essar refinery iosh presentation

TRANSCRIPT

Stanlow Manufacturing Complex

1

Stanlow Manufacturing Complex

Leading market position

• Positioned to serve the UK Energy

Corridor

• Integrated into extensive pipeline

logistics with good road links

Superior assets

• Complex Refinery with a

comprehensive product slate with

speciality production

• Strong focus on Asset Integrity and

Reliability, and managing Asset Lifecycle

2

Stanlow Refinery – Significant Potential

• Acquired by Essar Energy 31 July 2011

• Fully integrated Stanlow into Essar Energy

o Maintained strong operating and safety

performance

• Initiated 100 day plan; delivery well on track

o Reviewed all aspects of refinery operations

o Identified over US$3/bbl of sustainable GRM

improvement projects

o Benefits higher than original acquisition plan

• Inventory monetisation transaction with Barclays

o Repaid working capital facility and released

margin money

3

75

75

75

0

50

100

150

200

250

FY12-13 FY13-14 FY14-15

Optimisation Projects

• Identified US$3/bbl of sustainable

margin improvements to be

delivered by end FY2014

• Targeted capex investments with

high returns, e.g. natural gas

• Other margin enhancing projects

with minimal capex:

o Introduction of “opportunity

crudes” and crude blending

o Closure of lubricants production

• c.US$1/bbl margin benefit already

delivered, a further US$2/bbl being

secured over coming months

• c.US$225 million uplift to EBITDA is

achievable

Stanlow Incremental EBITDA Opportunity

Year

en

d r

un

rat

e (U

S$ m

illio

n)

4

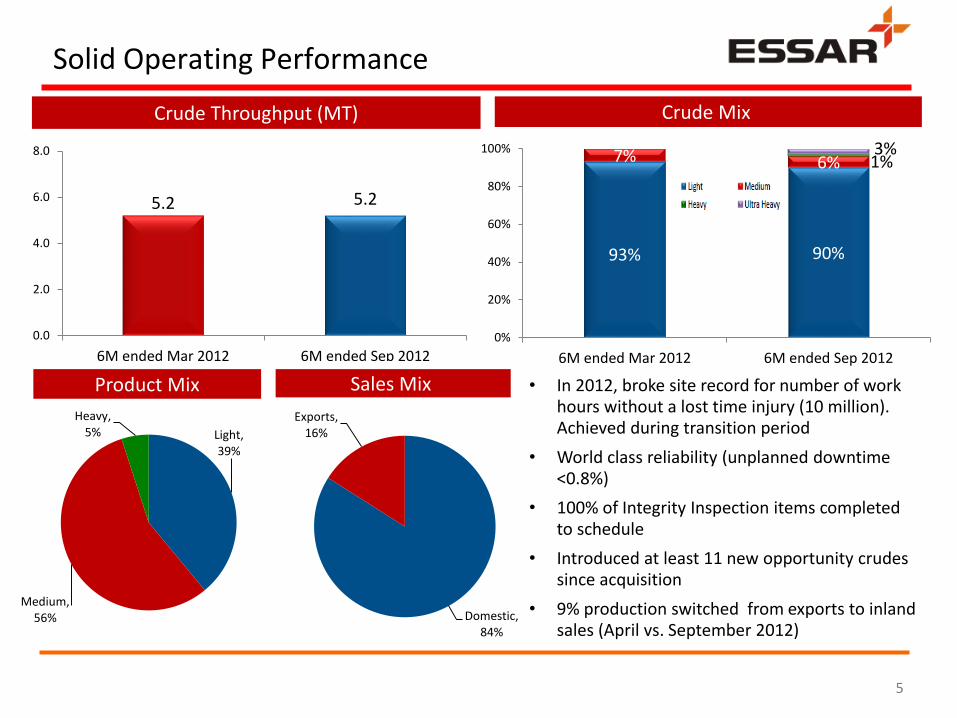

Solid Operating Performance

Crude Throughput (MT) Crude Mix

Product Mix Sales Mix

5.2 5.2

0.0

2.0

4.0

6.0

8.0

6M ended Mar 2012 6M ended Sep 2012

93% 90%

7% 6% 1%3%

0%

20%

40%

60%

80%

100%

6M ended Mar 2012 6M ended Sep 2012

Light, 39%

Medium, 56%

Heavy, 5%

Domestic, 84%

Exports, 16%

• In 2012, broke site record for number of work hours without a lost time injury (10 million). Achieved during transition period

• World class reliability (unplanned downtime <0.8%)

• 100% of Integrity Inspection items completed to schedule

• Introduced at least 11 new opportunity crudes since acquisition

• 9% production switched from exports to inland sales (April vs. September 2012)

5

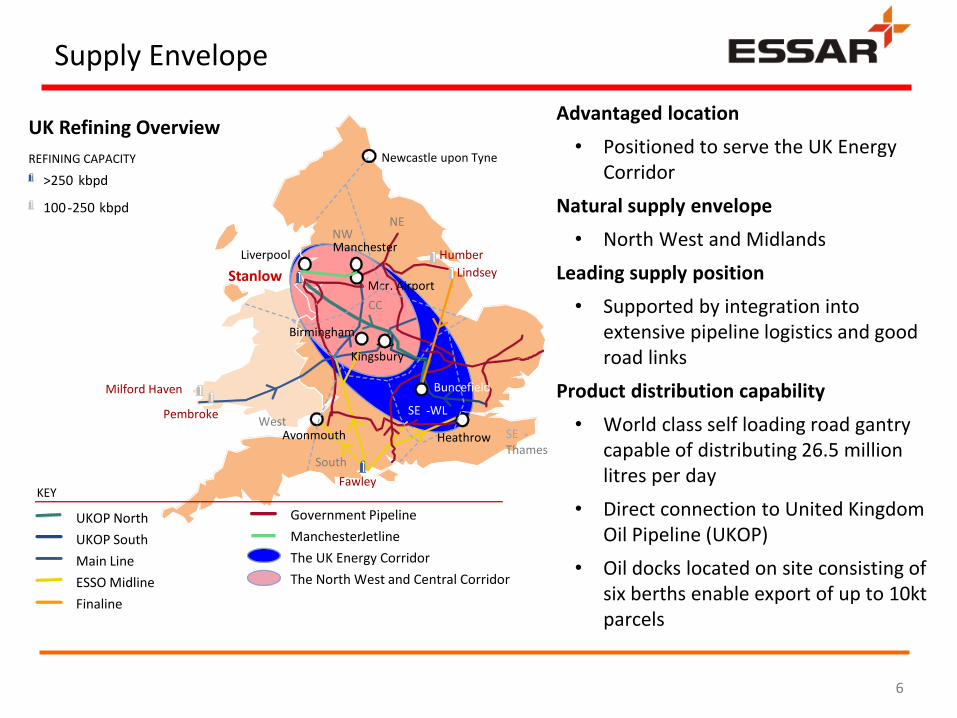

Supply Envelope

Advantaged location

• Positioned to serve the UK Energy Corridor

Natural supply envelope

• North West and Midlands

Leading supply position

• Supported by integration into extensive pipeline logistics and good road links

Product distribution capability

• World class self loading road gantry capable of distributing 26.5 million litres per day

• Direct connection to United Kingdom Oil Pipeline (UKOP)

• Oil docks located on site consisting of six berths enable export of up to 10kt parcels

UK Refining Overview

Humber

LindseyStanlow

Liverpool

Mcr. Airport

Newcastle upon Tyne

NWNE

CC

South

WestSE -WL

SE -Thames

Kingsbury

Manchester

HeathrowAvonmouth

Buncefield

Fawley

Pembroke

Milford Haven

Main Line

Government Pipeline

Finaline

UKOP North

UKOP South

ESSO Midline

Manchester Jetline

The UK Energy Corridor

KEY

The North West and Central Corridor

100 -250 kbpd

>250 kbpd

REFINING CAPACITY

Birmingham

6

Competitive Position

UK Refineries

Significant capacity and complexity

• Well positioned as one of the

lowest cost refineries delivering

product into the UK Market

Lowest cost supplier into the North

West

• The only refinery located in the

North West

Highly competitive in supplying

adjacent markets

• UKOP pipeline connection

• Closest refinery to Birmingham,

Manchester and Liverpool

7

Fawley

Stanlow

HumberLindsey

PembrokeGrangemouth

Milford Haven

100

150

200

250

300

350

4 6 8 10 12

Capacity

Complexity

Original Design Capacity

Operating Max Capacity

Closure of 80kbbls/d capacity in Jan 2012

Business Overview

• Track record of leading operational performance in HSSE, Reliability and Cost

o Continuous improvement

• Strong location and supporting infrastructure

o Waterfront, road and pipeline connections

o Good green belt segregation and supportive local communities

o Ample plot space available for expansion

• Well invested assets and robust asset management processes

• Clear pathways to stay compliant with developing environmental legislation

• On target to become robust against bottom-of-cycle margins

• Delivery of $3/bbl 100 Day Plan progressing ahead of schedule

8

Appendix: Background slides

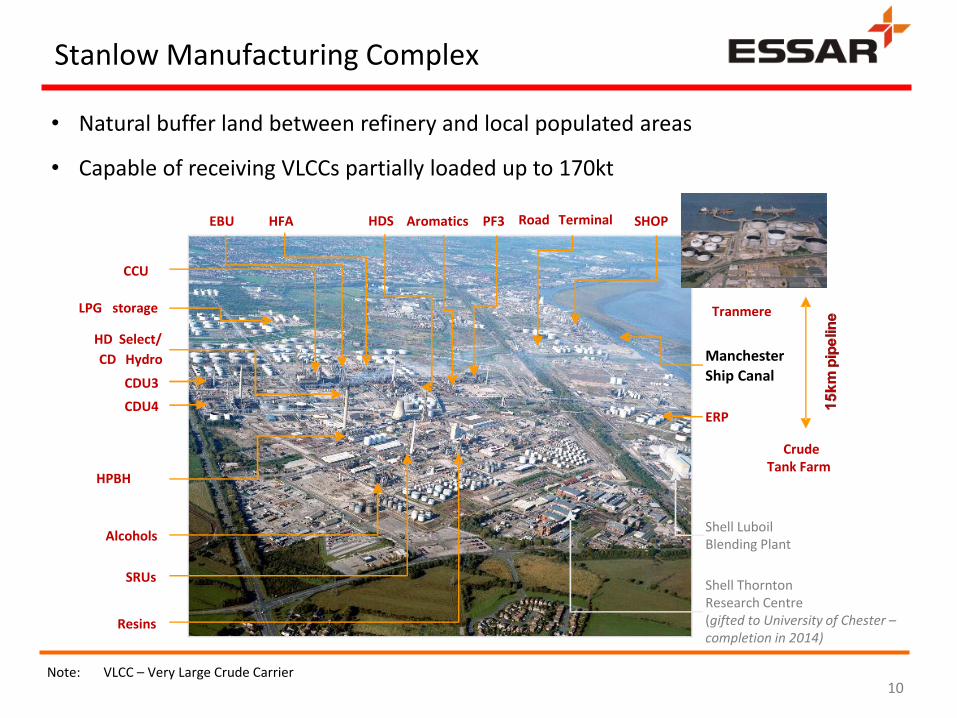

Stanlow Manufacturing Complex

• Natural buffer land between refinery and local populated areas

• Capable of receiving VLCCs partially loaded up to 170kt

HPBH

LPG storage

HD Select/

CD Hydro

CDU3

CDU4

Alcohols

SRUs

Resins

Shell Thornton Research Centre(gifted to University of Chester –completion in 2014)

Shell LuboilBlending Plant

CCU

EBU HFA Aromatics PF3 SHOPRoad Terminal

ManchesterShip Canal

ERP

CrudeTank Farm

Tranmere

HDS

10Note: VLCC – Very Large Crude Carrier

Road55%Pipeline

25%

Water20%

Modes of Distribution

Stanlow is sited on a 650 hectare site

• Natural buffer land between refinery and local populated areas

• Stanlow contained in an industrialised area

Product distribution capability

• World class self loading road gantry capable of distributing 26.5 million litres per day

• Direct connection to United Kingdom Oil Pipeline (UKOP)

• Oil docks located on site consisting of six berths enable export of up to 10kt parcels

Crude import facilities at Tranmere

• Capable of receiving VLCCs partially loaded up to 170kt

1 SCUK SHOP 2 LPG Terminal 3 ResinsLease 4 SCUK Alcs 5 Shell Lubes Plant

6 Shell Thornton* 7 Former Burmah Site (acquired post transition) 8 White Oil Docks

Stanlow Site, including non operational land

3rd Party Land Leased to 3rd Pty

Location & Supporting Infrastructure

* Shell Thornton gifted to University of Chester – to be phased over 18 months from Mar 2013

11

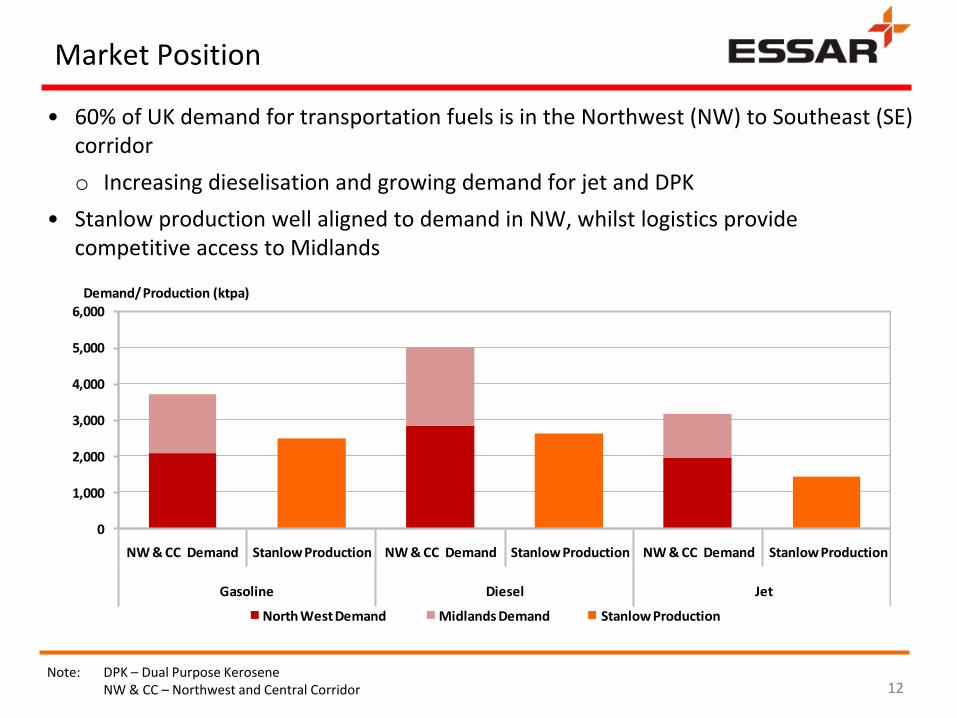

Market Position

0

1,000

2,000

3,000

4,000

5,000

6,000

NW & CC Demand Stanlow Production NW & CC Demand Stanlow Production NW & CC Demand Stanlow Production

Gasoline Diesel Jet

North West Demand Midlands Demand Stanlow Production

Demand/ Production (ktpa)

• 60% of UK demand for transportation fuels is in the Northwest (NW) to Southeast (SE) corridor

o Increasing dieselisation and growing demand for jet and DPK

• Stanlow production well aligned to demand in NW, whilst logistics provide competitive access to Midlands

12Note: DPK – Dual Purpose Kerosene

NW & CC – Northwest and Central Corridor

Inland Sales Profile

Diesel Mogas

Kerosene Gasoil

Chemicals Fuel Oil/Bitumen

LPG Base Oil/Waxes

Shell CBF

International Oil Co Hypers

Independents Chemicals

Marine

Essar sells ~84% of Stanlow production in UK market

13

9%

0%

0%

5%

2%

4%

9%

24%

15%

26%

6%

2%

0% 10% 20% 30%

Refinery Fuel/ Loss

Other

Bitumen

Chemicals

Base Oils

Fuel Oil

Gasoil

Diesel

Jet

Gasoline

Naphtha

LPG

Product Yield Profile

Typical Yield on CrudeHigh Nelson complexity of 8.2 enables high black to white oil conversion

• Fuel oil production is significantly lower than industry norm

• Since 2009, gas-to-liquid imports have supported increased jet and diesel production

Speciality grades

• Production of high octane fuels and bitumen is a differentiator to marker margins

• Aromatics production (Benzene, Toluene)

Chemical grades offer significant upgrading

• Propylene sold via pipeline to an upgrading customer within the UK

• Ethyl benzene is sold 3rd party plant in Netherlands

14

Safety Highlights

Stanlow cares about the safety of employees and Business Partners – We are

determined to stop people getting injured.

• 10 Million man hours without a Lost Time Injury was achieved on June 17th 2012.

• 5 million man hours achieved 3 times since

• Stanlow awarded the 2016 Order of Distinction for Occupational Health and Safety

by RoSPA, the Royal Society for the Prevention of Accidents. For the 20th

Consecutive year

15

Complex site with deep conversion

Large residue cat cracker

Comprehensive petrochemical linkages

CDU3

CDU4

Platformer

HVI Unit

Gasoline Blender

Merox

Propylene Splitter

Fuel Oil Blender

Alkylation

Ethyleneimport

CrudeEthyl Benzene

SHOP

Alcohols (SHF)

Fuel gas

LPG

Alpha Olefins

Internal Olefins

Alcohols

Gasoline

Toluene

Benzene

Ethylbenzene

Jet

Gasoil

Propylene

Fuel Oil

Bitumen

Cat Cracker

Gas Oil HDSGas Oil Blender

Products

Superior Assets

Aromatics Extraction

16