european union balance of payments/ international investment

TRANSCRIPT

��������������������� ����������

��������������������������������������������

���������

EUROPEAN UNIONBALANCE OF PAYMENTS/

INTERNATIONALINVESTMENT POSITIONSTATISTICAL METHODS

November 2000

© European Central Bank, 2000

Address Kaiserstrasse 29

D-60311 Frankfurt am Main

Germany

Postal address Postfach 16 03 19

D-60066 Frankfurt am Main

Germany

Telephone +49 69 1344 0

Internet http://www.ecb.int

Fax +49 69 1344 6000

Telex 411 144 ecb d

All rights reserved.

Reproduction for educational and non-commercial purposes is permitted provided that the source is acknowledged.

ISSN 1562-5036

ECB EU Balance of payments statistical methods � November 2000 3

Contents

List of abbreviations andacronyms ....................................... 7

1 FOREWORD ........................... 9

2 Compilation of euro areabalance of payments andinternational investmentposition statistics .................. 10

2.1 The legal framework of euro areabalance of payments andinternational investment positionstatistics .......................................... 10

2.2 Shared responsibility betweenthe European Central Bank(Directorate General Statistics)and the European Commission(Eurostat) ........................................ 10

2.3 The ECB�s contribution tothe euro area aggregates ............... 10

2.4 Statistical reporting requirementsfor national compilers ................... 11

2.4.1 ECB data requirementsin balance of paymentsstatistics ......................................... 11

2.4.2 ECB data requirements ininternational investmentposition statistics ......................... 14

2.4.3 ECB data requirements forthe Eurosystem�s internationalreserves position ......................... 15

2.5 Methods of compiling theeuro area aggregates ..................... 15

3 Concepts, definitions andagreed practices of the euroarea balance of payments andinternational investmentposition statistics .................. 16

3.1 General principles of balance ofpayments and internationalinvestment position statistics ...... 17

3.1.1 Balance of paymentsstatistics ......................................... 17

3.1.2 International investmentposition statistics ......................... 17

3.1.3 Accounting principles fortransactions and stocks ............. 18

3.1.4 Euro area residency ................... 193.1.5 Classification principles for

balance of payments andinternational investmentposition statements ..................... 20

3.1.6 Sectorisation ................................. 21

3.2 Goods .............................................. 24

3.3 Services ........................................... 24

3.4 Income ............................................. 25

3.4.1 Definition and coverageof income ...................................... 25

3.4.2 Definition of compensationof employees ................................ 25

3.4.3 Definition of investmentincome ........................................... 25

3.4.4 Main types of investmentincome ........................................... 25

3.4.5 Specific issues relatedto direct investmentincome ........................................... 26

3.4.6 Specific issues relatedto portfolio investmentincome ........................................... 27

3.4.7 Specific issues relatedto other investmentincome ........................................... 31

3.5 Current transfers ........................... 32

4 ECB EU Balance of payments statistical methods � November 2000

3.6 Capital account .............................. 33

3.6.1 Capital transfers andsub-components .......................... 33

3.6.2 Acquisition/disposal ofnon-produced non-financialassets .............................................. 35

3.7 Direct investment .......................... 35

3.7.1 Definition and coverage ............ 353.7.2 Recording direct

investment ona directional basis ....................... 36

3.7.3 Special issues relatedto stocks ........................................ 37

3.8 Portfolio investment ...................... 37

3.8.1 Definition and coverage ............ 373.8.2 Geographical allocation principle

for change of ownership ............ 383.8.3 Specific types of debt

securities ....................................... 393.8.4 Borderline cases .......................... 393.8.5 Special issues related

to stocks ........................................ 40

3.9 Financial derivatives ...................... 41

3.9.1 Definition and coverage ............ 413.9.2 Futures ........................................... 423.9.3 Options .......................................... 443.9.4 Swaps, forwards and forward

rate agreements ........................... 46

3.10Other investment ........................... 48

3.10.1 Definition and coverage ............ 483.10.2 Repurchase agreements,

bond lending and otherrelated instruments ..................... 48

3.10.3 Balances from TARGEToperations ..................................... 50

3.10.4 Recording of MFIs�transactions in loansand deposits ................................. 50

3.10.5 Special issues relatedto stocks ........................................ 50

3.11Reserve assets ................................ 51

3.11.1 Definition of the Eurosystem�sreserve assets .............................. 51

3.11.2 Concept of gross reserves ........ 523.11.3 Valuation principles .................... 523.11.4 Specific issues related

to gold ............................................ 523.11.5 Specific issues related to

the positions vis-à-vis the IMF(including SDRs) .......................... 53

3.11.6 Specific issues related tosecurities ....................................... 53

3.11.7 Specific issues relatedto currency and deposits .......... 53

3.11.8 Specific issues related tofinancial derivatives .................... 54

4 Country-specific details ........ 57

4.1 Belgium/Luxembourg .................... 57

4.1.1 Organisation chart(s) ................. 584.1.2 Institutional aspects .................... 604.1.3 Statistical system.......................... 624.1.4 Monthly key items ....................... 664.1.5 Investment income ...................... 674.1.6 Capital account ........................... 694.1.7 Direct investment ....................... 694.1.8 Portfolio investment ................... 714.1.9 Financial derivatives ................... 724.1.10 Other investment ........................ 734.1.11 Reserve assets .............................. 744.1.12 International investment

position .......................................... 744.1.13 Administration ............................. 76

4.2 Denmark .......................................... 77

4.2.1 Organisation chart(s) ................. 784.2.2 Institutional aspects .................... 804.2.3 Statistical system.......................... 814.2.4 Implementation ............................ 854.2.5 Investment income ...................... 864.2.6 Capital account ........................... 884.2.7 Direct investment ....................... 894.2.8 Portfolio investment ................... 894.2.9 Financial derivatives ................... 904.2.10 Other investment ........................ 914.2.11 Reserve assets .............................. 924.2.12 International investment

position .......................................... 924.2.13 Administration ............................. 93

ECB EU Balance of payments statistical methods � November 2000 5

4.3 Germany .......................................... 95

4.3.1 Organisation chart(s) ................. 964.3.2 Institutional aspects .................... 974.3.3 Statistical system.......................... 984.3.4 Monthly key items .................... 1024.3.5 Investment income ................... 1024.3.6 Capital account ........................ 1034.3.7 Direct investment .................... 1044.3.8 Portfolio investment ................ 1044.3.9 Financial derivatives ................ 1054.3.10 Other investment ..................... 1064.3.11 Reserve assets ........................... 1064.3.12 International investment

position ....................................... 1064.3.13 Administration .......................... 109

4.4 Greece ........................................... 111

4.4.1 Organisation chart(s) .............. 1124.4.2 Institutional aspects ................. 1134.4.3 Statistical system....................... 1144.4.4 Implementation ......................... 1164.4.5 Investment income ................... 1184.4.6 Capital account ........................ 1194.4.7 Direct investment .................... 1204.4.8 Portfolio investment ................ 1214.4.9 Financial derivatives ................ 1224.4.10 Other investment ..................... 1234.4.11 Reserve assets ........................... 1234.4.12 International investment

position ....................................... 1244.4.13 Administration .......................... 125

4.5 Spain .............................................. 127

4.5.1 Organisation chart(s) .............. 1284.5.2 Institutional aspects ................. 1294.5.3 Statistical system....................... 1304.5.4 Monthly key items .................... 1334.5.5 Investment income ................... 1344.5.6 Capital account ........................ 1364.5.7 Direct investment .................... 1364.5.8 Portfolio investment ................ 1374.5.9 Financial derivatives ................ 1384.5.10 Other investment ..................... 1394.5.11 Reserve assets ........................... 1404.5.12 International investment

position ....................................... 1404.5.13 Administration .......................... 144

4.6 France ............................................ 145

4.6.1 Organisation chart(s) .............. 146

4.6.2 Institutional aspects ................. 1474.6.3 Statistical system....................... 1474.6.4 Monthly key items .................... 1524.6.5 Investment income ................... 1554.6.6 Capital account ........................ 1574.6.7 Direct investment .................... 1584.6.8 Portfolio investment ................ 1594.6.9 Financial derivatives ................ 1614.6.10 Other investment ..................... 1614.6.11 Reserve assets ........................... 1624.6.12 International investment

position ....................................... 1634.6.13 Administration .......................... 164

4.7 Ireland............................................ 165

4.7.1 Organisation chart(s) .............. 1664.7.2 Institutional aspects ................. 1674.7.3 Statistical system....................... 1694.7.4 Monthly key items .................... 1774.7.5 Investment income ................... 1804.7.6 Capital account ........................ 1824.7.7 Direct investment .................... 1824.7.8 Portfolio investment ................ 1834.7.9 Financial derivatives ................ 1844.7.10 Other investment ..................... 1854.7.11 Reserve assets ........................... 1864.7.12 International investment

position ....................................... 1864.7.13 Administration .......................... 187

4.8 Italy ............................................... 189

4.8.1 Organisation chart(s) .............. 1904.8.2 Institutional aspects ................. 1914.8.3 Statistical system....................... 1924.8.4 Monthly key items .................... 1954.8.5 Investment income ................... 1964.8.6 Capital account ........................ 1984.8.7 Direct investment .................... 1984.8.8 Portfolio investment ................ 1994.8.9 Financial derivatives ................ 1994.8.10 Other investment ..................... 2004.8.11 Reserve assets ........................... 2014.8.12 International investment

position ....................................... 2014.8.13 Administration .......................... 202

4.9 The Netherlands .......................... 205

4.9.1 Organisation chart(s) .............. 2064.9.2 Institutional aspects ................. 2074.9.3 Statistical system....................... 2084.9.4 Monthly key items .................... 210

6 ECB EU Balance of payments statistical methods � November 2000

4.9.5 Investment income ................... 2114.9.6 Capital account ........................ 2114.9.7 Direct investment .................... 2124.9.8 Portfolio investment ................ 2124.9.9 Financial derivatives ................ 2134.9.10 Other investment ..................... 2134.9.11 Reserve assets ........................... 2144.9.12 International investment

position ....................................... 2144.9.13 Administration .......................... 215

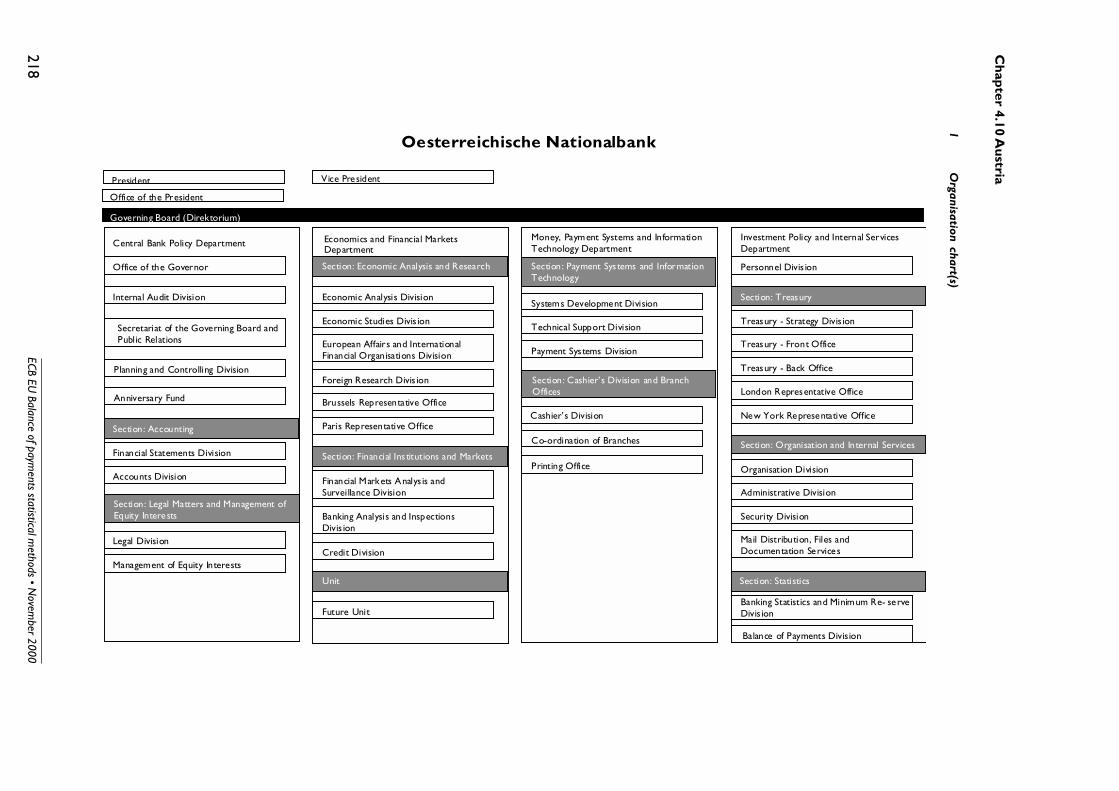

4.10Austria ........................................... 217

4.10.1 Organisation chart(s) .............. 2184.10.2 Institutional aspects ................. 2194.10.3 Statistical system....................... 2214.10.4 Monthly key items .................... 2264.10.5 Investment income ................... 2284.10.6 Capital account ........................ 2304.10.7 Direct investment .................... 2314.10.8 Portfolio investment ................ 2314.10.9 Financial derivatives ................ 2334.10.10 Other investment ..................... 2344.10.11 Reserve assets ........................... 2354.10.12 International investment

position ....................................... 2364.10.13 Administration .......................... 238

4.11Portugal ......................................... 239

4.11.1 Organisation chart(s) .............. 2404.11.2 Institutional aspects ................. 2414.11.3 Statistical system....................... 2424.11.4 Monthly key items .................... 2454.11.5 Investment income ................... 2474.11.6 Capital account ........................ 2494.11.7 Direct investment .................... 2494.11.8 Portfolio investment ................ 2504.11.9 Financial derivatives ................ 2514.11.10 Other investment ..................... 2524.11.11 Reserve assets ........................... 2534.11.12 International investment

position ....................................... 2544.11.13 Administration .......................... 255

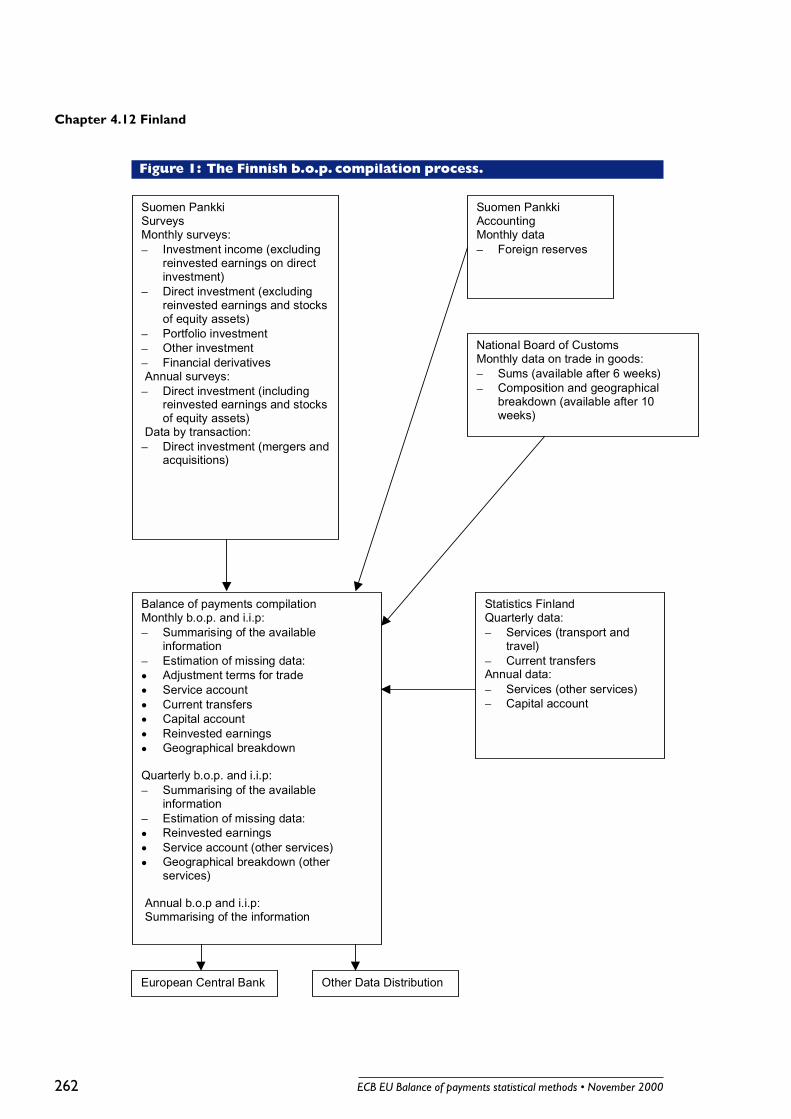

4.12Finland ........................................... 257

4.12.1 Organisation chart(s) .............. 2584.12.2 Institutional aspects ................. 2594.12.3 Statistical system....................... 2594.12.4 Monthly key items .................... 264

4.12.5 Investment income ................... 2654.12.6 Capital account ........................ 2684.12.7 Direct investment .................... 2684.12.8 Portfolio investment ................ 2704.12.9 Financial derivatives ................ 2724.12.10 Other investment ..................... 2744.12.11 Reserve assets ........................... 2754.12.12 International investment

position ....................................... 2754.12.13 Administration .......................... 276

4.13Sweden .......................................... 277

4.13.1 Organisation chart(s) .............. 2784.13.2 Institutional aspects ................. 2794.13.3 Statistical system....................... 2804.13.4 Implementation ......................... 2844.13.5 Investment income ................... 2854.13.6 Capital account ........................ 2874.13.7 Direct investment .................... 2874.13.8 Portfolio investment ................ 2884.13.9 Financial derivatives ................ 2894.13.10 Other investment ..................... 2894.13.11 Reserve assets ........................... 2904.13.12 International investment

position ....................................... 2904.13.13 Administration .......................... 293

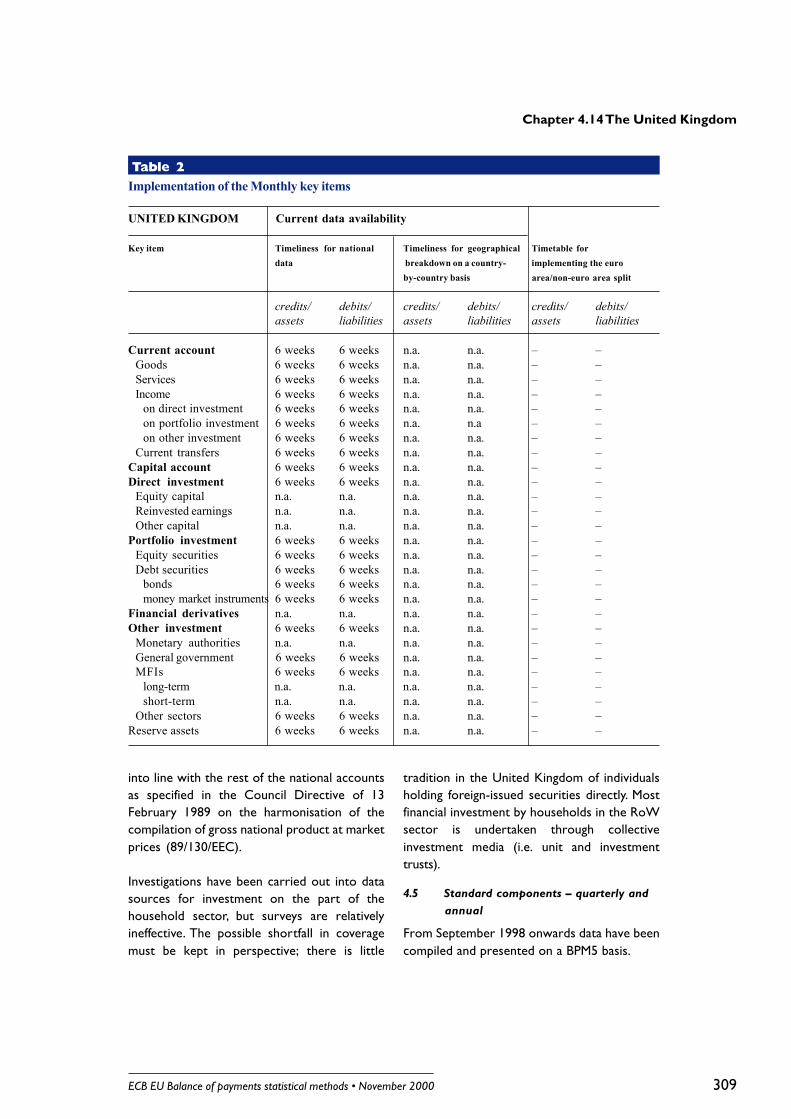

4.14The United Kingdom ................... 295

4.14.1 Organisation chart(s) .............. 2964.14.2 Institutional aspects ................. 2984.14.3 Statistical system....................... 3004.14.4 Implementation ......................... 3054.14.5 Investment income ................... 3104.14.6 Capital account ........................ 3114.14.7 Direct investment .................... 3114.14.8 Portfolio investment ................ 3134.14.9 Financial derivatives ................ 3144.14.10 Other investment ..................... 3164.14.11 Reserve assets ........................... 3174.14.12 International investment

position ....................................... 3184.14.13 Administration .......................... 320

5 Annex ................................... 321

5.1 Glossary ........................................ 321

5.2 Contributors ................................. 325

ECB EU Balance of payments statistical methods � November 2000 7

List of abbreviations and acronyms

ARIMA Auto-Regressive IntegratedMoving Average

b.o.p. Balance of paymentsBAFI Database on French financial

agentsBcL Banque centrale du LuxembourgBIS Bank for International SettlementsBLEI Belgian-Luxembourg Exchange

InstituteBLEU Belgian-Luxembourg Economic

UnionBOPFS Balance of Payments and

Financial SectorBOPSTA A sub-set of the EDIFACT

message �GESMES/ECOSER� forb.o.p. statistics

BPM5 IMF Balance of Payments Manual(5th edition)

BSG Business Statistics Group (UnitedKingdom)

c.i.f. Cost, insurance and freight atthe importer�s border

CBS Central Bureau of Statistics(Netherlands)

CCIRS Cross-currency interest rate swapsCII Collective investment institutionCNMV Comisión Nacional del Mercado

de Valores (Spanish nationalstock market Commission � Spain)

COE External Transaction Report(registers � Portugal)

COS Chamber of Shipping (UnitedKingdom)

CPB Central Planning Bureau(Netherlands)

CPE External Position Report(registers � Portugal)

CPI Consumer price indexCPIS IMF Co-ordinated Portfolio

Investment SurveyCREST Settlement system for UK shares

and other corporate securitiesCRP Compte-rendu de paiement

(standard record of payment -France)

CSDB ECB Centralised SecuritiesDatabase (in project)

CSO Central Statistical Office (Ireland)CVS Comunicazione valutaria

statistica (statistical reportingform - Italy)

DDG Déclarant direct général (generaldirect reporting company -France)

DRC Direct reporting company (France)EAGGF European Agricultural Guidance

and Guarantee FundEBRD European Bank for Reconstruction

and DevelopmentECB European Central BankECGD Export Credit Guarantee

DepartmentECOSER A sub-set of GESMESEDI Electronic Data InterchangeEDIFACT EDI for Administration,

Commerce and TransportationEMI European Monetary InstituteEMU European Economic and

Monetary UnionERDF European Regional Development

FundESAF Enhanced Structural Adjustment

FacilityESA European System of AccountsESA 95 European System of National

and Regional Accounts (ECRegulation No. 2223/96 dated25 June 1996)

ESCB European System of Central BanksEU European UnionEurostat Statistical Office of the European

Communities (Commission - DGESTAT)

Extrastat System for the collection andcompilation of statistics relatingto trade in goods betweenMember States and non-EUcountries

f.o.b. free on board at the exporter�sborder

FATS Foreign Affiliated Trade StatisticsFDI Foreign direct investmentFININFO A securities data vendor

(France)

8 ECB EU Balance of payments statistical methods � November 2000

FRA Forward rate agreementsFSA Financial Services Authority

(United Kingdom)FSO Federal Statistical Office

(Germany)GAB General Arrangements to

Borrow (under the umbrella ofthe IMF)

GDR General direct respondentGESMES Generic Statistical Message

based on EDIFACT SyntaxGNP Gross national producti.i.p. International investment positionIBRD International Bank for

Reconstruction andDevelopment (World Bank)

IFSC International Financial ServicesCentre (Ireland)

IMF International Monetary FundINE Instituto Nacional de Estatística

(National Institute of Statistics -Portugal)

INSEE French national institute forstatistics and economic research

Intrastat Intra-Community Trade StatisticalSystem

IPS International Passenger Survey(United Kingdom)

ISIN International SecuritiesIdentification Number

Istat Istituto nazionale di statistica(National Statistical Institute -Italy)

ITL Italian liraITRS International transactions

reporting systemLIFFE London International Financial

Futures ExchangeMESAG Macro-Economic Statistics and

Analysis GroupMFI Monetary Financial InstitutionMFSD Monetary and Financial Statistics

Division (United Kingdom)MMIs Money market instrumentsMUMS (European Economic and)

Monetary Union Member State(s)NBB/BNB Nationale Bank van België/

Banque Nationale de Belgique

NAB New Arrangements to Borrow(see GAB)

NCB National central bankNSSG National Statistical Service of

GreeceNTMA National Treasury Management

Agency (Ireland)OECD Organisation for Economic Co-

operation and DevelopmentOeNB Oesterreichische Nationalbank

(Austrian central bank)ONS Office for National Statistics

(United Kingdom)OTC Over-the-counterPGRF Poverty Reduction and Growth

FacilityPRDC Partial direct reporting companyRISC Computer system used by the

Bank of GreeceROW Rest of the WorldSAS Statistical Analysis Software

(trade mark)SDDS IMF Special Data Dissemination

StandardSDRs Special drawing rightsSFI Special financial institutionSIREN Identification code number of

French firmsSMEs Small and medium-sized

enterprisesSNA 93 System of National Accounts of

the United NationsSRS Share Register Survey (United

Kingdom)STATEC Service Central de la Statistique

et des Etudes économiques(Luxembourg)

STC ESCB Statistics CommitteeUIC Ufficio italiano dei cambi (Italian

Foreign Exchange Office)UK United KingdomWG BP ESCB Working Group on &ER Balance of Payments and

External Reserve StatisticsWTO World Trade Organization

ECB EU Balance of payments statistical methods � November 2000 9

1 Foreword

With this publication, which is commonlyreferred to as the �B.o.p. Book�, the EuropeanCentral Bank (ECB) aims to provide partiesinterested in balance of payments (b.o.p.)and international investment position (i.i.p.)statistics as users or compilers with informationrelating to all EU countries on (i) the contentand structure of statistical data and (ii) thecollection methods used. It also gives anoverview of the compilation of the euro areaaggregate figures by explaining the compilationprocedures and underlying methodologicalconcepts agreed by the EU Member States.

In accordance with the division of responsibilitiesin the field of b.o.p./i.i.p. statistics betweenthe European Commission (Eurostat) andthe ECB (Directorate General Statistics), the�B.o.p. Book� focuses mainly on the conceptsand definitions related to the b.o.p. financialaccount and related income and i.i.p. statistics.Nevertheless, it also contains a number ofreferences to items falling under theresponsibility of the European Commission(Eurostat) (i.e. goods, services, compensation ofemployees, the current account as a whole andthe capital account) since the ECB compilesmonthly key items for the entire balance ofpayments.

The initiative was taken in April 1993 that theEuropean Monetary Institute (EMI), the forerunnerof the ECB, would compile a description ofb.o.p. statistical data and collection methods.The Guideline of the European Central BankNo. ECB/1998/17 (1 December 1998) and itsupdated version No. ECB/2000/4 of May 2000state that the ECB �will monitor the compilationmethods used for the reporting of b.o.p. andi.i.p. statistics, as well as the concepts and

definitions applied on a regular basis by theMember States participating in the euro area�and, therefore, provides for a regular update ofthe B.o.p. Book.

The �B.o.p. Book� was first issued in January1998; updates were released in August 1998and in November 1999. The present update ofautumn 2000 provides, in particular, anextension of the Chapter 3 �euro area b.o.p./i.i.p. statistics: concepts, definitions and agreedpractices� in the form of a comprehensivesummary of the methodological concepts andprocedures applied by the ECB in compilingb.o.p. and i.i.p. statistics of the euro area.

The methodological concepts follow internationalstandards (i.e. the IMF Balance of PaymentsManual, 5th edition, the �BPM5�); in addition,further harmonisation proposals in special fieldshave been developed and agreed within theEuropean System of Central Banks (ESCB), inconsultation with the European Commission(Eurostat). EU Member States not initiallyparticipating in the euro area were alsoinvolved in the development of the concepts,definitions and agreed practices as described inChapter 3.

The �B.o.p. Book� is revised every year underthe responsibility of the ECB�s Balance ofPayments Statistics and External ReservesDivision and published on the ECB website(http://www.ecb.int/). It is also available inhardcopy on request from the ECB�s PressDivision. Specific enquiries relating to individualcountries may be addressed to the countriesconcerned, whose contributions are gratefullyacknowledged. A glossary is provided in theAnnex (see list in Chapter 5.1).

10 ECB EU Balance of payments statistical methods � November 2000

2 Compilation of euro area balance of payments and internationalinvestment position statistics

2.1 The legal framework of the euroarea balance of payments andinternational investment positionstatistics

The statistical requirements of the EuropeanCentral Bank (ECB) with respect to the euroarea national central banks (NCBs) and othercompetent national authorities are based onthe Guideline on the �Statistical reportingrequirements of the ECB in the field of balanceof payments, international reserves templateand international investment position statistics(ECB/2000/4)� of May 2000 which replaced theGuideline of 1 December 1998 (ECB/1998/17).This Guideline formalises the requirementsspecified in the �implementation package�(Statistical requirements for Stage Three of EMU,July 1996). It also addresses relevant needsspecified in other documents formally adoptedby the Governing Council of the ECB. Currentinternational standards, such as the IMF Balanceof Payments Manual (5th edition), released inOctober 1993 (BPM5), the UN System ofNational Accounts (SNA 93) and the EuropeanSystem of National and Regional Accounts(ESA 95), have been used as reference informulating these concepts and definitions.

2.2 Shared responsibility betweenthe European Central Bank(Directorate General Statistics)and the European Commission(Eurostat)

The European Commission (Eurostat) and theECB�s Directorate General Statistics (DG-ST)have laid down the framework for the jointdefinition and compilation of balance ofpayments (b.o.p.) and international investmentposition (i.i.p.) statistics at the European level.

The statistical competence of the twoorganisations is defined with respect to(i) conceptual issues and (ii) the compilationand publication of b.o.p./i.i.p. statistics at the

European level. With respect to (i) conceptualissues, the Commission (Eurostat) is responsiblefor the concepts and definitions related to theb.o.p. current and capital accounts, except forinvestment income, which is closely linked tothe financial account.

The ECB�s DG-ST is responsible for theconcepts and definitions related to the b.o.p.financial and investment income accounts andfor the i.i.p. statistics. Within the b.o.p. financialaccount and the i.i.p., the direct investmentaccount is of special interest to the Commission.For the same reason, Eurostat has a specialinterest in direct investment income.Additional iinformation on the items forwhich the European Commission (Eurostat)is responsible is made available on its website(http://europa.eu.int/en/comm/eurostat/serven/home.htm).

The allocation of data compilation tasks leads,in principle, to the following compilationresponsibility with respect to EU 15 and euroarea aggregates for b.o.p. and i.i.p. statistics:� the European Commission (Eurostat):

EU 15 b.o.p. and direct investment statistics;and

� the ECB (DG-ST): euro area b.o.p./i.i.p.statistics and international reserves.

Following this scheme, euro area monthly keyb.o.p. items are defined and compiled only bythe ECB.

2.3 The ECB�s contribution to theeuro area aggregates

The ECB�s own flows and positions vis-à-visnon-euro area counterparties must also bereflected in the external statistics of the euroarea. In other words, the data resulting from thecompilation of the ECB�s own external statisticshave to be added to the contributions of theeuro area Member States so as to compile the

ECB EU Balance of payments statistical methods � November 2000 11

total figures of the euro area aggregates (seeSection 2.5 �Methods of compiling the euroarea aggregates�).

In practice, the ECB�s �external� activities areconfined to the following items:� reserve assets: reserve assets of the ECB are

those assets vis-à-vis non residents which arepooled in accordance with Article 30 of theStatute of the ESCB and are, thus, consideredto be under the direct and effective control ofthe ECB. As long as no further transfer ofownership takes place, external assetsretained by the NCBs in accordance withArticle 30.4 are under their direct andeffective control and are treated as reserveassets of each individual NCB;

� other investment: this item encompassesthe flows of the ECB to and from theNCBs of Member States not participatingin the euro area that are related to theoperation of the TARGET system;

� portfolio investment: this item encompassesdebt securities (mainly bonds and notes)issued by other euro area residents(�intra-euro area� assets) and thoseissued in euro by non-euro area residents.(The ECB�s claims from debt securities inforeign currency which were issued bynon-euro area residents are includedunder the ECB�s reserve assets.) In thecase of portfolio investment, the �intra-euro area� assets are needed for thecompilation of the total euro areaaggregate figures of portfolio investmentliabilities (see Section 2.5 �Methods ofcompiling the euro area aggregates�).Since the ECB has not itself issued anydebt securities, it does not record anyliabilities in the field of portfolio liabilities;

� income on portfolio investment: income receivedfrom the above-mentioned portfolioinvestment assets which are held by the ECB.As in the case of the financial account, thesedata are needed for the compilation of thetotal euro area aggregate debits of portfolioinvestment income (see Section 2.5 �Methodsof compiling the euro area aggregates�);

� income on other investment: income

received from the management of theECB�s international reserves and fromTARGET operations.

Information on reserve assets is supported bymeans of a �bridging table� which links thestatistical concepts for reserve assets and theheader accounts of the ECB�s balance sheet ona very highly aggregated basis.

2.4 Statistical reporting requirementsfor national compilers

2.4.1 ECB data requirements in balance ofpayments statistics

Data on the b.o.p. for the euro area as a whole arerequired; the ECB does not use or require data oncross-border transactions within the euro area,with the important exception of portfolioinvestment and portfolio investment incomeaccounts (see Section 2.5 �Methods of compilingthe euro area aggregates�). B.o.p. statistics arerequired and published at three differentfrequencies: monthly, quarterly and annually. Thescope and breakdown are different for monthlydata, on the one hand, and for quarterly/annualdata, on the other. While the monthly b.o.p. for theeuro area aims at showing the main items affectingmonetary conditions and exchange markets, thequarterly/annual b.o.p. should permit furtheranalysis of external transactions.

The statistical requirements for the national b.o.p.compilers with respect to the aforementionedfrequencies of submission are outlined below:

2.4.1.1 Monthly requirements

On a monthly basis, the ECB�s b.o.p. datarequirements for the euro area are confined tobroad categories of transactions which areknown as key items and which have to betransmitted by the Member States six weeks(30 working days) after the end of the referencemonth in a highly aggregated form. More detailis required in the financial account, where largeand variable flows affect monetary conditions inthe euro area. The collection of data fromreporting agents is organised by the national

12 ECB EU Balance of payments statistical methods � November 2000

authorities with this deadline in mind. Owing tothis short period, it is permitted, to some extent,to depart from the international guidelines setout in the BPM5 (which was released inOctober 1993). Permitted are, inter alia, therecording of income on a cash basis, instead ofon an accruals basis, and the provision ofestimates. Furthermore, no sectoral breakdownis provided for portfolio investment andfinancial derivatives.

The aim of these monthly key items is toprovide a good picture of developments in themost important and variable items quicklyenough to be of use for the analysis of flowsaffecting the monetary and foreign exchangeconditions of the euro area.

These key items have been required since mid-March 1999 (January 1999 data), showingcredits/debits for the current and capitalaccount and assets/liabilities for the financialaccount, excluding financial derivatives. Datarelating to periods prior to January 1999 areprovided for the years 1997 (partially) and 1998.

Table: Monthly key items for the euroarea balance of payments

I. Current account (credits and debits)GoodsServicesIncome

Compensation of employeesInvestment income

Direct investmentPortfolio investmentOther investment

Current transfers

II. Capital account (credits and debits)

III. Financial accountDirect investment (abroad and in thereporting economy)

Equity capitalReinvested earningsOther capital

Portfolio investment (net assets and net

liabilities)Equity securitiesDebt securities

Bonds and notesMoney market instruments

Financial derivatives (net)Other investment (net assets and netliabilities)

Monetary authoritiesGeneral governmentMFIs (excluding central banks)

Long-termShort-term

Other sectorsReserve assets (only assets)

IV. Errors and omissions

2.4.1.2 Quarterly/annual requirements

The required breakdown of the quarterly/annual b.o.p. statistics adheres, as far aspossible, to the standards set out in the BPM5,which is consistent with the System of NationalAccounts 1993 (SNA 93) and with theEuropean System of Accounts 1995 (ESA 95).Exceptions from the application of BPM5standards mainly relate to:� income on direct investment, for which the

ECB does not require the breakdown ofincome on equity into distributed andundistributed profits (i.e. dividends andreinvested earnings);

� the capital account, for which the ECBcompiles only a lump-sum capital account,without requiring any breakdown;

� the other investment account, which issomewhat simplified by (i) not requiringany distinction between loans and depositson each side of the b.o.p. and (ii) notrequiring any maturity breakdown. Thereis also a change in the presentation of thebreakdown (i.e. sectors as first priority)which is compatible, but not identical,with the BPM5 where instruments havepriority.

The ECB requires quarterly details within threemonths of the end of the quarter to which the

ECB EU Balance of payments statistical methods � November 2000 13

data relate. The detailed quarterly breakdownwas required as of June 1999 (for first quarter1999 data). There is no difference in thebreakdown required for annual data (requestedas from March 2000 for 1999 data). Annualb.o.p. data differs from the quarterly data onlyin that revisions which took place during theyear are incorporated.

Table: Quarterly and annual balance ofpayments for the euro area

I. Current account (credits and debits)GoodsServicesIncome

Compensation of employeesInvestment income

Direct investmentIncome on equityIncome on debt (interest)

Portfolio investmentIncome on equity(dividend)Income on debt (interest)

Bonds and notesMoney market instruments

Other investmentCurrent transfers

II. Capital account (credits and debits)

III. Financial accountDirect investment (abroad and in thereporting economy)

Equity capitalReinvested earningsOther capital

Portfolio investmentEquity securities

Net assetsMonetary authoritiesGeneral governmentMFIs (excluding centralbanks)Other sectors

Net liabilitiesMFIs (excluding central

banks)Other sectors

Debt securities (net assets and netliabilities)

Bonds and notesMonetary authoritiesGeneral governmentMFIs (excluding centralbanks)Other sectors

Money market instrumentsMonetary authoritiesGeneral governmentMFIs (excluding centralbanks)Other sectors

Financial derivatives (net)Monetary authoritiesGeneral governmentMFIs (excluding central banks)Other sectors

Other investment (net assets and netliabilities)

Monetary authoritiesLoans/currency and depositsOther assets

General governmentTrade creditsLoans/currency and depositsOther assets

MFIs (excluding central banks)Loans/currency and depositsOther assets

Other sectorsTrade creditsLoans/currency and depositsOther assets

Reserve assets (assets only)Monetary goldSpecial drawing rightsReserve position in the InternationalMonetary FundForeign exchange

Currency and depositswith monetary authoritieswith MFIs (excludingcentral banks)

SecuritiesEquity

14 ECB EU Balance of payments statistical methods � November 2000

Bonds and notesMoney market instruments

Financial derivativesOther claims

IV. Errors and omissions

2.4.2 ECB data requirements forinternational investment positionstatistics

The compilation of the euro area i.i.p. aims atproviding an annual statement of the externalassets and liabilities of the euro area as a whole,for the purposes of monetary, financial andexchange market analysis, and at assisting in thecompilation of b.o.p. flows. The ECB requiresannual data on the i.i.p. within nine months ofthe end of the year to which the data relate. Therequired breakdown is based (i) on the IMFstandard components of the i.i.p., as presentedin the BPM5; and (ii) on the breakdown for thequarterly/annual b.o.p.

Table: Annual international investmentposition for the euro area

I. Direct investment (abroad and intothe reporting economy)Equity capital and reinvested earningsOther capital

II. Portfolio investmentEquity securities

AssetsMonetary authoritiesGeneral governmentMFIs (excluding central banks)Other sectors

LiabilitiesMFIs (excluding central banks)Other sectors

Debt securities (assets and liabilities)Bonds and notes

Monetary authoritiesGeneral governmentMFIs (excluding central banks)Other sectors

Money market instruments

Monetary authoritiesGeneral governmentMFIs (excluding central banks)Other sectors

III. Financial derivatives (assets andliabilities)Monetary authoritiesGeneral governmentMFIs (excluding central banks)Other sectors

IV. Other investment (assets andliabilities)Monetary authorities

Loans/currency and depositsOther assets

General governmentTrade creditsLoans/currency and depositsOther assets

MFIs (excluding central banks)Loans/currency and depositsOther assets

Other sectorsTrade creditsLoans/currency and depositsOther assets

V. Reserve assets (only assets)Monetary goldSpecial drawing rightsReserve position in the InternationalMonetary FundForeign exchange

Currency and depositswith monetary authoritieswith MFIs (excluding centralbanks)

SecuritiesEquitiesBonds and notesMoney market instruments

Financial derivativesOther claims

ECB EU Balance of payments statistical methods � November 2000 15

2.4.3 ECB data requirements for theEurosystem�s international reservesposition

Since April 1999, the ECB has required andpublished monthly data on the stock ofinternational reserves held by the Eurosystem(the ECB and the 11 participating NCBs). Thedefinition of Eurosystem�s reserve assets, whichwas approved by the ECB Governing Council inMarch 1999, is in conformity with the guidelinesoutlined in the BPM5 (see Section 3.11).Moreover, foreign currency-denominated claims(i.e. claims denominated in any currency otherthan the euro) on euro area residents held bythe Eurosystem are shown as a memorandumitem in the ECB Monthly Bulletin. This approachsupports an analysis for monetary purposes andpermits a reconciliation of the Eurosystem�sinternational reserves and its foreign currencyliquidity position. As from the April 2000release of the ECB Monthly Bulletin, the samebreakdown has been presented for the ECB�sreserves (and related assets) which are pooledin accordance with Article 30 of the Statute ofthe ESCB. In addition to the informationprovided in the ECB Monthly Bulletin, the ECBpublishes Eurosystem and ECB data in line withthe template entitled �International Reservesand Foreign Currency Liquidity�, which was setout in early 2000 in the IMF�s Special DataDissemination Standard (SDDS), on its website.This information covers not only data onreserve assets, but also data on the reserve-related liabilities of the Eurosystem, and differsin some respects from the data on internationalreserves included in the euro area b.o.p.

2.5 Methods of compiling the euroarea aggregates

From 1997 onwards, each broad category oftransaction is broken down into credits anddebits for the current and capital account, andinto assets and liabilities for direct investmentand, from 1998 onwards, also for portfolioinvestment and other investment. The ECBcompiles the figures for the euro area byaggregating the euro area Member States�transactions vis-à-vis non-residents of the euro

area for the current and capital account and forthe financial account, excluding the portfolioinvestment account and the financial derivativesaccount.

The compilation methods for portfolioinvestment and financial derivatives are basedon a different approach, owing to the difficultiesin identifying the residency of the holders ofsecurities issued by domestic residents. Thisdifficulty occurs regarding both portfolioinvestment flows and portfolio investmentincome flows. Therefore, the same approach isused to compile both items.

International standards require portfolioinvestment flows vis-à-vis non-residents of theeuro area to be classified as extra-euro areaflows and allocated according to the residencyof the ultimate investor (in case of liabilities ofthe euro area) and the non-resident debtor (incase of assets of the euro area), respectively.When euro area residents purchase securitiesissued by non-residents of the euro area, therelated flows can be measured directly, with aquarterly sectoral breakdown of the euro arearesidents undertaking the transactions.

However, when non-residents of the euro areapurchase securities issued by euro arearesidents, the correct classification of therelated flows is difficult because thesetransactions are often made through centralsecurities depositories or other intermediarieswhich may be located in the euro area (e.g.Euroclear and Clearstream, formerly Cedel). Atfirst sight, such a purchase appears to be anintra-euro area transaction (as the first knowncounterpart is a euro area resident) to thecountry of the seller, even though it is an extra-euro area flow (as the purchaser/holder of thesecurities is a non-resident of the euro area).Consequently, transactions/holdings related tosecurities issued by residents and traded/heldby non-residents of the euro area would bemisclassified since the national compilers maynot be able to identify the flows/positionscorrectly (i.e. as extra-euro area flows/positions).

16 ECB EU Balance of payments statistical methods � November 2000

In order to correctly compile the total amountof those extra-euro area transactions which arerelating to securities issued by euro arearesidents, the �liabilities� side of portfolioinvestment is calculated as transactions in totalsecurities issued by euro area residents minusthe recorded acquisitions of such securities byresidents of the euro area.

Analogously, euro area residents� income onsecurities issued by non-euro area residents(�extra� credits of the euro area, since thedebtors are non-euro area residents) can becorrectly identified as extra-euro area flows.However, income relating to securities issuedby euro area residents and held by non-residents is often paid to these non-residentsthrough central securities depositories or otherintermediaries and is therefore not identifiablefor the national compiler as extra-euro areaflows. Therefore, the amount of the total euroarea payments to non-euro area residents iscalculated as total payments made by euro arearesidents to recipients outside their homecountry minus the receipts from residents ofother euro area countries.

The net figures for euro area transactions infinancial derivatives are compiled by aggregatingthe national net transactions of the participatingMember States. A sectoral breakdown of thisaccount at the euro area level has not beencompiled so far.

As regards the Eurosystem�s internationalreserves position, the agreed definition ofreserve assets is applied consistently bothacross the Eurosystem and at the national level.Hence, the reserve assets held by theEurosystem are compiled by summing up thereserve asset holdings of the participating NCBsand of the ECB.

In contrast to most b.o.p. items, the euro areai.i.p. is compiled on a net basis (i.e. withoutseparate assets and liabilities), relying onaggregated national data (i.e. including the euroarea Member States� net positions vis-à-visother Member States), on the assumption thatcross-border positions within the euro areacancel out. It is planned that the ECB willrequire data in a form permitting the externalassets and liabilities of the euro area as a wholeto be compiled separately.

3 Concepts, definitions and agreed practices of the euro areabalance of payments and international investment positionstatistics

The main purpose of this chapter is:(i) to provide a comprehensive summary on

the methodological standards (such as theBPM5, the SNA 93 or the ESA 95) withwhich all participating Member States ofthe euro area and also within theEuropean Union in principle comply;

(ii) to serve as a benchmark to identify anyindividual country deviations, as currentlydescribed in the chapter �Country-specificdetails�; and

(iii) to supplement the �methodological notes�which are currently on the ECB Web siteto summarise the compilation standardsin place at present.

Most of these methodological standards havealready been implemented in line with ECBGuideline No. ECB/1998/17 of 1 December1998. Further progress is expected and theNCBs or other competent national authoritieswill, where necessary, steadily improve

ECB EU Balance of payments statistical methods � November 2000 17

in a b.o.p. context may not involve the transferof money, and some are not paid for in anysense. The inclusion of these transactions, inaddition to those matched by actual payments,constitutes a principal difference between ab.o.p. statement and a record of foreign payments.

3.1.2 International investment positionstatistics

Closely related to the flow-oriented b.o.p.framework is the stock-oriented i.i.p. Compiledat a specified date, the i.i.p. is a statisticalstatement of (i) the value and composition ofthe stock of an economy�s financial assets, or theeconomy�s claims on the rest of the world, and(ii) the value and composition of the stock of aneconomy�s liabilities to the rest of the world.Cross-border positions of the euro area comprisethe participating Member States� stocks offinancial claims and financial liabilities vis-à-visresidents of EU Member States not participatingin the euro area or residents of third countries.Also encompassed are land, other real propertyand other immovable assets which are:� physically located outside the economic

territory of the participating Member Statesand owned by residents of participatingMember States (considered as assets, fromthe euro area perspective); or

� physically located inside the economicterritory of the participating MemberStates and owned by residents of non-participating Member States or residentsof third countries (considered as liabilities,from the euro area perspective).

In addition, monetary gold and special drawingrights (SDRs) owned by residents ofparticipating Member States are included.

In some instances, it may be of analytical interestto compute the difference between the twosides of the balance sheet. The calculationwould provide a measure of the net position,and the measure would be equivalent to thatportion of the euro area�s net worth attributableto, or derived from, its relationship with the restof the world. A change in stocks during any

compliance with those recommendations byusing available information or, alternatively, bymaking estimates in consultation with the ECB.

This chapter concerns primarily thosemethodological concepts and definitions whichwere developed under the responsibility of theECB. Definitions on items under the responsibilityof the European Commission (Eurostat) are limited,in this release, to brief and general explanationsonly. The European Commission (Eurostat) mayprovide background material to these sectionsat a later stage.

3.1 General principles of balance ofpayments and internationalinvestment position statistics

3.1.1 Balance of payments statistics

The b.o.p. is a statistical statement that systematicallysummarises, for a specific time period, theeconomic transactions of an economy with therest of the world. A transaction itself is defined asan economic flow that reflects the creation,transformation, exchange, transfer, or extinctionof economic value and involves changes inownership of goods and/or financial assets orliabilities, the provision of services or theprovision of labour and capital. Cross-bordertransactions of the euro area are transactionsbetween residents of participating MemberStates, seen as one economic territory, andresidents of EU Member States not participatingin the euro area or residents of third countries.

Despite its name, which refers to standardsapplicable in the past following recommendationsof the IMF Manuals up to the 4th edition, theb.o.p. is now less concerned with payments, asthat term is generally understood, than withtransactions. This development from a financialtowards an economic approach was felt moreefficient in order (i) to foster a sound economicinterpretation of the figures, and (ii) to makethe b.o.p. concepts compliant with the nationalaccounts (the b.o.p. is also the �rest of theworld� account). Therefore, a number ofinternational transactions which are of interest

18 ECB EU Balance of payments statistical methods � November 2000

defined period can be attributable totransactions (i.e. b.o.p. flows), to revaluationsreflecting changes in exchange rates, prices, etc.or to other adjustments (e. g., reclassifications,corrections, uncompensated seizures).

Since the i.i.p. and the financial account of theb.o.p. share many sources and methods ofcompilation, these two accounts are dealt withtogether in the following sections so as to stresstheir close relationship.

3.1.3 Accounting Principles fortransactions and stocks

3.1.3.1 Double-entry system

The basic convention applied in constructing aeuro area b.o.p. statement is that everyrecorded transaction is represented by twoentries with equal values. One of these entries isdesignated a credit; the other is designated adebit. In principle, the sum of all credit entries isidentical to the sum of all debit entries, and thenet balance of all entries in the statement iszero. In practice, however, the accountsfrequently do not balance. Data for b.o.p.estimates are often derived independently fromdifferent sources and may be incomplete.Moreover, timing and valuation effects alongwith a variety of other factors tend to causeimbalances in the information recorded. As aresult individual b.o.p. accounts tend toaggregate to a summary net credit or net debit.A separate entry, equal to that amount with thesign reversed and labelled �net errors andomissions�, is then included to balance theoverall b.o.p. account.

3.1.3.2 Time of recording the transactions

In line with the BPM5, the ECB principallyrequires recording on a transactions basis(�accruals principle�), meaning that transactionshave to be recorded when economic value iscreated, transformed, exchanged, transferred orextinguished. Claims and liabilities arise whenthere is a change in ownership. The change maybe legal or economic. In practice, when a

change in ownership is not obvious, the changemay be assessed at the time that parties to atransaction record it in their books or accounts.

However, for the reporting of the monthly keyitems, recording on a full accruals ortransactions basis is not mandatory, owing tothe short deadline and the highly aggregatednature of the provision of monthly data. Inagreement with the ECB, the NCBs and othernational compilers may provide data on thecurrent and financial account in the monthlyb.o.p. statistics which is based on full/partialaccruals or on settlements (i.e. cash).

3.1.3.3 Valuation of transactions and stocks

In principle, market prices should be used as thebasis of valuation for both transactions andstocks. Thus, transactions are generally valuedat the actual prices agreed upon by transactors,and stocks of assets and liabilities are valued atthe market prices in effect at the times to whichthe balance sheet relates. Market valuationprovides the most meaningful measure of theeconomic value of the resources available to aneconomy. From a methodological point of view,alternatives to valuation at market price shouldonly be used if absolutely necessary.

In practice, however, some deviations from themarket principle may occur. Book values fromthe reporting agents� balance sheets may, insome cases, be the only readily available sourcefor the valuation of assets and liabilities. In thiscase, owing to the accounting principlesestablished by the appropriate authority and/ordifferent investment policies, those book valuesmay differ from the market value. Moreover,equity and debt securities are not alwaysrecorded on a security-by-security basis.Suitable means (e.g., indices) then have to bechosen by either the data provider or thecompiler to approach the market value. The i.i.p.is valued at current market prices, with theexception of direct investment stocks wherebook values are used to a large extent.

ECB EU Balance of payments statistical methods � November 2000 19

3.1.3.4 Reconciliation of stocks and flows

The reconciliation of changes in stocks andb.o.p. flow data allows sets of data to bevalidated when they are collected independentlyand gives possible explanations for the changesin positions at the beginning and end of a givenperiod owing to different factors. These factorsare:(i) the transactions that have taken place

during the period;(ii) price changes;(iii) exchange rate changes; and(iv) other adjustments reflecting changes

in stocks which are not due to theaforementioned factors.

The greater the level of detail of the basicinformation on both stocks and flows, the moreprecise the reconciliation is. In particular, thefollowing information is necessary:(i) a currency breakdown to capture the

exchange rate effect;(ii) a breakdown of applicable market prices,

especially for portfolio investment instruments,to isolate the market value effect;

(iii) the timing of transactions to select theappropriate price and exchange rate.

Reconciliation is particularly important whenstocks are derived from accumulated flows.

3.1.4 Euro area residency

In general, the terms �resident� and �residing�mean having a centre of economic interest inthe economic territory of a country, asdescribed in Annex A of the Council Regulation(EC) No. 2533/1998. In the case of the euroarea, the economic territory comprises (i) the economic territory of the EU MemberStates participating in Stage Three of Economicand Monetary Union (EMU) and (ii) the ECB,which is regarded as a resident unit of the euroarea.

The rest of the world (RoW) comprises theterritories outside the euro area, i.e. EU MemberStates not participating in EMU, all thirdcountries and non-European supranational and

international organisations, including thosephysically located within the euro area. All EUinstitutions except the ECB are consideredunits that are residents of the rest of the world,i.e. non-euro area residents. Consequently, alltransactions of participating Member States vis-à-vis EU Institutions are recorded and classifiedas non-euro area transactions in the euro areab.o.p./i.i.p. statistics. A list of supranational andinternational institutions is given in Eurostat�sBalance of Payments Vademecum booklet.

The following are examples of borderline casesin the determination of residence:(i) individuals from embassies and military

bases are to be classified as residents oftheir country of origin, thereby ensuringthat a distinction is made between staffemployed from among host countryresidents and those from the country whichthe embassy or military base represents;

(ii) when undertaking cross-bordertransactions in land and/or buildings(e.g. holiday homes), the owner is treatedas if he has transferred his ownership to anotional institutional unit that is actuallyresident in the country where theproperty is located. The notional unit is tobe treated as being owned and controlledby the non-resident owner;

(iii) where an institutional unit operates in anoffshore financial centre, it should betreated as a resident of the territory inwhich the centre is located.

Some territories belonging to, or countriesassociated with, EU Member States might giverise to difficulties in the statistical classification.These can be divided into the following groups:

Territories forming part of the euro area� Islas Canarias, Ceuta and Melilla: Spain;� Monaco, French Overseas Departments

(Guyana, Guadeloupe, Martinique andRéunion), Saint Pierre and Miquelon,Mayotte: France;

� Madeira, the Azores: Portugal;� The Åland Islands: Finland.

20 ECB EU Balance of payments statistical methods � November 2000

Territories associated with euro area MemberStates to be included in the RoW� Buesingen (not Germany);� Andorra (neither Spain nor France);� The Netherlands Antilles and Aruba (not

the Netherlands);� French Overseas Territories (French

Polynesia, New Caledonia and the Wallisand Futuna Islands) (not France);

� San Marino and the Vatican City (not Italy).

Territories associated with EU Member Statesnot participating in the euro area to be includedin the RoW� The Faroes, Greenland (not Denmark);� Guernsey, Jersey, the Isle of Man, Anguilla,

Montserrat, the British Virgin Islands, theTurks and Caicos Islands and the CaymanIslands (not the United Kingdom).

3.1.5 Classification principles for balanceof payments and internationalinvestment position statements

3.1.5.1 Standard components of balance of

payments and international investment

position statements

According to the BPM5, the two majorclassifications of transactions in the b.o.p. statementare the current account and the capitaland financial account. In brief, the currentaccount shows transactions in the realeconomy and relates to goods, services, incomeand current transfers; the capital and financialaccount shows the transactions in the financialeconomy.

The major classifications within the currentaccount are:� Goods;� Services;� Income; and� current transfers.

The capital account records an economy�scapital transfers and its transactions in non-produced, non-financial assets (such as patentsand copyrights). The financial account records

an economy�s transactions in external financialassets and liabilities.

The financial account of the euro area b.o.p.and the euro area i.i.p. are structured aroundfive accounts, differentiated by the type offinancial assets/liabilities involved in thetransaction:� direct investment;� portfolio investment;� financial derivatives;� other investment; and� reserve assets.

In addition, transactions within the euro areaportfolio investment, financial derivativesand other investment accounts are classifiedby sector, according to the institutional sectorto which the euro area resident undertakingthe transaction belongs (see Section 3.1.6Sectorisation). This sectoral analysis also appliesto the corresponding stock data requested forthe i.i.p.

3.1.5.2 Classification of financial flows by

credits/change in assets and debits/

change in liabilities

Economic transactions of the euro area b.o.p.are recorded (i) as credits or debits in the caseof all items of the current and capital accounts,and (ii) as changes in assets or liabilities in thecase of all items of the financial account. Creditsand debits are shown as gross figures, i.e.inflows from non-euro area residents willincrease the amount of credits, while outflowsto non-euro area residents mean an increase ofdebits. By contrast, changes in assets andliabilities are shown as net figures: increases(decreases) in assets indicate that a net outflow(inflow) has occurred, since the payments byeuro area residents in respect of theiracquisitions of assets issued by euro area non-residents are larger (smaller) than the receiptsderived from their sale or redemption. Increases(decreases) in liabilities indicate a net inflow(outflow), since the receipts from non-euro arearesidents in respect of their acquisitions ofassets issued by euro area residents are larger

ECB EU Balance of payments statistical methods � November 2000 21

(smaller) than the payments generated by theirsale or redemption.

3.1.5.3 Geographical allocation principle for

change of ownership in the case of

financial transactions and positions

For financial transactions/positions, there aretwo possible means of classification consideredto be in accord with the change-of-ownershipprinciple, the debtor/creditor principle and thetransactor principle. In order to achieve a moreprecise geographical allocation, the ECBrequires, in principle, the application of thedebtor/creditor principle, according to whichtransactions/positions in a country�s externalliabilities are classified by the country of theowner of the claim (the creditor) andtransactions/positions in a country�s financialassets are classified by the country that incursthe liability (the debtor). The transactor principle,on the other hand, means that transactions/positions are classified by the country of thenon-resident counterparty to the transaction.The latter principle can, in practice, be appliedin two different ways, i.e. classification either bycountry of first-known counterpart or bycountry of settlement, both of which may not inall cases reflect the residency of the actualowner of the asset/liability acquired/incurred.

3.1.6 Sectorisation

3.1.6.1 Institutional sectors

Four sectors are identified separately for euroarea b.o.p./i.i.p. statistics:(i) monetary authorities;(ii) general government;(iii) Monetary Financial Institutions (MFIs);(iv) other sectors.

Monetary authoritiesThe �monetary authorities� sector of the euroarea b.o.p./i.i.p. and international reservestatistics consists of the Eurosystem, i.e., theECB and the NCBs from participating MemberStates.

General governmentThe �general government� sector is consistentwith the sector of the same name in the ESA 95and consists of the following units:� central government: all administrative

departments, agencies, foundations,institutes and similar state bodies, thecompetence of which covers the entireeconomic territory of one country (withthe exception of the administration ofsocial security funds � see below);

� state/regional government: institutionalunits exercising some of the functions ofgovernment at a level below that ofcentral government and above that oflocal government (with the exception ofthe administration of social security funds� see below);

� local government: those types ofadministrative departments, agencies, etc.of Member States, the competence ofwhich covers only a restricted part of theeconomic territory of a country(excluding the local agencies for socialsecurity funds � see below); and

� social security funds: schemes managed bya central, state/regional or localgovernment, the principal objective ofwhich is to provide social benefits to thepopulation of the country. Certainpopulation groups are obliged to paycontributions to these schemes.

Public non-financial corporations and quasi-corporations which are market producersprincipally engaged in the production of goodsand non-financial services should be classifiedas �other sectors�. This also applies to publicproducers involved in the aforementionedactivities and recognised as independent legalentities by virtue of special legislation. Publicsector credit institutions should be included inthe �MFI sector� according to both the MFIdefinition and the ESA 95 definition, and notunder �general government�. Therefore, the fullconsistency of that sector with the SNA 93definition should be noted.

22 ECB EU Balance of payments statistical methods � November 2000

MFI sectorApart from the aforementioned institutionsincluded in the �monetary authorities� sector,the �MFI sector� identified in the euro areab.o.p./i.i.p. presentation coincides with the MFIsector for money and banking statistics. Hence,it comprises (i) euro area resident creditinstitutions, as defined in Community Law, i.e.institutions whose business is to receivedeposits or other repayable funds from thepublic (including the proceeds arising from thesales of bank bonds to the public) and to grantcredit for its own account, and (ii) all otherresident financial institutions located in the euroarea whose business is both to receive depositsand/or close substitutes for deposits fromentities other than MFIs, and, on their ownaccount (at least in economic terms), to grantcredits and/or to make investments in securities(e. g. money market funds). MFIs located in EUMember States that do not participate in theeuro area and banks outside the EU comprise:(i) MFIs located in EU Member States not

participating in the euro area, includingthose subsidiaries and branches, theparent institution of which is an MFIlocated in the euro area;

(ii) banks located outside the EU area,including those subsidiaries and branches,the parent institution of which is an MFIlocated in the euro area.

Subsidiaries are separate institutional units, withindependent legal status, either wholly ownedor with majority ownership held by anotherentity (the parent institution). Branches areentities without independent legal status (theyare wholly owned by the parent). However,when branches are located in another countrythan that in which the company controllingthem is located, they are deemed to be separateinstitutional units.

Other sectorsThe �other sectors� category is composed of:(a) other financial institutions not covered by

the MFI definition: this sector shouldinclude the following institutions:(i) collective investment institutions

(CIIs) not considered as moneymarket funds (MMFs) and, therefore,not included in the MFIs List;

(ii) real estate investment institutions;(iii) securities-dealer companies and

agencies;(iv) mortgage credit securitisation funds;(v) insurance companies;(vi) pension funds; and(vii) financial auxiliaries;

(b) non-financial institutions:(i) non-financial enterprises (public and

private);(ii) non-profit-making institutions serving

households; and(iii) households.

For analytical purposes and with regard to thepossible use of the euro area i.i.p. for thecompilation of other euro area statistics, such asthe euro area financial accounts, informationabout the different sub-sectors is useful.However, in general, it is difficult for MemberStates to split �other sectors� into households,non-financial enterprises and other (non-MFI)financial institutions.

In the field of reserve assets, claims on the Bankfor International Settlements (BIS) and theInternational Monetary Fund (IMF) have to beclassified as claims on other monetaryauthorities.

3.1.6.2 Sectorisation criteria for flows and

stocks

In principle, the sector attribution rules forfinancial flows and stocks seem to be easy toapply. Transactions and holdings in externalfinancial assets have to be assigned to theinstitutional sector to which the residentcurrent creditor (owner of the asset) belongs.Transactions in and holdings of externalfinancial liabilities have to be included in theinstitutional sector to which the resident issuerof the liability belongs.

Securities issued by euro area residents andowned by non-euro area residents are euro

ECB EU Balance of payments statistical methods � November 2000 23

area liabilities; those issued by non-euro arearesidents and owned by euro area residents areeuro area assets. Sectorisation should becarried out according to the above-mentionedprinciples.

With regard to other investment flows andstocks, it should be added that:(i) government-guaranteed and/or bank-insured

trade credits should be treated as privateoperations rather than as government orbank lending and should, therefore, beincluded under �other sectors�. Thereason for this is that in these cases thedebtors have incurred liabilities, but havenot as yet failed to discharge them;accordingly, liability for such loans wouldnot be transferred to the government orbank that guaranteed them until the loanrecipient defaulted in payment. Indeed,guarantees and financial intermediation inwhich the intermediary is not in fact thelegal creditor or debtor should not betaken into account. In addition, in someMember States it is not always clearwhether these loans are insured by thegovernment or by a public insurancecompany;

(ii) loans and deposits connected to repo-typeagreements have to be classified under theinstitutional sector to which the residentthat extends or receives the financingbelongs, regardless of the nature of theissuer of the securities acting as collateral.The residency of the borrower and lenderis the criterion that will attribute thecharacter of asset or liability to theoperations, not the residency of the issuerof the collateral.

3.1.6.3 Practical sectorisation problems

The following practical problems related tosectorisation issues could cause difficultiesregarding the compilation of a meaningful euroarea b.o.p. and i.i.p.

Transactions between resident sectorsOn the assets side � i.e. securities issued by

non-euro area residents and acquired by euroarea residents � flows are assigned to theinstitutional sector to which the residentsubscriber or buyer of the securities belongs. Asa result, the securities issued by non-residents,which are initially subscribed by creditinstitutions and subsequently sold to otherresidents, appear, at first place, in the �MFIsector� of the b.o.p. representing an increasein cross-border assets. If the subsequent salesby the resident MFI sector to the residentnon-banks are not recorded in the b.o.p., thesetransactions between euro area residentswould cause a discrepancy in the reconciliationexercise between b.o.p. and i.i.p. data. Thiswould be the case, in particular, if theoutstanding stocks are directly covered bypure stock data collection sources. As arecommendation, the compiler could derivethese transactions from balance sheet statisticswhere MFIs� sales of foreign securities to non-MFIs may be reflected. These types oftransactions between euro area residents couldbe particularly frequent and sizeable in the caseof non-euro area resident issues on domesticmarkets and debt securities denominated in thedomestic currency (bulldog bonds, Samuraibonds, etc.).

Assignment of an institution in a different residentsectorInstitutions subject to changes in their legalstatus (institutional changes) or changes inthe definition of the requirements to beconsidered for their inclusion in the differentsectors (functional changes) may require specialtreatment in order to avoid discrepancies inthe reconciliation exercise. A reasonablerecommendation is to proceed as follows:(i) in the flows statistics, transactions involving

an institution whose sector has changedshould be allocated to the appropriatenew sector from the date of the change;

(ii) in the stocks statistics, the reclassificationof the stocks attributed to the institutionin question should be made from theformer sector to the new sector by meansof an entry in the �other adjustments�column of the reconciliation statement.

24 ECB EU Balance of payments statistical methods � November 2000

Although the MFI definition could imply theinclusion in the �MFI sector� of certain CIIs thatwould normally have been included under�other sectors�, the reclassification of sectors isnot very common and should, therefore, notcause any particular difficulties with regard tothe compilation of the euro area i.i.p.

3.2 Goods

The goods item of the euro area b.o.p. statisticscovers general merchandise, goods forprocessing, repairs on goods, goods procuredin ports by carriers and non-monetary gold. Inaccordance with general b.o.p. principles,change of ownership is the principledetermining the coverage and time of recordingof international transactions in goods.

Exports and imports of goods are recordedon a f.o.b./f.o.b. basis, i.e. at market value atthe customs frontiers of exporting economies,including charges for insurance and transportservices up to the frontier of the exportingcountry. Moreover, in line with the guidelinesset out in the BPM5, the geographical allocationfor exports should be based on the country offinal destination and that of imports shouldbe based on the country of origin. However,there is some departure from these principlesas regards in transactions goods from or tonon-euro area countries which are channelledthrough one or more other euro areaMember States. In order to avoid double-counting or omissions in the euro area b.o.p.statistics, transactions in exports and importsare recorded as extra-euro area transactionsonly by the euro area Member State in whichthe goods cross the border of the euro area.By contrast, the euro area Member Statefrom which the goods were originally sentor from which the goods are finallyreceived apply the "country-of-consignment"principle and record this transaction asintra-euro area trade in goods going to orcoming from another euro area MemberState.

Incidentally, it should be mentioned that the"consignment principle" applies to tradebetween all EU Member States. However, thefocus of this Chapter is on the euro area andthe agreed treatment of these transactions inthe euro area b.o.p.

3.3 Services

The services account of the euro area b.o.p.statistics consists of the following items, whichare to be recorded according to their actual delivery:� Transportation covers all transportation

services (sea, air, and other - includingland, inland waterway, rail, space andpipeline) that are performed by euro arearesidents for non-euro area residents, orvice versa, and that involve the carriage ofpassengers, the movement of goods(freight), rentals (charters) of carriers withcrew and related supporting and auxiliaryservices. Excluded are passenger servicesprovided to non-euro area residents byeuro area carriers within the euro areaeconomies, or vice versa (these areincluded under travel).

� Travel includes primarily the goods andservices which euro area travellersacquire from non-euro area residents orwhich euro area residents provide tonon-euro area travellers during visits ofless than one year, net of any purchasesmade with money earned or providedlocally. Unlike other services, travel isnot a specific type of service, butan assortment of goods and servicesconsumed by travellers. Personal transport(only international transportation) inconnection with travel is not included inthis item but under transportation.

� Other services comprise those servicetransactions with non-euro area residentswhich are not covered under transportationand travel, such as communication services,construction services, insurance orfinancial services.

ECB EU Balance of payments statistical methods � November 2000 25

3.4 Income

3.4.1 Definition and coverage of income

Income covers two types of transactionsbetween residents and non-residents:(i) those involving compensation of employees,

which is paid to non-resident workers orreceived from non-resident employersand

(ii) those involving investment income receiptsand payments on external financial assets1

and liabilities. Income derived from theuse of tangible produced assets isexcluded from income and classified asappropriate under leasing or rentals,under other business services or undertransportation. Income from tangible non-produced assets is, however, classified asincome under "other investment income".

3.4.2 Definition of compensation ofemployees

Compensation of employees comprises wages,salaries, and other benefits (in cash or in kind)earned by individuals in economies other thanthe euro area in which they are resident, forwork performed for and paid by residents ofthose economies (and conversely). Included arethe contributions paid by employers, on behalfof employees, to social security schemes or toprivate insurance or pension funds to securebenefits for employees.

3.4.3 Definition of investment income