equity valuation of dscl

TRANSCRIPT

Value Analysis

Of

D.S Construction Ltd.

As On 2nd April 2009

Nipun Mahajan

Financial Analyst

+91-9971319385

V alue A nalysis of D SCL

2 | P a g e

Table of Contents

Topic Page No.

Background 3

Industry Analysis 4

Research Methodology 5

Valuation Methodology 6

Valuation of DSCL

� Valuation of EPC 7

� Valuation of SPV 10

� Valuation of Hydro Electric projects 26

Summary 28

Limitations 29

V alue A nalysis of D SCL

3 | P a g e

Background

D.S Constructions Ltd. DSCL is a part of DS group of companies, came

into existence in 1978.

DSCL is a part of the USD 3 billion D S Group with interests in retail &

trading, real estate development, hospitality, construction &

infrastructure development across 5 continents, DSCL is a pioneer in

BOT infrastructure development and engineering with projects under

execution in the Highways, Expressways & Railway, Hydro Power and

now pursuing Privatization of Airports & Ultra Mega Power Projects,

Special Economic Zones, etc. in a short span of 5 years.

It’s Business

� Engineering, Processing & Construction (EPC) business: It handles

EPC business for various infrastructure projects, Special Purpose

Vehicles viz. Roads, Railways & Urban infrastructure.

� Investment in SPV’s: DSCL has made investment in following eight

Special Purpose Vehicles (SPV)

� Hydro Business: DSCL has recently got two hydro electric projects

V alue A nalysis of D SCL

4 | P a g e

Industry Analysis

Key Characteristics

Comparative low project risk.

The infrastructure segment is expected to see investments of Rs 4356 billion till

2009, as compared to Rs 3320 billion

According to a recent report by Cris Infac on Indian construction industry,

government's spending on infrastructure has increased by 106 percent to Rs

8,163 billion in the tenth plan period compared to Rs 3959 billion during the

ninth plan period.

Competitive pricing due to competitive bidding in government projects.

Implementation of the build-operate-transfer (BOT), build-own-operate-transfer

(BOOT) mechanism by the government has generated interest from the private

sector and a lot of projects in the road and hydropower segments are already

underway.

Over Rs 380 billion will be spent on hydropower projects, resulting construction

contracts worth almost Rs 266 billion in the next five years.

Roads, urban infrastructure are expected to be still the key for investment in

infrastructure sector.

V alue A nalysis of D SCL

5 | P a g e

Research Methodology

The data collection includes both primary and secondary data collection methods.

Primary Method:

The profit & loss a/c & balance sheets for the year 2004-05 ,2005-06,2006-07

provided by DSCL.

The financial models, projections along with industrial& business analysis are

used to valuation.

Secondary Method:

Reports of various agencies such as CRISIL, RBI, FICCI etc.

Websites referred:

� www.dsconstructions.com

� www.rbi.org.in

� www.ficci.com

� www.crisil.com

6 | P a g e

The Valuation of DSCL is classified according to the type of the business they are

undertaking.

EPC

SPV

Hydro

Equity Valuation of EPV

Equity Valuation of SPV

Equity VAluation of Hydro Electric

Projects

V alue A nalysis of D SCL

Valuation Methodology

The Valuation of DSCL is classified according to the type of the business they are

• Equity Valuation of EPV business for various SPV

• Method Used market multiple i.e EV/EBDIT & PAT*P/E

• Equity Valuation of Investment made in Eight Projects

• Discounting Cash Flow to Equity (DCFE) method

• Equity valuation of Hydro power business

Equity Valuation

Equity Valuation

Equity VAluation of Hydro Electric

Equity Valuation of

DSCL

The Valuation of DSCL is classified according to the type of the business they are

Equity Valuation of EPV business

Method Used market multiple i.e

Equity Valuation of Investment

Discounting Cash Flow to Equity

Equity valuation of Hydro power

V alue A nalysis of D SCL

7 | P a g e

Valuation of DSCL

I) Valuation of EPC Business

D S Constructions Ltd. through its ability to think BIG & DELIVER

innovative and selective strategy has established itself as one of

prominent player in the infrastructure development sector in India.

DSCL is a pioneer in BOT infrastructure development and

engineering with projects under execution in the Highways,

Expressways & Railway, Hydro Power and now pursuing

Privatization of Airports & Ultra Mega Power Projects, Special

Economic Zones, etc. in a short span of 5 years.

The valuations approach:

Therefore for the purpose of valuation of SPV business it is

assumed that it as at par with the industry (construction-large

turnkey projects)

The market multiple method and P/E multiple of the industry

(includes 10 players).

Two methods have been used

i. EV/EBDIT Multiple

ii. P/E * PAT

Since DSCL is considered to be at par with industry, the Industry

EV/ EBDIT Multiple and industry P/E are treated as benchmark

for the computation.

V alue A nalysis of D SCL

8 | P a g e

Method 1 Industry Data for 3 months (jan-mar08) Particulars Amount in Rs. Cr EBDIT 3621.54 Mkt. Capitalization 62437.00 EV/EBDIT Multiple 17.24

EBDIT of DSCL 150

Market multiple 17.5

EV 2625

Less

Quasi equity treated as debt 563

Net Value 2062

Less Illiquidity Discount @ 25% 515.5

Equity Value 1546.5

Method 2 Industry P/E 53.88

*PAT of DSCL 45

Book Value 2424.6

Less

Quasi equity treated as debt 563

Net Value 1861.6

Less Illiquidity discount @25% 465.4

Equity Value 1396.2

Therefore the value of DSCL EPV Business is estimated as Rs.1469.43

V alue A nalysis of D SCL

9 | P a g e

Notes:

i. *Refer Annexure 1: Balance Sheet & Profit & Loss A/c of DSCL

ii. Illiquidity discount: Since the company is unlisted, the illiquidity discount is

treated as 25%.

iii. The valuation is exclusive of quasi equity which is treated as debt.

iv. Applied EV/EBDIT multiple is 17.5

10 | P a g e

II) Valuation of SPV Business

The valuation of SPV Business includes individual valuation of eight projects

The Methodology:

Method DCFE

FCFE=

Net Income + DepreciationExpenditure-increase in Working Cap+debt InfusionRepayments

The FCFE is discounted at expected rate of return by equity capital provider

Discounting Rate Risk Free Rate + Market Risk Premium

Risk Free Rate =7.75

Risk Premium=

Average Int. volatility

Discounting rate lower limit of the sector

Discounting rate upper limit of the sector

For valuation the discounting rate

Project Time Period

2 Years Old

1 Year Old

Up to 6 Months To Complete

6-12 Months to Complete

Above 1Year Note: 1. Average 5 year construction sector equity return 2.The discounting rate varies from project to project 3. For risk premium average beta is 0.7 4. Few projects of DSCL have already been completed & few are in WIP

V alue A nalysis of D SCL

Business

The valuation of SPV Business includes individual valuation of eight projects

Discounted Cash Flow To Equity

Net Income + Depreciation- Capital increase in Working

Cap+debt Infusion- debt

The FCFE is discounted at expected rate of return by equity capital provider

Risk Free Rate + Market Risk Premium

Interest Rate on Long Term Govt. Securities Source (www.rbi.org.in)

4.25

Beta ( Expected market return of the similar listed CompanyRate)

of the sector

of the sector

For valuation the discounting rate range is 10.5%-14%

Discounting Rate (%)

10.5

11.5

12.5

13.5

14 Note: 1. Average 5 year construction sector equity return

2.The discounting rate varies from project to project 3. For risk premium average beta is 0.7 . Few projects of DSCL have already been completed & few are in WIP

DGSCL

KMPE

LS

Raipur Express

DSC Ventures

Gwalior Jhansi Express Way

VMPL

Sandur Bypass Project

The valuation of SPV Business includes individual valuation of eight projects

Discounted Cash Flow To Equity

Interest Rate on Long Term Govt. Securities Source (www.rbi.org.in)

Beta ( Expected market return of the similar listed Company- Risk free

0.65

11.35

12.65

V alue A nalysis of D SCL

11 | P a g e

a) Delhi Gurgaon Super Connectivity Ltd.

D S Constructions Ltd. was awarded this project and commenced work in

January 2003. It was the first BOT project to be awarded on a negative

grant (INR 610.6 Million). The project envisaged conversion of the Delhi-

Gurgaon Section of NH-8 into an access controlled 6/8-lane highway with

service lanes across certain sections & strengthening of existing lane from

Km 14.3 to Km 42, falling partly in Delhi and Haryana

PROJECT DGSCL PARTICULARS RS. Cr COST 1053

Equity 371

Loan 483

Grant (cash basis) 199

Toll start date Jan-08

concession period ends Jan-23

Share Capital

Authorised Capital 164.2

Paid Up Capital 144.26

Share Holding %

D.S Construction Ltd 79.08

Alphametic Investments Ltd, UK 19.51

Jai Prakash Associates Ltd 1.41

V alue A nalysis of D SCL

12 | P a g e

FCFE projections

Year End 31-mar FCFE

2008 4

2009 83.1

2010 100.7

2011 119.1

2012 139.2

2013 178.18

2014 228.07

2015 291.92

2016 373.66

2017 478.29

2018 612.21

2019 783.63

2020 1003.04

2021 1003.04

2022 1003.04

2023 1003.04

The FCFE is projected after industry

analysis, historical data and future potential

estimates.

The discounting rate is 12.5%.

The project requires 4-6 months for its

completion.

The Equity Valuation of this project on the basis

of discounting of FCFE projections till

concession period is estimated at Rs.1153.95

Cr.

V alue A nalysis of D SCL

13 | P a g e

b) Kundli-Manesar-Palwal Expressway (KMPE)

The KMP Expressway, also known as the western peripheral expressway is

the largest expressway project in the country on Build Operate Transfer

(BOT) basis. Out of the total cost of INR 19,150 Million, a debt of INR 11,490

Million has been tied up through a consortium of 12 banks/financial

institutions led by IDBI Ltd. KMP Expressway project on BOT basis

envisages construction of the 135.6 Km, access controlled expressway from

NH-1 near Kundli (Sonipat) crossing NH-10 at west of Bahadurgarh,

crossing NH-8 at Manesar (Gurgaon) and joining NH-2 near Palwal

(Faridabad).

PROJECT KMP Expressway Project

Particulars In Rs./Cr

Total Cost 1950

Equity 801

Loan 1149

Concession period

23 years 9 months Includes 36 construction months

Share Capital Rs.Cr

Authorized Capital 0.1

Paid up cap 0.1

Share Holding Pattern % D.S Constructions Ltd. 67 Apollo Enterprises Ltd UK 33

V alue A nalysis of D SCL

14 | P a g e

Year End 31-mar FCFE

2008 51.8

2009 -347.8

2010 -180.9

2011 26.9

2012 64.2

2013 84.7

2014 111.9

2015 147.7

2016 194.9

2017 257.3

2018 339.6

2019 448.3

2020 591.7

2021 781.1

2022 1031.0

2023 1361.0

2024 1796.5

2025 2371.4

2026 3130.2

2027 3130.2

2028 3130.2

2029 3130.2

2030 3130.2

The FCFE is projected after industry

analysis, historical data and future

potential estimates.

The discounting rate is 14%.

The project requires 2 years for its

completion.

The Equity Valuation of this project on the basis of

discounting of FCFE projections till concession

period is estimated at Rs.468 Cr

V alue A nalysis of D SCL

15 | P a g e

c) Lucknow Sitapur Highway

The work involves improvement, operation and maintenance, including

strengthening and widening of the existing 2-lane road into 4-lane from Km

413.20 to Km 489.13 on NH-24. The total number of structures is 92

including one major bridge, 4 minor bridges along with 5 vehicular

underpasses.

Once completed, the project will enhance the accessibility of Western UP,

Uttaranchal, Northern Haryana, Punjab, Himachal Pradesh and Jammu &

Kashmir to the East-West Corridor and the Golden Quadrilateral.

PROJECT Lucknow Sitapur Expressway Ltd

Particulars Rs.Cr

Total Cost 375.00

Equity 113.00

Loan 262.00

Concession Period

20Years Including 36 months of Construction

Share Capital Rs.Cr

Authorized Capital 1.00

Paid Up Capital 1.00

V alue A nalysis of D SCL

16 | P a g e

FCFE Projections Year End 31-mar FCFE

2008 -33.10

2009 -31.30

2010 12.30

2011 19.80

2012 24.50

2013 31.85

2014 41.41

2015 53.83

2016 69.97

2017 90.97

2018 118.26

2019 153.73

2020 199.85

2021 259.81

2022 337.75

2023 439.08

2024 439.08

2025 439.08

2026 439.08

The FCFE is projected after industry

analysis, historical data and future

potential estimates.

The discounting rate is 14%.

The project requires 2 years for its

completion.

The Equity Valuation of this project on the basis of

discounting of FCFE projections till concession

period is estimated at Rs.126.53 Cr

V alue A nalysis of D SCL

17 | P a g e

d) Raipur Aurang Highway

The work involves improvement, operation and maintenance, rehabilitation

and strengthening of the existing 2-lane road into 4-lane starting from Km

239 to Km 282 on NH 6.

This road project joined with Durg-Raipur Expressway, already completed

by the Company, will be the first high speed urban expressway in

Chattisgarh linking Raipur with the surrounding industrial areas.

PROJECT Raipur Expressways

Particulars Rs.Cr

Total Cost 262

Equity 79

Loan 183

Concession Period

25 years including 30 months of construction period

Share Capital Rs.Cr

Authorised Cap 1.00

Paid Up Capital 1.00

V alue A nalysis of D SCL

18 | P a g e

FCFE Projections

Year End 31-mar FCFE

2008 -32.6

2009 6.2

2010 13.2

2011 16.1

2012 21.1

2013 34.0

2014 49.7

2015 68.7

2016 91.5

2017 118.7

2018 150.6

2019 188.0

2020 231.2

2021 281.0

2022 337.8

2023 402.4

2024 475.3

2025 557.3

2026 649.0

2027 649.0

2028 649.0

2029 649.0

2030 649.0

2031 649.0

The FCFE is projected after industry

analysis, historical data and future

potential estimates.

The discounting rate is 13.5%.

The project requires 1 year for its

completion.

The Equity Valuation of this project on the basis of

discounting of FCFE projections till concession

period is estimated at Rs.426 Cr

V alue A nalysis of D SCL

19 | P a g e

e) DSC Ventures Private Ltd.

The work entailed 4 laning of the existing 2-lane carriageway on the Raipur-

Durg section of NH-6 in Chattisgarh state. It connects Chhattisgarh with

Vishakapatnam, one of the most important ports of India and Mumbai, the

financial capital of the country, with Kolkata (Eastern / North Eastern

Markets). This project has ensured that this important route is decongested

thereby substantially speeding up the movement of goods and help in easing

the flow of traffic into the region. Over 18,000 vehicles are using the

highway every day.

PROJECT

DSC Ventures Private Ltd.

Particulars Rs.Cr

Total Cost 114.00

Equity 36.05

Loan 77.95

Concession Period Ends

march end 2015

Share Capital Rs. Cr

Authorised Cap 27.00

Paid Up Capital 27.00

FCFE Projections

Year End 31-mar FCFE

2008 15.7

2009 16

2010 18.5

2011 22.3

2012 21.5

2013 40.10

2014 61.25

2015 85.86

The FCFE is projected after industry

analysis, historical data and future

potential estimates.

The discounting rate is 11.5%.

The project is complete.

The Equity Valuation of this project on the basis of

discounting of FCFE projections till concession

period is estimated at Rs. 56.15 Cr

V alue A nalysis of D SCL

20 | P a g e

f) Gwalior Jhansi Highway

The work on the project entails design, construction, development, finance,

operation and maintenance of the project, including rehabilitation and

upgradation from the existing 2 lanes to 4 lanes, of Gwalior-Jhansi section

from Km 16 to 96 on NH-75 under North-South Corridor (NHDP – Phase II)

in the states of Uttar Pradesh and Madhya Pradesh. The scope of work

includes construction of three major bridges (1 two-lane Bridge and the

other 2 are four-lane bridges), 21 minor bridges, 1 4-lane flyover, 99

culverts, a bypass at Takenpur & Dabar and Service Roads on each side of

the highway.

Project Gwalior Jhansi Expressway Limited

Particulars Rs.Cr

Total Cost 721.3

Equity 504.92

Loan 216.38

Concession Period Ends

mar end 2027

Share Capital Rs.Cr

Authorised Cap 0.05

Paid Up Capital 0.05

Share Holding %

DS Constructions Ltd 100

V alue A nalysis of D SCL

21 | P a g e

FCFE Projections

Year End 31-mar FCFE

2008 40.9

2009 -45.6

2010 -86.1

2011 7.9

2012 10.8

2013 21.7

2014 36.2

2015 55.2

2016 79.5

2017 109.9

2018 147.3

2019 192.7

2020 246.9

2021 311.1

2022 386.3

2023 473.6

2024 574.4

2025 574.4

2026 574.4

2027 574.4

The FCFE is projected after industry

analysis, historical data and future

potential estimates.

The discounting rate is 12.5%.

The project requires 6 months for its

completion.

The Equity Valuation of this project on the basis of

discounting of FCFE projections till concession

period is estimated at Rs.22.44 Cr

V alue A nalysis of D SCL

22 | P a g e

g) Viramgam-Mahesana Gauge Conversion Project

The Viramgam-Mahesana gauge conversion project is the first Railway BOT

Project in India. This is one of the pilot projects for the Indian Railways The

success of this project has in large extent determined the future of privately

financed railway projects in India. The work envisaged is the conversion of

the present Metric Gauge into Broad Gauge track between Viramgam and

Mahesana in the Gujarat section of the Western Railway territory in India.

The complete length of track is 65 Kilometers.

Project Viramgam Mahsena Projecy Limited

Particulars Rs.Cr

Total Cost 102.00

Equity 27.00

Loan 63.00

Concession Period Ends 2017

Share Capital Rs.Cr

Authorized Capital 27.00

Paid Up Capital 27.00

Share Holding Pattern %

DS Constructions Ltd 100

FCFE Projections

Year End 31-mar FCFE

2008 5.50

2009 11.30

2010 13.56

2011 16.27

2012 19.53

2013 23.43

2014 28.12

2015 28.12

2016 28.12

2017 28.12

The FCFE is projected after industry

analysis, historical data and future

potential estimates.

The discounting rate is 10.5%.

The project is completed in 2004

The Equity Valuation of this project on the basis of

discounting of FCFE projections till concession

period is estimated at Rs.17.7 Cr

V alue A nalysis of D SCL

23 | P a g e

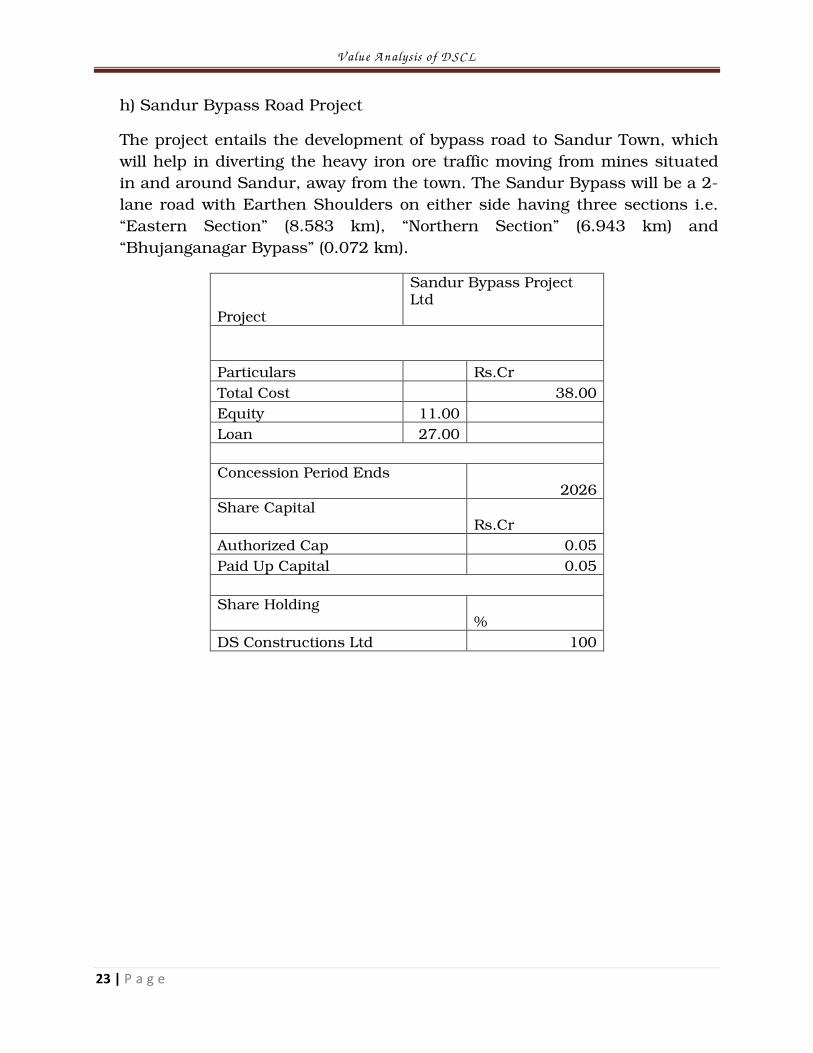

h) Sandur Bypass Road Project

The project entails the development of bypass road to Sandur Town, which

will help in diverting the heavy iron ore traffic moving from mines situated

in and around Sandur, away from the town. The Sandur Bypass will be a 2-

lane road with Earthen Shoulders on either side having three sections i.e.

“Eastern Section” (8.583 km), “Northern Section” (6.943 km) and

“Bhujanganagar Bypass” (0.072 km).

Project

Sandur Bypass Project Ltd

Particulars Rs.Cr

Total Cost 38.00

Equity 11.00

Loan 27.00

Concession Period Ends 2026 Share Capital Rs.Cr

Authorized Cap 0.05

Paid Up Capital 0.05

Share Holding %

DS Constructions Ltd 100

V alue A nalysis of D SCL

24 | P a g e

FCFE Projections

Year End 31-mar FCFE

2008 2.40

2009 4.70

2010 4.90

2011 5.50

2012 6.10

2013 7.02

2014 8.07

2015 9.28

2016 10.67

2017 12.27

2018 14.11

2019 16.23

2020 18.66

2021 21.46

2022 24.68

2023 28.38

2024 28.38

2025 28.38

2026 28.38

2027 28.38

The FCFE is projected after industry

analysis, historical data and future

potential estimates.

The discounting rate is 12.5%.

The project requires 2 months for its

completion.

The Equity Valuation of this project on the basis of

discounting of FCFE projections till concession

period is estimated at Rs.42.61 Cr

V alue A nalysis of D SCL

25 | P a g e

Equity Valuation of Special Purpose Vehicles

Project Equity Value

DSCL & its affairs Stake

Effective Value (In Cr)

DGSCL 1153.95 79.08 912.54

KMPE 468.00 96.1 449.75

LS 126.53 91.5 115.77

Raipur Exp 426.00 96.4 410.66

DSC Ventures 56.15 100 56.15

Gwalior Jhansi Exp Way 22.44 100 22.44

Virangam Mehsana 17.70 100 17.70

Sandhur Bypass 42.61 100 42.61

Total 2313.38 763.08 2027.63 less Illiquidity Discount @ 25% 506.91

Net Value 1520.72

V alue A nalysis of D SCL

26 | P a g e

III) Valuation of Hydro Electric Project

Projects in Hand

1. 260 MW Kutehr Hydro Electric Project (Chamba H.P)

Date of LOI Jan 2007 Capacity 260 MW (86.67 x 3)

Generation 1075.26 GWH Nature of contract Independent Power producer

Concession period 40 Years Investment Rs.1058.2Cr

The company has recently emerged as a successful Independent Power

Producer by winning the bid to develop, construct and operate the Kutehr

Hydro Project (260 MW) in the State of Himachal Pradesh amongst stiff

competitive bidding by 8 National and International players. D S Constructions

has made a bid for an up-front payment of INR 5.2 Million per MW for this

project.

The Company has already started the process of preparation of the Detailed

Project Report and subsequently the construction work on this project will be

completed over a period of 7 years from date of financial closure. The

concession period for the project is 40 years. Under the contract, 12% of the

power is to be given free to the State of Himachal Pradesh for the first 12 years,

18% for the 13th to 30th year, 30% for 31st to 40th year. DSCL can sell the

remaining power to any State in India

V alue A nalysis of D SCL

27 | P a g e

2. 1000 MW Naying Hydro Electric Project

Date of LOI Jan 200

Capacity 1000 MW Generation 4966.77 MU

Nature of contract BOT

Concession period 40 Years Investment Rs.5000Cr

The Naying Hydro Electric Project will be constructed on the Siyom River in

West Siang District of Arunachal Pradesh at an approximate cost of Rs. 5,000

crores through a SPV. The Project Cost anticipated as per Pre Feasibility Report

is Rs. 3,100 crores.

The SPV will have 89% equity participation by DSCL and 11% equity

participation by the State of Arunachal Pradesh. The Company has already

started the process of preparation of the Detailed Project Report and

subsequently the construction work on this project will be completed over a

period of 8 years. The concession period for the project is 40 years.

The Hydro projects are optimistically valued at Rs 270Cr till date

Note: Current Status: DPR in Progress

V alue A nalysis of D SCL

28 | P a g e

Summary

Valuation of DS Constructions Ltd.

Business Value Rs.Cr Valuation of EPC 1469.43

Valuation of Investments in SPV 1520.72 Valuation of Hydro Business 270

Total Valuation 3260.05

V alue A nalysis of D SCL

29 | P a g e

Limitations

The valuation is done on the basis of the data provided by the concern

The reliance is shown on the audited and unaudited financial

statements (may/may not be treated as benchmark for valuation).

The use of historical data, projections and valuation on the basis of it

may not accurate as uncertainty of future can’t be challenged.