evolution of the vod market in europe workshop europa distribution paris, 7th july 2009 andré lange...

TRANSCRIPT

Evolution of the VoD market in Europe

Workshop Europa Distribution

Paris, 7th July 2009André Lange

Head of Department

Information on Markets andFinancing

European Audiovisual Observatory

2

LEGAL EUROPEAN DEFINITION OF « AUDIOVISUAL MEDIA SERVICE ON DEMAND »

Directive SMAV (11 December 2007)

• "on-demand audiovisual media service" (i.e. a non-linear audiovisual media service) means an audiovisual media service provided by a media service provider for the viewing of programmes at the moment chosen by the user and at his individual request on the basis of a catalogue of programmes selected by the media service provider”

3

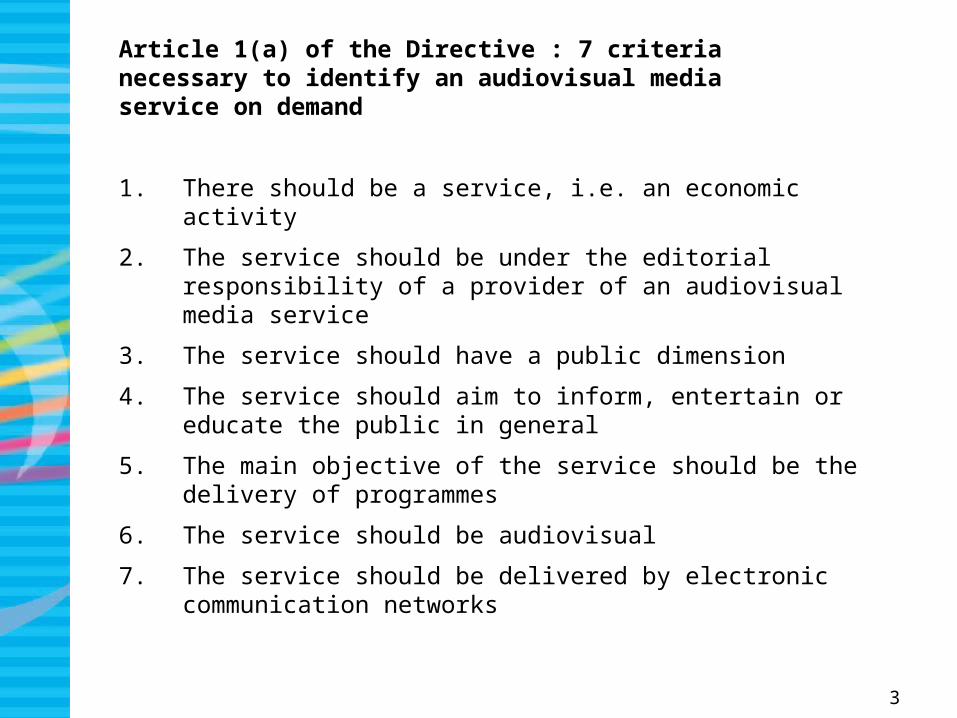

Article 1(a) of the Directive : 7 criteria necessary to identify an audiovisual media service on demand

1. There should be a service, i.e. an economic activity

2. The service should be under the editorial responsibility of a provider of an audiovisual media service

3. The service should have a public dimension

4. The service should aim to inform, entertain or educate the public in general

5. The main objective of the service should be the delivery of programmes

6. The service should be audiovisual

7. The service should be delivered by electronic communication networks

4

Definition of the provider of audiovisual media service (Article 1d of the Directive)

• “Media service provider" means the natural or legal person who has editorial responsibility for the choice of the audiovisual content of the audiovisual media service and determines the manner in which it is organised ».

Practical question for the statistician : how to identify the provider ?

Confusion between the provider of the service and the distributor

Frequent situations of « partnership »

How to consider partners channels on Youtube ?

5

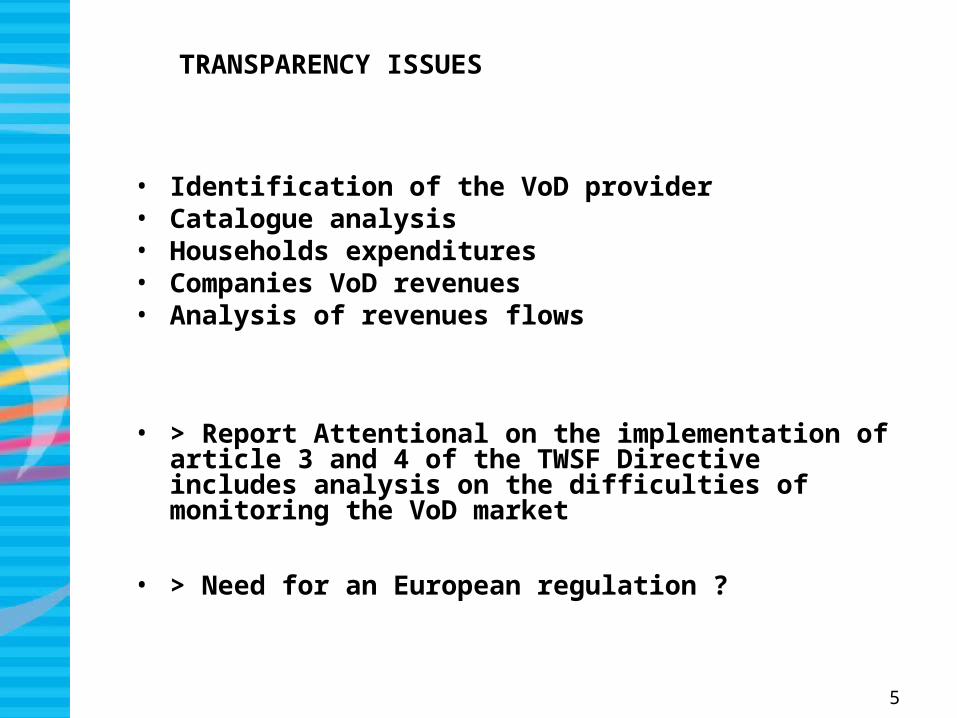

TRANSPARENCY ISSUES

• Identification of the VoD provider• Catalogue analysis• Households expenditures• Companies VoD revenues• Analysis of revenues flows

• > Report Attentional on the implementation of article 3 and 4 of the TWSF Directive includes analysis on the difficulties of monitoring the VoD market

• > Need for an European regulation ?

6

TECHNICAL MODELS OF ON-DEMAND SERVICES

Source : NPA Conseil

7

FILM IMMEDIATE DOWNLOAD POSSIBLE ON THE NEW iPhone 3GS THROUGH ATT Wifi, LAUNCHED IN USA June 19 2009

8

RESPECTIVE ADVANTAGES AND DISADVANTAGES OF DELIVERY PLATFORMS

PLUS MINUS

Internet - B to C model

- Editorial possibilities, search possibilities- Customized marketing- Allows niche strategies- Allows international strategies- Allows larger catalogues

- Viewing most often on PC screen- Breaks in the quality of service- Slow to download- Risks of piracy- Services most often not accessible on MAC

IPTV - Viewing on TV set- Existing basis of subscribers (different according countries)

- Capacity limits (>FTTH)-- EPG rather slow and not user friendly- More difficult of access for independent producers and niche programmes- Smaller catalogues than on Internet services

Cable - Viewing on TV set- Existing basis of subscribers (different according countries)

-Cost of digitization of networks-More difficult of access for independent producers and niche programmes- Reduced catalogues

Satellite

and DTT

- Viewing on TV set- Existing basis of subscribers (different according countries)

-No return path-Needs storage on PVR-More difficult of access for independent producers and niche programmes- Reduced catalogues

9

THE CHALLENGE OF VoD ON THE TV SCREEN

• VoD in the framework of cable or ADSL triple play offer (IPTV)

• VoD through PVR• Hybrid PVR – IPTV systems (Canalsat, Viasat)• Dedicated set-top box

– Apple TV, Vudu,…

– Maxdome,

– FNAC/Netgem

– CANVAS project of British PSB broadcasters and BT)

• Cable ipod > TV Screen• Web enabled TV set (The Yankee Group expects 50 million people will have Internet

connected HDTVs by 2013. Another 30 million, they say, will have connected Blu Ray players – and 11 million will have purchased media adaptors.

10

DIGITAL HOUSEHOLDS BY KIND OF PLATFORM(31.12.2007)Source : OBS

0%

20%

40%

60%

80%

100%

IPTV

DTT

DTH

CATV

IPTV 0,8% 1,2% 24,7% 2,9% 4,7%

DTT 44,1% 23,7% 39,5% 55,0% 70,6%

DTH 40,3% 58,4% 28,8% 42,2% 17,0%

CATV 14,8% 16,7% 6,9% 0,0% 7,7%

GB DE FR IT ES

11

PENETRATION OF BROADBAND, DIGITAL CABLE AND IPTV (2007) % of householdsSource : Screen Digest / OBS

0%

10%

20%

30%

40%

50%

60%

DE ES FR GB IT

BroadbandCableIPTV

12

NUMBER OF VoD SERVICES IN 24 EUROPEAN COUNTRIES (2002-2008)Source : NPA Conseil

110 21

61

142

258

325

0

50

100

150

200

250

300

350

2002 2003 2004 2005 2006 2007 mid-2008

13

NUMBER OF ON-DEMAND AUDIOVISUAL SERVICES IN

EUROPE (December 2008): 691 services Source : OBS

0

20

40

60

80

100

120

140

160

GB FR IT DE NL BE ES SE NO DK PL FI HU CH IE RU AT CZ SK TR EE LU IS CY RO GR PT SI BG LV

TNT

Satellite

Câble

IPTV

Internet

14

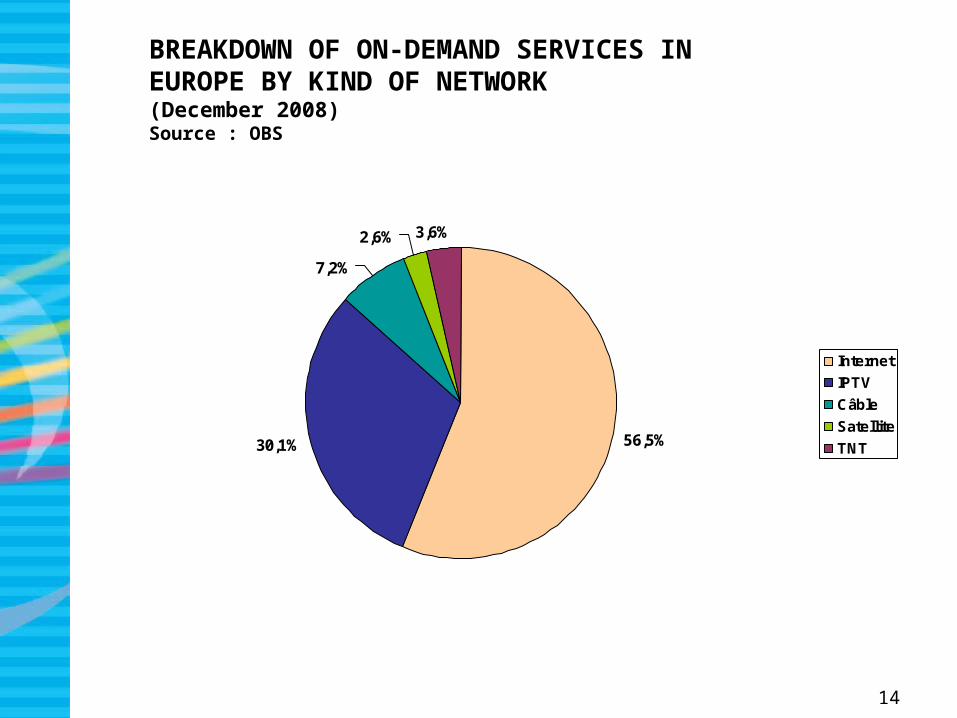

BREAKDOWN OF ON-DEMAND SERVICES IN EUROPE BY KIND OF NETWORK (December 2008)Source : OBS

56,5%30,1%

7,2%

2,6% 3,6%

Internet

IPTV

Câble

Satellite

TNT

15

PROVIDERS OF ON-DEMAND AUDIOVISUAL SERVICESIN EUROPE

- Telcos: T-Online, France Telecom, Belgacom, Telecom Italia, Telefonica

- ISP: Fastweb (IT), Arcor (DE), Absolut Medien (DE), Tiscali (GB)- Cable operators: Telenet, ntl, Telewest, ONO, Casema- Broadacsters : Canal+, TPS, TF1, RAI, RTLNederland, FT2,

ARTE, M6, BBC, Premiere, ProSiebenSat1, Sky, Mediaset,…- Film groups : SF (Svensk Filmindustry), MK2, Filmax- Producers associations : Universciné, FIDD- Archives Film & TV : British Pathe, NFI, INA- Video publishers: TF1 Video, Editions Montparnasse- Retailers : Lovefilm, Virgin, Glowria, Carrerfour- New companies (agregators) : Cinezime, 4friends, Live

Networks, Videonetwork…- Copyright collecting societies : SGAE, EGEDA- Manufacturers : Apple, Archos, Microsoft, Nintendo- Specialised services : Arts Alliance Media Ltd

16

BREAKDOWN OF PROVIDERS OF ON-DEMAND SERVICES BY PRIMARY ORIGIN (December 2008)Source : OBS

Telcos17,7%

Cable opérators3,9%

Satelitte/DTT packagers1,9%

Content agregators13,3%

Film companies3,9%

US Majors subsidiaries9,1%

Video publishers3,0%

TV producers3,0%

Manufacturers1,7%Retailers

4,1%

Copyright societies0,6%Services

2,2%

Archives1,1%

Broadcasters34,5%

17

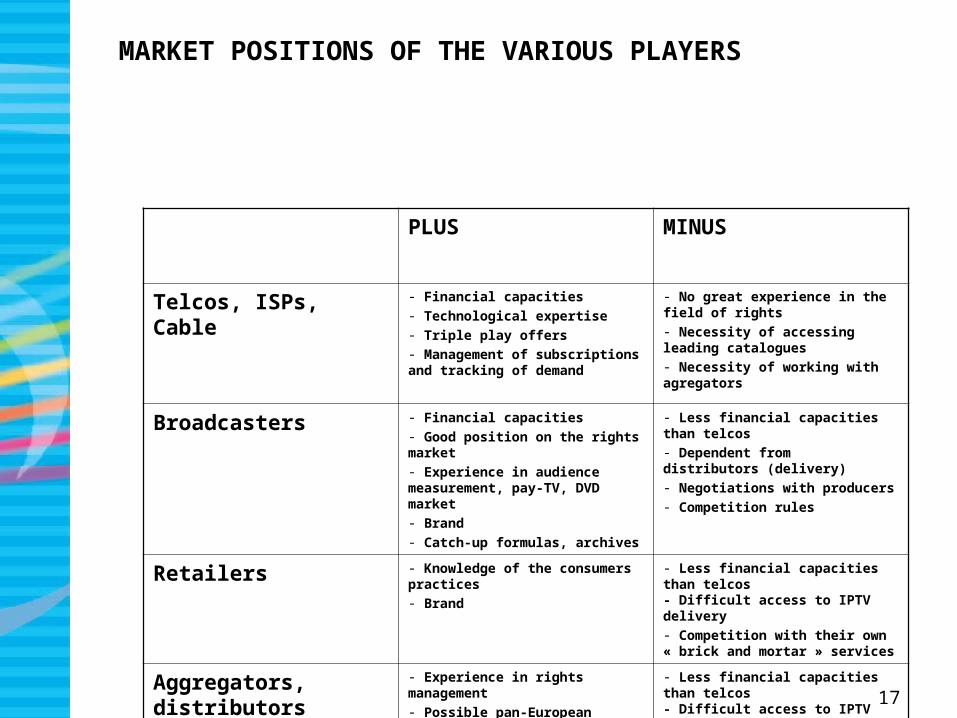

MARKET POSITIONS OF THE VARIOUS PLAYERS

PLUS MINUS

Telcos, ISPs,Cable

- Financial capacities- Technological expertise- Triple play offers- Management of subscriptions and tracking of demand

- No great experience in the field of rights- Necessity of accessing leading catalogues- Necessity of working with agregators

Broadcasters - Financial capacities- Good position on the rights market- Experience in audience measurement, pay-TV, DVD market- Brand- Catch-up formulas, archives

- Less financial capacities than telcos- Dependent from distributors (delivery)- Negotiations with producers- Competition rules

Retailers - Knowledge of the consumers practices- Brand

- Less financial capacities than telcos- Difficult access to IPTV delivery- Competition with their own « brick and mortar » services

Aggregators, distributors

- Experience in rights management- Possible pan-European strategies- Niche catalogues

- Less financial capacities than telcos- Difficult access to IPTV delivery

18

MANUFACTURERS (Apple, Microsoft, Sony, Nintendo,…)

• Strategic advantage : main objective is the sale of hardware• Possibility of offering good conditions to rights owners and

to increase rapidly the catalogue• Possibility of opening « channels » to other providers• Cumulating position of provider and distributors of third

services• Common platform for films, TV programmes and

videogames• Worldwide players

19

iTUNES STORE SUCCESS Source : Apple Inc. (data provided without geographical breakdown)

• 1 million videos sold as at 31.10.2005 (20 days after the launching)

• 8 millions videos sold early January 2006• 15 millions videos sold as at 23.2.2006• 50 millions TV shows and 1.3 millions films sold as at

10.1.2007• 2 millions films sold as at 11.4.2007• 200 millions TV shows sold as at 16.10.2008

20

USA – SHARE OF DIGITAL TRANSACTIONS FOR FILMS (2008)Source : Screen Digest February 2009

iTunes Stores

53%

Others14%

XBox Live Video

Marketplace33%iTunes

87%

Others13%

21

iTUNES STORES EUROPEAN TURNOVER (2005-2007) EUR millionSource : iTunes S.AR.L.

53

132,2

224,5

0

50

100

150

200

250

2005 2006 2007

22

VoD STRATEGIES OF THE VARIOUS CATEGORIES OF FILM PRODUCERS IN EUROPE

Majors US - Blockbusters and library « long tail « - Agreements with local providers of VoD services- No exclusivity - No direct investments in Europe- No pan-European deals

National film groups - few blockbuster, « long tail » libraries»

- Agreementts with local providers of VoD services- No exclusivity- Almost no direct investment (SF, MK2)

- VoD international sales through agents

Independent producers - Mainly « long tail » catalogues- Regroupment strategies with aggregators

(Universine, Filmotech,…)- Niche strategies, sometimes international- Looking for IPTV and cable access- Support of MEDIA 2007 Programme

Broadcasters - Catch-up TV - Difficulties in exploiting archives- Some operators have films catalogues- Mainly Internet services

- Alliances with YouTube, DailyMotion,…- Difficulties in accessing cable and IPTV

23

BUSINESS MODELS

• Digital rental (24 hours > 48 hours)– 1 title (1,5 to 6 EUR)– 1 pack (Credit)

• Sale (“Download to own” DTO)- Download to PC (5 to 15 EUR)- Download to burn (15 to 20 EUR)

• Online subscription VoD (SVoD)

• Free VoD : financed by advertising (MSN, Myvideo,…) or licence fee (BBC iPlayer)

• Catch-up TV of film pay-TV channels (Canal+, Canalsat, SkyPlayer, TopUpTV Anytime,…)

24

FRANCE : 8 leading services supply 3959 films (2753 in 2007, + 48,9 %) Source : CNC

US36,5%

French43,6%

European 14,0%

Others5,9%

25

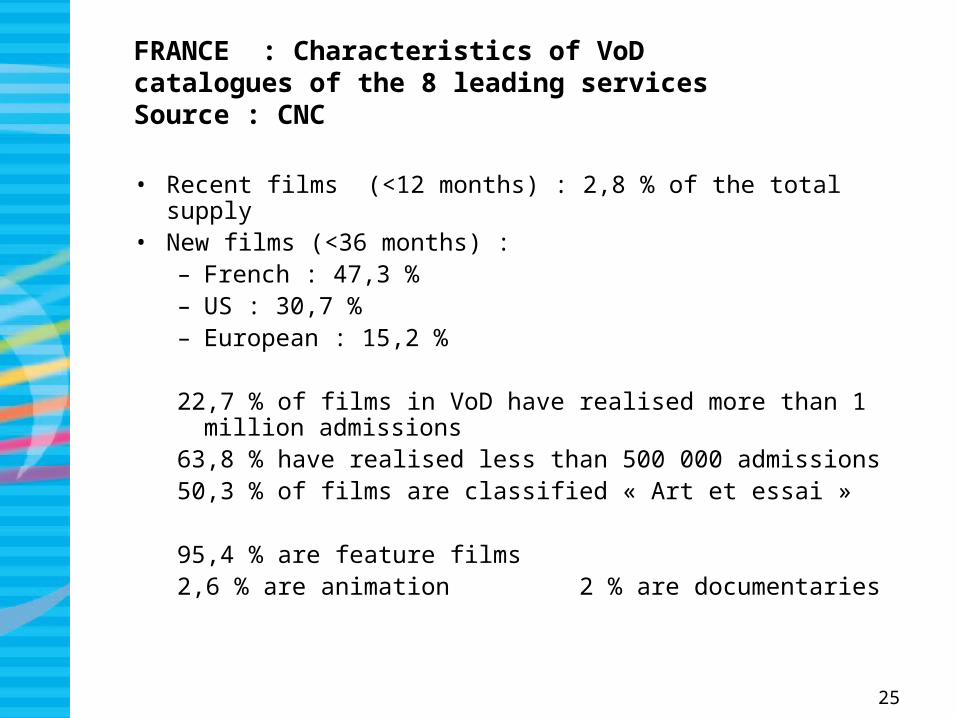

FRANCE : Characteristics of VoD catalogues of the 8 leading servicesSource : CNC

• Recent films (<12 months) : 2,8 % of the total supply• New films (<36 months) :

– French : 47,3 %– US : 30,7 %– European : 15,2 %

22,7 % of films in VoD have realised more than 1 million admissions

63,8 % have realised less than 500 000 admissions50,3 % of films are classified « Art et essai »

95,4 % are feature films 2,6 % are animation 2 % are documentaries

26

FRANCE : Availability of films by number of platformsSource : CNC

2087; 52,7%

971; 24,5%

511; 12,9%

390; 9,9%

1 platform

2 platforms

3 platforms

4 platforms or +

27

FRANCE : VoD IN FRONT OF OTHER CONSUMERS PRACTICES1st Semester 2007/2008

Sources : CNC, ALPA/Thomson, GfK/CNC, Gfk/NPA

94,24

100,9

76,5

55,9 53,28

3,7 6

0

20

40

60

80

100

120

Admissions Unauthorizeddowloads

Sales DVD (units) Legal VoDtransactions

1er half 20071er half 2008

28

FRANCE – EVOLUTION OF HOUSEHOLDS AUDIOVISUAL EXPENSES (2004-2008) EUR millionSource : CNC

0

500

1000

1500

2000

2500

3000

3500

4000

2004 2005 2006 2007 2008

Pay-TV (C+,cable/satellite)

Licence fee

Home vidéo

Box office

VoD

29

UNITED KINGDOM : UK film revenues (2004-2008) Millions £ Source : UK Film Council 2009 Statistical Yearbook (forthcoming)

0

200

400

600

800

1000

1200

1400

1600

1800

2004 2005 2006 2007 2008

Home video retail

Film on TV

Box office

Home video Rental

Film on VoD/nVoD

30

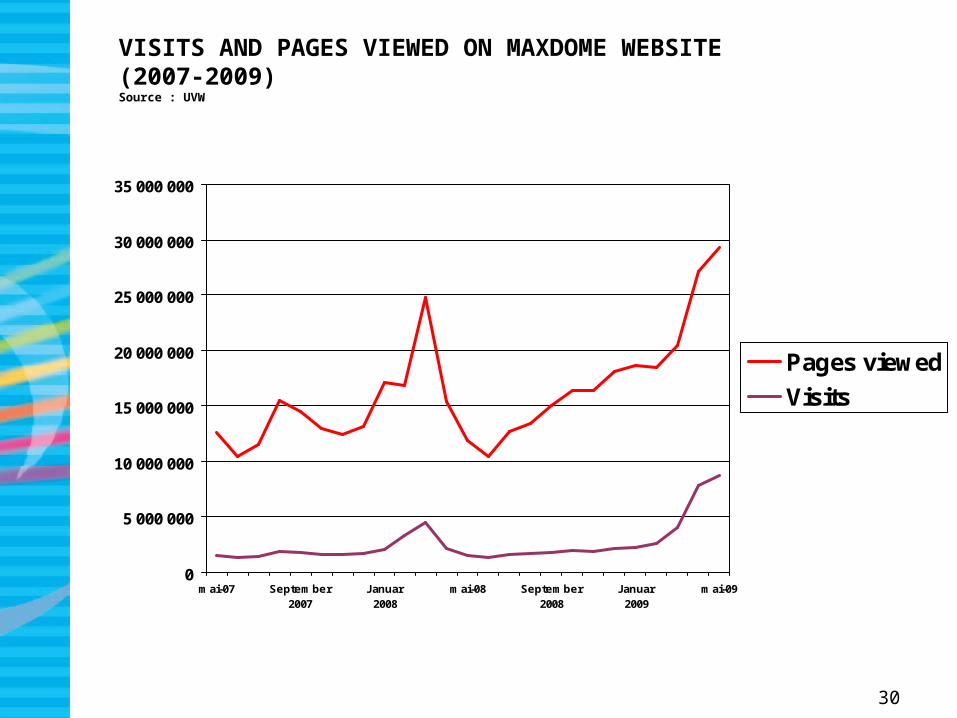

VISITS AND PAGES VIEWED ON MAXDOME WEBSITE (2007-2009)Source : UVW

0

5 000 000

10 000 000

15 000 000

20 000 000

25 000 000

30 000 000

35 000 000

mai-07 September2007

Januar2008

mai-08 September2008

Januar2009

mai-09

Pages viewed

Visits

31

GLOBAL ON-DEMAND REVENUESFORECAST 2012 - Includes nVoD - Euros BillionSource : Screen Digest – January 2009

North America; 7,5

Europe; 3,3

Asia-Pacific; 1,5

0

1

2

3

4

5

6

7

8

2012

32

CABLE vs IPTV VoD REVENUES IN WESTERN EUROPE – Euros millionSource : Screen Digest – January 2009

0

100

200

300

400

500

600

2005 2006 2007 2008 2009 2010 2011 2012

IPTV

Cable

33

Number of illegal film download (June 2009)Source : MARC

0

500000

1000000

1500000

2000000

2500000

3000000

3500000

4000000

4500000United Kingdom

United States

France

Canada

Italy

Spain

Brazil

Netherlands

Poland

Norway

34

QUESTIONS FOR THE DEBATE

• How to fight online piracy ?

• Films in iTunes Stores in more EUR countries ?

• Strategic importance of HD VoD ?

• Is the shortening of the windows a real threat for cinema-going ?

• Will VoD kill the video rental business ?

• How to ensure pre-eminence of European films in VoD catalogues ?

• Is the multi-territory licence a key issue for the development of a pan-European VoD market ?