equity & commodity markets brief reports/q2 2011...the appropriateness of any investment...

TRANSCRIPT

Equity & Commodity Markets Brief

• United States• Europe• Japan• India• China• Commodities

RISK GUIDED RETURN

Q2 / 2011

DISCLAIMER: The appropriateness of any investment strategy must be considered in relation to an investor’s own objectives and risk tolerance. The contents of this report are general in nature and for informativepurposes only. This report has not been prepared with regard to the specific objectives and circumstances of the receiver. Hayat Invest recommends that an investor independently evaluate particular investments andstrategies in consultation with a financial advisor. Past performance is not necessarily a guide to future performance and estimates of future performance are based on assumptions that may not be realized. We areunder no obligation to tell you when opinions or information in this report have changed. Every effort is made to use reliable, comprehensive information, but we do not represent that it is accurate or complete. HayatInvest may make investment decisions or take proprietary positions that are inconsistent with the recommendations or views in this report.

Overview: Equity Markets Outlook

RISK GUIDED RETURN

Market Outlook Remarks

Developed Markets

United States (US) Positive Signs of recovery. Improving conditions in labor market. Housing remains sluggish.

Japan Neutral Muted domestic growth, exports impacted by massive earthquake

United Kingdom (UK) Neutral Fragile Recovery, Strained Financial Services sector

Australia Neutral Tactically short in near term, positive long term

Europe ex-UK Neutral Slow recovery in 2010, Greece and other Sovereign risks remain a concern

Others:

Singapore Neutral Medium term positive, high exposure to global economy

South Korea Positive Reasonable valuations, high exposure to global economy

Emerging Markets

China Positive Domestic Economy

India Positive Domestic Economy

Others:

Thailand Positive Political risks under control. Underlying fundamentals remain robust.

Fiscal Balances Fiscal positionFiscal deficits started to decline across all country income groups in 2010, mostly due to an improved macroeconomic environment. In 2011, fiscal plans appear to be diverging significantly across advanced economies, partly reflecting differences in intensity of market pressure.

Advanced Economies• Most advanced economies are reducing fiscal deficits this year.• United States has put adjustment on hold.• Fiscal adjustment had been postponed in Japan to a large extent (even before the recent

earthquake, which will involve additional fiscal costs).

Emerging Economies• The fiscal outlook for emerging economies is more favorable, but this reflects in part the tailwinds

of high asset and commodity prices, low interest rates, and strong capital inflows; their reversal could leave fiscal positions exposed in many cases.

• Moreover, some of these economies may be gradually overheating.

RISK GUIDED RETURN

Source: IMF Fiscal Monitor, April 2011

United States

RISK GUIDED RETURN

Inflation expectations in the U.S. are increasing modestly, but the weakness of the labor market makes a dangerous acceleration unlikely.

Research by the International Monetary Fund and data published by the Federal Reserve Bank of New York also suggest almost no chance of wages increasing sharply.

"Given the state of the American labour market, there is very little upward wage pressure, and therefore very little risk of a wage-price inflation spiral.“ - The Economist/Free Exchange blog (April 2011)

United States Labor Market

RISK GUIDED RETURN

Both the economy and labor market appear to be improving.

There is general consensus that this trend will continue, helped to an extent by a continuation of accommodative monetary policy by the Fed.

Over the three months ended March 2011, nonfarm payroll gains averaged (a decent) 159,000 per month. Excluding temporary census hires, this is the fastest pace since the three months ending March 2007.

For the same three month period, the population-adjusted Household Survey has shown 1.130 million in job creation compared to 0.478 million in the Establishment Survey. Gains in household employment are expected to continue to outstrip projected gains in nonfarm payrolls. Source: Deutsche Bank US Economics Weekly

Europe

RISK GUIDED RETURN

Available indicators suggest that euro-area GDP growth in 1Q was stronger (around 0.7% QoQ) than the market consensus expectation.

Growth in the remainder of 2011 and in 2012 is expected to average only around 0.3% QoQ, due to headwinds from tighter fiscal policy, ongoing private balance sheet repair, the stronger EUR and increasing interest rates.

Inflation in the Eurozone is forecasted at 2.9% for 2011 and slowing down to 2.2% in 2012.

Further rate hikes are expected in 2011 and 2012, bringing interest rates to a more neutral level. Rates are expected to be around 2.25% by mid 2012, probably leading to real interest rates of around zero.

Source: Citigroup European Economic Forecasts

Europe

RISK GUIDED RETURN

Sovereign yields remain high in some euro area countries.

The market reaction to the successful first bond placement of the European Financial Stability Facility (EFSF)—€5 billion in late January 2011—and the announcement of steps to strengthen the crisis management tools was moderately positive.

However, market conditions remain tense in several smaller countries, in part due to ongoing concerns about possible feedback between the financial sector and the sovereign.

Thus, following a short respite, yields increased since end-January 2011 while at the same time, CDS spreads stayed close to historical peaks. Within Europe, investors are increasingly discriminating in favor of countries with credible policy frameworks.

Source: IMF Fiscal Monitor, April 2011

Europe

RISK GUIDED RETURN

Source: UBS Investment Research

Relative sizes of the different Euro Area countries

Germany is the largest with 27%. Spain, Greece, Portugal and Ireland combined reach only 18% of Euro Area GDP

Europe

RISK GUIDED RETURN

Poor general state of government finances and hard hit countries such as Greece, Spain, Portugal and Ireland are key concerns in the medium term. This may also put pressure on currency to depreciate.

Given the growth differential between developed and emerging economies next year the sensitivity of European exporters to EM growth will rise strongly again next year making the European market even more sensitive to global growth beta.

The UK economy is in the early stages of a cyclical upturn, the duration and magnitude of which remains highly uncertain.

There is a potential for GBP depreciation over the medium term (6 to 12 months). The primary negative for the GBP is tighter fiscal policy. Over the short to medium term, tighter fiscal policies tend to weaken economic activity, keep rates low for a longer duration and therefore have a negative effect on the currency.

Possible Risks

Japan Aftermath of the Earthquake

RISK GUIDED RETURN

Japanese economic data has gradually begun to reflect the true impact of the massive earthquake that struck the country on March 11.

Consumer confidence numbers showed the biggest drop on record while business surveys, such as the monthly Reuters Tankan and the PMI, have seen a similar decline.

The economy appeared to be picking up momentum well into early March when the earthquake occurred. Machine orders, industrial production, and service sector output all showed solid readings for February.

The government estimates the direct damage at ¥16-25trn, but the really serious economic impact will come from the secondary impacts, i.e. slowdown as a result of power shortages.

The yen hit a record high of ¥76.25/$ on speculation that Japanese insurance companies would repatriate foreign assets in the aftermath of the Great Eastern Japan Earthquake that struck on March 11.

Japan

RISK GUIDED RETURN

Overview of the devastation caused by the Great Eastern Japan Earthquake and the Great Hanshin Earthquake

Source: Mitsubishi UFJ Morgan Stanley, Asia Research Monthly, April

Japan

RISK GUIDED RETURN

Japan's trade balance: deficits possible from March 2011

Source: Mitsubishi UFJ Morgan Stanley, Asia Research Monthly, April

Imports continued to accelerate from 11.9% y-o-y in March from 10% the previous month. This was due to higher crude prices and surging car, iron, steel, and coal imports. Given that reconstruction activity is gearing up, this trend can be expected to continue for the foreseeable future.

As a result, the trade surplus, which narrowed sharply to JPY 96bn to JPY 556bn in March, may turn into a deficit in April and May, if not beyond.

Exports fell 2.2% over the year, compared to a 9% y-o-y rise in February, reflecting primarily productionoutages as well as transportation disruptions. Especially hard-hit were exports of cars (-21% y-o-y), Similarly, semiconductor exports still managed a 3% annual rise, but this masks disruptions in certain sub-categories.

India Corruption

RISK GUIDED RETURN

• Corruption

Recent wave of corruption scandals in India

July 2010 Alleged embezzlement of funds related to Delhi’s hosting the Commonwealth gamesNovember 2010 2G spectrum scandal (approx USD 40 billion)November 2010 Adarsh Housing Society (allegations that apartments in Mumbai intended for war widows were in

fact given to civil servants)March 2011 The head of the country's anti-corruption watchdog was forced to resign by the Supreme Court on

the grounds that he himself faced corruption charges.

• Scams are not a new phenomenonWebsite www.ekakizunj.com aims to catalogue scams in India and lists a number of scams going back to 1947 (the first year of independent India).

• Corruption is increasingly highlighted by the media and vocal activist groups - proof that the general attitude to corruption is slowly changing.

• New legislation being passed (RTI, Lokpal Bill)Campaigner Anna Hazare’s calls for an effective anti corruption bill in April 2011, found tremendous support with the general public. Under pressure to act, the government agreed to form a panel to draft a stronger law.

India Inflation

RISK GUIDED RETURN

Inflation in India appears entrenched due to pressure from both the demand side (from a growing, highly aspirational population) as well as the supply side (due to bad policies, infrastructure bottlenecks etc.)

Rising high inflation is not just due to rising cost of fuel and food products. For eg. For two months in a row, February and March 2011, core manufacturing non-food inflation was up 1.4% month-on-month. Textiles as a group saw prices rise by 2.5% in February over January and by a further 4.6% in March over February. Other product groups such as Rubbers, plastics and Chemicals also rose albeit more moderately.

Tackling demand side inflation is relatively easier than tackling supply side inflation (through the use of monetary policy). There is a growing consensus in India that more needs to be done to ease supply side constraints. However, tackling the supply side is largely policy based, more difficult to implement and requires a longer time frame to be effective.

India Expectations

• Inflation / Upward pressure: Oil prices are likely to remain elevated for the foreseeable future, resulting in rising inflation.

• Inflation / Downward pressure: Food production (based on expected production of cereals, a strong winter crop and the expectation of a good monsoon) is expected to reduce pressure from food inflation. This however, may be cancelled out by more food programs implemented by Indian states.

• Rate rises expected to continue: The general market view is for the RBI to hike rates by 100 basis points over the remainder of 2011.

• The central bank has already raised key rates eight times since March 2010 but these increases have proved only partially successful in taming high inflationary pressures.

India's headline inflation in March went up to nearly 9%, far above forecasts, due to higher fuel and manufacturing prices, adding pressure on the central bank to take bolder action.

RISK GUIDED RETURN

China Economy

RISK GUIDED RETURN

China’s economy continues to grow robustly.

Q1 GDP was up by 9.7% YoY – only marginally lower than the 9.8% gain seen in Q4 2010; March industrial production was up by almost 15% YoY ; last month’s nationwide electricity output (a useful cross-check) was up by a similar magnitude

The monthly manufacturing PMI surveys were reasonably robust in March, while the Hong Kong PMI survey’s “new business from China” component was the strongest since November 2010 (this indicator is always worth watching, especially as it turned sharply downwards ahead of China’s PMIs during 2008, thereby giving early warning of an impending hard landing).

China’s property price inflation – according to the recently-discarded nationwide house price index – slowed from a peak of 12.8% last April to 6.4% last December. The major city data ( eg. Beijing and Shanghai) published since suggests that property price momentum has kept waning. And upward pressure on wages is likely to be offset by higher productivity.

The main driver of higher inflation remains food prices, up by over 10% YoY in recent months. Ominously, though, non-food inflation has also been edging up, and stood at 2.7% YoY in March 2011.

Source: Evolution Securities, Macro Research, Economics

KoreaOur View:

Korea continues to look attractive over the medium to long term: Korean companies are well positioned to benefit from any pickup in global

capacity investments (CAPEX cycle). Sectors we favor are industrials, major constructors, ship builders and transportation companies.

Fiscal and monetary policies are not expected to turn very aggressive on tightening and should remain supportive of the market for the foreseeable future.

Korean companies have high earnings retention and investment ratios. On average, they retain close to 80% of their earnings and spend on capacity expansion. This compares with less than 50% for other emerging markets companies on average.

Among Korean companies, the tech sector has the highest retention ratio which implies higher reinvestment and faster future growth rates as well as higher multiples.

The Korean technology sector may also continue to outperform, because it is more dependent on Chinese consumers than on Chinese capital spending.

RISK GUIDED RETURN

ThailandOur View:

• Immediate political tensions have subsided and the political situation in Thailand appears largely stable. However, the possibility of fresh demonstrations or a sudden flaring up of tensions cannot be ruled out since the underlying issues that led to the violence over the past few months remain unresolved.

• The Thai economy remained resilient throughout protests, with Thai companies delivering relatively strong earnings results. We see this trend continuing going forward.

• Greater government spending is expected especially in the rural areas of the North and North-East. This will boost economic activity and in turn is likely to have a positive effect on the current administration’s popularity, particularly in more upcountry, pro-red regions. The largest beneficiaries are likely to be banks, contractors and retailers.

RISK GUIDED RETURN

Australia

RISK GUIDED RETURN

Our View:

• The Australian economy, fuelled by the mining boom, should grow robustly in 2011 and 2012 at a rate of between 3½ and 4% (OECD Estimates)

• Being largely a commodity player, the market is though exposed to news citing a weak global recovery especially any disappointing macro data from U.S, mounting debt in Europe and inflation concerns in the emerging economies like China and India.

• APEC plus India accounts for 85% of Australia’s exports. China and Japan are the largest while Europe accounts for 7%. High economic growth in India and China to ensure sustainability of growth for Australian Economy.

• Morgan Stanley expects 2011 index target of 5,350 implies around 15% price return from current levels

• Current multiples are below long term averages (12.6x) that should be re- rated to at least long term averages (14.5x) by December 2011 driven by low inflation and a reasonable domestic demand and regional outlook (Morgan Stanley estimates).

Commodities

RISK GUIDED RETURN

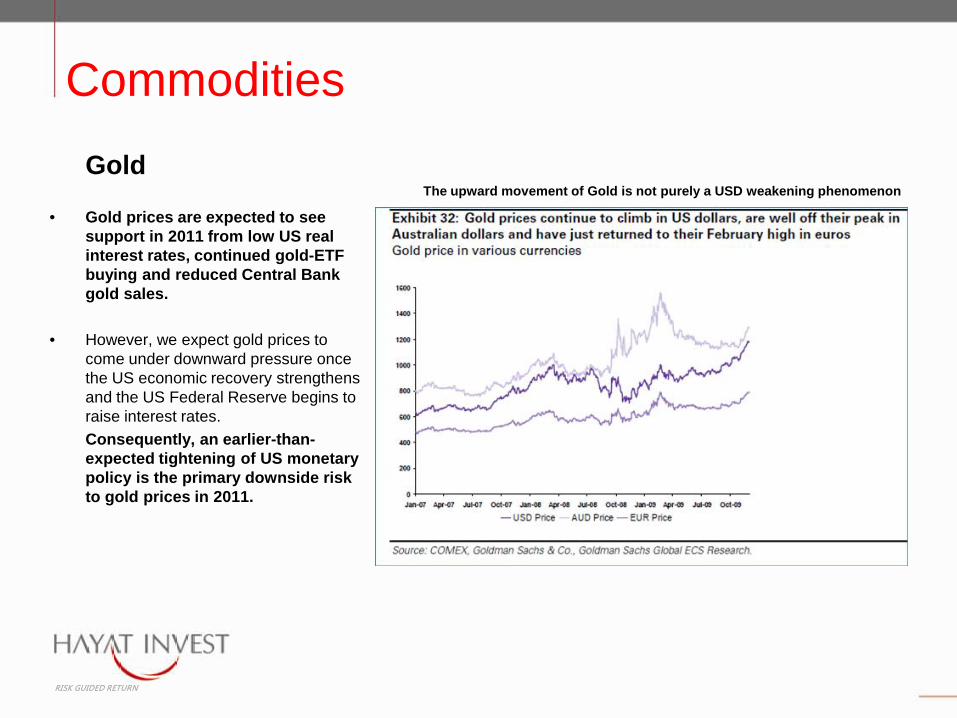

Gold

• Gold prices are expected to see support in 2011 from low US real interest rates, continued gold-ETF buying and reduced Central Bank gold sales.

• However, we expect gold prices to come under downward pressure once the US economic recovery strengthens and the US Federal Reserve begins to raise interest rates. Consequently, an earlier-than-expected tightening of US monetary policy is the primary downside risk to gold prices in 2011.

The upward movement of Gold is not purely a USD weakening phenomenon

Commodities

RISK GUIDED RETURN

Our View:

• Emerging markets will continue to drive demand. Growth in emerging markets has not stalled and the impact of global recession is fading away.

• Outlook for Chinese demand remains especially robust.• Developed countries that have lagged in the recovery, may see industrial production

take off in 2011.• Withdrawal of stimulus will affect the developing world less. • Long term, the demand supply dynamic remains supportive for commodities.• Commodities have become a recognized asset class and investment demand looks

set to continue as investors look for asset classes that offer possible hedges against inflation.

• Structural supply constraints in certain commodities (especially base metals) are likely to support prices.

RISK GUIDED RETURN

EVER EAGER TO SERVE YOU

RISK GUIDED RETURN