entrepreneurship & technology commercialization report...

TRANSCRIPT

Entrepreneurship&Technology

CommercializationReport2017:

GlobalTrendsandSpecificLookatTurkey

1

This report is prepared by Duygu Oktem Clark with contributions from DenizBayhan,DoganTaskent,HeathNaquin(VentureWell),EliVelasquez(VentureWell)andPatrickTerroir(LicensingExecutivesSocietyInternational).

TTATurkeyTeam

DuyguÖktemClarkBusinessDevelopmentLeader-TTATurkeyContact:[email protected]/[email protected]

DoganTaskentBusinessDevelopmentLeader-TTATurkeyContact:[email protected]/[email protected]

HeathNaquinStrategyDevelopmentandTrainingLeader-TTATurkeyContact:[email protected]

Editor:DuyguÖktemClark

Contact:EuropeanInvestmentFundİstanbulOfficeBüyükdereCaddesiNo:199,24thFloor,LeventTR-34394IstanbulTurkeyTel:+902123179010

İstanbul,January2018

Disclaimer:ThisReportshouldnotbereferredtoasrepresentingtheviewsoftheEuropeanInvestmentFund (EIF), Technology Development Foundation of Turkey, Ministry of Science, Industry andTechnology,theScientificandResearchCouncilofTurkey,theDelegationoftheEuropeanUniontoTurkey and the DG Regional Policy of the European Commission (stakeholders of the TTA-TurkeyAdvisoryServicesandNetworkingProject).Anyviewsexpressedherein,includinginterpretation(s)ofregulations,reflectthecurrentviewsoftheauthor(s),whichdonotnecessarilycorrespondtotheviewsof EIF or of the stakeholders of the TTA-Turkey Advisory Services and Networking Project. Norepresentationorwarranty,expressorimplied,isorwillbemadeandnoliabilityorresponsibilityisorwillbeacceptedbyEIForby thestakeholdersof theTTA-TurkeyAdvisoryServicesandNetworkingProjectinrespectoftheaccuracyorcompletenessoftheinformationcontainedhereinandanysuchliability is expressly disclaimed. Reproduction, publication and reprint are subject to prior writtenauthorizationoftheauthor(s).

This page intentionally left blank

3

Preface

TheTechnologyTransferAcceleratorTurkey(TTATurkey)-aninitiativemanagedbytheEuropeanInvestmentFund(EIF)-aimstocommercializeappliedresearchfromuniversitiesandscaleupthetechnologytransfermarketinTurkey,withaparticularfocusonspill-overstothecountry’slessdevelopedregions.

Launched in 2014, TTA was designed by EIF in cooperation with the Ministry ofScience,IndustryandTechnology,theScientificandResearchCouncilofTurkey,theDelegation of the European Union to Turkey and the DG Regional Policy of theEuropean Commission. TTA Turkey is co-financed by the EU and the Republic ofTurkeyundertheregionaldevelopmentcomponentofthecountry'sInstrumentforPre-AccessionAssistance(IPA)funds.TheRegionalDevelopmentComponentofIPAismanagedbytheMinistryofScience,IndustryandTechnology.

The term of TTA-Turkey Advisory Services Project is two years (December 2015 -December 2017), and the objective of the project is to improve the technicalcapacitiesofTechnologyTransferOffices(TTOs)includingthosewhicharelocatedin12NUTSIIRegionsofTurkey,toimproveTÜBİTAK’scapacitytocommercializeR&D,andtosupportTTA-Turkeyfundsthroughnetworkingactivitiesinfindingappropriateinvestmentopportunities.

Inthisreport,thecurrentsituationandglobaltrendsinentrepreneurshiparestated.WehaveaspecificlooktoTurkeybygivinginformationabouttheentrepreneurshiplandscape, related statistics as well as observations and recommendations withregardtotechnologycommercializationandtheentrepreneurialecosystem.

4

TableofContents

Preface……………………………………………………………………………………………………………………3TableofContents……………………………………………………………………………………………….…..4ListofFigures………………………………………………………………………………………………………….5ListofTables…………………………………………………………………………………………………………..6Chapters1. TheGlobalPerspective…………………………………………………………………………………….7

1.1. SocietalAttitudesandPerceptionsAboutEntrepreneurship……..…..………121.2. WomenEntrepreneurship……………………………………………………………………..131.3. VentureInvesting………………….……………………………………………………………….161.4. EffectivenessofTaxIncentivesforVentureCapitalandBusinessAngels..20

2. TurkishEntrepreneurshipEcosystem……………………………………………………………..23

2.1. VentureInvestinginTurkey……………………………………………………………………25

2.1.1. AdditionalRemarks……………………………………………………………………….272.2. GovernmentPrograms…………….……………………………………………………………..292.3. Universities,TechnologyTransferOfficesandTechnoparks……………………30

2.3.1. Universities………………………………………………………………………………….302.3.2. TechnologyTransferOffices…………………………………………………………302.3.3. Technoparks…………………………………………………………………………………312.3.4. WomenEntrepreneurship……………………………………………………………..32

3. OutputsandAchievementsoftheTTATurkeyProject…………………………………….33

4. ObservationsandRecommendations……………………………………..……………………...36

Appendix….……………………………………………………………………………………………………………40

5

ListofFigures

1 The2017StartupEcosystemRanking…………………………………………………………………….9

2 SomeAnalysisBasedon2018GEIforEachRegion………………………………………………..11

3 SocietalAttitudesandPerceptionsAboutEntrepreneurship…………………….……………12

4 SharesofMaleandFemaleStartupFounders(Europe,UKandAustria)…….………….14

5 PercentofFemaleEntrepreneursinEachIndustrybyRegion………………………………..15

6 GlobalVentureFinancingbyStage..……………………………….………………………….…………..17

7 DistributionofGlobalVentureFinancing……………….………………………………………………17

8 GlobalFinancingTrends………………….…………………….………………………………….…………..18

9 GlobalMedianPre-moneyValuations($M)bySeries……….………………………….………..18

10 GlobalMedianDealSize($M)byStage….…………………………………………..…….…………..19

11 CorporateVCParticipationinGlobalVentureDeals……………………..………….……………20

12 TopOECDCountriesbyAnnualAverageRealGDPGrowthRate(2003-2016)………..23

13 NumberofPatentsGrantedinTurkey(2006-2016)….…………………………………………….25

14 NumberofPatentApplicationsinTurkey(2006-2016)……….……………………..….…….…25

15 NumberofScientificPublicationsinTurkey(2006-2016)………………….….…………..…..25

16 VentureInvestmentsinTurkey(2010-2017)……………………………………………….……....26

17 VentureInvestmentsbyStageinTurkey(2010-2017)………………………..……….……....26

18 CVCInvestmentsinTurkey(2010-2017)…………………………….……………………….……....27

19 MostFundedVerticalsin2017……………..……………………………………………………….……..27

6

ListofTables

1 TheGlobalEntrepreneurshipIndex2018(Top20Countries).……………………………….10

2 TheGlobalGenderGap2017Index(Top20Countries)…………………………………………13

3 TTATurkeyProjectSynopsis………………..……………………………………………………………….33

4 PerformanceMetricsofAccelerators……………………………………………………………………38

7

Entrepreneurship&Technology

CommercializationReport2017:

GlobalTrendsandSpecificLookatTurkey1.TheGlobalPerspective

Entrepreneurshipisanimportantsourceofemploymentcreationandinnovationaswellassustainableeconomicgrowth.Asthisisunderstood,theimportancegiventoentrepreneurship by countries increases each passing day.Herearesomehighlightsfromaroundtheglobeshowcasingtherelationshipbetweenstartupsandeconomicdevelopment:

- AccordingtotheOECD,inallOECDcountries,aroundtwo-thirdsofalljobswerecreatedbynewfirmsin2014.1

- WhenwelookatthedataforEuropeoverall,weseethatstartupsprovidearound50%ofallnewjobs.2

- SmallbusinessescontinuetoplayavitalroleintheeconomyoftheUnitedStates.Thenumberofjobscreatedbyestablishmentslessthan1yearoldwas3millionin2015intheUSA.Smallbusinessesproduced46percentoftheprivatenonfarmGDPin2008(themostrecentyearforwhichthesourcedataisavailable).3

- Asof2015,smallbusinessesemployedover8.2millionindividualsinCanada,or70.5percentofthetotalprivatelaborforce.4

AccordingtotheEuropeanCommission,Europe’seconomicgrowthandjobsdependon its ability to support the growthof enterprises.Themost important sourcesofemployment in theEUareSmallandMedium-sizedEnterprises (SMEs).Therefore,theCommission’sobjectiveistoencouragepeopletobecomeentrepreneursandalsomakeiteasierforthemtosetupandgrowtheirbusinesses.5TheEntrepreneurship2020 Action Plan that was presented by The Commission aims to facilitate thecreationofnewbusinessesandtocreateamuchmoresupportiveenvironmentforexistingentrepreneurs to thriveandgrow.Therearealso special sub-programsonentrepreneurshipundertheCommission’sHorizon2020Program.TheCommissionistryingtokeepentrepreneurshiponeofthemostimportantagendaitemsinEurope.

1 http://www.oecd.org/std/business-stats/2 http://europeanstartupmonitor.com/fileadmin/esm_2016/report/ESM_2016.pdf 3http://sbecouncil.org/ 4https://www.ic.gc.ca/eic/site/061.nsf/vwapj/ksbs-psrpe_june-juin_2016_eng.pdf/$file/ksbs-psrpe_june-juin_2016_eng.pdf 5https://ec.europa.eu/growth/smes/

8

Inhisbook“StartupCommunities”,BradFeldwhoisawell-knownentrepreneurandventure capitalist states that it takes about 20 years to develop a vibrantentrepreneurial ecosystem. 6 Indeed, creating a sustainable entrepreneurialecosystem requires a lot of effort, dedication, resources, time and a change inmindset.

StartupGenomewhich is a global collaborative effort to help regions everywherenurtureandmaintainthrivingtechstartupecosystems,publishedtheirannualreporttorankthestartupecosystemsglobally.Asempasizedinthereport,inorderformorestartupsaroundtheworldtothriveweneedtounderstandtheunderlyinginfluencesofstartupecosystems’success.7Theindexisproducedbyrankingecosystemsalongfivemajorcomponents:

- Performance:Startupoutput,exits,valuations,early-stagesuccess,growth-stagesuccess,overallecosystemvalue

- Funding:Accessthroughmetricsoftotalandperstartupearly-stageinvestmentsas well as growth in early-stage investments, funding quality through thepresenceofexperiencedVCfirms

- Talent:Access, cost, and quality of talent. The Access sub-factor includes theproportionofsoftwareengineersandgrowthemployeeswithtwoormoreyearsofexperienceatapriorstartup,thetimerequiredtohireanengineer,andtheabilitytoobtainavisaforhiresfromabroad

- MarketReach:Globalconnectednessandglobaland local reach,basedonthestartups’proportionofforeigncustomersandthenationalGDP

- StartupExperience:TeamExperienceandEcosystemExperience.Theformerisbasedonfounderhyper-growthorunicornexperience,advisorswithequity,andstartups providing options to all their employees.Option grants to employeesreflect a founder’s knowledge of aligning incentives, as well as whetheremployees value stock options, indicating a strong startup culture in theecosystem. Ecosystem Experience is based on the number of exits above $50millionachievedwithinthelast10years.

ItisworthnotingthisyearStartupGenomeaddedthefollowingdimensionstotheirranking: Global Connectedness, Resource Attraction and Leakages, FounderAmbition,FounderGo-GlobalStrategyandCorporateInvolvement.

StartupGenomeassessed55startupecosystemsacross28countriesandrankedthetop20.Therankingisprimarilydrivenbyonequestion:inwhichecosystemsdoesanearly-stagestartuphavethebestchanceofbuildingaglobalsuccess?Herearetop20startupsecosystemsaroundtheworld.

6Brad Feld, Startup Communities: Building an Entrepreneurial Ecosystem in Your City (Wiley, 2012) 7https://startupgenome.com/about-us/

9

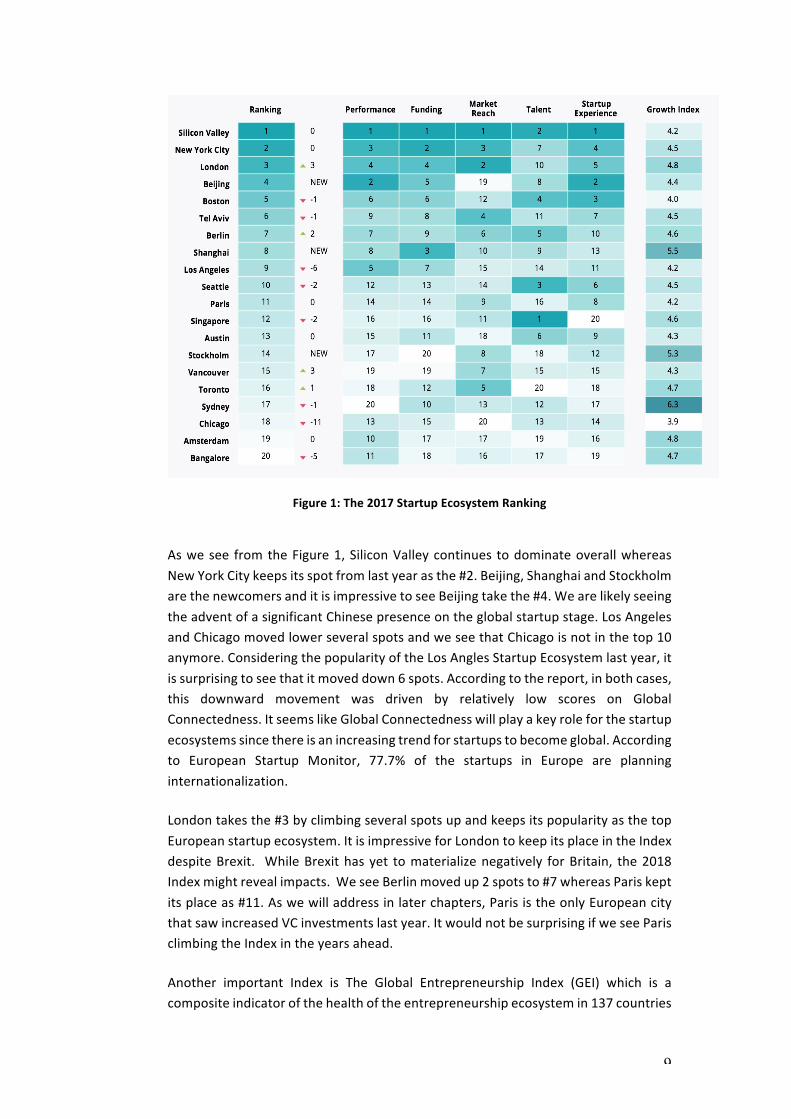

Figure1:The2017StartupEcosystemRanking

Aswesee fromtheFigure1,SiliconValleycontinues todominateoverallwhereasNewYorkCitykeepsitsspotfromlastyearasthe#2.Beijing,ShanghaiandStockholmarethenewcomersanditisimpressivetoseeBeijingtakethe#4.WearelikelyseeingtheadventofasignificantChinesepresenceontheglobalstartupstage.LosAngelesandChicagomovedlowerseveralspotsandweseethatChicagoisnotinthetop10anymore.ConsideringthepopularityoftheLosAnglesStartupEcosystemlastyear,itissurprisingtoseethatitmoveddown6spots.Accordingtothereport,inbothcases,this downward movement was driven by relatively low scores on GlobalConnectedness.ItseemslikeGlobalConnectednesswillplayakeyroleforthestartupecosystemssincethereisanincreasingtrendforstartupstobecomeglobal.Accordingto European Startup Monitor, 77.7% of the startups in Europe are planninginternationalization.

Londontakesthe#3byclimbingseveralspotsupandkeepsitspopularityasthetopEuropeanstartupecosystem.ItisimpressiveforLondontokeepitsplaceintheIndexdespiteBrexit. WhileBrexithasyet tomaterializenegatively forBritain, the2018Indexmightrevealimpacts.WeseeBerlinmovedup2spotsto#7whereasPariskeptitsplaceas#11.Aswewilladdressinlaterchapters,ParisistheonlyEuropeancitythatsawincreasedVCinvestmentslastyear.ItwouldnotbesurprisingifweseeParisclimbingtheIndexintheyearsahead.

Another important Index is The Global Entrepreneurship Index (GEI) which is acompositeindicatorofthehealthoftheentrepreneurshipecosystemin137countries

10

prepared by The Global Entrepreneurship and Development Institute. The GEImeasures both the quality of entrepreneurship and the extent and depth of thesupportingentrepreneurialecosystem.8Herearethetop20countriesintheGEI:

Table1:TheGlobalEntrepreneurshipIndex2018(Top20Countries)

HerearesomehighlightsbasedontheTheGlobalEntrepreneurshipIndex2018:

• Globally,GEIscoreshaveimprovedby3%onaveragesincelastyear’sIndex.

• In the 2018GEI, the Asia-Pacific region on average scores best in ProductInnovation.TheregionisalsostronginHumanCapital.

• Europe shows stable high scores in Technology Absorption andInternationalization,andregion’saveragescoreonStartupSkillshasrecentlyclimbedintothesameleague.

• TheMiddleEastandNorthAfricaregiondemonstratesstrengthinProductInnovationandRiskCapital.

8https://thegedi.org/2018-global-entrepreneurship-index/

11

• North America’s strongest areas are Opportunity Perception and RiskAcceptance

• South/CentralAmericaandtheCaribbeanisstrongestintheareasofStartupSkillsandProductInnovation

• Sub-SaharanAfricashowsgreateststrengthinOpportunityPerception.

• Globally,we’veseena22%increase inProduct Innovationscoressincethe2017GEI,andan11%increaseinStartupSkillsscoressincethe2017GEI.Thissuggests that the global population is becoming more educated andidentifyingmoreopportunitiestocreatenewproducts.

Figure2showssomeanalysisandrecommendationsfromtheReportforregions:

Figure2:SomeAnalysisBasedon2018GEIforEachRegion

12

1.1. SocietalAttitudesandPerceptionsAboutEntrepreneurship

As we stated before, the importance given to entrepreneurship by countries isincreasing.Asaresult,societalattitudesandperceptionsarechanginginapositiveway globally. This is important since in most countries, social norms and culturalchallengeshavebeenoneofthemainobstaclestoentrepreneurship.Thepositiveornegative perceptions that societyhas about entrepreneurship have a stronginfluenceontheentrepreneurship.9

Figure3:SocietalAttitudesandPerceptionsAboutEntrepreneurship

AccordingtotheGEMReport;inthe61economieswherethesurveywasconducted,working-age adults in efficiency-driven economies are most likely toseeentrepreneurship as a good career choice. On average, two-thirds of the adultpopulation in these economies consider starting a business a good careerchoice,comparedtoaround60%inthefactor-andinnovation-driveneconomies(Figure3).Morethantwo-thirdsof theadultpopulation,acrossall threephasesofeconomicdevelopment, believe that entrepreneurs arewell-regarded and enjoy high statuswithintheirsocieties.

Basedon the resultsof thesurvey, it isworthmentioning thatEuropereports thelowest rates of opportunity and capability perception, as well as the lowestentrepreneurialintentions(12%).Lessthan40%ofEuropeansperceiveopportunitiesintheirarea,andlessthanhalfbelievetheyhavetheskillstopursueentrepreneurialopportunities. The European Commission is putting a lot of effort to foster andstrengthenentrepreneurshipinEuropebutitseemsthereisroomforfurtherpolicyactions.

9http://www.gemconsortium.org/report/49812

13

In termsofdemographics, theoverall agepattern forentrepreneurship shows thehighestparticipationratesamongthe25–44yearolds,peopleintheirearlyandmid-careers which is exactly the same from last year. According to the report, theprevalenceofearly-stageentrepreneurialactivityisrelativelylowinthe18–24yearscohort,andshowsthesharpestdecreaseaftertheageof54.

1.2. WomenEntrepreneurship

Women entrepreneurs contribute substantially to economic growth even thoughtheyhavestruggledtoaccesstocapitalandhavetocontendwithsocialconstraints.Inordertohavesustainableeconomies,wehavetoworkonaddressingthegendergapandinequalities.

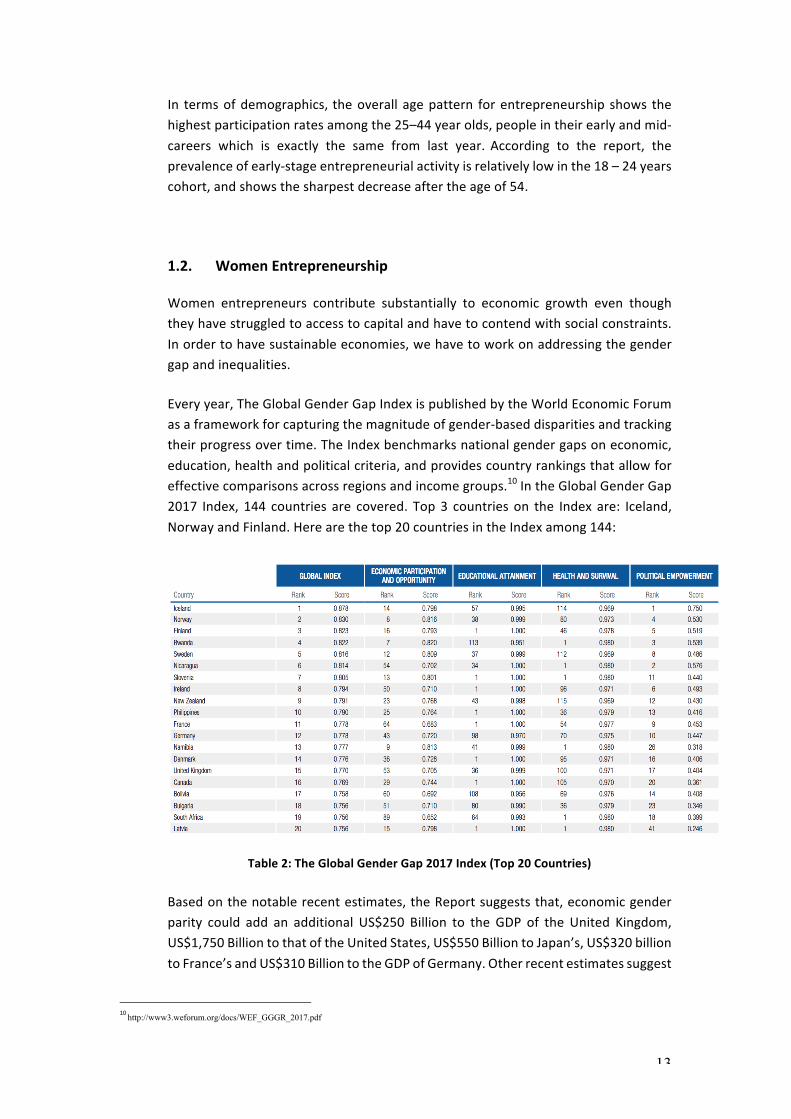

Everyyear,TheGlobalGenderGapIndexispublishedbytheWorldEconomicForumasaframeworkforcapturingthemagnitudeofgender-baseddisparitiesandtrackingtheirprogressovertime.TheIndexbenchmarksnationalgendergapsoneconomic,education,healthandpoliticalcriteria,andprovidescountryrankingsthatallowforeffectivecomparisonsacrossregionsandincomegroups.10IntheGlobalGenderGap2017 Index, 144 countries are covered. Top3 countries on the Index are: Iceland,NorwayandFinland.Herearethetop20countriesintheIndexamong144:

Table2:TheGlobalGenderGap2017Index(Top20Countries)

Basedonthenotablerecentestimates,theReportsuggeststhat,economicgenderparity could add an additional US$250 Billion to the GDP of the United Kingdom,US$1,750BilliontothatoftheUnitedStates,US$550BilliontoJapan’s,US$320billiontoFrance’sandUS$310BilliontotheGDPofGermany.Otherrecentestimatessuggest

10http://www3.weforum.org/docs/WEF_GGGR_2017.pdf

14

thatChinacouldseeaUS$2.5TrillionGDPincreasefromgenderparityandthattheworldasawholecouldincreaseglobalGDPbyUS$5.3Trillionby2025byclosingthegendergapineconomicparticipationby25%overthesameperiod.

OECD’sEntrepreneurshipataGlance2017Reportisanotherstudythatprovidesdataandinsightsonwomenentrepreneurship.11Accordingtothereport,agendergapisobservedinallOECDcountriesalsoamongyoungself-employed,i.e.individualslessthan 30 years old. In 2016, only in Chile andMexico the self-employment rate ofwomenwasslightlyhigherthanthatofmen.In2014,self-employedwomenearned10%lessthanmeninLuxembourgandLithuania,butalmost60%lessthanmeninPoland,theUnitedStatesandRomania.

AnotherstudywhichwasconductedbyEuropeanStartupMonitor(ESM)with2,515startups,6,340foundersand23,774employeesinEuroperevealsnotablestatisticsaboutwomenentrepreneurship.12ThereportshowsthattheshareofmalestartupfoundersinEuroperemainsalmostconstantat85.2%,while14.8%arefemale.Thesepercentages were 85.3% and 14.7% respectively in 2015. However, there aredifferencesbetweencountries.ThecountrieswiththehighestpercentageoffemalefoundersaretheUnitedKingdom(33.3%),Greece(28.4%)andIreland(23.3%),whilecountriessuchasAustria(7.1%),Switzerland(10.7%)andBelgium(11.1%)havethelowestpercentagesoffemalefounders.

Figure4:SharesofMaleandFemaleStartupFounders(Europe,UKandAustria)

Whenwelookatthedomainswherewomenentrepreneursstarttheirownbusiness,wesee thatmostparticipationamong femaleentrepreneurs is inwholesale/retail.Women entrepreneurs are less likely to be seen in the information andcommunications technology (ICT) sector. Overall, fewer than 2% are starting ICTbusinesses.GendergapsarewidestinICT,wherewomencompeteatone-thirdthelevelofmenonaverage,andingovernment/health/educationandsocialservices,wherewomencompetetwoandone-fourthtimesmorethanmen.13Figure4showsthepercentoffemaleentrepreneursineachindustrybyregion.

11http://www.keepeek.com/Digital-Asset-Management/oecd/employment/entrepreneurship-at-a-glance-2017 12 http://europeanstartupmonitor.com/ 13https://www.babson.edu/Academics/centers/blank-center/global-research/gem/Documents/GEM%202016-2017%20Womens%20Report.pdf

15

Figure5:PercentofFemaleEntrepreneursinEachIndustrybyRegion

Womenhavedisadvantages inthe investmentdomainaswell.Statisticsshowthatwomenhavemoredifficultiesgettingfundedbymale-dominatedVCfirms.AccordingtotheCrunchbaseWomeninVentureReportwhichwaspublishedinOctober2017,only 10 percent of venture dollars globally between 2012 and Q3 2017 went tostartupswithatleastonewomanfounder.14

According to a study conducted by the well-known San Francisco based venturecapitalfirmFirstRoundCapitalusingadatasetof300companies,companiestheyinvested inthathada femalefounderperformed63%betterthancompaniestheyinvested in that had all-male founding teams.15It isworth remembering thewell-knownHarvardBusinessSchoolstudyinwhichinvestorschosebusinessespresentedbymales68.3%ofthetime.Inthestudyonly31.7%ofinvestorschosetofundtheventureswhosepitcheswerepresentedbyfemales16.

The gender gap also exists when it comes to number of women in VC firms.CrunchbaseWomeninVentureReportstatesthatjust8percentofpartnersattop100venturefirmsarewomen.

Women entrepreneurship has come a long way but there is still much room forimprovement.

14https://techcrunch.com/2017/10/04/announcing-the-2017-update-to-the-crunchbase-women-in-venture-report/ 15http://10years.firstround.com/16http://www.hbs.edu/faculty/Publication%20Files/Brooks%20Huang%20Kearney%20Murray_59b551a9-8218-4b84-be15-eaff58009767.pdf

16

1.3. VentureInvesting

AngelinvestorsandVentureCapitalFundsarethebloodofthestartupecosystem.Inthissection,wewill lookattheangelandVCinvestmentamountsglobally,mediansize of deals in different stages, corporate venture capital investments, andinvestmenttrends.

Thetotalamountofglobalventurefinancingroseto$155Billionin2017comparedto$127Billionin2016.17Following2015’speakfundinglevels,2016wasachallengingyear for venture capital investment across the globe, with decreases in both thenumberofdealsand the total valueofVC investment.According to the reportonglobalVCtrendspublishedbyKPMGEnterprise,2017wastheyearofrecovery.Herearesomehighlightsfromthestudy:

• Globalmediandealsizeroseforeverydealstagein2017,withthemediandealsizeofangelandseeddealsrisingto$1millionfrom$800,000,earlystagedealsrisingto$5millionfrom$3.7million,andlaterstagedealsrisingto$10.8millionfrom$9.5million.

• VCinvestmentsintheU.S.roseto$83Billion.

• Pharmaceuticalsandbiotechnologysawamassiveyear-over-yearincreaseinVCinvestment,from$12.2billionin2016to$16.6billionin2017.

• VC investment in artificial intelligence andmachine learning doubled from $6billion in 2016 to $12billion in 2017.AR/VRalso saw significant interest frominvestorsgloballythroughout2017.

• IPOactivitygloballyremainedrelativelyslowcomparedtopreviousyears.

• In2017,therewere93fundingsofcurrentandnewlymintedunicorns(companieswithavaluationover$1billion)created,exceedingthe77fundingsduring2016.

• 2017sawasignificant increase in interest inalternativefinancingmechanisms,

particularlyInitialCoinOfferings(ICOs).Therewasasubstantial increaseinthenumberofICOsin2017,ICOsraisedover$2Billionincapital.

Anothertrendthatisseenintheventureinvestingin2017wasthatinvestorsprefertoinvestlargeramountsinfewerdeals.Inotherwords,the“sprayandpray”approachlostpopularity.

17https://assets.kpmg.com/content/dam/kpmg/xx/pdf/2018/01/venture-pulse-report-q4-17.pdf

17

Figure6:GlobalVentureFinancingbyStage

Inanotherstudy,weseethedistributionofglobalventurefinancingpercapita18.Wesee Israel as the leading countrywhen the investment amount is proportioned topopulation.

VCFundingperCapita

Figure7:DistributionofGlobalVentureFinancingNote: Based on capital invested ($B) in 2016

18Dealroom.co

18

When we look at the global financing trends for VC-backed companies by sector, we see that softwareunsurprisinglydominatesthelist19.

It can be noted that Consumer Goods lost popularitywherepharmaandbiotechhavebeenresilient.

ItisexpectedthatAIandblockchainwillbethetoptwodomainsundersoftwarein2018.

Figure8:GlobalFinancingTrends

Whenwe lookat theglobalmedianpre-moneyvaluationbyseries,weseethatatcloseto$300Millionthemedianpre-moneyvaluationforSeriesDorlaterfinancingshas never been higher. Such high valuations are believed to be one of the mainreasonscompanieschoosetostayprivateinsteadofgoingpublic.

Figure9:GlobalMedianPre-moneyValuations($M)bySeries

19 https://assets.kpmg.com/content/dam/kpmg/xx/pdf/2018/01/venture-pulse-report-q4-17.pdf

19

Globalmediandealsizeroseforeverydealstagein2017,withthemediandealsizeofangelandseeddealsrisingto$1Millionfrom$800,000,earlystagedealsrisingto$5Millionfrom$3.7Million,andlaterstagedealsrisingto$10.8Millionfrom$9.5Million.

Figure10:GlobalMedianDealSize($M)byStage

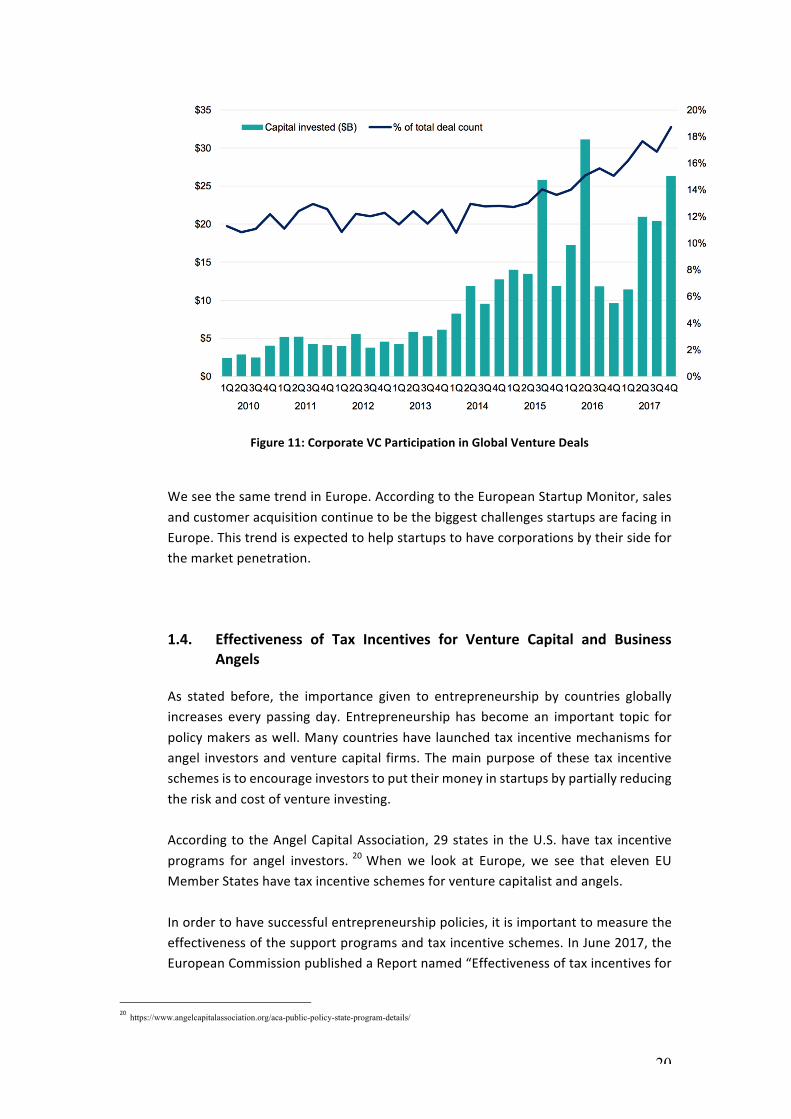

As mentioned earlier, another trend is the increased participation of CorporateVentureCapital (“CVC”) Firms. TheCVC scenehasbecomemore excitingwith the$100Billion SoftbankVision Fund. Corporations are important stakeholders in thestartup ecosystem, therefore it is promising to seemore corporate venture fundsbecoming active. Startup ecosystems are stronger when corporations collaboratewithandacquirestartups.

20

Figure11:CorporateVCParticipationinGlobalVentureDeals

WeseethesametrendinEurope.AccordingtotheEuropeanStartupMonitor,salesandcustomeracquisitioncontinuetobethebiggestchallengesstartupsarefacinginEurope.Thistrendisexpectedtohelpstartupstohavecorporationsbytheirsideforthemarketpenetration.

1.4. Effectiveness of Tax Incentives for Venture Capital and BusinessAngels

As stated before, the importance given to entrepreneurship by countries globallyincreases every passing day. Entrepreneurship has become an important topic forpolicymakersaswell.Manycountrieshavelaunchedtaxincentivemechanismsforangel investorsandventurecapital firms.Themainpurposeof these tax incentiveschemesistoencourageinvestorstoputtheirmoneyinstartupsbypartiallyreducingtheriskandcostofventureinvesting.

AccordingtotheAngelCapitalAssociation,29states intheU.S.havetax incentiveprograms for angel investors.20Whenwe look at Europe, we see that eleven EUMemberStateshavetaxincentiveschemesforventurecapitalistandangels.Inordertohavesuccessfulentrepreneurshippolicies,itisimportanttomeasuretheeffectivenessofthesupportprogramsandtaxincentiveschemes.InJune2017,theEuropeanCommissionpublishedaReportnamed“Effectivenessoftaxincentivesfor

20 https://www.angelcapitalassociation.org/aca-public-policy-state-program-details/

21

venturecapitalandbusinessangelstofostertheinvestmentofSMEsandstart-ups”21.TheaimoftheReportistomeasuretheeffectivenessofthetaxincentiveprogramsin EU-28, theU.S., Canada, Japan, SouthKorea, Turkey,Australia, Switzerland andIsrael,andto identifybenchmarkprogramsaswellasgoodpracticesamongthem.KeyfindingsfromtheReportarebelow:

• Intotal,46tax incentivesareofferedbythesecountries,with13countries

operatingmultipleschemes.FranceandtheUnitedKingdomhavethemostsophisticatedframeworksoftaxincentives,operatingsixschemeseach.

• Taxcreditsinrespectoftheamountinvestedarethemostpopularformofincentive, followed by tax exemptions on the returns (current or capital)generatedbytheinvestment.

• Investortargetingismixed,with28schemestargetingindividualinvestors,10schemestargetingcorporateinvestorsand8schemestargetingboth.

• Themajorityofschemespermittedtheparticipationofcross-borderinvestorsprovidingtheyhadsufficienttaxliabilitiesinthecountryinquestiontoabsorbthetaxrelief.

Top5taxincentiveprogramsamongEU-28,theU.S.,Canada,Japan,SouthKorea,Turkey,Australia,SwitzerlandandIsrael:1- TheUnitedKingdom’sSeedInvestmentScheme(SEIS)isthehighestrankedtax

incentive.SEISusesacombinationofage,sizeandspecificsectorexclusionstotargetentrepreneurialfirms.Itrestrictstheparticipationofrelatedparties,buthas introducedallowancesforbusinessangels. It targetsnewly issuedordinarysharecapital, imposingamaximuminvestmentvalueattractingtaxreliefandaminimumholdingperiod.

2- TheUnitedKingdom’sEnterpriseInvestmentScheme(EIS)comesinsecondplace.

Theschemeoffersupfronttaxreliefandprovideslossreliefonamorefavorablebasisthanallowedbythebaselinetaxsystem.Ittargetsentrepreneurialfirmsonthe basis of size and excluded sectors, but does not use age targeting. It hasintroducedallowancestorelatedpartyrestrictionstopermittheinvolvementofbusinessangels.

3- France’s “Madelin” tax reduction scheme features third in the ranking. The

schemeoffersanupfronttaxcreditof18%oninvestments,aswellasgrantingreliefforgainsrealizedondisposalofqualifyinginvestment.Theschemerestrictsparticipation through its partial targeting of business size, age and sector. Inaddition, it imposes a minimum holding period of five years and amaximuminvestmentallowancethatiseligibleforrelief.

4- TheUnitedKingdom’sSocialInvestmentTaxRelief(SITR)comesinfourthplace.

Theschemeoffersupfronttaxreliefbutdoesnotprovidelossreliefonamorefavorablebasis thanallowedby thebaseline tax system.AlthoughSITR is verysimilarindesigntoEIS,itsqualifyingcriteriascoredivergesasitspecificallytargets

21 https://ec.europa.eu/taxation_customs/sites/taxation/files/final_report_2017_taxud_venture-capital_business-angels.pdf

22

socialenterprisesanddoesnotcontainallowancestopermittheinvolvementofbusinessangels.

5- Germany’sVentureCapitalGrant(Invest)incentiveisrankedinjointfifthplace.

Theschemeoffersbothindividualandcorporateinvestorsanupfrontreliefintheformofagrantof20%oftheinvestmentsumontheacquisitionofshares.Thereisalsoanexitreliefthatappliestoindividualinvestorsonly.

TheUnitedKingdom’sVentureCapitalTrust(VCT)schemeisalsorankedinjointfifthplace.TheVCTschemeoffersupfrontreliefandreliefongainsforinvestors,aswellastaxtransparenttreatmentofinvestmentreturnsfortheVCTitself.

The Report also selects 10 good practice cases based on novel and promisingapproachesandthediversityofapproaches.Herearetheselected10goodpracticecases:

1- VentureCapitalGrant(Invest)-Germany2- EmploymentandInvestmentIncentiveScheme,Ireland3- TaxTreatmentofCrowdfundingLoans,Belgium4- “Madelin"TaxReductions,France5- AngelTaxSystem,Japan6- VentureCapitalTrust,UnitedKingdom7- SocialInvestmentTaxRelief,UnitedKingdom8- VentureCapitalLimitedPartnershipprogram,Australia9- TaxShelterforInvestmentsinStart-ups,Belgium10- BusinessAngelScheme,Turkey

TheOECDalsopublishedareportaddressingthetaxincentiveprogramsforventureinvesting22.InthisreporttheOECDhighlightsthatcapitalgainstaxisalsoanimportantfactor that shapes the seed and early stage equitymarket as it will influence theinvestmentandexitdecisionsbyangel investorsandventurecapitalists.Despiteaflighttoqualityselectioneffect,highercapitalgainstaxratesreduceboththenumberof VC-backed and successful companies. Beyond the arguments that increasedtaxation reduces the incentives to invest in seed and early stage ventures, capitalgainstaxeshavealsobeenarguedtoworkasabarriertoentrepreneurialactivityandcreationofnewfirms.

22 http://www.oecd.org/officialdocuments/publicdisplaydocumentpdf/?cote=DSTI/IND(2014)5/FINAL&docLanguage=En

23

2. TurkishEntrepreneurshipEcosystem

TurkeyhasatremendouspotentialinentrepreneurshipwithitsyoungandeducatedworkforceaswellasitsstrategiclocationbetweenkeymarketsinEurope,theMiddleEast, Russia andCentralAsia. To understand that potential, here are some recentstatisticsaboutTurkey:

• WithaGDPofaround$860Billion,Turkeyisthe17th-largesteconomyintheworldandthe6thlargesteconomywithinthebroaderEUcommunity.23

• Turkey’spopulationis79,8MillionasofDecember2016andthemedianageis31,4.24

• ThepercentageofInternetusersreached66.8%ofthetotalpopulation.• Themobile industry inTurkeycontinues togrow rapidly,with76.6Million

subscribersasofJune2017,representinga95.9%marketpenetrationrate.• Turkey’s economy grewat an annual average realGDP growth rate of 5.6

percentfrom2003to201625.

Figure12:TopOECDCountriesbyAnnualAverageRealGDPGrowthRate(2003-2016)

R&Dis a crucial component of innovation in knowledge-based economies.AccordingtotheresultsofR&DActivitiesSurvey2016conductedbyTurkStat26,grossdomestic expenditure on research and development surpassed 24.5 Billion TL inTurkeyin2016,anincreaseof19.5%comparedtothepreviousyear.ShareofgrossdomesticexpenditureonresearchanddevelopmentinGDPreached0.94%in2016.Thetotalnumberoffulltimeequivalent(FTE)R&Dpersonnelwas136,953wheretheratiooffemaleR&Dpersonnelwas31.4%.

23 http://pubdocs.worldbank.org/en/254861507539327826/Turkey-Snapshot-Fall2017.pdf 24http://www.turkstat.gov.tr/HbGetirHTML.do?id=21507

25 http://www.keepeek.com/Digital-Asset-Management/oecd/economics/quarterly-national-accounts/volume-2017 26 http://www.turkstat.gov.tr/

24

ThenumberofpatentsgrantedbytheTurkishPatentInstitutewas11,074whereasthenumberofpatentapplicationstotheTurkishPatentInstitutewas16,778in2016.Thenumberofscientificpublicationsin2016was31,555.27

Figure13:NumberofPatentsGrantedinTurkey(2006-2016)

Figure14:NumberofPatentApplicationsinTurkey(2006-2016)

Figure15:NumberofScientificPublicationsinTurkey(2006-2016)

27http://www.tubitak.gov.tr/en/news/rd-activities-survey-2016-results-are-announced

25

Having a quick process to start a new business is very important for startups.AccordingtotheOECD’s“StartingaBusinessRank2018”whereeconomiesarerankedon their ease of doing business, from 1–190, Turkey’s rank is 60 out of 190. 28Compared to the previous year’s ranking of 78, it is clear that there is a positivechangebutstillroomtoimprove.

AccordingtoTheGlobalEntrepreneurshipIndex2018,anannualindexthatmeasuresthehealthoftheentrepreneurshipecosystemsineachof137countries,Turkeyholdstherankof37.29

2.1. VentureInvesting

The Turkish Entrepreneurship Ecosystem is relatively young but it has beendevelopingrapidly.Inthissection,statisticswithregardtoventureinvestingwillbestated.TherecentecosystemmapcanbefoundintheAnnexA.

HerearesomestatisticsabouttheecosystemasofJanuary201830:

• NumberofaccreditedangelinvestorsinTurkey:42831• NumberofBusinessAngelsNetworks:15• NumberofIncubationCentersandAccelerators:41• NumberofEarlyStageVCFirms:29• NumberofPrivateEquity(PE)Firms:7• NumberofR&DCenters:77032• NumberofTechnoparks:5533• NumberofTechnologyTransferOffices:63• NumberofCrowdfundingPlatforms:6• NumberofNGOsthatareactivelyworkinentrepreneurship:18

According toStartupsWatch, the total investmentamount reached$177Million inTurkeyin2017.Figure16showstheventureinvestmentamountsinTurkeybyyearandFigure17showstheventureinvestmentsbystage.

AsitcanbeseenfromFigure17,seedstageinvestmentsdominateventureinvestinginTurkey.Itcanbealsonotedthattheseedstageinvestmentsalmostdoubledin2017comparedto201634.AnotherremarkablenoteisthatSeriesCinvestmentswere$15Millionin2017(TherewerenotanySeriesCinvestmentsin2016).Thisisanindicatorthattheecosystemismaturing.

28http://www.doingbusiness.org/rankings?region=europe-and-central-asia 29https://thegedi.org/2018-global-entrepreneurship-index/30https://startups.watch/ 31https://m.hazine.gov.tr/File/Index?id=E317E3E8-BA94-4D1D-9D55-FB2E20295470 32https://btgm.sanayi.gov.tr/DokumanGetHandler.ashx?dokumanId=407ad0ee-c332-461b-adaa-303396d50ca4 33https://teknopark.sanayi.gov.tr/ 34https://startups.watch/

26

Figure16:VentureInvestmentsinTurkey(2010-2017)

Figure17:VentureInvestmentsbyStageinTurkey(2010-2017)

Asitismentionedbefore,theshareofcorporateinvestmentsisgettinghigheryearbyyearglobally.WhenwelookatthedataforTurkey,weseethatthetrendissimilar.2017wasarecordyearforcorporateinvestmentsinTurkeywithashareof7.6%oftheventureinvesting.

27

Figure18:CVCInvestmentsinTurkey(2010-2017)

Whenwelookatthemostfundedverticals,weseethatFintechtakesthelion’ssharewith18%ofallinvestmentsin2017.

Figure19:MostFundedVerticalsin2017inTurkey

2.1.1. AdditionalRemarks

TheTurkeyTechnologyAcceleratorFunds–ACTVCandDCPVCplayedanimportantrolebothin2016and2017withtheirinvestments.Thetwofunds’contributionstotheventureinvestingaffectedthetotalinvestmentamountsdirectlyinboth2016and2017.

28

Otherhighlightsfrom2016and2017arebelow:

• MediterraCapitalsolddownitsstakeinenterprisesoftwarebusinessLogoYaziliminNovember2016,inthefirstexitaprivateequityfirmhasevermadetotheTurkishpublicmarkets.35

• ArealestateservicescompanyEvtikosecuredatotalof~$18,3Millionin3investmentroundsinJanuary2016,September2016andJune2017.

• TurkishonlinepaymentandfintechcompanyIyzicohassecured$15MillioninSeriesCfunding.VostokEmergingFinanceledtheroundwithparticipationfrom International Finance Corporation, Amadeus Capital Partners andTurkishVentureFund212inJanuary2017.

• PE Firm Turkven and VC Firm Earlybird bought themajority shares of theenterprisesoftwarecompanyMikroYaziliminApril2017.

• OneofthefirstprivateshoppingplatformsMarkafoniwasacquiredbySelectGroupfor$15MillioninJuly2017.

• InJuly2017AmazonannouncedthatitwillentertheTurkishmarket.Thee-commercegiantisexpectedtostartitsoperationsinTurkeyin2018.36

• TheSanFrancisco-basedonlinegamingpioneerZyngaacquiredthemobilecard game copyright from Turkish game companyPeak Gamesfor $100millioninNovember2017.

• Sojern,aSanFranciscobasedcompanyhasacquiredTurkishAdphorus,ad-techcompanyinNovember2017.

• Tasit.comwasacquiredbyGarajsepeti.cominDecember2017.

Thetopacquisitionstodateatorabove$100Mare:1- Yemeksepeti.com2- Gittigidiyor.com3- Markafoni.com4- Pozitron5- PeakGames

Allof theseacquisitionsare importantmilestones for theecosystem for twomainreasons:1- Astudy thatwaspublished inHBRTurkey that found thatNevzatAydin (a co-

founderofYemeksepeti.com),SinaAfra(aco-founderofMarkafoni),andHakanBaş (a co-founder of Lidyana.com) were key role models for young Turkishentrepreneurs.37Eachof theseentrepreneurshadsuccessfulexits.Theseexitshave given courage and inspiration to young entrepreneurs who want to besuccessful. Having successful role models is especially important inentrepreneurship. Moreover, since the acquirers are all outside from Turkey,youngentrepreneursunderstandthatiftheycreatestrongandviablebusinesses,theycanattractattentionfromaglobalaudience.

35 https://realdeals.eu.com/news/2016/11/16/mediterra-completes-first-private-equity-backed-exit-to-turkish-public-markets/ 36 https://www.dailysabah.com/technology/2017/08/31/amazons-website-for-turkey-operations-revealed 37 http://hbrturkiye.com/dergi/saglam-girisim

29

2- Co-foundersofallthesestartupshavebecomeangelinvestorsandmentors.This

isveryimportantforthesustainabilityandfortheimprovementoftheecosystem.

2.2. GovernmentPrograms

ThankstoTheMinistryofScience,IndustryandTechnology,TÜBİTAKandTheSmalland Medium Enterprises Development Organization (KOSGEB); entrepreneurs aresupportedandencouragedinTurkey.Therearedifferentsupportprogramsforthedifferentstagesofstartups.Wecoveredthesesupportprogramsinourreportin2016whichcanbestilldownloadedfromTheTechnologyTransferAccelerator-TTATurkeyWebsite38.Therefore,wewillnotcovertherelatedprogramshereagain.InsteadwewillfocusontheAngelInvestmentTaxIncentivesinceitwasselectedasoneofthegoodpracticesamong46programsinEU-28,theU.S.,Canada,Japan,SouthKorea,Turkey,Australia,SwitzerlandandIsraelbytheEuropeanCommission.

The tax incentive that is provided by the Under secretariat of Treasury for angelinvestors aims to encourage angel investors to invest in early stage startups. Inpractice,theTurkishTreasurylicensesbusinessangelswhowanttobenefitfromtaxincentives for their investments. Accordingly, 75% of the participation shares ofqualifying Turkish resident joint stock companies held by angel investors can bedeductedfromtheangelinvestors’annualincometaxbaseinthecalendaryear.Thatdeduction ratio is applied as 100% for those angel investors investing into thecompanieswhose projects are supportedby theMinistry of Science, Industry andTechnology, TÜBİTAK as well as the Small and Medium Enterprises DevelopmentOrganizationinthelast5years.Thevastmajorityoftheaccreditedangelinvestorssay the incentive program was effective on their decision on becoming an angelinvestor.39

Inthisyear’sreport,itisalsoworthmentioningthatTÜBİTAKisworkingonrevisingits1514VentureCapital SupportProgram.The revisedProgram is supposed tobelaunchedinQ12018.TÜBİTAKhasbeengatheringfeedbackonthedraftversionofthe revised Program fromuniversities, technoparks,NGOs and venture capitalists.TheeffortsofTÜBİTAKtocreateawell-designedandeffectiveProgrambygatheringthefeedbackofrelatedstakeholdersareappreciatedbytheecosystem.Webelievethat the revised Programwill be one of themost important agenda items in theecosystemin2018.

38https://www.ttaturkey.org 39www.treasury.gov.tr

30

2.3. Universities,TechnologyTransferOfficesandTechnoparks

2.3.1. Universities

AccordingtotheCouncilofHigherEducation,thereare185universitiesinTurkeyasof December 2017. Every year, TÜBİTAK announces The Entrepreneurial andInnovativeUniversityIndex.TheaimoftheIndexistoincreaseentrepreneurshipandinnovationorientedcompetitionbetweenuniversities,tomeasuretheperformanceof universities regarding entrepreneurship and innovation, and to contribute thedevelopment of entrepreneurship and innovation indirectly. TÜBİTAK leads theevaluation process and announces the Index every year. Some indicators that areusedinthecalculationsare:

*Numberoffirmsestablishedbyacademicians,*Numberoffirmsestablishedbystudents/graduatedstudents*Employmentinthosefirms*Patents*Licenses*R&Dandinnovationprojects*Entrepreneurship,innovationlessons/trainings

HerearethemostentrepreneurialandinnovativeuniversitiesinTurkeyaccordingtoTheEntrepreneurialandInnovativeUniversityIndex201740:

1. SabancıUniversity2. MiddleEastTechnicalUniversity3. GebzeTechnicalUniversity4. İstanbulTechnicalUniversity5. BoğaziçiUniversity6. İhsanDoğramacıBilkentUniversity7. KoçUniversity8. İzmirHighTechnologyInstitute9. ÖzyeğinUniversity10. YıldızTechnicalUniversity

2.3.2. TechnologyTransferOffices

Technology Transfer Offices (TTO) are quite important since they assist publicresearch organizations inmanaging their intellectual assets in ways that facilitatetheirtransformationintobenefitsforsociety.Therearemorethan60TTOsinTurkeyofwhich34weresupportedbyTÜBİTAKthroughthegrantprogram1513Technology

40 https://www.tubitak.gov.tr/tr/kurumsal/politikalar/icerik-girisimci-ve-yenilikci-universite-endeksi

31

Transfer Support Program and the 1601 Capacity Building for Innovation andEntrepreneurshipGrantProgram.41

The supportamount thatwasgiven fromTÜBİTAK to selectedTTOswasabout20MillionTLin2017,accordingtoastudyontheanalysisoftheTTOsthataresupportedthrough 1513 Technology Transfer Support Program.42Another highlight from thestudyshowsthatmostoftheTTOsstilldonotgenerateenoughrevenuetocovertheiroperationalcosts.ThestudyalsooffersrecommendationsforTTOs’effectivenessthatcanbefoundinthe“TechnologyTransferBookofKnowledgewithTurkishTTOGoodPractices”whichisanothervaluableoutputoftheTTATurkeyProject.TheBookaimstoprovidepractical,relevant,creative,andprovenbestpracticesfromTTOsacrossIPintake processing, technology licensing, supporting startups, access to funding,Industry/Universitycollaborationandmuchmore.TheBookcanbedownloadedfromtheTTATurkeywebsite.

2.3.3. Technoparks

According to Law No: 4691 regarding Technology Development Zones (TDZs), atechnopark hosts high tech based companies (or companies utilizing high tech),enablesthemtobenefit fromaspecifieduniversityortechnology instituteorR&Dcentertodeveloptheirtechnologyand/orsoftwareandtoconverttheirtechnologicalfindings into a commercial product, method or service. They contribute to theeconomicdevelopmentoftheareaandarelocatedinsideornearbythecollaboratinguniversity,technologyinstituteorR&Dcenter, integratingacademic,economicandsocialstructures.43

AccordingtotheTurkishAssociationofTechnologyDevelopmentZones,thereare69technoparksinTurkey,ofwhichof55areinoperationasofDecember2016.Thereare4510companiesthatarelocatedinthesetechnoparks.Ofthese,37%areinthesoftware development sector and 17% are in the communication sector.As of May 2016, a total of 46314 employees were employed in TechnologyDevelopment Zones. The number of R&D projects completed in the TechnologyDevelopmentRegionstodateis23007andthenumberofR&Dprojectscarriedoutin2017was8915.ThenumberofpatentsregisteredbythecompaniesoperatingintheTDZsis640andthenumberofpatentsintheapplicationprocessis1121.44

TheMinistryisevaluatingtheperformancesoftheTDZstodeterminetheirstrengthsand areas that are candidates for improvement. According to the TechnologyDevelopmentZonesPerformanceIndex2016,herearethetop10TDZs:

41https://www.tubitak.gov.tr/tr/destekler/akademik/ulusal-destek-programlari/icerik-1513-teknoloji-transfer-ofisleri-destekleme-programi42http://ttaturkey.org/upload/GoodPractice.pdf 43http://www.ariteknokent.com.tr/en/where/what-is-technopark44http://btgm.sanayi.gov.tr/

32

1. METUTechnopolisTDZ2. İTÜArıTechnopolisTDZ3. AnkaraTDZ(Cyberpark)4. MersinTDZ5. ErciyesUniversityTDZ6. İzmirTDZ7. YildizTechnicalUniversityTDZ8. İstanbulTDZ9. İstanbulUniversityTDZ10. AnkaraUniversityTDZ

2.3.4. WomenEntrepreneurship

Women entrepreneurs play an important role in local economies. Having fewerwomenentrepreneursinacountrymeansthatcountrydoesnotunleashitsfullworkforceandeconomicpotential.Thismeanslessinnovationandlessjobcreation.TheTurkishentrepreneurshipecosystemisgrowingrapidlyandwehavestartedtoseeglobalachievementsinthepastfewyearswithexamplessuchastheYemeksepeti’sacquisitionbyDeliveryHeroorPeakGame’sacquisitionbyZynga.Butwhenitcomestowomeninentrepreneurship,thereismuchroomforimprovement.

AsofDecember2016,49,8%ofthepopulationiswomen.Amongthepopulationaged15yearsandover,thelaborforceparticipationratewas71.6%formalesand31.5%forfemalesasofJanuary2016.

Despitethehugepotential,Turkeyholdsthe131thrankamong144countriesattheWorldEconomicForum’sTheGlobalGenderGap2017Indexwhichwasmentionedintheearliersections.

According to Startups.watch, proportion of women entrepreneurs in the ventureecosysteminTurkeyisaround15%.Moreover,betweenJanuary–September2017only 15% of the venture investment in Turkeywent to startupswith at least onewomanfounder.WhenwelookatthemostactiveVCfirmsinTurkeybasedontheStartupsWatchdata(ACTVC,DCPVC,500Istanbul,TRPE,GrowthCircuit,Earlybird,Revo,ZorluVentures)weseethatjust3ofthem(500Istanbul,TRPE,GrowthCircuit)haveafemalepartner.Efforts to close the gender gap are extremely important not just for theentrepreneurshipecosystembutalsoforsustainableeconomicdevelopment.Clearly,asthestakeholdersoftheecosystem,weneedtoworkonthisveryimportantissuealltogetherbysettinggoals,definingpoliciesandexecutingthem.Recommendationsonthisissuewillbestatedinthenextchapter.

33

3.OutputsandAchievementsoftheTTATurkeyProject

TheoverallobjectivesoftheTTATurkeyProjectistocontributetowardsimprovingthe R&D commercialization capabilities at TTOs and universities, and TÜBİTAK'scapacityoncommercializationofR&D,aswellassupportingbothfundmanagersofTTA Turkey Funds (ACT VC and DCP VC) for their deal sourcing and assessmentactivities.

Table3:TTATurkeyProjectSynopsis

HerearesomehighlightsoftheachievementsoftheProject:StrategyPlanningforTTOs:SelectedTTOswerementoredbyinternationalexpertsfor developing strategy plans after conducting needs assessment study throughsurveysandinterviewsthroughsitevisits.Hands-on (applied) Trainings for Academicians and TTOs: 20 TTOs and 40academiciansweretrainedonLeanStartupMethodology,CustomerDevelopment,Business Model Validation and Growth Marketing through The Venture PipelineDevelopmentProgram.Moreover,15webinarswereorganizedin2yearsonvarioustopics from IP licensing to TTO Strategies. The overwhelming majority of theparticipantsstatedthatthetrainingprogramwasveryhelpful,thattheylearnedalotandthattheywillteachwhattheylearnedtotheircolleaguesandstudents.TTOStaff-ExchangeProgram:TheTTOStaff-ExchangeProgramwasdesignedfor10selectedTTOs.TheseTTOsvisitedtheTTOsinFranceandtheU.S.tolearnfromeachother. Theparticipants from theTTOs stated that theybenefited from theon-sitevisitsandfromworkingwiththeirFrenchandAmericancounterpartstoenhancetheirTTOstrategyandexecution.

BusinessDevelopmentforTTATurkeyFunds(ACTVCandDCPVC):Themainfocusof the business development activities is to facilitate identification of investment

34

ready opportunities for the TTA Turkey Funds, namely ACT and DCP. BusinessDevelopmentLeadershaveworkedwiththeTTOs,technoparks,accelerators,angelinvestornetworksandotherVCFirmsinclosecollaborationwiththeTTATurkeyFundmanagers to identifyandevaluate investment readyopportunities.Hereare somehighlights:

• 66 Technopark & TTO visits (11 TTOs are visited by both Business

DevelopmentLeaders)• 944face-to-facemeetings• 914projectsevaluatedasbeingajurymember• 165startupprojectsmentoring• 40meetingswithACT&DCPintotal• 115dealssharedwithACT&DCPwhichof12gotinvestmentsfromACTand

DCPVC(DDisstillgoingonfor6projects). • ADemoDaywasorganizedforthe11VCFirmswiththeselectedprojectsout

of165projectsthattheymentored.

Moreover,BusinessDevelopmentLeaderscontributedtotheportfoliocompaniesoftheTTATurkeyFundsandtheFundsthemselvesthroughtheirnetworkingeffortsinTurkeyaswellasintheU.S.,especiallySanFrancisco.BusinessDevelopmentLeadersalsotrainedselectedTTOsonVentureInvesting101and Due Diligence Process. Moreover, since Business Development Leaders haveinteractedwith theoverwhelmingmajorityofTTOs inTurkey, theyhavesustainedpartnershipchannelsamongTTOsaswellasotherstakeholders.ProjectVisibilityandPublicity:TheProjectwebsitewascreated(www.ttaturkey.org)withgeneral informationabout theprogram,aswell industrynews,events, andaresourcelibrary.Project visibility activities are carried out through attendingmajor conferences asspeakersandarrangingpressmeetings.SeminarsbyBusinessDevelopmentLeaderson the ‘TTA Turkey Project’ and ‘The Importance of TTOs on TechnologyDevelopment’atmorethan50universitieswerecarriedout.Moreover,TheProjectreceivedmuchpresscoverageincludingcoveragebyForbesUK,DunyaNewspaper,HurriyetNewspaperandWebrazzi.International Conferences were held in 2016 and 2017 for the Project. Eachconferenceattractedmorethan200participantsfromtheecosystemaswellastheparticipationfromtheMinistry,EIFandTUBITAK

35

Publications:

• “Entrepreneurship and Technology Commercialization Report 2016:GlobalTrendsandSpecificLookatTurkey”waspublishedinJanuary2017:http://www.ttaturkey.org/upload/haberler/Entrepreneurship_TechCommReport2016_final(30Jan16).pdf

• “TechnologyTransferBookofKnowledgewithTurkishTTOGoodPractices”waspublishedinNovember2017:http://www.ttaturkey.org/upload/GoodPractice.pdf

• “Entrepreneurship and Technology Commercialization Report 2017:GlobalTrendsandSpecificLookatTurkey”waspublishedinJanuary2018whichcanbealsodownloadedfromtheTTATurkeywebsite.

36

4.ObservationsandRecommendations

Inthischapter,observationsandrecommendationsgleanedfromour2yearswiththeTTA Turkey Project are stated with regard to the Turkish Entrepreneurship andTechnologyTransferEcosystem.Althoughsomeof thesewere stated in last year’sreportaswell,theyarestillrelevantfor2017.Technology Commercialization: BusinessDevelopment Leaders and experts of theTTATurkeyProjectmade66TTOvisitsin2016and2017.Theyhadthechancetoholdoneononemeetingswithacademicians.EventhoughTTOshavedifferentlevelsofexperience,somebroadconclusionsemerged:• Ageneral issuewewitnessedisthatthetechnologicalpartsoftheprojectsare

greatwhereasthebusinessrelatedpartsareweak.Projectownersaregenerallyfromanengineeringorscientificbackgroundandusuallydon’t thinkaboutthebusiness-relatedpartsoftheproject.Moreover,sometechnicalprojectownerstold us that they don’t believe that the business aspects are important.Mostacademiciansdevelop solutionsandwould like to commercialize theirprojectswithoutsearchingfortheneedsortheproblemsoftheindustry.Thetendencyistovaluethetechnologybuttoignorethebusiness.Thismentalityisoneofthemost significant obstacles we found, and it will threaten innovation over asustainedperiodifattitudesdonotchange.

• Most of the TTOs that we visitedmentioned this issue as well and asked forrecommendations. We recommend that TTOs pair MBA students with theacademicianstoworkonprojects.InthismannerMBAstudentscanworkonsomerealprojectsandacademiciansdon’tneedtobotherwiththebusinessaspects.Iftheybothagree that theycanwork togetherand theprojecthaspotential forcommercialization,theycanbecomeco-founders.

• Someacademicianstoldusthatsincetheirmostimportantperformancemetricis

thenumberofpapersthattheypublish,theyfocusonthatanddon’tthinkaboutthecommercializationoftheirtechnologyprojects.Someindicatorsrelatedwithentrepreneurship and/or technology commercialization can be integrated intoperformance criteria of academicians to motivate academicians to put moreemphasisoncommercialization.

• ThankstoTÜBİTAK,therearemanysupportprogramsforacademicianstofund

thebasicresearchaswellasappliedresearchprojects.Likewise,techacceleratorfundslikeTTATurkeyFunds-ACTVCandDCPVCaregreatopportunitiesforIPbasedtechprojects.Butitseemsthatthereisalsoaneedtosetupamaturationfinancing mechanism which will allow first to improve the TRL level of theinventionstomakethemacceptabletoindustries,andsecondtodevelopallthecommercialization and legal studies which are necessary to transform an

37

inventioninaproductoraprocess.ThisfundmaybemanagedbyTTOsandbeusedfortheresearchprojectsthathavegreatpotentialforcommercialization.BybearinginmindthattherearenotmanyskilledTTOstaff;sometrainingprogramsforthepersonnelwhowillmanagethefundaswellastheperformanceevaluationcriteriashouldbedesigned.

SpecializedAccelerationProgramwhichistobeappliedbynumberofTTOswithacentralizedmonitoringsystembyTÜBİTAKmay increase thesuccessof technologycommercializationefforts.Theaccelerationprogramshouldaimforbusinessmodelvalidationthroughahighlevelofcustomerengagement.ItwouldbemorebeneficialtoorganizethematicaccelerationprogramswhichincreasethespecializationofTTOs.TTOStaffandSkillSets:DuringtheTTOvisits,wehadachancetoseetheTTOsonsiteandmeetthestaff.Althoughthestaffisworkingheartily,mostoftheTTOsdon’thavefullyskilledandexperiencedpeoplewhoworkontechnologycommercialization.SomeTTOstoldustheyneedtemplatestofollowfortechnologycommercializationbutsincethereisno“onesizefitsall”approachonthatmatter;theyneedtotailorthecurrent strategies toexecute them. Inorder todo this,TTOsneed tobegin todevelopbroaderskillsetsandpromoteprofessionaldevelopmentopportunities.MostoftheTTOstaffasmentionedearlierarenotexperiencedenoughintechnologytransfernorhaveindustryexperienceeither.Itisneededtoplacemoreemphasisandeffortonrelationshipbuildingwiththeobjectiveofbuildingmorecapacity.ToruntheModules,3,4&5efficiently,theymayneedahighcalibersteeringcommitteefromwithintheindustry.Thiscommitteecansupporttheuniversity–industryrelationship,effectivelyengagetheregionalecosystemandprovideinsightsaboutwhichresearchprojectsshouldbepulledintocommercialization.Endorsement of the UniversityManagement is Decisive: The TTOs are the maininterface between the university and the outside world. Their role is crucial forrelationshipbuildingamongacademia,industryandgovernment,andforsuccessfultechnologytransferandcommercialization.Manyoftheuniversitymanagementareprimarily focused on the revenue generation potential of technology transferoperationsandlessonthesocietalbenefitsoreconomicengagement.TTOscannotoperate effectively if the universitymanagement does not endorse, communicatetheirroleandappreciatethem.Collaboration Among TTOs is Necessary: Since Business Development LeadersinteractedwithalmosteveryTTOs inTurkey,theynoticedthatcooperationamongTTOsshouldbefostered.OneofthecontributionsoftheTTAProjectwassustainingpartnerchannelsamongTTOsandcatalyzingcooperationamongthedifferentTTOs.WealsoreceivedfeedbackfromTTOManagersthatthetrainingandeventsthatwereheldunderTTATurkeyProjectweregreatchancesfortomeetcounterpartsandshareexperiences. There is a clear need for platforms and perhaps periodic events thatenableTTOTeamstogettogether,learnfromeachotherandembarkonmeaningfulcooperation.

38

ForreasonofexpertisethequestiontosetupcommonservicesforTTOsmightbeconsidered.Itisclearthatsometechnicaltools,softwareandservices,likeadvancedmarket research or IP cartography are not accessible to a sole TTO and commonservicesshouldbeenvisaged.CommonservicesmightenlargehavingacommonIPportfoliosinceIPportfoliosofsomeindividualTTOsaresmallandhavingacommonportfoliowouldbringcollaborationandallowfasterscaling.AcommonIPportfoliowouldalsoincreaseopeninnovationsystems.CorporationsShouldContributeMoretotheEcosystem:Neithertheacquisitionofstartups nor collaboration with startups and academicians is common amongcorporationsinTurkey.CorporationsshouldcontributemoretotheentrepreneurialecosystemthroughpartnershipswithstartupsandacademiciansaswellasthroughM&A activities. The efforts of corporations through sponsorship of events ororganizinghackathonsareappreciatedbuttheyshouldhavestructuredprogramsanddedicatedteamsforcollaborationwithstartupsandacademiciansinordertocreaterealvalueandmeaningfulresults.MetricsMatter:Performance of the incubation centers and accelerator programsshould be measured and transparent. As stated before an incubator and anacceleratoraredifferentstructuresandthereforetheirmetricsshouldbedifferent.Anincubatorcouldbeevaluatedforthenumberofnewbusinessesthatstart.TheU.S.SmallBusinessAdministration states theperformancemetricsof anacceleratorasbelows45(thesetypeofmetricsshouldbeevaluatedforTurkey):

Table4:PerformanceMetricsofAccelerators

ImportanceofAngelInvestors:Thereare428accreditedangelinvestorsinTurkeyasofNovember2017.Itisestimatedthatthereare150activeangelinvestorsinTurkeywhohaveinvestedinatleast1startup.Thismeanstherearearound280silentangelinvestors.Sincethenumberofsilentangelinvestorsishigh,findingthereasonsthat

45https://www.sba.gov/sites/default/files/rs425-Innovation-Accelerators-Report-FINAL.pdf

39

liebehindtheirinactivityisaworthyeffort.Anin-depthstudy,alongwithinvestmentforumsandtrainingscanbeconductedtoincreaseangelactivityinTurkey.Women Entrepreneurship: The participation of women in entrepreneurialecosystemsisaglobal issue.Copingwiththeobstaclesthatsetbackwomenisnotjustcrucialforwomenbutalsoforthesakeofbroadereconomicdevelopmentwithincountries. Inthisregard,Turkeyshouldtakeactiontoovercometheobstaclesthatpreventmorewomenfrombecomingentrepreneurs.Oneoftheseactionscouldbeto appreciatewomen entrepreneurs and outstanding female academicians and tomake themmorevisible. Youngwomenneed to seewomen rolemodelswhowillinspire and motivate them to achieve more. In this regard, it is important forsuccessfulwomenasrolemodelstohelptheyounggeneration.AsMagdalenaYesilwhoisafounder,anentrepreneur,andaventurecapitalisttomanyoftheworld’stoptechnologycompaniesincludingSalesforcestatesinherbook“PowerUp:HowSmartWomenWinintheNewEconomy”;“Itistimethatwomenwhohavebeensuccessfulstepupandexplicitly,publiclysupportthenextgenerationmakingtheirwayinthistoughfield”.46 Moreover,VCfirmsshouldemployeemorewomen.Webelievethatthiswillnotonlyincrease the women in venture investing but also the number of funded femaleentrepreneurs.Thisveryimportantsubjectdeservesmoreattention,effortandworktohaveabetterunderstandingandtofindbettersolutions.

46Magdalena Yesil, Power Up: How Smart Women Win in the New Economy (Seal Press, 2017)

40

Appendix:TurkishStartupEcosystemMap