european office investment market outlook - · pdf fileeuropean office investment market...

TRANSCRIPT

European Office Investment Market OutlookMarch 2014

UK€25.21bn 13%

Belgium€1.32bn 43%

Luxembourg€0.44bn 7%

France€10.57bnÈ -8%

Germany€13.99bn 31%

Netherlands€1.73bn 54%

Denmark€0.86bn 50%

Portugal€0.11bn 15%

Norway€2.00bnÈ -36%

Switzerland€1.39bnÈ -43%

Ireland€1.00bn 141%

Spain€0.69bnÈ -23%

European office investment 2013European Office Investment Volumes (€ billion)

Greece€0.23bn 337%

Hungary€0.21bn 371% Romania

€0.06bnÈ -61%

Russia€2.40bnÈ -24%

Germany€13.99bn 31%

Austria€0.54bn 32%

Italy€1.48bn 103%

Bulgaria€0.01bn 82%

Turkey€0.49bn 105%

Czech Rep€0.64bn 35%

Poland€1.12bn 7%

Slovakia€0.05bn 246%

Norway€2.00bnÈ -36%

Sweden€3.03bnÈ -28%

Finland€0.76bnÈ -25%

We would like to thank all of our clients from Europe and across the world for choosing to work with JLL. Together we completed more than €34 billion of commercial real estate transactions, joint ventures and refinancing across Europe in 2013. As the recovery in Europe continues to gather momentum we look forward to working with you on new opportunities in 2014 and beyond.

Contents

2013 Review

Strong investment momentum across Europe’s office markets 6

2014 Outlook

Office investors will continue to move “up the risk curve” 14

More “Equity and Expertise” joint ventures with global partners 20

Office occupier market fundamentals will catch up 26

Domestic and European capital will remain highly competitive 32

The recovery in peripheral European markets is for real 38

JLL Contacts 46

2013 Review – Strong investment momentum across Europe’s office markets

6

2013 Review – Strong investment momentum across Europe’s office markets

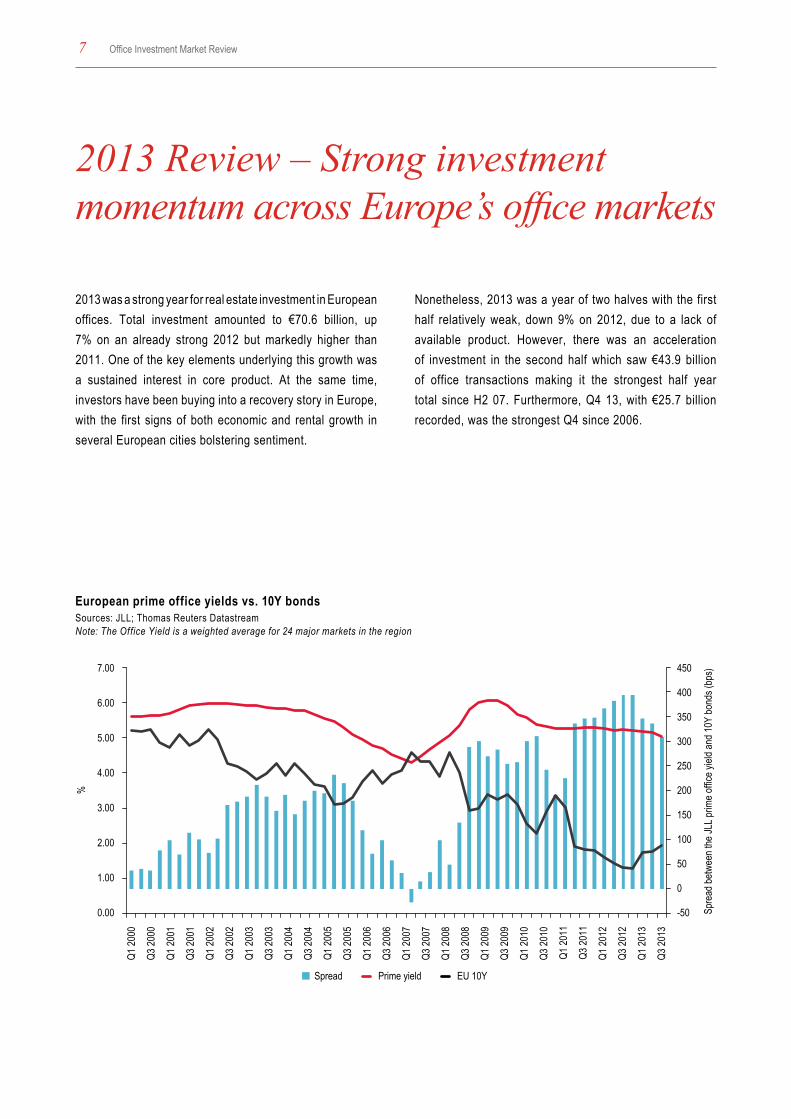

2013 was a strong year for real estate investment in European offices. Total investment amounted to €70.6 billion, up 7% on an already strong 2012 but markedly higher than 2011. One of the key elements underlying this growth was a sustained interest in core product. At the same time, investors have been buying into a recovery story in Europe, with the first signs of both economic and rental growth in several European cities bolstering sentiment.

Nonetheless, 2013 was a year of two halves with the first half relatively weak, down 9% on 2012, due to a lack of available product. However, there was an acceleration of investment in the second half which saw €43.9 billion of office transactions making it the strongest half year total since H2 07. Furthermore, Q4 13, with €25.7 billion recorded, was the strongest Q4 since 2006.

European prime office yields vs. 10Y bondsSources: JLL; Thomas Reuters DatastreamNote: The Office Yield is a weighted average for 24 major markets in the region

-50

0

50

100

150

200

250

300

350

400

450

Q1 20

00

Q3 20

00

Q1 20

01

Q3 20

01

Q1 20

02

Q3 20

02

Q1 20

03

Q3 20

03

Q1 20

04

Q3 20

04

Q1 20

05

Q3 20

05

Q1 20

06

Q3 20

06

Q1 20

07

Q3 20

07

Q1 20

08

Q3 20

08

Q1 20

09

Q3 20

09

Q1 20

10

Q3 20

10

Q1 20

11

Q3 20

11

Q1 20

12

Q3 20

12

Q1 20

13

Q3 20

13

Spre

ad be

twee

n the

JLL p

rime o

ffice y

ield a

nd 10

Y bo

nds (

bps)

0.00

1.00

2.00

3.00

4.00

5.00

6.00

7.00

%

Spread Prime yield EU 10Y

7 Office Investment Market Review

The demand for core markets did not relent in 2013 and investment volumes in some of Europe’s major office markets, notably London and the German Big 5, exceeded the already strong figures for 2012 growing by 11% and 27% y-o-y respectively. However, the main highlight in 2013 was the rise of the regions as investors began looking “beyond prime” across Europe. For example, the UK regional office markets recorded a 71% increase y-o-y while German second tier markets (outside the Big 5) increased by 43%.

Behind these strong numbers is a trinity of capital sources: growing global capital, a resurgent domestic investor base and “supersized” opportunity funds following a record fundraising year. Non-European capital increased its purchaser market share to 27% in 2013 from 18% in 2009. The make-up is also increasingly global, with Asia Pacific and Middle East each accounting for 8% of total office volumes, the Americas accounting for 7%, and with global funds making up the difference. With most funds not even halfway through the execution of their global real estate strategies, we expect the inflows of global capital to continue.

Most active sellers and buyers of offices in Europe in 2013Sources: JLL; Property Data (UK); Akershus Eiendom (Norway); Athens Economics (Greece); Sadolin & Albaek (Denmark); RCA Analytics

Largest Sellers Largest Buyers

€ Billion € Billion-15 -13 -11 -9 -7 -5 -3 -1 1

Austria

Netherlands

Sweden

Norway

Armenia

Global

USA

France

Germany

UK

0 2 4 6 8 10 12 14

Germany

UK

France

USA

Sweden

Global

Kuwait

Norway

Russia

China

5%

11%

4%

4%

4%

3%

3%

2%

3%

3%

3%

6%

7%

9%

19%

20%

2%

2%

13%

18%

JLL European Capital Markets 8

The inflow of global capital has been magnified by a resurgent domestic investor base. Traditional real estate investors have returned to the real estate investment markets in force. In fact, domestic capital has gained market share in rising markets in all three major office markets. Whereas domestic capital was confined to competing for medium lot sizes following the Global Financial Crisis, it is now increasingly competitive on larger lot sizes.

Finally, last year the amount of capital raised globally by private real estate funds was over €115 billion, a total which bettered 2008 according to Indirex. About half of this has been earmarked for opportunistic strategies. Private equity or opportunistic funds are already active in Europe, but this new injection of capital will make them even more competitive in even more markets.

Office investment activity in lot sizes over €100 million 2008–2013Sources: JLL; Property Data (UK); Akershus Eiendom (Norway); Athens Economics (Greece); Sadolin & Albaek (Denmark); RCA Analytics

95

53

97 92

140 138

0

20

40

60

80

100

120

140

160

0

5

10

15

20

25

30

35

40

2008 2009 2010 2011 2012 2013

Inves

tmen

t Volu

mes (

€ Billi

on)

Numb

er of

Tra

nsac

tions

Office Volumes No. Transactions

9 Office Investment Market Review

Office investment activity by purchaser source of capital (2004–2013)Sources: JLL; Property Data (UK); Akershus Eiendom (Norway); Athens Economics (Greece); Sadolin & Albaek (Denmark); RCA Analytics

60%

65%

70%

75%

80%

85%

Market share (%)

2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 0

20

40

60

80

100

120

140

€ Billi

on

European (non-domestic)Domestic Non-European Share of European investors

These inflows of capital have had an impact on pricing. In 2013, office capital values rose by 4.3% in Europe, predominantly driven by yield compression. However, there is a diverging picture across European cities. In core/safe haven cities such as London, Zurich and Munich, prime office capital values are now well above their long-term trend and prime yields have returned close to – or even reached their 2007 peak levels. However, in smaller office markets such as Dublin and Madrid office capital values remain below their long-term average despite recent improvements.

Underpinning the strong prime yields in core markets and the broadening of office investment markets is a slow but steady improvement in occupier fundamentals. Rental growth has been evident in Central London for the first time since 2010 and take-up in the City in 2013 was the strongest since 2000. Several other office markets are now seeing rental growth although the recovery is still fragile.

JLL European Capital Markets 10

In 2013 ● For the third year running, Asia Pacific capital was

the biggest group of non-domestic investors in Greater London

● Asia Pacific capital invested 132% more into continental Europe than in 2012

● French investors accounted for 70% of total office transactions in France

● JLL advised on 26% of all office transactions in Europe involving capital from the Americas (US, Canadian, South America)

● JLL advised on 35% of all office transactions in Europe involving Asian capital

● Office investment transactions in Central London totalled £15.8 billion, the third highest ever

● There were 8 office transactions in Europe of >€500 million

● The Euribor interest rate (5 year) was up 50 bps / 66% during 2013 (from 0.76% to 1.26%).

At the start of 2014 ● Prime office rents in London are 40% higher than they

were in Q1 2010 ● Office Capital Values in London West End have

doubled since 2009 ● Prime office rents in many cities remain well below

their 2008 peak level: Barcelona (-36%), Dublin (-42%), Madrid (-41%), Milan (-21%), Moscow (-40%) and Warsaw (-27%)

● The weighted average office yield across Europe stands at 5.03% – more than 100 bps lower than mid-2009 (and just 70 basis points higher than the 2007 peak)

● Prime office yields in London, Paris, German Big 5 and Stockholm are 25 bps or more below their 10 year averages

● Yields in peripheral office markets remain significantly higher than their previous peak: Barcelona (250 bps), Dublin (205 bps) and Madrid (185 bps)

● Capital values in Dublin have risen 52% since Q3 2012 but are still 62% below the 2007 peak

● The Moscow office market has doubled in size since 2007 ● Office development completions will increase by 20%

in 2014 compared to 2013

Office capital values rise throughout EuropeSource: JLL

Prim

e Offic

e Cap

ital V

alue I

ndex

(Q4 2

002 =

100)

250

250

210

190

170

150

130

110

90

70

50

Q4 2002

Q2 2003

Q4 2003

Q2 2004

Q4 2004

Q2 2005

Q4 2005

Q2 2006

Q4 2006

Q2 2007

Q4 2007

Q2 2008

Q4 2008

Q2 2009

Q4 2009

Q2 2010

Q4 2010

Q2 2011

Q4 2011

Q2 2012

Q4 2012

Q2 2013

Q4 2013

Europe (weighted average) Paris CBD Warsaw London West End Munich Madrid

11 Office Investment Market Review

Capital flows in European offices – Global flows of capital into offices 2013 (€ Billion)Sources: JLL; Property Data (UK); Akershus Eiendom (Norway); Athens Economics (Greece); Sadolin & Albaek (Denmark); RCA Analytics

Global Sources of Funds Europe Americas Middle East & Africa Asia Pacific Global

2.6

5.2

5.8

5.4

YoY increase in capital flows from other regions (2012 vs. 2013)Sources: JLL; Property Data (UK); Akershus Eiendom (Norway); Athens Economics (Greece); Sadolin & Albaek (Denmark); RCA Analytics

-20

0

20

40

60

MEA Asia Pacific Americas

% C

hang

e

JLL European Capital Markets 12

2014 Outlook – Office investors will continue to move “up the risk curve”

14

2014 Outlook – Office investors will continue to move “up the risk curve”

For us it is clear that investors are “moving up the risk curve”. The increased appetite for risk has been supported on the one hand by more positive economic indicators and improving office market fundamentals and, on the other hand, by the increasingly competitive conditions in the core office markets. Given that we expect these trends to further strengthen in 2014, we should see a further increase in risk appetite in 2014. Essentially, we expect growth in four areas:

Firstly, in 2014 we expect to see a further broadening of the investable office market in Europe. In 2013 we saw regional cities in the major markets report strong growth in investment and we expect this to continue in 2014. Furthermore, within core markets, like Central London, we expect there to be increased investment into non-core assets that have an asset management angle or that are located at the fringe. However, the largest impetus could

come from markets outside the core, such as Southern Europe, Ireland, the Benelux and CEE. Nevertheless, the adage of buying non-core assets in core markets and core assets in non-core market still holds true.

Secondly, we expect to see more portfolio sales in 2014. Even though the volume of office portfolios fell slightly to €7.0 billion in 2013 from €8.9 billion in 2012, it increased sharply in Southern Europe. Many of Europe’s banks are still holding large real estate portfolios. This, together with other structural market conditions such as the liquidation of German open-ended funds and private funds and the maturing of ‘bad banks’ such as NAMA, FMS and Sareb, are likely to result in more portfolios being traded. Additionally, the strong fundraising by opportunistic funds in 2013 will create an investor-led demand for larger transactions and clearly portfolio transactions are one of the best ways to achieve scale.

Colisee III & IV, ParisGrosvenor

Blackstone Group

€99 million

JLL Acquisition

15 Office Investment Market Outlook

Aviva Portfolio, UKAvivaApollo€428 million

Number of assets: 133

JLL Sale

Thirdly, 2013 has been a very strong year for fundraising by private real estate funds with opportunistic strategies. According to Indirex, opportunistic funds accounted for 49% of the record €115 billion of global real estate fundraising in 2013. The top three largest global fund raisers, Lone Star (€8.7 billion), Brookfield (€8.6 billion) and Blackstone (€6.8 billion) accounted for 20% of the total capital raised. We expect US investors to be a driving force behind the move towards opportunistic strategies as they typically demand higher returns when investing internationally. This was confirmed by the 2014 INREV Intentions Survey which found that without US investors the intended exposure to value add/opportunistic would actually have dropped.

Finally, we expect development to return in 2014. A lack of financing and subdued occupier markets have held back development in recent years. Over the last five years, the delivery of new product has been below the long-term average. However, we are forecasting a 20% increase in office development completions in 2014 and again in 2015. This is not yet a full return to speculative development, as 50% of total office supply to be delivered in 2014 has already been pre-let, but it is nevertheless a welcome change. Moreover, the competitive conditions in core markets could lead to more development partnerships where core investors are securing quality assets at the development stage.

JLL European Capital Markets 16

Ulysees, Dublin

Lloyds Banking Group

Brehon / Pimco

€152 million

In early 2013 JLL was appointed by the Asset managers and Receivers for Lloyds Banking Group to review the Ulysees portfolio with a view to a disposal before the end of 2013. Following a thorough review on pricing, portfolio mix, asset management future requirements and pre-sale due-diligence our strategy was to maximise pricing by offering the portfolio in three separate lots or as a single portfolio based on the asset mix, tenant profile and geographical spread.

● Ulysees portfolio is a mixed use portfolio of 25 properties in the centre of Dublin.

● Strong weighting towards Government tenants, who accounted for over 53% of the total income of €13.94 million per annum.

● Launched in late October at a guide price of €140 million.

JLL’s experience in large scale complex portfolio transactions enabled us to deal with any obstacles in advance of marketing in order to present the portfolio to the market in its cleanest light. The bidding process secured over €1.15 billion of bids. The deal closed in December fitting the required timeframe but exceeded the clients expectations with a €152 million final sale price.

JLL Sale

90 Long Acre, LondonPelham Associates

Northwood Investors

€200 million

JLL Sale

Tour Pacific, ParisIvanhoé Cambridge

Tishman Speyer

€200 million

JLL Sale

However, investors will need to keep a close watch on the impact of Fed tapering. We have already experienced major falls in emerging market currencies and a sell-off in stock markets around the globe in mid-January as the Fed

continued to reign-in its bond purchasing. As a result, volatility increased globally which was illustrated by the CBOE VIX S&P500 volatility index reaching a 12 month high; investors will need to remain wary if venturing into risk-on strategies.

JLL European Capital Markets 18

More “Equity and Expertise” joint ventures with global partners

20

More “Equity and Expertise” joint ventures with global partners

Over the last five years, c. €64 billion of global capital has been invested in European offices. Many purchasers were first-time investors executing global real estate strategies in order to diversify their domestic real estate exposure. A preferred way of access, deployed by these investors, has been “Equity and Expertise” joint ventures, where the equity is provided by the global investor while the local expert partner manages the assets. We estimate that in 2013 one in six deals over €100 million across all sectors was an “Equity and Expertise” deal.

Better control over investment decisions and a full alignment between both partners are the main reasons for this structure. Hence most “Equity and Expertise” joint ventures have been 50:50 equity arrangements. As the deal size tends to be quite large, the expert partners typically already own the assets (e.g. Crown Estate selling a 25% stake in Quadrant 3 to Norges Bank IM) or have sizeable balance sheets to carry the investment (e.g. Axa and NBIM buying the RBS portfolio in Germany).

21 Office Investment Market Outlook

Belair, BrusselsBreevast & Immobel

Hanover Leasing / Asian Investor

€392 million

JLL Acquisition

JLL was appointed on the sale of Tour Sequana, an iconic office building in Paris.

● This iconic office tower of the Parisian landscape is located in the heart of the well-established business district of Issy-les-Moulineaux, fronting the Paris ring road.

● The high-rise building was delivered in 2010 and benefits from an HQE® environmental certification.

● Provides 43,000 sq m of lettable area arranged over 23 floors with 539 parking spaces.

● The tower is fully leased to Bouygues Telecom as their French headquarters.

Hines acquired Tour Sequana in joint-venture with a Korean investment fund.

Tour Sequana, Paris

Les Docks Lyonnais

Hines

€316 million

JLL Sale

Early in 2013 JLL was appointed by Segro to sell IQ Winnersh in Reading.

● The site is an 85-acre business park located 16 miles from the M25 and 23 miles west of Heathrow.

● IQ Winnersh is in single ownership extending to 1.272 million sq ft in 36 buildings with a mixture of office and R&D use.

● There are a further 4 development sites for 450,000 sq ft of accommodation.

● Average weighted unexpired term to break is 5.6 years and to expiry 8.6 years with a low overall rent of £16.55 psf. Low void of only 7.1%.

JLL’s experience on the ground and relationships with investors worldwide was essential to the completion of the deal. £3.3 billion of offers were received from 15 parties with 75% of this representing North American equity. Our timeline, meticulous planning and rigorous sales approach meant that when investors were ready to proceed – we could facilitate the deal close in a very short space of time. From an initial quoting price £275 million, final sale price of €380 million represented 7.4% yield.

IQ Winnersh, Reading

Segro

Oaktree Patrizia

€380 million

JLL Sale

In 2013 we have also seen these global equity investors active in smaller European markets. Examples include Hannover leasing’s acquisition of the Belair office building in Brussels in joint venture with an Asian capital partner for approximately €300 million and the acquisition of Ropemaker Place in London by AXA in joint venture involving two Asian capital partners for circa €560 million (£470 million).

With better access to cheap equity and debt in a growing number of European markets, domestic investors will reduce their need for equity injections from global capital. Hence, apart from increased competition for core assets, we are likely to see more innovative ways in which these “Equity and Expertise” partnerships access product. One option is buying into the development phase, as illustrated by Oxford Property’s acquisition of a 50% stake in the Crown Estate’s St James’ Market Scheme for £160 million.

Though we expect “Equity and Expertise” transactions to be a preferred route, separate account mandates with limited or no partner equity participation will also remain an option for global capital. This will particularly be the case when the expert operates in a niche market and does not have the balance sheet to fund sizeable equity investments. As a result, we believe we will see more “Equity and Expertise” joint ventures with smaller expert stakes and maybe a greater number of equity partners to share the risk.

Competition will reshape markets and the “Equity and Expertise” joint venture model will evolve for sure. However, the underlying trends of globalising real estate markets and a requirement for more control over investment decisions will continue to support the model in 2014. Furthermore, with the market moving “up-the-risk-curve” towards more asset management heavy strategies, the need for local real estate expertise is becoming ever more important.

JLL European Capital Markets 24

Waterside, LondonD2 Private

GAW Capital

€250 million

JLL Sale

Office occupier market fundamentals will catch up

26

Office occupier market fundamentals will catch up

One of the risks in 2013 was the divergence between buoyant office investment capital markets and subdued or even deteriorating occupier markets. While the investment market rose sharply, take-up remained below average and rents were stable at best. However, we believe that occupier market fundamentals will start to converge with investment trends in 2014. Firstly, we have now seen rental growth in several European cities and, secondly, the European economy looks set for a modest recovery. In addition, an increasing number of cities are seeing low levels of new development and a shortage of quality floor space.

Our in-house forecasts for office rental growth for 45 cities in Europe predict that average European prime rents will increase by 3.3% in 2014, 2.6% in 2015 and 2.3% in 2016. All major markets should see rental growth. In the second half of 2013, we had already seen an improvement.

Whereas only eight office markets in Europe recorded positive year-on-year rental growth at the end of the third quarter, the number had already increased to fourteen by the end of December 2013. The strongest improvements were recorded in London and Dublin.

In Central London, we witnessed the return of rental growth with one of the best occupier market years in the last decade. In the City take-up soared to 660,000 sq m (7.1 million sq ft), the strongest figure since 2000 and the second highest on record, while the West End saw take-up rise to 316,000 sq m (3.4 million sq ft), up 30% on 2012. Furthermore, the return of strong pre-letting activity was a key feature of the market in 2013 and we expect this to continue in 2014. As a result, our rental growth forecasts until 2017 are for strong growth: +5.5% on average per annum for the West End and +5.7% for the City.

27 Office Investment Market Outlook

Perspective Defense, ParisAXA REIM

Hines

€127 million

JLL Sale

Devonshire House is a landmark office and retail freehold property located opposite the Ritz Hotel, in Mayfair, London’s most prestigious and exclusive address. With only three owners in the last 100 years, Devonshire House is one of only a handful of buildings in Mayfair over 100,000 sq ft and represented a rare opportunity to acquire the freehold of an iconic London property.

● One of the largest single assets in the West End and considered one of the finest buildings in Mayfair.

● Rare 0.75 acre freehold island site.● Prime position on Piccadilly

with views over Green Park and Buckingham Palace.

● Attractive mix of secure income and asset management opportunities.

● Diverse income stream: multi-let to a broad base of high profile retail and office tenants.

JLL provided in depth advice to the purchaser to facilitate and advise on the acquisition.

Devonshire House, London

Witkoff Group

Pontegadea

Confidential

JLL Acquisition

JLL was appointed on the sale of 33 Rue Lafayette in Paris by Ivanhoé Cambridge.

● An exceptional island site in the heart of the financial district of Paris, the Opéra sector.

● A total lettable area of approximately 28,700 sq m.

● Fully refurbished in 2005 combining prestige with efficiency.

Our relationships with investors across EMEA and our understanding of their investment criteria enabled us to quickly identify Deka Immobilien as a potential purchaser. Deka Immobilien later purchased the property for €278 million.

33 Rue Lafayette, Paris

Ivanhoé Cambridge

Deka Immobilien

€278 million

JLL Sale

Ireland not only saw a strong recovery in its investment markets, but leasing markets also reported a strong bounce back. Dublin prime yields contracted by 150 bps from 7.25 to 5.75 during 2013 and take-up in Q4 2013 was 68% up on the previous quarter. This is the highest level of quarterly take-up since Q2 2008 and rents in Dublin are now 17% higher than at the end of 2012. Nevertheless, prime rents remain well below peak levels which offers further potential for growth if the Irish economy continues its upwards trend.

Despite the improvement in rents and yields, capital values are still way below peak levels in most peripheral markets. For example, capital values in Dublin are still 62% below peak and in madrid 57%. Even when compared to 10 year averages (which include both peak and trough valuation), these markets are priced at considerable discounts (-27% in both markets). Other markets, like Stockholm (+33%) and London West End (+28%) are trading well above their 10-year average, underlining that when occupier trends improve investors are willing to price in these better prospects.

With yields close to or even exceeding prior peak levels, rental growth is the main driver for capital growth. While our in-house forecasts are based on only modest economic growth, the global recovery is still fragile and the effects of Fed tapering on economic growth are unknown. However, we believe that if this modest growth materialises then, combined with a shortage of quality office space in key inner-city locations, this should drive occupier demand more broadly across Europe’s office markets, which should support our positive forecasts.

JLL European Capital Markets 30

99 Kensington High Street, LondonGenting HPC Capitaland

Sirosa

€275 million

JLL Sale

Domestic and European capital will remain highly competitive

32

Domestic and European capital will remain highly competitive

One of the major trends in 2013 was the resurgence of domestic capital in Europe. Despite global capital increasing its share of the overall European real estate investment market from 25% to 27%, domestic capital gained market share in each of the three major office markets. In fact, even in the UK, Europe’s most international market, European and UK capital combined accounted for over half of office investment in 2013.

German investors were once again the largest buyers in the European office market acquiring €13.1 billion in 2013, up 17% on 2012. Moreover, German investment in European offices was more than double that of all Asian capital combined and accounted for €4.2 billion worth of cross-border transactions. This is 21% higher than the second largest group, US investors. In contrast

with 2012, German capital is now able to compete for very large deals, outbidding global capital, as shown by Deka’s €559 million acquisition of the St Botolph building in London and Allianz’s €300 million acquisition of Skyper in Frankfurt.

The strongest increase in domestic activity was recorded in Paris where domestic purchasers increased their market share from 61% to 69%. Like German capital, French capital is now increasingly bidding on larger deals and competing directly with global capital. Looking at office deals >€100 million, the share of domestic investors increased from 48% in 2012 to 52%. It is notably the traditional French real estate investors, such as the life insurance companies and pension funds, that have come back in force. Almost all French capital targeting offices (91%) is still invested domestically.

42 Avenue de Friedland, ParisIvanhoé Cambridge

Assurances du Crédit mutuel

€161 million

JLL Sale

33 Office Investment Market Outlook

WestEnd Duo, FrankfurtING / CBRE Global Investors

DeAWM

€240 million

JLL Sale

JLL European Capital Markets 34

Skyper, FrankfurtUBS

Allianz

€300 million

JLL Sale

White Gardens, Moscow

AIG Lincoln / VTBC / TPG

Millhouse Capital

€545 million

JLL Sale

White Gardens Office Centre is a premium office development built to the highest standards including BREEAM requirements. The office complex consists of two buildings of 63,700 sq m of rentable area and is the second of two phases of White District, one of the most prestigious business locations in Moscow. The sale represents the largest office investment transaction on the Moscow market in 2013.

● Top quality office centre located in the heart of Moscow central business district.

● Most recent prime office property to be completed in Moscow compliant with the highest environmental standards.

● Close proximity to major transport routes of the city.

● White District – the master-planned area encompassing both White Gardens and neighbouring White Square – has become one of Moscow’s most popular dining and networking destinations.

● Contemporary design, efficient architectural solutions and floor layouts with terraces on higher floors.

JLL advised on the sale. The sale was structured as an off-market transaction with the asset introduced to the buyer at the final stage of construction. Despite leasing risks associated with the new development, JLL ensured successful deal closing immediately after construction completion.

Greater London offices remained the near-exclusive domain for overseas capital with UK capital accounting for just 32% of the market in 2013. However domestic capital heavily targetted the regional office markets. Total investment in regional offices increased by 71% to £3.8 billion (€4.5 billion), of which £2.6 billion (€3.1 billion) was bought by UK capital. Overall, UK investors were net sellers in UK offices in 2013, but it appears that at

least part of the net outflows from Greater London offices (£3.3 billion) was redeployed in UK regional offices.

In our view, the outlook for 2014, for a further strengthening of domestic capital in Europe, is positive with 46% of European investors surveyed in the 2014 INREV Intentions survey confirming their intention to increase their allocations to real estate versus 7% who will decrease them.

The Circle, ZurichFlughafen Zürich AG

Swiss Life AG (49%)

€470 million

JLL Sale

JLL European Capital Markets 36

Jericho, StockholmAllianz

AMF Fashigheter

€181 million

JLL Sale

The recovery in peripheral European markets is for real

38

The recovery in peripheral European markets is for real

2013 witnessed a strong growth in markets outside the three major core markets and the Nordics. These peripheral markets, Southern Europe, the Benelux and Ireland, which accounted for only €5.1 billion of office investment in 2011, grew 51% in 2013 compared to 2012 and now account for 10% of all European office transactions. With an abundance of opportunistic capital eyeing Europe and the general trend of “moving up the risk curve” now well established, the recovery in these markets is for real.

In Southern Europe, 2013 saw office investment rise 41% year-on-year to reach €2.5 billion. In Italy, it increased by 103% to €1.5 billion, while even Greece saw growth to €229 million (from just €52 million). Although office investment in Spain decreased from €899 million to €694 million, Spain saw a major deal by an international institution, with AXA acquiring an office portfolio in Barcelona for €172 million. If we adjust for price changes, the 2013 volume of “bricks and mortar” accounted for 32% of the 2007 volume, indicating the return of some liquidity.

Catalan Government Portfolio, BarcelonaGeneralitat

AXA REIM

€172 million

JLL Acquisition

39 Office Investment Market Outlook

Bodio Centre: Buildings 4–5, MilanAberdeen Immobilien

AXA REIM

€64 million

JLL Sale

A strong improvement in Ireland’s occupier market in 2013 was accompanied by a 150 bps drop in Dublin prime office yields and €1.0 billion invested in offices. Further evidence of the Irish market’s recovery was demonstrated by the introduction of the market’s first ever REITs. Two IPOs raised approximately €500 million in equity on the Dublin stock exchange and Green REIT, the first to list, has already invested two thirds of its capital. In addition, Ireland has also seen further workout transactions, notably NPL portfolios such as the €250 million Project Club sold by NAMA to CarVal, and large-scale real estate portfolios such as the c. €155 million Ulysses portfolio in Dublin.

Although not usually included in peripheral Europe, the Benelux office markets have also witnessed hard times, with the banking system scaling back lending, developers moving into receivership and oversupply in some cities. In addition the markets are relatively small within Europe and suffered from a lack of liquidity. However, this changed in 2013, when we saw Asian capital investing in Brussels and the German open ended funds returning to Amsterdam. Overall office investment in the Benelux increased 42% year-on-year. The outlook for 2014 is positive with many opportunistic funds also actively seeking product, the return of German lenders and some signs of economic growth.

JLL European Capital Markets 40

Miasteczko Orange, WarsawBouygues Immobilier

Qatar Holding

Confidential

JLL Sale

La Touche House, DublinWarren Private Clients

Credit Suisse

€46 million

JLL Sale

Further impetus for these markets should come from the “bad banks” and workouts from acquired NPL portfolios. NAMA is now fully established in Ireland, while Sareb in Spain has sold its first NPL portfolio, which is linked to major property companies and worth €900 million. Additionally, banks are increasingly using the window

of opportunity created by the strong fundraising of opportunistic debt and NPL funds to sell NPL books. In the UK, Lloyds and RBS have been actively selling and numerous investors are currently pouring over Eurohypo’s €5 billion Spanish loan portfolio which Commerzbank recently put up for sale.

41 Office Investment Market Outlook

Waverley Gate, EdinburghPruPIM

Highcross Fund

€71 million

JLL Acquisition

The Lakeview, BucharestAIG Lincoln and Dinu Patriciu Global Properties

New Europe Property Investors

€63 million

JLL Sale

Spain and Madrid have been cited by many investors as the most interesting market for value add/opportunistic investments. For the office markets, the value case is clear: Madrid prime office rents are now back at 1995 levels when adjusted for inflation and Madrid office capital values are more than a quarter (27%) below their 10-year

average and 57% below the last peak. Furthermore, our forecasts suggest that Madrid prime rents could rise by 32% over the period 2013–17.

JLL European Capital Markets 42

However, with the economy still weak, competition for quality assets is on the rise and, given the absence of fully distressed and motivated sellers, we expect that some investors will be disappointed as they cannot

source the right product. Nevertheless, in 2014 we see bid-ask spreads in these less competitive and debt-starved markets narrow under the pressure of increasing capital inflows and stabilising rental markets.

43 Office Investment Market Outlook

Senator, WarsawGhelamco Group

Union Investment

€120 million

JLL Sale

Dauphine Part Dieu, LyonGecina

ACM

€56 million

JLL Sale

JLL European Capital Markets 44

The Park is a landmark business park, one of the most recognisable in Central Europe situated in the popular non-CBD office hub of Prague 4, Czech Republic. Forming a development that has seen additional buildings constructed on the park since its origination approximately ten years ago, the office hub’s critical mass combines with it’s prominent and dominating position along the main arterial route in to the city to form an unparalleled development. The Park represented a landmark transaction and a substantial distribution of North American capital in to the Czech real estate sector:

● The largest business park in CEE constructed with excellent build quality.

● A park boasting almost exclusively blue-chip international tenants.

● Excellent public and private access options and employee amenities.

● International business hub employing people from all over the world.

● Diverse income stream: multi-let to a broad base of high profile office tenants.

JLL provided in depth advice to the purchaser to facilitate and advise on the acquisition.

The Park, Prague

Aberdeen Immobilien

Starwood Capital

C. €300 million

JLL Acquisition

JLL Contacts

46

European Office Capital Markets Specialists

Pan European

Debt

International Capital Group

Research

Oliver Kummerfeldt +44 (0)203 147 [email protected]

Alex Fortescue +44 (0)207 399 [email protected]

Robert Stassen +44 (0)203 147 [email protected]

Daniel Bumpstead+44 (0)207 852 [email protected]

Cyril Hoyaux+33 1 40 55 17 [email protected]

Christophe Murciani+33 1 40 55 [email protected]

Jörg Schürmann+49 (0) 69 2003 [email protected]

Chris Holmes+44 (0)207 399 [email protected]

Alistair Meadows (Asia)[email protected]

Fadi Mousalli (ME)[email protected]

Stephen Collins (US)[email protected]

Matthew Richards (EU)+44 (0)207 399 [email protected]

Fraser Bowen+44 (0)207 399 [email protected]

Gemma Brown+44 (0)207 087 [email protected]

Penny Hacking+44 (0)207 087 [email protected]

Peter Hensby+44 (0)207 399 [email protected]

Chris Staveley+44 (0)207 399 [email protected]

Troy Javaher+420 227 04 [email protected]

Contact any of the team for access to the latest market opportunities

47 JLL European Capital Markets

Christian Hohenthal +358 40 737 [email protected]

Finland

Stephan von Barczy+33 1 40 55 17 [email protected]

France

Marcus Lütgering+49 (89) 290088 [email protected]

Germany

Benjamin [email protected]

Hungary

John Moran+353 1 6731 637 [email protected]

Ireland

Davide Dalmiglio+00 39 02 85 86 86 [email protected]

Italy

Gaurav [email protected]

MENA

Dre van Leeuwen+31 (0)20 [email protected]

Netherlands

Tomasz Puch+48 22 318 [email protected]

Poland

Pedro Lancastre+351 213 58 [email protected]

Portugal

Gijs [email protected]

Romania

Thomas Devonshire-Griffin+7 495 [email protected]

Russia

Juan-Manuel Ortega+34 93 445 [email protected]

Spain

Daniel Gorosch+46 (8) 453 51 [email protected]

Sweden

Jan Eckert [email protected]

Switzerland

Idil Hamzadi+90 212 350 08 [email protected]

Chris Ireland+44 207 087 [email protected]

Damian Corbett+44 (0)207 399 [email protected]

Turkey UK

Jean-Philippe Vroninks +32 2 550 [email protected]

Belux

Stuart Jordan+420 227 043 [email protected]

Czech Republic

JLL European Capital Markets 48

www.joneslanglasalle.eu

Copyright © Jones Lang LaSalle IP, INC 2014No part of this publication may be reproduced or transmitted in any form or by any means without prior written consent of Jones Lang LaSalle. It is based on material that we believe to be reliable. Whilst every effort has been made to ensure its accuracy, we cannot offer any warranty that it contains no factual errors. We would like to be told of any such errors in order to correct them.