energy, romania 03 march 2017 romanian oil and gas · pdf fileenergy, romania 03 march 2017...

TRANSCRIPT

Energy, Romania 03 March 2017

Romanian Oil and Gas Sector report

Growth in the pipeline

In this report, we reiterate our bullish view on Romgaz and Petrom,

increasing our price targets (PTs) for Petrom (to RON 0.361 from

RON 0.302) and Romgaz (to RON 36.6 from RON 36.4). The natural gas

price recovery since October 2016 should rescue the Romanian market

and players from the asymmetric risks associated from being an

import-only market, in our view. In the near team, we see a recovery in

volumes, as well as prices, a renewal of the taxation and royalty

system, and investments in infrastructure and new development

projects from both companies as driving sentiment, production

volumes and earnings. Of the two companies, we prefer Romgaz

slightly, which we see as a bigger beneficiary of the recovery, and able

to capitalise faster on new markets when the infrastructure is

completed. On the other hand, we like Petrom’s management, its lower

risk diversified business model, and its long term prospects. However,

the company is not as well-positioned to take advantage of the market

changes, in our view. Nonetheless, although Petrom’s share price

performance since the SPO in October 2016 has reduced the level of

potential upside, the company is still undervalued, in our view.

Romanian macro. We expect the Romanian economy to enjoy high GDP

growth (+4.5% in 2017E and +4.0% in 2018E), and see upside in energy

demand in such a scenario. Petrom’s retail business should be a beneficiary

here, in our view.

Emerging Romania. With increased liquidity of existing stocks and an

eventual listing of Hidroelectrica, which we expect in the next 12-24 months,

we see a greater chance of Romania being upgraded from Frontier to

Emerging Market status. As two of the largest companies, Romgaz and

Petrom would benefit from the resulting inflows.

Gas price recovery. European gas prices reached extremely low levels in

2016, driven by low oil prices and excess natural gas volumes. There was a

correction in 4Q16, with prices 33% higher than the first nine months, and

prices have been even better so far in 2017, up a further 19% ytd.

Refinery margins. We believe that 2017E could turn out to be a good year

for refining margins in Europe. We estimate that Petrom will generate 30%

of its EBITDA from downstream in 2017E.

Royalties and taxes. With the election of a new government in December

2016, we expect to see the issue of royalties decided once and for all. We

believe that there will be no significant increases in rates and that the

separate treatment of offshore projects would catalyse investments.

Unexploited resources. Both companies have significant undeveloped

resources that can be developed, once the export infrastructure is in place.

Export infrastructure. Pipeline infrastructure connecting Romania with

markets elsewhere in Europe, which should be completed in the next two

years, in our view, should be a big game changer for both companies, in our

view.

Romgaz

BUY (maintained)

Price: RON 28.5

Price target: RON 36.6 (from

RON 36.4)

Petrom

BUY (maintained)

Price: RON 0.307

Price target: RON 0.361 (from

RON 0.302)

EQUITY

RESEARCH Analysts: Jonathan Lamb, Lucian Albulescu, Ondrej Slama London: +44 20 3530 0621

E-mail: [email protected], [email protected] Website: www.wood.com

Price Upside Mkt EV/EBITDA Div yield

Rating target potential Cap 12M Perf 2016E 2017E 2018E 2016E 2017E 2018E

Romgaz BUY 36.6 28.3% 2,582 21.0% 4.9x 4.1x 4.2x 10.5% 9.9% 9.2%

Petrom BUY 0.361 17.6% 3,374 29.0% 5.0x 4.1x 3.9x 5.0% 5.6% 6.0%

Energy, Romania 2 WOOD & Company

Contents

Investment summary ........................................................................................................................................ 3

Valuation ............................................................................................................................................................ 5

Financial forecast changes ............................................................................................................................. 7

Sector discussion ............................................................................................................................................. 8

Romania’s potential for reclassification to Emerging Markets ................................................................. 14

Company sections

Romgaz .................................................................................................................................................... 17

OMV Petrom ............................................................................................................................................ 27

Important disclosures .................................................................................................................................... 37

Closing Prices as of 01 March 2017

© 2017 by WOOD & Company Financial Services, a.s. All rights reserved. No part of this report may be reproduced or transmitted in any form or by any means electronic or mechanical without written permission from WOOD & Company Financial Services, a.s. This report may not be lent, resold, hired out or otherwise disposed of by way of trade in any form of binding or cover other than that in which it is published without written permission from WOOD & Company Financial Services, a.s. Requests for permission to make copies of any part of this report should be mailed to: WOOD & Company Financial Services a.s. Palladium, Namesti Republiky 1079/1a, 110 00 Prague 1 – Czech Republic tel.: +420 222 096 111 fax: +420 222 096 222 http//:www.wood.cz

Energy, Romania 3 WOOD & Company

Investment summary

We believe the Romanian macro environment should be supportive for energy demand going

forward. In 2016, the European gas price was below Romania’s, which created a major problem,

by drawing imports into a market where gas transfers can only go one way. Romgaz was forced

to reduce production, as well as accept a lower price. A 33% recovery in gas prices in 4Q16 bodes

well for 2017E, in our view, as it removes this asymmetric risk. In the longer term, the risk should

be eliminated by interconnection with the other major markets of Eastern and Central Europe,

which we expect in 2019E. In addition, we see the renewal of the royalties system as a catalyst

that should drive further investment, as well as remove uncertainty from both names.

Romanian macro. Romania shares a positive economic outlook for 2017E with many of its neighbours,

and is also enjoying a newly-elected centre-left government, which is largely a known entity and poses

few risks, in our view. Growing prosperity and increasing vehicle numbers should drive the demand for

energy in the coming years, providing a positive outlook for doing business in Romania, in our view.

Gas price recovery. European gas prices reached extremely low levels in 2016, driven by low oil prices

and excess natural gas volumes. However, from 4Q16, there has been a substantial improvement in

prices, removing the incentives to import gas. Therefore, we see less competitive pressure in the gas

market in 2017E, as well as better unit costs.

Quarterly European spot gas prices (EUR/MWh)

Source: Bloomberg, WOOD Research

Refinery margins. Margins in the region have continued to be strong in 2017 ytd, continuing to benefit

from a mixture of low oil prices, recovering regional demand and a slowdown in capacity additions. Our

expectation for margins in the region in 2017E is about 10% higher than in 2016. Current margins are

even better than this, suggesting that there is upside potential, as well as downside, for our expectations.

Royalties and taxes. After three years of uncertainty, we expect to see the finalisation of a new taxation

and royalty system in 2017E. The temporary system in place for the past three years solved the problem

of the government revenue raising in a high oil price environment, but added a new element of

uncertainty to the companies’ investment thesis. We see a new system as positive for investor

perceptions, but also as a possible catalyst for new investment.

Special treatment for offshore investments is particularly important here as tax incentives can have a

very significant impact on the feasibility of capitally-intensive offshore investments. The government

stated publicly last year that it was its aim to treat offshore in a different way, for this reason.

Unexploited resources. Both companies have major resources that are potential development projects.

If the decision is made to proceed with these projects, the future outlook for reserves and production

replacement is better than in the recent past. Decisions will be based on infrastructure investments and

favourable royalties, which we believe are likely to be forth coming.

Export infrastructure. The construction of a natural gas pipeline link between Romania and Hungary

should substantially change the nature of the market, in our view. It would enable gas produced in the

companies’ growth projects to be exported, improving the returns on large projects in particular. It would

also better enable the complete liberalisation of the market, as Romanian gas prices move into line with

the large markets of Central Europe.

Investment opportunities. Both companies have investment opportunities that required the

confirmation of the new royalty system, as well as investments in pipeline infrastructure. The pipelines

are already under construction, and we believe that 2017E is likely to be a year of big decisions for both

companies.

21.6 21.120.1

17.3

13.2 13.2 13.0

17.4

20.8

0.0

5.0

10.0

15.0

20.0

25.0

1Q 2Q 3Q 4Q

2015 2016 2017

Energy, Romania 4 WOOD & Company

The potential of the deep. In June 2016, Romgaz announced that it had discovered a substantial new

natural gas reservoir. Although the results are very preliminary, it estimated the resource at 150-

170m boe. The gas was discovered at a depth of 4,000 metres. Beyond the immediate impact of this

specific discovery on Romgaz, we believe that it increases the likelihood of further discoveries at depth,

in the only substantially unexplored area in Romania.

Romania no longer frontier. Growing liquidity has put the Romanian stock market in a position where

it may be upgraded from Frontier to Emerging Market status. The increase in Petrom’s free float,

following the SPO in 2016, should help Romania to gain Emerging Market status, in our view. We are

seeing greatly increased interest in the market, as well as passive inflows, which should be a catalyst for

market performance. As two of the largest companies in Romania, Petrom and Romgaz would be

substantial beneficiaries of this reclassification.

Energy, Romania 5 WOOD & Company

Valuation

Romgaz trades at a P/E of 8.6x for 2017E and 8.7x for 2018E, based on our estimates, while Petrom

trades at a P/E of 8.2x for 2017E and 7.6x for 2018E. The European integrated peer companies’ average

P/E ratios of 10.1x for 2017E and 9.2x for 2018E, based on consensus estimates, suggest that Petrom

is undervalued and Romgaz is fairly valued, compared to their peers.

On a price to book metric, the peer average ratio is 1.0x for 2017E and 0.9x for 2018E, based on both

consensus and our estimates. In comparison, Romgaz is trading at 1.1x for both 2017E and 2018E,

while Petrom trades at 0.6x for both 2017E and 2018E, suggesting that Petrom is relatively undervalued

vs. the peer group, in our view.

European peers, group multiples

P/E (x) P/CF (x) P/BV (x)

European integrateds MCAP USD m

Local price 2016 2017E 2018E 2016 2017E 2018E 2016E 2017E 2018E

OMV AT 12,485 36.1 10.9 11.1 8.6 3.6 3.1 3.0 1.0 1.2 1.1

MOL HU 7,329 20,865.0 n.m. 8.3 7.1 4.4 4.0 3.6 1.0 0.9 0.8

Petrom RO 3,987 0.3 15.8 8.2 7.6 3.7 3.1 3.0 0.6 0.6 0.6

PGNiG PL 8,846 6.1 14.9 13.7 12.6 7.4 6.7 6.4 1.1 1.1 1.0

Romgaz RO 2,537 28.2 10.6 8.6 8.7 5.4 5.2 5.0 1.1 1.1 1.0

Average 13.1 10.1 9.2 4.9 4.4 4.2 1.0 1.0 0.9

P/E (x) P/CF (x) P/BV (x)

European downstream MCAP USD m

Local price 2016 2017E 2018E 2016 2017E 2018E 2016E 2017E 2018E

PKN PL 9,902 94.5 8.5 7.2 8.8 5.5 5.1 5.7 1.5 1.2 1.1

TUPRAS TR 5,853 84.1 14.2 9.6 8.8 6.9 5.8 5.7 2.5 2.5 2.2

HELLENIC PETROLEUM GR 1,547 4.8 7.3 9.4 8.6 (1.7) 3.9 3.3 0.0 0.0 0.0

MOTOR OIL (HELLAS) GR 1,706 14.6 6.3 8.3 8.0 23.5 5.8 5.7 2.1 1.9 1.6

LOTOS PL 2,217 49.0 7.6 8.4 10.7 4.8 4.0 4.2 1.0 0.9 0.8

UNIPETROL CP 1,507 212.5 9.0 4.4 5.8 3.5 1.0 0.8

NESTE OYJ SF 9,225 34.0 11.4 13.2 13.0 7.3 8.8 8.3 2.4 2.1 2.0

SARAS SPA IT 1,588 1.6 8.8 9.9 11.2 4.0 4.4 4.3 1.6 1.5 1.4

Average 9.1 8.8 9.9 7.0 5.2 5.3 1.5 1.4 1.3

Source: Bloomberg, WOOD Research

On EV/EBITDA, Petrom’s ratios are 4.1x for 2017E and 3.77x for 2018E, while Romgaz’s ratios are 4.1x

for 2017E and 4.2x for 2018E, on our estimates, compared with 4.6x and 4.2x for its peer group, on

consensus estimates. On this metric, both Petrom and Romgaz look undervalued, in our view.

Energy, Romania 6 WOOD & Company

EV/EBITDA and dividend yields

EV/EBITDA (x) Div yield

European integrateds 2016 2017E 2018E 2016 2017E 2018E

OMV AT 6.0 5.5 4.8 2.8% 3.1% 3.5%

MOL HU 4.3 3.6 3.2 2.6% 2.8% 3.3%

Petrom RO 4.9 4.1 3.8 5.0% 5.6% 6.0%

PGNiG PL 6.0 5.6 5.2 3.4% 3.4% 3.8%

Romgaz RO 4.9 4.1 4.2 9.7% 9.2% 10.7%

Average 5.2 4.6 4.2 4.7% 4.8% 5.0%

EV/EBITDA (x) Div yield

European downstream 2016 2017E 2018E 2016 2017E 2018E

PKN PL 6.2 4.8 5.3 2.3% 3.9% 4.0%

TUPRAS TR 9.7 6.7 6.3 5.8% 8.3% 9.1%

HELLENIC PETROLEUM SA GR 4.8 4.8 4.6 0.0% 3.2% 3.5%

MOTOR OIL (HELLAS) SA GR 3.5 4.2 3.8 6.4% 4.8% 5.0%

LOTOS PL 5.0 5.4 5.9 0.0% 0.0% 0.0%

UNIPETROL CP 4.7 2.4 n.m. 2.4% 2.8%

NESTE OYJ SF 6.7 7.5 7.1 3.5% 3.7% 3.7%

SARAS SPA IT 2.8 3.0 3.0 5.9% 5.5% 5.4%

Average 5.4 4.8 5.1 3.3% 4.0% 4.4%

Source: Bloomberg, WOOD Research

Energy, Romania 7 WOOD & Company

Financial forecast changes

Since our previous report, published on 15 April 2016 (CEE Oil and Gas_Transfer of

Coverage_15Apr2016.pdf, (2 MB)), the problems with natural gas imports cut Romgaz’s sales and

revenues to below our expectations for 2016. We had previously assumed that gas price deregulation

would proceed as planned. However, as the planned increase did not happen in 2016, we have taken a

more conservative view on the process. On the positive side, we assume that exports will start in 2019E,

enabling the company to take advantage of its spare capacity and new discovery. Therefore, the

company’s EBITDA is lower from 2016-19E, but higher after that.

In the case of Petrom, once again, 2016 was below our expectations, but successful cost cutting means

that earnings should be higher from 2017E-onwards, in our view.

EBITDA forecast changes since our last report (RON m)

Source: WOOD Research

0

500

1,000

1,500

2,000

2,500

3,000

3,500

2016 2017E 2018E 2019E 2020E

Romgaz

Previous Current

0

1,000

2,000

3,000

4,000

5,000

6,000

7,000

8,000

2016 2017E 2018E 2019E 2020E

OMV Petrom

Previous Current

Energy, Romania 8 WOOD & Company

Sector discussion

Oil price update

At the end of a year when oil prices had recovered from their early lows, the announcement of production

cuts made by OPEC on 30 November appears to have stabilised oil prices. Brent crude averaged

USD 54.9/bbl in December 2016, USD 55.5/bbl in January 2017 and USD 56.6/bbl in February 2017.

Compared to the recent past, this is an unprecedented low level of volatility.

The key drivers of oil prices in 2017, in our view, are the OPEC cuts, drawdowns of global inventories,

and the recovery of US tight oil production, as well as the usual supply shocks.

OPEC oil production

In December 2016, OPEC was producing 33.14 million barrels per day (m bpd), which fell to 32.3m bpd

in January 2017. This cut has successfully stabilised the global oil price at around USD 55/barrel. The

plan is to cut production by 1.8m bpd for six months, but this may be extended for a longer period if

necessary, according to OPEC. On their own, the cuts will not be enough to completely balance the

market, but should significantly reduce excess stocks, in our view.

OPEC oil production

Source Bloomberg

There are a number of OPEC wildcards that may have a significant impact on crude production volumes.

The most important of these is Libya, which has potential output of 1.5m bpd, but was only producing

380,000 per day on average in 2016. In January 2017, this rose to 670,000 bpd, and we expect this to

increase further. Meanwhile, Iraqi production grew by 400,000 bpd in 2016 and, given the improving

security situation, could continue to grow over 2017E.

The tight oil reaction

The oil price of above USD 50/barrel has already triggered a greater level of activity in the US oil patch

in 4Q16 and so far this year. The rig count reached a nadir of just 323 active rigs in May 2016, which

rebounded to 502 by the end of the year, and 534 in January 2017.

Meanwhile, since reaching its lowest level of 8.48m bpd in July 2016, US crude oil production has

increased by nearly 500,000 bpd as of February 2017. This is still 650,000 bpd below the 2015 peak,

which in itself understates the maximum short-term potential, in our view, given the improvements in

pipeline infrastructure that have been made since that date.

25

26

27

28

29

30

31

32

33

34

35

Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec

Mil

lio

n B

arr

els

pe

r D

ay

Min / Max Average 2015 2016 2017

Energy, Romania 9 WOOD & Company

US rig count and production

Source: EIA, Baker Hughes, WOOD Research

Crude inventories

During 2016, the oil market was in contango, with 12-month futures prices approximately USD 4.5/barrel

higher than spot prices for the first 11 months of the year. This situation means that oil can be stored at

a profit, with no price risk. This drives inventory levels up. Following the announcement of the OPEC

production cut, spot prices rose, but forward prices did not. The price differential between today and in

12 months’ time fell to USD 1.8 in December and just USD 0.73 for January 2017. We believe that the

disappearance of the contango means that inventories should be released to the market as their related

contracts finish. Therefore, in our view, the primary trend in the oil markets in 2017E should be a

drawdown of inventories, rather than significant changes in price.

Brent crude forward curves

Source: Bloomberg, WOOD Research

0

200

400

600

800

1,000

1,200

1,400

1,600

1,800

Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec

US oil rig count

Max/Min Average 2015

2016 2017

4.0

5.0

6.0

7.0

8.0

9.0

10.0

Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov DecMill

ion

Ba

rre

ls p

er

Da

y

US crude production

Min / Max (2010-2014) 2015

2016 Average

2017

30.00

35.00

40.00

45.00

50.00

55.00

60.00

Jan2016

Feb2016

Mar2016

Apr2016

May2016

Jun2016

Jul 2016 Aug2016

Sep2016

Oct2016

Nov2016

Dec2016

Jan2017

1 Month 6 Months 12 Months

Energy, Romania 10 WOOD & Company

European natural gas markets

Given the global glut of natural gas, and the lack of bullish catalysts for oil prices, we expect gas prices

to remain moderate in Europe in the medium term.

The German market is the largest and most liquid, so we use it to illustrate the general European price

trends. The Romanian spot price does not currently follow its German counterpart given that gas can

only flow in one direction.

German natural gas spot prices (EUR/MWh)

Source: Bloomberg, Wood Research

Despite talk over recent years by many industry spokespeople of a decoupling of gas prices from oil

prices and alterations to some supply contracts when oil prices were high, the lagged correlation between

the two still appears to be in place. The graph below compares the current spot price for gas to the

average Brent price for the previous six months, and illustrates nicely, we believe, that the oil price gas

price linkage is still in place.

Crude oil/natural gas price relationship

Source: Bloomberg, WOOD Research

Romanian natural gas business

Although Romania has a connection to pipelines bringing gas from Russia, it remains a gas island, with

the majority of the gas consumed produced locally, and no exports. The market is also heavily regulated,

which is unavoidable given Petrom and Romgaz’s dominance, and the lack of connectivity with

other markets.

With mature fields, gas production volumes have been falling gradually for many years. Improvements

in technology are slowing the declines, but current prices have led to reduced budgets and a reversal of

this trend.

Significant potential exists offshore, but will not be producing this decade because both companies have

a lot of preparation before the final investment decisions (FIDs) can be reached.

0.0

5.0

10.0

15.0

20.0

25.0

30.0

35.0

Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec

Min / Max (2010-2014) Average 2015 2016 2017

0.0

5.0

10.0

15.0

20.0

25.0

30.0

0.0 10.0 20.0 30.0 40.0 50.0 60.0 70.0 80.0

Gas price/trailing 6M oil price

Energy, Romania 11 WOOD & Company

Natural gas infrastructure

The natural gas transmission system is operated by Transgaz. It was built largely as a closed system,

for delivering domestically-produced gas to domestic customers. The pressure in the lines is lower than

in neighbouring countries, which makes exporting technically impossible. Imports, however, are possible

and happen when prices or volumes necessitate them. It is a priority for the European Union to see

energy markets integrated, to reduce the risks to energy supplies, and it has pressured the Romanian

government to speed up investments to integrate its markets.

Transgaz is constructing a gas corridor between Bulgaria and Hungary, which is expected to be

completed in 2019E. With this in place, Romanian gas producers would be able to export gas and

consumers would have a greater choice of suppliers. Further enhancements in this pipeline would also

enable bigger volumes to be exported from Black Sea projects if necessary. The European Union has

contributed EUR 179m to the project already, which it views as an enhancement for energy security and

vital for the integration of gas markets in the region.

Romanian natural gas consumption and production (mcm)

Source: WOOD Research, BP

Regulation

As of 1 July 2007, the Romanian gas market became fully open for all consumers, allowing them to freely

choose a gas supplier from the ones licensed by ANRE, and directly negotiate the gas supply clauses

and prices (law no.123/2012 sets the legal framework to converge the domestic gas price with the import

gas price; while government decision no.22/2013 provides for a calendar of domestic gas price increases

with respect to the regulated market).

In June 2016, the Romanian government decided to suspend the price increase for domestic consumers

for nine months. Prices were to have risen from RON 60 to RON 66 as of the beginning of July 2016,

but the government decided against it at the last minute.

The regulator is trying to make it a true market, with gas traded on centralised platforms, while a really

competitive market would be created by connecting Romania to other regional markets. The wholesale

markets for gas were deregulated at the beginning of 2015, and domestic gas prices are going through

the process of deregulation. Current low gas prices make this process politically smoother, but there are

always political risks associated with such moves.

Currently, the regulator is attempting to increase the volumes of gas sold through the trading exchange.

The combination of deregulation and interconnection offers opportunities for the two main players, but

comes with risks attached, especially in light of the current global gas glut.

European refining sector

The European refining sector continues to benefit from a mixture of low oil prices, recovering regional

demand and a slowdown in capacity additions.

As a method of monitoring the market conditions, we have created our own benchmark, which we

calculate from daily product prices. It is based on a mixture of heavy Middle Eastern crude oils, a 50%

diesel yield, 25% gasoline and 25% fuel oil. This margin was very strong in 4Q16, and has continued to

be so in 1Q17 qtd.

10

11

12

13

14

15

16

17

18

19

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014

Production Consumption

Energy, Romania 12 WOOD & Company

WOOD’s Mediterranean benchmark margin

Source: Bloomberg, WOOD Research

Romanian refining sector

There are three refineries operating currently in Romania: Petrom’s Petrobrazi Refinery, LUKOIL’s

Ploiești Refinery and Rompetrol’s Petromidia plant. All are relatively small but high complexity plants.

They process predominantly Russian and domestically produced crude oil. Previously, Romania had a

number of other refineries, which have all been closed or are used for the production of niche products.

Capacity and complexity of Romanian refineries

Source: WOOD Research

The Romanian market is also supplied with products from Bulgaria, Hungary, Belarus and elsewhere.

Romanian petrol retail sector

Car numbers

The Romanian car parc is one of the fastest growing in the region. In the five years to 2015, the number

of cars in Romania grew by an average 3.9% per year to reach more than 5m. In addition to new car

sales, large numbers of second-hand cars are imported from other EU countries, which lowers the cost

of increasing motor vehicle penetration and therefore speeds the process up.

0.0

2.0

4.0

6.0

8.0

10.0

12.0

14.0

16.0

Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec

Med 2,1,1 margin

Min / Max Average 2015 2016 2017

Petrom

Lukoil

Rompetrol

0.0

1.0

2.0

3.0

4.0

5.0

6.0

9.6 9.8 10.0 10.2 10.4 10.6 10.8 11.0 11.2 11.4 11.6 11.8

Ca

pa

city, m

illio

n to

nn

es

Nelson Complexity

Energy, Romania 13 WOOD & Company

Number of cars in Romania (millions)

Source: ACEA, WOOD Research

Romanian refined product demand, monthly (m tonnes)

Source: Bloomberg, WOOD Research

The main players in the Romanian market are: Petrom/OMV, MOL, Rompetrol, LUKOIL, as well as some

other small players.

4.24.3 4.3

4.5

4.7

4.9

5.15

4.0

4.2

4.4

4.6

4.8

5.0

5.2

5.4

2009 2010 2011 2012 2013 2014 2015

Mill

ion

s

0.40

0.50

0.60

0.70

0.80

0.90

1.00

1.10

Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec

Mil

lio

n t

on

ne

s

Min / Max 2016 2015 Average

Energy, Romania 14 WOOD & Company

Romania’s potential for reclassification to Emerging Markets

Investors’ attention has started to focus on the potential chances of Romania being reclassified to the

Emerging Markets group. In our view, the chances for such a development have increased along with

OMV Petrom’s free float being boosted by the MSCI in December 2016 (as announced along with the

SAIR in November 2016) from 9% to 20%. As a general rule, the MSCI requires a stock market to have

three companies meeting (simultaneously) the criteria below (in use for the November 2016 SAIR;

updated on a semi-annual basis) to put it on the “watch list” for potential reclassification from frontier to

the emerging markets group:

a) A minimum of three companies with full market capitalisation of a minimum of USD 1,269m;

b) A minimum of three companies with free float adjusted market capitalisation at a minimum of

USD 635m; and

c) A minimum of three companies with both 3M and 12M ATVRs at a minimum of 15%.

According to our calculations, out of the five members of the MSCI Romania index, three stocks met

these requirements as of the end of January 2017. In our view, this means that Romania’s stock market

fulfils (in theory) the very basic size and liquidity criteria set by the MSCI for a market to be put on

its watchlist.

MSCI Romania index members (closing prices as of 1 March 2017; ATVRs calculated as of 28 February 2017)*

Weights in MSCI RO Index MCap (USDm) MSCI FF FF-Mcap (USDm) 3M ATVR 12M ATVR

Banca Transilvania SA 38.9% 2,346 0.70 1,642 24% 25%

ROMGAZ SA 18.1% 2,547 0.30 764 18% 22%

Electrica SA 12.2% 1,145 0.45 515 11% 12%

BRD-Groupe Societe Generale SA 11.5% 1,943 0.25 486 22% 17%

OMV Petrom SA 19.2% 4,054 0.20 811 23% 17%

Source: WOOD Research, Bloomberg, MSCI; *shaded areas denote that the mentioned figures meet the MSCI’s minimum requirements

However, we also note that the MSCI also requires these criteria to be met with a “comfortable” margin.

Moreover, the index provider always has certain discretion over its final decisions on reclassification, so

fulfilling the criteria does not automatically guarantee inclusion. Given that, from our point of view, it

seems that the 2ppts margin with which OMV Petrom meets the 12M ATVR requirement is unlikely to

be deemed “comfortable”, we stress that Romania fulfils the requirements only “in theory”. However, if

the liquidity of the stock continues to improve, and the margin widens, the probability of placing Romania

on the list improves as well, in our view. Therefore, we stress that it is definitely worth monitoring the

situation on Romania’s stock market, as its chances of joining the Emerging Markets group are

increasing, in our view.

Energy, Romania 15 WOOD & Company

Company sections

Energy, Romania 16 WOOD & Company

This page has been left intentionally blank

Energy, Romania 03 March 2017

Romgaz Buy

Maintained

Price: RON 28.5 Price target: RON 36.6

(From RON 36.4)

Not just a pipe dream

We maintain our BUY recommendation on Romgaz, with an updated 12-

month price target (PT) of RON 36.6, offering upside of 28%. Romgaz had

a terrible 2016, driven by competition from imports: a function of the very

low natural gas prices in Europe. The company had to cut production and

prices in response to the intense level of competition. We see 2017E as

a potentially better year, due to a recovery in natural gas prices. We also

see Romgaz as well-placed to benefit from changes in the Romanian gas

market, driven by pipeline connections to the European markets and

price deregulation. Romgaz has spare capacity and is sitting on a major

new discovery, both of which are awaiting suitable customers. With the

completion of the pipeline connection due in 2019E, Romgaz should add

a substantial export business to its current domestic one, in our view.

Higher prices. Better prices for gas would boost the company’s results in

2017E and beyond. The recovery in gas prices should be beneficial as

importers are deterred from the market. As the biggest loser last year in terms

of sales, we see Romgaz as potentially the biggest winner in 2017E.

MSCI potential. In our view, the chances of Romania gaining reclassification

to the Emerging Markets group has increased with Petrom’s better free float

following the deals in 2016, and the potential transactions to come in 2017E.

As one of the Romanian market’s biggest companies, Romgaz stands to

benefit from any upgrade, in our view.

Dividends. Romgaz is one of the best dividend payers among its peers and

we see its ability to pay dividends increasing with rising gas prices and

potential improvements in its sales volumes. New rules demand a 90% payout

from state-owned companies for this year. We forecast lower payouts in the

following years, but 90% may be also imposed in the future.

Deregulation. Although we are aware that the timelines for deregulation have

not been set in stone, the biggest participant in the regulated market should,

by definition, be the biggest beneficiary once the rules are changed.

Exports. From 2019E-onwards, we see Romgaz becoming an exporter of

natural gas, making use of its spare capacity and newly-discovered resources.

This would enable revenues to grow by 33% between 2018-20E, on

our estimates.

Big new resource. Romgaz discovered a large new gas resource last year,

beneath its existing operations. The contingent resource is estimated at

150-170m boe. We believe this can be fast-tracked at a relatively low cost, and

exported.

Reserves replacement. Romgaz has a better reserves replacement track

record than its competitor OMV Petrom, with an 85% RRR over the past three

years. This should also improve once the new discovery can be classified as

reserves, following an investment decision.

Expected events

1Q17 results 12 May

2Q17 results 11 August

Key data

Market Cap USD 2,540m

Free float 30%

Shares outstanding 385.0m

Major shareholder Government 70%

Reuters code ROSNG.BX

Bloomberg code SNG.RO

Price performance

52-w range RON 19.28-28.90

52-w performance 21%

Relative performance -3.5%

Romgaz 12M share price performance

18.0

22.0

26.0

30.0

34.0

Ma

r-16

Apr-

16

Ma

y-1

6

Ju

n-1

6

Ju

l-1

6

Aug

-16

Sep

-16

Oct-

16

Nov-1

6

Dec-1

6

Ja

n-1

7

Fe

b-1

7

SNG RO Equity BETI Index

EQUITY

RESEARCH Analysts: Jonathan Lamb, Lucian Albulescu, Ondrej Slama London: +44 20 3530 0621

E-mail: [email protected], [email protected] Website: www.wood.com

Sales EBITDA EBIT Net income EPS P/E P/CF P/BV EV/EBITDA ROCE DPS Div yield

RONm RONm RONm RONm RON x x x x % RON %

2014 4,493 2,541 1,764 1,410 3.66 9.37 5.53 1.36 3.16 18% 3.15 9.2%

2015 4,053 2,242 1,449 1,194 3.10 8.45 4.91 1.07 3.57 16% 3.025 11.3%

2016 3,412 1,573 1,262 1,025 2.66 10.65 5.47 1.13 4.91 14% 2.961 10.5%

2017E 4,079 1,947 1,521 1,268 3.29 8.60 5.20 1.11 4.07 17% 2.796 9.9%

2018E 4,202 2,021 1,566 1,253 3.25 8.71 4.96 1.09 4.19 15% 2.600 9.2%

2019E 4,853 2,412 1,938 1,550 4.02 7.04 4.84 1.04 3.61 17% 3.017 10.7%

Romgaz 18 WOOD & Company

Company snapshot – BUY, PT RON 36.6

RomgazBUY SHARE PRICE PERFORMANCE COMPANY DESCRIPTION

Bloomberg ticker SNG RO

Closing price (RON) 28.5

Price target (RON) 36.6

Upside to PT 28.3%

Shares outstanding (m) 385.0

MCAP (USD m) 2,582

Free float 30.0%

ADTV (USD m) 0.8

52 Week Range (RON) 19.28-28.90

RATIOS

PER SHARE RATIOS 2014 2015 2016 2017E 2018E 2019E FINANCIAL RATIOS 2014 2015 2016 2017E 2018E 2019E

EPS 3.66 3.10 2.66 3.29 3.25 4.02 Working capital to sales, days 80 92 85 62 55 55

CEPS 19.78 19.38 18.40 19.26 21.14 23.17 Capex/depreciation 0.9x 1.5x 1.0x 1.0x 0.9x 0.8x

BVPS 25.20 25.15 25.11 25.44 25.89 27.31 Capex/net fixed assets 0.29x (0.07)x 0.20x 0.10x 0.09x 0.12x

DPS 3.15 3.03 2.96 2.80 2.60 3.02 Op. cash flow/capex 1.3x (5.5)x 1.4x 2.6x 2.6x 2.1x

EBITDA margin 56.5% 55.3% 46.1% 47.7% 48.1% 49.7%

VALUATION RATIOS 2014 2015 2016 2017E 2018E 2019E EBIT margin 61.4% 61.0% 60.2% 70.4% 69.4% 71.8%

P/E 9.4x 8.4x 10.6x 8.6x 8.7x 7.0x Pre-tax margin 39.8% 36.2% 37.5% 37.3% 37.3% 39.9%

P/CF 5.5x 4.9x 5.5x 5.2x 5.0x 4.8x Net margin 31.4% 29.5% 30.0% 31.1% 29.8% 31.9%

P/BV 1.4x 1.1x 1.1x 1.1x 1.1x 1.0x ROE 14.5% 12.3% 10.6% 12.9% 12.6% 14.7%

EV/EBITDA 3.2x 3.6x 4.9x 4.1x 4.2x 3.6x ROCE (avg) 18.5% 16.0% 14.4% 17.1% 15.4% 17.4%

EV/CE 1.1x 1.1x 1.1x 1.1x 1.0x 1.0x

EV/Sales 1.8x 2.0x 2.3x 1.9x 2.0x 1.8x

EV/EBIT 2.9x 3.2x 3.8x 2.8x 2.9x 2.5x

FCF, RON m 569 2,902 438 1,082 1,031 1,016

FCF yield 5.2% 26.6% 4.0% 9.9% 9.5% 9.3%

Dividend yield 9.2% 11.3% 10.5% 9.9% 9.2% 10.7%

COMPANY FINANCIALS

INCOME STATEMENT, RON m 2014 2015 2016 2017E 2018E 2019E BALANCE SHEET, RON m 2014 2015 2016 2017E 2018E 2019E

Net Sales 4,493 4,053 3,412 4,079 4,202 4,853 Cash & cash equivalents 1,954 740 281 76 30 43

Operating Expenses -1,231 -1,384 -997 -1,003 -1,080 -1,111 Accounts receivable 1,000 601 829 757 700 809

EBITDA 2,541 2,242 1,573 1,947 2,021 2,412 Inventories 392 560 576 407 525 607

DD&A -777 -794 -456 -426 -455 -474 Other CA 1,018 2,286 3,034 3,034 2,534 2,284

EBIT 1,764 1,449 1,262 1,521 1,566 1,938 Total current assets 4,364 4,188 4,719 4,274 3,789 3,743

Other Expenses -1,035 -1,041 -882 -1,252 -1,249 -1,445 PP&E 5,963 5,996 5,787 6,365 7,035 7,720

Pre-tax profit 1,788 1,469 1,280 1,521 1,566 1,938 Other LT assets 485 501 470 470 470 470

Net profit 1,410 1,194 1,025 1,268 1,253 1,550 Total fixed assets 6,448 6,497 6,257 6,835 7,505 8,189

Total assets 10,812 10,685 10,976 11,109 11,293 11,932

Accounts payable 217 187 569 575 584 674

CASH FLOW, RON m 2014 2015 2016 2017E 2018E 2019E Other ST liabilities 452 439 377 377 377 377

Total current liabilities 669 626 946 952 961 1,051

CF from Operations 2,327 2,454 1,595 1,747 1,656 1,925

Thereof depreciation 485 582 354 426 455 474 Asset retirement obligations 202 201 194 194 194 194

Thereof changes in w/c -511 -382 -473 -200 -365 -487 Pension obligation 97 103 120 120 120 120

CF from Investments -1,758 448 -1,157 -665 -625 -909 Other 131 63 40 40 40 40

Dividends -988 -1,215 -1,041 -1,141 -1,078 -1,002 Total LT liabilities 431 366 354 354 354 354

Change in Net debt -419 1,687 -603 -59 -47 14 Minority interest - - - - - -

Total shareholders' equity 9,712 9,692 9,676 9,803 9,978 10,526

Total liab. & equity 10,812 10,685 10,976 11,109 11,293 11,932

OPERATIONS 2014 2015 2016 2017E 2018E 2019E

Net Working Capital 2,194 3,260 3,870 3,623 3,176 3,025

Production, mmcm 5,664 5,563 4,218 5,100 5,000 5,500

Production, boepd 97,000 95,000 72,000 87,000 85,000 94,000 MACRO ASSUMPTIONS 2014 2015 2016 2017E 2018E 2019E

Growth, % 0% -2% -24% 21% -2% 10% Brent crude, USD/bbl 99.0 52.5 43.6 53.8 55.0 60.0

German hub price, EUR/MWh 22.2 20.7 14.8 18.9 19.2 19.8

Regulated gas price, RON/mcm 51 58 60 60 65 70 RON/USD 3.35 4.01 4.00 4.00 4.04 4.08

Market gas price, RON/mcm 99 92 67 85 87 91

PROFITABILITY TRENDS

Per barrel economics (USD/bbl)

Revenues, USD/boe 37.7 31.5 27.2 30.6 31.9 33.2

EBITDA, USD/boe 21.4 16.1 15.0 15.3 16.1 17.2

Opex. USD/boe -10.4 -10.0 -9.5 -7.9 -8.6 -7.9

Romgaz is the largest domestic natural gas exploration and production (E&P) company in Romania,

producing c.50% of the Romanian output (4.2bcm in 2016 ). Romgaz had 62bcm of proved (1P) and 75bcm of

proved and probable (2P) reserves as of end-2015. Romgaz has 147 commercial reservoirs in Transylvania its

largest producing basin, with 90%+ of production, Moldavia and Muntenia, mostly in mature fields, which it

has been producing for 30+ years, in most cases. Romgaz also has successful exploration activities, with a

c.65% drilling success rate and a very major find in 2016. The company has non-operated stakes in some

Black Sea offshore fields, exploration interests in Slovakia and Poland, and some JVs for the production

enhancement of depleted fields. Romgaz owns and operates six underground gas storage (UGS) facilities,

with a total capacity of 2.76bcm. Storage is a fully regulated. 18.0

22.0

26.0

30.0

34.0

Ma

r-16

Apr-

16

May-1

6

Jun-1

6

Jul-16

Aug

-16

Sep

-16

Oct-

16

Nov-1

6

De

c-1

6

Ja

n-1

7

Fe

b-1

7

SNG RO Equity BET Index

3.23.0

3.0

2.8

2.63.0

0

0.5

1

1.5

2

2.5

3

3.5

0

1

1

2

2

3

3

4

4

5

2014 2015 2016 2017E 2018E 2019E

EPS DPS

37.72

31.55

27.17

30.6031.88

33.19

21.44

16.14 14.95 15.33 16.13 17.22

0

5

10

15

20

25

30

35

40

2014 2015 2016 2017E 2018E 2019E

Revenue / Bbl Ebitda / Bbl

Romgaz 19 WOOD & Company

Investment case

We see Romgaz as a major potential beneficiary from the recovery in European gas prices from

the extremely low levels seen in 2016. We believe that, in the longer term, Romgaz should be the

biggest beneficiary of interconnection between the Romanian and other European gas markets.

Given that it is purely a gas company, Romgaz was the biggest loser in volume terms from the

extremely low price environment that we saw in 2016. It also has a bigger share of the regulated

domestic market than OMV Petrom. Conversely, we would expect it to be the biggest beneficiary

of a purely market price-based environment, which we expect to see in 2019E. Access to a bigger

market should also enable it to utilise its spare capacity and to develop its new gas discovery, in

our view. We also see few other companies with the same dividend yield as Romgaz in

our universe.

European gas prices. So far in 2017, the European spot gas price has averaged EUR 21.2/MWh vs.

EUR 14.2/MWh in 2016. Although we do not see this affecting Romanian prices to the same degree, we

believe that it should stem the flow of cheap imports, which was such a problem in 2016. For 2017E, we

believe that Romgaz should obtain better prices and be able to produce higher volumes on the back of

this price trend.

Reserve replacement. Compared to its competitor OMV Petrom, Romgaz has a better track record of

reserve replacement, which has been at 85% in the past three years. When the major discovery from

2016 is added in, this should improve to over 100%, in our view.

Dividends. Traditionally, Romgaz has paid out around 70% of its earnings, which already put it on an

attractive dividend yield. New state-imposed rules this year are forcing a 90% payout ratio, and we see

dividend yields of 9.2% and 8.1% for 2017E and 2018E, respectively.

Romgaz: expected DPS, RON

Source: Wood Research

Deregulation. The liberalisation of the prices for the domestic consumption and district heating

segments has been delayed from 2016, but will eventually have to be implemented over the coming

years, in our view. Romgaz should benefit disproportionately from this because a great percentage of its

sales comes from this segment.

Export infrastructure. The construction of a natural gas pipeline link between Romania and Hungary

should benefit Romgaz the most, in our view, thanks to its significant spare capacity, as well as its newly

discovered resources, which we believe can be fast-tracked into production, if demand necessitates it.

Given the oversupply in the Romanian market, we see the export pipeline as the only way of unlocking

this potential.

Spare capacity. Romgaz already has significant spare capacity, which management estimates to be at

least equivalent to 25% of current production. The only thing missing is customer demand. The ability to

export should unlock this, and we see this as a significant driver of earnings in 2019E and beyond.

Big new resource. In 2016, Romgaz discovered a large new hydrocarbon resource, beneath its existing

operations. The contingent resource is estimated at 150-170m boe. We believe this could be fast-tracked

at a relatively low cost, depending on access to new customers. Moreover, as the first major deep-level

find onshore, there is a possibility that there may be more such discoveries to come.

2.732.58

2.28

2.65

3.01

3.39

0.00

0.50

1.00

1.50

2.00

2.50

3.00

3.50

4.00

2016E 2017E 2018E 2019E 2020E 2021E

Romgaz 20 WOOD & Company

Valuation

DCF

Our valuation for Romgaz is derived using a 10-year DCF, with -5% terminal growth. We calculate a 12-

month price target (PT) of RON 36.6, offering upside of 28%.

Romgaz: 10-year DCF

RON m 2017E 2018E 2019E 2020E 2021E 2022E 2023E 2024E 2025E 2026E

EBITDA 1,947 2,021 2,412 2,851 3,165 3,146 3,127 3,107 3,068 3,011

Taxes 254 244 253 264 258 241 217 194 173 173

Capex 1,004 1,125 1,159 1,194 1,229 1,266 1,304 1,343 1,384 1,425

Change in WC 13 39 -100 -112 -75 0 0 1 5 0

FCF 676 613 1,100 1,505 1,753 1,638 1,606 1,570 1,507 1,413

PV of FCF 620 515 848 1,064 1,137 974 875 785 691 594

Source: WOOD Research

Romgaz: DCF summary and WACC calculation

SUM of PV 7,509 Risk free rate 4.5%

PV of TV 2,129 ERP 4.5%

Levered beta 1.10

Total EV 9,639 Cost of equity 9.5%

Net debt 3,173 Tax rate 16.0%

Equity value 12,812 After-tax cost of debt 5.5%

Per share (RON) 33.3 % of debt 10.0%

% of equity 90.0%

12M PT (RON) 36.6 WACC 9.1%

Source: WOOD Research

Ratios

At current prices, Romgaz trades at P/E ratios of 8.6x for 2017E and 8.7x for 2018E, on our estimates,

vs. 10.1x and 9.2x for its European peer group, on both WOOD and consensus estimates. On

EV/EBITDA, the company’s ratios are 4.1x for 2017E and 4.2x for 2018E, on our estimates, compared

with 4.6x and 4.2x for its peer group. On these metrics, Romgaz looks slightly undervalued, in our view.

We see the company becoming cheaper as its sales volumes increase from 2019E-onwards.

Romgaz: valuation ratios

2014 2015 2016E 2017E 2018E 2019E 2020E

P/E 9.37 8.45 10.65 8.60 8.71 7.04 5.78

P/CF 5.53 4.91 5.47 5.20 4.96 4.84 4.64

P/BV 1.36 1.07 1.13 1.11 1.09 1.04 0.97

EV/EBITDA 3.16 3.57 4.91 4.07 4.19 3.61 3.09

EV/CE 1.05 1.07 1.09 1.07 1.04 0.98 0.90

EV/sales 1.79 1.98 2.26 1.94 2.02 1.79 1.58

EV/EBIT 2.91 3.24 3.76 2.76 2.91 2.50 2.13

FCF, RONm 569 2,902 438 1,082 1,031 1,016 1,124

FCF yield 5.2% 26.6% 4.0% 9.9% 9.5% 9.3% 10.3%

Dividend yield 9.2% 11.3% 10.5% 9.9% 9.2% 10.7% 12.1%

Source: WOOD Research

WOOD vs. the consensus

We are slightly below the consensus on EBITDA for both 2017E and 2018E, but above the consensus

in 2019E. We believe this is due to the consensus numbers not including the impact of the export

business in 2019E and beyond as of yet.

WOOD vs. the consensus

RON m Revenues EBITDA EBIT Net profit

2017E 2018E 2019E 2017E 2018E 2019E 2017E 2018E 2019E 2017E 2018E 2019E

WOOD Research 4,079 4,202 4,853 1,947 2,021 2,412 1,521 1,566 1,938 1,268 1,253 1,550

Consensus 3,775 3,933 3,866 2,031 2,185 2,325 1,310 1,435 1,434 1,130 1,203 1,309

% difference 8.1% 6.8% 25.5% -4.12% -7.50% 3.72% 16.11% 9.13% 35.11% 12.18% 4.18% 18.40%

Source: Bloomberg, WOOD Research

Romgaz 21 WOOD & Company

Company background

Romgaz is the largest natural gas producer and the main gas supplier in Romania. It has three production

areas: the Transylvanian Basin, which accounts for around 90% of production; the Muntenia Moesian

Platform; and the Moldavia Platform.

Reserves

The company has a mature onshore natural gas reserves base of 62bcm 1P and 75bcm 2P reserves.

Its 25 largest fields contain c.70% of Romgaz’s reserves (the average size of the proved reserves per

average field is 450m m3; with 17 fields with over 1bcm). The recovery factors are between 55% and

85% for most fields, with 90% in the more mature fields.

Reserves replacement ratios

Source: Romgaz, WOOD Research

Ownership structure

Romgaz is a joint stock company whose majority shareholder is the Romanian sate, which owns a 70%

stake. The company is listed on the Bucharest Stock Exchange, and its GDRs are also traded on the

London Stock Exchange. Following Fondul Proprietatea’s disposal of its 5.85% stake in April 2016, 30%

of the shares are now in free float.

Company history

In 1991, the Romanian national gas company was named Romgaz, which became a brand for natural

gas exploration, production and storage in Romania after 2000.

In 2013, Romgaz acquired the lernut electricity power plant, in lieu of the payment of outstanding debts.

In 2016, it made the most significant onshore discovery for years, at Muntenia Nord-Est.

Operations

Exploration and production

Romgaz is the titleholder of petroleum operations for exploration, development and production in nine

blocks in Romania, with 100% participation interest, and is co-titleholder in four blocks, based on

concession contracts. These blocks include 141 commercial fields, and five fields recording experimental

production. It also holds exploration and production rights in Slovakia and Poland.

The Transylvanian Basin accounts for around 90% of Romgaz’s production.

Production was 4.2bcm in 2016, which was a 24% yoy decline.

Development areas

The company has been exploring deeper layers beneath its existing gas fields, which it believes hold a

lot of potential. In June 2016, gas was discovered in the Moesian Platform, within the Caragele structure.

The contingent resources were estimated at 150-170mboe, or between 25-28bcm.

Romgaz has also been exploring two blocks in the Black Sea, in partnership with Lukoil and PanAtlantic

Petroleum: EX29 Est Rapsodia and EX30 Trident. In February 2016, the Rapsodia block was

relinquished, following disappointing results. Exploration activities are continuing in the Trident Block,

57% 49%

92%

155%

323%

70%

94%82%

0%

50%

100%

150%

200%

250%

300%

350%

2008 2009 2010 2011 2012 2013 2014 2015

Romgaz 22 WOOD & Company

where a major gas accumulation was discovered in 2015 (potentially 30bcm of gas). Romgaz’s

participation in these blocks is 10% in each.

Electricity generation

Romgaz owns CTE Iernut, a condensation electric power plant with intermediate superheating and

800MWh of installed power. Its capacity accounts for 5% of the domestic/national market share of

electricity production. However, it requires significant investment to remain competitive.

Gas storage

The underground gas storage business operates six storage units, with total active capacity of

2.77bcm/cycle, equivalent to a market share of over 90% in Romania.

Sales

In 2015, 54.1% of Romgaz’s gas sales were to households and thermal plants for the gas used for

household heating, which are sold at regulated prices. The other 45.9% of sales were to industry.

Around 63% of Romgaz’s gas sales, in terms of volumes, were to E.ON Energie and Engie (formerly

GDF Suez).

Management

The board of directors consists of seven members, three of which are independent.

Romgaz 23 WOOD & Company

Risks

We associate the following risks with Romgaz

As the dominant supplier of gas to the Romanian regulated domestic and district heating

segments, Romgaz has the most to lose from delays in price liberalisation.

As a pure-play natural gas company, a repeat of the very low gas prices of 2016 would suppress

volumes and earnings significantly.

The district heating business, in particular, is susceptible to bad payment problems. These could

lead to write-offs, or the company taking ownership of low-value assets as payment.

With 70% state ownership, management is susceptible to interference.

Romgaz 24 WOOD & Company

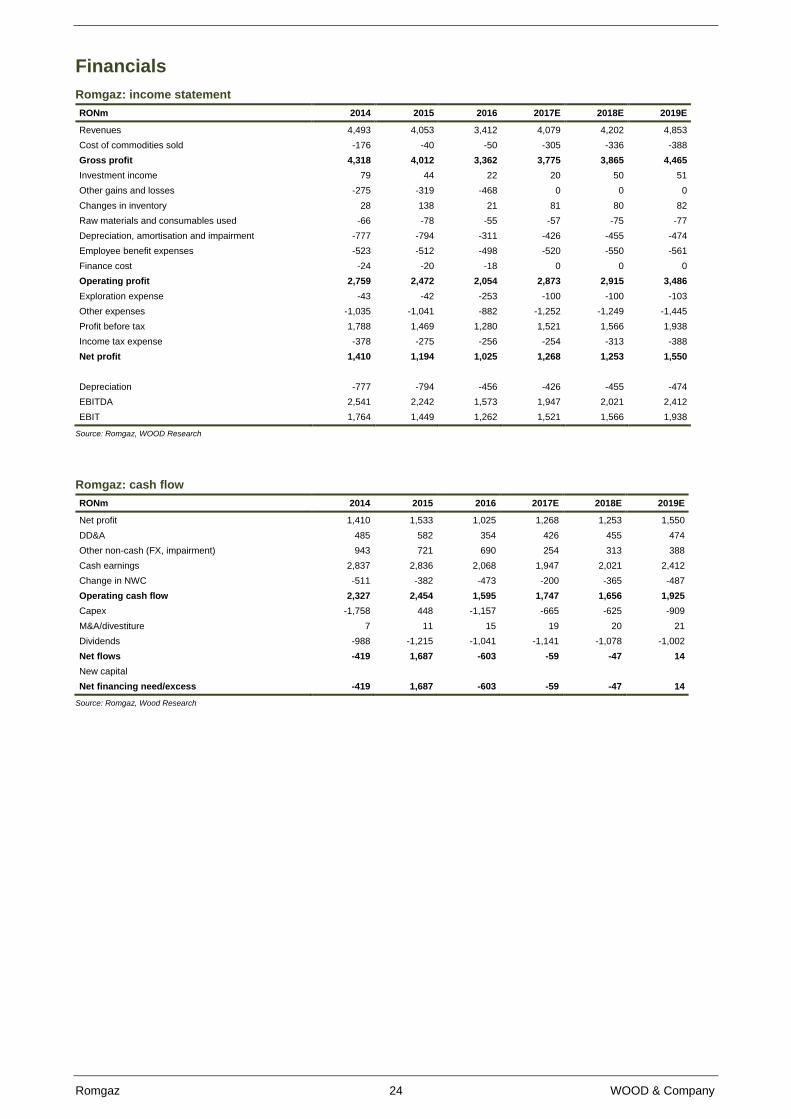

Financials

Romgaz: income statement

RONm 2014 2015 2016 2017E 2018E 2019E

Revenues 4,493 4,053 3,412 4,079 4,202 4,853

Cost of commodities sold -176 -40 -50 -305 -336 -388

Gross profit 4,318 4,012 3,362 3,775 3,865 4,465

Investment income 79 44 22 20 50 51

Other gains and losses -275 -319 -468 0 0 0

Changes in inventory 28 138 21 81 80 82

Raw materials and consumables used -66 -78 -55 -57 -75 -77

Depreciation, amortisation and impairment -777 -794 -311 -426 -455 -474

Employee benefit expenses -523 -512 -498 -520 -550 -561

Finance cost -24 -20 -18 0 0 0

Operating profit 2,759 2,472 2,054 2,873 2,915 3,486

Exploration expense -43 -42 -253 -100 -100 -103

Other expenses -1,035 -1,041 -882 -1,252 -1,249 -1,445

Profit before tax 1,788 1,469 1,280 1,521 1,566 1,938

Income tax expense -378 -275 -256 -254 -313 -388

Net profit 1,410 1,194 1,025 1,268 1,253 1,550

Depreciation -777 -794 -456 -426 -455 -474

EBITDA 2,541 2,242 1,573 1,947 2,021 2,412

EBIT 1,764 1,449 1,262 1,521 1,566 1,938

Source: Romgaz, WOOD Research

Romgaz: cash flow

RONm 2014 2015 2016 2017E 2018E 2019E

Net profit 1,410 1,533 1,025 1,268 1,253 1,550

DD&A 485 582 354 426 455 474

Other non-cash (FX, impairment) 943 721 690 254 313 388

Cash earnings 2,837 2,836 2,068 1,947 2,021 2,412

Change in NWC -511 -382 -473 -200 -365 -487

Operating cash flow 2,327 2,454 1,595 1,747 1,656 1,925

Capex -1,758 448 -1,157 -665 -625 -909

M&A/divestiture 7 11 15 19 20 21

Dividends -988 -1,215 -1,041 -1,141 -1,078 -1,002

Net flows -419 1,687 -603 -59 -47 14

New capital

Net financing need/excess -419 1,687 -603 -59 -47 14

Source: Romgaz, Wood Research

Romgaz 25 WOOD & Company

Romgaz: balance sheet

RONm 2014 2015 2016E 2017E 2018E 2019E

PPE 5,963 5,996 5,787 6,365 7,035 7,720

Intangible assets 407 400 399 399 399 399

Other long-term assets 78 101 71 71 71 71

Fixed assets 6,448 6,497 6,257 6,835 7,505 8,189

Inventories 392 560 576 407 525 607

Receivables 1,000 601 829 757 700 809

Cash & cash equivalents 1,954 740 281 76 30 43

Other short-term financial assets 916 2,147 2,893 2,893 2,393 2,143

Other short-term assets 102 140 141 141 141 141

Current assets 4,364 4,188 4,719 4,274 3,789 3,743

Total assets 10,812 10,685 10,976 11,109 11,293 11,932

Share capital 385 385 385 385 385 385

Reserves 2,142 2,582 3,020 3,020 3,020 3,020

Retained earnings 7,184 6,725 6,271 6,398 6,573 7,121

Equity 9,712 9,692 9,676 9,803 9,978 10,526

Decommissioning provisions 202 201 194 194 194 194

Pension liabilities 97 103 120 120 120 120

Total non-current liabilities 431 366 354 354 354 354

Trade and other payables 217 187 569 575 584 674

Short-term debt 0 0 0 0 0 0

Other short-term liabilities 452 439 377 377 377 377

Total current liabilities 669 626 946 952 961 1,051

Total liabilities and equity 10,812 10,685 10,976 11,109 11,293 11,932

Net debt -1,751 -539 -87 127 168 128

Working capital 2,194 3,260 3,870 3,623 3,176 3,025

Net capital employed 7,623 7,471 7,093 7,425 8,067 8,760

Source: Romgaz, WOOD Research

Romgaz 26 WOOD & Company

This page has been left intentionally blank

Energy, Romania 03 March 2017

OMV Petrom Buy

Maintained

Price: RON 0.307 Price target: RON 0.361

(From RON 0.302)

Patience is a virtue

We maintain our BUY recommendation on OMV Petrom (Petrom), with an

updated 12-month price target (PT) of RON 0.361, offering upside of 18%.

We see Petrom as a disciplined, low-cost producer, with a balanced

business model. It has a small, but profitable, downstream business,

which mitigates the downside risk; and also dominates its own retail

market. Important catalysts include government decisions on the fiscal

regime, and further news on the Neptun Deep offshore project. However,

we see few major catalysts in the short term, with the final investment

decision (FID) for the Neptun project not expected until 2018E. Prior to

the secondary offering in 2016, we believed that liquidity was a major

impediment to performance. Following that offering, however, the share

price has risen 36%. Despite this, we believe the company is still

undervalued, given the low multiples and improving macro outlook.

Reserves replacement a worry. Petrom has done a very good job of

maintaining production, but has lagged in reserve replacement (RR) in recent

years. Currently, only the Neptun project offers RR upside.

Higher prices. Better prices for oil and gas should boost the company’s results

in 2017E and beyond. The recovery in gas prices, in particular, should to be

beneficial as importers are deterred from the market.

Liquidity. Since October, when the offering occurred, daily trading volume in

the stock has been about five times higher than before. We believe this has

led directly to a rerating of the stock. The existence of a GDR, though

accounting for less than 1% of trades currently, should make it easier to attract

new investors to the company.

MSCI potential. In our view, the chances of Romania gaining reclassification

to the Emerging Markets group has increased along with OMV Petrom’s free

float being boosted by the MSCI in December 2016, from 9% to 20%.

Dividends. The return of the dividend, and at a level above that which we (and

our peers) had expected, is a welcome development. Given the strength of the

balance sheet, we see further opportunities for increased payouts.

Lower costs. Operating costs/bbl have been trending down, as cost control

became a major priority, due to lower prices. This improves leverage to rising

prices, and strengthens cash flow.

Resilient downstream. As the period of low oil prices has shown, Petrom’s

downstream segment provides a hedge against upstream problems. The

refinery is complex, with incremental upgrade potential and its retail business

is the market leader.

Neptun Deep. This is be an investment that could transform the company’s

prospects, but its realisation is still years in the future.

Expected events

1Q17 results 11 May 2017

2Q17 results 10 August 2017

Key data

Market cap USD 3,374m

Free float 28.3%

Shares outstanding 56,644m

Major shareholder OMV 51%

Reuters code SNPP.BX

Bloomberg code SNP.RO

Price performance

52-w range 0.22-0.31

52-w performance 29%

Relative performance 2%

OMV Petrom 12M share price

performance

0.20

0.22

0.24

0.26

0.28

0.30

0.32

Ma

r-16

Ma

r-16

Apr-

16

Ma

y-1

6

Ju

n-1

6

Ju

l-1

6

Aug

-16

Sep

-16

Oct-

16

Nov-1

6

Dec-1

6

Ja

n-1

7

Fe

b-1

7

SNP RO Equity BET Index rebased

EQUITY

RESEARCH Analysts: Jonathan Lamb, Lucian Albulescu, Ondrej Slama London: +44 20 3530 0621

E-mail: [email protected], [email protected] Website: www.wood.com

Sales EBITDA EBIT Net income EPS P/E P/CF P/BV EV/EBITDA ROCE DPS Div yield

RON m RON m RON m RON m RON x x x x % RON %

2014 21,541 8,144 3,338 2,100 0.04 8.12 2.50 0.63 3.17 6% 0.01 3.7%

2015 18,145 6,231 -530 -690 -0.01 -24.72 3.23 0.66 4.20 -2% 0.000 0.0%

2016 16,247 4,932 1,469 1,038 0.02 16.43 3.83 0.64 5.02 3% 0.015 5.0%

2017E 18,436 5,844 2,484 2,086 0.04 8.17 3.12 0.61 4.06 6% 0.017 5.6%

2018E 18,342 6,040 2,675 2,235 0.04 7.63 3.00 0.58 3.87 6% 0.018 6.0%

2019E 19,193 6,366 2,996 2,516 0.04 6.78 2.85 0.56 3.64 7% 0.020 6.8%

OMV Petrom 28 WOOD & Company

Company snapshot – BUY, PT RON 0.361

OMV PetromBUY SHARE PRICE PERFORMANCE COMPANY DESCRIPTION

Bloomberg ticker SNP RO

Closing price (RON) 0.307

Price target (RON) 0.361

Upside to PT 17.6%

Shares outstanding (m) 56,644

MCAP (USD m) 3,374

Free float 28.3%

ADTV (USD m) 0.9

52 Week Range (RON) 0.22-0.31

RATIOS

PER SHARE RATIOS 2014 2015 2016 2017E 2018E 2019E FINANCIAL RATIOS 2014 2015 2016 2017E 2018E 2019E

EPS 0.037 (0.012) 0.018 0.037 0.039 0.044 Working capital to sales, days 13.7x 23.1x 28.2x 22.3x 21.1x 20.7x

CEPS 0.671 0.653 0.641 0.645 0.661 0.683 Capex/depreciation 1.9x 1.0x 0.7x 1.1x 1.3x 1.4x

BVPS 0.477 0.453 0.471 0.493 0.516 0.542 Capex/net fixed assets 0.2x 0.1x 0.1x 0.1x 0.1x 0.1x

DPS 0.011 0.000 0.015 0.017 0.018 0.020 Op. cash flow/capex 1.1x 1.4x 1.8x 1.5x 1.3x 1.3x

EBITDA margin 37.8% 34.3% 30.4% 31.7% 34.4% 34.7%

VALUATION RATIOS 2014 2015 2016 2017E 2018E 2019E EBIT margin 15.5% -2.9% 9.0% 13.5% 14.6% 15.6%

P/E 8.1x n.m. 16.4x 8.2x 7.6x 6.8x Pre-tax margin 13.5% -4.0% 7.8% 13.3% 14.5% 15.6%

P/CF 2.5x 3.2x 3.8x 3.1x 3.0x 2.8x Net margin 9.7% -3.8% 6.4% 11.3% 12.2% 13.1%

P/BV 0.6x 0.7x 0.6x 0.6x 0.6x 0.6x ROE 7.8% -2.7% 3.9% 7.5% 7.6% 8.2%

EV/EBITDA 3.2x 4.2x 5.0x 4.1x 3.9x 3.6x ROCE (avg) 5.5% -1.9% 2.9% 5.7% 6.0% 6.5%

EV/Sales 1.2x 1.4x 1.5x 1.3x 1.3x 1.2x Net debt/EBITDA 7.3% 15.9% -9.0% -25.3% -30.7% -32.3%

EV/EBIT 5.1x (32.2)x 11.6x 6.9x 6.4x 5.7x

Cash flow from ops, RON m 6,830 5,283 4,454 5,473 5,679 5,990

EV, RON m 25,824 26,188 24,752 23,719 23,344 23,142

FCF, RON m 1,172 329 1,559 1,853 1,319 1,230

FCF yield 6.9% 1.9% 9.1% 10.9% 7.7% 7.2%

Dividend yield 3.7% 0.0% 5.0% 5.6% 6.0% 6.8%

COMPANY FINANCIALS

INCOME STATEMENT, RON m 2014 2015 2016 2017E 2018E 2019E BALANCE SHEET, RON m 2014 2015 2016 2017E 2018E 2019E

Net Sales 21,541 18,145 16,247 18,436 18,342 19,193 Cash & cash equivalents 1,268 813 1,996 2,829 3,104 3,206

EBITDA 8,144 6,231 4,932 5,844 6,040 6,366 Accounts receivable 1,424 1,318 1,540 1,553 1,457 1,472

Depreciation 3,344 3,947 3,566 3,360 3,400 3,501 Inventories 2,250 1,965 1,950 1,874 1,910 1,998

EBIT 3,338 (530) 1,469 2,484 2,675 2,996 Other CA 926 884 526 526 526 526

EBIT by segments Total current assets 5,868 4,980 6,012 6,783 6,997 7,203

Exploration & Production 3,832 -1,836 509 1,342 1,333 1,636 Long-term investments 2,192 2,628 2,593 2,593 2,593 2,593

Downstream -179 1,208 1,299 1,141 1,365 1,422 PP&E 32,290 29,278 28,326 28,586 29,546 30,805

Corporate & Other -315 98 -339 0 -22 -62 Intangibles 1,657 2,430 2,536 2,536 2,536 2,536

Net financials -429 -196 -204 -30 -15 0 Other non-current assets 1,104 1,684 1,675 1,675 1,675 1,675

Associates contribution 11 7 7 0 0 0 Total fixed assets 37,243 36,020 35,129 35,389 36,349 37,609

Pre-tax profit 2,909 (726) 1,265 2,454 2,660 2,996 Total assets 43,125 41,118 41,414 42,445 43,619 45,084

Income tax -810 36 -227 -368 -426 -479 Short-term debt 274 379 410 410 410 410

Minority interest -3 -14 -6 0 0 0 Accounts payable 2,899 2,318 2,290 2,292 2,291 2,368

Net profit 2,100 (690) 1,038 2,086 2,235 2,516 Total current liabilities 6,160 5,038 4,485 4,479 4,478 4,555

Long-term debt 1,589 1,424 1,141 941 841 741

CASH FLOW, RON m 2014 2015 2016 2017E 2018E 2019E Provisions 7,538 8,180 8,148 8,148 8,148 8,148

CF from Operations 6,830 5,283 4,454 5,473 5,679 5,990 Other non-current liabilities 833 778 798 798 798 798

Thereof depreciation 4,806 6,761 3,464 3,360 3,400 3,501 Total LT liabilities 9,960 10,382 10,087 9,887 9,787 9,687

Thereof changes in w/c 31 -342 -106 130 -66 27 Minority interest (36) (55) (63) (63) (63) (63)

CF from Investments -5,658 -4,953 -2,896 -3,620 -4,360 -4,760 Total shareholders' equity 27,005 25,688 26,706 27,942 29,218 30,706

Dividends -1,731 -631 -1 -850 -959 -1,028 Total liab. & equity 43,125 41,118 41,414 42,445 43,619 45,084

Net equity issues 0 0 0 0 0 1 Net Debt 595 990 (446) (1,479) (1,854) (2,056)

Change in Net debt -140 -455 1,183 833 275 102 Net Working Capital 775 966 1,200 1,135 1,076 1,103

OPERATIONS 2014 2015 2016 2017E 2018E 2019E MACRO ASSUMPTIONS 2014 2015 2016 2017E 2018E 2019E

Total production (m boe) 65.8 65.2 63.7 62.0 60.8 59.5 RON/USD avg. 3.35 4.01 4.05 4.00 4.04 4.08

Total production (boepd) 180.5 178.8 174.0 170.1 166.7 163.4 Brent oil price, USD/bbl 99.1 52.4 42.7 53.8 55.0 60.0

growth, % -1.0% -2.7% -2.2% -2.0% -2.0% Urals/Brent differential, USD/bbl 1.02 0.88 1.60 1.50 1.50 1.50

Liquids production, bpd 85 83 80 79 83 82 Indicator Refining Margin 1.68 8.70 7.00 7.38 7.18 6.53

Natgas production, boepd 96 95 94 91 83 82

Refinery throughput, kt 4,010 4,180 4,220 4,200 4,123 4,123

Filling stations 781 780 784 780 780 780

Profitability PROFITABILITY TRENDS

E&P EBITDA/bbl, USD 32.7 15.7 12.0 15.9 15.9 17.5

R&M EBITDA/bbl, reported, USD 6.0 15.0 16.3 15.5 17.1 16.8

Petrom, majority-owned (51%) by OMV, is an integrated oil&gas company in Romania, with some activity in

Kazakhstan and the Balkans. It produces c. 180,000 boepd oil&gas (172,000 boepd in Romania) and is physically

integrated with refining (Petrobrazi, with 4.5m tpa capacity) to best monetise its oil. Petrom has a filling station

network of 777 sites (548 in Romania with c. 38% market share). Petrom E&P operates in a fixed fiscal regime until

the end of 2015 with a benign royalty of c.7%. It has mature fields with an annual base-line decline rate of c.5-10%,

on our estimates. Heavy capex is aimed at reducing the decline rate and achieving a 50% RRR. Petrom made a

major off-shore gas discovery in the Black Sea in 2012 with Exxon. While the oil market is liberalised, Romania used

to regulate gas prices until 2013. The natgas price deregulation is to be completed in 2018. The key risks relate to

the oil macro, politics and regulation (gas prices, royalties and taxes), geology (reservoir quality).0.20

0.22

0.24

0.26

0.28

0.30

0.32

Mar-

16

Mar-

16

Apr-

16

May-1

6

Ju

n-1

6

Jul-16

Aug

-16

Sep

-16

Oct-

16

Nov-1

6

De

c-1

6

Jan-1

7

Feb-1

7

SNP RO Equity BET Index rebased

0.378065164

0.3434007640.3035854820.316968064

0.3441533760.347027474

0

0.05

0.1

0.15

0.2

0.25

0.3

0.35

0.4

3,000

4,000

5,000

6,000

7,000

8,000

9,000

2014 2015 2016 2017E 2018E 2019E

EBITDA EBITDA margin

32.6

8545182

15.6

9393286

11.9

9503811

15.8

9637097

15.9

285325

17.4

9641327

6.0

21837981

15.0

260513

16.3

4198365

15.5

0378343

17.1

0009544

16.7

9238067

0

5

10

15

20

25

30

35

2014 2015 2016 2017E 2018E 2019E

E&P EBITDA/bbl, USD R&M EBITDA/bbl, reported, USD

OMV Petrom 29 WOOD & Company

Investment case

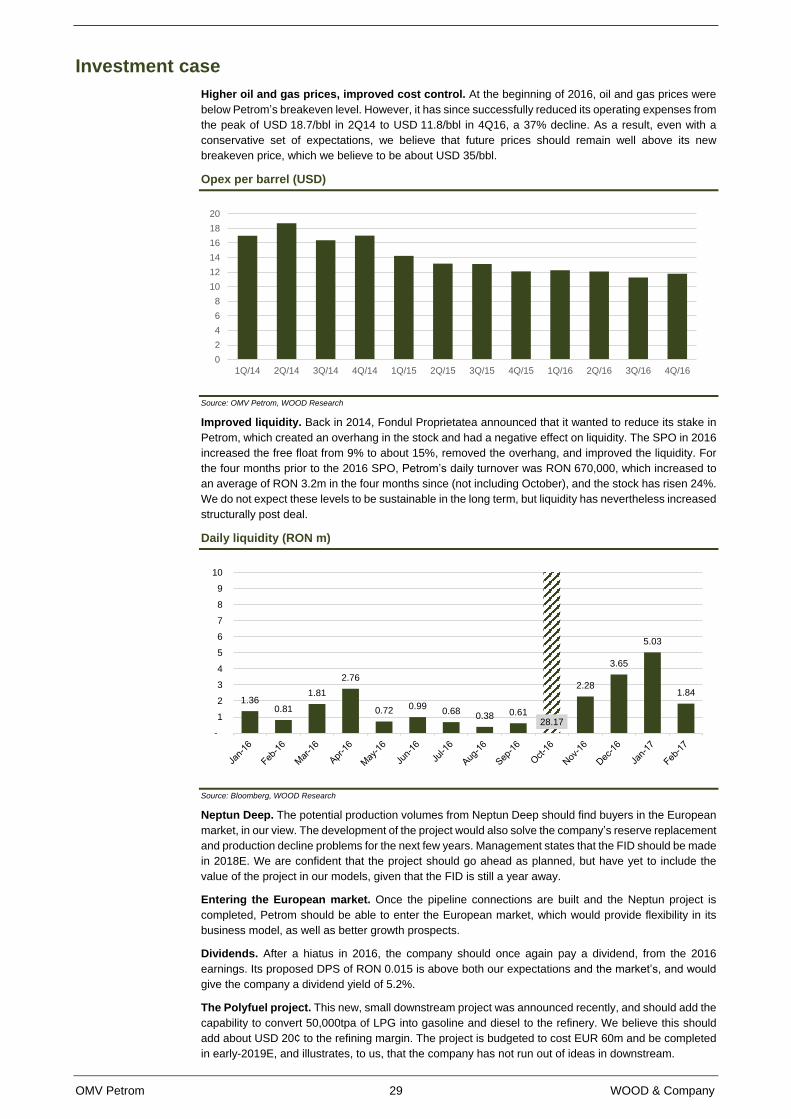

Higher oil and gas prices, improved cost control. At the beginning of 2016, oil and gas prices were

below Petrom’s breakeven level. However, it has since successfully reduced its operating expenses from

the peak of USD 18.7/bbl in 2Q14 to USD 11.8/bbl in 4Q16, a 37% decline. As a result, even with a

conservative set of expectations, we believe that future prices should remain well above its new

breakeven price, which we believe to be about USD 35/bbl.

Opex per barrel (USD)

Source: OMV Petrom, WOOD Research

Improved liquidity. Back in 2014, Fondul Proprietatea announced that it wanted to reduce its stake in

Petrom, which created an overhang in the stock and had a negative effect on liquidity. The SPO in 2016

increased the free float from 9% to about 15%, removed the overhang, and improved the liquidity. For

the four months prior to the 2016 SPO, Petrom’s daily turnover was RON 670,000, which increased to

an average of RON 3.2m in the four months since (not including October), and the stock has risen 24%.

We do not expect these levels to be sustainable in the long term, but liquidity has nevertheless increased

structurally post deal.

Daily liquidity (RON m)

Source: Bloomberg, WOOD Research

Neptun Deep. The potential production volumes from Neptun Deep should find buyers in the European

market, in our view. The development of the project would also solve the company’s reserve replacement

and production decline problems for the next few years. Management states that the FID should be made

in 2018E. We are confident that the project should go ahead as planned, but have yet to include the

value of the project in our models, given that the FID is still a year away.

Entering the European market. Once the pipeline connections are built and the Neptun project is

completed, Petrom should be able to enter the European market, which would provide flexibility in its

business model, as well as better growth prospects.

Dividends. After a hiatus in 2016, the company should once again pay a dividend, from the 2016

earnings. Its proposed DPS of RON 0.015 is above both our expectations and the market’s, and would

give the company a dividend yield of 5.2%.

The Polyfuel project. This new, small downstream project was announced recently, and should add the

capability to convert 50,000tpa of LPG into gasoline and diesel to the refinery. We believe this should

add about USD 20¢ to the refining margin. The project is budgeted to cost EUR 60m and be completed

in early-2019E, and illustrates, to us, that the company has not run out of ideas in downstream.

0

2

4

6

8

10

12

14

16

18

20

1Q/14 2Q/14 3Q/14 4Q/14 1Q/15 2Q/15 3Q/15 4Q/15 1Q/16 2Q/16 3Q/16 4Q/16

1.360.81

1.81

2.76

0.720.99

0.680.38 0.61

28.17

2.28

3.65

5.03

1.84

-

1

2

3

4

5

6

7

8

9

10

OMV Petrom 30 WOOD & Company

Valuation

DCF

Our valuation for Petrom is derived using a 10-year DCF, with a zero terminal growth rate for the

downstream business and -3% for upstream. We calculate a 12-month price target (PT) of RON 0.361,

offering upside of 18%.

OMV Petrom: 10-year DCF

RONm 2017E 2018E 2019E 2020E 2021E 2022E 2023E 2024E 2025E 2026E

Downstream 1,901 2,079 2,063 2,092 2,118 2,149 2,181 2,214 2,247 2,277

Upstream 3,942 3,910 4,252 4,390 4,504 4,655 4,791 4,936 5,082 5,174

Total EBITDA 5,844 5,990 6,314 6,482 6,623 6,805 6,972 7,150 7,330 7,451

Taxes 369 426 479 474 476 493 503 514 525 522

Capex 3,620 4,360 4,760 4,838 4,918 4,999 5,081 5,166 5,252 5,340

Change in WC 66 -27 -8 -8 -25 -19 -20 -20 -3 0

FCF 1,790 1,231 1,083 1,178 1,254 1,332 1,409 1,491 1,556 1,589

PV of FCF 1,641 1,035 835 833 813 792 768 745 713 668

Source: WOOD Research

OMV Petrom: DCF summary and WACC calculation

SUM of PV 8,845 Risk-free rate 4.5%

PV of TV 9,291 ERP 4.5%

Levered beta 1.10

Total EV 18,137 Cost of equity 9.5%

Net debt/cash 446 Tax-rate 16.0%

Equity value 18,582 After-tax cost of debt 5.5%

Per share (RON) 0.328 % of equity 90.0%

% of debt 10.0%

12M PT (RON) 0.361 WACC 9.1%

Source: WOOD Research

Ratios

At current prices, OMV Petrom trades at P/E ratios of 8.2x for 2017E and 7.6x for 2018E, on our

estimates, vs. 10.1x and 9.2x for its European peer group, on WOOD/consensus estimates. On an

EV/EBITDA, the company’s ratios are 4.1x for 2017E and 3.8x for 2018E, on our estimates, compared

with 4.6x and 4.2x for its peer group. On these metrics, Petrom looks undervalued, in our view.

OMV Petrom: valuation ratios

2014 2015 2016E 2017E 2018E 2019E 2020E

P/E 7.82 -23.82 16.43 8.17 7.63 6.75 6.83

P/CF 2.41 3.11 3.83 3.12 3.00 2.84 2.79

P/BV 0.61 0.64 0.64 0.60 0.58 0.55 0.53

EV/EBITDA 3.09 4.10 5.02 4.06 3.77 3.56 3.46

EV/CE 0.66 0.69 0.68 0.65 0.62 0.59 0.57

EV/sales 1.17 1.41 1.52 1.29 1.24 1.18 1.16

EV/EBIT 4.92 -31.01 11.60 6.86 6.37 5.69 5.77

FCF, RONm 1,172 329 1,559 1,853 1,919 1,152 1,209

FCF yield 7.1% 2.0% 9.1% 10.9% 11.3% 6.8% 7.1%

Dividend yield 3.8% 0.0% 5.0% 5.6% 6.0% 6.8% 6.7%

Source: WOOD Research

WOOD vs. the consensus

We are roughly in line with the consensus on EBITDA and EBIT for both 2017E and 2018E, but are a

little above for 2019E. The figures are based on a small number of forecasts, however, and may not be

up to date, which is almost certainly the case for the 2019E net profit expectations, where we are

considerably higher than the consensus.

WOOD vs. the consensus

RONm Revenues EBITDA EBIT Net profit

2017E 2018E 2019E 2017E 2018E 2019E 2017E 2018E 2019E 2017E 2018E 2019E

WOOD Research 18,436 18,342 19,193 5,844 6,040 6,366 2,484 2,675 2,996 2,086 2,235 2,516

Consensus 17,578 18,053 18,377 6,024 6,364 5,855 2,393 2,766 2,833 2,420 2,329 1,608

% difference 4.9% 1.6% 4.4% -3.0% -5.1% 8.7% 3.8% -3.3% 5.8% -13.8% -4.0% 56.4%

Source: Bloomberg, WOOD Research

OMV Petrom 31 WOOD & Company

Company background

OMV Petrom is the largest oil and gas group in south-east Europe, with activities in upstream,

downstream gas and downstream oil. It accounts for almost all crude oil production in Romania, and

supplies around half of the internal gas production. OMV Petrom operates 239 commercial oil and gas

fields in Romania, from which a combined volume of 171.41kboe/d was produced in 2014. OMV Petrom

supplies gas through the natural gas division. Its annual oil and gas production is c.66m boe (mboe).

The company also operates in the Caspian region, specifically Kazakhstan.

As of 31 December 2015, the total proved oil and gas reserves in OMV Petrom Group’s portfolio

amounted to 582mboe, of which Romania represented 558mboe; while proved and probable oil and gas

reserves amounted to 977mboe, of which Romania represented 930mboe.

OMV Petrom processes crude at the Petrobrazi refinery, near Ploiesti, with refining capacity of 4.5mtpa.

The refinery underwent a EUR 600m modernisation programme from 2010-14, allowing it to process all

of OMV Petrom’s Romanian crude production, while improving energy efficiency and product yields.

OMV Petrom is also present in the distribution market for oil products in Romania, the Republic of

Moldova, Bulgaria and Serbia, through a network of c.780 filling stations, operated under two brands,

Petrom and OMV.

Ownership structure

OMV, Austria’s largest listed industrial company, holds a 51.0% share in Petrom. The Romanian state,

via the Ministry of Economy, holds another 20.6%, Fondul Proprietatea (FP) holds 12.6% and 15.8% is

free float on the Bucharest Stock Exchange. We expect to see further reductions in FP’s stake, resulting

in increases in free float, although there is a 12-month lock-up period following the recent SPO.

OMV Petrom: shareholder structure

Source: OMV Petrom, WOOD Research

Company history

Petrom was created from a number of companies in 1997, as the national oil company of Romania. In

2004, it was privatised and 51% of the shares were sold to OMV. The Arpechim refinery was closed in