eu sugar and its evolving role on the world stage- how are … kingsman eu sugar seminar geneva...

TRANSCRIPT

1

Kingsman EU Sugar Seminar Geneva 14-15 April 2016

EU sugar and its evolving role on the world stage- how are the value chain

adapting?

A buyers perspective

Marc Painsmaye

2

1. Couplet sugars in few words

2. What will the post 2017 quota free EU sugar market look like?

3. The challenges for the Users

3

Sucrerie de Fontenoy SA

Couplet sugars is transforming sugar into specialities for more than 150 years

4

1847 First sugar production of Couplet family in Marchiennes (FR) 1890 Transfer to Wez (actual place) 1937 Start of production of « Cassonade » (brown sugar) 1987 First production of PEARL SUGAR 1992 First production of FONDANT POWDER 1993 Transfer of sugar production to Fontenoy 2000 Couplet sugar 100% independent company 2007 First production of coated sugars 2015-2017 Increase capacity on our lines

HISTORY

5

Our product range

6

OUR MISSION:

We deliver to consumers more taste and pleasure , developing with and for the food industry, sugar specialities that bring taste,

texture and colour.

7

• 100% family company since 5 generations

• 1 factory close to TOURNAI, Belgium

• Recognised technical expertise and know-how

• A team of 60 people

8

• We sell our products to industrial bakeries, chocolate and ice cream factories

• We export in more than 30 countries

• Our products are key ingredients for top quality European food

9

• We buy high quality EU2 sugar (<25 ICU)

• We need full flexible supplies in bulk trucks

• We have a storage capacity

• We compete with local sugar

10

As many European sugar users, we have a lot of questions regarding the post 2017 sugar market

11

A new EU sugar market

2 changes which are the main drivers for the future:

No production limit for sugar and fructose syrups/ isoglucose (quota system is abolished)

Producers can export as much as they want

BUT 2 factors remain unchanged:

Import possibilities are restricted to ACP, CXL and some FTAs.

Prohibitive MFN Import Duties remain for other sources

11

12

New opportunities for the whole

supply chain will happen:

13

PRODUCTION

• Farmers will be able to optimise their

returns/ha as sugar beet is entering

into competition with other crops.

• Mills will optimise their industrial

capacity.

• Mills will have the opportunity to use

various commercial channels

(ethanol, sugar, etc.)

13

14

14

IMPORTS :

• Access to imports are restricted and limited

• Level of imports will continue to depend on the

price gap between the world and the EU market

price.

EXPORTS :

• EU farmers/industry should be competitive

producer on the world market. *

• EU sugar market should be in surplus, leading to

significant exports.**

• Due to EU exports, domestic prices should be

partly linked to world market prices.

•

* Assuming that the world price stay at decent level

** Source: e.g. D-G for Agriculture and Rural Development, CGAAER report

World sugar (Brazil, Thailand

etc.)

EBA/EPA , CXL, Balkans etc.

EU exporting after 2017

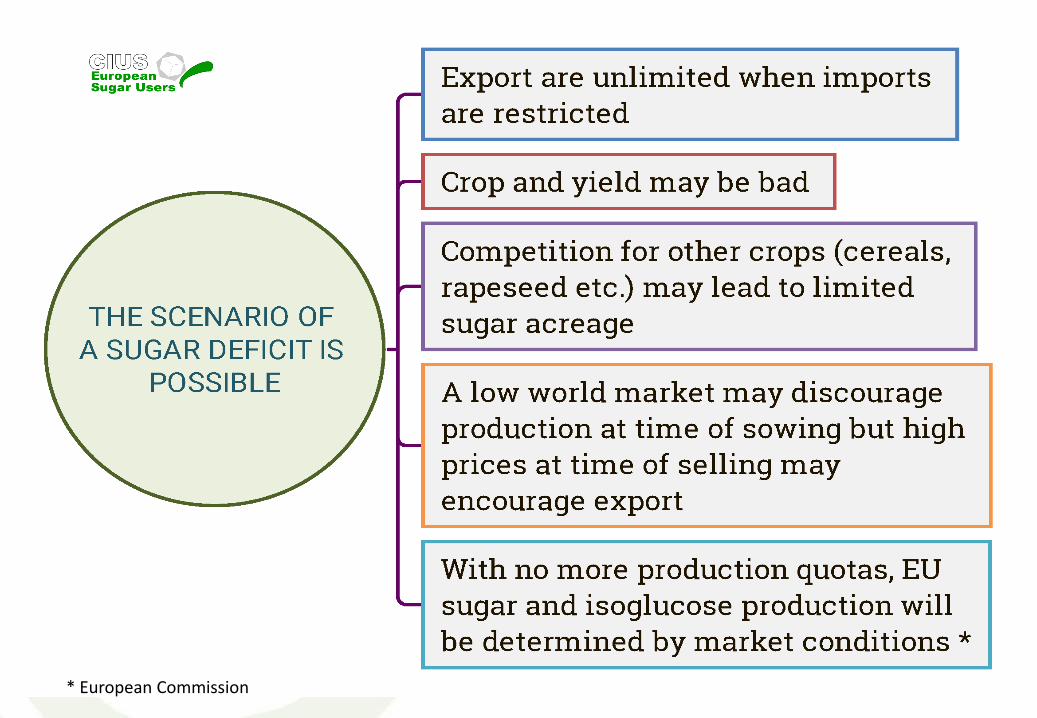

There is an unbalanced situation between restricted imports and unlimited exports

Will EU sugar suppliers serve their European customers FIRST and then export the surplus to avoid a market in deficit ?

16

A new challenge for EU sugar users: predicting the future

16

17

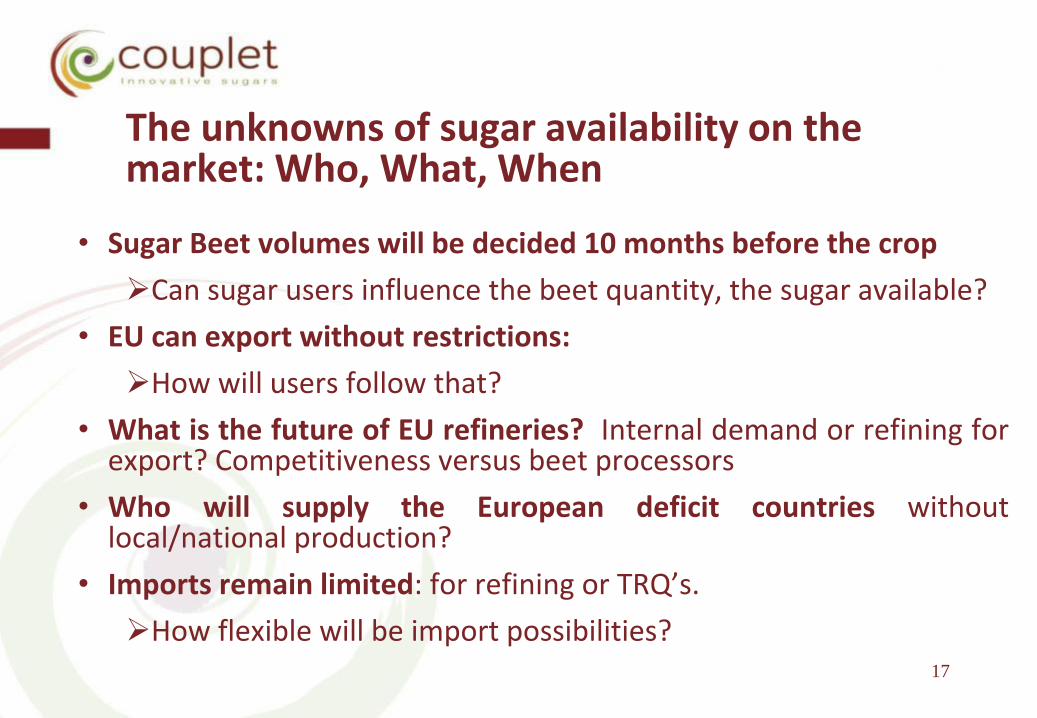

The unknowns of sugar availability on the market: Who, What, When

• Sugar Beet volumes will be decided 10 months before the crop

Can sugar users influence the beet quantity, the sugar available?

• EU can export without restrictions:

How will users follow that?

• What is the future of EU refineries? Internal demand or refining for export? Competitiveness versus beet processors

• Who will supply the European deficit countries without local/national production?

• Imports remain limited: for refining or TRQ’s.

How flexible will be import possibilities?

17

18

What will the sugar price do? • Ups and downs of the world market will influence EU

prices

How can the users monitor this? Protect themselves?

Will we need to change contracting methods?

• Energy price complex : influence of oil/ethanol prices

How will users follow that?

• 1 single market for food sugar and fermentation sugar

Will Food prices follow the volatility of current fermentation prices?

18

19

• What will the sugar price do?

• What influence will cereal / isoglucose prices have on the

market?

• Exchange rate factor: €/$ , Real/$

• Will further concentration of the sugar industry influence price levels for European users?

19

20

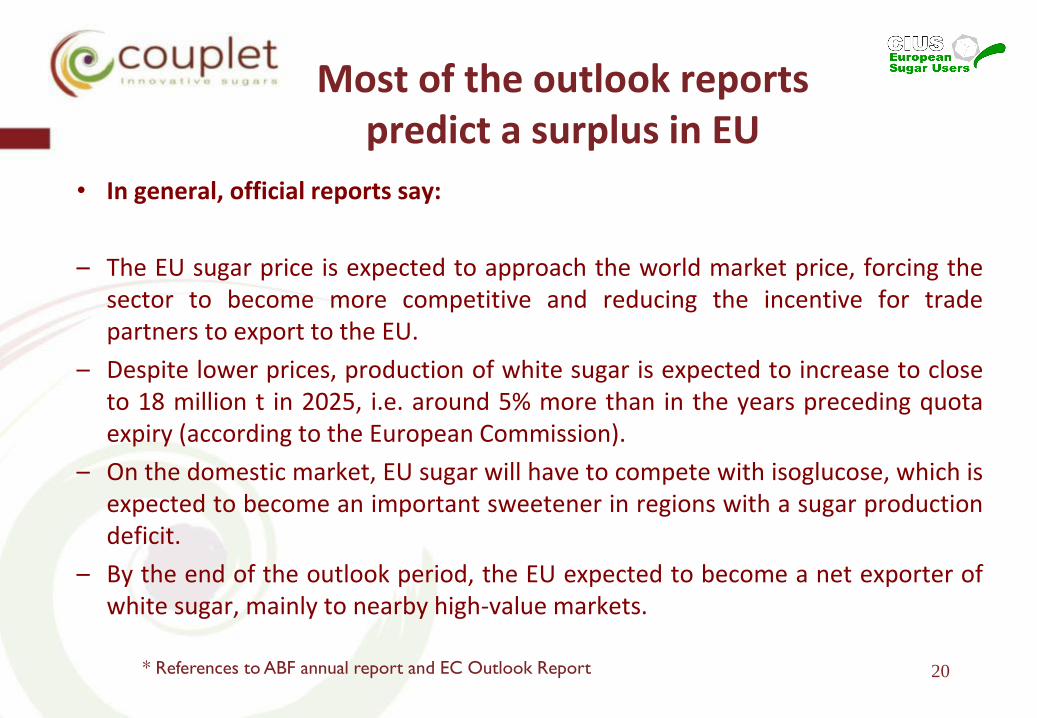

Most of the outlook reports predict a surplus in EU

• In general, official reports say:

– The EU sugar price is expected to approach the world market price, forcing the sector to become more competitive and reducing the incentive for trade partners to export to the EU.

– Despite lower prices, production of white sugar is expected to increase to close to 18 million t in 2025, i.e. around 5% more than in the years preceding quota expiry (according to the European Commission).

– On the domestic market, EU sugar will have to compete with isoglucose, which is expected to become an important sweetener in regions with a sugar production deficit.

– By the end of the outlook period, the EU expected to become a net exporter of white sugar, mainly to nearby high-value markets.

20 * References to ABF annual report and EC Outlook Report

21

21 * Source: EU Commission * European Commission

22

22

23

Thank You

Marc Painsmaye – Sales & Marketing director

April 14th, 2016