estate planning with education trusts and 529...

TRANSCRIPT

Estate Planning with Education Trusts and 529 Plans Establishing Education Trusts for Tax Savings, Drafting Education Provisions in Revocable Trusts, and Incorporating 529 Plans

Today’s faculty features:

1pm Eastern | 12pm Central | 11am Mountain | 10am Pacific

The audio portion of the conference may be accessed via the telephone or by using your computer's

speakers. Please refer to the instructions emailed to registrants for additional information. If you

have any questions, please contact Customer Service at 1-800-926-7926 ext. 10.

WEDNESDAY, JANUARY 9, 2013

Presenting a live 90-minute webinar with interactive Q&A

Gregory Herman-Giddens, President, TrustCounsel, Chapel Hill, N.C.

Robert Deschene, Attorney, Deschene Law Office, North Attleborough, Mass.

Sound Quality

If you are listening via your computer speakers, please note that the quality of

your sound will vary depending on the speed and quality of your internet

connection.

If the sound quality is not satisfactory and you are listening via your computer

speakers, you may listen via the phone: dial 1-866-961-9091 and enter your PIN

when prompted. Otherwise, please send us a chat or e-mail

[email protected] immediately so we can address the problem.

If you dialed in and have any difficulties during the call, press *0 for assistance.

Viewing Quality

To maximize your screen, press the F11 key on your keyboard. To exit full screen,

press the F11 key again.

For CLE purposes, please let us know how many people are listening at your

location by completing each of the following steps:

• In the chat box, type (1) your company name and (2) the number of

attendees at your location

• Click the SEND button beside the box

FOR LIVE EVENT ONLY

If you have not printed the conference materials for this program, please

complete the following steps:

• Click on the + sign next to “Conference Materials” in the middle of the left-

hand column on your screen.

• Click on the tab labeled “Handouts” that appears, and there you will see a

PDF of the slides for today's program.

• Double click on the PDF and a separate page will open.

• Print the slides by clicking on the printer icon.

Estate Planning with Education Trusts and 529 Plans

January 9, 2013

Robert Deschene, Attorney at Law

Massachusetts ▪ Rhode Island 508-316-3853 800-347-1097

[email protected] www.deschenelaw.com

95 Church Street ♦ North Attleborough MA 02760

Material in this PowerPoint is drawn from Incorporating Education Trusts and 529 Plans in in Estate Plans, by Gregory Herman-Giddens © 2013. Used with permission for educational purposes. All rights reserved.

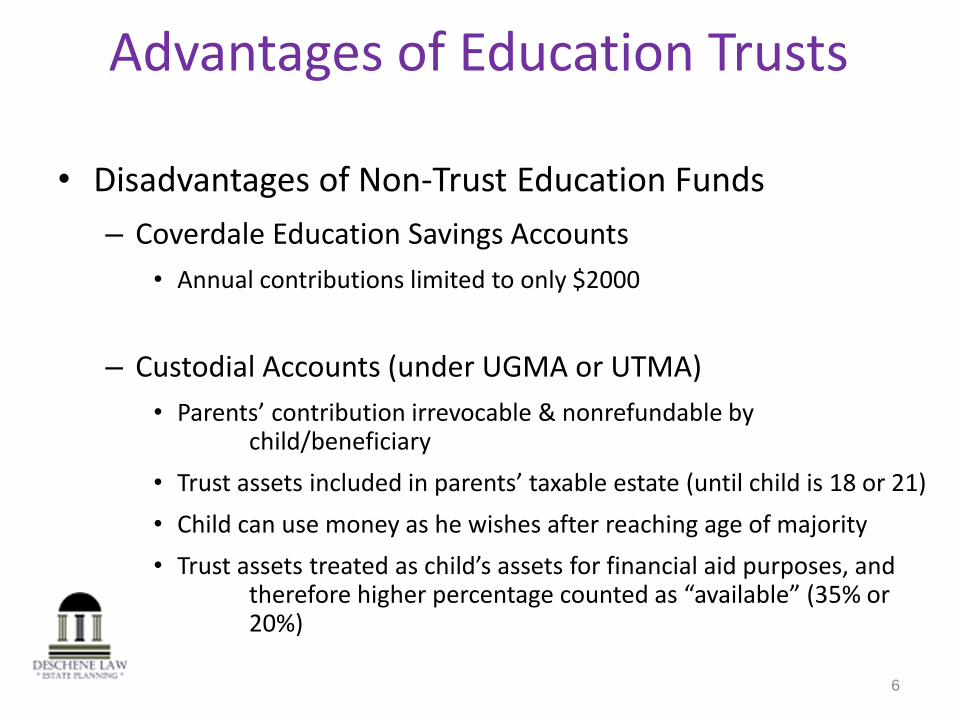

Advantages of Education Trusts

• Disadvantages of Non-Trust Education Funds

– Coverdale Education Savings Accounts

• Annual contributions limited to only $2000

– Custodial Accounts (under UGMA or UTMA)

• Parents’ contribution irrevocable & nonrefundable by child/beneficiary

• Trust assets included in parents’ taxable estate (until child is 18 or 21)

• Child can use money as he wishes after reaching age of majority

• Trust assets treated as child’s assets for financial aid purposes, and therefore higher percentage counted as “available” (35% or 20%)

6 6

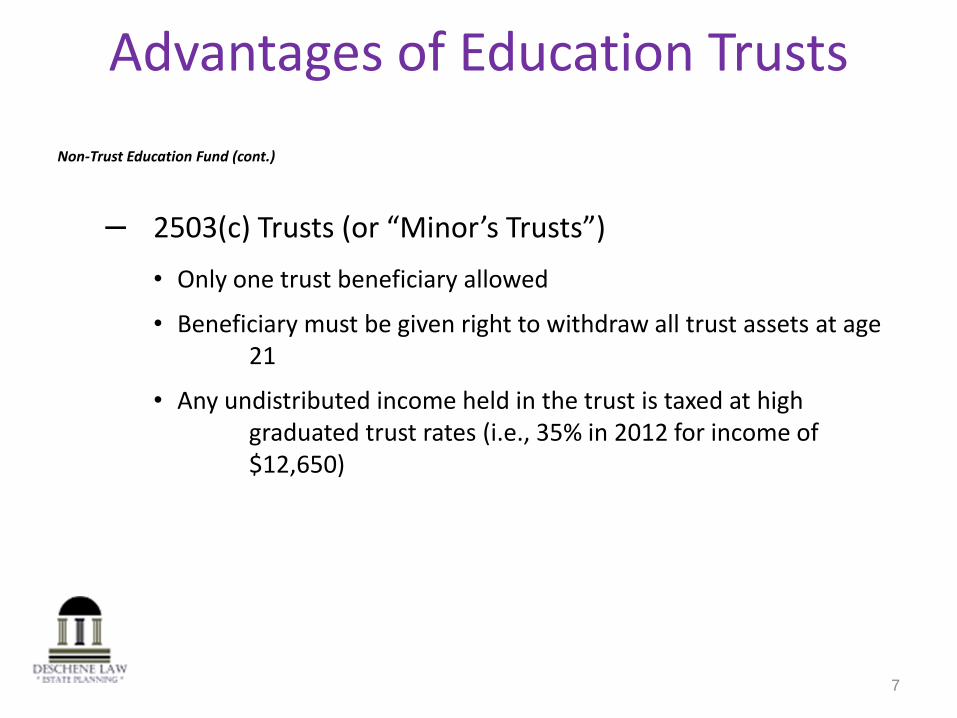

Advantages of Education Trusts

Non-Trust Education Fund (cont.)

– 2503(c) Trusts (or “Minor’s Trusts”)

• Only one trust beneficiary allowed

• Beneficiary must be given right to withdraw all trust assets at age 21

• Any undistributed income held in the trust is taxed at high graduated trust rates (i.e., 35% in 2012 for income of $12,650)

7 7

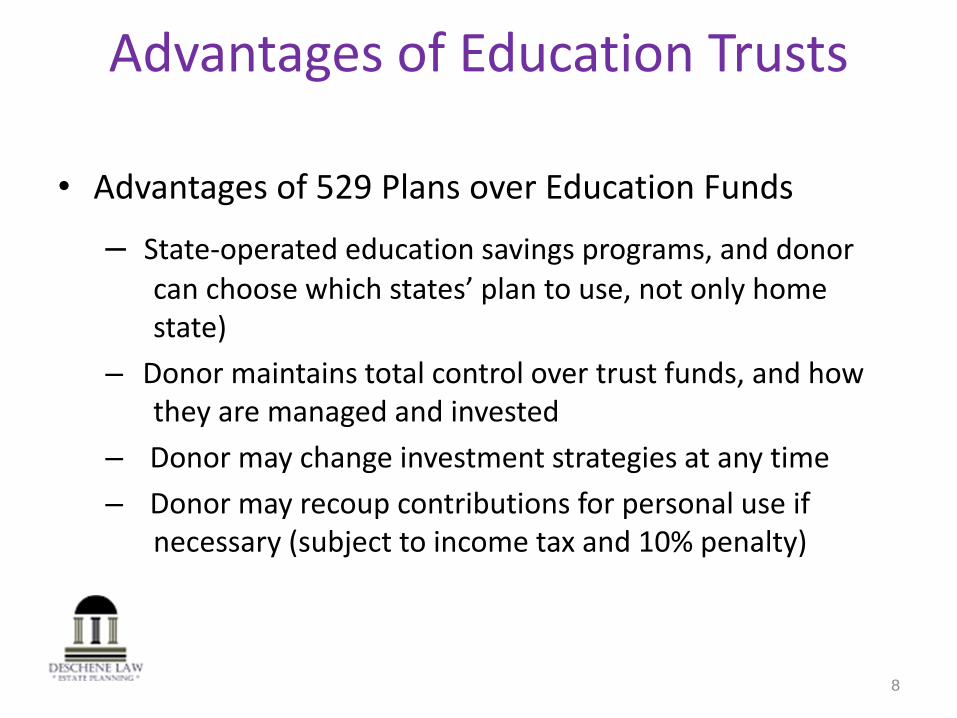

Advantages of Education Trusts

• Advantages of 529 Plans over Education Funds

– State-operated education savings programs, and donor can choose which states’ plan to use, not only home state)

– Donor maintains total control over trust funds, and how they are managed and invested

– Donor may change investment strategies at any time

– Donor may recoup contributions for personal use if necessary (subject to income tax and 10% penalty)

8 8

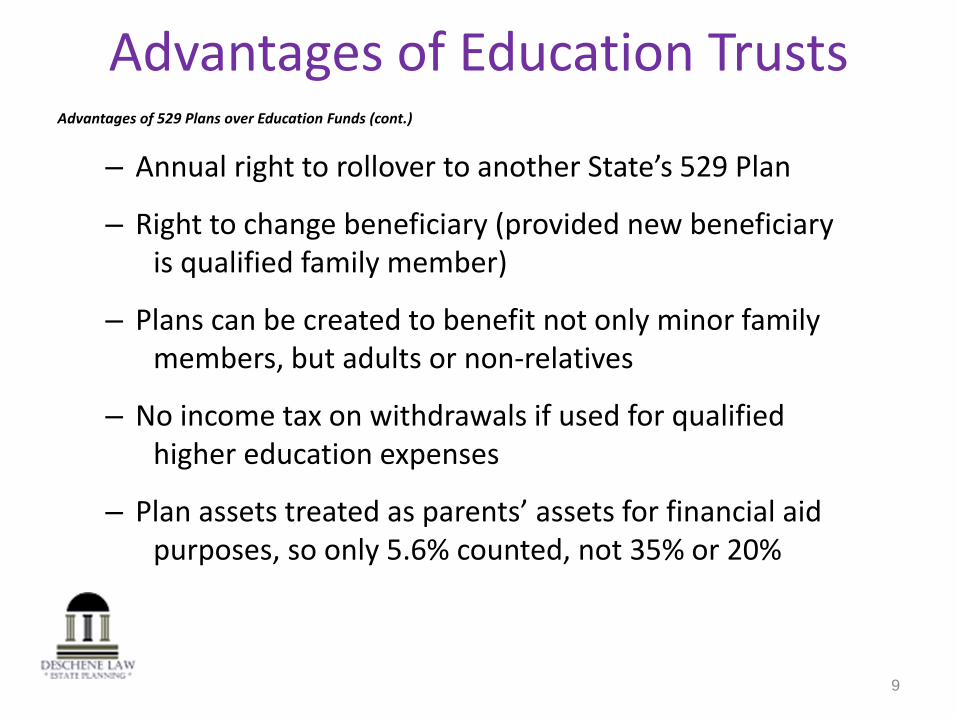

Advantages of Education Trusts Advantages of 529 Plans over Education Funds (cont.)

– Annual right to rollover to another State’s 529 Plan

– Right to change beneficiary (provided new beneficiary is qualified family member)

– Plans can be created to benefit not only minor family members, but adults or non-relatives

– No income tax on withdrawals if used for qualified higher education expenses

– Plan assets treated as parents’ assets for financial aid purposes, so only 5.6% counted, not 35% or 20%

9 9

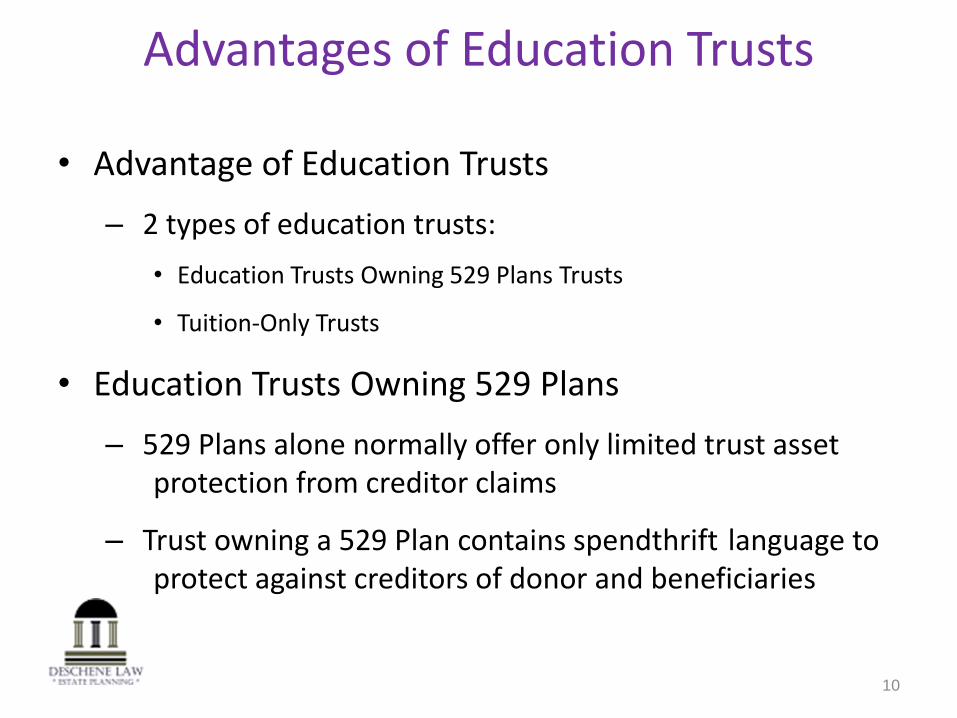

Advantages of Education Trusts

• Advantage of Education Trusts

– 2 types of education trusts:

• Education Trusts Owning 529 Plans Trusts

• Tuition-Only Trusts

• Education Trusts Owning 529 Plans

– 529 Plans alone normally offer only limited trust asset protection from creditor claims

– Trust owning a 529 Plan contains spendthrift language to protect against creditors of donor and beneficiaries

10 10

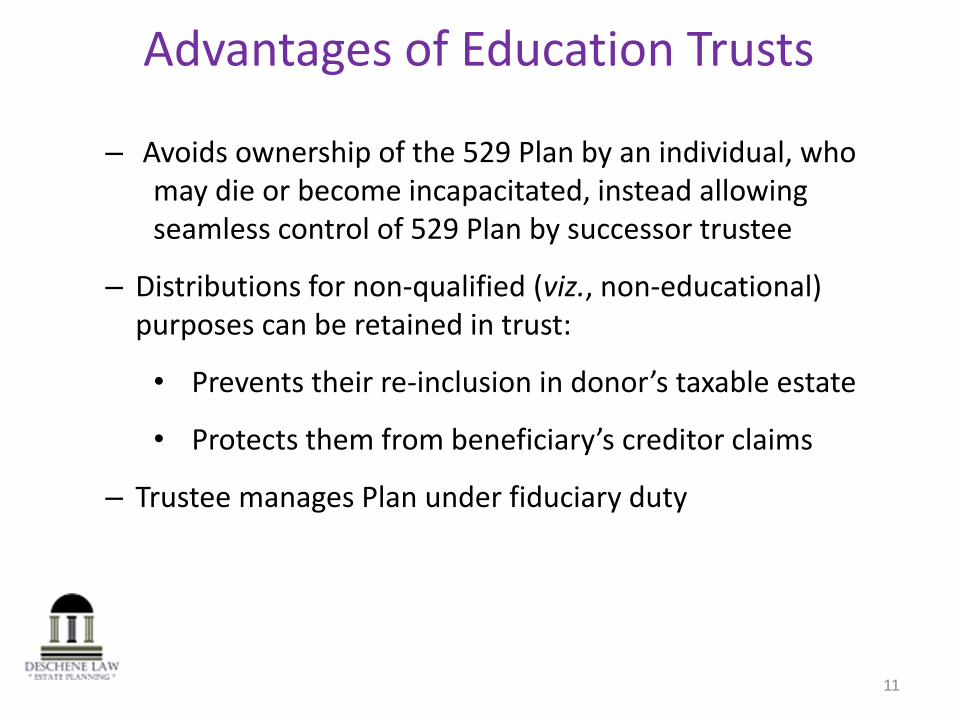

Advantages of Education Trusts

– Avoids ownership of the 529 Plan by an individual, who may die or become incapacitated, instead allowing seamless control of 529 Plan by successor trustee

– Distributions for non-qualified (viz., non-educational) purposes can be retained in trust:

• Prevents their re-inclusion in donor’s taxable estate

• Protects them from beneficiary’s creditor claims

– Trustee manages Plan under fiduciary duty

11 11

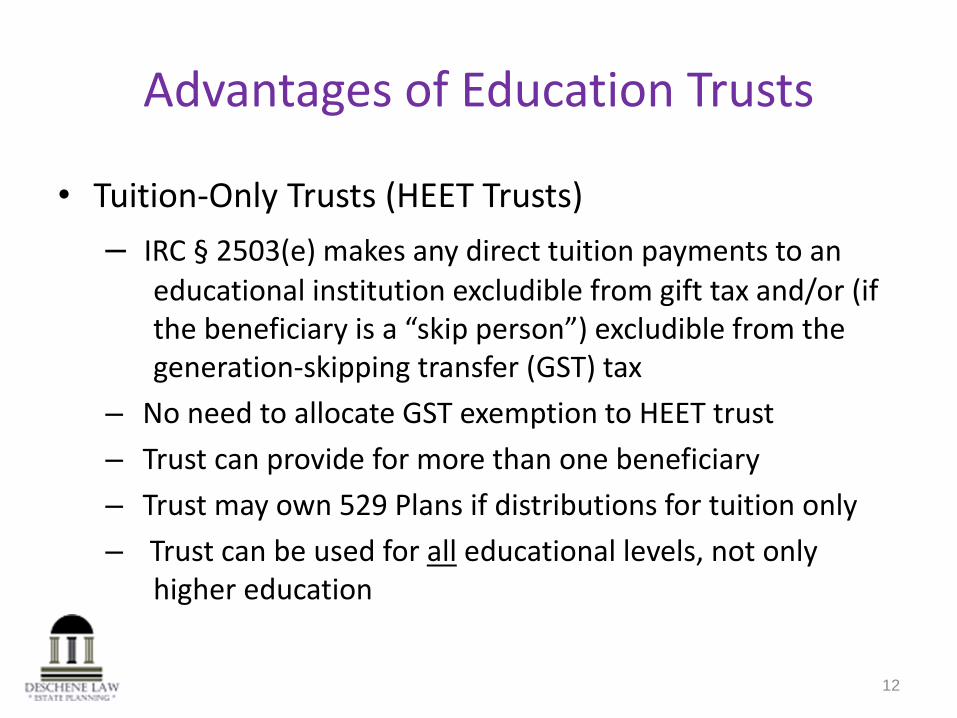

Advantages of Education Trusts

• Tuition-Only Trusts (HEET Trusts)

– IRC § 2503(e) makes any direct tuition payments to an educational institution excludible from gift tax and/or (if the beneficiary is a “skip person”) excludible from the generation-skipping transfer (GST) tax

– No need to allocate GST exemption to HEET trust

– Trust can provide for more than one beneficiary

– Trust may own 529 Plans if distributions for tuition only

– Trust can be used for all educational levels, not only higher education

12

Estate Planning with Education Trusts and 529 Plans January 9, 2013

Gregory Herman-Giddens, JD, LLM, TEP, CFP Attorney at Law

North Carolina ▪ Florida ▪ New York 800-201-0413

[email protected] www.trustcounselpa.com

Main Office 205 Providence Rd., Chapel Hill, NC 27514

© 2013 Gregory Herman-Giddens

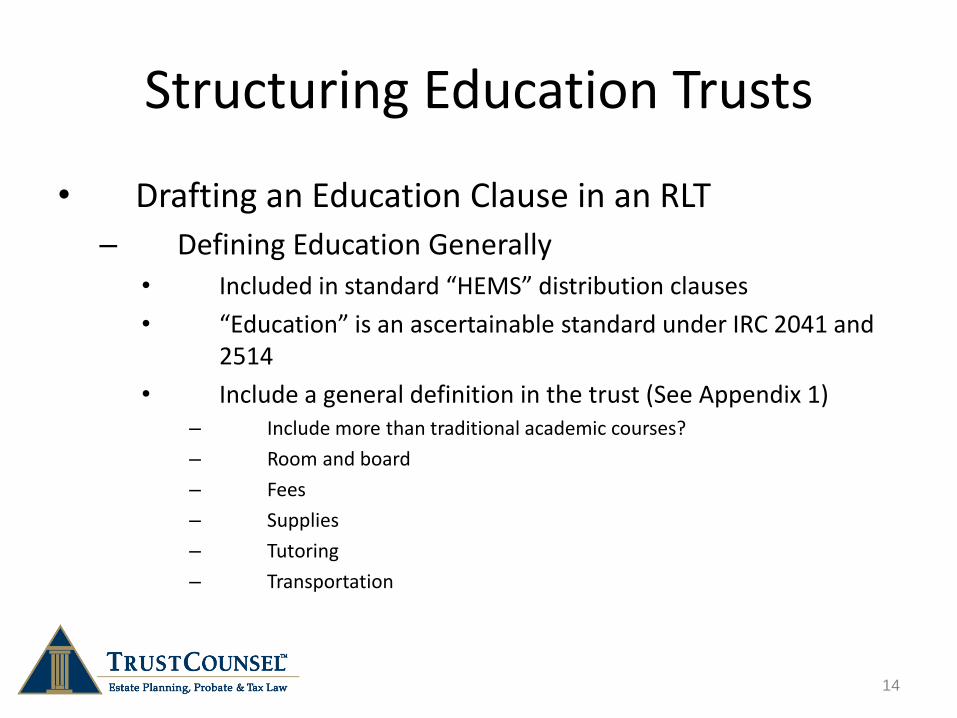

Structuring Education Trusts

• Drafting an Education Clause in an RLT

– Defining Education Generally • Included in standard “HEMS” distribution clauses

• “Education” is an ascertainable standard under IRC 2041 and 2514

• Include a general definition in the trust (See Appendix 1) – Include more than traditional academic courses?

– Room and board

– Fees

– Supplies

– Tutoring

– Transportation

14

Structuring Education Trusts

• Specific Education Clauses – For trust grantors who desire to fund only certain types of

education and/or levels of achievement – Factors to consider

• What levels/types of education? – Primary, secondary, college, grad school – Community college or trade school – Beauty school – Certain institutions only

• All or only certain courses of study • Certain GPA required? • Time period • What happens if the beneficiary doesn’t meet conditions

– See Appendix 2

15 15

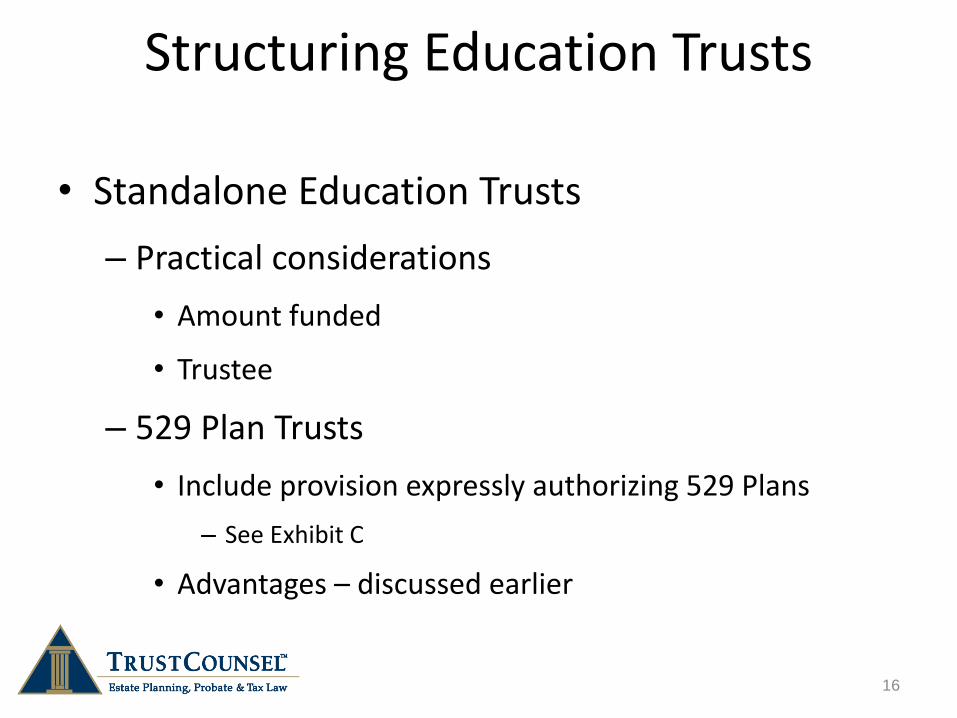

Structuring Education Trusts

• Standalone Education Trusts

– Practical considerations

• Amount funded

• Trustee

– 529 Plan Trusts

• Include provision expressly authorizing 529 Plans

– See Exhibit C

• Advantages – discussed earlier

16 16

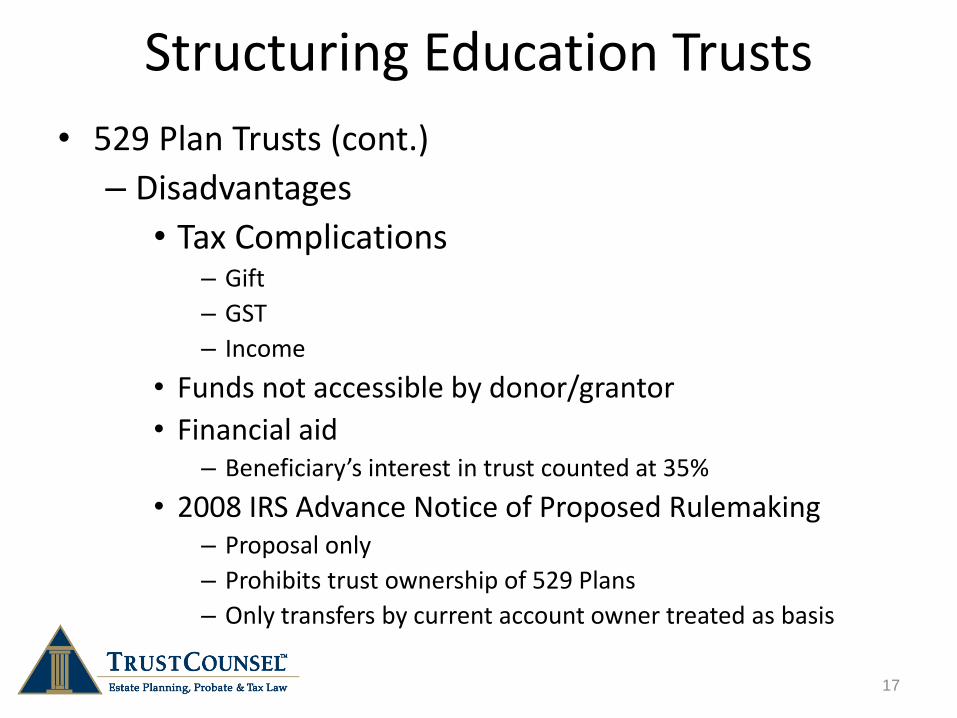

Structuring Education Trusts

• 529 Plan Trusts (cont.)

– Disadvantages

• Tax Complications – Gift

– GST

– Income

• Funds not accessible by donor/grantor

• Financial aid – Beneficiary’s interest in trust counted at 35%

• 2008 IRS Advance Notice of Proposed Rulemaking – Proposal only

– Prohibits trust ownership of 529 Plans

– Only transfers by current account owner treated as basis

17 17

Structuring Education Trusts

• Tuition Only Trusts – Health and Education Exclusion Trusts (HEETS)

• IRC § 2503(e) exempts direct payments for tuition/healthcare from GST

• HEET Trusts do not require allocation of GST exemption

• Can be for tuition only or include medical payments

• Include charity as beneficiary to avoid GST taxable termination

• Can be used for primary and secondary education, unlike 529 Plans

• Can invest in 529 Plans with limitations to use of those funds for college tuition only

18 18

Incorporating 529 Plans in Education Trusts

• 529 Plans in General – State-run college education savings programs

• Post –secondary education expenses only – “Qualified Higher Education Expenses” (QHEE)

– College, grad or professional school, community college

– Expenses for room and board permitted

• Not limited to state of residence

• No limits on out of state colleges

– Contribution limits • Vary, but usually $250-350K

19 19

Incorporating 529 Plans in Education Trusts

• 529 Plans in General (cont.)

– Federal guidelines for state operation

• 1998 Notice of Proposed Rulemaking

• 2008 Advance Notice of Proposed Rulemaking

• Guidance Notices

• Final regulations pending

– Direct sold vs. Advisor sold

20 20

Incorporating 529 Plans in Education Trusts

• Features of 529 Plans

– Wide investment choices

• Conservative to aggressive

• Target date (college start)

– Online management

• Reallocation of investments

• Contributions

• Withdrawals/payments

21 21

Incorporating 529 Plans in Education Trusts

• Features of 529 Plans (cont.)

– Donor retains full control

• Ability to change beneficiaries (within family)

• Right to withdraw funds for any purpose

• Ability to rollover to another plan (once annually)

22 22

Incorporating 529 Plans in Education Trusts

• Gift Tax Considerations

– Contributions qualify for annual exclusion

– 5 year gift tax annual exclusion front-loading

• Not for gifts to trust directly

• Estate Tax Considerations

– Excluded from estate of owner

– Included in taxable estate of beneficiary

23

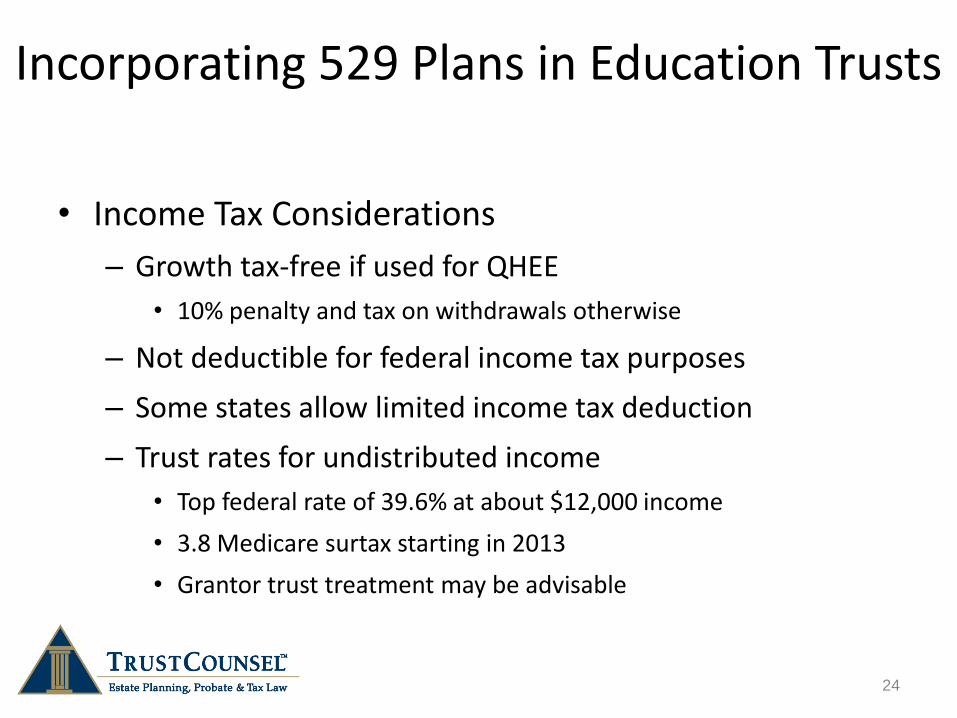

Incorporating 529 Plans in Education Trusts

• Income Tax Considerations

– Growth tax-free if used for QHEE

• 10% penalty and tax on withdrawals otherwise

– Not deductible for federal income tax purposes

– Some states allow limited income tax deduction

– Trust rates for undistributed income

• Top federal rate of 39.6% at about $12,000 income

• 3.8 Medicare surtax starting in 2013

• Grantor trust treatment may be advisable

24 24

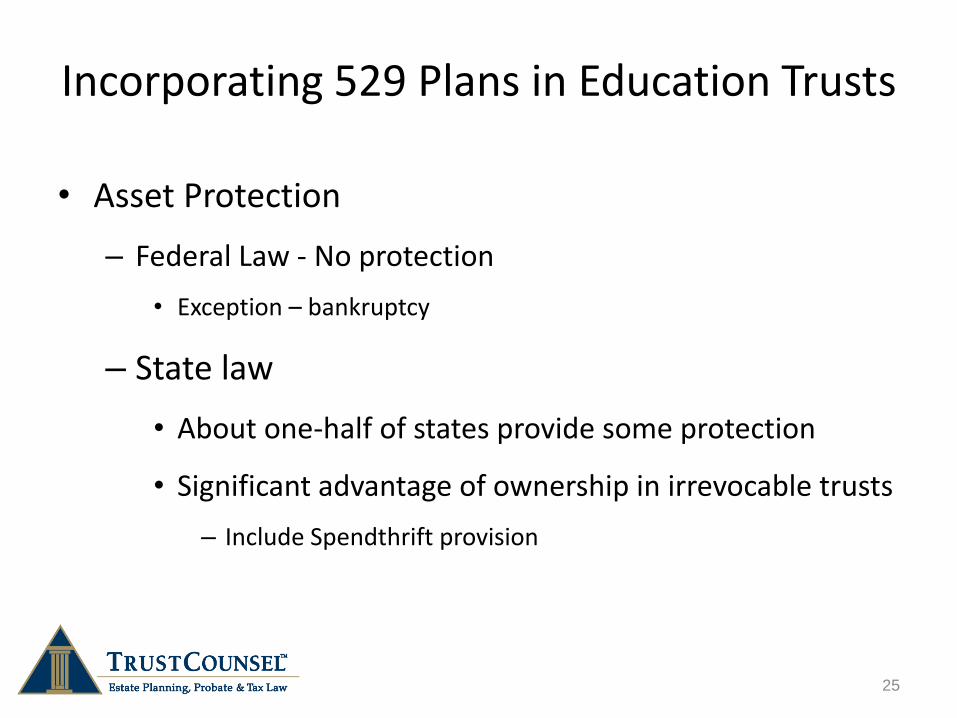

Incorporating 529 Plans in Education Trusts

• Asset Protection

– Federal Law - No protection

• Exception – bankruptcy

– State law

• About one-half of states provide some protection

• Significant advantage of ownership in irrevocable trusts

– Include Spendthrift provision

25 25

Incorporating 529 Plans in Education Trusts

• Financial aid considerations

– 529 Plans considered asset of parent for FAFSA purposes

• Assessed at 5.6%

• Student asset rate is 35%

– Independent students – 20%

– Trust assets

• Beneficiary’s interest in a trust assessed at 35%

• Cannot practically draft around issue

26 26

Resource on 529 Plans

SavingForCollege.com – run by CPA Joe Hurley

- State-by-state comparisons

- Q & A

- Calculators

27

Contact Information

Gregory Herman-Giddens, JD, LLM, TEP, CFP

Attorney at Law (NC, FL, TN, NY)

Offices in North Carolina, Miami and New York City

800-201-0413

www.trustcounselpa.com

www.trustprotectorllc.com

www.ncestateplanningblog.com

28 28

Thank You for Attending!

Tax Implications and Benefits

• Custodial Accounts (UGMA/UTMA)

– Income taxation:

• Taxed to child/beneficiary up to threshold ($1900 in 2012), then at donor/parent’s rate

– Estate/Gift taxation:

• Trust assets included in parent/donor’s taxable estate until beneficiary reaches majority

• § 2503(c) Trusts (“Minors’ Trusts”)

– Income taxation:

• Retained income taxed at higher trust rates

29 29

Tax Implications and Benefits

Taxation of § 2503(c) Trusts (“Minors’ Trusts”) (cont.)

– Estate/gift taxation:

• Contributions qualify for annual gift tax exclusion ($14K in 2013)

• 529 Plans

– Income taxation:

• Tax-free growth if distributions for “educational” purposes

• Non- “educational” distributions are taxable, with 10% penalty

• Contributions not deductible for federal tax, maybe for some States’ income tax

30 30

Tax Implications and Benefits

31 31

Taxation of 529 Plans (cont.)

– Estate/gift taxation:

• Removed from donor’s taxable estate (but retains control)

• Change of beneficiary to qualified family member has no tax consequences (but: if to “skip person,” then GST tax?)

• Contributions qualify for the annual gift tax exclusion ($14K)

• Lump-sum initial “front-loaded” contribution of 5 years of annual exclusion (or $70,000) permitted (note: must file election)

• But note: If donor fails to survive 5 years, portion of excluded assets pulled back into donor’s taxable estate

Tax Implications and Benefits

32

• Trusts Owning 529 Plans

– Income taxation:

• If created as grantor trust, then taxed to donor/parent

• No state income tax deduction allowed for contributions

– Estate/gift taxation:

• Excluded from donor’s taxable estate (provided donor does not serve as trustee)

• Non-qualified distributions can be held in trust, rather than being pulled back into donor’s taxable estate

• Contributions qualify for annual gift tax exclusion ($14K), provided beneficiary is given Crummey right of withdrawal

Tax Implications and Benefits

33

Taxation of Trusts Owning 529 Plans (cont.)

• No 5-year front-loading of annual exclusion is available (as with 529 Plans)

• Tuition-Only Trusts (HEET Trusts)

– Income taxation:

• If non-grantor trust, taxed to trust, but with charitable deduction if distributions to charitable beneficiary

• If grantor trust, taxed to donor (not trust), and since tax payments not treated as gift, allows trust corpus to grow faster

– Estate/gift taxation:

• Contributions subject to estate and gift tax (but ways to avoid or minimize)

Tax Implications and Benefits

Taxation of Tuition-Only Trusts (HEET Trusts) (cont.)

• No Gift/GST tax if structured so that: – No distributions are made to any “skip person” for other than qualified

educational (or medical) purposes; and

– The trust has at least one non-”skip person” (e.g., a charity) as a beneficiary, thereby avoiding potential for “taxable termination” for GST tax purposes

• Generation-Skipping Tax & Education Trusts

– Education trusts for benefit of any “skip person” (viz., family members more than one generation younger than donor (e.g., grandchild), or other beneficiaries who are more than 37½ years younger than donor)

34

Tax Implications and Benefits

Generation-Skipping Tax & Education Trusts (cont.)

– Applies to any gifts made to skip persons exceeding lifetime GST tax exemption

– Gifts made pursuant to the annual exclusion ($14K in 2013) not subject to GST tax provided: • Trust is for skip person’s benefit only; and

• Trust assets will be includable in skip person’s taxable estate, or skip person’s death will be a “taxable termination”

– Allocate lifetime GST tax exemption to ensure trust has GST tax exclusion ratio of zero

35

Contact Information

Robert Deschene

Attorney at Law (MA & RI)

508-316-3853

800-201-0413

www.deschenelaw.com

36 36

Thank You for Attending!