essential learning for ctp candidates ny cash …c.ymcdn.com/sites/ learning for ctp candidates ny...

TRANSCRIPT

1

Essential Learning for CTP CandidatesNY Cash Exchange 2017 – Session #CTP-10

Copyright © 2017 – The Treasury Academy, Inc.All Rights Reserved

NY Cash Exchange – 2017: CTP TrackAdvanced CTP MathSession #10 (Fri. (6/02) 10:15 am – Noon)

Advanced CTP Math: ETM5 Calculations– Part Two

What to Do WhenPanic Sets In

© 2017 - The Treasury Academy, Inc. - All Rights Reserved 1

Essentials of Treasury Management, 5th Ed. (ETM5) is published by the AFP which holds the copyright and all rights to the related materials.

As a prep course for the CTP exam, significant portions of these lectures are based on materials from the Essentials text.

ETM5: Calculations

These slides cover most of the advanced calculations in ETM5 –Examples include both those from the text and additional problems

2© 2017 - The Treasury Academy, Inc. - All Rights Reserved

Due to time constraints, we will NOT be able to cover all of the examples in this session. Students are encouraged to spend some time on their own reviewing these problems at a later date.

ETM5: Chapters 12 & 14 CalcsCash Management & Forecasting

Breakeven Concentration CostReceipts & Disbursements ForecastDistribution ForecastPro-forma Financial StatementsMoving AverageExponential Smoothing

3© 2017 - The Treasury Academy, Inc. - All Rights Reserved

2

Essential Learning for CTP CandidatesNY Cash Exchange 2017 – Session #CTP-10

Copyright © 2017 – The Treasury Academy, Inc.All Rights Reserved

More on Concentration Systems Two frequently used concentration systems in

U.S.◦ EDT: Electronic Depository Transfer◦ Wire Transfer

Assume the following:◦ ACH Cost = $1.00; Wire Cost = $10.00◦ Opp Cost = 3.5%; 1-day speed-up with wire

© 2017 - The Treasury Academy, Inc. - All Rights Reserved 4

Wire Cost ACH CostMin. Transfer =

Opportunity CostDays Accelerated

365 Days

$10.00 $1.00 $9.00= = $93,858

1 .000095890.0351 Day

365 Days

Source: ETM5 - © AFP

Receipts and Disbursements Forecast

© 2017 - The Treasury Academy, Inc. - All Rights Reserved 5

$ Amounts in $1,000 Week 1 Week 2 Week 3

Cash Receipts $1,000 $1,000 $950

Cash Disbursements (870) (1,350) (1,000)

Net Cash Flow 130 (350) (50)

Beginning Cash Balance 100 230 (120)

Ending Cash Balance 230 (120) (170)

Minimum Cash Required(Target Balance)

(50) (50) (50)

Financing Needed(Negative = Deficit)

$170 $220

Investable Funds(Positive = Surplus)

$180

Source: ETM5 - © AFP

Distribution Method ForecastExampleA company has used regression analysis to estimate the proportion of dollars that will clear on a given business day. It has determined that this proportion depends on the number of business days since the checks were distributed. The estimated proportions are given below.

Business Days Since Distribution

Percentage of $ Expected to Clear

1 13%

2 38%

3 28%

4 13%

5 8%

Total 100%

6© 2017 - The Treasury Academy, Inc. - All Rights ReservedSource: ETM5 - © AFP

3

Essential Learning for CTP CandidatesNY Cash Exchange 2017 – Session #CTP-10

Copyright © 2017 – The Treasury Academy, Inc.All Rights Reserved

Distribution Method ForecastTherefore, if $100,000 in checks are distributed on Wednesday, May 1,

the checks are estimated to clear according to the schedule below.

DateBusiness Days

After Distribution

Day of the Week

% of Dollars

Clearing

Forecast Dollars

Clearing

May 2 1 Thur. 13% $ 13,000

May 3 2 Fri. 38% $ 38,000

May 6 3 Mon. 28% $ 28,000

May 7 4 Tues. 13% $ 13,000

May 8 5 Wed. 8% $ 8,000

Total 100% $ 100,000

7© 2017 - The Treasury Academy, Inc. - All Rights Reserved

Source: ETM5 - © AFP

Pro-Forma Financial Statements

Medium and long-term forecasting

Percentage-of-sales method

Involves projecting financial

statements based on the historical

relationship between sales and

balance sheet accounts that tend to

change in value along with sales

Cash, A/R, inventory and A/P are the

most important accounts, followed by

fixed assets

© 2017 - The Treasury Academy, Inc. - All Rights Reserved 8

Three Steps to the Percentage-of-Sale Method

1. Forecast the income statement and balance sheet based on the relationships between revenues and balance sheet items

2. Calculate projected ending cash balance by determining how the forecasted income statement and balance sheet values impact cash

3. Compare the projected ending cash balance with the company’s target cash balance and adjust the pro-format statement to show the source of funding for a cash shortfall or the investment of a cash surplus

© 2017 - The Treasury Academy, Inc. - All Rights Reserved 9

4

Essential Learning for CTP CandidatesNY Cash Exchange 2017 – Session #CTP-10

Copyright © 2017 – The Treasury Academy, Inc.All Rights Reserved

Pro-Forma Statements – Base Year

© 2017 - The Treasury Academy, Inc. - All Rights Reserved 10Source: ETM5 - © AFP

Pro-Forma Forecast -Assumptions Sales will increase by 10% to $2,200 in the year 2017

Costs of goods sold, selling and administrative expenses, non-cash current assets (receivables and inventory), and payables are a constant percentage of sales

Cash balance is derived from the cash flow statement

Additional fixed assets in the amount of $100 will be purchased

Depreciation will be $50

Notes will be reduced to $100 at the beginning of the year

Dividends will be $24

© 2017 - The Treasury Academy, Inc. - All Rights Reserved 11

Source: ETM5 - © AFP

Pro-Forma Financial Statements

© 2017 - The Treasury Academy, Inc. - All Rights Reserved 12

All the projected account balances except cash are calculated based on the given assumptions. The ending cash balance is determined by evaluating the impact on cash of the income statement activity and balance sheet changes and adjusting the beginning cash balance accordingly.

Source: ETM5 - © AFP

5

Essential Learning for CTP CandidatesNY Cash Exchange 2017 – Session #CTP-10

Copyright © 2017 – The Treasury Academy, Inc.All Rights Reserved

Pro-Forma: Statement of Cash Flows

© 2017 - The Treasury Academy, Inc. - All Rights Reserved 13

If the projected ending cash balance is less than the company’s established target balance, the shortfall must be funded through taking on additional debt, issuing equity of selling assets. Conversely, if the projected cash balance exceeds the target, the surplus may be invested in additional assets, used to reduce debt and/or distributed to shareholders.

In the above example, if the target cash balance were $110, then $15 in additional cash would need to be raised. If this were accomplished though an increase in notes payables, then the projected balance sheet would appear as before, except that cash would be $110 and notes payable would be $115.

Source: ETM5 - © AFP

Five-Period Moving Avg Forecast

© 2017 – The Treasury Academy - All Rights Reserved 14

Day Actual Cash Flow (Xt)

Forecast(N = 5)

Error(Act –F)

1 890,000

2 812,500

3 775,000

4 754,000

5 716,000

6 748,500 789,500 - 41,000

7 1,009,000 761,200 247,800

8 824,000 800,500 23,500

9 874,000 810,300 63,700

10 955,000 834,380 120,620

Moving Average Forecast for Day 7 is:(812,500 + 775,000 + 754,000 + 716,000 + 748,500) / 5 = 761,200Which results in a forecast error of: 1,009,000 – 761,200 = 247,800

Source: ETM5 - © AFP

Forecast with Exponential Smoothing

© 2017 – The Treasury Academy - All Rights Reserved 15

Day ActualCash Flow

(Xt)

Forecast (α=0.40)

(Ft)

Error

6 $ 748,500 $ 789,500 - $ 5,400

7 $ 1,009,000 $ 773,100 $ 235,900

8 $ 824,000 $ 867,460 - $ 43,460

9 $ 874,400 $ 850,076 $ 24,324

t+1 t tF = αX + (1 α)(F )

The exponential smoothing forecast begins with the Day 6 Forecast of $789,500 based on the moving average forecast.

Then, the Day 7 forecast using exponential smoothing is:F7 = 0.40(748,500) + (1 – 0.40)(789,500) = $773,100

This results in a forecast error of: $1,009,000 – $773,100 = $235,900

Source: ETM5 - © AFP

6

Essential Learning for CTP CandidatesNY Cash Exchange 2017 – Session #CTP-10

Copyright © 2017 – The Treasury Academy, Inc.All Rights Reserved

ETM5: Chapter 12 and 14 CalcsConcentration & Forecasting

Additional Calculations

16© 2013 - The Treasury Academy, Inc. - All Rights Reserved© 2017 - The Treasury Academy, Inc. - All Rights Reserved

Wire vs. ACH Concentration

A company can concentrate funds using either a wire or an ACH transfer. The all-in cost for a wire transfer is $12.00 and the cost of an ACH transfer is $0.50. What is the approximate (to the nearest $1000) minimum transfer amount for funds going from a collection account to the concentration account on a Friday? (Assume opp. cost of 2.5%)

A. $ 56,000B. $ 58,000C. $ 84,000D. $167,000

© 2017 - The Treasury Academy, Inc. - All Rights Reserved 17

Blank This slide intentionally blank

© 2017 - The Treasury Academy, Inc. - All Rights Reserved 18

7

Essential Learning for CTP CandidatesNY Cash Exchange 2017 – Session #CTP-10

Copyright © 2017 – The Treasury Academy, Inc.All Rights Reserved

Wire vs. ACH Concentration

A company can concentrate funds using either a wire or an ACH transfer. The all-in cost for a wire transfer is $12.00 and the cost of an ACH transfer is $0.50. What is the approximate (to the nearest $1000) minimum transfer amount for funds going from a collection account to the concentration account on a Friday? (Assume opp. cost of 2.5%)

A.$ 56,000B.$ 58,000C.$ 84,000D.$167,000

© 2017 - The Treasury Academy, Inc. - All Rights Reserved 19

Concentration System Transfers 2 frequently used concentration systems in U.S.

◦ EDT vs. Wire Transfer

Assume the following:

◦ ACH Cost = $0.50; Wire Cost = $12.00

◦ Opp Cost = 2.5%; 3-day speed-up with wire

© 2017 - The Treasury Academy, Inc. - All Rights Reserved 20

Wire Cost ACH CostMin. Transfer =

Opportunity CostDays Accelerated

365 Days

$12.00 $0.50 $11.50= = $55,967

3 .000068490.0253 Days

365 Days

ETM5: Chapter 17 CalculationsFinancial Risk Management

Call/Put Option PricingFX RatesFX Derivative ContractsInterest Rate Derivative Contracts

21© 2017 - The Treasury Academy, Inc. - All Rights Reserved

8

Essential Learning for CTP CandidatesNY Cash Exchange 2017 – Session #CTP-10

Copyright © 2017 – The Treasury Academy, Inc.All Rights Reserved

Relationship Between an Option Premium and Strike (Exercise) Price

Call or put option

At-the-money If the underlying asset price is equal to the strike price of the option

Call option

Out-of-the-money

If the asset price is less than the strike price of the option

Put option

Out-of-the-money

If the asset price exceeds the strike price of the option

Call option

In-the-money If the asset price is greater than the strike price of the option

Put option

In-the-money If the asset price is less than the strike price of the option

© 2017 - The Treasury Academy, Inc. - All Rights Reserved 22Source: ETM5 - © AFP

Call Option Pricing

© 2017 - The Treasury Academy, Inc. - All Rights Reserved 23Source: ETM5 - © AFP

Put Option Pricing

© 2017 - The Treasury Academy, Inc. - All Rights Reserved 24

Source: ETM5 - © AFP

9

Essential Learning for CTP CandidatesNY Cash Exchange 2017 – Session #CTP-10

Copyright © 2017 – The Treasury Academy, Inc.All Rights Reserved

Foreign Exchange (FX) Risk Management in Treasury

Challenges in International/Global Treasury Management◦ Foreign Exchange (FX) Risk

◦ Cash Flow Complexity

◦ Tax Issues

Foreign Exchange (FX) Rates◦ FX rates are quoted in several ways,

depending on the currencies and the markets involved

◦ An FX rate is expressed as the equivalent unit of one currency per unit of another currency at a given moment in time

25© 2017 - The Treasury Academy, Inc. - All Rights Reserved

Sample Foreign Currency Quotation Formats

Most common formats are in Bold/Italic

© 2017– The Treasury Academy - All Rights Reserved 26

Currency USDEquivalent

Unit of Currency per one USD

GBP-British pound GBP/USD 1.3199 USD/GBP 0.7576

CAD-Canadian dollar CAD/USD 0.7744 USD/CAD 1.2914

EUR-Euro EUR/USD 1.1307 USD/EUR 0.8844

JPY-Japanese yen JPY/USD 0.009976 USD/JPY 100.24

Foreign Exchange (FX) Rates

Example: The quoted rate for the USD equivalent is EUR/USD 1.1307. How many euros would $2 million buy?

Example: The quoted rate for the USD equivalent is GBP/USD 1.3199. How many pounds would $2 million buy?

$2,000,000 = EUR1,768,816

1.1307

$2,000,000 = GBP1,515,266

1.3199

© 2017– The Treasury Academy - All Rights Reserved 27

10

Essential Learning for CTP CandidatesNY Cash Exchange 2017 – Session #CTP-10

Copyright © 2017 – The Treasury Academy, Inc.All Rights Reserved

Foreign Exchange (FX) Rates

Example: The quoted rate for the Japanese yen USD/JPY 100.25. How many yen would $2 million purchase?

Example: The quoted rate for the Can. dollar is USD/CAD 1.2914. CAD2,000,000 would be equivalent to how many USD?

CAD2,000,000 = USD1,548,707

1.2914

x$2,000,000 100.25

= JPY200,500,000

© 2017– The Treasury Academy - All Rights Reserved 28

Foreign Exchange (FX) Rates:Bid-Offer Spreads and Dealer Profit

Bid rate: Dealer buys currency Offer rate: Dealer sells currency Bid/offer spread or bid/ask spread:

Difference between rates (dealer’s profit) Dealer bid-offer quote; e.g., USD/JPY 100.22/26

ScenarioCompany Delivers

Dealer Buys

Dealer Sells

Company Receives

Company wants to buy JPY

USD USD at bid rate

(JPY100.22)

JPY JPY

Company wants to sell JPY for USD

JPY JPY USD at offer rate

(JPY100.26)

USD

© 2017– The Treasury Academy - All Rights Reserved 29

Pricing of Derivative Contracts for FX and Interest Rates

This chapter provides some detailed examples of these items (See listed pages below); due the extreme complexity of these examples, coverage is provided through the on-line course

Currency Derivatives (Pgs. 487-495) ◦ Currency or FX Forwards

◦ Currency Futures

◦ Currency Swaps

◦ Currency Options

Interest Rate Derivatives (495-500)◦ Interest Rate Futures

◦ Interest Rate Swaps

© 2017 - The Treasury Academy, Inc. - All Rights Reserved 30

Source: ETM5 - © AFP

11

Essential Learning for CTP CandidatesNY Cash Exchange 2017 – Session #CTP-10

Copyright © 2017 – The Treasury Academy, Inc.All Rights Reserved

ETM5: Chapter 17 CalculationsFinancial Risk Management

Additional Calculations

31© 2017 - The Treasury Academy, Inc. - All Rights Reserved

FX Calculation

A U.S. company has to pay one of their French suppliers EUR1.25M in the next 30 days. The dealer is quoting a forward rate of EUR/USD1.4215/325. What is the expected amount of dollars the company would be paying for this transaction?

A. $ 872,600B. $ 879,353C. $1,776,875D. $1,790,625

© 2017 - The Treasury Academy, Inc. - All Rights Reserved 32

Blank This slide intentionally blank

© 2017 - The Treasury Academy, Inc. - All Rights Reserved 33

12

Essential Learning for CTP CandidatesNY Cash Exchange 2017 – Session #CTP-10

Copyright © 2017 – The Treasury Academy, Inc.All Rights Reserved

FX Calculation

A U.S. company has to pay one of their French suppliers EUR1.25M in the next 30 days. The dealer is quoting a forward rate of EUR/USD1.4215/325. What is the expected amount of dollars the company would be paying for this transaction?

A. $ 872,600B. $ 879,353C. $1,776,875D. $1,790,625

© 2017 - The Treasury Academy, Inc. - All Rights Reserved 34

FX Calculation Quote: EUR/USD 1.4215/325◦ Bid: EUR/USD 1.4215 Ask: EUR/USD 1.4325

Always use the quote side that is worst deal for the user and best for the dealer

In this case, using the ask side of the quote will give the large amount of USD that will be needed for the transaction

© 2017 - The Treasury Academy, Inc. - All Rights Reserved 35

USD Amount = EUR Amount × Ask Rate

= EUR 1,250,000 1.4325

= USD 1,790,625

Blank This slide intentionally blank

© 2017 - The Treasury Academy, Inc. - All Rights Reserved 36

13

Essential Learning for CTP CandidatesNY Cash Exchange 2017 – Session #CTP-10

Copyright © 2017 – The Treasury Academy, Inc.All Rights Reserved

ETM5: Chapter 12 CalculationsWorking Capital Metrics

Lockbox Cost/Benefit Analysis

37© 2017 - The Treasury Academy, Inc. - All Rights Reserved

Source: ETM5 - © AFP

Lockbox Selection

Cost/benefit analysis: Lockbox versuscompany processing center

Compare differences in collection (mail, processing and availability) float.

◦ Collection study estimates float savings (endpoint

analysis).

◦ Obtain mail time studies from treasury consulting

companies.

◦ Combine mail time studies with availability schedules from

each bank.

Compare differences betweenfixed and variable costs.

© 2017 - The Treasury Academy, Inc. - All Rights Reserved 38

Lockbox Cost/Benefit Analysis

Annual Sales = $108 Million($9M/month)

Average check size = $9,000 Annual vol. of checks = 12,000 Opportunity costs = 9% Internal processing = $0.25/item Lockbox costs = $10,000/yr plus

$0.50 per item

© 2017 - The Treasury Academy, Inc. - All Rights Reserved 39

14

Essential Learning for CTP CandidatesNY Cash Exchange 2017 – Session #CTP-10

Copyright © 2017 – The Treasury Academy, Inc.All Rights Reserved

Without Lockbox

Batch Dollar Amount Calendar Days of Collection Float

Total Dollar-Days

1 $1,500,000 X 4 = $6,000,000

2 $4,500,000 X 2 = $9,000,000

3 $3,000,000 X 6 = $18,000,000

Total Deposits $9,000,000 Total Float $33,000,000

Divided by 30 Calendar Days $1,100,000

Annual Cost of Float= Average Dollar-Days times Opportunity Cost= $1,100,000 x .09 = $99,000

© 2017 - The Treasury Academy, Inc. - All Rights Reserved 40

Source: ETM5 - © AFP

Lockbox Assumptions Lockbox can deliver the following float

reductions:◦ Batch 1 from 4 days to 3 days◦ Batch 2 from 2 days to 1 day◦ Batch 3 from 6 days to 5 days

Lockbox costs◦ $10,000 annual fee◦ $0.50 per item processing fee

© 2017 - The Treasury Academy, Inc. - All Rights Reserved 41

With Lockbox

Batch Dollar Amount Calendar Days of Collection Float

Total Dollar-Days

1 $1,500,000 X 3 = $4,500,000

2 $4,500,000 X 1 = $4,500,000

3 $3,000,000 X 5 = $15,000,000

Total Deposits $9,000,000 Total Float $24,000,000

Divided by 30 Calendar Days $800,000

Annual Cost of Float= Average Dollar-Days times Opportunity Cost= $800,000 x .09 = $72,000

© 2017 - The Treasury Academy, Inc. - All Rights Reserved 42

Source: ETM5 - © AFP

15

Essential Learning for CTP CandidatesNY Cash Exchange 2017 – Session #CTP-10

Copyright © 2017 – The Treasury Academy, Inc.All Rights Reserved

Comparison of Alternatives

Without Lockbox Float Cost = $99,000

With Lockbox Scenario

◦ Float cost savings = $99,000 – $72,000 = $27,000

◦ Fixed Costs of Lockbox = $10,000

◦ Variable Costs of Lockbox = 12,000 x $0.50 = $6,000

◦ Elimination of internal processing costs

= 12,000 x $0.25 = $3,000

◦ Net Benefit = Savings minus lockbox costs

= ($27,000 + $3,000) – ($10,000 + $6,000)

= $30,000 – $16,000 = $14,000

© 2017 - The Treasury Academy, Inc. - All Rights Reserved 43

Source: ETM5 - © AFP

ETM5: Chapter 13 CalculationsS/T Investing & Borrowing

Tax Equivalent YieldHolding Period YieldAnnual YieldDollar Discount/Discount RateMoney Market Yield (MMY)Bond Equivalent Yield (BEY)T-Bill Quotes & Yield CalculationCost for Commercial Paper (CP) IssueCost for Bank Line of CreditDebt Financing

44© 2017 - The Treasury Academy, Inc. - All Rights Reserved

Tax Status When computing taxable vs. tax-exempt

instruments, use the formula below

Assume a taxable security with a 4.6% yield and a tax-exempt security with a 3.2% yield (both have similar risk and maturity) – marginal tax rate is 35%

© 2017 - The Treasury Academy, Inc. - All Rights Reserved 45

1

Tax-exempt YieldTaxable Equivalent Yield =

( Investor's Marginal Tax Rate)

1

0.032Taxable Equivalent Yield = 0.0492 or 4.92%

( 0.35)

After-Tax Yield = Taxable Yield x (1 – Marginal Tax Rate)

After-Tax Yield = 4.60% x (1 – 0.35) = 2.99%

In this example – the tax-exempt security should be chosen

16

Essential Learning for CTP CandidatesNY Cash Exchange 2017 – Session #CTP-10

Copyright © 2017 – The Treasury Academy, Inc.All Rights Reserved

Yield Calculations for S-T Investments

Usually made on a simple interest basis Yield is usually a function of:◦ Cash flows received from the investment

◦ Amount paid for that investment

◦ Maturity or holding period

Different types of yield◦ Holding period yield

◦ Money market yield(360 day year basis)

◦ Bond equivalent yield(365 day year basis)

© 2017 - The Treasury Academy, Inc. - All Rights Reserved 46

The Key Formulas for Investing and Borrowing

© 2017 - The Treasury Academy, Inc. - All Rights Reserved 47

What You GetWhat You Pay

What You PayWhat You Get

Yield Calculations

© 2017 - The Treasury Academy, Inc. - All Rights Reserved 48

Cash Rec. at Maturity Amt InvestedHolding Period Yield =

Amt Invested

Days in YearAnnual Yield = Holding Period Yield

Days to Maturity

Assume a $100,000, 90-day T-bill sells for $98,800

$100,000 $98,800Holding Period Yield =

$98,800

$1,200 = = 0.01215 or 1.215%

$98,800

360360-Day Basis Yield = 0.01215

90= 0.01215 4 = 0.0486 or 4.86%

Source: ETM5 - © AFP

17

Essential Learning for CTP CandidatesNY Cash Exchange 2017 – Session #CTP-10

Copyright © 2017 – The Treasury Academy, Inc.All Rights Reserved

Converting Year Basis To determine the yield on a 365-day basis

versus a 360-day basis use the following:

© 2017 - The Treasury Academy, Inc. - All Rights Reserved 49

365365-Day Basis Yield = 360-Day Basis Yield

360

365365-Day Basis Yield = 0.0486 = 0.0493 or 4.93%

360

Using the information from the previous slide:

Source: ETM5 - © AFP

Discount Instruments T-bills, CP and BAs are discounted instruments◦ Dollar discount = Par value – purchase price◦ Consider $1M , 182-day T-bill, sold for $974,216

© 2017 - The Treasury Academy, Inc. - All Rights Reserved 50

$1,000,000 $974,216 $25,784Holding Period Yield = =

$974,216 $974,216

= 0.0265 or 2.65%

360360-Day Basis Yield = 0.0265 = 0.0524 or 5.24%

182

Dollar Discount = $1,000,000 – $974,216 = $25,784

Dollar Discount 360Discount Rate =

Par Value Days to Maturity

$25,784 360= = 0.0510 or 5.10%

$1,000,000 182

Source: ETM5 - © AFP

Re-arranging the Yield Equations

© 2017 - The Treasury Academy, Inc. - All Rights Reserved 51

Days to MaturityDollar Discount = Discount Rate Par Value

360182

= 0.051 $1,000,000 = $25,784360

360Money Market Yield = Holding Period Yield

Days to Maturity

$1,000,000 $974,216 360=

$974,216 182

= 0.0265 1.978 = 0.0524 or 5.24%

365Bond Equivalent Yield = Money Market Yield

360365

= 0.0524 = 0.0531 or 5.31%360

Source: ETM5 - © AFP

18

Essential Learning for CTP CandidatesNY Cash Exchange 2017 – Session #CTP-10

Copyright © 2017 – The Treasury Academy, Inc.All Rights Reserved

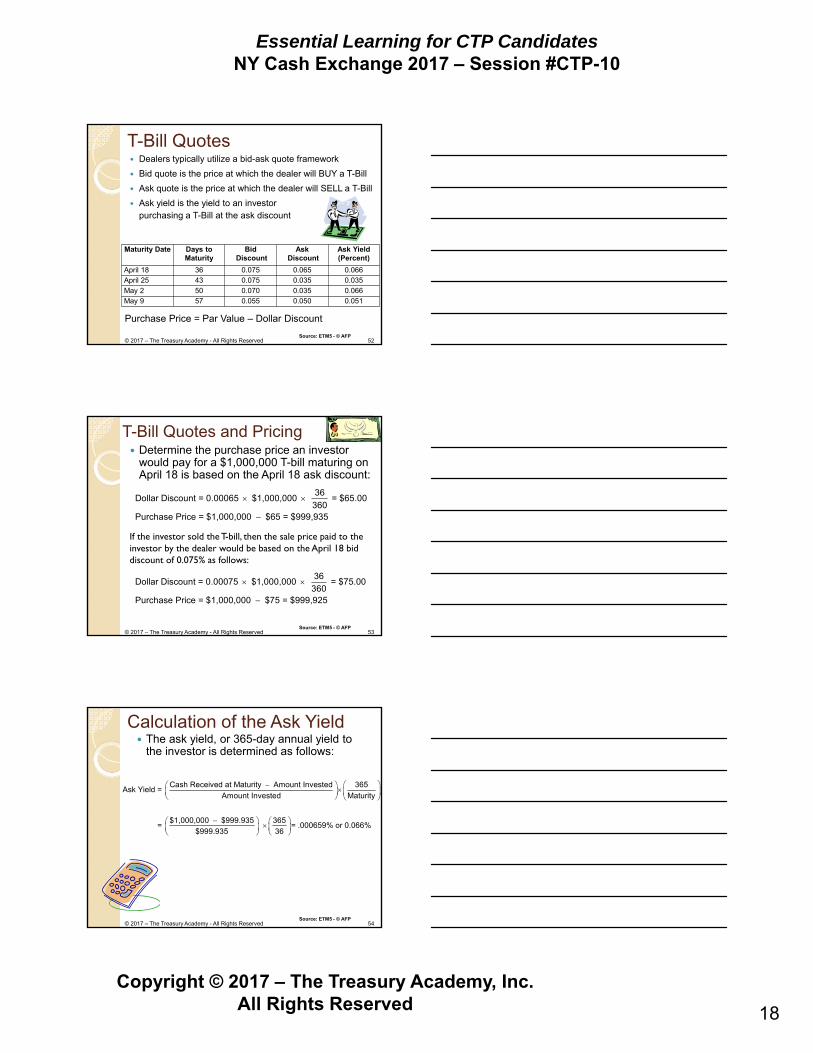

T-Bill Quotes Dealers typically utilize a bid-ask quote framework

Bid quote is the price at which the dealer will BUY a T-Bill

Ask quote is the price at which the dealer will SELL a T-Bill

Ask yield is the yield to an investorpurchasing a T-Bill at the ask discount

© 2017 – The Treasury Academy - All Rights Reserved 52

Maturity Date Days to Maturity

BidDiscount

AskDiscount

Ask Yield(Percent)

April 18 36 0.075 0.065 0.066

April 25 43 0.075 0.035 0.035

May 2 50 0.070 0.035 0.066

May 9 57 0.055 0.050 0.051

Purchase Price = Par Value – Dollar Discount

Source: ETM5 - © AFP

T-Bill Quotes and Pricing Determine the purchase price an investor

would pay for a $1,000,000 T-bill maturing on April 18 is based on the April 18 ask discount:

© 2017 – The Treasury Academy - All Rights Reserved 53

36Dollar Discount = 0.00065 $1,000,000 = $65.00

360Purchase Price = $1,000,000 $65 = $999,935

If the investor sold the T-bill, then the sale price paid to the investor by the dealer would be based on the April 18 bid discount of 0.075% as follows:

36Dollar Discount = 0.00075 $1,000,000 = $75.00

360Purchase Price = $1,000,000 $75 = $999,925

Source: ETM5 - © AFP

Calculation of the Ask Yield The ask yield, or 365-day annual yield to

the investor is determined as follows:

© 2017 – The Treasury Academy - All Rights Reserved 54

Cash Received at Maturity Amount Invested 365Ask Yield =

Amount Invested Maturity

$1,000,000 $999.935 365= = .000659% or 0.066%

$999.935 36

Source: ETM5 - © AFP

19

Essential Learning for CTP CandidatesNY Cash Exchange 2017 – Session #CTP-10

Copyright © 2017 – The Treasury Academy, Inc.All Rights Reserved

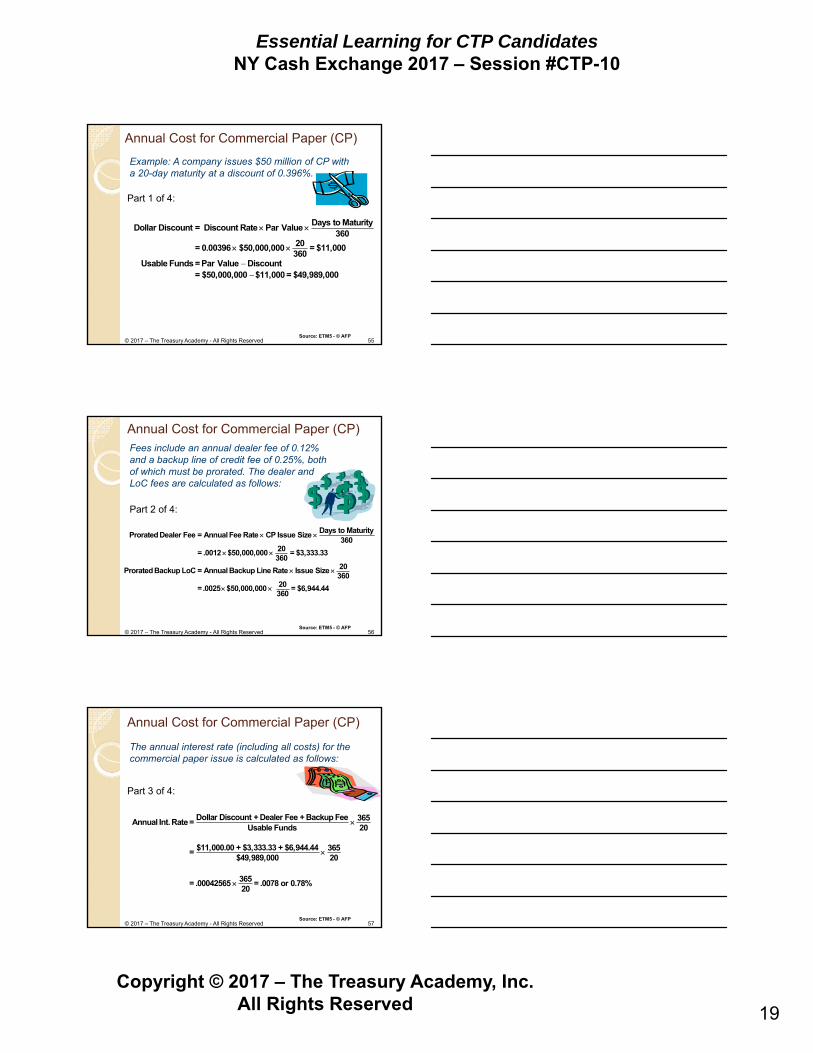

Annual Cost for Commercial Paper (CP)

Days to MaturityDollar Discount = Discount Rate Par Value

36020= 0.00396 $50,000,000 = $11,000360

Usable Funds = Par Value Discount= $50,000,000 $11,000 = $49,989,000

Part 1 of 4:

Example: A company issues $50 million of CP with a 20-day maturity at a discount of 0.396%.

© 2017 – The Treasury Academy - All Rights Reserved 55Source: ETM5 - © AFP

Annual Cost for Commercial Paper (CP)

Days to MaturityProrated Dealer Fee = Annual Fee Rate CP Issue Size

36020= .0012 $50,000,000 = $3,333.33360

20Prorated Backup LoC = Annual Backup Line Rate Issue Size 360

=.0025 $50,000,000

20 = $6,944.44360

Fees include an annual dealer fee of 0.12% and a backup line of credit fee of 0.25%, both of which must be prorated. The dealer and LoC fees are calculated as follows:

Part 2 of 4:

© 2017 – The Treasury Academy - All Rights Reserved 56Source: ETM5 - © AFP

Annual Cost for Commercial Paper (CP)

Dollar Discount + Dealer Fee + Backup Fee 365Annual Int. Rate= Usable Funds 20

$11,000.00 + $3,333.33 + $6,944.44 365= $49,989,000 20

365= .00042565 = .0078 or 0.78%20

Part 3 of 4:

The annual interest rate (including all costs) for the commercial paper issue is calculated as follows:

© 2017 – The Treasury Academy - All Rights Reserved 57Source: ETM5 - © AFP

20

Essential Learning for CTP CandidatesNY Cash Exchange 2017 – Session #CTP-10

Copyright © 2017 – The Treasury Academy, Inc.All Rights Reserved

Annual Cost for Commercial Paper (CP)

Dollar Discount 365CP Nominal Yield= × Purchase Price Days to Maturity

$11,000 365= × = .0040 or 0.40%$49,989,000 20

Part 4 of 4:

The nominal, or annual, yield to an investor is calculated as follows:

© 2017 – The Treasury Academy - All Rights Reserved 58Source: ETM5 - © AFP

Annual Cost for a Line of Credit

A line of credit lender charges interest and a commitment fee on the line.

Interest is charged on the used portion of the line.

The commitment fee may be charged on the line or its unused portion.

The overall interest rate on the line is determined by the total interest paid on the line’s used portion and the amount paid per the commitment fee relative to the average used portion of the credit line over the borrowing period.

© 2017 - The Treasury Academy, Inc. - All Rights Reserved 59

Annual Cost for a Line of CreditExample: A company expects to use $1.6 M of short-

term borrowings and wants a $3 M line of credit. A lender offers LIBOR (at 0.70%) plus a risk premium of 2.50% with a commitment fee of 0.30% on the unused portion of the line. The rate on the used portion of the line is LIBOR plus 2.50%, or 3.20% (the all-in rate). All interest and fees are calculated as follows:

Part 1 of 5:

Interest Paid = Average Borrowing × All-in Rate

= $1,600,000 × .032 = $51,200

Fee on Unused Portion = Unused Portion × Commitment Fee

= $1,400,000 × 0.0030 = $4,200

© 2017 – The Treasury Academy - All Rights Reserved 60Source: ETM5 - © AFP

21

Essential Learning for CTP CandidatesNY Cash Exchange 2017 – Session #CTP-10

Copyright © 2017 – The Treasury Academy, Inc.All Rights Reserved

Annual Cost for a Line of Credit

The annual interest rate as total costs relative to the amount used on the line is calculated as follows:

Part 2 of 5:

Interest Rate + Fee on Unused PortionAnnual Int. Rate =

Used Portion of Line

$51,200 + $4,200 = = .0346 or 3.46%

$1,600,000

© 2017 – The Treasury Academy - All Rights Reserved 61Source: ETM5 - © AFP

Annual Cost for a Line of Credit

The lender (a bank) requires a 10% compensating balance; the borrower must maintain a balance in its DDA (checking) account ≥ 10% of the amount borrowed on the credit line. The DDA is a zero balance account (ZBA).

Part 3 of 5:

Interest + Fee on Unused PortionAnnual Int. Rate =

Used Portion of the Line Compensating Balance

$51,200 + $4,200Annual Int. Rate = = .0385 or 3.85%

$1,600,000 $160,000

© 2017 – The Treasury Academy - All Rights Reserved 62Source: ETM5 - © AFP

Annual Cost for a Line of CreditThe amount borrowed on the line is calculated as follows (assuming the available loan amount must be $1,600,000).

Part 4 of 5:

Available Amt = Borrowed Amt Compensating Balance % Borrowed Amt

$1,600,000 = Borrowed Amount .10 Borrowed Amount

.90 Borrowed Amount = $1,600,000

Borrowed Amount = $1,777,777.78

The larger amount increases the total interest and fees paid.

Interest Paid = Average Borrowing × All-in Rate

= $1,777,777.78 × .032 = $56,888.89

Fee on Unused Portion = Unused Portion × Commitment Fee

= $3,000,000 $1,777,777.78 0.0030 = $3,666.67

© 2017 – The Treasury Academy - All Rights Reserved 63Source: ETM5 - © AFP

22

Essential Learning for CTP CandidatesNY Cash Exchange 2017 – Session #CTP-10

Copyright © 2017 – The Treasury Academy, Inc.All Rights Reserved

Annual Cost for a Line of Credit

The annual interest rate can be recalculated as a total cost relative to the borrowed amount that is actually usable as follows:

Part 5 of 5:

Interest Paid+ Fee on Unused PortionAnnual Int. Rate =

Amount Borrowed Compensating Balance

$56,888.89 + $3,666.67=

$1,777,777.78 .10 $1,777,777.78

$60,555.56= = .0378 or 3.78%

$1,600,000

© 2017 – The Treasury Academy - All Rights Reserved 64Source: ETM5 - © AFP

ETM5: Chapter 11 CalculationsS/T Investing & Borrowing

Additional Calculations

65© 2017 - The Treasury Academy, Inc. - All Rights Reserved

How much would you be willing to pay for 91-day $1M T-bill selling at a discount rate of 50 basis points?

A. $987,361

B. $998,736

C. $998,753

D. $1,000,000

© 2017 - The Treasury Academy, Inc. - All Rights Reserved 66

23

Essential Learning for CTP CandidatesNY Cash Exchange 2017 – Session #CTP-10

Copyright © 2017 – The Treasury Academy, Inc.All Rights Reserved

How much would you be willing to pay for 91-day $1M T-bill selling at a discount rate of 50 basis points?

A. $987,361

B. $998,736

C. $998,753

D. $1,000,000

© 2017 - The Treasury Academy, Inc. - All Rights Reserved 67

T-Bill Pricing Determine the purchase price an investor

would pay for a $1,000,000 T-bill maturing in 91 days at a discount rate of 50 bp:

© 2017 - The Treasury Academy, Inc. - All Rights Reserved 68

91Dollar Discount = 0.005 $1,000,000 = $1,264

360Purchase Price = $1,000,000 $1,264 = $998,736

What is the annual yield (365) to an investor for a 30-day $10M CP issue with a discount rate of 175 basis points (bp), a dealer fee of 30 bp and a credit enhancement fee of 45 bp?

A. 1.75%

B. 1.78%

C. 2.50%

D. 2.54%

69© 2017 - The Treasury Academy, Inc. - All Rights Reserved

24

Essential Learning for CTP CandidatesNY Cash Exchange 2017 – Session #CTP-10

Copyright © 2017 – The Treasury Academy, Inc.All Rights Reserved

What is the annual yield (365) to an investor for a 30-day $10M CP issue with a discount rate of 175 basis points (bp), a dealer fee of 30 bp and a credit enhancement fee of 45 bp?

A. 1.75%

B. 1.78%

C. 2.50%

D. 2.54%

70© 2017 - The Treasury Academy, Inc. - All Rights Reserved

CP Calculations

Dollar Discount 365CP Yield= × Purchase Price Days to Maturity

$14,583 365= × = .0178 or 1.78%$9,985,417 30

The annual, yield (365) to an investor is calculated as follows:

Days to MaturityDollar Discount = Discount Rate Par Value

36030= 0.0175 $10,000,000 = $14,583360

Purchase Price = Par Value Discount= $10,000,000 $14,583 = $9,985,417

© 2017 - The Treasury Academy, Inc. - All Rights Reserved 71

Annual Cost for Commercial Paper (CP)

Days to MaturityProrated Dealer Fee = Annual Fee Rate CP Issue Size

36030= .0030 $10,000,000 = $2,500360

30Prorated Backup LoC = Annual Backup Line Rate Issue Size 360

=.0045 $10,000,000

30 = $3,750360

Fees include an annual dealer fee of 0.30% and a backup line of credit fee of 0.45%, both of which must be prorated.

Dollar Disc. + Dealer Fee + Backup Fee 365Annual Int. Rate = Usable Funds 30

$14,583 + $2,500 + $3,750 365= = .0254 or 2.54%$9,985,417 30

The annual interest rate (including all costs) for the commercial paper issue is calculated as follows:

© 2017 - The Treasury Academy, Inc. - All Rights Reserved 72

25

Essential Learning for CTP CandidatesNY Cash Exchange 2017 – Session #CTP-10

Copyright © 2017 – The Treasury Academy, Inc.All Rights Reserved

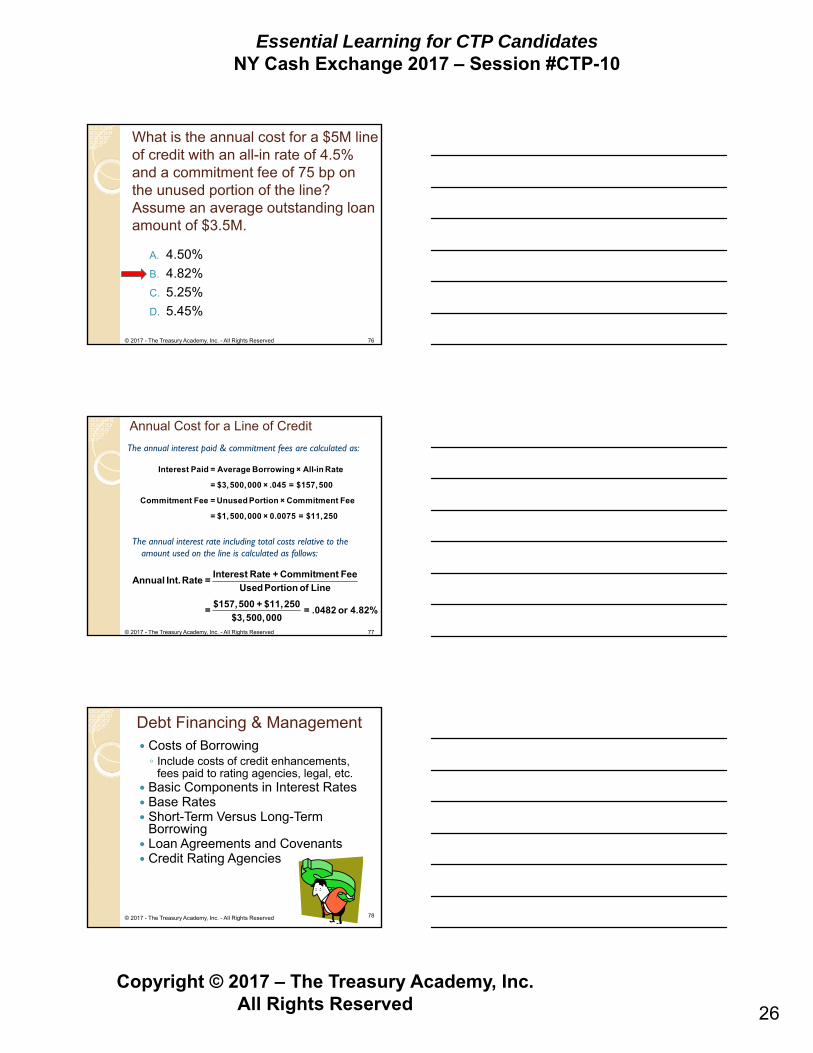

What is the annual cost for a $5M line of credit with an all-in rate of 4.5% and a commitment fee of 75 bp on the unused portion of the line? Assume an average outstanding loan amount of $3.5M.

A. 4.50%

B. 4.82%

C. 5.25%

D. 5.45%

73© 2017 - The Treasury Academy, Inc. - All Rights Reserved

Blank This slide intentionally blank

© 2017 - The Treasury Academy, Inc. - All Rights Reserved 74

Blank This slide intentionally blank

© 2017 - The Treasury Academy, Inc. - All Rights Reserved 75

26

Essential Learning for CTP CandidatesNY Cash Exchange 2017 – Session #CTP-10

Copyright © 2017 – The Treasury Academy, Inc.All Rights Reserved

What is the annual cost for a $5M line of credit with an all-in rate of 4.5% and a commitment fee of 75 bp on the unused portion of the line? Assume an average outstanding loan amount of $3.5M.

A. 4.50%

B. 4.82%

C. 5.25%

D. 5.45%

76© 2017 - The Treasury Academy, Inc. - All Rights Reserved

Annual Cost for a Line of Credit

The annual interest rate including total costs relative to the amount used on the line is calculated as follows:

Interest Rate + Commitment FeeAnnual Int. Rate =

Used Portion of Line

$157,500 + $11,250 = = .0482 or 4.82%

$3,500,000

Interest Paid = Average Borrowing × All-in Rate

= $3,500,000 × .045 = $157,500

Commitment Fee = Unused Portion × Commitment Fee

= $1,500,000 × 0.0075 = $11,250

The annual interest paid & commitment fees are calculated as:

© 2017 - The Treasury Academy, Inc. - All Rights Reserved 77

Debt Financing & Management Costs of Borrowing◦ Include costs of credit enhancements,

fees paid to rating agencies, legal, etc. Basic Components in Interest Rates Base Rates Short-Term Versus Long-Term

Borrowing Loan Agreements and Covenants Credit Rating Agencies

78© 2017 - The Treasury Academy, Inc. - All Rights Reserved

27

Essential Learning for CTP CandidatesNY Cash Exchange 2017 – Session #CTP-10

Copyright © 2017 – The Treasury Academy, Inc.All Rights Reserved

Basic Components in Interest Rates

Interest rates depend on many factors r = r*RF + IP + DP + LP + MP◦ Where: r*RF = Real risk-free interest rate

IP = Inflation premiumDP = Default premiumLP = Liquidity premiumMP = Maturity premium

Some observations◦ Treasuries: DP and LP = 0

◦ Both corporate and muni’s have DP and LP

◦ Most L-T bonds have some MP

◦ MP increases with issue’s time to maturity

© 2017 - The Treasury Academy, Inc. - All Rights Reserved 79

Calculation of Interest Rates

© 2017 - The Treasury Academy, Inc. - All Rights Reserved 80

Calculation of Interest Rates or Yields on Different InvestmentsInvestmen

tReal Risk-Free Rate

Inflation Premium

Default Premium

Liquidity Premium

Maturity Premium

Cost of Borrowing

1-year Treasury

2.0% 3.0% 0% 0% 0% 5.0%

5-year Treasury

2.0% 5.0% 0% 0% 0.4% 7.4%

10-year Treasury

2.0% 7.0% 0% 0% 0.9% 9.9%

1-year Corporate

2.0% 3.0% 2.5% 0.5% 0% 8.0%

5-year Corporate

2.0% 5.0% 2.5% 0.5% 0.4% 10.4%

10-year Corporate

2.0% 7.0% 2.5% 0.5% 0.9% 12.9%

1-year Municipal

2.0% 3.0% 1.5% 1.0% 0% 7.5%

5-year Municipal

2.0% 5.0% 1.5% 1.0% 0.4% 9.9%

10-year Municipal

2.0% 7.0% 1.5% 1.0% 0.9% 12.4%

Source: ETM5 - © AFP

ETM5: Chapter 19 CalculationsLong-Term and Capital Instruments

Capital Asset Pricing Model (CAPM)Portfolio Risk and ReturnPreferred Stock ValuationCommon Stock Valuation

81© 2017 - The Treasury Academy, Inc. - All Rights Reserved

28

Essential Learning for CTP CandidatesNY Cash Exchange 2017 – Session #CTP-10

Copyright © 2017 – The Treasury Academy, Inc.All Rights Reserved

Equity (Stock) Portfolio Mgmt. Defining and Measuring Investment Risk◦ Expected return and standard deviation◦ Use of covariance in portfolio management

Benefits of Diversification◦ Reduces the overall riskiness of a portfolio

Capital Asset Pricing Model (CAPM)◦ Beta is a measure of relative market risk◦ In a diversified portfolio, Beta is the only relevant measure to

an investor CAPM – Model Relationship

© 2017 – The Treasury Academy - All Rights Reserved 82

E

RF

M

E RF M RF i

Where: r Required rate of return on stockholder's equity

r Expected rate of return on the risk-free asset

r Expected rate of return on the market portfolio

r r (r r )

i Beta value for stock i

CAPM Calculation Example Assume a risk-free rate (T-bill) of 2.0%, a

market rate of return of 8.0%, and historic Beta for Apple Computer of 1.5:

Assume the same information as above, but for H.J. Heinz with a Beta of 0.60:

© 2017 – The Treasury Academy - All Rights Reserved 83

E RF M RF i

E

r r (r r )

r 0.02 (0.08 0.02)(1.5) 0.110 11.0%

E RF M RF i

E

r r (r r )

r 0.02 (0.08 0.02)(0.6) 0.056 5.6%

Source: ETM5 - © AFP

Determining Portfolio Risk & Return

One of the biggest benefits of using CAPM and Beta is the

ability to determine a portfolios average return and overall

riskiness as a function of simple weighted averages

Using the stocks from the previous slide with weights of

Apple(A) = 70% and Heinz(H) = 30%

© 2017 - The Treasury Academy, Inc. - All Rights Reserved 84

Portfolio β = (% of A-Stock β ) + (% of H-Stock β )

= (.70 1.5) + (.30 0.60) = 1.23

A H

Port. Return = (% of A-Stock r ) + (% of H-Stock r )

= (.70 11.0%) + (.30 5.6%) = 9.38%

A H

E RF M RF Portfolior r (r r )

= .02 + (.08 .02)(1.23)= 0.0938 or 9.38%

Source: ETM5 - © AFP

29

Essential Learning for CTP CandidatesNY Cash Exchange 2017 – Session #CTP-10

Copyright © 2017 – The Treasury Academy, Inc.All Rights Reserved

Valuation of Long-Term Securities

Publicly traded corporate securities are valued by financial markets

The value is based on the cash flow stream expected by the investor as well as the relevant discount rate:

◦ Where: PV0 = Current value of the assetCFt = Cash flow in period tki = Opportunity cost for asset i

© 2017 - The Treasury Academy, Inc. - All Rights Reserved 85

nt 1 2 n

0 t 1 2 nt 1 i i i i

CF CF CF CFPV ....

(1 k ) (1 k ) (1 k ) (1 k )

Source: ETM5 - © AFP

Bond or Fixed Income Valuation Valuation of bonds or any fixed income security is

fairly easy because the cash flows and their timing is well known

Required rate on a bond issue is typically called the Yield to Maturity (YTM)

Some bonds have call provisions, and the Yield to Call (YTC) should also be computed

Another approach with callable bonds is to compute Yield to Worst (YTW), where the lowest possible yield is determined

YTW can also be used with other types of bonds to determine the impact of all potentially negative provisions (pre-payments, sinking funds, etc.)

© 2017 - The Treasury Academy, Inc. - All Rights Reserved 86

Preferred Stock Valuation Preferred stock is equity, but has features of

debt financing in its payments Assume a $50 par value, with a 6.6% annual

dividend and an 8.0% required return

Now, assume required return increases to 10%

© 2017 – The Treasury Academy - All Rights Reserved 87

Pref. Stock Div. = Pref. Stock Div. Rate Par Value

= 6.6% $50 $3.30

Pref. Stock Annual Div.Price of Pref. Stock =

Required Rate of Return

$3.30$41.25

.08

$3.30

Price of Preferred Stock = $33.00.10

Source: ETM5 - © AFP

30

Essential Learning for CTP CandidatesNY Cash Exchange 2017 – Session #CTP-10

Copyright © 2017 – The Treasury Academy, Inc.All Rights Reserved

Common Stock Valuation Neither the timing or the amount of the cash flows

are known with certainty

To value common stock, it is necessary to estimate the dividend stream and liquidation price, as well as a required rate of return on the stock

Where: P0 = Current value of the stockDt = Dividend in period tks = Required rate of return for the stock

© 2017 – The Treasury Academy - All Rights Reserved 88

31 20 1 2 3

s s s s

tt

t=1 s

DD D DP = + + + ... +

(1+k ) (1+k ) (1+k ) (1+k )

D=

(1+k )

Common Stock Valuation Common assumption is to assume that dividends

will grow at some constant rate in the future

Dividend in period t = Dt = D0(1+g)t

Substituting this into the general equation, we get:

Assuming that D1 = D0(1+g), we get:

This formulation works well for companies paying a steadily growing dividend, which includes a significant portion of large cap firms in the U.S.

© 2017 – The Treasury Academy - All Rights Reserved 89

t0

0 tt=1 s

D (1 g)P =

(1+k )

t+11

0s s

DDP = or P =

(k g) (k g)t

Source: ETM5 - © AFP

Common Stock Valuation - Example

Assume the following:◦ Last dividend (D0) = $2.00

◦ Estimate growth rate (g) = 6%

◦ Return on stock (ks) = 13%

© 2017 – The Treasury Academy - All Rights Reserved 90

010

s s

D (1 + g)DP = =

(k g) (k g)

$2.00 (1 + .06) $2.12= = = $30.29

(0.13 0.06) 0.07

Source: ETM5 - © AFP

31

Essential Learning for CTP CandidatesNY Cash Exchange 2017 – Session #CTP-10

Copyright © 2017 – The Treasury Academy, Inc.All Rights Reserved

ETM5: Chapter 20Cost of DebtCost of EquityWeighted Average Costof Capital (WACC)Firm Valuation (EVA)

91© 2017 - The Treasury Academy, Inc. - All Rights Reserved

Cost of Capital and Firm Value Cost of capital is the basic target number that

asset returns must exceed if the company is to create shareholder value

Capital Components and Costs◦ Primary sources of “permanent” capital are long-term

debt (bonds) and equity (common stock and retained earnings)

◦ The relevant costs ofthese sources are theirmarginal cost

◦ Be sure to use onlyafter-tax values for the costs

Typically calculated as WACC◦ Weighted Average Cost of Capital

92© 2017 – The Treasury Academy - All Rights Reserved

Cost of Debt Relevant cost is after-tax YTM

After-tax kd = Before-tax kd(1 – T)

Calculation Example – AssumeYTM of 5% and marginal tax rate of 30%:◦ After-tax kd = 5%(1 – .3) = 3.5%

In companies with complicated tax liabilities, the marginal tax rate may be difficult to estimate from standard financial statements

Though flotation costs of debt are usually low, they should be considered if they are significant

© 2017 – The Treasury Academy - All Rights Reserved 93

32

Essential Learning for CTP CandidatesNY Cash Exchange 2017 – Session #CTP-10

Copyright © 2017 – The Treasury Academy, Inc.All Rights Reserved

Cost of Common Equity

Two sources of common equity◦ Retained earnings during the period

◦ Issue new common stock

CAPM may be used to estimate the market’s required rate of return on equity

Flotation costs are usually not considered for retained earnings, but may be significant for new common stock issues

© 2017 – The Treasury Academy - All Rights Reserved 94

Common Equity Calculation Example

Assume a risk-free rate of 4.0%, a return on the stock market of 10.0% and a Beta of 1.2

In this case the cost of equity is:

© 2017 – The Treasury Academy - All Rights Reserved 95

E RF M RFr r (r r )

= .04 + (.10 .04)(1.2) = .112 or 11.2%

Source: ETM5 - © AFP

Weighted Average Cost of Capital (WACC)

Assume 1/3 of total financing is from debt and 2/3 is from equity, and the costs of debt and equity are those found on previous slides:

© 2017 – The Treasury Academy - All Rights Reserved 96

D D E EWACC = W r (1 T) W r

D D E EWACC = W r (1 T) W r

[.333 0.05 (1 0.3)] (.667 0.112)

8.64%

Source: ETM5 - © AFP

33

Essential Learning for CTP CandidatesNY Cash Exchange 2017 – Session #CTP-10

Copyright © 2017 – The Treasury Academy, Inc.All Rights Reserved

Firm Value According to EVA (Economic

Value Added) concepts, a firm must earn a rate of return on assets that exceeds the cost of capital in order to create shareholder value

Assume a tax rate of 30%, $50M of capital employed and an operating profit of $6.8M

© 2017 – The Treasury Academy - All Rights Reserved 97

EVA = EBIT(1 Tax Rate) (WACC)(L-T Debt + Equity)

$6,800,000(1 .30) (.0864)($50,000,000)

$4,760,000 $4,320,000 $440,000

Source: ETM5 - © AFP

What to Do When the Panic Sets In!!!

Remember that one of the answers ISthe solution to the calculation

Don’t waste precious time, just come back to the question later

Try to narrow down your choices using a little common sense

When all else has failed, just take a guess – you might get lucky

© 2017 - The Treasury Academy, Inc. - All Rights Reserved 98

NY Cash Exchange – 2017: CTP TrackEssential Learning for CTP Candidates

End of This Track

Be sure to sign up for the on-line course available from The Treasury Academy

E-Mail: [email protected]: 850-293-1253

© 2017 - The Treasury Academy, Inc. - All Rights Reserved 99