essays in financial economics - cmu

TRANSCRIPT

DISSERTATION

Essays in Financial Economics

Presented by

EMILIO BISETTI

Submitted to the Tepper School of Business

in partial fulfillment of the requirements for the degree of

Doctor of Philosophy

at

CARNEGIE MELLON UNIVERSITY

April 2018

Dissertation Committee:

Burton Hollifield (Co-Chair)

Stephen A. Karolyi

Stefan Lewellen

Pierre Jinghong Liang

Chris Telmer

Ariel Zetlin-Jones (Co-Chair)

c© Emilio Bisetti 2018ALL RIGHTS RESERVED

Acknowledgments

I am deeply indebted to Burton Hollifield, Ariel Zetlin-Jones, and Chris Telmer, for their endlesssupport and guidance throughout the years. They taught me much of what I know about research,economics, and finance. They spent countless hours listening to, discussing, and helping me de-velop my research ideas. They always treated me as a colleague and a friend, and never stoppedencouraging me to do better.

I am extremely grateful to Steve Karolyi and Stefan Lewellen for their invaluable energy and support.The first chapter of this dissertation greatly improved in quality and depth thanks to their selflesshelp, and they have been fantastic mentors during my job market.

I thank Laurence Ales and Finn Kydland for organizing Macro-Finance PhD workshops and stimu-lating a collaborative research environment between Tepper PhD students. I am also grateful to themany Tepper faculty who generously offered their time to provide feedback to my work. I am parti-cularly grateful to Pierre Liang for serving in my dissertation committee.

I thank my friends and fellow PhD students for years of intense work and fun. In particular, I thankHakkı Ozdenoren, Alex Schiller, and Ben Tengelsen, for endless conversations about economics andfinance. Both the content of my research and my ability to communicate my research to others havegreatly benefited from these conversations. I am especially grateful to Lawrence Rapp and Laila Leefor their invaluable assistance with administrative matters.

I consider myself lucky for having such wonderful friends outside of work as Giorgio Antongio-vanni; Alessandro Biggi; Francesco Brachetti; Ciprian Domnisoru; Daniela Frattini; Christian Frem;Maria Pia Guffanti; Francesco Maccarana; Fulvio Mazza; Andrea Mazzanti; Giacomo Meo; FrancescoMorandi; Marie-Lou and Dana Nahhas; Fares Nimri; Nicola Paccanelli; Pietro Pollichieni; CristinaSangaletti; Andrea Tremaglia; and Dario Zocchi. Their friendship has been essential for me to succeedin graduate school.

Finally, I am truly grateful to Jana for her love and for her patient support during the last years ofmy doctorate. My biggest thanks goes to family for listening to, understanding, and supporting meat every step of my life. This dissertation is dedicated to them.

i

A Silvia, Paolo,Alberto, e Francesco.

Abstract

In the first essay, I address the current debate on the costs and benefits of financial regulation, andI show that financial regulation can increase bank shareholder value by reducing shareholder moni-toring costs. I use a regression discontinuity design to study the effect of an unexpected decrease insmall-bank reporting requirements to the Federal Reserve. Using the reporting change as a negativeshock to regulatory monitoring by the Fed, I find that reduced Fed monitoring leads to a 1% lossin Tobin’s q and a 7% loss in equity market-to-book. I show that these losses come from increasedinternal monitoring expenditures, managerial rents, and monitoring conflicts between shareholders.My results are among the first to quantify the shareholder value of monitoring.

In the second essay (with Benjamin Tengelsen and Ariel Zetlin-Jones), we re-examine the importanceof separation between ownership and labor in team production models that feature free riding. Insuch models, conventional wisdom suggests an outsider is needed to administer incentive schemesthat do not balance the budget. We analyze the ability of insiders to administer such incentive sche-mes in a repeated team production model with free riding when they lack commitment. Specifically,we augment a standard, repeated team production model by endowing insiders with the ability toimpose group punishments which occur after team outcomes are observed but before the subsequentround of production. We extend techniques from Abreu (1986) to characterize the entire set of perfect-public equilibrium payoffs and find that insiders are capable of enforcing welfare enhancing grouppunishments when they are sufficiently patient.

In the third essay, I re-examine an important prediction of asset pricing theory which has historicallyfound little support in the data—that expected consumption growth and equity returns should becorrelated. I first show empirically that advertising growth is a good proxy for expected consumptiongrowth, as it predicts both consumption growth and equity returns in aggregate post-war US data.To shed light on the link between advertising growth, expected consumption, and expected returns, Ithen build and calibrate a dynamic model of goods market frictions where firms invest in advertisingto build their customer capital (as in Gourio and Rudanko (2014)). Within the model, I show that theseverity of goods market frictions is a key element to replicate the predictability patterns I observe inthe data.

iii

Contents

Acknowledgments i

Abstract iii

1 The Value of Regulators as Monitors: Evidence from Banking 1

1.1 Introduction . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 2

1.2 Institutional Background and Motivating Theory . . . . . . . . . . . . . . . . . . . . . . 6

1.2.1 Institutional Background . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 6

1.2.2 Predictions from Agency Theory . . . . . . . . . . . . . . . . . . . . . . . . . . . 7

1.3 Empirical Setting . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 11

1.3.1 Data Sources and Measurement . . . . . . . . . . . . . . . . . . . . . . . . . . . 11

1.3.2 Estimation Strategy and Identification . . . . . . . . . . . . . . . . . . . . . . . . 15

1.4 The Value of Regulatory Monitoring . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 18

1.4.1 Main Results . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 18

1.4.2 Robustness, Placebo, and Falsification Tests . . . . . . . . . . . . . . . . . . . . . 21

1.5 How does Regulatory Monitoring Benefit Shareholders? . . . . . . . . . . . . . . . . . 23

1.5.1 Bank Value, Monitoring Expenditure, and Managerial Rents . . . . . . . . . . . 23

1.5.2 Regulatory Monitoring and Shareholder Free-Riding . . . . . . . . . . . . . . . 30

1.6 Discussion and Tests of Alternative Hypotheses . . . . . . . . . . . . . . . . . . . . . . 32

1.7 Conclusion . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 35

v

vi CONTENTS

2 Group Punishments without Commitment 37

2.1 Introduction . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 38

2.2 A Generalized Model of Repeated Team Production . . . . . . . . . . . . . . . . . . . . 42

2.2.1 Stage Game . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 42

2.2.2 Infinitely-Repeated Game . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 46

2.3 An Application: Repeated Oligopoly with a Principal . . . . . . . . . . . . . . . . . . . 57

2.3.1 Stage Game . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 57

2.3.2 Infinitely-Repeated Game . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 59

2.3.3 Substitutability and Price Externalities . . . . . . . . . . . . . . . . . . . . . . . 62

2.4 Conclusion . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 65

3 Advertising, Consumption, and Asset Prices 67

3.1 Introduction . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 68

3.2 Aggregate Advertising Expenditures and Equity Returns . . . . . . . . . . . . . . . . . 71

3.2.1 Consumption Growth and Excess Returns Predictability . . . . . . . . . . . . . 72

3.2.2 Robustness . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 78

3.3 Model . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 83

3.3.1 Firm Problem and Return on Equity . . . . . . . . . . . . . . . . . . . . . . . . . 86

3.3.2 Household Problem . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 89

3.3.3 Equilibrium . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 90

3.4 Results . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 91

3.4.1 Calibration and Computation . . . . . . . . . . . . . . . . . . . . . . . . . . . . 91

3.4.2 Simulated Moments and Predictability . . . . . . . . . . . . . . . . . . . . . . . 92

3.4.3 The Quantitative Impact of Goods Market Frictions . . . . . . . . . . . . . . . . 93

3.5 Conclusion . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 96

CONTENTS vii

A Appendix to Chapter 1 99

A.1 Solving for the Optimal Contract . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 100

A.2 Additional Results: Bank Value . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 101

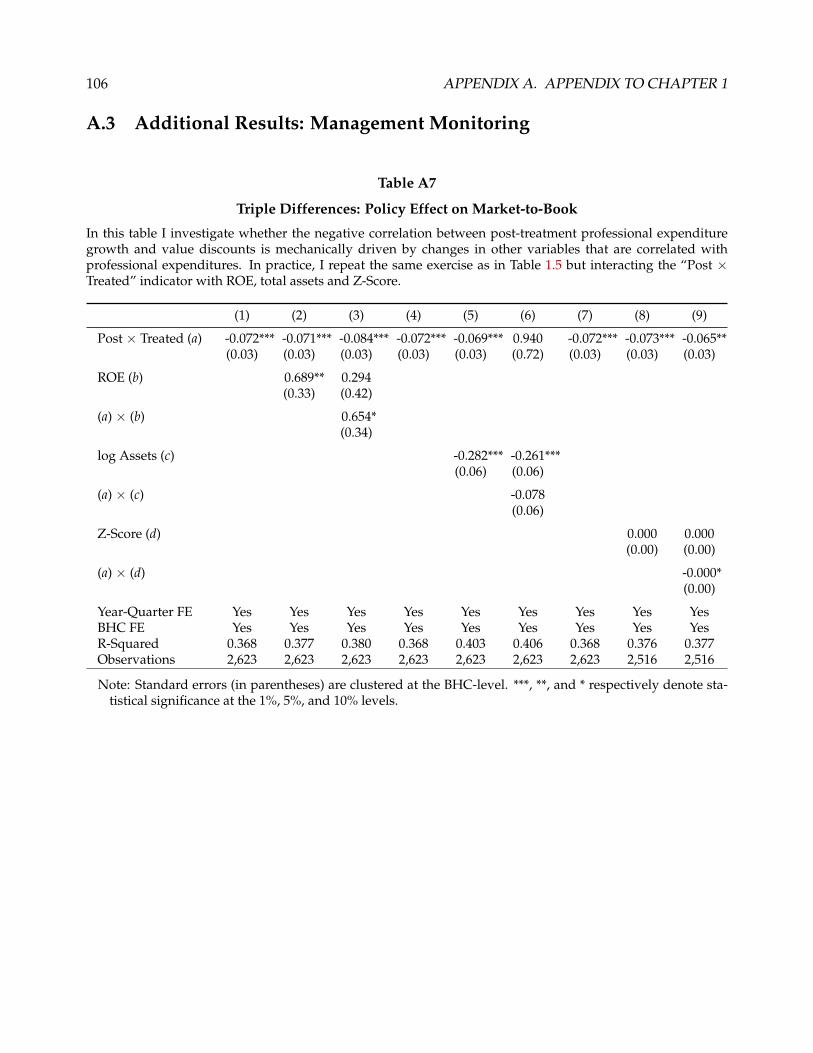

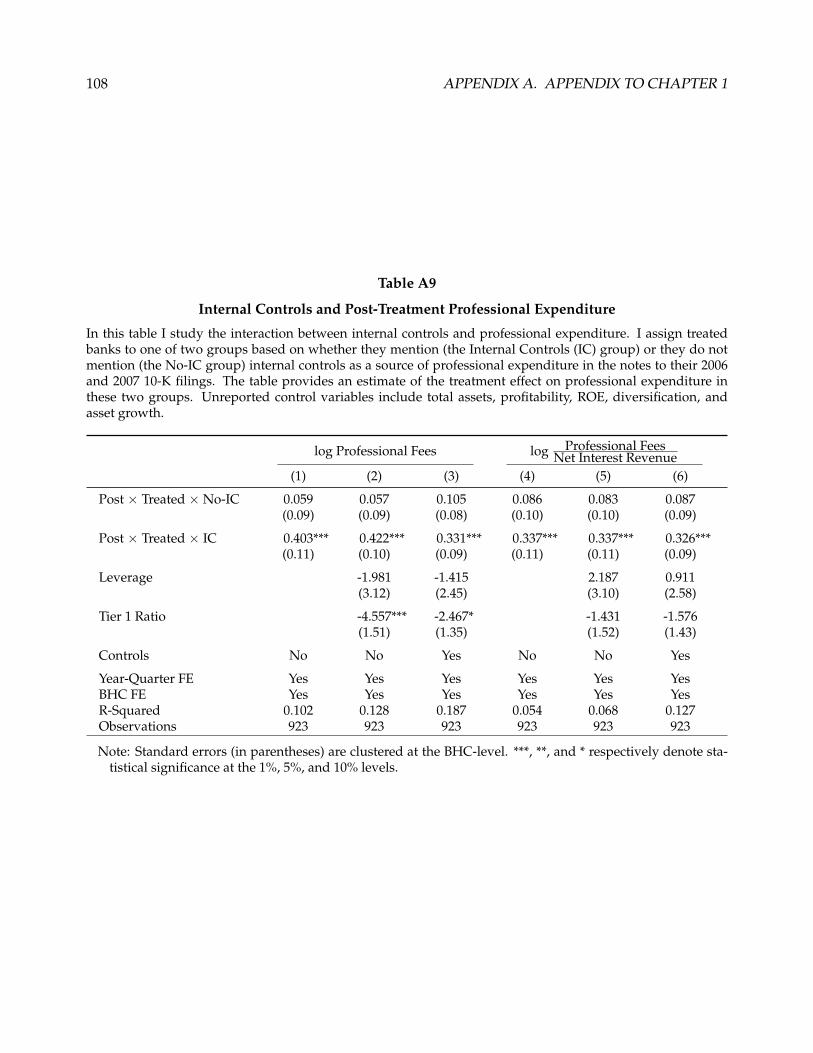

A.3 Additional Results: Management Monitoring . . . . . . . . . . . . . . . . . . . . . . . . 106

A.4 Tests of Additional Hypotheses . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 115

B Appendix to Chapter 2 119

B.1 Substitutability and Price Externalities . . . . . . . . . . . . . . . . . . . . . . . . . . . 120

B.1.1 Stage Game . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 120

B.1.2 Infinitely-Repeated Game . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 121

B.2 Definitions and Proofs . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 124

B.2.1 Definitions and Proofs from Sections 2.2 and 2.3 . . . . . . . . . . . . . . . . . . 124

B.2.2 Proofs from Appendix B.1 . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 131

B.3 Computational Algorithm . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 137

C Appendix to Chapter 3 139

C.1 Cointegration Tests . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 140

C.2 Advertising Expenditures and Long-Run Risk . . . . . . . . . . . . . . . . . . . . . . . 142

C.3 Derivation of the Stochastic Discount Factor . . . . . . . . . . . . . . . . . . . . . . . . . 144

C.4 Computational Algorithm . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 144

List of Tables

1.1 Summary Statistics . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 13

1.2 The Policy Effect on Bank Shareholder Value . . . . . . . . . . . . . . . . . . . . . . . . 19

1.3 Robustness and Placebo Tests: Tobin’s q . . . . . . . . . . . . . . . . . . . . . . . . . . . 22

1.4 The Policy Effect on Bank Professional Expenditure . . . . . . . . . . . . . . . . . . . . 24

1.5 Professional Expenditure Growth and Post-Treatment Value Losses . . . . . . . . . . . 26

1.6 Managerial Rents: Earnings Smoothing in the Financial Crisis . . . . . . . . . . . . . . 29

1.7 Cash Flow Risk, Shareholder Value, and Professional Expenditures . . . . . . . . . . . 30

1.8 Ownership, Management Monitoring, and Value . . . . . . . . . . . . . . . . . . . . . . 31

3.1 Summary Statistics for Predictors, Post-War Period . . . . . . . . . . . . . . . . . . . . 76

3.2 Consumption Growth and Excess Returns Predictability, Post-War Period . . . . . . . 77

3.3 Excess Returns Predictive Regressions, Post-War Period . . . . . . . . . . . . . . . . . . 78

3.4 Tri-Variate Excess Returns Predictive Regressions, Post-War Period . . . . . . . . . . . 79

3.5 VAR Model for Advertising and Consumption Growth, Post-War Period . . . . . . . . 80

3.6 VAR Model for Advertising and Consumption Growth, 1922-2009 and 1982-2009 . . . 81

3.7 Consumption Growth Predictive Regressions, Post-War Period . . . . . . . . . . . . . 82

ix

x LIST OF TABLES

3.8 Out-of-Sample Excess Returns Predictive Regressions . . . . . . . . . . . . . . . . . . . 85

3.9 Model-Simulated Moments . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 93

3.10 Results: Returns Predictability . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 94

3.11 Predictability in the Centralized Economy . . . . . . . . . . . . . . . . . . . . . . . . . . 96

A1 Robustness and Placebo Tests: Market-to-Book . . . . . . . . . . . . . . . . . . . . . . . 101

A2 Bank Size Manipulation Tests . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 102

A3 Event Study Around Policy Date . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 102

A4 Additional Robustness . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 103

A5 Quarterly Treatment Effects . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 104

A6 Falsification Tests: Non-Fed-Regulated Firms . . . . . . . . . . . . . . . . . . . . . . . . 105

A7 Triple Differences: Policy Effect on Market-to-Book . . . . . . . . . . . . . . . . . . . . 106

A8 Audit Fees . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 107

A9 Internal Controls and Post-Treatment Professional Expenditure . . . . . . . . . . . . . 108

A10 SEC Accelerated Filers . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 109

A11 Summary Statistics: Funding Costs, Profitability, and Earnings Smoothing . . . . . . . 110

A12 Funding Costs and Earnings Smoothing: Robustness and Placebo . . . . . . . . . . . . 111

A13 Robustness: Cash Flow Risk, Shareholder Value, and Professional Expenditure . . . . 112

A14 Chairman Ownership and Professional Expenditure Persistence . . . . . . . . . . . . . 113

A15 Chairman Ownership and Market-to-Book Discount Persistence . . . . . . . . . . . . . 114

A16 Government Tail Risk Insurance . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 115

A17 Voluntary Reporting . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 116

A18 Liquidity, Volatility, and Market Frictions . . . . . . . . . . . . . . . . . . . . . . . . . . 117

A19 Leverage and Capital Ratios . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 118

C1 Philips-Ouliaris and Johansen Tests for Cointegration . . . . . . . . . . . . . . . . . . . 141

C2 Vector-Error-Correction Model for Consumption Growth Predictions, Post-War Period 142

List of Figures

1.1 Common Trends in Pre-Policy Bank Valuation . . . . . . . . . . . . . . . . . . . . . . . 17

1.2 Bank Size Manipulation . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 18

2.1 Equilibrium Value Sets and Group Punishments . . . . . . . . . . . . . . . . . . . . . . 62

2.2 Input Substitutability and the Welfare Impact of Group Punishments . . . . . . . . . . 64

3.1 Expenditures in Physical and Non-Physical Advertising in the U.S., 1950-2010 . . . . . 72

3.2 Per-Capita Consumption and Advertising in the U.S., 1950-2010 . . . . . . . . . . . . . 73

3.3 Advertising Expenditures Growth, Consumption Growth and Excess Returns in theU.S., 1950-2010 . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 74

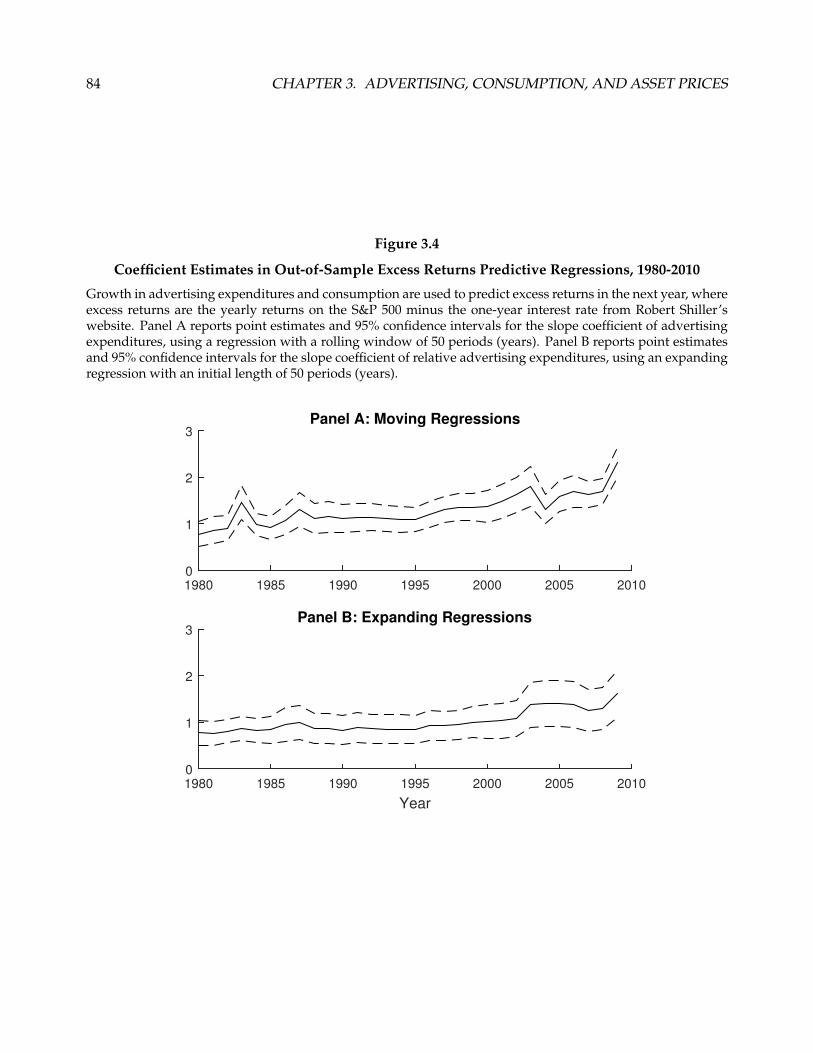

3.4 Coefficient Estimates in Out-of-Sample Excess Returns Predictive Regressions, 1980-2010 84

3.5 Customer Capital Investment . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 95

B1 Comparative Statics: Marginal Cost of Production and Welfare . . . . . . . . . . . . . . 124

xi

Chapter 1

The Value of Regulators as Monitors:Evidence from Banking

1

2 CHAPTER 1. THE VALUE OF REGULATORS AS MONITORS: EVIDENCE FROM BANKING

1.1 Introduction

A common view in the banking industry is that financial regulation has a negative impact on share-

holder value: regulatory compliance subtracts resources from lending and deposit-making activities,

reduces profits, and ultimately hurts investors. As a result, the recent decline of small and medium-

sized banks in the United States has often been attributed to regulation, and regulatory burden re-

duction for small banks is now a priority on the agenda of the US Federal Reserve (the Fed). In a

recent testimony to the House Financial Services Committee, the Chair of the Fed Board of Gover-

nors Janet Yellen stated: “With respect to small and medium-sized banks, we must build on the steps we have

already taken to ensure that they do not face undue regulatory burdens.”1 While the current policy discus-

sion highlights the costs of financial regulation for bank investors, agency theory suggests a positive

role for regulation in reducing the costs incurred by shareholders to monitor bank mangement.

In this paper, I exploit the regulatory environment of US Bank Holding Companies (BHCs) to study

the value impact of regulatory monitoring.2 The US Federal Reserve (the Fed) is the primary re-

gulator of BHCs, and a pervasive component of the Fed’s monitoring activity is the collection and

analysis of BHC financial statements. Both the frequency and the volume of BHC reporting to the

Fed are based on a fixed asset size threshold, such that smaller BHCs falling below the threshold are

exempted from most of the reporting requirements faced by larger BHCs above the threshold. I use

a 2006 Fed policy raising this size threshold as a shock to regulatory monitoring, and study changes

in bank value around the new threshold in a regression discontinuity design. My identification stra-

tegy comes from the quasi-random assignment of treated banks just below the threshold and control

banks just above the threshold before the Fed implements its policy, such that any systematic value

difference after the policy implementation is only due to differences in regulatory monitoring.

Following the predictions of agency theory, I interpret the change in Fed regulatory monitoring as a

shock to shareholder monitoring costs. To provide a structure to my empirical tests, I build a stylized

model of monitoring in the class of Townsend (1979), and derive three key predictions on the impact

1Yellen (2016).2Even if a BHC can include more than one bank, I will use the two terms interchangeably in the rest of the paper.

1.1. INTRODUCTION 3

of monitoring costs on shareholder value. In the model, a manager has private incentives to mis-

report bank cash flows and a shareholder can pay a monitoring cost to verify the cash flows reported

by the manager. When monitoring costs are small, the shareholder always monitors and extracts

the entire surplus from the bank. As monitoring becomes more expensive (as for treated banks),

shareholder value drops due to increased monitoring expenditures and increased managerial rents.

The first model prediction is therefore that reduced regulatory monitoring should lead to shareholder

value losses.

My main finding is consistent with the first prediction of the model: I show that, relative to control

banks, treated banks experience a 1% decrease in Tobin’s q (the market value of bank assets divided

by the book value of bank assets) and a 7% decrease in Market-to-Book (the market-to-book value of

bank equity) after the treatment. The finding is robust across a number of empirical specifications,

sample restrictions, placebo tests, and falsification tests. For example, the treatment effect is stronger

around the policy implementation date and threshold and disappears when I use arbitrary placebo

dates and thresholds to separate treatment and control groups, reducing sample selection concerns.

Moreover, my estimate of the treatment effect is not driven by pre-existing differences in valuation

across treated and control groups, and it is not biased by pre-treatment size manipulation.3 Impor-

tantly, the finding is not driven by changes in government bailout guarantees (Gandhi and Lustig

(2015)), financial disclosure (Hutton, Marcus, and Tehranian (2009)), stock liquidity and volatility,

and other size-based regulations implemented by the Fed at the beginning of 2006.

The second model prediction is that the value losses experienced by treated banks should be due

to increased monitoring expenditures and increased managerial rents. In line with this prediction,

I show that treated banks experience a 25% increase in their professional expenditures after the tre-

atment. These professional expenditures are largely related to bank internal controls, and strongly

correlated with post-treatment losses in shareholder value. Moreover, during the financial crisis

banks below the policy implementation threshold engage in more aggressive earnings smoothing

than banks above the threshold, confirming the prediction of increased managerial rents (Fudenberg

3Reporting exemptions are based on June 2005 BHC assets, but the threshold change is first announced by the Fed onlyin November 2005. Additionally, McCrary (2008) tests show no evidence of pre-treatment asset size manipulation.

4 CHAPTER 1. THE VALUE OF REGULATORS AS MONITORS: EVIDENCE FROM BANKING

and Tirole (1995)). Specifically, banks below the threshold decrease their Loan Loss Provisions (LLPs)

by more than banks above the threshold, and these LLP changes are due to managerial discretion

rather than to bank performance.

The third model prediction is that value losses and monitoring expenditures in treated banks should

both be positively correlated with the risk of their unobservable cash flows. Intuitively, high cash

flow risk increases the likelihood of tail states where cash flows are low or managerial rents are high,

decreasing bank value and increasing the marginal value of monitoring. Empirically, I proxy the risk

of unobservable cash flows with the absolute difference between analyst-forecasted and realized

bank profitability. I find that treated banks with high cash flow risk experience larger value losses

and professional expenditure growth than banks with low expected cash flow risk.

Finally, I argue that the increased monitoring costs faced by treated banks’ shareholders increase their

incentives to free-ride on each other’s monitoring (Grossman and Hart (1980), Holmstrom (1982)).

Consistent with Shleifer and Vishny (1986), the presence of a large shareholder—the board chair-

man—helps to mitigate shareholder free-riding problems after the treatment. I show that treated

banks with high chairman ownership experience higher professional expenditure growth and larger

value losses than treated banks with low chairman ownership. Moreover, post-treatment professi-

onal expenditure growth is more persistent and value drops are less persistent in banks with high

chairman ownership.

Overall, my paper is among the first to quantify the shareholder value of monitoring. Quantitatively,

I attribute around sixty percent of the loss in shareholder value for deregulated banks to increased

monitoring expenditure and managerial rents, and I attribute around forty percent of the loss to

increased free-riding problems. I conclude that regulation can be value-increasing for shareholders

when regulators monitor the management. My results are potentially applicable to other heavily-

regulated industries besides the banking industry, and provide new evidence against the standing

consensus that financial regulation negatively affects bank shareholders.

1.1. INTRODUCTION 5

Related Literature A long-standing question in financial economics is the extent to which moni-

toring affects shareholder value. Motivated by theoretical arguments (Shleifer and Vishny (1986),

Kahn and Winton (1998), Maug (1998)), the literature has traditionally focused on institutional ow-

nership as a measure of monitoring to estimate the impact of monitoring on firm value (McConnell

and Servaes (1990), Ferreira and Matos (2008)). Causal inference is however difficult in these studies,

because firm ownership and value are endogenously determined by firms’ contracting environment

(Himmelberg, Hubbard, and Palia (1999), Coles, Lemmon, and Meschke (2012)). My paper contribu-

tes to this literature by using a novel identification strategy to estimate a large and positive impact of

monitoring on value. To the best of my knowledge, my paper is the first to test the predictions of a

traditional class of monitoring models (Townsend (1979), Gale and Hellwig (1985)), and among the

first to show that monitoring is valuable because it reduces managerial rent-seeking.4

Theoretical and emprical research shows that agency frictions are particularly severe in the context of

banking. The risk profile of bank assets is difficult to observe by outsiders and easy to modify by in-

siders (Morgan (2002), Dang, Gorton, Holmstrom, and Ordonez (2017)), and deposit insurance gives

bank lenders low incentives to monitor the management (Gorton and Pennacchi (1990)). Moreover,

deposit insurance and other bank regulations might distort shareholder incentives to take risk (Mer-

ton (1977)), possibly in contrast with managerial preferences (Saunders, Strock, and Travlos (1990)).

Previous empirical work has argued that agency frictions and managerial rent-seeking can have a

negative impact on bank value (Laeven and Levine (2007), Goetz, Laeven, and Levine (2013)). My

work provides causal evidence on the impact of agency frictions on bank value, and demonstrates

regulatory monitoring as an effective tool to mitigate these frictions.

The recent crisis has stimulated academic interest in the costs and benefits of financial regulation.

While many papers show that financial regulation is positively related to bank efficiency (Barth, Lin,

Ma, Seade, and Song (2013)), and negatively related to bank risk-taking and failure (Agarwal, Lucca,

Seru, and Trebbi (2014), Hirtle, Kovner, and Plosser (2016), Kandrac and Schlusche (2017)), a recent

4In this respect, my results are close to Bertrand and Mullainathan (2003), Kempf, Manconi, and Spalt (2016), andSchmidt and Fahlenbrach (2017), who focus on different outcome variables to show that monitoring reduces rent-seeking.Falato, Kadyrzhanova, and Lel (2014) show a positive impact of monitoring on firm value, but are silent about the specificmechanism through which monitoring increases value.

6 CHAPTER 1. THE VALUE OF REGULATORS AS MONITORS: EVIDENCE FROM BANKING

study by Buchak, Matvos, Piskorski, and Seru (2017) shows that bank regulatory burden is one of

the main reasons for the raise of shadow banking. My paper adds to this literature by providing the

first estimate of the value of monitoring by financial regulators.

1.2 Institutional Background and Motivating Theory

The banking industry provides an ideal laboratory to study the impact of regulatory monitoring on

shareholder value. A common view in the banking industry is that regulatory burden is particularly

detrimental to bank profitability and value, and financial regulation is a commonly-cited reason

for the decline of small banks in the United States. This view gained momentum among financial

authorities since the Dodd-Frank Act of 2010, and small bank regulatory burden reduction is now

an important priority on the policymaker’s agenda (Yellen (2016)). While the costs and benefits of

financial regulation are yet not fully understood, agency theory predicts that financial regulation can

have a positive impact on bank value by reducing shareholder monitoring costs.

1.2.1 Institutional Background

The Bank Holding Company Act of 1956 broadly defines a BHC as any company that owns and/or

has control over one or more banks. Commercial banks in the United States are not mandated to

be part of a BHC structure. However, being part part of a BHC offers substantial benefits, such as

increased flexibility in raising external financing and acquiring other banks, as well as the ability to

acquire non-bank subsidiaries. In practice, these benefits are such that at the end of 2016 around

eighty-four percent of commercial banks in the US were part of a BHC.5

The benefits of being part of a BHC come at the cost of compliance with the regulatory and supervis-

ory requirements imposed by the Fed. From a regulatory standpoint, Regulation Y from 1980 gives

the Fed exclusive jurisdiction in establishing BHC capital requirements, regulating BHC mergers

5https://www.fedpartnership.gov/bank-life-cycle/grow-shareholder-value/bank-holding-companies.

1.2. INSTITUTIONAL BACKGROUND AND MOTIVATING THEORY 7

and acquisitions, and defining and regulating non-banking activities performed by BHC subsidia-

ries. From a supervisory standpoint, Section 5 of the Bank Holding Company Act provides guidance

for the off-site and on-site inspections regularly conducted by regional Fed officials under delegated

authority from the Board.

The main information source for Fed off-site inspections is a set of financial statements collected

and reviewed by the Fed on a regular basis. In practice, specialized teams of Fed officials focus on

the analysis and cross-bank comparison of these statements to monitor the safety and soundness of

individual banks, and to identify potential threats to the financial system (Eisenbach, Haughwout,

Hirtle, Kovner, Lucca, and Plosser (2017)). The process through which the Fed collects financial sta-

tements is different for large and small BHCs. Large BHCs need to file every quarter consolidated

financial statements (form FR Y-9C) and holding parent company statements (FR Y-9LP) which con-

tain detailed balance sheet, income statement, and off-balance sheet information about the bank’s

activity. To avoid reporting burden, the Fed allows smaller BHCs to only file an annual statement

for the holding parent company (FR Y-9SP), such that small BHCs face substantially lower reporting

requirements than large BHCs.

The Fed separates small and large reporting BHCs based on a fixed, bank-independent asset size

threshold. From 1986 until the end of 2005, this size threshold was set to $150 million in total assets.

In March 2006, the Fed implemented a regulation increasing the threshold to $500 million (regulation

71-FR-11194), therefore providing new reporting exemptions to all BHCs with assets between $150

and $500 million. I use this change in reporting requirements as a shock to the monitoring costs of

deregulated banks’ shareholders.

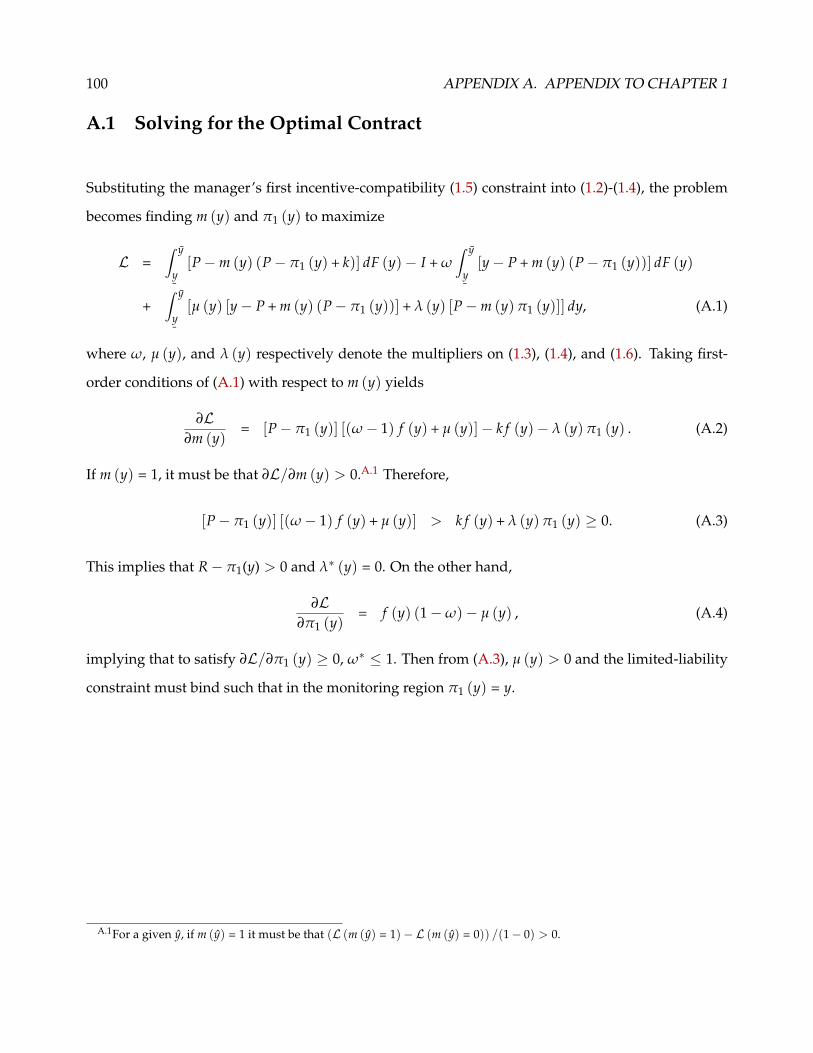

1.2.2 Predictions from Agency Theory

What kind of responses can be expected following a shock to shareholder monitoring costs? In this

section I use the lens of a classic model of monitoring (Townsend (1979)) to derive three key testable

predictions and provide structure to the empirical tests of the rest of the paper.

8 CHAPTER 1. THE VALUE OF REGULATORS AS MONITORS: EVIDENCE FROM BANKING

There are two agents in the model, a penniless manager and a shareholder with deep pockets. The

manager and the shareholder are both risk-neutral, and the risk-free rate is zero. The manager has

monopoly access to a project with cost I, which will generate a random cash flow y ∈[

¯y, y]⊆ R+

with cdf F and pdf f at the end of the period. The project has positive NPV, which I denote by Vf :

Vf =∫ y

¯y

ydF (y)− I > 0. (1.1)

The manager costlessly observes the realized project cash flow, and must report the cash flow to

shareholder. The manager can consume the difference between the realized cash flow and the cash

flow that she reports to the shareholder, and therefore has an incentive to under-report to the share-

holder. On the other hand, the shareholder can pay an audit cost k to perfectly observe the realized

cash flow.

The shareholder has full bargaining power, and her problem is to maximize her expected profits

while eliciting truthful cash flow revelation by the manager. Resorting to the revelation principle, I

characterize contracts in which the manager always reveals the true cash flow. A contract is then a

couple {π (y) , m (y)} that specifies payments from the manager to the shareholder π (y) :[

¯y, y]→

R and monitoring decisions m (y) :[

¯y, y]→ {0, 1} as functions of the cash flow reported by the

manager. I assume that audits are deterministic, in the sense that for all y, m (y) is either 0 or 1. This

partitions the set[

¯y, y]

in a region where the shareholders always audits the manager and a region

where the shareholder never audits the manager.

The shareholder maximizes her expected profits

∫ y

¯y[π (y)−m (y) k] dF (y)− I, (1.2)

subject to the manager’s participation constraint

∫ y

¯y[y− π (y)] dF (y) ≥ 0, (1.3)

the manager’s limited liability constraint that, for all y,

y ≥ π (y) , (1.4)

1.2. INSTITUTIONAL BACKGROUND AND MOTIVATING THEORY 9

and the incentive-compatibility constraints ensuring that the manager always reveals the true cash

flow. For the contract to be incentive-compatible, the following conditions must be verified. First, in

the non-monitoring region the shareholder must always receive a constant payment P.6 This allows

to write the payment π (y) as

π (y) = (1−m (y)) P + m (y)π1 (y) , (1.5)

where π1 (y) is the payment in the monitoring region. Second, to prevent the manager to report cash

flows in the non-monitoring region when the observed cash flow is in the monitoring region, it must

be that

m (y)π1 (y) ≤ P. (1.6)

Constraints (1.5) and (1.6) characterize incentive-compatibility by the manager. The shareholder’s

problem then becomes finding m (y) and π1 (y) to maximize her expected profits, subject to con-

straints (1.3)-(1.6).

In the appendix, I solve for the optimal contract. As in Gale and Hellwig (1985), the optimal contract

is such that the monitoring region is the low cash flow region for which π (y) = y < P, and the non-

monitoring region is the high cash flow region for which y ≥ π (y) = P. In the monitoring region, the

shareholder pays the monitoring cost k and the manager gives all the cash flow to the shareholder.

In the non-monitoring region, the shareholder receives the fixed payment P and the manager keeps

y− P.

Finally, conditional on the optimal contract, the optimal fixed payment P∗ is chosen by the sharehol-

der to solve the unconstrained maximization problem

maxP

∫ P

¯y

(y− k) dF (y) + P (1− F (P))− I. (1.7)

6If for some cash flow realization in the monitoring region the contract specifies a lower payment to the shareholderthan for other realizations in the monitoring region, there is an incentive for the manager to report the cash flow associatedwith the lower payment.

10 CHAPTER 1. THE VALUE OF REGULATORS AS MONITORS: EVIDENCE FROM BANKING

Taking the first-order conditions of this problem and re-arranging, I get

1− F (P∗) = k f (P∗) , (1.8)

showing that at the optimum, the shareholder balances the benefits of increasing P coming from

reduced managerial rents with the costs coming from increased monitoring.

The first testable prediction of the model therefore comes from inspection of Equation (1.8), by noting

that as the monitoring cost k becomes small, the probability F (P∗) that the shareholder monitors the

manager approaches one. In other words, when monitoring is inexpensive the shareholder always

monitors and extracts the entire NPV from the project.

Prediction 1. An increase in shareholder monitoring costs leads to shareholder value losses.

Next, let Vc denote shareholder value when monitoring is costly (i.e. k > 0):

Vc =∫ P∗

¯y

(y− k) dF (y) + P∗ (1− F (P∗))− I. (1.9)

The loss in shareholder value from a world where monitoring is costless and the shareholder extracts

the entire project NPV is then

Vf −Vc = kF (P∗) +∫ y

P∗(y− P∗) dF (y) , (1.10)

which consists of monitoring expenditures and managerial rents.

Prediction 2. When shareholder monitoring costs increase, losses in shareholder value are due to increased

monitoring expenditure and managerial rents.

The last model prediction requires assumptions on the distribution of bank cash flows. To provide

intuition, I assume that cash flows are uniformly distributed over the interval[

¯y, y]. The model

generates similar predictions for other types of distributions (e.g. lognormal). Using a uniform

distribution, some simple algebra shows that the shareholder value loss (1.10) becomes

Vf −Vc = k

(1− 1

2k

y−¯y

), (1.11)

1.3. EMPIRICAL SETTING 11

which is increasing in the term y −¯y. Noting that expected monitoring expenditure, kF (P∗), is

also increasing in y−¯y, and that y−

¯y is proportional to cash flow risk, the last prediction directly

follows.7

Prediction 3. When shareholder monitoring costs increase, shareholder value losses and monitoring expendi-

ture are increasing in cash flow risk.

Intuitively, when cash flow risk increases the likelihood of states where income is low or managerial

rents are high increases, and this reduces shareholder value relative to a world where monitoring is

costless and the manager cannot extract any rents. Over the next few sections I show that regulatory

monitoring reduces shareholder monitoring costs by testing the predictions of my stylized model in

the data.

1.3 Empirical Setting

In this section I describe how I measure bank value, monitoring expenditure, and cash flow risk

in the data, and describe how I use these variables to estimate the shareholder value of regulatory

monitoring.

1.3.1 Data Sources and Measurement

The data on BHC total consolidated assets comes from the Federal Reserve Regulatory Dataset. This

dataset is publicly available on the Federal Reserve of Chicago’s website, and contains information

directly coming from the FR Y-9C, FR Y-9LP, and FR Y-9SP reports. I use the dataset to categorize

BHCs into treated and control groups based on their 2005 average consolidated assets, and to keep

track of which BHCs file which forms in each quarter.8 Since the Fed policy allows treated banks to

stop reporting their FR Y-9C consolidated statements, I use Compustat Bank as my main source of

7The standard deviation of a uniform distribution with support [a, b] is given by (b− a) /√

12.8This is important because, as I show in Section 1.6, some BHCs voluntarily keep filing forms FR Y-9C and FR Y-9LP

even if their total assets are below $500 million after the treatment.

12 CHAPTER 1. THE VALUE OF REGULATORS AS MONITORS: EVIDENCE FROM BANKING

BHC consolidated financial data. I combine this dataset with CRSP to obtain end-of-quarter BHC

market-to-book values, and in turn merge the Compustat-CRSP combined dataset with the Federal

Reserve Regulatory Dataset using the link table available on the Federal Reserve of New York’s

website. Finally, I obtain data on analyst forecasts of bank profitability from I/B/E/S.

The observation frequency is quarterly, starting with the first quarter of 2004 and ending with the

last quarter of 2007. Within this time period, I construct my main sample as follows. I focus on top-

tier BHCs (defined as in Goetz, Laeven, and Levine (2016)) with average 2005 total assets between

$150 and $850 million, and with stock price data available on CRSP. I assign individual BHCs to the

treated group if their average total assets in 2005 are between $150 million and $500 million, and to

the control group if their average total assets in 2005 are between $500 million and $850 million.9

The final sample consists of 2,780 observations on 208 distinct BHCs, out of which 108 belong to the

treated group and 100 belong to the control group. These BHCs represent around ten percent of the

total number of BHCs in the US at the end of 2005, and around forty-six percent of the BHCs listed

on the stock market at the end of 2005. In terms of size, these banks represent around one percent of

the total assets in the banking sector at the end of 2005, and around five percent of the assets in the

bottom ninety-nine percent of the asset distribution. Finally, the average pre-treatment BHC asset

size in my sample is $519 million, right above the policy implementation threshold.

Table 1.1 reports summary statistics for my main measures of bank value, monitoring expenditure,

and cash flow risk, both in the full sample and in the treated and control sub-samples.10 The first

two rows of Panel A show summary statistics for my measures of bank shareholder value, Tobin’s

q and the Market-to-Book ratio of bank equity. The data shows little dispersion in these valuation

ratios, both within the main sample and across the treated and control sub-samples. The average

and median Tobin’s q in the main sample are 1.07 and 1.06, respectively, and the average and median

Market-to-Book are 1.75 and 1.65.

9I choose the upper bound of $850 million in total assets in such a way that the final treated and control samples containapproximately the same number of banks. In Section 3.2.2, I use $1 billion and $1.5 billion as alternative upper bounds,and show that the main results of the paper are not sensitive to these choices.

10Since I only observe evidence of managerial rents during the financial crisis, I leave a description of how I measurethese rents to Section 1.5.1.

1.3. EMPIRICAL SETTING 13

Table 1.1

Summary Statistics

This table reports summary statistics for the variables in the paper, both in the main sample and in the treatedand control sub-samples. In Panel A, Tobin’s q is the market value of total assets (market value of equityplus book value of debt) divided by the book value of total assets. Market-to-Book is the market value ofequity divided by the book value of equity. Professional Services are fees paid to management consultingfirms, investment banks, and auditing firms, in millions of US dollars. Cash flow risk is a quarterly averageof the absolute difference between monthly analyst consensus forecast of two-year-forward bank EPS and therealized EPS value corresponding to each consensus forecasts. In Panel B, leverage is total liabilities divided bytotal assets, Tier 1 Ratio is Tier 1 Capital divided by Risk-Weighted Assets, Profitability is net income dividedby net interest income, and ROE is net income divided by book value of equity. Total Assets are reported inmillions of US dollars. Finally, diversification is non-interest income divided by net interest income, and assetgrowth is quarterly growth in BHC total assets.

Panel A: Shareholder Value, Monitoring Expenditure, and Cash Flow Risk

Full Sample Treated Control

N Mean Med. SD N Mean Med. SD N Mean Med. SD

Tobin’s q 2,623 1.07 1.06 0.05 1,329 1.06 1.06 0.05 1,294 1.07 1.06 0.05Market-to-Book 2,623 1.75 1.65 0.57 1,329 1.71 1.60 0.57 1,294 1.80 1.72 0.56Professional Fees 1,756 0.14 0.10 0.16 862 0.13 0.10 0.14 894 0.16 0.12 0.18Cash Flow Risk 937 0.87 0.24 2.38 306 1.54 0.34 3.80 631 0.55 0.22 1.04

Panel B: Additional Variables

Full Sample Treated Control

N Mean Med. SD N Mean Med. SD N Mean Med. SD

Leverage 2,624 0.91 0.91 0.03 1,329 0.91 0.91 0.03 1,295 0.91 0.91 0.02Tier 1 Ratio 2,289 0.12 0.12 0.03 1,096 0.13 0.12 0.04 1,193 0.12 0.11 0.03Total Assets 2,703 554.9 535.6 232.5 1,341 386.5 382.8 128.5 1,362 720.6 696.8 188.8Profitability 2,701 0.23 0.26 0.34 1,340 0.20 0.24 0.44 1,361 0.25 0.27 0.19ROE 2,624 0.02 0.03 0.03 1,329 0.02 0.02 0.03 1,295 0.03 0.03 0.02Diversification 2,701 0.27 0.22 0.24 1,340 0.26 0.20 0.29 1,361 0.27 0.24 0.18Asset Growth 2,655 0.03 0.02 0.06 1,308 0.03 0.02 0.06 1,347 0.03 0.02 0.05

14 CHAPTER 1. THE VALUE OF REGULATORS AS MONITORS: EVIDENCE FROM BANKING

The third row of Panel A shows summary statistics for bank professional expenditures, in millions

of US dollars. These expenditures are recorded as a separate item on bank income statements, and

include fees paid to consultants, auditors, and investment bankers. In Section 1.5.1, I show that

professional expenditures are a good proxy for shareholder monitoring in my sample, because they

are mostly related to the implementation of internal controls. Banks in the treated group pay slightly

lower professional fees than banks in the control group. On average, treated banks spend 0.13 million

of dollars per quarter in professional services, with a standard deviation of 0.14 million. Control

banks spend on average 0.16 million of dollars per quarter in professional services, with a standard

deviation of 0.18 million.

The last row of Panel A finally presents my primary cash flow risk measure, the absolute difference

between analyst consensus forecast of two-year-forward bank EPS and the realized EPS value corre-

sponding to each consensus forecast. By construction, this variable provides a time-varying measure

of analyst uncertainty about future bank profitability, and therefore represents a close approximation

to the risk of unobservable cash flows in my model. The table shows that cash flow risk is on average

higher for treated banks than for control banks, partially reflecting lower analyst coverage of small

banks. Both before and after the treatment, the average treated bank is covered by approximately

four analysts analysts in a given quarter, while the average control bank is covered by six analysts.

Panel B of Table 1.1 reports summary statistics for the other key variables in the paper, which I

borrow from the literature as potential determinants of cross-sectional heterogeneity in bank value

(Laeven and Levine (2007), Minton, Stulz, and Taboada (2017)). These variables include leverage

(total liabilities minus noncontrolling interest divided by total assets), the regulatory Tier 1 Regula-

tory Capital Ratio (henceforth Tier 1 Ratio, the bank self-reported ratio of Tier 1 Capital divided by

Risk-Weighted Assets), total assets, profitability (net income divided by net interest income), Return

on Equity (ROE, net income divided by book value of equity), diversification (noninterest income

divided by net interest income), and quarterly asset growth. As in Panel A, the data reveals little

differences in these variables across treated and control groups, thus confirming the comparability

of these two sets of banks.

1.3. EMPIRICAL SETTING 15

1.3.2 Estimation Strategy and Identification

In this section, I describe my strategy to test the model predictions in the data and to measure the

shareholder value of regulatory monitoring. I exploit the change in regulatory reporting require-

ment to the Fed as a quasi-natural source of variation in shareholder monitoring costs. My empiri-

cal strategy consists in comparing the value and monitoring expenditure of smaller, treated banks

with pre-treatment total assets just below $500 million with the value of larger, control banks with

pre-treatment total assets just above $500 million, before and after the treatment. More precisely, I

estimate the model

Yit = β0 + β1 (Postt × Treatedi) + β2Xit + γi + δt + εit, (1.12)

where Yit is an outcome variable (e.g. Tobin’s q) for BHC i in quarter t, Postt is an indicator equal

to one if quarter t follows the last quarter of 2005 and zero otherwise, Treatedi is an indicator equal

to one if the average assets of BHC i during 2005 are just below $500 million, Xit is a matrix of time-

varying control variables (such as assets and profitability), γi is a time-invariant and BHC-specific

fixed effect, δt is a BHC-invariant and time-specific fixed effect, and εit is a normally-distributed error

term. The coefficient of interest is β1, my estimate of the value difference between treated and control

banks before and after the treatment.

My empirical strategy relies on the key identification assumption of quasi-random assignment of

treated and control banks around the threshold before the Fed changes the reporting requirements of

treated banks, such that any systematic value difference after the policy implementation is arguably

only due to differences in regulatory monitoring. In practice, this assumption can be violated for

two reasons. First, the assumption is violated if the threshold change results from lobbying, making

the treatment an endogenous outcome. Second, the assumption is violated if, even in absence of

lobbying, banks engage in size manipulation around the new threshold before its implementation.

Although the institutional details of the policy suggest that lobbying was unlikely, whether the po-

licy was unanticipated by bank shareholders is ultimately an empirical question.11 In Figure 1.1 I11The first proposal for public comment on the policy dates to November 2005, and the policy was quickly implemented

at the beginning of March 2006 without modifications to the initial proposal.

16 CHAPTER 1. THE VALUE OF REGULATORS AS MONITORS: EVIDENCE FROM BANKING

report a diagnostic test aimed at detecting pre-existing differences in the average valuation of tre-

ated and control banks before the treatment. Panels A and B report these diagnostics for Tobin’s

q and Market-to-Book, respectively, and are constructed as follows. I first divide the sample into

two sub-samples, the pre-treatment sample before the first quarter of 2006 and the post-treatment

sample starting with the first quarter of 2006. In each of these sub-samples, I run a kernel-weighted

local polynomial regression to obtain a smoothed estimate of the trend component of treated and

control banks’ valuation. In Figure 1.1 I then plot these estimated trend components and their as-

sociated confidence intervals as functions of the observation quarter, both in the pre- and in the

post-treatment periods.12 Figure 1.1 shows that the trend components of treated and control banks’

valuation are statistically indistinguishable from each other in the pre-treatment period, supporting

the claim that the threshold change was unanticipated. Moreover, the figure shows an increase in

the difference between treated and control banks’ average valuation after the treatment, providing a

visual preview of the results in the next section.

In Figure 1.2, I report the results of a McCrary (2008) discontinuity test to reduce concerns of bank

size manipulation around the $500 million threshold. Specifically, I construct a finely-gridded his-

togram of bank total assets, which I then smooth on each size of the threshold using local linear

regression. In Figure 1.2, I then report point estimates and 95% confidence intervals of smoothed as-

set densities during the 2005-2007 period (Panel A) and during the four quarters immediately before

the treatment (Panel B). Both before and after the treatment, the estimated asset density below the

threshold is not statistically different from the estimated asset density above the threshold.13 Impor-

tantly, a specific institutional feature of the policy reduces residual concerns of asset manipulation

before the treatment. The policy states that individual BHCs qualify for reporting exemptions only

if their June 2005 consolidated assets are below $500 million. At the same time, the Fed first publicly

announces the threshold change in November 2005, preventing pre-treatment size manipulation.

12I divide the sample to avoid post-treatment observations entering the estimation of the pre-treatment trend, andvice-versa. All panels of Figure 1.1 are constructed using an Epanechnikov kernel and the rule-of-thumb bandwidth sizesuggested in Fan and Gijbels (1996). Different kernel and bandwidth choices generate similar results.

13All the results are calculated using the histogram bin size and local linear regression bandwidth suggested in McCrary(2008).

1.3. EMPIRICAL SETTING 17

Figure 1.1

Common Trends in Pre-Policy Bank Valuation

This figure reports a parallel trends diagnostic test on treated and control banks’ Tobin’s q (Panel A) andMarket-to-Book (Panel B). I first divide the sample into two sub-samples, the pre-treatment sample before thefirst quarter of 2006 and the post-treatment sample starting with the first quarter of 2006. In each of thesesub-samples, I run a kernel-weighted local polynomial regression to obtain a smoothed estimate of the trendcomponent of valuation. The local polynomial regression uses an Epanechnikov kernel and the rule-of-thumbbandwidth suggested in Fan and Gijbels (1996). The figure reports point estimates and 95% confidence in-tervals of the trend component of treated and control banks’ valuation as functions of the estimation quarter.Tobin’s q and Market-to Book are defined as in Table 1.1.

1.02

1.04

1.06

1.08

1.1

Policy Change

2004q1 2005q1 2006q1 2007q1 2008q1

Control 95% C.I.Treated 95% C.I.

Panel A: Tobin's q

1.2

1.4

1.6

1.8

2

Policy Change

2004q1 2005q1 2006q1 2007q1 2008q1

Control 95% C.I.Treated 95% C.I.

Panel B: Market-to-Book Ratio

18 CHAPTER 1. THE VALUE OF REGULATORS AS MONITORS: EVIDENCE FROM BANKING

Figure 1.2

Bank Size Manipulation

This figure shows point estimates and 95% confidence intervals of the smoothed cross-sectional density ofbank total assets during the 2005-2007 period (Panel A) and during the four quarters preceding the Policy(Panel B). The goal of the figure is to detect discontinuities indicative of size manipulation around the Policythreshold. The smoothed densities are obtained by first constructing finely-gridded histograms of the cross-section of bank total assets, and by then smoothing the histograms on each size of the threshold using locallinear regression. The optimal histogram bin size and local linear regression bandwidth are calculated usingthe procedure in McCrary (2008).

0.0

005

.001

.001

5.0

02.0

025

Policy Threshold

0 500 1000 1500 2000Total Assets (USD Millions)

Panel A: 2005-2007 BHC Asset Density

0.0

005

.001

.001

5.0

02.0

025

Policy Threshold

0 500 1000 1500Total Assets (USD Millions)

Panel B: 2005 BHC Asset Density

1.4 The Value of Regulatory Monitoring

In this section I present my main results on the value impact of regulatory monitoring.

1.4.1 Main Results

Table 1.2 shows my main findings on the value impact of regulatory monitoring. The table reports

point estimates for the coefficients in Equation (1.12), along with their standard errors (clustered at

the BHC-level). The main coefficient of interest is associated with the “Post × Treated” term, which

represents an estimate of the percentage change in Tobin’s q and Market-to-Book due to the change

in reporting requirements.

When I estimate Equation (1.12) only including quarter- and BHC-level fixed effects, the policy treat-

ment leads to a one percent decline in treated bank Tobin’s q, relative to control banks. The economic

1.4. THE VALUE OF REGULATORY MONITORING 19

Table 1.2

The Policy Effect on Bank Shareholder Value

This table reports estimates of the treatment effect on bank valuation using the empirical specification in Equa-tion (1.12). The coefficient associated with the “Post × Treated” interaction term captures the percentagechange in treated bank valuation due to the treatment. The table includes year-quarter Fixed Effects (FE)and BHC FE. All the variables are defined as in Table 1.1.

log Tobin’s q log Market-to-Book

(1) (2) (3) (4) (5) (6)

Post × Treated -0.010*** -0.011*** -0.010*** -0.069*** -0.079*** -0.074***(0.00) (0.00) (0.00) (0.03) (0.02) (0.02)

Leverage 0.318*** 0.253** 5.473*** 5.170***(0.12) (0.10) (0.81) (0.68)

Tier 1 Ratio 0.376*** 0.280*** 2.539*** 1.746***(0.08) (0.07) (0.51) (0.48)

log Assets -0.032*** -0.234***(0.01) (0.05)

Profitability -0.004 0.041(0.00) (0.04)

ROE 0.091** 0.292(0.04) (0.47)

Diversification -0.004 -0.054(0.00) (0.04)

Asset Growth -0.006 -0.021(0.01) (0.07)

Year-Quarter FE Yes Yes Yes Yes Yes YesBHC FE Yes Yes Yes Yes Yes YesR-Squared 0.360 0.393 0.418 0.413 0.470 0.503Observations 2,177 2,177 2,177 2,177 2,177 2,177

Note: Standard errors (in parentheses) are clustered at the BHC-level. ***, **, and * respectively denote sta-tistical significance at the 1%, 5%, and 10% levels.

20 CHAPTER 1. THE VALUE OF REGULATORS AS MONITORS: EVIDENCE FROM BANKING

magnitude and statistical significance of the treatment effect are not affected by the inclusion of le-

verage and Tier 1 Ratio, reducing concerns that the effect might be due to contemporaneous changes

in small bank capital requirements (see Section 1.6). Everything else equal, a ten percent increase in

leverage and Tier 1 Ratio are respectively associated to a 3.2 and 3.8 percent increase in Tobin’s q, but

the treatment still induces a 1.1 percent decrease in Tobin’s q after the inclusion of these variables.

Finally, the results are robust to the inclusion of size, profitability, diversification, and asset growth

as additional controls.

In the last three specifications of the table, I repeat the same exercise using Market-to-Book as de-

pendent variable. The table shows that the treatment induces a 6.9 percent loss in Market-to-Book

for treated banks, and this value loss is as high as 7.9 percent when I add time-varying controls to

the specification. To put these numbers in perspective, a seven percent relative decrease in Market-

to-Book corresponds to a $4 million relative decrease in market capitalization for the average treated

bank, implying an aggregate market capitalization loss of approximately $430 million. Finally, a

comparison of the first three and the last three columns of Table 1.2 shows that the treatment effect

on Tobin’s q is almost one order of magnitude smaller than the treatment effect on Market-to-Book.

This is due to leverage, which reduces the impact of equity fluctuations on the market value of bank

assets.14 Overall, the results of the table are consistent with the prediction that increased monitoring

costs reduce bank shareholder value.

14A simple example can illustrate this point. Respectively define by Et, Dt and Mt the book value of equity, the bookvalue of debt and the market value of equity in quarter t. Suppose that Et and Dt do not change between quarter t andquarter t + 1 (i.e. Et = Et+1 ≡ E and Dt = Dt+1 ≡ D), but Mt changes to Mt+1. Let ∆Mt+1 ≡ Mt+1 −Mt. Finally, let mbt andqt respectively define the Market-to-Book ratio and Tobin’s q at time t. The change in Market-to-Book between time t andt + 1 is given by

∆mbt+1 =Mt+1Et+1

− MtEt

=∆Mt+1

E. (1.13)

Then, changes in Tobin’s q can be expressed as a function of changes in Market-to-Book and bank leverage:

∆qt+1 =Mt+1 + Dt+1Et+1 + Dt+1

− Mt + DtEt + Dt

=∆Mt+1E + D

=(

1− DE + D

)∆mbt+1, (1.14)

where the term in parentheses in (1.14) is on average equal to 9% in my sample.

1.4. THE VALUE OF REGULATORY MONITORING 21

1.4.2 Robustness, Placebo, and Falsification Tests

Table 1.3 reports two sets of tests aimed at reducing sample selection concerns. In the interest of

space, I only present results for Tobin’s q, leaving the results for Market-to-Book to the appendix.

In Panel A, I test the impact of different sample bandwidth restrictions on my main result. In the

first four specifications of the table, I use two small samples of BHCs with average 2005 total assets

between $400 and $600 million, and between $300 and $700 million. In the last four specifications,

I conversely use two large samples of BHCs with total assets between $150 million and $1 billion,

and between $150 million and $1.5 billion. To mitigate the impact of confounding factors at the onset

of the financial crisis as the sample size changes, the results in Table 1.3 only include data for 2005

and 2006. The table shows that the main results of the paper are not sensitive to different sample

bandwidth choices. Moreover, the first four specifications—which measure the treatment effect on

banks closest to the threshold—show that the treatment leads to an average 1.2 percent discount in

Tobin’s q, slightly larger than the effect found in Table 1.2.

In Panel B I conversely show that the statistical and economic magnitude of my results disappear

when I separate treated and control banks using arbitrary treatment thresholds and quarters. The

first six specifications show that the results disappear when I use asset thresholds of $300 million,

$750 million and $1 billion to separate treated and control banks. Similarly, Specifications (7) and (8)

show that the results disappear when I use the last quarter of 2004 as treatment quarter, and the last

two specifications show that the results disappear when I use the last quarter of 2006 as treatment

quarter.

In the appendix, I provide additional robustness tests. First, I run an event study to show that the

observed drop in Tobin’s q and Market-to-Book are driven by a drop in the market value of treated

banks as opposed to an increase in their book value or an increase in the market value of control

banks. Second, I apply different restrictions on my sample to include the financial crisis, exclude

banks that drop out of the sample, and exclude banks that are not listed on the stock market before

the policy. Again, my results are robust to these restrictions. Third, I show that the treatment effect

on bank value is roughly uniform at the peak of the business cycle in 2006 and at the beginning of

22 CHAPTER 1. THE VALUE OF REGULATORS AS MONITORS: EVIDENCE FROM BANKING

Table 1.3

Robustness and Placebo Tests: Tobin’s q

This table reports sample bandwidth selection tests (Panel A) and placebo tests (Panel B) on my main Tobin’s qresult. In the first four specifications of Panel A, I use two small samples of BHCs with average 2005 total assetsbetween $400 and $600 million (Specifications (1) and (2)), and between $300 and $700 million (Specifications(3) and (4)). In the last four specifications, I use two large samples of BHCs with total assets between $150 mil-lion and $1 billion (Specifications (5) and (6)), and between $150 million and $1.5 billion (Specifications (7) and(8)). In the first six specifications of Panel B, I use asset thresholds of $300 million, $750 million and $1 billionto separate treated and control BHCs. In Specifications (7) and (8) I use the last quarter of 2004 as treatmentquarter, dropping post-2005 observations from the sample. In the last two specifications, I use the last quarterof 2006 as treatment quarter. The dependent variable in all specifications is the natural logarithm of Tobin’s q.Unreported control variables include leverage, Tier 1 Ratio, total assets, profitability, ROE, diversification, andasset growth.

Panel A: Sample Bandwidth Selection

$400M-600M $300M-700M $150M-1B $150M-1.5B

(1) (2) (3) (4) (5) (6) (7) (8)

Post × Treated -0.012** -0.012** -0.011** -0.012*** -0.010*** -0.012*** -0.011*** -0.012***(0.01) (0.01) (0.00) (0.00) (0.00) (0.00) (0.00) (0.00)

Controls No Yes No Yes No Yes No Yes

Year-Quarter FE Yes Yes Yes Yes Yes Yes Yes YesBHC FE Yes Yes Yes Yes Yes Yes Yes YesR-Squared 0.117 0.169 0.087 0.131 0.058 0.105 0.046 0.089Observations 355 355 724 724 1,313 1,313 1,611 1,611

Panel B: Placebo Tests

$300M Threshold $750M Threshold $1B Threshold After 12/2004 After 12/2006

(1) (2) (3) (4) (5) (6) (7) (8) (9) (10)

Post × Treated -0.00 -0.00 0.00 -0.00 0.00 0.00 0.00 -0.00 -0.00 -0.00(0.01) (0.01) (0.00) (0.00) (0.00) (0.00) (0.00) (0.00) (0.00) (0.00)

Controls No Yes No Yes No Yes No Yes No Yes

Year-Quarter FE Yes Yes Yes Yes Yes Yes Yes Yes Yes YesBHC FE Yes Yes Yes Yes Yes Yes Yes Yes Yes YesR-Squared 0.385 0.459 0.339 0.403 0.360 0.422 0.054 0.146 0.351 0.408Observations 1,056 1,056 1,509 1,509 2,076 2,076 1,028 1,028 2,177 2,177

Note: Standard errors (in parentheses) are clustered at the BHC-level. ***, **, and * respectively denote sta-tistical significance at the 1%, 5%, and 10% levels.

1.5. HOW DOES REGULATORY MONITORING BENEFIT SHAREHOLDERS? 23

the financial crisis in 2007, supporting the validity of my results outside the specific environment of

early 2006. Fourth, using Compustat data I construct two falsification samples of non-financial firms

and non-BHC financial firms (e.g. insurance companies and banks that are not BHCs), and study

whether the valuation of firms with 2005 average total assets just below $500 million changes after

the treatment date, relative to the valuation of firms with total assets just above $500 million. The

results show no evidence of value changes in these falsification samples, confirming that the Fed

threshold change, as opposed to other size-based regulations, drives the drop in treated bank value.

1.5 How does Regulatory Monitoring Benefit Shareholders?

In this section I provide additional evidence for my proposed mechanism by testing the remainng

model predictions, namely that reduced regulatory monitoring increases shareholder monitoring

expenditure and managerial rents, and that bank value losses and monitoring expenditure are po-

sitvely correlated with cash flow risk. Moreover, I show that increased shareholder monitoring costs

increase shareholder incentives to free-ride on each other’s monitoring.

1.5.1 Bank Value, Monitoring Expenditure, and Managerial Rents

The second prediction of the costly state verification model is that the observed losses in treated

bank value should be due to increased shareholder monitoring expenditure and managerial rents.

Table 1.4, provides a first test of this prediction by showing that the policy results in a twenty-five

percent increase in treated bank professional expenditure. This relative professional expenditure in-

crease is economically large for treated banks, amounting to approximately twenty-seven thousand

dollars per quarter or 3.8 percent of the average treated bank’s pre-treatment quarterly net income.

Consistent with the model’s predictions, when I discount these increased professional expenditures

(after-taxes) at an average quarterly ROE of two percent, their discounted present value amounts

to slightly less than a million dollars, around twenty-five percent of the four million relative drop

in market value experienced by the average treated bank. In other words, increased monitoring

expenditures only account for a fraction of the loss in treated bank market value.

24 CHAPTER 1. THE VALUE OF REGULATORS AS MONITORS: EVIDENCE FROM BANKING

Table 1.4

The Policy Effect on Bank Professional Expenditure

This table shows the treatment effect on treated banks’ professional expenditure. In the first three specificationsI use the natural logarithm of professional fees as dependent variable, while in the last three specifications Iuse the natural logarithm of professional fees normalized by net interest income. Additional control variablesnot reported in the table include total assets, profitability, ROE, diversification, and asset growth.

log Professional Fees log Professional FeesNet Interest Income

(1) (2) (3) (4) (5) (6)

Post × Treated 0.259*** 0.267*** 0.244*** 0.225** 0.224** 0.232***(0.09) (0.09) (0.07) (0.09) (0.09) (0.08)

Leverage -2.080 -1.640 2.051 0.885(3.22) (2.49) (3.08) (2.53)

Tier 1 Ratio -4.471*** -2.173 -1.436 -1.290(1.51) (1.34) (1.46) (1.35)

Other Controls No No Yes No No Yes

Year-Quarter FE Yes Yes Yes Yes Yes YesBHC FE Yes Yes Yes Yes Yes YesR-Squared 0.076 0.101 0.182 0.047 0.062 0.129Observations 999 999 999 999 999 999

Note: Standard errors (in parentheses) are clustered at the BHC-level. ***, **, and * respectively denote sta-tistical significance at the 1%, 5%, and 10% levels.

1.5. HOW DOES REGULATORY MONITORING BENEFIT SHAREHOLDERS? 25

Next, in Table 1.5, I show that the post-treatment losses in market value are strongly correlated

with professional expenditures. In practice, I augment the main specification of Table 1.2 with an

interaction term for professional expenditures incurred by treated banks only after the treatment,

capturing the post-treatment correlation between treated bank professional expenditure and value.

In most specifications, I include time-varying risk controls such as Z-Score, equity return volatility,

and a tail risk measure borrowed from Ellul and Yerramilli (2013). The table shows that the statistical

significance of the treatment effect is entirely captured by post-treatment professional expenditures

by treated banks. While the magnitude of this triple-differences estimate has no clear economic inter-

pretation, its significance suggests a strong positive correlation between post-treatment professional

expenditure and losses in shareholder value. Moreover, in the appendix I show that this correlation

does not seem to be mechanically driven by changes in profitability, size, or risk variables that are

potentially correlated with both professional expenditure and value.

Finally, a more in-depth analysis reveals that post-treatment professional expenditure growth for tre-

ated banks is mainly related to increased management monitoring, as opposed to other professional

services such as auditing and investment banking. In the appendix, I show that fees paid to consul-

tants experience a much larger increase after the treatment than fees paid to auditors (from annual

AuditAnalytics). Moreover, when I divide treated banks based on whether their post-treatment 10-K

notes cite internal controls consulting as a component of professional expenditure, the increase in

professional expenditure is larger for treated banks that cite internal controls as a significant source

of expenditure.15

Managerial Rents

In this section I provide empirical support for the hypothesis that reduced monitoring costs increase

managerial rents, where I measure managerial rents by earnings smoothing (Fudenberg and Tirole

(1995)). Specifically, I use the August 2007 rise in money market interest rates as a shock to the

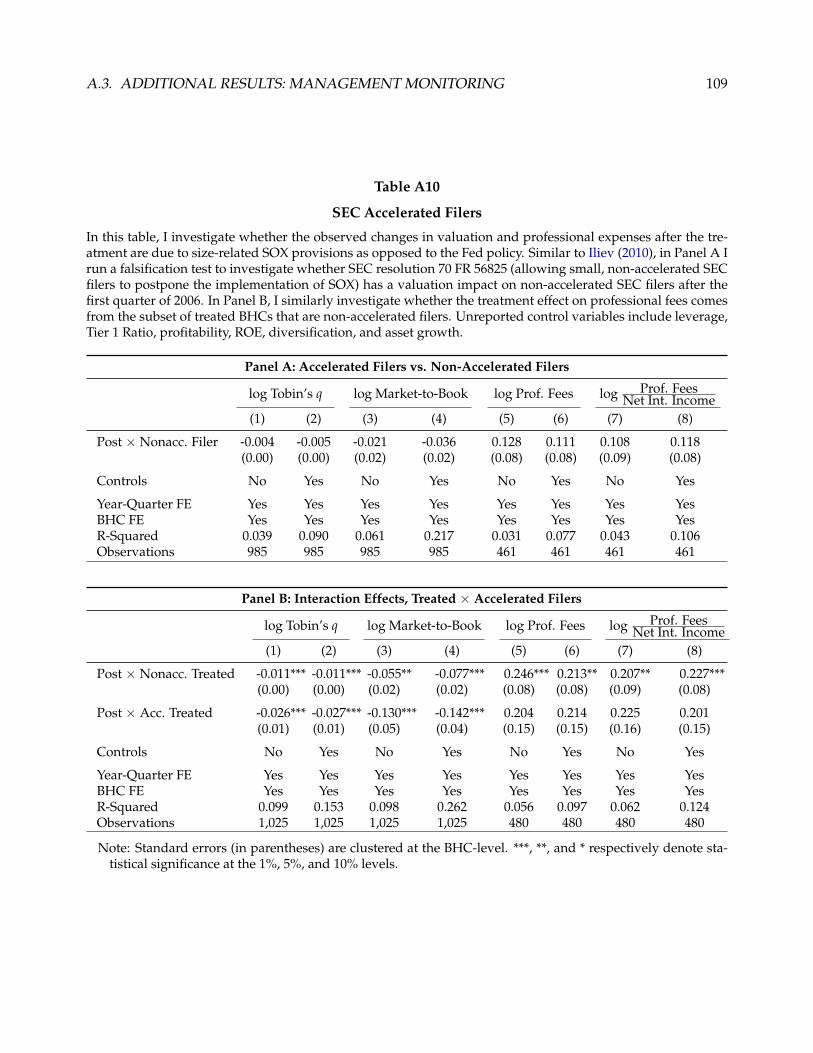

15In many banks, internal controls expenditures are related to Sarbanes-Oaxley (SOX). In the appendix, I show that theobserved decline in treated banks’ valuation is however not due to interactions between the policy and size-related SOXprovisions (see, for example, Iliev (2010)).

26 CHAPTER 1. THE VALUE OF REGULATORS AS MONITORS: EVIDENCE FROM BANKING

Table 1.5

Professional Expenditure Growth and Post-Treatment Value Losses

In this table I study the interaction between post-treatment professional expenditure growth and post-treatment bank value losses. In the table, the term “Post × Treated × Prof. Fees” captures treated banks’professional expenditures that only occur after the treatment. Z-Score is computed as the moving average ofbank capital-asset ratio (book value of equity divided by book value of assets), plus the moving average ofROA, divided by the moving standard deviation of ROA. Moving averages are calculated over a horizon ofthree quarters. Equity Volatility is the quarterly standard deviation of daily equity returns. Tail risk is thenegative of the average return over the 5% worst return days that a bank’s stock experiences in a given quar-ter (Ellul and Yerramilli (2013)). Professional fees are normalized by net interest income. Unreported controlvariables include total assets, leverage, profitability, ROE, diversification, and asset growth.

log Tobin’s q log Market-to-Book

(1) (2) (3) (4) (5) (6)

Post × Treated -0.001 -0.001 -0.000 0.003 -0.000 0.004(0.01) (0.01) (0.01) (0.04) (0.03) (0.03)

Prof. Fees -0.037 -0.067 -0.075* -0.103 -0.244 -0.437(0.05) (0.04) (0.04) (0.52) (0.45) (0.36)

Post × Treated × Prof. Fees -0.139*** -0.105** -0.124** -1.447*** -1.196*** -1.188***(0.05) (0.05) (0.06) (0.54) (0.43) (0.39)

Z-Score 0.000 0.000 0.000 0.000(0.00) (0.00) (0.00) (0.00)

Equity Volatility 1.681*** 1.681*** 11.419*** 10.430***(0.29) (0.25) (1.41) (1.55)

Tail Risk -0.813*** -0.789*** -6.008*** -5.713***(0.11) (0.10) (0.63) (0.54)

Other Controls No No Yes No No Yes

Year-Quarter FE Yes Yes Yes Yes Yes YesBHC FE Yes Yes Yes Yes Yes YesR-Squared 0.290 0.336 0.376 0.368 0.417 0.485Observations 1,641 1,641 1,641 1,641 1,641 1,641

Note: Standard errors (in parentheses) are clustered at the BHC-level. ***, **, and * respectively denote sta-tistical significance at the 1%, 5%, and 10% levels.

1.5. HOW DOES REGULATORY MONITORING BENEFIT SHAREHOLDERS? 27

funding costs of BHCs with total assets around $500 million, and analyze the impact of this negative

shock on managerial earnings smoothing right above and right below the threshold. Since money

market interest rates are determined in the interbank lending market of large banks, non-systemic

banks with assets around $500 million arguably play a negligible role in determining this funding

shock. Any observed difference in funding costs and earnings smoothing of banks right above and

below the threshold should therefore only arise from the different exposure of these banks to Fed

monitoring.

To test whether the 2007 shock has a different impact on banks with assets right above and right

below the threshold, I construct two new groups of treated and control BHCs. The new group of

treated, “unmonitored” BHCs consists of BHCs with less than $500 million in assets during the 2006-

2008 period. The new group of control, “monitored” BHCs consists of BHCs with more than $500

million in assets during the same period. To avoid potential bias due to the change in the definition

of small BHCs, I drop observations before the first quarter of 2006. Moreover, I drop BHCs with

total assets above $700 million such that systemic banks are excluded from the sample and such that

the unmonitored and monitored groups have roughly the same number of banks (sixty-seven and

fifty-seven, respectively). My results are not sensitive to this sample bandwidth choice.

In Table 1.6 I report my main results on the impact of Fed supervision on funding costs, profitability,

and earnings smoothing during the crisis.16 Panel A shows the impact of Fed supervision on the

funding costs and profitability of unmonitored banks relative to monitored banks. In the first two

specifications of Panel A, I use total interest expense divided by total loans as a measure of BHC

funding costs. The table shows that during the crisis the difference between the cost of funding of

unmonitored and monitored banks increases by 5.3 percent relative to the pre-crisis period, and that

this effect is robust to the inclusion of lagged Tobin’s q, leverage, Tier 1 Ratio, total assets, diver-

sification and asset growth as regression covariates. The next specifications show that this relative

increase in unmonitored bank funding costs is however not associated with an increase in interest

revenue (interest income divided by total loans), and only by a marginally significant decrease in

16Summary statistics for the dependent variables used in this section are reported in the appendix.

28 CHAPTER 1. THE VALUE OF REGULATORS AS MONITORS: EVIDENCE FROM BANKING

ROE. As a result, unmonitored banks’ higher funding costs must be followed by higher noninterest

revenue, lower noninterest expense, or both.

In the first two specifications of Panel B, I show that unmonitored bank Loan Loss Provisions—a

component of noninterest expense—indeed experience a large decline during the financial crisis.

While the results of the baseline Specification (1) are not statistically significant, the second specifica-

tion of Panel B shows that during the crisis unmonitored bank LLPs decrease by fifty-three percent

relative to monitored bank LLPs after controlling for size, profitability, and other sources of bank

heterogeneity. The observed decline is not due to bank size or performance, and is therefore consis-

tent with the hypothesis of earnings smoothing (as previously documented by Huizinga and Laeven

(2012)). In the last four specifications of Panel B, I confirm this hypothesis by showing a relative in-