evolution of fixed income investments: the path to a … files/gk_yanni...proprietary information...

TRANSCRIPT

Proprietary information – not for distribution beyond intended recipient.

Evolution of Fixed Income Investments:The Path to a New World Approach

Bill NemereverPartner

GMO LLC

CFA Society of PittsburghApril 21, 2011

Proprietary information – not for distribution to the public. Copyright © 2011 by GMO LLC. All rights reserved. GMOGK_Yanni Partners_4-11 2

State of Play

• A brief history of fixed income investing-- Expanding investment options-- Advances in technology-- Evolution of portfolio management

Proprietary information – not for distribution to the public. Copyright © 2011 by GMO LLC. All rights reserved. GMOGK_Yanni Partners_4-11 3

State of Play

• A brief history of fixed income investing-- Expanding investment options-- Advances in technology-- Evolution of portfolio management

• Problems with popular investment mandates

Proprietary information – not for distribution to the public. Copyright © 2011 by GMO LLC. All rights reserved. GMOGK_Yanni Partners_4-11 4

State of Play

• A brief history of fixed income investing-- Expanding investment options-- Advances in technology-- Evolution of portfolio management

• Problems with popular investment mandates• “New World Bond Management”

Proprietary information – not for distribution to the public. Copyright © 2011 by GMO LLC. All rights reserved. GMOGK_Yanni Partners_4-11 5

Expanding Investment Options

1960s

Proprietary information – not for distribution to the public. Copyright © 2011 by GMO LLC. All rights reserved. GMOGK_Yanni Partners_4-11 6

Expanding Investment Options

1960s 1970s

Proprietary information – not for distribution to the public. Copyright © 2011 by GMO LLC. All rights reserved. GMOGK_Yanni Partners_4-11 7

Expanding Investment Options

1960s 1970s 1980s

Proprietary information – not for distribution to the public. Copyright © 2011 by GMO LLC. All rights reserved. GMOGK_Yanni Partners_4-11 8

Expanding Investment Options

1990s

Proprietary information – not for distribution to the public. Copyright © 2011 by GMO LLC. All rights reserved. GMOGK_Yanni Partners_4-11 9

Expanding Investment Options

1990s 2000s

Proprietary information – not for distribution to the public. Copyright © 2011 by GMO LLC. All rights reserved. GMOGK_Yanni Partners_4-11 10

Advances in Technology

1960s

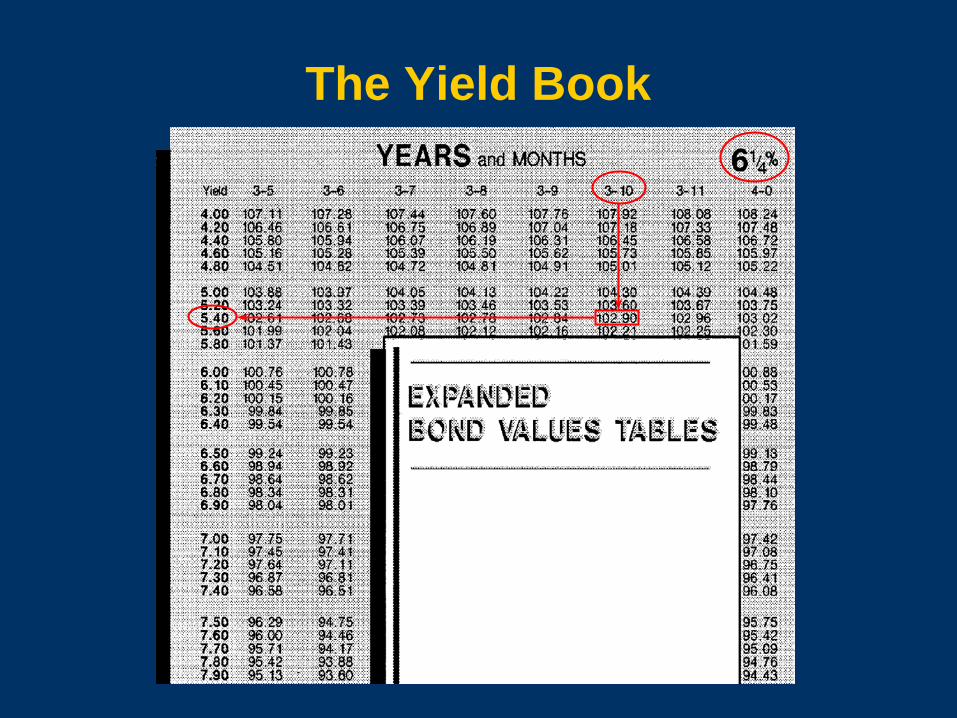

The Yield Book

The Yield Book

Proprietary information – not for distribution to the public. Copyright © 2011 by GMO LLC. All rights reserved. GMOGK_Yanni Partners_4-11 13

Advances in Technology

1960s 1970s

Proprietary information – not for distribution to the public. Copyright © 2011 by GMO LLC. All rights reserved. GMOGK_Yanni Partners_4-11 14

Advances in Technology

1960s 1970s

Proprietary information – not for distribution to the public. Copyright © 2011 by GMO LLC. All rights reserved. GMOGK_Yanni Partners_4-11 15

Advances in Technology

1960s 1970s

Proprietary information – not for distribution to the public. Copyright © 2011 by GMO LLC. All rights reserved. GMOGK_Yanni Partners_4-11 16

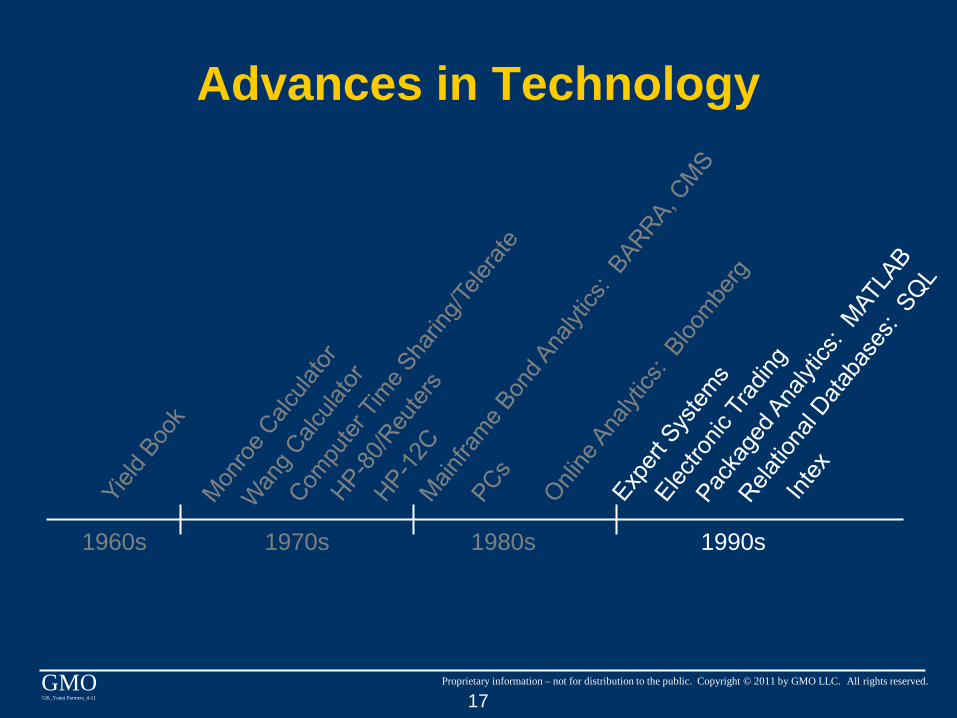

Advances in Technology

1960s 1970s 1980s

Proprietary information – not for distribution to the public. Copyright © 2011 by GMO LLC. All rights reserved. GMOGK_Yanni Partners_4-11 17

Advances in Technology

1960s 1970s 1980s 1990s

Proprietary information – not for distribution to the public. Copyright © 2011 by GMO LLC. All rights reserved. GMOGK_Yanni Partners_4-11 18

Advances in Technology

2000s 2010s

Proprietary information – not for distribution to the public. Copyright © 2011 by GMO LLC. All rights reserved. GMOGK_Yanni Partners_4-11 19

Evolution of Portfolio Management

1950s

Proprietary information – not for distribution to the public. Copyright © 2011 by GMO LLC. All rights reserved. GMOGK_Yanni Partners_4-11 20

Evolution of Portfolio Management

1950s 1960s

Proprietary information – not for distribution to the public. Copyright © 2011 by GMO LLC. All rights reserved. GMOGK_Yanni Partners_4-11 21

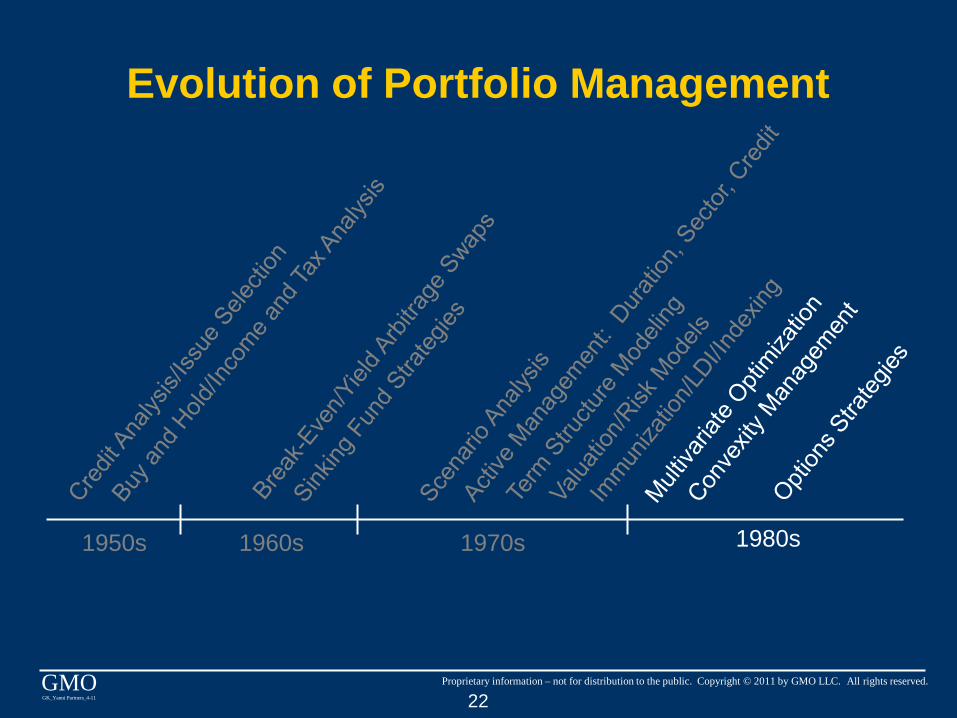

Evolution of Portfolio Management

1950s 1960s 1970s

Proprietary information – not for distribution to the public. Copyright © 2011 by GMO LLC. All rights reserved. GMOGK_Yanni Partners_4-11 22

Evolution of Portfolio Management

1950s 1960s 1970s 1980s

Proprietary information – not for distribution to the public. Copyright © 2011 by GMO LLC. All rights reserved. GMOGK_Yanni Partners_4-11 23

Evolution of Portfolio Management

1990s 2000s

Proprietary information – not for distribution to the public. Copyright © 2011 by GMO LLC. All rights reserved. GMOGK_Yanni Partners_4-11 24

Typical Benchmark-Oriented Bond Management is Bad

• Index composition drifts over time; the past is not representative

Proprietary information – not for distribution to the public. Copyright © 2011 by GMO LLC. All rights reserved. GMOGK_Yanni Partners_4-11 25

Typical Benchmark-Oriented Bond Management is Bad

• Index composition drifts over time; the past is not representative

• Popular benchmarks represent a fraction of the fixed income market

Proprietary information – not for distribution to the public. Copyright © 2011 by GMO LLC. All rights reserved. GMOGK_Yanni Partners_4-11 26

Typical Benchmark-Oriented Bond Management is Bad

• Index composition drifts over time; the past is not representative

• Popular benchmarks represent a fraction of the fixed income market

• Most indexes have little relation to investor objectives

Proprietary information – not for distribution to the public. Copyright © 2011 by GMO LLC. All rights reserved. GMOGK_Yanni Partners_4-11 27

Why own Bonds?

• Diversify equity exposure

Proprietary information – not for distribution to the public. Copyright © 2011 by GMO LLC. All rights reserved. GMOGK_Yanni Partners_4-11 28

Why own Bonds?

• Diversify equity exposure• Hedge liabilities

Proprietary information – not for distribution to the public. Copyright © 2011 by GMO LLC. All rights reserved. GMOGK_Yanni Partners_4-11 29

Why own Bonds?

• Diversify equity exposure• Hedge liabilities• Hedge deflation/inflation

Proprietary information – not for distribution to the public. Copyright © 2011 by GMO LLC. All rights reserved. GMOGK_Yanni Partners_4-11 30

Why own Bonds?

• Diversify equity exposure• Hedge liabilities• Hedge deflation/inflation• Gain foreign bond and currency exposure

Proprietary information – not for distribution to the public. Copyright © 2011 by GMO LLC. All rights reserved. GMOGK_Yanni Partners_4-11 31

Why own Bonds?

• Diversify equity exposure• Hedge liabilities• Hedge deflation/inflation• Gain foreign bond and currency exposure• Provide a source of liquidity

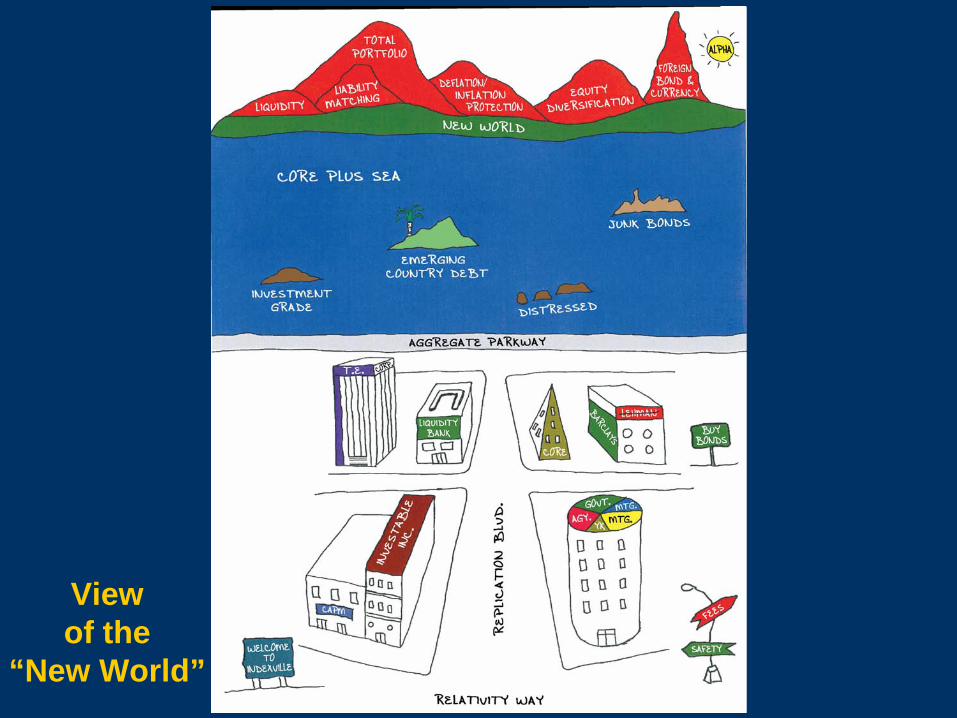

Viewof the

“New World”

Proprietary information – not for distribution to the public. Copyright © 2011 by GMO LLC. All rights reserved. GMOGK_Yanni Partners_4-11 33

What’s the Right Beta?

Proprietary information – not for distribution to the public. Copyright © 2011 by GMO LLC. All rights reserved. GMOGK_Yanni Partners_4-11 34

What’s the Right Beta?

• Interest rate risk is the most important

Proprietary information – not for distribution to the public. Copyright © 2011 by GMO LLC. All rights reserved. GMOGK_Yanni Partners_4-11 35

What’s the Right Beta?

• Interest rate risk is the most important• Beta through derivatives requires little cash

Proprietary information – not for distribution to the public. Copyright © 2011 by GMO LLC. All rights reserved. GMOGK_Yanni Partners_4-11 36

What’s the Right Beta?

• Interest rate risk is the most important• Beta through derivatives requires little cash• Local government term structures explain

most bond price moves

Proprietary information – not for distribution to the public. Copyright © 2011 by GMO LLC. All rights reserved. GMOGK_Yanni Partners_4-11 37

What’s the Right Beta?

• Interest rate risk is the most important• Beta through derivatives requires little cash• Local government term structures explain

most bond price moves• Secondary exposures like credit or sector

are best addressed when thinking about alpha

Proprietary information – not for distribution to the public. Copyright © 2011 by GMO LLC. All rights reserved. GMOGK_Yanni Partners_4-11 38

Equity Market Diversification

• Is it reasonable to expect bonds to offset stock market declines?

Proprietary information – not for distribution to the public. Copyright © 2011 by GMO LLC. All rights reserved. GMOGK_Yanni Partners_4-11 39

Equity Market Diversification

• Is it reasonable to expect bonds to offset stock market declines?

• What is the proper hedge ratio?

Proprietary information – not for distribution to the public. Copyright © 2011 by GMO LLC. All rights reserved. GMOGK_Yanni Partners_4-11 40

Worst Case Examples

Total ReturnS&P 500

Quarterly 1980-2010

-25%

-20%

-15%

-10%

-5%

0%

5%

4Q87

4Q08

3Q02

3Q01

3Q90

2Q02

1Q01

2Q10

1Q09

3Q81

3Q98

1Q08

3Q08

4Q00

1Q82

3Q96

3Q99

1Q80

3Q85

1Q94

4Q07

1Q03

1Q90

2Q08

2Q00

2Q84

1Q92

1Q84

2Q81

1Q05

3Q04

2Q82

2Q06

3Q00

2Q91

3Q83

Source: GMO, Barclays

Proprietary information – not for distribution to the public. Copyright © 2011 by GMO LLC. All rights reserved. GMOGK_Yanni Partners_4-11 41

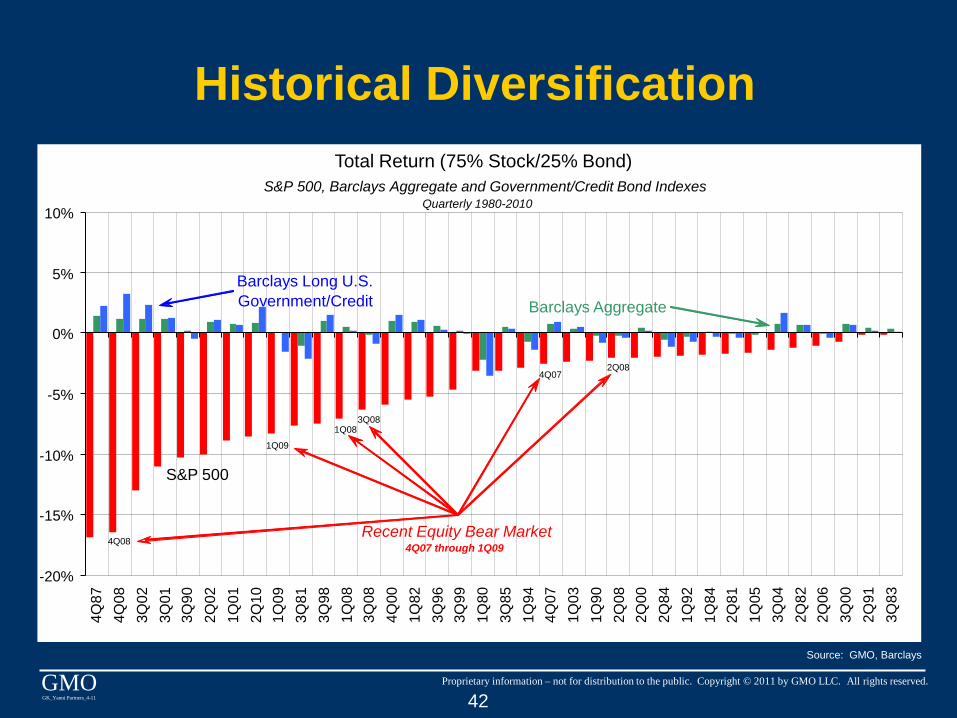

Historical Diversification Total Return (75% Stock/25% Bond)

S&P 500, Barclays Aggregate and Government/Credit Bond IndexesQuarterly 1980-2010

Proprietary information – not for distribution to the public. Copyright © 2011 by GMO LLC. All rights reserved. GMOGK_Yanni Partners_4-11 42

Historical Diversification

Source: GMO, Barclays

Total Return (75% Stock/25% Bond)S&P 500, Barclays Aggregate and Government/Credit Bond Indexes

Quarterly 1980-2010

-20%

-15%

-10%

-5%

0%

5%

10%

4Q87

4Q08

3Q02

3Q01

3Q90

2Q02

1Q01

2Q10

1Q09

3Q81

3Q98

1Q08

3Q08

4Q00

1Q82

3Q96

3Q99

1Q80

3Q85

1Q94

4Q07

1Q03

1Q90

2Q08

2Q00

2Q84

1Q92

1Q84

2Q81

1Q05

3Q04

2Q82

2Q06

3Q00

2Q91

3Q83

S&P 500

Barclays Long U.S. Government/Credit Barclays Aggregate

Recent Equity Bear Market 4Q07 through 1Q094Q08

2Q08

1Q09

3Q08

4Q07

1Q08

Proprietary information – not for distribution to the public. Copyright © 2011 by GMO LLC. All rights reserved. GMOGK_Yanni Partners_4-11 43

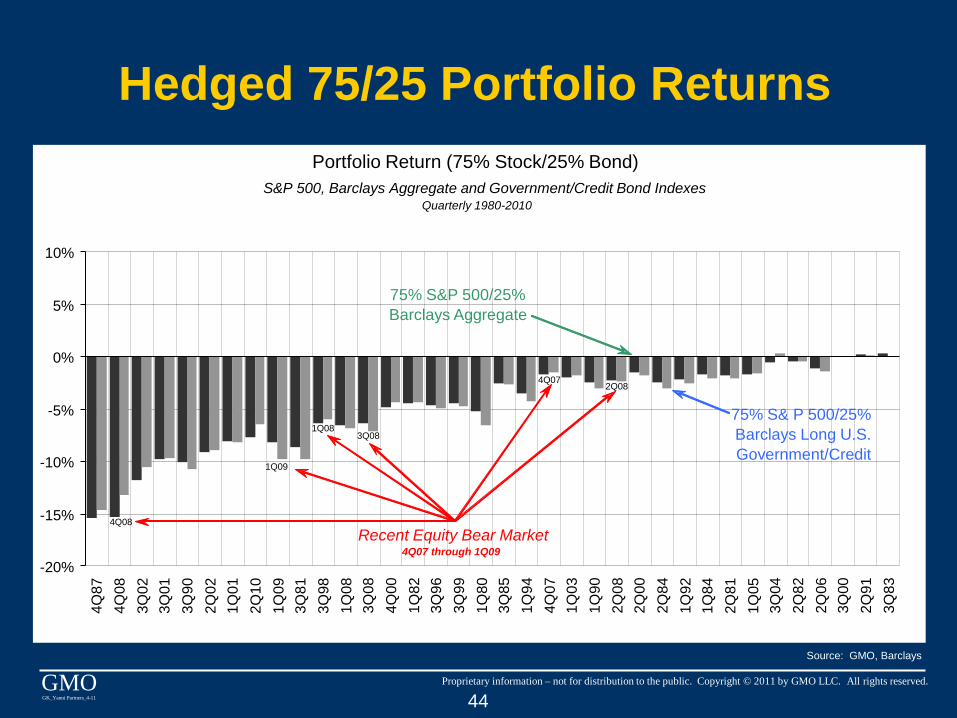

Hedged 75/25 Portfolio ReturnsPortfolio Return (75% Stock/25% Bond)

S&P 500, Barclays Aggregate and Government/Credit Bond IndexesQuarterly 1980-2010

Proprietary information – not for distribution to the public. Copyright © 2011 by GMO LLC. All rights reserved. GMOGK_Yanni Partners_4-11 44

Hedged 75/25 Portfolio Returns

Source: GMO, Barclays

Portfolio Return (75% Stock/25% Bond)S&P 500, Barclays Aggregate and Government/Credit Bond Indexes

Quarterly 1980-2010

-20%

-15%

-10%

-5%

0%

5%

10%

4Q87

4Q08

3Q02

3Q01

3Q90

2Q02

1Q01

2Q10

1Q09

3Q81

3Q98

1Q08

3Q08

4Q00

1Q82

3Q96

3Q99

1Q80

3Q85

1Q94

4Q07

1Q03

1Q90

2Q08

2Q00

2Q84

1Q92

1Q84

2Q81

1Q05

3Q04

2Q82

2Q06

3Q00

2Q91

3Q83

75% S& P 500/25% Barclays Long U.S. Government/Credit

75% S&P 500/25% Barclays Aggregate

Recent Equity Bear Market 4Q07 through 1Q09

4Q08

2Q08

1Q09

3Q08

4Q07

1Q08

Proprietary information – not for distribution to the public. Copyright © 2011 by GMO LLC. All rights reserved. GMOGK_Yanni Partners_4-11 45

Hedged 25/75 Portfolio ReturnsPortfolio Return (25% Stock/75% Bond)

S&P 500, Barclays Aggregate and Government/Credit Bond IndexesQuarterly 1980-2010

Proprietary information – not for distribution to the public. Copyright © 2011 by GMO LLC. All rights reserved. GMOGK_Yanni Partners_4-11 46

Hedged 25/75 Portfolio Returns

Source: GMO, Barclays

Portfolio Return (25% Stock/75% Bond)S&P 500, Barclays Aggregate and Government/Credit Bond Indexes

Quarterly 1980-2010

-20%

-15%

-10%

-5%

0%

5%

10%

4Q87

4Q08

3Q02

3Q01

3Q90

2Q02

1Q01

2Q10

1Q09

3Q81

3Q98

1Q08

3Q08

4Q00

1Q82

3Q96

3Q99

1Q80

3Q85

1Q94

4Q07

1Q03

1Q90

2Q08

2Q00

2Q84

1Q92

1Q84

2Q81

1Q05

3Q04

2Q82

2Q06

3Q00

2Q91

3Q83

25% S& P 500/75% Barclays Long U.S. Government/Credit

25% S&P 500/75% Barclays Aggregate

Recent Equity Bear Market 4Q07 through 1Q09

4Q08 2Q08

1Q09

3Q08

4Q07

1Q08

Proprietary information – not for distribution to the public. Copyright © 2011 by GMO LLC. All rights reserved. GMOGK_Yanni Partners_4-11 47

Hedging Specific Liabilities

• A more-tractable problem

Proprietary information – not for distribution to the public. Copyright © 2011 by GMO LLC. All rights reserved. GMOGK_Yanni Partners_4-11 48

Hedging Specific Liabilities

• A more-tractable problem• Regulatory changes are increasing the

focus on liability-driven investing

Proprietary information – not for distribution to the public. Copyright © 2011 by GMO LLC. All rights reserved. GMOGK_Yanni Partners_4-11 49

Hedging Specific Liabilities

• A more-tractable problem• Regulatory changes are increasing the

focus on liability-driven investing• It’s key to determine how much hedging

is desired and what form it should take

Proprietary information – not for distribution to the public. Copyright © 2011 by GMO LLC. All rights reserved. GMOGK_Yanni Partners_4-11 50

Hedging Specific Liabilities

• A more-tractable problem• Regulatory changes are increasing the

focus on liability-driven investing• It’s key to determine how much hedging

is desired and what form it should take• Actuaries can provide a schedule of

risk-free interest rate exposures to serve as a pension benchmark

Proprietary information – not for distribution to the public. Copyright © 2011 by GMO LLC. All rights reserved. GMOGK_Yanni Partners_4-11 51

Sample Liability Benchmark

Maturity (Years) Weight

1 -1.8%2 -0.1%5 4.1%

10 12.1%20 21.5%30 41.3%40 18.0%50 4.9%

100.0%

Liability Value €245 million

Proprietary information – not for distribution to the public. Copyright © 2011 by GMO LLC. All rights reserved. GMOGK_Yanni Partners_4-11 52

Deflation/Inflation Protection

• What degree of protection is desired?

Proprietary information – not for distribution to the public. Copyright © 2011 by GMO LLC. All rights reserved. GMOGK_Yanni Partners_4-11 53

Deflation/Inflation Protection

• What degree of protection is desired?• Scenario analysis is helpful in

quantifying hedge ratios

Proprietary information – not for distribution to the public. Copyright © 2011 by GMO LLC. All rights reserved. GMOGK_Yanni Partners_4-11 54

Deflation/Inflation Protection

• What degree of protection is desired?• Scenario analysis is helpful in

quantifying hedge ratios• If inflation falls (or rises) by X% what

response is expected from bond portfolio?

Proprietary information – not for distribution to the public. Copyright © 2011 by GMO LLC. All rights reserved. GMOGK_Yanni Partners_4-11 55

Foreign Bond & Currency Diversification

• Foreign bonds: efficient way to gain non-domestic interest rate and currency exposure

Proprietary information – not for distribution to the public. Copyright © 2011 by GMO LLC. All rights reserved. GMOGK_Yanni Partners_4-11 56

Foreign Bond & Currency Diversification

• Foreign bonds: efficient way to gain non-domestic interest rate and currency exposure

• Additionally can provide exposure to offshore credit risks

Proprietary information – not for distribution to the public. Copyright © 2011 by GMO LLC. All rights reserved. GMOGK_Yanni Partners_4-11 57

Foreign Bond & Currency Diversification

• Foreign bonds: efficient way to gain non-domestic interest rate and currency exposure

• Additionally can provide exposure to offshore credit risks

• Excellent for hedging liabilities tied to foreign risk factors

Proprietary information – not for distribution to the public. Copyright © 2011 by GMO LLC. All rights reserved. GMOGK_Yanni Partners_4-11 58

Establishing a Beta Benchmark

• Must convert investment objectives into an investable bond benchmark

Proprietary information – not for distribution to the public. Copyright © 2011 by GMO LLC. All rights reserved. GMOGK_Yanni Partners_4-11 59

Establishing a Beta Benchmark

• Must convert investment objectives into an investable bond benchmark

• Assumptions about correlations between risks to be hedged and benchmark are required

Proprietary information – not for distribution to the public. Copyright © 2011 by GMO LLC. All rights reserved. GMOGK_Yanni Partners_4-11 60

Establishing a Beta Benchmark

• Must convert investment objectives into an investable bond benchmark

• Assumptions about correlations between risks to be hedged and benchmark are required

• Liability benchmarks are easy, equity hedging using bond benchmarks, more challenging

Proprietary information – not for distribution to the public. Copyright © 2011 by GMO LLC. All rights reserved. GMOGK_Yanni Partners_4-11 61

Equity Hedging Example

• A scenario approach is a useful way to frame the problem

Proprietary information – not for distribution to the public. Copyright © 2011 by GMO LLC. All rights reserved. GMOGK_Yanni Partners_4-11 62

Equity Hedging Example

• A scenario approach is a useful way to frame the problem

• An example:-- Expect to offset a third of S&P 500

losses in a quarter

Proprietary information – not for distribution to the public. Copyright © 2011 by GMO LLC. All rights reserved. GMOGK_Yanni Partners_4-11 63

Equity Hedging Example

• A scenario approach is a useful way to frame the problem

• An example:-- Expect to offset a third of S&P 500

losses in a quarter-- Assume when stocks decline,

Barclays Long G/C Index rises by an amount equal to half the equity market loss

Proprietary information – not for distribution to the public. Copyright © 2011 by GMO LLC. All rights reserved. GMOGK_Yanni Partners_4-11 64

The Math

%Stocks X Stock Return X 1/3=

%Bonds X Stock Return X 1/2

Proprietary information – not for distribution to the public. Copyright © 2011 by GMO LLC. All rights reserved. GMOGK_Yanni Partners_4-11 65

The Math

%Stocks X Stock Return X 1/3=

%Bonds X Stock Return X 1/2

Rearranging gives us our Stock/Bond allocation ratio

%Stocks / %Bonds = 1.5~ 60% Stocks / 40% Bonds

Proprietary information – not for distribution to the public. Copyright © 2011 by GMO LLC. All rights reserved. GMOGK_Yanni Partners_4-11 66

Issues

• Relationship between stock and bond index returns is variable and not always negatively correlated

Proprietary information – not for distribution to the public. Copyright © 2011 by GMO LLC. All rights reserved. GMOGK_Yanni Partners_4-11 67

Issues

• Relationship between stock and bond index returns is variable and not always negatively correlated

• More reasonable to look at interest rate changes associated with falling stock prices and select a benchmark duration to produce the required result

Proprietary information – not for distribution to the public. Copyright © 2011 by GMO LLC. All rights reserved. GMOGK_Yanni Partners_4-11 68

Important Steps

• Provide a specific answer to the question, “Why do I own bonds?”

Proprietary information – not for distribution to the public. Copyright © 2011 by GMO LLC. All rights reserved. GMOGK_Yanni Partners_4-11 69

Important Steps

• Provide a specific answer to the question, “Why do I own bonds?”

• Establish an executable benchmark that captures the spirit, and in some cases the letter, of your objective

Proprietary information – not for distribution to the public. Copyright © 2011 by GMO LLC. All rights reserved. GMOGK_Yanni Partners_4-11 70

What About Alpha?

• Secondary to establishing an effective benchmark

Proprietary information – not for distribution to the public. Copyright © 2011 by GMO LLC. All rights reserved. GMOGK_Yanni Partners_4-11 71

What About Alpha?

• Secondary to establishing an effective benchmark

• Active strategies shouldn’t compromise benchmark effectiveness in meeting investment objectives

Proprietary information – not for distribution to the public. Copyright © 2011 by GMO LLC. All rights reserved. GMOGK_Yanni Partners_4-11 72

What About Alpha?

• Secondary to establishing an effective benchmark

• Active strategies shouldn’t compromise benchmark effectiveness in meeting investment objectives

• Good active bond managers can add value that is competitive with, and diversifies, equity alpha

Proprietary information – not for distribution to the public. Copyright © 2011 by GMO LLC. All rights reserved. GMOGK_Yanni Partners_4-11 73

Investment Management Template

Currency

Cumulative Liquidity

I. Beta Exposures

Term Structure (Nominal or

Inflation-Linked)

Credit Duration

Proprietary information – not for distribution to the public. Copyright © 2011 by GMO LLC. All rights reserved. GMOGK_Yanni Partners_4-11 74

Investment Management TemplateII. Active

Management Guidelines

Currency

Cumulative Liquidity

I. Beta Exposures

Term Structure (Nominal or

Inflation-Linked)

Credit Duration

Proprietary information – not for distribution to the public. Copyright © 2011 by GMO LLC. All rights reserved. GMOGK_Yanni Partners_4-11 75

Investment Management TemplateII. Active

Management Guidelines

Currency

III. Account Structure

Cumulative Liquidity

Investment Universe

Performance Objectives

Fee Structure

I. Beta Exposures

Term Structure (Nominal or

Inflation-Linked)

Credit Duration

Proprietary information – not for distribution to the public. Copyright © 2011 by GMO LLC. All rights reserved. GMOGK_Yanni Partners_4-11 76

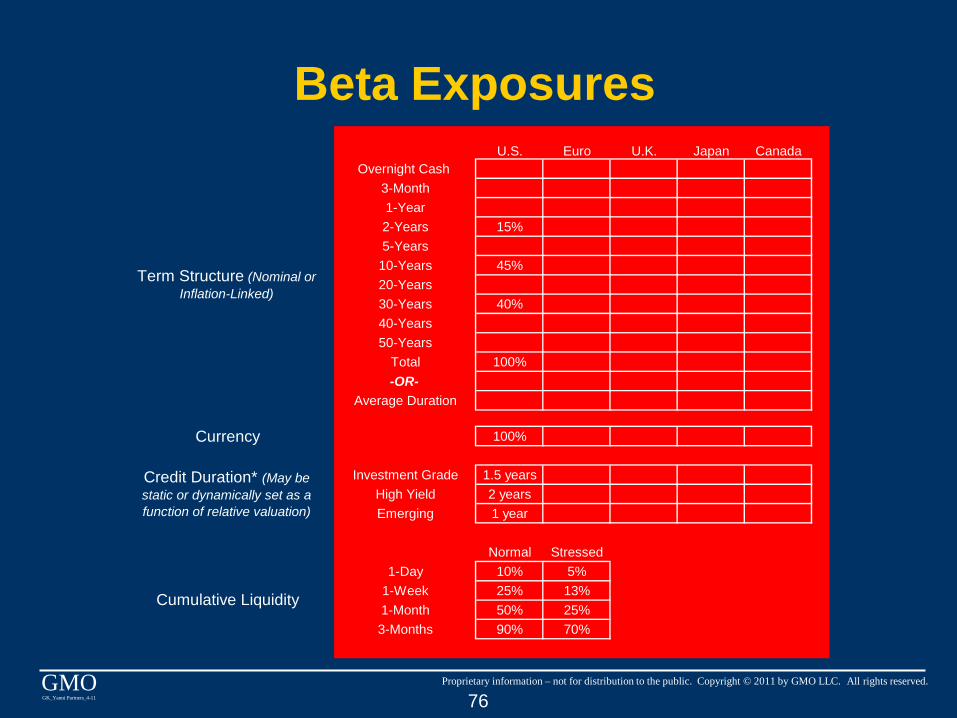

Beta ExposuresU.S. Euro U.K. Japan Canada

Overnight Cash 3-Month1-Year2-Years 15%5-Years10-Years 45%20-Years30-Years 40%40-Years50-Years

Total 100%-OR-

Average Duration

Currency 100%

Investment Grade 1.5 yearsHigh Yield 2 yearsEmerging 1 year

Normal Stressed1-Day 10% 5%

1-Week 25% 13%1-Month 50% 25%3-Months 90% 70%

Term Structure (Nominal or Inflation-Linked)

Credit Duration* (May be static or dynamically set as a function of relative valuation)

Cumulative Liquidity

Proprietary information – not for distribution to the public. Copyright © 2011 by GMO LLC. All rights reserved. GMOGK_Yanni Partners_4-11 77

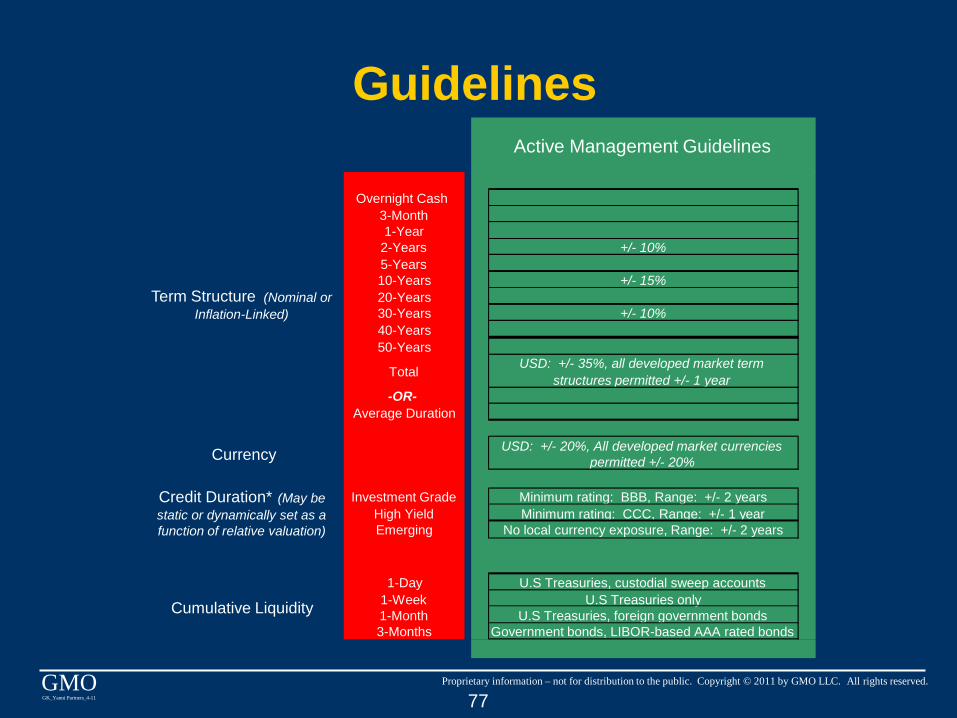

Guidelines

Overnight Cash 3-Month1-Year

2-Years5-Years10-Years20-Years30-Years40-Years50-Years

Total

-OR-Average Duration

Currency

Investment GradeHigh YieldEmerging

1-Day1-Week1-Month3-Months

Term Structure (Nominal or Inflation-Linked)

Credit Duration* (May be static or dynamically set as a function of relative valuation)

Cumulative Liquidity

Active Management Guidelines

+/- 10%

+/- 15%

+/- 10%

USD: +/- 35%, all developed market term structures permitted +/- 1 year

USD: +/- 20%, All developed market currencies permitted +/- 20%

Minimum rating: BBB, Range: +/- 2 yearsMinimum rating: CCC, Range: +/- 1 year

No local currency exposure, Range: +/- 2 years

U.S Treasuries, custodial sweep accountsU.S Treasuries only

U.S Treasuries, foreign government bondsGovernment bonds, LIBOR-based AAA rated bonds

Proprietary information – not for distribution to the public. Copyright © 2011 by GMO LLC. All rights reserved. GMOGK_Yanni Partners_4-11 78

Structure

Excess ReturnInformation Ratio

Tracking ErrorHorizon

Base-Plus-

Incentive

Investment Universe

Performance Objectives

Fee Structure

III. Account Structure

Derivatives permittedNo: Equities, municipal bonds, convertibles

Counterparties rated A or better, maximum 10%Co-mingled funds require look-through

150 basis points, annualized, net of fees0.4 to 0.8150 to 300 basis pointsRolling 5 years

20 basis points-Plus-25% of excess or return over beta, net of base fee and net of 3-month LIBOR; subject to high water mark

Proprietary information – not for distribution to the public. Copyright © 2011 by GMO LLC. All rights reserved. GMOGK_Yanni Partners_4-11 79

Fixed Income Can Play a Valuable Role in Endowment Portfolios

• Diversification: Significant outperformance in bear equity markets

Proprietary information – not for distribution to the public. Copyright © 2011 by GMO LLC. All rights reserved. GMOGK_Yanni Partners_4-11 80

Fixed Income Can Play a Valuable Role in Endowment Portfolios

• Diversification: Significant outperformance in bear equity markets

• Deflation/inflation hedging

Proprietary information – not for distribution to the public. Copyright © 2011 by GMO LLC. All rights reserved. GMOGK_Yanni Partners_4-11 81

Fixed Income Can Play a Valuable Role in Endowment Portfolios

• Diversification: Significant outperformance in bear equity markets

• Deflation/inflation hedging• Adding value: Many bond strategies are

more effective than equity counterparts

Proprietary information – not for distribution to the public. Copyright © 2011 by GMO LLC. All rights reserved. GMOGK_Yanni Partners_4-11 82

Conclusions

• It’s critical to align portfolio beta benchmarks with investment objectives

Proprietary information – not for distribution to the public. Copyright © 2011 by GMO LLC. All rights reserved. GMOGK_Yanni Partners_4-11 83

Conclusions

• It’s critical to align portfolio beta benchmarks with investment objectives

• Process begins by articulating explicit goals and incorporating them in an investable benchmark

Proprietary information – not for distribution to the public. Copyright © 2011 by GMO LLC. All rights reserved. GMOGK_Yanni Partners_4-11 84

Conclusions

• It’s critical to align portfolio beta benchmarks with investment objectives

• Process begins by articulating explicit goals and incorporating them in an investable benchmark

• Bond beta and alpha decisions must fit within a broader asset allocation framework

The End