ethekwini industrial land study and development strategy - durban€¦ · ethekwini industrial land...

TRANSCRIPT

Jeffery J. McCarthy Ph.D.

Development Research

and Strategy

eThekwini Industrial Land Study and Land Development Strategy

Stakeholder Workshop

14 November 2013

1

Purpose of the Project

Project context

Employment in eThekwini is dominated by manufacturing

But the comparative advantage could be slipping – general view that there are shortages of suitable land, land costs are relatively high and developers are experiencing very long search times for land

Need to develop an understanding of the current industrial land supply and demand

Develop a shared vision of the management of industrial land to support economic growth and job creation

Develop a Municipal Industrial Land Strategy that is

Complex and diverse in terms of its sub-components, and thus flexible in terms of reactions to demand-side needs (for example the needs of airfreight oriented logistical firms are different to secondary manufacturers, heavy goods oriented firms, etc.); and

Pro-active in intent and not necessarily constrained to existing notions of land supply, currently designated industrial areas and currently conceived planning and regulatory frameworks

2

Project Outcomes

Industrial Land Inventory / Information System: a GIS based tool that will facilitate the management of data and provide an on-going management tool.

Industrial Land Study: a report setting out a review of existing policy, land management systems, the current situation and future possibilities for industrial land development using the output from the land inventory and information system.

Industrial Land Strategy: a report that sets out clear policy recommendations and strategies for taking industrial development in the eThekwini Municipality to a new level.

Implementation Framework: a report that will include concrete recommendations, interventions and actions emanating from the strategy developed.

Monitoring Plan based on the GIS database management tool established.

3

Methodology and ProgrammePOLICY /INSTITUTIONS INTEGRATION SUPPLY & DEMAND SIDE

INCEPTION Task 0: Project Setup and Inception

Inception Meeting 1: 7 June 2013

REVIEW Task 1: Review National Provincial and Local

policy contexts

Task 2 : Review institutional models

Steering Committee Meeting 2: 4 Sept ‘13

Task 3: Industrial Demand Assessment

Task 4: Industrial Supply Assessment & GIS

Tools

Task 5: Review and workshop demand and supply side assessments interventionsSteering Committee 3: 23 October 2013

Task 6: Implement studies of alternative areas or methods

Wider Reference Forum 1: week of 14 November 2013

STRATEGY Task 7: Provide the Framework for Strategy

Principles and Concepts

Task 8: Develop a strategy applying concepts to

implementation

Task 9: Institutional model recommendations

Steering Committee 4: week of 17 Feb 2014

Task 10: Detailed implementation plans

Wider Reference Forum 2: Week of 24 March 2014

CLOSEOUT Task 11 Close Out Report

Close out Meeting: week of 21 April 2014 4

Work Completed Brief Policy Review

Review of International and local examples

Locational theory update

Development of GIS database

Existing land zoned for industrial development

Extent of existing development: 2012 aerial photography – industrial building footprints

Extent of growth since 2002: 2002 and 2007 aerial photography – industrial building footprints to establish take-up rates

Vacant land in 2012 that is zoned for industrial development

Valuation Roll analysis

SAPOA vacancy survey

SAPOA Comparison of Municipal Costs Study

GGP analysis

Comparison of Land prices and Land Rentals

Rates Comparison

Interviews – Russell Curtis, Frikkie Brooks, Andrew Layman, Glen Robbins, Miles Taylor and Mel Clark

5

2012 GIS Database

6

Purpose of Todays Workshop

Introduce the project to a wider stakeholder group

Briefly present some of the research findings on the supply and demand for industrial land in eThekwini

Discuss the challenges to industrial land supply in eThekwini

Workshop a framework for the development of a Municipal Industrial Land Strategy

Welcome 08h30

Outline of the purpose of the project, methodology, programme and work

completed to date

08h45

Presentation of information on Supply and Demand trends 09h00

Tea 10h00

Workshop on opportunities and constraints to industrial land development;

developing a framework for a strategy for industrial land development

10h30

Lunch 12h30

Concluding remarks and way forward 13h00

7

Research Findings

Policy Review

Highly developed industrial policy framework at a National, Provincial and Local level.

Many institutions involved in incentivising and promoting industrial development.

Forward Planning Projects have identified over 3,500 ha of land for industrial development and 2,500 ha for business parks

But still eThekwini is reportedly facing the challenge of limited land supply and high prices

Where to from here?

9

Source: The Mercury

The Industrial Land Market

Recent Locational theory – industry still wants to locate in metropolitan areas and land price is a key factor in choice of locality. Minimum time is also a key locational choice factor now rather than cost and profit - access.

This Study is therefore about the availability, appropriate location and price of industrial land.

Normally price is determined by interactions of the market forces of demand and supply;

but in the case of land this is often impeded (land is immovable; regulated by government; requires public services) which results in dis-equilibrium in the market.

Signs of this are evident in the slow growth of rentals compared to high land prices which suggest a dis-equilibrium in the market which is unlikely to be sustainable.

10

eThekwini Land Prices and RentalsDURBAN ZONED INDUSTRIAL: Building Rentals vs Land Values (SAIV 2006; Knight Frank 2013)

Location Suburb

Rentals per m22500 - 500m²

Land ValuesR/m²

Rental Growth Growth in Land Values

May-06 Aug-13Rental

GrowthMay-06 Aug-13

Growth in Land Values

By Area Overall By Area Overall

South Mobeni /Jacobs R25-26 R32-40 44%R450 -R600 R 1 250 136%

46%

50%

127%

191%

Yard R8-10 R10-15 50%

Prospecton <15 years old R25-27 R40-45 58%R450 -R600 R1200-1350 127%Prospecton - B Grade

(Old)R25-26 R35-40 49%

Southgate R28-30 R35-40 29% R500-R600 R 1 200 118%

Central Umbilo (Congela/Sydney) R18-28 R32-40 50% R450-R550 R 1 500 200%

40% 192%Umgeni Road R 25 R35-45 30%

R 550 R 1 700 209%

Stamfordhill Rd R 600 R 1 600 167%

North Springfield Park R 30 R45-55 58% R 400 R1600-1800 325%

40% 243%

Sea Cow Lake R 22 R 40 60% R 300 R1,500 400%

North Coast Road R 30 R35-40 25% R450-550 R1,650 230%

Briardene R30-35 R45-55 54% R650+R1,800 -

2,000192%

Glen Anil/Avoca R30-35 R45-50 31% R450-550 R 1 450 190%

Riverhorse Estate R48-55 R55-65 22% R 750 R1,800-2,200 147%

Phoenix R20-30 R30-35 31% R 350 R1,100 214%

Inner West New Germany R22-28 R 35 40% R 450 R1000-1500 178%

52% 179%Westmead

R25-30 R45-50 55% R 500 R1250-1500 175%Mahogany Ridge

Marianhill Industrial 25 R35-45 60% R 350 1000 185%

Outlying Verulam/Canelands R25-30 R40-45 55% R 400 R850-1250 163%

75% 215%Tongaat R 20 R30-32 55% R 300 R550-850 233%

Cato Ridge R15-20 R35-40 114% R 150 R450-600 250%11

Location of Existing Supply

Total eThekwini Area: 229,193 ha

Total amount of Zoned Industrial Land (or Zones that allow Industrial Development as a free entry or Special Consent Use) 2012: 9,000 ha

30% in Central area and South Durban Basin; 18% each in the North and South; 13% Inner West and 22% in Outer West

Of the zoned land 6,900 ha is zoned Noxious, General, General Business, Light and Service Industry

The balance is Zoned Extractive or a Special or Mixed Use Zone that allows some industrial development (2,100 ha)

Total number of industrial sites 2012: 26,000

12

Emergence of Spatial Structure of Industrial Land Initially development was focused on the port where older warehouses and

factories can still be found and are now a focus of redevelopment.

1960’s to 1980’s – Manufacturing became concentrated in the Southern Industrial Basin and Pinetown/New Germany areas. In all these instances the Councils were very proactive in creating these areas.

Late 1980’s – areas were full; perceptions of crime and grime were growing – desire for secure, high quality estates and freeway visibility for warehousing – Umgeni Park area and Riverhorse Valley – again the Council was active in the development of these areas.

Recent attention has been in the Outer West and the North around the new airport, although proximity to the port remains a key factor, hence the back-of-port redevelopment plans.

13

Vacant Land and New Opportunities Vacancy Rates in existing buildings - average of about 2.5% (SAPOA sample surveys). But relatively low.

Brownfield redevelopment opportunities

The total amount of vacant land within zones that are solely for industrial use i.e. Noxious, General, Light and Service Industry in 2012 is: 1,370 ha

Identified New Industrial Opportunities (not zoned or serviced) as per the Spatial Development Plans prepared by the Framework Planning Unit of the Development Planning Branch: Gross 3,500 ha and a further 2,500 ha of Business Park area = 6,000 ha (Gross) which, assuming about 40% is developable = 2,400 ha of developable land

Also - Yet to be identified opportunities

eThekwini

Planning Regions

Total Vacant Zoned

Industrial Land (Ha)

North North 180

South South 120

Central South Durban Basin 40

City and Port 50

Inner West 280

Outer West Outer West 700

TOTAL 1 370

14

New Opportunities – Planned

15

RegionCurrent

Industrial

Areas

Planned

Industrial

Areas

Existing

Business

Park and

Related

Planned

Business

Park

Total

Existing

Total

PlannedComment

North 1 166 2 510 0 2 035 1 166 4 545Major new growth

area

South 1 139 92 0 88 1 139 180redevelopment

role

South Durban

Basin773 0 0 0 773 0

Redevelopment

opportunity

City and Port 1 954 0 80 320 2 033 320

Suitable for

redevelopment

with new port and

freight route

Inner West 1 288 0 0 0 1 288 0Consolidate the

current area

Outer West 608 909 0 115 608 1 023 New growth Area

Overall Total

(Ha)6 929 3 511 80 2 558 7 008 6 069

Take-up of Industrial Land Total ground floor area of industrial buildings (in zoned and non-industrial area) as digitised from aerial

photography

2012: 1,821 ha

2008 : 1,716 ha

2002: 1,509 ha

Increase in ground floor area of industrial buildings (in zoned and non-industrial area) between 2008 and 2012: 105 ha which equates to 21 ha of building footprint per annum over 5 years (15% growth in the north and 18% growth in Outer West and 10% growth in South)

Assuming an Coverage of 60% this equates to a take –up of 35 ha per annum between 2008 and 2012

Increase in ground floor area of industrial buildings (in zoned and non-industrial area) between 2002 and 2007: 207 ha which equates to 41 ha of building footprint per annum over 5 years

Assuming an Coverage of 60% this equates to a take-up of 68 ha per annum between 2002 and 2008

Completed Building Plans –

2006: 38 ha; 2007: 74 ha; 2008: 56 ha; 2009: 59 ha; 2010: 23 ha; 2011: 44 ha; 2012: 46 ha

Significant slow down in take up

KZN GGP has slowed in the past 2 years = 2% p.a. for manufacturing – but fluctuations

Urban Econ report 2012(IHS Global Insight) – growth in transport, storage and communications (including warehouses) and contraction in manufacturing

16

Challenge

Significant amount of vacant land and new industrial opportunities (2,400 ha @ a take up rate of 25 ha p.a. = supply for 96 years and @ 80 ha p.a. = supply for 30 years).

Challenge

Is it correctly located to meet demand trends and

How the Municipality should shift from planning to implementation and release of land

17

A Start – Key Development Projects Identified

18

Challenges to the release of Industrial land SAPOA Survey - Property Development Comparison of

Municipal Services Costs 2013: eThekwini is not overly expensive in aggregate terms – property rates (second highest of metros), vacant land rates and planning application fees were high.

Sensitivity to land pricing – industrial costs and revenue considerations; Different price and locational sensitivities in sub-markets

Price – prevailing price twice that of Gauteng

180 degree land form and topography

Project Management challenges within Projects

Political and Business culture – delays in approvals; bureaucratic red tape, non-response on queries about customs/import duties and working with government staff

China and India competitive costs

Competition from other Municipalities – KwaDukuza, Umsunduzi and Richards Bay

Primary constraint – Lack of funding for Bulk Infrastructure - Need for new models to fund infrastructure

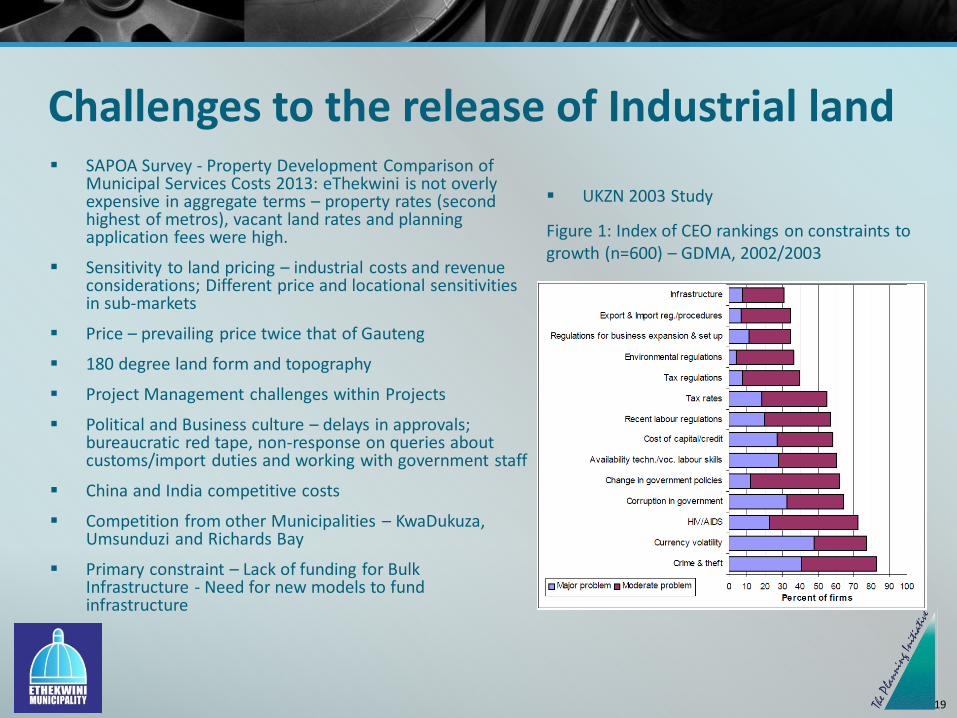

UKZN 2003 Study

Figure 1: Index of CEO rankings on constraints to growth (n=600) – GDMA, 2002/2003

19

SAPOA: - Gross Value Added (Property Development Comparison of Municipal Services Costs 2013)

20

Questions of Clarity

21

Challenges – results of cards

Investor confidence and global economic forces/ macro-economic conditions 7

Rates and financial incentives 9

Relationship between developers and municipalities 16

Red tape/ regulations/ delays/ pro-active planning/ approach – planning too reactive/ bold decisions 25

EIAs/ Act 70 of 1970 8

Lack of para-statals and infrastructure costs 11

Bulk infrastructure costs / limited municipal finance / developers contributions 18

Land price – too high; in the hands of a few; reducing 14

Project management and marketing 6

Broad Interventions

Improve Council and Roleplayers Interactions through a development forum;

Create incentives for development through infrastructure financing, PPPs, one stop shop;

Review approval processes and frameworks including building local municipal capacity and monitor+review processes;

23