european commission - agrilifeagrilife.jrc.ec.europa.eu/documents/casestudies_1-baena.pdf ·...

TRANSCRIPT

EUROPEAN COMMISSION DIRECTORATE-GENERAL JRC JOINT RESEARCH CENTRE Institute for Prospective Technological Studies (Seville) Sustainability in Agriculture, Food and Health

Case studies

1. Baena

30/11/06

DG JRC/IPTS

Preface:

"Case studies: A detailed report for each case study, including data sources, data sets, discussion of findings and results with regards to the above objectives."

"Objectives:

• to assess the benefits and costs of quality assurance and certification schemes for farmers, processors, retailers and consumers;

• to analyse the effects of quality assurance and certification schemes on European farmers with special focus on small-scale farmers;

• to analyse the contribution of quality assurance and certification schemes to the development of rural areas."

Each case study assesses the benefits and costs of quality assurance and certification schemes along the food supply-chain from farmers to consumers. In the section on farmers particular attention is paid to the effects on small-scale farmers. The contribution of quality assurance and certification schemes to the development of rural areas is included in the case studies at various points and an in-depth discussion of this aspect is conducted in the "Final Report". The following case studies have been conducted by ETEPS AISBL and JRC-IPTS: 1. Baena, olive oil, Spain 2. Boerenkaas, cheese, the Netherlands 3. Comté, cheese, France 4. Dehesa de Extremadura, cured ham, Spain 5. EurepGAP, fruit & vegetable, Europe 6. Label Rouge, chicken, France 7. Neuland, pork, Germany 8. Parmigiano Reggiano, cheese, Italy 9. Red Tractor, potatoes, United Kingdom

Legal notice The orientation and content of this report cannot be taken as indicating the position of the European Commission or its services. The European Commission retains the copyright to this publication. Reproduction is authorised, except for commercial purposes, provided the source is acknowledged. Neither the European Commission nor any person acting on behalf of the Commission is responsible for the use that might be made of the information in this report.

© European Communities, 2006

1

Case study: “Baena” PDO extra virgin olive oil Francisco Cáceres Clavero Cecilia Riccioli Encarnación Martínez Navarro Rosana García Collado JRC-IPTS Contribution by: Fatma Handan Giray Stephan Hubertus Gay

Foresight Studies Area / Área de Estudios y Prospectiva

2

Table of Contents INTRODUCTION ........................................................................................................ 3 Framework and purposes of the study................................................................................................................ 3 Criteria for selecting the case studies .................................................................................................................. 3 Research methodology.......................................................................................................................................... 4 CASE STUDY: PDO “BAENA” OLIVE OIL............................................................... 6 Introduction to the product: Olive oil ................................................................................................................. 6 Overview of the QAS .......................................................................................................................................... 11

Organization and general objectives of the scheme ......................................................................................... 11 Importance of the scheme................................................................................................................................. 13 Regulatory requirements and controls.............................................................................................................. 17 Products covered by the scheme ...................................................................................................................... 18

Overview of the chain: From producer to consumer ....................................................................................... 20 Producers: farmers ............................................................................................................................................. 22

Main characteristics.......................................................................................................................................... 22 Requirements.................................................................................................................................................... 23

Processors: milling industries and bottling industries ..................................................................................... 23 Main characteristics.......................................................................................................................................... 23 Requirements.................................................................................................................................................... 25

Traders................................................................................................................................................................. 25 Main characteristics.......................................................................................................................................... 25 Strategies. ......................................................................................................................................................... 26

Retailers ............................................................................................................................................................... 26 Main characteristics.......................................................................................................................................... 26 Strategies. ......................................................................................................................................................... 29

Consumers ........................................................................................................................................................... 30 Prices at different stages of the supply Chain................................................................................................... 33 PRELIMINARY CONCLUSIONS ............................................................................. 34 Concerning PDO implantation and development. ........................................................................................... 34 PDO benefits........................................................................................................................................................ 35 Policy Recommendations.................................................................................................................................... 35 ANNEXES ................................................................................................................ 37

FIGURES AND TABLES INDEX.............................................................................. 53

BIBLIOGRAPHY ...................................................................................................... 53

3

Introduction

Framework and purposes of the study

The general objective of the current case study is to carry out an assessment of the added value created by quality assurance schemes (QAS) to the product, comparing benchmark products with certified ones, and determining which steps of the supply chain contribute to create value added. In order to carry out this general objective this case study involves the following purposes:

• building up a qualitative description of the selected QAS,

• describing the supply chain of the product identifying key stakeholders (from farmer to consumers) and indicating possible differences, if they exists, between products under QAS and non certified ones,

• compiling quantitative data (prices and quantities) of QAS and benchmark products in different segments of the supply chain

Criteria for selecting the case studies

Different criteria have been considered to choose this case study as representative. In the first place, the product picked out, extra virgin olive oil (EVOO) is a representative and emblematic product Spain, considered as high quality valuable product in its category. Extra virgin olive oil is the highest quality from all olive oils, as it is obtained through mechanical processes or other physical means 0,8 g maximum acidity per 100 g and no defects on tasting panels as opposed to other refined olive oils or oils with higher levels of acidity, presenting some defects on tasting panels. These circumstances guarantee more valuable organoleptic characteristics making the product distinguishable and richer in aroma and flavour. Secondly, the QAS chosen is the Protected Designation of Origin (PDO). This scheme is one of the most important food quality guaranteed certification systems in the Mediterranean countries, especially relevant in the Spanish case. In fact, much earlier before the EU protected those schemes, many wine and food Designation of Origins had been under protection by national legislation. These schemes established and consolidated as many of them have existed for decades, and have lived an evolution of important proliferation, demonstrated by the fact of the massive increase in numbers of such certifications. In the third place, from the existing extra virgin olive oil PDOs in Spain, the case of “Baena” has been selected for various reasons:

• It is one of the oldest PDOs for this product, working for around 25 years

• It possesses a good consolidated reputation among consumers from the whole country and abroad.

4

• High quantities of olive oil are produced and commercialized under this scheme each year, representing around 17% of the total PDO extra virgin olive oil commercialized in the last years.

Finally, two different presentations from this product have been selected for further investigation with the help of the Ruling Council criterion: Glass bottles of ½ liter and metal tins of 5 liters1. Both are, according to Ruling Council, the most representative containers for PDO extra virgin olive oil in terms of quantities commercialised and production. Besides, the consumer’s eye they are appropriated presentations of high quality olive oil as opposed to other kind of presentations made of plastic materials not permitted by the “Baena” PDO statute.

Research methodology

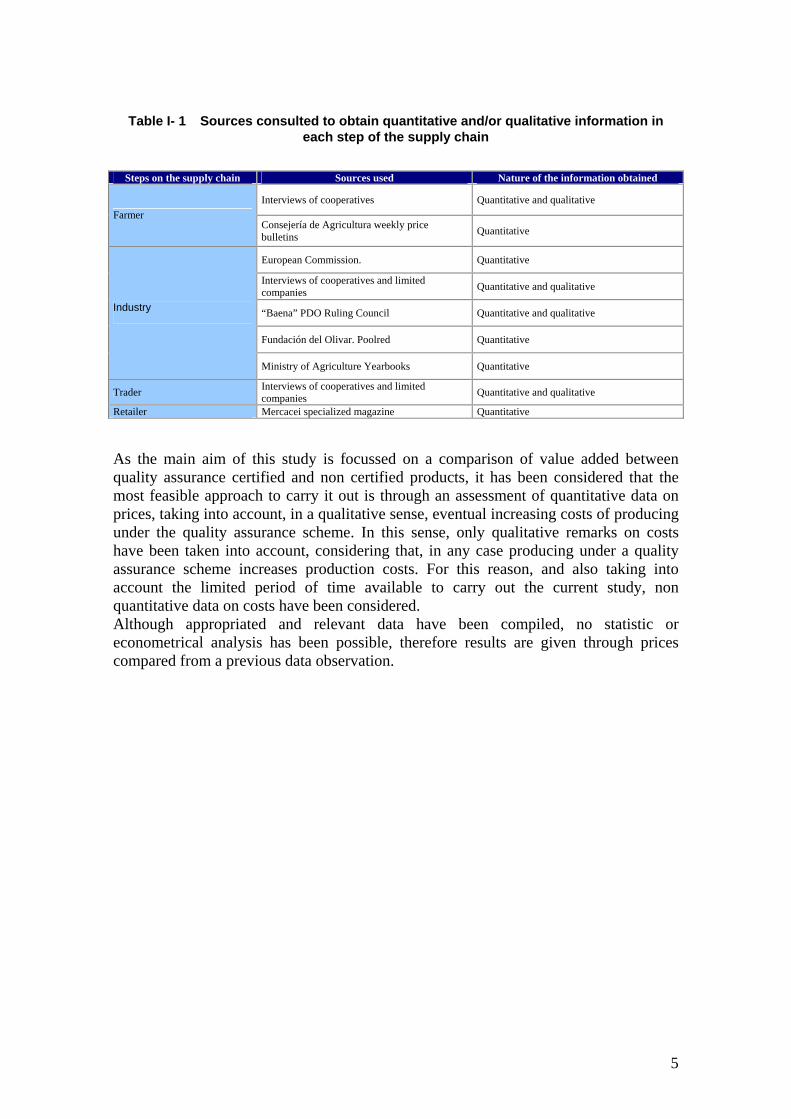

In order to reach the previously mentioned objectives of the study, two different approaches have been carried out. First, a revision of previous studies and information available on the specific scheme and the olive oil sector has been conducted, which constitutes the secondary information approach. In this stage existing previous studies or published information have been consulted from different sources such as official institutions (Agricultural Ministry publications, Regional Agricultural Ministry Price Bulletins, Ruling Council Yearbooks, etc), specialized magazines’ sections and articles and specialized web sites. Secondly, some primary information has been obtained from interviews to representatives of the stakeholders on the QAS. These interviews have been carried out in the form of semi-structured questionnaires addressed to Ruling Councils, farmers, cooperatives and limited companies which have been visited and/or telephoned. A model for each questionnaire can be found in the Annex 1 and a description of each of the firms interviewed can be found in Annex 2. The questionnaire basically contains questions on prices, quantities as well as more descriptive aspects on the food supply chain. A total number of 6 interviews were conducted between the 10th and 20th October in Baena and Córdoba, Spain. Both approaches have provided quantitative and qualitative information useful for the purposes of the study. The following Table I- 1 includes a list of the different sources that have been consulted to obtain quantitative information on each step of the supply chain. Each of the steps considered is referred to prices to which the mentioned stakeholder sell the product to the following stakeholder in the supply chain, e.g., farmer stage refers to prices of the farmer to the industry. All of these sources have provided quantitative information and some descriptive or qualitative information have been obtained as it is specified below.

1 In spite of the research have been focused in these two presentations (see questionnaries in Annex 1), almost all comments regarding to quantities and prices in this report are refered to 5 liters tin, due to sales in glass bottle means less than 2% of total olive oil commerzialiced under PDO protection.

5

Table I- 1 Sources consulted to obtain quantitative and/or qualitative information in each step of the supply chain

Steps on the supply chain Sources used Nature of the information obtained

Interviews of cooperatives Quantitative and qualitative Farmer

Consejería de Agricultura weekly price bulletins Quantitative

European Commission. Quantitative

Interviews of cooperatives and limited companies Quantitative and qualitative

“Baena” PDO Ruling Council Quantitative and qualitative

Fundación del Olivar. Poolred Quantitative

Industry

Ministry of Agriculture Yearbooks Quantitative

Trader Interviews of cooperatives and limited companies Quantitative and qualitative

Retailer Mercacei specialized magazine Quantitative As the main aim of this study is focussed on a comparison of value added between quality assurance certified and non certified products, it has been considered that the most feasible approach to carry it out is through an assessment of quantitative data on prices, taking into account, in a qualitative sense, eventual increasing costs of producing under the quality assurance scheme. In this sense, only qualitative remarks on costs have been taken into account, considering that, in any case producing under a quality assurance scheme increases production costs. For this reason, and also taking into account the limited period of time available to carry out the current study, non quantitative data on costs have been considered. Although appropriated and relevant data have been compiled, no statistic or econometrical analysis has been possible, therefore results are given through prices compared from a previous data observation.

6

CASE STUDY: PDO “Baena” olive oil

Introduction to the product: Olive oil

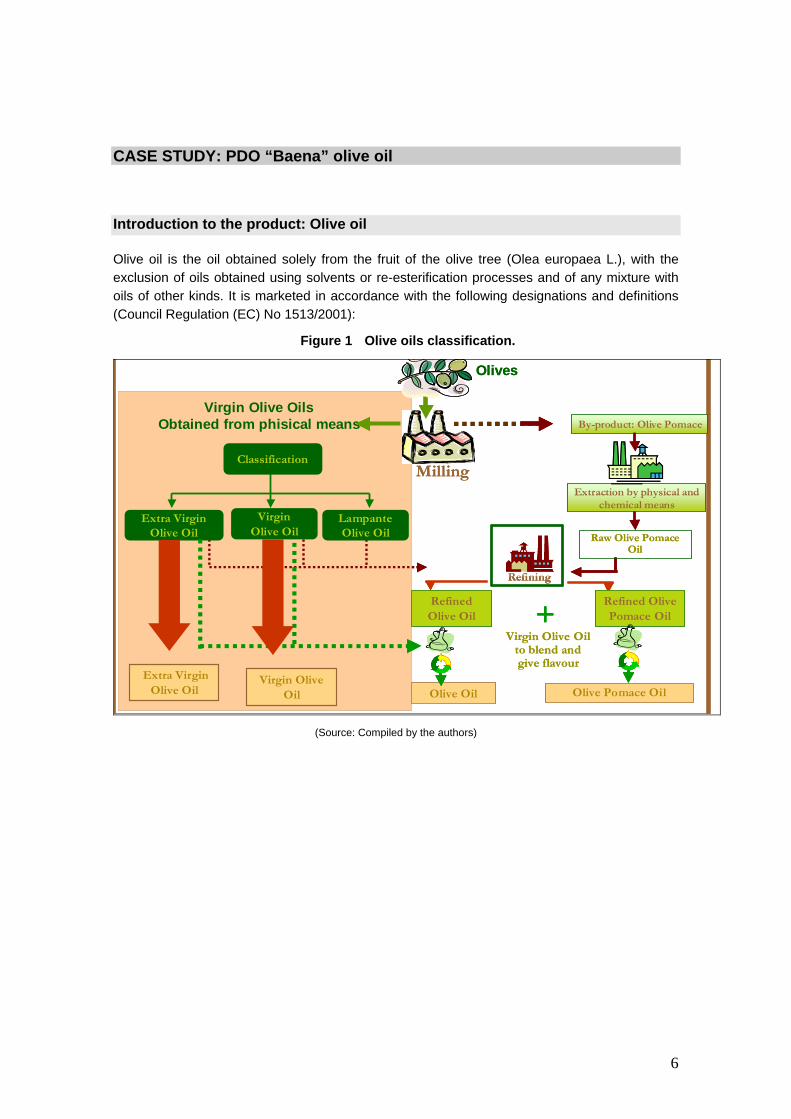

Olive oil is the oil obtained solely from the fruit of the olive tree (Olea europaea L.), with the exclusion of oils obtained using solvents or re-esterification processes and of any mixture with oils of other kinds. It is marketed in accordance with the following designations and definitions (Council Regulation (EC) No 1513/2001):

Figure 1 Olive oils classification.

Virgin Olive OilsObtained from phisical means

Extra VirginOlive Oil

Classification

Lampante Olive Oil

VirginOlive Oil

Extra Virgin Olive Oil

Virgin Olive Oil Olive Pomace OilOlive Oil

RefinedOlive Oil +

By-product: Olive Pomace

Extraction by physical and chemical means

Raw Olive Pomace Oil

Refined Olive Pomace Oil

Virgin Olive Oil to blend and give flavour

Milling

Refining

Olives

Virgin Olive OilsObtained from phisical means

Extra VirginOlive Oil

Classification

Lampante Olive Oil

VirginOlive Oil

Extra Virgin Olive Oil

Virgin Olive Oil Olive Pomace OilOlive Oil

RefinedOlive Oil +

By-product: Olive Pomace

Extraction by physical and chemical means

Raw Olive Pomace Oil

Refined Olive Pomace Oil

Virgin Olive Oil to blend and give flavour

Milling

Refining Refining

Olives

(Source: Compiled by the authors)

7

1. VIRGIN OLIVE OILS Oils obtained from the fruit of the olive tree solely by mechanical or other physical means under conditions that do not lead to alteration in the oil, which have not undergone any treatment other than washing, decantation, centrifugation or filtration, to the exclusion of oils obtained using solvents or using adjuvants having a chemical or biochemical action, or by re-esterification process and any mixture with oils of other kinds. Virgin olive oils are exclusively classified and described as follows: (a) Extra virgin olive oil Virgin olive oil having a maximum free acidity, in terms of oleic acid, of 0,8 g per 100 g, the other characteristics of which comply with those laid down for this category. (b) Virgin olive oil Virgin olive oil having a maximum free acidity, in terms of oleic acid, of 2 g per 100 g, the other characteristics of which comply with those laid down for this category. (c) Lampante olive oil Virgin olive oil having a free acidity, in terms of oleic acid, of more than 2 g per 100 g, and/or the other characteristics of which comply with those laid down for this category.

2. REFINED OLIVE OIL Olive oil obtained by refining virgin olive oil, having a free acidity content expressed as oleic acid, of not more than 0,3 g per 100 g, and the other characteristics of which comply with those laid down for this category.

3. OLIVE OIL - COMPOSED OF REFINED OLIVE OILS AND VIRGIN OLIVE OILS Olive oil obtained by blending refined olive oil and virgin olive oil other than lampante oil, having a free acidity content expressed as oleic acid, of not more than 1 g per 100 g, and the other characteristics of which comply with those laid down for this category.

4. CRUDE OLIVE-POMACE OIL Oil obtained from olive pomace by treatment with solvents or by physical means or oil corresponding to lampante olive oil, except for certain specified characteristics, excluding oil obtained by means of re-esterification and mixtures with other types of oils, and the other characteristics of which comply with those laid down for this category.

5. REFINED OLIVE-POMACE OIL Oil obtained by refining crude olive-pomace oil, having a free acidity content expressed as oleic acid, of not more than 0,3 g per 100 g, and the other characteristics of which comply with those laid down for this category.

6. OLIVE-POMACE OIL Oil obtained by blending refined olive-pomace oil and virgin olive oil other than lampante oil, having a free acidity content expressed as oleic acid, of not more than 1 g per 100 g, and the other characteristics of which comply with those laid down for this category."

8

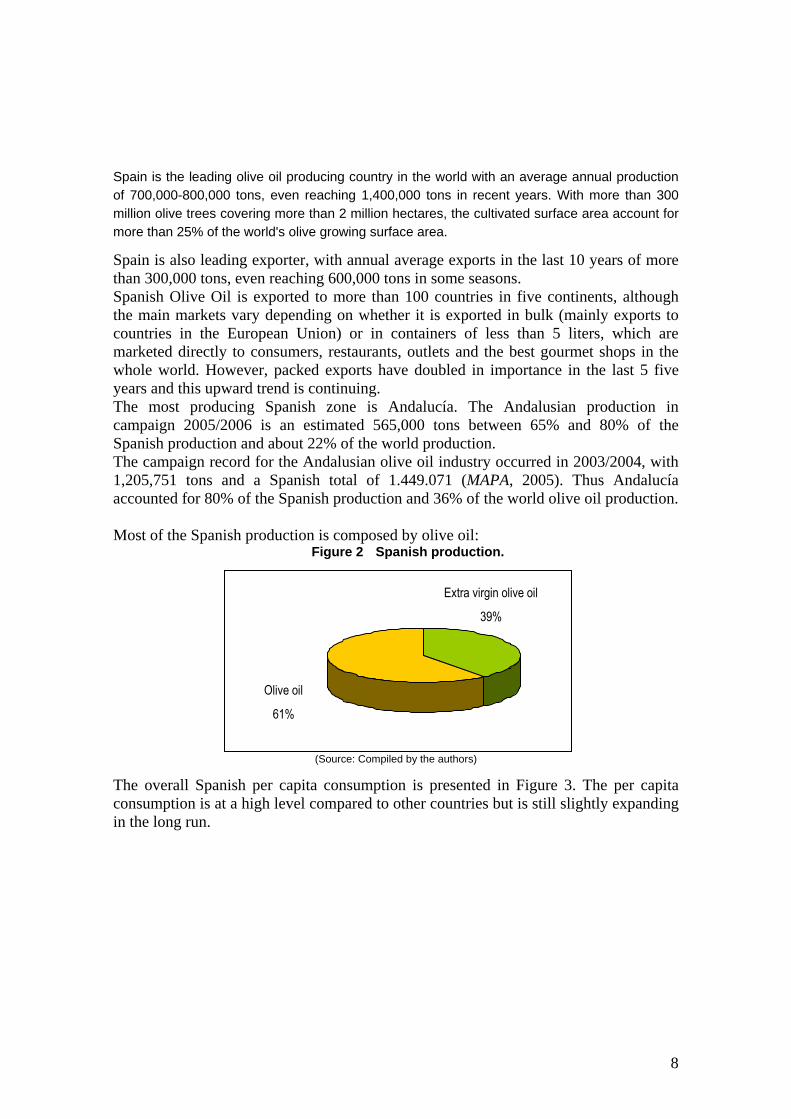

Spain is the leading olive oil producing country in the world with an average annual production of 700,000-800,000 tons, even reaching 1,400,000 tons in recent years. With more than 300 million olive trees covering more than 2 million hectares, the cultivated surface area account for more than 25% of the world's olive growing surface area.

Spain is also leading exporter, with annual average exports in the last 10 years of more than 300,000 tons, even reaching 600,000 tons in some seasons. Spanish Olive Oil is exported to more than 100 countries in five continents, although the main markets vary depending on whether it is exported in bulk (mainly exports to countries in the European Union) or in containers of less than 5 liters, which are marketed directly to consumers, restaurants, outlets and the best gourmet shops in the whole world. However, packed exports have doubled in importance in the last 5 five years and this upward trend is continuing. The most producing Spanish zone is Andalucía. The Andalusian production in campaign 2005/2006 is an estimated 565,000 tons between 65% and 80% of the Spanish production and about 22% of the world production. The campaign record for the Andalusian olive oil industry occurred in 2003/2004, with 1,205,751 tons and a Spanish total of 1.449.071 (MAPA, 2005). Thus Andalucía accounted for 80% of the Spanish production and 36% of the world olive oil production. Most of the Spanish production is composed by olive oil:

Figure 2 Spanish production.

Extra virgin olive oil

39%

Olive oil

61%

Extra virgin olive oil

39%

Extra virgin olive oil

39%

Olive oil

61%

(Source: Compiled by the authors)

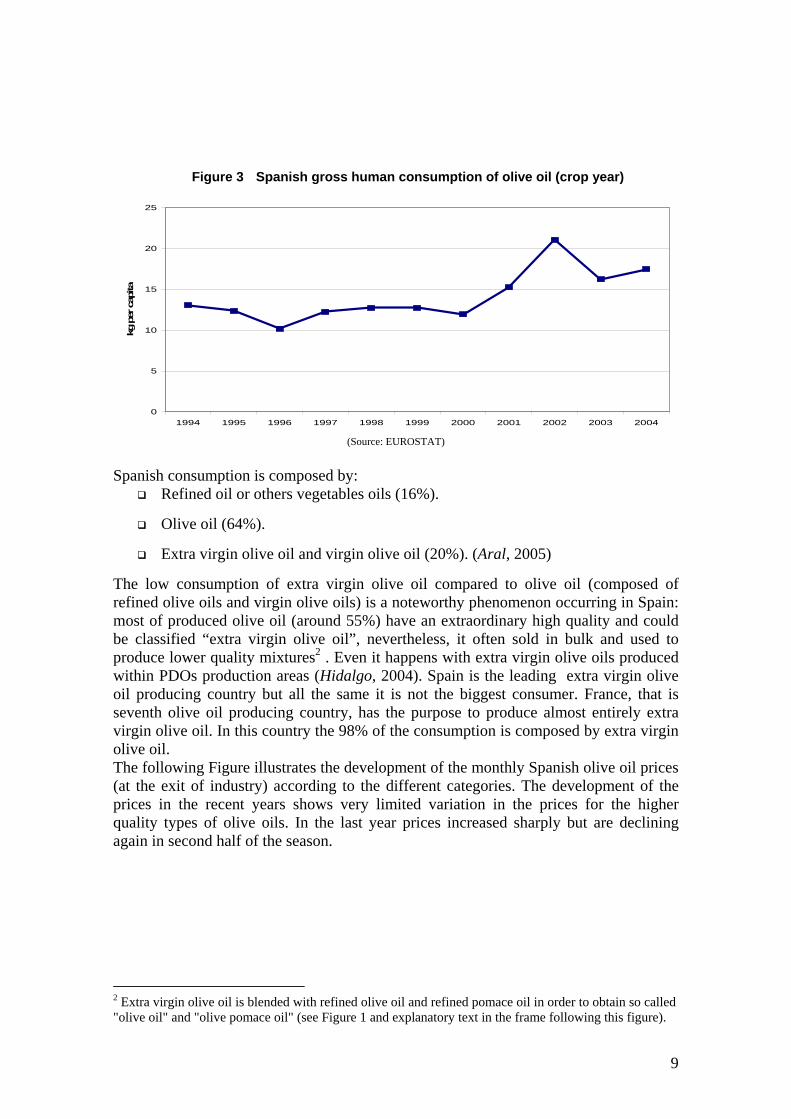

The overall Spanish per capita consumption is presented in Figure 3. The per capita consumption is at a high level compared to other countries but is still slightly expanding in the long run.

9

Figure 3 Spanish gross human consumption of olive oil (crop year)

0

5

10

15

20

25

1994 1995 1996 1997 1998 1999 2000 2001 2002 2003 2004

kg p

er c

apita

(Source: EUROSTAT)

Spanish consumption is composed by:

Refined oil or others vegetables oils (16%).

Olive oil (64%).

Extra virgin olive oil and virgin olive oil (20%). (Aral, 2005)

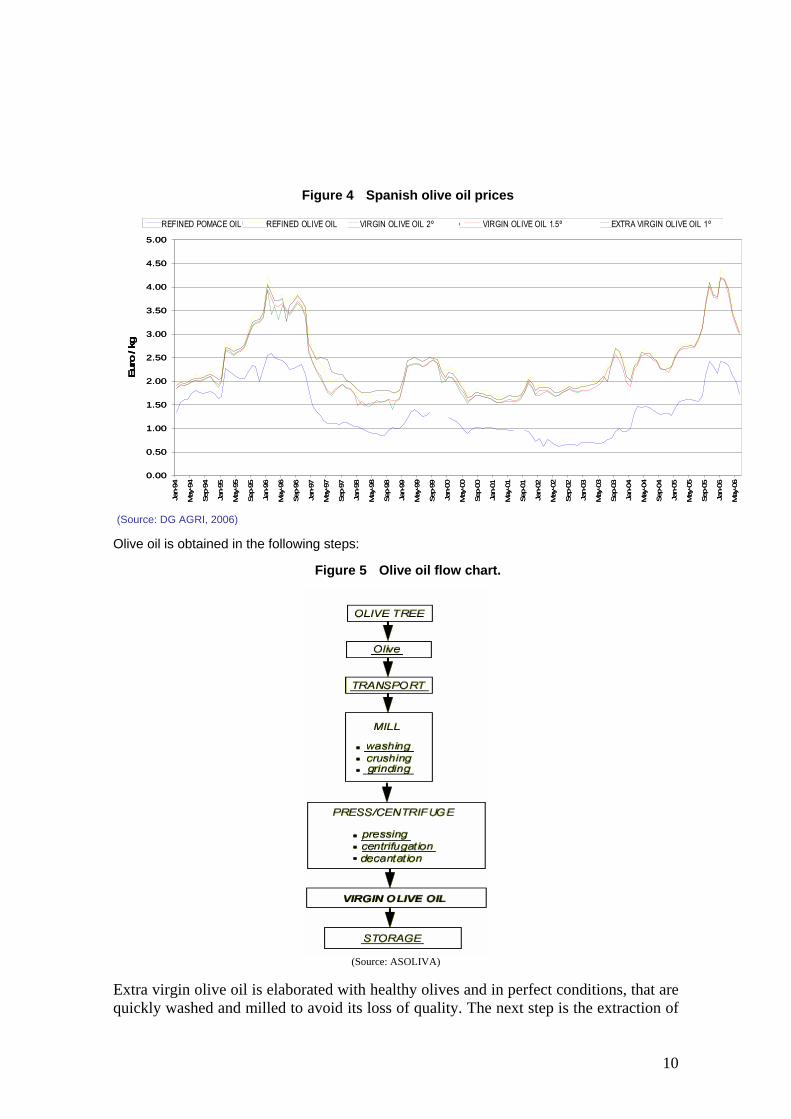

The low consumption of extra virgin olive oil compared to olive oil (composed of refined olive oils and virgin olive oils) is a noteworthy phenomenon occurring in Spain: most of produced olive oil (around 55%) have an extraordinary high quality and could be classified “extra virgin olive oil”, nevertheless, it often sold in bulk and used to produce lower quality mixtures2 . Even it happens with extra virgin olive oils produced within PDOs production areas (Hidalgo, 2004). Spain is the leading extra virgin olive oil producing country but all the same it is not the biggest consumer. France, that is seventh olive oil producing country, has the purpose to produce almost entirely extra virgin olive oil. In this country the 98% of the consumption is composed by extra virgin olive oil. The following Figure illustrates the development of the monthly Spanish olive oil prices (at the exit of industry) according to the different categories. The development of the prices in the recent years shows very limited variation in the prices for the higher quality types of olive oils. In the last year prices increased sharply but are declining again in second half of the season.

2 Extra virgin olive oil is blended with refined olive oil and refined pomace oil in order to obtain so called "olive oil" and "olive pomace oil" (see Figure 1 and explanatory text in the frame following this figure).

10

Figure 4 Spanish olive oil prices

0.00

0.50

1.00

1.50

2.00

2.50

3.00

3.50

4.00

4.50

5.00

Jan-

94

May

-94

Sep

-94

Jan-

95

May

-95

Sep

-95

Jan-

96

May

-96

Sep

-96

Jan-

97

May

-97

Sep

-97

Jan-

98

May

-98

Sep

-98

Jan-

99

May

-99

Sep

-99

Jan-

00

May

-00

Sep

-00

Jan-

01

May

-01

Sep

-01

Jan-

02

May

-02

Sep

-02

Jan-

03

May

-03

Sep

-03

Jan-

04

May

-04

Sep

-04

Jan-

05

May

-05

Sep

-05

Jan-

06

May

-06

Euro

/ kg

ORUJO REFINADO OLIVA REFINADO OLIVA VIRGEN FINO 2% OLIVA VIRGEN FINO 1,5% OLIVA VIRGEN EXTRA 1%REFINED POMACE OIL REFINED OLIVE OIL VIRGIN OLIVE OIL 2º VIRGIN OLIVE OIL 1.5º EXTRA VIRGIN OLIVE OIL 1º

0.00

0.50

1.00

1.50

2.00

2.50

3.00

3.50

4.00

4.50

5.00

Jan-

94

May

-94

Sep

-94

Jan-

95

May

-95

Sep

-95

Jan-

96

May

-96

Sep

-96

Jan-

97

May

-97

Sep

-97

Jan-

98

May

-98

Sep

-98

Jan-

99

May

-99

Sep

-99

Jan-

00

May

-00

Sep

-00

Jan-

01

May

-01

Sep

-01

Jan-

02

May

-02

Sep

-02

Jan-

03

May

-03

Sep

-03

Jan-

04

May

-04

Sep

-04

Jan-

05

May

-05

Sep

-05

Jan-

06

May

-06

Euro

/ kg

ORUJO REFINADO OLIVA REFINADO OLIVA VIRGEN FINO 2% OLIVA VIRGEN FINO 1,5% OLIVA VIRGEN EXTRA 1%REFINED POMACE OIL REFINED OLIVE OIL VIRGIN OLIVE OIL 2º VIRGIN OLIVE OIL 1.5º EXTRA VIRGIN OLIVE OIL 1º

(Source: DG AGRI, 2006)

Olive oil is obtained in the following steps:

Figure 5 Olive oil flow chart.

(Source: ASOLIVA)

Extra virgin olive oil is elaborated with healthy olives and in perfect conditions, that are quickly washed and milled to avoid its loss of quality. The next step is the extraction of

11

the oil in low temperature conditions. Later the olive oil is stored in warehouses, in deposits suitable for its conservation in order that possible aroma and flavour cannot distort the sensorial qualities of the green or mature olive. Often the consumer does not know the existence of a very strict methodology that approaches the sensorial evaluation of extra virgin olive oil by professional tasting panels. According to this expert panel, an extra virgin olive oil must be a product with an irreproachable flavour and aroma, that presents zero defects. The defects counted are imperceptibles by most of consumers, and it is very hard to perceive some aroma to know they belong to a certain category of defects (wine flavour, rancid, humid, among others).

Overview of the QAS

Organization and general objectives of the scheme

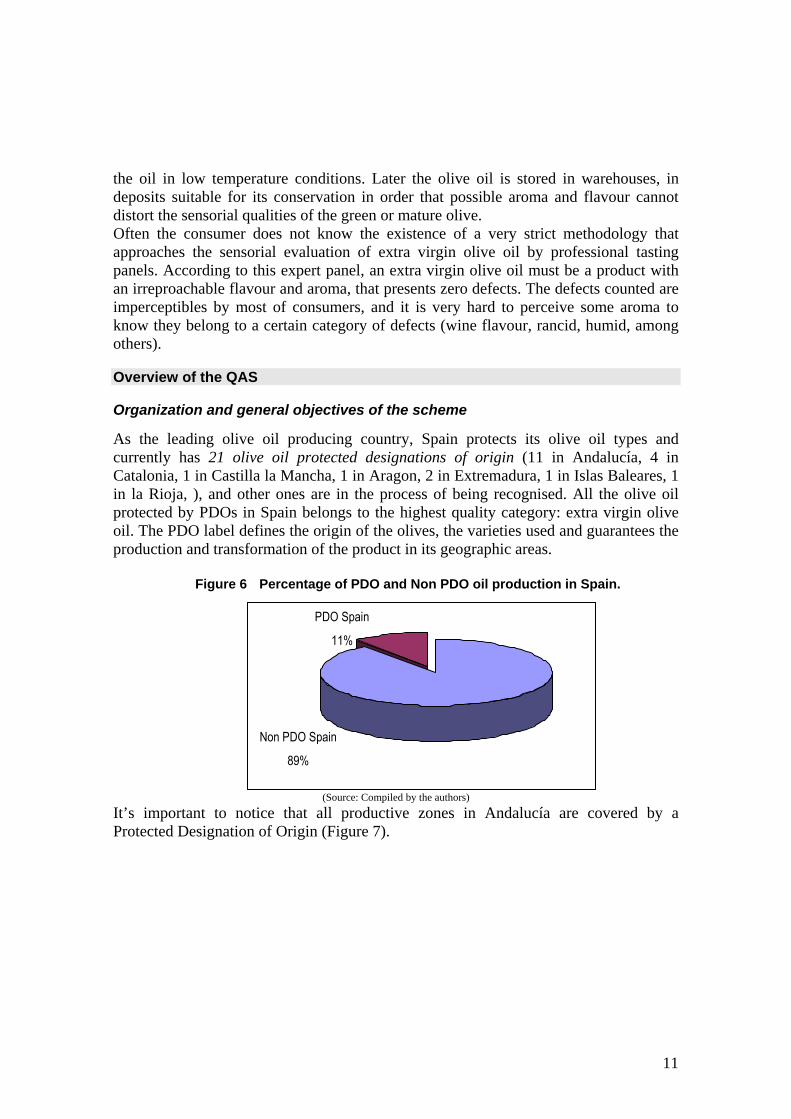

As the leading olive oil producing country, Spain protects its olive oil types and currently has 21 olive oil protected designations of origin (11 in Andalucía, 4 in Catalonia, 1 in Castilla la Mancha, 1 in Aragon, 2 in Extremadura, 1 in Islas Baleares, 1 in la Rioja, ), and other ones are in the process of being recognised. All the olive oil protected by PDOs in Spain belongs to the highest quality category: extra virgin olive oil. The PDO label defines the origin of the olives, the varieties used and guarantees the production and transformation of the product in its geographic areas.

Figure 6 Percentage of PDO and Non PDO oil production in Spain.

Non PDO Spain

89%

PDO Spain

11%

Non PDO Spain

89%

PDO Spain

11%

(Source: Compiled by the authors)

It’s important to notice that all productive zones in Andalucía are covered by a Protected Designation of Origin (Figure 7).

12

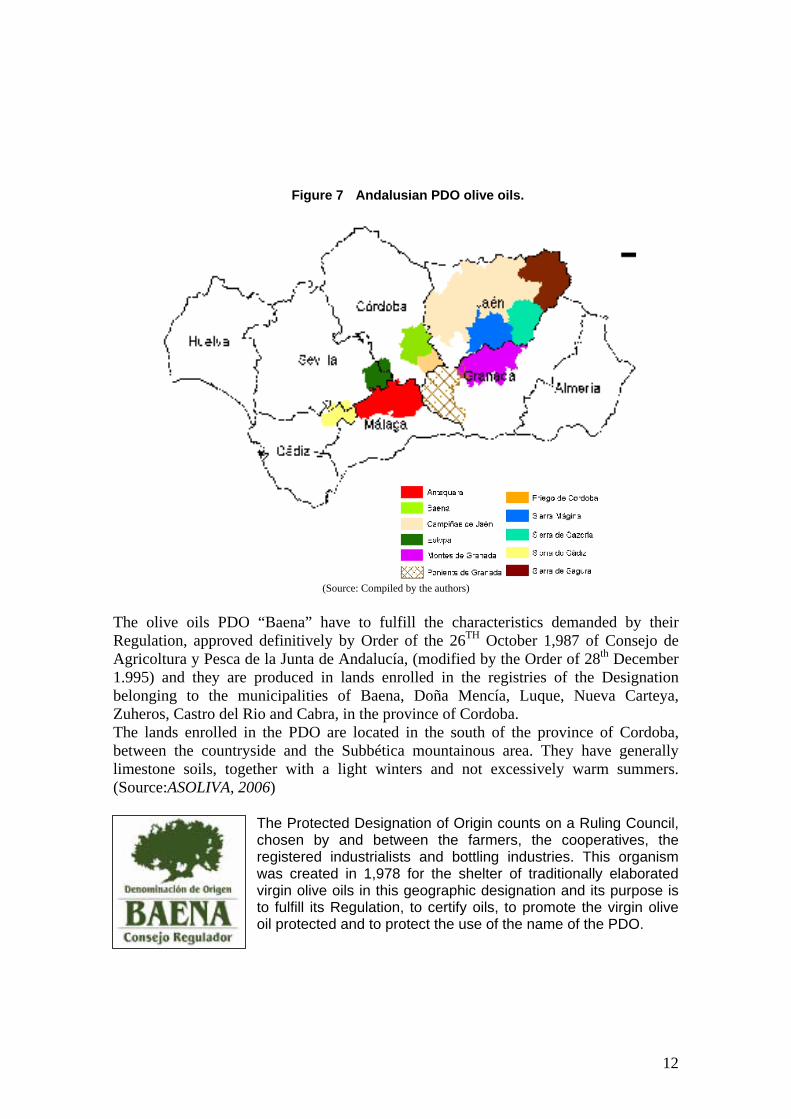

Figure 7 Andalusian PDO olive oils.

(Source: Compiled by the authors)

The olive oils PDO “Baena” have to fulfill the characteristics demanded by their Regulation, approved definitively by Order of the 26TH October 1,987 of Consejo de Agricoltura y Pesca de la Junta de Andalucía, (modified by the Order of 28th December 1.995) and they are produced in lands enrolled in the registries of the Designation belonging to the municipalities of Baena, Doña Mencía, Luque, Nueva Carteya, Zuheros, Castro del Rio and Cabra, in the province of Cordoba. The lands enrolled in the PDO are located in the south of the province of Cordoba, between the countryside and the Subbética mountainous area. They have generally limestone soils, together with a light winters and not excessively warm summers. (Source:ASOLIVA, 2006)

The Protected Designation of Origin counts on a Ruling Council, chosen by and between the farmers, the cooperatives, the registered industrialists and bottling industries. This organism was created in 1,978 for the shelter of traditionally elaborated virgin olive oils in this geographic designation and its purpose is to fulfill its Regulation, to certify oils, to promote the virgin olive oil protected and to protect the use of the name of the PDO.

13

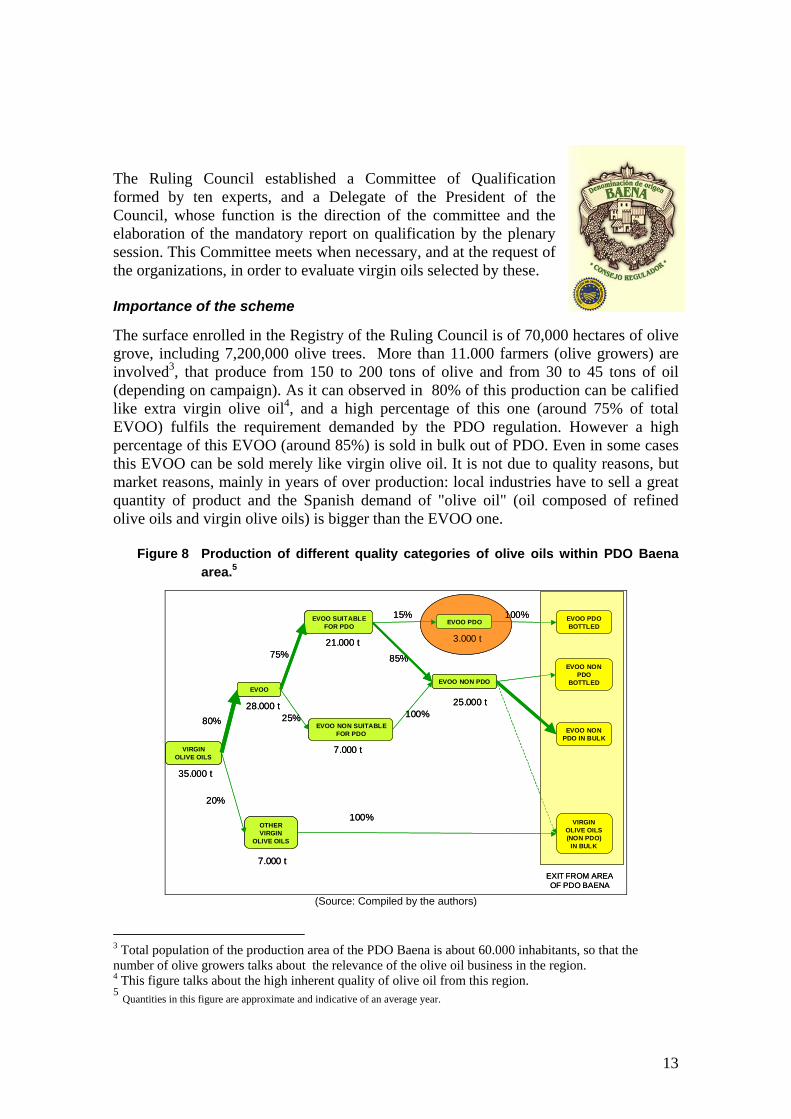

The Ruling Council established a Committee of Qualification formed by ten experts, and a Delegate of the President of the Council, whose function is the direction of the committee and the elaboration of the mandatory report on qualification by the plenary session. This Committee meets when necessary, and at the request of the organizations, in order to evaluate virgin oils selected by these. Importance of the scheme

The surface enrolled in the Registry of the Ruling Council is of 70,000 hectares of olive grove, including 7,200,000 olive trees. More than 11.000 farmers (olive growers) are involved3, that produce from 150 to 200 tons of olive and from 30 to 45 tons of oil (depending on campaign). As it can observed in 80% of this production can be calified like extra virgin olive oil4, and a high percentage of this one (around 75% of total EVOO) fulfils the requirement demanded by the PDO regulation. However a high percentage of this EVOO (around 85%) is sold in bulk out of PDO. Even in some cases this EVOO can be sold merely like virgin olive oil. It is not due to quality reasons, but market reasons, mainly in years of over production: local industries have to sell a great quantity of product and the Spanish demand of "olive oil" (oil composed of refined olive oils and virgin olive oils) is bigger than the EVOO one.

Figure 8 Production of different quality categories of olive oils within PDO Baena area.5

VIRGIN OLIVE OILS

EVOO

OTHER VIRGIN

OLIVE OILS

EVOO SUITABLE FOR PDO

EVOO NON SUITABLE FOR PDO

EVOO PDO

EVOO NON PDO

EVOO PDO BOTTLED

EVOO NON PDO

BOTTLED

EVOO NON PDO IN BULK

VIRGIN OLIVE OILS (NON PDO)

IN BULK

80%

20%

EXIT FROM AREA OF PDO BAENA

35.000 t

28.000 t

75%

25%

21.000 t

7.000 t

15%

85%

3.000 t

100%

100%

100%

25.000 t

7.000 t

VIRGIN OLIVE OILS

EVOO

OTHER VIRGIN

OLIVE OILS

EVOO SUITABLE FOR PDO

EVOO NON SUITABLE FOR PDO

EVOO PDO

EVOO NON PDO

EVOO PDO BOTTLED

EVOO NON PDO

BOTTLED

EVOO NON PDO IN BULK

VIRGIN OLIVE OILS (NON PDO)

IN BULK

80%

20%

EXIT FROM AREA OF PDO BAENA

35.000 t

28.000 t

75%

25%

21.000 t

7.000 t

15%

85%

3.000 t

100%

100%

100%

25.000 t

7.000 t

(Source: Compiled by the authors)

3 Total population of the production area of the PDO Baena is about 60.000 inhabitants, so that the number of olive growers talks about the relevance of the olive oil business in the region. 4 This figure talks about the high inherent quality of olive oil from this region. 5 Quantities in this figure are approximate and indicative of an average year.

14

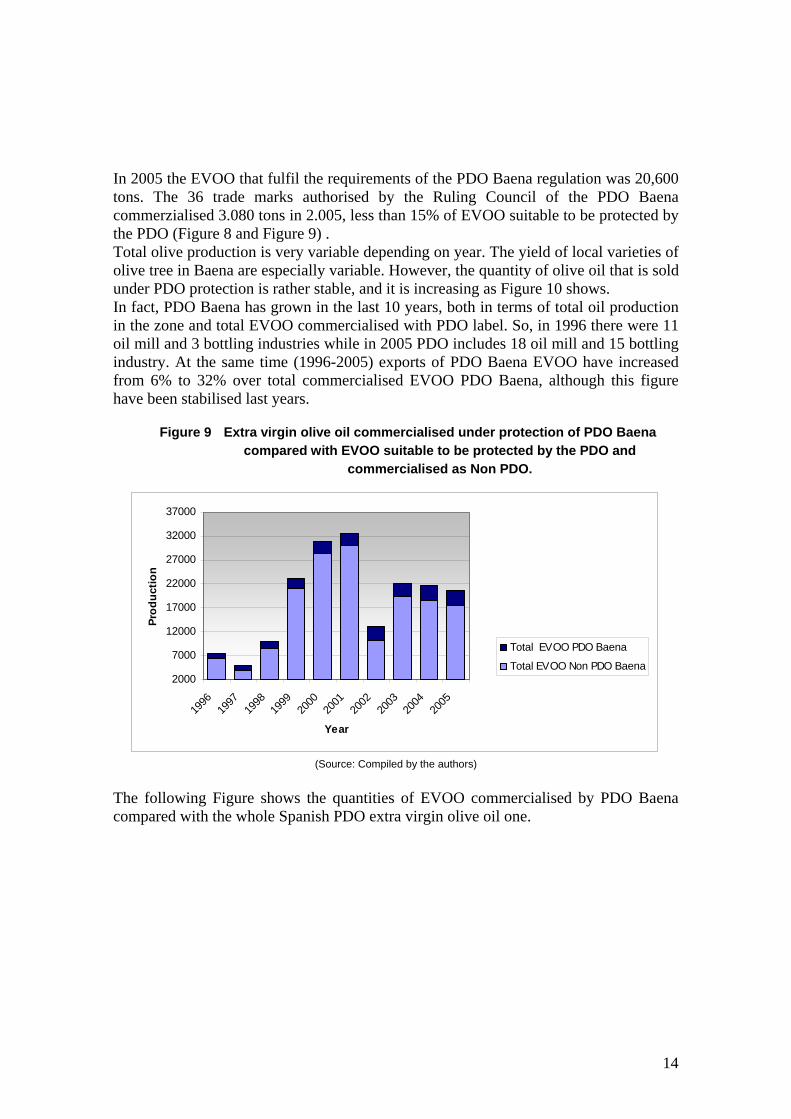

In 2005 the EVOO that fulfil the requirements of the PDO Baena regulation was 20,600 tons. The 36 trade marks authorised by the Ruling Council of the PDO Baena commerzialised 3.080 tons in 2.005, less than 15% of EVOO suitable to be protected by the PDO (Figure 8 and Figure 9) . Total olive production is very variable depending on year. The yield of local varieties of olive tree in Baena are especially variable. However, the quantity of olive oil that is sold under PDO protection is rather stable, and it is increasing as Figure 10 shows. In fact, PDO Baena has grown in the last 10 years, both in terms of total oil production in the zone and total EVOO commercialised with PDO label. So, in 1996 there were 11 oil mill and 3 bottling industries while in 2005 PDO includes 18 oil mill and 15 bottling industry. At the same time (1996-2005) exports of PDO Baena EVOO have increased from 6% to 32% over total commercialised EVOO PDO Baena, although this figure have been stabilised last years.

Figure 9 Extra virgin olive oil commercialised under protection of PDO Baena

compared with EVOO suitable to be protected by the PDO and commercialised as Non PDO.

2000

7000

12000

17000

22000

27000

32000

37000

1996

1997

1998

1999

2000

2001

2002

2003

2004

2005

Year

Prod

uctio

n

Total EVOO PDO Baena

Total EVOO Non PDO Baena

(Source: Compiled by the authors)

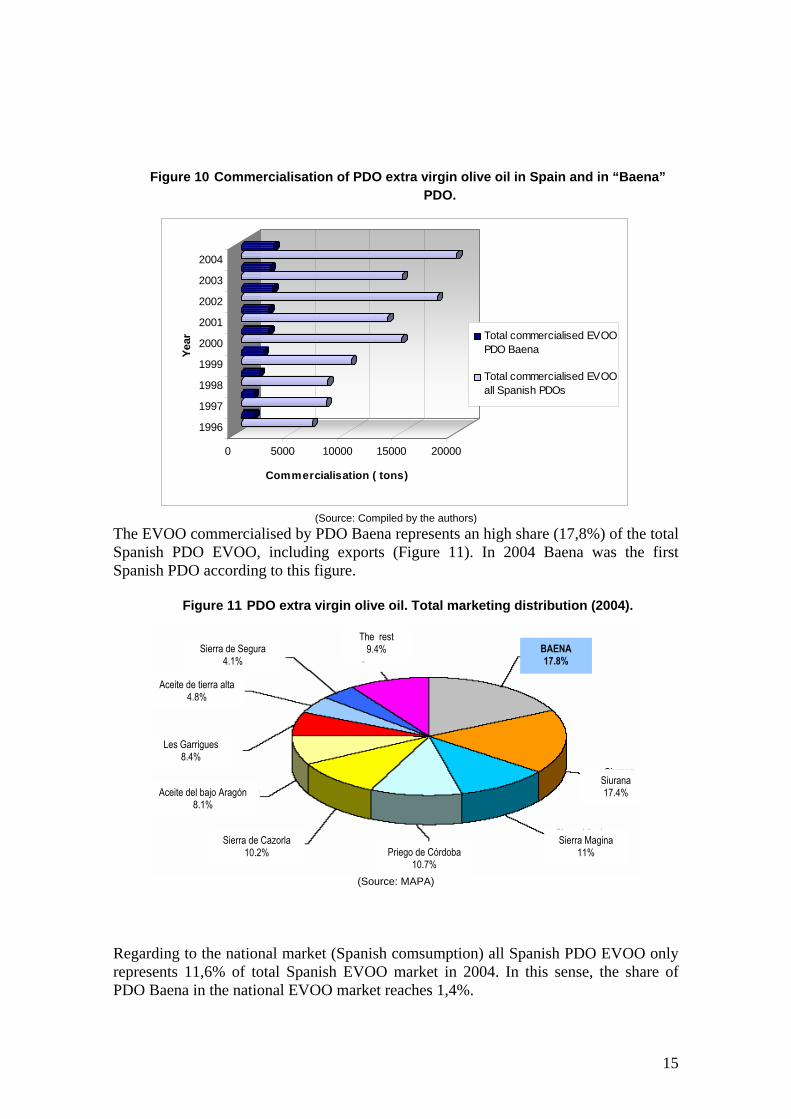

The following Figure shows the quantities of EVOO commercialised by PDO Baena compared with the whole Spanish PDO extra virgin olive oil one.

15

Figure 10 Commercialisation of PDO extra virgin olive oil in Spain and in “Baena” PDO.

0 5000 10000 15000 20000

Commercialisation ( tons)

1996

1997

1998

1999

2000

2001

2002

2003

2004

Year Total commercialised EVOO

PDO Baena

Total commercialised EVOOall Spanish PDOs

(Source: Compiled by the authors)

The EVOO commercialised by PDO Baena represents an high share (17,8%) of the total Spanish PDO EVOO, including exports (Figure 11). In 2004 Baena was the first Spanish PDO according to this figure.

Figure 11 PDO extra virgin olive oil. Total marketing distribution (2004).

(Source: MAPA)

Regarding to the national market (Spanish comsumption) all Spanish PDO EVOO only represents 11,6% of total Spanish EVOO market in 2004. In this sense, the share of PDO Baena in the national EVOO market reaches 1,4%.

Aceite del bajo Aragón 8.1%

Priego de Córdoba 10.7%

Sierra Magina 11%

BAENA 17.8%

Siurana 17.4%

The rest 9.4% Sierra de Segura

4.1%

Aceite de tierra alta 4.8%

Les Garrigues 8.4%

Sierra de Cazorla 10.2%

16

In the last 10 years an average of 9.300 tons per year of PDO olive oil in Spain was sold. Approximately 16% of this is Baena PDO olive oil.

1996 1997 1998 1999 2000 2001 2002 2003 2004Baena PDO commercialised in Spain (Ton) 1.068 758 1.410 1.500 1.800 1.800 1.975 1.985 2.009PDO commercialised in Spain (Ton) 5.051 6.167 5.932 8.422 10.612 10.640 12.195 12.833 16.841

Last 6 years the price of the bottled oil PDO Baena at the exit of the local industry has been quite stable (and slightly increasing) as the next graph shows (Figure 12)

Figure 12 Price and commercialised production of extra virgin olive oil PDO Baena.

500 1000 1500 2000 2500 3000 3500

1996 1997 1998 1999 2000 2001 20022003 2004 2005

Year

Tons

0,00

1,00

2,00

3,00

4,00

5,00

6,00

7,00

Price (Euro/kg)

Total PDO Baena EVOO (commercialised Price of bottled PDO Baena EVOO (Exit of industry)

(Source: Compiled by the authors)

PDO fulfils several general commercial functions, that generate added value to PDO brands:

Guarantees that foodstuffs are produced, processed and prepared in a given geographical area using a recognised know-how.

Protects product names from misuse and imitation.

Sends to the market quality assurance signals of the product beyond the specific organoleptic characteristics (O’Neil and Charters, 2000).

Reduces risk associated with the product purchase.

Makes easy consumer purchasing decision by structuring the supply (Erdem, 1998).

Furthermore, the entrance in operation of quality signs induces in the regional olive oil business improvements such as: − a greater control in the production,

17

− an improvement of commercial presentations of products (only tin an glass bottle are allowed to package PDO Baena olive oil, and there are a general awareness to improve design of label),

− an increase of the packaging in origin (before PDO establishment in Baena zone, almost all the olive oil was sold in bulk by cooperatives) so higher share of value added remains in producing regions),

− a better advantage of the segments of the suitable niches of market, so there are presence of PDO Baena EVOO in delicatessen shops and in the specialized zone of great stores.

In addition PDO affects on the effort of the tourist reclamations (wine tourism, tourism surroundings to the olive grove, typical candies, etc.), So that the importance of the PDO is related also to the concept of prestige of the area: through the designation the zone of Baena has been well-known and now it’s being developed a rural tourism6 every day in increase (Langreo, 2004). It reinforces a regional feeling (rural identity), among the different rural communities (municipalities) included in the PDO production area, under the driving force of the olive oil production. Regulatory requirements and controls.

The requirements for PDO extra virgin olive oils are described in the Regulation. In the olive production phase the Regulation specifies:

The allowed olive varieties.

The PDO area demarcation.

The harvesting date

Norms on the collection rate of the olive by zones, in order to be in relation to the capacity of absorption of oil mills.

In the oil production phase there are norms about: • Maximum duration of olive milling.

• Hygienic and sanitary characteristics of the oil mills.

• Extraction technique.

• Oil storage conditions.

6 In fact an incipient hotel industry (and leisure business in general) has been developed last years in the area, although it is difficult to measure its economic and social impact within the region, as well as distinguishing the efects of PDO from the success of rural development policy. Many of the restaurants, hotels, museums and rural houses of the region are closely linked to the olive oil culture, so many of them takes adventage from ancient milling industries and typical rural cottage. In this region (where local economy is based exclusively on agriculture) rural tourism was very less development some years ago. .

18

• Chemical and physical oil characteristics (acidity, colour, humidity, peroxides, impurities).

• Organoleptic characteristics. Periodically the Ruling Council organize a oil tasting to determine the level of negative and positive attributes of the oil. There is a scale and the components of the panel test decide the apt oil to be commercialized with PDO.

The packaging is also controlled by the Regulation, so that an oil can be certified with “Designation of Origin BAENA”, if it is package in anyone of the sixteen packing plants enrolled in the Registries of the PDO (six Societies and ten of different legal personality), in tin plate or glass bottles. In addition the bottle or tin has a special label with an identification number given by the Ruling Council. All these requirements and controls intend to guarantee the consumers that the extra virgin olive oil, with designation of origin Baena, is an olive oil that comes from the origin that gives the name, and it has a registered and guaranteed quality. Products covered by the scheme

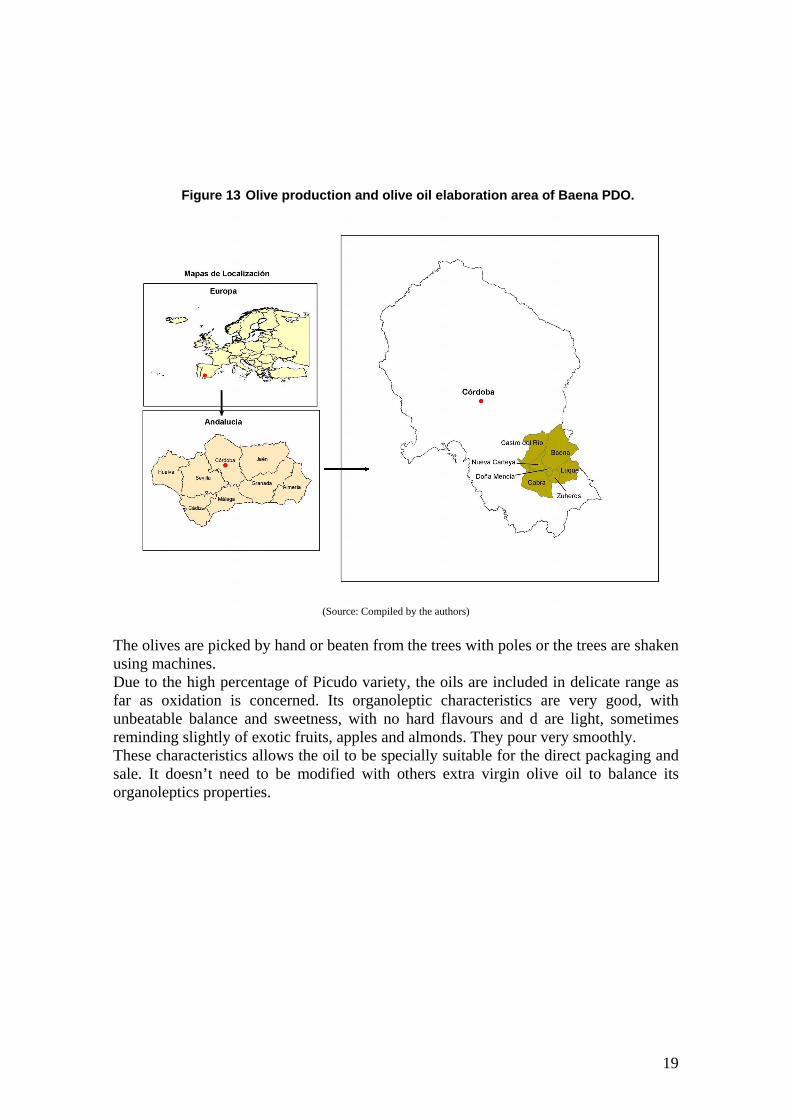

The producing area of this designation is in the south-east of the province of Cordoba, covering the 7 municipal areas (Figure 12). It protects extra virgin olive oils produced from different Spanish varieties.

19

Figure 13 Olive production and olive oil elaboration area of Baena PDO.

(Source: Compiled by the authors)

The olives are picked by hand or beaten from the trees with poles or the trees are shaken using machines. Due to the high percentage of Picudo variety, the oils are included in delicate range as far as oxidation is concerned. Its organoleptic characteristics are very good, with unbeatable balance and sweetness, with no hard flavours and d are light, sometimes reminding slightly of exotic fruits, apples and almonds. They pour very smoothly. These characteristics allows the oil to be specially suitable for the direct packaging and sale. It doesn’t need to be modified with others extra virgin olive oil to balance its organoleptics properties.

20

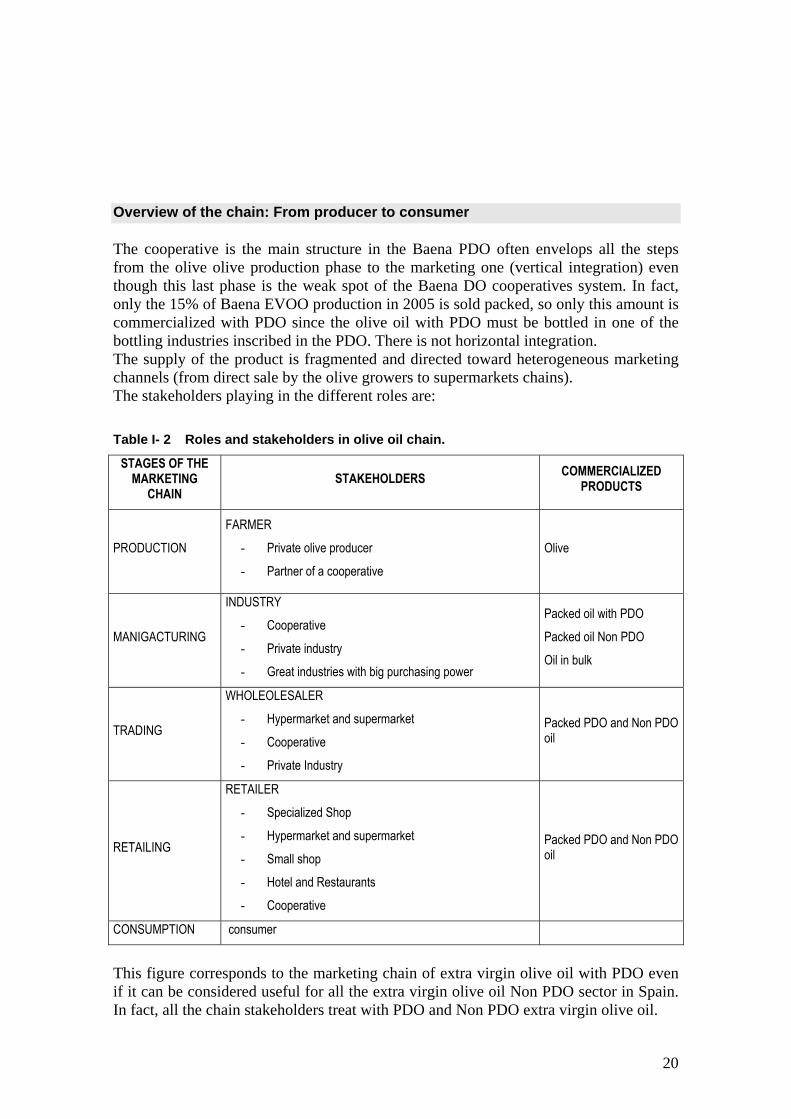

Overview of the chain: From producer to consumer

The cooperative is the main structure in the Baena PDO often envelops all the steps from the olive olive production phase to the marketing one (vertical integration) even though this last phase is the weak spot of the Baena DO cooperatives system. In fact, only the 15% of Baena EVOO production in 2005 is sold packed, so only this amount is commercialized with PDO since the olive oil with PDO must be bottled in one of the bottling industries inscribed in the PDO. There is not horizontal integration. The supply of the product is fragmented and directed toward heterogeneous marketing channels (from direct sale by the olive growers to supermarkets chains). The stakeholders playing in the different roles are: Table I- 2 Roles and stakeholders in olive oil chain.

STAGES OF THE MARKETING

CHAIN STAKEHOLDERS COMMERCIALIZED

PRODUCTS

PRODUCTION

FARMER

- Private olive producer

- Partner of a cooperative

Olive

MANIGACTURING

INDUSTRY

- Cooperative

- Private industry

- Great industries with big purchasing power

Packed oil with PDO

Packed oil Non PDO

Oil in bulk

TRADING

WHOLEOLESALER

- Hypermarket and supermarket

- Cooperative

- Private Industry

Packed PDO and Non PDO oil

RETAILING

RETAILER

- Specialized Shop

- Hypermarket and supermarket

- Small shop

- Hotel and Restaurants

- Cooperative

Packed PDO and Non PDO oil

CONSUMPTION consumer

This figure corresponds to the marketing chain of extra virgin olive oil with PDO even if it can be considered useful for all the extra virgin olive oil Non PDO sector in Spain. In fact, all the chain stakeholders treat with PDO and Non PDO extra virgin olive oil.

21

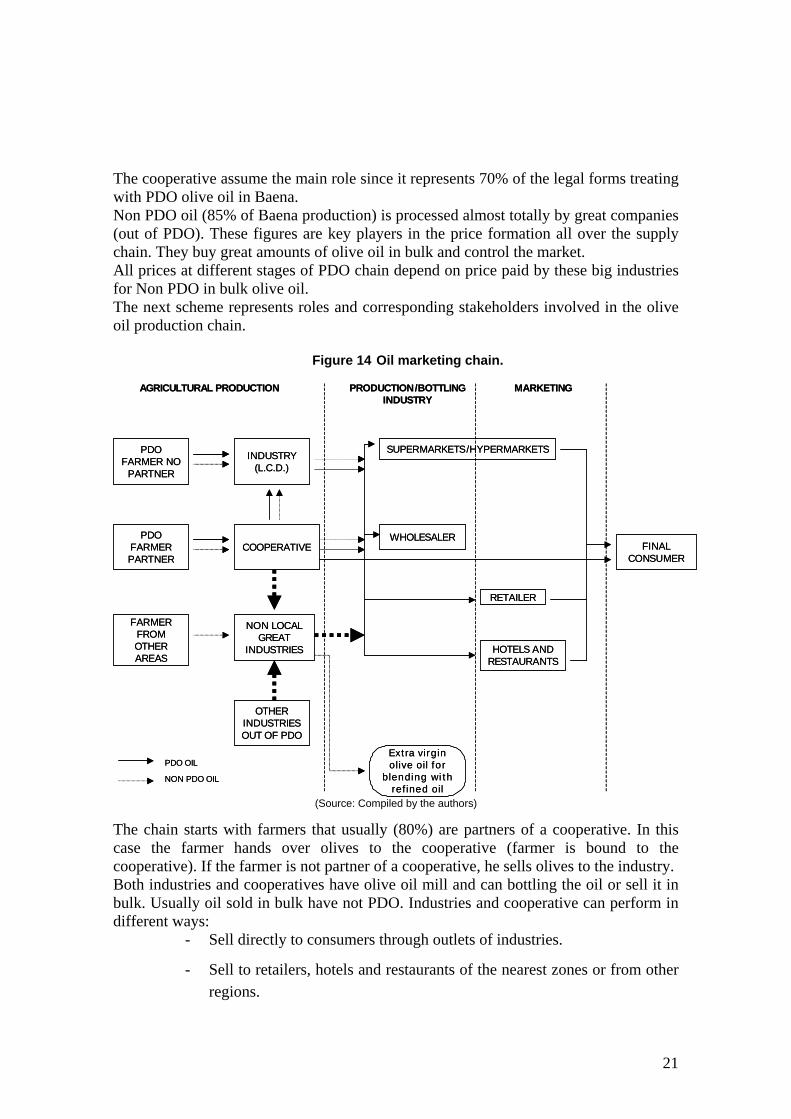

The cooperative assume the main role since it represents 70% of the legal forms treating with PDO olive oil in Baena. Non PDO oil (85% of Baena production) is processed almost totally by great companies (out of PDO). These figures are key players in the price formation all over the supply chain. They buy great amounts of olive oil in bulk and control the market. All prices at different stages of PDO chain depend on price paid by these big industries for Non PDO in bulk olive oil. The next scheme represents roles and corresponding stakeholders involved in the olive oil production chain.

Figure 14 Oil marketing chain.

PDO FARMER NO

PARTNER

PDO FARMER PARTNER

FARMER FROM OTHER AREAS

OTHER INDUSTRIES OUT OF PDO

INDUSTRY (L.C.D.)

COOPERATIVE

NON LOCAL GREAT

INDUSTRIES

PDO OIL

NON PDO OIL

Ext ra virgin olive oil for

blending wi th refined oil

SUPERMARKETS/HYPERMARKETS

WHOLESALERFINAL

CONSUMER

RETAILER

HOTELS AND RESTAURANTS

AGRICULTURAL PRODUCTION PRODUCTION/BOTTLING INDUSTRY

MARKETING

PDO FARMER NO

PARTNER

PDO FARMER PARTNER

FARMER FROM OTHER AREAS

OTHER INDUSTRIES OUT OF PDO

INDUSTRY (L.C.D.)

COOPERATIVE

NON LOCAL GREAT

INDUSTRIES

PDO OIL

NON PDO OIL

Ext ra virgin olive oil for

blending wi th refined oil

SUPERMARKETS/HYPERMARKETS

WHOLESALERFINAL

CONSUMER

RETAILER

HOTELS AND RESTAURANTS

AGRICULTURAL PRODUCTION PRODUCTION/BOTTLING INDUSTRY

MARKETING

(Source: Compiled by the authors)

The chain starts with farmers that usually (80%) are partners of a cooperative. In this case the farmer hands over olives to the cooperative (farmer is bound to the cooperative). If the farmer is not partner of a cooperative, he sells olives to the industry. Both industries and cooperatives have olive oil mill and can bottling the oil or sell it in bulk. Usually oil sold in bulk have not PDO. Industries and cooperative can perform in different ways:

- Sell directly to consumers through outlets of industries.

- Sell to retailers, hotels and restaurants of the nearest zones or from other regions.

22

- Sell through wholesalers that distribute the product to retailers, hotels and restaurants

The following chapters examine every single stakeholder inside his role and the interactions with the others subjects.

Producers: farmers

Main characteristics

In accordance with the 2006 Official Culture Declaration (C.A.P. Junta de Andalucía) the number of farmers inside the 7 communes of the Baena PDO is 11,236 olive growers are distributed in 70,000 hectares. The average farm size (6,2 ha) shows up the little dimenssion of the farms. Most of olive growers can be considered like little farmers with less than 5 hectares of olive grove.The particular structure of the Baena PDO causes that the majority of the producers (about 80%) are partners of a cooperative so they are forced to sell its olives to the cooperative. The rest of the olive production is sold to private industries (mainly local industries). The price that the cooperative pays for the olive varies according to the characteristic of the obtained oil. There is a series of chemical analyses that determine the percentage of fat and the degree of acidity. The olive price to farmers in the last 9 years does not distinguish between olives to produce PDO and olives to produce Non PDO oil7:

1997 1998 1999 2000 2001 2002 2003 2004 2005

0,43 0,50 0,58 0,60 0,30 0,42 0,42 0,36 Olive price (Euro/Kg) 0,57

Every marketing year the cooperative calculate the balance between the incomes (oil sales) and the expenses (milling, corporative, financial and marketing expenses, investments, etc). The result of this calculation is divided by the produced oil amount resulting a price for the oil (euros por kg) to deliver among partners (farmers). This price is usually called “settlement price”. The price for olives is estimated from this settlement price, according to the olive oil yield of the olives sold by each farmer. Furthermore, depending on the each cooperative decision, there are others factors determining the olive price paid to the farmer, such as:

Oil acidity.

Use of Picudo variety.

Harvesting mode: olives shook loose ("de vuelo") are considered better than the overripe ones that fall by themselves ("de suelo"). In fact, the presence of olives “De Suelo” causes a loss of quality in the oil, mainly, an increase of acidity and sensorial defects (mould, humidity, dirty, etc.) as well as sweeter oil with decayed flavour (Besana, 2006).

7 These olive prices can be converted into equivalent olive oil price taking into account the average olive oil yield of 21%.

23

Therefore, there is not any price difference between the price of olives used to produce PDO oil and the price of the olives used to produce Non PDO oil. The price received by the farmer depends on the cooperative commercial managements. Anyway, for the farmer partner of a cooperative, it’s better that the cooperative could sell bigger quantity of PDO olive oil since this product can be sold with a higher price. In the private industry case (no cooperatives) the price paid to the farmers is established according to the price predicted by the industry. That to say that the industry assume any risk about the olive oil price determined by the market situation. Requirements

The PDO demands to the farmer some requests: - Olive variety: Picudo or Carrasqueño of Cordoba (local variety), Lechin, Chorrúo

or Jardúo, Hojiblanca and Picual.

- Date harvesting: the beginning date of harvesting and its completion, so that the fruit is in its advisable maturity degree.

- The division in harvesting phase between “de vuelo” olives and “de suelo” ones. Only olives in perfect conditions would be used to produce PDO extra virgin olive oil.

These requirements can involve additional cost to the farmers8, although most of these requirements have been assumed in the region as mainstream practices. All the farmers are inscribed in a Olive Grove Official Register and have to pay a tax of Inscribed Plantation that represents the 0.3% of the average production value of one hectare of the last year.

Processors: milling industries and bottling industries

Main characteristics

Actually there are 18 industries in Baena PDO: - 11 of these enclose both milling and bottling phase.

- 4 of these enclose bottling phase.

- 3 of these enclose milling phase.

The 70% of the industries constitutes a cooperative (Source:Ruling Council, 2006). The cooperative can:

- bottle olive oil and sell it to a trader or to a retailer or directly to the final consumer. In this case the olive has the PDO.

8 There are olive varieties with a more regular production and easier to harvest; restriction on date harvesting can involve problems of availability of working force, and olives separation ("suelo/vuelo") increases cost of harvesting.

24

- sell the olive oil in bulk (this is the main channel representing the 85% of total olive oil production) to a big industry. In this case almost all the olive oil sold by the cooperative is Non PDO.

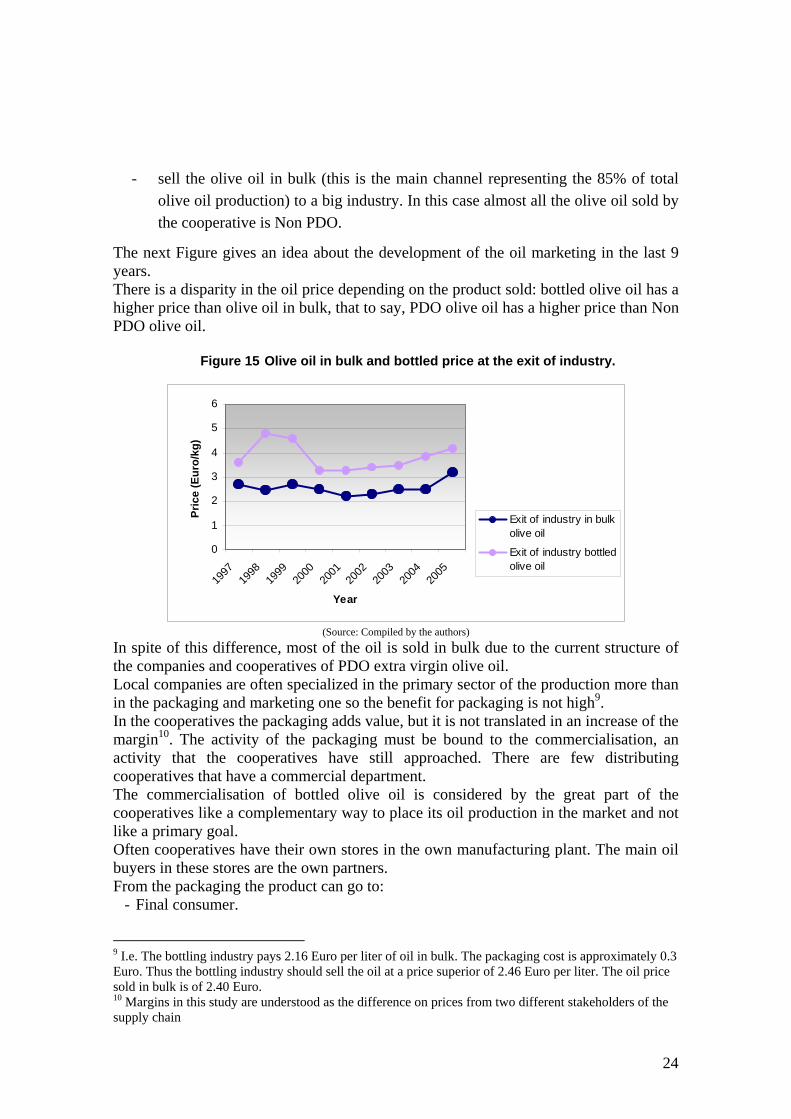

The next Figure gives an idea about the development of the oil marketing in the last 9 years. There is a disparity in the oil price depending on the product sold: bottled olive oil has a higher price than olive oil in bulk, that to say, PDO olive oil has a higher price than Non PDO olive oil.

Figure 15 Olive oil in bulk and bottled price at the exit of industry.

0

1

2

3

4

5

6

1997

1998

1999

2000

2001

2002

2003

2004

2005

Year

Pric

e (E

uro/

kg)

Exit of industry in bulkolive oil

Exit of industry bottledolive oil

(Source: Compiled by the authors)

In spite of this difference, most of the oil is sold in bulk due to the current structure of the companies and cooperatives of PDO extra virgin olive oil. Local companies are often specialized in the primary sector of the production more than in the packaging and marketing one so the benefit for packaging is not high9. In the cooperatives the packaging adds value, but it is not translated in an increase of the margin10. The activity of the packaging must be bound to the commercialisation, an activity that the cooperatives have still approached. There are few distributing cooperatives that have a commercial department. The commercialisation of bottled olive oil is considered by the great part of the cooperatives like a complementary way to place its oil production in the market and not like a primary goal. Often cooperatives have their own stores in the own manufacturing plant. The main oil buyers in these stores are the own partners. From the packaging the product can go to:

- Final consumer.

9 I.e. The bottling industry pays 2.16 Euro per liter of oil in bulk. The packaging cost is approximately 0.3 Euro. Thus the bottling industry should sell the oil at a price superior of 2.46 Euro per liter. The oil price sold in bulk is of 2.40 Euro. 10 Margins in this study are understood as the difference on prices from two different stakeholders of the supply chain

25

- Trader or distributor. In this case the following phase can be the retailer, another distributor or great surfaces.

- Retailer, store gourmet, small stores.

Usually ½ L glass bottle price are bigger 5 L tin price although not always it follows the same principle since this price depends on the distribution or retail policy. Requirements

The PDO demands to the company or cooperative sensorial and practical requisite, as it was mentioned in section 0 (Regulatory requirements and controls). The Ruling Council organizes tasting where the sensorial characteristics of the oil are valuated if oil is apt PDO. Two scales are considered (from 1 to 10), that represent negative and positive attributes. The apt extra virgin olive oil must fulfil the following characteristics:

- In the scale of positive attributes to have a value >4.

- In the scale of negative attributes to have a value =0.

The Non PDO extra virgin olive oil produced in the zone of Baena has the following characteristics:

- In the scale of positive attributes has a value >0.

- In the scale of negative attributes has a value <2.5.

The Regulation demands in addition particular conditions of temperature of elaboration and a series of chemical analyses. There are also two taxes that the cooperative pays to the DO:

- Tax on the sold product that is 1.25% of the sale price per kg of olive oil.

- Tax for control labelling. It depends on the bottle type and on the volume commercialized under that format.

Traders

Main characteristics

There are two main stakeholders playing a role in the distribution: the wholesaler and big retailers (hyper and supermarkets). Usually the wholesaler has knowledge about a specific zone. Distribution centres are usually located in strategic a points (near big cities and homogeneously distributed in the country). This stakeholder possesses own infrastructure, sells bottled oil with the name of the cooperative or bottling industry to:

- Commercial retail.

- Hotels and restaurants.

- General stores.

26

Often the trader have an exclusive contract with the industry: the company have the guarantee that it’s the only distributor selling the one label. This fact cause that many companies and cooperatives sell PDO oil with different labels to open multiples channels. Ruling Council admits eight trading companies (both wholesaler and big retailers) selling PDO olive oil with own labels. They are located in Spain (Madrid, Cordoba, Malaga, Gijón, Tarrega) and Europe (Brussels). Olive oil is bottled and labeled in local industries (cooperatives and privates industries) using the distributor's labels. Often privates industries and cooperatives engage a sales agent, a expert whose function is to find new channel sales. This figure can be considered as an extension of the industry such he never goes to be owner of the product. He only renders a service to the industry and receives a commission. Strategies.

Big trader groups are actually trying to reinforce the quality requirements of the products commercialized under their retail own label (white label) so that these marks enter in competition with other quality seals. The homogeneity of olive oil product and the producers scant innovation let distributor to unload its product on the market with a lower price and with the same quality (Recio y Román, 1999). In 2004 white label represented 49% of olive oil total sales. Another strategy is opening new marketing channels. For that reason, it is more and more important for the PDO to be introduced in these channels of distribution (Caceres et al., 2004). The big retailer has a big purchasing power and sells olive oil to the final consumer so that this stakeholder plays in the following chain step too, the marketing one.

Retailers

Main characteristics

In this step there are different stakeholders, all of them sell the product to the final consumer:

- Small specialized shop. In this group there are delicatessen shop selling high quality food products. Consumers go to this kind of store specifically to find a particular product. In this case, the willingness to pay is higher.

- Supermarket. Usually big shops like hypermarkets and supermarket count on quantity more than quality even though sometimes it can happen that the product with PDO is publicized and promoted inside a special offer.

- Restaurants and hotels. This sector buys oil usually in larger quantities . Therefore it

is not very common they buy PDO extra virgin olive oil since usually restaurants do

not show the label of the oil bottle. Thus, they do not prevail an opportunity to

27

publicize the product. Usually restaurants and hotels buy the oil with a 4% of

discount to the normal price.

Product is sold also in different ways:

Internet sale. This channel is nowadays expanding since every day the number of internet users increasing. It is a potential source of benefits for productive sector since it allow to spare intermediaries.

Direct sale. Some companies and cooperatives have their own shops at the head office. These stores have local customers or clients that want to discover the “origin” place.

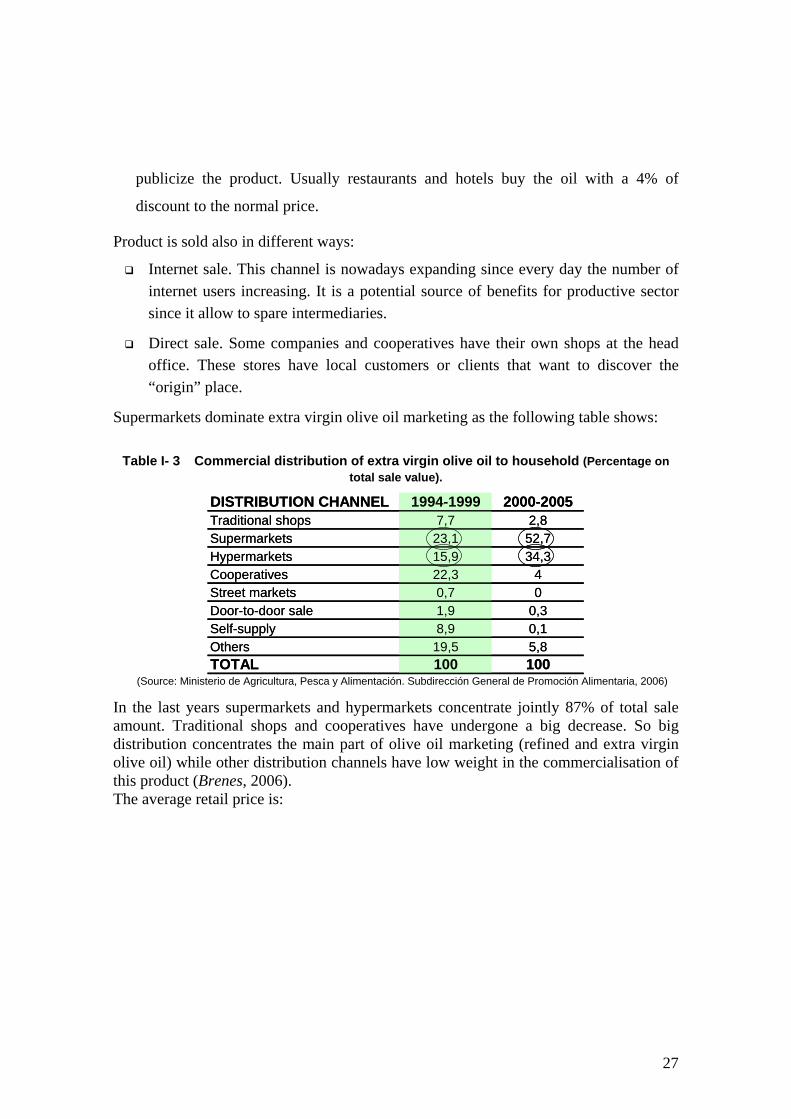

Supermarkets dominate extra virgin olive oil marketing as the following table shows:

Table I- 3 Commercial distribution of extra virgin olive oil to household (Percentage on total sale value).

DISTRIBUTION CHANNEL 1994-1999 2000-2005Traditional shops 7,7 2,8Supermarkets 23,1 52,7Hypermarkets 15,9 34,3Cooperatives 22,3 4Street markets 0,7 0Door-to-door sale 1,9 0,3Self-supply 8,9 0,1Others 19,5 5,8TOTAL 100 100

DISTRIBUTION CHANNEL 1994-1999 2000-2005Traditional shops 7,7 2,8Supermarkets 23,1 52,7Hypermarkets 15,9 34,3Cooperatives 22,3 4Street markets 0,7 0Door-to-door sale 1,9 0,3Self-supply 8,9 0,1Others 19,5 5,8TOTAL 100 100

(Source: Ministerio de Agricultura, Pesca y Alimentación. Subdirección General de Promoción Alimentaria, 2006)

In the last years supermarkets and hypermarkets concentrate jointly 87% of total sale amount. Traditional shops and cooperatives have undergone a big decrease. So big distribution concentrates the main part of olive oil marketing (refined and extra virgin olive oil) while other distribution channels have low weight in the commercialisation of this product (Brenes, 2006). The average retail price is:

28

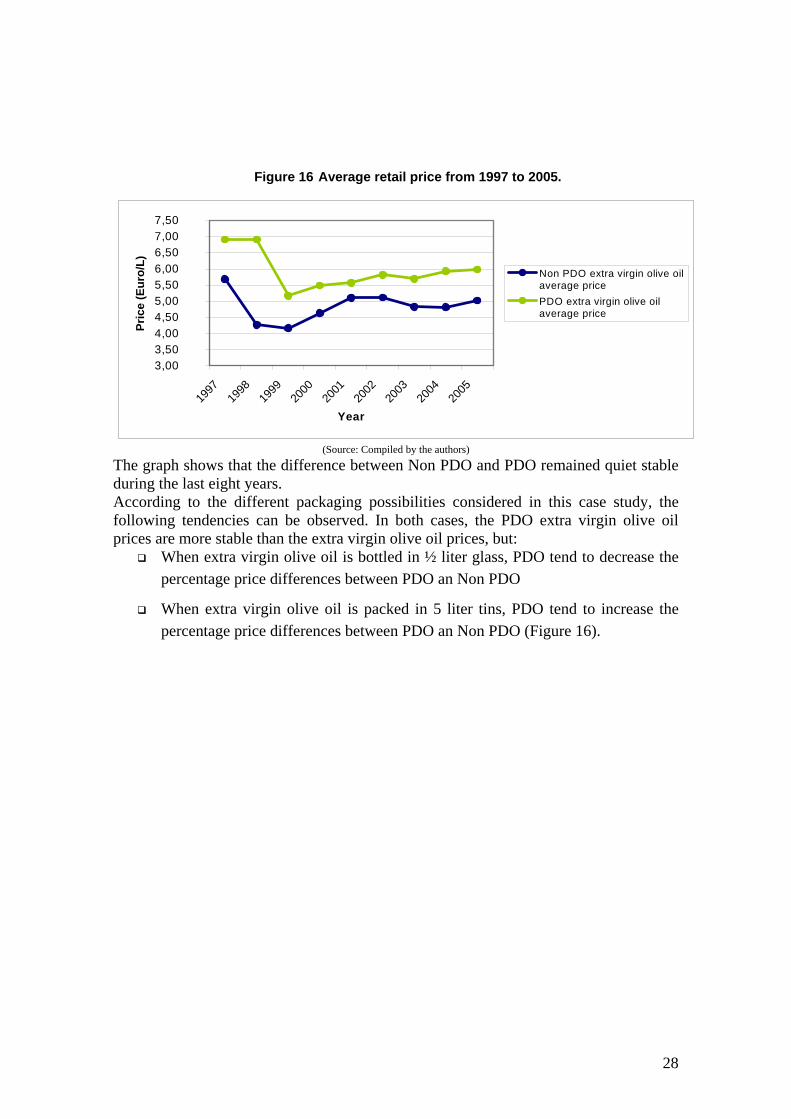

Figure 16 Average retail price from 1997 to 2005.

3,00 3,50 4,00 4,50 5,00 5,50 6,00 6,50 7,00 7,50

1997

1998

1999

2000

2001

2002

2003

2004

2005

Year

Pric

e (E

uro/

L)

Non PDO extra virgin olive oilaverage pricePDO extra virgin olive oilaverage price

(Source: Compiled by the authors)

The graph shows that the difference between Non PDO and PDO remained quiet stable during the last eight years. According to the different packaging possibilities considered in this case study, the following tendencies can be observed. In both cases, the PDO extra virgin olive oil prices are more stable than the extra virgin olive oil prices, but:

When extra virgin olive oil is bottled in ½ liter glass, PDO tend to decrease the percentage price differences between PDO an Non PDO

When extra virgin olive oil is packed in 5 liter tins, PDO tend to increase the percentage price differences between PDO an Non PDO (Figure 16).

29

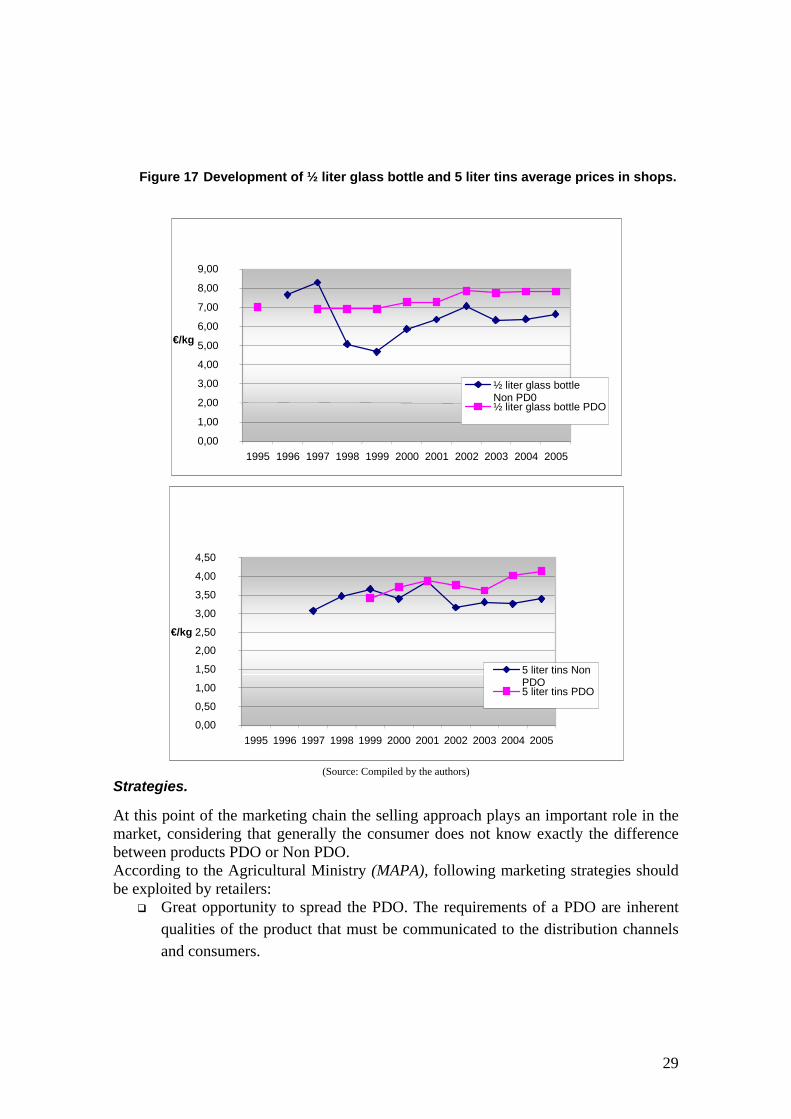

Figure 17 Development of ½ liter glass bottle and 5 liter tins average prices in shops.

0,00 1,00 2,00 3,00 4,00 5,00 6,00 7,00 8,00 9,00

1995 1996 1997 1998 1999 2000 2001 2002 2003 2004 2005

€/kg

½ liter glass bottle Non PD0½ liter glass bottle PDO

0,00 0,50 1,00 1,50 2,00 2,50 3,00 3,50 4,00 4,50

1995 1996 1997 1998 1999 2000 2001 2002 2003 2004 2005

€/kg

5 liter tins Non PDO5 liter tins PDO

(Source: Compiled by the authors)

Strategies.

At this point of the marketing chain the selling approach plays an important role in the market, considering that generally the consumer does not know exactly the difference between products PDO or Non PDO. According to the Agricultural Ministry (MAPA), following marketing strategies should be exploited by retailers:

Great opportunity to spread the PDO. The requirements of a PDO are inherent qualities of the product that must be communicated to the distribution channels and consumers.

30

Tie the inseparable qualities of the product to an improvement in sensorial aspects (flavor, scent, texture, etc.), general characteristics of health and/or to a certain production process.

Tie the production with the Region of Origin standing out in aspects related to the product (landscape, people, climate, ecology, tradition, history, etc.).

Emphasize the differentiating character of the PDO as opposed to commercial brands. Existing confusion between both concepts by consumers should be reduced.

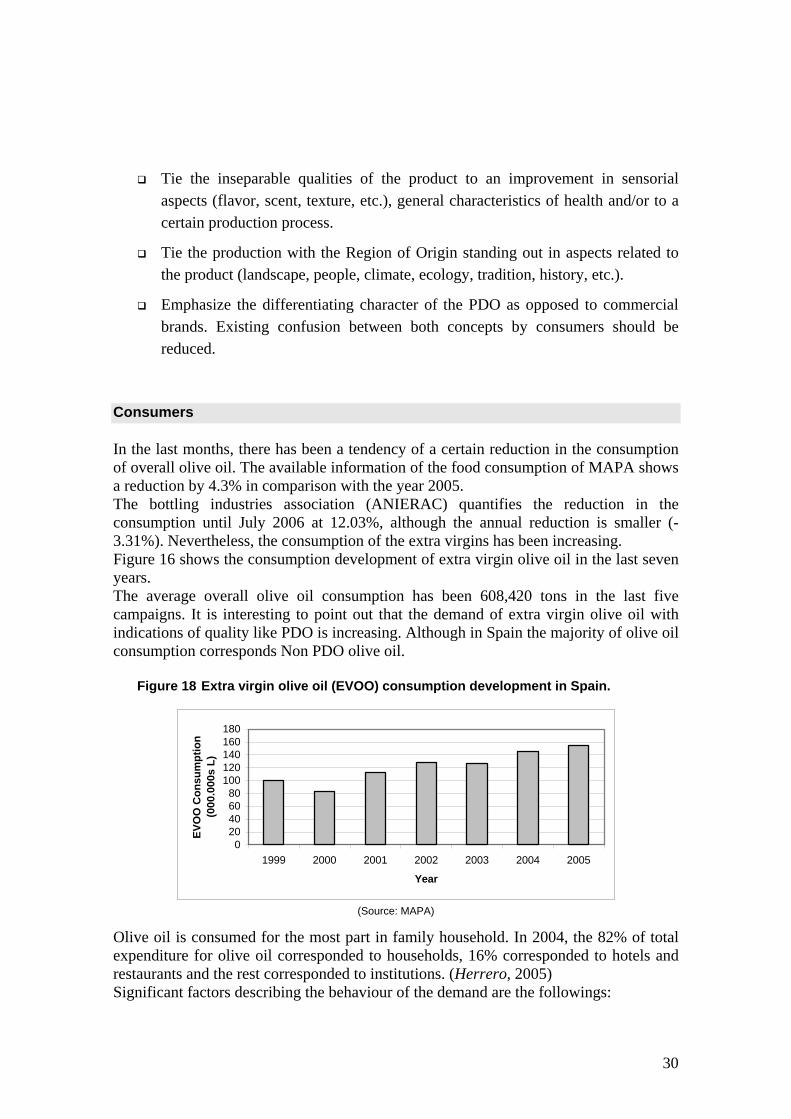

Consumers

In the last months, there has been a tendency of a certain reduction in the consumption of overall olive oil. The available information of the food consumption of MAPA shows a reduction by 4.3% in comparison with the year 2005. The bottling industries association (ANIERAC) quantifies the reduction in the consumption until July 2006 at 12.03%, although the annual reduction is smaller (-3.31%). Nevertheless, the consumption of the extra virgins has been increasing. Figure 16 shows the consumption development of extra virgin olive oil in the last seven years. The average overall olive oil consumption has been 608,420 tons in the last five campaigns. It is interesting to point out that the demand of extra virgin olive oil with indications of quality like PDO is increasing. Although in Spain the majority of olive oil consumption corresponds Non PDO olive oil.

Figure 18 Extra virgin olive oil (EVOO) consumption development in Spain.

020406080

100120140160180

1999 2000 2001 2002 2003 2004 2005

Year

EVO

O C

onsu

mpt

ion

(000

.000

s L)

(Source: MAPA)

Olive oil is consumed for the most part in family household. In 2004, the 82% of total expenditure for olive oil corresponded to households, 16% corresponded to hotels and restaurants and the rest corresponded to institutions. (Herrero, 2005) Significant factors describing the behaviour of the demand are the followings:

31

Flavour, health, acidity and price appear to support virgin olive oil and virgin extra olive oil at the time of selection.

The culinary use of virgin olive oil (salads and cocked dishes, 19%), extra virgin olive oil (salads 30%, and breakfast 17%), and olive oil (frying 24%) appears a determining factor between the products, something that consumers make spontaneously.

A study made by the Ruling Council (Ruling Council, 2006) about consumers habits shows that people relate “PDO” word to Spanish wines overall (Figure 18). At andalusian PDO olive oils level, Baena PDO receives the higher index.

Figure 19 Spanish PDO known by consumers.

5 ,9 %

2 ,1 % 2 ,1 %

9 ,2 %

7 ,1 %

5 ,4 %

1 7 , 4 %

0 %

1 0 %

2 0 %

T h e re s t B a e n a H u e lvah a m

J e re z M o n ti lla -M o r i le s

R ib e ra d e lD u e ro

R i o ja

(Source: Ruling Council)

Another interesting data is the consumer knowledge about Baena PDO. 36% of the asked people knows “Baena PDO” and 43.3% knows “Baena olive oils”. According to the same study consumers associate PDO olive oil with:

32

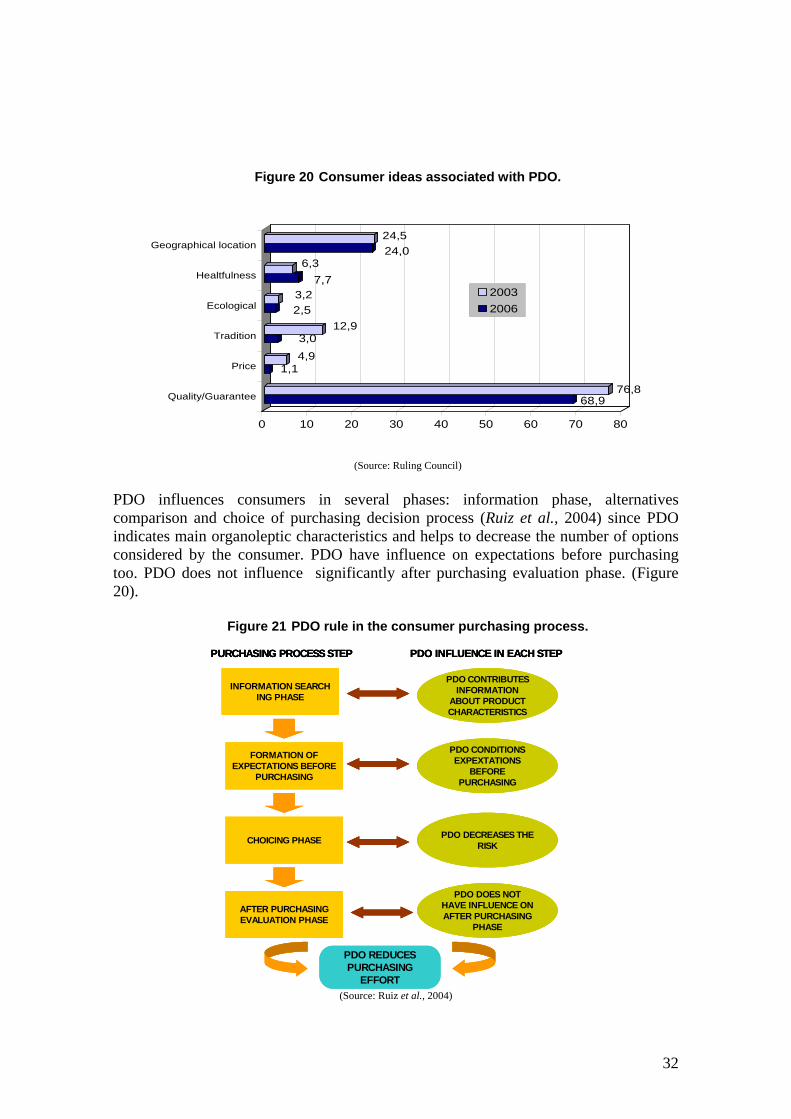

Figure 20 Consumer ideas associated with PDO.

68,976,8

1,14,93,0

12,92,53,2

7,76,3

24,024,5

0 10 20 30 40 50 60 70 80

Quality/Guarantee

Price

Tradition

Ecological

Healtfulness

Geographical location

20032006

(Source: Ruling Council)

PDO influences consumers in several phases: information phase, alternatives comparison and choice of purchasing decision process (Ruiz et al., 2004) since PDO indicates main organoleptic characteristics and helps to decrease the number of options considered by the consumer. PDO have influence on expectations before purchasing too. PDO does not influence significantly after purchasing evaluation phase. (Figure 20).

Figure 21 PDO rule in the consumer purchasing process.

PURCHASING PROCESS STEP PDO INFLUENCE IN EACH STEP

INFORMATION SEARCH ING PHASE

FORMATION OF EXPECTATIONS BEFORE

PURCHASING

CHOICING PHASE

AFTER PURCHASING EVALUATION PHASE

PDO CONTRIBUTES INFORMATION

ABOUT PRODUCT CHARACTERISTICS

PDO CONDITIONS EXPEXTATIONS

BEFORE PURCHASING

PDO DECREASES THE RISK

PDO DOES NOT HAVE INFLUENCE ON AFTER PURCHASING

PHASE

PDO REDUCES PURCHASING

EFFORT

PURCHASING PROCESS STEP PDO INFLUENCE IN EACH STEPPURCHASING PROCESS STEP PDO INFLUENCE IN EACH STEP

INFORMATION SEARCH ING PHASE

FORMATION OF EXPECTATIONS BEFORE

PURCHASING

CHOICING PHASE

AFTER PURCHASING EVALUATION PHASE

PDO CONTRIBUTES INFORMATION

ABOUT PRODUCT CHARACTERISTICS

PDO CONDITIONS EXPEXTATIONS

BEFORE PURCHASING

PDO DECREASES THE RISK

PDO DOES NOT HAVE INFLUENCE ON AFTER PURCHASING

PHASE

INFORMATION SEARCH ING PHASE

FORMATION OF EXPECTATIONS BEFORE

PURCHASING

CHOICING PHASE

AFTER PURCHASING EVALUATION PHASE

PDO CONTRIBUTES INFORMATION

ABOUT PRODUCT CHARACTERISTICS

PDO CONDITIONS EXPEXTATIONS

BEFORE PURCHASING

PDO DECREASES THE RISK

PDO DOES NOT HAVE INFLUENCE ON AFTER PURCHASING

PHASE

PDO REDUCES PURCHASING

EFFORT (Source: Ruiz et al., 2004)

33

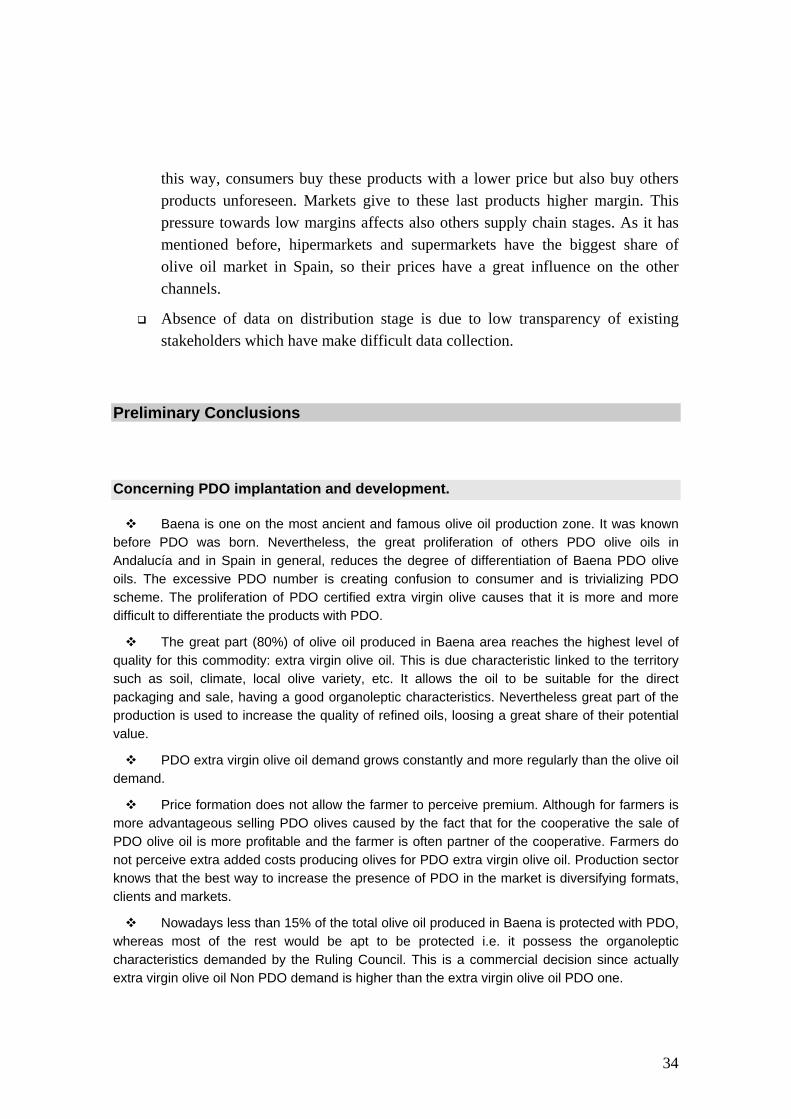

Prices at different stages of the supply Chain

In the next figure shows a price summary along the olive oil supply chain.

Figure 22 Price summary

30%

FARMING

RETAIL

INDUSTRY

2.86*EquivalentOlive Oil

2.86*EquivalentOlive Oil

DISTRIBUTION

3.185 L

4.125 L

4.145 L

3.395 L

0.5%

6.2%44%

11%

0.6Olives

0.6Olives

22%

PDO NON PDOPrice difference

12%

2%

3.20BULK

2.93BULK

10%

•RC for PDO

•Poolred for Non PDO

•Representative industry for calculating differences between PDO and Non PDObottled oil

Source: Source: Mercacei

(*) Equivalent olive oil price has been calculated from price of olive considering olive oil y ield = 21%

0%

0% 30%

FARMING

RETAIL

INDUSTRY

2.86*EquivalentOlive Oil

2.86*EquivalentOlive Oil

DISTRIBUTION

3.185 L

4.125 L

4.145 L

3.395 L

0.5%

6.2%44%

11%

0.6Olives

0.6Olives

22%

PDO NON PDOPrice difference

PDO NON PDOPrice difference

12%

2%

3.20BULK

2.93BULK

10%

•RC for PDO

•Poolred for Non PDO

•Representative industry for calculating differences between PDO and Non PDObottled oil

Source: Source: Mercacei

(*) Equivalent olive oil price has been calculated from price of olive considering olive oil y ield = 21%

0%

0%

(Source: Compiled by the authors)

It can be noted some interesting topics:

Farmers perceive the same price for PDO & non-PDO extra virgin olive oil.

In the industry stage there is the highest difference between prices of PDO y Non PDO bottled olive oil.

It seems to be the bottling phase adds value to PDO olive oil more than Non PDO one in fact there is not big difference between Non PDO olive oil sold in bulk and Non PDO olive oil sold in bottled form. Every way is better to sell bottled oil: from farmer stage to industry one the PDO price grows 12% for oil in bulk and 44% for bottled oil.

In retail step the margin is quite low. This fact is probably related to the different source used to collect data at this stage. Although the reason for the generic low margin at retail level is due to a big distribution centres strategy: in Spain olive oil is considered an essential product with low differentiation level. According to supermarkets and hypermarkets, this kind of product has a “hook” function since it increases the attraction capacity of the supermarket (Rebollo, 1993). In

34

this way, consumers buy these products with a lower price but also buy others products unforeseen. Markets give to these last products higher margin. This pressure towards low margins affects also others supply chain stages. As it has mentioned before, hipermarkets and supermarkets have the biggest share of olive oil market in Spain, so their prices have a great influence on the other channels.

Absence of data on distribution stage is due to low transparency of existing stakeholders which have make difficult data collection.

Preliminary Conclusions

Concerning PDO implantation and development.

Baena is one on the most ancient and famous olive oil production zone. It was known before PDO was born. Nevertheless, the great proliferation of others PDO olive oils in Andalucía and in Spain in general, reduces the degree of differentiation of Baena PDO olive oils. The excessive PDO number is creating confusion to consumer and is trivializing PDO scheme. The proliferation of PDO certified extra virgin olive causes that it is more and more difficult to differentiate the products with PDO.

The great part (80%) of olive oil produced in Baena area reaches the highest level of quality for this commodity: extra virgin olive oil. This is due characteristic linked to the territory such as soil, climate, local olive variety, etc. It allows the oil to be suitable for the direct packaging and sale, having a good organoleptic characteristics. Nevertheless great part of the production is used to increase the quality of refined oils, loosing a great share of their potential value.

PDO extra virgin olive oil demand grows constantly and more regularly than the olive oil demand.

Price formation does not allow the farmer to perceive premium. Although for farmers is more advantageous selling PDO olives caused by the fact that for the cooperative the sale of PDO olive oil is more profitable and the farmer is often partner of the cooperative. Farmers do not perceive extra added costs producing olives for PDO extra virgin olive oil. Production sector knows that the best way to increase the presence of PDO in the market is diversifying formats, clients and markets.

Nowadays less than 15% of the total olive oil produced in Baena is protected with PDO, whereas most of the rest would be apt to be protected i.e. it possess the organoleptic characteristics demanded by the Ruling Council. This is a commercial decision since actually extra virgin olive oil Non PDO demand is higher than the extra virgin olive oil PDO one.

35

Practically all the PDO olive oil with produced by the cooperatives is commercialised in packed format, whereas the Non PDO extra virgin olive oil is commercialized in bulk. There is a poor development of the marketing strategy. Nowadays cooperatives do not take advantage of the added value contributed by packaging and labelling.

Non PDO Baena production (more than 85% of total production) is managed by great industries having big purchasing and sale power. These stakeholders influences market prices, sometimes speculating on them. Price speculation on the prices of the extra virgin olive oil in the marketing sector can weaken the production sector.

PDO benefits

Rural development in the region and reinforcement of rural identity. PDO has given the production area a recognised name very important for the development of the region (tourism, marketing, and other sectors). PDO affects on the effort of the tourist reclamation and traditional products valuation.

Guarantee in the market. PDO olive oil has more stable prices than non DO olive oil and industry can choose the better moment of sale. Furthermore, PDO olive oil price is higher than Non PDO price cause PDO products transmit confidence to the consumer. The PDO olive oil price collects product added values and the PDO imagine creates an expectation on the product.

Awareness on quality issues and general quality improvement. Since the PDO is running, many cooperatives give more relevance to the quality of the olives they receive as well as to the olive oil they elaborate.

Industry modernization and implementation of tracing systems. Innovation in bottling designs and marketing issues.

Constant growing of production & sales. PDO brings stability to product commercialisation. According to the sector, PDO products are sold more easily as industries can find a position in the market or market niches differentiating their products. Furthermore, promotion of “Baena” PDO benefits olive oil production of the zone, including Non PDO olive oil.

Policy Recommendations.

1. Production stage. Efforts should be oriented to promote high quality extra virgin olive oil production and bottled PDO extra virgin olive oil. The marketing of bottled extra virgin olive oil is one of the great challenges which the cooperative sector faces to benefit from the competitive advantages the PDO contributes. The bottling as part of the marketing process creates an opportunity to increase the added value of a product. Furthermore, the packaging is a tool to describe quality characteristics of the product.

2. Promotion and marketing. The sector should promote the origin of the product and the identification of new market niches. Consumers have low knowledge about PDO olive oil though this situation is changing actually. They are not at all ready to pay more for the PDO. In this sense the sector should improve available information for consumers

36

(seminaries, olive oil tasting, breakfast to promote nutritional and health olive oil properties, edition of promotional DVD and divulged papers. Finally, olive oil production sector should increase the degree of differentiation, that suppose a fragmentation of consumers. In this way the retail margin could increase substantially. Throughout alternatives, one can be the concentration of the agri-foodstuff industry. Another alternative is the internet sale: this marketing way encourages the direct commercialization form with competitive prices through the elimination of many intermediaries. The “intangible” value of the PDO has a potential not yet totally developed. In the future PDOs should promote the collective mark to increase the global demand of high quality olive oil.

37

Annexes

Annex 1. ENCUESTA 1. COOPERATIVAS DE LA DOP “BAENA” La Empresa Pública Desarrollo Agrario y Pesquero, S.A. participa en un estudio europeo que pretende analizar el valor añadido en cada una de las fases de comercialización de los productos denominados de calidad. Dicho estudio se compone, para cada país, de una parte general y dos análisis de casos para los productos más significativos. De la revisión de los volúmenes de producción comercializados y otros indicadores de calidad, se ha considerado la PDO “Baena” un caso de estudio representativo de nuestra región y del conjunto de España. El presente estudio pretende obtener datos de precios en las distintas fases de la cadena (olivicultor-transformación-almacenamiento-envasado-distribución-comercialización), y en aquellos casos que sea posible, disponer de series anuales, siendo óptimo disponer de datos relativos a 10 años. Esta encuesta ha sido elaborada a partir de la información telefónica facilitada por el Consejo Regulador “Baena” a ésta Empresa, con la intención de profundizar en información que nos puedan facilitar cooperativas de esta Denominación de Origen responsables de una parte importante de la producción de la PDO 1. Presentaciones más representativas: Se han elegido para este estudio dos productos representativos de la PDO que están presentes en lineales de productos de calidad, en espacios gourmet, en restaurantes de calidad... y canalizan una parte importante del volumen total de aceite producido. Para el presente estudio las dos presentaciones elegidas son:

Botella de vidrio de ½ litro. Hojalata de 5 litros.

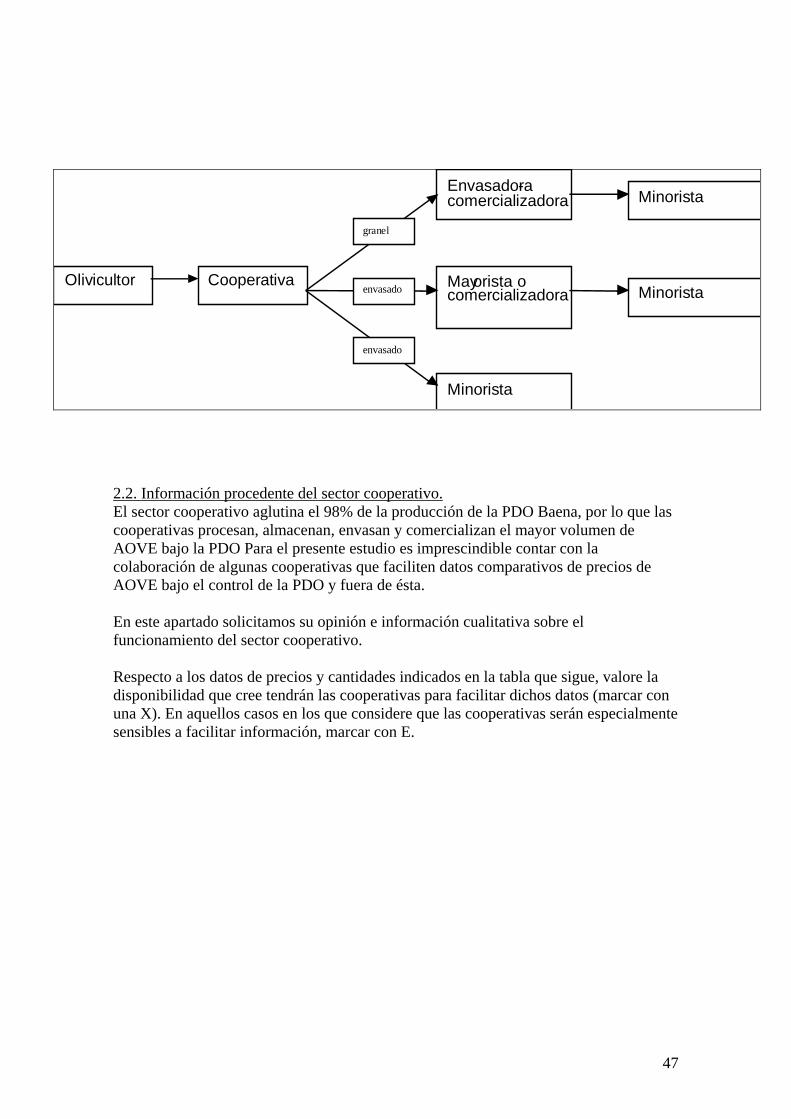

2. Descripción de la cadena de comercialización más usual. El sector cooperativo aglutina el 98% de la producción de la PDO Baena, por lo que las cooperativas producen, procesan, almacenan, envasan y comercializan el mayor volumen de AOVE bajo la PDO Para el presente estudio es imprescindible contar con su colaboración para comparar precios de AOVE con PDO y sin PDO en toda la cadena de comercialización.

38

A continuación se recoge una tabla con la relación de datos solicitados por anualidades, siguiendo el proceso productivo hasta la comercialización. Posteriormente se profundiza cualitativamente en cada una de estas fases del proceso de comercialización a través de un cuestionario de preguntas.

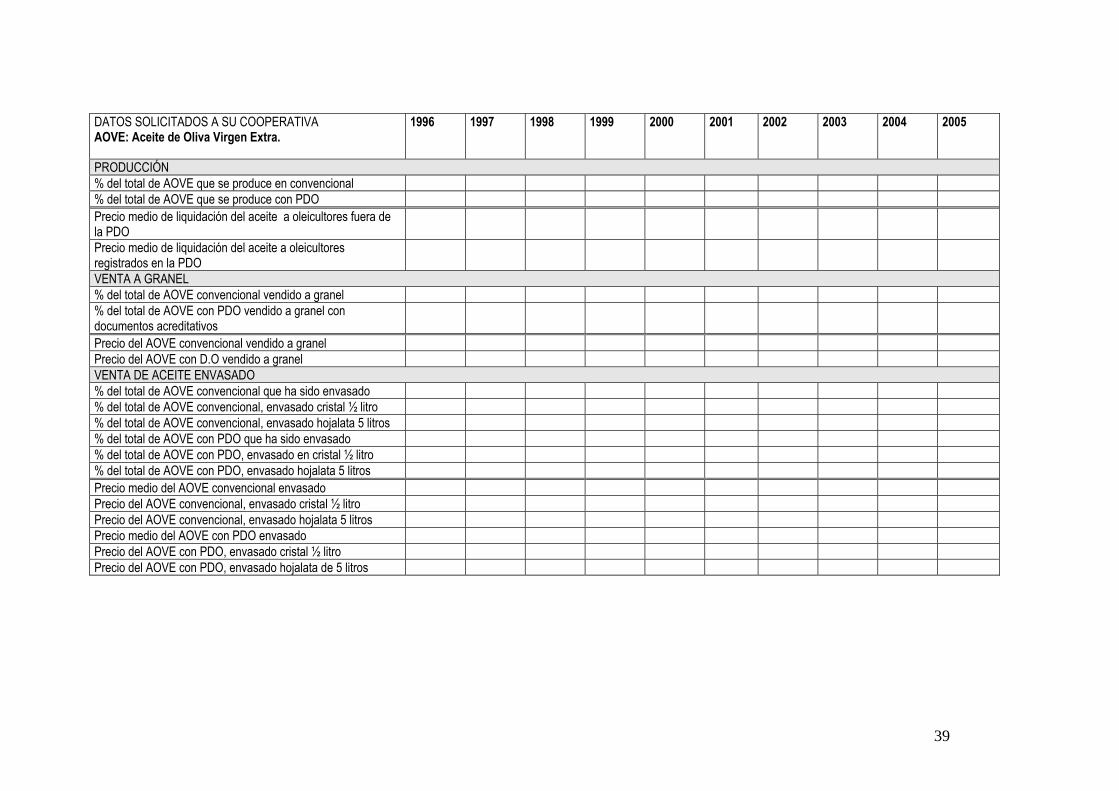

39

DATOS SOLICITADOS A SU COOPERATIVA AOVE: Aceite de Oliva Virgen Extra.

1996 1997 1998 1999 2000 2001 2002 2003 2004 2005

PRODUCCIÓN % del total de AOVE que se produce en convencional % del total de AOVE que se produce con PDO Precio medio de liquidación del aceite a oleicultores fuera de la PDO

Precio medio de liquidación del aceite a oleicultores registrados en la PDO

VENTA A GRANEL % del total de AOVE convencional vendido a granel % del total de AOVE con PDO vendido a granel con documentos acreditativos

Precio del AOVE convencional vendido a granel Precio del AOVE con D.O vendido a granel VENTA DE ACEITE ENVASADO % del total de AOVE convencional que ha sido envasado % del total de AOVE convencional, envasado cristal ½ litro % del total de AOVE convencional, envasado hojalata 5 litros % del total de AOVE con PDO que ha sido envasado % del total de AOVE con PDO, envasado en cristal ½ litro % del total de AOVE con PDO, envasado hojalata 5 litros Precio medio del AOVE convencional envasado Precio del AOVE convencional, envasado cristal ½ litro Precio del AOVE convencional, envasado hojalata 5 litros Precio medio del AOVE con PDO envasado Precio del AOVE con PDO, envasado cristal ½ litro Precio del AOVE con PDO, envasado hojalata de 5 litros

40