employee fringe benefits and sect. 409a deferred...

TRANSCRIPT

Employee Fringe Benefits and Sect.

409A Deferred Compensation: Tax Issues Evaluating Exclusions or Potential Federal Taxability

Today’s faculty features:

1pm Eastern | 12pm Central | 11am Mountain | 10am Pacific

Please refer to the instructions emailed to the registrant for the dial-in information.

Attendees can still view the presentation slides online. If you have any questions, please

contact Customer Service at 1-800-926-7926 ext. 10.

WEDNESDAY, JUNE 12, 2013

Presenting a live 110-minute teleconference with interactive Q&A

Tara Silver-Malyska, Tax Principal, UHY Advisors, Dallas

James Davis, Shareholder and Chairman, Tax Practice Group, Gunster, Fort Lauderdale, Fla.

Stefan Smith, Partner, Locke Lord, Dallas

Cynthia A. Moore, Member, Dickinson Wright, Troy, Mich.

For this program, attendees must listen to the audio over the telephone.

Tips for Optimal Quality

Sound Quality

Call in on the telephone by dialing 1-866-873-1442 and enter your PIN when

prompted.

If you have any difficulties during the call, press *0 for assistance. You may also

send us a chat or e-mail [email protected] immediately so we can address

the problem.

Viewing Quality

To maximize your screen, press the F11 key on your keyboard. To exit full screen,

press the F11 key again.

Continuing Education Credits

Attendees must stay on the line throughout the program, including the Q & A

session, in order to qualify for full continuing education credits. Strafford is

required to monitor attendance.

Record verification codes presented throughout the seminar. If you have not

printed out the “Official Record of Attendance,” please print it now (see

“Handouts” tab in “Conference Materials” box on left-hand side of your computer

screen). To earn Continuing Education credits, you must write down the

verification codes in the corresponding spaces found on the Official Record of

Attendance form.

Please refer to the instructions emailed to the registrant for additional

information. If you have any questions, please contact Customer Service

at 1-800-926-7926 ext. 10.

FOR LIVE EVENT ONLY

Program Materials

If you have not printed the conference materials for this program, please

complete the following steps:

• Click on the + sign next to “Conference Materials” in the middle of the left-

hand column on your screen.

• Click on the tab labeled “Handouts” that appears, and there you will see a

PDF of the slides and the Official Record of Attendance for today's program.

• Double-click on the PDF and a separate page will open.

• Print the slides by clicking on the printer icon.

Employee Fringe Benefits and Sect. 409A Deferred Compensation: Tax Issues Seminar

Tara Silver-Malyska, UHY Advisors

James Davis, Gunster

June 12, 2013

Cynthia A. Moore, Dickinson Wright

Stefan Smith, Locke Lord

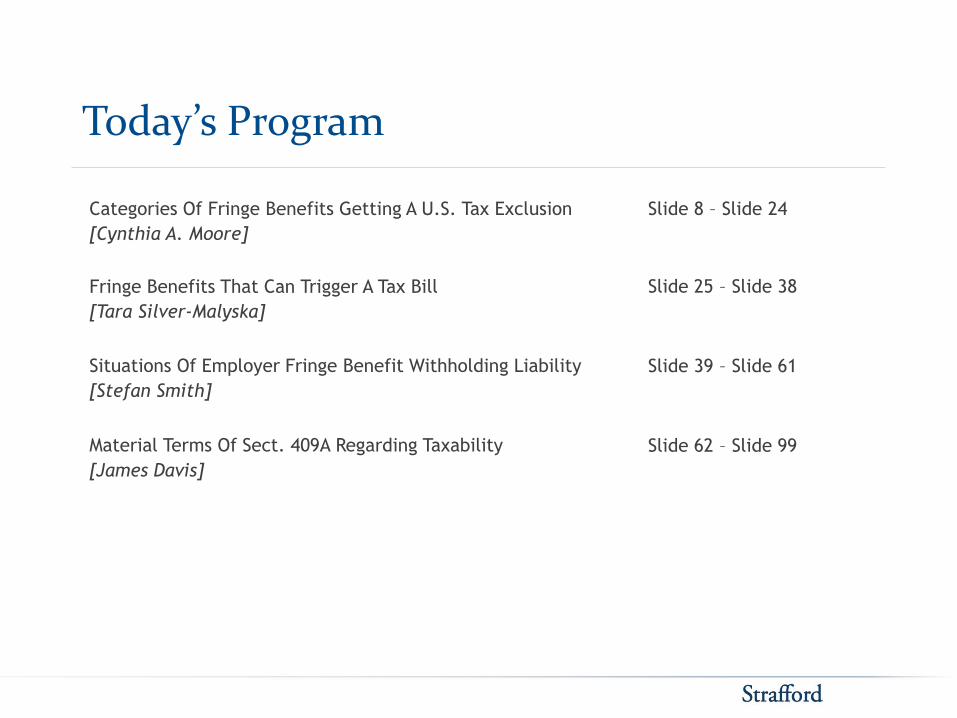

Today’s Program

Categories Of Fringe Benefits Getting A U.S. Tax Exclusion

[Cynthia A. Moore]

Fringe Benefits That Can Trigger A Tax Bill

[Tara Silver-Malyska]

Situations Of Employer Fringe Benefit Withholding Liability

[Stefan Smith]

Material Terms Of Sect. 409A Regarding Taxability

[James Davis]

Slide 8 – Slide 24

Slide 62 – Slide 99

Slide 25 – Slide 38

Slide 39 – Slide 61

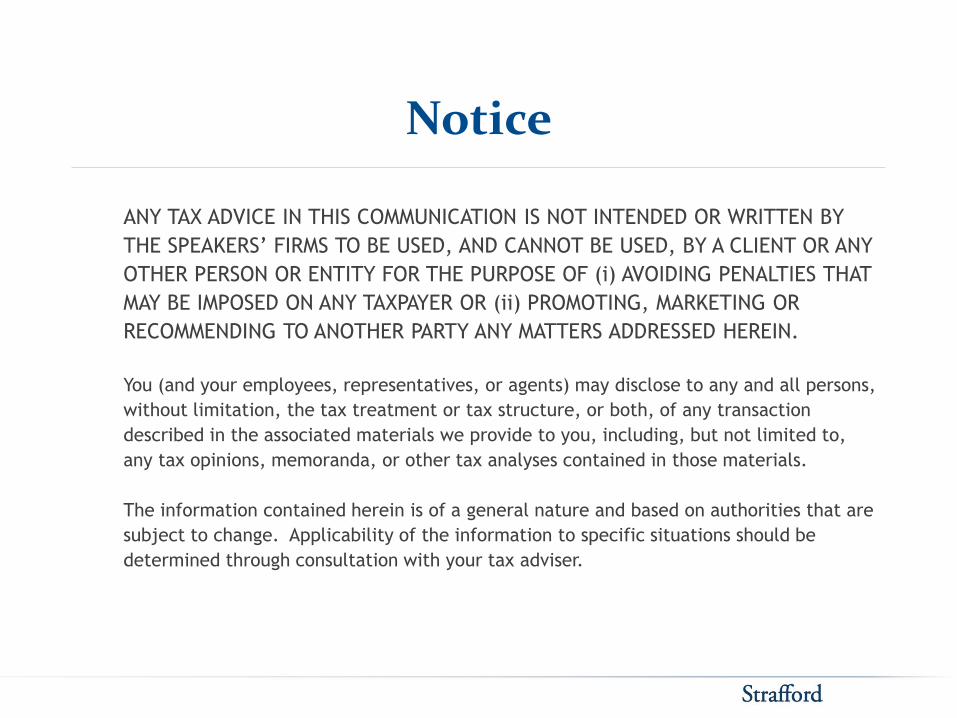

Notice

ANY TAX ADVICE IN THIS COMMUNICATION IS NOT INTENDED OR WRITTEN BY

THE SPEAKERS’ FIRMS TO BE USED, AND CANNOT BE USED, BY A CLIENT OR ANY

OTHER PERSON OR ENTITY FOR THE PURPOSE OF (i) AVOIDING PENALTIES THAT

MAY BE IMPOSED ON ANY TAXPAYER OR (ii) PROMOTING, MARKETING OR

RECOMMENDING TO ANOTHER PARTY ANY MATTERS ADDRESSED HEREIN.

You (and your employees, representatives, or agents) may disclose to any and all persons,

without limitation, the tax treatment or tax structure, or both, of any transaction

described in the associated materials we provide to you, including, but not limited to,

any tax opinions, memoranda, or other tax analyses contained in those materials.

The information contained herein is of a general nature and based on authorities that are

subject to change. Applicability of the information to specific situations should be

determined through consultation with your tax adviser.

CATEGORIES OF FRINGE BENEFITS GETTING A U.S. TAX EXCLUSION

Cynthia A. Moore, Dickinson Wright

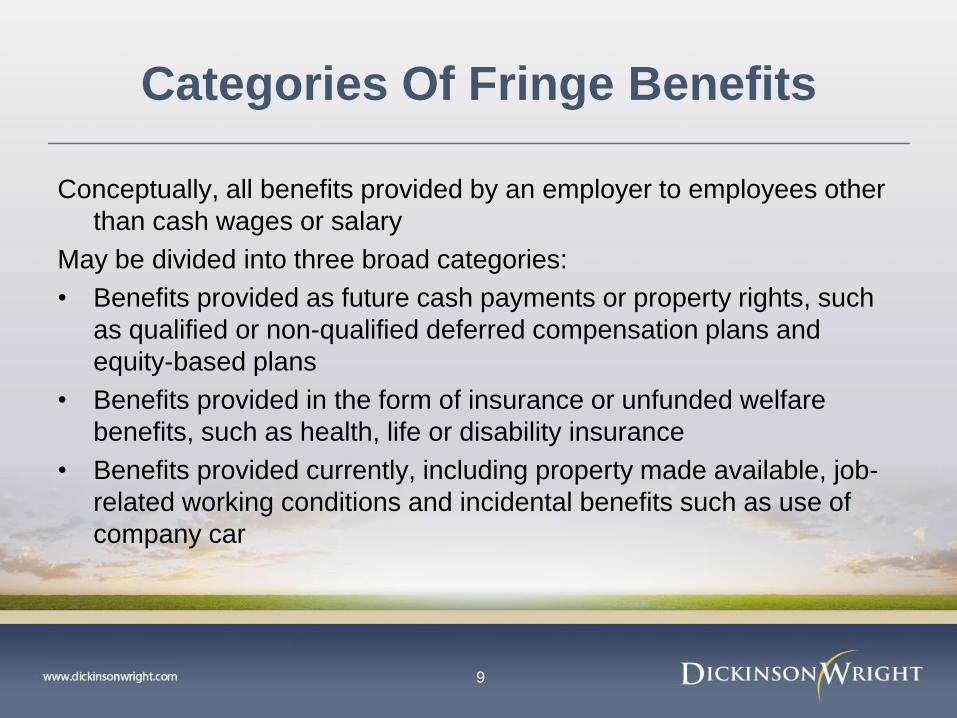

Categories Of Fringe Benefits

Conceptually, all benefits provided by an employer to employees other

than cash wages or salary

May be divided into three broad categories:

• Benefits provided as future cash payments or property rights, such

as qualified or non-qualified deferred compensation plans and

equity-based plans

• Benefits provided in the form of insurance or unfunded welfare

benefits, such as health, life or disability insurance

• Benefits provided currently, including property made available, job-

related working conditions and incidental benefits such as use of

company car

9

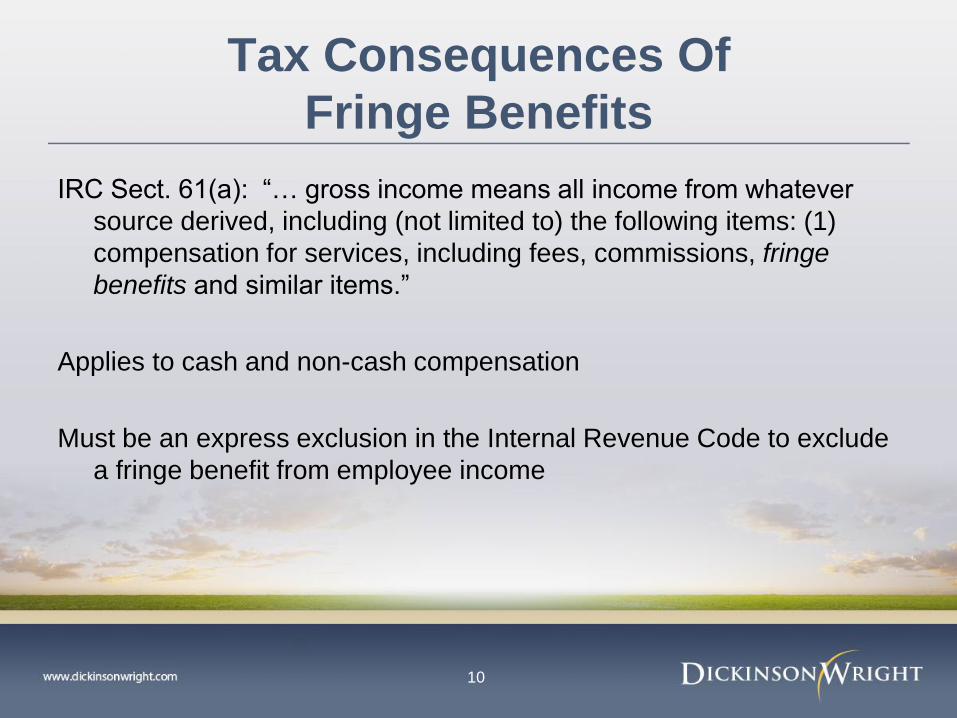

Tax Consequences Of

Fringe Benefits

IRC Sect. 61(a): “… gross income means all income from whatever

source derived, including (not limited to) the following items: (1)

compensation for services, including fees, commissions, fringe

benefits and similar items.”

Applies to cash and non-cash compensation

Must be an express exclusion in the Internal Revenue Code to exclude

a fringe benefit from employee income

10

Deferred Compensation Benefits

• IRC Sect. 402: Contributions to a qualified retirement plan are not

taxable until distributed.

• An employer’s unsecured promise to pay deferred compensation also

defers tax until distributions are made, subject to compliance with IRC

Sect. 409A. Deferred compensation plans of tax-exempt employers that

do not comply with the rules of IRC Sect. 457(b) are taxable when they

are no longer subject to a substantial risk of forfeiture under IRC Sect.

457(f).

• Under IRC Sect. 83, property that is subject to a substantial risk of

forfeiture is taxable when the risk of forfeiture lapses, unless the

employee makes an 83(b) election to recognize income on the date the

property is transferred to him or her.

• Note that the taxation of these benefits is deferred, not excluded from

income.

11

Welfare Benefit Plan Exclusions

• IRC Sect. 79: Group-term life insurance up to $50,000

• IRC Sect. 105/106: Accident and health benefits. Employer contributions

are excludible (up to certain limits noted below) under IRC Sect.106.

Benefit payments for medical care of the employee, spouse and

dependents are excluded from income under IRC Sect. 105(b).

A self-insured medical reimbursement plan cannot discriminate in favor

of highly compensated individuals, under IRC Sect. 105(h).

Contributions to a health savings account are limited to $3,250 for self-

only coverage and $6,450 for family coverage; employer contributions

must be “comparable.”

Employee pre-tax contributions to a health flexible spending account are

limited to $2,500 for plan years on or after Jan. 1, 2013. An employer

may contribute an additional “flex credit” to a health FSA.

12

Welfare Benefit Exclusions (Cont.)

• IRC Sect. 125: Cafeteria plan allows employees to make pre-tax

contributions for qualified benefits.

• IRC Sect. 127: An educational assistance program allows an

employee to exclude up to $5,250 per year.

• IRC Sect. 129: A dependent care assistance program allows an

employee to exclude up to $5,000 per year.

• IRC Sect. 137: An adoption assistance program allows an employee

to exclude a cumulative limit of $12,970 in 2013.

13

Incidental Fringe Benefits

IRC Sect. 132: Eight categories of excludible benefits

• Working condition fringes

• No-additional cost services

• Qualified employee discounts

• De minimis fringes

• Qualified transportation fringes

• Qualified moving expense reimbursements

• Qualified retirement planning services

• Qualified military base realignment and closure fringes

14

Working Condition Fringes

Definition: Any property or service that, if the employee had paid for it,

would be deductible under IRC sections 162 or 167.

Examples:

• Business use of company car or airplane

• Office décor

• Employer-provided cell phone

• Professional memberships, dues and publications

• Job-related educational assistance

• Security arrangements (if the need for security is substantiated)

• Outplacement services (if the employer derives a substantial

business benefit from the service)

15

No-Additional Cost Services

Definition: A service provided to an employee for which the employer

does not incur any substantial additional cost

Examples:

• Space-available travel on an airplane, train or bus

• Use of available hotel rooms

16

Qualified Employee Discounts

Definition: An employee discount on qualified property or services. The

maximum excludible discount on services is 20% of the price at

which the employer offers the service to non-employee customers.

The maximum excludible discount on property or merchandise is the

employer’s “gross profit percentage” (the excess of the aggregate

sales price of the products sold to non-employee customers over the

aggregate cost of the property divided by the aggregate sales price).

“Qualified property or services” means property or services offered for

sale to customers in the ordinary course of business of the line of

business of the employer in which the employee provides services.

Does NOT include real property or personal property of a kind held

for investment

17

De Minimis Fringe Benefits

Definition: The fair market value (FMV) of the property or service is so

small that accounting for the property or service would be

unreasonable or administratively impracticable. The frequency with

which the benefit is provided is also considered.

Examples:

• Occasional use of office support staff and equipment (such as

copiers)

• Occasional payment of supper money and taxi fare, if an employee

is required to work overtime.

• Holiday gifts of low FMV (such as a turkey or ham)

• Occasional theater or sports tickets

• Dependent life insurance up to $2,000

18

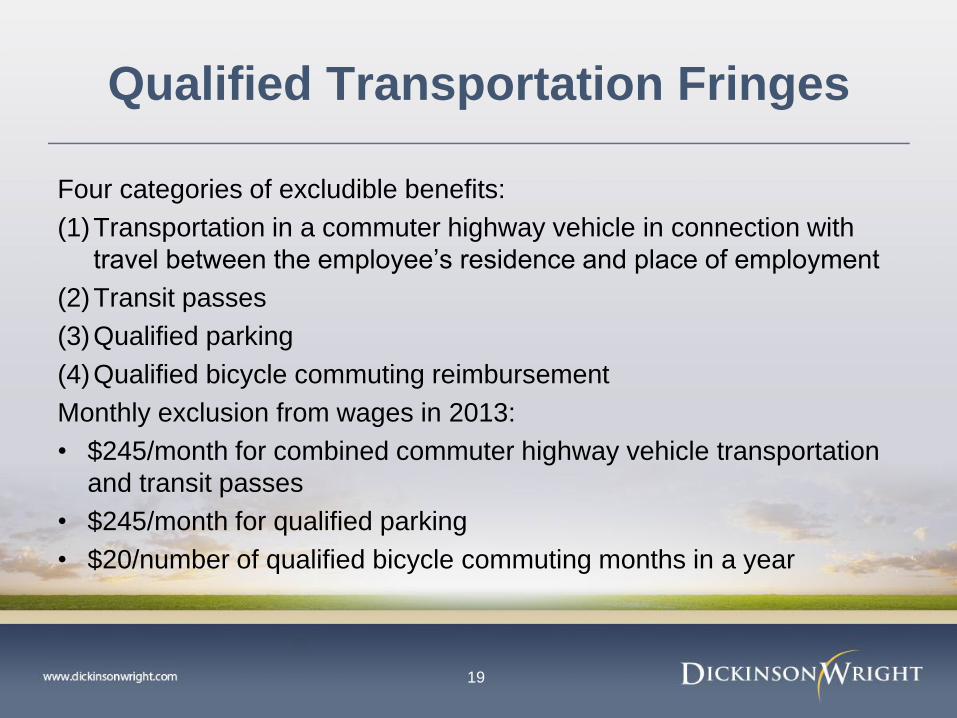

Qualified Transportation Fringes

Four categories of excludible benefits:

(1)Transportation in a commuter highway vehicle in connection with

travel between the employee’s residence and place of employment

(2)Transit passes

(3)Qualified parking

(4)Qualified bicycle commuting reimbursement

Monthly exclusion from wages in 2013:

• $245/month for combined commuter highway vehicle transportation

and transit passes

• $245/month for qualified parking

• $20/number of qualified bicycle commuting months in a year

19

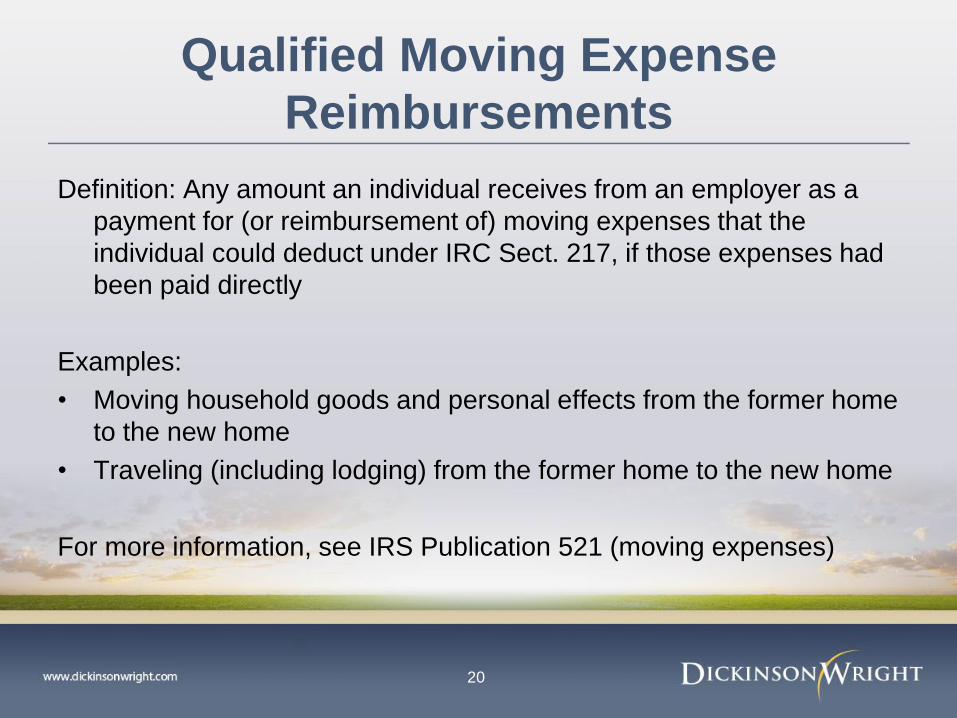

Qualified Moving Expense

Reimbursements

Definition: Any amount an individual receives from an employer as a

payment for (or reimbursement of) moving expenses that the

individual could deduct under IRC Sect. 217, if those expenses had

been paid directly

Examples:

• Moving household goods and personal effects from the former home

to the new home

• Traveling (including lodging) from the former home to the new home

For more information, see IRS Publication 521 (moving expenses)

20

Slide Intentionally Left Blank

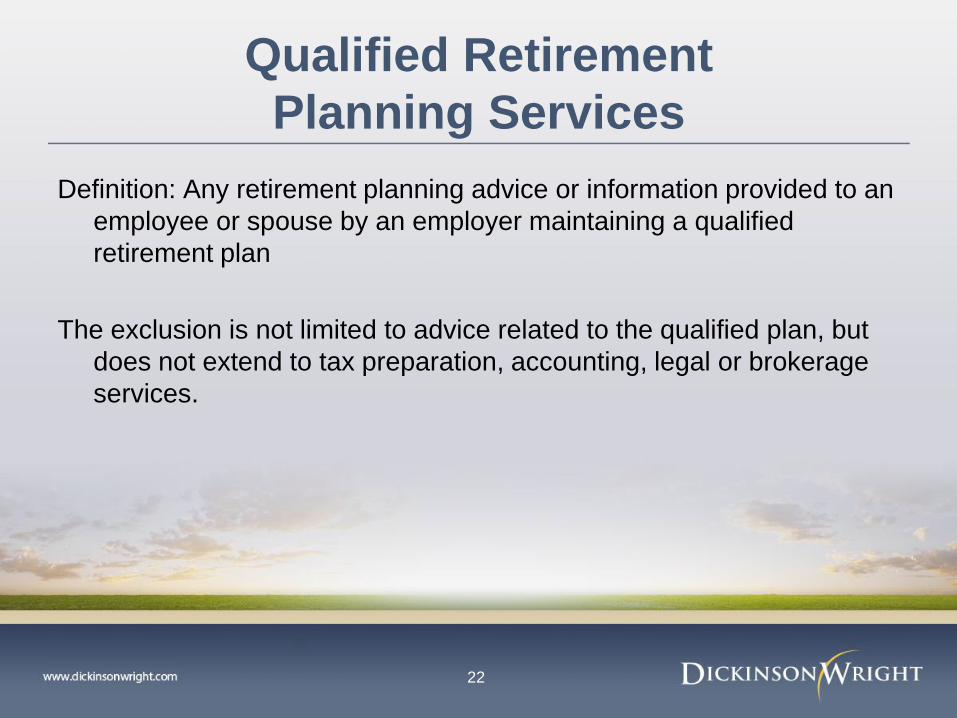

Qualified Retirement

Planning Services

Definition: Any retirement planning advice or information provided to an

employee or spouse by an employer maintaining a qualified

retirement plan

The exclusion is not limited to advice related to the qualified plan, but

does not extend to tax preparation, accounting, legal or brokerage

services.

22

Qualified Military Base Realignment

And Closure Fringes

Excludes certain housing assistance payments (such as compensation

for losses sustained in a private sale or foreclosure of a home) made

with respect to military base realignment and closures

Limited applicability, due to numerous technical requirements

23

Other Developments/Resources

• IRS commenced a three-year employment tax national research

project in February 2010. Information collected during the project will

help the IRS select and audit future employment tax returns with the

greatest compliance risk. Fringe benefits were one of the areas

identified by the IRS as a primary focus of the project. Results of the

project could lead to increased scrutiny of the tax treatment of fringe

benefits during an audit.

• Helpful resource: IRS Publication 15-B (employer’s tax guide to

fringe benefits)

24

FRINGE BENEFITS THAT CAN TRIGGER A U.S. TAX BILL

Tara Silver-Malyska, UHY Advisors

An independent member of UHY International

The next level of

service

EMPLOYER-PROVIDED PERQUISITES

Perquisites or fringe benefits are non-cash benefits provided to executives at no cost or at a very modest cost.

Taxation of fringe benefits has always been important, but why the focus or discussion now? − IRS released six audit techniques guides focusing on executive

compensation. Included in this group is the Fringe Benefits Audit Techniques Guide.

− Taxation of executive compensation is currently included in routine corporate audits of large and mid-size business (LMSB) taxpayers and as evidenced by related IDRs

− In January 2013, the IRS issued the FSLG Fringe Benefit Guide.

26

An independent member of UHY International

The next level of

service

TAXABLE FRINGE BENEFITS

Tax treatment of the particular fringe benefit varies, depending upon facts and circumstances, and it is important to follow the three-step analysis when examining a particular item.

First, identify the fringe benefit and start with the assumption that its value will be taxable as compensation to the employee

Second, check to see if there are any statutory provisions that exclude the fringe benefit from the executive’s gross income

Third, value any portion of the benefit that is not excludable for inclusion in the executive’s gross income

Also, consider valuation and non-discrimination rules

27

An independent member of UHY International

The next level of

service

TAXABLE FRINGE BENEFITS (CONT.)

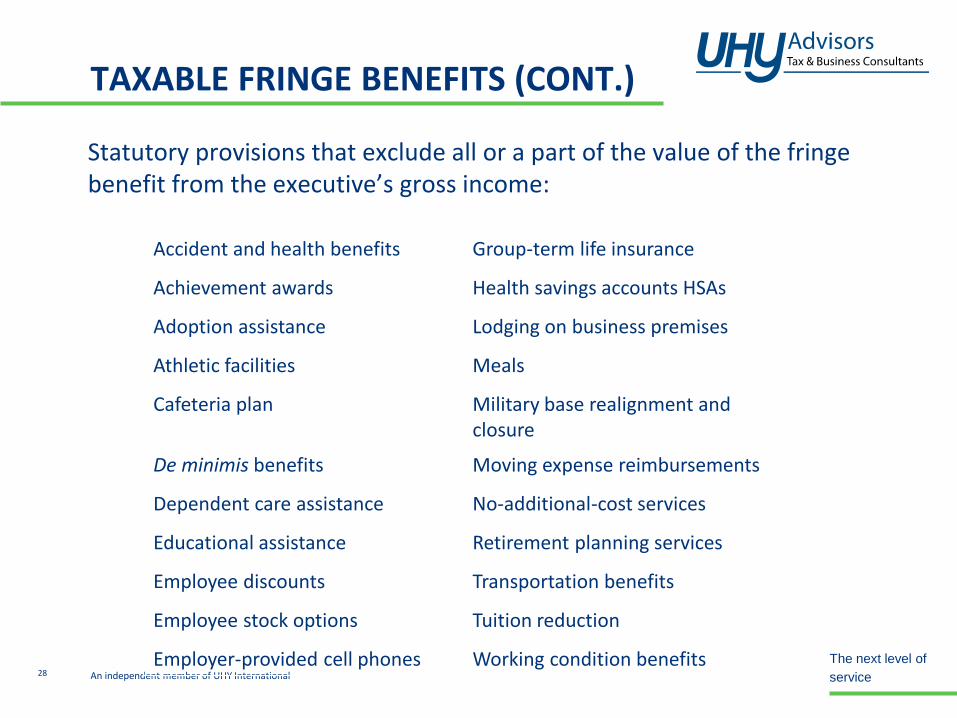

Statutory provisions that exclude all or a part of the value of the fringe benefit from the executive’s gross income:

Accident and health benefits Group-term life insurance

Achievement awards Health savings accounts HSAs

Adoption assistance Lodging on business premises

Athletic facilities Meals

Cafeteria plan Military base realignment and closure

De minimis benefits Moving expense reimbursements

Dependent care assistance No-additional-cost services

Educational assistance Retirement planning services

Employee discounts Transportation benefits

Employee stock options Tuition reduction

Employer-provided cell phones Working condition benefits 28

An independent member of UHY International

The next level of

service

TAXABLE FRINGE BENEFITS (CONT.)

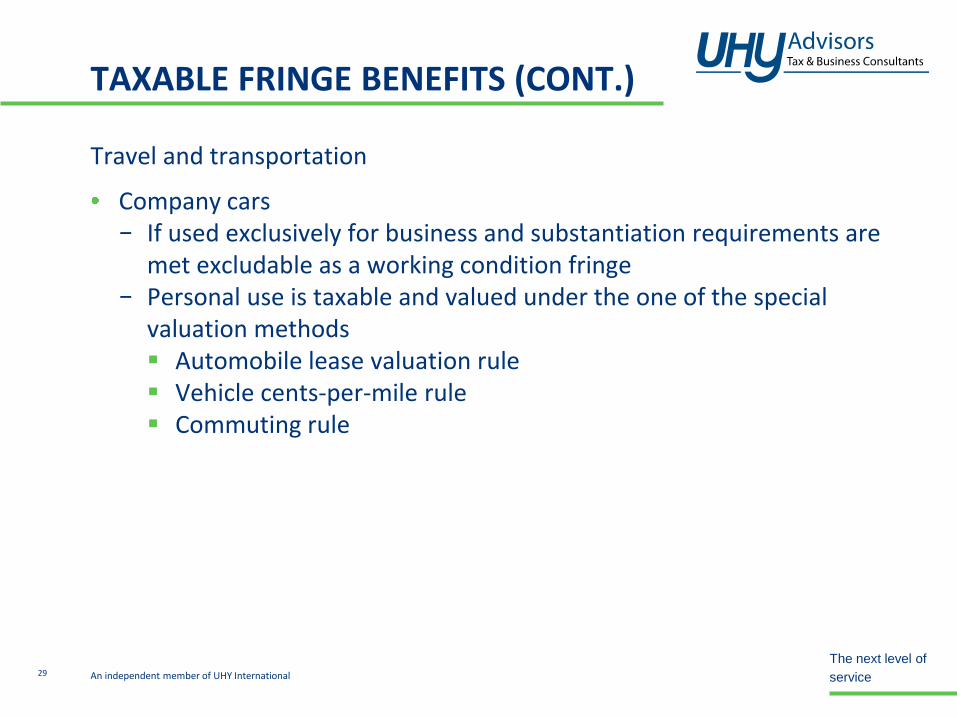

Travel and transportation

Company cars − If used exclusively for business and substantiation requirements are

met excludable as a working condition fringe − Personal use is taxable and valued under the one of the special

valuation methods Automobile lease valuation rule Vehicle cents-per-mile rule Commuting rule

29

An independent member of UHY International

The next level of

service

TAXABLE FRINGE BENEFITS (CONT.)

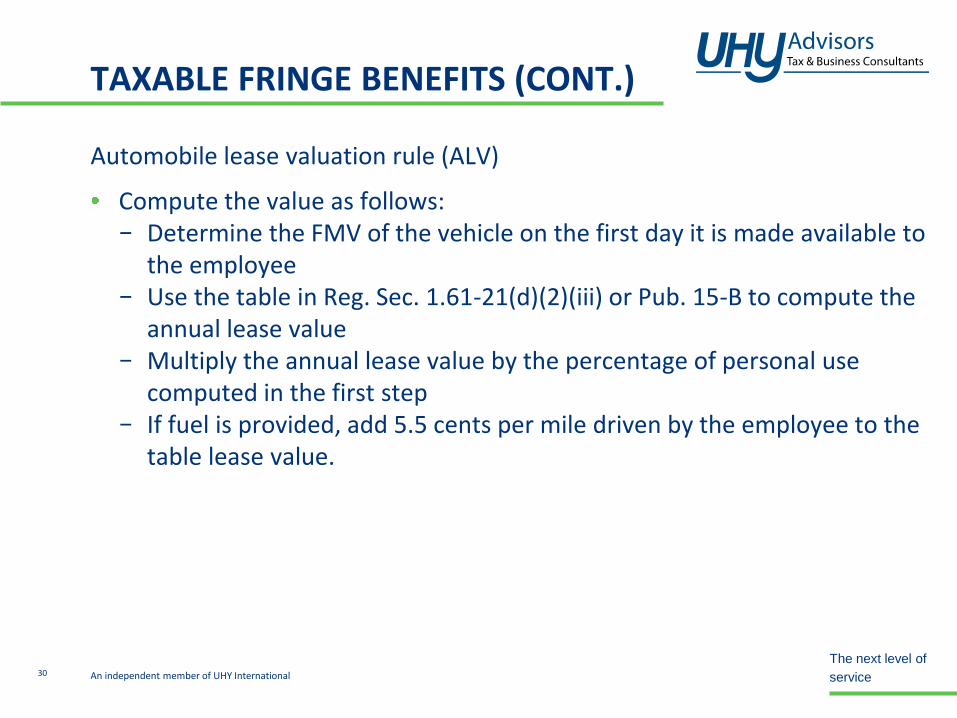

Automobile lease valuation rule (ALV)

Compute the value as follows: − Determine the FMV of the vehicle on the first day it is made available to

the employee − Use the table in Reg. Sec. 1.61-21(d)(2)(iii) or Pub. 15-B to compute the

annual lease value − Multiply the annual lease value by the percentage of personal use

computed in the first step − If fuel is provided, add 5.5 cents per mile driven by the employee to the

table lease value.

30

An independent member of UHY International

The next level of

service

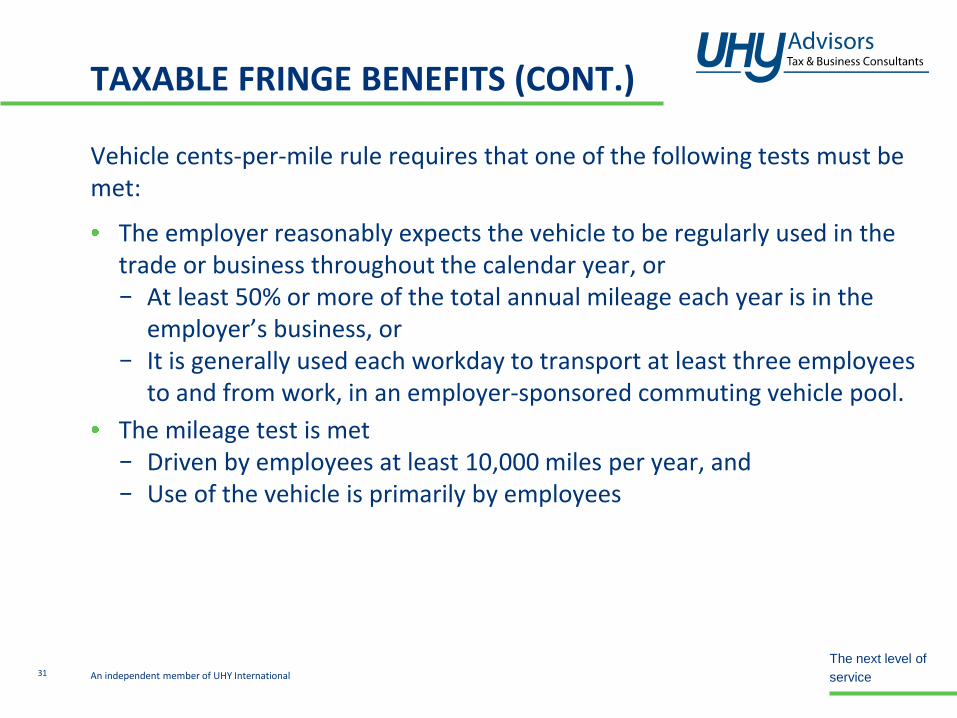

Vehicle cents-per-mile rule requires that one of the following tests must be met:

The employer reasonably expects the vehicle to be regularly used in the trade or business throughout the calendar year, or − At least 50% or more of the total annual mileage each year is in the

employer’s business, or − It is generally used each workday to transport at least three employees

to and from work, in an employer-sponsored commuting vehicle pool.

The mileage test is met − Driven by employees at least 10,000 miles per year, and − Use of the vehicle is primarily by employees

TAXABLE FRINGE BENEFITS (CONT.)

31

An independent member of UHY International

The next level of

service

TAXABLE FRINGE BENEFITS (CONT.)

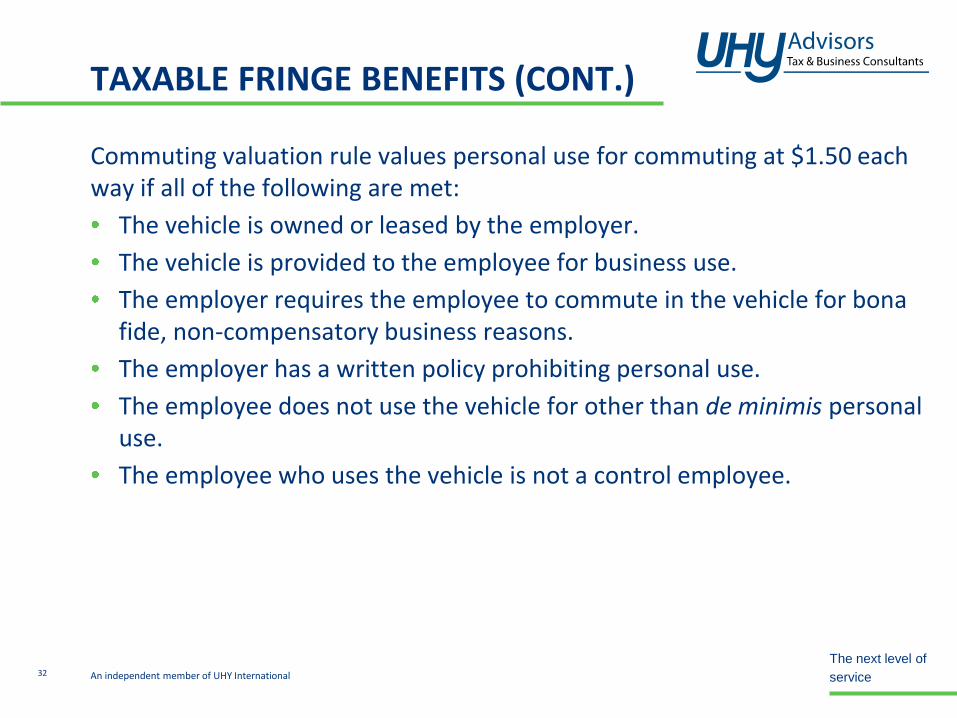

Commuting valuation rule values personal use for commuting at $1.50 each way if all of the following are met:

The vehicle is owned or leased by the employer.

The vehicle is provided to the employee for business use.

The employer requires the employee to commute in the vehicle for bona fide, non-compensatory business reasons.

The employer has a written policy prohibiting personal use.

The employee does not use the vehicle for other than de minimis personal use.

The employee who uses the vehicle is not a control employee.

32

An independent member of UHY International

The next level of

service

TAXABLE FRINGE BENEFITS (CONT.)

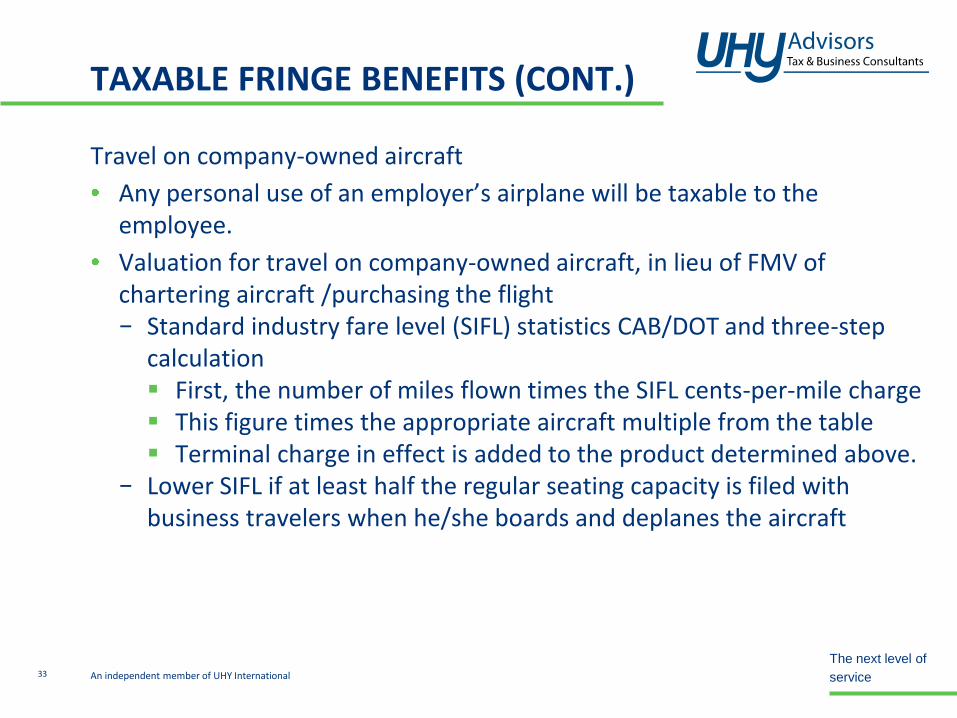

Travel on company-owned aircraft

Any personal use of an employer’s airplane will be taxable to the employee.

Valuation for travel on company-owned aircraft, in lieu of FMV of chartering aircraft /purchasing the flight − Standard industry fare level (SIFL) statistics CAB/DOT and three-step

calculation First, the number of miles flown times the SIFL cents-per-mile charge This figure times the appropriate aircraft multiple from the table Terminal charge in effect is added to the product determined above.

− Lower SIFL if at least half the regular seating capacity is filed with business travelers when he/she boards and deplanes the aircraft

33

An independent member of UHY International

The next level of

service

TAXABLE FRINGE BENEFITS (CONT.)

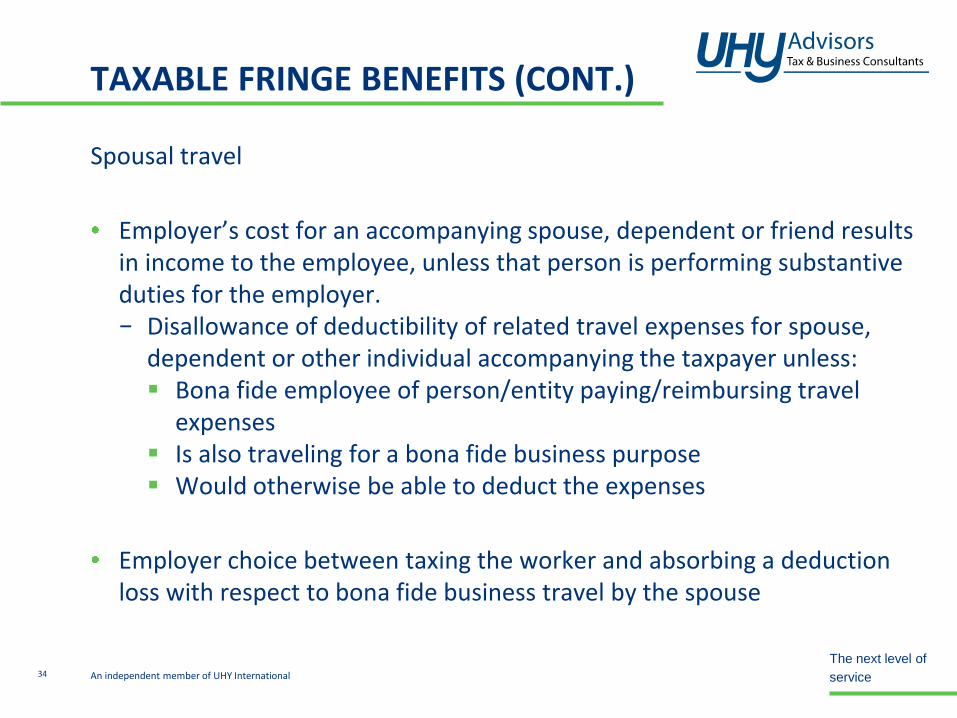

Spousal travel

Employer’s cost for an accompanying spouse, dependent or friend results in income to the employee, unless that person is performing substantive duties for the employer. − Disallowance of deductibility of related travel expenses for spouse,

dependent or other individual accompanying the taxpayer unless: Bona fide employee of person/entity paying/reimbursing travel

expenses Is also traveling for a bona fide business purpose Would otherwise be able to deduct the expenses

Employer choice between taxing the worker and absorbing a deduction loss with respect to bona fide business travel by the spouse

34

An independent member of UHY International

The next level of

service

TAXABLE FRINGE BENEFITS (CONT.)

Security protection

Expenditures “primarily for the safety of employees” are excludable as working condition fringes, if safety precautions are necessary and detailed regular requirements and valuation rules are satisfied. − Exclusion amount is the difference between the amount paid for the

transportation and the amount paid absent the security concerns.

Substantiation requires demonstration of the existence of a bona fide business-oriented security concern. − Must establish external circumstances requiring security, and − Establish an “overall security program”

35

Slide Intentionally Left Blank

An independent member of UHY International

The next level of

service

TAXABLE FRINGE BENEFITS (CONT.)

Country club memberships

No deduction is allowed for the payment of dues to any club organized for business, pleasure, recreation or other social purpose.

A club is defined as any membership organization with a principal purpose of: − Conducting entertainment activities for members of the organization or

their guests, or − Providing members or their guest with access to entertainment

facilities. − Business leagues, trade associations and professional organizations are

not clubs.

Employer choice to not tax the employee without deduction, or to treat as employee comp and tax and deduct the club dues

37

An independent member of UHY International

The next level of

service

TAXABLE FRINGE BENEFITS (CONT.)

Additional benefits subject to current tax:

Vacations and holidays

Tuition payment and tuition reduction plans

Financial counselling

Interest-free or low-interest loans

Gifts and awards

Unrelated employer facility benefits

Commuting

Excess moving expense reimbursements

Housing assistance benefits

Leave sharing programs

Employer-provided cell phones

38

SITUATIONS OF EMPLOYER FRINGE BENEFIT WITHHOLDING LIABILITY

Stefan Smith, Locke Lord

40

Wages

• Code Sect. 61(a)(1) provides that, except as otherwise provided in

Subtitle A of the Code, gross income includes compensation for

services including fees, commissions, fringe benefits, and similar

items. (Treas. Reg. 1.61-21(a))

Wages (Cont.)

• For purposes of FICA, FUTA and collection of income taxes at the

source, the term “wages” means all remuneration for services

performed by and employee for his or her employee, including the

cash value of all remuneration (including benefits) paid in any

medium other than cash. (Code sections 3121(a), 3306(b), and

3401(a))

41

The Withholding Period

• Employers may elect to treat fringe benefits as paid on a pay period,

quarterly, semi-annual, or other basis.

– At a minimum, the benefits MUST be treated as paid no less

frequently than annually.

– Employers need not make the same withholding election for all

employees.

– Employers may change their elections as frequently as desired.

42

The Withholding Period (Cont.)

• The value of a single fringe benefit may be treated as having been

paid on one or multiple dates.

– Example: Employee receives a benefit valued at $1,000 in a

single pay period.

• The employer may treat the full $1,000 value as having been

paid in a single pay period.

• The employer may also elect to treat the benefit has having

been paid in four equal $250 amounts over four pay periods.

43

The Withholding Period (Cont.)

• The election for reporting and withholding does not apply to a fringe

benefit that is a transfer of tangible or intangible personal property of

a kind normally held for investment or a transfer of real property.

– For this kind of fringe benefit, the employer MUST use the actual

date on which the property was transferred to the employee.

44

The Withholding Period (Cont.)

• Special rule for fringe benefits provided during November and

December

– The employer may choose to treat the value of fringe benefits

actually provided during the last two months of the calendar year

as paid during the subsequent calendar year.

– The special rule does not permit an employer that elects to treat

benefits as provided during the last two months to defer the

entire value of all benefits to the next year.

45

The Withholding Period (Cont.)

– If this special rule is elected, the affected employee must be

notified of the period in which it was used.

• This notice must be given at or near the date the Form W-2 is

provided, but not earlier than with the employee's last

paycheck of the calendar year.

• If the employer uses this special rule, the employee also

must use it for the same period, and the employee cannot

use the special rule unless the employer does.

46

The Withholding Period (Cont.)

• The IRS need not be notified of any employer elections with respect

to the period(s) in which fringe benefits will be treated as having

been paid.

47

Withholding And Deposits

• How much should be withheld?

– The employer may add the value of the fringe benefit to other

wages for the period, and withhold based on the total.

– Alternatively, the employer may withhold on the value of fringe

benefits at the flat 25% rate that applies to supplemental wages.

• This flat rate increases to 39.6% when supplemental wage

payments to an individual exceed $1 million during the year.

48

Withholding And Deposits (Cont.)

– The employee tax rate for Social Security is 6.2% for 2013.

• The employer tax rate for Social Security remains unchanged

at 6.2%.

• The 2013 Social Security wage base limit is $113,700.

49

Withholding And Deposits (Cont.)

– In addition to withholding Medicare tax at 1.45%, the employer

must withhold a 0.9% additional Medicare tax from wages paid

to an employee in excess of $200,000 in a calendar year.

• This obligation begins when aggregate wages for the year

reach $200,000.

• There is no corresponding employer portion of this additional

tax.

50

Withholding And Deposits (Cont.)

– For 2013, the FUTA tax rate is 6.0%.

• The tax applies to the first $7,000 paid to each employee as

wages during the year.

• The $7,000 is the federal wage base. The state wage base

may be different.

• Generally, a credit may be taken against FUTA for amounts

paid into state unemployment funds.

– The credit may be as much as 5.4% of FUTA taxable

wages.

– If a taxpayer is entitled to the maximum 5.4% credit, the

FUTA tax rate after credit is 0.6%.

51

Withholding And Deposits (Cont.)

• Special rule for use of highway vehicle

– An employer may choose not to withhold income tax on the

value of an employee's personal use of a highway motor vehicle.

– This choice need not be made for all employees.

– The employer must, however, withhold the applicable Social

Security and Medicare taxes on such benefits.

52

Withholding And Deposits (Cont.)

– Requirements for using this special rule

• Notify the employee in writing of the choice not to withhold by

Jan. 31 of the election year or, if later, within 30 days after a

vehicle is first provided to the employee; and

• Include the value of the benefits in boxes 1, 3, 5 and 14 on a

timely furnished Form W-2

53

Reporting

• The actual value of fringe benefits provided during a calendar year

(or other period) must be determined by Jan. 31 of the following

year.

• Report the actual value on Forms 941 (or Form 944) and W-2

• An employer may use a separate Form W-2 for fringe benefits and

any other benefit information.

54

Slide Intentionally Left Blank

Special Social Security

And Medicare Rule

• Paying Social Security and Medicare taxes on behalf of an

employee

– Step 1: Divide the stated pay (the amount that you pay without

taking into account your payment of Social Security and

Medicare taxes) by a factor for that year.

• For 2013, the factor is .9235 for stated pay of $105,001.95 or

less.

56

Special Social Security

And Medicare Rule (Cont.)

– Step 2: Figure the correct wages (wages plus employer-paid

employee taxes) to report by dividing the stated pay by .9235

• This will give you the wages to report in Box 1 and the Social

Security and Medicare wages to report in Boxes 3 and 5 of

Form W-2.

– Step 3: Figure the correct Social Security tax to enter in Box 4 by

multiplying the amount in Box 3 by the Social Security

withholding rate of 6.2%, and enter the result in Box 4

57

Special Social Security

And Medicare Rule (Cont.)

– Step 4: Figure the correct Medicare tax to enter in Box 6 by

multiplying the amount in Box 5 by the Medicare withholding rate

of 1.45%, and enter the result in Box 6

58

Special Social Security

And Medicare Rule (Cont.)

• What if the stated pay is greater than $105,001.95?

– The portion of stated wages subject to Social Security tax is

$105,001.95 (the first $113,700 of wages × .9235).

• Stated pay in excess of $105,001.95 is not subject to Social

Security tax, since the tax only applies to the first $113,700 of

wages.

• Enter $113,700 in Box 3 of Form W-2

59

Special Social Security

And Medicare Rule (Cont.)

• The Social Security tax to enter in Box 4 is $7,049.40

($113,700 x .062).

– To figure the correct Medicare wages for Box 5, subtract

$105,001.95 from the stated pay, divide the result by .9855, and

add $113,700

• Enter this amount in Box 5

• The Medicare tax to enter in Box 6 is then obtained by

multiplying the amount from Box 5 by .0145.

60

Special Social Security

And Medicare Rule (Cont.)

• Although these employment tax amounts are not actually withheld

from the employee's pay, the employer reports them as withheld on

Form 941 and deposits the calculated amounts as Social Security

and Medicare taxes.

61

MATERIAL TERMS OF SECT. 409A REGARDING TAXABILITY

James Davis, Gunster

GUNSTER

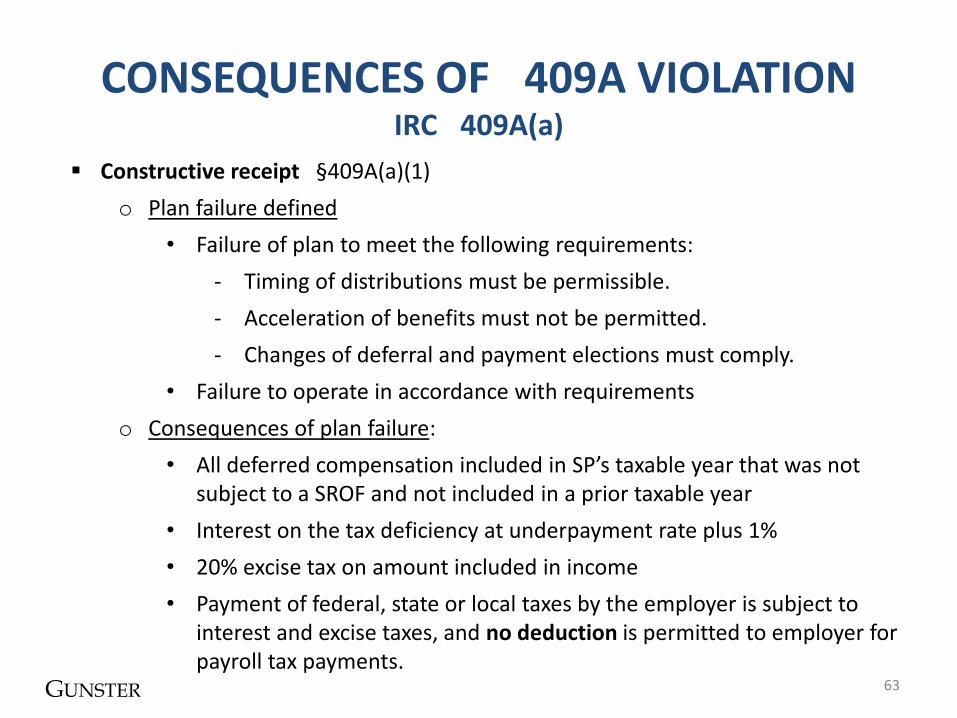

CONSEQUENCES OF

409A VIOLATION IRC

409A(a)

63

Constructive receipt §409A(a)(1)

o Plan failure defined

• Failure of plan to meet the following requirements:

- Timing of distributions must be permissible.

- Acceleration of benefits must not be permitted.

- Changes of deferral and payment elections must comply.

• Failure to operate in accordance with requirements

o Consequences of plan failure:

• All deferred compensation included in SP’s taxable year that was not subject to a SROF and not included in a prior taxable year

• Interest on the tax deficiency at underpayment rate plus 1%

• 20% excise tax on amount included in income

• Payment of federal, state or local taxes by the employer is subject to interest and excise taxes, and no deduction is permitted to employer for payroll tax payments.

GUNSTER

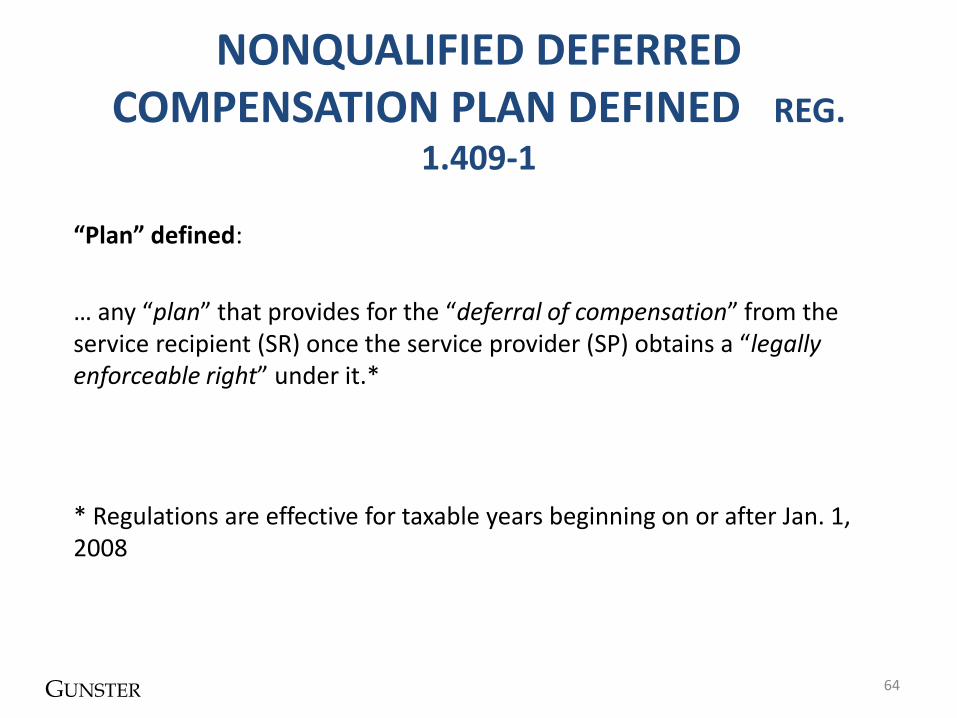

NONQUALIFIED DEFERRED COMPENSATION PLAN DEFINED REG.

1.409-1

“Plan” defined:

… any “plan” that provides for the “deferral of compensation” from the service recipient (SR) once the service provider (SP) obtains a “legally enforceable right” under it.*

* Regulations are effective for taxable years beginning on or after Jan. 1, 2008

64

GUNSTER

PLAN DEFINED (CONT.)

65

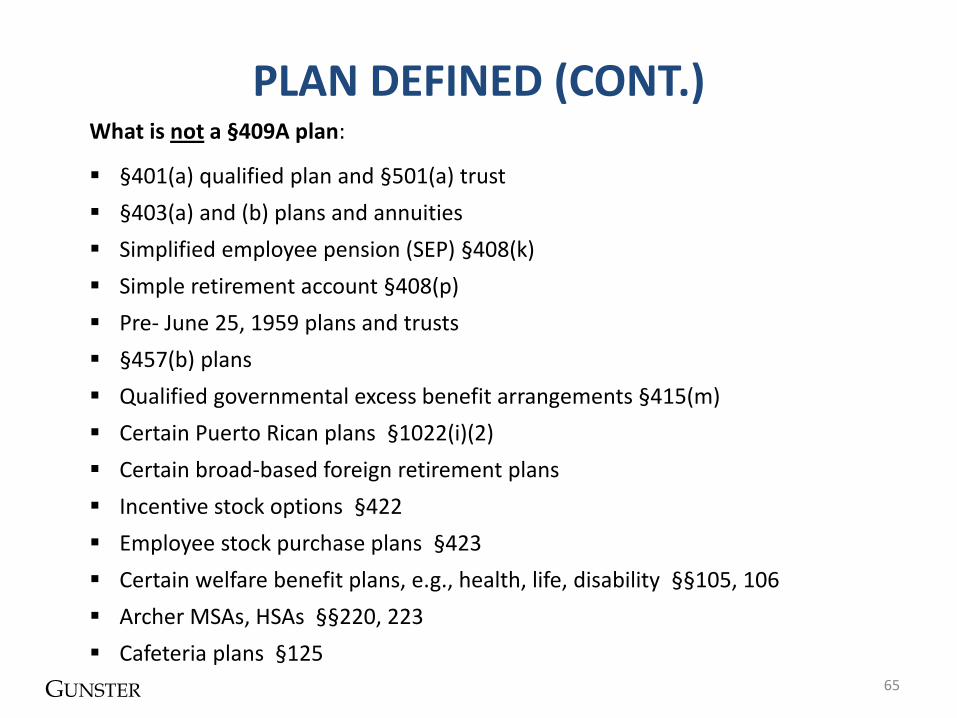

What is not a §409A plan:

§401(a) qualified plan and §501(a) trust

§403(a) and (b) plans and annuities

Simplified employee pension (SEP) §408(k)

Simple retirement account §408(p)

Pre- June 25, 1959 plans and trusts

§457(b) plans

Qualified governmental excess benefit arrangements §415(m)

Certain Puerto Rican plans §1022(i)(2)

Certain broad-based foreign retirement plans

Incentive stock options §422

Employee stock purchase plans §423

Certain welfare benefit plans, e.g., health, life, disability §§105, 106

Archer MSAs, HSAs §§220, 223

Cafeteria plans §125

GUNSTER

PLAN DEFINED (CONT.)

66

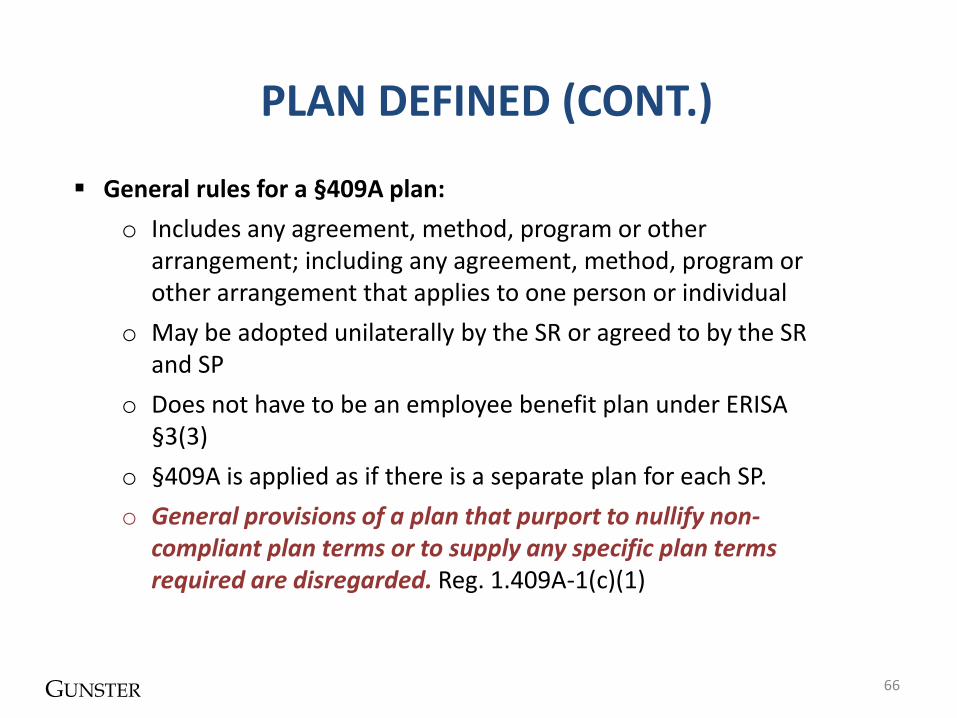

General rules for a §409A plan:

o Includes any agreement, method, program or other arrangement; including any agreement, method, program or other arrangement that applies to one person or individual

o May be adopted unilaterally by the SR or agreed to by the SR and SP

o Does not have to be an employee benefit plan under ERISA §3(3)

o §409A is applied as if there is a separate plan for each SP.

o General provisions of a plan that purport to nullify non-compliant plan terms or to supply any specific plan terms required are disregarded. Reg. 1.409A-1(c)(1)

GUNSTER

PLAN DEFINED (CONT.)

67

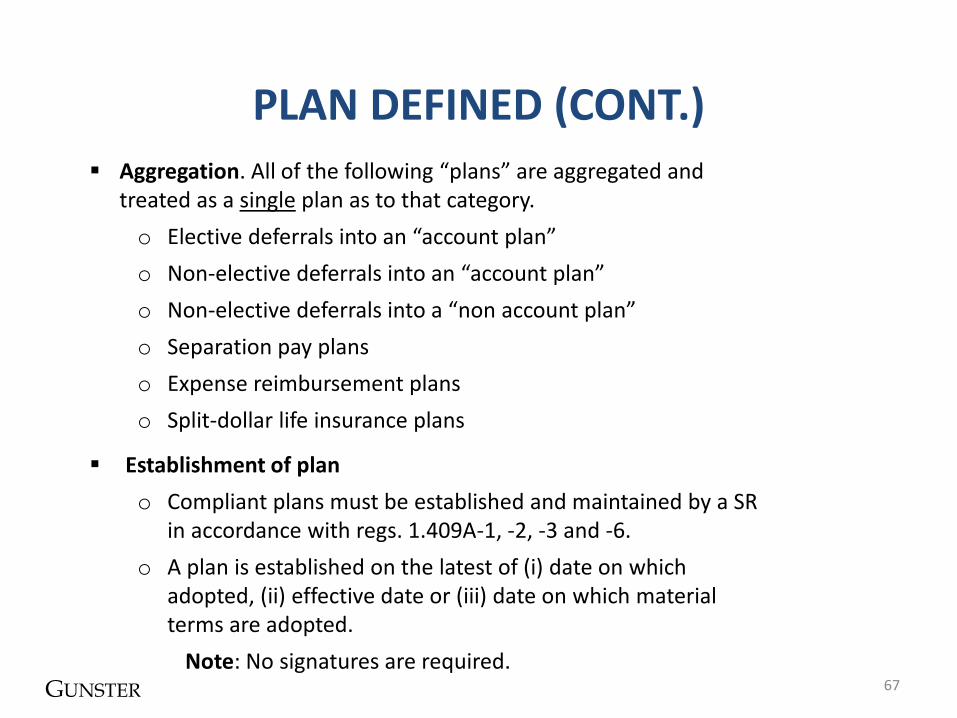

Aggregation. All of the following “plans” are aggregated and treated as a single plan as to that category.

o Elective deferrals into an “account plan”

o Non-elective deferrals into an “account plan”

o Non-elective deferrals into a “non account plan”

o Separation pay plans

o Expense reimbursement plans

o Split-dollar life insurance plans

Establishment of plan

o Compliant plans must be established and maintained by a SR in accordance with regs. 1.409A-1, -2, -3 and -6.

o A plan is established on the latest of (i) date on which adopted, (ii) effective date or (iii) date on which material terms are adopted.

Note: No signatures are required.

GUNSTER

PLAN DEFINED (CONT.)

68

Regardless of the foregoing, a plan will be deemed to be established as of the date the SP obtains a legally binding right to deferral of compensation.

GUNSTER

DEFERRAL OF COMPENSATION DEFINED

69

“A plan provides for the deferral of compensation if the SP had a legally binding right during a taxable year to compensation that may be payable to the SP in a later taxable year.” Reg. 1.401A-1(b)(1)

Deferred compensation also includes any right to earnings on the compensation so deferred.

A SP does not have a legally binding right to compensation, to the extent that it may be eliminated or reduced by the SR, unless SP or family controls SR.

Example: The ability to terminate SP’s employment by SR without cause that would forfeit SP’s severance compensation

GUNSTER

DEFERRAL (CONT.)

70

Exceptions to deferred compensation definition

o Short-term (S-T) deferrals

• Any payment is actually or constructively received (§83) by SR by the 15th day of the third month after the end of the later of (i) the SP’s first taxable year, or (ii) the SR’s first taxable year in which the payment is no longer subject to a substantial risk of forfeiture (SROF) (“applicable 2 ½ month period”) Reg. 1.409A-1(b)(4)

• S-T deferral exception does not apply to a deferred payment, i.e., a payment that will or may occur after the end of the applicable 2 ½-month period such as on account of separation from service, death, disability, change in control event, specific time or scheduled payment or unforeseeable emergency.

o Certain delayed payments: Payments made after the applicable 2 ½-month period if the “taxpayer” establishes that it was administratively impracticable to make the payment within such period and was unforeseeable or payment would have jeopardized the ability of the SR to continue as a going concern. Reg. 1.401A-1(b)(4)ii)

GUNSTER

DEFERRAL (CONT.)

71

Equity based compensation:

o Non-statutory stock options (NSOs): There is no deferral to the right to purchase the SR’s stock if:

• The exercise price may never be less than the FMV of the underlying stock as of the date the option is granted disregarding lapse restrictions and SROF;

• The transfer is taxed pursuant to §83; and

• The option does not include any feature for the deferral of compensation until exercise of the option.

Reg. 1.409A-1(b)(5)(i)(A)

o Stock appreciation rights (SARs): There is no deferral of compensation based on the appreciation in value of a specified number of shares of SR stock between grant and exercise dates if:

• Compensation cannot be greater than the FMV of the stock on the exercise date over the FMV on the grant date;

GUNSTER

DEFERRAL (CONT.)

72

• SAR exercise price can never be less than the FMV of the underlying stock at the date it is granted; and

• Option does not include any feature for the deferral of compensation until exercise of the option. Reg. 1.409A-1(b)(5)(i)(B)

o Dividends: A right to receive dividends contingent on the purchase of stock from the NSO or SAR treated as a reduction or offset of the purchase price, i.e., deferred compensation and thus is subject to §409A. If dividends are not contingent upon purchase, it is not a deferral of compensation. Reg. 1.409A-1(b)(5)(i)(E)

o ISO and employee stock purchase plans: Plans under §§422 and 423 are exempt from 409A; but if the plan is modified, extended or renewed, it may be treated as a new plan and not an ISO and thus subject to §409A. Reg. 1.409A-1(b)(5)(ii)

o Non-corporate entities: Equity interests other than a corporation generally constitute SR stock, for purposes of 409A.

GUNSTER

DEFERRAL (CONT.)

73

o Substitutions and assumption from corporate transactions/modifications to plans

A change in the terms of a stock right or a change in the terms of the plan that has the effect of reducing the exercise price is a modification and will be subject to §409A at the time of the change. Reg. 1.409A-1(b)(5)(v)(B)

An extension of the exercise period at a time when the exercise price of the stock right equals or exceeds the FMV of the SR stock is treated as a new right.

A substitution of stock from a corporate transaction will not itself constitute a modification, provided the above does not occur.

A change to a plan will not be considered a modification if the change is rescinded before the earlier of the stock right exercise or the last day of the SP’s taxable year in which the change occurred. Reg. 1.409A-1(b)(5)(v)(I)

A change in the number of shares purchasable is not a modification, if the exercise price is proportionately adjusted.

GUNSTER

DEFERRAL (CONT.)

74

o Restricted property; §402(b) trusts Reg. 1.409A-1(b)(6)(i)

• No deferral of income occurs merely because:

- Property is substantially non-vested,

- From a §83(b) election, or

- From income inclusion under §402(b)(4)(A)

o Tax equalization payments Reg. 1.409A-1(b)(6)(iii)

• Payments must be made no later than the end of the second taxable year of the SP beginning after the taxable year of the SP in which the SP’s U. S. income tax return (including extensions) is to be filed for the year to which the compensation subject to the tax equalization relates or within such period after the SP’s foreign income tax return is to be filed.

• If litigation or audit occurs, payment must be made by the end of the tax year following the year in which taxes are paid. Reg. 1.409A-1(b)(8)(iii)

GUNSTER

DEFERRAL (CONT.)

75

Severance pay plans Reg. 1.409A-1(b)(9)(i) o A plan that provides compensation upon SFS provides for a deferral of

compensation, with the following exceptions:

• Collectively bargained plans

• Involuntary separation from service/window plans, provided that:

i) Separation pay does not exceed two times lesser of:

- Annualized compensation in preceding year, or

- §401(a)(17) compensation limit for qualified plans; and

ii)Must be paid no later than last day of taxable year following separation by SP

•Foreign separation pay plans

NOTE: These exceptions may be used in combination with other compensation payments. Reg. §1.401A-1(b)(9)

GUNSTER

DEFERRAL (CONT.)

76

Reimbursements/other separation payments (voluntary or involuntary separation from service) Reg. 1.409A-1(b)(9)(v)

o Reimbursements for expenses SP could otherwise deduct under §§162, 167, e.g., moving expenses, outplacement expenses if:

• Time period limited to two years following separation year

• Medical benefits incurred and paid by SP otherwise deductible under §213 are limited to COBRA coverage period

• Di minimis payment limit to §402(g)(1)(B) amount, if no exception

o Indemnification and insurance plans

o Legal settlements for FLSA

o Educational benefit plans for SP (and no other, i.e., not spouse or dependents)

GUNSTER

DEFINITIONS

77

Substantial risk of forfeiture (SROF) 1.409A-1(d)(1) o Conditioned on the performance of future services or the occurrence of a

condition related to the purpose of the compensation, and

o The possibility of forfeiture is substantial and will be enforced.

Performance-based compensation 1.409A-1(e)(1)

o Compensation is contingent on the satisfaction of pre-established organizational or individual performance criteria relating to a performance period of at least 12 consecutive months.

o Criteria must be established in writing within 90 days after commencement of the relevant 12 month period.

o Compensation based on stock valuation increase is performance-based .

Service provider (SP) 1.409A-1(f)(1)

o Includes an individual, corporation, S corporation, partnership personal service corporation that reports on cash basis accounting

GUNSTER

DEFINITIONS (CONT.)

78

o Independent contractors are generally not SPs if SP:

• Not an employee or on board of directors

• Provides significant services to two or more SRs

• SP not related to SR

• Services are not “management services”

Service recipient (SR) 1.409A-1(g)

o The person for whom the services are performed and with whom the legally binding obligation arises

o Aggregation rules for SR apply - §§414(b) & (c) but “50%” for “80%”

Separation from service (SFS) 1.409A-1(h)

o Death, disability, retirement or termination of employment

o Employment continues up to six months for military leave, sick leave or other bona fide absence, unless there is a reasonable expectation or return to employment.

GUNSTER

DEFINITIONS (CONT.)

79

o Termination of employment based on facts and circumstances

• Employer and employee agree that no further services to be provided either as employee or independent contractor and services:

- Decrease to a 20% level pre-SFS presumes termination - Services at 50% or more presumed not a SFS

o In a sale or disposition of “substantial” assets the SR (seller) and the unrelated buyer may agree whether SPs being transferred to buyer have a SFS provided all SPs are treated consistently. Reg. 1.409-1(h)(4)

Specified employee (SE) Reg. 1.409-1(i)

o A SP who is a “key employee” (KE) of a publicly traded corporation

o KE is defined in §416(i)(1)(A)(i), (ii) or (iii)

• Employee with > $130,000 ($165,000 in 2013 with COLA) • 5% or more owner • 1% owner with > $150,000 (no COLA)

GUNSTER

DEFINITIONS (CONT.)

80

o A SP is a SE if he/she is a KE on any Dec. 31 or at any time during the preceding 12-month period and becomes an SE for the 12-month period commencing on the following April 1.

o There are special rules to identify SE in corporate acquisitions.

Separation pay plan 1.409A-1(m)

o Any plan that provides for “separation pay” in whole or part upon SFS

o “Separation pay” is any deferral of compensation that will not be paid prior to a SFS, whether voluntary or involuntary.

Involuntary SFS Reg. 1.409A-1(n)

o SFS due to the independent exercise of the SR’s decision to terminate the SP other than due to SP’s implicit or explicit request

o “Good reason” SFS is treated for all 409A as an involuntary SFS.

• “Material negative change to the service relationship, e.g. material compensation reduction, duties, authority, location, etc.

• See safe harbor conditions in Reg. 1.409A-1(n)(2)(ii)(A)

• SFS must occur within a pre-determined period (2 years maximum) upon initial existence of good reason.

GUNSTER

DEFERRAL ELECTIONS REG. 1.409A-2

81

Deferral elections Reg. 1.409A-2(a)(below)

o General: Election to defer compensation by SP must be made by SP no later than close of SP’s taxable year next preceding the service year (3).

o Initial year limited exception: Election to defer may be made before the 30th day after eligibility, if vesting of the deferred benefits requires 12 months of employment (7).

o Fiscal year compensation: Election to defer must be made on or before SR’s immediately preceding fiscal year (6).

o Performance-based compensation: Election must be made at least 6 months before the end of the performance period (8).

o Contingent severance pay: Initial deferral election may be made at any time prior to obtaining a legally binding right to payment.

o Sales commissions: Compensation for services is the SR taxable year in which customer remits payment to SP (12).

• NOTE: Election includes (i) deferral election and (ii) time and form of payment, if the plan does not specify them.

GUNSTER

DEFERRAL ELECTIONS (CONT.)

82

Subsequent changes in time and form of payment Reg.409A-2(b)

o Includes any changes in (i) delay of payment or (ii) form of payment

o Plan must require:

• Election must occur at least 12 months before changes occur, and

• Payment must be deferred for at least 5 years from original payment date.

o “Payment” means:

• Each separately identifiable payment

• Life annuity is treated as one single payment.

• Installment payments (series of substantively equal payments) are treated as one single payment, unless plan provides otherwise.

o Rules apply to both participants and beneficiaries.

o Change in form of payment from series of payments to single payment is not a prohibited acceleration, if there is compliance with “change” rules.

GUNSTER

RULES RELATING TO FUNDING IRC

409A(B)

83

Offshore assets: Property set aside in a trust or other arrangement outside the U.S. to pay deferred compensation is deemed transferred pursuant to §83 at the time of the transfer offshore §409A(b)(1).

o Whether or not assets are subject to claims of employer’s general creditors

o Not applicable if substantially all the services are performed offshore

Financial condition of employer: §409A(b)(2)

o Property is deemed transferred pursuant to §83 as of the earlier of:

• Date that the plan first provides assets will become restricted to pay benefits with a change in the employer’s financial condition, or

• Date on which the assets are so restricted; and

• Regardless of whether assets are subject to claims of employer’s general creditors.

GUNSTER

FUNDING (CONT.)

84

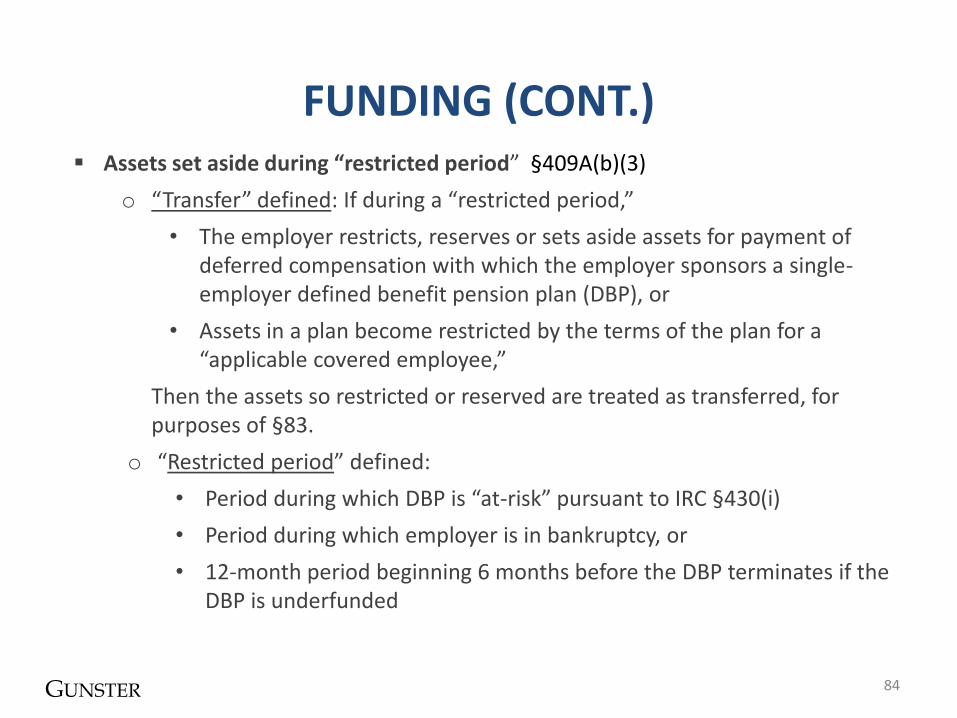

Assets set aside during “restricted period” §409A(b)(3)

o “Transfer” defined: If during a “restricted period,”

• The employer restricts, reserves or sets aside assets for payment of deferred compensation with which the employer sponsors a single-employer defined benefit pension plan (DBP), or

• Assets in a plan become restricted by the terms of the plan for a “applicable covered employee,”

Then the assets so restricted or reserved are treated as transferred, for purposes of §83.

o “Restricted period” defined:

• Period during which DBP is “at-risk” pursuant to IRC §430(i)

• Period during which employer is in bankruptcy, or

• 12-month period beginning 6 months before the DBP terminates if the DBP is underfunded

GUNSTER

FUNDING (CONT.)

85

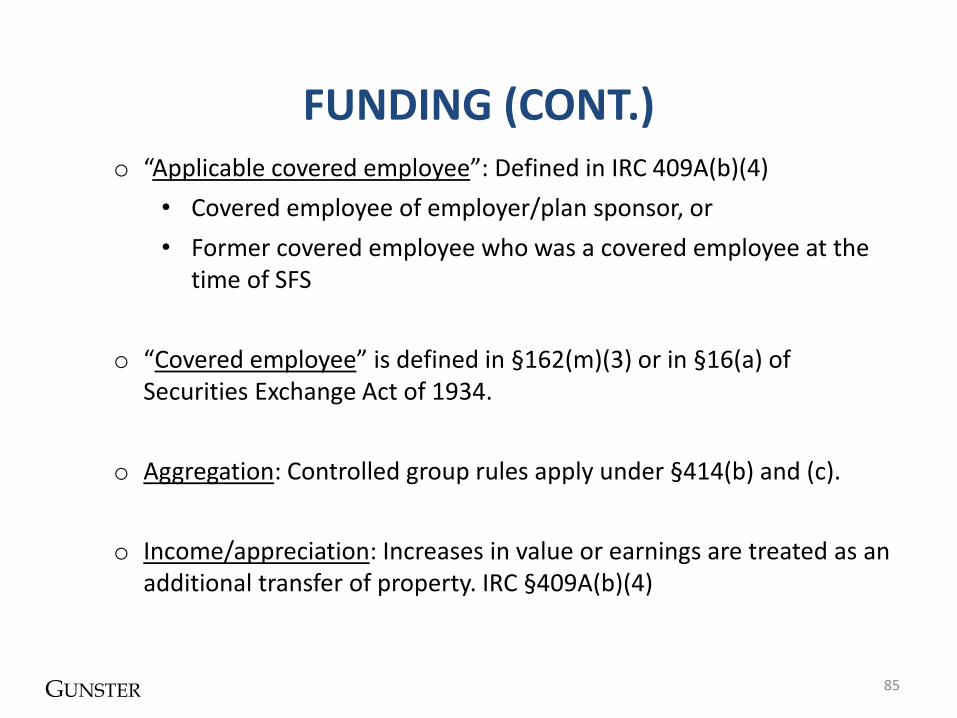

o “Applicable covered employee”: Defined in IRC 409A(b)(4)

• Covered employee of employer/plan sponsor, or

• Former covered employee who was a covered employee at the time of SFS

o “Covered employee” is defined in §162(m)(3) or in §16(a) of Securities Exchange Act of 1934.

o Aggregation: Controlled group rules apply under §414(b) and (c).

o Income/appreciation: Increases in value or earnings are treated as an additional transfer of property. IRC §409A(b)(4)

GUNSTER

PERMISSIBLE PAYMENTS REG. 1.409A-3

86

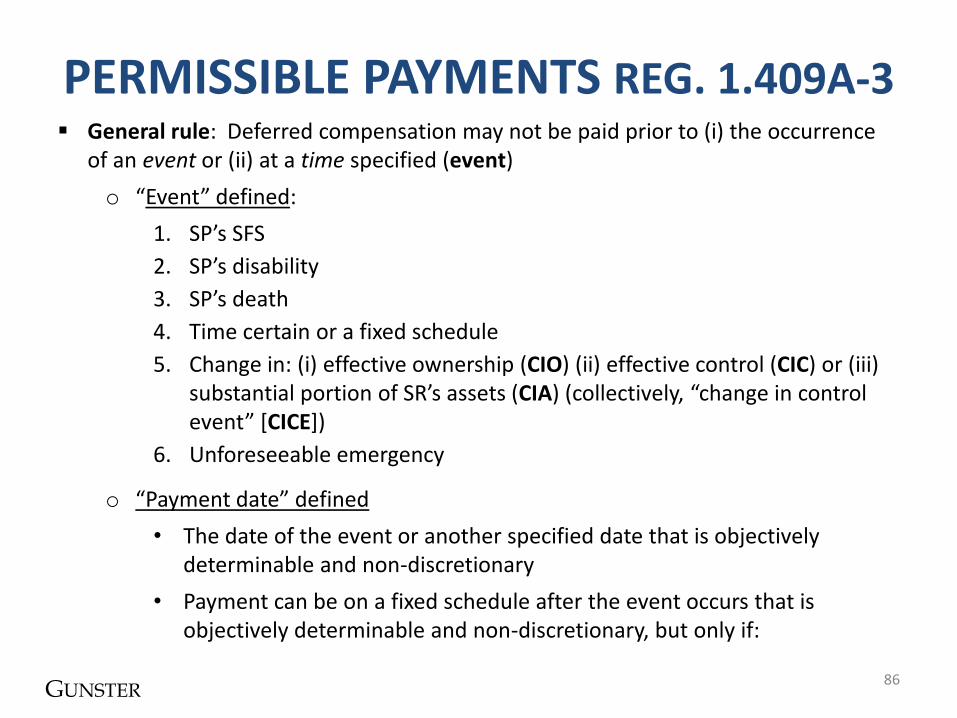

General rule: Deferred compensation may not be paid prior to (i) the occurrence of an event or (ii) at a time specified (event)

o “Event” defined:

1. SP’s SFS

2. SP’s disability

3. SP’s death

4. Time certain or a fixed schedule

5. Change in: (i) effective ownership (CIO) (ii) effective control (CIC) or (iii) substantial portion of SR’s assets (CIA) (collectively, “change in control event” *CICE])

6. Unforeseeable emergency

o “Payment date” defined

• The date of the event or another specified date that is objectively determinable and non-discretionary

• Payment can be on a fixed schedule after the event occurs that is objectively determinable and non-discretionary, but only if:

GUNSTER

PERMISSIBLE PAYMENTS (CONT.)

87

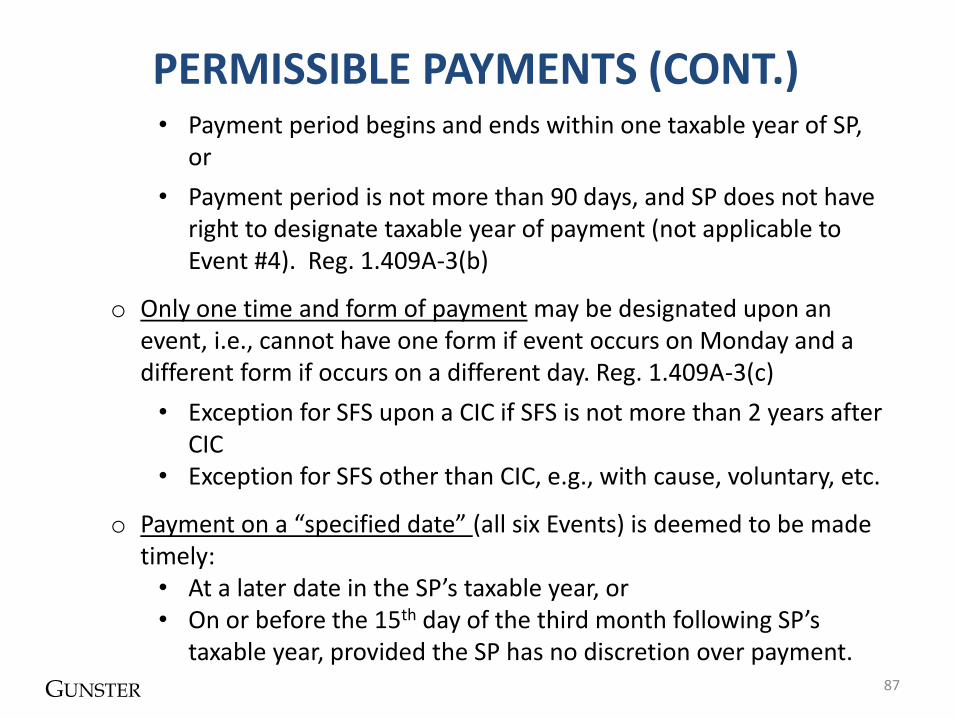

• Payment period begins and ends within one taxable year of SP, or

• Payment period is not more than 90 days, and SP does not have right to designate taxable year of payment (not applicable to Event #4). Reg. 1.409A-3(b)

o Only one time and form of payment may be designated upon an event, i.e., cannot have one form if event occurs on Monday and a different form if occurs on a different day. Reg. 1.409A-3(c)

• Exception for SFS upon a CIC if SFS is not more than 2 years after CIC

• Exception for SFS other than CIC, e.g., with cause, voluntary, etc.

o Payment on a “specified date” (all six Events) is deemed to be made timely:

• At a later date in the SP’s taxable year, or • On or before the 15th day of the third month following SP’s

taxable year, provided the SP has no discretion over payment.

GUNSTER

PERMISSIBLE PAYMENTS (CONT.)

88

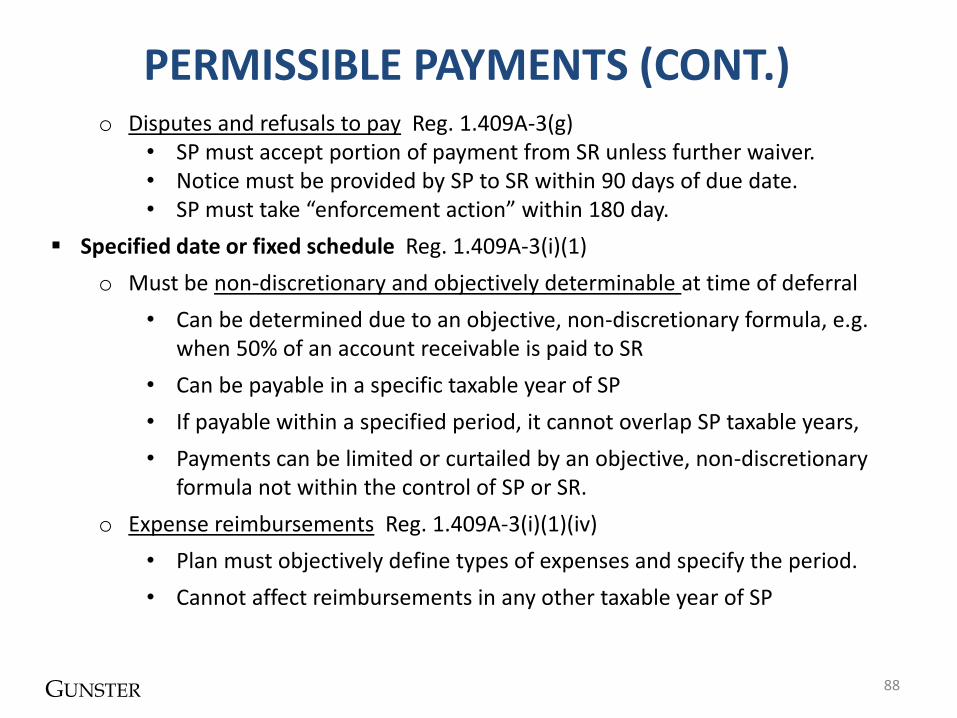

o Disputes and refusals to pay Reg. 1.409A-3(g) • SP must accept portion of payment from SR unless further waiver. • Notice must be provided by SP to SR within 90 days of due date. • SP must take “enforcement action” within 180 day.

Specified date or fixed schedule Reg. 1.409A-3(i)(1)

o Must be non-discretionary and objectively determinable at time of deferral

• Can be determined due to an objective, non-discretionary formula, e.g. when 50% of an account receivable is paid to SR

• Can be payable in a specific taxable year of SP

• If payable within a specified period, it cannot overlap SP taxable years,

• Payments can be limited or curtailed by an objective, non-discretionary formula not within the control of SP or SR.

o Expense reimbursements Reg. 1.409A-3(i)(1)(iv)

• Plan must objectively define types of expenses and specify the period.

• Cannot affect reimbursements in any other taxable year of SP

GUNSTER

PERMISSIBLE PAYMENTS (CONT.)

89

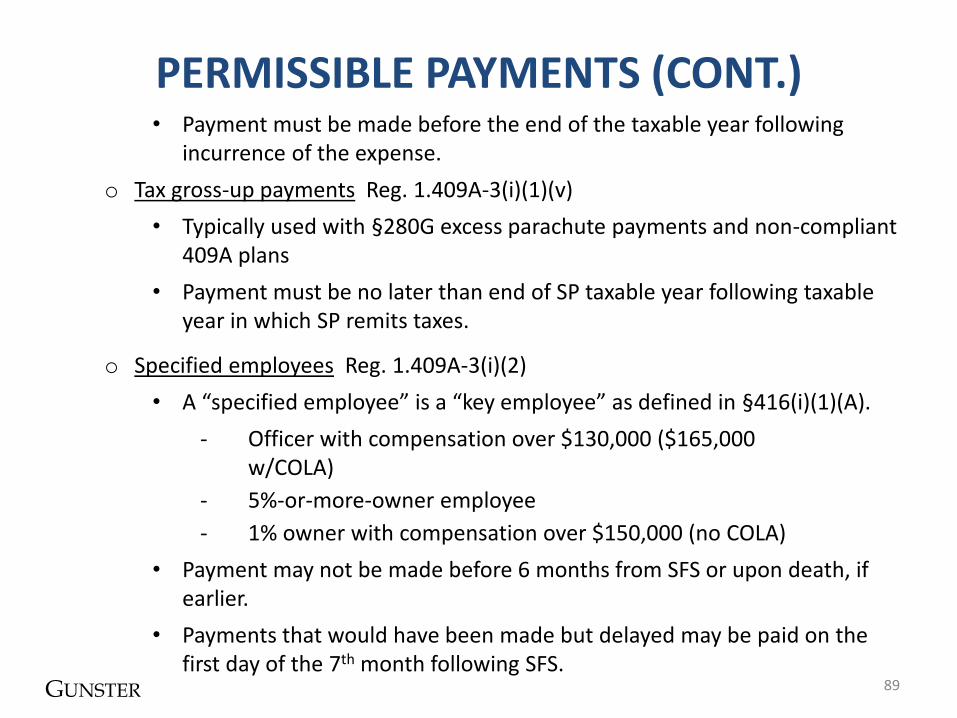

• Payment must be made before the end of the taxable year following incurrence of the expense.

o Tax gross-up payments Reg. 1.409A-3(i)(1)(v)

• Typically used with §280G excess parachute payments and non-compliant 409A plans

• Payment must be no later than end of SP taxable year following taxable year in which SP remits taxes.

o Specified employees Reg. 1.409A-3(i)(2)

• A “specified employee” is a “key employee” as defined in §416(i)(1)(A).

- Officer with compensation over $130,000 ($165,000 w/COLA)

- 5%-or-more-owner employee

- 1% owner with compensation over $150,000 (no COLA)

• Payment may not be made before 6 months from SFS or upon death, if earlier.

• Payments that would have been made but delayed may be paid on the first day of the 7th month following SFS.

GUNSTER

PERMISSIBLE PAYMENTS (CONT.)

90

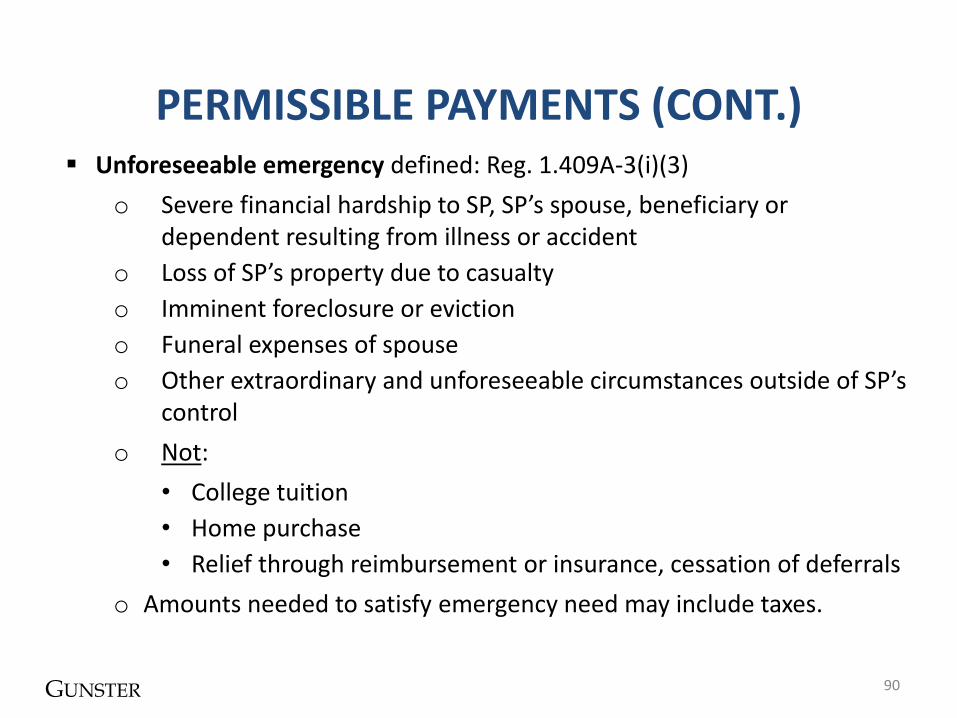

Unforeseeable emergency defined: Reg. 1.409A-3(i)(3)

o Severe financial hardship to SP, SP’s spouse, beneficiary or dependent resulting from illness or accident

o Loss of SP’s property due to casualty

o Imminent foreclosure or eviction

o Funeral expenses of spouse

o Other extraordinary and unforeseeable circumstances outside of SP’s control

o Not:

• College tuition

• Home purchase

• Relief through reimbursement or insurance, cessation of deferrals

o Amounts needed to satisfy emergency need may include taxes.

GUNSTER

PERMISSIBLE PAYMENTS (CONT.)

91

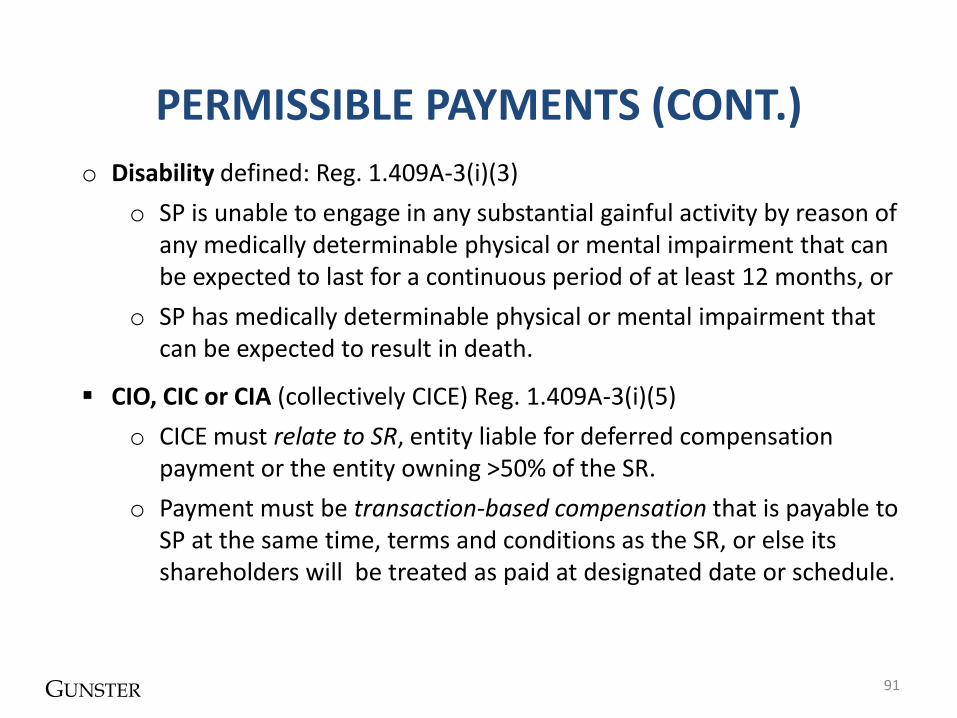

o Disability defined: Reg. 1.409A-3(i)(3)

o SP is unable to engage in any substantial gainful activity by reason of any medically determinable physical or mental impairment that can be expected to last for a continuous period of at least 12 months, or

o SP has medically determinable physical or mental impairment that can be expected to result in death.

CIO, CIC or CIA (collectively CICE) Reg. 1.409A-3(i)(5)

o CICE must relate to SR, entity liable for deferred compensation payment or the entity owning >50% of the SR.

o Payment must be transaction-based compensation that is payable to SP at the same time, terms and conditions as the SR, or else its shareholders will be treated as paid at designated date or schedule.

GUNSTER

PERMISSIBLE PAYMENTS (CONT.)

92

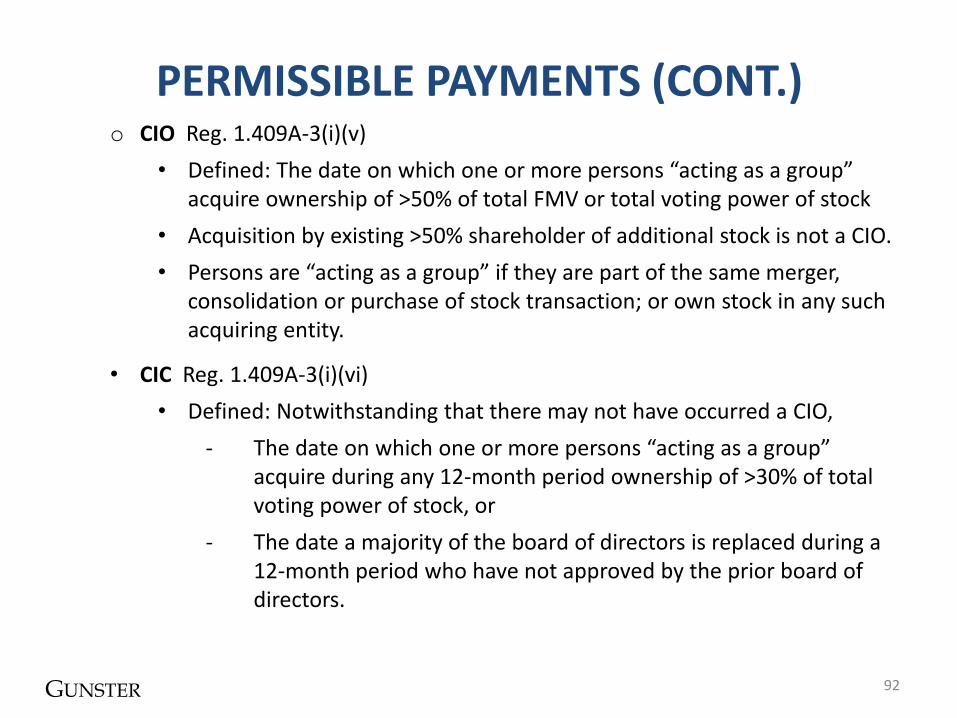

o CIO Reg. 1.409A-3(i)(v)

• Defined: The date on which one or more persons “acting as a group” acquire ownership of >50% of total FMV or total voting power of stock

• Acquisition by existing >50% shareholder of additional stock is not a CIO.

• Persons are “acting as a group” if they are part of the same merger, consolidation or purchase of stock transaction; or own stock in any such acquiring entity.

• CIC Reg. 1.409A-3(i)(vi)

• Defined: Notwithstanding that there may not have occurred a CIO,

- The date on which one or more persons “acting as a group” acquire during any 12-month period ownership of >30% of total voting power of stock, or

- The date a majority of the board of directors is replaced during a 12-month period who have not approved by the prior board of directors.

GUNSTER

PERMISSIBLE PAYMENTS (CONT.)

93

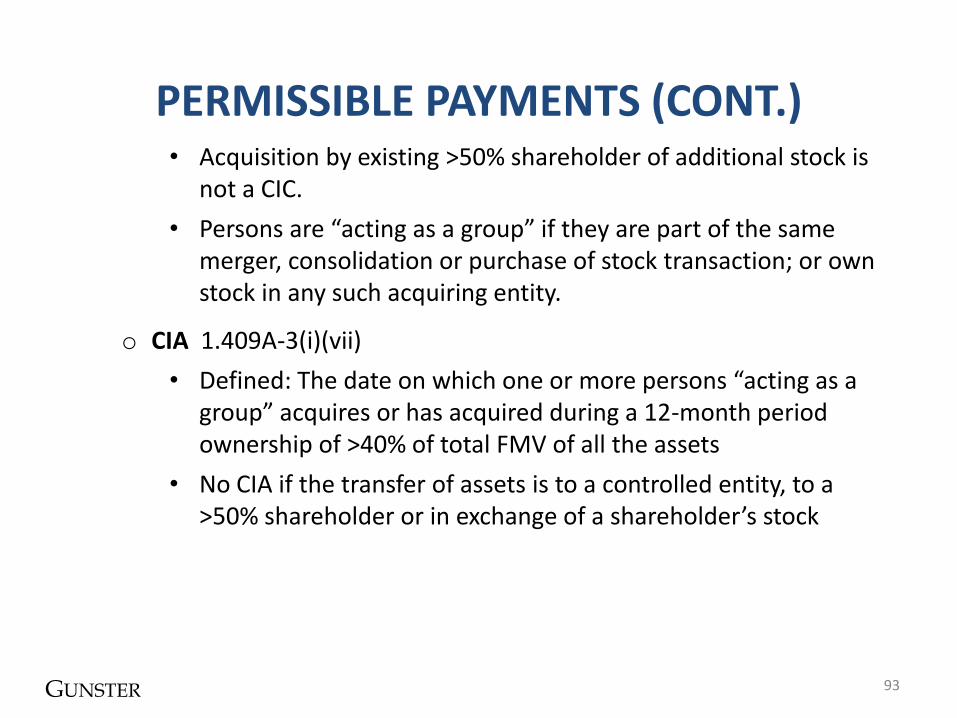

• Acquisition by existing >50% shareholder of additional stock is not a CIC.

• Persons are “acting as a group” if they are part of the same merger, consolidation or purchase of stock transaction; or own stock in any such acquiring entity.

o CIA 1.409A-3(i)(vii)

• Defined: The date on which one or more persons “acting as a group” acquires or has acquired during a 12-month period ownership of >40% of total FMV of all the assets

• No CIA if the transfer of assets is to a controlled entity, to a >50% shareholder or in exchange of a shareholder’s stock

GUNSTER

PERMISSIBLE PAYMENTS (CONT.)

94

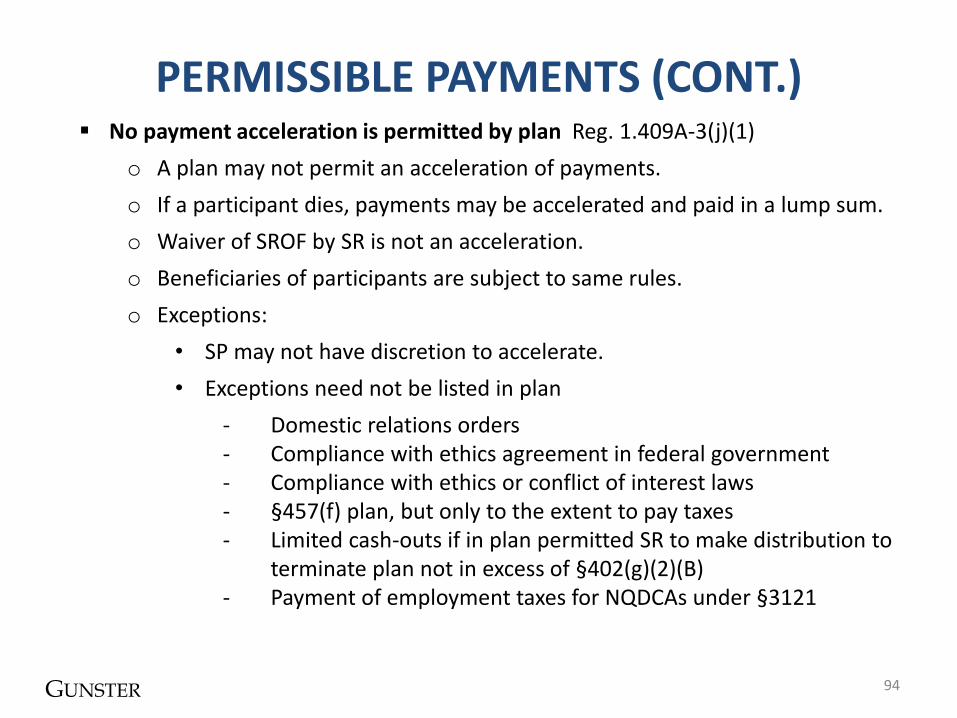

No payment acceleration is permitted by plan Reg. 1.409A-3(j)(1)

o A plan may not permit an acceleration of payments.

o If a participant dies, payments may be accelerated and paid in a lump sum.

o Waiver of SROF by SR is not an acceleration.

o Beneficiaries of participants are subject to same rules.

o Exceptions:

• SP may not have discretion to accelerate.

• Exceptions need not be listed in plan

- Domestic relations orders - Compliance with ethics agreement in federal government - Compliance with ethics or conflict of interest laws - §457(f) plan, but only to the extent to pay taxes - Limited cash-outs if in plan permitted SR to make distribution to

terminate plan not in excess of §402(g)(2)(B) - Payment of employment taxes for NQDCAs under §3121

GUNSTER

PERMISSIBLE PAYMENTS (CONT.)

95

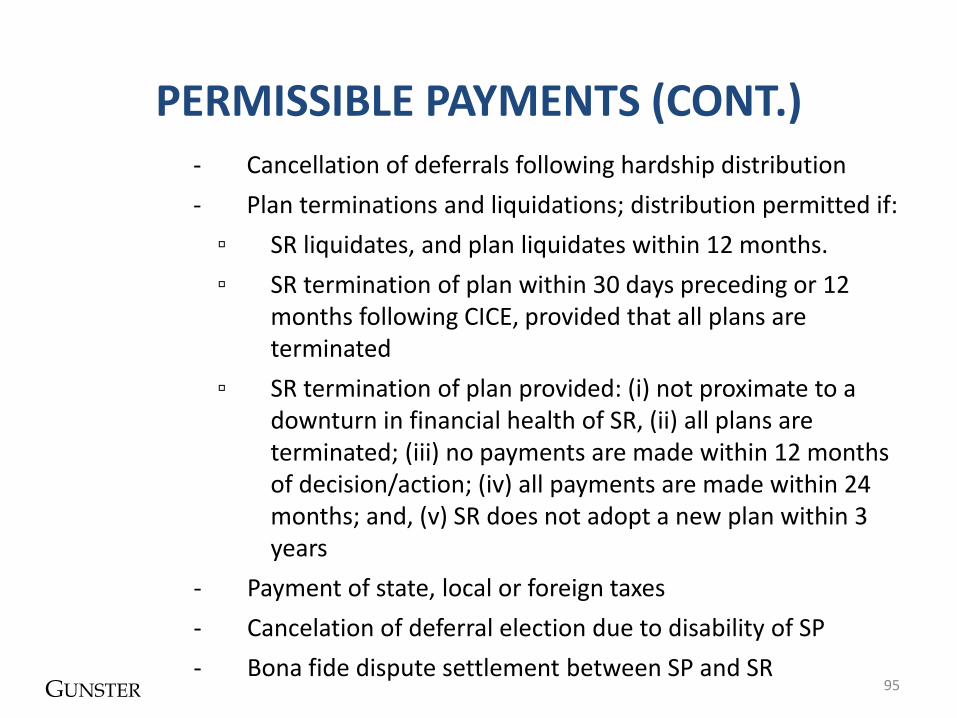

- Cancellation of deferrals following hardship distribution

- Plan terminations and liquidations; distribution permitted if:

▫ SR liquidates, and plan liquidates within 12 months.

▫ SR termination of plan within 30 days preceding or 12 months following CICE, provided that all plans are terminated

▫ SR termination of plan provided: (i) not proximate to a downturn in financial health of SR, (ii) all plans are terminated; (iii) no payments are made within 12 months of decision/action; (iv) all payments are made within 24 months; and, (v) SR does not adopt a new plan within 3 years

- Payment of state, local or foreign taxes

- Cancelation of deferral election due to disability of SP

- Bona fide dispute settlement between SP and SR

GUNSTER

PERMISSIBLE PAYMENTS (CONT.)

96

o Linkage to qualified employer plans Reg. 1.409A-3(j)(5)

• Decreases in amounts deferred to plan due to the amount determined by formula in a qualified plan are not an acceleration.

o Changes in elections under cafeteria plan do not result in an accelerated payment under a plan.

Slide Intentionally Left Blank

GUNSTER

APPLICATION OF

409A AND EFFECTIVE DATES REG. 1.409A-6

98

Effective date: §409A applies to amounts deferred in taxable years beginning after Dec. 31, 2004 and amounts deferred prior to Jan. 1, 2005, if the plan is materially modified after Oct. 3, 2004.

o Amounts are considered deferred prior to Jan. 1, 2005 only if the benefits were not subject to a SROF at that date.

o Benefits that were not substantially vested as of Dec. 31, 2004 are treated as being deferred on and after Jan. 1, 2005.

Material modifications: A modification is material if a benefit or right existing as of Oct. 3, 2004, is materially enhanced or a new material benefit or right is added that affects amounts earned and vested before Jan. 1, 2005. Reg. 1.409A-3(a)(4)(i) o Examples:

• Addition of a provision permitting distribution in SP discretion if a 20% forfeiture occurs

• SR exercises discretion to accelerate vesting prior to Jan. 1, 2005.

GUNSTER

409A APPLICATION (CONT.)

99

o Amendment of a plan to bring it into 409A compliance is not a material modification. Reg. 1.409A-6(a)(4)(i)

o Adoption of a new plan after Oct. 3, 2004 and prior to Jan. 1, 2005 is a material modification of a plan.

o Suspension or termination of a plan is not a material modification if permitted by the terms of the plan. Reg. 1.409A-6(a)(4)(iii)

NOTE: This regulation was effective for taxable years beginning or after Jan. 1, 2008.