eric peterson - abc conference jan 2015

TRANSCRIPT

Pipeline Access to MarketsDetailing Pipeline Perspectives on Bakken and Niobrara Market

Destinations to Increase Takeaway Capacity Out of the Region

Eric Peterson

Senior Business Analyst

Bakken & Niobrara Crude Takeaway and Markets

Denver, CO

January 2015

Introduction to ARB Midstream

• Denver based infrastructure development company providing midstream solutions

• Strong financial support from private equity

• Utilize in-depth fundamental analysis to identify value propositions of our assets

• Emphasis on early stage development opportunities

• Developing a new crude-by-rail terminal• Niobrara Connector “NiCon”

• Centrally located in the DJ Basin

• Unit train capable

• Scheduled in-service date: June 2015

2

Observations

3

• Rockies crude oil fights for market share in Gulf Coast refining market

• Crude quality varies significantly between Bakken, DJ & PRB and it is crude quality that determines the best end market

• Most of the imported lights in the Gulf Coast have been pushed out – East and West Coasts still importing significant volumes

• Best end markets for Bakken are the West and East Coasts. Best markets for the DJ are West Coast and Gulf Coast by pipe.

DJ Basin Hitting an Inflection Point in Production, But Still Way Below “Big 3”

-

200,000

400,000

600,000

800,000

1,000,000

1,200,000

1,400,000

1,600,000

0 12 24 36 48 60 72

Incre

me

nta

l P

rod

uctio

n (

bp

d)

Months Developed

Bakken

PRB

DJ Basin

Permian

Eagle Ford

4

Mature Plays

Growing Plays

Source: HPDI, ARB Midstream

Pipeline Routes Out of Rockies Basins

5

DJ

PRB

NECL (90)

Bakken

Cushing

Existing

Under

Construction/Planned

Open Season

Crude Quality by Basin

Homogeneous Crude Quality From the Bakken

7

Cru

de A

PI G

ravity

Source: HPDI, Rig Data

Bakken Has An Average Production Quality of 42 API

8

-

50,000

100,000

150,000

200,000

250,000

300,000

350,000

400,000

Pro

du

ctio

n (

bp

d)

API Gravity

Bakken Production by API(May 2014)

Source: HPDI

Wide Variety of Crude Quality Produced Throughout the PRB

9

Cru

de A

PI G

ravity

Source: HPDI, Rig Data

PRB Produces Some of the Heaviest Crude in the Rockies

10

-

2,000

4,000

6,000

8,000

10,000

12,000

14,000

16,000

18,000

Pro

du

ctio

n (

bp

d)

API Gravity

PRB Production by API(May 2014)

Source: HPDI

High API Production Centered in the Core Area of the Wattenberg Field

11

Cru

de A

PI G

ravity

Source: HPDI, Rig Data

Bulk of DJ Basin Production Volumes are +45 API

12

-

5,000

10,000

15,000

20,000

25,000

30,000

35,000

Pro

du

ctio

n (

bp

d)

API Gravity

DJ Production by API(May 2014)

Source: HPDI, F.E.R.C.

Market Destinations and End Users

14

Bakken

Niobrara

Anadarko

Permian

Eagle Ford

Pipe with Firm Commitments

Under Construction

Completed Pipelines

No

Pipelines

to the West

Coast

New Pipelines Move Crude to Cushing and Gulf Coast – Nothing Going to the West

Source: Company Data, ARB Midstream

-

50,000

100,000

150,000

200,000

250,000

300,000

350,000

400,000

Pro

du

ctio

n (

bp

d)

API Gravity

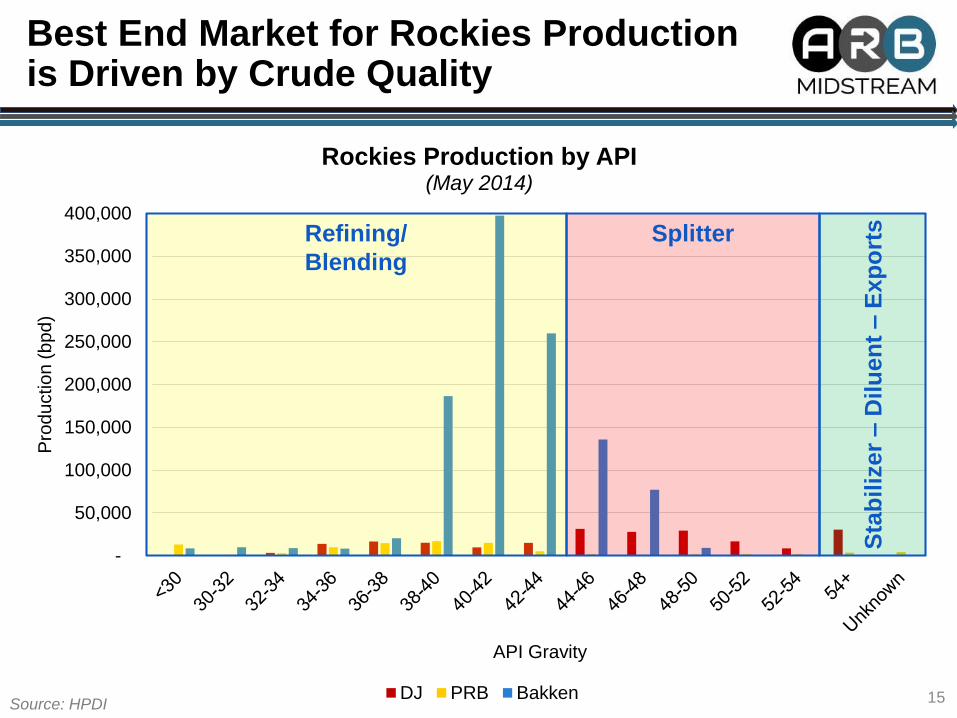

Rockies Production by API(May 2014)

DJ PRB Bakken

Best End Market for Rockies Production is Driven by Crude Quality

15

Splitter

Sta

bil

izer

–D

ilu

en

t –

Exp

ort

sRefining/

Blending

Source: HPDI

Gulf Coast Waterborne Imports –Q3 2009 vs Q3 2014

-

200,000

400,000

600,000

800,000

1,000,000

1,200,000

Wa

terb

orn

e Im

po

rts (

bp

d)

API Gravity

Q3 2009 Q3 201416

Imports have decreased from

4.8MM to 3.2MMbpd (-32%)

Source: EIA Company Level Imports

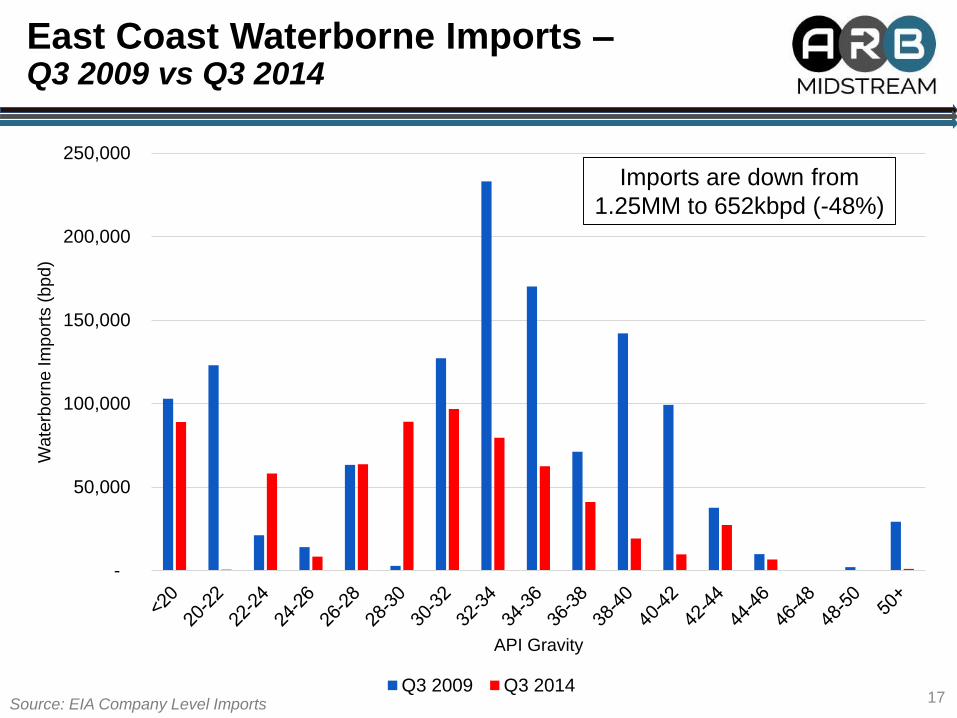

East Coast Waterborne Imports –Q3 2009 vs Q3 2014

-

50,000

100,000

150,000

200,000

250,000

Wate

rborn

e Im

port

s (

bp

d)

API Gravity

Q3 2009 Q3 201417

Imports are down from

1.25MM to 652kbpd (-48%)

Source: EIA Company Level Imports

West Coast Waterborne Imports –Q3 2009 vs Q3 2014

-

50,000

100,000

150,000

200,000

250,000

300,000

Wa

terb

orn

e Im

po

rts (

bp

d)

API Gravity

Q3 2009 Q3 201418

Imports have increased from

1.06MM to 1.18MMbpd (+11%)

Source: EIA Company Level Imports

Comparing Economics of Pipe vs Rail Out of Rockies Basins

Diffs Between Interior and Coastal Markets Drive Infrastructure Build Out

20

ANSWTI + 5

BakkenWTI - 6

LLSWTI + 4

BrentWTI + 6

WTI

Based off of 2014 Average Prices and DifferentialsSource: Argus

Bakken: LLS – ANS Price Differential Greater Than $1.58 = Pipe to LLS Wins

21

-15

-10

-5

0

5

10

LLS

–A

NS

Diffe

ren

tia

l

LLS - ANS Rail to West Coast

Pipe to Gulf Coast Wins

Rail to Washington Wins

Source: EIA, Argus, F.E.R.C.

Bakken : LLS – Brent Price Differential Greater Than -$0.35 = Pipe to LLS Wins

22

-20

-15

-10

-5

0

5

10

LLS

–B

ren

t D

iffe

ren

tia

l

LLS - Brent Rail to East Coast

Pipe to Gulf Coast Wins

Rail to East Coast Wins

Source: EIA, Argus, F.E.R.C.

23

$(5)

$-

$5

$10

$15

$20

0

200

400

600

800

1,000

1,200

Vo

lum

es T

ran

sp

ort

ed

(M

bp

d)

Refining Demand Pipe Volumes Rail Volumes ANS-WTISource: NDPA, BTU Analytics, Argus

Historical Bakken Demand Shows a Correlation Between the ANS-WTI Spread and Crude Pipeline Volumes

Rail Offers Optionality to Better Netbacks Based on Economics

24

BakkenWTI-6

ANSWTI +5

LLSWTI +4

BrentWTI +6

ANSWTI +5

~$10

~$12

~$12~$11

+$1

-$1

-$2+$1

Source: EIA, Argus, F.E.R.C.

~$11-$1

~$14-$4

1

234

5

6

DJ: LLS – ANS Price Differential greater than -$0.96 = Pipe to LLS Wins

25

-15

-10

-5

0

5

10

LLS

–A

NS

Diffe

ren

tia

l

LLS - ANS Rail to West Coast

Pipe to Gulf Coast Wins

Rail to West Coast Wins

Source: EIA, Argus, F.E.R.C.

DJ: LLS – Brent Price Differential greater than -$3.09 = Pipe to LLS Wins

26

-20

-15

-10

-5

0

5

10

LLS

–B

ren

t D

iffe

ren

tia

l

LLS - Brent Rail to East Coast

Pipe to Gulf Coast Wins

Rail to East Coast Wins

Source: EIA, Argus, F.E.R.C.

Rail to the West Coast and Pipe to LLS Market Tie for Best Netbacks

27

DJ*WTI-6

ANSWTI +5

LLSWTI +4

BrentWTI +6~$10

~$10

~$12$0+$1

Source: EIA, Argus, F.E.R.C.

$0~$9

~$12

+$1

-$2

11

34

5

Niobrara Connector “NiCon” Crude by Rail Terminal

Niobrara Connector “NiCon” –Centrally located in the DJ Basin

29

PXP NECL

A Look at Niobrara Connector “NiCon” Crude-by-Rail Terminal Specifications

30

• 79,000 bpd nameplate capacity

• 120 car unit train capable

• 224 Acres

• Industrial spur serviced by the UP

• In Service date June 2015

• Segregation of product in up to 4 - 100,000 bbl tanks

Summary

31

• Rockies crude oil fights for market share in Gulf Coast refining market

• Crude quality varies significantly between Bakken, DJ & PRB and it is crude quality that determines the best end market

• Most of the imported lights in the Gulf Coast have been pushed out – East and West Coasts still importing significant volumes

• Best end markets for Bakken are the West and East Coasts. Best markets for the DJ are West Coast and Gulf Coast by pipe.