: Based on US respondents only

Debt capital for development and refinancing

Substantially under-supplied

Moderately undersupplied

In balance

Modestly oversupplied

Substantially oversupplied

3.1%

24.1%

52.2%

17.2%

3.4%

15.9%

42.9%

30.2%

10.4%

0.7%

Debt capital for development Debt capital for refinancing

Source: Emerging Trends in Real Estate 2014 surveyNote: Based on US respondents only

Debt Underwriting Standards Forecast

2011

2012

2013

2014

29.8%

33.0%

39.1%

17.4%

29.2%

35.1%

41.5%

39.4%

41.0%

31.9%

19.4%

43.3%

More rigorous Remain the same Less rigorous

Source: Emerging Trends in Real Estate 2014 surveyNote: Based on US respondents only

Emerging trends barometer 2014

2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014

Buy

SellHold

Source: Emerging Trends in Real Estate surveysNote: Based on US respondents only

Excellent

Poor

Fair

Abysmal

Good

Change in Availability of Equity Capital for Real Estate

Public Equity REITs

Private REITs

Private Local Investors

Private Equity/Opportunity/Hedge Funds

Institutional Investors/Pension Funds

Foreign Investors

0 1 2 3 4 5 6 7 8 9

5.38

5.70

6.00

6.12

6.18

6.43

Very large decline Stay the Same Very large increase

Equity source

Source: Emerging Trends in Real Estate 2014 surveyNote: Based on US respondents only

Change in Availability of Debt Capital for Real Estate

Government Sponsored Enterprises

Mortgage REITs

Non-Bank Financial Institutions

Mezzanine Lenders

Insurance Companies

Commercial Banks

Securitized Lenders/CMBS

0 1 2 3 4 5 6 7 8 9

4.55

5.54

5.95

6.00

6.03

6.12

6.24

Very large decline Stay the Same Very large increase

Lending source

Source: Emerging Trends in Real Estate 2014 surveyNote: Based on US respondents only

CMBS Revival Continues

CMBS 2013 issuance expected to exceed $80 billion

CMBS 2014 issuance anticipated to exceed $100 billion

CMBS lenders continue to fill the gaps left by conventional lenders in terms of:

--deal size (under $25 million) and

--property location (secondary versus solely primary locations)

Commercial Banks

Regional and local banks are expected to become increasingly active as their balance sheets improve

National banks, searching for opportunities, will increasingly compete on a regional and local basis

Development and construction loans will become increasingly available for borrowers with strong credentials and track records, and with substantial pre-leasing

1991

1991

1992

1993

19

9419

94

1995

1996

19

9719

97

1998

1999

20

0020

00

2001

2002

20

0320

03

2004

2005

20

0620

06

2007

2008

20

0920

09

2010

2011

20

122,

012

0%

2%

4%

6%

8%

10%

12%

14%

16%

18%

Construction and development loans noncurrent rate

Multifamily mortgages noncurrent rate

Commercial mortgages noncurrent rate

Bank Real Estate Loan Delinquency Rates

Source: Federal Deposit Insurance Corp.

Note: Delinquent loans defined her as those that are noncurrent, either 90 days or more past due or in noncurrent status

*as of second quarter 2013

1990

1990

1991

1992

1993

1993

1994

1995

1996

1996

1997

1998

1999

1999

2000

2001

2002

2002

2003

2004

2005

2005

2006

2007

2008

2008

2009

2010

2011

2011

2012

2013

0

1

2

3

4

5

6

7

8

Delinquency

Life insurers mortgage delinquency rates

Source: Moody’s Analytics, American Council of Life Insurers

In-foreclosure

%

Mezzanine Financing

Interviewees and survey participants seem of two minds regarding the roll of mezzanine financing in 2014

Some interviewees predict an “increase in B-piece, mezzanine, and debt funds to fill gaps in transaction structure” and “an increase in the use of mezzanine financing combined with higher-cost senior debt.”

“The biggest question on mezzanine is where the returns are going to be. If mezzanine rates don’t increase enough and we don’t feel we’re getting paid enough, we’ll stop. At a 200 [basis point] difference, we don’t think we’re getting paid for the risk.”

Markets to watch

More markets begin to look attractive

Growing Strength Across Many Metro Areas

Investment Prospects Development Prospects Homebuilding Prospects0%

10%

20%

30%

40%

50%

60%

70%

41%

16%

6%

57%

39%

28%

65%

47%

59%

Percent of markets ranked moderately good or better

201220132014

Source: Emerging Trends in Real Estate 2014 surveyNote: Based on US respondents only

1. San Francisco

2. Houston

3. San Jose

4. New York

5. Dallas/Ft. Worth

6. Seattle

7. Austin

8. Miami

9. Boston

10. Orange County, CA

7.0

7.0

6.8

6.8

6.8

6.8

6.7

6.6

6.6

6.6

6.9

6.6

6.7

6.6

6.4

6.4

6.3

6.4

6.4

6.2

7.7

7.5

7.4

7.2

7.4

7.2

7.3

7.1

6.9

6.9

Top 10 total rank2014

Investment Development Homebuilding

Source: Emerging Trends in Real Estate 2014 surveyNote: Based on US respondents only

11. Denver

12. Nashville

13. Los Angeles

14. San Antonio

15. San Diego

16. Charlotte

17. Raleigh/Durham

18. Salt Lake City

19. Portland, OR

20. Minneapolis/St. Paul

6.5

6.5

6.5

6.3

6.5

6.4

6.3

6.4

6.5

6.3

6.1

6.2

6.2

6.1

5.9

5.9

5.9

6.0

5.9

6.3

6.8

6.8

6.7

6.8

6.7

6.8

6.8

6.5

6.3

5.9

Next 10 markets2014

Investment Development Homebuilding

Source: Emerging Trends in Real Estate 2014 surveyNote: Based on US respondents only

Outlook improves for more markets

Markets with Investment Prospects of Good or Better

2011 2012 2013 2014

New York City Austin Austin Austin

Washington D.C. Boston Boston Boston

New York City Houston Dallas/Ft. Worth

San Francisco New York City Houston

San Jose San Francisco Miami

Seattle San Jose New York City

Washington D.C. Seattle Orange County

Portland

San Francisco

San Jose

Seattle

Changing positions Best and worst

Las V

egas

Sacram

ento

Atla

nta

Inla

nd E

mpir

e

Phoenix

St. L

ouis

India

napolis

Tam

pa/S

t. P

etersburg

Nashville

San A

ntonio

Alb

uquerque

Milw

aukee

Balt

imore

Rale

igh/D

urham

Honolu

lu/H

aw

aii

Vir

gin

ia B

each/N

orfolk

Westchester/F

air

field

Okla

hom

a C

ity

Northern N

ew

Jersey

Washin

gton, D

C

-15

-10

-5

0

5

10

15

20

Rank Change from 2013

Position change

Source: Emerging Trends in Real Estate surveysNote: Based on US respondents only

The impact of uncertainty and new supplyfor Washington, DC

2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 20140.00

1.00

2.00

3.00

4.00

5.00

6.00

7.00

8.00

9.00

0

5

10

15

20

25

30

Rank Score

The outlook for Washington, DC succumbs to fed fatigue

Market Rank

Investment Score

Excellent

Fair

Poor

Source: Emerging Trends in Real Estate surveysNote: Based on US respondents only

Top 10 investment markets

2014 2013 Rank Change

1. Houston 7.00 6.84 +4

2. San Francisco 6.98 7.21 -1

3. New York 6.84 7.14 -1

4. Seattle 6.83 6.72 +2

5. San Jose 6.78 6.89 -2

6. Dallas/ Fort Worth 6.76 6.47 +4

7. Austin 6.69 6.71 -

8. Boston 6.64 6.85 -4

9. Orange County, CA

6.60 6.48 -

10. Miami 6.57 6.47 +1

Top 10 development markets

2014 2013 Rank Change

1. San Francisco 6.88 6.87 -

2. San Jose 6.75 6.58 +1

3. Houston 6.64 6.36 +2

4. New York 6.58 6.76 -2

5. Miami 6.38 5.89 +6

6. Dallas/Fort Worth 6.37 6.20 +1

7. Seattle 6.36 6.13 -1

8. Boston 6.35 6.31 -29. Minneapolis/St. Paul

6.27 5.06 +16

10. Austin 6.25 6.40 -6

Source: Emerging Trends in Real Estate 2014 surveyNote: Based on US respondents only

Top 10 homebuilding markets

2014 2013 Rank Change

1. San Francisco 7.74 6.80 -

2. Houston 7.48 6.15 +4

3. San Jose 7.40 6.58 -1

4. Dallas/Fort Worth 7.36 5.86 +6

5. Austin 7.34 6.26 -

6. New York 7.19 6.42 -3

7. Seattle 7.19 6.14 -

8. Miami 7.06 5.44 +8

9. Boston 6.87 6.05 -1

10. Orange County, CA 6.85 5.91 -1

Source: Emerging Trends in Real Estate 2014 surveyNote: Based on US respondents only

Markets: 2014 emerging trendsMarkets: 2

East coast

Boston 6.6

Washington DC5.9

New York 6.8

Providence 4.3

Pittsburgh 5.5

Philadelphia 5.6

Northern NJ 5.9

Westchester/Fairfield, CT 5.5

Baltimore 5.1

West coast

Seattle 6.8

San Francisco 7.0

Los Angeles 6.5

Portland 6.5

San Jose 6.8

Sacramento 5.0

Inland Empire 5.9

Orange County 6.6San Diego 6.5

Honolulu 5.7

Southwest

Las Vegas 5.5

Phoenix 6.1

Tucson 5.1

Albuquerque 4.6

Oklahoma City 4.8

Denver 6.5

Dallas 6.8

Houston 7.0

Austin 6.7

San Antonia 6.3

Salt Lake City 6.4

Southeast

Atlanta 6.1

New Orleans 4.5

Charlotte 6.4

Raleigh/Durham 6.3

Nashville 6.5 Memphis 4.5

Virginia Beach/Norfolk 5.2

Florida

Miami 6.6

Jacksonville 5.0

Tampa 6.0

Orlando 5.9

Midwest

Minneapolis 6.3

Kansas City 5.3

St. Louis 5.2

Chicago 6.1

Indianapolis 5.3

Cincinnati 5.0

Columbus 4.9

Cleveland 4.2

Milwaukee 4.8 Detroit 3.1

Property type outlook

Industrial leads the pack

Industrial takes the top spot

Retail

Office

Apartment Residential (Rental)

Hotels

Industrial/Distribution

0.00 1.00 2.00 3.00 4.00 5.00 6.00 7.00 8.00 9.00

5.72

5.76

6.14

6.23

6.45

Investment Prospects for major commercial property types

Source: Emerging Trends in Real Estate 2014 surveyNote: Based on US respondents only

Abysmal Fair Excellent

Subsector outlook shows diversity of recovery

Suburban Office

Regional Malls

Apartment Rental--high-income

Central City Office

Limited-Service Hotels

Warehouse Industrial

0.00 1.00 2.00 3.00 4.00 5.00 6.00 7.00 8.00 9.00

4.93

4.95

5.29

5.72

5.92

6.00

6.08

6.11

6.17

6.30

6.56

Investments prospects for commercial subsectors in 2014

Source: Emerging Trends in Real Estate 2014 surveyNote: Based on US respondents only

Abysmal Fair Excellent

Commercial development begins to look up

Office

Retail

Hotels

Apartment Residential (Rental)

Industrial/Distribution

0 1 2 3 4 5 6 7 8 9

4.58

4.63

5.31

5.52

6.74

Prospects for major commercial property types in 2014

Source: Emerging Trends in Real Estate 2014 surveyNote: Based on US respondents only

Abysmal Fair Excellent

Development prospects reflect where market is strongest

Regional Malls

Suburban Office

Power Centers

Full-Service Hotels

R&D Industrial

Central City Office

Neigh./Community Shopping Ctrs.

Limited-Service Hotels

Apartment Rental--moderate-income

Apartment Rental--high-income

Warehouse Industrial

0 1 2 3 4 5 6 7 8 9

3.43

3.55

3.92

4.96

5.11

5.14

5.23

5.52

6.00

6.25

6.44

Prospects for commercial subsectors in 2014

Source: Emerging Trends in Real Estate 2014 surveyNote: Based on US respondents only

Abysmal Fair Excellent