excella trader derivative class

TRANSCRIPT

www.excellatrader.com

Understanding Futures & Options

www.excellatrader.com

What we will cover?

Introductions to DerivativePricing – The Greeks Trading options in IndiaOption trading strategies

www.excellatrader.com

A Financial Instrument That Derives

What is a derivative? A Financial instrument that derives its

value from An Underlying asset

The asset can be a share, index, interest rate, bond, rupee dollar exchange rate, sugar, crude oil, cotton, coffee and etc.

www.excellatrader.com

Case of a wheat farmer:

A wheat farmer may wish to contract to sell his harvest at a future date to eliminate the

risk of a change in prices by that date

www.excellatrader.com

Uses of Derivatives

HedgingSpeculationArbitrage

www.excellatrader.com

Index Futures

A barometer for market behaviorA benchmark for portfolio performanceAn underlying in derivative instruments

www.excellatrader.com

What are options?

An option is a contract, which gives the buyer (holder) the right, but not the obligation, to buy or sell specified quantity of the underlying assets, at a specific (strike) price on or before a specified time (expiration date).

www.excellatrader.com

Call Option Put Option

Option Buyer

Buys the right to buy the underlying asset at the Strike Price

Buys the right to sell the underlying asset at the Strike Price

Option Seller

Has the obligation to sell the underlying asset to the option holder at the Strike Price

Has the obligation to buy the underlying asset from the option holder at the Strike Price

www.excellatrader.com

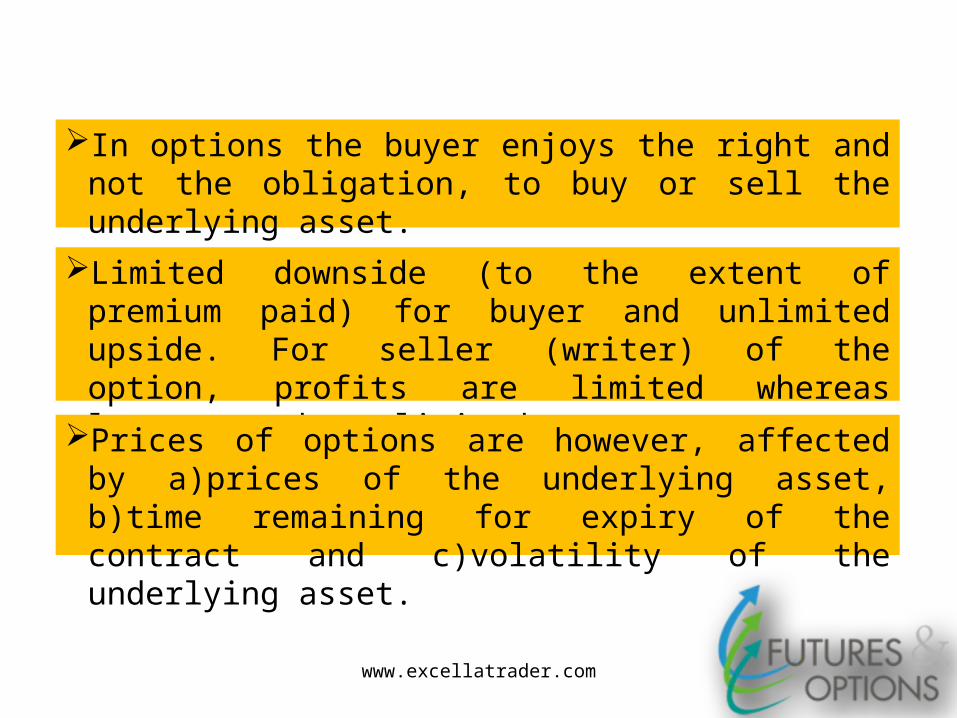

In options the buyer enjoys the right and not the obligation, to buy or sell the underlying asset.

Limited downside (to the extent of premium paid) for buyer and unlimited upside. For seller (writer) of the option, profits are limited whereas losses can be unlimited.

Prices of options are however, affected by a)prices of the underlying asset, b)time remaining for expiry of the contract and c)volatility of the underlying asset.

www.excellatrader.com

Terms

Underlying Strike priceExpiry datePremiumExercise Lot sizeAmerican optionEuropean option

www.excellatrader.com

Pay Rs.10 Buy Reliance at Rs 900

But only if it is above

900

www.excellatrader.com

Option Buyer

Right to buy

Pays premium

Option seller

obligation to sell

Gets premium

www.excellatrader.com

Pricing

An option price consists of two partsTime value andIntrinsic value

Example

If Nifty is at 5050And Nifty 5000 call option is at Rs. 75

Intrinsic value 50

Time value 25

www.excellatrader.com

General Electric is considered a stock with low volatility with a beta of 0.49 for this example.

www.excellatrader.com

www.excellatrader.com

LONG CALL

Market Opinion - Bullish

Profit +

0

DR

Loss -

Underlying Asset Price

Stock Price

Lower Higher

BEP

S

www.excellatrader.com

In-the-money option (ITM)At-the-money option (ATM)Out-of-the-money option (OTM)

www.excellatrader.com

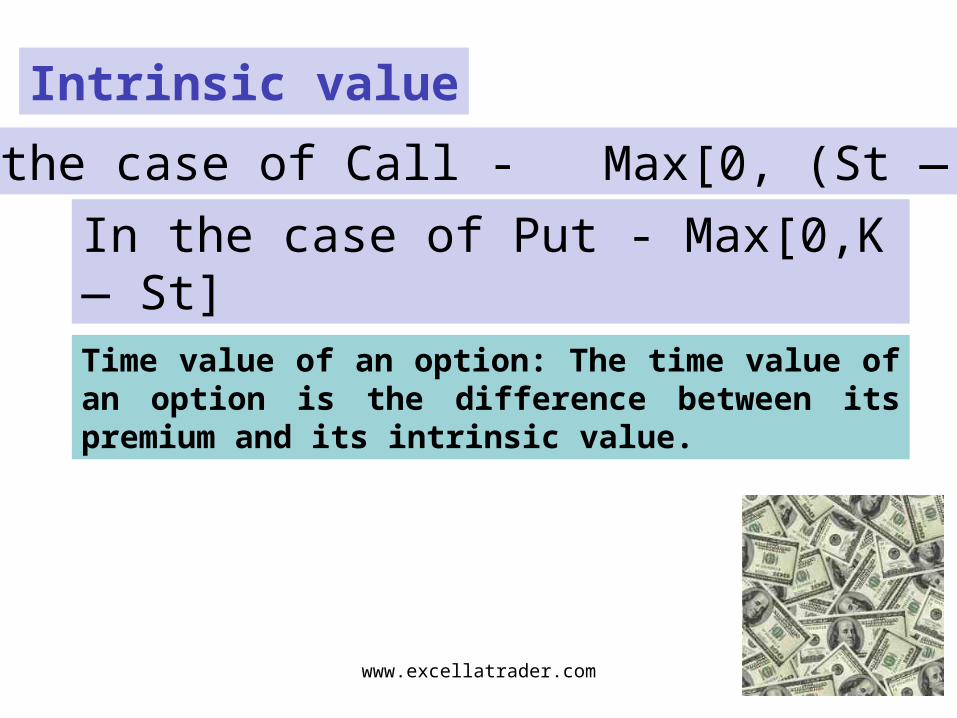

In the case of Call - Max[0, (St — K)]

In the case of Put - Max[0,K — St]

Intrinsic value

Time value of an option: The time value of an option is the difference between its premium and its intrinsic value.

www.excellatrader.com

Option pay offsPayoff profile of buyer of asset: Long asset

www.excellatrader.com

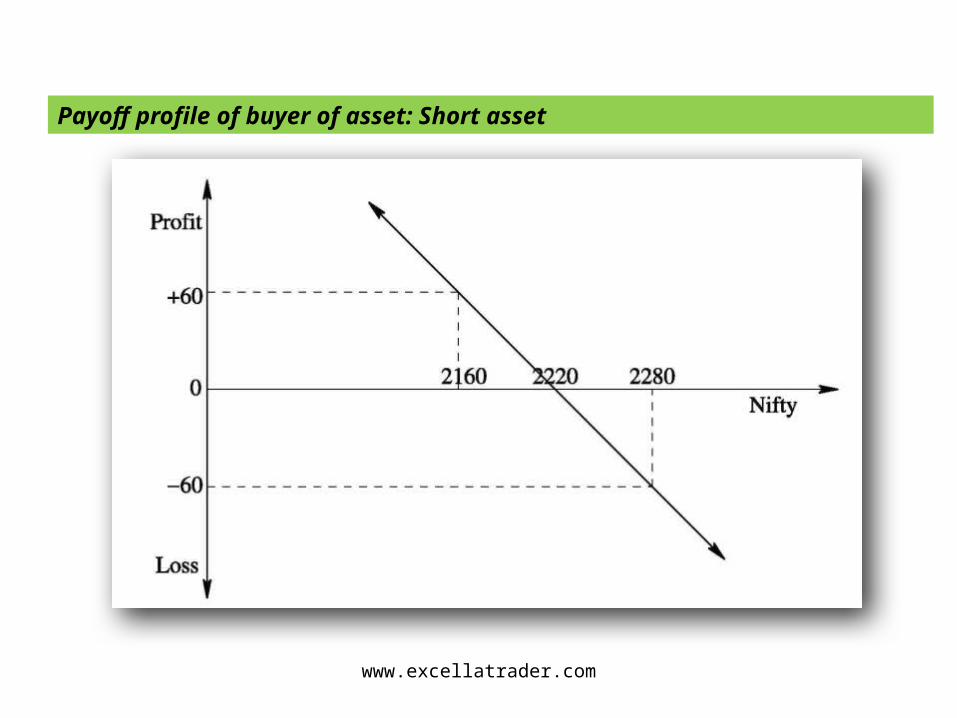

Payoff profile of buyer of asset: Short asset

www.excellatrader.com

Payoff for buyer of call option

www.excellatrader.com

Payoff for writer of call option

www.excellatrader.com

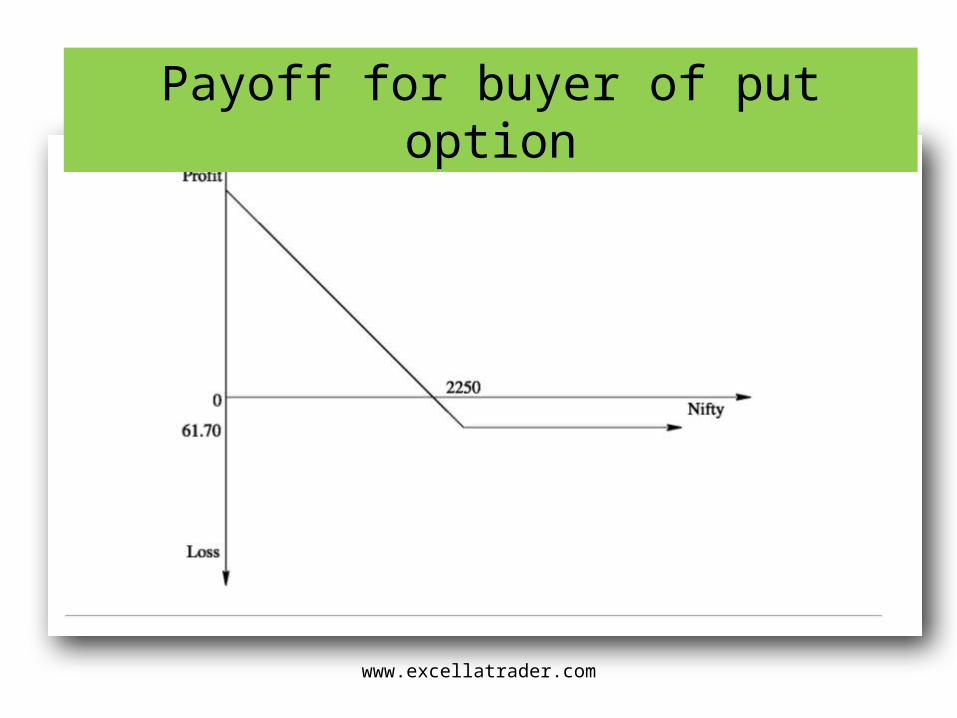

Payoff for buyer of put option

www.excellatrader.com

Payoff for writer of put option

www.excellatrader.com

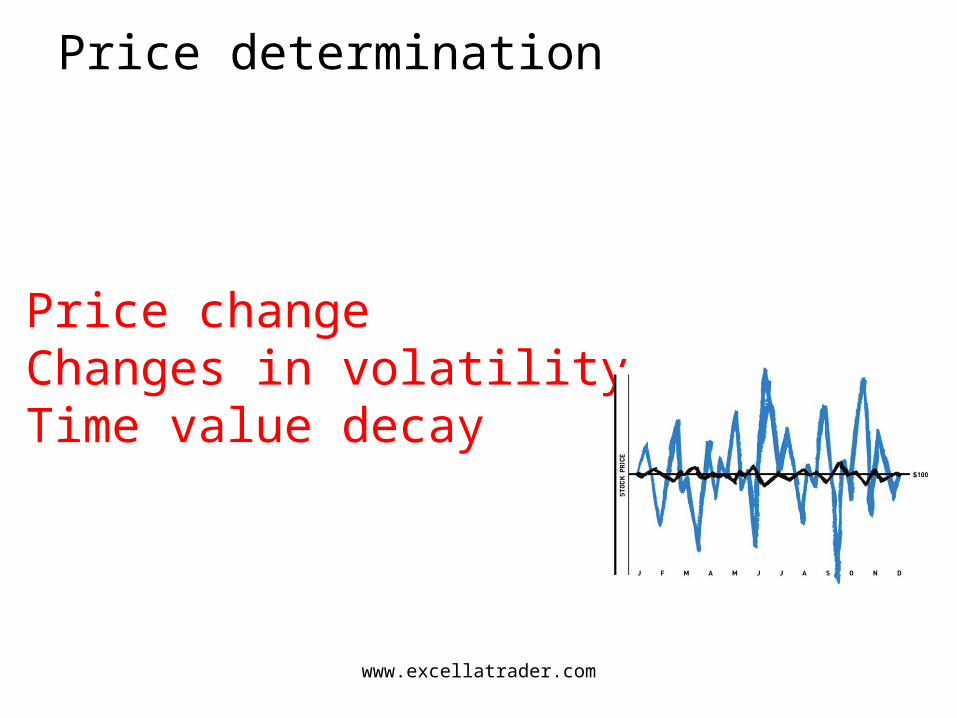

Price determination

Price changeChanges in volatilityTime value decay

www.excellatrader.com

Delta Measures of risk from a move of the underlying price

www.excellatrader.com

Delta

When the Underlying Security...

Increase in Value

Decrease in Value

The Long Call will…. Increase in Value Decrease in ValueThe Short Call will…. Decrease in Value Increase in ValueThe Long Put will…. Decrease in Value Increase in ValueThe Short Put will…. Increase in Value Decrease in Value

www.excellatrader.com

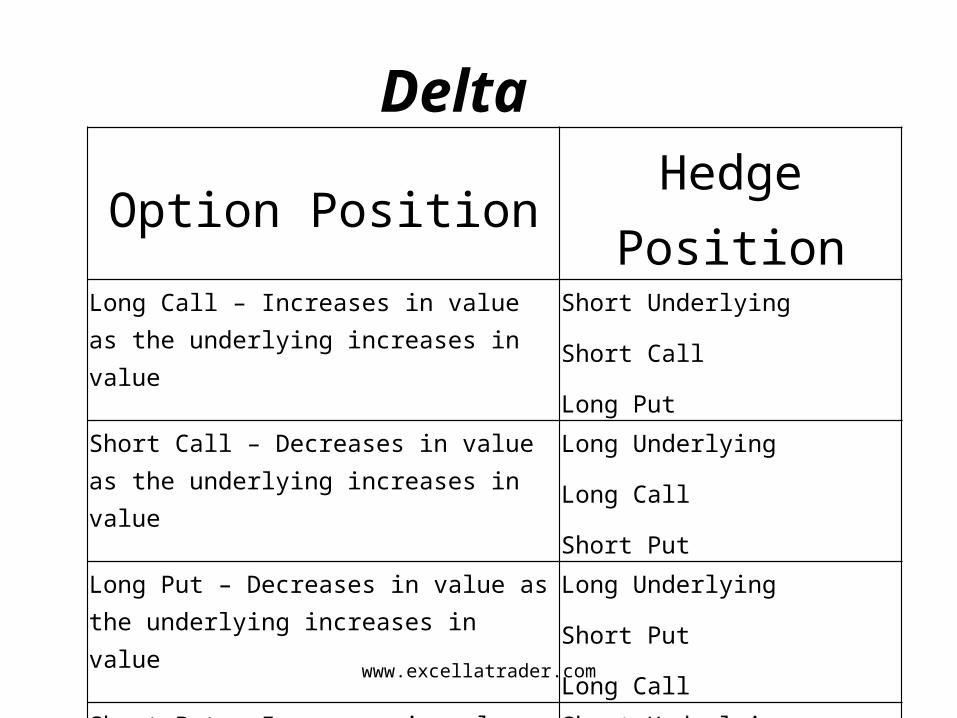

Delta Option Position Hedge Position

Long Call – Increases in value as the underlying increases in value

Short Underlying

Short Call

Long PutShort Call – Decreases in value as the underlying increases in value

Long Underlying

Long Call

Short PutLong Put – Decreases in value as the underlying increases in value

Long Underlying

Short Put

Long CallShort Put – Increases in value as the underlying decreases in value

Short Underlying

Long Put

Short Call

www.excellatrader.com

Constructing a Delta-neutral strategy

Statistical Volatility 25%

Option Strike Price 100

Days remaining 30

Price of underlying

Call Option Put OptionDelta of

underlying

80 0.0013 -0.9987 1.0000

85 0.0148 -0.9852 1.0000

90 0.0843 -0.9157 1.0000

95 0.2668 -0.7332 1.0000

100 0.5371 -0.4629 1.0000

105 0.7805 -0.2195 1.0000

110 0.9226 -0.0774 1.0000

115 0.9795 -0.0205 1.0000

120 0.9958 -0.0042 1.0000

www.excellatrader.com

Constructing a Delta-neutral strategy

•The absolute value of the delta increases as the option goes further in-the-money and decreases as the option goes out-of-the-money. •At-the-money call and put options have a delta that is right around 0.50 and -0.50 respectively. •Put options have a negative delta, which means if the price of an asset goes up, the price of a put option on that asset goes down. •Deep in-the-money call options have a delta that approaches +1.00. Conversely, deep in-the-money put options have a delta that approaches -1.00. •Deep out-of-the-money calls and puts have deltas that approach zero. •The delta of the underlying asset itself always remains constant at 1.00.

Price of underlying Call Option Put Option Delta of underlying

80 0.0013 -0.9987 1.0000

85 0.0148 -0.9852 1.0000

90 0.0843 -0.9157 1.0000

95 0.2668 -0.7332 1.0000

100 0.5371 -0.4629 1.0000

105 0.7805 -0.2195 1.0000

110 0.9226 -0.0774 1.0000

115 0.9795 -0.0205 1.0000

120 0.9958 -0.0042 1.0000

www.excellatrader.com

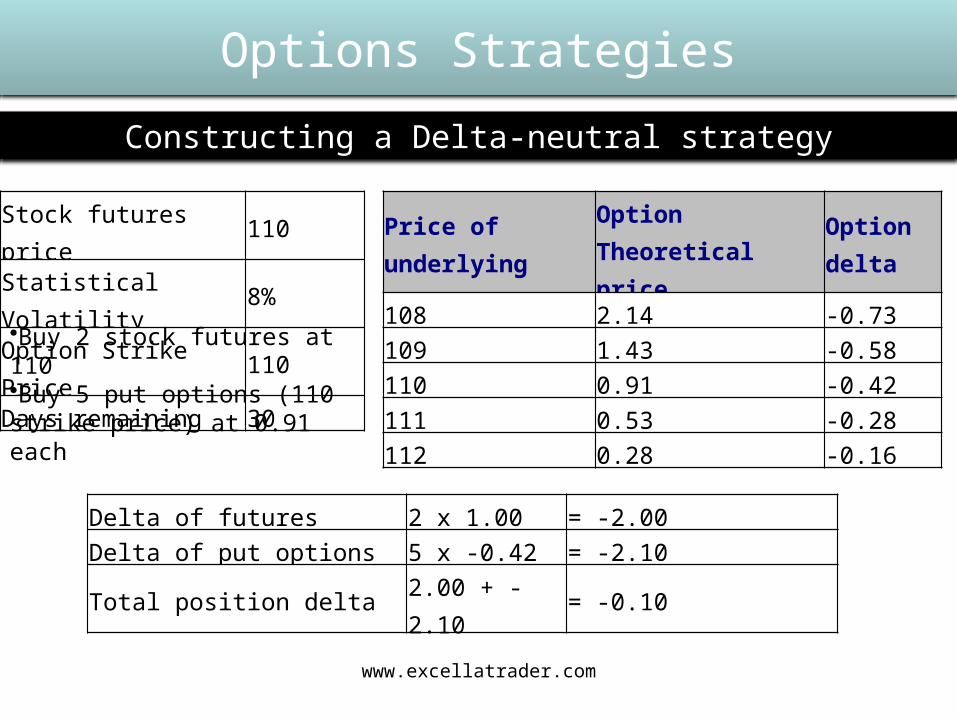

Options Strategies

Constructing a Delta-neutral strategy

Stock futures price 110

Statistical Volatility 8%

Option Strike Price 110

Days remaining 30

Price of underlying

Option Theoretical price

Option delta

108 2.14 -0.73

109 1.43 -0.58

110 0.91 -0.42

111 0.53 -0.28

112 0.28 -0.16

•Buy 2 stock futures at 110 •Buy 5 put options (110 strike price) at 0.91 each

Delta of futures 2 x 1.00 = -2.00

Delta of put options 5 x -0.42 = -2.10

Total position delta 2.00 + -2.10 = -0.10

www.excellatrader.com

Options Strategies

Constructing a Delta-neutral strategy

If you buy the underlying and buy put options so your position is delta neutral:

•When the market goes up, you have a profit on the underlying and you have a smaller loss on the options (because their delta decreased), so you wind up with a net profit.

•When the market goes down, you have a loss on the underlying but you have a bigger profit on the options (because their delta increased), so again you have a net profit.

www.excellatrader.com

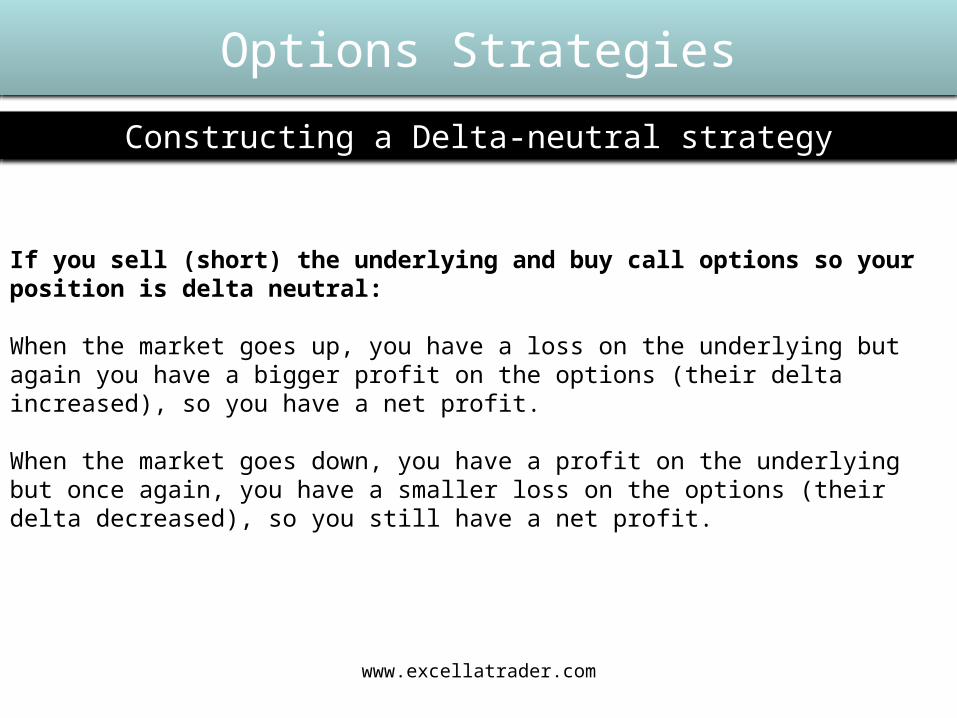

Options Strategies

Constructing a Delta-neutral strategy

If you sell (short) the underlying and buy call options so your position is delta neutral:

When the market goes up, you have a loss on the underlying but again you have a bigger profit on the options (their delta increased), so you have a net profit.

When the market goes down, you have a profit on the underlying but once again, you have a smaller loss on the options (their delta decreased), so you still have a net profit.

www.excellatrader.com

Vega Changes in implied volatility.

www.excellatrader.com

Theta Theta is a measure of the rate of time premium decay

www.excellatrader.com

www.excellatrader.com

Theta

As Time Moves Forward...

Underlying Security Value remains constantLong Call Decrease in ValueShort Call Increase in ValueLong Put Decrease in ValueShort Put Increase in Value

www.excellatrader.com

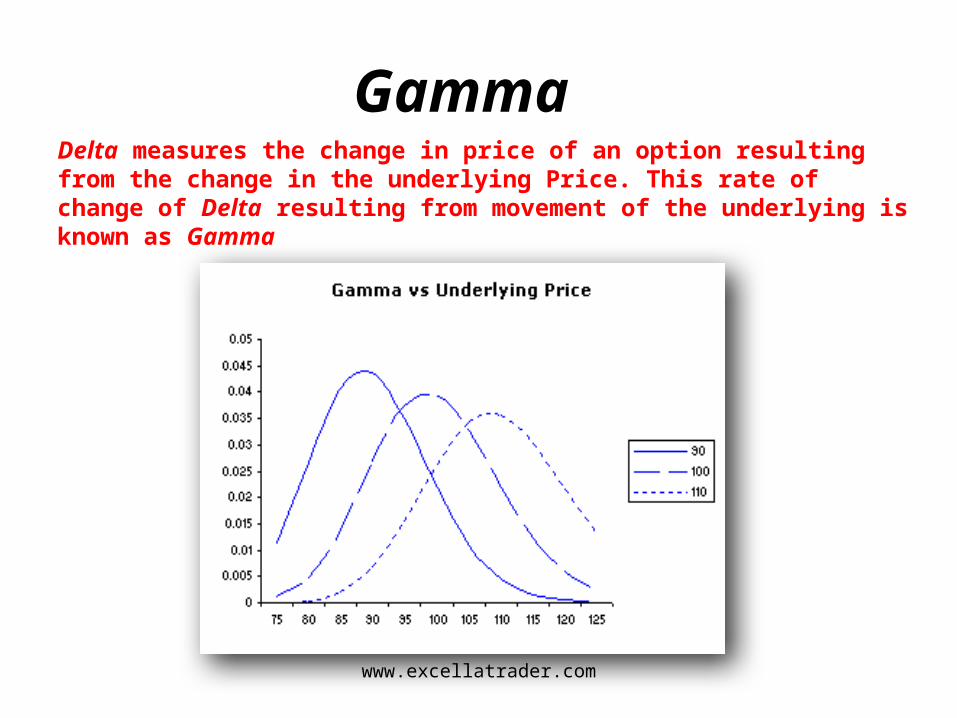

Gamma Delta measures the change in price of an option resulting from the change in the underlying Price. This rate of change of Delta resulting from movement of the underlying is known as Gamma

www.excellatrader.com

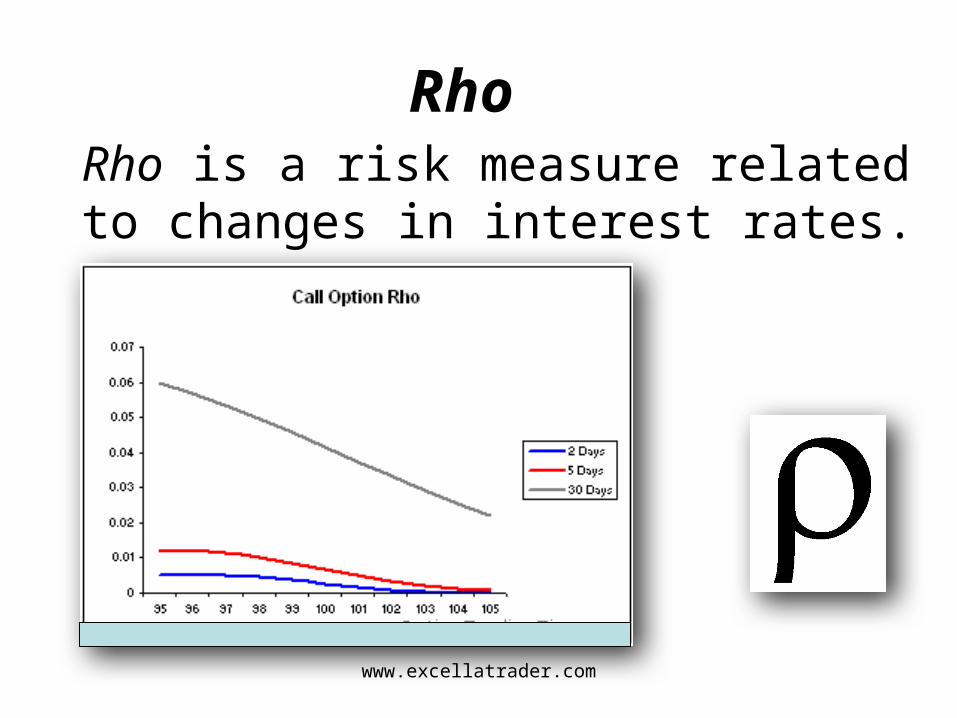

Rho Rho is a risk measure related to changes in interest rates.

www.excellatrader.com

Varying market conditionsAs market conditions change the values of...

Rise in price of the underlying...

Interest rates Rise...

Volatility Rise...

Passage of time...

Dividends Rise...

Long Underlying Increase No effect No effect No effect Increase

Short Underlying Decrease No effect No effect No effect Decrease

Long Call Increase Increase Increase Decrease Decrease

Short Call Decrease Decrease Decrease Increase Increase

Long Put Decrease Decrease Increase Decrease Increase

Short Put Increase Increase Decrease Increase Decrease

www.excellatrader.com

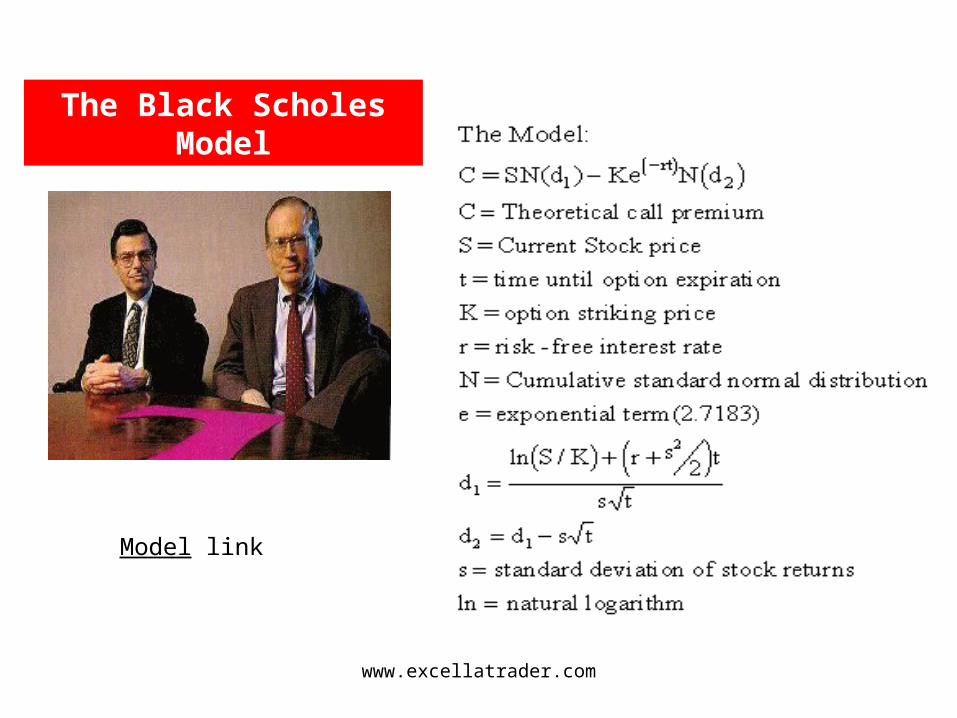

The Black Scholes Model

Model link

www.excellatrader.com

Option strategies

www.excellatrader.com

SYNTHETIC LONG CALL: BUY STOCK, BUY PUT

Mr. XYZ is bullish about ABC Ltd stock.

He buys ABC Ltd. at current market price of Rs. 4000 on 4th July. To protect against fall in the price of ABC Ltd. (his risk), he buys an ABC Ltd. Put option with a strike price Rs.3900 (OTM) at a premium of Rs. 143.80 expiring on 31st July

www.excellatrader.com

Profit +

BEP Strike Price3900

Loss - Lower Higher

Stock Price

www.excellatrader.com

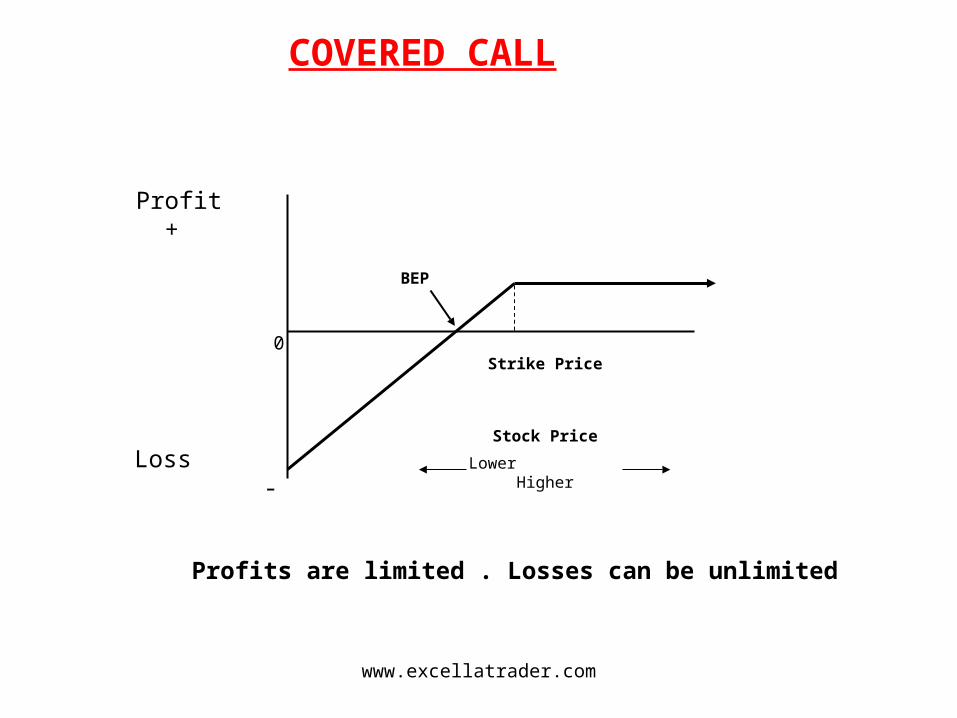

COVERED CALL

Profit +

0

Loss -

Strike Price

Stock Price

Lower Higher

BEP

Profits are limited . Losses can be unlimited

www.excellatrader.com

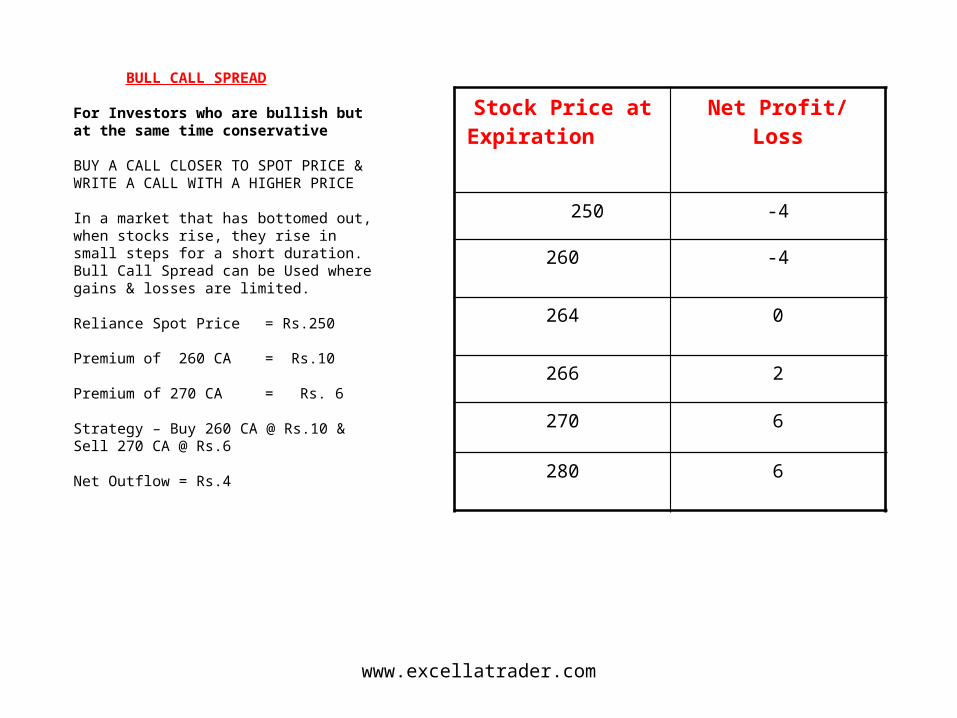

BULL CALL SPREAD For Investors who are bullish but at the same time conservative BUY A CALL CLOSER TO SPOT PRICE & WRITE A CALL WITH A HIGHER PRICE In a market that has bottomed out, when stocks rise, they rise in small steps for a short duration. Bull Call Spread can be Used where gains & losses are limited. Reliance Spot Price = Rs.250 Premium of 260 CA = Rs.10 Premium of 270 CA = Rs. 6 Strategy – Buy 260 CA @ Rs.10 & Sell 270 CA @ Rs.6 Net Outflow = Rs.4

Stock Price at Expiration

Net Profit/ Loss

250 -4

260 -4

264 0

266 2

270 6

280 6

www.excellatrader.com

Options Trading in India

Day TradersPremium SellersSpread TradersTheoretical Traders

Private Banks

Financial Institutions

Others

Public Sector Banks

Foreign Banks

www.excellatrader.com

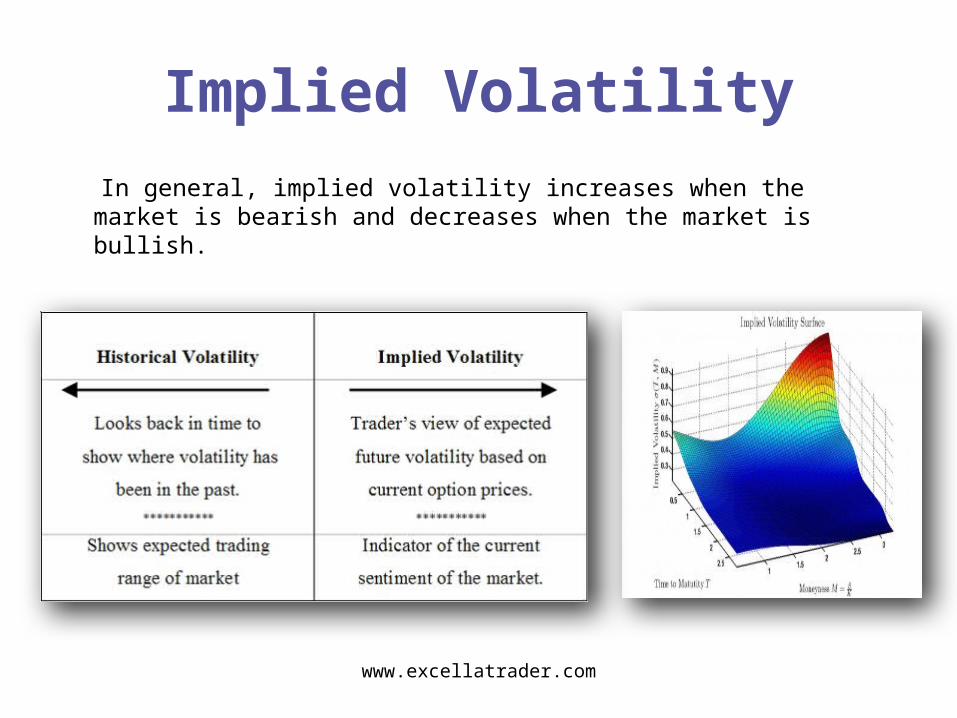

Implied Volatility

In general, implied volatility increases when the market is bearish and decreases when the market is bullish.

www.excellatrader.com

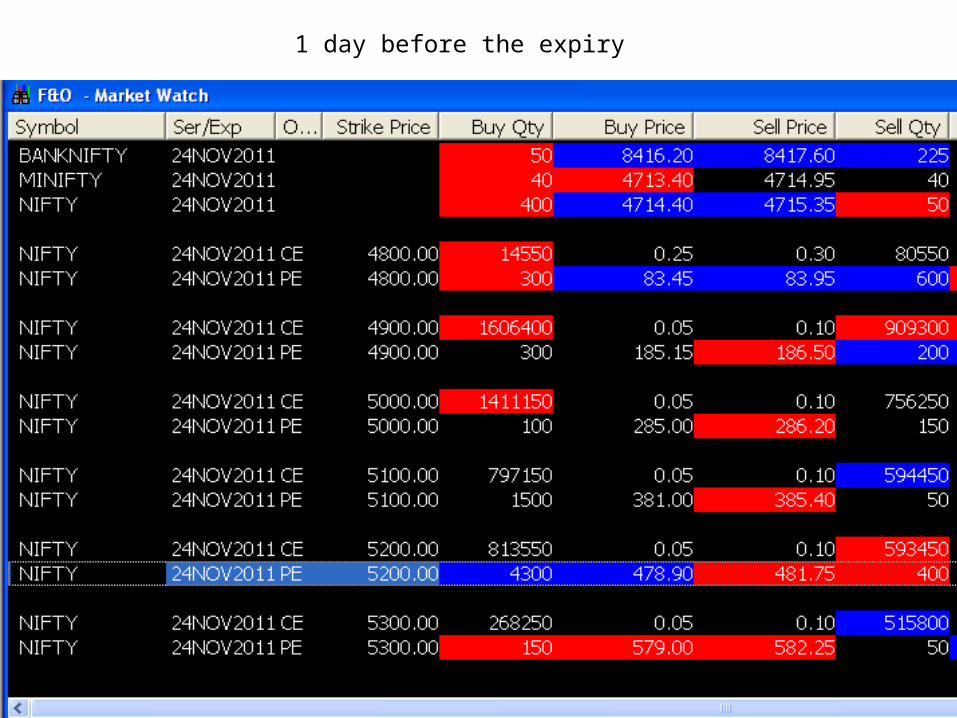

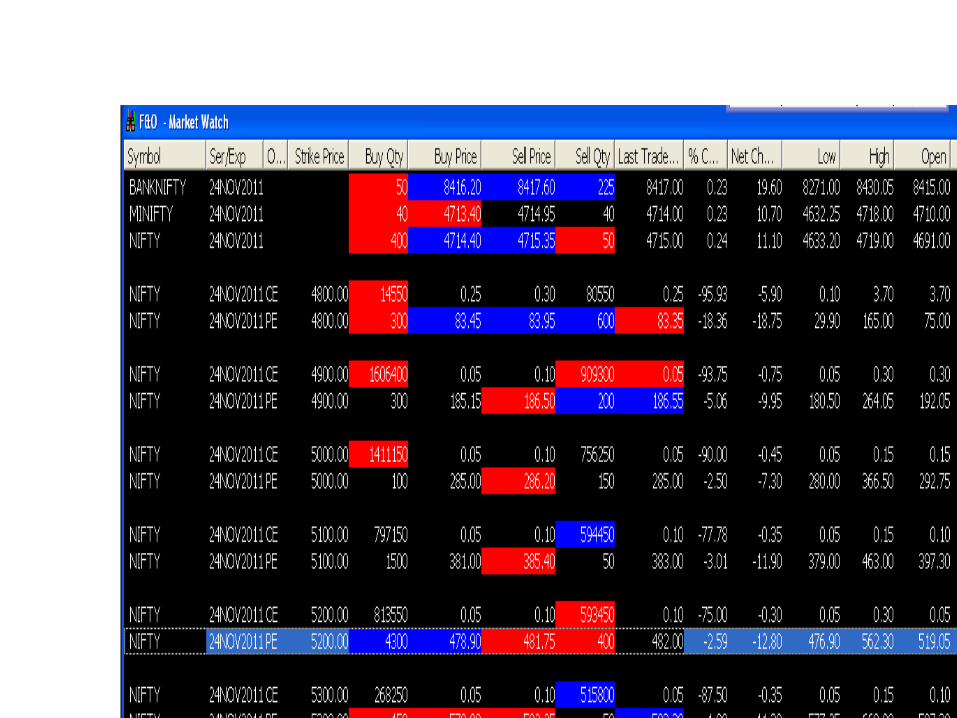

1 day before the expiry

www.excellatrader.com

www.excellatrader.com

www.excellatrader.com

www.excellatrader.com

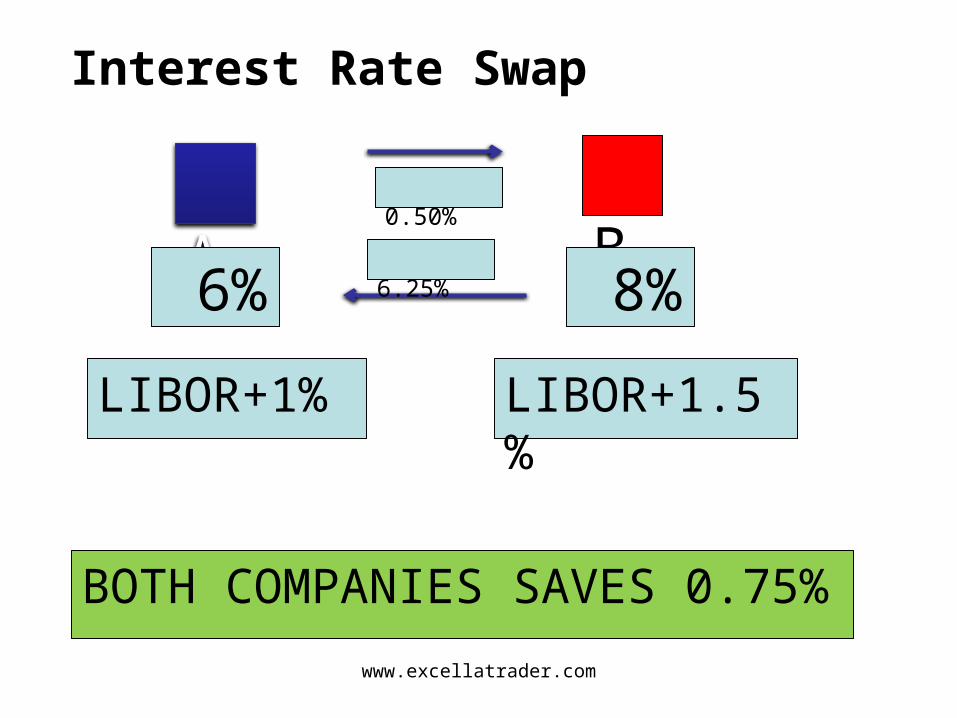

Interest Rate Swap

A B

6%

LIBOR+1% LIBOR+1.5%

8% 6.25%

0.50%

BOTH COMPANIES SAVES 0.75%

www.excellatrader.com

Triangular Arbitrage

suppose you have $1 million and you are provided with the following exchange rates:

EUR/USD = 0.8631, EUR/GBP = 1.4600 USD/GBP = 1.6939.

With these exchange rates there is an arbitrage opportunity:

Sell dollars for euros: $1 million x 0.8631 = 863,100 eurosSell euros for pounds: 863,100/1.4600 = 591,164.40 poundsSell pounds for dollars: 591,164.40 x 1.6939 = $1,001,373 dollars

$1,001,373 - $1,000,000 = $1,373