employee tax setup guide - adp · enterprise payroll documentation library ... 8-3 supplemental...

TRANSCRIPT

HR. Payro

ADP Enterprise HR®

Employee Tax Setup Guide

Versions 5.0 and higherVersion 5.03

ll. Benefits.

Copyright 1993–2013 by ADP, Inc.Portions copyright 1988–1998 PeopleSoft, Inc.

Third-Party Copyright InformationFor copyright information about the third-party software used in ADP’s HR/payroll solutions, click Copyright Information.

This manual supports ADP Enterprise HR Versions 5.0 and higher. Published Fall 2013.

All rights reserved. The information contained in this document is proprietary and confidential to ADP. No part of this document may be reproduced or transmitted in any form or by any means, mechanical or electronic, including photography and recording, for any purpose without the express written permission of ADP.

The core software technology for ADP’s product offering has been acquired through a licensing agreement with PeopleSoft, Inc., Pleasanton, California. Portions of the following text have been copied by permission of PeopleSoft, Inc. Product specifications are subject to change without notice. No product warranty should be implied from this document.

ADP and the ADP Logo are registered trademarks of ADP of North America, Inc. Enterprise HR is a service mark of ADP of North America Inc. Adobe is a registered trademark and Acrobat is a trademark of Adobe Systems Incorporated. Lotus Notes is a registered trademark of Lotus Development Corporation. Microsoft, Windows, Internet Explorer are registered trademarks, and Excel is a trademark of Microsoft Corporation. PeopleSoft and Java are registered trademarks of Oracle Corporation.SQR is a registered trademark of Hyperion Solutions Corporation. PCL is a registered trademark of Hewlett-Packard Company.

Printed in the United States.

Contents

About This Guide

Introduction. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .xviAudience for This Guide . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . xviiEnterprise Payroll Documentation Library. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .xviiiWhat’s in This Book. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .xixWhat’s New . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . xxRelated Documentation . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . xxDocumentation Conventions . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .xxiProviding Comments . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .xxiii

1 Setting Up Federal Tax Withholding

Understanding the Basics . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .1-2Paying a New Employee . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .1-2Transferring an Employee to Another Company . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .1-2Taxing in Multiple Jurisdictions . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .1-2

Understanding ADP Enterprise HR Calculations. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .1-3Regular Earnings. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .1-3Other Earnings . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .1-3Multiple Earnings . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .1-4Supplemental. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .1-4

Advance Payments for Earned Income Credit . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .1-5Selecting the Federal Filing Status and Entering Withholding Data . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .1-6

Selecting the Filing Status. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .1-6Entering Withholding Allowances . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .1-6

Setting Up Federal Taxes for an Employee . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .1-7Entering IRS Tax Lock-In Data . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .1-13

Specifying Tax Lock-In Data for an Employee . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .1-13Verifying Allowances and Filing Status . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .1-16

Printing a Hard Copy of an Electronically Submitted Federal W-4 (PER052) . . . . . . . . . . . . . . . . . . . . .1-17

2 Setting Up State Tax Withholding

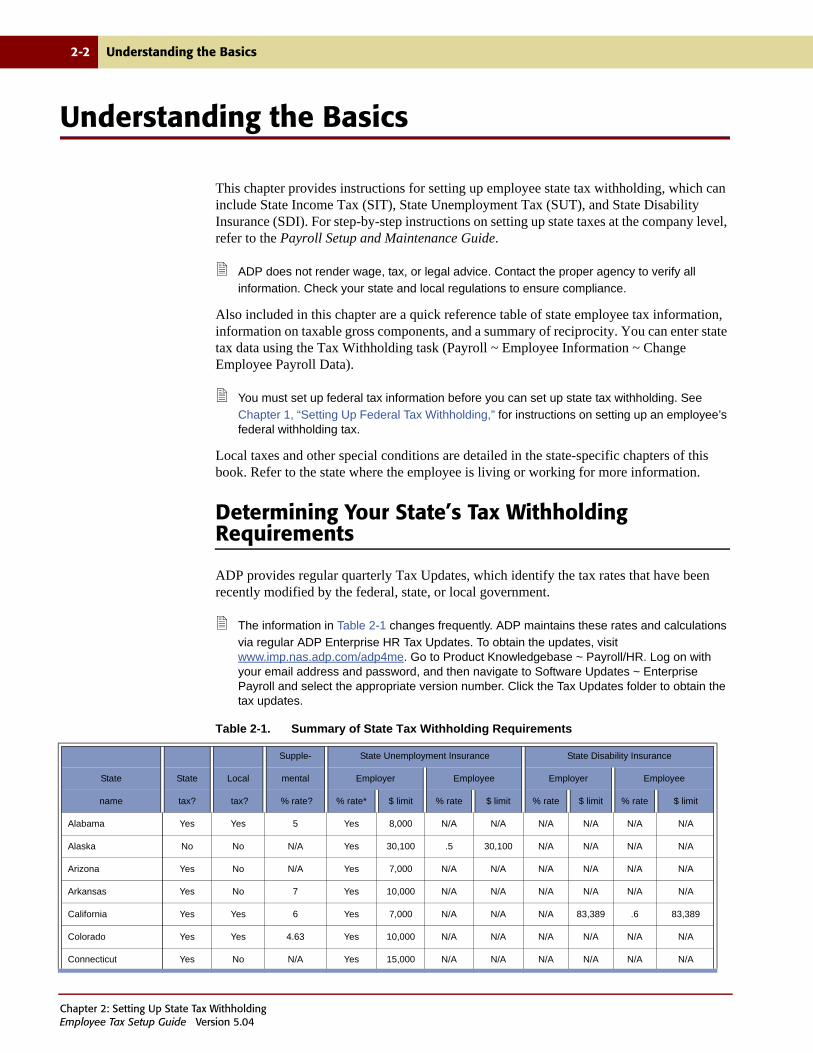

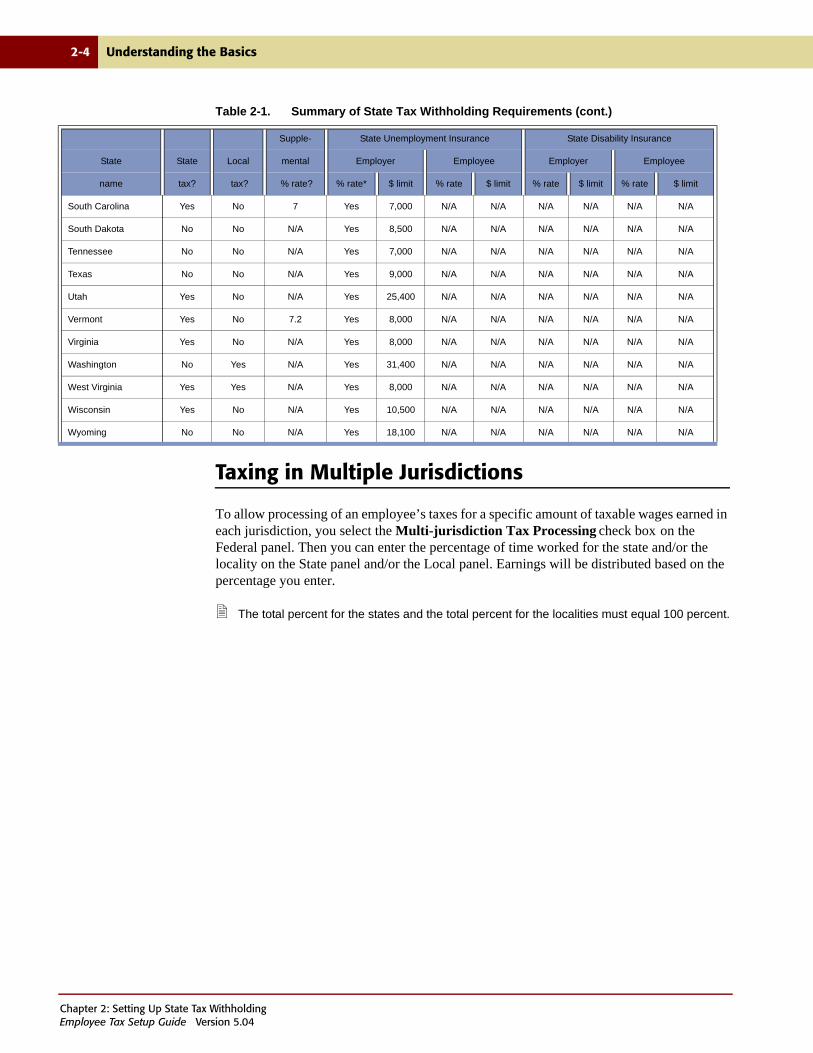

Understanding the Basics . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .2-2Determining Your State’s Tax Withholding Requirements . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .2-2Taxing in Multiple Jurisdictions . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .2-4

Using Form W-4 for State Tax Purposes . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .2-5Entering State Tax Data for an Employee . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .2-6

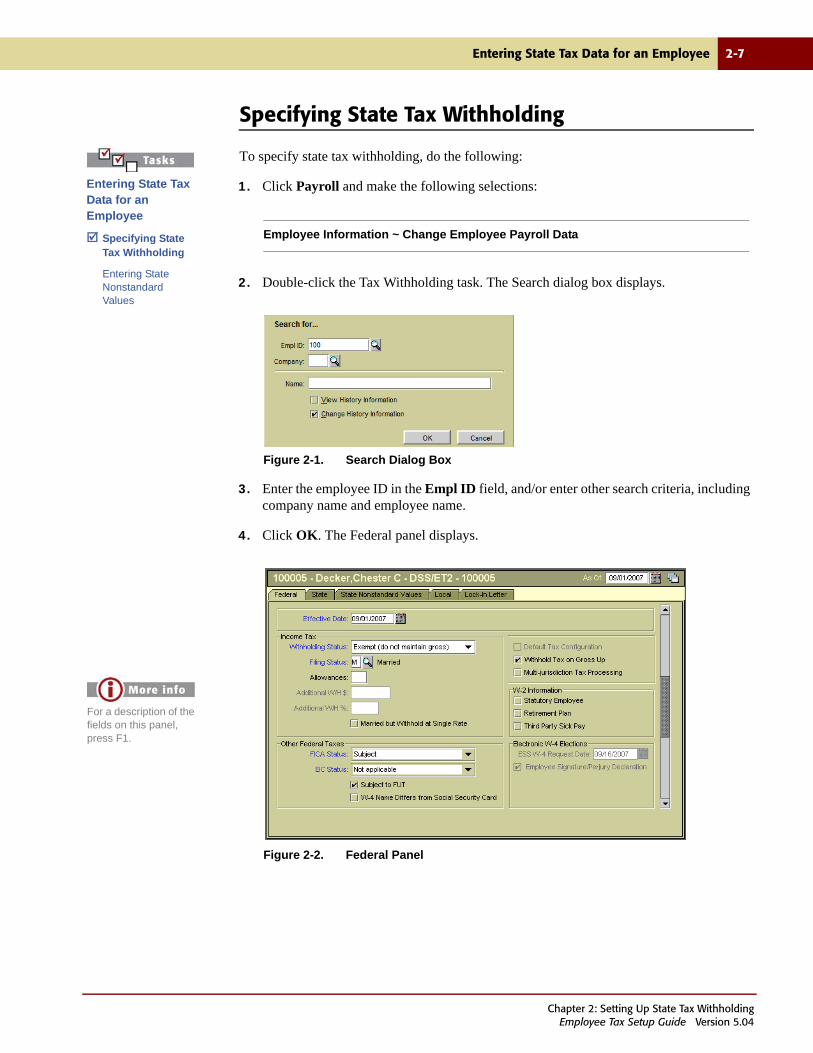

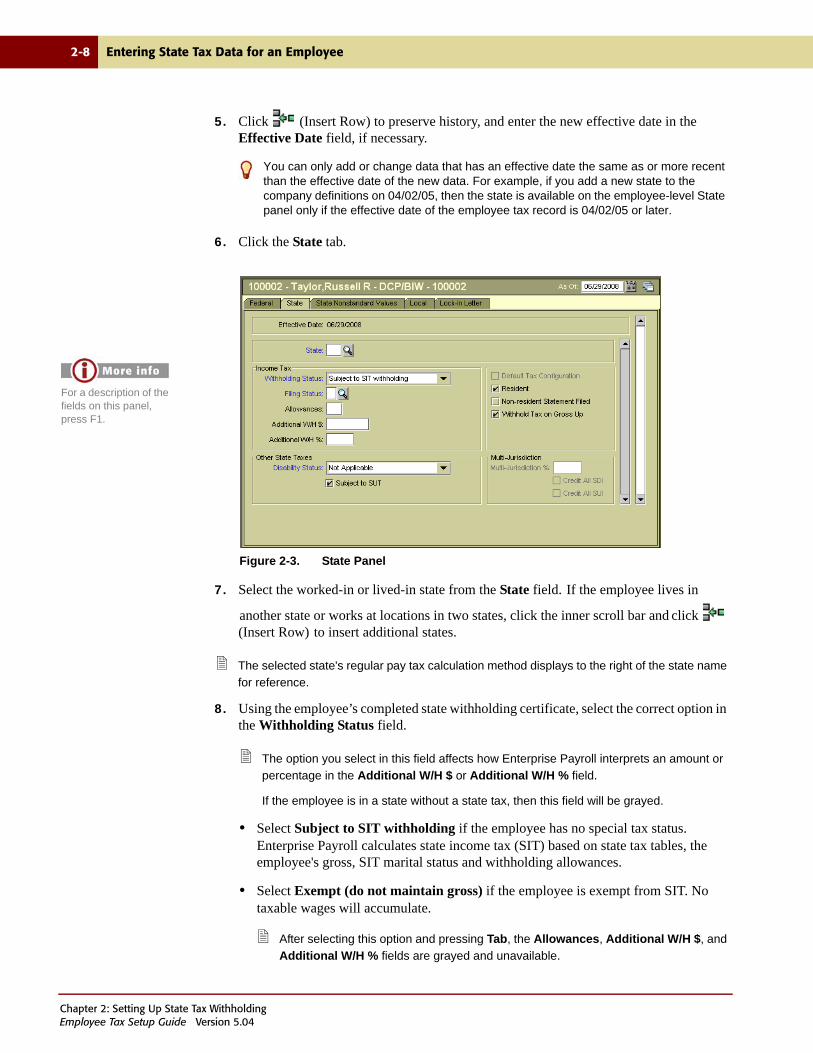

Specifying State Tax Withholding . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .2-7Entering State Nonstandard Values . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .2-12

ContentsEmployee Tax Setup Guide Version 5.04

iv Contents

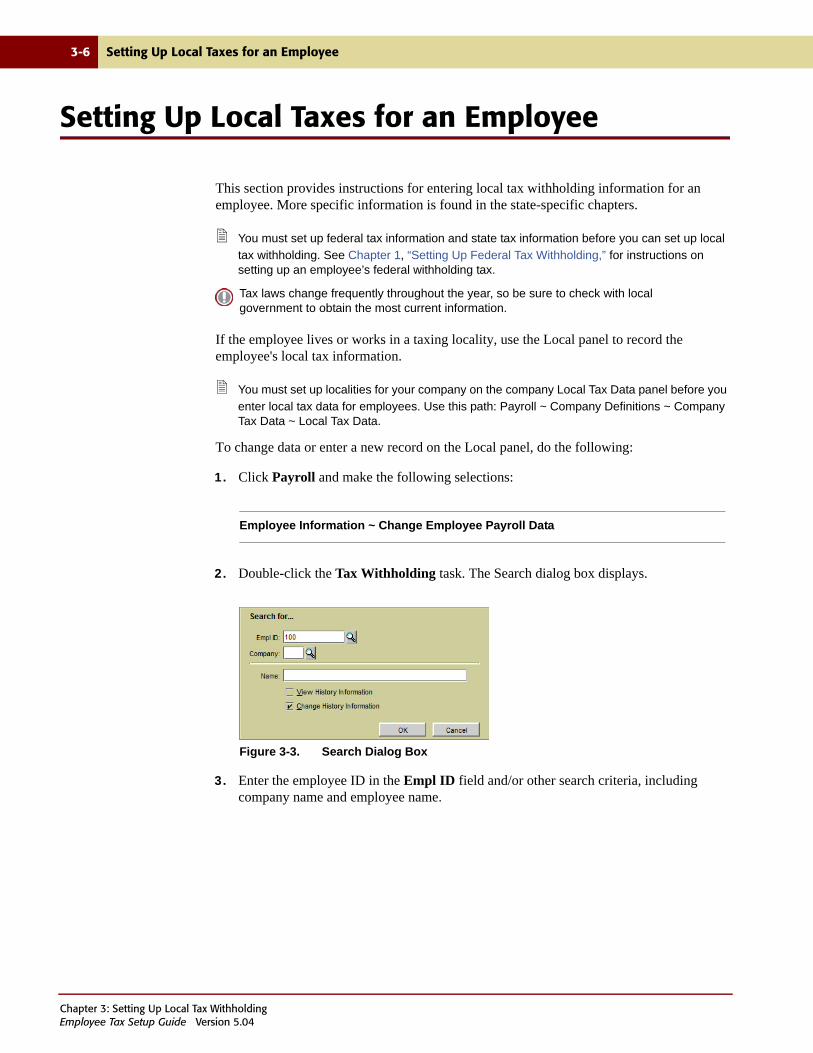

3 Setting Up Local Tax Withholding

Understanding the Basics . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 3-2Understanding the Different Types of Local Taxes. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 3-3Calculating Local Taxes . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 3-3Taxing in Multiple Jurisdictions . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 3-3

Determining Whether Local Taxes Apply . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 3-4Setting Up Local Taxes for an Employee . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 3-6

4 Alabama—Setting Up Employee Taxes

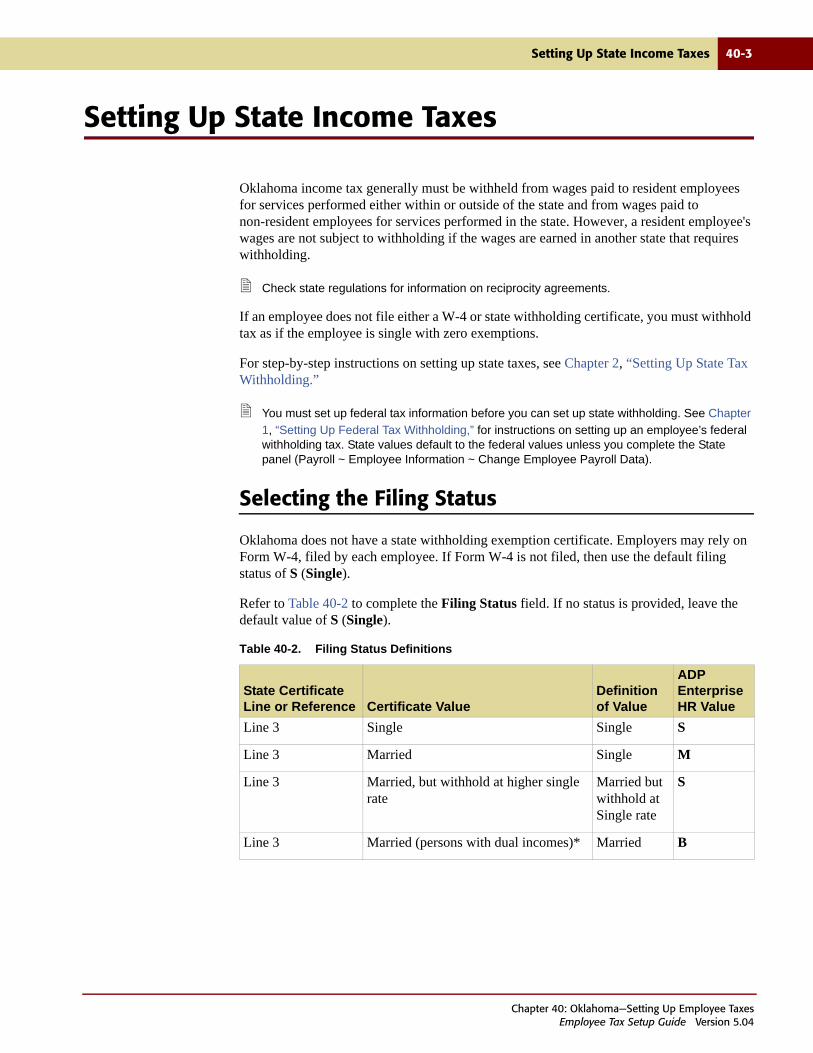

Summarizing Payroll Taxes . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 4-2Setting Up State Income Taxes . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 4-3

Selecting the Filing Status . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 4-3Entering Withholding Allowances. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 4-4Entering Additional Amounts . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 4-4

Setting Up Local Income Taxes . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 4-5Worked-in Taxes . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 4-5Special Conditions for Birmingham . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 4-5

5 Alaska—Setting Up Employee Taxes

Summarizing Payroll Taxes . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 5-2Setting Up State and Local Income Taxes . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 5-3

6 Arizona—Setting Up Employee Taxes

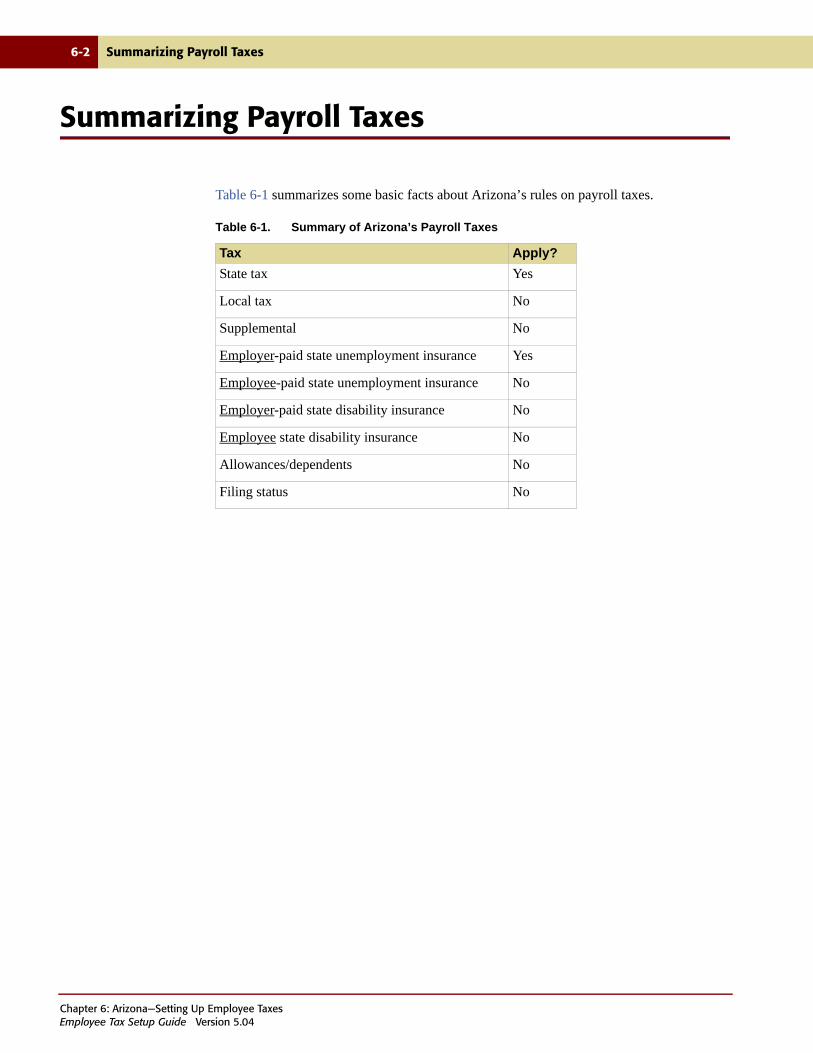

Summarizing Payroll Taxes . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 6-2Setting Up State Income Rates . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 6-3

Selecting the Filing Status . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 6-3Entering Withholding Allowances. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 6-3Entering Additional Amounts . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 6-4

Setting Up Local Income Taxes . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 6-5

7 Arkansas—Setting Up Employee Taxes

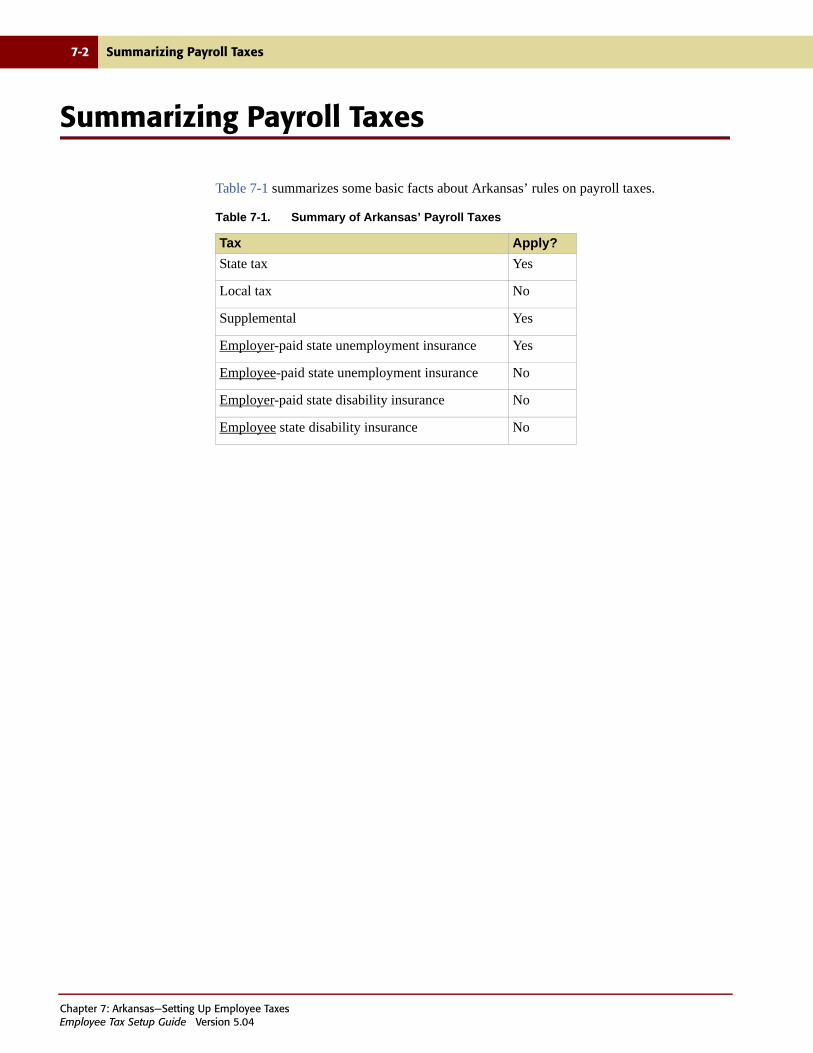

Summarizing Payroll Taxes . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 7-2Setting Up State Income Taxes . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 7-3

Selecting the Filing Status . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 7-3Entering Withholding Allowances. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 7-3Entering Additional Amounts . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 7-3

Setting Up Local Income Taxes . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 7-4

ContentsEmployee Tax Setup Guide Version 5.04

Contents v

8 California—Setting Up Employee Taxes

Summarizing Payroll Taxes . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .8-2Setting Up State Income Taxes . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .8-3

Supplemental Rates. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .8-3Selecting the Filing Status . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .8-4Entering Withholding Allowances . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .8-4Entering Personal Allowances . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .8-4Entering Additional Amounts . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .8-5Selecting the Disability Status . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .8-5

Setting Up Local Income Taxes . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .8-6

9 Colorado—Setting Up Employee Taxes

Summarizing Payroll Taxes . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .9-2Setting Up State Income Taxes . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .9-3

Selecting the Filing Status . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .9-3Entering Withholding Allowances . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .9-3Entering Additional Amounts . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .9-4

Setting Up Local Income Taxes . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .9-5Paying Local Taxes. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .9-5Entering Withholding Information . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .9-5

10 Connecticut—Setting Up Employee Taxes

Summarizing Payroll Taxes . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .10-2Setting Up State Income Taxes . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .10-3

Selecting the Filing Status . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .10-3Entering Withholding Allowances . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .10-4Entering Additional Amounts . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .10-4

Setting Up Local Income Taxes . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .10-5

11 Delaware—Setting Up Employee Taxes

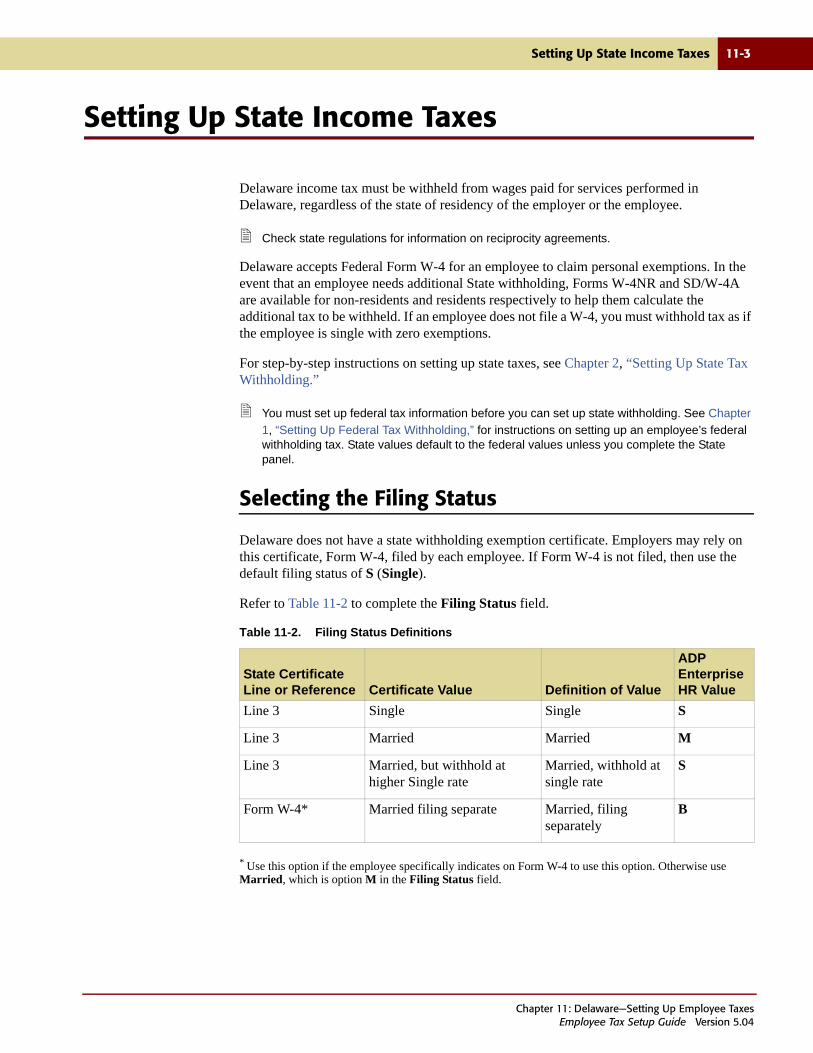

Summarizing Payroll Taxes . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .11-2Setting Up State Income Taxes . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .11-3

Selecting the Filing Status . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .11-3Entering Withholding Allowances . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .11-4Entering Additional Amounts . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .11-4

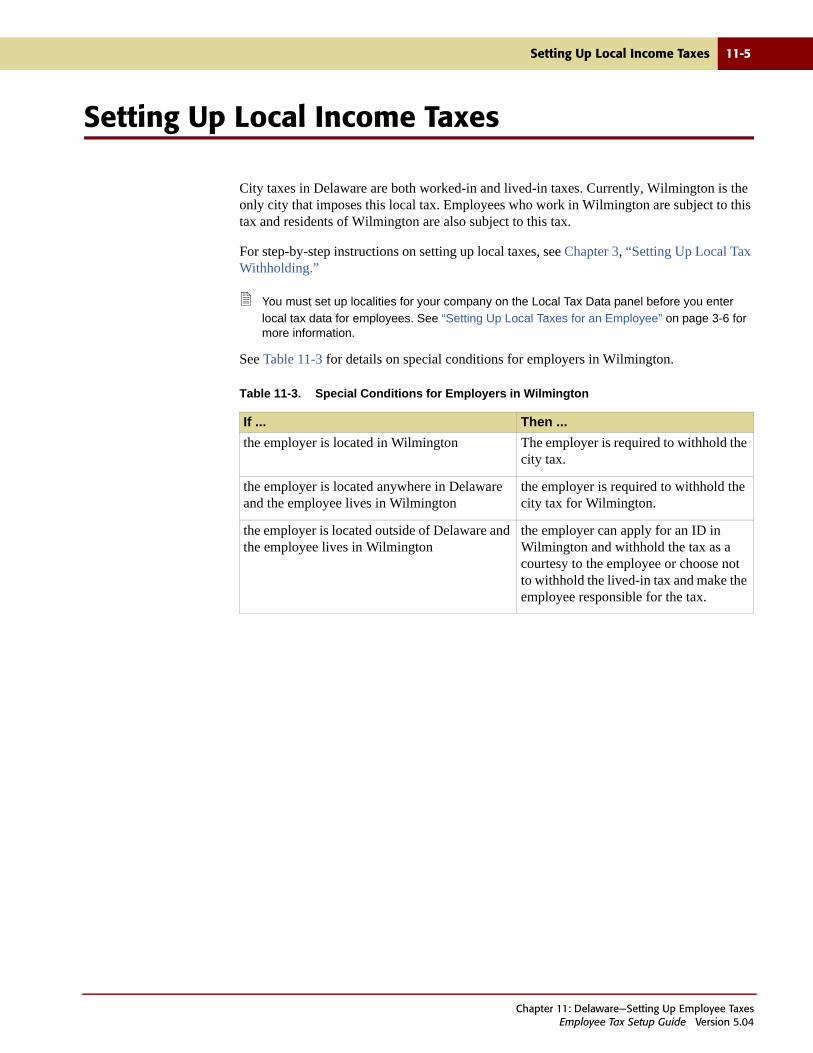

Setting Up Local Income Taxes . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .11-5

12 District of Columbia—Setting Up Employee Taxes

Summarizing Payroll Taxes . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .12-2

ContentsEmployee Tax Setup Guide Version 5.04

vi Contents

Setting Up State Income Taxes . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 12-3Selecting the Filing Status . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 12-3Entering Withholding Allowances. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 12-3Entering Additional Amounts . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 12-4

Setting Up Local Income Taxes . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 12-5

13 Florida—Setting Up Employee Taxes

Summarizing Payroll Taxes . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 13-2Setting Up State and Local Income Taxes . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 13-3

14 Georgia—Setting Up Employee Taxes

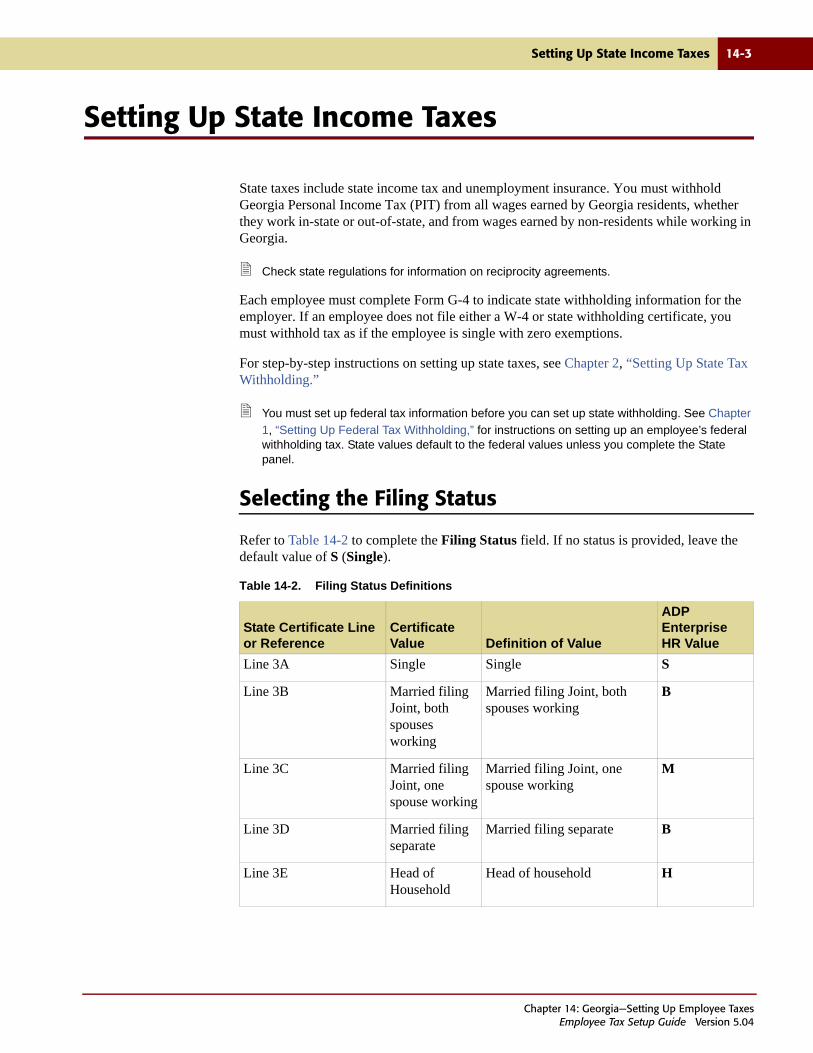

Summarizing Payroll Taxes . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 14-2Setting Up State Income Taxes . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 14-3

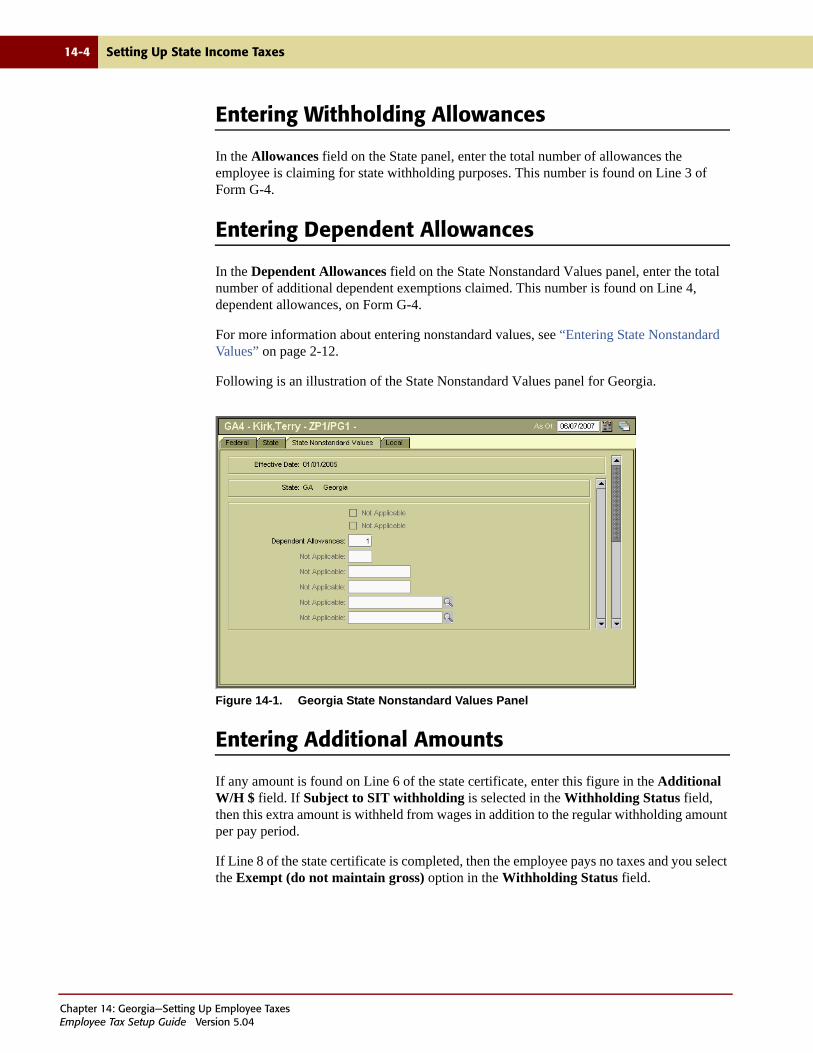

Selecting the Filing Status . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 14-3Entering Withholding Allowances. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 14-4Entering Dependent Allowances . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 14-4Entering Additional Amounts . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 14-4

Setting Up Local Income Taxes . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 14-5

15 Hawaii—Setting Up Employee Taxes

Summarizing Payroll Taxes . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 15-2Setting Up State Income Taxes . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 15-3

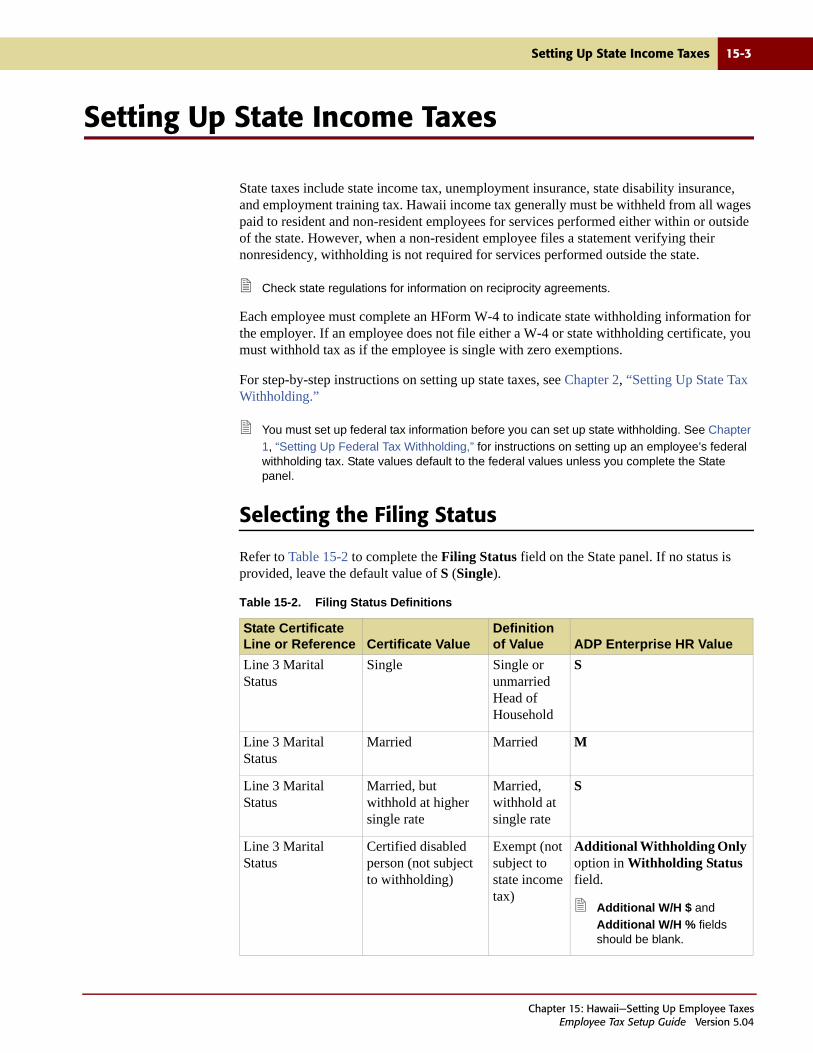

Selecting the Filing Status . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 15-3Entering Withholding Allowances. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 15-4Entering Additional Amounts . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 15-4Selecting the Disability Status . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 15-4

Setting Up Local Income Taxes . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 15-5

16 Idaho—Setting Up Employee Taxes

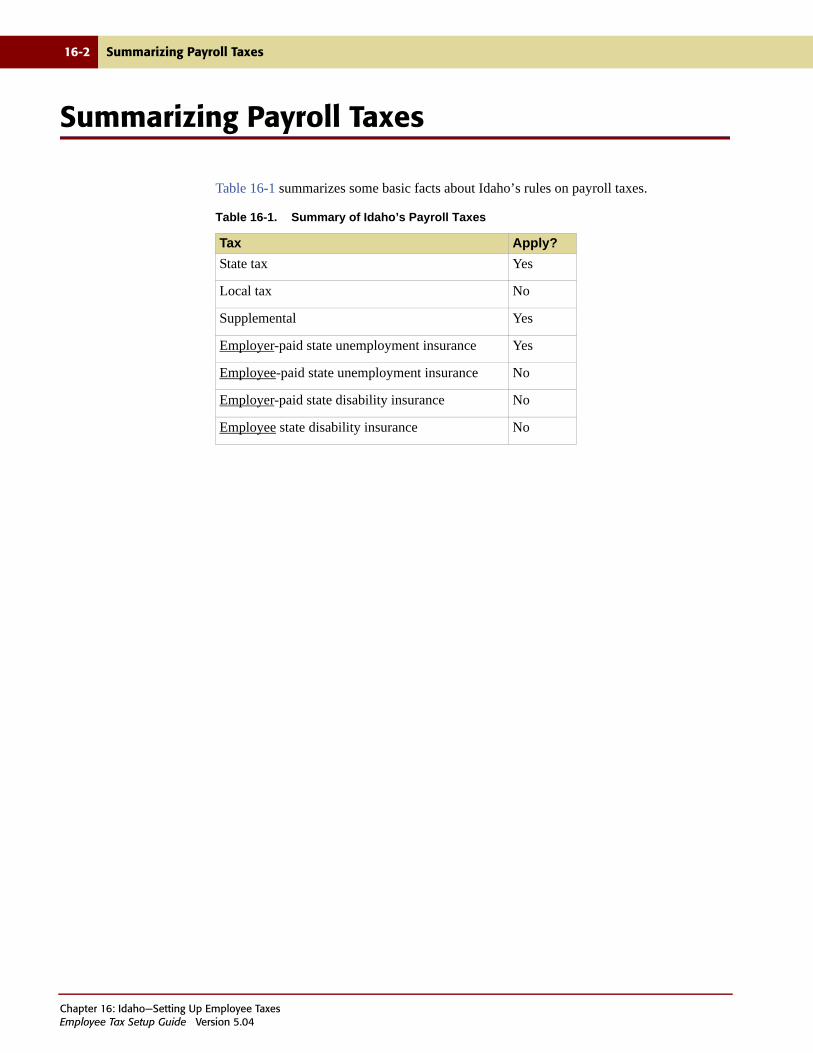

Summarizing Payroll Taxes . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 16-2Setting Up State Income Taxes . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 16-3

Selecting the Filing Status . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 16-3Entering Withholding Allowances. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 16-3Entering Additional Amounts . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 16-4

Setting Up Local Income Taxes . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 16-5

17 Illinois—Setting Up

ContentsEmployee Tax Setup Guide Version 5.04

Contents vii

Employee Taxes

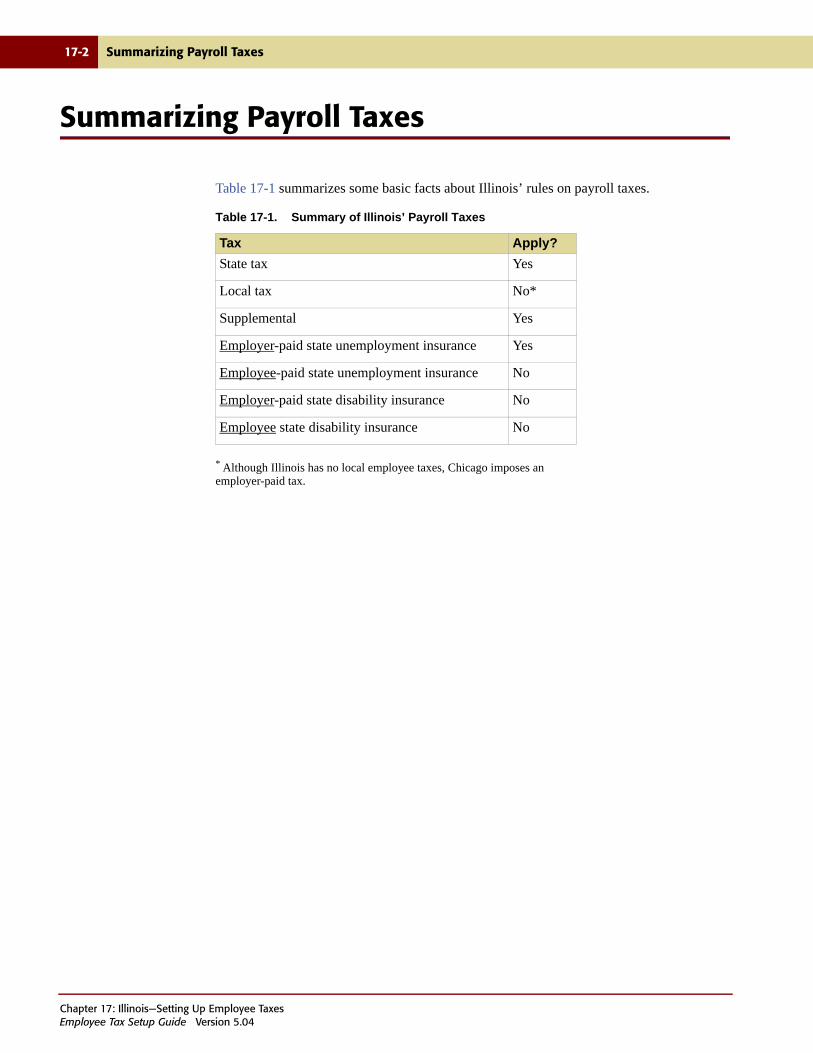

Summarizing Payroll Taxes . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .17-2Setting Up State Income Taxes . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .17-3

Selecting the Filing Status . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .17-3Entering Withholding Allowances . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .17-3Entering Personal Allowances . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .17-3Entering Additional Amounts . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .17-4

Setting Up Local Income Taxes . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .17-5

18 Indiana—Setting Up Employee Taxes

Summarizing Payroll Taxes . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .18-2Setting Up State Income Taxes . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .18-3

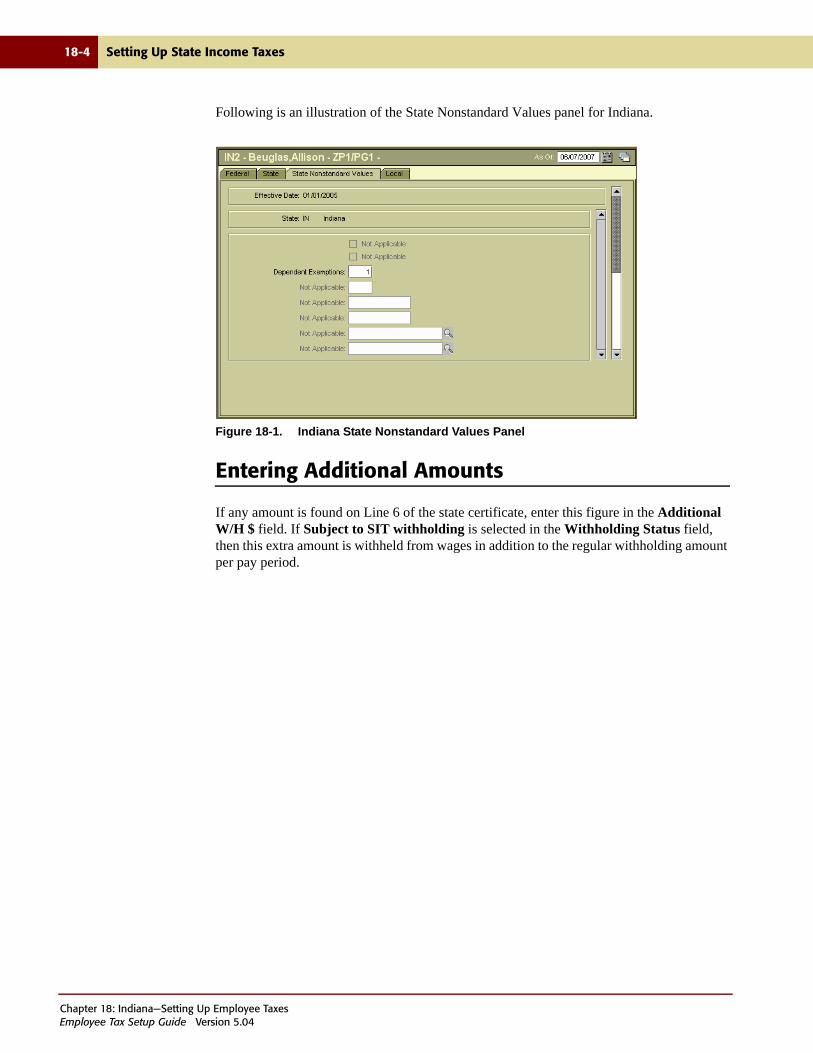

Selecting the Filing Status . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .18-3Entering Withholding Allowances . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .18-3Entering Dependent Exemptions . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .18-3Entering Additional Amounts . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .18-4

Setting Up Local Income Taxes . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .18-5Special Conditions . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .18-6

19 Iowa—Setting Up Employee Taxes

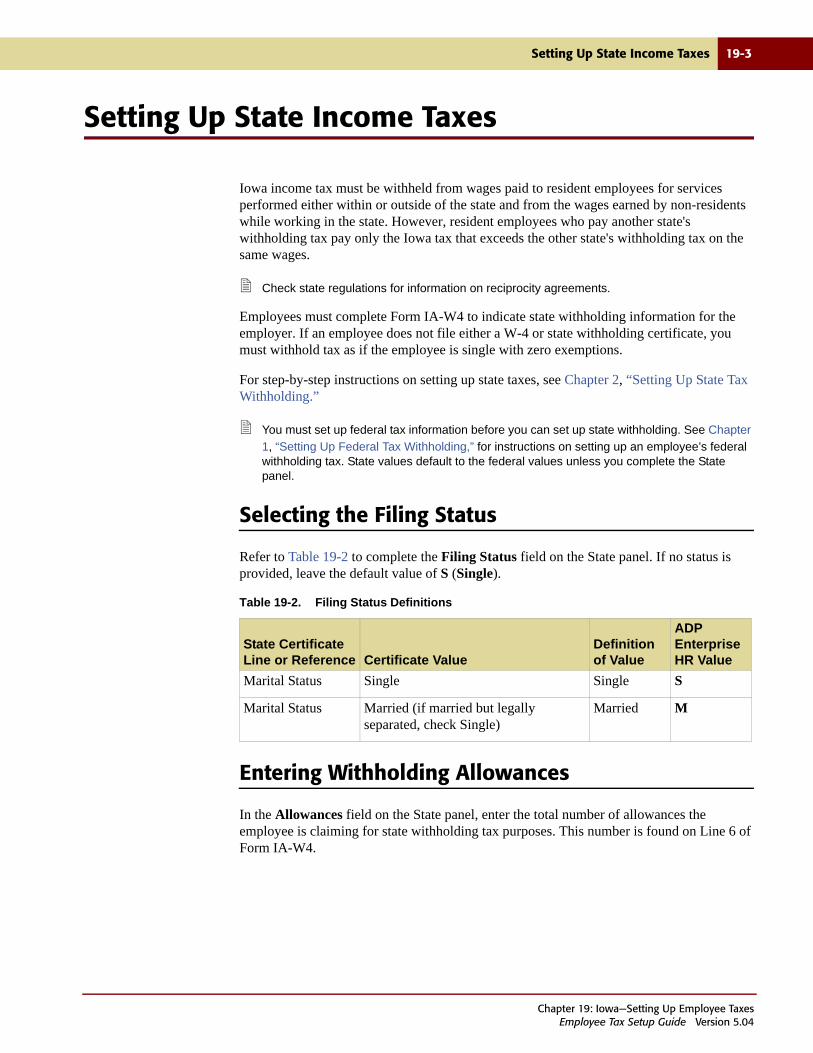

Summarizing Payroll Taxes . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .19-2Setting Up State Income Taxes . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .19-3

Selecting the Filing Status . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .19-3Entering Withholding Allowances . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .19-3Entering Additional Amounts . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .19-4

Setting Up Local Income Taxes . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .19-5

20 Kansas—Setting Up Employee Taxes

Summarizing Payroll Taxes . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .20-2Setting Up State Income Taxes . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .20-3

Selecting the Filing Status . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .20-3Entering Withholding Allowances . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .20-3Entering Additional Amounts . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .20-4

Setting Up Local Income Taxes . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .20-5

21 Kentucky—Setting Up Employee Taxes

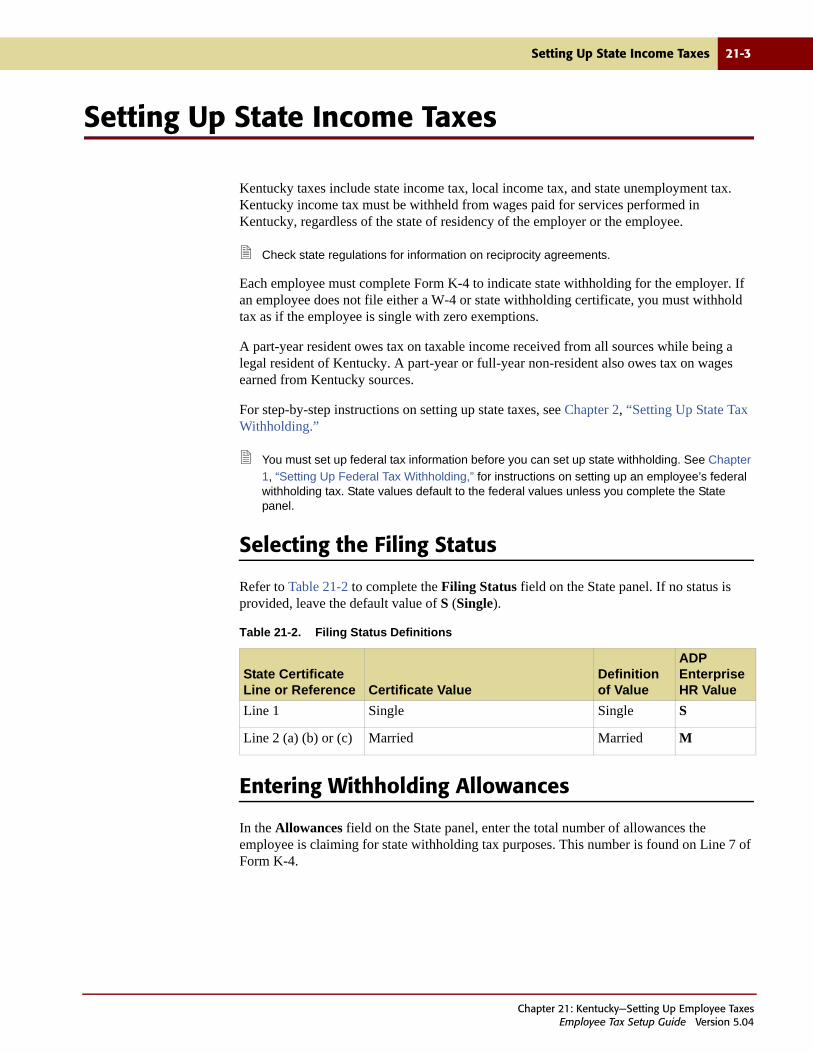

Summarizing Payroll Taxes . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .21-2Setting Up State Income Taxes . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .21-3

Selecting the Filing Status . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .21-3

ContentsEmployee Tax Setup Guide Version 5.04

viii Contents

Entering Withholding Allowances. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 21-3Entering Additional Amounts . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 21-4

Setting Up Local Income Taxes . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 21-5Special Conditions for Louisville and Jefferson County . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 21-5Special Conditions for Boone County, Florence, Walton, Verona, and Erlanger . . . . . . . . . . . . . . . 21-6

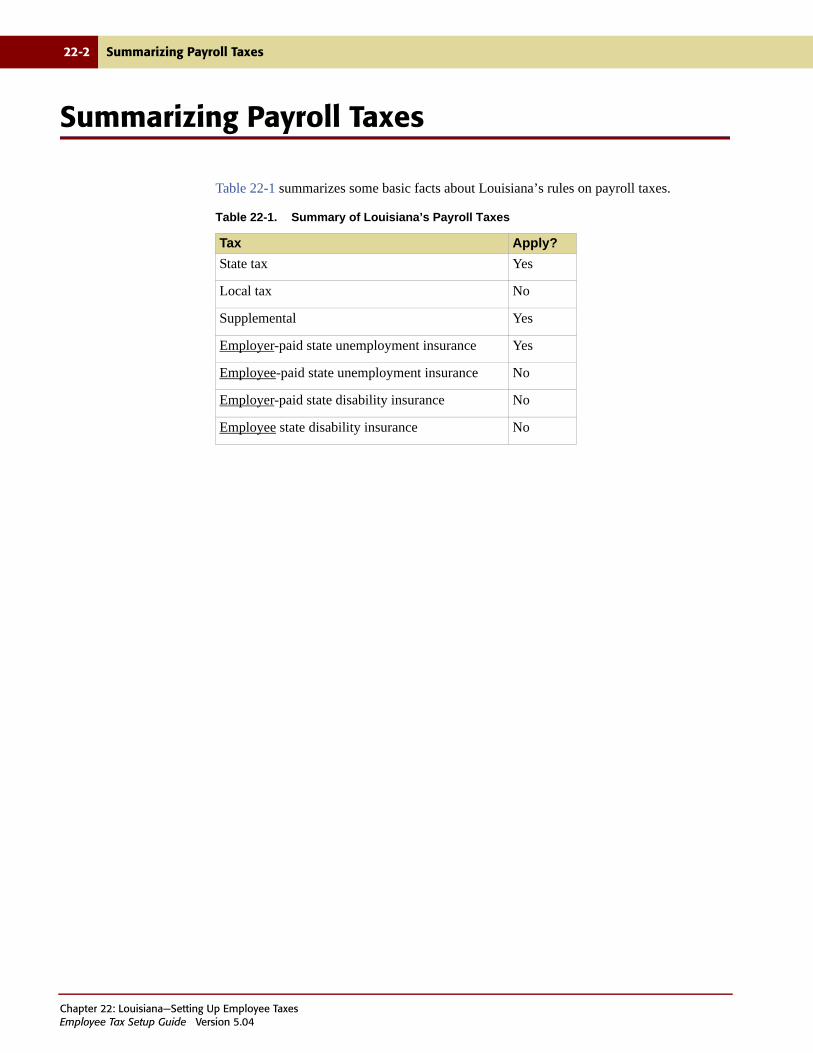

22 Louisiana—Setting Up Employee Taxes

Summarizing Payroll Taxes . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 22-2Setting Up State Income Taxes . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 22-3

Calculating Income Tax. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 22-3Selecting the Filing Status . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 22-3Entering Withholding Allowances. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 22-4Entering Additional Amounts . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 22-4

Setting Up Local Income Taxes . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 22-5

23 Maine—Setting Up Employee Taxes

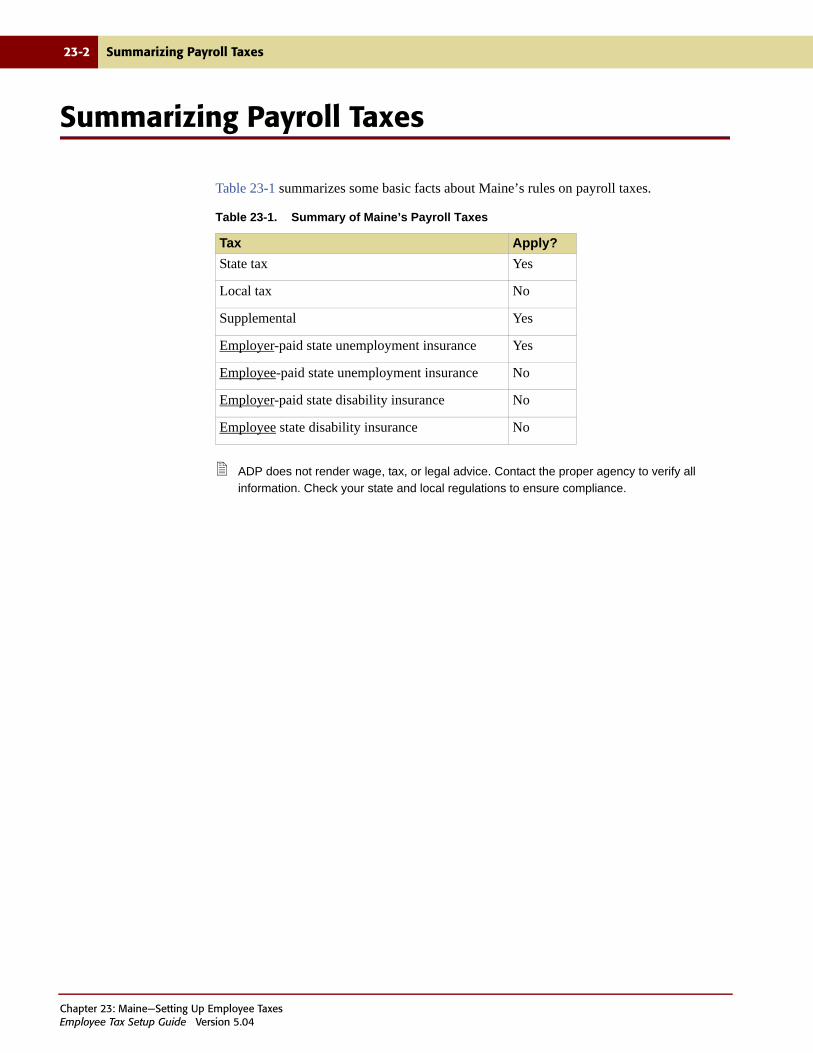

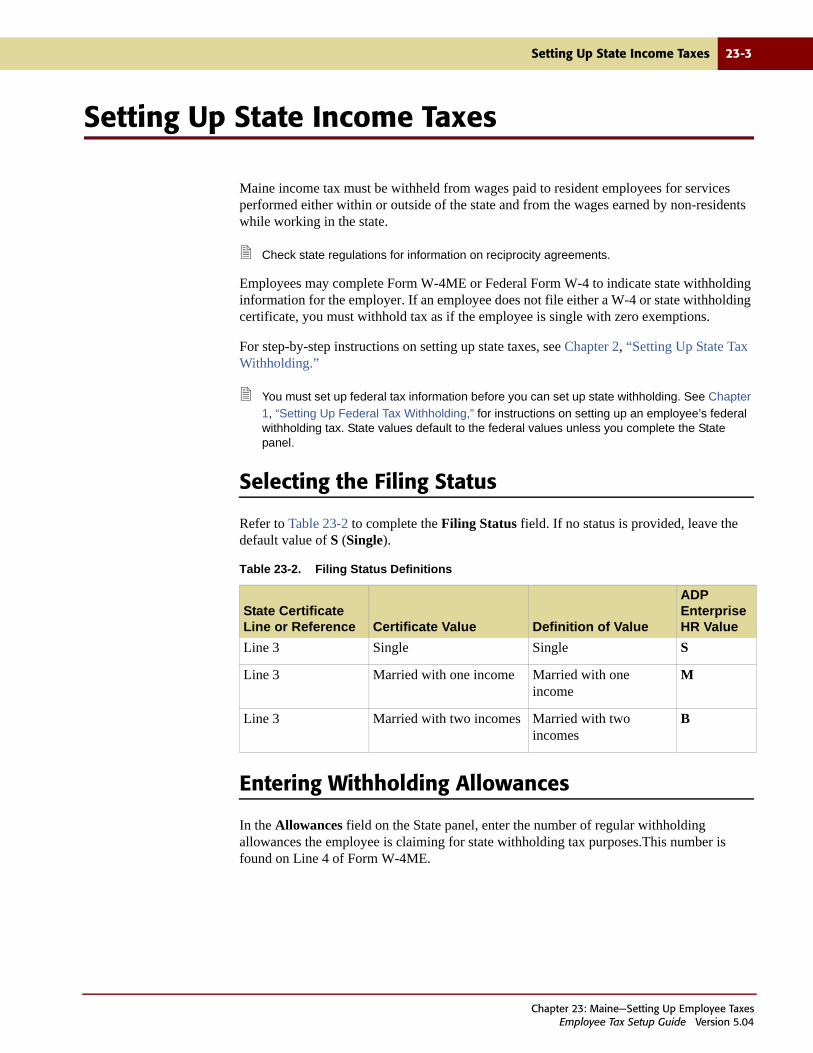

Summarizing Payroll Taxes . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 23-2Setting Up State Income Taxes . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 23-3

Selecting the Filing Status . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 23-3Entering Withholding Allowances. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 23-3Entering Additional Amounts . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 23-4

Setting Up Local Income Taxes . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 23-5

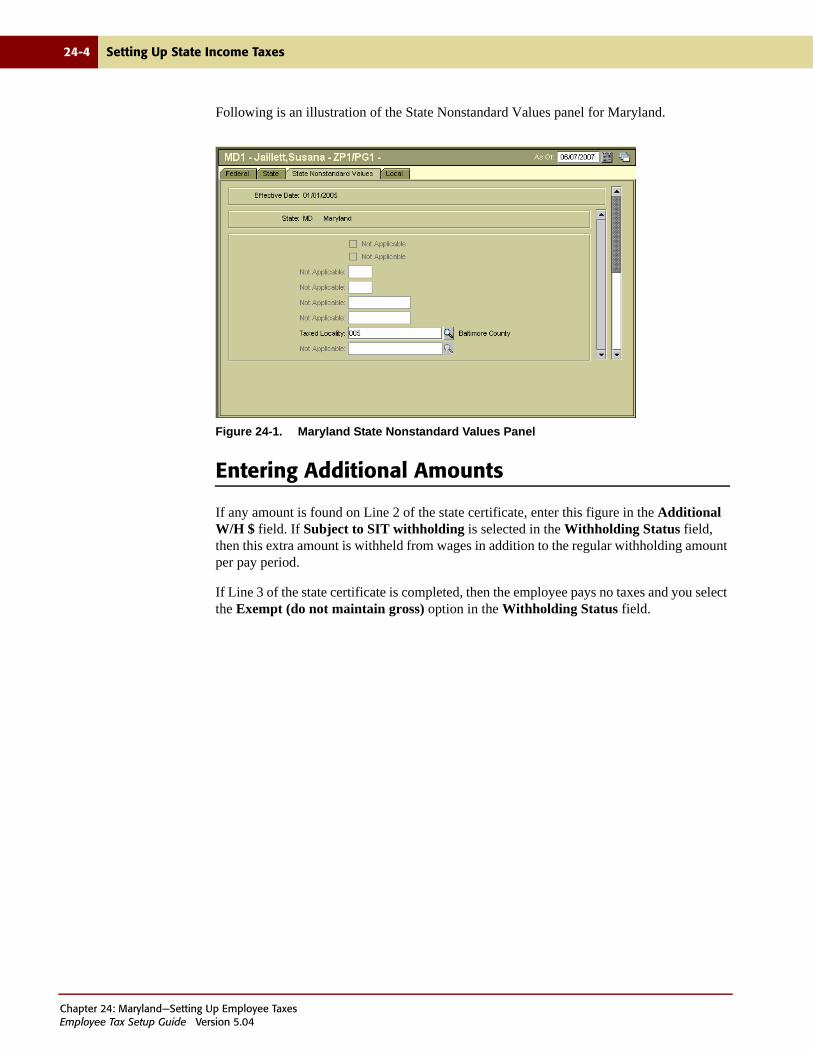

24 Maryland—Setting Up Employee Taxes

Summarizing Payroll Taxes . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 24-2Setting Up State Income Taxes . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 24-3

Selecting the Filing Status . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 24-3Entering Withholding Allowances. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 24-3Entering Additional Amounts . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 24-4

Setting Up Local Income Taxes . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 24-5

25 Massachusetts—Setting Up Employee Taxes

Summarizing Payroll Taxes . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 25-2Setting Up State Income Taxes . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 25-3

Selecting the Filing Status . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 25-3Entering Withholding Allowances. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 25-3Entering Additional Amounts . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 25-3Indicating Head of Household Status . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 25-4

Setting Up Local Income Taxes . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 25-5

ContentsEmployee Tax Setup Guide Version 5.04

Contents ix

26 Michigan—Setting Up Employee Taxes

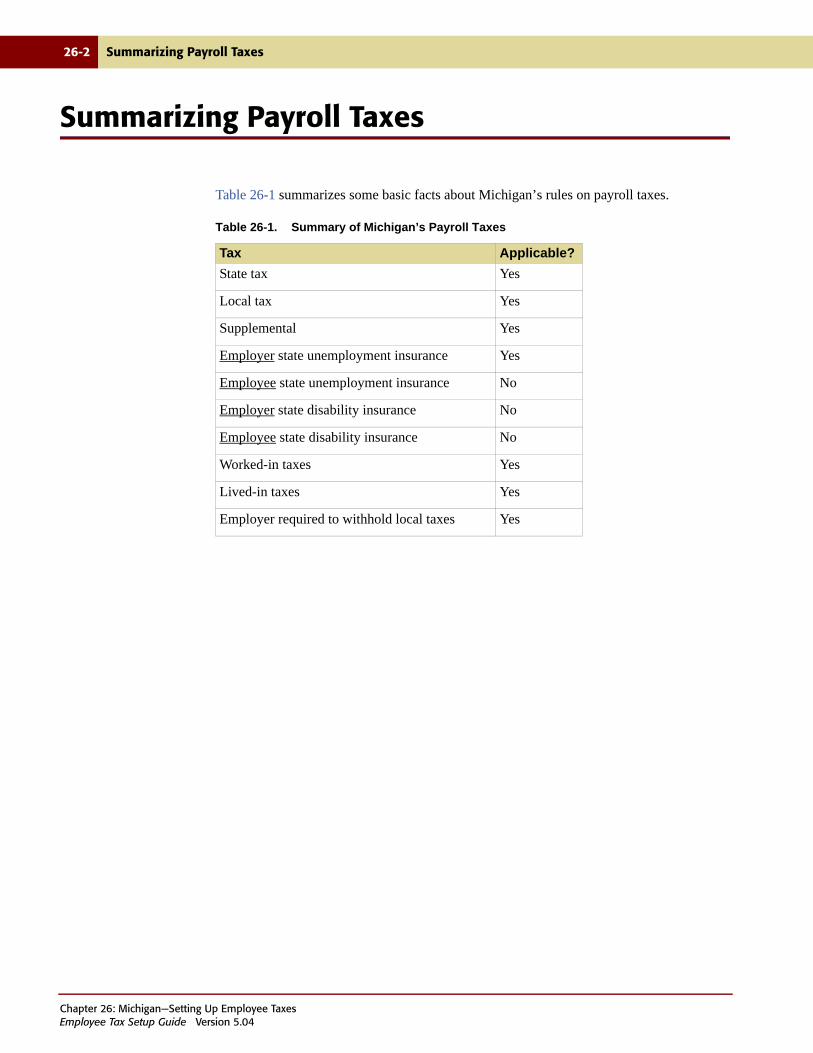

Summarizing Payroll Taxes . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .26-2Setting Up State Income Taxes . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .26-3

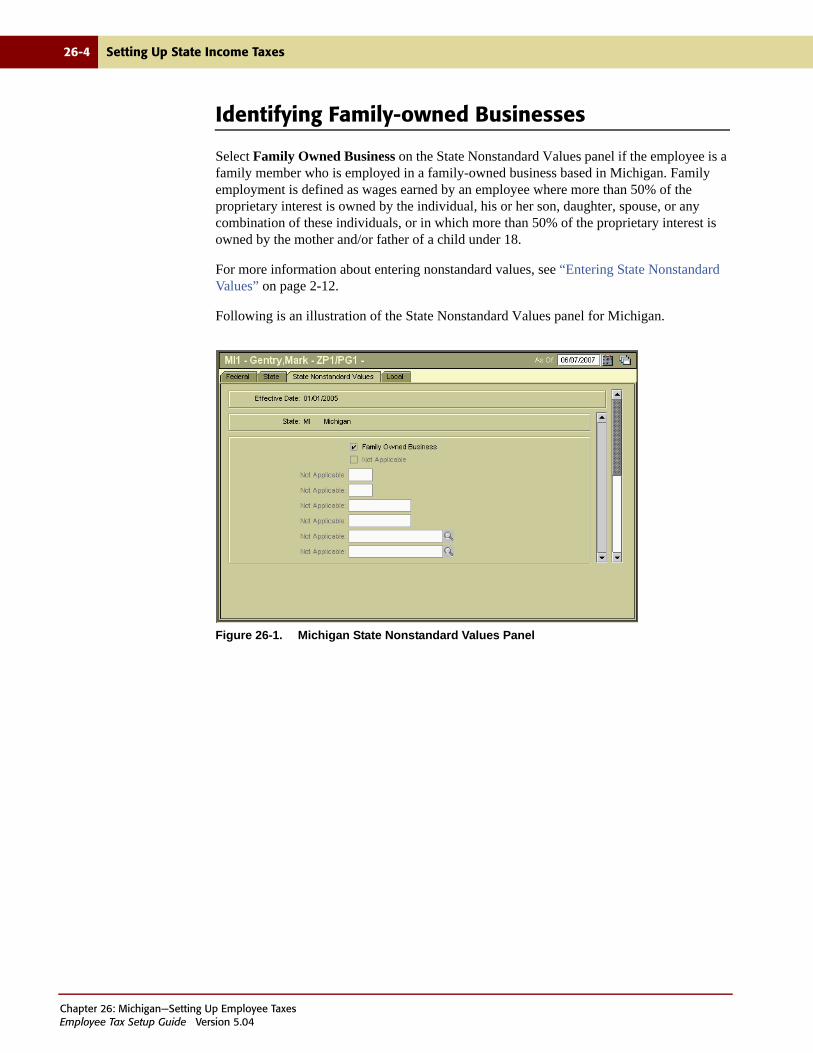

Selecting the Filing Status . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .26-3Entering Withholding Allowances . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .26-3Entering Additional Amounts . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .26-3Identifying Family-owned Businesses . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .26-4

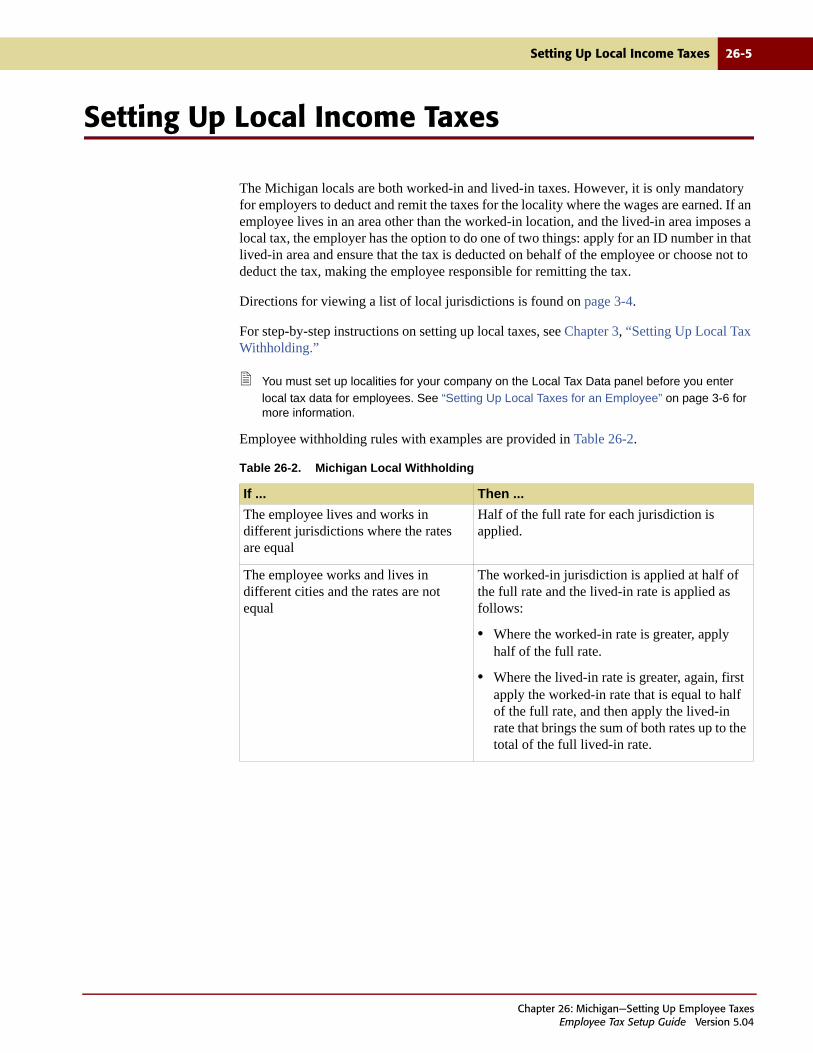

Setting Up Local Income Taxes . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .26-5

27 Minnesota—Setting Up Employee Taxes

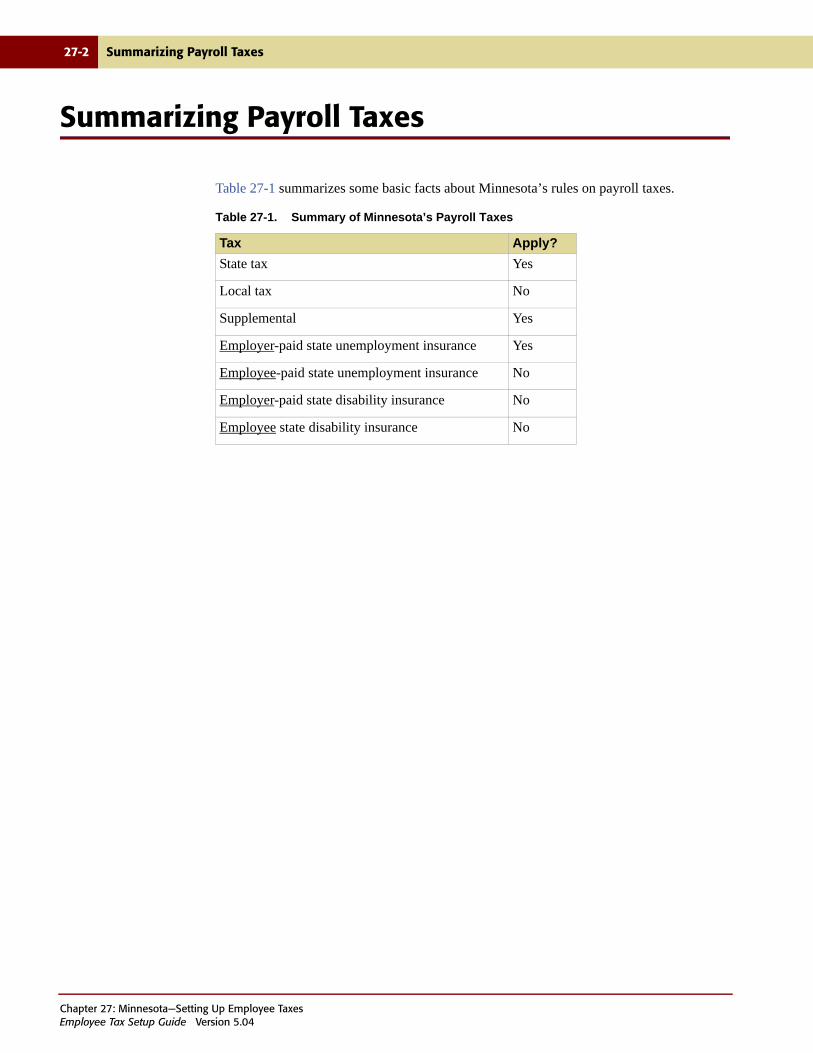

Summarizing Payroll Taxes . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .27-2Setting Up State Income Taxes . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .27-3

Selecting the Filing Status . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .27-3Entering Withholding Allowances . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .27-3Entering Additional Amounts . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .27-4

Setting Up Local Income Taxes . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .27-5

28 Mississippi—Setting Up Employee Taxes

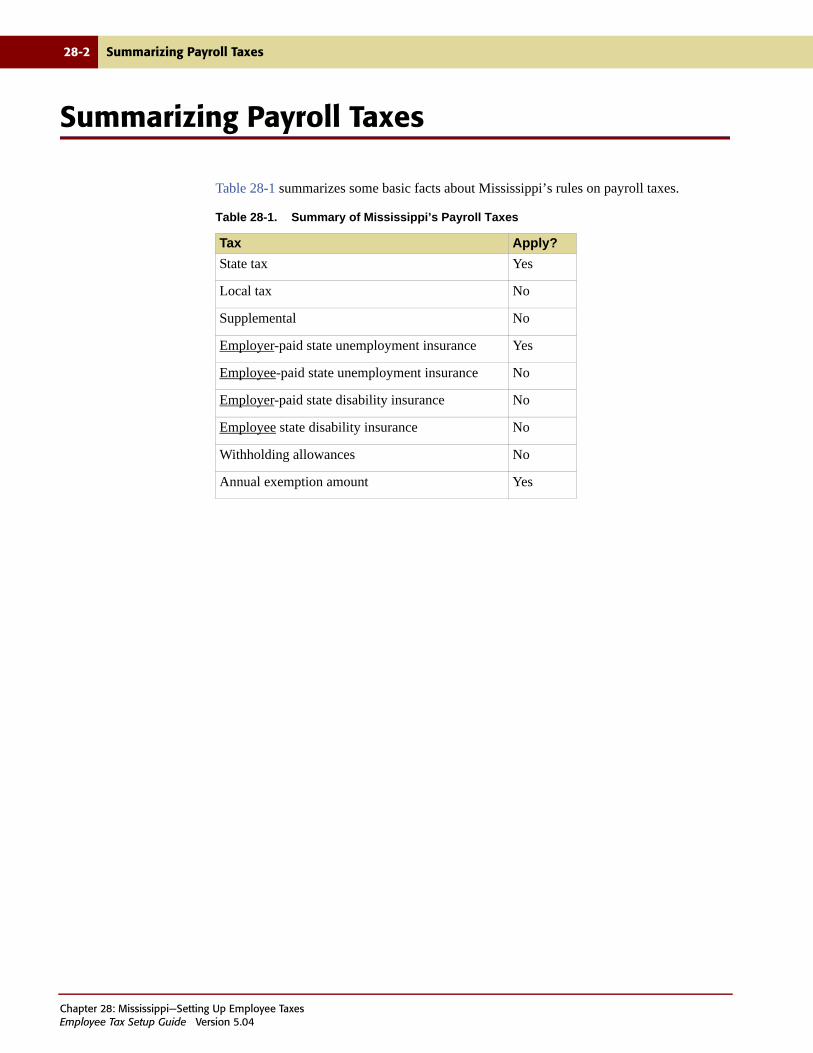

Summarizing Payroll Taxes . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .28-2Setting Up State Income Taxes . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .28-3

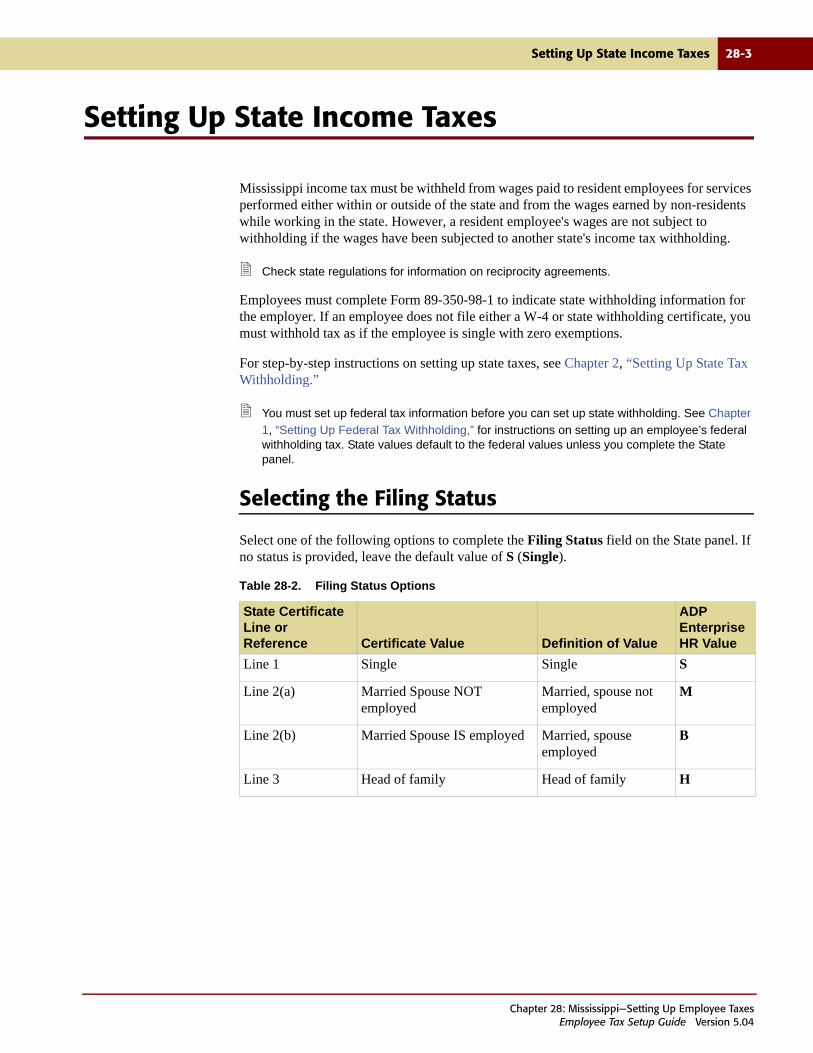

Selecting the Filing Status . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .28-3Entering Withholding Allowances . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .28-4Entering Additional Amounts . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .28-4

Setting Up Local Income Taxes . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .28-5

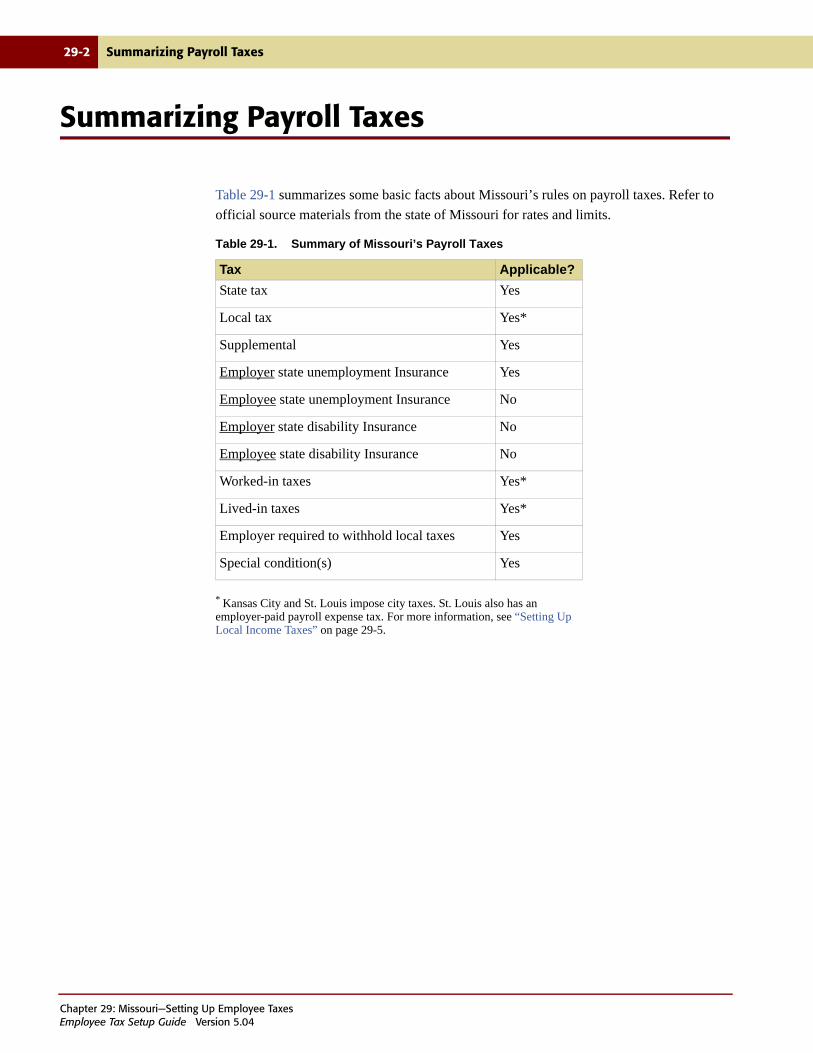

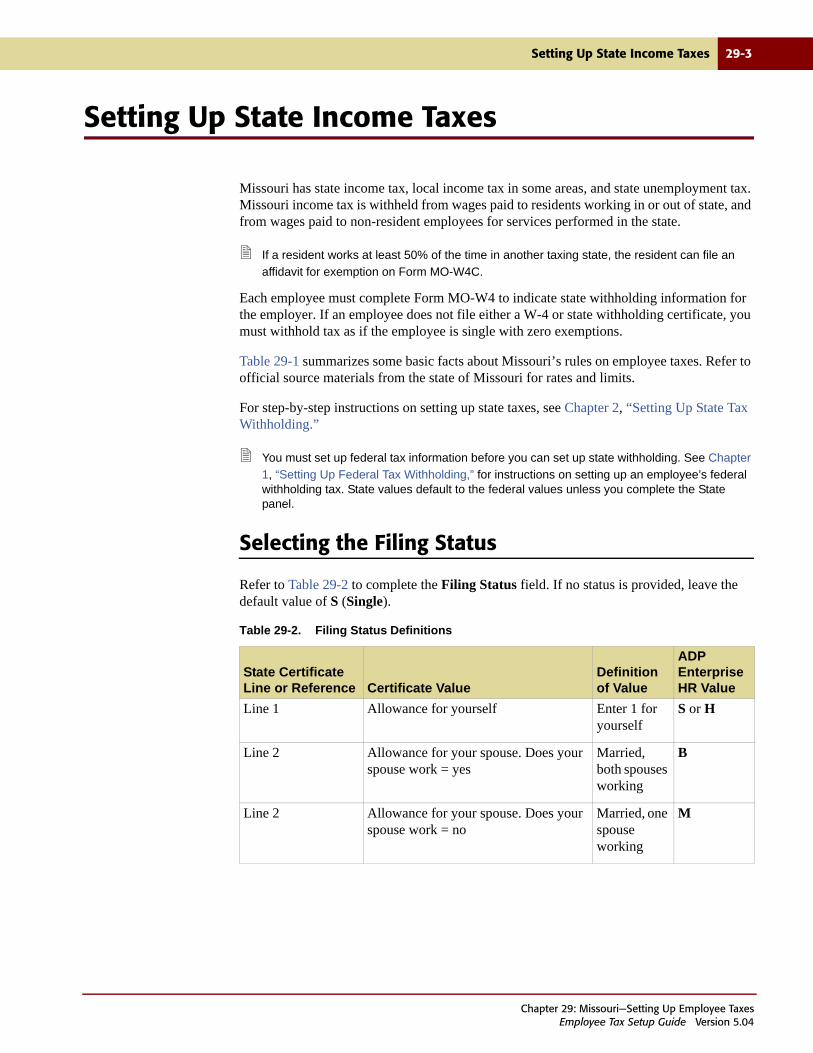

29 Missouri—Setting Up Employee Taxes

Summarizing Payroll Taxes . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .29-2Setting Up State Income Taxes . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .29-3

Selecting the Filing Status . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .29-3Entering Withholding Allowances . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .29-4Entering Additional Amounts . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .29-4

Setting Up Local Income Taxes . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .29-5

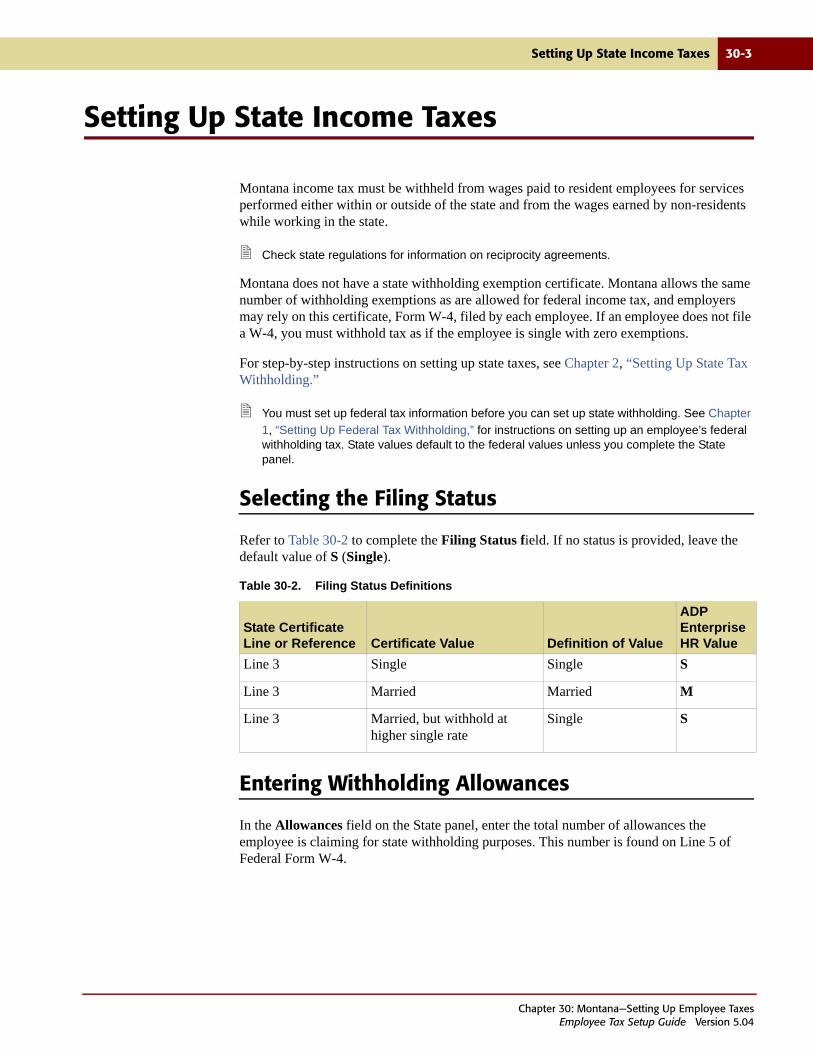

30 Montana—Setting Up Employee Taxes

Summarizing Payroll Taxes . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .30-2Setting Up State Income Taxes . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .30-3

Selecting the Filing Status . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .30-3Entering Withholding Allowances . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .30-3

ContentsEmployee Tax Setup Guide Version 5.04

x Contents

Entering Additional Amounts . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 30-4Setting Up Local Income Taxes . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 30-5

31 Nebraska—Setting Up Employee Taxes

Summarizing Payroll Taxes . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 31-2Setting Up State Income Taxes . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 31-3

Selecting the Filing Status . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 31-3Entering Withholding Allowances. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 31-4Entering Additional Amounts . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 31-4

Setting Up Local Income Taxes . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 31-5

32 Nevada—Setting Up Employee Taxes

Summarizing Payroll Taxes . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 32-2Setting Up State and Local Income Taxes . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 32-3

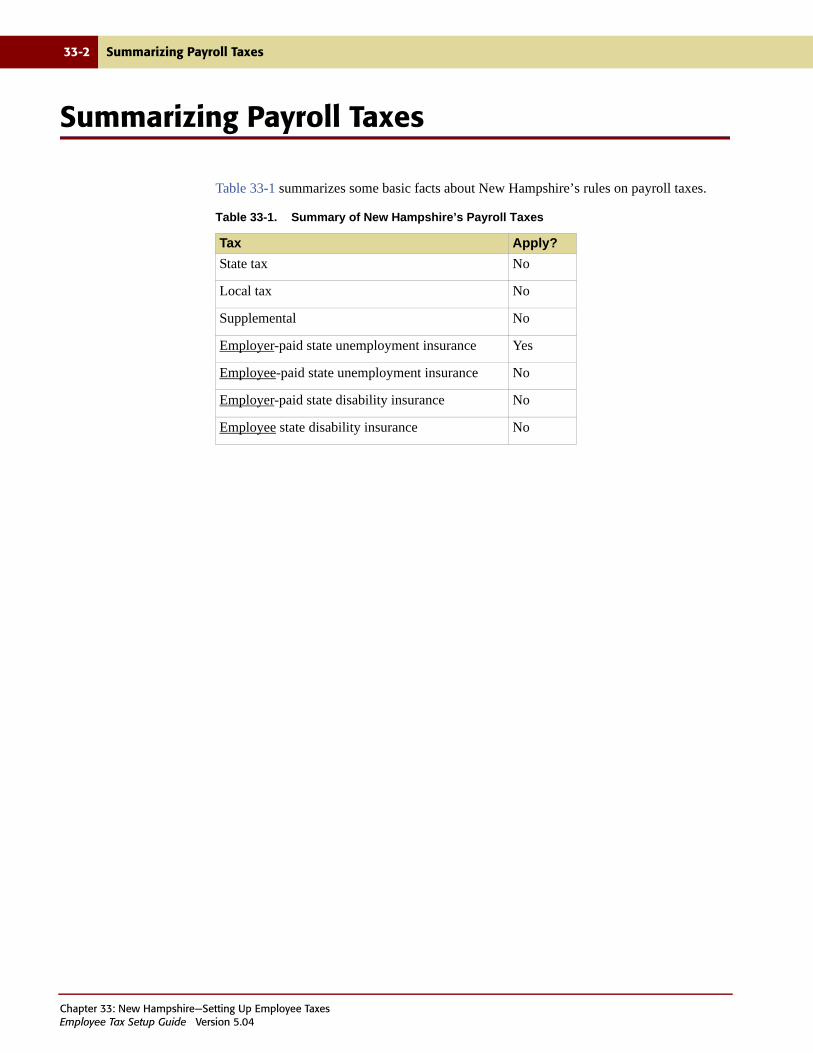

33 New Hampshire—Setting Up Employee Taxes

Summarizing Payroll Taxes . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 33-2Setting Up State and Local Income Taxes . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 33-3

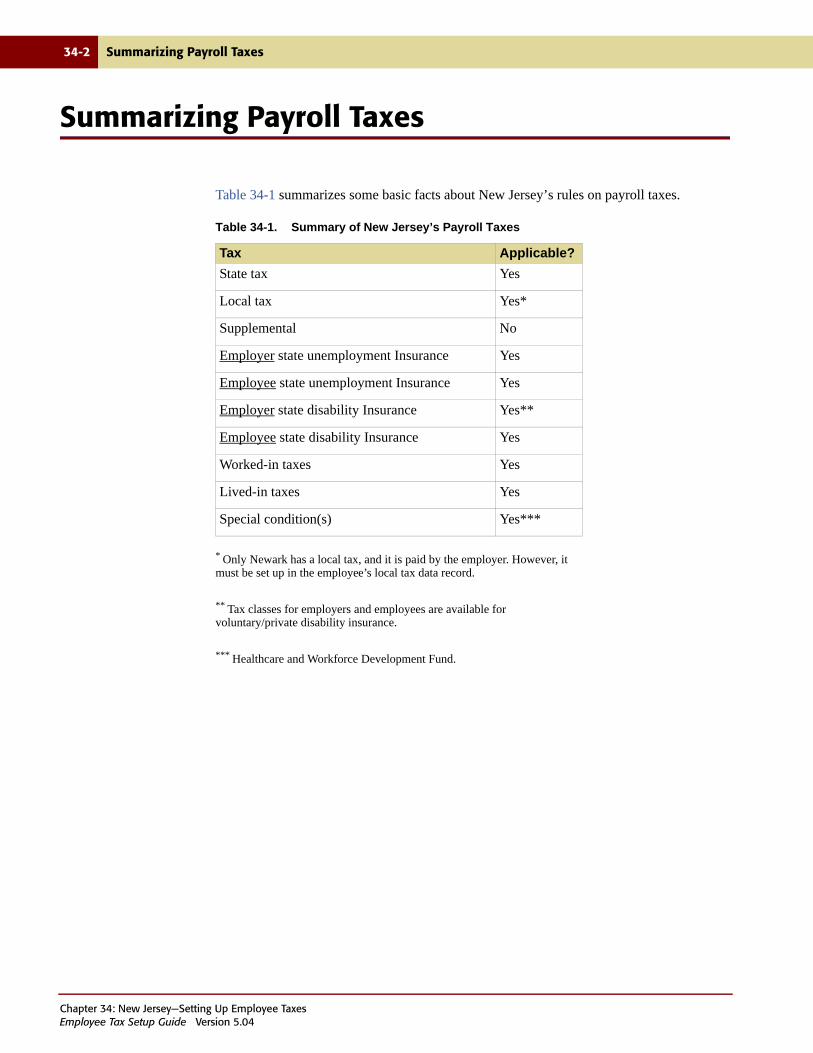

34 New Jersey—Setting Up Employee Taxes

Summarizing Payroll Taxes . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 34-2Setting Up State Income Taxes . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 34-3

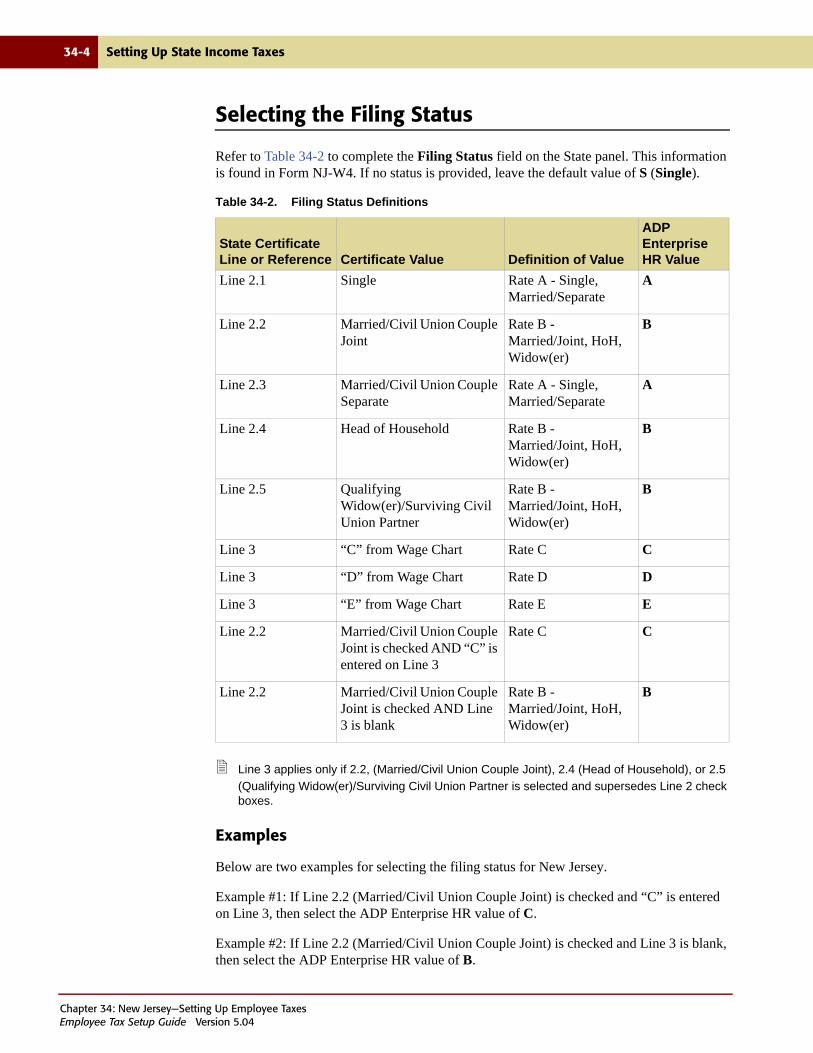

Selecting the Filing Status . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 34-4Examples . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 34-4

Entering Withholding Allowances. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 34-5Entering Additional Amounts . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 34-5Selecting the Disability Status . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 34-5

Setting Up Local Income Taxes . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 34-6Special Conditions for New Jersey . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 34-6Understanding Medical Malpractice Insurance Premium Assistance Assessment (MMIPAA) . . . . 34-6

Setting Up Medical Malpractice Insurance Premium Assistance Assessment (MMIPAA) . . . 34-6

35 New Mexico—Setting Up Employee Taxes

Summarizing Payroll Taxes . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 35-2Setting Up State Income Taxes . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 35-3

Selecting the Filing Status . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 35-3Entering Withholding Allowances. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 35-4

ContentsEmployee Tax Setup Guide Version 5.04

Contents xi

Entering Additional Amounts . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .35-4Setting Up Local Income Taxes . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .35-5

36 New York—Setting Up Employee Taxes

Summarizing Payroll Taxes . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .36-2Setting Up State Income Taxes . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .36-3

Selecting the Filing Status . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .36-3Entering Withholding Allowances . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .36-4Entering Additional Amounts . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .36-4Selecting the Disability Status . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .36-4

Setting Up Local Income Taxes . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .36-5

37 North Carolina—Setting Up Employee Taxes

Summarizing Payroll Taxes . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .37-2Setting Up State Income Taxes . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .37-3

Selecting the Filing Status . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .37-3Entering Withholding Allowances . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .37-4Entering Additional Amounts . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .37-4

Setting Up Local Income Taxes . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .37-5

38 North Dakota—Setting Up Employee Taxes

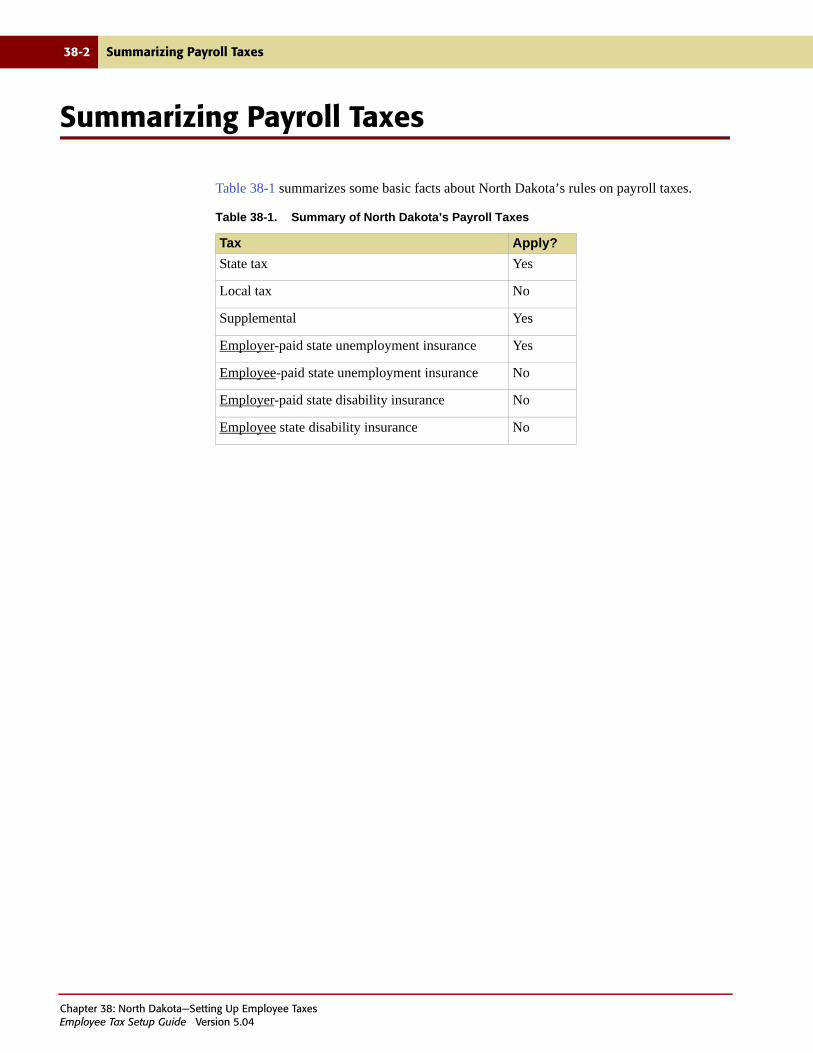

Summarizing Payroll Taxes . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .38-2Setting Up State Income Taxes . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .38-3

Selecting the Filing Status . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .38-3Entering Withholding Allowances . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .38-4Entering Additional Amounts . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .38-4

Setting Up Local Income Taxes . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .38-5

39 Ohio—Setting Up Employee Taxes

Summarizing Payroll Taxes . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .39-2Setting Up State Income Taxes . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .39-3

Selecting the Filing Status . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .39-3Entering Withholding Allowances . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .39-3Entering Additional Amounts . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .39-3

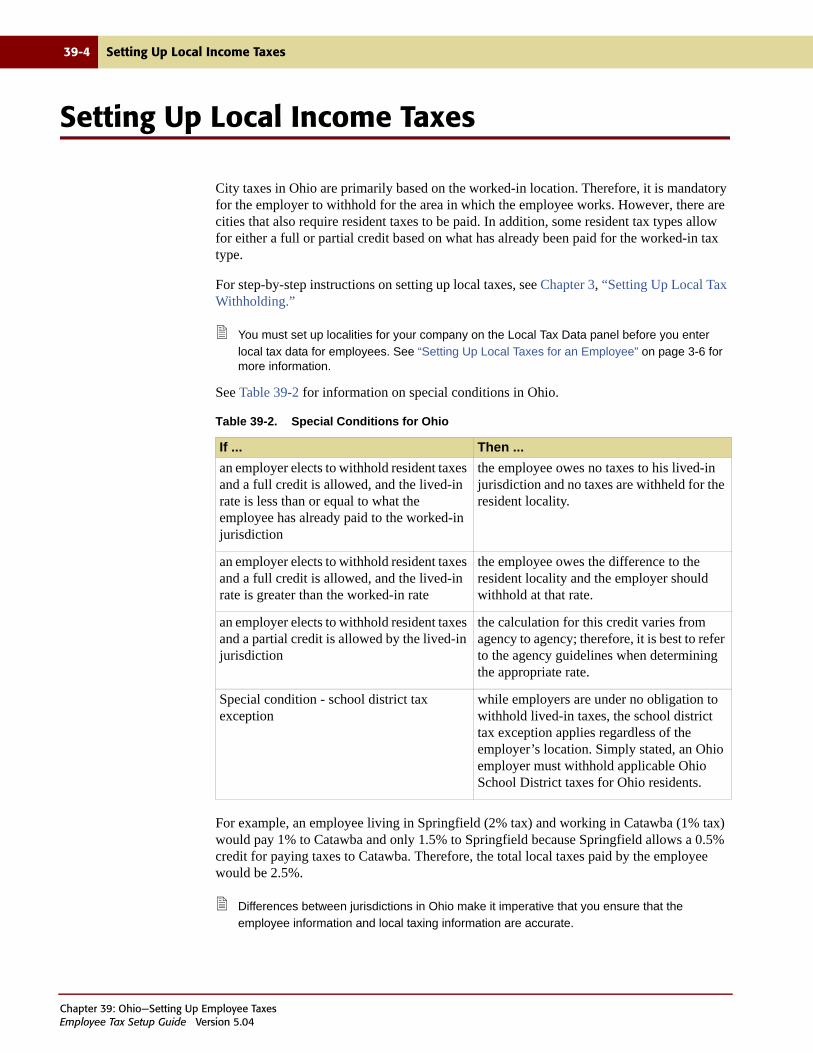

Setting Up Local Income Taxes . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .39-4

40 Oklahoma—Setting Up

ContentsEmployee Tax Setup Guide Version 5.04

xii Contents

Employee Taxes

Summarizing Payroll Taxes . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 40-2Setting Up State Income Taxes . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 40-3

Selecting the Filing Status . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 40-3Entering Withholding Allowances. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 40-4Entering Additional Amounts . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 40-4

Setting Up Local Income Taxes . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 40-5

41 Oregon—Setting Up Employee Taxes

Summarizing Payroll Taxes . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 41-2Setting Up State Income Taxes . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 41-3

Selecting the Filing Status . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 41-3Entering Withholding Allowances. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 41-3Entering Additional Amounts . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 41-4

Setting Up Local Income Taxes . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 41-5Understanding Workers’ Compensation . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 41-5Setting Up Worked-in Tax. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 41-6

42 Pennsylvania—Setting Up Employee Taxes

Summarizing Payroll Taxes . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 42-2Setting Up State Income Taxes . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 42-3

Selecting the Filing Status . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 42-3Entering Withholding Allowances. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 42-3Entering Additional Amounts . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 42-3

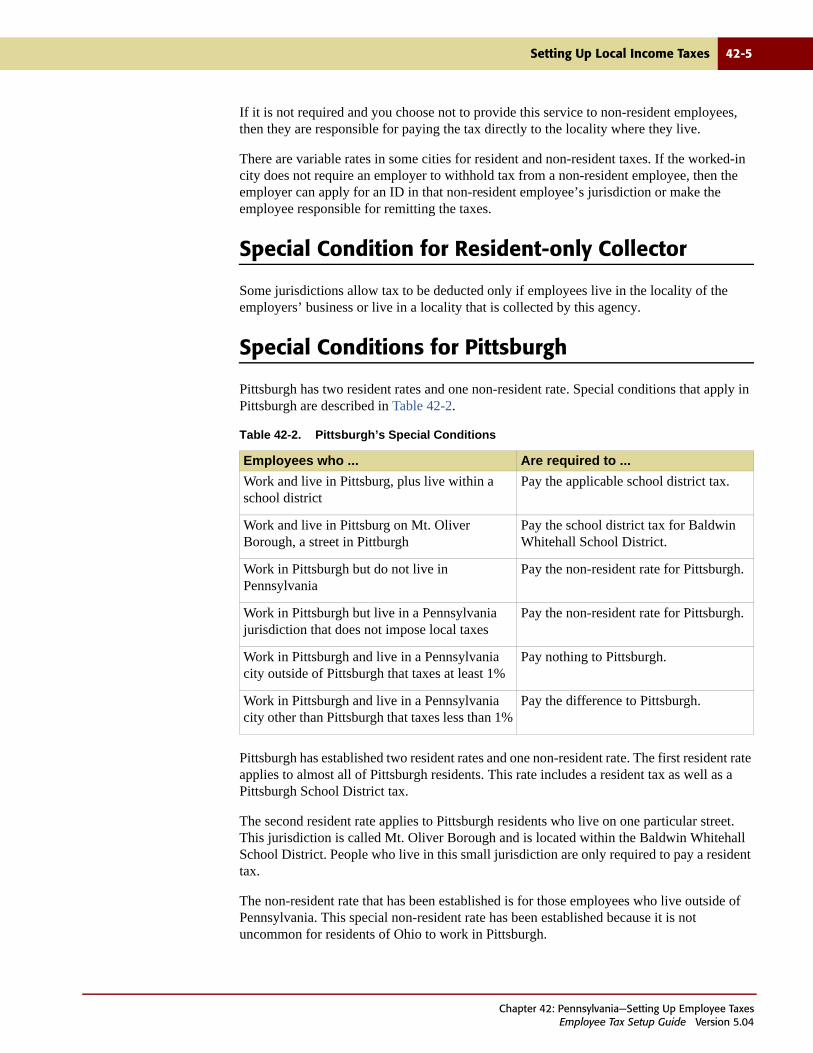

Setting Up Local Income Taxes . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 42-4Withholding Local and School District Taxes. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 42-4Withholding for Employees Who Live in a Different Locality. . . . . . . . . . . . . . . . . . . . . . . . . . . . . 42-4Special Condition for Resident-only Collector . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 42-5Special Conditions for Pittsburgh . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 42-5

Taxing Exception . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 42-6Special Conditions for Philadelphia . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 42-6

43 Puerto Rico—Setting Up Employee Taxes

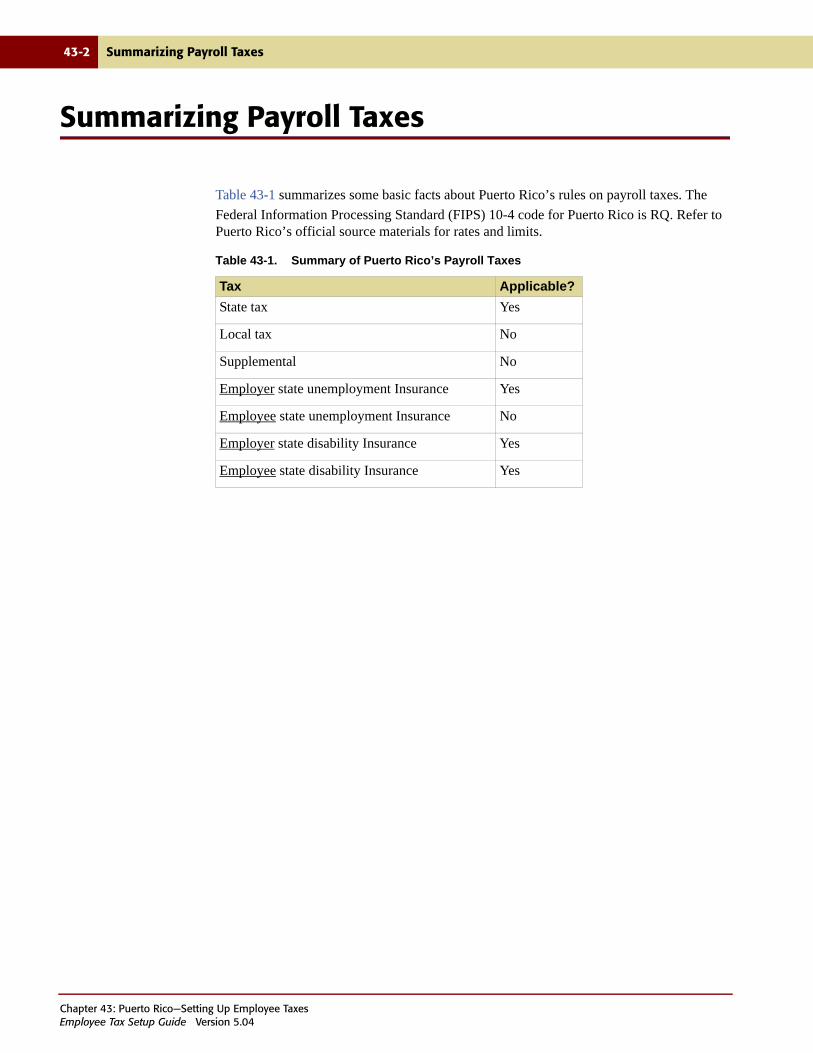

Summarizing Payroll Taxes . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 43-2Setting Up State Income Taxes . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 43-3

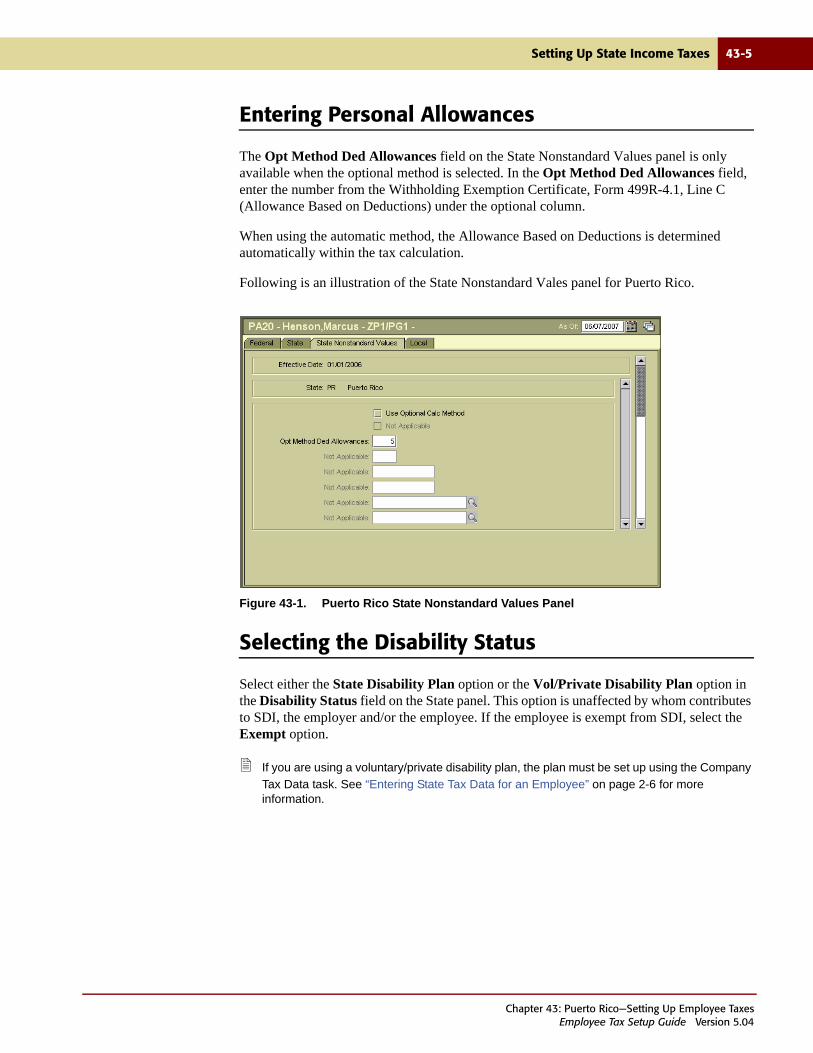

Selecting the Filing Status . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 43-4Entering Withholding Allowances. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 43-4Entering Personal Allowances . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 43-5Selecting the Disability Status . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 43-5

44 Rhode Island—Setting Up

ContentsEmployee Tax Setup Guide Version 5.04

Contents xiii

Employee Taxes

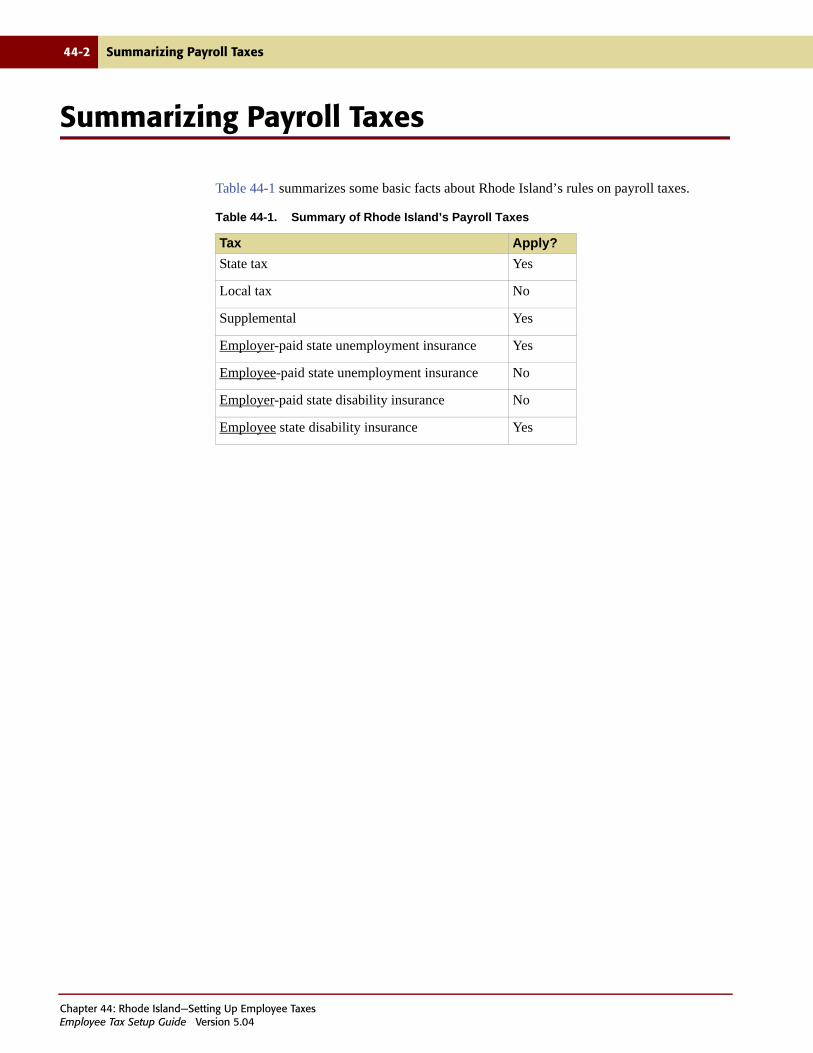

Summarizing Payroll Taxes . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .44-2Setting Up State Income Taxes . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .44-3

Selecting the Filing Status . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .44-3Entering Withholding Allowances . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .44-3Entering Additional Amounts . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .44-4Selecting the Disability Status . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .44-4

Setting Up Local Income Taxes . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .44-5

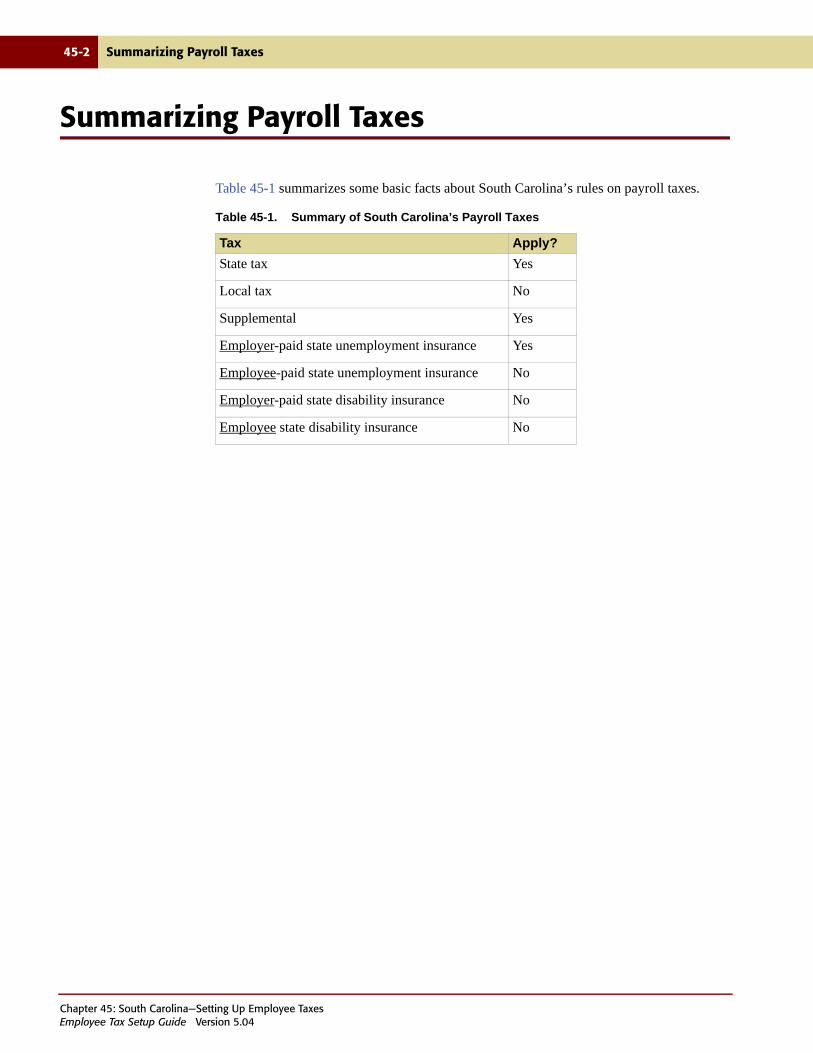

45 South Carolina—Setting Up Employee Taxes

Summarizing Payroll Taxes . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .45-2Setting Up State Income Taxes . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .45-3

Selecting the Filing Status . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .45-3Entering Withholding Allowances . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .45-4Entering Additional Amounts . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .45-4

Setting Up Local Income Taxes . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .45-5

46 South Dakota—Setting Up Employee Taxes

Summarizing Payroll Taxes . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .46-2Setting Up State and Local Income Taxes . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .46-3

47 Tennessee—Setting Up Employee Taxes

Summarizing Payroll Taxes . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .47-2Setting Up State and Local Income Taxes . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .47-3

48 Texas—Setting Up Employee Taxes

Summarizing Payroll Taxes . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .48-2Setting Up State and Local Income Taxes . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .48-3

49 Utah—Setting Up Employee Taxes

Summarizing Payroll Taxes . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .49-2Setting Up State Income Taxes . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .49-3

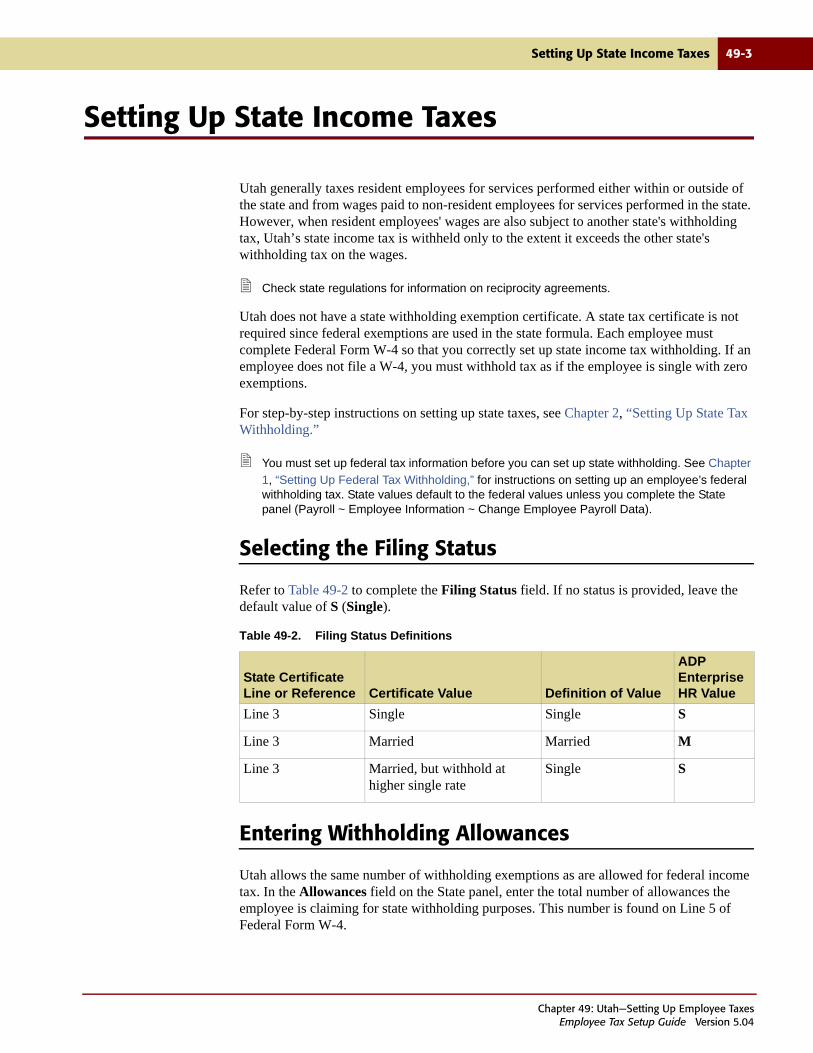

Selecting the Filing Status . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .49-3Entering Withholding Allowances . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .49-3Entering Additional Amounts . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .49-4

Setting Up Local Income Taxes . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .49-5

ContentsEmployee Tax Setup Guide Version 5.04

xiv Contents

50 Vermont—Setting Up Employee Taxes

Summarizing Payroll Taxes . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 50-2Setting Up State Income Taxes . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 50-3

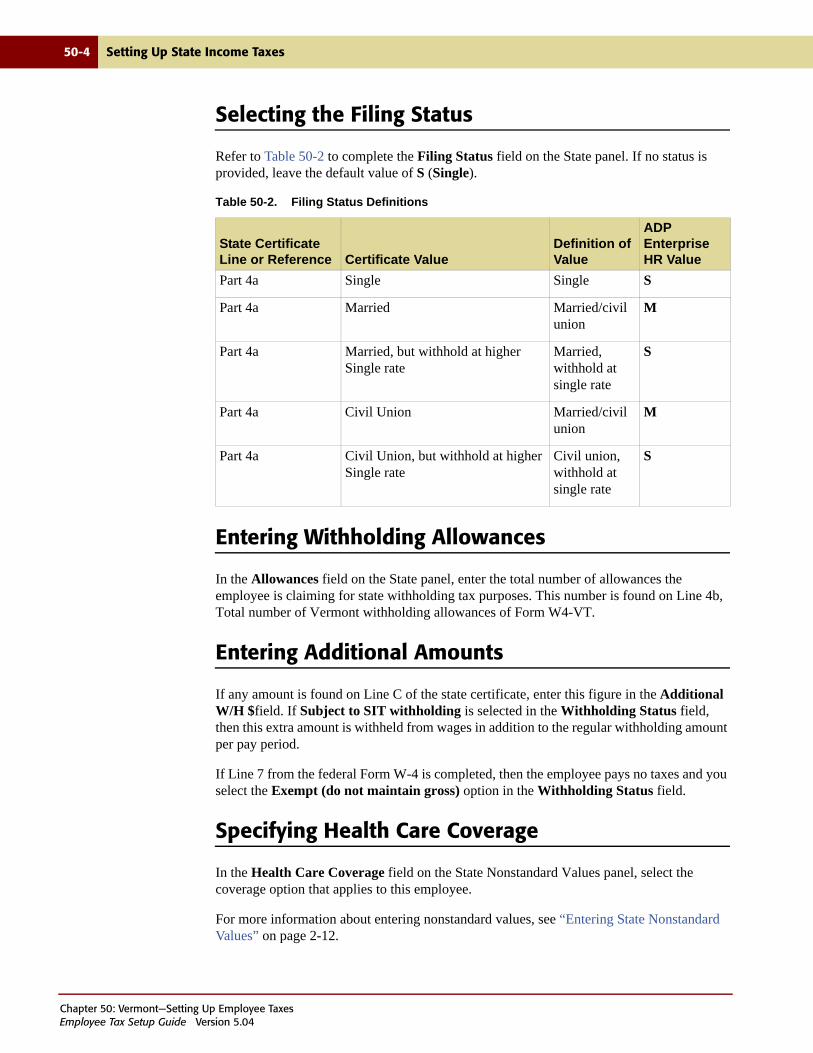

Selecting the Filing Status . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 50-4Entering Withholding Allowances. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 50-4Entering Additional Amounts . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 50-4Specifying Health Care Coverage . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 50-4

Setting Up Local Income Taxes . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 50-6

51 Virginia—Setting Up Employee Taxes

Summarizing Payroll Taxes . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 51-2Setting Up State Income Taxes . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 51-3

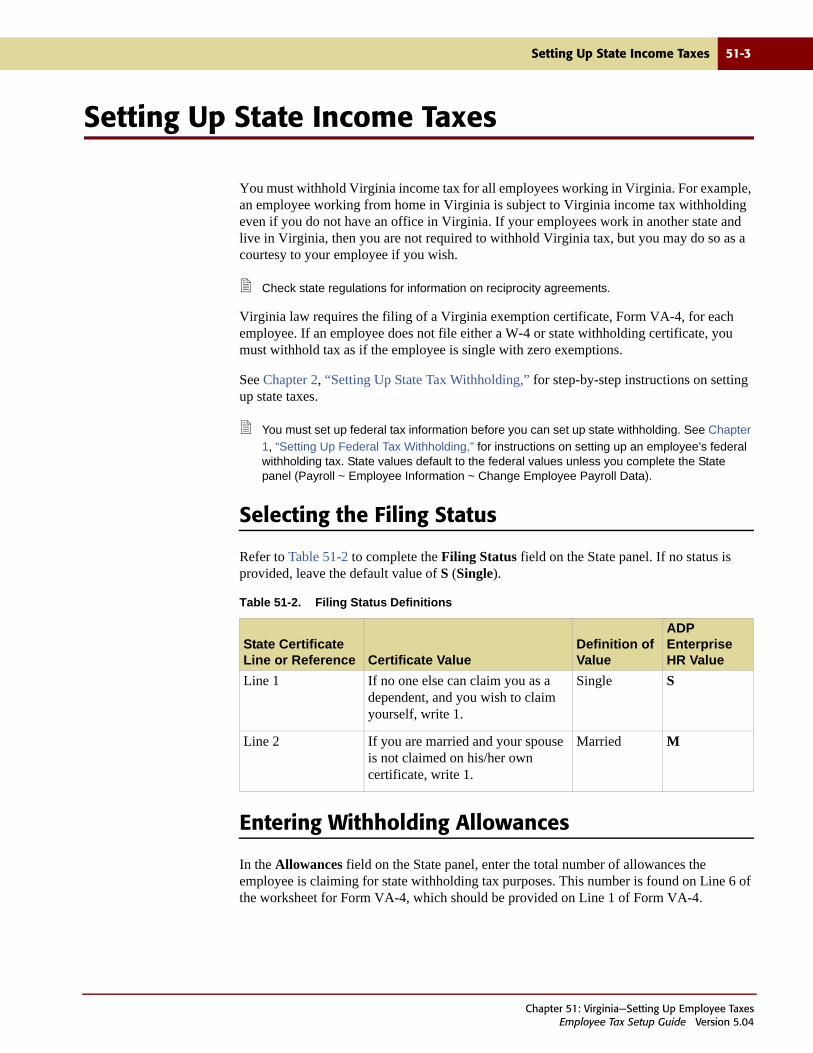

Selecting the Filing Status . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 51-3Entering Withholding Allowances. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 51-3Entering Additional Amounts . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 51-4

Setting Up Local Income Taxes . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 51-5

52 Washington—Setting Up Employee Taxes

Summarizing Payroll Taxes . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 52-2Setting Up State and Local Income Taxes . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 52-3

53 West Virginia—Setting Up Employee Taxes

Summarizing Payroll Taxes . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 53-2Setting Up State Income Taxes . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 53-3

Selecting the Filing Status . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 53-4Entering Withholding Allowances. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 53-4Entering Additional Amounts . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 53-4

Setting Up Local Income Taxes . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 53-5

54 Wisconsin—Setting Up Employee Taxes

Summarizing Payroll Taxes . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 54-2Setting Up State Income Taxes . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 54-3

Selecting the Filing Status . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 54-3Entering Withholding Allowances. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 54-3Entering Additional Amounts . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 54-4

Setting Up Local Income Taxes . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 54-5

ContentsEmployee Tax Setup Guide Version 5.04

Contents xv

55 Wyoming—Setting Up Employee Taxes

Summarizing Payroll Taxes . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .55-2Setting Up State and Local Income Taxes . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .55-3

A ADP Financial and Compliance Services

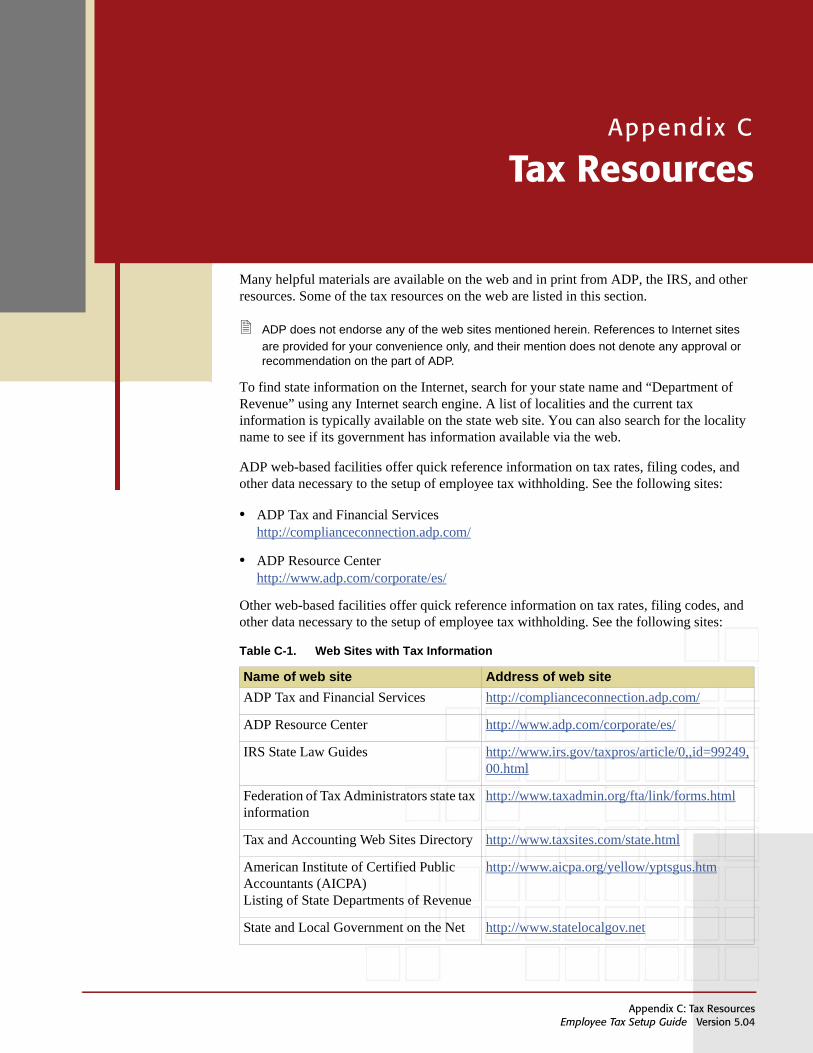

Introduction . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . A-2Accessing ADP Web-based Information . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . A-3Referencing Current Tax Information . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . A-4Locating a Local Code for Tax Filing Purposes. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . A-5Understanding Comment Code Definitions . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . A-7

B Abbreviations

C Tax Resources

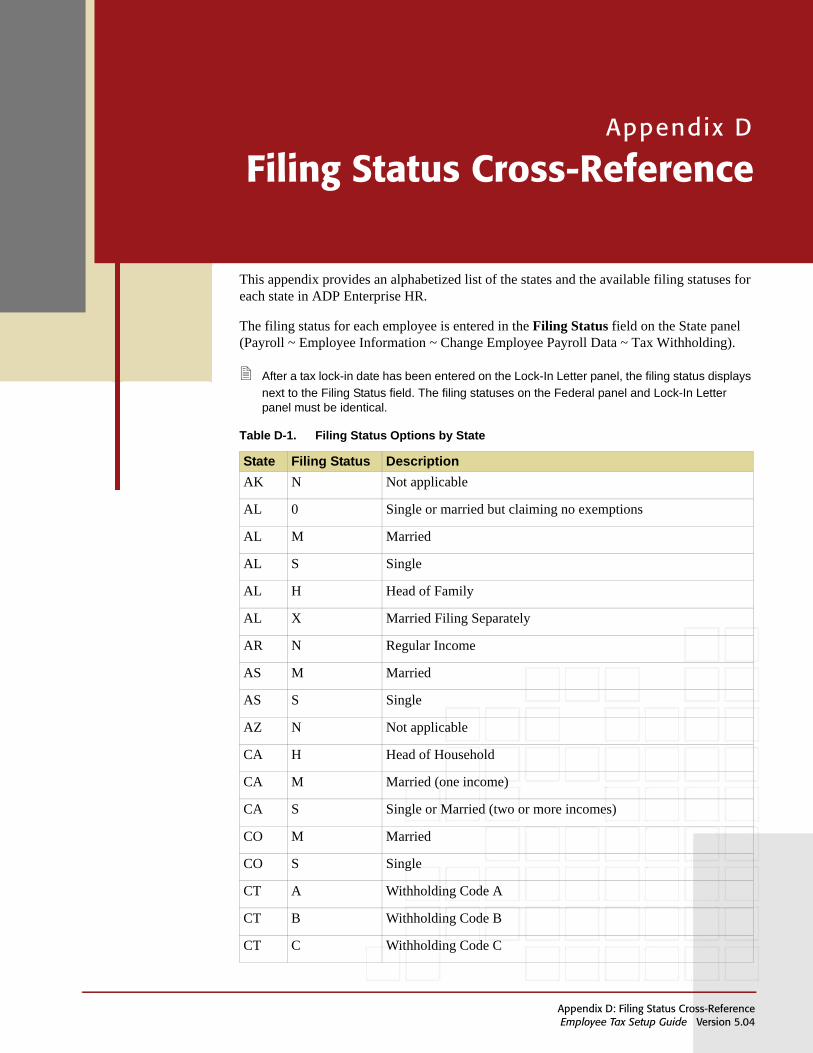

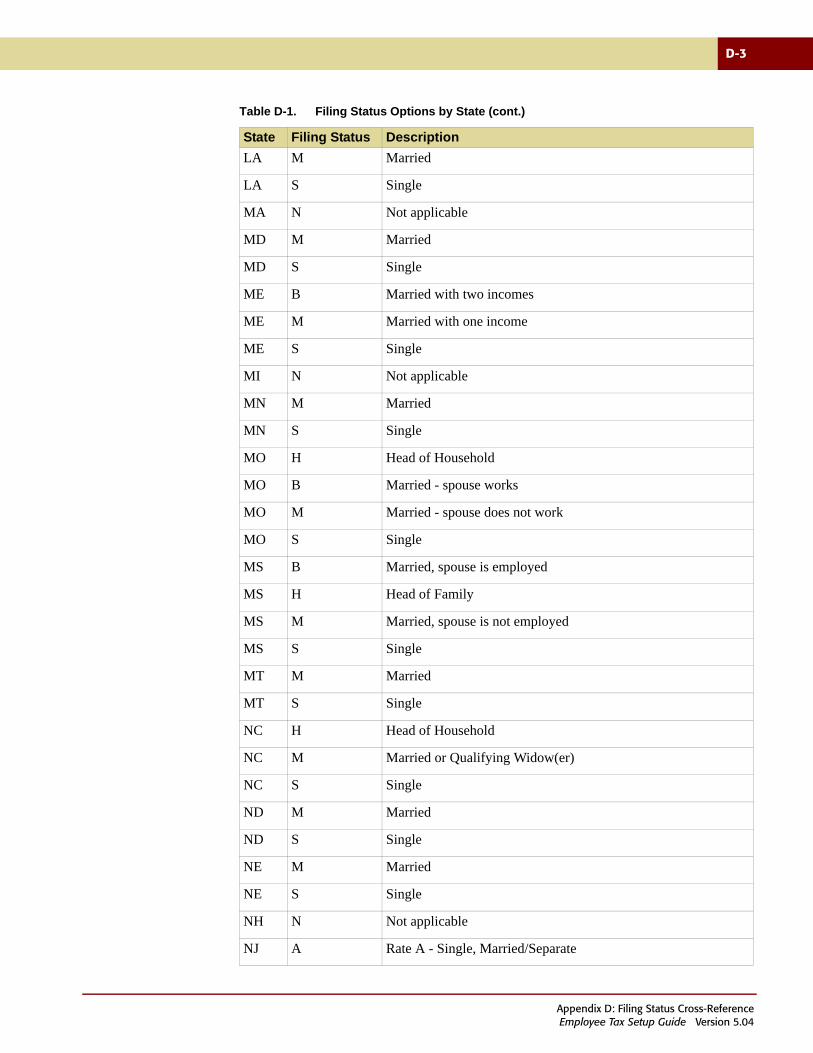

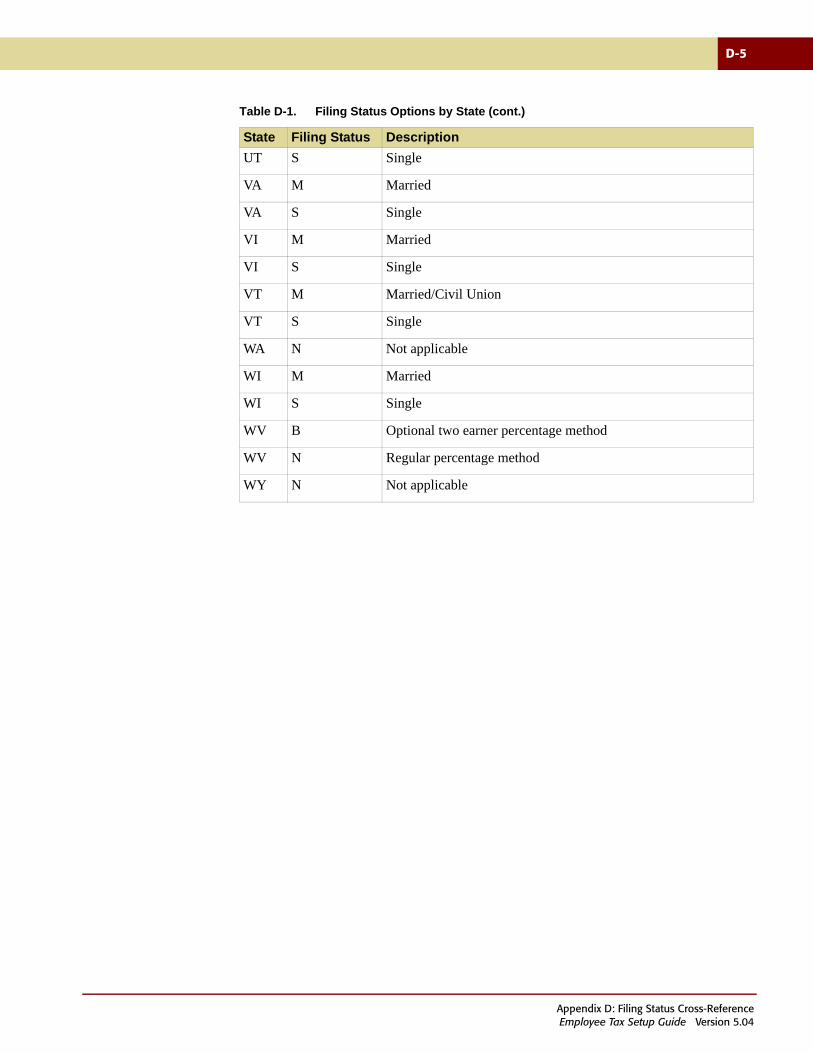

D Filing Status Cross-Reference

E Employee Tax Setup Examples

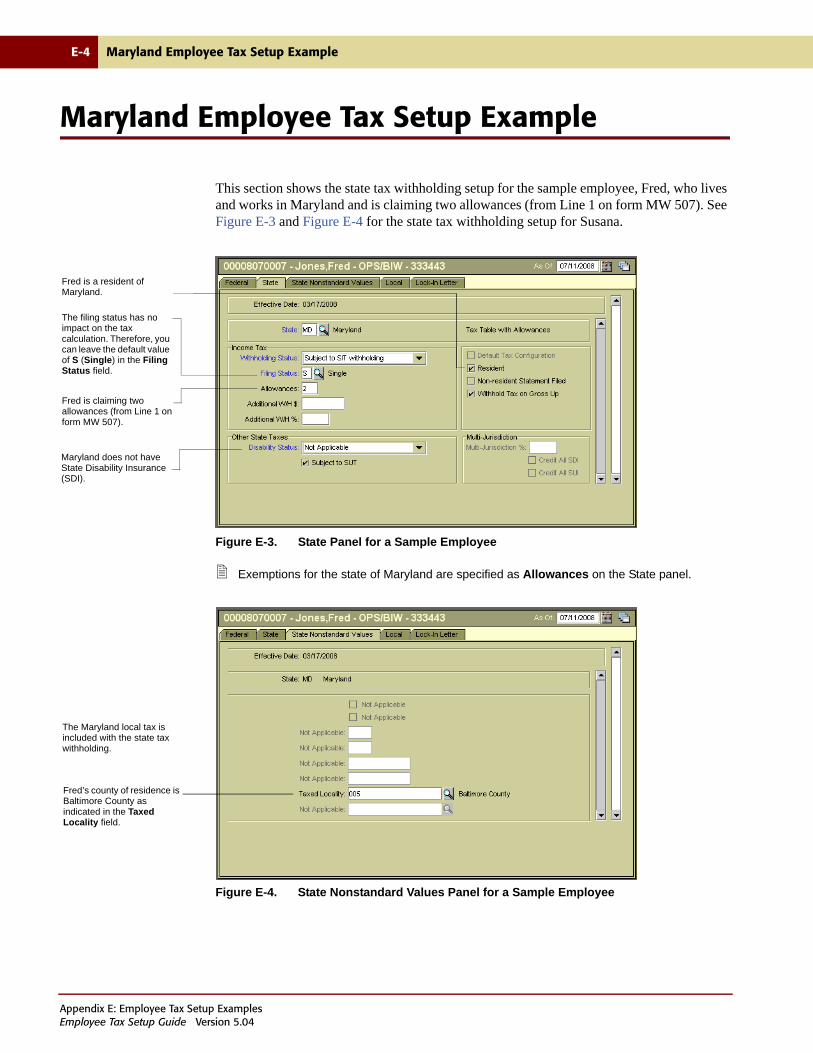

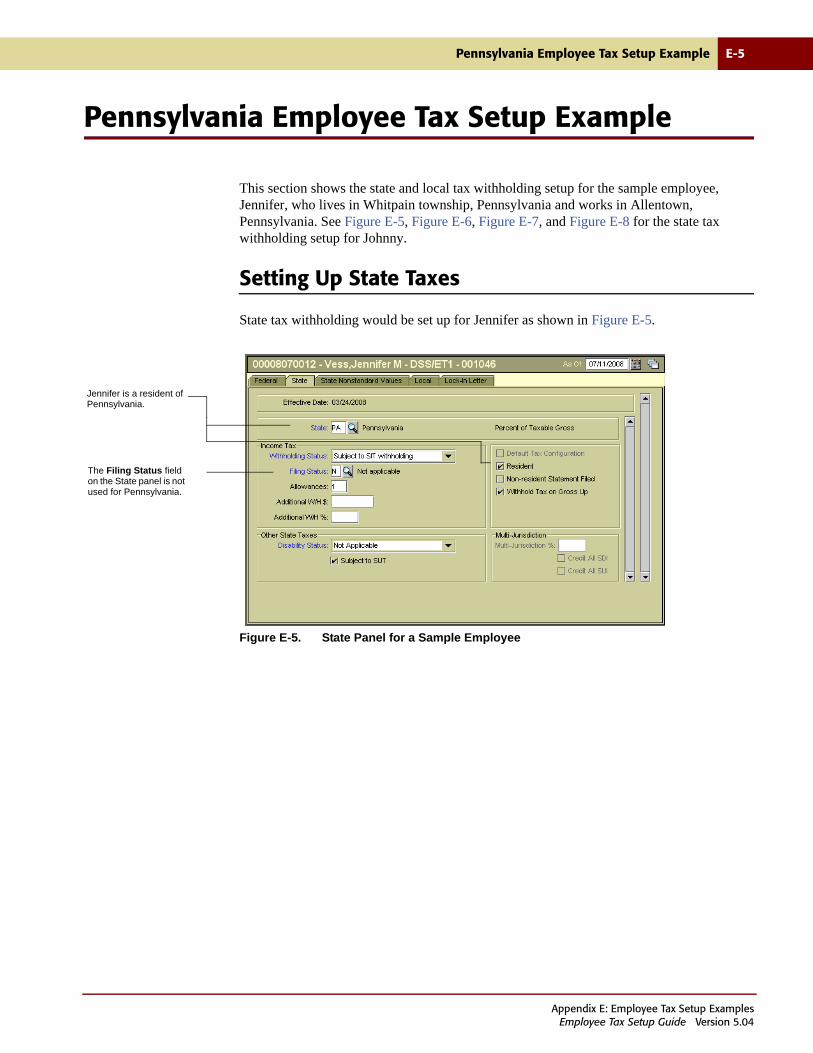

Introduction . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . E-2California Employee Tax Setup Example . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . E-3Maryland Employee Tax Setup Example. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . E-4Pennsylvania Employee Tax Setup Example . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . E-5

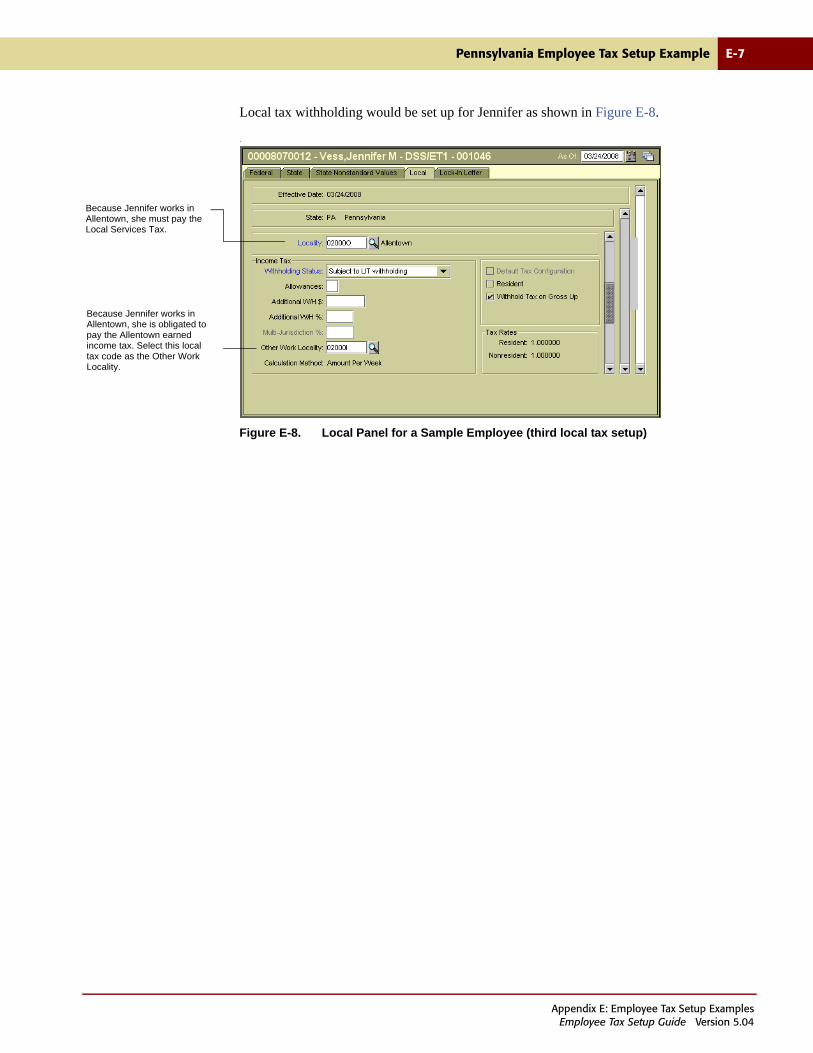

Setting Up State Taxes . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . E-5Setting Up Local Taxes. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . E-6

Glossary

Index

ContentsEmployee Tax Setup Guide Version 5.04

xvi Contents

ContentsEmployee Tax Setup Guide Version 5.04

About This Guide

PAGE TOPIC

xvi Introduction

xvii Audience for This Guide

xviii Enterprise Payroll Documentation Library

xix What’s in This Book

xx Related Documentation

xxi Documentation Conventions

xxiii Providing Comments

About This GuideEmployee Tax Setup Guide Version 5.04

xvi Introduction

Introduction

This guide provides the procedures and information necessary to set up employee tax

withholding information using ADP®’s Enterprise HR® payroll solution (referred to as Enterprise Payroll). Customized instructions are provided for states and localities with special withholding requirements.

The examples in this guide are based on fictional employees, and bear no relationship to any

ADP employees or employees at any other companies.

ADP provides regular tax updates, which identify the tax rates that have been recently modified by the federal, state, or local government. Tax information changes very frequently, so consult ADP Tax Updates and source material from the IRS, state government, or local jurisdiction for the most current information.

The information in this guide is current as of the publication date noted on the inside front cover.

ADP does not render wage, tax, or legal advice. Contact the proper agency to verify all

information. Check with the Internal Revenue Service (IRS) to ensure compliance.

About This GuideEmployee Tax Setup Guide Version 5.04

Audience for This Guide xvii

Audience for This Guide

This guide is written for payroll professionals who are using ADP®’s Enterprise HRSM solution (referred to as ADP Enterprise HR) to set up or modify employee tax withholding information.

To take full advantage of this guide, you should have a basic understanding of how to use the ADP Enterprise HR product, including how to add, modify, and delete information. In addition, you should be comfortable with using a graphical user interface, as well as a web-enabled application. This guide is not intended to be a tutorial.

About This GuideEmployee Tax Setup Guide Version 5.04

xviii Enterprise Payroll Documentation Library

Enterprise Payroll Documentation Library

The Enterprise Payroll library includes this book and the following guides:

• Payroll Setup and Maintenance Guide - describes all the payroll activities that you must complete before you can process a payroll, such as setting up and maintaining company definitions and employee payroll information.

• Payroll Processing Guide - describes the process of running a typical payroll. In addition, it provides instructions on running an off-cycle payroll for on-demand or on-line checks, adjustments, and reversals. It also provides information on post-payroll cycle processes such as preparing your payroll distributions and building your ADP Financial and Compliance Services interface file. It describes all payroll activities that you must complete on a monthly, quarterly, and yearly basis. In addition, it includes tasks that you can complete during the year in preparation for running your year-end tax reports.

About This GuideEmployee Tax Setup Guide Version 5.04

What’s in This Book xix

What’s in This Book

This guide, the Employee Tax Setup Guide, covers the following topics:

Chapter 1, “Setting Up Federal Tax Withholding,” provides general information about income tax and step-by-step instructions for setting up employee federal withholding.

Chapter 2, “Setting Up State Tax Withholding,” provides general information about state taxes and step-by-step instructions for setting up employee state withholding.

Chapter 3, “Setting Up Local Tax Withholding,” provides general information about local taxes and step-by-step instructions for setting up employee local withholding.

Chapters 4-55 provide information for each of the states, plus Puerto Rico and the District of Columbia. The chapters are alphabetized by state name, beginning with Alabama and ending with Wyoming. If a state has local taxes, then state and local withholding instructions are provided in the chapter. In addition, states with occupational taxes or other worked-in taxes provide steps for your convenience. If the state has neither local taxes or special state conditions, then you are referred to Chapter 2, “Setting Up State Tax Withholding,”

Appendix A, “ADP Financial and Compliance Services,” provides helpful information for clients who use ADP Financial and Compliance Services.

Appendix B, “Abbreviations,” lists common tax abbreviations and their meanings.

Appendix C, “Tax Resources,” provides external web sites and other resources that may benefit you in the tax setup process.

Appendix D, “Filing Status Cross-Reference,” lists the filing status options for each state.

Appendix E, “Employee Tax Setup Examples,” provides example setups for three sample employees to illustrate the type of information needed for state and local employee tax withholding.

A Glossary defines terms and acronyms pertinent to employee tax withholding.

An Index is also provided.

About This GuideEmployee Tax Setup Guide Version 5.04

xx What’s New

What’s New

The following change has been made for Version 5.04:

• The Social Security Number field has been removed from the Tax Withholding search dialog box.

Related Documentation

This guide provides the procedures and information necessary to set up employee tax withholding information. Customized instructions are provided for states and localities with special withholding requirements.

You may need to refer to related documentation for other areas of the product. You can access the documentation in the following locations:

• Online manuals through the ADP Enterprise HR application Help menu

• Printed and online manuals on the web at adp4me.adp.com, select the Product Knowledgebase tab and then select Payroll / HR

The Using ADP Enterprise HR Guide also includes a related documentation table which lists

the documentation set delivered with the application, the purpose of the documents, and where the documents can be located. This table also includes a list of delivered online help.

To access the ADP Enterprise HR guides on this web site, you must be assigned the ADP4ME User role in the ADP Netsecure Security Management System. This role is issued a digital certificate. For more information, contact your system administrator.

About This GuideEmployee Tax Setup Guide Version 5.04

Documentation Conventions xxi

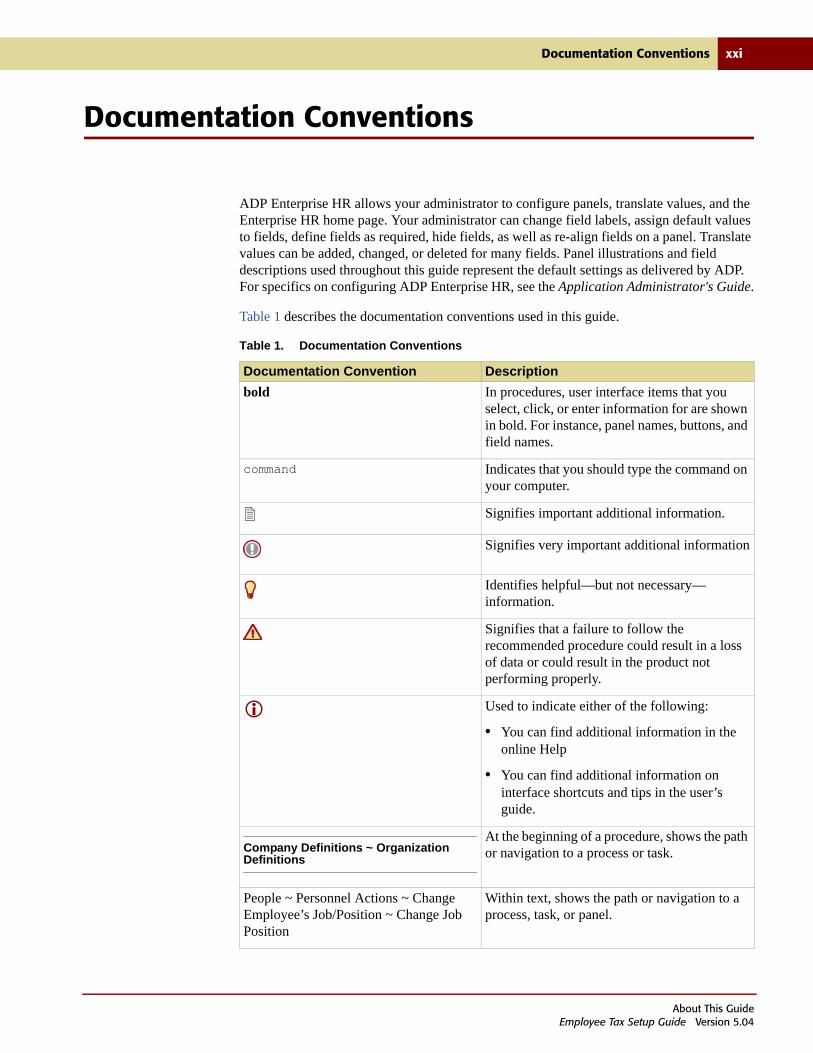

Documentation Conventions

ADP Enterprise HR allows your administrator to configure panels, translate values, and the Enterprise HR home page. Your administrator can change field labels, assign default values to fields, define fields as required, hide fields, as well as re-align fields on a panel. Translate values can be added, changed, or deleted for many fields. Panel illustrations and field descriptions used throughout this guide represent the default settings as delivered by ADP. For specifics on configuring ADP Enterprise HR, see the Application Administrator's Guide.

Table 1 describes the documentation conventions used in this guide.

Table 1. Documentation Conventions

Documentation Convention Description

bold In procedures, user interface items that you select, click, or enter information for are shown in bold. For instance, panel names, buttons, and field names.

command Indicates that you should type the command on your computer.

Signifies important additional information.

Signifies very important additional information

Identifies helpful—but not necessary—information.

Signifies that a failure to follow the recommended procedure could result in a loss of data or could result in the product not performing properly.

Used to indicate either of the following:

• You can find additional information in the online Help

• You can find additional information on interface shortcuts and tips in the user’s guide.

Company Definitions ~ Organization Definitions

At the beginning of a procedure, shows the path or navigation to a process or task.

People ~ Personnel Actions ~ Change Employee’s Job/Position ~ Change Job Position

Within text, shows the path or navigation to a process, task, or panel.

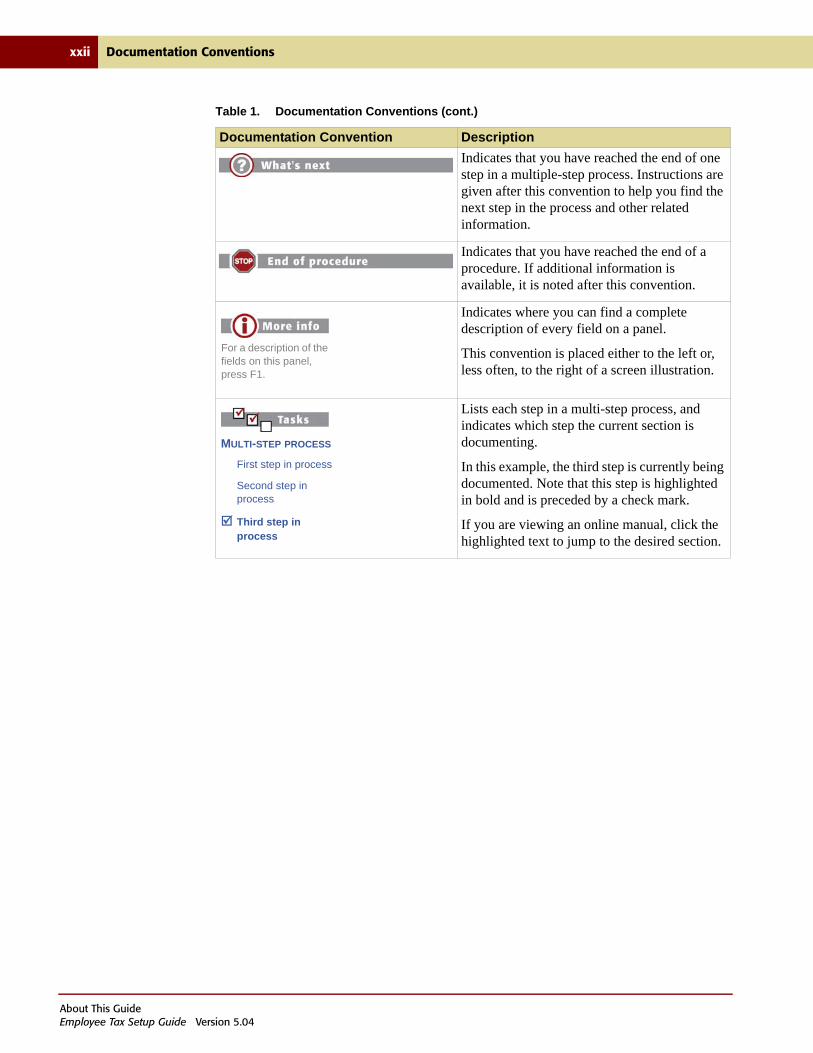

About This GuideEmployee Tax Setup Guide Version 5.04

xxii Documentation Conventions

Indicates that you have reached the end of one step in a multiple-step process. Instructions are given after this convention to help you find the next step in the process and other related information.

Indicates that you have reached the end of a procedure. If additional information is available, it is noted after this convention.

Indicates where you can find a complete description of every field on a panel.

This convention is placed either to the left or, less often, to the right of a screen illustration.

Lists each step in a multi-step process, and indicates which step the current section is documenting.

In this example, the third step is currently being documented. Note that this step is highlighted in bold and is preceded by a check mark.

If you are viewing an online manual, click the highlighted text to jump to the desired section.

Table 1. Documentation Conventions (cont.)

Documentation Convention Description

For a description of the fields on this panel, press F1.

MULTI-STEP PROCESS

First step in process

Second step in process

Third step in process

About This GuideEmployee Tax Setup Guide Version 5.04

Providing Comments xxiii

Providing Comments

We welcome your comments and suggestions about the documentation delivered with ADP Enterprise HR. That way, we can continue to improve the manuals and online Help. You can provide comments in one of the following ways:

• Select Help ~ Online Manuals from the ADP Enterprise HR application and then click the link to submit your suggestions.

• Give us feedback by visiting the web at www.adp4me.nas.adp.com. Select the Product Knowledgebase tab, and then select Payroll / HR.

About This GuideEmployee Tax Setup Guide Version 5.04

xxiv Providing Comments

About This GuideEmployee Tax Setup Guide Version 5.04

Chapter 1

Setting Up Federal Tax Withholding

PAGE TOPIC

1-2 Understanding the Basics

1-3 Understanding ADP Enterprise HR Calculations

1-5 Advance Payments for Earned Income Credit

1-6 Selecting the Federal Filing Status and Entering Withholding Data

1-7 Setting Up Federal Taxes for an Employee

1-13 Entering IRS Tax Lock-In Data

1-17 Printing a Hard Copy of an Electronically Submitted Federal W-4 (PER052)

Chapter 1: Setting Up Federal Tax WithholdingEmployee Tax Setup Guide Version 5.04

1-2 Understanding the Basics

Understanding the Basics

This chapter provides instructions for setting up federal tax withholding. Federal taxes include federal income tax, Social Security and Medicare tax, and Federal Unemployment Tax Act (FUTA) tax.

ADP does not render wage, tax, or legal advice. Contact the proper agency to verify all

information. Check with the Internal Revenue Service (IRS) to ensure compliance.

If the employee works for multiple companies, the tax data is defined by company. In addition, this chapter provides information on rates and calculations.

FICA is better known as Social Security, and it includes Medicare withholding.

You can enter federal, as well as state and local, tax data using the Tax Withholding task.

Paying a New Employee

You can pay a new employee on time even if you have not yet received the employee’s withholding certificates using the Default Tax Configuration option. When you initially hire a new employee, Enterprise Payroll automatically generates a set of default tax data records. This feature allows Enterprise Payroll to pay the employee by calculating the maximum applicable income tax for the jurisdictions. Once you receive the employee’s withholding certificates, you use them to update the employee tax data. See the Payroll Setup and Maintenance Guide for more information.

Transferring an Employee to Another Company

When an employee transfers from one company to another, you can view both the employee tax withholding data for the previous company as well as the employee tax data for the current company to which the employee transferred. The Search dialog box for the Tax Withholding task displays multiple lines for an employee who has been in more than one company so that you can select the company tax information you want to view.

Taxing in Multiple Jurisdictions

To allow processing of an employee’s taxes for a specific amount of taxable wages earned in each jurisdiction, you select the Multi-jurisdiction Tax Processing check box on the Federal panel. Then you can enter the percentage of time worked for the state and/or the locality on the State panel and/or the Local panel. Earnings will be distributed based on the percentage you enter.

The total percent for the states and the total percent for the localities should equal 100

percent.

Chapter 1: Setting Up Federal Tax WithholdingEmployee Tax Setup Guide Version 5.04

Understanding ADP Enterprise HR Calculations 1-3

Understanding ADP Enterprise HR Calculations

ADP Enterprise HR uses formulas to calculate income tax. The formulas instruct the Enterprise Payroll calculation engine how to calculate taxes. Information about the formulas is presented on the Federal/State Formulas panel for those who would like to see how the formulas work. For more information, see the Federal/State Formulas task (Payroll ~ Company Definitions ~ System Tax Data ~ Federal/State Formulas) in the Payroll Setup and Maintenance Guide.

Some of the tax calculations performed by ADP Enterprise HR are described in this section. You indicate the tax method desired for the paysheet or you can use the default information set up in company definitions. For more information, see the Earnings task (Payroll ~ Company Definitions ~ Earnings) in the Payroll Setup and Maintenance Guide.

The rules that apply depend upon how ADP Enterprise HR is initially set up.

Regular Earnings

This method uses the ADP Enterprise HR earnings code to calculate withholding. This method, which is aggregate and annualized, overrides any information that may be set up differently on the paysheet (unless you set the option to specify on paysheet).

Regular earnings must have a lower sequence number than any earnings types that reduce regular earnings. Regular earnings are calculated using the following formula:

Pay Rate + Rate Adjustmentx Hours + Hours Adjustmentx Multiplication Factor + Earnings Adjustment

EARNINGS

Other Earnings

In general, earnings are calculated either by amount or hours.

Amount

Multiplication Factor x Current Pay Period Earnings

(per the earnings or special accumulator code)Hours

Current Period Hours (per the earnings or special accumulator code)

x Hourly Rate (on the paysheet entry)x Multiplication factor

Federal/State formulas are maintained by ADP. If you make a change or addition to the standard tax information delivered with Enterprise Payroll, you are responsible for maintaining the change until it is incorporated into our tax tables.

Chapter 1: Setting Up Federal Tax WithholdingEmployee Tax Setup Guide Version 5.04

1-4 Understanding ADP Enterprise HR Calculations

Multiple Earnings

Multiple earnings occur when a worker has two different jobs, is paid two different ways, or works for two different companies that use the same payroll system. For example, a salaried worker paid overtime by the hour would have multiple earnings, with one earnings code applied to the salaried work and another code applied to the overtime hours.

You must set up multiple earnings codes to use the multiple earnings method. You can use a special accumulator code to indicate multiple earnings. The calculation is set for each of the multiple earnings codes.

The following rules apply for calculations with multiple earnings. Examples assume that the

regular earning is set to Specified on paysheet and that the supplemental tax method is Percent of Taxable Gross as displayed on the Federal/State Tax Configuration panel (Payroll ~ Company Definitions ~ System Tax Data ~ Federal/State Tax Configuration).

Supplemental

Enterprise Payroll’s tax processing supports various tax calculation methods for supplemental earnings, including the use of aggregate tax methods where required. The method Enterprise Payroll uses for calculating withholding tax on supplemental payments may differ (in California only) depending on whether the employee receives a supplemental payment along with regular wages, or instead, receives a separate check for supplemental payment.

To view the method of supplemental withholding tax calculation, use the Federal/State Tax Configuration task (Payroll ~ Company Definitions ~ System Tax Data). See the Payroll Setup and Maintenance Guide for more information.

Table 1-1. Multiple Earnings Rules

When the other earning is set to...

And the paysheet is set to... Then ADP Enterprise HR calculates...

Specified on paysheet

N/A*

* This column is not applicable in this row.

Both earnings based on what is selected in the paysheet.

Annualized Annualized Both earnings as annualized.

Supplemental Regular earning as supplemental and other earning as annualized.

Cumulative Regular earning as cumulative and other earning as annualized.

Supplemental Annualized Regular earning as annualized and other earning as supplemental.

Supplemental Both earnings as supplemental.

Cumulative Regular earning as cumulative and other earning as supplemental.

Chapter 1: Setting Up Federal Tax WithholdingEmployee Tax Setup Guide Version 5.04

Advance Payments for Earned Income Credit 1-5

Advance Payments for Earned Income Credit

EIC is a refundable tax credit for people who work and have earned income from employment or self-employment below established amounts. The credit is available to anyone who qualifies for the credit and files a federal income tax return (even if no tax is due).

EIC reduces the amount of tax owed and may also provide a refund, which the employer provides by adding advance payments to the employee’s paychecks. Generally, employers make the advance EIC payment from the deposit for withheld income tax and employee Social Security and Medicare taxes.

You apply EIC to Federal Tax Withholding by having the employee complete a W-5 form and entering the data on the Federal panel (Employee Information ~ Change Employee Payroll Data ~ Tax Withholding) in the EIC Status field.

The W-5 form specifies the marital status of the employee and whether the spouse has also completed a W-5. Enterprise Payroll uses this information and the gross wages of the employee to determine whether advance payments apply.

The W-5 form expires at the end of the year, so the employee must complete a W-5 every

year.

Refer to Table 1-3 to reference Earned Income Credit values on the Federal panel.

Table 1-2. Earned Income Credit

Federal Certificate Line or Reference Certificate Value

ADP Enterprise HR Value

Line 2 Single, head of household, or qualifying widow(er) S

Line 2 Married filing jointly M

Line 3 If married, does spouse have a Form W-5 in effect = Yes

B

Line 3 If married, does spouse have a Form W-5 in effect = No

M

Chapter 1: Setting Up Federal Tax WithholdingEmployee Tax Setup Guide Version 5.04

1-6 Selecting the Federal Filing Status and Entering Withholding Data

Selecting the Federal Filing Status and Entering Withholding Data

The filing status and withholding allowances work together to determine federal income tax.

Selecting the Filing Status

Refer to Table 1-3 to complete the Filing Status field on the Federal panel. If no status is provided by the employee, leave the default value of S (Single).

Entering Withholding Allowances

In the Allowances field on the Federal panel, enter the total number of allowances the employee is claiming for federal withholding tax purposes. This number is found on Line 5 of Form W-4.

Table 1-3. Filing Status Definitions

Federal Certificate Line or Reference Certificate Value

Definition of Value

ADP Enterprise HR Value

Line 3 Single Single S

Line 3 Married Married M

Line 3 Married, but withhold at a higher Single rate

Married, using single rate

S

N/A N/A Non-Resident O

Chapter 1: Setting Up Federal Tax WithholdingEmployee Tax Setup Guide Version 5.04

Setting Up Federal Taxes for an Employee 1-7

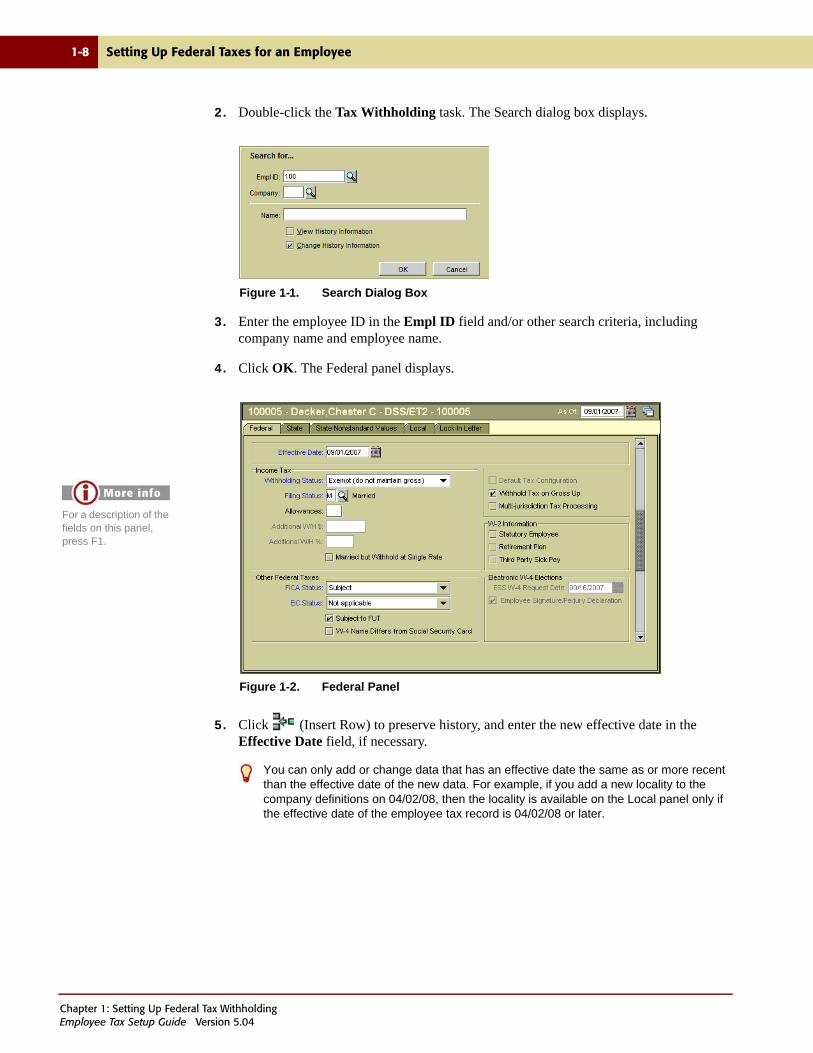

Setting Up Federal Taxes for an Employee

This section provides instructions for entering federal tax withholding information for an employee. Use the Federal panel (Employee Information ~ Change Employee Payroll Data ~ Tax Withholding) to set up the employee’s income tax information.