euro medium term note programme (wholesale programme)

TRANSCRIPT

Base Prospectus dated 3 July 2020

1

(a société anonyme incorporated under the laws of the Grand Duchy of Luxembourg having its registered office

at 24-26 boulevard d’Avranches, L-1160 Luxembourg, Grand Duchy of Luxembourg, and registered with the Registre de Commerce et des Sociétés, Luxembourg under number B82.454)

€10,000,000,000

Euro Medium Term Note Programme (wholesale programme)

_________________________________

This Base Prospectus has been approved by the Luxembourg Commission de Surveillance du Secteur Financier (the “CSSF”), which is the Luxembourg competent authority for the purpose of Regulation (EU) 2017/1129 of the European Parliament and of the Council of 14 June 2017 on the prospectus to be published when securities are offered to the public or admitted to trading on a regulated market, and repealing Directive 2003/71/EC (the “Prospectus Regulation”) and the Luxembourg law of 16 July 2019 on prospectuses for securities (the “Luxembourg Prospectus Law”), as a base prospectus (the “Base Prospectus”) issued in compliance with the Prospectus Regulation for the purpose of giving information with regard to the notes (“Notes”) issued under the €10,000,000,000 Euro Medium Term Note Programme (the “Programme”) described in this Base Prospectus during the period of twelve (12) months after the date hereof. The CSSF has only approved this Base Prospectus as meeting the standards of completeness, comprehensibility and consistency imposed by the Prospectus Regulation. Such an approval should not be considered as an endorsement of the Issuer that is the subject of this Base Prospectus nor as an endorsement of the quality of any Notes. In accordance with Article 6(4) of the Luxembourg Law of 16 July 2019 on prospectuses for securities, the CSSF does not make any representation as to the economic or financial opportunity of the issue of the Notes nor as to the quality and solvency of the Issuer. Investors should make their own assessment as to the suitability of investing in such Notes. Application has been made for the Notes, during the period of twelve (12) months after the date hereof, to be admitted to trading on the Luxembourg Stock Exchange's Regulated Market (Bourse de Luxembourg) and to be listed on the official list of the Luxembourg Stock Exchange, which is a regulated market (a “Regulated Market”) as defined in the Markets in Financial Instruments Directive 2014/65/EU, as amended (“MiFID II”) and published on the list of the regulated markets in the Official Journal of the European Union. This Base Prospectus shall be valid until 3 July 2021, 12 months after the date of approval by the CSSF, provided that it is completed until such date by any supplement pursuant to Article 23 of the Prospectus Regulation, following the occurrence of a significant new factor, a material mistake or a material inaccuracy relating to the information included in this Base Prospectus which may affect the assessment of the Notes. Pursuant to article 6(4) of the Luxembourg Prospectus Law, by approving this Base Prospectus, the CSSF gives no undertaking as to the economic and financial characteristics of the Notes to be issued hereunder or the quality or solvency of ArcelorMittal (“ArcelorMittal”, the “Issuer” or the “Company”). The Programme also permits Notes to be issued on the basis that they will not be admitted to listing, trading and/or quotation by any competent authority, stock exchange and/or quotation system or to be admitted to listing, trading and/or quotation by such other or further competent authorities, stock exchanges and/or quotation systems as may be agreed with the Issuer. In the case of any Notes which are to be listed and admitted to trading on a Regulated Market within the European Economic Area and/or offered to the public in a Member State of the European Economic Area which would otherwise require the publication of a prospectus under the Prospectus Regulation (as defined herein) in respect of such offering, the minimum specified denomination shall be €100,000 (or its equivalent in any other currency as at the date of issue of the Notes).

Notes issued under the Programme may, or may not, be rated. The rating (if any) may be specified in the relevant Final Terms (as defined herein). Whether or not each credit rating applied for in relation to a relevant Series of

2

Notes (as defined herein) will be issued by a credit rating agency established in the European Union or in the United Kingdom and registered under Regulation (EU) No 1060/2009, as amended (the “CRA Regulation”) will be disclosed in the Final Terms. The list of registered and certified rating agencies published by the European Securities and Markets Authority (“ESMA”) will appear on its website (http://www.esma.europa.eu/page/List-registered-and-certified-CRAs) in accordance with the CRA Regulation. A rating is not a recommendation to buy, sell or hold securities and may be subject to suspension, change, or withdrawal at any time by the assigning rating agency.

Investing in Notes issued under the Programme involves certain risks. The principal risk factors that may affect the abilities of the Issuer to fulfil its respective obligations under the Notes are discussed under “Risk Factors” below.

Arranger BNP PARIBAS

Dealers

Banca IMI BofA Securities

Citigroup Crédit Agricole CIB

HSBC J.P. Morgan

MIZUHO SECURITIES NatWest Markets

RBC Capital Markets SMBC Nikko

Société Générale Corporate & Investment Banking

BBVA BNP Paribas

BMO Capital Markets Commerzbank

Goldman Sachs International ING

NATIXIS Rabobank

Santander Corporate & Investment Banking UniCredit Bank

Date: 3 July 2020

3

TABLE OF CONTENTS

IMPORTANT NOTICES ....................................................................................................................... 1

KEY ELEMENTS OF THE PROGRAMME ......................................................................................... 5

RISK FACTORS .................................................................................................................................. 10

INFORMATION INCORPORATED BY REFERENCE .................................................................... 49

SUPPLEMENTS TO THE BASE PROSPECTUS .............................................................................. 62

FORMS OF THE NOTES .................................................................................................................... 63

TERMS AND CONDITIONS OF THE NOTES ................................................................................. 67

USE OF PROCEEDS ......................................................................................................................... 114

FORM OF FINAL TERMS ................................................................................................................ 115

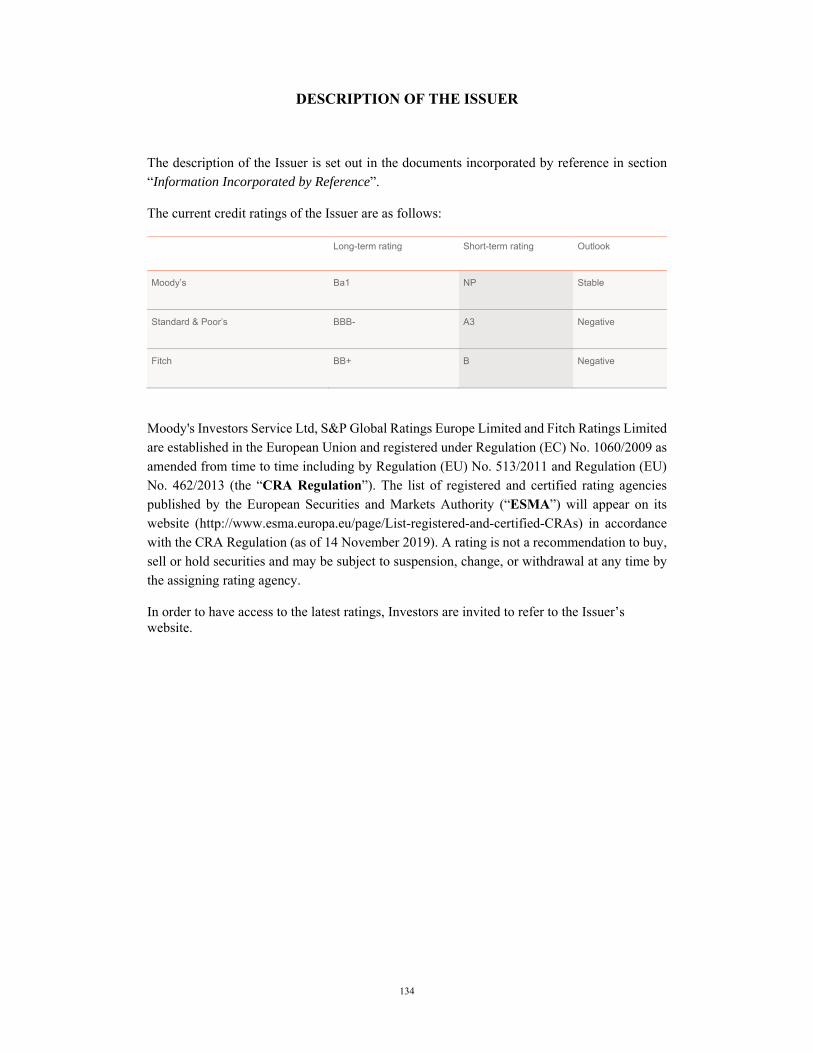

DESCRIPTION OF THE ISSUER ..................................................................................................... 134

RECENT DEVELOPMENTS ............................................................................................................ 135

TAXATION ........................................................................................................................................ 136

SUBSCRIPTION AND SALE ........................................................................................................... 138

GENERAL INFORMATION ............................................................................................................. 143

Base Prospectus dated 3 July 2020

1

IMPORTANT NOTICES

This Base Prospectus comprises a base prospectus for the purposes of Article 8.1 of Regulation (EU) 2017/1129 (the “Prospectus Regulation”). ArcelorMittal (the “Issuer”, the “Company”, “ArcelorMittal” or the “Responsible Person”) accepts responsibility for the information contained in this Base Prospectus and for the Final Terms (as defined below) for each Tranche of Notes issued under the Programme. To the best of the knowledge of the Responsible Person (who has taken all reasonable care to ensure that such is the case), the information contained in this Base Prospectus is in accordance with the facts and does not omit anything likely to affect the import of such information.

Each Tranche (as defined herein) of Notes will be issued on the terms set out herein under “Terms and Conditions of the Notes” (the “Conditions”) as completed by a document specific to such Tranche called final terms (the “Final Terms”). This Base Prospectus must be read and construed together with any supplements hereto and with any information incorporated by reference herein and, in relation to any Tranche of Notes, must be read and construed together with the relevant Final Terms.

No person has been authorized to give any information or to make any representation concerning the Issuer, the Programme or the Notes, other than as contained or incorporated by reference in this Base Prospectus and, if given or made, any such other information or representation should not be relied upon as having been authorized by the Issuer or any Dealer.

Neither the Dealers (as defined herein) nor any of their respective affiliates have authorised the whole or any part of this Base Prospectus and none of them makes any representation or warranty or accepts any responsibility as to the accuracy or completeness of the information contained in this Base Prospectus. Neither the delivery of this Base Prospectus or any Final Terms nor the offering, sale or delivery of any Note shall, in any circumstances, create any implication that the information contained in this Base Prospectus is true subsequent to the date hereof or the date upon which this Base Prospectus has been most recently amended or supplemented or that there has been no adverse change, or any event reasonably likely to involve any adverse change, in the prospects or financial performance or financial position of the Issuer since the date thereof or, if later, the date upon which this Base Prospectus has been most recently amended or supplemented or that any other information supplied in connection with the Programme is correct at any time subsequent to the date on which it is supplied or, if different, the date indicated in the document containing the same.

The distribution of this Base Prospectus and any Final Terms and the offering, sale and delivery of the Notes in certain jurisdictions may be restricted by law. Persons into whose possession this Base Prospectus or any Final Terms comes are required by the Issuer and the Dealers to inform themselves about and to observe any such restrictions. Any investor purchasing the Notes under this Base Prospectus and any Final Terms is solely responsible for ensuring that any offer or resale of the Notes it purchased under this Base Prospectus and any Final Terms occurs in compliance with applicable laws and regulations. For a description of certain restrictions on offers, sales and deliveries of Notes and on the distribution of this Base Prospectus or any Final Terms and other offering material relating to the Notes, see “Subscription and Sale”. In particular, Notes have not been and will not be registered under the United States Securities Act of 1933, as amended (the “Securities Act”), and Notes that are not in registered form for U.S. federal tax purposes are subject to U.S. tax law requirements. Subject to certain exceptions, Notes that are not in registered form for U.S. federal tax purposes may not be offered, sold or delivered within the United States or to U.S. persons.

Neither this Base Prospectus nor any Final Terms constitutes an offer or an invitation to subscribe for or purchase any Notes and should not be considered as a recommendation by the Issuer, the Dealers or any of them that any recipient of this Base Prospectus or any Final Terms should subscribe for or purchase any Notes.

2

Each recipient of this Base Prospectus or any Final Terms shall be taken to have made its own investigation and appraisal of the condition (financial or otherwise) of the Issuer.

The maximum aggregate principal amount of Notes outstanding at any one time under the Programme will not exceed €10,000,000,000 (and for this purpose, any Notes denominated in another currency shall be translated into euro at the date of the agreement to issue such Notes calculated in accordance with the provisions of the Dealer Agreement). The maximum aggregate principal amount of Notes which may be outstanding at any one time under the Programme may be increased from time to time, subject to compliance with the relevant provisions of the Dealer Agreement as defined under “Subscription and Sale”.

In this Base Prospectus, unless otherwise specified, references to a “Member State” are references to a Member State of the European Economic Area, references to “$”, “U.S. dollars” or “dollars” are to United States dollars and references to “€”, “EUR” or “euro” are to the single currency introduced at the start of the third stage of European Economic and Monetary Union pursuant to the Treaty establishing the European Community, as amended.

Certain figures included in this Base Prospectus have been subject to rounding adjustments; accordingly, figures shown for the same category presented in different tables may vary slightly and figures shown as totals in certain tables may not be an arithmetic aggregation of the figures which precede them.

This Base Prospectus has been prepared on the basis that, except to the extent sub-paragraph (ii) below may apply, any offer of Notes in any Member State of the European Economic Area or in the United Kingdom (each, a “Relevant State”) will be made pursuant to an exemption under the Prospectus Regulation from the requirement to publish a prospectus for offers of Notes. Accordingly any person making or intending to make an offer in that Relevant State of Notes which are the subject of an offering contemplated in this Base Prospectus as completed by Final Terms in relation to the offer of those Notes may only do so (i) in circumstances in which no obligation arises for the Issuer or any Dealer to publish a prospectus pursuant to Article 3 of the Prospectus Regulation or supplement a prospectus pursuant to Article 23 of the Prospectus Regulation, in each case, in relation to such offer, or (ii) if a prospectus for such offer has been approved by the competent authority in that Relevant State or, where appropriate, approved in another Relevant State and notified to the competent authority in that Relevant State and (in either case) published, all in accordance with the Prospectus Regulation, provided that any such prospectus has subsequently been completed by Final Terms which specify that offers may be made other than pursuant to Article 3(2) of the Prospectus Regulation in that Relevant State and such offer is made in the period beginning and ending on the dates specified for such purpose in such prospectus or final terms, as applicable, and the Issuer has consented in writing to its use for the purpose of such offer. Except to the extent sub-paragraph (ii) above may apply, neither the Issuer nor any Dealer have authorised, nor do they authorise, the making of any offer of Notes in circumstances in which an obligation arises for the Issuer or any Dealer to publish or supplement a prospectus for such offer.

This document is only being distributed to and is only directed at (i) persons who are outside the United Kingdom or (ii) investment professionals falling within Article 19(5) of the Financial Services and Markets Act 2000 (Financial Promotion) Order 2005 (the “Order”) or (iii) high net worth entities, and other persons to whom it may lawfully be communicated, falling within Article 49(2)(a) to (d) of the Order (all such persons together being referred to as “Relevant Persons”). Any Notes will only be available to, and any invitation, offer or agreement to subscribe, purchase or otherwise acquire such Notes will be engaged in only with Relevant Persons. Any person who is not a Relevant Person should not act or rely on this document or any of its contents.

3

For a more complete description of certain restrictions on offering and sale of Notes and on distribution of this Base Prospectus and any Final Terms, see “Subscription and Sale”.

Copies of this document will be available free of charge during normal business hours on any week day (except public holidays) at the offices of the Issuer.

This document will be published on the website of the Issuer at https://corporate.arcelormittal.com/investors/fixed-income-investors/emtn-programme and the Luxembourg Stock Exchange at www.bourse.lu.

In connection with the issue of any Tranche of Notes, the Dealer or Dealers (if any) named as the stabilising manager(s) (the “Stabilising Manager(s)”) (or persons acting on behalf of any Stabilising Manager(s)) in the applicable Final Terms may over allot Notes or effect transactions with a view to supporting the market price of the Notes at a level higher than that which might otherwise prevail. However, stabilisation may not necessarily occur. Any stabilisation action may begin on or after the date on which adequate public disclosure of the final terms of the offer of the relevant Tranche of Notes is made and, if begun, may cease at any time, but it must end no later than the earlier of 30 calendar days after the issue date of the relevant Tranche of Notes and 60 calendar days after the date of the allotment of the relevant Tranche of Notes. Any stabilisation action or over-allotment must be conducted by the Stabilising Manager(s) (or persons acting on behalf of the Stabilising Manager(s)) in accordance with all applicable laws and rules.

Forward-Looking Statements

This Base Prospectus contains forward-looking statements based on estimates and assumptions. Forward-looking statements include, among other things, statements concerning the business, future financial condition, results of operations and prospects of ArcelorMittal, including its subsidiaries. These statements usually contain the words “believes”, “plans”, “expects”, “anticipates”, “intends”, “estimates” or other similar expressions. For each of these statements, you should be aware that forward-looking statements involve known and unknown risks and uncertainties. Although it is believed that the expectations reflected in these forward-looking statements are reasonable, there is no assurance that the actual results or developments anticipated will be realised or, even if realised, that they will have the expected effects on the business, financial condition, results of operations or prospects of ArcelorMittal.

These forward-looking statements speak only as of the date on which the statements were made, and no obligation has been undertaken to publicly update or revise any forward-looking statements made in this prospectus or elsewhere as a result of new information, future events or otherwise, except as required by applicable laws and regulations.

PRIIPs / IMPORTANT / EUROPEAN ECONOMIC AREA (“EEA”) AND UNITED KINGDOM (“UK”) RETAIL INVESTORS – If the Final Terms in respect of any Notes includes a legend entitled “Prohibition of Sales to EEA and UK Retail Investors”, the Notes are not intended to be offered, sold or otherwise made available to and should not be offered, sold or otherwise made available to any retail investor in the EEA or in the UK. For these purposes, a retail investor means a person who is one (or more) of: (i) a retail client as defined in point (11) of Article 3(2) of Directive 2014/65/EU, as amended (“MiFID II”), (ii) a customer within the meaning of Directive (EU) 2016/97, as amended, where that customer would not qualify as a professional client as defined in point (10) of Article 3(2) of MiFID II. Consequently no key information document required by Regulation (EU) No. 1286/2014 (as amended, the “PRIIPs Regulation”) for offering or selling the Notes or otherwise making them available to retail investors (as defined above) in the EEA or in

4

the UK has been prepared and therefore offering or selling the Notes or otherwise making them available to any such retail investor in the EEA or in the UK may be unlawful under the PRIIPs Regulation.

MiFID II product governance / target market – The Final Terms in respect of any Notes will include a legend entitled “MiFID II Product Governance” which will outline the target market assessment in respect of the Notes and which channels for distribution of the Notes are appropriate. Any person subsequently offering, selling or recommending the Notes (a “distributor”) should take into consideration the target market assessment; however, a distributor subject to MiFID II is responsible for undertaking its own target market assessment in respect of the Notes (by either adopting or refining the target market assessment) and determining appropriate distribution channels.

A determination will be made in relation to each issue of Notes about whether, for the purpose of the product governance rules under EU Delegated Directive 2017/593 (the “MiFID II Product Governance Rules”), any Dealer subscribing for any Notes is a manufacturer in respect of such Notes, but otherwise neither the Arranger nor the Dealers nor any of their respective affiliates will be a manufacturer for the purpose of the MiFID II Product Governance Rules.

5

KEY ELEMENTS OF THE PROGRAMME

The following general description does not purport to be complete and is taken from, and is qualified in its entirety by the remainder of this Base Prospectus and, in relation to any Terms and Conditions of Notes, the relevant Final Terms.

This section “Key Elements of the Programme” constitutes a general description of the Programme for the purposes of Article 25.1(b) of the Commission Delegated Regulation (EU) 2019/980.

I. KEY INFORMATION RELATING TO THE NOTES

Issuer: ArcelorMittal having its registered office at 24-26 boulevard d’Avranches, L-1160 Luxembourg, Grand Duchy of Luxembourg, registered with the Registre de Commerce et des Sociétés, Luxembourg under number B 82.454.

LEI : 2EULGUTUI56JI9SAL165

The website of the Issuer is https://corporate.arcelormittal.com/. The information on such website does not form part of the Base Prospectus, unless that information has been incorporated by reference into the Base Prospectus, and has not been scrutinised or approved by the CSSF.

Arranger: BNP Paribas

Dealers: Banca IMI S.p.A., Banco Bilbao Vizcaya Argentaria, S.A., Banco Santander, S.A., Bank of Montreal, London Branch, BNP Paribas, BofA Securities Europe S.A., Citigroup Global Markets Europe AG, Citigroup Global Markets Limited, Commerzbank Aktiengesellschaft, Coöperatieve Rabobank U.A., Crédit Agricole Corporate and Investment Bank, Goldman Sachs International, HSBC Bank plc, ING Bank N.V., Belgian Branch, J.P. Morgan Securities plc, Merrill Lynch International, Mizuho International plc, Mizuho Securities Europe GmbH, NATIXIS, NatWest Markets Plc, RBC Europe Limited, SMBC Nikko Capital Markets Limited, SMBC Nikko Capital Markets Europe GmbH, Société Générale, UniCredit Bank AG and any other Dealer appointed from time to time by the Issuer either generally in respect of the Programme or in relation to a particular Tranche of Notes.

Fiscal Agent: BNP Paribas Securities Services, Luxembourg branch

Luxembourg Listing Agent: BNP Paribas Securities Services, Luxembourg branch

Listing and Trading: Applications have been made for Notes to be admitted during the period of twelve (12) months after the date hereof to listing on the official list of the Luxembourg Stock Exchange and to trading on the Regulated Market of the Luxembourg Stock Exchange. The Programme also permits Notes to be issued on the basis that they will

6

not be admitted to listing, trading and/or quotation by any competent authority, stock exchange and/or quotation system or to be admitted to listing, trading and/or quotation by such other or further competent authorities, stock exchanges and/or quotation systems as may be agreed with the Issuer.

Clearing Systems: Euroclear and/or Clearstream, Luxembourg and, in relation to any Tranche of Notes, any other clearing system as may be specified in the relevant Final Terms.

Initial Programme Amount: Up to €10,000,000,000 (or its equivalent in other currencies) aggregate principal amount of Notes outstanding at any one time.

Issuance in Series: Notes will be issued in Series. Each Series may comprise one or more Tranches issued on different issue dates. Notes of a given Series will have identical terms, except that the issue date, the issue price and the amount of the first payment of interest may be different in respect of different Tranches. The Notes of each Tranche will all be subject to identical terms in all respects save that a Tranche may comprise Notes of different denominations.

Forms of Notes: Notes may only be issued in bearer form (“Bearer Notes”).

Each Tranche of Notes will initially be in the form of either a Temporary Global Note or a Permanent Global Note, in each case as specified in the relevant Final Terms. Each Global Note which is not intended to be issued in new global note form (a “Classic Global Note” or “CGN”), as specified in the relevant Final Terms, will be deposited on or around the relevant issue date with a depositary or a common depositary for Euroclear and/or Clearstream, Luxembourg and any other relevant clearing system and each Global Note which is intended to be issued in new global note form (a “New Global Note” or “NGN”) will be deposited on or around the relevant issue date with a common safekeeper for Euroclear and/or Clearstream, Luxembourg. Each Temporary Global Note will be exchangeable for a Permanent Global Note or, if so specified in the relevant Final Terms, for Definitive Notes. If the TEFRA D Rules are specified in the relevant Final Terms as applicable, certification as to non-U.S. beneficial ownership will be a condition precedent to any exchange of an interest in a Temporary Global Note or receipt of any payment of interest in respect of a Temporary Global Note. Each Permanent Global Note will be exchangeable for Definitive Notes in accordance with its terms. Definitive Notes will, if interest-bearing, have Coupons attached and, if appropriate, a Talon for further Coupons.

Currencies: Notes may be denominated in euro or in any other currency or currencies as may be agreed between the Issuer and the relevant Dealer(s) (as indicated in the applicable Final Terms) subject to

7

compliance with all applicable legal and/or regulatory and/or central bank requirements. Payments in respect of Notes may, subject to such compliance, be made in and/or linked to, any currency or currencies other than the currency in which such Notes are denominated.

Status of the Notes: Notes will be issued on an unsubordinated basis.

Issue Price: Notes may be issued at any price on a fully-paid or partly-paid basis and at an issue-price which is at par or at a discount to, or premium over-par, as specified in the relevant Final Terms. The price and amount of Notes to be issued under the Programme will be determined by the Issuer and the relevant Dealer(s) at the time of issue in accordance with prevailing market conditions.

Maturities: Any maturity greater than twelve (12) months or no fixed maturity date, subject, in relation to specific currencies, to compliance with all applicable legal and/or regulatory and/or central bank requirements.

Redemption: Notes may be redeemable at par or at such other Redemption Amount as may be specified in the relevant Final Terms.

Clean-up Call Option If so specified in the relevant Final Terms, in respect of any issue of Notes, in the event that at least 80 per cent. of the initial aggregate principal amount of the Notes has been purchased and cancelled by the Issuer, the Issuer will have the option to redeem all, but not some only, of the Notes.

Optional Redemption: Notes may be redeemed before their stated maturity at the option of the Issuer (either in whole or in part) and/or the Noteholders to the extent (if at all) specified in the relevant Final Terms.

Make-whole Redemption by the Issuer

Unless otherwise specified in the relevant Final Terms, in respect of any issue of Notes, the Issuer will have the option to redeem the Notes, in whole or in part, at any time or from time to time, prior to their Maturity Date at their relevant Make-whole Redemption Amount.

Residual Maturity Call Option If a Residual Maturity Call Option is specified in the relevant Final Terms, the Issuer may, on giving not less than 15 nor more than 30 calendar days’ irrevocable notice in accordance with Condition 18 to the Noteholders redeem the Notes, in whole but not in part, at par together with interest accrued to, but excluding, the date fixed for redemption, which shall be no earlier than three (3) months before the Maturity Date.

Redemption on Put Restructuring Event or Change of Control:

Notes may be redeemed before their stated maturity at the option of the Noteholders in the event of a Put Restructuring Event if specified as applicable in the relevant Final Terms as described in Condition

8

9(h) (Redemption and Purchase – Redemption at the Option of Noteholders upon a Put Restructuring Event) or a Change of Control as described in Condition 9(j) (Redemption and Purchase – Offer to Purchase upon a Change of Control).

Tax Redemption: Early redemption will be permitted for tax reasons as described in Condition 9(b) (Redemption and Purchase - Redemption for tax reasons).

Interest: Notes may be interest-bearing or non-interest bearing. Interest (if any) may accrue at a fixed rate or a floating rate and the method of calculating interest may vary between the Issue Date and the Maturity Date of the relevant Series.

Denominations: Notes will be issued in such denominations as may be specified in the relevant Final Terms, subject to compliance with all applicable legal and/or regulatory and/or central bank requirements provided that the minimum denomination of each Note admitted to trading on a regulated market within the EEA or offered to the public in a Member State of the EEA in circumstances which require the publication of a prospectus under the Prospectus Regulation will be €100,000 (or, if the Notes are denominated in a currency other than euro, the equivalent amount in such currency).

Negative Pledge: The Notes will have the benefit of a negative pledge as described in Condition 5 (Negative Pledge).

Events of Default: The Notes will have the benefit of events of default and a cross default provision as described in Condition 12 (Events of Default).

Taxation: All payments in respect of Notes will be made free and clear of withholding for or on account of any taxes, duties, assessments, fees or other governmental charges of Luxembourg save as required by law. If any such withholding or deduction is so required, the Issuer will (subject as provided in Condition 11 (Taxation)) pay such additional amounts as will result in the Noteholders receiving such amounts as they would have received in respect of such Notes had no such withholding been required.

Governing Law of the Notes: English law.

Enforcement of Notes in Global Form:

In the case of Global Notes, Noteholders' rights against the Issuer will be governed by a Deed of Covenant dated 3 July 2020, a copy of which will be available for inspection at the specified office of the Fiscal Agent.

9

Selling Restrictions: For a description of certain restrictions on offers, sales and deliveries of Notes and on the distribution of offering materials in the United States of America, the EEA, the United Kingdom, Republic of Italy, France and Switzerland, see “Subscription and Sale” below.

10

RISK FACTORS

Prior to investing in any Notes issued under the Programme, potential investors should take into account, together with all other information contained in this Base Prospectus, the risk factors described below. These considerations are not exhaustive and other considerations, including some which may not be presently known to the Responsible Person, or which the Responsible Person currently deems immaterial, may impact any investment in the Notes. In addition, the value of the relevant Series of Notes could decline due to any of these risks, and prospective investors may lose some or all of their investment.

Words and expressions defined in the “Terms and Conditions of the Notes” below or elsewhere in this Base Prospectus have the same meanings in this section.

Investing in Notes issued under the Programme involves certain risks. Prospective investors should consider, among other things, the risk factors set out below.

ArcelorMittal’s business, financial condition, results of operations, reputation or prospects could be materially adversely affected by any of the risks and uncertainties described below.

Risks Related to ArcelorMittal

I. Risks Related to the Global Economy and the Mining and Steel Industry

Prolonged low steel and (to a lesser extent) iron ore prices would likely have an adverse effect on ArcelorMittal’s results of operations.

As an integrated producer of steel and iron ore, ArcelorMittal’s results of operations are sensitive to the market prices of steel and iron ore in its markets and globally. The impact of market steel prices on its results is direct while the impact of market iron ore prices is both direct, as ArcelorMittal sells iron ore on the market to third parties (in which case it benefits from higher iron ore market prices), and indirect as iron ore is a principal raw material used in steel production and fluctuations in its market price are typically and eventually (with the timing dependent on steel market conditions) passed through to steel prices (with any lags in passing on higher prices “squeezing” steel margins, as discussed below). Steel and iron ore prices are affected by supply and demand trends and inventory cycles. In terms of demand, steel and iron ore prices are sensitive to trends in cyclical industries, such as the automotive, construction, appliance, machinery, equipment and transportation industries, which are significant markets for ArcelorMittal’s products. More generally, steel and iron ore prices are sensitive to macroeconomic fluctuations in the global economy which are impacted by many factors ranging from trade and geopolitical tensions to global and regional monetary policy to specific disruptive events such as pandemics and natural disasters. In the past, substantial price decreases during periods of economic weakness have not always been offset by commensurate price increases during periods of economic strength. In addition, as further discussed below, excess supply relative to demand for steel in local markets generally results in increased exports and drives down global prices. In terms of inventory, steel stocking and destocking cycles affect apparent demand for steel and hence steel prices and steel producers’ profitability. For example, steel distributors may accumulate substantial steel inventories in periods of low prices and, in periods of rising real demand for steel from end-users, steel distributors may sell steel from inventory (destock), thereby delaying the effective implementation of steel price increases. Conversely, steel price decreases can sometimes develop their own momentum, as customers adopt a “wait and see” attitude and destock in the expectation of further price decreases.

11

As a result of these factors, steel and iron ore prices have come under pressure at various points in recent periods. For example, in 2015, both steel and iron ore prices recorded historical lows, which led to significant declines in ArcelorMittal’s revenues and operating income for 2015. Moreover, the particularly sharp decline in steel prices in the second half of 2015 triggered inventory related losses of $1.3 billion, and the significant decline in iron ore and coal prices led to a $3.4 billion impairment of mining assets and goodwill in the fourth quarter of 2015. More recently, in 2019, steel market conditions deteriorated significantly as a result of a negative price-cost effect due to a decline in steel prices (lower demand in Europe and the U.S., higher imports in Europe and additional domestic supply and the effect of customer destocking in the U.S.) and higher raw material costs (particularly in iron ore due to supply-side developments in Brazil and Australia). As a result, ArcelorMittal’s steel segments recorded significantly lower operating income, including charges of $0.8 billion primarily related to inventory and impairment charges of $1.9 billion in 2019. Steel market conditions have further deteriorated to date in 2020 due to the COVID-19 pandemic and its economic ramifications; in response ArcelorMittal has reduced production and temporarily idled steelmaking and finishing assets, adapted on a country by country basis in alignment with regional demand as well as government requirements, with a corresponding adverse volume and (as discussed below) price effects. This started to weigh on ArcelorMittal’s results of operations in the first quarter of 2020 and is expected to have a material adverse effect on its results of operations in the second quarter of 2020; the extent of the adverse impact thereafter will depend on the timing and extent of potential improvement in steel market conditions, which remains uncertain at this stage.

Steel and iron ore price trends are difficult to predict, particularly in the current geopolitical and economic environment. For example, while the imposition of tariffs in the United States and Europe at a rate of 25% supported local market steel prices in 2018, further tariffs on a widening list of imported products and retaliatory protectionist measures by other countries, particularly in the broader context of global trade tensions (especially between the United States and China), may have a significant negative impact on global trade and ultimately economic growth, steel demand and steel and iron ore prices. Given the demand impacts of the COVID-19 pandemic, steel prices are likely to exhibit greater volatility than previously expected. The general effect to date (subject to some specific geographic exceptions) has been a decline which began towards the end of the first quarter of 2020 (after prices had generally improved in the beginning of the year). The impact on prices going forward will be determined by such factors as the duration of the pandemic, the industry supply response and any impacts on input costs, including potential changes in raw material input prices (the latter having increased in recent weeks due to improved demand conditions (e.g., renewed economic activity in China) and supply constraints in Brazil due to the impact of COVID-19). The extent of the economic damage attributable to the COVID-19 pandemic is highly uncertain, differs from country to country due to the duration and scope of the restrictions put in place to “flatten the curve” of infection and both health and regulatory dynamics post lock-down until a vaccine is available. While activity in steel consuming industries has recommenced or increased in recent weeks and is expected to continue to increase as restrictions continue to be either partially or fully lifted, the level to which GDP and steel demand rebounds is likely to be below normal for longer than the period during which the restrictions are in place and dependent on the increase in unemployment and fall in wider corporate profitability resulting from the measures to contain the crisis, the restrictions and recommendations that remain in place post-lockdown and the level of fiscal policy support available. The Company has therefore made and will continue to need to make ongoing decisions to adjust production in various geographies in accordance with the level of steel demand and government requirements. Overall, the Company’s steel production has been reduced significantly, with steel shipments in the second quarter of 2020 expected to decline by approximately 25-30% relative to the first quarter of 2020 and an expected decline in the Company’s operating results in the second quarter of 2020, and production is not expected to increase until demand conditions improve. A scenario of prolonged low steel and (to a lesser extent or if simultaneous) iron ore prices, including as a result of negative geopolitical or macroeconomic trends (such

12

as those currently being encountered in the world economy as a result of the COVID-19 pandemic), would have a material adverse effect on ArcelorMittal’s results of operations and financial condition (see the 7 May PR incorporated by reference in this Base Prospectus).

Volatility in the supply and prices of raw materials, energy and transportation, and volatility in steel prices or mismatches between steel prices and raw material prices could adversely affect ArcelorMittal’s results of operations.

The prices of steel, iron ore, coking coal and scrap have been highly volatile in recent years. Volatility in steel and raw material prices can result from many factors including: trends in demand for iron ore in the steel industry itself, and particularly from Chinese steel producers (as the largest group of producers); industry structural factors (including the oligopolistic nature of the sea-borne iron ore industry and the fragmented nature of the steel industry); the expectation or imposition of corrective trade measures such as tariffs; massive stocking and destocking activities (sudden drops in prices can lead end-users to delay orders pushing prices down further); speculation; new laws or regulations; changes in the supply of iron ore, in particular due to new mines coming into operation; business continuity of suppliers; changes in pricing models or contract arrangements; expansion projects of suppliers; worldwide production, including interruptions thereof by suppliers; capacity-utilization rates; accidents or other similar events at suppliers’ premises or along the supply chain as occurred in 2019; wars, natural disasters, public health epidemics (such as the outbreak of the COVID-19 pandemic starting in early 2020, which substantially depressed demand for steel for an extended period and continues to weigh on the market), political disruption and other similar events; fluctuations in exchange rates; the bargaining power of raw material suppliers and the availability and cost of transportation. For further information on the movement of raw material prices in recent years, see “Item 5—Operating and financial review and prospects—Key factors affecting results of operations—Raw materials” of the 2019 Form 20-F (incorporated by reference in this Base Prospectus).

As a producer and seller of steel, the Company is directly exposed to fluctuations in the market price for steel, iron ore, coking coal and other raw materials, energy and transportation. In particular, steel production consumes substantial amounts of raw materials including iron ore, coking coal and coke, and the production of direct reduced iron, the production of steel in electric arc furnaces and the re-heating of steel involve the use of significant amounts of energy, making steel companies dependent on the price of and their reliable access to supplies of raw materials and energy. Although ArcelorMittal has substantial sources of iron ore and coal from its own mines (the Company’s self-sufficiency rates were 52% for iron ore and 12% for PCI and coal in 2019), it nevertheless remains exposed to volatility in the supply and price of iron ore and coking coal given that it obtains a significant portion of such raw materials under supply contracts from third parties. For additional details on ArcelorMittal’s raw materials supply and self-sufficiency, see “Item 4.B—Information on the Company—Business overview—Mining products—Other raw materials and energy” of the 2019 Form 20-F (incorporated by reference in this Base Prospectus).

Furthermore, while steel and raw material (in particular iron ore and coking coal) price trends have historically been correlated, a lack of correlation or an abnormal lag in the corollary relationship between raw material and steel prices may also occur and result in a “price-cost effect” in the steel industry. ArcelorMittal has experienced negative price-cost effects (or “squeezes”) at various points in recent years including in 2019 and may continue to do so. In some of ArcelorMittal’s segments, in particular Europe and NAFTA, there are several months between raw material purchases and sales of steel products incorporating those materials, rendering them particularly susceptible to price-cost effect. For example, coking coal sourced from Australia takes several weeks to reach Europe (e.g. ~4 weeks sailing time, plus loading/unloading time at ports), creating a structural lag. Sudden spikes in raw materials, such as coking coal, have occurred in the past and may occur in

13

the future. Because ArcelorMittal sources a substantial portion of its raw materials through long-term contracts with quarterly (or more frequent) formula-based or negotiated price adjustments and as a steel producer sells a substantial part of its steel products at spot prices, it faces the risk of adverse differentials between its own production costs, which are affected by global raw materials and scrap prices, on the one hand, and trends for steel prices in regional markets, on the other hand. In 2019, the significant decline in steel prices (due to lower demand and higher imports, among other things) and significant increase of iron ore prices among other trends due in part to supply shocks following the collapse of the Brumadinho dam owned by Vale in Brazil and a heavy cyclone season in Australia weighed heavily on the profitability of the Company's steel business. To the extent raw material prices increase (as seen recently due to an increase in Chinese demand and supply constraint in Brazil) before demand for steel increases in the wake of the Covid-19 pandemic, the steel sector will experience a negative price-cost effect.

Another area of exposure to price volatility is transportation. Freight costs (i.e., shipping) are an important component of ArcelorMittal’s cost of goods sold. In particular, if freight costs were to increase before iron ore or steel prices or if transportation is significantly disrupted as a result of measures implemented to limit the spread of COVID-19, this would directly and mechanically weigh on ArcelorMittal’s profitability (although it would make imports into its markets less competitive).

Excess capacity and oversupply in the steel industry and in the iron ore mining industry have in the past and may continue in the future to weigh on the profitability of steel producers, including ArcelorMittal.

The steel industry is affected by global and regional production capacity and fluctuations in steel imports and exports, which are themselves affected by the existence and amounts of tariffs and customer stocking and destocking cycles. The steel industry has historically suffered from structural overcapacity globally, and the current global steelmaking capacity exceeds the current global consumption of steel. This overcapacity is affected by global macroeconomic trends and amplified during periods of global or regional economic weakness due to weaker global or regional demand. In particular, China is both the largest global steel consumer and the largest global steel producer by a large margin, and the balance between its domestic production and consumption has been an important factor influencing global steel prices in recent years, such as in 2015, when Chinese domestic steel demand weakened resulting in a surge in Chinese steel exports. While the structural imbalance between Chinese supply and demand has been reduced by capacity eliminations in recent years, less strict capacity constraints and capacity creep may result in increasing overcapacity. In addition, a significant increase in Chinese capacity and/or a significant decrease in Chinese demand could lead to a renewed flood of Chinese steel exports. In the long-term, Chinese steel demand is expected to decline, as the economy slows, the need for large infrastructure projects wanes and pace of urbanization moderates. In addition, other developing markets (such as Brazil, Russia and Ukraine) continue to show structural overcapacity after experiencing decreased domestic demand as a result of weakening economic conditions, and developed Asia continues to exhibit overcapacity and the need to export significant volumes. Regional steel markets are also vulnerable at times of economic crisis in countries with significant steelmaking capacity. One such example is Turkey where a currency crisis caused domestic demand to decline sharply during the second half of 2018 and led to an increase in exports, particularly long steel products. The European steel market is particularly sensitive to decreases in demand as well as supply spikes from imports due to remaining structural overcapacity. For example, in response to a weak demand environment in Europe in the first half of 2019, the Company announced that it would temporarily reduce its European steelmaking capacity with total annualized production cuts of 4.2 million tonnes. Should demand not improve and/or exports be curtailed and/or supply increased, European steel market conditions could remain weak against the backdrop of continued, and even increased, structural overcapacity. Finally, in the United States, improved economic conditions and pricing support from the Section 232 tariffs led to new capacity being built and previously idled

14

capacity being re-opened during 2018. However, apparent steel consumption (“ASC”) for flat products declined by over 4% in 2019, due not only to a downturn in real steel consumption (“RSC”) but also significant destocking at both stockists and end-users. The reduction in inventories was amplified by steel prices falling from high levels, meaning stockists reduced purchases to rebuild stocks at lower prices. Such was the impact of destocking that changes in inventories directly accounted for over 50% of the decline in flat products apparent demand in the United States and for almost 50% in the EU 28 last year. Although at the beginning of 2020 the Company had expected ASC to grow in 2020, as it became more closely aligned to RSC, steel demand has decreased substantially in response to the economic ramifications of the COVID-19 pandemic. In light of this, together with the high level of uncertainty with respect to containment or remediation of the COVID-19 pandemic and the extent of the economic damage that will ultimately be attributable to it, in its first quarter 2020 results announcement the Company withdrew its ASC guidance for 2020. The level to which GDP and steel demand may eventually rebound and the timing of any rebound will be dependent on a number of factors beyond the Company’s control, including the nature and duration of restrictions and recommendations that remain in place or may be reinstituted, levels of unemployment, the fall in wider corporate profitability resulting from measures taken to contain the COVID-19 pandemic, and the level of fiscal policy support available, among others, and the lack of or a delayed or slow rebound, which is more likely the longer restrictions remain in place, would materially and adversely affect the Company's sales and profitability.

The overcapacity of steel production in the developing world and in China in particular has weighed on global steel prices at times over the past decade, as exports have surged to Europe and NAFTA, ArcelorMittal’s principal markets, often at low prices that may be at or below the cost of production, depressing steel prices in regional markets world-wide. See “Unfair trade practices, import tariffs and/or barriers to free trade could negatively affect steel prices and ArcelorMittal’s results of operations in various markets”. If global demand continues to weaken or does not improve, the effects of such a phenomenon could increase.

Finally, excess iron ore supply coupled with decreased demand in iron ore consuming industries, such as steel, led to a prolonged depression of iron ore prices at various points in recent years, for example in 2015, which in turn weighed on steel prices as iron ore is a principal raw material in steelmaking. While the iron ore supply/demand balance has been more favorable in the subsequent period and iron ore prices were strong in 2019, no assurance can be given that it will not deteriorate again, particularly if Chinese steel demand declines, worldwide capacity increases due to new construction or the restart of production or the current decline in steel demand due to the COVID-19 pandemic continues (the extent and duration of which are highly uncertain and may be prolonged). A renewed phase of steel and iron ore oversupply would likely have a material adverse effect on ArcelorMittal’s results of operations and financial condition.

Unfair trade practices, import tariffs and/or barriers to free trade could negatively affect steel prices and ArcelorMittal’s results of operations in various markets.

ArcelorMittal is exposed to the effects of “dumping” and other unfair trade and pricing practices by competitors. Moreover, government subsidies to the steel industry remain widespread in certain countries, particularly those with centrally-controlled economies such as China. In periods of lower global demand for steel, there is an increased risk of additional volumes of unfairly-traded steel exports into various markets, including North America and Europe and other markets such as South Africa, in which ArcelorMittal produces and sells its products. Such imports have had and could in the future have the effect of further reducing prices and demand for ArcelorMittal’s products.

Exports of low-cost steel products from developing countries, along with a lack of effective remedial trade policies, can depress steel prices in various markets globally, including in ArcelorMittal’s key markets.

15

Conversely, ArcelorMittal is exposed to the effects of import tariffs, other trade barriers and protectionist policies more generally due to the global nature of its operations. Various countries have instituted, and may institute import tariffs and barriers that could, depending on the nature of the measures adopted, adversely affect ArcelorMittal’s business by limiting the Company’s access to or competitiveness in steel markets. While such protectionist measures can help the producers in the adopting country, they may be ineffective, raise the risk of exports being directed to markets where no such measures are in place or are less dissuasive and/or result in retaliatory measures. For example, the adoption of steel and aluminum tariffs in the United States in March 2018 under “Section 232” led to a surge of steel imports in other markets and consequently provoked retaliatory safeguard measures by other countries, including the European Union, Canada and Mexico. With regard to ArcelorMittal in particular, the positive effect of the Section 232 tariffs in the United States in 2018 on its U.S. sales was partially offset by the negative effects on ArcelorMittal’s exports from Canada and Mexico into the United States. While on 17 May 2019, the United States, Canada and Mexico reached an agreement to remove the 25% tariffs on aluminum and steel products, it remains unclear what impact these and other protectionist measures (including additional European import quotas adopted in August 2019) will have and whether they will be effective in increasing or maintaining steel prices in the adopting country or countries or adversely impact global macroeconomic conditions. While it is difficult to predict the effect of the economic ramifications of the COVID-19 pandemic on steel imports into ArcelorMittal’s principal markets, there is a risk of increased imports into Europe, as the effectiveness of the current safeguard measures is limited, and the impact of new country specific quotas that may be in effect as of July 1, 2020 is expected to be limited. In this respect, a joint statement by CEOs of European steel producers (including the CEO of ArcelorMittal Europe – Flat Products) published on June 8, 2020 indicated that steel demand had fallen by 50% since the start of the COVID-19 pandemic in March, and that, given that countries such as China, India, Indonesia and Russia have continued, or are restoring, steel production and stockpiling, there is an imminent risk of cheap steel offers flooding the market.

In February 2019, President Trump received from the U.S. Department of Commerce the findings of another Section 232 investigation into whether imported vehicles pose a national security threat to the United States. On 15 May 2019, the Trump administration announced its intention to defer a decision on whether to impose tariffs on cars and auto parts by up to six months, but no such decision has yet been taken. The imposition of such tariffs could weigh significantly on U.S. demand for imported vehicles (particularly from Europe) and could therefore impact demand for steel from European auto manufacturers who are among ArcelorMittal Europe’s principal clients. The overall adverse impact on ArcelorMittal would depend in part on the extent to which this decrease in demand is offset by an increase in demand from U.S. auto manufacturer clients (who would benefit from the protectionist tariffs) as well as from ones based in Canada and Mexico, all of which would benefit ArcelorMittal’s NAFTA operations.

More generally, the current state of trade relations globally with trade disputes leading to the imposition of tariffs and then retaliatory measures, as seen in the recent period in various markets (U.S./China, U.S./Europe, etc.) has and could continue to directly (in the case of tariffs) or indirectly (in the case of economic growth generally) have a significant adverse effect on demand for and the price of steel and hence on ArcelorMittal’s results of operations and financial condition.

Developments in the competitive environment in the steel industry could have an adverse effect on ArcelorMittal’s competitive position and hence its business, financial condition, results of operations or prospects.

The markets in which steel companies operate are highly competitive. Competition—in the form of established producers expanding in new markets, smaller producers increasing production in anticipation of demand

16

increases or amid recoveries, or exporters selling excess capacity from markets such as China—could cause ArcelorMittal to lose market share, increase expenditures or reduce pricing. For example, in NAFTA, competition in the form of significant new U.S. mini-mill capacity could impact pricing and in the CIS, as regional competitors improve operational efficiency and increase capacity, ArcelorMittal’s market share may be affected. Any of these developments could have a material adverse effect on its business, financial condition, results of operations or prospects.

Competition from other materials and alternative steel based technologies could reduce market prices and demand for steel products and thereby reduce ArcelorMittal’s cash flows and profitability.

In many applications, steel competes with other materials that may be used as substitutes, such as aluminum, concrete, composites, glass, plastic and wood. In particular, as a result of increasingly stringent regulatory requirements, as well as developments in alternative materials, designers, engineers and industrial manufacturers, especially those in the automotive industry have increased their use of lighter weight and alternative materials, such as aluminum and plastics in their products.

In the automotive area, ArcelorMittal has introduced new advanced high-strength steel products, such as Usibor® 2000, Ductibor® 1000 and Fortiform® a new 3rd generation advanced high strength steel for cold stamping, new engineering S-in motion® projects and a dedicated electric iCARe® range to respond to the shift toward electric cars. In the construction area, ArcelorMittal has launched Steligence®, a unique holistic commercial approach to serve this market with a complete set of products, services and solutions. See “Item 4.B—Information on the Company—Business overview—Competitive strengths—Research and development” in the 2019 Form 20-F (incorporated by reference in this Base Prospectus). Despite these product innovations, a loss of market share to substitute materials, increased government regulatory initiatives favoring the use of alternative materials, as well as the development of additional new substitutes for steel products could significantly reduce market prices and demand for steel products and thereby reduce ArcelorMittal’s cash flows and profitability.

In addition, new technologies such as carbon free steelmaking or additive manufacturing could result in a loss of market share if competitors develop and deploy this kind of technology before ArcelorMittal.

II. Risks Related to ArcelorMittal’s Operations

ArcelorMittal’s level of profitability and cash flow currently is and, depending on market and operating conditions, may in the future be, substantially affected by its ability to reduce costs and improve operating efficiency.

The steel industry has historically been cyclical, periodically experiencing difficult operating conditions. In light of this, ArcelorMittal has historically and increasingly in recent periods, taken initiatives to reduce its costs and increase its operating efficiency. These initiatives have included various asset optimization and other programs throughout the Company. The most recent of these programs is the Action 2020 plan announced in February 2016 that included, among other aspects, several volume-based and cost-based efficiency improvement initiatives, and the next phase of the Transformation Plan that was announced in March 2019 and targeting further gains through 2023 to be driven by digitalization and seeking to increase the Company’s performance gap compared to competitors in Europe for flat carbon. Given that 2019 market conditions frustrated the Company’s efforts to increase volumes by the Action 2020 target amount, it announced additional cost improvement plans in February 2020. In light of the challenging economic conditions caused by the COVID-19 pandemic, and in order to mitigate the effect of lower shipment volumes as production is reduced to align with decreased demand, the Company has been implementing measures to temporarily reduce

17

its fixed costs in line with lower production rates through temporary labor cost savings (including reductions in salaries of senior management and the members of the Board of Directors, utilization of available economic unemployment schemes, temporary layoffs, federal and state subsidy/grants, salary cuts, reduction/elimination of contractors and overtime reduction), and other costs (such as nonessential maintenance and SG&A). See the 7 May PR (incorporated by reference in this Base Prospectus). While these measures are largely temporary, they also far exceed those planned under Action 2020 as updated by the cost improvement plans announced in February 2020. If and when demand recovers and activity levels begin to normalize, the Company will be able to focus on the variable cost improvements part of Action 2020 and to analyze whether structural changes to its fixed cost base are needed going forward. Failure to implement the Company’s announced cost-saving initiatives fully would prevent the attainment of announced profitability, cash flow improvement and deleveraging targets, and more generally could have a material adverse effect on the Company’s profitability and cash flow.

ArcelorMittal has incurred and may incur in the future operating costs when production capacity is idled or increased costs to resume production at idled facilities.

ArcelorMittal’s decisions about which facilities to operate and at which levels are made based upon customers’ orders for products as well as the capabilities and cost performance of the Company’s facilities. Considering temporary or structural overcapacity in the current market situation, production operations are concentrated at several plant locations and certain facilities are idled in response to customer demand, although operating costs are still incurred at such idled facilities. When idled facilities are restarted, ArcelorMittal incurs costs to replenish raw material inventories, prepare the previously idled facilities for operation, perform the required repair and maintenance activities and prepare employees to return to work safely and resume production responsibilities. Such costs could have an adverse effect on its results of operations or financial condition. See “Item 4.A—Information on the Company—History and development of the Company—Key transactions and events in 2019” in the 2019 Form 20-F (incorporated by reference in this Base Prospectus) for information about actual and potential production cuts. In particular, given the significant deterioration in economic activity and steel market conditions since governmental and regulatory authorities worldwide introduced measures to contain the COVID-19 pandemic, the Company has reduced steel production significantly and is pursuing broad-based measures to reduce costs (both operating expenses and capital expenditures) in-line with exceptionally low capacity utilization levels (see the 7 May PR, incorporated by reference in this Base Prospectus).

ArcelorMittal could experience labor disputes that may disrupt its operations and its relationships with its customers and its ability to rationalize operations and reduce labor costs in certain markets may be limited in practice or encounter implementation difficulties.

A majority of the employees of ArcelorMittal and of its contractors are represented by labor unions and are covered by collective bargaining or similar agreements, which are subject to periodic renegotiation. Strikes or work stoppages could occur prior to, or during, negotiations preceding new collective bargaining agreements, during wage and benefits negotiations or during other periods for other reasons, in particular in connection with any announced intentions to adapt the footprint. ArcelorMittal may experience strikes and work stoppages at various facilities. Prolonged strikes or work stoppages, which may increase in their severity and frequency, may have an adverse effect on the operations and financial results of ArcelorMittal. The risk of strikes and work stoppages is particularly acute during collective bargaining agreement negotiations. For example, in March 2019, industrial action was initiated in South Africa by NUMSA, the largest union operating at ArcelorMittal South Africa. They demanded the insourcing and/or the equalization of the remuneration and

18

benefits of the employees of a service provider to ArcelorMittal South Africa, which led to a two-month strike from March to May 2019.

Faced with temporary or structural overcapacity in various markets, particularly developed ones, ArcelorMittal has in the past sought and may in the future seek to rationalize operations through temporary or permanent idling and/or closure of plants. For example, on 6 May 2019 and 29 May 2019, ArcelorMittal announced a series of temporary production cuts in steelmaking operations in Europe, totaling 4.2 million tonnes in annualized production for 2019. In a depressed economic environment in South Africa, ArcelorMittal South Africa initiated a Business Transformation project in 2018 and a strategic workforce planning process that started in January 2019 and led to the announcement of a workforce reorganization and reduction in July 2019. As a result, ArcelorMittal South Africa engaged in consultations with employee representatives which concluded in November 2019. In addition, ArcelorMittal South Africa announced in November 2019 its intention to cease operations at Saldanha which led to a consultation process with employee representatives that concluded on 7 January 2020. Most recently, in response to the economic ramifications of the COVID-19 pandemic, ArcelorMittal has reduced production and has implemented, and continues to implement, cost reduction measures, including temporary workforce reductions (see the 7 May PR, incorporated by reference in this Base Prospectus). Initiatives such as these have in the past and may in the future lead to protracted labor disputes and political controversy. While the Company has not experienced significant labor disputes in connection with measures associated with the COVID-19 pandemic, it cannot guarantee that no such disputes will arise in the future, in particular if the foregoing COVID-19-related measures are prolonged.

Disruptions to ArcelorMittal’s manufacturing processes caused for example by equipment failures, natural disasters, pandemics or extreme weather events could adversely affect its operations, customer service levels and financial results.

Steel manufacturing processes are dependent on critical steel-making equipment, such as furnaces, continuous casters, rolling mills and electrical equipment (such as transformers), and such equipment may incur downtime as a result of unanticipated failures or other events, such as fires, explosions, furnace breakdowns or as a result of natural disasters, pandemics or severe weather conditions. ArcelorMittal’s manufacturing plants have experienced, and may in the future experience, plant shutdowns or periods of reduced production as a result of such equipment failures or other events, one example being the collapse of the oxygen and nitrogen pipelines in November 2018 at ArcelorMittal Temirtau or the fire in a conveyor belt of the coke plant in ArcelorMittal Asturias in Aviles in October 2018. An electrical failure in the third quarter of 2019 resulted in a temporary stoppage of the concentrator at ArcelorMittal Mines and Infrastructure Canada, impacting iron ore production. To the extent that lost production as a result of such a disruption cannot be compensated for by unaffected facilities, such disruptions could have an adverse effect on ArcelorMittal’s operations, customer service levels and results of operations. Most recently, in response to the economic ramifications of the COVID-19 pandemic, ArcelorMittal has reduced production (see the 7 May PR, incorporated by reference in this Base Prospectus).

In addition, natural disasters and severe weather conditions could lead to significant damage at ArcelorMittal’s production facilities and general infrastructure. For example, ArcelorMittal Mexico’s production facilities located in Lázaro Cárdenas, Michoacán, Mexico are located in or close to areas prone to earthquakes. The Lázaro Cárdenas area has, in addition, been subject to a number of tsunamis in the past. The site of the joint venture AM/NS Calvert (“Calvert”) in the United States is located in an area subject to tornados and hurricanes. ArcelorMittal also has assets in locations subject to bush fires, specifically in Kazakhstan and South Africa, and to Arctic freeze. More generally, changing weather patterns and climatic conditions in recent years, possibly due to the phenomenon of global warming, have added to the unpredictability and frequency of natural disasters.

19

For example, on 10 July 2019 an extreme storm disabled a crane that unloads from ships iron ore used in the blast furnaces at the Taranto plant in Italy, causing a fatality and subsequently affecting a portion of its raw material supply. Severe weather conditions can also affect ArcelorMittal’s operations in particular due to the long supply chain for certain of its operations and the location of certain operations in areas subject to harsh winter conditions (i.e., the Great Lakes Region, Canada and Kazakhstan) or areas that are susceptible to droughts (i.e., South Africa, Brazil). Flooding has also affected ArcelorMittal's operations, including at ArcelorMittal Asturias in Aviles, Spain in June 2018 and in Liberia in the third quarter of 2018, when heavy rains during the wet season caused handling and logistic constraints that impacted shipment volumes. Damage to ArcelorMittal production facilities due to natural disasters and severe weather conditions could, to the extent that lost production cannot be compensated for by unaffected facilities, adversely affect its business, results of operations or financial condition.

ArcelorMittal’s insurance policies provide limited coverage, potentially leaving it uninsured against some business risks.

The occurrence of an event that is uninsurable or not fully insured could have a material adverse effect on ArcelorMittal’s business, financial condition, results of operations or prospects. ArcelorMittal maintains insurance on property and equipment in amounts believed to be consistent with industry practices, but it is not fully insured against all such risks. ArcelorMittal’s insurance policies cover physical loss or damage to its property and equipment on a reinstatement basis as arising from a number of specified risks and certain consequential losses, including business interruption arising from the occurrence of an insured event under the policies. Under ArcelorMittal’s property and equipment policies, damages and losses caused by certain natural disasters, such as earthquakes, floods and windstorms, are also covered.

ArcelorMittal also purchases worldwide third-party public and product liability insurance coverage for all of its subsidiaries. Various other types of insurance are also maintained, such as comprehensive construction and contractor insurance for its greenfield and major capital expenditures projects, directors and officers liability, transport, and charterers’ liability, as well as other customary policies such as car insurance, travel assistance and medical insurance.

In addition, ArcelorMittal maintains trade credit insurance on receivables from selected customers, subject to limits that it believes are consistent with those in the industry, in order to protect it against the risk of non-payment due to customers’ insolvency or other causes. Not all of ArcelorMittal’s customers are or can be insured, and even when insurance is available, it may not fully cover the exposure.

Notwithstanding the insurance coverage that ArcelorMittal and its subsidiaries carry, the occurrence of an event or series of events (such as, among others, a pandemic) that may result in losses in excess of limits specified under the relevant policy, or losses not covered by insurance policies, could materially harm ArcelorMittal’s financial condition and future operating results.

ArcelorMittal’s reputation and business could be materially harmed as a result of data breaches, data theft, unauthorized access or successful hacking.

ArcelorMittal’s operations depend on the secure and reliable performance of its information technology systems. An increasing number of companies, including ArcelorMittal, have recently experienced intrusion attempts or even breaches of their information technology security, some of which have involved sophisticated and highly targeted attacks on their computer networks. ArcelorMittal’s corporate website was the target of a hacking attack in January 2012, which brought the website down for several days, and phishing, ransomware and virus attacks have been increasing in more recent years through 2019, with WannaCry impacting the

20

Company in March 2018. Implementation of digitalization, Industry 4.0 and Cloud computing result in new risks with increasing threats to ArcelorMittal’s operations and systems.

Because the techniques used to obtain unauthorized access, disable or degrade service or sabotage systems change frequently and often are not recognized until launched against a target, the Company may be unable to anticipate these techniques or to implement in a timely manner effective and efficient countermeasures.

If unauthorized parties attempt or manage to bring down the Company’s website or force access into its information technology systems, they may be able to misappropriate confidential information, cause interruptions in the Company’s operations, damage its computers or process control systems or otherwise damage its reputation and business. In such circumstances, the Company could be held liable or be subject to regulatory or other actions for breaching confidentiality and personal data protection rules. Any compromise of the security of the Company’s information technology systems could result in a loss of confidence in the Company’s security measures and subject it to litigation, civil or criminal penalties, and adverse publicity that could adversely affect its reputation, financial condition and results of operations.

III. Risks Related to ArcelorMittal’s Mining Activities

ArcelorMittal’s mining operations are subject to risks associated with mining activities.

ArcelorMittal’s mining operations are subject to the hazards and risks usually associated with the exploration, development and production of natural resources, any of which could result in production shortfalls or damage to persons or property. In particular, the hazards associated with open-pit mining operations include, among others:

• flooding of the open pit;

• collapse of the open-pit wall;

• accidents associated with the operation of large open-pit mining and rock transportation equipment;

• accidents associated with the preparation and ignition of large-scale open-pit blasting operations;

• production disruptions or difficulties associated with mining in extreme weather conditions;

• hazards associated with the disposal of mineralized waste water, such as groundwater and waterway contamination; and

• collapse of tailings ponds dams.

Hazards associated with underground mining operations, of which ArcelorMittal has several, include, among others:

• underground fires and explosions, including those caused by flammable gas;

• gas and coal outbursts;

• cave-ins or falls of ground;

• discharges of gases and toxic chemicals;

• flooding;

21

• sinkhole formation and ground subsidence; and

• blasting, removing, and processing material from an underground mine.