erc andrew marquard and harald winkler a carbon tax for south africa? energy research centre...

TRANSCRIPT

ERC

Andrew Marquard and Harald Winkler

A Carbon tax for South Africa?A Carbon tax for South Africa?

Energy Research Centre University of Cape Town

Presentation at a side event on PUTTING A PRICE ON CARBON at the 2009 Climate Change Summit

Tuesday 3 March 2009

ERC

Why would we institute a carbon tax?Why would we institute a carbon tax?

To provide an economic incentive for reducing GHG To provide an economic incentive for reducing GHG emissionsemissions

This would (ideally) have two effects:This would (ideally) have two effects: A demand effect, which would incentivise A demand effect, which would incentivise

consumers to use less GHG-emitting goods and consumers to use less GHG-emitting goods and servicesservices

A substitution effect, which would incentivise A substitution effect, which would incentivise switching from more to less carbon-intensive switching from more to less carbon-intensive processes / energy carriersprocesses / energy carriers

As a result, the economy would ultimately shift from a As a result, the economy would ultimately shift from a high-carbon to a low-carbon economy (ideallyhigh-carbon to a low-carbon economy (ideally

ERC

Is it this easy?Is it this easy?

Not very:Not very:

Need to make important decisions, such as:Need to make important decisions, such as: scope of tax (which sectors and gases to include)scope of tax (which sectors and gases to include) tax level (how many Rands/ton of COtax level (how many Rands/ton of CO22-eq) -eq) What to do with the revenueWhat to do with the revenue How to relate to other taxes (revenue neutrality)How to relate to other taxes (revenue neutrality)

Different sectors respond differently, depending on Different sectors respond differently, depending on available lower-carbon alternatives and their costsavailable lower-carbon alternatives and their costs

Different parts of society are affected differently Different parts of society are affected differently (distributional effects), which needs to be taken into (distributional effects), which needs to be taken into accountaccount

ERC

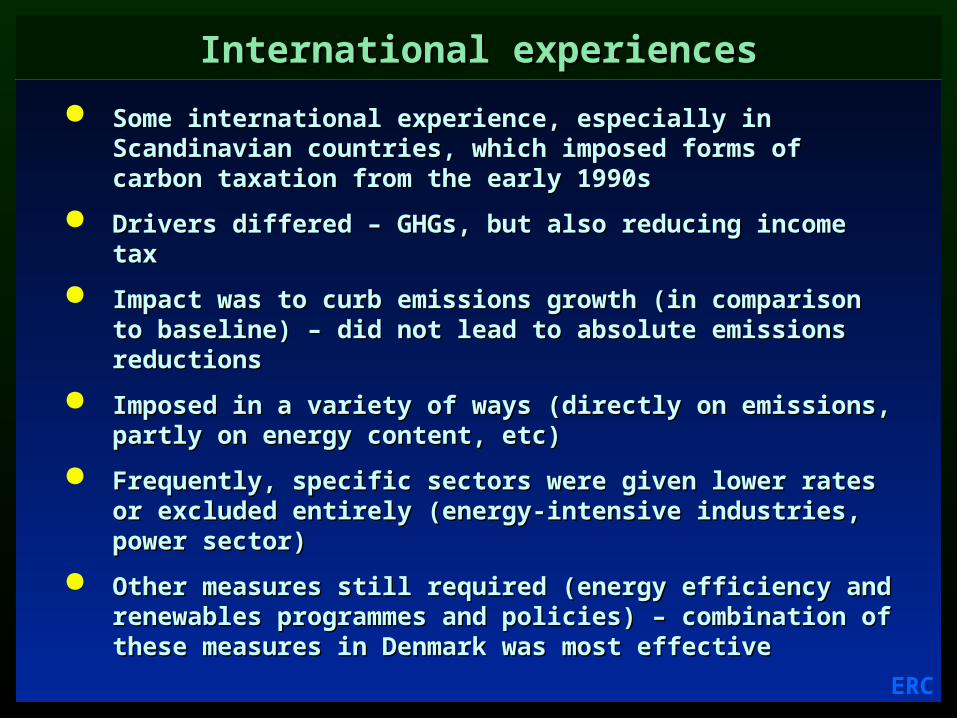

International experiencesInternational experiences

Some international experience, especially in Scandinavian Some international experience, especially in Scandinavian countries, which imposed forms of carbon taxation from the countries, which imposed forms of carbon taxation from the early 1990searly 1990s

Drivers differed – GHGs, but also reducing income taxDrivers differed – GHGs, but also reducing income tax

Impact was to curb emissions growth (in comparison to Impact was to curb emissions growth (in comparison to baseline) – did not lead to absolute emissions reductionsbaseline) – did not lead to absolute emissions reductions

Imposed in a variety of ways (directly on emissions, partly on Imposed in a variety of ways (directly on emissions, partly on energy content, etc)energy content, etc)

Frequently, specific sectors were given lower rates or Frequently, specific sectors were given lower rates or excluded entirely (energy-intensive industries, power sector)excluded entirely (energy-intensive industries, power sector)

Other measures still required (energy efficiency and Other measures still required (energy efficiency and renewables programmes and policies) – combination of renewables programmes and policies) – combination of these measures in Denmark was most effectivethese measures in Denmark was most effective

ERC

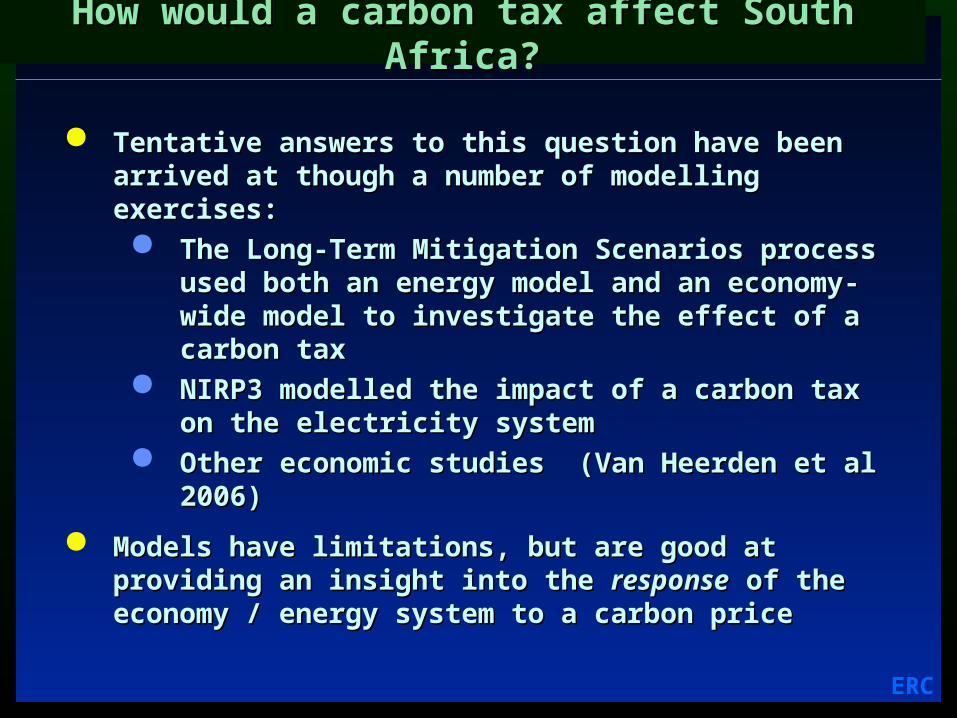

How would a carbon tax affect South Africa?How would a carbon tax affect South Africa?

Tentative answers to this question have been arrived at Tentative answers to this question have been arrived at though a number of modelling exercises:though a number of modelling exercises: The Long-Term Mitigation Scenarios process used The Long-Term Mitigation Scenarios process used

both an energy model and an economy-wide both an energy model and an economy-wide model to investigate the effect of a carbon taxmodel to investigate the effect of a carbon tax

NIRP3 modelled the impact of a carbon tax on the NIRP3 modelled the impact of a carbon tax on the electricity systemelectricity system

Other economic studies (Van Heerden et al 2006)Other economic studies (Van Heerden et al 2006)

Models have limitations, but are good at providing an Models have limitations, but are good at providing an insight into the insight into the responseresponse of the economy / energy of the economy / energy system to a carbon pricesystem to a carbon price

ERC

Impact of a CO2 tax on emissions (2003 Rands)Impact of a CO2 tax on emissions (2003 Rands)

ERC

Marginal impact of tax levels (2003 Rands)Marginal impact of tax levels (2003 Rands)

ERC

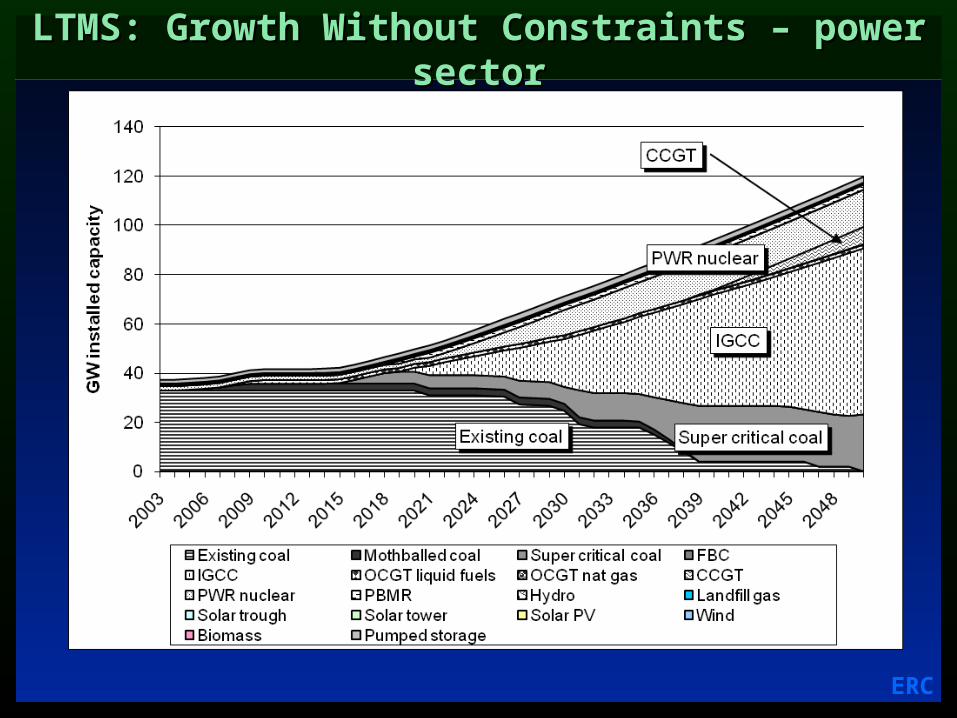

LTMS: Growth Without Constraints – power sectorLTMS: Growth Without Constraints – power sector

ERC

LTMS: impact of an escalating CO2 tax on the power sectorLTMS: impact of an escalating CO2 tax on the power sector

Existing coal

PWR nuclear

Solar towerWind

0

20

40

60

80

100

120

140

160

GW

in

stal

led

cap

acit

y

Existing coal Mothballed coal Super critical coal FBCIGCC OCGT liquid fuels OCGT nat gas CCGTPWR nuclear PBMR Hydro Landfill gasSolar trough Solar tower Solar PV WindBiomass Pumped storage

ERC

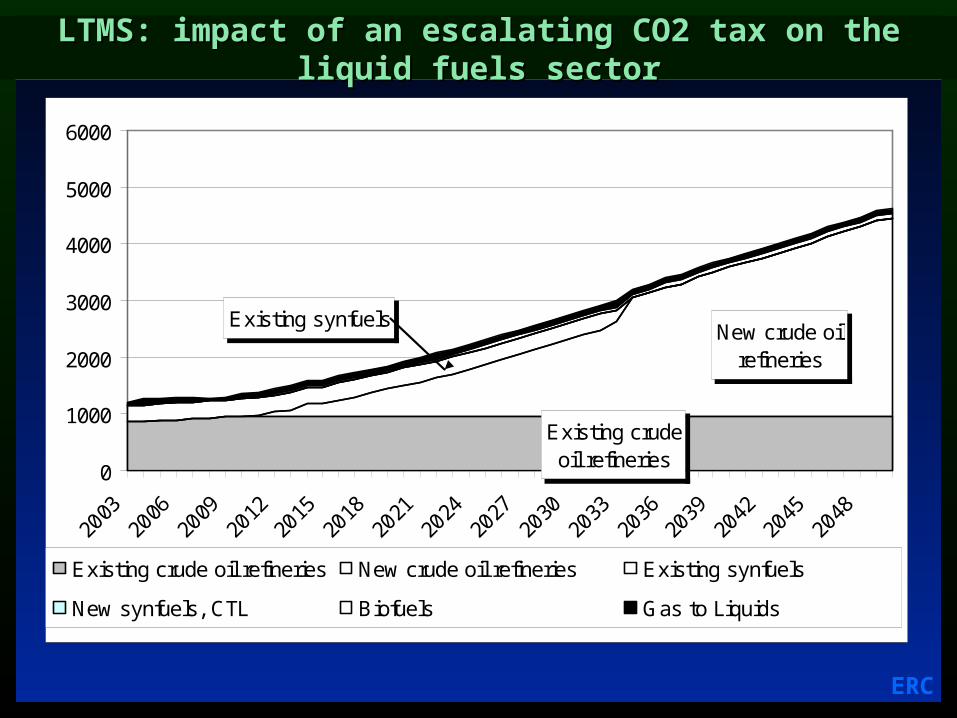

LTMS: Growth Without Constraints – liquid fuelsLTMS: Growth Without Constraints – liquid fuels

ERC

LTMS: impact of an escalating CO2 tax on the liquid fuels LTMS: impact of an escalating CO2 tax on the liquid fuels sectorsector

Existing crude oil refineries

New crude oil refineries

Existing synfuels

0

1000

2000

3000

4000

5000

6000

2003

2006

2009

2012

2015

2018

2021

2024

2027

2030

2033

2036

2039

2042

2045

2048

Existing crude oil refineries New crude oil refineries Existing synfuels

New synfuels, CTL Biofuels Gas to Liquids

ERC

Other model resultsOther model results

NIRP3 – modelled the electricity system, and found that NIRP3 – modelled the electricity system, and found that a tax level of R200/ton (2006 Rands) was sufficient to a tax level of R200/ton (2006 Rands) was sufficient to incentivise low-carbon alternativesincentivise low-carbon alternatives

Economy-wide modelling:Economy-wide modelling: LTMS static modelling – tax above R200 has LTMS static modelling – tax above R200 has

negative economic effects, but distributive effects negative economic effects, but distributive effects are positive up to R200 (2003 Rands)are positive up to R200 (2003 Rands)

LTMS dynamic modelling – impact of escalating LTMS dynamic modelling – impact of escalating tax is economically positive, employment effects tax is economically positive, employment effects positivepositive

Van Heerden et al – recycling revenue, e.g. food Van Heerden et al – recycling revenue, e.g. food price subsidies, leads to a ‘triple dividend’ (reduce price subsidies, leads to a ‘triple dividend’ (reduce GHGs, grow economy and reduce poverty)GHGs, grow economy and reduce poverty)

ERC

Policy issues to be addressedPolicy issues to be addressed

More detailed investigation of the effectiveness of a More detailed investigation of the effectiveness of a carbon tax in reducing GHG emissions carbon tax in reducing GHG emissions

Tax-setting and adjusting mechanismsTax-setting and adjusting mechanisms

Equity, distributional impacts and addressing poverty and Equity, distributional impacts and addressing poverty and developmentdevelopment

Combining a tax with incentives and recycling of revenuesCombining a tax with incentives and recycling of revenues

Legislative compatibilityLegislative compatibility

Technical and administrative viability, including the tax Technical and administrative viability, including the tax base and definitions of taxable events base and definitions of taxable events

Competitiveness effects and a structured approach to Competitiveness effects and a structured approach to energy-intensive exporting sectorsenergy-intensive exporting sectors

Adjoining policy areasAdjoining policy areas

ERC

3 Key Issues: 1 – setting the tax level3 Key Issues: 1 – setting the tax level

Problem is to set the lowest tax level which will achieve Problem is to set the lowest tax level which will achieve policy aims, i.e. incentivise economic behaviour in policy aims, i.e. incentivise economic behaviour in such a way that emissions follow a desired emissions such a way that emissions follow a desired emissions pathwaypathway

Therefore need to know cost of mitigation, but this is Therefore need to know cost of mitigation, but this is only know fully ex-postonly know fully ex-post

A solution to this problem is to have an adjustment A solution to this problem is to have an adjustment mechanism – set initial tax in accordance with mechanism – set initial tax in accordance with expected response, then adjust if emissions stray expected response, then adjust if emissions stray outside of preset bandsoutside of preset bands

Carbon price would react to emissions levels, as in a Carbon price would react to emissions levels, as in a carbon market, premised on responsiveness of carbon market, premised on responsiveness of economyeconomy

ERC

Tax adjustment mechanismTax adjustment mechanism

ERC

3 Key Issues: 2 – avoiding impacts on the poor3 Key Issues: 2 – avoiding impacts on the poor

Two impacts:Two impacts: Direct impacts – more expensive energy carriers, Direct impacts – more expensive energy carriers,

especially electricity – households would use less especially electricity – households would use less and potentially shift to more harmful fuels. and potentially shift to more harmful fuels.

Indirect impacts – structural effects, effect on Indirect impacts – structural effects, effect on services such as transportservices such as transport

Impacts best addressed by a) enhanced service Impacts best addressed by a) enhanced service delivery programmes (household energy policy, energy delivery programmes (household energy policy, energy regulatory policy, transport) which have significant regulatory policy, transport) which have significant sustainable development benefits, and b) options for sustainable development benefits, and b) options for revenue recycling.revenue recycling.

ERC

3 Key Issues: 3 – energy-intensive industries3 Key Issues: 3 – energy-intensive industries

Problem of current energy-intensive industries which Problem of current energy-intensive industries which compete internationally – in South Africa, very energy-compete internationally – in South Africa, very energy-inefficient – in some instances, unable to adjust to higher inefficient – in some instances, unable to adjust to higher energy pricesenergy prices

Special dispensation is possible, but it should exclude Special dispensation is possible, but it should exclude ALL new investments (this may create barriers to entry, ALL new investments (this may create barriers to entry, but less likely since industries are export-oriented)but less likely since industries are export-oriented)

Price signal to consumers should be preservedPrice signal to consumers should be preserved

Possible solution: Swedish solution – existing energy-Possible solution: Swedish solution – existing energy-intensive industries can pay reduced tax or no tax in intensive industries can pay reduced tax or no tax in exchange for embarking on MRVd energy efficiency exchange for embarking on MRVd energy efficiency programme – can use international benchmarksprogramme – can use international benchmarks

Criteria would have to be carefully developed to avoid Criteria would have to be carefully developed to avoid exempting bulk of emissionsexempting bulk of emissions

ERC

ConclusionConclusion

A carbon tax would incentivise emissions reduction, A carbon tax would incentivise emissions reduction, but would require careful consideration of a number of but would require careful consideration of a number of key issues, including:key issues, including: Tax level and mechanismsTax level and mechanisms Impact on poor householdsImpact on poor households Impact on energy-intensive industriesImpact on energy-intensive industries

Issues such as revenue-neutrality and revenue Issues such as revenue-neutrality and revenue recycling have a significant impact on the broader recycling have a significant impact on the broader effects of a carbon taxeffects of a carbon tax

‘‘partner programmes’ are important, will enhance the partner programmes’ are important, will enhance the response of the economy, cut costs for firms, and response of the economy, cut costs for firms, and offset negative impactsoffset negative impacts

ERC

Thank youThank you

Energy Research Centre University of Cape Town

www.erc.uct.ac.za