endesa chile may 2007 - iis windows serverlibrary.corporate-ir.net/library/10/106/106239/items/...13...

TRANSCRIPT

1

Endesa Chile

May 2007

2

Index

Financial Profile and Dividend Distributionüü

üü Operating Highlights and Investments

üü Introduction

üü Sustainability and Social Responsibility

üü Value Drivers

3

Simplified Ownership Structure

ARGENTINA

Pangue

94,99%

Celta

100,00%

San Isidro

100,00%

Costanera

69,76%1

El Chocón

64,69%2

GENERATION

Ingendesa

100%

Túnel El Melón

99,95%

ENDESA

VPP

(Affiliates)

COLOMBIA

Betania

99,99%

Emgesa

23,45%

PERÚCHILE

Edegel

33,06%

Pehuenche

92,65%

Other Businesses

Enigesa

100,00%

CEMSA

45,00%

Gas Atacama

50,00%

ENDESA BRASIL

33,6%3

Electrogas

42,50%Endesa Eco

100,00%

HidroAysén

51,0%

1 y 2Considers recent interest purchases in El Chocón (additional 17,2%) and in Costanera (additional 5,5%)

3Considers the exercise of convertible bonds of AMPLA estimated by year 2008

4

4,477 MW36% Installed Cap.

22 Plants

1,430 MW30% Installed Cap.

9 Plants

2,829 MW21% Installed Cap.

11 Plants

TOTAL: 12.374 MWTOTAL: 12.374 MW

47 Plants47 Plants

3,639 MW15% Installed Cap.

5 Plants

Gx: 980 MW (2 plants)Dx: 4.8 mm Clients

Tx: 2,100 MW

COLOMBIA

PERU

CHILE

Equity AffiliateEndesa Brasil

ARGENTINA

(33.6%)

Figures as of March 2007

Hydro 64%

Thermo 36%

Installed Capacity per Country

5

90

105

120

135

150

165

180

195

210

225

240

255

270

1993

1994

1995

1996

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

Mar-07

Regional Energy Demand Index

Base 1993 = 100%

ü Increasing demand in all 5 countries in which we are present

ü Lack of investments necessary to face the increase in demand

ü Regional scenario of pressures for an increase in energy prices

CHILE

PERU

ARGENTINA

BRAZIL

COLOMBIA

Demand Growth during 1Q07 vs. 1Q06:

Chile 5.9% Argentina 4.5% Brasil 3.7%

Perú 9.5% Colombia 5.2%

6

Endesa Chile – Strengths & Opportunities

Ø Financial Results Improving

Ø Highly efficient Generation Assets

Ø Stable Cash Flow

Ø Strengthened Balance Sheet

Ø Know-how of the Business

Investment Opportunities

Región à muy bien

Ø Economic Stability

Ø Growing Demand

Ø Positive Changes in Regulation

Region à Growing

Endesa à well prepared

7

Argentina10%

Perú12%

Chile55%

Colombia23%

EBITDA Distribution per Country

Figures presented in Chilean GAAP expressed in historical US$

Total EBITDA 1Q07Total EBITDA 1Q07

US$ 406 millionUS$ 406 million Chile58%

Argentina8%

Colombia21%

Peru13%

Total EBITDA 2006Total EBITDA 2006

US$ 1,279 millionUS$ 1,279 million

8

Thermopeakers

Operational Efficiencies

2/3 EOC plants à most efficient in their markets

00

2,000

4,000

Hydro

7,932 MW 64%

Thermo(efficient)

3,769 MW 31%

00

6,000

8,000

10,000

99,29%99.29%99,15%99.15%

aaParPar meter Endesa Benchmark

Availability

0505

93,45%93.45%

NERC 04 NERC 04

89,27%89.27%

Figures as of March 31st, 2007

aaParPar meter Endesa Benchmark

Reliability

0505 NERC 04 NERC 04

Hydro Thermo(efficient)

Thermo(peakers)

673 MW 5%

NERC: North American Electric Reliability Council

9

Commercial Policy

ü Key strategic instrument for adding value to our portfolio

ü Optimizes our commercial portfolioü Reduces risks associated with overexposing our

capacity

0%

20%

40%

60%

80%

100%

120%

1998-2000 2007-2010

Regulated

Un-regulated

Spot28%

56%

35%

36%

16%29%

10

Index

Financial Profile and Dividend Distributionüü

üü Operating Highlights and Investments

üü Introduction

üü Sustainability and Social Responsibility

üü Value Drivers

11

High

light

s

Fina

ncia

l Inf

o

Consolidated Energy Sales & Average Sale PriceEnergy Sales & Average Sale Priceü Increasing operating performance and EBITDA

throughout the years.ü Highly competitive generation assets (64%

Hydro).ü Stable growth (energy consumption growing). ü Investment opportunities.

52,98646,86545,038 49,54156,942 57,988

30.926.1

38.534.944.241.9

0

20,000

40,000

60,000

Dec-02 Dec-03 Dec-04 Dec-05 Dec-06 Mar-07

Gigawatt Hours

5

20

35

50

65

(US$/MWh)

As of March 2007 (3M)As of March 2007 (3M)

36%21%

64%79%

Capacity mix Generation mix

Hydro

Thermal24%

36%

40%

Physical SalesMix

Regulated

Un-regulated

Spot

(US$ million) Mar-06 Mar-07 % Var.Operating Revenues 552 731 32%Operating Income 227 316 39%Financial Debt 3,925 3,947 1%EBITDA 305 406 33%

Mar-07 figures in this graph are expressed in TTM.

12

High

light

s

Fina

ncia

l Inf

o

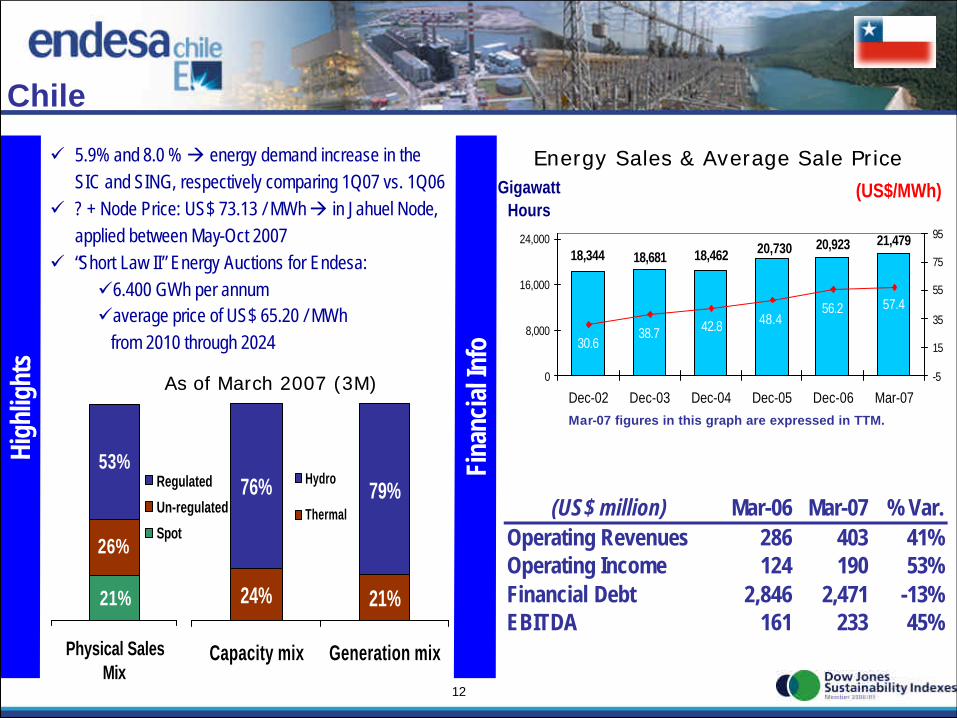

Chile

26%

21%

53%

Physical SalesMix

Regulated

Un-regulated

Spot

21,47920,92318,46218,344 18,681

20,730

56.2 57.4

42.8 48.4

30.638.7

0

8,000

16,000

24,000

Dec-02 Dec-03 Dec-04 Dec-05 Dec-06 Mar-07

Gigawatt Hours

-5

15

35

55

75

95

(US$/MWh)

Energy Sales & Average Sale PriceEnergy Sales & Average Sale Priceü 5.9% and 8.0 % à energy demand increase in the SIC and SING, respectively comparing 1Q07 vs. 1Q06

ü ? + Node Price: US$ 73.13 / MWh à in Jahuel Node, applied between May-Oct 2007

ü “Short Law II” Energy Auctions for Endesa:ü6.400 GWh per annumüaverage price of US$ 65.20 / MWh

from 2010 through 2024

24% 21%

76% 79%

Capacity mix Generation mix

Hydro

Thermal (US$ million) Mar-06 Mar-07 % Var.Operating Revenues 286 403 41%Operating Income 124 190 53%Financial Debt 2,846 2,471 -13%EBITDA 161 233 45%

Mar-07 figures in this graph are expressed in TTM.

As of March 2007 (3M)As of March 2007 (3M)

13

High

light

s

ü 4.5% à energy demand increase in the MEM comparing 1Q07 vs. 1Q06

ü Over 20% increase in average spot prices during 1Q07 vs 1Q06 à recognition of higher Natural Gas prices for industrial users

ü Foninvemem 1,600 MW : 21% share

Fina

ncia

l Inf

o

Argentina

17%

83%

Physical SalesMix

Un-regulated

Spot

13,86113,92611,603

7,8979,260

12,578

31.7 33.322.9 24.3

17.3 20.20

4,000

8,000

12,000

16,000

Dec-02 Dec-03 Dec-04 Dec-05 Dec-06 Mar-07

Gigawatt Hours

0

20

40

60

80

(US$/MWh)

Energy Sales & Average Sale PriceEnergy Sales & Average Sale Price

64% 63%

36% 37%

Capacity mix Generation mix

Hydro

Thermal

(US$ million) Mar-06 Mar-07 % Var.Operating Revenues 79 99 25%Operating Income 13 17 31%Financial Debt 218 320 47%EBITDA 29 33 14%

Mar-07 figures in this graph are expressed in TTM.

As of March 2007 (3M)As of March 2007 (3M)

14

High

light

s

Fina

ncia

l Inf

o

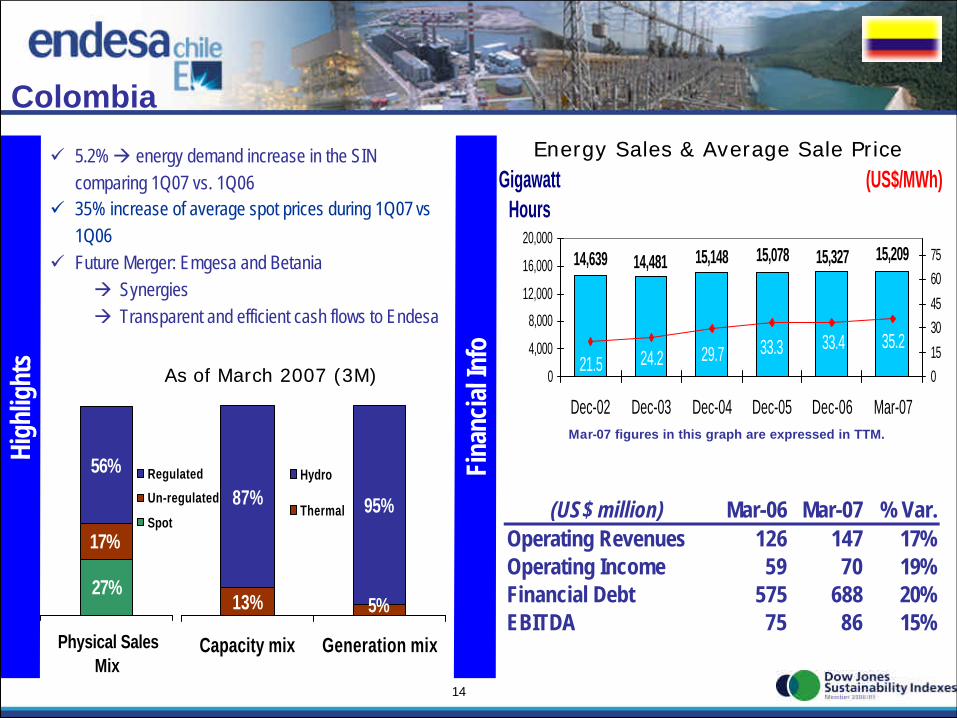

Colombia

Energy Sales & Average Sale PriceEnergy Sales & Average Sale Priceü 5.2% à energy demand increase in the SIN comparing 1Q07 vs. 1Q06

ü 35% increase of average spot prices during 1Q07 vs1Q06

ü Future Merger: Emgesa and Betaniaà Synergiesà Transparent and efficient cash flows to Endesa

15,20915,32715,14814,639 14,481 15,078

33.4 35.229.7 33.3

21.5 24.20

4,000

8,000

12,000

16,000

20,000

Dec-02 Dec-03 Dec-04 Dec-05 Dec-06 Mar-07

Gigawatt Hours

015

3045

6075

(US$/MWh)

13%

87% 95%

5%

Capacity mix Generation mix

Hydro

Thermal

17%

27%

56%

Physical SalesMix

Regulated

Un-regulated

Spot(US$ million) Mar-06 Mar-07 % Var.

Operating Revenues 126 147 17%Operating Income 59 70 19%Financial Debt 575 688 20%EBITDA 75 86 15%

Mar-07 figures in this graph are expressed in TTM.

As of March 2007 (3M)As of March 2007 (3M)

15

High

light

s

Fina

ncia

l Inf

o

PerúEnergy Sales & Average Sale PriceEnergy Sales & Average Sale Priceü 9.5% à energy demand increase in the SINAC

comparing 1Q07 vs. 1Q06.ü Low prices of natural gas from Camisea ü June 2006à merger with Etevensa:

üAddition of 457 MW of Thermal Capacityü Improved hydrological exposure

ü Law 28,832: (i) energy bidding process; (ii) long-term contracts with regulated consumers; (iii) fixed pricessubject to indexation

7,4396,776

4,3284,158 4,443 4,600

46.3 45.052.3 48.039.1 40.6

0

2,000

4,000

6,000

8,000

Dec-02 Dec-03 Dec-04 Dec-05 Dec-06 Mar-07

Gigawatt Hours

0

30

60

90

120

(US$/MWh)

48%32%

52%68%

Capacity mix Generation mix

Hydro

Thermal

46%

12%

42%

Physical SalesMix

Regulated

Un-regulated

Spot (US$ million) Mar-06 Mar-07 % Var.Operating Revenues 62 83 34%Operating Income 30 39 30%Financial Debt 277 469 69%EBITDA 40 54 35%

Mar-07 figures in this graph are expressed in TTM.

As of March 2007 (3M)As of March 2007 (3M)

16

Expected LNG Arrival: Mid of 2009Expected LNG Arrival: Mid of 2009

Liquefied Natural Gas Project in Chile

ü Chilean government initiative, led by ENAPü LNG à Reliable source of generation fuelü Price in line with other commodity pricesü LNG supplied by British Gasü Endesa Chile will participate in the re-gasification terminal (9.5

m3/day)

17

üInstalled Cap.: 377 MW (with LNG)

üInvestment: US$ 210.5 millionüTurbine Manufacturer: Mitsubishi

üFirst LNG Power Plant in Chile

üDUAL Technology for Operations (LNG and Fuel Oil)

Expected Date of Completion:Expected Date of Completion:

üü Open Cycle: April 2007 (operating)Open Cycle: April 2007 (operating)

üü Combined Cycle: March 2008Combined Cycle: March 2008

San Isidro Plant Expansion Project, Chile

18

üPass-through Plant

üInstalled capacity: 32 MW

üInvestment: US$ 44 million

üEnvironmental permits

approved

Expected Date of Completion: 2nd Semester 2007Expected Date of Completion: 2nd Semester 2007

Palmucho, Pass-Through Hydroelectric Plant, Chile

19

Expected Date of Completion: April 2008 Expected Date of Completion: April 2008

Upcoming Endesa ECO Projects:

üMini-hydro “Ojos de Agua”üMaule Region, ChileüInstalled capacity: 9.0 MWüInvestment: US$ 19 millionüRegistered as CDM Project under UNFCCC

üMini-hydro “Ojos de Agua”üMaule Region, ChileüInstalled capacity: 9.0 MWüInvestment: US$ 19 millionüRegistered as CDM Project under UNFCCC

üFirst wind farm “Canela” (I, II) in SICüInstalled capacity: 18.15 MWüInvestment: US$ 30 million

üFirst wind farm “Canela” (I, II) in SICüInstalled capacity: 18.15 MWüInvestment: US$ 30 million

Expected Date of Completion: 2nd semester 2007Expected Date of Completion: 2nd semester 2007

20

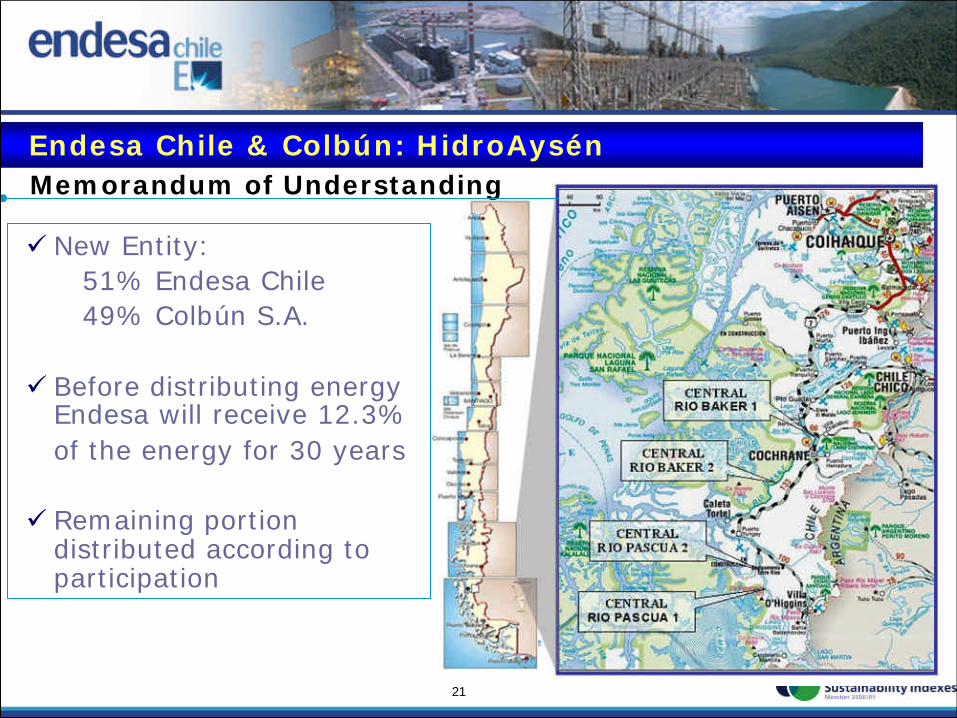

Aysen Project

ü Plants: El Salto, Baker 1, Pascua 2, Pascua 1 and Baker 2

ü Installed capacity: 2,400 MW

ü Total investment: US$ 4,000 million(including transmission line)

Expected Time of Completion all plants: 2018Expected Time of Completion all plants: 2018

üInvestment includes a 2,000 kms Direct Current (HVDC) transmission line from Cochrane to Santiago (US$1.5 billion)

üAgreement with Transelec for research and valuation

Expected Date of Completion (first plant): 2012Expected Date of Completion (first plant): 2012

21

Endesa Chile & Colbún: HidroAysén

ü New Entity:51% Endesa Chile49% Colbún S.A.

ü Before distributing energy Endesa will receive 12.3%of the energy for 30 years

ü Remaining portion distributed according to participation

Memorandum of Understanding

22

Aysen Project: Environmental Issues

ü Consciousness of sustainable development based on the protection of

nature and social development

ü Environmental Impact Studies to comply and respond to:

à minimize flooding surface

à protection of wild life (flora and fauna)

à impact in glaciers

à impact in touristic and agricultural zones

à minimize reallocations of local inhabitants

23

Thermo

Hydro

ChoshuencoChoshuenco

134 MW134 MW

Los CLos Cóóndoresndores

156 MW156 MWNeltumeNeltume

403 MW403 MW

Bocamina IIBocamina II

350 MW350 MW

QuinteroQuintero

385 MW385 MW

Steffen y PortSteffen y Portóónn

685 MW685 MW

Projects Currently Being Studied:

24

ü Authority’s response to high energy demand in the country

ü Financed by MEM account receivables

ü 89% of the generators adhered

ü 7% projected property of plants without direct contributions by Endesa

ü Commitment to recover market prices by 2008

2 New Combined Cycles

totalizing 1,600 MW

Argentina

FONINVEMEM

Expected date of completion:Open cycle: End of 2008Combined cycle: During 2009

25

Index

Financial Profile and Dividend Distributionüü

üü Operating Highlights and Investments

üü Introduction

üü Sustainability and Social Responsibility

üü Value Drivers

26

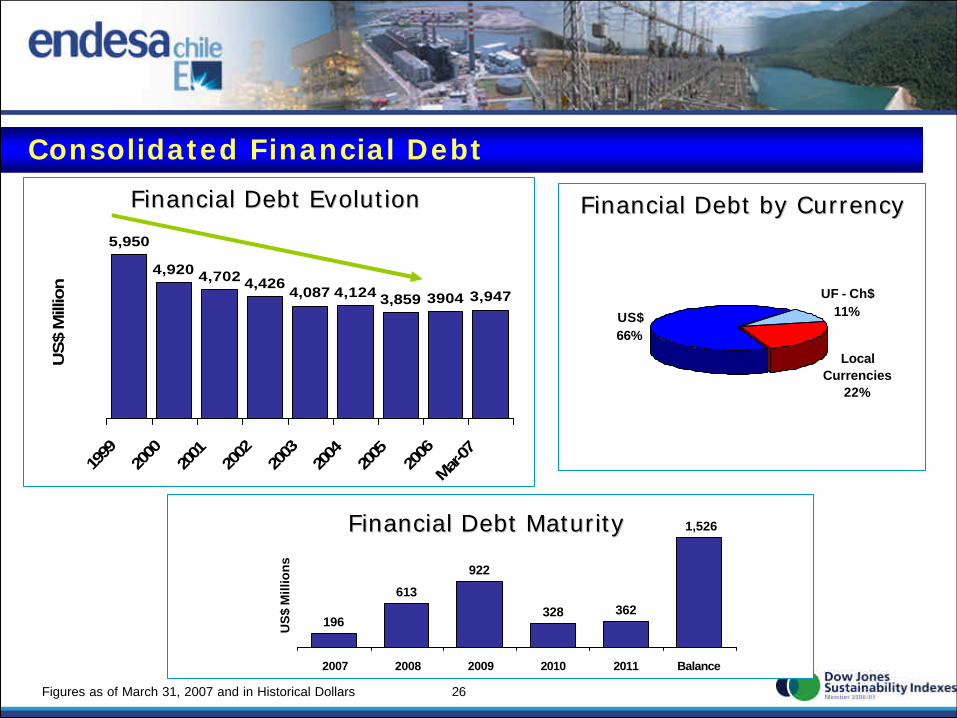

5,950

4,920 4,702 4,4264,087 4,124 3,859 3,9473904

1999

2000

2001

2002

2003

2004

2005

2006

Mar-07

US

$ M

illio

n

Financial Debt EvolutionFinancial Debt Evolution

Consolidated Financial Debt

Local Currencies

22%

US$66%

UF - Ch$11%

Financial Debt by CurrencyFinancial Debt by Currency

196

613

922

362328

1,526

2007 2008 2009 2010 2011 Balance

US

$ M

illio

ns

Financial Debt MaturityFinancial Debt Maturity

Figures as of March 31, 2007 and in Historical Dollars

27

Financial Ratios

323

1,380

758875

9711,105

1,279

296 335 346 349 322

2.9

4.67

3.54.25

5.84

3.1

4.3

2.6 2.6 2.8 3.2

4.0

0

250

500

750

1000

1250

1500

2002 2003 2004 2005 2006 Mar-07

US

$ M

illio

ns

0

1

2

3

4

5

6

7

Tim

es

EBITDA Financial Expenses

Financial Debt/EBITDA Coverage

Figures expressed in historical US$. Figures as of Mar-07 are TTM.

28

*

* Considers the exercise of a Yankee Bond Put Option in 2009 worth US$ 220 million, which matures in 2037.

Debt Profile by Country

Figures as of March 31, 2007

ChileTotal Financial Debt:

US$ 2,471 million

23586 13

414

14213

12 14

384

41

414631*

2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017 After2017

35 3280

8 17 0 0 085

14372

2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017

63 58 61

4 0 0 0 0 0

5974

2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017

ColombiaTotal Financial Debt:

US$ 687 million

PeruTotal Financial Debt:

US$ 471 million

ArgentinaTotal Financial Debt:

US$ 320 millones44 26

123023

26 2223 42

Mitsubishi El Chocón

2973

110

0 0

96

1878

139

0

144

2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017

29

ü Investment Grade from all international rating agencies.

ü Current ratings: – Moody's Baa3 Stable– Standard and Poor's BBB- Positive *– Fitch BBB Stable

* S&P under review for possible upgrade

Rating Agencies

30

Index

Financial Profile and Dividend Distributionüü

üü Operating Highlights and Investments

üü Introduction

üü Value Drivers

üü Sustainability and Social Responsibility

31

2000 2001 2002 2003 2004 2005 2006 2007

DSE

Ad

din

g V

alu

e

MAC

SGA

Sustainability & Social Responsability

32

39%

63%

86%98% 98%

2002 2003 2004 2005 2006

Environment and Corporate Social Responsibility

Installed Capacity ISO 14001 Certified

Installed Capacity OHSAS 18001 Certified

0% 3%

28%

95% 96%

2002 2003 2004 2005 2006

Figures as of December 31st, 2006

33

Index

Financial Profile and Dividend Distributionüü

üü Operating Highlights and Investments

üü Introduction

üü Sustainability and Social Responsibility

üü Value Drivers

34

ü Increasing efficiency and capacity

ü Improving operating performance

ü Continuous efforts over issues concerning:ü Sustainability ü Corporate Governance

ü Optimization of asset portfolio

Endesa Chile

Increasing Return for our InvestorsIncreasing Return for our InvestorsValue Drivers

Portfolio consisting of investments in 5

countries, but anchored in Chile

35

Contact us at:

Endesa Chile’s Investor Relations Team

Jaime MonteroInvestor Relations

DirectorEndesa Chile

(56-2) [email protected]

Irene AguilóInvestor Relations

Executive(56-2) 630 96 04

Jacqueline MichaelInvestor Relations

Executive(56-2) 630 95 [email protected]

This presentation may contain statements that constitute forward-looking statements within the meaning of the Private Securities Litigation Reform Act of 1995. These statements may appear in a number of places in this announcement and include statements regarding the intent,

belief or current expectations of Endesa Chile and management with respect to, among other issues: (1)Endesa Chile business and cost-reduction plans; (2) trends affecting Endesa Chile financial condition or results of operations, including market trends in the electricity sector in Chile or elsewhere; (3) supervision and regulation of the electricity sector in Chile or elsewhere; and (4) the future effects of any changes in the

laws and regulations applicable to Endesa Chile and its affiliates. Such forward-looking statements are not guarantees of future performance and involve risks and uncertainties. Actual results may differ materially from those in the forward-looking statements as a result of various factors.

Readers are cautioned not to place undue reliance on those forward-looking statements, which speak only as of their dates. Endesa Chile undertakes no obligation to release the results of any revisions to these forward-looking statements.

Juan Pablo ReitzeHead of Investor

Relations(56-2) 630 96 [email protected]