esg in real estate - home - risklab · 2 esg in real estate one of the most popular voluntary...

TRANSCRIPT

Please note: the conclusions from the research studies analysed and summarised in this report do not necessarily reflect Allianz Global Investors’ investment opinion. The research does not imply investment advice or investment performance related forecasts.

Executive summary

Objective

Following two recent independent surveys among Real Estate investment managers, more best practice standards and better reporting on ESG in private Real Estate investments are required as interest in this field is growing. The main goal of this research is to determine the materiality of ESG factors for private Real Estate investments. We look into which ESG dimension – Environmental, Social or Corporate Governance – appears most relevant, or most measurable for private Real Estate investments. In this context, we also take a look at ESG regulations and certifications. To determine the possible impact of ESG on Real Estate value, we examine several studies focused on residential as well as office buildings around the world including different samples, regions and measurements for “green financial benefits” i.e. sales and rental premia. Finally, we take a look at current best practice examples conducting interviews with private Real Estate investments experts from Allianz Real Estate and the Townsend Group.

Results

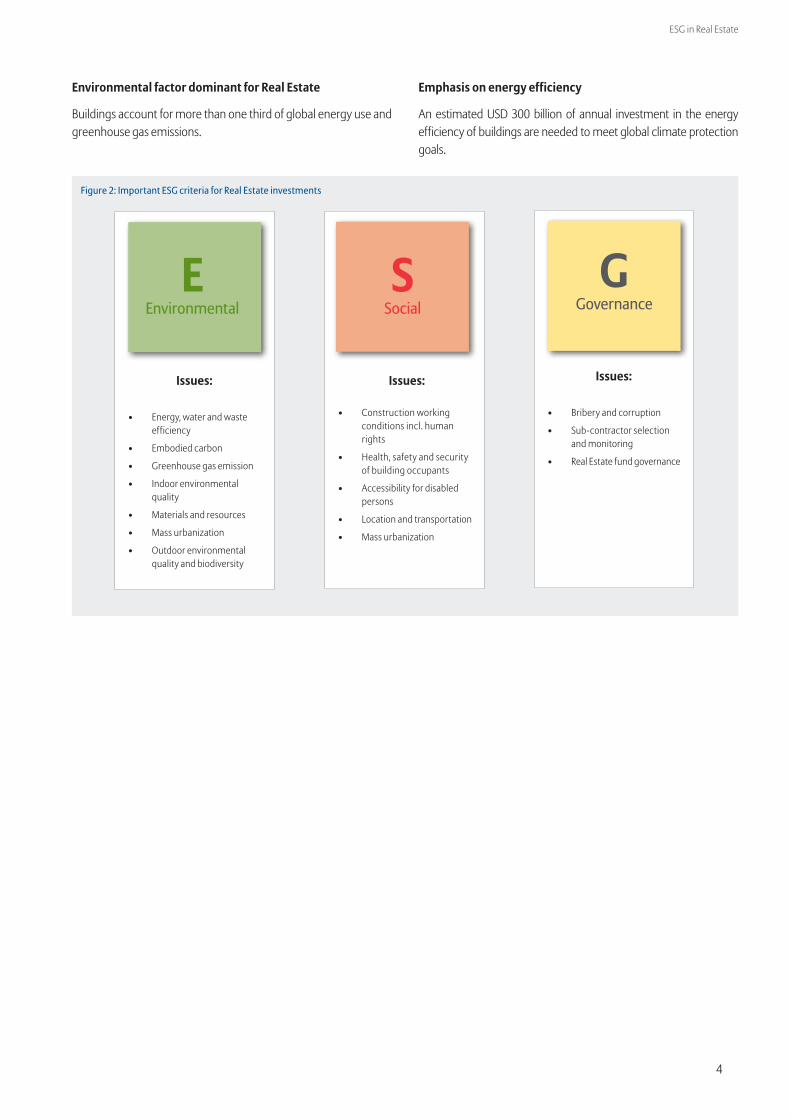

“The Environment” is the most dominant ESG Dimension for Real Estate. Buildings account for more than one third of global green house gas emissions and global energy consumption and may therefore be heavily accountable for contributing to global warming and climate change. In light of this the ESG focus for Real Estate has been on the environmental dimension.

Due to a multitude of environmental regulations and certifications – both mandatory and voluntary – the environmental dimension appears to be most measurable and most relevant in terms of sustainable private Real Estate investments. For example, following the energy performance of buildings directive of the European Union (EU), the Energy Performance Certificate (EPC) is one of the mandatory building certifications in measuring a building’s promised energy performance.

In addition, there are a multitude of voluntary building certifications such as the LEED (Leadership in Energy and Environmental Design, US), BREEAM (Building Research Establishment Environmental Assessment Methodology, UK) and NABERS (National Australian Built Environment Rating System, Australia). All of these take into account a building’s energy and water efficiency as well as its proximity to public transport and its indoor environmental quality.

ESG in Real Estate

Research analysis on Environmental, Social and Corporate Governance factor materiality for private Real Estate portfolios

The objective of this research study is to analyze the financial materiality of Environmental, Social and Corporate Governance factors (ESG) for (illiquid) Private Real Estate as an asset class.

AllianzGI Global Solutions

FOR INSTITUTIONAL AND PROFESSIONAL INVESTORS ONLY

2

ESG in Real Estate

One of the most popular voluntary certifications for private Real Estate portfolios (as opposed to single buildings) is the Global Real Estate Sustainability Benchmark (GRESB). Conducting annual surveys collecting sustainability data from property companies and private funds, participants receive scores in two dimensions: Management and Policy as well as Implementation and Measurement.

Beyond the Environmental dimension, Social and Governance aspects should not be neglected:

• Social factors may have financial impact as well for Real Estate. For example CAPEX to be considered to make an office building accessible for handicapped or making a building healthy, safe and secure for occupants.

• Governance factors may relate to the managing standards of a developer or building company on a grassroots level including issues such as bribery and corruption. For Real Estate funds governance risks relate to the investment manager and fund guidelines.

On the reputational risk side, labour relations in service providers, community perception of Real Estate developments, tenant perception (compliance with exclusion lists) etc. are important examples.

Green building premia tilting to brown building discounts

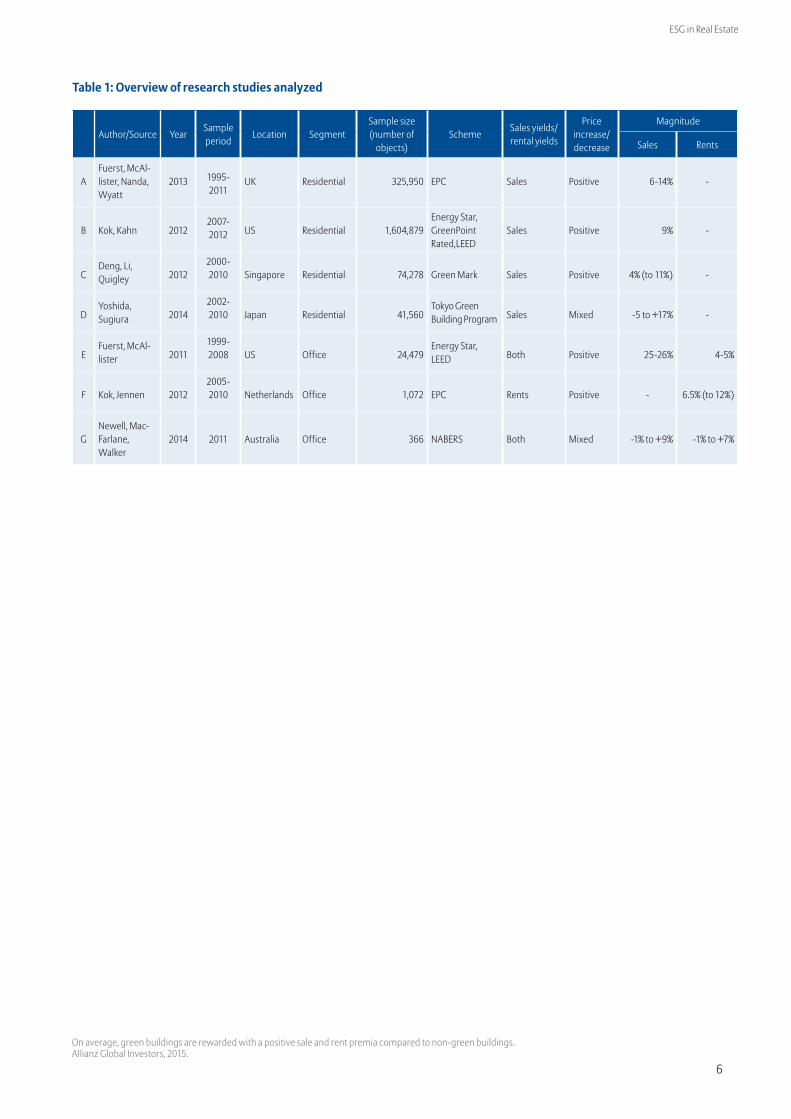

In order to determine the financial relevance of ESG for Real Es-tate, we investigate studies measuring differences in sales prices and rents between green and non-green residential and office buildings (see table 1).

Significant green building premia exist. They seem to be decreasing over time and Brown Building discounts appear to emerge instead:

• Several studies across the world (US, UK, Netherlands, Singapore, Japan, Australia) have analyzed the existence of green premia.

• Most studies came to the conclusion that green buildings are rewarded with a positive sale and rental premia compared to non-green buildings. The reported figures range up to 17% (residential sale) and up to 26% and 12% (office sale and rent respectively).

• However, it is important to note that sale premia have been decreasing in the past years. This development might be due to increasing awareness and availability of green buildings.

Better practice ESG policies of Real Estate investors:

Leading Real Estate investors such as Allianz Real Estate and The Townsend Group have a well-defined global Real Estate investment ESG policy reflecting highest standards.

Important pillars of these Real Estate ESG policies are:

• Policies and processes describing how material ESG factors are identified and assessed on a regular basis

• Analyzing ESG (risk) trends such as climate change, regulatory trends / legislation, tenant preferences, investor sentiment

• Policies and processes describing how ESG considerations are integrated into Real Estate portfolio construction and management strategies following a full investment cycle approach covering acquisition, management and exit

• Summary of set of tools and processes to assist management of ESG risks for Real Estate such as due diligence procedures, object life-cycle audit and environmental strategy

• Reputational risk management procedures such as business partner validation and exclusion list compliance handling

• Legal and regulatory compliance handling

• Policies also distinguish specific ESG handlings for different types of investments such as Direct Real Estate Equity vs. Direct Real Estate Debt vs. Real Estate Funds

Eventually, this might lead to a materialization of so-called brown discounts, i.e. discounts for non-green buildings.

• In general, existence and magnitude of price premia significantly depend on regions, in particular on climate and environmental standards. Within these differences, some studies even reported negative sale premia for residential and office buildings.

On an ESG opportunity level, low carbon funds are emerging such as the Low Carbon Workplace Fund, a partnership established in 2010 investing in refurbishments of UK office buildings.

3

ESG in Real Estate

One step deeper 1. What is the relevant dimension for Real Estate: E, S, G?

2. Green building premia? Materiality of ESG for Real Estate

3. Better practice: ESG policies for Real Estate Investors

1. What is the relevant dimension for Real Estate: E, S, G?

Objective

We determine the most relevant ESG dimension and criteria for Real Estate investment decision-making. Further, we give an introduction to portfolio- and building- level certification that will turn out to have a significant impact on Real Estate value.

Results

Buildings account for more than one third of global energy consumption and greenhouse gas emissions. Therefore, environmental criteria such as energy-, water- and waste-efficiency as well as embodied carbon come up as the main focus for ESG in Real Estate. Further, as regulatory pressures on energy efficiency etc. are expected to rise in the future, the variety of mandatory and voluntary certifications both on the portfolio- and on the building-level should be taken into consideration:

• Following the EU Energy Performance of Buildings Directive, Energy Performance Certificates (EPCs) are to be included in all advertisements for the sale or the rental of buildings. As the implementation of those mandatory certificates and the assessment of buildings under this directive vary across countries, a comparison of properties across countries might lead to difficulties.

• The UK Energy Act 2011 provides for powers to ensure that from April 2018, it will be unlawful to rent out a residential or business premise that does not reach a minimum energy efficiency standard (the intention is for this to be set at EPC rating “E”).

The Global Real Estate Sustainability Benchmark (GRESB), an industry-driven organization, assesses the sustainability performance of Real Estate portfolios. Conducting an annual survey collecting sustainability data, portfolios are rated in two dimensions: Management and Policy as well as Implementation and Measurement.

Building certifications focus on energy efficiency and envi-ronmental impact

A variety of voluntary (national) building level certifications assess the sustainability performance of Real Estate. Three of the most famous building level certifications are the US American LEED (Leadership in Energy and Environmental Design), the British BREEAM (Building Research Establishment Environmental Assessment Methodology) and the Australian NABERS (National Australian Built Environment Rating System). Each of these certifications take several rating categories into account such as energy and water efficiency or location and transport and results in four, five and seven different rankings respectively.

While we focus on residential and office buildings throughout this study, these certifications also assess retail or logistic buildings.

The consideration and inclusion of ESG factors into industrial Real Estate investments is not analyzed as part of this research.

Figure 1: Global energy consumption 1 Global CO2 emission 1

Buildings

33%40%

1 Source: http://www.unep.org/sbci/AboutSBCI/Background.asp, 2015.

4

ESG in Real Estate

Environmental factor dominant for Real Estate

Buildings account for more than one third of global energy use and greenhouse gas emissions.

Emphasis on energy efficiency

An estimated USD 300 billion of annual investment in the energy efficiency of buildings are needed to meet global climate protection goals.

Figure 2: Important ESG criteria for Real Estate investments

Issues:

• Energy, water and waste efficiency

• Embodied carbon

• Greenhouse gas emission

• Indoor environmental quality

• Materials and resources

• Mass urbanization

• Outdoor environmental quality and biodiversity

EEnvironmental

Issues:

• Bribery and corruption

• Sub-contractor selection and monitoring

• Real Estate fund governance

GGovernance

Issues:

• Construction working conditions incl. human rights

• Health, safety and security of building occupants

• Accessibility for disabled persons

• Location and transportation

• Mass urbanization

SSocial

5

ESG in Real Estate

2. Green building premia? Materiality of ESG for Real Estate

Objective

In this chapter, we determine the materiality of ESG for Real Estate by investigating several studies on this topic. In particular, we look into whether there is a green premia, i.e. if so-called green build-ings are rewarded with a sale and / or rental premia.

The US Green Building Council defines green buildings as the planning, design, construction, and operations of buildings with several central, foremost considerations: energy use, water use, indoor environmental quality, material section and the building’s effects on its site. See figure 5 and green building examples Allianz in the appendix. As opposed to that, code-compliant buildings are non-green buildings meeting local or national regu-lations. Brown buildings are non-green buildings not meeting lo-cal or national regulations.

Results

As basis of this research we analyze 7 selected scientific studies (see Table 1). Several studies across the world (US, UK, Nether-lands, Singapore, Japan, Australia) discussed the existence of green premia. We investigate studies measuring differences in sale prices and rents between green and non-green residential and office buildings. For voluntary certifications such as LEED, NABERS etc., these studies compared certified buildings to non-certified buildings. For mandatory certifications such as EPC, high-rated buildings were compared to low-rated buildings.

Most studies came to the conclusion that green buildings are re-warded with a positive sale and rental premia compared to non-green buildings. The reported figures range up to 17% (residential sale) and up to 26% and 12% (office sale and rent respectively). See figures 3 and 4 on page 7.

However, it is important to note that sale premia have been de-creasing in the past years. This development might be due to in-creasing awareness of green buildings. Eventually, this might lead to a materialization of so-called brown discounts, i.e. discounts for non-green buildings.

In general, the existence and magnitude of price premia significantly depend on regions, in particular on climate and environmental crite-ria. Within these differences, some studies even reported negative sale premia for residential and office buildings.

In Tokyo, the green premia of a residential building is initially neg-ative and increases with rising building age. This is due to higher construction costs and lower depreciation rates of green build-ings compared to non-green buildings. Further, long-life design is associated with a price premia as long-life design is especially ef-fective in Japan, where residential structures have relatively short economic lives.

2 Nelson, 2009.3 BCO Conference, 2012: “Building Wealth: Is sustainability worth it?”.4 PwC, 2014: “Real Estate 2020: Building the future”.

In Australia, there is evidence of so-called brown discounts for office buildings, i.e. non-green (low-rated) buildings having a lower value compared to green (median- and high-rated) buildings.

These so-called brown discounts are expected to further emerge in the future.

• “...many major markets will reach the critical mass where green buildings account for enough of the building stock that tenants have a choice. At this point, the performance premia for green buildings will flip to a discount for older, less efficient, conventional buildings. We are already at or near this point in the mature economies of Europe and de-veloped Asia, and getting closer in the major money centers of the United States.” 2

• “Regulation for minimum energy efficiency standards could impact market value and investment worth of buildings, since increasingly buildings which do not meet an ‘E’ on the EPC scale will face obsolescence. This could result in a ‘brown discount’, where the worst performing buildings will be less attractive to owners and occupiers until their energy effi-ciency is addressed.” 3

• “If the pressure to increase buildings’ eco-efficiency mounts faster than the market currently anticipates, then many buildings could suffer a large ‘brown discount’.” 4

Besides the awareness of emerging brown discounts and the need to determine the extent of brown discounts for non-certified proper-ties, further lessons regarding ESG in Real Estate have been learnt:

• There is a need for greater transparency and consistency of approach in order to minimize any perceived risks of devalu-ation or of decreasing expected benefits from the inclusion of sustainability features on building projects.

• More data is needed on the impact not just of certification, but of individual measures or strategies, and how they are perceived by appraisers. Existing studies for rental and occu-pancy rates in particular are based on small sample sets and need to be built up to increase their reliability and robustness.

• The industry needs to gain a better understanding of the im-plications of changes in the ratio of certified versus non-certi-fied buildings, the trend in legal requirements to upgrade buildings and other external factors related to political, eco-nomic and environmental issues, all of which will impact the asset value of both green and non-green buildings.

• Investors need to understand the implications of regulatory and climate change and factor this into sustainability risk assessments for the development, ownership and occupancy of buildings.

• Building owners need to appreciate occupier preferences for ‘green’ buildings, particularly which ‘green’ features appeal to them.

6

ESG in Real Estate

Table 1: Overview of research studies analyzed

Author/Source YearSample period

Location SegmentSample size (number of

objects)Scheme

Sales yields/rental yields

Price increase/decrease

Magnitude

Sales Rents

AFuerst, McAl-lister, Nanda, Wyatt

2013 1995- 2011

UK Residential 325,950 EPC Sales Positive 6-14% -

B Kok, Kahn 20122007- 2012 US Residential 1,604,879

Energy Star, GreenPoint Rated,LEED

Sales Positive 9% -

CDeng, Li, Quigley 2012

2000-2010 Singapore Residential 74,278 Green Mark Sales Positive 4% (to 11%) -

DYoshida, Sugiura 2014

2002-2010 Japan Residential 41,560

Tokyo Green Building Program Sales Mixed -5 to +17% -

EFuerst, McAl-lister 2011

1999-2008 US Office 24,479

Energy Star, LEED Both Positive 25-26% 4-5%

F Kok, Jennen 20122005-2010 Netherlands Office 1,072 EPC Rents Positive - 6.5% (to 12%)

GNewell, Mac-Farlane, Walker

2014 2011 Australia Office 366 NABERS Both Mixed -1% to +9% -1% to +7%

On average, green buildings are rewarded with a positive sale and rent premia compared to non-green buildings.Allianz Global Investors, 2015.

7

ESG in Real Estate

5 Source: Fuerst, McAllister, Nanda, Wyatt (2013). Kok, Kahn (2012), Deng, Li, Quigley (2012), Yoshida, Sugiura (2014).6 Source: Fuerst, McAllister (2011), Kok, Jennen (2012), Newell, MacFarlane, Walker (2014). This is for guidance only and not indicative of future results.

Explanation:

Maximum green sale premia for residential buildings.

The sale price premia was measured as the difference in sale prices between labeled and non-labeled buildings within the vol-untary certificates (US, Singapore, Japan) and between high-rated and low-rated buildings within the mandatory certificates (UK).

Maximum green sale and rental premia for office buildings.

The sale price premia was measured as the difference in sale prices between labeled and non-labeled buildings within the voluntary certificates (US, Australia) and between high-rated and low-rated buildings within the mandatory certificates (Netherlands).

Figure 4: Office buildings are rewarded with sale/rental premia of up to 26%/12% 6

Sale premiaRent premia

Energy Star, LEED US, 2011

Energy Performance Certificate (EPC)

Netherlands, 2012

NABERSAustralia, 2014

26%

5%

12%

9%

7%

Figure 3: Residential buildings are rewarded with a sale premia of up to 17% 5

Sale premia

Energy Star, Green Point Rated, LEED

for HomesUS, 2012

Energy Performance Certificate (EPC)

UK, 2013 Singapore Green Mark Program

Singapore, 2012

Tokyo Green Building ProgramJapan, 2014

9%

14%

11%

17%

8

ESG in Real Estate

How green buildings investments influence value creation

There are a variety of factors that influence a building‘s value such as the building‘s location. Recent studies have shown though that „green buildings“ tend to achieve better rental and occupancy rates as well as higher sales prices than „non-green assets“.8 However, this effect is different across regions and seems to di-minish in the last years.

Based on the unique conditions of each market the magnitude of the financial benefits may vary depending on other influencing factors.

7 Source: http://www.usgbc.org/articles/what-green-building. 8 Source: World Green Building Council, 2013: The Business Case for Green Buildings. Primarily based on data gathered from LEED-certified buildings in the United States.

Summary of research findings for several studies

There is evidence of an - in general - positive cost premia which seems to be proportional to the certification level. However, some studies report an almost zero or even nega-tive cost premia.

There is evidence that operational cost savings exceed any cost premia associated with green building design and construction.

There is evidence of an in general positive but volatile rental premia for green-labeled buildings. However, the shift of regional focus in these studies is important to note.

There is evidence of an in general positive but recently de-creasing occupancy rate difference compared to conven-tional code-compliant buildings.

There is evidence of an in general positive but recently de-creasing sale premia for green-labeled buildings. However, some studies report a negative sale premia.

Based on the unique conditions of each market the magnitude of the financial benefits may vary depending on other influencing factors.

A

B

C

D

E

What is a ‘Green Building’?

The US Green Building Council defines a green building as “the planning, design, construction and operations of buildings with several central, foremost considerations: water use, energy use, material section, indoor environmental quality and the building’s effects on its site”.7

Code-compliant buildings are non-green buildings that meet local or national regulations.

Planning

Design

ConstructionOperations

• Water use• Energy use• Material section• Indoor environmental quality• Building’s effects on its site

Figure 5:

Green buildings investment economics

Gree

n bu

ildin

g pr

emia

CAPEX

Valuation

Exit

Higher sales price

Lower operating expenses

Higher occupancy rates

Higher rental/lease rates

Lower tenant fluctuation …

Higher net asset value

+

+

+

+

+

Future-proofing for legislative / regulatory and environmental changes

Marketing benefits

A

B

C

D

E

Figure 6:

9

ESG in Real Estate

9 Source: World Green Building Council, 2013: The Business Case for Green Building. Please note: This is for guidance only and not indicative of future results.

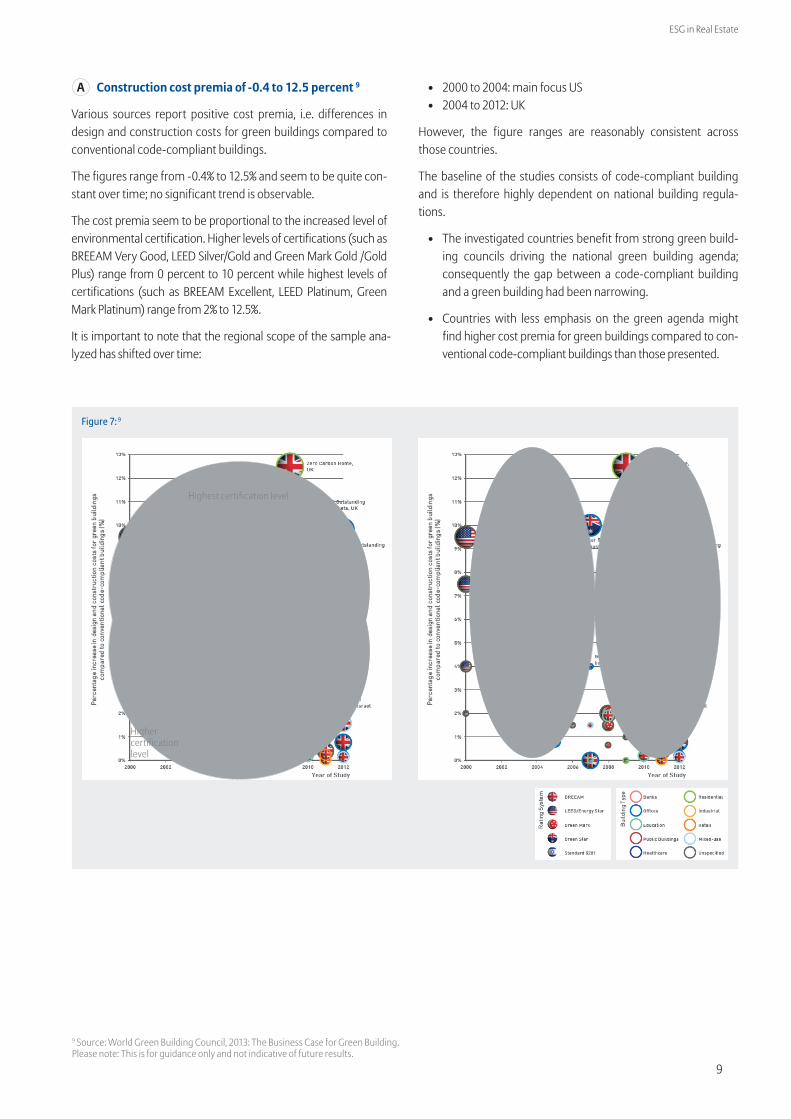

A Construction cost premia of -0.4 to 12.5 percent 9

Various sources report positive cost premia, i.e. differences in design and construction costs for green buildings compared to conventional code-compliant buildings.

The figures range from -0.4% to 12.5% and seem to be quite con-stant over time; no significant trend is observable.

The cost premia seem to be proportional to the increased level of environmental certification. Higher levels of certifications (such as BREEAM Very Good, LEED Silver/Gold and Green Mark Gold /Gold Plus) range from 0 percent to 10 percent while highest levels of certifications (such as BREEAM Excellent, LEED Platinum, Green Mark Platinum) range from 2% to 12.5%.

It is important to note that the regional scope of the sample ana-lyzed has shifted over time:

Figure 7: 9

Highest certification level

Higher certification level

• 2000 to 2004: main focus US • 2004 to 2012: UK

However, the figure ranges are reasonably consistent across those countries.

The baseline of the studies consists of code-compliant building and is therefore highly dependent on national building regula-tions.

• The investigated countries benefit from strong green build-ing councils driving the national green building agenda; consequently the gap between a code-compliant building and a green building had been narrowing.

• Countries with less emphasis on the green agenda might find higher cost premia for green buildings compared to con-ventional code-compliant buildings than those presented.

10

ESG in Real Estate

Reported cost premia associated with LEED certifications illus-trate a gradual trend towards reduction in cost premia over time. However, cost premia associated with LEED certified levels have risen from 2007 to 2011.9

Further, the proportionality of cost premia to certification levels is demonstrated.

Figure 8: 9

There are several reasons supporting this trend towards cost pre-mia reduction over time:

• The building industry has been steadily developing its capa-bility for delivering green buildings.

• There is increasing awareness, acceptance and education around green building certification and assessment tools leading to more and more professionals becoming well-equipped to design and certify green buildings.

• Clients are increasingly aware of sustainability and energy issues and demand more expertise from industry and col-laborative teams.

• Minimum standards for building code are progressively be-coming stricter, hence baseline requirements and associated costs are progressively getting higher, and therefore narrow-ing the gap between the cost of code-compliant buildings and the cost of green buildings.

9 Source: World Green Building Council, 2013: The Business Case for Green Building. Please note: This is for guidance only and not indicative of future results.

The main benefits of green buildings include reduced energy costs from heating, cooling, ventilation, lighting and reduced wa-ter consumption.

A 2003 study reported reduced energy use for LEED rated build-ings compared to conventional code-compliant buildings of 18%, 30% and 37% for LEED Certified, LEED Silver and LEED Gold rated buildings respectively. It is important to note that since these re-sults are based on 2003 data, the figures may no longer be valid. However, the trend of greater energy reductions corresponding to higher certification levels should still be valid.

Further benefits, such as reduced operational costs and maintenance requirements, require effective green building management proce-dures to be put in place prior to the building’s occupation.

In addition, green buildings potentially offer indirect benefits re-lated to reductions in property taxes, insurance rates and refur-bishment costs.

As energy prices rise, the relative benefits of energy efficiency will become increasingly important and the business case for energy-efficient buildings will strengthen et. vice versa.

A 2003 study found that operational cost savings exceed any cost premia associated with green building design and construction. It is important to note that since this graph is based on 2003 data, these values may no longer be accurate due to economic changes.

Figure 9: 9

B Operating cost savings exceed initial building/refur-bishment costs 9

11

ESG in Real Estate

9 Source: World Green Building Council, 2013: The Business Case for Green Building. Please note: This is for guidance only and not indicative of future results.

No significant trend in rental premia 9

Various sources report positive rental premia for green-building compared to conventional code-com-pliant buildings in Australia, the UK and the US.

No significant trend is observable throughout the overall quite volatile research results. However, it is im-portant to note that the regional focus has shifted in the past years.

One result shows a negative rental premia. This discount is associated with lower NABERS performance levels. However, higher NABERS performance levels are linked with a positive rental premia.

Figure 10: 9 C

Various sources report increasing occupancy rate for green buildings compared to conventional code-com-pliant buildings.

However, occupancy rate differences between green buildings and conventional code-compliant buildings seem to have been decreasing in recent years. This decrease might be due to a general increased aware-ness of green building.

The differences in reported figures result from differences in methodology and data.

Figure 11: 9 D Occupancy rate for green buildings higher but decreasing effect 9

12

ESG in Real Estate

9 Source: World Green Building Council, 2013: The Business Case for Green Building. Please note: This is for guidance only and not indicative of future results.

Various sources report sale price increases for green-building compared to conventional code-compliant buildings around the world (UK, US, Singapore, Austra-lia, Japan, Netherlands).

However, sale premia have been decreasing in the last years. This decrease might be due to an increased awareness of green building in general.

Two studies even find negative sale premia.

In the Australian case, this discount is associated with lower NABERS performance levels (while higher NA-BERS performance levels are rewarded with a positive price premia).

In the Japanese case, one potential reason for this dis-count might be the prevalence of highly-efficient appli-ances and equipment in Japan. On the other hand, long-life design is associated with a positive price premia.

Figure 12: 9 E Sale premia for green buildings decreasing in the past years 9

13

ESG in Real Estate

3. Better practice: ESG policies for Real Estate Investors

Objective

We investigate and summarize ‘policy and process best practices’ regarding the integration of ESG into Real Estate investment deci-sions and investments.

We give examples of how investors can include ESG criteria into their asset and portfolio management decisions and thereby aim to achieve financial benefits on their Real Estate investments.

Results

The 2012 UNEP FI Responsible Property Investment (RPI) report describes current best practices on how to integrate ESG into the property investment process:

• The ESG framework is defined in order to set minimum stan-dards for asset selection, for asset allocation and portfolio management

Real Estate asset managers’ best practice ESG policies focus on the identification, analysis and management of ESG. The impact of ESG criteria are analyzed on an asset and portfolio level all through-out the investment process:

• Life-cycle based ESG Real Estate analysis (buy, manage and exit / sale ESG analysis)

• Including due diligence of business partners and funds

• ESG risk based audits and annual reporting such as GRESB

Policies should differentiate and adjust for the various types of real investments:

• (Direct) Private Real Estate Equity

• (Direct) Private Real Estate Debt

• Fund-Based Real Estate Investments

10 Source: http://www.unepfi.org/work-streams/property/rpi/ ; UNEP FI, 2012: Responsible Property Investment – What the leaders are doing.

UNEP FI Responsible Property Investment Report 10

The 2012 report “Responsible Property Investment – What the leaders are doing” by the United Nations Environment Pro-gramme Finance Initiative (UNEP FI), a strategic public-pri-vate partnership between the United Nations Environment

Programme (UNEP) and about 200 financial institutions, de-scribes current ESG best practices in Responsible Property In-vestment (RPI).

In the simplest sense, RPI is the integration of ESG criteria into investors’ decisions regarding Real Estate.

Responsible Property Investment (RPI)

Objectives

• Need to better understand the impact of ESG factors on Real Estate investments possibly damaging or enhancing its long-term performance.

• Gaining a competitive advantage by get-ting ahead of more stringent regulatory environmental and social requirements.

• Responding to tenant demands for more environmentally efficient buildings possi-bly contributing to lower occupancy costs.

Use of RPI criteria to set minimum standards for asset selection

Integration of RPI into asset allocation and portfolio management

Integration of RPI into asset management strategies

Integration of RPI principles into the property investment process

14

ESG in Real Estate

Asset manager example: Best practice Real Estate ESG policy 11

Goals

1. Provide investors with outstanding performance

2. Take ESG considerations into account in any investment decision to enhance returns and to preserve value

• Checklist approach throughout due diligence process to identify ESG risks and opportunities currently or poten-tially materializing over the investment horizon

• Consideration of risks and opportunities in asset pricing, effective management and acquisition

• Inclusion of external advisors where specialist skills or technical knowledge is required

• Validation of business partners using ESG exclusion lists

• Active management:

• Environmental strategy (using environmental certifi-cation schemes)

• Best standard monitoring

• Tenant satisfaction survey

• Property specific risk assessment

• Support and education of partners on ESG issues

• Annual report containing sustainability and manage-ment of ESG issues …

Buy

Manage

Sell

Life cycle ESG audits

11 Source: Allianz Real Estate, 2015.

Iden

tific

atio

n

Anal

ysis

Man

agem

ent

15

ESG in Real Estate

Appendices

APPENDIX 1: Environmental standards and tools

APPENDIX 2: ESG Surveys Alternative Investments

APPENDIX 3: Surveys ESG in Real Estate

APPENDIX 4: Research studies financial materiality of ESG in Real Estate

EU Energy performance building directive

European Union energy performance of buildings directive (implementation in 2003, recast in 2010)

The goal is to promote energy performance improvements in buildings: „Member states shall ensure that, when buildings are constructed, sold or rented out, an energy performance certifi-cate is made available to the owner or by the owner to the pro-spective buyer or tenant.“ (Article 7, Energy Performance of Build-ings Directive, EU, 2009)

Target

All new buildings must be nearly zero energy buildings by 2020. EU countries must set minimum energy performance require-ments for new buildings, for the major renovation of buildings and for the replacement or retrofit of building elements.

Implementation of national energy performance certificates (EPCs)

Aspiration Practice

Energy performance certificate shows a building’s prom-ised energy use. 12

Display energy certificate shows a building’s energy use in practice. 13

Figure 13: Mandatory environmental assessment tool for Real Estate across the EU

12 Source: http://de.fotolia.com.13 Source: http://www.allianz-realestate.com/index.php?cID=578.

APPENDIX 1: Environmental standards and tools

16

ESG in Real Estate

Voluntary environmental assessment tools for Real Estate

Building level certification schemes

Country Certification schemes

USA• LEED Leadership in Energy and Environmental Design• Energy Star

Europe• BREEAM Building Research Establishment Environmental Assessment Methodology• DGNB: Gesellschaft für Nachhaltiges Bauen (Germany)• HQE: Haute Qualité Environnementale (France)

Australia• BREEAM Building Research Establishment Environmental Assessment Methodology• NABERS National Australian Built Environment Rating System• GreenStar

Asia• Tokyo green building Program (Tokyo)• Singapore Green Mark Program (Singapore)• CASBEE Comprehensive Assessment System for Built Environment Efficiency

There exists a broad variety of certifications measuring Real Estate sustainability. This leads to challenges comparing sustainability objectively unless one common standard is applied.

Environmental assessment tools in Europe

• The number of certifications of commercial buildings in Eu-rope has notably increased from 2012 to 2013.

• The decrease of HQE certifications has been due to new reg-ulations in France.

• The age of the certification system seems to play an impor-tant role. BREEAM has been introduced in 1990 and is more established in its home country (UK) than the other certifica-tion systems in their home countries.

• It is important to note that apart from these certification so-called ‘Certificates in Use’ certifying existing buildings – e.g. BREEAM in Use, HQE-Exploitation, and LEED-EBOM 14 – have been increasing in the past years.

Figure 14: Number of certificates of commercial buildings in Europe 14

0

1000

2000

3000

4000

5000

6000

7000

8000

9000

10000

BREEAM HQE DGNB LEED Total

20122013

+67.0%

+111.0% +51.3%-3.2%

+55.4%

14 Leed for Existing Buildings: Operations & Maintenance.15 Source: RICS, 2013: Going for Green – Sustainable Building Certification Statistics Europe.

BREEAM

HQE

DGNB

LEED

Figure 15: Certificates of commercial buildings in Europe 15

2013, Total: 8.978

10,79%

80,89%

3,64% 4,67%

4,79%2,68%

17,32%

75,20%

2012, Total: 5.779

17

ESG in Real Estate

Table 2: Building level certification 16

LEED (Leadership in Energy and Environmental Design)

BREEAM (Building Research Establishment Environmental Assessment Methodology)

NABERS (National Austra-lian Built Environment Rating System)

Establishment US Green Building Council (2000)Building Research Establishment (1990)

NSW Office of Environment and Heritage (1999)

Categories

Energy and atmosphere Energy Energy

Water efficiency Water Water

Location and transportation Transport Commuter transport

Waste Waste

Indoor environmental quality Indoor environment

Innovation Innovation

Materials and resources Materials

Sustainable sites Land use and ecology

Integrative process Management

Regional priority credits

Health and wellbeing

Pollution

Ranking

• Platinum: 80+ Points• Gold: 60-79 Points• Silver: 50-59 Points• Certified: 40-49 Points

• Outstanding: 85+ %• Excellent: 70-85 %• Very Good: 55-70 %• Good: 45-55 %• Pass: 30-45 %

• 6 Star: market leading• 5 Star: excellent• 4 Star: very good• 3 Star: good• 2.5 Star: median• 2 Star: below average• 1 Star: poor

16 Source: http://www.usgbc.org/LEED, http://www.breeam.org/, http://www.nabers.gov.au.

18

ESG in Real Estate

Portfolio level certification: GRESB 17

About GRESB

The Global Real Estate Sustainability Benchmark (GRESB) is an industry-driven organization committed to assessing the sustainability performance of Real Estate portfolios (public, private and direct) around the globe. It was founded in 2009.

Aim

GRESB’s aim is to provide an assessment of ESG performance of Real Estate portfolios that can be used as a benchmark in order to encourage shifts towards more economically efficient Real Estate investments.

Method

GRESB conducts an annual survey collecting sustainability data from property companies and private funds.

Rating

The survey includes seven sustainability aspects.

Dimensions

The total GRESB score is divided into two dimensions:

• Management & Policy (MP): The means by which a company or fund manages sustainability in its organization, portfolio and stakeholders and the principles of action adopted by the company/fund.

• Implementation & Measurement (IM): The process of exe-cuting a decision or plan, or the act of measuring something related to the portfolio. A participant's score for Implemen-tation & Measurement comprises two-thirds of the total GRESB score.

New: GRESB debt

Starting in 2015, GRESB serves institutional investors in Real Estate debt, applying similar methodology and benchmarking to enable institutional investors to extend ESG integration to their Real Estate debt investments. The GRESB Debt Survey assesses the sustainability engagement and performance of Real Estate lenders. By capturing the ESG performance of Real Estate managers through the GRESB Survey, and lenders by way of the GRESB Debt Survey, GRESB serves the full spectrum of Real Estate capital providers.

Management Policy & disclosure

Risk &opportunities

Monitoring &environmental management

systems

Performance indicators (energy,

GHG emissions, water and waste)

Building certifications

Stakeholder engagement

Figure 16: Rating sustainability aspects 17

17 Source: https://www.gresb.com, https://www.gresb.com/debt-survey.

19

ESG in Real Estate

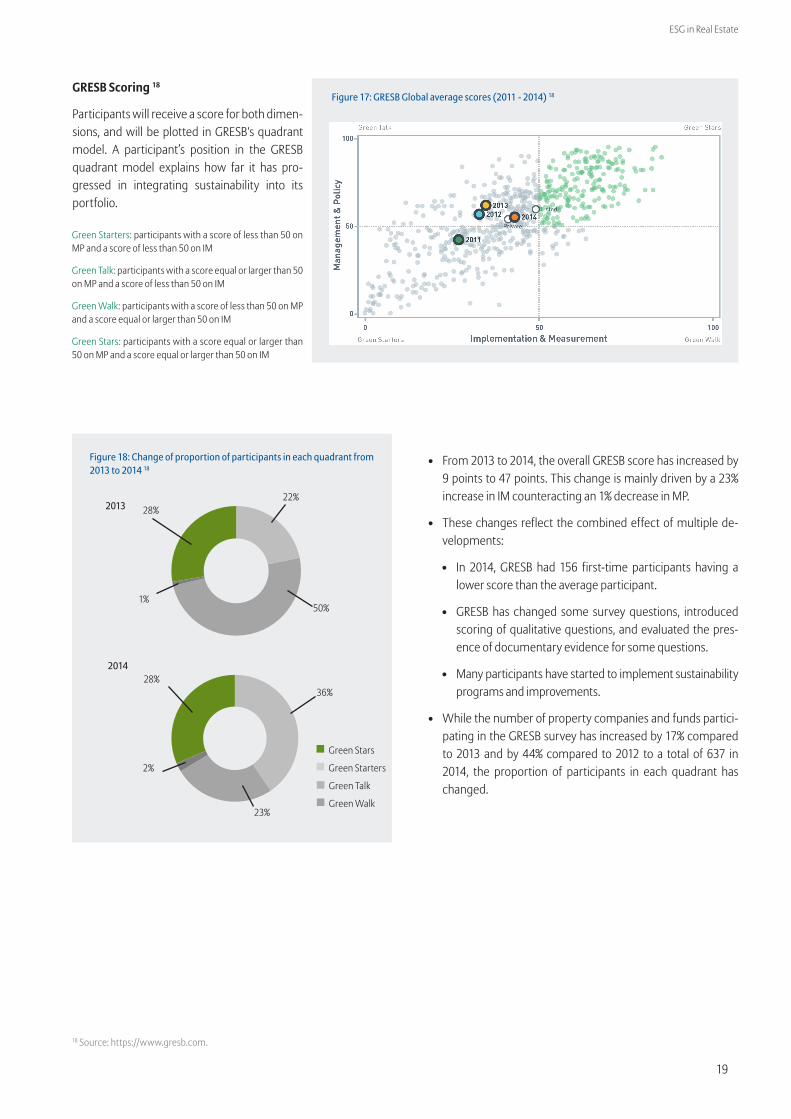

GRESB Scoring 18

Participants will receive a score for both dimen-sions, and will be plotted in GRESB's quadrant model. A participant’s position in the GRESB quadrant model explains how far it has pro-gressed in integrating sustainability into its portfolio.

Green Starters: participants with a score of less than 50 on MP and a score of less than 50 on IM

Green Talk: participants with a score equal or larger than 50 on MP and a score of less than 50 on IM

Green Walk: participants with a score of less than 50 on MP and a score equal or larger than 50 on IM

Green Stars: participants with a score equal or larger than 50 on MP and a score equal or larger than 50 on IM

Figure 17: GRESB Global average scores (2011 - 2014) 18

18 Source: https://www.gresb.com.

• From 2013 to 2014, the overall GRESB score has increased by 9 points to 47 points. This change is mainly driven by a 23% increase in IM counteracting an 1% decrease in MP.

• These changes reflect the combined effect of multiple de-velopments:

• In 2014, GRESB had 156 first-time participants having a lower score than the average participant.

• GRESB has changed some survey questions, introduced scoring of qualitative questions, and evaluated the pres-ence of documentary evidence for some questions.

• Many participants have started to implement sustainability programs and improvements.

• While the number of property companies and funds partici-pating in the GRESB survey has increased by 17% compared to 2013 and by 44% compared to 2012 to a total of 637 in 2014, the proportion of participants in each quadrant has changed.

Green Stars

Green Starters

Green Talk

Green Walk

201428%

36%

23%

2%

Figure 18: Change of proportion of participants in each quadrant from 2013 to 2014 18

2013 28%22%

50%1%

20

ESG in Real Estate

Climate change and water scarcity as top environmental issues

AI Survey 2015 19

The most important environmental issues among alternative investors

EuropeAsia

Australia

North America

• Climate change• Water scarcity

• Climate change• Water scarcity• Environmental

degradation• Nuclear power

• Climate change• Water scarcity• Nuclear power

• Water scarcity • Climate change• Environmental

degradation

APPENDIX 2: ESG Surveys Alternative Investments

19 Source: Mercer, Capital Partners, 2015: Global Insights on ESG in Alternative Investing.

Human rights and child labor as top social issues

AI Survey 2015 19

The most important social issues among alternative investors

Europe Asia

Australia

North America

• Human rights• Child labor

• Child labor• Controversial

weapons • Human rights• Labor standards

• Human rights• Child labor

• Controversial weapons

• Child labor• Human rights

21

ESG in Real Estate

Bribery and corruption as top governance issues

AI Survey 2015 19

19 Source: Mercer, Capital Partners, 2015: Global Insights on ESG in Alternative Investing.

Europe Asia

Australia

North America

• Board quality • Accounting practices• Bribery and corruption

• Bribery and corruption• Accounting practices• Board quality• Political contributions

• Bribery and corruption • Accounting practices• Board quality

• Board quality • Accounting practices• Bribery and corruption

22

ESG in Real Estate

Emerging trends on ESG and alternative investments in-cluding Real Estate 20

Results of ESG in alternative investing survey 2015 for Europe

• Focus on ESG is expected to increase: Many respondents in the early stages of embedding responsible investing principles expect a greater focus on ESG in the future.

• There is a growing interest in reporting on ESG: Among those with established processes for incorporating ESG considerations, a majority state their intent to establish more formal ESG reporting.

• Best practice standards could improve ESG uptake: More than half of respondents believe that their current approach to ESG issues would be significantly improved through greater clarity on techniques and strategies for ESG incorporation.

Figure19: To what extent does a manager’s ESG approach factor into manager selection? 20

SignificantlyTo some extendNot at all

27%

56%

17%

20 Source: Mercer, Capital Partners, 2015: Global Insights on ESG in Alternative Investing.21 Source: PwC, Urban Land Institute, 2015: Emerging Trends in Real Estate® Europe 2015.

Growing interest in ESG requires more best practice standards and ESG reporting.

APPENDIX 3: Surveys ESG in Real Estate

Emerging ESG trends Real Estate investors 21

Results of emerging trend in Real Estate survey 2015 for Europe

• Regulations and rapidly approaching energy efficiency targets have brought the green agenda into sharp focus.

• Approx. 70% of respondents have adopted sustainability in their Real Estate business strategy, and 74% are preparing Real Estate portfolios to make them more sustainable.

• Many investors are convinced that sustainability is synonymous with good business.

• „Climate, energy and building regulations bring about obsolescence and depreciation faster than anticipated. Investment in operations, maintenance and refurbishment needs to be in tune with these changes.“

It is assumed that regulatory and market pressures will increas-ingly reward high-performance buildings.

Figure 20: Do you include sustainability in your Real Estate business strategy? 21

YesNo

69%

31%

Figure 21: Do you achieve higher rents on sustainable assets? 21

YesExpectingNo

46%

36%18%

23

ESG in Real Estate

B. US: Labeled homes sell for 9% more than non-labeled homes 23

A. UK: Value premia of up to 14% 22

APPENDIX 4: Research studies financial materiality of ESG in Real Estate

22 Allianz Global Investors, 2015. 23 As measured by the number of registrations of hybrid vehicles.Please note: This is for guidance only and not indicative of future results.

Study Kok, Kahn, 2012The Value of Green Labels in the California Housing Market

Findings

• Labeled homes sell for 9 percent more (+/- 4%) than comparable non-labeled homes.

• The resale premia changes considerably from region to region and is highest in areas with hot climate.

• The resale premia is correlated to the environmental ideology of the area.28

Data 1.6 million single-family homes (US: California, 2004-2012)4,321 certified under Energy Star, GreenPoint Rated or LEED for Homes

Methodology Comparison between labeled and non-labeled build-ings

Green labeled homes sell at higher prices

A green label adds an average 9%

price premia to sale price versus

other comparable homes.

AVERAGE HOME SALE PRICE IN

CALIFORNIA

$ 400,000$ 434,800

NON-LABELED HOME GREEN LABELED HOME

Figure 23: Value of Green Labels 23

Study Fuerst et al., 2013 An Investigation of the effect of Energy Performance Certificate (EPC) ratings on house prices

Findings

• There is a positive relationship between energy rat-ing and sale price per square meter.

• The price difference (compared to EPC G rated build-ings) increases with improving EPC performance.

• The price effects of superior energy performance tend to be higher for terraced buildings compared to (semi-) detached buildings.

Data 325,950 buildings EPC rated A-G (UK, 1995-2011)

Methodology Comparison between EPC A-F rated and EPC G rated buildings

Figure 22: Value premia (Reference: G rated building) 23

13,8%

9,9%

7,6%6,6% 6,0%

0%

2%

4%

6%

8%

10%

12%

14%

16%

A/B C D E F

Diff

eren

ce in

sal

e pr

ice

per s

quar

e m

eter

in p

erce

nt(R

efer

ence

: G ra

ted

build

ings

)

EPC rating

A : 7B : 4434C : 78204D : 148665E : 75778F : 16068G : 2791

24

ESG in Real Estate

C. Singapore: Labeled buildings sell for 11% more than non-labeled

D. Japan: Initial negative premia gets positive after one year

Study Deng et al., 2011Economic returns to energy-efficient investments in the housing market: Evidence from Singapore

Findings

• There is a positive relationship between energy rat-ing and sale price per square meter.

• The price difference (compared to non-labeled buildings) increases with improving label (Platinum, Gold Plus, Gold).

Data 74,278 buildings (Singapore: 2000-2010)18,296 green-labeled under the Singapore Green Mark Program

Methodology Comparison between labeled and non-labeled buildings

Figure 24: Value premia (Reference: G rated building) 24

0%

2%

4%

6%

8%

10%

12%

Full sample Propensity scorematching

Diff

eren

ce in

sal

e pr

ice

per s

quar

e m

eter

in p

erce

nt

Study Yoshida, Sugiura, 2014The Effects of Multiple Green Factors on Condo-minium Prices

Findings

• The initial green premia can be negative but be-comes positive as the building ages (due to slower depreciation rate of green buildings).

• Longer-life design is associated with a price premia.

• Use of renewable energy and recycled materials and water is associated with a price discount (due to high marginal costs for improving energy efficiency).

Data 11,933 buildings (Japan: Tokyo, 2002-2010)1,452 green-labeled unter the Tokyo Green Building Program

Methodology Comparison between labeled and non-labeled build-ings

Figure 25: Value premia (Reference: Same-aged non-labeled building) 24

-0,1

-0,05

0

0,05

0,1

0,15

0,2

0-1 1-2 2-3 3-4 4-5 5-6

Diff

eren

ce in

log

pric

e pe

r squ

are

met

er

AgeLow and median scores High scores

24 Allianz Global Investors, 2015. Please note: This is for guidance only and not indicative of future results.

Platinum : 3.07%Gold Plus : 20.74%Gold : 56.62%Certified : 19.57%

25

ESG in Real Estate

E. US: Sale premia is higher than rent premia

Study Fuerst,McAllister, 2011Green Noise or Green Value? Measuring hat Effects of Environmental Certification on Office Values

Findings

• The sale premia of office buildings is higher than the rent premia.

• This difference is possibly due to combined effects on capital value of higher rental income, lower oper-ating costs, increased occupancy rates, image bene-fits and a lower risk premia.

Data 16,000+ office building rents834 Energy Star, 197 LEED certified9,000+ office building sales prices559 Energy Star, 127 LEED certified(US, 1999-2010)

Methodology Comparison between labeled and non-labeled build-ings

Figure 26: Value premia (Reference: non-certified building) 24

0%

5%

10%

15%

20%

25%

30%

Rent Sale

Diff

eren

ce in

sal

e pr

ice

per s

quar

e m

eter

in p

erce

nt

LEED-certified

Energy Star-certified

F. Netherlands: Access to public transport and facilities is rewarded

Study Kok, Jennen, 2012The Impact of Energy Labels and Accessibility on Office Rents

Findings

• On average, a less efficient “non-green“ building (rated D-G) achieves a 6.5% lower rent as compared to a similar “green“ building (rated A-C).

• Office buildings in multi-functional areas with access to public transport and facilities achieve rental pre-mia compared to mono-functional areas.

Data 1072 buildings EPC rated A-G(Netherlands, 2005-2010)

Methodology Comparison between EPC A-C rated and EPC F-G rated buildings

Evidence of impact of social factor

24 Allianz Global Investors, 2015. Please note: This is for guidance only and not indicative of future results.

26

ESG in Real Estate

G. Australia: Especially high premia in Canberra

Study Newell et al., 2014Assessing energy rating premia in the performance of green office buildings in Australia

Findings

• There is evidence of value premia in higher rated NABERS categories and value discounts in lower rat-ed NABERS categories.

• Comparably high premia in Canberra might be due to mandatory energy rating requirements for tenant-ing offices.

• Energy rating premia were generally evident in re-duced vacancy, reduced outgoings, reduced incen-tives and reduced yields.

Data 366 buildings (Australia, 2011)206 NABERS certified

Methodology Comparison between labeled and non-labeled rated buildings

Figure 27: Value premia 24

-15

-10

-5

0

5

10

15

20

25

Overall Sydney CBD Sydneysuburban

Canberra

Valu

e pr

emiu

m/d

isco

unt (

%)

2/2.5

3/3.5

4/4.5

5

Figure 28: Net effective rent premia by NABERS rating 24

-8-6-4-202468

1012

Overall Sydney CBD Sydneysuburban

Canberra

Net

effe

ctiv

e re

nt

prem

ium

/dis

coun

t (%

)2/2.53/3.54/4.55

24 Allianz Global Investors, 2015. Please note: This is for guidance only and not indicative of future results.

27

ESG in Real Estate

Green building examples

Allianz France Acacia (La Défense) 25

Driving energy consumption in buildings downwards

Reducing greenhouse gas emissions from buildings (the 2nd big-gest source accounting for 34% of all emissions) means reducing energy consumption and, where possible, replacing fossil fuels with renewable energy or energy from sources that generate lower emissions.

To reduce energy consumption Allianz France is focusing on sev-eral areas:

• Improving the energy efficiency of buildings

• Optimising building use in terms of management

• Raising the awareness of building occupants in good prac-tices for energy use

• Making information technology more energy efficient

The main operational buildings accommodating 80% of Allianz France employees have significantly reduced their energy con-sumption through a number of initiatives:

• The closure of several less energy-efficient sites

Figure 29: Energy need of buildings 25

• Special focus on management and control of energy use by service providers using the buildings, with special measures included in maintenance contracts

• Research into energy control products

With regard to the last point, two products have been rolled out on a test basis, one at the Acacia site in La Défense and the other in the Lyon building. In each case the approach taken is based on real time supervision of fluid consumption (electricity, gas, urban heating and cooling networks, and later) and of building heat be-havior models.

The changes in the energy needs of the sites can be tracked by reference to climate variations. These variations are taken into ac-count via a UDD (Unified Degree Days base 18) calculation, which in particular represents heating needs depending on the weather.

The almost immediate detection of anomalies (leaks, over-con-sumption at night or weekends) and the highlighting of differ-ences with the benchmark levels mean the building’s operation can be optimised. Better use of building management systems will help improve performance.

25 Source: https://www.allianz.com/v_1399880502000/media/responsibility/documents/Allianz_France_SD_Report_2013.pdf.

SiteEnergy control Solutions/

Provider Date of implementationReduction in the site’s energy need in kWh /

occupant / UDD since implementation

Acacia (La Défense) ERGELIS December 2011 > 50%

Lyon UBIGREEN November 2011 > 20%

28

ESG in Real Estate

Allianz Germany Unterföhring 26

The buildings in Unterföhring, Allianz Germany’s largest site worldwide with approximately 6800 employees, have been aligned with Environmental Protection Guidelines. Based on this, Allianz Germany achieved high energy savings in 2014:

• Electricity production: with the aid of photovoltaic panels covering an area of 532m2 on the south façade, approx.

Allianz Tower Jakarta 26

Allianz has made an eye-catching commitment to sustainability in design with the new 28-storey Allianz Tower in the central business district of Jakarta. The Tower serves as the headquarters of all Allianz’ Indonesian operations since 2012. This striking landmark in downtown Jakarta incorporates many aspects of environmental sustainable design, including:

• Building orientation: Designed to be slimmest on the east and west facades to reduce heat and UV radiation.

26 Source: https://www.allianz.com/en/sustainability/engagement/sustainability_in_practice/europe/Allianz_in_Green_Allianz_Germany.

• Natural water absorption: Thanks to the Tower’s minimal foot-print 70 percent of the site functions as a natural rainwater ab-sorbent to reduce the flooding risk in Jakarta.

• 80 percent of grey and black water recycled: Water reused and rainwater collected for air-conditioning, toilet flushing or flower watering; only a fifth of wastewater discharged.

• Green environment: Numerous large trees on the water-rich site.

• High-tech double-glazing: Heat drastically reduced and ex-cessive traffic noise eliminated.

The design of the Allianz Tower reflects the principles of “openness, transparency, flow of information and harmonious integration of a modern office building in an environmentally friendly manner”. Allianz wants to serve as a good example for the future develop-ment of sustainable high-rise buildings.

18,500 kWh renewable energy was produced in 2014. Since the panels were installed, they have supplied around 368,000 kWh renewable energy to the building.

• The heat produced by nearby data centers is used to heat the company building and the two administrative build-ings. The use of waste heat enabled 11,900,000 kWh (which would otherwise have been used for generating heat) to be saved in 2014. This corresponds to 78% of the heating re-quirements for the 3 buildings at Unterföhring. The savings in district heating as a result of using waste heat total around 174,000,000 kWh since its installation.

In addition to reducing the amount of energy and resources con-sumed, the use of renewable energy sources has been a key ele-ment of this plan. The most relevant measure is the switch to hydro-electric power. Already since 2010, all large Allianz Germany premises have been supplied with 100% hydro-electric power.

29

ESG in Real Estate

Allianz Global Investors’ Triton-Haus 27

Triton-Haus in Frankfurt’s Westend has been completely revital-ized in the past few years in line with the highest ecological stan-dards. The office area measures 28,540m² incl. lobby, storage space of 2,408m² and terrace of 1,200m².

One year after the 10-storey high building went into operation, it was officially certified with DGNB Gold:

• Optimized building shell, sunshade facilities (3-pane heat in-sulation glazing and external sun protection)

• Highly energy-efficient systems for the supply of energy, combined heat and power station (CHPS) run by biogas, heat output of approx. 200kW. The use of organic gas is another important contribution to CO2 reduction.

• Ventilation systems and pumps with high electric efficiency. Surface cooling and heating creates a physiologically pleas-ant room climate through the high cooling and low heating temperatures.

• Innovative concepts for LED lighting with movement sensors both inside and outside are important components of the energy concept. Triton-Haus is one of the first office buildings in Germany that has been equipped with LED lighting not only in the common areas, but also in the offices.

• Sound protection: Airborne and footfall sound protection against exterior noise, third-party working rooms as well as noise insula-tion against technical plants exceeded by at least 1dB(A).

27 Source: http://www.allianz-realestate.com/en/responsibility/case-study-triton-haus.28 Source: http://www.thomas-daily.de/en/project/detail/id/d0362e45-3c1f-42d2-9f06-0ceb2d269492/lt/Paris-France/t/Athena-Tower.

Tour Allianz One 28

Athena Tower is a 27-story skyscraper in one of the most prestigious business districts of Europe, La Défense, in Paris. The tower was built in 1984 and was completely refurbished in 2014. The tower provides 35,000m² of leasable office space and 128 parking spaces.

The building includes a restaurant, cafeteria and meeting rooms. The glass volume resembles a crystalline shape. The refurbished Athena Tower will use 40 % less energy than a regular office build-ing of its size. It was awarded the HQE, BREEAM, CERTIVEA and LEED GREEN BUILDING certification for environmentally friendly con-structions.

• Building management system (BMS);

• Good natural lighting;

• The use of photovoltaic panels;

• Efficient façade system: the southern and western facades were provided with a double skin system and horizontal sun shading louvers for better control of direct sunlight;

• Energy-efficient air-conditioning system, using chilled beams.

30

ESG in Real Estate

Please note: the conclusions from the research studies analysed and summarised do not necessarily reflect AllianzGI‘s – risklab‘s investment opinion. The research does not imply investment advice or investment performance related forecasts. risklab GmbH (“risklab”) is a company of Allianz Global Investors GmbH and is the Investment and Risk Advisory Expert of AllianzGI Global Solutions. risklab is registered in Germany with Bundesanstalt für Finanzdienstleistungsaufsicht (www.bafin.de) as a provider of financial services. risklab is not licensed to conduct business outside of Germany and is not registered with the US Securities and Exchange Commission or any regula-tory authority in Asia Pacific. The services of risklab are not available directly to persons outside of Germany. risklab provides risk management and strategic and dynamic asset allocation solutions to support the investment advisory activities of properly registered and licensed affiliates of AllianzGI throughout the world.

Investing involves risk. The value of an investment and the income from it could fall as well as rise and investors might not get back the full amount invested. Past performance is not indicative of future performance.

Unlike actual performance data, simulations are not based on actual transactions; thus, their significance underlies inherent limitations. Simulations are not able to account for the impact of actual portfolio trading as it may have been affected by economic and market factors, such as a lack of liquidity. If the currency in which the past perfor-mance is displayed differs from the currency of the country in which the investor resides, then the investor should be aware thatdue to the exchange rate fluctuations the performance shown may be higher or lower if converted into the investor’s local currency.

This is a marketing communication. It is for informational purposes only. This document does not constitute investment advice or a recommendation to buy, sell or hold any security and shall not be deemed an offer to sell or a solicitation of an offer to buy any security.

The views and opinions expressed herein, which are subject to change without notice, are those of the issuer or its affiliated companies at the time of publication. Certain data used are derived from various sources believed to be reliable, but the accuracy or completeness of the data is not guaranteed and no liability is assumed for any direct or consequential losses arising from their use. The duplication, publication, extraction or transmission of the contents, irrespective of the form, is not permitted.

This material has not been reviewed by any regulatory authorities. In mainland China, it is used only as supporting material to the offshore investment products offered by commercial banks under the Qualified Domestic Institutional Investors scheme pursuant to applicable rules and regulations.

This document is being distributed by the following Allianz Global Investors companies: Allianz Global Investors U.S. LLC, an investment adviser registered with the U.S. Securities and Exchange Commission (SEC); Allianz Global Investors GmbH, an investment company in Germany, authorized by the German Bundesanstalt für Finanzdien-stleistungsaufsicht (BaFin); Allianz Global Investors Asia Pacific Ltd., licensed by the Hong Kong Securities and Futures Commission; Allianz Global Investors Singapore Ltd., regulated by the Monetary Authority of Singapore [Company Registration No. 199907169Z]; and Allianz Global Investors Japan Co., Ltd., registered in Japan as a Financial Instruments Business Operator; Allianz Global Investors Korea Ltd., licensed by the Korea Financial Services Commission; and Allianz Global Investors Taiwan Ltd., licensed by Financial Supervisory Commission in Taiwan.

As at December 2015

Key contact

Dr. Steffen HörterCo-Head Investment & Risk Consulting

risklab GmbHThe Investment and Risk Advisory Experts ofAllianz Global Investors, Global SolutionsSeidlstraße 24-24aD-80335 Munich

Phone: +49 - (0)89 - 1220 – 7704e-mail: [email protected]: www.risklab.com

Basis for the research were recent publicly available research studies and interviews with selected Real Estate experts. This research was performed in H1 2015.

Please note: the conclusions from the research studies analyzed and summarized in this report do not necessarily reflect AllianzGI’s – risklab‘s investment opinion. The research does not imply investment advice or investment performance related forecasts.

As part of the study I am extremely grateful for the following contributors:

• Patrick Stekelorom, Allianz Real Estate France / Développement Durable

• Kieran Farrely, The Townsend Group

• Dominik Werner, Allianz Global Investors, Global Solutions / Manager Research & Selection

• Annika Börsch, Technical University of Munich (Research Project Manager)

Dr. Steffen Hörter