establishing business in indiavijaysaini.in/wp-content/uploads/2018/02/ebook-establishing... ·...

TRANSCRIPT

1

[Typethedocumentsubtitle]|

EstablishingBusinessinIndia

Vijay Saini & Associates 104, Tower-1, Assotech Business Cresterra, Sector-135, Noida, Uttar Pradesh-201301, India Phone: +91-120-7195254 Email: [email protected] Website: www.vijaysaini.in

2

IntroductiontoVijaySaini&AssociatesVijaySaini&Associates(VSA)wasestablishedin1999asanauditingandconsultingfirm.Withacumulativeconsultingexperienceofover20years,ouraimistodelivercompletebusinesssolutionstobusinessentrepreneursbytakinguptheirchallengingprojectsandtransformingthemintoreality.

We are a one-stop solution firm engaged in a multidisciplinary practice.VSA has a team of highly qualified professionals comprising charteredaccountants,companysecretariesandadvocates.Takingfullresponsibility,right fromtheplanningstageto implementation,ourexpertprofessionalsdoanin-depthanalysissoastodeliverqualitativeratherthanquantitativeresults. Our services include business establishment and registration,corporate finance, raising corporate finance consultancy, finance andaccountsoutsourcing,researchandanalysis,managementconsultancyandmuchmore.

3

Index

IntroductiontoVijaySaini&Associates................................................................................................2

I. INDIAFACTFILE.............................................................................................................................4

II. ENTRYOPTIONS.............................................................................................................................5

OperatingasanIndianEntity............................................................................................................5

Operatingasaforeigncompany........................................................................................................5

III. FUNDINGOPTIONS....................................................................................................................6

IV. SIGNIFICANTEXCHANGECONTROLREGULATIONS...................................................................7

Currentaccounttransactions............................................................................................................8

Capitalaccounttransactions.............................................................................................................8

V. COMPANYFORMATIONININDIA–PRIVATELIMITED.................................................................10

Pre-registrationRequirements........................................................................................................10

NameApproval................................................................................................................................10

PreparationofDocuments..........................................................................................................10

PaymentofRoCfeesandstampduty..........................................................................................10

ObtainingCertificateofIncorporation........................................................................................10

VI. COMPANYFORMATION(PROCEDURE,TIME&COST):...........................................................11

VII. COMPLIANCEREQUIREMENTSFORCOMPANIESININDIA......................................................12

VIII. CORPORATETAXATIONININDIA.............................................................................................12

CorporateTaxRatesforFY2017-2018............................................................................................13

IX. INDIANTAXSTRUCTUREATAGLANCE(RELEVANTTOFY2017-2018)...................................14

DirectTaxes.................................................................................................................................14

IndirectTaxes...............................................................................................................................14

X. SPECIALECONOMICZONESININDIA...........................................................................................15

XI. BUSINESSANDEMPLOYMENTVISASCHEMESFORFOREIGNERSININDIA.............................16

BusinessVisa/‘B’Visa..................................................................................................................16

EmploymentVisa/‘E’Visa............................................................................................................16

XII. GUIDETOBUSINESSLICENSESININDIA..................................................................................17

XIII. GUIDETOEMPLOYMENTLAWSININDIA................................................................................18

Disclaimer............................................................................................................................................19

4

I. INDIAFACTFILE

GeographicProfile:Region SouthAsiaTimeZone 5hours30minutesaheadofGreenwichMeanTime(GMT)Capital NewDelhiLandArea 3.29millionsquarekmClimate Broadly,India’sclimatecanbeclassifiedastropicalmonsoon.The

countryhasfourseasons:summer(March-June),monsoon(June-September),post-monsoon(October–November)andwinter(December–February).

NaturalResources

Coal(fourth-largestreservesintheworld),manganese,bauxite,ironore,mica,chromite,diamond,limestone,titaniumore,naturalgas,petroleum,arableland.

Coastline 7,516.6kmincludingthemainland,theAndamanandNicobarIslands,andLakshadweep.

DemographicProfile:Population 1,210,193,422(2011CensusofIndia,GovernmentofIndia)

1,324,171,354(WorldPopulationProspects:The2017Revision,UnitedNationsDepartmentofEconomicandSocialAffairs)

Religions Hinduism,Islam,ChristianityandSikhismarethefourmajorreligionsfollowedinIndia.OtherreligionsincludeBuddhism,JainismandZoroastrianism.

Languages BusinesslanguageEnglish;22officiallyrecognizedlanguages(mostprominent:Hindi)

LiteracyRate

74%(Census2011)

LabourForce

487.6Million(2011CensusofIndia,GovernmentofIndia)

EconomicProfile:Currency IndianRupee(INR)GDP Growthrateof7.1%(2016-17)FDI FDIinflowstoIndiain2016-17were$60.1trillionGNIpercapita

6,490PPPIntl$

5

II. ENTRYOPTIONS

OperatingasanIndianEntitya. Wholly-owned subsidiary

companyA foreign company can set up awholly-owned subsidiary in India tocarry out business activities. Such asubsidiary is treated as an Indianresident.Atleasttwoshareholdersfora private limited company and sevenshareholders for a public limitedcompany are mandatory. In addition,there isalsotherequirementthat thedirectorshouldbeanIndianresident.Theactivitiesofsuchacompanyneedto comply with the provisions of theforeigndirectinvestment(FDI)policy.

b. Jointventure(JV)withanIndianpartner (equity participation)Although a wholly-owned subsidiaryis generally the preferred option inview of the associated brands andtechnologies involved, foreigncompanies also consider carrying outoperations in India by formingstrategic alliances with Indianpartners.Typically,foreigncompaniesidentify partners in the same area ofactivity, or those that can addsynergies to the foreign investor’sstrategic plans in India. Sometimes,JVs are necessitated due torestrictions on foreign ownership inselect sectors under the FDI policy.

c. Limited liability partnership(LLP)An LLP is a hybrid form of entitystructure in India. It combines theadvantages of a company, such asbeing a separate legal entity havingperpetual succession, along with thebenefits of organizational flexibilityassociatedwithapartnership.Atleasttwopartnersare required to formanLLP, and they have limited liability.With less stringent annual statutorycompliance requirements and ease of

set-up, maintenance and exit,compared to a company form, LLP isbecoming a preference. There is notaxondistributionofprofitsinanLLP,unlike in a company,where dividenddistribution tax or buy-back tax isapplicable.The setting up of an LLP requiresprior approval of the ForeignInvestment Promotion Board (FIPB).

Operatingasaforeigncompanya. Liaison offices (LOs)

Setting up an LO or representativeoffice is common practice for foreigncompaniesseekingtoentertheIndianmarket. The role of LOs is limited tocollecting information about themarket and providing informationaboutthecompanyanditsproductstoprospective Indian customers. Suchofficesactascommunicationchannelsbetween the foreign company and itsexisting or prospective Indiancustomers. An LO is not allowed toundertakeanythingotherthanliaisonactivities in India, and therefore,cannotearnanyincomeinthecountryunder the terms of approval grantedby the Reserve Bank of India (RBI).

b. Branch officesForeign companies engaged inmanufacturing and trading activitiesabroad can set up branch offices inIndiaforthefollowingpurposes,withRBI’spriorapproval:

• Exportandimportofgoods;• Professional or consultancy

services;• Research work in which the

parent company is engaged,promote technical or financialcollaboration between Indiancompanies and the parentcompany;

• Representing the parentcompanyinIndiaandactingasabuyingorsellingagentinIndia;

• Informationtechnology(IT)andsoftware development servicesinIndia;

6

• Technical support for productssuppliedbytheparentorgroupcompanies;

• Acting as a foreign airline orshipping company.

c. Project officesForeign companies planning toexecutespecificprojectsinIndiahavethe option of setting up temporaryprojectandsiteoffices.TheRBIgrantsgeneral permission to foreigncompanies for establishing projectoffices in India, provided they havesecured a contract from an Indiancompany or a project sanctioningauthority for executing the project,

and meet any of the followingconditions:

• Theprojectisfundeddirectlybyinwardremittancefromabroad;

• It is funded by a bilateral ormultilateral internationalfinancingagency;

• It has been cleared by anappropriateauthority;

• A company or entity in Indiaawarding the contract has beengranted a term loanby apublicfinancialinstitutionorabankinIndiafortheproject.

III. FUNDINGOPTIONS

a. Equity CapitalThe issue of equity shares by anIndian company to a foreign residentmustcomplywiththesectoralcapsasstatedintheforeigndirectinvestment(FDI) policy of the Government ofIndia.Partly paid equity shares andwarrants can also be issued by anIndian company to a foreign residentin accordance with the provisions ofthe FDI policy, Companies Act, 2013,and the Securities and ExchangeBoard of India (SEBI) guidelines, asmay be applicable.

b. Fully and compulsorilyconvertible preference sharesand debenturesIndian companies can also receiveforeign investment through the issueof fully and compulsorily convertiblepreference shares and debentures.The conversion formula or price forissue of equity shares upon

conversion must be determinedupfront at the time of their issue.

c. External commercial borrowings(ECBs)ECBs refers to commercial loans (intheformofbankloans,buyers’credit,suppliers’ credit, securitizedinstruments (e.g. floating rate notesand fixed rate bonds) obtained fromnon-resident lenders with minimumaverage maturity of three years ormore.ECBcanbeavailedofeitherundertheautomatic or the approval route.Eligibleborrowerssuchascorporatesin the industrial, infrastructure andservice sectors raise funds throughECBs for permissible end uses fromrecognized lenders. Under theapproval route, prior permission ofthe RBI is required for raising ECBs.

d. Pledge of sharesPromoters of an Indian company canpledge shares of the borrowingcompany or those of its associateresident companies to secure ECBs

7

raised by the borrowing company,provided that a no objection isobtained from the AD (AuthorizedDealer) bank and the prescribedconditions are met. A non-residentshareholderinanIndiancompanycanalsopledgeitsstakeinthecompanyinfavourofanADbankinIndiainorderto secure a credit facility extended tosuch an Indian company.

e. Global depository receipts(GDRs), American depositoryreceipts (ADRs) and foreigncurrency convertible bonds(FCCBs)Foreign investment through GDRs,ADRsandFCCBsisalsotreatedasFDI.Indian companies are permitted toraise capital in the internationalmarket through the issue of GDRs,ADRs and FCCBs, subject torestrictions.The issue of ADRs or GDRs does notrequire any prior approval (eitherfrom theMinistryof Finance, ForeignInvestment Promotion Board (FIPB)or RBI), except when the FDI after

such issue exceeds sectoral caps orpolicy requirements, in which caseprior approval fromFIPB is required.There are no end-use restrictions onADRs or GDRs, except for a ban ontheir deployment in the real estatebusiness or the stock market.

f. Foreign currency exchangeablebonds (FCEBs)FCEBsarebondsexpressedinforeigncurrency,theprincipalandinterestofwhichispayableinthesamecurrency.

AnFCEBis issuedbyacompanywhichispart of the promoter group of a listedcompany (offered company) and shallhold the equity share(s) being offered atthe time of the issuance of FCEB. Theoffered company should be engaged in asectoreligibletoreceiveFDI.TheFCEBissubscribedtobyapersonresidingoutsideIndia and is exchangeable into an equityshareoftheofferedcompanyonthebasisofanyequityrelatedwarrantsattachedtodebtinstruments.

IV. SIGNIFICANTEXCHANGECONTROLREGULATIONS

TheRBIhasdelegateditspowersrelatingtomonitoring and permitting remittancesunder the current account window toauthorized dealer (AD) banks (entitiesauthorizedby theRBI).All currentaccounttransactionsaregenerallypermittedunlessspecificallyprohibitedorrestricted.Transactions that alter the assets orliabilities, including contingent liabilities,outside India of a person residing in India,or assets or liabilities in India of a person

residing outside India, includingtransactions referredunderSection6(3)ofthe FEMA, are classified as capital accounttransactions.Transactionsother than theseare classified under current accounttransactions.The INR is fully convertible for currentaccount transactions, subject to a negativelist of transactions which are eitherprohibitedorwhich requirepriorapprovalof the central government or the ReserveBankofIndia(RBI).

8

CurrentaccounttransactionsTheRBIhasdelegateditspowersrelatingtomonitoring and permitting remittancesunder the current account window toauthorized dealer (AD) banks (entitiesauthorizedby theRBI).All currentaccounttransactionsaregenerallypermittedunlessspecificallyprohibitedorrestricted.As per the CAT Rules, drawl of foreignexchange for the following purposes isprohibited:

• Remittancesfromlotterywinnings;• Remittance of income from racing,

ridingoranysuchhobby;• Remittanceforthepurchaseoflottery

tickets, banned or proscribedmagazines, football pools,sweepstakes,etc.

• Payment of commission on exportsmade towards equity investments injoint ventures (JVs) or wholly-ownedsubsidiaries abroad of Indiancompanies;

• Remittance of dividend by anycompanytowhichtherequirementofdividendbalancingisapplicable;

• Payment of commission on exportsunder the rupee state credit route,except commission up to 10% of theinvoice value of exports of tea andtobacco;

• Paymentrelatedto‘call-backservices’oftelephones;

• Remittances of interest income offunds held in a non-resident specialrupee(account)scheme.

The CAT Rules further specify thosetransactions for which drawl of foreignexchange is permitted only with priorapproval of the government. However,governmentapproval isnot requiredwhenpayment is made out of funds held in theresident foreign currency account of theremitter.CapitalaccounttransactionsThe general principle for capital accounttransactions is that these are restrictedunlessspecificallyorgenerallypermittedbythe RBI, which has prescribed a list of

permitted capital account transactions forpersonsresidinginoroutsideIndia:

• Investment by a person residing inIndiainforeignsecurities;

• Investment in India by a personresidingoutsidethecountry;

• Borrowing or lending in foreignexchange;

• Depositsbetweenpersons residing inIndiaandthoseresidingoutsideIndia;

• Exportorimportofcurrency;• Transfer or acquisition of immovable

propertyinoroutsideIndia,etc.Under the LRS, resident individuals canremitup to250,000USDper financialyearfor any permitted capital accounttransaction. The permissible transactionsareasfollows:

• Opening of foreign currency accountoutsideIndia;

• Purchaseofpropertyabroad;• Makinginvestmentsabroad;• Settingupwholly-owned subsidiaries

andJVsabroad;• Extending loans including those in

INRtoNRIrelatives.For overseas investments in a JV or awholly-owned subsidiary, the limit offinancial commitmenthasbeen restored to400% (from 100% in 2013) of the networth of the Indian entity as on the lastaudited balance sheet date. However, anyfinancial commitment exceeding 1 billionUSD (or its equivalent) in a financial yearrequires RBI’s prior approval, even whenthetotalfinancialcommitmentoftheIndianparty is within the eligible limit under theautomaticroute(i.e.within400%ofthenetworthasperthelastauditedbalancesheet).Forthepurposeofsettingupofficesabroad,ADbanksmaypermit remittances towardsinitial expenses up to 15% of the averageannual salesor income,or turnoverduringthelasttwofinancialyears,orupto25%ofthe net worth, whichever is higher.However, for meeting recurring expenses,remittances up to 10% of the averageannual salesor income,or turnoverduringthelasttwofinancialyearsmaybemadefor

9

the purpose of normal business operationssubjecttothefollowingterms:

• The overseas branch or office hasbeen set up or a representative isposted overseas for conductingnormal business activities of theIndianentity.

• The overseas branch, office orrepresentativeshallnotenterintoanycontract or agreement incontravention of the act, rules orregulationsmade.

• The overseas office (trading or non-trading), branch or representativeshould not create any financialliabilities,contingentorotherwise,fortheheadofficeinIndia,andnotinvestsurplus funds abroad without RBI’sprior approval. Any funds renderedsurplusshouldberepatriatedtoIndia.

RepatriationofcapitalForeigncapitalinvestedinIndiaisgenerallyrepatriable,alongwithcapitalappreciation,if any, after the payment of taxes due,provided the investment was originallymadeonarepatriationbasis.AcquisitionofimmovablepropertyinIndiaForeign nationals of non-Indian originresidingoutside India arenotpermitted toacquire any immovable property in IndiaunlessitisinheritedfromapersonwhowasresidinginIndia.However,theycanacquire

ortransfer immovablepropertyinIndiaonleasenotexceedingfiveyearswithoutRBI’spriorpermission.Foreign companies that have beenpermittedtoopenabranchorprojectofficein India are allowed to acquire anyimmovable property in India which isnecessary for or incidental to carrying outsuch activity. In case of foreign companiesthat have beenpermitted to open a liaisonoffice (LO), property can be acquired bywayofleasenotexceedingfiveyears.Royaltiesandtechnicalknow-howfeesIndian companies can make paymentsagainst lump sum technology fees androyaltieswithoutanyrestrictionsundertheautomaticroute.RemittancesbybranchorprojectofficeNopriorapproval is required for remittingprofits earned by the Indian branches offoreign companies to their head officesoutside India. However, such remittance issubject to furnishing of prescribeddocuments to the satisfaction of the ADbankthroughwhichtheremittanceismade.Remittances of thewinding-upproceedsofa branch or liaison or project office of aforeign company in India are permitted,subject to furnishing of prescribeddocumentationtotheADbank.

10

V. COMPANYFORMATIONININDIA–PRIVATELIMITED

Pre-registrationRequirements• APrivateLimitedCompanymusthave

aPaid-upcapitalofINR100,000andaPublic Limited Companymust have apaid-upcapitalofINR500,000.

• APrivateLimitedCompanymusthaveaminimum of two directors and twoshareholders and Public LimitedCompany must have a minimum ofthree directors and sevenshareholders.

• The directors must have a validDirector IdentificationNumber (DIN),allotted by the Ministry of CorporateAffairs.

• At least two directors should have avalid Digital Signature Certificateissued by the Certifying Authorities(CA)andapprovedby theMinistryofCorporateAffairs.

NameApprovalThefirststepintheprocessofformationisthe application for MCA’s approval of thedesired name for the proposed company.Once, Company name is allotted, companyregistration documents are filed withrespectiveRoCforregistration.PreparationofDocumentsAfterobtainingnameapprovalfromtheRoCthefollowingformsmustbefiled/uploadedontheMCAwebsite:1. FormINC-7:Applicationof

Incorporationofthecompanya. Mandatoryattachmentstoe-

formINC7:i. MOA;ii. AOA;iii. Declarationbyprofessionals

inINC-8;

iv. AffidavitfromthesubscribertotheMemoranduminFormNo.INC-9;

v. Proofofresidentialaddresswhichshouldnotbeolderthan2months;

vi. Proofofidentity.b. Optionalattachmentsdepending

uponcase:i. Proofofnationalityincase

thesubscriberisaforeignnational;

ii. PANcardofsubscribersforIndiannationalitysubscribers.

2. FormINC-22:Noticeofsituationofregisteredofficea. Attachmentstoe-formINC-22:

i. Proofofregisteredofficeaddress;

ii. Copiesofutilitybills;iii. Certificationofe-formINC-

22byCS/CA/CWA(inwholetimepractice).

3. FormDIR-12:Providinginformationaboutparticularsofappointmentofdirectorsofthecompanyandkeymanagerialpersonnel.

PaymentofRoCfeesandstampdutyAfter filingofdocuments,weneed tomakepayment of RoC fees and stamp dutyelectronically which varies with theauthorizedcapitalofthecompany.ObtainingCertificateofIncorporationThe RoC will issue the digitally signedCertificate of Incorporation (only in theelectronic format) after careful review ofdocuments submitted. A private limitedcompanycanstartitsbusinessimmediatelyon receiving the Certificate ofIncorporation.

11

VI. COMPANYFORMATION(PROCEDURE&NORMALTIME)

No. Procedure CompletionTime1 Obtaindigitalsignaturecertificate(DSC) 1-2day2 Obtaindirectoridentificationnumber(DIN) 1-2days3 Reserve thecompanynamewith theRegistrarof

Companies(ROC)2-3days

4 File all incorporation forms and documents, paystamp duty, apply for PAN and TAN and obtainthecertificateofincorporation

3-7days

5 Make a common seal of the company and printmemorandumandarticlesofassociation

5-7day

6 Open bank account and deposit sharesubscription money by the subscriber(s) to thememorandumofassociation

7days

7* RegisterforGST 5days8* Registerforprofessiontax(ifapplicable) 2 days, simultaneously with

procedure79* Register with Employees’ Provident Fund (EPF)

Scheme(ifapplicable)12 days, simultaneously withprocedure7

10* Register with Employees’ State InsuranceCorporation(ESIC)(ifapplicable)

9 days, simultaneously withprocedure7

* Takes place simultaneously with another procedure Startingaforeigncompany:AnyforeigncompanycanestablishitsplaceofbusinessinIndiabyfillingForm44(Documentsdelivered for registration by a foreign company). The e-Form has to be digitally signed byauthorizedrepresentativeoftheforeigncompany.There is no need to apply and obtainDIN forDirectors of a foreign company butDSC of theauthorizedrepresentativesismandatory,whichagainisnotrequiredtoberegisteredonMCAApplication

12

VII. COMPLIANCEREQUIREMENTSFORCOMPANIESININDIA

The Companies Act, 2013 has elaborateprovisions relating to Governance ofCompanies, which deal with managementand administration of companies. Itcontains special provisionswith respect to

the annual compliance requirements.CompaniesincorporatedundertheActhaveto file various forms, returns anddocumentsundervarioussectionswith theRegistrar of Companies (RoC) in anelectronicmodewithintheprescribedtimealong with the prescribed fees or withpayment of additional fees in the event ofdelayedfiling.

VIII. CORPORATETAXATIONININDIA

For the purpose of taxation companies inIndia are broadly classified into domesticcompanies and foreign companies or inother words resident or non-resident.Basedontheirresidence,theyaresubjecttodifferenttaxtreatments.Companiesthatareregistered in India according to theCompaniesAct,2013oranyotherpreviouscompany law are deemed to be domesticcompanies, and companies whose chiefcontrolandmanagementarelocatedwhollywithin India are also known as domesticcompanies. A domestic companymaybe apublic companyor aprivate company. If acompany is not registered in India andmanagerialcontrolisexercisedonitfromaforeign country, it is treated as a foreigncompany.KeyProvisions:

• Adomestic/residentcompanyistaxedon:1. Anyincomewhichisreceivedor

is deemed to be received inIndia in the relevant PreviousYear by or on behalf of suchcompany;

2. Any income which accrues orarisesorisdeemedtoaccrueorarise in India during therelevantPreviousYear;

3. Any income which accrues orarises outside India during therelevantPreviousYear.

• A Foreign/non-resident company istaxedon:

1. Any income which isreceived or is deemed to bereceived in India during therelevantPreviousYearbyoronbehalfofsuchcompany;

2. Any income which accruesor arises or is deemed toaccrueorarise to it in Indiaduringtherelevantpreviousyear.

• A domestic/resident companywouldbesubjectedtoanadditionaltax called dividend tax on theamount of dividend declared,distributed or paid. Dividend tax ischarged on the company and notcharged on the hands of theshareholders.Suchtaxmustbepaidwithin 14 days of declaration ordistribution, whichever is earlier.Any deduction on account of suchtaxisnotallowedtothecompany.

• Companies with a total income ofmore than INR 10 million aresubjecttoasurchargeontheirtaxes.Domestic companies pay asurcharge of 5% as against foreigncompanies that pay a surcharge ofonly2%.

• Withholding tax is applicable onpayments made to foreigncompanies operating in Indiawithoutpermanentestablishment.

• Capital gains are subjected to tax.

13

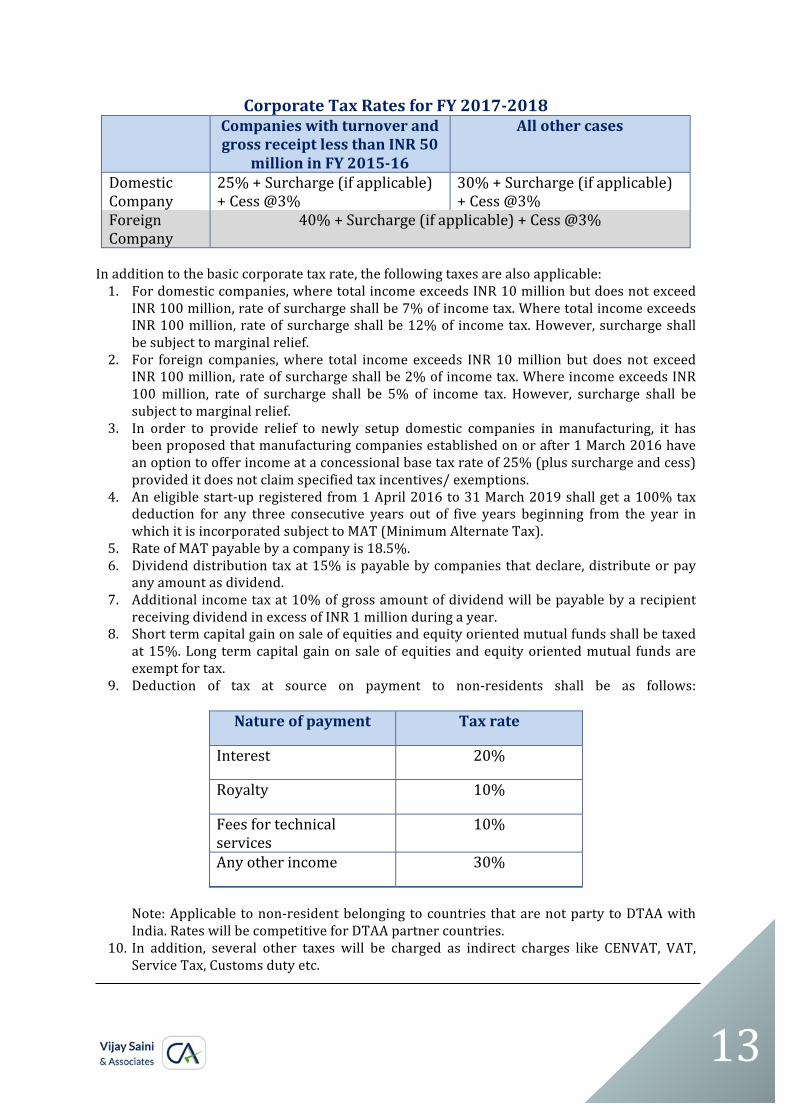

CorporateTaxRatesforFY2017-2018 Companieswithturnoverand

grossreceiptlessthanINR50millioninFY2015-16

Allothercases

DomesticCompany

25%+Surcharge(ifapplicable)+Cess@3%

30%+Surcharge(ifapplicable)+Cess@3%

ForeignCompany

40%+Surcharge(ifapplicable)+Cess@3%

Inadditiontothebasiccorporatetaxrate,thefollowingtaxesarealsoapplicable:1. Fordomesticcompanies,wheretotalincomeexceedsINR10millionbutdoesnotexceed

INR100million,rateofsurchargeshallbe7%ofincometax.WheretotalincomeexceedsINR100million,rateofsurchargeshallbe12%of incometax.However,surchargeshallbesubjecttomarginalrelief.

2. For foreign companies,where total incomeexceeds INR10millionbutdoesnot exceedINR100million,rateofsurchargeshallbe2%ofincometax.WhereincomeexceedsINR100million, rate of surcharge shall be 5% of income tax. However, surcharge shall besubjecttomarginalrelief.

3. In order to provide relief to newly setup domestic companies in manufacturing, it hasbeenproposedthatmanufacturingcompaniesestablishedonorafter1March2016haveanoptiontoofferincomeataconcessionalbasetaxrateof25%(plussurchargeandcess)provideditdoesnotclaimspecifiedtaxincentives/exemptions.

4. Aneligiblestart-upregisteredfrom1April2016to31March2019shallgeta100%taxdeduction for any three consecutive years out of five years beginning from the year inwhichitisincorporatedsubjecttoMAT(MinimumAlternateTax).

5. RateofMATpayablebyacompanyis18.5%.6. Dividenddistributiontaxat15%ispayablebycompaniesthatdeclare,distributeorpay

anyamountasdividend.7. Additionalincometaxat10%ofgrossamountofdividendwillbepayablebyarecipient

receivingdividendinexcessofINR1millionduringayear.8. Shorttermcapitalgainonsaleofequitiesandequityorientedmutualfundsshallbetaxed

at15%.Long termcapitalgainonsaleofequitiesandequityorientedmutual fundsareexemptfortax.

9. Deduction of tax at source on payment to non-residents shall be as follows:

Natureofpayment Taxrate

Interest 20%

Royalty 10%

Feesfortechnicalservices

10%

Anyotherincome 30%

Note:Applicable tonon-residentbelongingtocountries thatarenotpartytoDTAAwithIndia.RateswillbecompetitiveforDTAApartnercountries.

10. In addition, several other taxes will be charged as indirect charges like CENVAT, VAT,ServiceTax,Customsdutyetc.

14

IX. INDIANTAXSTRUCTUREATAGLANCE(RELEVANTTOFY2017-2018)

Direct Taxes IndividualIncomeTax&CorporateTaxThe provisions relating to income tax arecontained in the IncomeTaxAct,1961andthe Income Tax Rules, 1962. The IncomeTaxDepartment isgovernedbytheCentralBoardforDirectTaxes(CBDT)whichispartof the Department of Revenue under theMinistryofFinance.IntermsoftheIncomeTaxAct,1961,a taxon income is leviedonindividuals, corporations and body ofpersons. Tax rates are prescribed by thegovernment in the Finance Act, popularlyknownastheUnionBudget,everyyear.CapitalGainsTaxThecentralgovernmentalsochargestaxoncapital gains that are derived from sale ofassets. A capital gain is the differencebetween the money received from sellingtheassetandtheindexedcostoftheasset.SecuritiesTransactionTax(STT)Transactions in equity shares, derivativesand units of equity-oriented funds enteredin a recognized stock exchange attractsecurities transaction tax. Service tax,surcharge and education cess are notapplicableonSTT.Taxationofprofitorlossfrom securities transactions depends onwhether the activity of purchasing andsellingof shares/derivatives is classifiedasaninvestmentactivityorabusinessactivity.Treatment of STT also depends uponwhether the income from these securitiestransactions is included under the head‘Income from Capital Gains’ or ‘Profits andGainsofBusinessorProfession’.Indirect Taxes CustomsDutyCustoms duty in India falls under theCustomsAct, 1962 and CustomsTariff Act,1975. Customs duty is the tax levied ongoods imported into India as well as ongoods exported from India. Additionally,educational cess is also charged. Customsduty is evaluated on the value of the

transactionofthegoods.TheCentralBoardofExciseandCustomsundertheMinistryofFinancemanages thecustomsdutyprocessinthecountry.GoodsandServicesTaxGoods and Services Tax (GST) came intoeffect from 1 July 2017 through theimplementationofthe101stamendmentofthe Constitution of India. GST is acomprehensive, multi-stage, destination-based indirect tax levied on the supply ofgoodsandservices.TheintroductionofGSTremoved cascading effect of various taxesleviedbythecentralandstategovernmentsin thepreviousregime.The taxrates, rulesandregulationsaregovernedby theGoodsand Services Tax Council which comprisesof finance ministers ofcentreand all thestates. GST simplified a slew of indirecttaxes with a unified tax and is thereforeexpected to dramatically reshape thecountry's2trilliondollareconomy.StampDutyIt is a tax that is levied on the transactionperformed by means of a document orinstrumentasper theregulationsof IndianStamp Act, 1899. Stamp duty is paid oninstruments, which are essentiallydocumentstocreate,transfer, limit,extend,extinguish or record a right or liability. Adocument acquires legality once it isstampedproperly after the payment of therequisitestampdutycharges.Stampdutyispayable on transfer of shares, sharecertificates, partnership deeds, bills ofexchange, leave and license agreements,debentures, gift deeds, bank guarantees,bonds, demat shares, developmentagreements,demergers,powersofattorney,home loans, purchase of property, leasedeeds, loan agreements and leaseagreements.OtherState/LocalTaxesCertain indirect taxes which were notsubsumed byGST continue to be levied bythe state/local governments and aregovernedbytheirrespectiveActs,Rulesandrateswhichdifferfromstatetostate.Someofthesearetaxonalcoholicandpetroleumproducts, tax on sale and consumption ofelectricity, etc.

15

X. SPECIALECONOMICZONESININDIA

Special Economic Zone (SEZ) is aspecifically delineated duty-free enclaveandshallbedeemedtobeforeignterritoryfor the purposes of trade operations andduties and tariffs. In orderwords, SEZ is ageographicalregionthathaseconomiclawsdifferent fromacountry's typicaleconomiclawsThe Special Economic Zone (SEZ) policy inIndia first came into inception on April 1,2000. The prime objectivewas to enhanceforeign investment and provide aninternationally competitive and hassle freeenvironment for exports. The idea was topromote exports from the country andrealising the need that level playing fieldmust be made available to the domesticenterprises and manufacturers to becompetitiveglobally.The SEZ Act, 2005, provided the umbrellalegal framework, covering all importantlegal and regulatory aspects of SEZdevelopment aswell as for units operatinginSEZs.Businessunitsthatsetupestablishmentsinan SEZ would be entitled for a package ofincentives and a simplified operatingenvironment. Some of these are listedbelow.The incentives and facilities offered tothe units in SEZs for attractinginvestments into the SEZs, includingforeigninvestmentinclude:

• Duty free import/domesticprocurement of goods fordevelopment, operation andmaintenanceofSEZunits;

• 100% Income Tax exemption onexport income for SEZ units underSection10AAoftheIncomeTaxAct

for first 5 years, 50% for next 5years thereafter and 50% of theploughedbackexportprofitfornext5years;

• Exemptionfromminimumalternatetax under section 115JB of theIncomeTaxAct;

• External commercial borrowing bySEZunitsuptoUS$500millioninayear without any maturityrestriction through recognizedbankingchannels;

• ExemptionfromCentralSalesTax;• ExemptionfromServiceTax;• Singlewindowclearance forcentral

andstatelevelapprovals;• Exemption from state sales tax and

other levies as extended by therespectivestategovernments.

The major incentives and facilitiesavailabletoSEZdevelopersinclude:

• Exemption from custom/exciseduties for development of SEZs forauthorized operations approved bytheBOA;

• Income Tax exemption on incomederived from the business ofdevelopmentoftheSEZinablockof10 years in 15 years under Section80-IABoftheIncomeTaxAct;

• Exemptionfromminimumalternatetax under Section 115 JB of theIncomeTaxAct;

• Exemption from dividenddistributiontaxunderSection115OoftheIncomeTaxAct;

• Exemption from Central Sales Tax(CST);

• Exemption from Service Tax(Section7, 26 and Second Scheduleof the SEZ Act).

16

XI. BUSINESSANDEMPLOYMENTVISASCHEMESFORFOREIGNERSININDIA

Business Visa/‘B’ Visa EligibilityA business visa is given strictly to thosewho would like to make only businessrelatedtripstoIndiaDurationandvalidityA business visamay be valid for 1 year ormore with multiple validities (U.S. citizenscan get 5 years or 10 yearsmultiple-entryvisa). However, the period of stay in Indiafor each visit is limited to six months. Amultiple entry business visa valid for 10years may be available to foreignbusinessmenwhohavesetuporintendedtosetupjointventuresinIndia.The visa duration starts on the day ofissuance and not on the day of entry toIndia.VisaExtensionIf the business visa is granted for a periodlessthan5years,itcanbeextendeduptoamaximum period of 5 years subject tofollowing:

• The gross annual turnover from thebusiness activities, for which theforeignerhasbeengrantedthevisa,isnot less than INR 10 million (to beachieved within two years of settingupthebusiness.

• The first extension of the businessvisa shall be granted by Ministry ofHomeAffairs.

• Further extensions, if required, maybe granted by state governments/UTadministrations/FRRS/FROs on ayear-to-year basis subject to goodconduct, production of necessarydocuments in support of continuedbusiness activity and no adverseinputs, security related or otherwise,abouttheforeigner.

DocumentsrequiredThe documents required may varydepending on the High Commission or

Embassy processing it, therefore thefollowing is not an exhaustive list. Pleasecheck with the relevant processingauthority.1. Theforeignnationalmusthaveavalid

travel document and a re-entrypermit, if required, under the law ofthecountryconcerned.

2. Proofoffinancialstanding.3. Proof of expertise in the field of

intendedbusiness.4. Documents/papers pertaining to

proposedbusinessactivitysuchastheregistrationofthecompanyundertheCompanies Act, proof of registrationof the firm with the State IndustriesDepartment or the Export PromotionCouncil concerned or any recognizedpromotionalbodyintherelevantfieldofindustryortrade,etc.

Employment Visa/‘E’ Visa EligibilityAn employment visa is granted to anemployee or paid intern of an Indiancompany.DurationandValidityThe embassy may grant an employmentvisa,whichisvalidforayear,irrespectiveofthedurationofcontact.Furtherextensionofup to 5 years may be obtained fromMHA/FRROintheconcernedstateinIndia.The Visa duration starts on the day ofissuance and not on the day of entry toIndia.

• A foreign technician may get anemployment visa for a period of 5years or the duration of the bilateralagreement between India and theforeigngovernment,whicheverisless,withmultipleentries.

• ForhighlyqualifiedforeignpersonnelbeingemployedintheITsoftwareandITenabledsectors, thevalidity isof3years or the term of assignment,whichever is less with multipleentries.

• Otherscanbegrantedanemploymentvisa with a validity up to 2 years or

17

the term of assignment, whichever isless,withmultipleentries.

ForeignerRegistrationThosewithvisadurationof180daysorlessdo not require foreigner registration. Anemploymentvisavalid for180dayshasanendorsement indicatingthat the foreigner’sregistrationwiththeFRRO/FROisrequiredwithin14daysofarrival.For those whose registration is required,FRRO/FRO may issue a residential permitforthevalidityofvisaperiod.ExtensionThe employment visa can be extended bythe state governments/UTs/FRROs/FROsbeyondtheinitialvisavalidityperiod,uptoa total period of 5 years from the date ofissue of initial employment visa, on anannual basis, subject to good conduct,production of necessary documents insupport of continued employment, filing ofIncome Tax Returns and no adversesecurityinputsabouttheforeigner.

DocumentsRequiredThe documents required may varydepending on the High Commission orEmbassy processing it. Therefore thefollowing is not an exhaustive list. Pleasecheck with the relevant processingauthority.1. Valid travel document and a re-entry

permit, if required under the law ofthecountryconcerned.

2. Proof of employment of contract orengagement by the company /organization,etc.inIndia.

3. Documentary proof of educationalqualifications and professionalexpertise.

4. Documents/ papers pertaining to theproposed employment, like theregistrationofthecompanyundertheCompanies Act, proof of registrationof the firm in the State IndustriesDepartment or the Export PromotionCouncil concerned, or any recognizedpromotional body in the field ofindustryandtradeetc.

5. Undertaking in theprescribed formatfromtheconcernedcompany

XII. GUIDETOBUSINESSLICENSESININDIA

The existence of several enforcement andregulatory authorities, at central, state andlocals levels, governing a business entityrequires quite a number of licenses andapprovals to be obtained beforecommencing operations. The licenses andpermits are required besides other basicregistrations such as registration for PAN,VAT,TAN,ESI,PF,etc.Anon-exhaustivelistoftheimportantlicensesisgivenbelow.IndustrialLicenseIndustrial licenses areregulated under theIndustries Development Regulation Act,1951.IndustriallicensesaregrantedbytheSecretarialofIndustrialAssistance(SIA)onthe recommendation of the Licensing

Committee. Presently, Industrial Licensingformanufacturingisrequiredincaseof:

• Industries under compulsorylicensing;

• Manufacture of item reserved for(Small Scale Industries) SSI sector bynonSSIunits;

• Projects affected by locationrestrictions.

EnvironmentalClearanceFactoryLicenseShopsandEstablishmentLicenseImportLicenseExportLicenseImportExportCode(IEC)CentralExciseLicenseStateExciseLicenseTradeLicenseOtherLicenses

18

XIII. GUIDETOEMPLOYMENTLAWSININDIA

Ministry of Labour and Employment isresponsible for formulation andadministrationof the rules and regulationsand laws relating to labour andemployment. Familiarizing with theemployment laws and regulations will beimmenselyuseful fora foreignersettingupanenterpriseinIndia.Thefollowingarticleis a bird’s-eye view of some of theimportant employment laws thatwill beofsignificancetoemployersandemployees.LawsRelatingtoWorkingConditions

• FactoriesAct,1948• MinesAct,1972• Dock Workers (Safety, Health &

Welfare)Act,1986LawsRelatingtoIndustrialRelations

• IndustrialDisputesAct,1947(IDA)• TradeUnionsAct,1926(TUA)

• The IndustrialEmployment (StandingOrders)Act,1946

LawsRelatingtoWages&Benefits

• MinimumWagesAct,1948• PaymentofBonusAct,1965• PaymentofWagesAct,1936

LawsRelatingtoSocialSecurity

• Employees’ Provident Fund andMiscellaneous Provisions Act, 1952(EPFMPA)

• Employees State Insurance Act, 1948(ESI)

• Workmen’sCompensationAct,1923• MaternityBenefitAct,1961• The Payment of Gratuity Act, 1972

(PGA)OtherLaws

• ShopsandEstablishmentsAct• The Contract Labour (Regulation and

Abolition)Act,1970

19

DisclaimerAll information presented in “Establishing Business in India”, is fromgovernmentandotherpublic sourcesavailableasof January2018.Whileeffortshavebeenmadetoavoiderrorsoromissionsinthispublication,anymistake, error or discrepancy notedmay be brought to the notice of ouroffice.Detailedadviceshouldbeobtainedbeforetakingactionorrefrainingfromtakingaction,asaresultof the information inthispublication.VijaySaini&Associatesshallnotbeheldresponsible foranydamageor lossofactiontoanyone,ofanykind,inanymannertherefrom.ItisthereforestronglyrecommendedthatpotentialinvestorscontactVijaySaini&Associatestoobtainthemostrecent informationandprofessionaladvicerelatedtoestablishingabusinessinIndia.

20

Vijay Saini & Associates 104, Tower-1, Assotech Business Cresterra, Sector-135, Noida, Uttar Pradesh-201301, India Phone: +91-120-7195254 Email: [email protected] Website: www.vijaysaini.in