estate planning basics and advanced directives-09-15

TRANSCRIPT

Estate Planning Basics and Advance Directives

https://learn.extension.org/events/2149#.VZ6EW03bKM8

Barbara O’Neill, Ph.D., CFP® Rutgers Cooperative Extension

Webinar Objectives Define and discuss estate planning

Define and discuss probate

Discuss the advantages and limitations of wills

Define and discuss trusts

Define and discuss estate taxes

Discuss estate planning resources

Estate Planning is Related to Many Other Financial

Planning Decisions Source: Madura, J. Personal Finance (2004), Pearson Education

So What Exactly is Estate Planning?

• Estate planning is the process of determining the distribution of your assets upon your death

• Estate planning also covers the management of your personal affairs in the event of incapacity

In Other Words… • You give what you have

• To whom you want

• When you want

• The way that you want

• At the lowest possible cost (e.g., taxes and administrative costs) to yourself and loved ones

• And have instructions left to make medical and financial decisions if you are unable to do so

Estate Planning Phases 1. Accumulation: Build estate through earnings,

savings, investments, insurance, gifts, etc.

2. Distribution: Ensure that your estate is distributed as you wish after your death – Make sure important documents are accessible,

understandable, and legally proper

Nobody knows how long their accumulation phase will last and when their distribution phase will begin!

When Should You Plan Your Estate?

Today Mental

Incapacity Catastrophic

Illness Death

Your Planning Opportunity

Revocable Living Trust

Will Living Will

Powers of Attorney

Irrevocable Trust

Source: Goldberg Law Center, PC

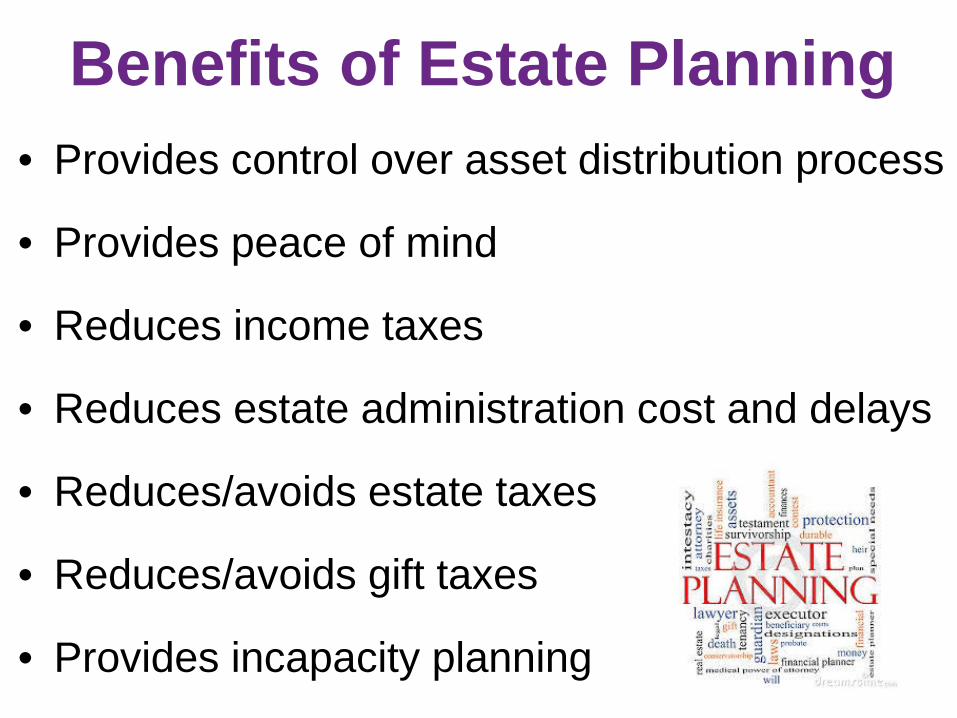

Benefits of Estate Planning • Provides control over asset distribution process

• Provides peace of mind

• Reduces income taxes

• Reduces estate administration cost and delays

• Reduces/avoids estate taxes

• Reduces/avoids gift taxes

• Provides incapacity planning

The Perfect Estate Plan • Documents that are properly drafted

• Documents that are regularly updated

• Assets that are properly titled

• No conflicts between titles to assets and a will

• Communication of wishes among family

• Regularly reviewed beneficiary designations: http://njaes.rutgers.edu/money/pdfs/beneficiary-designations.pdf

What is Included in an Estate? Assets Included in definition of “Estate”

• Real property

• Life insurance policies (face value)

• Checking, savings, CDs, other liquid accounts

• Business Interests – Sole Proprietor/Corporation/ LLC/ Partnership

• Stocks, bonds, mutual funds, annuities

• Retirement and pension plans

• Personal property

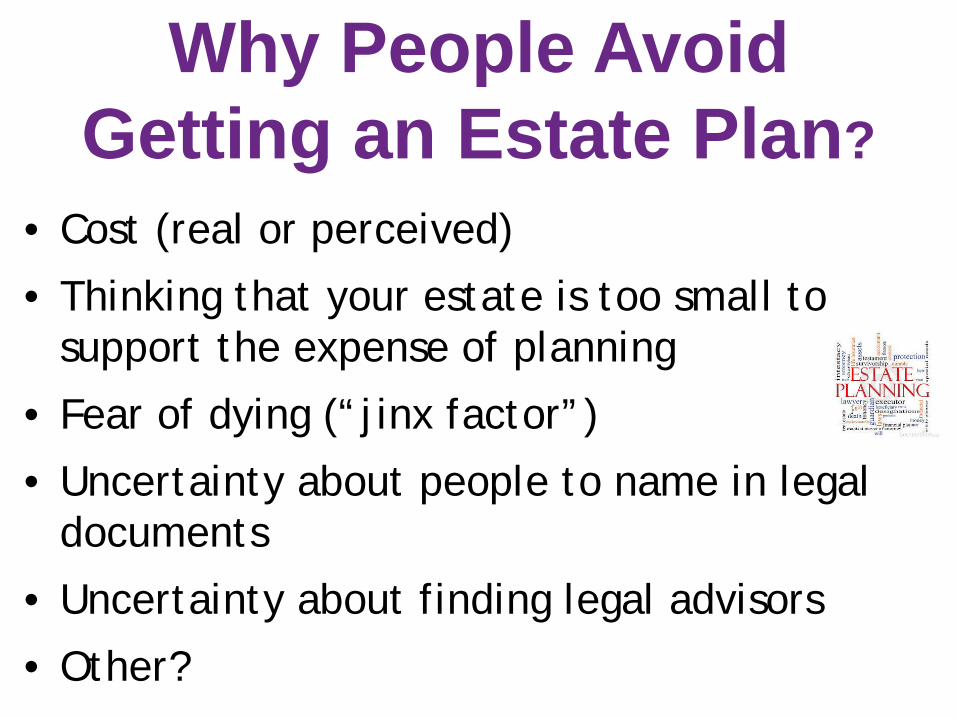

Why People Avoid Getting an Estate Plan?

• Cost (real or perceived)

• Thinking that your estate is too small to support the expense of planning

• Fear of dying (“jinx factor”)

• Uncertainty about people to name in legal documents

• Uncertainty about finding legal advisors

• Other?

Estate Planning Process

Gross Estate

Your Will

Non-probate transfers

Jointly owned property Life Insurance IRAs 401(k)s, 403(b)s, TSP Annuities Assets with named beneficiaries Planned distributions

Property titled in your name

Probate Process

Adapted From: Goldberg Law Center, PC

Probate Process • Legal process by which a will is proved valid or invalid and

the estate of a decedent is administered

• Involves paying a deceased person’s debts and retitling that person’s individually owned assets to the names of heirs listed in a will

• Executor files forms in probate court, provides a copy of the will, prepares a list of assets and liabilities of deceased, pays debts and sells necessary assets

• Typically opens a bank account for this purpose

Resource: http://definitions.uslegal.com/p/probate/

Ways to Avoid Probate • Own property jointly with survivorship rights

• Beneficiary designations (insurance policies, IRA, 401(k), etc.)

• Use a revocable or irrevocable trust

• Make lifetime gifts

Note: It is often difficult to totally avoid probate: automobile and pro-rated refund payments often need to be probated

How to Distribute Assets to Heirs

• Outright – No protection

• In Trust – Creditor protection

– Estate tax protection

– Self protection (e.g., spendthrift heirs)

– Predator protection

Common Estate Planning Tools During Your Lifetime

• Power of Attorney

• Gifting

• Revocable Living Trust

• Guardianship (encompasses all personal affairs of protected person including support and health care)

• Conservatorship (limited to the management of property and financial affairs of protected person)

Common Estate Planning Tools After Your Death

• Will

• State Intestacy Laws

• Joint Tenancy

• Beneficiary Designations

• Revocable Living Trust

Preparing a Will • Specifies how your estate should be distributed upon

your death

• If can also identify a preferred guardian for surviving minor children

• Have an attorney draft your will to avoid difficulties

• A standard simple will generally cost between $300 to $500

Will Formats • Holographic Will

– Will that you write, date and sign, entirely in your handwriting

– May not be recognized in some states

• Formal Will – Usually prepared with an attorney’s assistance

– Must date, sign, and have proper witnesses

• Statutory Will – A type of formal will on a preprinted form

– Available online or from a stationery store

– May include “boilerplate” provisions not in the best interest of heirs

Key Designees in a Will Executor: Person willing and able to execute provisions of

someone’s will (can be family member, friend, lawyer, etc.) Tasks may include: • Preparing an inventory of assets

• Collecting any money due and paying off debts

• File all income and estate tax returns

• Decisions about investing or selling assets to pay debts or provide income

• Distribute the estate and make financial accounting to beneficiaries

Guardian: Person who assumes responsibility for providing personal care to the minor children of a deceased person and/or managing the estate for them

• Reasons to Review a Will: – You move to a new state with different laws – You have sold property mentioned in the will – Size and composition of your estate has changed – You have married, divorced or remarried – Potential heirs are born or have died

• Adding a Codicil – Document that explains, adds, or deletes

provisions in an existing will – Appropriate for minor revisions

Altering or Rewriting a Will

Requirements for Preparing a Will

• Attain legal age of majority: Age 18 in most states • Mentally competent • Not under undue influence of others • Must be signed and dated; video will supplement?

• 2 or 3 witnesses who are not beneficiaries (in most states)

• Preparation by an attorney highly recommended Resources: http://www.lectlaw.com/filesh/qfl06.htm

http://nationalparalegal.edu/willsTrustsEstates_Public/ExecutionValidityComponentsOfWills/StatutoryRequirementsForWill.asp

Sample Will Language

Exhibit 20.1: A Sample Will Source: Madura, J. Personal Finance (2004), Pearson Education

Sample Will Language

Exhibit 20.1: A Sample Will Source: Madura, J. Personal Finance (2004), Pearson Education

Wills Can Fall Short of Estate Planning Goals

• Won’t provide for disability or incapacity

• Won’t necessarily transfer what you have: – to whom you want

– the way you want

– when you want

• Won’t avoid the probate process Adapted From: Goldberg Law Center, PC

Advanced Estate Planning Tools

• Gifting programs

• Charitable trusts (lead trust, remainder trust)

• Other irrevocable trusts

• Special needs trusts

• Life insurance trusts

• Trusts for minor children Adapted From: Goldberg Law Center, PC

Will vs. Revocable Living Trust

Probate

My Property

Heirs

Property in My Living

Trust

(No Probate)

Heirs

Adapted From: Daniela Lungu, Attorney at Law

Trusts Legal document that transfers assets to manage for designated beneficiaries; fee usually based on AUM

• Grantor (Trustor): Person who creates a trust

• Trustee: Person (e.g., family member, friend, lawyer) or financial institution (e.g., commercial bank) named in a trust to manage trust assets for beneficiaries

• Beneficiary: Person(s) who receive the benefits of a trust (e.g., income and assets)

Types of Trusts Living Trust (a.k.a., “Inter vivos trust”)

A trust to which someone assigns the management of their assets to a trustee while they are living

• Revocable Living Trust: A living trust that can be dissolved

• Irrevocable Living Trust: A living trust that cannot be changed, although it can provide income to the grantor

Testamentary Trust • Established by your will; takes effect after death

http://www.americanbar.org/content/dam/aba/migrated/publiced/practical/books/wills/chapter_5.authcheckdam.pdf

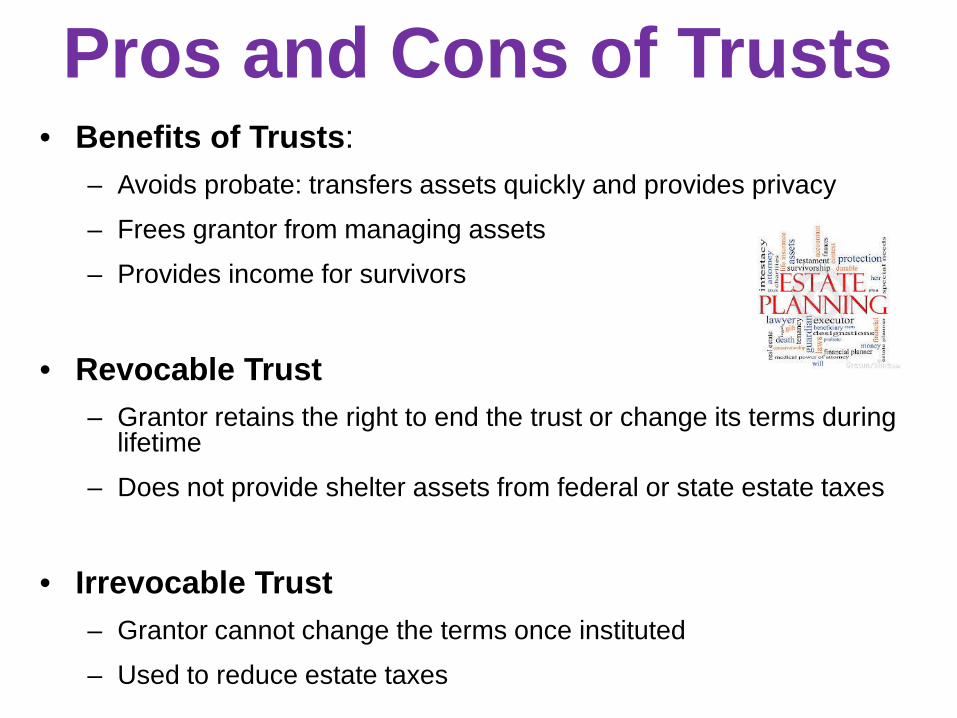

Pros and Cons of Trusts • Benefits of Trusts:

– Avoids probate: transfers assets quickly and provides privacy

– Frees grantor from managing assets

– Provides income for survivors

• Revocable Trust – Grantor retains the right to end the trust or change its terms during

lifetime

– Does not provide shelter assets from federal or state estate taxes

• Irrevocable Trust – Grantor cannot change the terms once instituted

– Used to reduce estate taxes

What if You Do Nothing? • At Incapacity (e.g., brain dead on life support)

– Guardianship/Conservatorship – Court controls assets

• At Death – Court proceeding to determine who will be guardian for minor children – Assets distributed according to state law – intestacy

Failure to Do Advanced Planning for Larger Estates: – Family money goes to taxes and legal expenses instead of to heirs – Kids blow inheritance – Control issues and fighting among family members left behind

Adapted From: Daniela Lungu, Attorney at Law

Intestacy: What Happens? • You die without a will • The state distributes your assets according to a pre-

determined formula (“My State Will”) – Typically splits property between surviving spouse, children – http://www.mystatewill.com/statutes/statute_links.htm

• May mean the state will decide on a guardian for your children – Very complicated if a “blended” family

• Generally takes longer to settle an estate and costs more (e.g., bonding an appointed administrator)

http://www.nolo.com/legal-encyclopedia/how-estate-settled-if-theres-32442.html

Celebrity Estate Planning Horror Stories

• Jerry Garcia of the Grateful Dead band • Elvis • Anna Nicole Smith • Chief Justice Warren Burger • Casey Kasem • Tom Clancy http://wfplaw.com/law-news/estate-planning/celebrity-estate-planning-horror-stories.html

http://www.clearcounsel.com/estate-planning-horror-stories/

http://trialandheirs.com/blog/celebrities/top-10-celebrity-stories-spark-holiday-estate-planning-conversations

Taxes And Estate Planning • Estate Taxes (Federal and Some States)

– Tax on value of property at death – Based on fair market value of estate assets (minus estate liabilities) – $5,430,000 federal estate tax exclusion in 2015 – Maximum federal estate tax rate: 40% (taxable estates > $1 million)

• Estate and Trust Income Taxes – Estates and certain trusts must file tax returns

• Inheritance Taxes – Tax on property left by a person in their will – Imposed by states: http://www.forbes.com/sites/ashleaebeling/2014/09/11/where-not-to-die-in-2015/

– Tax rate generally based on heirs’ relationship to the deceased

• Gift Taxes – Tax on gifts given by one person to another in a single year – Imposed by Federal government and two states (MN and CT) – $14,000 annual federal gift tax exclusion in 2015; inflation indexed

More About Estate Taxes • It is important for affluent households to calculate the

value of their estate periodically to plan appropriately if net worth exceeds the estate tax exclusion – Federal estate tax affects only about 0.12% of estates

• May want to consider state estate taxes in retirement housing decisions

• Portability of federal estate tax exemption between married couples is permanent (for now)

http://wills.about.com/od/2015-Estate-Tax-Rules/fl/Overview-of-2015-Estate-Tax-Gift-Tax-amp-Generation-Skipping-Transfer-Tax-Laws.htm

http://blogs.wsj.com/totalreturn/2014/10/30/estate-tax-exemption-for-2015-announced-by-irs/

Timing is Everything! Scenario #1

$20,000 Original Basis $180,000 Current Value $160,000 Appreciation If you gift house DURING your lifetime, the recipient is obligated to pay capital gains tax on the full appreciated value

Scenario #2

Source: David Ennis, Esq.

$20,000 Original Basis $180,000 Current Value $160,000 Appreciation If you gift house through a will or trust, the recipient is ONLY obligated to pay capital gains tax on any appreciated value that occurs AFTER your death (theoretically $0)

Advance Directives Broad Definition Instructions about a person’s wishes, goals, and values regarding what will be done in case he or she become incapable of making decisions

Three Common Documents: • Living Will: Specifies desired medical treatment

• Health Care Proxy (Durable Power of Attorney for Health Care): Designates person to make health care decisions

• Durable Power of Attorney: Designates person to make financial transactions (e.g., pay bills, make deposits, sign checks)

More About Advance Directives

• Power of Attorney authorizes someone to legally act on someone’s until the creator revokes it or dies

• Estate planning and advance directive documents need to be kept in safe, convenient places (copy with your attorney) – Original: Safe deposit box (with photocopies at home), desk drawer or

file cabinet at home (fire resistant), wrapped in plastic in freezer?

– Back-Up Copies: Cloud storage, scanned files on flash drive, family

• Key individuals need to know where documents are kept! http://www.silvesterlaw.com/index.php?option=com_content&view=article&id=59:where-should-i-keep-my-estate-planning-documents&catid=14:trust-housekeeping&Itemid=14

http://wills.about.com/od/preparingtodraftaplan/a/storedocuments.htm

Living Wills • Allows you to specify whether or not to be kept on

artificial life support • “Do Not Resuscitate” (DNR) orders; feeding tubes

• Guide choices for doctors and caregivers when someone is seriously injured or near end of life

• Avoids unnecessary suffering by patient • Relieves caregivers of decision-making burdens • Reduces disagreement among family members • Not just for older adults! http://www.mayoclinic.org/healthy-lifestyle/consumer-health/in-depth/living-wills/art-20046303

Letter of Last Instruction • Not legally binding

• Provides heirs with valuable information

• Could include:

– Funeral/memorial service preferences

– Names of people to be notified of your death

– Location of bank accounts, safe deposit box, etc.

– Disposition of personal effects (untitled property)

Resource: Who Gets Grandma’s Yellow Pie Plate? http://www.extension.umn.edu/family/personal-finance/who-gets-grandmas-yellow-pie-plate/

Digital Assets • Personal information that is stored electronically on

either a computer or online “cloud” server account • Often provide access to financial assets • Generally require a username and/or password or

PIN to access and can be difficult or impossible to retrieve if someone is incapacitated or passes away

Resources: http://www.extension.org/pages/72624/dou-you-know-your-digital-assets#.VZ_4Wk3bKM8 (eXtension article)

http://njaes.rutgers.edu/money/pdfs/Digital-Assets-Worksheet.pdf (Digital Assets Inventory worksheet)

Estate Planning Resources • Prepare Your Estate Plan (eXtension): http://www.extension.org/pages/15749/prepare-your-estate-plan#.VZ_7k03bKM9

http://www.extension.org/pages/15800/prepare-your-estate-plan:-print-this-lesson#.VZ_8iE3bKM8 • Money Talk: A Financial Guide for Women, Session

V, Planning for Future Life Events (Rutgers Cooperative Extension): http://njaes.rutgers.edu/money/pdfs/session-v.pdf

Estate Planning Resources • Getting Ready for Estate Planning (Purdue

University): https://ag.purdue.edu/programs/areyouprepared/readyestate/Pages/default.aspx

• Estate Planning (North Carolina State University Extension): http://forestry.ces.ncsu.edu/estate-planning/

• Annual Limits Relating to Financial Planning (College for Financial Planning): http://www.cffpinfo.com/annual-limits/

Key Take-Aways • Estate planning is not just for the wealthy

– Even simple estates need plans; no magic number

• Incapacity can strike at any time

– Failing to plan means court will appoint a guardian

• Health Care PoA and Durable PoA designate an agent to act on your behalf

• Wills must be property signed and witnessed

• Intestacy cases distribute assets according to state law

• Executor is personally responsible to pay debts and distribute property

Key Take-Away Applications • Prepare or review your estate plan; look for gaps

• Have documents in place to address potential incapacity

• Review your PoA designees and discuss your wishes with them (never “surprise” people with key roles after you die!)

• Review your will periodically and revise when needed

• Don’t die intestate!

• Prepare a letter of last instructions and digital assets inventory

• Think carefully about choosing to be an executor or performing executor duties