exchange rate management in ghanapdf.usaid.gov/pdf_docs/pnabq007.pdf · · 2011-01-13the auction...

TRANSCRIPT

FEBRUARY 1993

WORKING PAPER 38

Exchange Rate Management in Ghana

Stephen D Younger

CORNELL FOOD AND NUTRITION POLICY PROGRAM

EXCHANGE RATE MANAGEMENT IN GHANA

Stephen D Younger

This paper has benefited greatly from helpful discussions at the Bank of Ghana and the Non-Performing Assets Recovery Trust In particular Stephen Ameyaw Acting Director of Research at the Bank of Ghana and Edward Asare Manager at NPART went out of their way to cl3rify my understanding of certain key issues in exchange rate policy Patrick Connolly Chad Leechor Jeff Lewis Malcolm McPherson and Jon Walters also made helpful comments I owe special thanks to Clifford Zinnes and EE Walden whose comments and conversaticns during the writing of this paper greatly improved the final product I am grateshyful for financial support from USAID under cooperative agreement PDC-0095-Z-O0shy9053-00 with HIID

The Cornell Food and Nutrition Policy Program (CFNPP) was created in 1988 within the Division of Nutritional Sciences College of Human Ecology Cornall University to undertake research training and technical assistance in food and nutrition policy with emphasis on developing countries

CFNPP is served by an advisory committee of faculty from the Division of Nutritional Sciences College of Human Ecology the Departments of Agricultural Economics Nutrition City and Regional Planning Rural Sociology and from the Cornell Institute for International Food Agriculture and Development Graduate students and faculty from these units sometimes collaborate with CFNPP on specific project- The CFNPP professional staff includes nutritionists economists and anthropologists

CFNPP is unded by several donors including the Agency for International Development the World Bank UNICEF the United States Department of Agriculture the New York State Department of Health The Thrasher Research Fund and individual country governments

Preparation of this document was financed by the US Agency for International Development under USAID Cooperative Agreement AFR 000-A-0-8045-000 and USAID Cooperative Agreement PDC-0095-Z-00-9053-O0 with HIID

copy 1993 Cornell Food and Nutrition Policy Program ISBN 1-56401-138-0

This Working Paper series provides a vehicle for vapid and informal reporting of results from CFNPP research Some of the findings may be preliminary and subject to further analysis

This document was word processed by Precious Muheret The manuscript was edited by Elizabeth Mercadc The text was formatted by Jan Zeilic and Gaudencio Dizon The cover was produced by Jake Smith

For information about ordering this manuscript and other working papers in the series contact

CFNPP Publications Department 308 Savage Hall

Cornell University Ithaca NY 14853 607-255-8093

CONTENTS

LIST OF TABLES iv

LIST OF FIGURES v

LIST OF ABBREVIATIONS vi

1 INTRODUCTION 1

2 HYSTORY OF EXCHANGE RATE POLICY IN GHANA 4

The Auction Market 7 The Interbank Market 12 The Bureau Market 17

3 EVALUATION OF THE EXCHANGE REFORMS UNDER ERP 19

Gradualism vs Shock Therapy 25

4 POLICY OPTIONS 27

Objectives for Exchange Rate Policy 27 The Economic Environment for Exchange Rate Policy in Ghana 28 Choice of an Exchange Rate Regime -Considerations

An Undervalued Exchange Rate Capital Account Convertibility

Choice of an Exchange Rate Regime shyfor Ghana

Capital Account Convertibility

5 CONCLUSIONS 41

REFERENCES

Some General 29 34 35

Specific Considerations 36 39

43

LIST OF TABLES

1 - Macroeconomic Indicators for Ghana 1983-1991 9

2 - Aid Indicators for Ghana and Sub-Saharan Africa 10

3 - Export and Import Values and Volumes for Ghana 20

4 Firms Debts to NPART Resulting from Loans Denominated-

in Foreign Currency (millions of cedis) 24

5 - Ghanas Real Effective Exchange Rate (REER) (1980=100) 33

-ivshy

LIST OF FIGURES

1 - Exchange Rates and Consumer Prices in Ghana 1982-1992 8

2 - Exchange Rates and Consumer Prices in Ghana 1988-1992 14

3 - Taxes as a Proportion of GDP in Ghana 22

-Vshy

ABBREVIATIONS

NLC National Liberation Council

OGL Open General License

NRC National Redemption Council

PNDC Provisional National Defense Council

ERP Economic Recovery Program

RIC Reconstruction Import Credits

NPART Non-Performing Assets Recovery Trust

SOE State Owned Enterprise

EMS European Monetary System

LDC Less Developed Countries

-vishy

1 INTRODUCTION

The history of exchange rate management in Ghana is one of the richest and most interesting inAfrica Before most African countries had established their own currencies a balance of payments crisis inGhana provoked an adverse terms of trade shock and expansionary aggregate demand policies At its nadir Ghanas exchange rate was overvalued by more than 3000 percent and the governmentcontrolled foreign trade with a complex set of trade and exchange restrictions On the other hand Ghana has embarked on an ambitious set of foreign exchange reforms in the past 10 years to the extent that the cedi is now virtually a convertible currpncy This wide range of experiences with different trade and exchange regimes makes Ghana a good case to include in this study

Before embarking on our examination of exchange rate management in Ghana it is important to fix the terms of the discussion In the academic literature on exchange rate policies economists write hundreds of papers a year most of them debating whether or under what conditions fixed exchange rates are preferable to floating exchange rates This debate is a longstanding one and it remains unresolved with eminent economists on both sides of the issue Yet that same group of economists if asked whether a developing country should devalue its exchange rate in response to a balance of payments crisis would overwhelmingly say yes What accounts for this difference Why would a significant proportion of economists view the Netherlands rigid peg to the detitschmark favorably but encourage Ghana to vary its exchange rate

The academic literature is directed largely toward the concerns of the Western industrial economies where international transactions are unencumbered by import licensing exchange controls etc In this context economists and policymakers understand that to maintain a fixed exchange rate a country such as the Netherlands must subordinate its monetary policy to the goal of defendingthe exchange rate In particular the Netherlands must be willing to pursue a contractionary monetary policy inthe face of reserve losses if it does not wish to devalue This policy is sometimes called the classical medicine since it can be unpleasant but necessary to maintain the fixed exchange rate Indeed some of the fixed vs flexible exchange rate debate revolves around the tradeoff between the costs of classical medicine vs those of a devaluation

Many developing countries on the other hand have been unwilling to accepteither devaluation or contractionary demand policies Instead they have responded to balance of payments problems by taking direct control of the supplyof foreign exchange through surrender requirements and then imposing a varietyof restrictions on the access to that foreign exchange including import licensing and quota restrictions on imports These policies do succeed in defending the exchange rate but at the cost of sacrificing the benefits of free international trade and suffering the arbitrary allocations of foreign

-2shy

exchange (and the accompanying rent-seeking) that control systems often entail Free trade isone issue on which economists generally agree and this agreement explains their widespread support for devaluation in a typical developing country with balance of payments problems any country that wishes to relax or remove its foreign exchange rationing scheme must devalue to eliminate excess demand for foreign exchange Because economists so strongly oppose exchange restrictions they favor devaluation for developing countries that use them

Of course professional economists argue strongly both for and against perfectly free trade But it is important to recognize that the merit of both arguments rests on certain strategic considerations either economic -- such as the infant industries argument - or political - such as the need to maintain certain industries in the interest of national defense Mot trade protection in developing countries however has come about for quite different reasons to defend the balance of payments position without devaluing the currency2

This is especially true of foreign exchanqe controls which serve no useful strategic purpose

There are then two distinct issues that one might address concerning exchange rate management The first is in an environment free of exchange restrictions on the current account how and to what extent should the authorities intervene inthe foreign exchange market The second issue concprns the desirability of exchange and trade restrictions in defending an exchange rate The answer to the first question can vary between the extremes of a rigidly fixed exchange rate (where the monetary authorities must intervene regularly and sometimes heavily via sales and purchases of foreign exchange) and a perfectly floating rate (where there is no intervention whatsoever) I have already noted that economists do not have a uniform opinion on this matter On the second however they maintain a much stronger consensus In situations where a country maintains exchange and trade controls to defend its balance of payments position it is preferable to eliminate those controls while devaluing the exchange rate to absorb the excess demand for foreign exchange In these cases the question of interest is how can a country best unwind its restrictive regime

I Itisalso possible at least intheory to contract domestic demand through a tight monetary policy But the size of the contraction would be so overwhelmshying inmost cases that this policy isnot practically feasible

2 This characteristic of trade and exchange controls indeveldping countries

was an important finding of the National Bureau of Economic Research studies directed by Bhagwati and Krueger inthe early 1970s Ghana was included inthose studies arid Leith (i974) provides an excellent account of trade and exchange policy in Ghana

3 We will discuss the capital account later in the paper

-3-

It is useful to distinguish between two broad concerns in exchange rate management the generally accepted importance of unwinding exchange controls and other restrictions to current account transactions and the difficulty in identifying an optimal exchange rate policy once the goal of current account convertibility isattained As ithappens Ghana isan interesting case on both counts Over the past ten years the government has gradually dismantled a complex system of trade and exchange controls to the point that no foreign exchange restrictions for current account transactions and only a few trade restrictions remain in place all for non-economic reasons Ghana provides then an example of how a country has fared under extensive trade liberalization accompanied by large devaluations of the exchange rate At the same time Ghana now faces the more traditional questions of exchange rate management such as the choice between fixed or flexible exchange rates and the degree of capital account convertibility it should allow This case study addresses both of these issues first describing Ghanas liberalization experience and then considering the type of exchange rate management that might be appropriate from this point forward

-4shy

2 HISTORY OF EXCHANGE RATE POLICY IN GHANA

From independence in 1957 through the early 1980s Ghanas exchange rate policy followed a pattern much like that of other African economies Immediately after independence Ghana had an open economy - exports were 28 percent of GDP - and foreign exchange reserves equal to 13 months of merchandise importsGhana was part of the sterling area and thus had the same exchange restrictions as Great Britain Within the sterling area there were few restrictions on current or capital account transactions Imports and exports had to be licensedbut the licenses were granted automatically without need for prior approvalwithin the sterling area Even outside the area current account restrictions were mild the most important being the mandatory surrender of export proceedswithin six months of the sale and prior approval for invisible and capital account transfers

As early as 1960 however the balance of payments came under increasing pressure from expansionary aggregate demand policies at home and declining cocoa prices in the international markets Ghana responded in a typical fashion byborrowing as much as it could trying (mostly unsuccessfully) to stabilize aggregate demand and increasingly turning to trade restrictions and foreignexchange controls in response to the excess demand for foreign currency In 1961 the government first expanded application of the exchange controls that had been used for nonsterling area countries to the sterling area as well Thus all exporters had to surrender their foreign exchange within six months and all invisible and capital account transactions required approval Later that same year the government took even stronger measures virtually scrapping the systemof Open General Import Licenses and replacing itwith a requirement that almost all imports receive prior approval via a Specific License Throughout this crisis the government was reluctant to devalue but by 1965 it was forced to ask its foreign creditors to reschedule its debts and the creditors in turn insisted that the government reach an agreement with the IMF Itdid so but the military overthrew Nkrumah in February of 1966 before the agreement could be signed

Inmany ways the experiences of 1961-1966 were pivotal for Ghanas future trade and exchange rate policies First use of the exchange rate as a constructive policy instrument was shunned a pattern that plagued Ghana for two decades Second the exchange and trade controls that were used instead of a devaluation to address the balance of payments problems brought with them a budding bureaucracy to impose the controls and manage foreign exchange That bureaucracy quickly learned the value of the licenses that 4t controlled and

-5shy

began to extract some of the rents soon after the system was in place4 Once installed the bureaucracy did not completely release its grip on the licensing system until 1989

The military government that overthrew Nkrumah the National Liberation Council (NLC) took stronger orthodox policy measures than its predecessor devaluing the exchange rate by 43 percent improving tax revenues and tightening up government expenditures This government also succeeded in renegotiating Ghanas medium-term debts At the same time the NLC began to relax the tight import controls of the last Nkrumah years moving items from the Specific License list to the Open General License (OGL) list Busias civilian government elected to succeed the NLC in 1969 continued these more conservative policies But a second sharp decline incocoa prices together with a continuation of the import liberalization that brought 59 percent of imports to the OGL list by the end of 1970 put strong pressure on foreign exchange reserves The government again sought help from its creditors who insisted on a devaluation The government acquiesced inDecember of 1971 devaluing the cedi by 80 percent Two weeks later General Acheampongs National Redemption Council (NRC) overthrew the Busia government

The NRC not only reversed much of the Busia governments devaluation by rolling the value of the cedi back to 128 cedis per dollar from 182 the military jailed many civil servants and politicians who they viewed as being resporsible for the devaluation and sharply condemned the influence of foreign advisors (including the World Bank and IMF) in the Busia government This strongly nationalistic position made itpolitically impossible for Acheampong to devalue later in his tenure Instead the NRC adopted a strategy of extensive government controls including renewed tightening of the import licensing system (which was immediately necessary after the revaluation) nationalization of many businesses (especially those with foreign ownership) and extensive price controls in response to the acceleration of inflation that came with a rapidly expanding public sector deficit

For the first three years of its reign Acheampongs government managed to make the control system work at least inthe sense that the macroeconomy did not explode but it was aided by high international cocoa prices and a temporary suspension of foreign debt service Beginning in 1975 however Ghana began a dramatic 10-ycar economic slide that saw real per capita income fall by a third International cocoa prices returned to more normal levels creditors forced renewed payment of foreign debt service under a rescheduling agreement government spending ballooned in a campaign to promote industrialization through investments in state-owned enterprises inflation accelerated and exceeded 100 percent during the drought of 1977 a rate unheard of inWest Africa Obviously the exchange rate became extremely overvalued and the import licensing system

4 As early as 1963 corruption in the granting of import licenses was a serious problem (see Leith 1974 for a discussion) Indeed in the debates over import controls that persisted through the 1960s corruption seems to have been a more influential criticism than the loss of exchange convertibility

-6shy

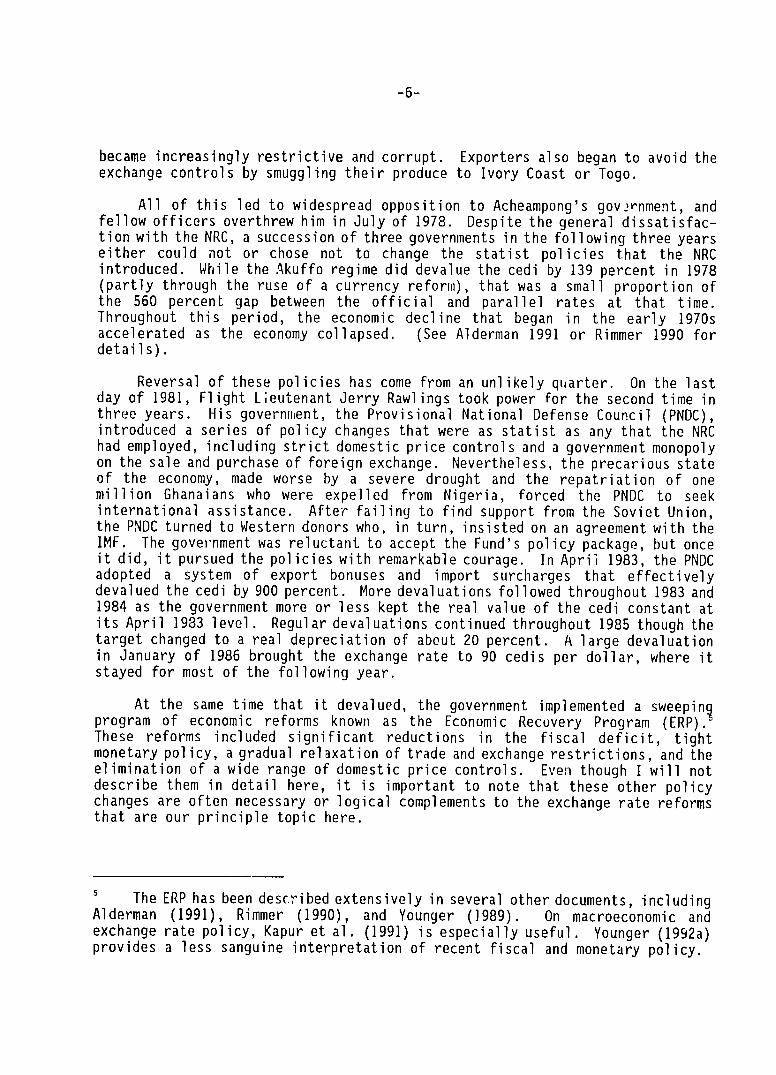

became increasingly restrictive and corrupt Exporters also began to avoid the exchange controls by smuggling their produce to Ivory Coast or Togo

All of this led to widespread opposition to Acheampongs gov2rnment and fellow officers overthrew him inJuly of 1978 Despite the general dissatisfacshytion with the NRC a succession of three governments inthe following three years either could not or chose not to change the statist policies that the NRC introduced While the Akuffo regime did devalue the cedi by 139 percent in 1978 (partly through the ruse of a currency reform) that was a small proportion of the 560 percent gap between the official and parallel rates at that time Throughout this period the economic decline that began in the early 1970s accelerated as the economy collapsed (See Alderman 1991 or Rimmer 1990 for details)

Reversal of these policies has come from an unlikely qiiarter On the last day of 1981 Flight Lieutenant Jerry Rawlings took power for the second time in three years His government the Provisional National Defense Council (PNDC) introduced a series of policy changes that were as statist as any that the NRC had employed including strict domestic price controls and a government monopoly on the sale and purchase of foreign exchange Nevertheless the precarious state of the economy made worse by a severe drought and the repatriation of one million Ghanaians who were expelled from Nigeria forced the PNDC to seek international assistance After failing to find support from the Soviet Union the PNDC turned to Western donors who inturn insisted on an agreement with the IMF The government was reluctant to accept the Funds policy package but once itdid itpursued the policies with remarkable courage InApril 1983 the PNDC adopted a system of export bonuses and import surcharges that effectively devalued the cedi by 900 percent More devaluations followed throughout 1983 and 1984 as the government more or less kept the real value of the cedi constant at its April 1983 level Regular devaluations continued throughout 1985 though the target changed to a real depreciation of about 20 percent A large devaluation in January of 1986 brought the exchange rate to 90 cedis per dollar where it stayed for most of the following year

At the same time that it devalued the government implemented a sweeping program of economic reforms known as the Economic Recovery Program (ERP) These reforms included significant reductions in the fiscal deficit tight monetary policy a gradual relaxation of trade and exchange restrictions and the elimination of a wide range of domestic price controls Even though I will not describe them in detail here it is important to note that these other policy changes are often necessary or logical complements to the exchange rate reforms that are our principle topic here

The ERP has been described extensively inseveral other documents including Alderman (1991) Rimmer (1990) and Younger (1989) On macroeconomic and exchange rate policy Kapur et al (1991) isespecially useful Younger (1992a) provides a less sanguine interpretation of recent fiscal and monetary policy

5

-7-

Through the entire reform period the Bank of Ghana has been the main seller of foreign exchange inGhana The Bank dispenses the proceeds of foreign loans and the government maintained foreign exchange srrender requirements for exporters until last year That isexporters had to sell their foreign exchange earnings to the Bank of Ghana at the marginal auction exchange rate In many cases however exporters are allowed to retain a part of the foreign exchange earnings for their own use inpurchasing imports These funds can be deposited indollar-denominated accounts inGhanaian commercial banks This type of bonus for exporters has a long history in Ghana but the government greatly increased the proportion of export receipts that could be allocated to retention accounts in the early years of the ERP as a means of improving exporters earnings and guaranteeing their access to foreign exchange As the reforms progressed the amount that some exporters could retain was reduced forcing them into the auction market although exporters of nontraditional goods are still allowed 35 percent retention

Despite the substantial devaluations that took place from 1983 to 1986 the cedi remained overvalued during the mid-1980s as evidenced by the substantial premium inthe parallel market (see Figure 1) Thus the government maintained a system of import licensing to -uppress the demand for foreign exchange trying only to streamline the cumbersome bureaucratic procedures and clarify the rules for allocating foreign exchange This was made easier by the increased inflows of foreign exchange that accompanied the new policies After the drought ended exports began to recover (Table 1) an the governments vigor in pursuing more responsible macroeconomic policy began to attract considerable support from the donor community which had shunned Ghana in the late 1970s (Table 2) These inflows eased the foreign exchange constraint allowing a significant increase in imports that were used to reconstruct the economy

Even though the PNDC government has usually made good policy moves ithas not always done so enthusiastically There isa real sense inwhich the Bank and Fund have coaxed the government along with the carrot of international financial support But as the foreign exchange situation improved in the mid-1980s the governments bargaining position vis-a-vis the Bank and Fund improved The government showed reluctance to devalue further after January 1986 (Fiscal and monetary policy however remained tight The PNDC government has always been convinced of the importance of fiscal prudence even if it has not accepted the importance of free market capitalism) The government eventually broke the impasse with the IMF by agreeing to adopt a second foreign exchange window whose exchange rate would be determined in an auction

THE AUCTION MARKET

Initially the auction market functioned as a second window source of foreign exchange The government maintained a first window for several key items - cocoa petroleum some pharmaceuticals and debt service - at the 90 cedis per dollar exchange rate that prevailed after January 1986 The auction was open to most importers of raw materials and intermediate goods including capital

-8-

Figure 1 - Exchange Rates and Constimer Prices in Ghana 1982-1992

1000 1000

100 11

L S 100 (D

o

0 100 C

_

1982 1984 1986 1988 1990 1992 1983 1985 1987 1989 1991

Date

-

--

CP I Official Auction

Bureau Buy---Bureau Sell Parallel

Table 1 - Macroeconomic Indicators for Ghana 1983-1991

1983 1984 1985 1986 1987 1988 1989 1990 1991

Annual Percentage Change Unless Otherwise Specified

Real GDP -46 86 51 52 48 56 51 33 60

Consumer price inde (end of period) 1424 60 195 333 342 266 305 359 103

Exports fob -277 291 116 185 100 69 -82 110 109

Imports fob -151 233 90 93 273 61 15 226 48

Real effective exchange rate -328 -614 -273 -425 -229 -43 -58 -02 36

Net domestic assets of the Banking System 444 843 771 498 118 85 -107 -196 -42

Credit to the government 674 152 85 44 -86 -74 -77 -88 -177

Credit to the rest of the economy -229 630 357 144 165 60 60 126 94

Broad money 381 721 95 537 530 430 269 180 151

Velocity (M2GDP) 013 013 016 017 018 018 017 015 014

In percent of GDP

Gross investment 37 69 96 97 134 142 155 160 165

Surplus or deficit (-) -27 -18 -22 01 05 04 07 02 16

Overall surplus or deficit (-)b -27 -23 -30 -33 -24 -2A -21 -24 -16

Current account balance -08 -10 -25 -15 -21 -17 -18 -46 -34

External debt outstanding 97 264 341 465 637 580 552 563 577

Debt service 07 33 58 67 108 125 98 64 51

Source Kapur et al (1991)

Excluding capital outlays finance through external project aid Including capital expenditure financed through external project aid

Including official grants

Table 2 - Aid Indicators for Ghana and Sub-Saharan Africa

Item 1980 1981 1982 1983 1984 1985 1986 1987 1988 1989 1990 1991

Official Development Assistance (millions of US$)

Including MF

Excluding IMF

197 166

166 178

192 197

359 100

490 276

259 137

257 24

315 340

336 382

416 412

456 504

646 565

ODAGDP

Evaluated at Official Exchange Rate (percent)

Including IMF Excluding IMF

13 11

06 07

06 06

17 05

65 37

41 22

45 42

65 70

65 74

79 78

78 86

101 88

Evaluated at Parallel Exchange Rate (percent)

Including IMF Excluding IMF

73 62

60 64

137 141

149 42

175 99

99 52

93 87

90 97

81 92

96 95

86 96

110 96

-11shy

equipment but not consumer goods The market was a retail market inthe sense that all bids had to come from specific importers who had both an import license and guaranteed cedi cover from their bank The Bank of Ghana accepted bids once a week under a Dutch auction system Even though the exchange rate was technically free to float in this system the Bank of Ghana in fact maintained exchange rate targets and adjusted the amount of foreign exchange itsold ineach weeks auction in order to hit those targets

During the 18 months after the auction began the system underwent several important changes Almost immediately after its inception the guvernment liberalized the import licensing system so that all nonconsumer imports were granted a license (and the right to bid for foreign exchange at the auction) automatically no quotas were set for the number or quantity rf licenses In February of 1987 the auction absorbed the official market (still at 90 cedis per dollar) and the marginal auction rate became the official exchange rate used to value export receipts and aid inflows All nonconsumer goods importers could now bid for foreign exchange in the auction6 Throughout the year broad categories of consumer goods were allowed access to the auction so that by 1988 virtually all imports of voods and most services had access to the auction This made the import licensing system obsolete and the government abolished it in January of 1989

Movements inthe auction exchange rate were rather smooth during this periodof enlarged access to the official foreign exchange auction The government met the increased demand for foreign exchange from its own sources (largely increases in foreign aid) and as the auction rate approached the parallel rate in later years by reducing some exporters right to foreign exchange retention forcing them to sell at the auction rate The government also let the exchange rate depreciate smoothly in real terms in the first few months of the auction after which it tried to keep the real exchange rate (measured against a basket of currencies) roughly constant

The next major development in the official exchange rate market came in April of 1990 when the government converted the auction from a retail to a wholesale market The Bank of Ghana discontinued the direct sale of foreign exchange to end users and instead accepted bids only from authorized dealeshybanks These institutions were then allowed to bid for any amount of foreign exchange in the auction provided the final customer to whom the dealer sold foreign exchange used it for approved transactions7 In addition authorized dealers were permitted to trade foreign exchange among themselves The

6 Public sector importers did not bid inthe auction but after February 1987 they did purchase all foreign exchange at the marginal auction rate The government financed these imports with foreign exchange itreceived from foreign borrowing and grants as well as some cocoa revenues

7 Basically these were all current account transactions Most capital account transactions still do not have access to the official foreign exchange market

-12shy

responsibility for documenting the customers use of foreign exchange now falls on the dealer bank rather than the Bank of Ghana This incombination with the removal of the few remaining restrictions on current account transactions meant that the cedi became a convertible currency

InJune of 1991 the Bank of Ghana stepped back from its central position in the foreign exchange market by allowing exporters except COCOBOD (the sole exporter of cocoa) and the gold mining companies to surrender their foreign exchange earnings to authorized dealer banks rather than itself8 Then in March of 1992 the Bank of Ghana terminated the auction system entirely turning over the allocation of foreign exchange to the interbank market

THE INTERBANK MARKET

The government launched the interbank market in the spring of 1992 While the Bank of Ghana has permitted interbank foreign exchange transactions since April 1990 the focus of the market remained the auction mostly because exporters were required to surrender their foreigi exchange to the central bank for resale in the auction Those surrender requirements were actually relaxed inJune 1991 so the closing of the auction last March has more importance as a symbol of the Bank of Ghanas stepping back from its central position in the foreign exchange market than it has actual policy content As long as the central bank sells its foreign exchange at a competitive rate the exact form of the sale - jction or intervention inthe interbank market - isnot important The most recent reforms have included one important policy charge however Until the closing of the auction the regulations required commercial banks to pay the marginal auction rate (the official exchange rate) for all export aceipts during the following week Since April 1992 however the authorities have permitted exporters to negotiate whatever rate they can with the commercial banks While the banks did not bid aggressively for foreign exchange in the early months of the new market it now appears that competition for exporting clients has piced up9

Nevertheles the new interbank market has not found its sea legs to date A variety of problems some due to the markets novelty and others to governmentpolicy have imneded the smooth functioning of this market Even though this is an interbank i3rket foreign exchange transactions between banks are extremely

a COCOBOD is the only entity allowed to sell cocoa overseas Because it is

a state-owned marketing agency its surrender requirement is moot The goldmining companies have special arrangements inwhich they are allowed to retain varying percentages of their export revenues in dollar-denominated accounts either abroad or in Ghana the remainder is surrendered to Bank of Ghana

It appears that banks maintained the old practice of paying the official exchange rate until July or August when the Bank of Ghana issued a circular encouraging exporters to negotiate for better rates

9

-13shy

rare One commercial bank has not made a single interbank transaction since April 1992 Thus the market that should provide smooth transfers of foreignexchange from exporters to importers isat present probably less liquid than the auction that preceded it0 Importers complain that the banks sometimes do not have foreign exchange to sell but the exchange rate does not rise to clear this apparent excess demand

Variouis factors seem to be behind this lack of transactions Itmay simplyreflect some uncertainty on the part of the banks about how they should operateinthe new market (The money market had a similar lack of activity when itwas inaugurated but trading picked up within a few months) Inaddition seasonal factors have probably led to the perceived scarcity of foreign exchange under the new system since the summer months generally have lower export sales than the rest of the year But there are policy problems as well First the Bank of Ghana tightly limits each banks foreign exchangc exposure the limits for all banks sum te only US$ 4 million (about 3 percent of one months imports) This restriction essentially forces the foreign exchange market to equilibrate on a flow basis foreign exchange that flows in from export receipts must flow out as import aemand at exactly the same time (or within a week) because the banks have very little foreign exchange of their own with which to provideliquidity to the market This flow equilibrium is a very difficult condition to satisfy Export proceeds and importers demands do not flow smoothly inconstant amounts per week but rather are lumpy Normally one function of dealer banks is to buy up export receipts when exporters wish to sell and hold them until an importer wishes to buy To do this they must hold liquid balances of foreignexchange perhaps for some extended period if export receipts do not come inat the same time that importers want to use them Without this intertemporalsmoothing by banks une might expect the exchange rate to gyrate wildly because the supply and demand wiould rarely match at exactly the same time But infact the exchange rate has depeciated smoothly since the interbank market beganoperations (Figure 2) Itappears that the banks are treating importers demands for foreign exchange as orders to be filled when supplies are available rather than spot demands Importers do not always get their foreign exchange at the moment they request it instead their bankers put them in a queue to purchase foreign exchange when it becomes available Under this arrangement the waitingtime rather than the exchange rate absorbs short-term fluctuations inthe flow excess demand for foreign exchange

10 It is not clear that this situation isdue to the switch from an auction to an interbank market Macroeconomic conditions have been such that foreignexchange has been particularly scarce in the past few months and this security rather than the change inmarket structure may be behind the lack of liquidity

11 This limit applies to balances above and beyond the banks commitments to supply foreign exchange to importers Qualifying commitments include letters of credit which guarantee foreign exchange payment for a Ghanaian importer to his or her supplier and the following weeks demands from importers who have contracted to pay their suppliers on a collection basis

-14-

Figure 2 - Exchange Rates and Consumer Prices inGhana 1988-1992

600- 600

550 -550

500- 500

450 -450

400- - 400UII 350 -350

c) 300 300 2)00- -200 shy

2 5 0 -1 of2 50

150 -150

100 100

1988 1989 1990 1991 1992

Date

CPI Auction Bureau Buy

SBureau Sell Interbank

-15-

The queues clearly serve the commercial banks interests in the sense that they reduce the probability that a bank will end up with a stock of foreign exchange that itmust unload at a loss inorder to stay under its exposure limit The pent-up demand for foreign exchange allows the banks to sell extra foreign exchange receipts quickly Nevertheless one wonders why importers are willing to wait to purchase foreign exchange Waiting involves a variety of costs including exchange rate risk (the price for foreign exchange sales isnot settled until the sale actually occurs) interest charges on suppliers credits and perhaps their suppliers good will if payment is delayed To some extent the banks queuing system helps to minimize these costs by establishing priorities for importers who have outstanding letters of credit who have been waiting a long time or who have a suppliers credit about to come due But the real problem comes from a second policy of the Bank of Ghana foreign exchange dealers are not allowed to make more than I percent profit on any foreign exchange transaction Inthe short run this restriction makes itimpossible for an importer to jump the queue by offering a higher rate for existing supplies of foreign exchange the banks cannot sell it at that higher rate Whats more banks cannot quickly gain access to larger supplies of foreign exchange by increasing their offer rate Unlike a foreign exchange market inthe West there are (by law) no stocks of foreign exchange that traders can draw down or build up quickly in response to price changes Instead the supply must come entirely from increasing the flow of export receipts which cannot be very responsive in the short run Insum the combination of a limit on trading profits and foreign exchange exposure appears to determine that the equilibrium will involve queuing on the part of importers making itappear that there is excess demand in the foreign exchange market

Of course neither of these restrictions prevents banks from competing for export clients by offering higher exchange rates that are then passed on to their importers In fact competition for export clients has been heavy in recent months and the exchange rate has depreciated considerably (Figure 2) albeit more smoothly and slowly than one might have expected But the exchange rate is only one factor inthat competition Banks offer exporters a variety of services (financing document processing international transfers) and competition for export clients occurs along each of these fronts Infact until recently banks continued to pay the official exchange rate - the average cf the previous days interbank transactions - to their exporters as they had done during the auction so competition occurred exclusively in the realm of other services Furthermore the link between the foreign exchange sale and these other services makes itdifficult for an exporter to quickly change her sale to another bank in response to a change in the exchange rate All the other paperwork must be

These restrictions also account for the lack of trading between banks Any

bank with an inflow of export receipts basically must choose between satisfying its own clients and making I percent and satisfying another banks demands to make the same 1 percent Given that each bank has a queue the preference for satisfying ones own clients is obvious

12

-16shy

carried along with the foreign exchange and that fixed cost adds a certain stickiness to the market

Another explanation for the lack of foreign exchange trading between banks and the persistence of importers queues lies inthe Bank of Ghanas intervention strategy The Bank of Ghana appears to have taken the opportunity that the change in market structure presented to wean the commercial banks from relying on it as a source of foreign exchange The central bank remains a net seller of foreign exchange only because receipts from cocoa gold and program aid are lirger than the governments foreign exchange demands The Bank of Ghana isnot irtervening in the market to defend any particular exchange rate and its sales are not based on competitive bidding Rather the Bank decides how much foreignexchange itwould like to sell in a week based on its target for reserve holdingsand market conditions and then sells that amount to commercial banks that approach it based on the central banks perception of the purchasers need for foreign exchange to satisfy its clients Need appears to depend on the amount of export receipts and import demands that a particular banks clients providerather than the price it is willing to bid since the central bank sells its foreign exchange at an average of the previous days interbank rates The Bank of Ghana does deny requests for foreign exchange ifthe requesting bank does notneed it and the commercial banks cannot reverse that decision by bidding a higher rate

While a policy of limited foreign exchange intervention (ie a floatingexchange rate) is certainly defensible this particular strategy may help to explain why banks are reluctant to buy and sell foreign exchange to each other Banks with a large number of export clients can reasonably expect the Bank of Ghana to refuse tieir requests for forign exchange and will therefore be reluctant to release toreign exchange that they might need for their own clients On th2 other hand bnks with fcw export clients can go to the Bank of Ghana and plead their case of need for fceign exchange rather than trying to bid itaway

3from other banks with offers of higher exchange rates If the Bank respondsto this type of request it effectively usurps normal interbank transactions In sum Bank of Ghana interventions inthe foreign exchange market are now less competitive and more arbitrary than they were during the auction This is a significant step backwards in the development of the foreign exchange markets

The novelty of the interbank market and the paucity of data from itmake it difficult to weigh the importance of each of the problems I have discussed Nevertheless ifthe market isto function normally itseems clea that the Bankof Ghana should raise the limit on foreign exchange exposure for dealer banksabandon the I percent rule and begin to sell its foreign exchange competitivelyoperating as any other market participant would While some limit on the banks exposure is necessary to prevent de facto capital account convertibility the current limit is far too low The Bank of Ghana might arrive at a more reascnable limit by looking at the variance inexport receipts and import demands

13 In any case the 1 percent rule on profits makes this difficult to do inthe short run

-17shy

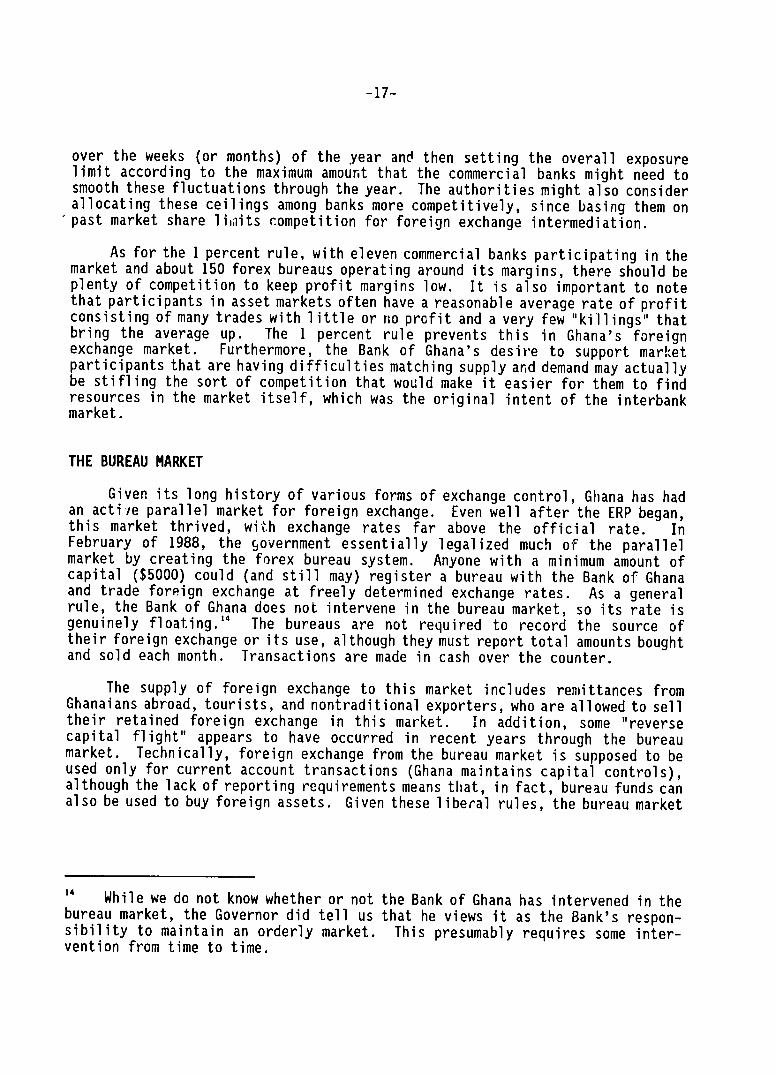

over the weeks (or months) of the year and then setting the overall exposurelimit according to the maximum amount that the commercial banks might need to smooth these fluctuations through the year The authorities might also consider allocating these ceilings among banks more competitively since basing them onpast market share liaits competition for foreign exchange intermediation

As for the 1percent rule with eleven commercial banks participating inthe market and about 150 forex bureaus operating around its margins there should be plenty of competition to keep profit margins low It is also important to note that participants inasset markets often have a reasonable average rate of profitconsisting of many trades with little or no profit and a very few killings that bring the average up The 1 percent rule prevents this in Ghanas foreignexchange market Furthermore the Bank of Ghanas desire to support market participants that are having difficulties matching supply and demand may actuallybe stifling the sort of competition that would make it easier for them to find resources in the market itself which was the original intent of the interbank market

THE BUREAU MARKET

Given its long history of various forms of exchange control Ghana has had an actie parallel market for foreign exchange Even well after the ERP beganthis market thrived with exchange rates far above the official rate In February of 1988 the government essentially legalized much of the parallelmarket by creating the forex bureau system Anyone with a minimum amount of capital ($5000) could (and still may) register a bureau with the Bank of Ghana and trade foreign exchange at freely determined exchange rates As a generalrule the Bank of Ghana does not intervene inthe bureau market so its rate is genuinely floating4 The bureaus are not required to record the source of their foreign exchange or its use although they must report total amounts boughtand sold each month Transactions are made in cash over the counter

The supply of foreign exchange to this market includes remittances from Ghanaians abroad tourists and nontraditional exporters who are allowed to sell their retained foreign exchange in this market in addition some reverse capital flight appears to have occurred in recent years through the bureau market Technically foreign exchange from the bureau market is supposed to be used only for current account transactions (Ghana maintains capital controls)although the lack of reporting requirements means that infact bureau funds can also be used to buy foreign assets Given these liberal rules the bureau market

While we do not know whether or not the Bank of Ghana has intervened inthe bureau market the Governor did tell us that he views it as the Banks responshysibility to maintain an orderly market This presumably requires some intershyvention from time to time

14

-18shy

has marginalized the once-thriving parallel market for foreign exchange in Ghana 15

When the bureau market first opened there was a large spread between the exchange rates in that market and the auction market but it narrowed to insignificant levels by mid-1991 After an initial period of rapid depreciation the bureau rate began to fluctuate around 3q0 cedis per dollar for nearly two years The steady expansion of access to tne auction market and the increased sales of foreign exchange there contributed to this stability as did increased repatriation of funds held abroad Meanwhile the auction rate depreciated steadily so that the two have been quite close in the past year

As the authorities work out the kinks inthe interbank market that market is likely to squeeze the operations of the bureaus During the operation of the auction imports continued to be financed through the bureaus even after all imports were allowed access to the auction Purchasing foreign exchange in the bureaus requi-ed no bank cover no prior approval and less paperwork than bidding in the auction and this added convenience determined a premium for the bureau exchange rate 6 As the commercial banks learn to manage the documentashytion associated with interbank exchange rate purchases more deftly for their customers the premium on the bureau rate should decline and the banks will regain some of the importers business At the same time the traditional suppliers of foreign exchange to the bureau market (Ghanaians abroad and nontraditional exporters) will probably find that the convenience of dealing with a bank including wire transfers and the ability to credit and debit accounts without handling cash outweighs the small margin they could receive at the bureaus Itseems likely then that the bureau market as we know itwill shrink to a marginal retail market for small-scale transactors inmuch the same way that the former parallel market did after the introduction of the bureaus

15 While many former black market traders have opened bureaus a few still operate outside the legal markets mostly attracting a market of small-scale traders by shaving a cedi or two off the margins that the bureaus maintain

16 Note that once the auction rate approached the bureau rate in 1991 the

latter began to move up with the auction rate after having been stable for a long period On the one hand exporters with partial retention rights probably began to find it more convenient to sell all their export receipts to their bankers to avoid the extra transaction cost of taking their allowed retention to the bureaus for only a slightly higher price That reduces the supply of funds to the bureaus On the other hand some importers probably began to shift their demand to the bureau market to avoid the auction paperwork once the rates drew close

17 Note however that at least one bureau has opened an office in the US to transfer remittances to Ghana

LwaLqojd Sq4 J0 S~skL2Uueup oJ (eZ661) 485un0A aaS 46L4 SajeJ 4S3JaUL pue a~aps uaaq sPq 41aj se aouewjojjad 4UOWISaAU 44flq seq uo~4e~jUL A--O 04 pansind 4i[od Ae~auow 446[4 aq1 4Ua4Xa aW05 01

asuas Owos ul (Q a~qej) S~seq ejdeo jad e uO Pp d09 JO uo440d04d e se q~oq S6aA4ufl0 Ue3D~4V Aaqj0 Xq P8A0364 aSOq4 44[M 8ULL ut A~q~fl04 842 smOLJ Ne~ 4uaj4n3 s~eueqg aaow s4eqM SA~S8AJ9S6euetyxa u6A~ao64j UL paleinwn)e sw4 uOILLL~w OM~ -A40uP Pp dd3 a44 04 JOLAd P4e[LnwflJJ2 peq I41 5428442 a84Lla4 04 PasSfleM aSMOJUL l2q4 JO UOL[~w OSV$ 4P41 040u Os[2 Isnw auo - 1661 UU0L[~q VS 04 pound861 UL UO4[ Z$ wo44 umoj6 seq jqop U568404 - smO[4 Pe UL 85284DU a~qeAapsuo) paABAJ Seq 4UaWUJAo6 Bq4 jeqj MAI4 SL 41 aIM pansAnd Seq IUaWU48A05 44 J41~ SaLOLLd aqj upq4 4Oqj24 smO[4 pe PaSea4OU 04 aouew40448d paAojdw seueqq) o4fl All 01 ejtL sA44)L2448 s~dHi] 8q1 X4Mpo aAnpoid sRjjufl0) aqj 40 6U4244qeqa4 UL OL[04 amp8j 2 pake~d aA2eq 4qqM (2 a~qq) eueqg 04 5440d 40 mOLJ Pdeu A4[LeUesqls 2 p844wiad aAeq aDUP45SSP

U5aJo4 UL OSPJDfU 06-4[ e 41M p8u~qw0J sSuu~ea 4iodxa Aafiuo4S

i(dH3 aqj 0 asuodsaj sialiodna JO M8AL4 aAsj3qa4dwoo 2 apAAd Z661 2Lea unqar) dH3 aqj 6uJp kLpdpa IABA UMOAf5 aAeq qOLqM s4Jtodx 12u04PeJ4uOu w044 awo seq safiueqo 8424 aflueqoxa aq4 o4 asuadsaA 5u5noou 450w aqj sdeqAad -(E a [qej) s[8Aa[ LeOL404S 4Sq4[ 48ql 04 Ufl464 04 jaA aAeq Ruem q~no44e s0861 i(Lle aq uL SMOL 4J8q4 W044j N[qepSUOD Pa48A0284 aAeq sjj0dx8 LeuOM4PP44 Is0w SUO4)2SuPJI [eUO42U484U 404 SV

(I a[qei) SLAL a~qeuoseaA 04 um0P 8w0) fi~mLs[Sseq U042[4ulA(4[3edP3 8A4mnpoid Leuo4PPe jo juatudo~aAap 0q ueq A44eA4 ndlno 40 k6AOJad

SL 64ep 04 PaSS8UIM aAeq aM qjM045 aqj J 4 qnw lpq4 aAaL[8q 04 Ouo 6upeaLqlm046 OL~W0U038 484Sej ALJP 04 mOL 004 SU2Wa4 JUaWjS8AUj SOa44ufo asoqj M44q Le48q[L aaoW UaAa sdeq48d pup) 04 4eL[WmS MOU SL OWLA AJLod s~eupqgjq~noqj UaAa S8W0U00a U2SV fiUM04 AR[pdA aqj 40 sajPA aqj mo~aq SU~ema 4[ 4flq 4Aeea oa 4uai4d S4fl0q2 42 PLOs uaaq seq4 dag 40 qim045 L[24AA padoq aAeq lq5m aulo ueq paounouoid ssaiL aae sipak( 01 Ised aqj Up9SSaU4M seq eUP49 I44 s4UWOAo~id a4 40 amos q6n4[e [LnjssaJns R~qeuoseaj uaaq seq dH3 4l 004 a8H Xw0u0~a 8If124s R~L2)mU0J804JW 6UMOAS RLPded 2 fiUdoLAap 404 sluawn4su Lnjasn jaqjej 4nq UL LeOf 40 84saA[8swaql 40 Pp SP0 s9)L40d asaqj asjflJ joJ SUO4344584 4uflo~o 4U844fJ LL2 iX[LefjL4A PaA0Wa4 seq IUOmU18A06 a44 81M pound861 anUs 4Uaj48d 06 Rq p84eJ84Ad~p seq 8424 6ueqi)xo aA4)j844 L~ aqj -qu044 a~ueqixa pupeA a4q4 uo papaaoons se dU3 aqj jeq4 jqnop E)[44IL L ) squawn44SU L X L[Ld aq4 Xw0u0J8 Palua40-4alA2wAE)44 40 [6Aa L a44 IV aAt448dWOJ 6Udo~aAaP 42 pOW2 S4P44 wPf504Ad i(48A0)a 3[WOUO0J3AJ 46421 4l 40 442ed 842u jUod SLq 04 passnSLp SW40484 ape41 PUP 06Ueq)Xa aqj

M~iH3UN SWH0O33H 39NVH3X3 3HI A0 NOIIVfl1VA3 E

-61shy

Table 3 - Export and Import Values and Volumes for Ghana

Itemi 1983 1984 1985 1986 1987 1988 1989 1990 1991

Cocoa beans (US$ m) Volume (metric tons)

Unit value (US$ton)

242 159280 1520

352 149574 2351

376 171747

2189

470 195224 2406

451 197

2278

422 200904

2102

381 255860 1490

324 247380

1309

320 246200

1300

Cocoa products CUSS m) Volume (metric tons) Unit value (US$ton)

27 15000 1767

30 15265 1965

36 15956 2256

34 15645 2141

44 20893 2125

40 20250 1965

26 14940 1767

37 20756 1773

33 25000 1300

Gold CUSS m) Volume (fine ounces) Unit value (US$ounce)

114 278000

410

103 286759

360

91 285138

318

106 292211

364

140 323496

432

169 382993

440

160 420096

381

202 526361

383

301 835340

360

Diamonds (US$ m) Volume (carats) Unit value (US$carat)

28 439000

64

28 425035

66

55 639593

86

48 564950

85

40 396720

101

35 305787

114

52 262691

198

165 636371

259

179 650000

275

Bauxite (US$ m) Volume (metric tons) Unit value (US$ton)

15 82000

183

09 45000

200

27 124453

217

50 226461

221

52 226415

230

69 299939

230

91 374646

243

100 368629

271

94 340000

276

Manganese CUSS m) 31 83 90 82 78 88 117 142 165 Volume (metric tons) Unit value (US$ton)

127000 244

247780 335

263441 342

245794 334

235123 332

282337 312

284645 411

255310 556

300000 550

Timber (US$ m) Volume Ccubic meters) Unit value (US$cubic m)

15 103303

142

21 148252

143

28 246812

113

44 291382

151

90 493543

182

106 545778

195

80 375826

213

118 370000

319

125 396500

316

Electricity (US$ m) 12 21 35 46 49 74 83 87 91

Nontraditional CUSS m) 10 36 75 44 96 309 310 567 600

Total exports (US$ m) 749 749 749 749 824 881 808 895 993

Trade indices C1985=100)

ExportsPrice index Volume index Value index

86 81 69

109 83 90

100 100 100

107 111 119

110 119 130

105 133 139

87 147 128

90 157 142

88 180 157

Imports Price index Volume index Value index

105 71 74

102 90 92

100 100 100

95 111 106

106 128 136

111 129 144

111 131 146

126 142 179

128 147 188

Terms of trade 82 106 100 113 104 94 78 71 68

-21shy

then we have witnessed a recovery of aid flows to normal levels rather than an extraordinary commitment to Ghana

Even though a common objection to strong devaluations isthat they may cause inflation for the most part this has not been the case in Ghana As one can see from Figure 1 there were substantial devaluations of the official exchange rate in the early years of the ERP yet consumer prices did not move with those devaluations In a more formal test Younger (1992) uses time series techniques on monthly Ghanaian data to investigate the impact of devaluations on inflation during the period 1974-1986 when exchange controls were severe That work finds that the effect is small oh the order of 5-10 percent for a 100 percentdevaluation The reason for this is that when foreign exchange is severely rationed its marginal value is reflected in the parallel rate rather than the official market and changes inthe official rate tend only to squeeze the rents that importers earned on their rationed foreign exchange rather than the prices that they charge

Another concern about devaluation is its effect on the governments fiscal pcsition Some authors (eg Edwards 1989) have argued that devaluation can raise the local currency value of the governments expenditures for impu- Es and especially for debt service forcing it to finance that extra expenditure byprinting money (borrowing from the banking system) thus driving prices up and forcing another devaluation to compensate the price increase and so on To date this has not been the case In fact the fiscal situation has improvedbecause of the devaluations Tax revenues from trade taxes increase with the devaluation since the taxes are mostly ad valorem taxes based on the cedi value of the goods and import demand is highly inelastic under quantity rationing Figure 3 shows the sharp increase in trade tax revenues (including the implicit tax on cocoa exports) in the early years of the ERP when devaluations were largest At the same time governments purchases of imports (apart from those financed by foreign aid) are very small and the government has received enough new capital (foreign aid denominated in foreign exchange) to cover its debt servicing Thus devaluation has not caused fiscal problems in Ghana

The devaluations have however caused problems inGhana for firms that held liabilities denominated in foreign exchange before the devaluations While Ghanaian firms generally could not find financing abroad in Foreign currencies because of the country risk the government used several credits from donors to provide import financing to industrial firms in different sectors in the early years of the ERP I do not know whether the firms bore the foreign exchange risk on these loans except in the case of two Reconstruction Import Credits (RICs) from the World Bank The Banks articles of agreement prevent it from acceptingforeign exchange risk so some domestic agent must do so In the case of the RICs the government set the terms of on-lending to importers such that the borrowing firm did not bear all of the foreign exchange risk but neither were the loans risk-free Each loan was converted from dollars (or other foreigncurrency) into cedis at the official exchange rate at the time of disbursement rather than at the time of the loan agreement Disbursement was sometimes drawn out over long periods of time (up to two years) and the exchange rate was charging by huge amounts during this period so some firms suffered large

-22-

Figure 3 - Taxes as a Proportion of GDP in Ghana

016

Non-Tax Revenues

C

v

012

006

004shy

002shy

-- -__

~Income

Domestic IndirectI Trade Taxes

amp Property

000shy1980 1982 1984 1986 1988 1990

1981 1983 1985 197 1989 1991

Year

-23shy

increases in the cedi value of their liabilities While the book value of the corresponding asset also rose its economic valiie often did not leaving the firm with a loss large enough to wipe out its net worth 9 Since Ghana has no clearly established bankruptcy proceedings there are few possibilities for a financial workout for the affected firms At the same time foreclosure is a difficult legal process in Ghana so creditors often have not claimed their debtors assets to resell them The affected firms end up in a state of limbo with little incentive to invest their own funds inthe operation because profitsfrom the investment and even the nvestment funds themselves could be claimed by the firms creditors In addition creditors will not generally lend more funds to a bankrupt company Thus a firm may continue to operate at a reduced level with its existing assets or itmay shut down entirely but itwill surely not invest or grow20

It isdifficult to evaluate the quantitative importance of this phenomenonOn the one hand the large size of the discrete devaluations and the amount of money lent to firms inforeign exchange under various donor programs suggest that the problem could be severe For example if we consider just the World Banks two RICs and assume that 80 percent of the total amount of these credits (US$ 40 million and US$ 87 million for 1983 and 1985 respectively) was on-lent to firmsthen the implied amount of credit (converted to cedis at the end-cF-year exchange rate for each loan) is51 billion or 20 percent of all outstanding credit from the banking system to private firms and state-owned enterprises (SOEs) While the RICs were especially large programs they were not unique so the total amount of this type of credit issomewhat higher Unfortunately it isdifficult to find details of the terms and amounts of other loans that may have gone to firms

Another source of information is the Non-Performing Assets Recovery Trust (NPART) Ghanas analog to the Resolution Trust Corporation inthe United States NPART has taken most of the commercial banks bad loans off the banks books and replaced them with government bonds thus cleaning up the financial institutions

19 Technically the assets value to the firm will increase by an amount equalto the depreciation of the nominal exchange rate only if the stream of income that flows from the asset increases by the same amount This could happen ifthe firm were exporting its production since the devaluation would affect the firms income stream (which is in dollars for an exporter) he same way it affects its liability The income stream could also increase if the 1rice of the good the firm sells changed in proportion with the cedi value of its debt Given the strong real depreciation of the cedi during this period it is unlikely that this happened for firms who were not exporting a large portion of their output 20 The problem is analogous to the investment disincentive for countries that suffer from a debt crisis since there isno bankruptcy court for these countries either For example Froot (1989) and (Rogoff 1990) discuss the market failure responsible for low investment in heavily indebted countries

-24-

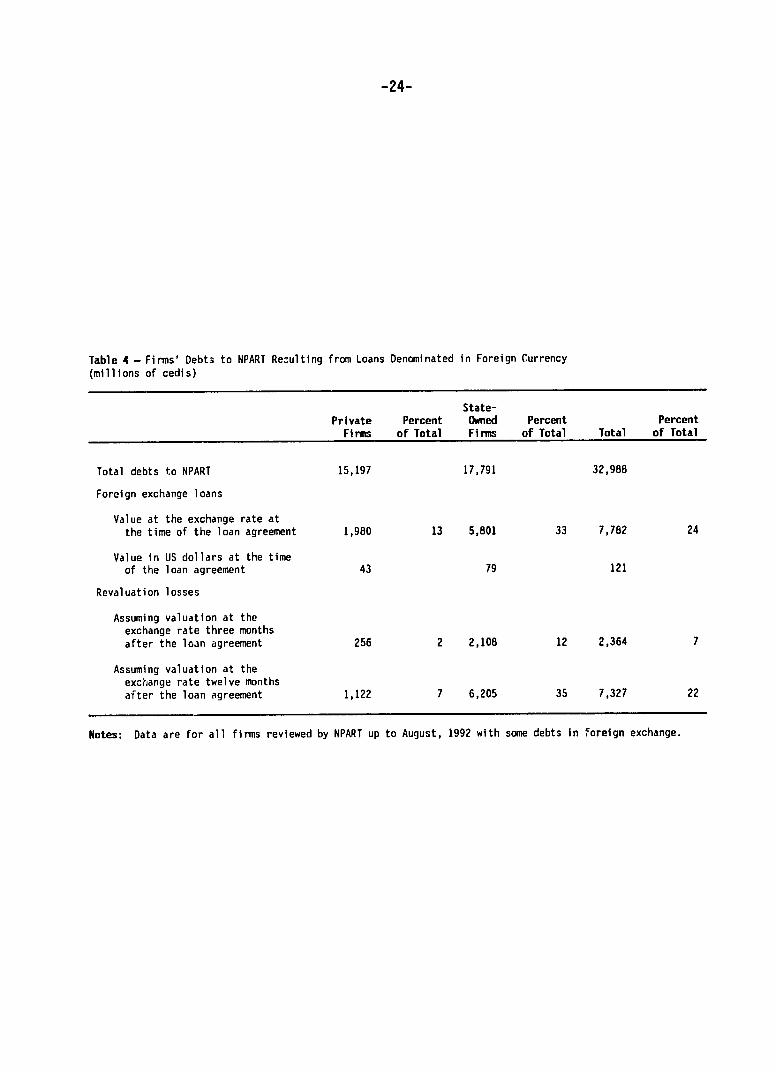

Table 4 - Firms Debts to NPART Rezulting from Loans Denominated in Foreign Currency (millions of cedis)

State-Private Percent Owned Percent Percent Firms of Total Fisrm of Total Total of Total

Total debts to NPART 15197 17791 32988

Foreign exchange loans

Value at the exchange rate at the time of the loan agreement 1980 13 5801 33 7782 24

Value in US dollars at the time

of the loan agreement 43 79 121

Revaluation losses

Assuming valuation at the exchange rate three months after the loan agreement 256 2 2108 12 2364 7

Assuming valuation at the exchange rate twelve months after the loan agreement 1122 7 6205 35 7327 22

Notes Data are for all firms reviewed by NPART up to August 1992 with some debts in foreign exchange

-25shy

portfolios21 NPART is now charged with recovering as much as poscible through a special tribunal that will act as a type of bankruptcy ourt for NPART cases While NPARTs information on its debtor firms is confidential it has provided us with a summary of its firms debts in cedis and foreign currencies Table 4 shows information on the firms reviewed by NPART which had borrowed inforeignexchange For these firms which include the vast majority of the firms whose finances NPART has reviewed to date loans in foreign exchange account for 24 percent of total debts to NPART when they are evaluated at the exchange rate prevailing when the loan agreement was signed 1we assume that all of these loans had terms similar to the World Bank RICs and that they were disbursed one year after the loan agreements were signed then the corresponding revaluation losses would be 73 billion cedis or 22 percent of those firms total debts to NPART Thus while these losses are clearly an important part of distressed firms financial difficulties they are among many problems that Ghanaian firms have had in managing and servicing their debts

Another problem that one might expect from the trade and exchange reforms is that domestic firms could not easily compete with imports afte trade is liberalized Again it isdifficult to assess the quantitative impact of this problem but evaluations by the NPART and a local consultants report based on domestic resource costs suggest that many firms that are currently experiencingfinancial distress actually have reasonably good chances to compete once their balance sheets are cleaned Lip NPART has recommended that the tribunal liquidateonly 40 of the 126 firms it has analyzed to date Similarly a consultants report that reviews the financial condition of distressed firms with bad debts inexcess of 20 million cedis (about US$ 40000) found that only 9 of 68 firms are not viable in the sense that after a financial workout and with improved management and marketing practices the analysts do not believe they can function profitably Both institutions began their analysis with larger more heavilyindebted firms Thus while many firms will surely be unable to survive in the face of competing imports (and other problems) they do not appear to be an overwhelming proportion of the total

GRADUALISM VS SHOCK THERAPY

Given that Ghana devalued by 900 percent in 1983 it may seem odd to characterize its exchange rate policies as gradualist but in fact that is appropriate Ittook six years from the advent of the ERP for Ghana to eliminate all exchange controls on current account and eight years to close the gapbetween the official and parallelbureau exchange rates This raises the question of whether Ghana might not have benefited by more rapidly implementingits liberalization program There is now a wide range of opinions theon appropriate speed of adjustment and the debate is intensifying inthe context of economic reform in Eastern Europe Arguments favoring shock therapy ie

The banks have not escaped scot-free The bonds that they received carry lower-than-market interest rates I percent to 9 percent for bonds replacing loans to a private debtor and 12 percent for SOEs

21

-26shy

rapidly eliminating distortions in the economy include the common sense notion that the faster a country can eliminate inappropriate policies the more quickly itbenefits from a more efficient allocation of resources Inaddition radical policy changes may send a clear signal to the private sector that the government intends to liberalize and thus foster a more rapid response to the policy changes Finally some countries with gradualist reform programs have found them stalled after a few years as adjustment fatigue sets in and the goverrnent loses its enthusiasm for reform On the other hand a more gradualist approach to reform may avoid some of the unemployment losses that can accompany a radical change in relative prices as firms are forced to shut down Less abrupt changes may also be more politically feasible because they involve less dramatic changes in incomes and income distribution

While there are several arguments about the appropriate speed of adjustment I will review two that I have riot encountered in the academic literature One factor in favor of gradualism in Ghana is the need for institution-building Many of the reforms that make up the ERP have required not just that policies change but that new institutions be created (for example the foreign exchange bureaus) or that existing institutions change their operations dramatically The Bank of Gharia for example has evolved from an institution that directly allocated credit and foreign exchange based on planning objectives or political considerations to an institution that monitors and intervenes in private money and foreign exchange markets only in the interest of macroeconomic objectives These changes require that existing staff be retrained and that some new staff with technical skills (eg traders auditors statistical analysts) be hired all of which takes time The same is true for a variety of other public and private institutions that operate in and regulate the new markets that have sprung up Without taking the time for this institutional retooling it is doubtful that the transition to market-oriented policies would have gone as smoothly as it has in Ghana

On the other hand the debt revaluation problem I discussed inthe previous section argues for rapid exchange rate adjustment As long as the exchange rate remains overvalued someone in the local economy accepts an almost certain exchange rate loss every time the country receives a loan in foreign currency as long as the couitry sticks with the reform program donors will continue to insist on real depreciation until the exchange rate reaches equilibrium As we have seen real depreciation can cause serioJs financial problems for firms who do not anticipate it and sell their output on domestic markets On the other hand if the government accepts the risk future devaluations will cause budgetary problems as the local currency value of debt service increases with the exchange rate22 On these grounds then one might favor a rapid devaluation to a level where the authorities feel they can reasonably expect to hold the real exchange rate constant before accepting large amounts of foreign aid inthe form of loans

One could also object to the governments acceptance of foreign exchange

risk for some borrowers especially firms on equity grounds because their owners are likely to be relatively wealthy

22

-27shy

4 POLICY OPTIONS

Ghana has now achieved the goal of current account convertibility Once the kinks in the interbank market are worked out itwill be at the point where the country can and must address the exchange rate issues that are more contentious (at least among academics) should it float the exchange rate fix it rigidly or adjust it gradually If the government chooses to adjust the exchange rate regularly should itdo so according to a set of rules or should itrely on the discretion of the central bank Each of these options in turn brings with it a set of further questions concerning their potential economic effects their institutional demands and their political feasibility

OBJECTIVES FOR EXCHANGr RATE POLICY

Different governments have different goals for their exchange rate policy If import demand and export supply have any price elasticity at all in a small economy then exchange rate movements can be useful in stabilizing aggregate demand (and therefore output) On the other hand a liberalizing economy with a history of inflation may be able to bring inflation down to international rates more rapidly by using the exchange rate as a nominal anchor By pegging the exchange rate rigidly against a low inflation currency the authorities can link local prices of tradables to their international levels thus holding their rate of change (inflation) to international levels A fixed exchange rate may also help a small economy integrate itself into the world economy by reducing the riskiness of international transactions through a policy that minimizes the volatility of the real exchange rate 3 Finally some developing countries are attempting to mimic the rapid growth of the Asian economies by promoting export growth Among other policies export promotion may require exchange market intervention to maintain a relatively depreciated exchange rate that favors exports (and import substitutes)

In Ghana our conversations with the authorities suggest that their principle goals are to maintain the competitiveness of Ghanaian firms in international markets and to maintain price stability2 To these goals I would add the importance of maintaining a relatively predictable exchange rate Ghana is a small country and so must look to its trade relations with the rest

23 This is the rationale for the European Monetary System (EMS)

24 These goals may not always be consistent with one another ifmacroeconomic

policies do not complement exchange rate policy In particular if aggregate demand grows more rapidly at home than abroad the real exchange rate will become overvalued if it does not depreciate but a depreciation will hasten a rise in domestic prices

-28shy

of the world as an engine of growth The exchange rate is in especially important price in a small economy because it directly influences the relative prices that many firms and consumers face in an open economy Ghana has placed strong emphasis on getting the exchange rate right in the sense that it reflects the true scarcity value of foreign exchange in a relatively open trading environment a policy which is well-advised and should continue At the same time it is important to use the exchange rate to promote relative price stability (as opposed to nominal price stability that should be the goal of monetary policy) The exchange rate when left to float freely can move by large amounts in a short time introducing an extra element of uncertainty for Ghanaian firms who rely on imported inputs or export proceeds This uncertainty does not exist for firms that trade within the same currency area This risk if it is substantial will discourage Ghanaian firms from pursuing activities that involve them in international trade That can only be detrimental to Ghanas economic development

THE ECONOMIC ENVIRONMENT FOR EXCHANGE RATE POLICY INGHANA

The type of exchange rate policy that Ghana elects to pursue depends to a great extent on the kinds of shocks that it can expect to face Given the structure of the Ghanaian economy it is likely to suffer changes inits economic environment that are different and more severe than most industrial economies These shocks affect the foreign exchange markets inways that any policy regime should consider25

It is useful to classify disturbances in the foreign exchange market into three types short-term (daily or weekly) fluctuations in the supply or demand of foreign exchange that have to do only with the timing of different traders activities predictable seasonal fluctuations related to harvest patterns holidays etc and unpredictable shocks that might be temporary (eg a drought) or permanent (eg an increase in the money supply to finance a fiscal deficit) Before we consider possible policy responses to these shocks it is useful to describe the most important ones in greater detail Short-term fluctuations and seasonal variation are fairly straightforward and by definition temporary In general policies to respond to these shocks are equally straightforward (at least conceptually) so I will leave them for the next section A brief review of potential unpredictable shocks which could be either temporary or permanent follows

Historically the most important shock to the foreign exchange market in Ghana has been expansionary aggregate demand policies With the exception of the past few years fiscal deficits have been large and they have been financed through the banking system The resulting aggregate demand puts strong pressure

The discussion in this section assumes that the authorities maintain

controls on capital account transactions and so concentrates on how different shocks will affect the excess demand for foreign exchange coming from current account transactions only

25

-29shy

on the foreign exchange market through import demand While fiscal and monetarydiscipline have been hallmarks of the ERP itwould be imprudent to suppose that Ghana will never again suffer rxcessive aggregate demand We have to consider the impact of loose fiscal andor monetary policy on the exchange markets when deciding on an exchange rate system

Ghana is also subject to shocks over which it has no control Roughly 60 percent of exports come from cocoa and gold two commodities whose pricesfluctuate widely Inaddition petroleum comprises 15 percent of imports ThusGhana suffers strong terms of trade fluctuations (Table 3) that directly affect the foreign exchange market Ghana is also subject to periodic droughts Given that agriculture comprises about half of GDP bad rains can cause considerable macroeconomic disturbances which spill over into the foreign exchange markets through reduced supplies of cocoa and increased demand for imported food

Ghana must also be concerned with the possibility of a variety of financial and quasi-financial shocks to its foreign exchange markets First remittances from Ghanaians living abroad are an important source of foreign exchange While technically current account transactions (unrequited transfers) remittances do have a potentially speculative aspect since remitters can choose to vary the timing of their transaction depending on the perceived strength of the cedi In particular a sudden loss of confidence inthe value of the cedi (stemming sayfrom an expected depreciation) could greatly reduce the inflow of remittances thus adding further downward pressure on the cedi

On the other hand strong capital inflows could force an appreciation of the cedi To some extent this has already occurred as donors have increased their grants and loans to Ghana in support of the ERP26 In addition reformingcountries in Latin America and Asia have recently been buffeted by significantprivate capital inflows as these economies become fashionable places to invest Of course the confidence that drives these inflows can evaporate quickly and force the exchange rate to revert to its former levels often abruptly

CHOICE OF AN EXCHANGE RATE REGIME - SOME GENERAL CONSIDERATIUdS

Itseems unlikely that a floating rate would be appropriate for most African economies27 Because balance of payments shocks can be quite large and the

26 Younger (1992a) discusses this problem

27 A floating rate is a system in which the monetary authorities do not intervene inthe foreign exchange markets at all The exchange rate is free to move at any time and by any amount to balance the supply and demand for foreignexchange Some discussions of Ghanas foreign exchange policy describe the auction rate andor the interbank as floating exchange rates but that is not entirely correct During the auction the authorities regularly intervened in

(continued)

-30shy

elasticities for exports and imports are probably small28 a freely floating exchange rate is likely to be quite volatile Maintaining tight controls on capital account transactions would exacerbate this volatility because they limit the liquidity in the market to the rather tenuous adjustment of importers foreign payments discussed above To use a purely floating exchange rate regime then would probably require a significant degree of capital account convertshyibility the desirability of which I will discuss below Yet even with capital account transactions legalized a floating exchange rate would be volatile for the reasons that I have mentioned as well as the standard overshooting arguments (Dornbusch 1976)