· pdf fileequity research│june 1, 2016 asia pacific daily - 1 june 2016. equity research...

TRANSCRIPT

Equity research│June 1, 2016

Asia Pacific Daily - 1 June 2016

Equity Research Reports…

▌IDEA OF THE DAY | China/Hong Kong Strategy Note - The rationale behind continuous southbound inflow | P2 We have noticed continuous southbound inflow to H-shares via Stock Connect. We see three rationales behind the inflow: 1) incentive to position offshore assets to hedge currency risk, 2) attractive valuation and 3) anticipation of SZ-HK Connect. We maintain our positive market view on continuous southbound flow and a correction of previous overly-bearish sentiment. The southbound flow favors 1) HSBC, 2) large SOEs such as Chinese banks and China Mobile and 3) Tencent. ——————————————————————————————————————————————————————————————————————————————————————— ▌REGIONAL / ASEAN / APAC Plantations (NEUTRAL) - Malaysia raises biodiesel mandates | P3 ——————————————————————————————————————————————————————————————————————————————————————— ▌China/Hong Kong Environmental (OVERWEIGHT) - Minimum utilisation hours set for renewables | P4 ——————————————————————————————————————————————————————————————————————————————————————— ▌India Mphasis (HOLD, tp:Rs500.00▲) - Improving growth outlook priced in | P5 Tata Motors (REDUCE, tp:Rs340.00▲) - Short-term relief in 4QFY16 | P6 ——————————————————————————————————————————————————————————————————————————————————————— ▌Indonesia Strategy Note - CIMB Portfolio Tracker – May 2016 | P7 ——————————————————————————————————————————————————————————————————————————————————————— ▌South Korea Hyundai Mipo Dockyard (ADD, tp:W140,000.00) - STX windfall – full consolidation ahead | P8 Kolon Industries (ADD, tp:W83,000.00) - Asia NDR feedback: All eyes on CPI | P9 ——————————————————————————————————————————————————————————————————————————————————————— ▌Malaysia 7-Eleven Malaysia Holdings Berhad (HOLD, tp:RM1.44) - Growth priced in | P10 Asia File Corporation (ADD▲, tp:RM5.14) - 4QFY16 results: Profit margin expansion | P11 Astro Malaysia (ADD, tp:RM3.36) - A good start to the year | P12 AWC Berhad (ADD, tp:RM1.13) - Plumbing TRX | P13 Malaysian Resources Corp (ADD, tp:RM1.32▼) - A toned-down quarter | P14 Media Chinese Int'l (REDUCE, tp:RM0.64) - In need of new growth drivers | P15 Muhibbah Engineering (ADD, tp:RM2.96▼) - More than meets the eye | P16 QL Resources (ADD, tp:RM5.05) - Growing but underwhelmed expectations | P17 SBC Corp (ADD, tp:RM1.20▼) - 4QFY16 results: No approvals yet for JQ | P18 Banks (OVERWEIGHT) - Apr 16 tracker – still holding tight to asset quality | P19 ——————————————————————————————————————————————————————————————————————————————————————— ▌Philippines Philippine Long Distance Tel (HOLD, tp:PHP1,832.00) - Splitting the spectrum | P20 ——————————————————————————————————————————————————————————————————————————————————————— ▌Singapore Cache Logistics Trust (HOLD, tp:S$0.94) - Caught in a cauldron | P21 Sembcorp Industries (ADD, tp:S$3.10) - Europe NDR – scenario planning for marine | P22 ——————————————————————————————————————————————————————————————————————————————————————— ▌Taiwan First Financial (ADD▲, tp:NT$18.50▲) - Better off | P23 Technology - Overall (NEUTRAL) - Computex 2016 snapshot | P24 ——————————————————————————————————————————————————————————————————————————————————————— ▌Thailand Bangkok Chain Hospital (HOLD▲, tp:THB11.20▲) - 1st price hike after two years | P25

Showcasing CIMB Research Ideas

IND: Mitra Keluarga Karyasehat 30/05 A healthy prognosis >PDF

———————————————————————————————————————————————————————————————————————————————————

IND: Strategy Note 27/05 How to position if tax amnesty is passed..>PDF

———————————————————————————————————————————————————————————————————————————————————

TW: Test & Assembly 26/05 The curtain drops but a window opens..>PDF

———————————————————————————————————————————————————————————————————————————————————

TW: Semiconductor 25/05 Recovery likely a moderate one, but the..>PDF

———————————————————————————————————————————————————————————————————————————————————

SIN: Cityneon Holdings 24/05 The era of superheroes >PDF

Regional Equity Research Contacts

Kenneth NG, CFA Head of Research T: (65) 6210 8610 E: [email protected]

———————————————————————————————————————————————————————————————————————————————————

Show Style "View Doc Map"

CIMB Conference / Events |

CIMB Malaysia Consumer Corporate Day 01 June 2016, Malaysia, Kuala Lumpur

———————————————————————————————————————————————————————————————————————————————————

CIMB 10th Annual Indonesia Conference 08-12 August 2016, Bali

———————————————————————————————————————————————————————————————————————————————————

IMPORTANT DISCLOSURES, INCLUDING ANY REQUIRED RESEARCH CERTIFICATIONS, ARE PROVIDED AT THE END OF THIS REPORT. IF THIS REPORT IS DISTRIBUTED IN THE UNITED STATES IT IS DISTRIBUTED BY CIMB SECURITIES (USA), INC. AND IS CONSIDERED THIRD-PARTY AFFILIATED RESEARCH.

Powered by the EFA Platform

China, Hong Kong│Equity research│May 31, 2016

Strategy Note

IMPORTANT DISCLOSURES, INCLUDING ANY REQUIRED RESEARCH CERTIFICATIONS, ARE PROVIDED AT THE END OF THIS REPORT. IF THIS REPORT IS DISTRIBUTED IN THE UNITED STATES IT IS DISTRIBUTED BY CIMB SECURITIES (USA), INC. AND IS CONSIDERED THIRD-PARTY AFFILIATED RESEARCH.

Powered by the EFA Platform

China, Hong Kong Strategy The rationale behind continuous southbound inflow

We have noticed continuous southbound inflow to H-shares via Stock Connect. ■ We see three rationales behind the inflow: 1) incentive to position offshore assets to ■hedge currency risk, 2) attractive valuation and 3) anticipation of SZ-HK Connect.

We maintain our positive market view on continuous southbound flow and a ■correction of previous overly-bearish sentiment.

The southbound flow favors 1) HSBC, 2) large SOEs such as Chinese banks and ■China Mobile and 3) Tencent.

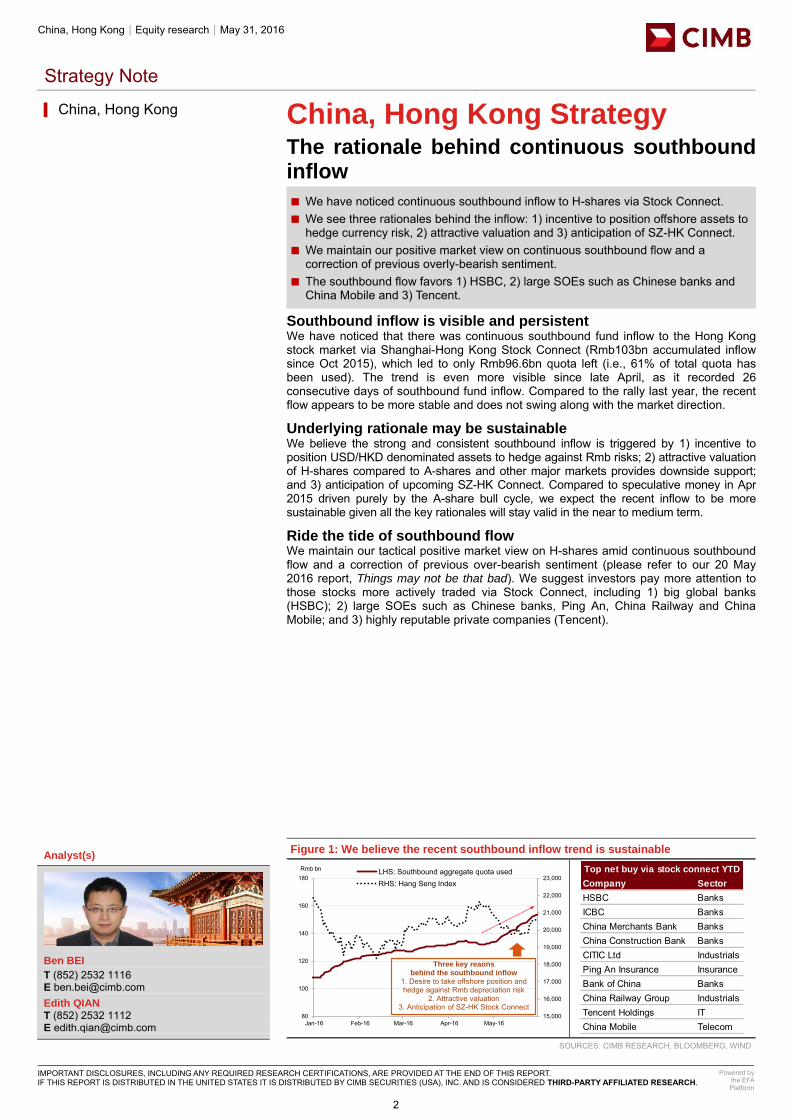

Southbound inflow is visible and persistent We have noticed that there was continuous southbound fund inflow to the Hong Kong stock market via Shanghai-Hong Kong Stock Connect (Rmb103bn accumulated inflow since Oct 2015), which led to only Rmb96.6bn quota left (i.e., 61% of total quota has been used). The trend is even more visible since late April, as it recorded 26 consecutive days of southbound fund inflow. Compared to the rally last year, the recent flow appears to be more stable and does not swing along with the market direction.

Underlying rationale may be sustainable We believe the strong and consistent southbound inflow is triggered by 1) incentive to position USD/HKD denominated assets to hedge against Rmb risks; 2) attractive valuation of H-shares compared to A-shares and other major markets provides downside support; and 3) anticipation of upcoming SZ-HK Connect. Compared to speculative money in Apr 2015 driven purely by the A-share bull cycle, we expect the recent inflow to be more sustainable given all the key rationales will stay valid in the near to medium term.

Ride the tide of southbound flow We maintain our tactical positive market view on H-shares amid continuous southbound flow and a correction of previous over-bearish sentiment (please refer to our 20 May 2016 report, Things may not be that bad). We suggest investors pay more attention to those stocks more actively traded via Stock Connect, including 1) big global banks (HSBC); 2) large SOEs such as Chinese banks, Ping An, China Railway and China Mobile; and 3) highly reputable private companies (Tencent).

[ X ]

Figure 1: We believe the recent southbound inflow trend is sustainable

SOURCES: CIMB RESEARCH, BLOOMBERG, WIND

▎China, Hong Kong

Analyst(s)

Ben BEI

T (852) 2532 1116 E [email protected] Edith QIAN T (852) 2532 1112 E [email protected]

15,000

16,000

17,000

18,000

19,000

20,000

21,000

22,000

23,000

80

100

120

140

160

180

Jan-16 Feb-16 Mar-16 Apr-16 May-16

Rmb bn LHS: Southbound aggregate quota usedRHS: Hang Seng Index

Three key reaons behind the southbound inflow

1. Desire to take offshore position and hedge against Rmb depreciation risk

2. Attractive valuation 3. Anticipation of SZ-HK Stock Connect

Company Sector

HSBC BanksICBC BanksChina Merchants Bank BanksChina Construction Bank BanksCITIC Ltd IndustrialsPing An Insurance InsuranceBank of China BanksChina Railway Group IndustrialsTencent Holdings ITChina Mobile Telecom

Top net buy via stock connect YTD

2

Commodities│ASEAN│Equity research

Sector Flash Note

IMPORTANT DISCLOSURES, INCLUDING ANY REQUIRED RESEARCH CERTIFICATIONS, ARE PROVIDED AT THE END OF THIS REPORT. IF THIS REPORT IS DISTRIBUTED IN THE UNITED STATES IT IS DISTRIBUTED BY CIMB SECURITIES (USA), INC. AND IS CONSIDERED THIRD-PARTY AFFILIATED RESEARCH.

Powered by the EFA Platform

Plantations Malaysia raises biodiesel mandates

Malaysia has agreed to raise the biodiesel blend for the transport sector to B10 and ■implement B7 in the industrial sector progressively, starting 1 Jun 2016.

The government estimates that this will raise biodiesel consumption to 709k tonnes. ■ This is mildly positive for regional planters and Malaysian biodiesel producers. ■Maintain Neutral and an average CPO price of RM2,450 per tonne for 2016.

Malaysia agrees to B10 for transport and B7 for industrial sector ● The Government of Malaysia has agreed to strengthen the biodiesel programme by

increasing the blend for the transport sector to B10 (blend of 10% palm methyl ester with 90% petroleum diesel) and implementing the B7 programme (blend of 7% palm methyl ester with 93% petroleum diesel) in the industrial sector (commercial and power generation sectors).

All diesel sold at retail pumps will be B10 starting Jun 2016 ● The government has revealed that both programmes will be implemented

progressively beginning in Jun 2016. All diesel sold at the retail pumps nationwide will be B10 effective Jun 2016. The B7 programme will be introduced for the first time in the industrial sector. However, it is not clear from the statement if B7 will be implemented fully or progressively starting 1 Jun 2016.

This will raise biodiesel consumption to 709,000 tonnes per annum ● The implementation of B10 for the transport sector and B7 for the industrial sector is

expected to contribute to annual consumption of 709,000 tonnes of biodiesel in Malaysia and lead to savings of 820m litres of diesel as well as 2.16m tonnes of carbon dioxide equivalent annually.

Stakeholders have been consulted on the higher biodiesel blend ● The government has conducted a series of stakeholders’ engagement with transport

sector representatives, petroleum companies and biodiesel producers on its plans to raise the biodiesel blend. In addition, the Federation of Malaysian Manufacturers (FMM), representing the industrial sector, was also consulted.

Projected potential biodiesel consumption lower than expected ● We are not surprised by the government’s move to raise the biodiesel blend as this

has been hinted before. However, we are slightly surprised by the government’s estimate that the higher biodiesel blend will only raise Malaysia’s biodiesel consumption to 709,000 tonnes. This is 34% lower compared to our calculation of 1.08m tonnes of biodiesel usage based on previous statistics provided.

● This also suggests that biodiesel consumption in Malaysia may increase by only 23% (or 134,000 tonnes) compared to the previous practice of the B7 blend for the transport sector, which was estimated to have absorbed 575,000 tonnes of biodiesel. We suspect the more conservative figure provided for biodiesel consumption could be due to lower diesel usage in Malaysia, following the removal of fuel subsidies.

Positive for CPO price but… ● This development is positive for CPO prices. However, the incremental demand for

palm oil is not as significant compared to earlier expectations at around 139,000 tonnes per annum or 0.7% of Malaysia’s 2016 palm oil output. Assuming the biodiesel mandates lead to a take-up of 709,000 tonnes of biodiesel uptake in 2016, it will only represent around 3.6% of Malaysia’s estimated CPO output and utilise 28% of total installed biodiesel capacity in Malaysia of approximately 2.5m tonnes.

● This is not as aggressive compared to Indonesia’s biodiesel targets of B20 (or 20% biodiesel blend) which is expected to raise biodiesel usage in Indonesia to 2.35m in 2016, representing around 7-8% of the country’s total CPO output. In view of our preliminary calculation that this policy will have only a marginal positive impact on incremental demand, we have kept our average CPO price forecast unchanged at RM2,450 per tonne for 2016 and RM2,600 for 2017.

Impact on planters and biodiesel players in Malaysia ● We are of the view that the higher biodiesel mandate will be mildly positive for

biodiesel producers in Malaysia (Sime, FGV, KLK, GENP and Wilmar) and CPO producers. However, this could be slightly negative for consumers who may have to fork out slightly higher retail diesel prices (which incorporates the blended biodiesel costs). Maintain Neutral with AALI, GENP and First Resources as our top picks.

▎ASEAN May 31, 2016 - 6:40 PM

Neutral (no change)

Highlighted companies

Astra Agro Lestari ADD, TP Rp17,000, Rp14,925 close

Astra Agro is our top pick among the Indonesian planters due to its strong corporate governance and attractive valuation.

First Resources Ltd ADD, TP S$1.98, S$1.61 close

Our preferred pick in Singapore for its superiour output growth prospects against peers, and low cost of production.

Genting Plantations ADD, TP RM11.80, RM10.62 close

We like its young estates, solid balance sheet and strong management.

Summary valuation metrics

Analyst(s)

Ivy NG Lee Fang, CFA

T (60) 3 2261 9073 E [email protected]

P/E (x) Dec-16F Dec-17F Dec-18F

Astra Agro Lestari 14.00 11.23 9.49 First Resources Ltd 21.94 10.74 8.78 Genting Plantations 36.74 21.86 19.21

P/BV (x) Dec-16F Dec-17F Dec-18F

Astra Agro Lestari 1.77 1.61 1.45 First Resources Ltd 1.76 1.58 1.40 Genting Plantations 1.84 1.73 1.62

Dividend Yield Dec-16F Dec-17F Dec-18F

Astra Agro Lestari 2.47% 1.68% 2.40%First Resources Ltd 1.37% 2.79% 3.41%Genting Plantations 0.67% 1.12% 1.27%

3

Consumer Discretionary│Hong Kong│Equity research│May 31, 2016

Sector Note

IMPORTANT DISCLOSURES, INCLUDING ANY REQUIRED RESEARCH CERTIFICATIONS, ARE PROVIDED AT THE END OF THIS REPORT. IF THIS REPORT IS DISTRIBUTED IN THE UNITED STATES IT IS DISTRIBUTED BY CIMB SECURITIES (USA), INC. AND IS CONSIDERED THIRD-PARTY AFFILIATED RESEARCH.

Powered by the EFA Platform

Environmental Minimum utilisation hours set for renewables

NEA has released the 2016 minimum utilisation hours for wind and solar power. ■ Nine provinces have the minimum wind power utilisation hours set at significant ■premium over the actuals in 2015

Datang Renewable may see 100% jump in FY16 net profit if effectively executed. ■ Huaneng Renewables and Longyuan may also see 12-23% earnings increase. ■ We reiterate Overweight call and Huaneng Renewables as top pick. ■

NEA sets minimum utilisation hours for wind and solar power Today, the National Energy Administration (NEA) has released further details about the Guaranteed Purchase of Renewable Power announced in Mar 2016. The 2016 minimum wind power utilisation hours of nine provinces are set at 1,800-2,000 hours and minimum solar power utilisation hours of eleven provinces are set at 1,300-1,500 hours. These minimum hours are applicable to 2016 and will be revised in the future.

Minimum utilisation hours at huge premium to hours in 2015 We believe this is positive for wind power producers. The minimum utilisation hours for wind power are at a significant premium over the utilisation hours achieved in 2015. Provinces with high premium include Gansu (52%), Jilin (26%), Heilongjiang (22-25%), Xinjiang (15-21%) and Ningxia (15%). These provinces suffered from severe power curtailment last year.

Datang Renewable’s FY16 earnings may double Datang Renewable (1798 HK, HOLD) is a key beneficiary as 65% of its FY16 wind power production is located in the nine provinces. We estimate that if the minimum utilisation hours are effectively executed, Datang Renewable would see an 8% increase in wind power generation and 100% increase in its FY16 net profit.

Huaneng Renewables would see 23% lift in FY16 net profit Huaneng Renewables (958 HK, ADD) has exposure in six of the nine provinces, which account for 54% of its wind power production in FY16. The effective execution of the minimum utilisation hours would lift its FY16 net profit by 23%. Longyuan’s (916 HK, ADD) FY16 net profit would be lifted by only 12% as it also has earnings contribution from coal-fired power.

Reiterate Overweight sector call There are uncertainties as to whether the minimum utilisation hours can be effectively executed, and if not whether the compensation can be satisfactorily received by the renewable energy producers. However, we still expect meaningful rebound in the utilisation hours of the three listed wind power producers. We reiterate our Overweight sector call and Huaneng Renewables as our top pick due to its potential earnings rebound and attractive FY16 P/E of 8.8x.

[ X ]

Figure 1: Minimum wind power utilisation hours set by NEA for 2016

SOURCES: CIMB RESEARCH, NEA

▎Hong Kong

Overweight (no change) Highlighted companies

China Longyuan Power ADD, TP HK$8.70, HK$5.34 close

Longyuan is the largest wind power producer in China, with a geographically diversified portfolio. We expect Longyuan to continue to add new capacity of 2-3GW p.a. in FY16-18.

Huaneng Renewables ADD, TP HK$3.70, HK$2.36 close

Huaneng Renewables is the wind power flagship arm of Huaneng Group and has expanded rapidly in the last few years. We think it is a beneficiary of the reduction in wind power curtailment in Inner Mongolia.

Summary valuation metrics

Analyst(s)

Keith LI

T (852) 2532 1110 E [email protected]

Minimum wind power 2015 wind power Upside/

Province utilisation hour utilisation hour (downside)

Hebei 2000 1808 10.6%Shanxi 1900 1697 12.0%Inner Mongolia 1,900-2,000 1865 1.9-7.2%Liaoning 1850 1780 3.9%Jilin 1800 1430 25.9%Heilongjiang 1,850-1,900 1520 21.7-25.0%Gansu 1800 1184 52.0%Ningxia 1850 1614 14.6%Xinjiang 1,800-1,900 1571 14.6-20.9%

P/E (x) Dec-16F Dec-17F Dec-18F

China Longyuan Power 8.76 7.46 6.57 Huaneng Renewables 8.83 7.12 5.93

P/BV (x) Dec-16F Dec-17F Dec-18F

China Longyuan Power 0.88 0.80 0.73 Huaneng Renewables 0.98 0.88 0.78

Dividend Yield Dec-16F Dec-17F Dec-18F

China Longyuan Power 2.28% 2.68% 3.04%Huaneng Renewables 1.81% 2.25% 2.70%

4

IT Services│India│Equity research│May 31, 2016

Company Note

IMPORTANT DISCLOSURES, INCLUDING ANY REQUIRED RESEARCH CERTIFICATIONS, ARE PROVIDED AT THE END OF THIS REPORT. IF THIS REPORT IS DISTRIBUTED IN THE UNITED STATES IT IS DISTRIBUTED BY CIMB SECURITIES (USA), INC. AND IS CONSIDERED THIRD-PARTY AFFILIATED RESEARCH.

Powered by the EFA Platform

MphasiS Improving growth outlook priced in

Mphasis’s 1.6% qoq decline in US$ revenues was higher than our expectation but ■HP channel revenue decline was lower than our forecast.

EBIT margin in 4QFY16 was better than expected. ■ HP channel sales likely to stabilise post completion of Blackstone deal by 2QFY17. ■ FY16 recurring net profit was above, at 102% of our forecast, due to higher-than-■expected margins. We raise our FY17-FY18F EPS by 3-6%.

Maintain Hold. Our target price is based on 1-year forward P/E of 12x. ■4QFY16 sales continued to dip; smaller decline in HP channel Post the 3.4% qoq dip in US$ sales (ex-forex) in 3Q, revenues fell 1.6% in 4Q. This was largely led by a qoq decline in digital risk due to a subdued performance by its project-based business. Revenues in HP channel declined by 1.2% qoq, the lowest decline rate in the last 19 quarters. Based on our estimates, growth in the direct international market (ex-digital risk) was ~3% which is healthy given the seasonal softness.

EBIT margins better than expected EBIT margin rose 108bp qoq to 14.3% vs. our expectation of a 30bp+. This was led by lower cost of revenues (with 2.2% dip in manpower costs) while SG&A cost rose to 12.1% vs. 11.3% in 3Q. With one-time charge of Rs316m (US$4.7m) in 4Q for future years’ losses in the domestic ATM business, it expects 60-70bp margin improvement in 1QFY17. It raised its EBIT guidance to 14-16% (albeit for 1HFY17) from 13-15%.

Blackstone Group deal likely to result in business stability… Blackstone Group recently said it plans to buy a majority stake in Mphasis from its parent HP, followed by an open offer at Rs457.5/share. This has resulted in changes to MSA with HP with minimum sales guarantee of US$990m over five years along with a preferred partner status to Mphasis (binding only post required regulatory approvals). This indicates US$198m yearly run rate (current US$220m). It will lead to stable/improving sales from HP and direct channel (with Blackstone’s large investee portfolio of 80 companies) after the deal is approved.

…but portfolio-related business risks remain However, business risks persist as: i) the announcement by HP-CSC for a merger of some IT services may result in lower outsourcing to partners given their combined large scale in global delivery locations (incl. India), ii) high project base revenues in digital risk (though worst of the decline is now behind) and risk of increasing mortgage rates in the US, and iii) increasing competitive pressures in the crowded BFSI sector, its only high focus non-HP business, and impact from any macro issues on discretionary projects.

Maintain Hold Despite the likely improvement in revenue predictability, we maintain Hold given the recent share price spike and other business risks. Our revised target price is based on 1-year forward P/E of 12x (up from 11x due to improving earnings visibility) and set at close to its 1-3 year mean. We expect a dividend announcement for FY16 before the AGM (likely in Sep) as no dividend was announced with the 4Q results. Key risk to our view include any faster and bigger-than-expected revenue ramp-up in HP channel.

▎India

HOLD (no change) Consensus ratings*: Buy 11 Hold 10 Sell 7

Current price: Rs506.3 Target price: Rs500.0 Previous target: Rs425.0

Up/downside: -1.2% CIMB / Consensus: 2.1%

Reuters: MBFL.BO Bloomberg: MPHL IN Market cap: US$1,584m Rs106,409m Average daily turnover: US$1.68m Rs112.1m Current shares o/s: 210.2m Free float: 39.5% * Source: Bloomberg Key changes in this note

FY17F US$ Revenue decreased by 0.8%. FY17F EPS increased by 3.2%. FY18F EPS increased by 5.8%.

Source: Bloomberg

Price performance 1M 3M 12M Absolute (%) 4.3 20.4 36.9 Relative (%) -0.1 4.2 40.9

Major shareholders % held EDS Group Companies 60.5 Aberdeen and related entities 6.4 LIC of India 1.6

Analyst(s)

Sandeep SHAH

T (91) 22 6602 5159 E [email protected]

[ X ]

SOURCE: COMPANY DATA, CIMB FORECASTS

Financial Summary Mar-15A Mar-16A Mar-17F Mar-18F Mar-19F

Revenue (Rsm) 57,949 60,879 62,236 68,231 74,801Net Profit (Rsm) 6,746 6,694 7,818 8,798 9,549Core EPS (Rs) 32.25 34.46 37.19 41.83 45.39Core EPS Growth (9.0%) 6.8% 7.9% 12.5% 8.5%FD Core P/E (x) 15.81 14.80 13.75 12.27 11.36Price To Sales (x) 1.84 1.75 1.71 1.56 1.42DPS (Rs) 16.00 17.23 18.59 20.91 22.69Dividend Yield 3.16% 3.40% 3.67% 4.13% 4.48%EV/EBITDA (x) 9.71 9.06 8.02 6.81 5.95P/FCFE (x) 10.44 NA 17.75 15.98 13.45Net Gearing (39.9%) (43.0%) (47.4%) (51.9%) (55.9%)P/BV (x) 1.94 1.82 1.73 1.63 1.54ROE 12.8% 12.8% 13.0% 13.9% 14.2%% Change In Core EPS Estimates 3.25% 5.78%CIMB/consensus EPS (x) 0.98 0.98

95.0

111.7

128.3

145.0

350

400

450

500

Price Close Relative to SENSEX (RHS)

1234

Jun-15 Sep-15 Dec-15 Mar-16

Vol m

5

Autos│India│Equity research│May 31, 2016

Company Note

IMPORTANT DISCLOSURES, INCLUDING ANY REQUIRED RESEARCH CERTIFICATIONS, ARE PROVIDED AT THE END OF THIS REPORT. IF THIS REPORT IS DISTRIBUTED IN THE UNITED STATES IT IS DISTRIBUTED BY CIMB SECURITIES (USA), INC. AND IS CONSIDERED THIRD-PARTY AFFILIATED RESEARCH.

Powered by the EFA Platform

Tata Motors Short-term relief in 4QFY16

■ Consolidated 4QFY16 EPS surged 60% qoq to Rs13.5, beating our estimate by 15%, due to lower depreciation and interest cost. EBITDA was in line.

■ Doubling of JLR’s China PAT qoq impressive; we raise JLR’s FY17-18 PAT by 2-7%. ■ We lift our consolidated FY17-18 EPS forecasts by 2-5% to factor in the strong

4QFY16, but await for sustained recovery of stand-alone entity to profitability. ■ Notwithstanding the strong 4QFY16, Tata faces risks of weakening product mix,

volatility at Brexit, and peaking global car demand. Maintain Reduce.

EBITDA margin recovers after dipping for five consecutive quarters JLR’s IGAAP EBITDA rose 20% yoy and qoq to £1.1bn, as EBITDA margin rose 70bp yoy and 110bp qoq to 16.1%, the first yoy increase since 2QFY15. Adjusted for £166m one-off costs, EBITDA would have been £1.26bn, beating our estimate by 20%. Sharp improvement in working capital (£1.16bn) and China JV profit (+123% qoq to £49m) were impressive, but management guides caution on both fronts.

Consolidated EBITDA in line At the standalone level, the company returned to a PBT profit of Rs682m, thanks to a 400bp qoq dip in raw material cost. EBITDA jumped 80% qoq to Rs10.7bn, 12% higher than our estimate. Consolidated EBITDA rose 34.7% yoy and 21.7% to Rs124.6bn, in line with our estimate but 25% higher than Bloomberg consensus. However, due to lower interest and depreciation expenses, normalised PAT was at Rs45.7bn (+60% qoq), surprising us on the upside by 15%.

JLR profit upgrade by 2-7% Good response to the new Jaguar crossover, F-Pace, is encouraging. However, the yoy decline in JLR’s most profitable segment, Range Rover and Range Rover Sport, in 4QFY16 (Fig 6) is a concern. The much awaited Jaguar XE launch in the US may further dilute JLR’s product mix and profitability especially as the US car market seems to be weakening. As such, we upgrade JLR’s PAT by only 2-7% for FY17-18, even as we build in EBIDTA margin of 15.6% on the back of strong sales volume CAGR of 17%.

Consolidated FY17-18 EPS raised by 2-5% For the standalone entity, we raise our FY17-18 EPS estimates by 2% on back of the recovery in light commercial vehicle (LCV) sales, and foresee EBITDA margin pressure in FY18F due to emission upgrade costs. As for the consolidated entity, we marginally raise our EBITDA forecast for FY17-18 and factor in the lower depreciation seen in 4QFY16 leading to EPS upgrades. Working capital surprises are subject to new product success and strong demand, which may be difficult to sustain in the coming quarters, in our view.

Reduce rating maintained Tata’s sharp bounce back in recent months has priced in its 4QFY16 sales volume and margin recovery. As the weakness of JLR’s premium SUV portfolio and new products will likely dilute its margin, we see unfavourable risk reward at current stock price, especially in view of peaking global car demand and Brexit volatility. We keep our non-consensus Reduce rating with a higher SOP-based target price as we roll forward our valuation; JLR still valued at 2x EV/EBITDA.

▎India

REDUCE (no change) Consensus ratings*: Buy 43 Hold 4 Sell 1

Current price: Rs459.7 Target price: Rs340.0 Previous target: Rs289.1

Up/downside: -26.0% CIMB / Consensus: -24.2%

Reuters: TAMO.BO Bloomberg: TTMT IN Market cap: US$22,139m Rs1,487,019m Average daily turnover: US$48.00m Rs3,942m Current shares o/s: 3,396m Free float: 67.0% * Source: Bloomberg Key changes in this note

FY17-18F Revenue cut by 1-4%. FY17-18F EPS increased by 2-5%.

Source: Bloomberg

Price performance 1M 3M 12M Absolute (%) 12.6 53.4 -4.6 Relative (%) 8.5 37.5 -0.4

Major shareholders % held Tata Group 33.0 LIC 6.9 ICICI Pru Life 2.3

Analyst(s)

Pramod AMTHE

T (91) 22 6602 5167 E [email protected]

[ X ]

SOURCE: COMPANY DATA, CIMB FORECASTS

Financial Summary Mar-15A Mar-16A Mar-17F Mar-18F Mar-19F

Revenue (Rsm) 2,627,963 2,752,785 3,090,166 3,803,908 4,417,343Operating EBITDA (Rsm) 421,460 396,390 478,483 587,559 674,103Net Profit (Rsm) 139,863 110,238 138,133 170,672 201,126Core EPS (Rs) 44.11 33.08 40.68 50.26 59.23Core EPS Growth 0.0% (25.0%) 23.0% 23.6% 17.8%FD Core P/E (x) 10.42 13.89 11.30 9.15 7.76DPS (Rs) 0.00 0.20 3.00 4.00 5.00Dividend Yield 0.00% 0.04% 0.65% 0.87% 1.09%EV/EBITDA (x) 4.70 4.72 3.81 2.96 2.17P/FCFE (x) 64.93 NA 29.66 13.07 5.61Net Gearing 73.2% 37.0% 26.7% 15.2% (8.4%)P/BV (x) 2.77 1.93 1.67 1.42 1.21ROE 24.6% 16.4% 15.9% 16.8% 16.8%% Change In Core EPS Estimates 4.49% 2.28%CIMB/consensus EPS (x) 0.93 0.94

65.073.081.089.097.0105.0

250300350400450500

Price Close Relative to SENSEX (RHS)

50

100

150

Jun-15 Sep-15 Dec-15 Mar-16

Vol m

6

Indonesia│Equity research│May 31, 2016

Strategy Note

IMPORTANT DISCLOSURES, INCLUDING ANY REQUIRED RESEARCH CERTIFICATIONS, ARE PROVIDED AT THE END OF THIS REPORT. IF THIS REPORT IS DISTRIBUTED IN THE UNITED STATES IT IS DISTRIBUTED BY CIMB SECURITIES (USA), INC. AND IS CONSIDERED THIRD-PARTY AFFILIATED RESEARCH.

Powered by the EFA Platform

Indonesia Strategy CIMB Portfolio Tracker – May 2016

CIMB Portfolio lost 1.3% mom in May, underperforming JCI by 0.4%%. Last minute ■selling of BMRI and ACES roiled our portfolio. YTD it returned 6.6% vs. JCI’s 4.4%.

It was a volatile May with foreigners leading the selling until the last week of May ■when mood brightened despite the higher probability of an FFR hike in summer.

Lacking corporate news, FFR and Brexit decisions may cloud market sentiment in ■Jun, while the passing of tax amnesty could just cheer it up.

We expect tax amnesty to be positively decided, hence we rotate to laggards and ■cyclicals.

The selling mood eases… CIMB portfolio declined -1.3% mom in May against the benchmark JCI’s -0.9%. It gained 6.6% YTD vs. JCI’s 4.4%. In May, the key outperformers were the infra, property/construction and consumer sectors. The key underperformers were commodities and basic materials, the latter being led by INTP.

…despite higher chances of a summer Fed Funds Rate (FFR) hike The mood turned cheerier towards month-end, despite the higher probability of a summer FFR hike. Bank shares tumbled initially, made a mini U-turn, and ended withaggregate losses of only -0.7% mom. Foreigners turned net buyers of US$89m in the fourth week of May, trimming its net sold to US$17m for the month (vs. +US$22m in Apr, with YTD net buy of +US$320m). The key outperformers in CIMB’s portfolio were TLKM, WSKT and PWON, while the key underperformers were BMRI, INTP and ACES.

Which shall triumph in Jun: external or internal drivers? The external risks are the FFR decision in mid-Jun and Brexit referendum on 23 Jun. Judging by the calmer mood at end-May, the former is possibly priced in, though the market is arguably still complacent over the latter. Internally, the tax amnesty’s fate is the game changer. Meanwhile, macro indicators point to further stabilisation of the current account deficit (CAD) and inflation. Expect more stimulus from the government and BI equally to further boost growth.

Putting more weight on laggards and cyclicals In our view, tax amnesty shall: 1) be passed by end-Jul at the latest, with newsflow turning more supportive in Jun; 2) lift local consumer’s sentiment and the capital market’s mood. This forms basis of our view that underperformers and cyclicals mighthence see better days. Such and valuations underpin our reshuffling: 1) replacing INTP with SMGR; 2) INDF with BSDE; 3) cut WSKT, replace with laggards and cheaper PTPP and WIKA; 4) trim defensive HMSP, cut expensive SCMA while adding BSDE, PTPP and WIKA to the balance.

The new metrics After the adjustments, the weighted average of CIMB’s portfolio valuation is 17.4x forward P/E, about in line with market valuations (including HMSP) of 16.9x forward P/E. The adjusted portfolio’s beta is relatively unchanged at 1.2. The weighted forward ROE is 30% vs. JCI’s 17% against the weighted-average cost of equity estimate of 19%.

[ X ]

Figure 1: CIMB Portfolio has outperformed JCI by 2.8% YTD

SOURCES: CIMB RESEARCH, COMPANY

▎Indonesia

CIMB portfolio outperformed JCI by 0.2% in May

Change in weighting

Analyst(s)

Erwan TEGUH T (62) 21 3006 1720 E [email protected] Peter P. SUTEDJA, CFA T (62) 21 3006 1726 E [email protected]

9698

100102104106108110112

CIMB Portfolio JCI

-1.2%

-1.0%

-0.8%

-0.6%

-0.4%

-0.2%

0.0%

0.2%

0.4%

0.6%

0.8%

-4.5%

-4.0%

-3.5%

-3.0%

-2.5%

-2.0%

-1.5%

-1.0%

-0.5%

0.0%

0.5%

1.0%

30-Apr-16 14-May-16 28-May-16

Outperform (Underperform) - RHS

CIMB Portfolio

JCI

Old weight New weight NoteHMSP 8% 7%SMGR 0% 6% AdditionBSDE 0% 5% AdditionPTPP 0% 3% AdditionWIKA 0% 3% AdditionINTP 6% 0% DroppedWSKT 4% 0% DroppedINDF 4% 0% DroppedSCMA 2% 0% Dropped

7

Shipbuilding│South Korea│Equity research

Company Flash Note

IMPORTANT DISCLOSURES, INCLUDING ANY REQUIRED RESEARCH CERTIFICATIONS, ARE PROVIDED AT THE END OF THIS REPORT. IF THIS REPORT IS DISTRIBUTED IN THE UNITED STATES IT IS DISTRIBUTED BY CIMB SECURITIES (USA), INC. AND IS CONSIDERED THIRD-PARTY AFFILIATED RESEARCH.

Powered by the EFA Platform

Hyundai Mipo Dockyard STX windfall – full consolidation ahead

STX has filed for court receivership on 30 May. We see consolidation rapidly picking ■up pace for PCs, along with the recent acquisition deal failure of SPP Shipbuilding.

We think 25-30 units of STX’s orders could be cancelled (of a total 54 units in the ■backlog), and potentially redirected to HMD at a firm newbuild price and 5-7% OPM.

We maintain our Add recommendation and SOP-based target price of W140,000. ■

Why we believe patience will be rewarded ● According to FSS disclosure, STX O&S officially filed for court receivership on 30 May.

While the final outcome is subject to the Central District Court’s decision, we expect STX’s major newbuild activities to come to a halt in the near term (except for those ships targeting imminent delivery). This event also follows the recently failed deal between SPP and SM Group, foreshadowing another potential consolidation, in our view.

● As contracts typically entail clauses related to liquidation damage and counterparty risks, we see growing cancellation risks to STX’s current order book, as owners will be exempt from cancellation charges and refund-guarantee loans remain valid.

● STX’s previous contracts will sequentially be redirected to HHI Group, in our view, especially for those from tier-1 owners (who previously placed orders to STX), which look set to undergo renegotiation of contract terms for new vessel spectrum.

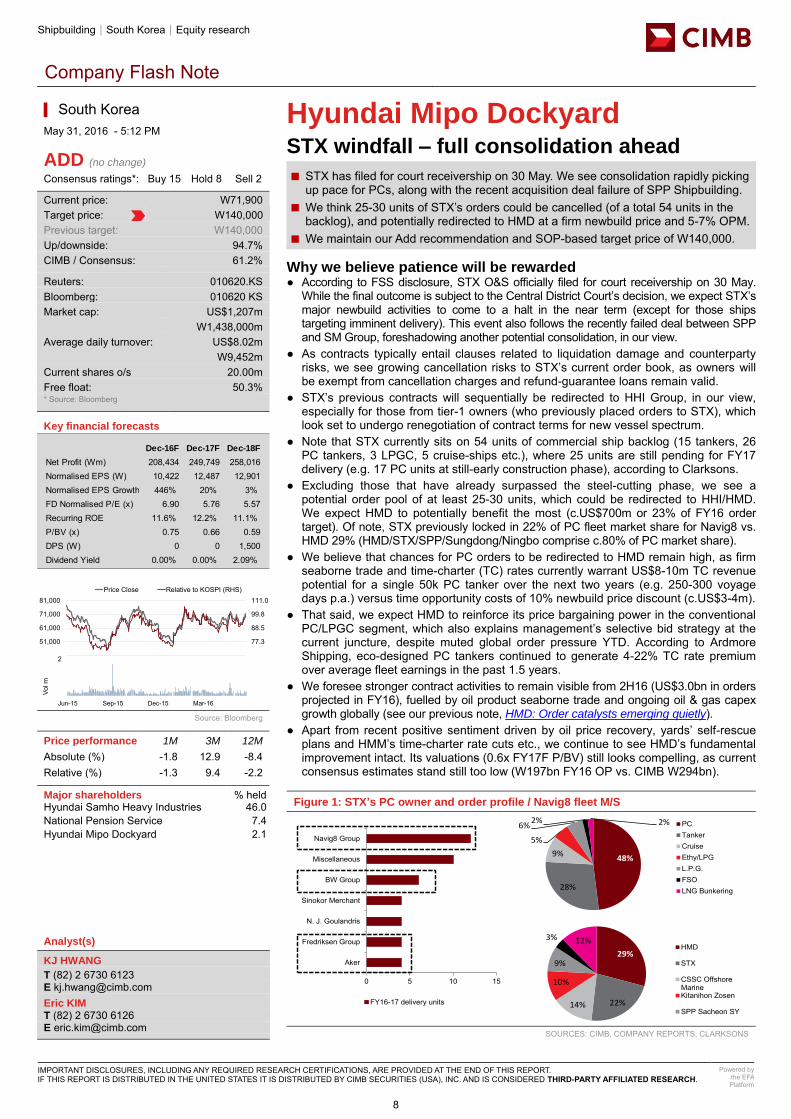

● Note that STX currently sits on 54 units of commercial ship backlog (15 tankers, 26 PC tankers, 3 LPGC, 5 cruise-ships etc.), where 25 units are still pending for FY17 delivery (e.g. 17 PC units at still-early construction phase), according to Clarksons.

● Excluding those that have already surpassed the steel-cutting phase, we see a potential order pool of at least 25-30 units, which could be redirected to HHI/HMD. We expect HMD to potentially benefit the most (c.US$700m or 23% of FY16 order target). Of note, STX previously locked in 22% of PC fleet market share for Navig8 vs. HMD 29% (HMD/STX/SPP/Sungdong/Ningbo comprise c.80% of PC market share).

● We believe that chances for PC orders to be redirected to HMD remain high, as firm seaborne trade and time-charter (TC) rates currently warrant US$8-10m TC revenue potential for a single 50k PC tanker over the next two years (e.g. 250-300 voyage days p.a.) versus time opportunity costs of 10% newbuild price discount (c.US$3-4m).

● That said, we expect HMD to reinforce its price bargaining power in the conventional PC/LPGC segment, which also explains management’s selective bid strategy at the current juncture, despite muted global order pressure YTD. According to Ardmore Shipping, eco-designed PC tankers continued to generate 4-22% TC rate premium over average fleet earnings in the past 1.5 years.

● We foresee stronger contract activities to remain visible from 2H16 (US$3.0bn in orders projected in FY16), fuelled by oil product seaborne trade and ongoing oil & gas capex growth globally (see our previous note, HMD: Order catalysts emerging quietly).

● Apart from recent positive sentiment driven by oil price recovery, yards’ self-rescue plans and HMM’s time-charter rate cuts etc., we continue to see HMD’s fundamental improvement intact. Its valuations (0.6x FY17F P/BV) still looks compelling, as current consensus estimates stand still too low (W197bn FY16 OP vs. CIMB W294bn).

Figure 1: STX’s PC owner and order profile / Navig8 fleet M/S

SOURCES: CIMB, COMPANY REPORTS, CLARKSONS

48%

28%

9%

5%

6%2% 2% PC

TankerCruiseEthy/LPGL.P.G.FSOLNG Bunkering

0 5 10 15

Aker

Fredriksen Group

N. J. Goulandris

Sinokor Merchant

BW Group

Miscellaneous

Navig8 Group

FY16-17 delivery units

29%

22%14%

10%

9%

3% 12%HMD

STX

CSSC OffshoreMarineKitanihon Zosen

SPP Sacheon SY

▎South Korea May 31, 2016 - 5:12 PM

ADD (no change) Consensus ratings*: Buy 15 Hold 8 Sell 2

Current price: W71,900 Target price: W140,000 Previous target: W140,000

Up/downside: 94.7% CIMB / Consensus: 61.2%

Reuters: 010620.KS Bloomberg: 010620 KS Market cap: US$1,207m W1,438,000m Average daily turnover: US$8.02m W9,452m Current shares o/s 20.00m Free float: 50.3% * Source: Bloomberg Key financial forecasts

Source: Bloomberg Price performance 1M 3M 12M

Absolute (%) -1.8 12.9 -8.4 Relative (%) -1.3 9.4 -2.2

Major shareholders % held Hyundai Samho Heavy Industries 46.0 National Pension Service 7.4 Hyundai Mipo Dockyard 2.1

Analyst(s)

KJ HWANG

T (82) 2 6730 6123 E [email protected] Eric KIM T (82) 2 6730 6126 E [email protected]

Dec-16F Dec-17F Dec-18F

Net Profit (Wm) 208,434 249,749 258,016Normalised EPS (W) 10,422 12,487 12,901Normalised EPS Growth 446% 20% 3%FD Normalised P/E (x) 6.90 5.76 5.57Recurring ROE 11.6% 12.2% 11.1%P/BV (x) 0.75 0.66 0.59DPS (W) 0 0 1,500Dividend Yield 0.00% 0.00% 2.09%

66.0

77.3

88.5

99.8

111.0

41,000

51,000

61,000

71,000

81,000Price Close Relative to KOSPI (RHS)

1

1

2

Jun-15 Sep-15 Dec-15 Mar-16

Vol m

8

Chemicals - Others│South Korea│Equity research

Company Flash Note

IMPORTANT DISCLOSURES, INCLUDING ANY REQUIRED RESEARCH CERTIFICATIONS, ARE PROVIDED AT THE END OF THIS REPORT. IF THIS REPORT IS DISTRIBUTED IN THE UNITED STATES IT IS DISTRIBUTED BY CIMB SECURITIES (USA), INC. AND IS CONSIDERED THIRD-PARTY AFFILIATED RESEARCH.

Powered by the EFA Platform

Kolon Industries Asia NDR feedback: All eyes on CPI

We found that investors were keen on the potential of CPI film which seems to be ■the only one that passed the quality standard of its prospective customer.

The management reassured investors on the company’s commitment to capacity ■expansion for its core products that are seeing sustained margin improvements.

Upside risks: expansion announcement and introduction of foldable mobile devices. ■

Key takeaways We hosted an Asia NDR with management of Kolon Industries (KI). Key takeaways include: 1) further margin improvement potential of tyre cord upon competitor’s change in pricing policy; 2) volume expansion of airbag fabric after completion of manufacturing plant in Mexico; 3) further capacity expansion plans on key industrial materials products; and 4) development stage of colourless polyimide (CPI) film and its potential as the protective cover for foldable and unbreakable mobile devices.

All eyes on CPI film ● Most investors were keen to learn more on the potential of CPI film given its potential

as the key to enable foldable mobile devices. More interestingly, KI claimed that only its CPI film passed the quality standard of its largest prospective customer. We believe that KI’s continued efforts on developing the product since 2005 and working with the customer in the past three years have helped the company to come up with light transmission rate close to c.94-95% level vs. competitors at 87-89% (Mar 2015).

Company’s plans for the CPI film ● The company was not able to share potential price range, volume or margin given

that CPI film is not yet mass produced (previously produced on order of customers at a lab). Also, the company expects its production yield to be low in the initial production stage starting from Jun. However, the management guided that unit price would be higher than Gorilla Glass and current pilot capacity will be sufficient to meet demand for the first generation of foldable mobile phone in 2017.

Upcoming capacity expansion plans ● The management also highlighted its growth potential from capacity expansion for: 1)

polyester tyre cord in Vietnam (adding c.20% to current capacity); 2) air bag fabric in China and Mexico (2H16); 3) de-bottlenecking aramid production (additional 60% capacity); 4) participation in equity raising by subsidiary Kolon Plastic (138490 KS, N/R) for a new engineering plastic (POM) plant in joint venture with BASF (BAS GR, N/R); and 5) mass production line of CPI film that will increase its capacity by fivefold.

Re-iterate Add ● Maintain Add, with a target price of W83k based on an SOP valuation which implies

10x 2016 P/E. We think the company could re-rate on potential key catalysts, including: 1) further improvement in industrial materials margins; 2) official announcement of capacity expansion plans and 3) introduction of foldable mobile devices adopting KI’s CPI film. Key risks include slowdown in auto parts including tyres, earlier than expected technological advancement in CPI film of competitors.

Figure 1: We think current prices of protective film for smartphones may serve as a guideline to the price range of KI’s CPI film

NOTE: BASED ON LOWEST PRICE ON KOREA NAVER SHOPPING PRICE COMPARISON FOR PROTECTIVE FILM OF

IPHONE 6S FRONT DISPLAY (4.7 INCH) / ASSUME USDKRW=1,180 / SOURCES: CIMB, NAVER SHOPPING

HohooSky Digital

Glass protectorTraum

NewPlus

OHI

Araree ProtectM Glass Gorilla

Iloome Korea

SuperF

LuvN

Liphobia

ProtectM Guard BP

ViewfineProtectM Embo Matt

0

5

10

15

20

25

30

35

90% 91% 92% 93% 94% 95% 96% 97% 98% 99% 100%

(US$)

(Transparency rate)

More than 100% price premium forhigh quality protective cover based on Gorilla Glass overaverage products

(Note: PET-based cover in blue, glass-based cover in red)

▎South Korea May 31, 2016 - 6:00 PM

ADD (no change) Consensus ratings: Buy 11 Hold 0 Sell 0

Current price: W69,200 Target price: W83,000 Previous target: W83,000

Up/downside: 19.9% CIMB / Consensus: -10.2%

Reuters: 120110.KS Bloomberg: 120110 KS Market cap: US$1,459m W1,738,331m Average daily turnover: US$6.37m W7,409m Current shares o/s 25.10m Free float: 61.3% Key financial forecasts

Source: Bloomberg Price performance 1M 3M 12M

Absolute (%) -1 3 3.7 Relative (%) -0.5 -0.5 9.9

Major shareholders % held Kolon Corp, etc 33.7 National Pension Service 12.2 KB Asset Management 6.4

Analyst(s)

TJ OK

T (82) 2 6730 6134 E [email protected]

Dec-16F Dec-17F Dec-18F

Net Profit (Wb) 230.5 260.8 279.3Normalised EPS (W) 9,181 10,390 11,124Normalised EPS Growth 13.2% 7.1%FD Normalised P/E (x) 8.51 7.52 7.02Recurring ROE 12.2% 12.3% 12.0%P/BV (x) 0.86 0.77 0.72DPS (W) 900 1,000 1,100Dividend Yield 1.30% 1.45% 1.59%

81.0

93.9

106.7

119.6

46,000

56,000

66,000

76,000

Price Close Relative to KOSPI (RHS)

200

400

600

Jun-15 Sep-15 Dec-15 Mar-16

Vol t

h

9

Retail│Malaysia│Equity research│May 31, 2016

Company Note

IMPORTANT DISCLOSURES, INCLUDING ANY REQUIRED RESEARCH CERTIFICATIONS, ARE PROVIDED AT THE END OF THIS REPORT. IF THIS REPORT IS DISTRIBUTED IN THE UNITED STATES IT IS DISTRIBUTED BY CIMB SECURITIES (USA), INC. AND IS CONSIDERED THIRD-PARTY AFFILIATED RESEARCH.

Powered by the EFA Platform

7-Eleven Malaysia Holdings Berhad Growth priced in

■ We maintain our neutral stance on 7-Eleven’s earnings prospects. ■ Gunning ahead with plans to increase store count and refurbish its stores in 2016. ■ Maintain Hold, with unchanged 12-month target price of RM1.36. We prefer Bison,

which trades at a more attractive valuation. ■ Upside risks include stronger-than-expected consumer sentiment and the continuity

of its franchise scheme. ■ Downside risks include increased competition from domestic and foreign players.

1Q16 results briefing We attended 7-Eleven’s 1Q16 analyst briefing earlier today. It was chaired by CEO Mr Gary Brown. There were no major surprises but management pointed out that it had deliberately held back its store expansion during the quarter as the group did not want to complicate the implementation of its new IT system. Nonetheless, it emphasised that its expansion plants are back on track. The topics discussed mainly revolved around the group’s 1Q16 performance and its key strategies for 2016.

GP margin expanded due to improved product mix Recall that 7-Eleven’s 1Q16 revenue increased 4.2% yoy while core net profit grew 10.8% yoy to RM15.9m. The stronger topline growth was mainly driven by new stores (net seven stores for 1Q16) and improved product mix. Its GP margin also grew 0.4% yoy to 30.4%, mainly coming from higher sales of its health and beauty products (+9% yoy) and good coffee sales (which typically carry higher margins).

Other key briefing highlights 1) Tobacco sales has not bounced back (down 15-20% yoy) vs. previous years given the significant hike in selling prices last year; 2) expansion and refurbishment plans are on track for the year despite the intentional slow down in store expansion in 1Q16; and 3) 7-Eleven is positive on its long-term partnership with Brahim’s to manufacture ready-to-eat (RTE) products under its “Fresh to Go” house brand. It is currently removing smaller suppliers and will eventually push more for Brahim’s food manufacturing.

Maintain Hold call; target price stays at RM1.44 While we like the group’s healthy expansion and refurbishment plans so far, we believe these have already been factored into its share price. As such, we make no changes to our call and target price. Our target price is still based on CY17F P/E of 23.6x (20% premium over its global peer average). We prefer Bison Consolidated (BISON MK, Add, TP: RM1.80) in the convenience store sector given its healthy 3-year earnings CAGR of 27% and undemanding valuations.

▎Malaysia

HOLD (no change) Consensus ratings*: Buy 0 Hold 3 Sell 2

Current price: RM1.36 Target price: RM1.44 Previous target: RM1.44

Up/downside: 5.5% CIMB / Consensus: 0.3%

Reuters: SEM.KL Bloomberg: SEM MK Market cap: US$386.9m RM1,593m Average daily turnover: US$0.15m RM0.59m Current shares o/s: 1,233m Free float: 49.0% * Source: Bloomberg Key changes in this note

No changes.

Source: Bloomberg

Price performance 1M 3M 12M Absolute (%) -2.2 -6.2 -20.9 Relative (%) 0.4 -4.7 -14.2

Major shareholders % held Berjaya Retail 51.0 Genesis Investment 6.8 Smallcap world fund 6.2

Analyst(s)

Kristine WONG

T (60) 3 2261 9085 E [email protected]

[ X ]

SOURCE: COMPANY DATA, CIMB FORECASTS

Financial Summary Dec-14A Dec-15A Dec-16F Dec-17F Dec-18F

Revenue (RMm) 1,893 2,006 2,226 2,543 2,882Operating EBITDA (RMm) 117.0 122.9 133.0 153.2 169.5Net Profit (RMm) 57.01 55.80 63.95 74.89 82.90Core EPS (RM) 0.046 0.045 0.052 0.061 0.067Core EPS Growth 10.1% (2.1%) 14.6% 17.1% 10.7%FD Core P/E (x) 29.44 30.06 26.23 22.40 20.23DPS (RM) 0.051 0.051 0.031 0.036 0.040Dividend Yield 3.75% 3.75% 2.29% 2.68% 2.97%EV/EBITDA (x) 12.32 12.67 11.50 9.75 8.51P/FCFE (x) NA 35,689 25 21 17Net Gearing (100%) (71%) (83%) (89%) (98%)P/BV (x) 7.10 9.86 9.47 8.10 6.98ROE 36.8% 27.5% 36.8% 39.0% 37.1%CIMB/consensus EPS (x) 0.98 0.98 0.97

79.0

89.0

99.0

109.0

1.300

1.500

1.700

1.900Price Close Relative to FBMKLCI (RHS)

2468

Jun-15 Sep-15 Dec-15 Mar-16

Vol m

10

Retail│Malaysia│Equity research│May 31, 2016

Company Note

IMPORTANT DISCLOSURES, INCLUDING ANY REQUIRED RESEARCH CERTIFICATIONS, ARE PROVIDED AT THE END OF THIS REPORT. IF THIS REPORT IS DISTRIBUTED IN THE UNITED STATES IT IS DISTRIBUTED BY CIMB SECURITIES (USA), INC. AND IS CONSIDERED THIRD-PARTY AFFILIATED RESEARCH.

Powered by the EFA Platform

Asia File Corporation 4QFY16 results: Profit margin expansion

At 98% of our full-year forecast, Asia File’s FY3/16 net profit was in line with our ■expectations.

9 sen final DPS was declared for 4Q. In FY16, total DPS of 16 sen was declared, ■above our 13 sen forecast.

Management focused on profit margin expansion in FY16. ■ RM135m (US$33m) net cash or RM0.70 net cash per share at end-FY16. ■ Upgrade from Hold to Add. ■

FY16 net profit up 54% yoy FY16 revenue growth was only 0.6% yoy but net profit growth was higher at 54% yoy. The higher net profit was mainly due to wider profit margins. FY16 EBITDA margin was 26% compared to 18% in FY15. Final DPS of 9 sen was declared, above our expectation of 13 sen. Total DPS of 16 sen was declared in FY16.

Forex loss in 4QFY16 Given the strong ringgit environment in 4QFY16, the company posted a RM2.8m (US$6.9m) forex loss during the quarter. However, the ringgit has started to show weakness against major currencies since Apr this year. For FY16, the company recorded RM6.2m (US$1.4m) forex gain.

Europe is still main revenue contributor Asia File’s main market is still Europe and the UK, which contributed more than 65% of the group’s revenue in FY16. The group’s second-largest market was Malaysia, which contributed less than 10% of FY16 sales.

Consolidation phase in the past year After purchasing overseas assets in the past few years, Asia File has been consolidating its business in the past year. Management’s main focus this financial year was profit margin expansion, as quarterly revenue stabilised at the RM90m-100m (US$42-46m) levels. The company achieved higher profit margin in FY16 mainly through better production efficiency and more favourable product mix.

Cash-rich balance sheet At end-Mar, the company’s balance sheet was in net cash position of RM135m (US$33m) or 70 sen net cash per share. The strong balance sheet would allow the company to acquire any of its financially-troubled competitors, if the opportunity arises.

Upgrade from Hold to Add We maintain FY17-18 EPS and introduce FY19 EPS. Our target price is unchanged at 10.8x CY17 P/E (10% discount to sector target P/E of 12x in order to reflect its small free float and market cap). After the 20% share price correction in Mar, Asia File’s valuation is now attractive at less than 10x CY17 P/E. As such, we upgrade the stock from Hold to Add. Re-rating catalysts include continued profit margin expansion and undemanding stock valuations. Risk is sharp slowdown in Europe’s economy.

▎Malaysia

ADD (previously HOLD) Consensus ratings: Buy 0 Hold 1 Sell 0

Current price: RM4.27 Target price: RM5.14 Previous target: RM5.14

Up/downside: 20.4% CIMB / Consensus: 0.0%

Reuters: AFCB.KL Bloomberg: AF MK Market cap: US$198.6m RM819.8m Average daily turnover: US$0.02m RM0.10m Current shares o/s: 180.5m Free float: 28.7% Key changes in this note

Introduced FY19 EPS.

Source: Bloomberg

Price performance 1M 3M 12M Absolute (%) -2.5 -13.7 25.6 Relative (%) 0.3 -12 32.6

Major shareholders % held Prestige Elegance S/B 47.2 Amanah Raya Trustee 24.1

Analyst(s)

Nigel FOO

T (60) 3 2261 9069 E [email protected]

[ X ]

SOURCE: COMPANY DATA, CIMB FORECASTS

Financial Summary Mar-15A Mar-16A Mar-17F Mar-18F Mar-19F

Revenue (RMm) 381.0 389.9 405.5 425.8 442.8Operating EBITDA (RMm) 71.3 84.6 95.7 102.7 108.2Net Profit (RMm) 50.20 76.60 82.95 86.90 91.25Core EPS (RM) 0.28 0.35 0.39 0.42 0.44Core EPS Growth (16.9%) 24.7% 12.3% 7.9% 5.7%FD Core P/E (x) 15.35 12.31 10.96 10.16 9.61DPS (RM) 0.11 0.16 0.16 0.16 0.16Dividend Yield 2.58% 3.75% 3.75% 3.75% 3.75%EV/EBITDA (x) 9.61 7.82 6.55 5.64 4.86P/FCFE (x) 36.70 27.66 16.14 12.44 11.42Net Gearing (18.5%) (21.4%) (25.7%) (31.1%) (36.0%)P/BV (x) 1.67 1.51 1.37 1.25 1.13ROE 11.3% 12.9% 13.1% 12.9% 12.3%% Change In Core EPS Estimates 0% 0%CIMB/consensus EPS (x) 1.18 1.15

92

119

145

172

2.80

3.80

4.80

5.80Price Close Relative to FBMKLCI (RHS)

1

2

3

Jun-15 Sep-15 Dec-15 Mar-16

Vol m

11

TV - Satellite│Malaysia│Equity research│May 31, 2016

Company Note

IMPORTANT DISCLOSURES, INCLUDING ANY REQUIRED RESEARCH CERTIFICATIONS, ARE PROVIDED AT THE END OF THIS REPORT. IF THIS REPORT IS DISTRIBUTED IN THE UNITED STATES IT IS DISTRIBUTED BY CIMB SECURITIES (USA), INC. AND IS CONSIDERED THIRD-PARTY AFFILIATED RESEARCH.

Powered by the EFA Platform

Astro Malaysia A good start to the year

Astro posted a good set of results, as 1QFY17 net profit was broadly in line at 28% ■of our and Bloomberg consensus FY1/17 estimates.

Core EPS rose 6.5% yoy in 1QFY17 due to stronger TV and radio adex growth, ■lower depreciation charges and higher finance income.

Astro is exploring potential price revision for its sports package subs in 2HFY17. ■ It declared an interim DPS of 3 sen, which was in line with our expectations. ■ Maintain Add and target price. Astro remains our top pick due to its dominant market ■position and lower sensitivity to adex volatility.

1QFY17 results broadly in line Revenue in 1QFY17 increased by 2.5% yoy, driven by advertising revenue that rose from RM132m (US$32.1m) in 1QFY16 to RM150m (US$36.5m) in 1QFY17 and robust home shipping sales that surged 74% yoy. Overall, Astro posted higher 1QFY17 core net profit of RM179m (US$43.6m), up 6.5% yoy, after adjusting for unrealised forex gain.

NJOI to drive new subscribers growth At end-Apr 2016, Astro had reached 69% of Malaysian TV households with over 3.5m pay-TV subs. While NJOI (subscription-free satellite TV service) customers contribute lower ARPU, they present a huge base of 1.4m potential customers who could switch to the pay-TV platform. Astro targets to add 250k NJOI customers in FY17. Management said that 33k NJOI customers switched over to the pay-TV platform in FY16.

Aspiring to be platform-agnostic provider Astro aspires to be a platform-agnostic content provider in order to stay relevant and capture the shift in content consumption from TV to online. Astro has launched an online video service called “Tribe” in its bid to extend its customer reach beyond Malaysia, following its launch in Indonesia. Management is targeting launch Tribe service in Philippines in 2HFY17 following its recent tie-up with Globe Telecom.

Potential price revision in 2HFY17 Pay-TV ARPU fell by 0.3% qoq in 1QFY17. Management attributed the decline to churn from low-paying subs, with monthly ARPU of below RM60. Management maintains its ARPU guidance of RM100 for FY17. We have assume an ARPU of RM100 in FY17 and RM102 in FY18. Astro is planning to carry out price revision for its sports package subs in 2HFY17, partly to offset the rising content cost for sports programmes.

Astro Go Shop on track to break even in FY17 The home shopping segment posted 74% yoy revenue growth in 1QFY17, driven by increase in products sold. It also posted yoy lower loss before tax of RM2.9m (US$700k) in 1QFY17 versus RM4.1m (US$1m) in 1QFY16. We expect home shipping segment to break even at pretax level this year driven by stronger sales.

Maintain Add and target price Maintain Add with an unchanged DCF-based target price of RM3.36. Astro remains our sector top pick due to its defensive earnings and dominant market position (69% household penetration at end-Apr 2016). Rising ARPU from value-added services and stronger home shopping contribution are potential catalysts. Key risks to our Add call are decline in premium subs base and higher-than-expected content cost.

▎Malaysia

ADD (no change) Consensus ratings*: Buy 14 Hold 11 Sell 1

Current price: RM2.76 Target price: RM3.36 Previous target: RM3.36

Up/downside: 21.6% CIMB / Consensus: 5.0%

Reuters: ASTR.KL Bloomberg: ASTRO MK Market cap: US$3,480m RM14,366m Average daily turnover: US$1.43m RM5.75m Current shares o/s: 5,202m Free float: 41.5% * Source: Bloomberg Key changes in this note

No changes.

Source: Bloomberg

Price performance 1M 3M 12M Absolute (%) -0.4 1.1 -11.5 Relative (%) 2.4 2.8 -4.5

Major shareholders % held Astro Networks (M) Sdn Bhd 42.4 Pantai Cahaya Bulan Ventures 8.3 All Asia Media Equities 7.8

Analyst(s)

Mohd Shanaz NOOR AZAM

T (60) 3 2261 9078 E [email protected]

[ X ]

SOURCE: COMPANY DATA, CIMB FORECASTS

Financial Summary Jan-15A Jan-16A Jan-17F Jan-18F Jan-19F

Revenue (RMm) 5,231 5,475 5,633 6,028 6,276Operating EBITDA (RMm) 1,808 1,941 1,791 1,836 1,916Net Profit (RMm) 519.4 615.3 629.9 698.8 761.6Core EPS (RM) 0.10 0.12 0.12 0.13 0.15Core EPS Growth 16.0% 18.5% 2.4% 10.9% 9.0%FD Core P/E (x) 27.62 23.31 22.77 20.53 18.83DPS (RM) 0.11 0.12 0.12 0.13 0.15Dividend Yield 3.99% 4.29% 4.39% 4.87% 5.31%EV/EBITDA (x) 9.13 9.03 9.78 9.45 9.01P/FCFE (x) 10.10 13.13 22.72 16.79 17.02Net Gearing 301% 516% 518% 495% 485%P/BV (x) 20.67 23.88 23.88 23.88 23.88ROE 79% 95% 105% 116% 127%% Change In Core EPS Estimates 0% 0% 0%CIMB/consensus EPS (x)

80.0

86.7

93.3

100.0

106.7

2.30

2.50

2.70

2.90

3.10

Price Close Relative to FBMKLCI (RHS)

5101520

Jun-15 Sep-15 Dec-15 Mar-16

Vol m

12

Ind Goods & Services│Malaysia│Equity research

Company Flash Note

IMPORTANT DISCLOSURES, INCLUDING ANY REQUIRED RESEARCH CERTIFICATIONS, ARE PROVIDED AT THE END OF THIS REPORT. IF THIS REPORT IS DISTRIBUTED IN THE UNITED STATES IT IS DISTRIBUTED BY CIMB SECURITIES (USA), INC. AND IS CONSIDERED THIRD-PARTY AFFILIATED RESEARCH.

Powered by the EFA Platform

AWC Berhad Plumbing TRX

■ AWC wins RM18.15m plumbing contract in TRX. ■ This is a positive surprise and improves AWC’s earnings visibility in FY06/17-18. ■ Maintain EPS forecasts and Add rating, with an unchanged SOP-based target price.

Potential catalysts are special dividends and more contract wins.

QDT wins plumbing works for Signature Tower, TRX ● AWC’s plumbing subsidiary, QDT, was awarded an RM18.15m (US$4.4m) plumbing

contract for Signature Tower at the Tun Razak Exchange (TRX). Signature Tower is being developed by the Mulia Group of Indonesia and will be TRX’s tallest building. The building is a Prime Grade A office tower comprising a 92-storey office tower with a five-storey office annex.

A positive surprise ● This is a positive surprise to us and improves AWC’s earnings visibility in FY17-18.

The 28-month contract will commence immediately, with a targeted completion date of 15 Sep 2018. We had assumed RM20m in contract wins for QDT in FY06/17 in our EPS forecasts. This win means that 90% of our contract win estimate has been fulfilled. As the job commences immediately, there is scope for upside surprises to earnings in FY17 if QDT wins more jobs.

Firing on all cylinders ● We view the recent pullback in AWC’s share price as an excellent buying opportunity.

The strong 3Q16 results, special dividends and the high-profile TRX contract win for Signature Tower are expected to boost AWC’s execution credibility in the eyes of investors. AWC also recently secured a 3-year RM7m maintenance contract for Menara Felda.

QDT and STREAM are high-margin businesses ● Apart from the concession business, QDT and STREAM are highly profitable

businesses for AWC given the niche markets they operate in respectively. We estimate QDT’s pretax margins to be 15% and STREAM’s 22%. AWC has an estimated tenderbook of c.RM400m (US$98m) across the various divisions: 1) facilities (RM120m), 2) STREAM (RM90m), 3) M&E/HVAC (RM150M), and 4) plumbing (RM30m).

Still cheap at 9.3x FY17 P/E; 4.7x ex-cash P/E ● We maintain our Add rating on AWC with an unchanged SOP-based target price of

RM1.13. The stock is attractively valued at 9.3x FY17 P/E and FY17F ex-cash P/E of 4.7x. Key risks to the achievement of our target price include project execution and delays.

Figure 1: Net profit to take off from FY16 (RM m)

SOURCES: CIMB, COMPANY REPORTS

0.000

5.000

10.000

15.000

20.000

25.000

0.050.0

100.0150.0200.0250.0300.0

2012 2013 2014 2015 2016F 2017F 2018FRevenue Net profit

▎Malaysia May 31, 2016 - 7:44 AM

ADD (no change) Consensus ratings*: Buy 1 Hold 0 Sell 0

Current price: RM0.70 Target price: RM1.13 Previous target: RM1.13

Up/downside: 60.9% CIMB / Consensus: -0.3%

Reuters: AWCF.KL Bloomberg: AWCF MK Market cap: US$43.58m RM179.4m Average daily turnover: US$1.33m RM5.32m Current shares o/s 256.0m Free float: 66.0% * Source: Bloomberg Key financial forecasts

Source: Bloomberg Price performance 1M 3M 12M

Absolute (%) 18.6 60.9 94.4 Relative (%) 21.2 62.4 101.1

Major shareholders % held Dato' Ahmad Kabeer 34.0

Analyst(s)

Marcus CHAN, CFA

T (60) 3 2261 9070 E [email protected]

Jun-16F Jun-17F Jun-18F

Net Profit (RMm) 15.05 19.34 21.56Core EPS (RM) 0.063 0.076 0.084Core EPS Growth 75.6% 20.8% 11.5%FD Core P/E (x) 11.19 9.27 8.31Recurring ROE 15.6% 17.9% 17.8%P/BV (x) 1.77 1.57 1.40DPS (RM) 0.020 0.025 0.030Dividend Yield 2.86% 3.57% 4.29%

75

135

195

255

0.23

0.43

0.63

0.83Price Close Relative to FBMKLCI (RHS)

20

40

60

Jun-15 Sep-15 Dec-15 Mar-16

Vol m

13

Construction│Malaysia│Equity research│May 31, 2016

Company Note

IMPORTANT DISCLOSURES, INCLUDING ANY REQUIRED RESEARCH CERTIFICATIONS, ARE PROVIDED AT THE END OF THIS REPORT. IF THIS REPORT IS DISTRIBUTED IN THE UNITED STATES IT IS DISTRIBUTED BY CIMB SECURITIES (USA), INC. AND IS CONSIDERED THIRD-PARTY AFFILIATED RESEARCH.

Powered by the EFA Platform

Malaysian Resources Corp A toned-down quarter

■ Annualised 1Q16 core net profit made up 16% of our and 17% of consensus full-year numbers. The results were below expectations due to slow progress billings.

■ Construction margins remain depressed even though revenue shot up 69% yoy. ■ Core property development earnings surged in 1Q16, and could remain robust in

future quarters. Management targets RM1bn (US$250m) sales in 2016. ■ Management has turned aggressive in pursuing new larger-value infra jobs. ■ Job wins remain key catalysts and could surprise on the upside. Add retained.

1Q16 below expectations MRCB’s annualised 1Q16 core net profit made up 16-17% of our and consensus full-year forecasts. While 1Q is traditionally weaker, the 1Q16 results were still below expectations due to weaker progress billings for construction, though this was partially offset by still-robust margins for property. Prevailing construction EBIT margin was lower than the 2% achieved in 1Q15, even though construction revenue jumped 69% yoy. The absence of any gains from property asset sale also dampened the 1Q16 numbers.

Aggressive sales target amidst a challenging market MRCB achieved total sales of RM850m (US$212m) in FY15. The group targets RM1bn (US$250m) total property sales in 2016, but we believe there could be downside if new property launches and progress billings remain weak in 2H16. The RM1.5bn (US$374m) total unbilled sales as at end-1Q16 could largely mitigate any downside. The group has lined up RM2.2bn (US$549m) worth of launches this year, to be driven by Sentral Suites, Menara MRCB, Prima Homes, and Bandar Iskandar.

PDP for Kwasa Damansara township Recent positive news was that MRCB has been appointed the Project Delivery Partner (PDP) to develop the main infrastructure for the new Kwasa Damansara township. MRCB will earn a PDP fee based on 5% of the RM2.2bn (US$549m) development cost. We have not factored in the RM20m-40m estimated PDP fees into our EPS forecasts given the limited visibility on the timing of the new earnings flow.

Still an execution year The group’s strategy this year continues to be on execution, mainly for phase 1 of the Bukit Jalil Sport Complex refurbishment/privatisation deal. Overall, the over RM600m in potential new funds from its 20% share placement will largely be earmarked to fund this venture. The 1st tranche of the placement deal had raised RM109m as at end May, with the remaining tranche to be finalised in the next six months. We continue to expect earnings contribution from Bukit Jalil to flow through no sooner than FY18.

Add retained; Job flow prospects still look buoyant We cut our FY16-18 EPS to factor in slower progress billings and lower construction margins. Our RNAV-based target price, still pegged to 30% RNAV discount, dips as we update for balance sheet items. Key downside risk is sustained soft margins for construction and weaker property market. Even with a c.RM4bn outstanding order book (including Kwasa’s infra portion), MRCB’s strategy is to go aggressive on tenders for incoming infrastructure projects. Job wins are likely catalysts in the medium term.

▎Malaysia

ADD (no change) Consensus ratings*: Buy 6 Hold 4 Sell 0

Current price: RM1.16 Target price: RM1.32 Previous target: RM1.40

Up/downside: 13.8% CIMB / Consensus: -15.7%

Reuters: MYRS.KL Bloomberg: MRC MK Market cap: US$531.6m RM2,188m Average daily turnover: US$0.45m RM1.78m Current shares o/s: 1,783m Free float: 34.9% * Source: Bloomberg Key changes in this note

FY16F EPS cut by 10% FY17F EPS cut by 12%. FY18F EPS cut by 13%

Source: Bloomberg

Price performance 1M 3M 12M Absolute (%) -4.1 2.7 -7.9 Relative (%) -1.3 4.4 -0.9

Major shareholders % held EPF 38.3 Gapurna Sdn Bhd 16.7 Lembaga Tabung Haji 10.1

Analyst(s)

Sharizan ROSELY

T (60) 3 2261 9077 E [email protected]

[ X ]

SOURCE: COMPANY DATA, CIMB FORECASTS

Financial Summary Dec-14A Dec-15A Dec-16F Dec-17F Dec-18F

Revenue (RMm) 1,515 1,697 1,884 2,014 2,154Operating EBITDA (RMm) 110.1 159.9 234.5 255.9 283.1Net Profit (RMm) 136.5 330.4 97.4 111.5 131.6Core EPS (RM) 0.033 0.081 0.042 0.039 0.046Core EPS Growth 146% (48%) (7%) 18%FD Core P/E (x) 35.09 14.25 34.03 29.73 25.19DPS (RM) 0.025 0.025 0.030 0.030 0.030Dividend Yield 2.16% 2.16% 2.59% 2.59% 2.59%EV/EBITDA (x) 46.18 29.65 22.85 23.23 20.87P/FCFE (x) 7.52 NA NA 56.99 36.66Net Gearing 181% 155% 154% 153% 152%P/BV (x) 1.30 1.15 1.91 1.93 1.94ROE 3.61% 8.58% 5.52% 6.45% 7.68%% Change In Core EPS Estimates (9.8%) (11.9%) (13.1%)CIMB/consensus EPS (x) 0.95 0.70 0.72

67.0

80.3

93.7

107.0

120.3

0.70

0.90

1.10

1.30

1.50

Price Close Relative to FBMKLCI (RHS)

10

20

30

Jun-15 Sep-15 Dec-15 Mar-16

Vol m

14

Media - Integrated│Malaysia│Equity research│May 31, 2016

Company Note

IMPORTANT DISCLOSURES, INCLUDING ANY REQUIRED RESEARCH CERTIFICATIONS, ARE PROVIDED AT THE END OF THIS REPORT. IF THIS REPORT IS DISTRIBUTED IN THE UNITED STATES IT IS DISTRIBUTED BY CIMB SECURITIES (USA), INC. AND IS CONSIDERED THIRD-PARTY AFFILIATED RESEARCH.

Powered by the EFA Platform

Media Chinese Int'l In need of new growth drivers

■ Management maintains its cautious outlook for FY17 due to ongoing economic uncertainties in its key operating markets.

■ Challenging outlook for travel segment due to weaker consumer sentiment in Hong Kong, rising competition and safety concerns.

■ We like the effort to grow its online platform but the potential earnings impact may be too small to offset the decline in the traditional print segment.

■ Maintain Reduce and RM0.64 target price, based on 9x CY17F P/E. ■ Switch to Astro for better exposure to the media sector and lower sensitivity to adex.

No surprises from 4QFY16 results briefing MCIL held its 4QFY16 results briefing this morning for approximately 15 analysts and fund managers, hosted by group CEO Francis Tiong and Executive Director Patrick Leong. There were no surprises from the briefing as management reiterated its cautious outlook given the poor consumer sentiment in Malaysia following the goods and services tax (GST) implementation, and soft advertising environment in Hong Kong.

Expect another challenging year in FY17 In addition, management expects FY17 to be another challenging year for the group amidst the soft advertising environment both in the domestic and international markets. We agree with management as we expect consumer sentiment to stay weak for the remaining of 2016, and this could be a de-rating catalyst. We forecast flat adex growth in FY17 and 3% growth in FY18. However, we expect MCIL’s print adex to contract by 3-5% in FY17-18 due to the structural shift from print to digital platforms.

Muted prospects for travel segment Following the strong travel segment performance in FY16, management expects a more challenging outlook for the segment in FY17 in view of the weaker consumer sentiment in Hong Kong, coupled with rising competition from the online segment and safety concerns due to increasing terrorist activities globally.

Growing its digital platform Nevertheless, we are encouraged by the positive traction from its e-commerce portal “LogOn”, for which it has successful acquired 1.4k merchants as at Mar 2016. Management also plans to launch two new mobile applications for healthcare and event directory providers in Hong Kong. While we like the effort to grow its online business, we remains wary of its monetisation strategy as the potential earnings impact from digital may be too small to offset the decline in the traditional print segment.

Maintain Reduce and target price We maintain our Reduce rating and RM0.64 target price, based on 9x CY17F P/E, 40% discount to our target market P/E of 15x. While the stock offers attractive FY17/18 dividend yields of 5.7%/5.8%, we prefer Astro for greater exposure to the media sector due to its defensive earnings structure and lower sensitivity to adex. Key upside risks to our Reduce call are stronger adex recovery and pick-up in travel package sales.

▎Malaysia

REDUCE (no change) Consensus ratings*: Buy 1 Hold 1 Sell 1

Current price: RM0.74 Target price: RM0.64 Previous target: RM0.64

Up/downside: -13.6% CIMB / Consensus: -0.7%

Reuters: MDCH.KL Bloomberg: MCIL MK Market cap: US$301.3m RM1,240m Average daily turnover: US$0.05m RM0.22m Current shares o/s: 1,687m Free float: 45.1% * Source: Bloomberg Key changes in this note

No changes.

Source: Bloomberg

Price performance 1M 3M 12M Absolute (%) 1.4 12.2 18.5 Relative (%) 4 13.7 25.2

Major shareholders % held Tan Sri Datuk Tiong Hiew King 50.0 EPF 4.9

Analyst(s)

Mohd Shanaz NOOR AZAM

T (60) 3 2261 9078 E [email protected]

[ X ]

SOURCE: COMPANY DATA, CIMB FORECASTS

Financial Summary Mar-15A Mar-16A Mar-17F Mar-18F Mar-19F

Revenue (RMm) 1,675 1,362 1,376 1,403 1,424Operating EBITDA (RMm) 277.0 205.4 207.4 211.6 208.8Net Profit (RMm) 122.6 104.0 117.3 119.7 117.0Core EPS (RM) 0.090 0.066 0.069 0.071 0.069Core EPS Growth (15.0%) (26.6%) 5.0% 2.1% (2.3%)FD Core P/E (x) 8.15 11.11 10.58 10.36 10.60DPS (RM) 0.029 0.043 0.042 0.043 0.043Dividend Yield 3.96% 5.87% 5.67% 5.79% 5.90%EV/EBITDA (x) 4.74 5.67 5.40 5.11 4.98P/FCFE (x) 7.25 7.28 11.38 12.01 11.90Net Gearing 5.8% (11.4%) (15.6%) (18.8%) (21.9%)P/BV (x) 1.52 1.49 1.41 1.34 1.28ROE 18.7% 13.5% 13.7% 13.3% 12.3%% Change In Core EPS Estimates 0% 0% 0%CIMB/consensus EPS (x) 3.66 3.73

86.0

97.3

108.5

119.8

131.0

0.400

0.500

0.600

0.700

0.800Price Close Relative to FBMKLCI (RHS)

1

2

3

Jun-15 Sep-15 Dec-15 Mar-16

Vol m

15

Construction│Malaysia│Equity research│May 31, 2016

Company Note

IMPORTANT DISCLOSURES, INCLUDING ANY REQUIRED RESEARCH CERTIFICATIONS, ARE PROVIDED AT THE END OF THIS REPORT. IF THIS REPORT IS DISTRIBUTED IN THE UNITED STATES IT IS DISTRIBUTED BY CIMB SECURITIES (USA), INC. AND IS CONSIDERED THIRD-PARTY AFFILIATED RESEARCH.

Powered by the EFA Platform

Muhibbah Engineering More than meets the eye

Annualised 1Q16 core net profit was largely in line at 91-95% of our and consensus’ ■full-year numbers. We expect stronger quarters ahead.

Strong turnaround in infra; 154% yoy surge in earnings in 1Q16. ■ Shipyard/vessel building division is seeing signs of recovery, with new contracts in ■the pipeline. Capacity still below its peak.

Rapid contracts are likely to make a comeback with larger value jobs. ■ Positive 2H16 outlook with scope for earnings expansion. Add maintained. ■

1Q16 results in line – stronger quarters ahead Annualised 1Q16 core net profit made up 95% of our full-year forecast and 91% of the consensus number. The results were broadly in line, with strong turnaround numbers for the infra segment where pretax profit jumped 154% yoy on the back accelerated billings for specialised projects in Rapid. We expect stronger quarters ahead, with the shipyard segment beginning to recover, and the 21%-owned Cambodian airport concession on track to contributing an all-time high associate profit in FY16.

Contract flows YTD decent; more wins in 2H16? We retain our targeted RM800m worth of new contracts for FY16. YTD, the RM157m total wins (based on effective JV stakes) was relatively small, but margins are likely to be lucrative. With ample capacity to take on highway jobs, Muhibbah has tendered for at least two packages for the Dash and Suke highways. We continue to expect recovery in order flows from Petronas’s Rapid, as higher-value jobs relevant to Muhibbah’s track record could be up for awards. Outstanding order book stands at RM2.1bn (US$522m).

Shipyard division on the road to recovery? There already signs of a recovery for the group’s shipbuilding division, which has a track record of building vessels at its yard in Telok Gong, Klang, before orders deteriorated due to the slump in offshore oil & gas activities. The group recently won a maiden vessel order for the Malaysian Marine Department worth RM92m. We think this could be the start of more new orders from other non-oil & gas clients. The group’s vessel building capacity has more room for upside in 2016 and could turn around in 2017.

Private placement in the works The 10% share placement would raise as much as RM111m in proceeds, based on a hypothetical issue price of RM2.32/share (2.11% discount to 5-day VWAMP). 75% of the amount will be utilised to partially repay debt while the balance is earmarked for working capital. We estimate up to a 7% dilution to our current RNAV of RM4.23/share, and 5-7% dilution to FY16-18F EPS after taking into account interest income from the proceeds and the enlarged share base. The placement is targeted to complete by 4Q16.

Positive 2H16 outlook; maintain Add Muhibbah remains our top mid-cap sector pick. We retain our FY16-18 EPS forecasts but cut our RNAV-based target price as we update for the lower market cap of Favelle Favco (cranes business). We continue to peg our target price to a 30% discount to RNAV, which implies an attractive upside of 35%. Key medium term catalysts include a pickup in infra wins and a recovery in order flow for the shipyard division driven by new prospects from the non-oil & gas space, in our view. Downside risk is delays in job wins.

▎Malaysia

ADD (no change) Consensus ratings*: Buy 6 Hold 0 Sell 0

Current price: RM2.19 Target price: RM2.96 Previous target: RM3.03

Up/downside: 35.2% CIMB / Consensus: -1.4%

Reuters: MUHI.KL Bloomberg: MUHI MK Market cap: US$251.3m RM1,034m Average daily turnover: US$0.32m RM1.28m Current shares o/s: 469.2m Free float: 72.5% * Source: Bloomberg Key changes in this note

No changes

Source: Bloomberg

Price performance 1M 3M 12M Absolute (%) -6.8 -4 -9.5 Relative (%) -4.2 -2.5 -2.8

Major shareholders % held Mac Ngan Boon 17.0 Lembaga Tabung Haji 10.6

Analyst(s)

Sharizan ROSELY

T (60) 3 2261 9077 E [email protected]

[ X ]

SOURCE: COMPANY DATA, CIMB FORECASTS

Financial Summary Dec-14A Dec-15A Dec-16F Dec-17F Dec-18F

Revenue (RMm) 1,693 1,599 1,988 2,187 2,406Operating EBITDA (RMm) 170.3 185.8 248.4 273.2 253.9Net Profit (RMm) 81.6 85.6 98.7 112.8 129.6Core EPS (RM) 0.17 0.18 0.21 0.24 0.28Core EPS Growth (4.2%) 4.9% 15.3% 14.4% 14.8%FD Core P/E (x) 12.59 12.01 10.42 9.11 7.93DPS (RM) 0.040 0.050 0.055 0.060 0.060Dividend Yield 1.83% 2.28% 2.51% 2.74% 2.74%EV/EBITDA (x) 9.65 8.58 6.43 5.69 5.96P/FCFE (x) 3.11 3.48 3.19 2.46 2.32Net Gearing 73.8% 65.0% 59.0% 51.9% 45.6%P/BV (x) NA NA NA 38.90 10.57ROE 13.5% 13.3% 15.2% 16.9% 18.3%% Change In Core EPS Estimates 0% 0% 0%CIMB/consensus EPS (x) 0.96 0.95 0.94

74.0

90.7

107.3

1.50

2.00

2.50

Price Close Relative to FBMKLCI (RHS)

2

4

6

Jun-15 Sep-15 Dec-15 Mar-16

Vol m

16

Food & Beverages│Malaysia│Equity research│May 31, 2016

Company Note