exchange rate regimes in emerging europe - imf.org · unilateral use of the euro: kosovo,...

TRANSCRIPT

Exchange Rate Regimes in Emerging Europe

5th Regional Meeting of Governors

Umag, March 30-31, 2017

Bas B. Bakker

Senior Regional Resident Representative

for Central and Eastern Europe

Almost any type of Exchange Rate

Regime can be found in (non-CIS) CESEE

Fixed

Euro area membership: Estonia, Latvia, Lithuania, Slovak Republic, Slovenia

Unilateral use of the euro: Kosovo, Montenegro

Currency boards: Bosnia & Herzegovina, Bulgaria

Flexible

Managed arrangements: Croatia, Macedonia

Inflation targeting and floating: Albania, Czech Republic, Hungary, Poland, Romania, Serbia

2

Over time, exchange rate regimes have moved

towards either floating or very hard arrangement

3

Pros and cons exchange rate regimes:

fixed exchange rates

Supporters hard pegs argue they result in

More credibility

Lower inflation

More stable economic environment

Encourages international trade

Lower interest rates higher investment

Faster growth

4

Example: introduction of currency board

in Bulgaria

5

-20

0

20

40

60

80

100

1992 1994 1996 1998 2000 2002 2004 2006 2008 2010 2012 2014 2016

Currency board introduced

CPI inflation in Bulgaria

(Percent, 3-month annualized change)13,636

Pros and cons exchange rate regimes:

floating exchange rates

Supporters floating exchange rates argue

Under flexible exchange rate, economy has

greater ability to adjust to external trade

shocks

As they make adjustment easier, they result in

faster growth

6

Example: Poland

7

-4

-2

0

2

4

6

8

2000 2004 2008 2012 2016

80

85

90

95

100

105

110

115

120

125

130

2000 2004 2008 2012 2016

Real GDP growth

(Percent y/y)

EUR exchange rate

(Index, 2000=100)

Poland

Bulgaria

Poland

Bulgaria

Another difference: as countries get richer,

their price level increases…

8

AlbaniaBelarus

Bosnia and Herzegovina

Bulgaria

Croatia

Czech Republic

Estonia

Hungary

Latvia

Lithuania

Macedonia, FYR

Moldova

Montenegro, Rep. of Poland

Romania

Russia

Serbia

Slovak Republic

Slovenia

Turkey

Ukraine

y = 0.574x + 22.119

R² = 0.5945

20

25

30

35

40

45

50

55

60

65

70

0 10 20 30 40 50 60 70

GDP per capita, PPP-adjusted

(Percent of USA)

Pri

ce level

(Perc

en

t o

f U

SA

)

Income per capita and price level, 2016

If exchange rate is fixed, this will happen

through higher inflation

9

100

120

140

160

180

Jan-99 Jan-03 Jan-07 Jan-11 Jan-15

90

100

110

120

130

140

150

160

170

Jan-99 Jan-03 Jan-07 Jan-11 Jan-15

CPI index

(Jan-1995=100)

Exchange rates vis-à-vis EUR

(Jan-1999=100)

EST

CZE

EST

CZE

appreciation

Feasibility of exchange rate regime also

depends on whether REER is overvalued

Baltics had fixed exchange rates and rapid growth

They pegged exchange rate when wages were still very low

Other countries with limited exchange rate flexibility but higher

wages had much lower growth

10

0

2

4

6

8

10

12

14

16

18

20

1991 1995 1999 2003 2007 2011 2015

Nominal compensation per employee

(EUR thousands)

HRVEST

HUN

POLCZE

With flexible exchange rate, volatile capital flows

can lead to large fluctuations in REER

11

40

50

60

70

80

90

100

110

120

2000 2002 2004 2006 2008 2010 2012 2014 2016

Nominal and real effective exchange rate of Brazilian Real

(Indices, 2010=100)

NEER

REER

What are advantages and disadvantages

of various exchange rate regime for SEE?

What is better—fixed or flexible?

Average growth

Volatility

Ability to deal with shocks

Focus on experience in last decade and half

What are future options for SEE countries?

12

We will compare de facto exchange rate

flexibility using “fear of floating” index

13

0.0

0.2

0.4

0.6

0.8

1.0

1.2

CZE POL ROU HUN SRB HRV ALB LVA SLV MKD BGR LTU EST BiH MNE

Calvo-Reinhart “fear of floating” index, 2003-14

High flexibility Low flexibility

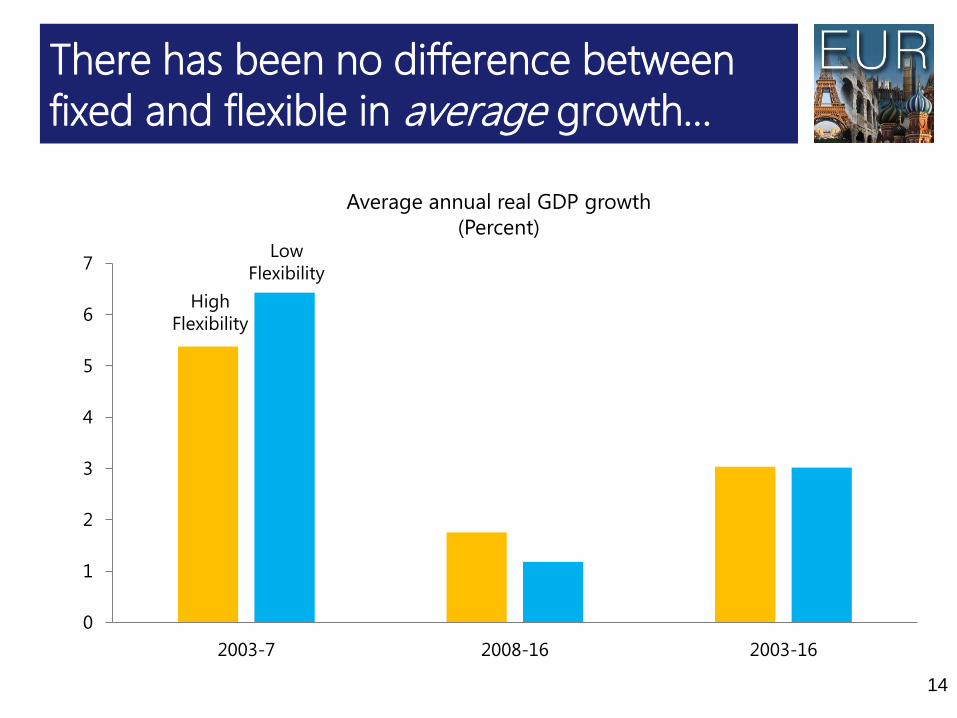

There has been no difference between

fixed and flexible in average growth…

14

0

1

2

3

4

5

6

7

2003-7 2008-16 2003-16

High

Flexibility

Low

Flexibility

Average annual real GDP growth

(Percent)

…but growth has been more volatile in

countries with fixed exchange rates…

15

-12

-10

-8

-6

-4

-2

0

2

4

6

8

10

2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016

High flexibility

Low flexibility

Average real GDP growth

(Percent)

…as was inflation.

16

-2

0

2

4

6

8

10

12

14

2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017

High flexibility

Low flexibility

Average CPI inflation

(Percent)

During boom floaters let exchange rate appreciate,

which tightened monetary conditions

17

90

95

100

105

110

115

120

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

2013

2014

2015

2016

2017

High flexibility

Low flexibility

Nominal effective exchange rate

(Index, 2002=100)

-3

-2

-1

0

1

2

3

4

5

LTU

MN

E

MK

D

BG

R

BiH

LV

A

EST

RO

U

HR

V

ALB

SR

B

PO

L

HU

N

CZ

E

SV

K

REER

Contributions to monetary conditions, 2003-07

(Percent)

Real Interest Rate

Monetary Conditions

Index

Tighter

conditions

-16

-14

-12

-10

-8

-6

-4

-2

0

2

2000 2002 2004 2006 2008 2010 2012 2014 2016

High flexibility

Low flexibility

As a result, they built up less imbalances, had less

pronounced booms, and lower current account deficits

18

Average current account balance

(Percent of GDP)

Why this difference?—during crisis

During crisis

Floaters had less

overhang from pre-

crisis boom

They could further

boost growth by

exchange rate

depreciation

19

-5

-4

-3

-2

-1

0

1

2

3

4

5

6

PO

LR

OU

SR

BK

OS

LTU

ALB

CZ

EB

GR

HR

VB

iHH

UN

SV

KM

KD

SLV

EST

MN

ELV

A

REER

Contributions to monetary conditions, 2008-10

(Percent)

Real Interest Rate

Monetary Conditions Index

Tighter

conditions

So is floating exchange rate better?

Floating may be more difficult for small

countries

Floating may be a problem with extensive

euroization (balance sheet effects)

20

Smaller countries are more likely to have

less flexible exchange rate

21

0

5

10

15

20

25

30

35

40

Population and exchange rate arrangements

(Millions of people)

High

FlexibilityLow

Flexibility

Among countries with de jure flexible

arrangements, exchange rate flexibility is higher in

larger countries

22

Poland

Romania

Czech Republic

Hungary

SerbiaCroatia

Albania

Macedonia

y = 0.0265x + 0.0156

R² = 0.75560.0

0.2

0.4

0.6

0.8

1.0

1.2

0 5 10 15 20 25 30 35 40

Population and exchange rate arrangement

Population size, 2016

(Millions)

Exc

han

ge r

ate

fle

xib

ilit

y, a

vera

ge 2

011-1

5

(Calv

o-R

ein

hart

In

dex)

Low FX flexibility is linked to

hyperinflation during transition

23

Effective Exchange Rate Flexibility and the Peak Annual Inflation during Transition

Calv

o-R

ein

hart

In

dex

(Avera

ge, 2006-0

8) Low

Inflation

(<100%)

High

Inflation

(<1000%)

Hyper-

inflation

Floating is more difficult if you have large

scale euroization

Euroization

Loan euroization

Deposit euroization

Loan and deposit euroization are not always

linked

24

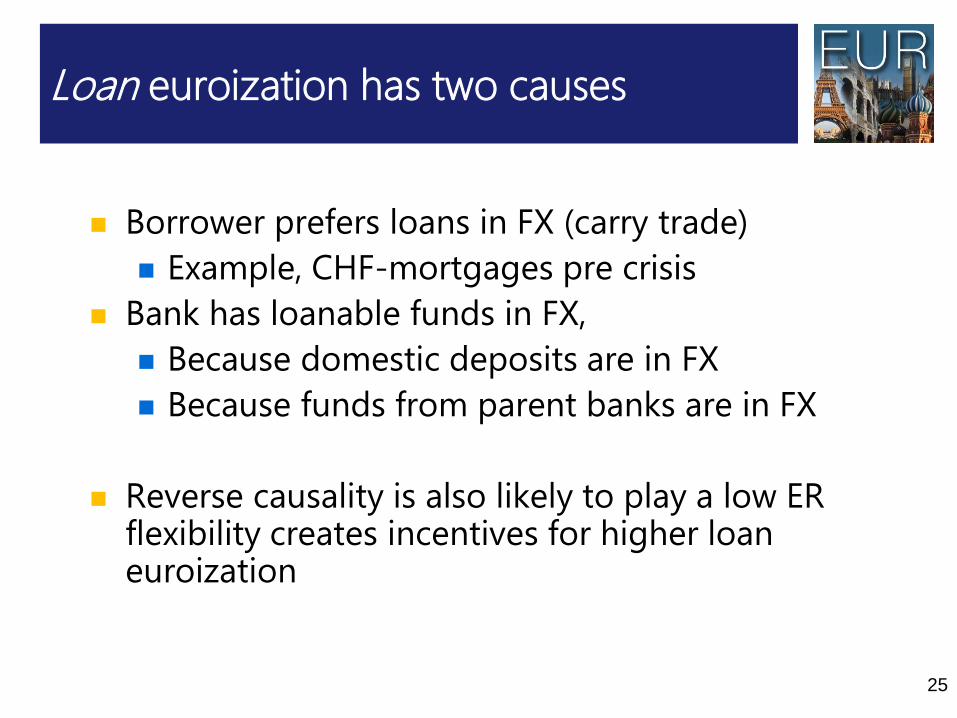

Loan euroization has two causes

Borrower prefers loans in FX (carry trade)

Example, CHF-mortgages pre crisis

Bank has loanable funds in FX,

Because domestic deposits are in FX

Because funds from parent banks are in FX

Reverse causality is also likely to play a low ER flexibility creates incentives for higher loan euroization

25

Pre-crisis, carry trade and bank funding

flows played an important role

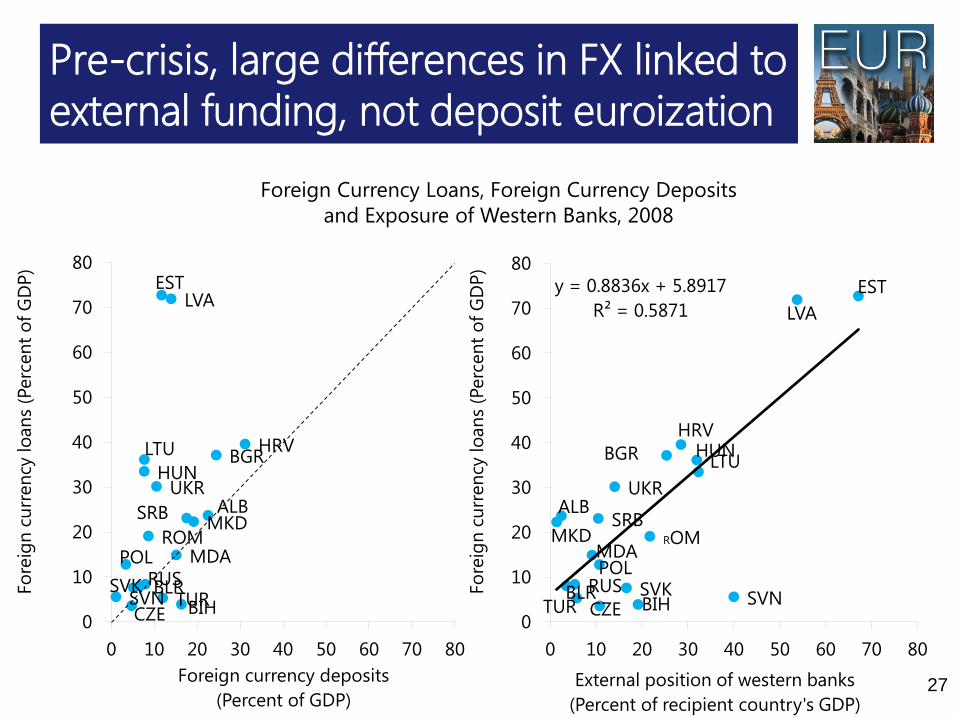

Pre-crisis loan euroization in EU New Member

States was driven by

Funding inflows from Western Banks

Carry trade

Not by excessive deposit euroization

26

Pre-crisis, large differences in FX linked to

external funding, not deposit euroization

27

Foreign Currency Loans, Foreign Currency Deposits

and Exposure of Western Banks, 2008

ALB

BLRBIH

BGRHRV

CZE

EST

HUN

LVA

LTU

MKD

MDAPOLROM

RUS

SRB

SVKSVN TUR

UKR

0

10

20

30

40

50

60

70

80

0 10 20 30 40 50 60 70 80

Fo

reig

n c

urr

en

cy lo

an

s (P

erc

en

t o

f G

DP

)

Foreign currency deposits

(Percent of GDP)

ALB

BLRBIH

BGR

HRV

CZE

EST

HUN

LVA

LTU

MKDMDAPOL

ROM

RUS

SRB

SVKSVNTUR

UKR

y = 0.8836x + 5.8917

R² = 0.5871

0

10

20

30

40

50

60

70

80

0 10 20 30 40 50 60 70 80

Fo

reig

n c

urr

en

cy lo

an

s (P

erc

en

t o

f G

DP

)

External position of western banks

(Percent of recipient country's GDP)

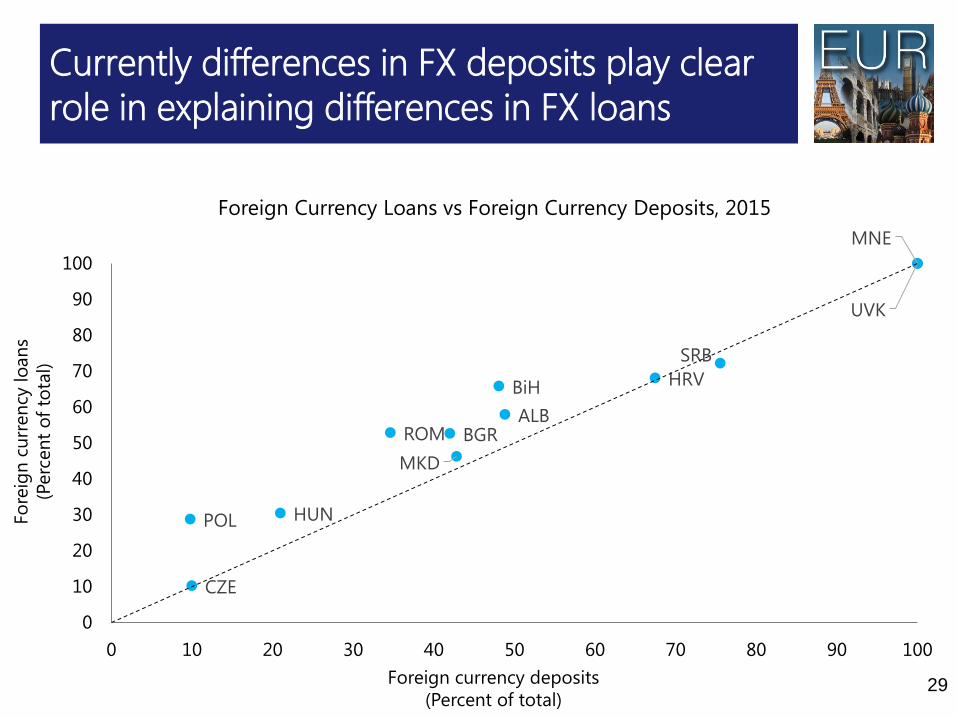

Post-crisis, drivers of FX loans have

changed

Carry trade no longer prevalent (no new Swiss

franc loans)

Bank funding flows have reversed

28

Currently differences in FX deposits play clear

role in explaining differences in FX loans

29

ALB

BiH

BGR

HRV

CZE

HUN

UVK

MKD

MNE

POL

ROM

SRB

0

10

20

30

40

50

60

70

80

90

100

0 10 20 30 40 50 60 70 80 90 100

Foreign Currency Loans vs Foreign Currency Deposits, 2015

Foreign currency deposits

(Percent of total)

Fo

reig

n c

urr

en

cy lo

an

s

(Perc

en

t o

f to

tal)

Memories of hyperinflation

(Lack of) institutional quality

ALB

BIH

BGR

HRV

CZE

ESTHUN

LVA

LTU

MKD

POL

ROU

SRB

SVK

SVN

0

20

40

60

80

-0.6 -0.1 0.4 0.9

ICRG, 2006

Higher institutional quality

R2 = 0.45

What determines deposit euroization?

30

Institutional Quality and Deposit

Euroization

Peak Annual Inflation During Transition

(Percent, logarithmic scale)

ALB

BGR

HRV

CZE

ESTHUN

LVA

LTU

MKD

POL

ROM

SRB

SVK

SVN

0

20

40

60

80

10 100 1000 10000 100000

Peak Inflation during Transition and

Deposit Euroization

FX

dep

osi

ts, 2006

(Sh

are

of

tota

l)

>100000

Exchange rate options going forward

At some point in future, SEE countries will

Have converged a lot further with Western

Europe

Are all EU members

Have adopted the euro

31

However, it may take a long time before

sufficient convergence

32

ALB

ROU

RUSPOL

UKRBIH

SRB & MNE

MKD

BLR BGR

HRV

LVA LTUHUN

SVK

EST

CZE

SVN

0

5000

10000

15000

20000

25000

30000

35000

40000

45000

50000

1950 1960 1970 1980 1990 2000 2010

GDP per capita in Germany

(Constant 2014 dollars, PPP-adjusted)

Per capita income in CESEE

countries as of 2015

What to do in the run-up to euro area

membership?

For countries with flexible exchange rates:

Little reason for strategic re-orientation.

Some floaters could gradually introduce more flexibility into their floats

For countries with fixed exchange rates, two options:

Either stick to fixed rate regime (“Baltic path”)

Or move to a flexible exchange rate regime/ inflation targeting.

33

Baltic path may be bumpy

34

-15

-10

-5

0

5

10

15

1996 2000 2004 2008 2012 2016

0

2

4

6

8

10

12

14

16

18

20

1996 2000 2004 2008 2012 2016

LTU

EST

LVA

Real GDP growth

(Percent)

Unemployment rate

(Percent)

Pre-conditions for more flexible

exchange rate

Substantial technical apparatus. (Building this

may be beyond the means of very small

economies.)

Orderly transition: uncontrolled move to (more)

floating risks de-anchoring monetary policy.

Floating requires dealing simultaneously with

euroization

35

De-euroization easiest when exchange

rate is under upward pressure

Move to flexibility difficult when depositors fear

depreciation -> risks more euroization/capital flight.

Best introduced when there are appreciation

expectations -> financial incentive for savers to move

into domestic currency.

36

Some final thoughts

Some exchange rate regimes may make it easier

to deal with particular type of shocks

But future shocks may not resemble past shocks

In 1990s, when problem was lack of

confidence in domestic currency, fixed

exchange rates helped

In 2000s, when problem was large capital

inflows, fixed exchange rate did not

37

Neither euro adoption nor free float are

panacea

Economic problems and crises can occur under

any type of exchange rate regimes

Pre-2010, we used to think that euro area

countries could not have BOP crisis

We now know this was not true

38

Further information and discussion:

39

Thank you