exchange rates chapter 8. firm in home serve foreign markets / source from abroad? stay domestic...

TRANSCRIPT

Exchange Rates

Chapter 8

Firm in Homeserve foreign markets / source from abroad?

Stay domestic

Export

Export or local production?

Import or local production?

ImportMultinational activity:

horizontalMultinational activity:

vertical

no

yes, serve foreign market

yes, source from abroad

exportlocal

productionimportlocal

production

Selling in foreign currency

Producing and selling in foreign

currency

Producing in foreign currency

Buying in foreign currency

nature of exchange rate risk nature of exchange rate risk

Figure 8.1 Exchange rates, trade and multinational activity

Exposure to exchange rate risks

• Economic exposure– Transaction risk– Translation risk

• Spot versus forward exchange rates

Table 8.1 Some international currency symbols

Country Currency Symbol ISO code Australia dollar A$ AUD Canada dollar C$ CAD China yuan CNY EMU countries euro € EUR India rupee Rs INR Iran rial RI IRR Japan yen ¥ JPY Kuwait dinar KD KWD Mexico peso Ps MXP Saudi Arabia riyal SR SAR Singapore dollar S$ SGD South Africa rand R ZAR Switzerland franc SF CHF United Kingdom pound £ GBP United States dollar $ USD

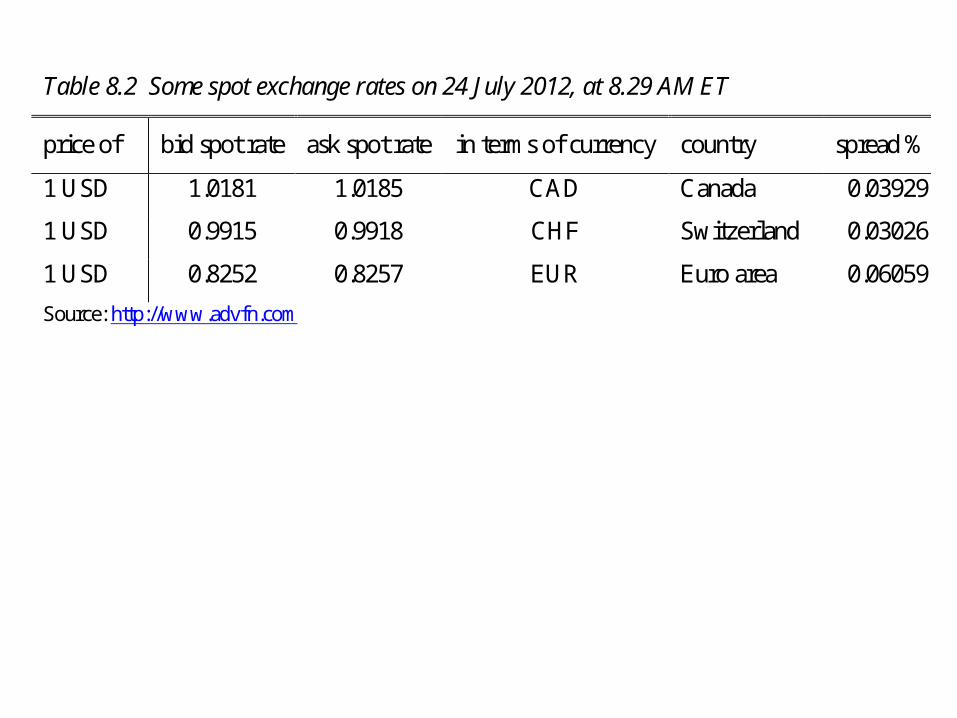

Table 8.2 Some spot exchange rates on 24 July 2012, at 8.29 AM ET

price of bid spot rate ask spot rate in terms of currency country spread %

1 USD 1.0181 1.0185 CAD Canada 0.03929

1 USD 0.9915 0.9918 CHF Switzerland 0.03026

1 USD 0.8252 0.8257 EUR Euro area 0.06059

Source: http://www.advfn.com

Figure 8.2 Some exchange rates; daily data, 2000 – 2011

Exchange rates: price of US dollar in local currency (daily rates)

0

1

2

2000 2002 2004 2006 2008 2010 2012

0

10

20

Canada; CAD/US

Switzerland; CHF/USD

S Africa; ZAR/USD(right-hand scale)

Data source: www.federalreserve.gov

Figure 8.3 Australia – USA; spot and forward exchange rates of US dollar, 1976-2011

Australia; spot and 3-month forward rates (AUD/USD)

0.7

0.9

1.1

1.3

1.5

1.7

1.9

2.1

1976 1981 1986 1991 1996 2001 2006 2011

spot

forward

Data source: IFS.

• Arbitrage (Table 8.3)

• Players and markets

• Forward exchange rates and hedging

• Trading volume (Fig. 8.4)

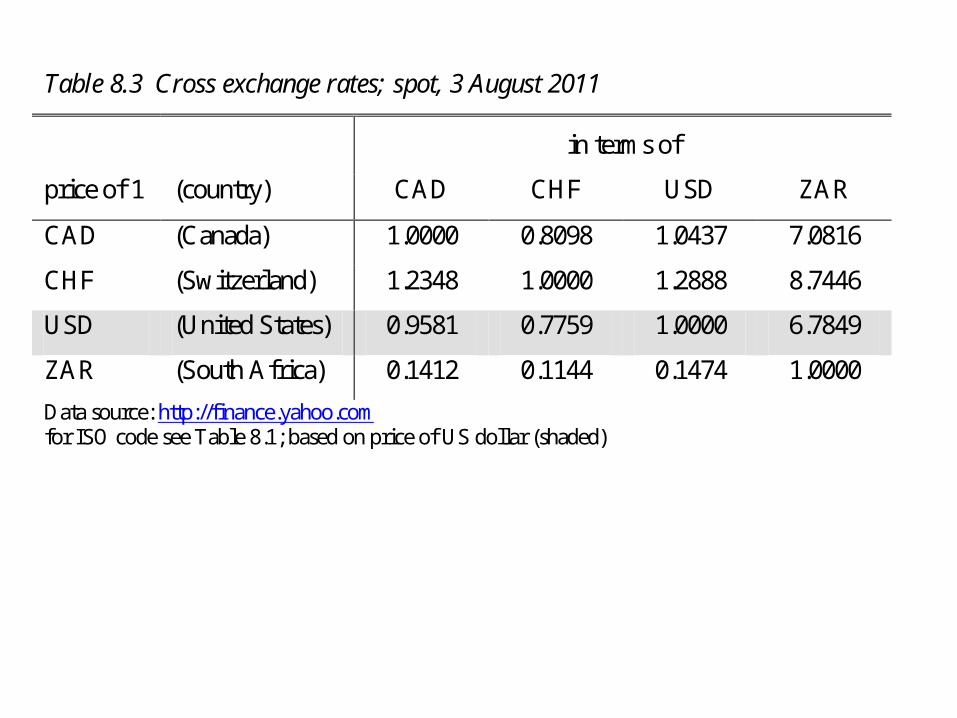

Table 8.3 Cross exchange rates; spot, 3 August 2011

in terms of

price of 1 (country) CAD CHF USD ZAR

CAD (Canada) 1.0000 0.8098 1.0437 7.0816

CHF (Switzerland) 1.2348 1.0000 1.2888 8.7446

USD (United States) 0.9581 0.7759 1.0000 6.7849

ZAR (South Africa) 0.1412 0.1144 0.1474 1.0000

Data source: http://finance.yahoo.com for ISO code see Table 8.1; based on price of US dollar (shaded)

Figure 8.4 Global foreign exchange market turnover, 1998 – 2010

Global foreign exchange market turnover; daily averages in April 2010 (bn US $)

0

400

800

1200

1600

2000

1998 2001 2004 2007 2010

foreign exchange swaps

spot transactions

outright forwards

Data source: BIS (2010), triennial central bank survey

Figure 8.5 Most used currencies on the foreign exchange market, 1998 – 2010

Currency distribution of reported foreign exchange market turnover; percentage shares of average daily turnover in April

0

10

20

30

40

50

60

70

80

90

1998 2001 2004 2007 2010

US dollar Euro Japanese yen Pound sterling Australian dollar Swiss franc

Data source: BIS (2010); * Because two currencies are involved in each transaction, the sum of the percentage shares of individual currencies totals 200 percent instead of 100 percent.

• Exchange rates and prices

• Effective exchange rates

Figure 8.6 Exchange rates and prices, 1960-2009

US exchange rates and consumer prices, 1960-2009

-5

0

5

10

15

20

25

30

-5 0 5 10 15 20 25 30

exchange rate differential

infla

tion

diff

eren

tial

Argentina

Peru

Uruguay

BoliviaTurkey

Calculations based on World Development Indicators online; 64 observations; the line has a 45 slope.

Figure 8.7 Exchange rates and intervention

S

European goods

S0

S M(S)0

X(S)

S M(S)1

A

intervention

DC

B

parity band

S

European goods

S0

S M(S)0

X(S)

S M(S)1

A

intervention

DC

B

parity band

Figure 8.8 De facto exchange rate arrangements, April 30, 2010

De facto exchange rate regimes; # of countries, April 2010

0 5 10 15 20 25 30 35 40 45

No separate legal tender

Currency board

Conventional peg

Stabilized arrangement

Crawling peg

Crawl-like arrangement

Pegged rate with band

Other managed arrangement

Floating

Free floating

Ecuador

Hong Kong

Venezuela, Niger, Morocco, Cameroon

China, Bangladesh

Nicaragua

Ethiopia

Belarus

Russia, Singapore, Egypt

Indonesia, India, Pakistan, Philippines

Australia, UK, USA, Eurozone

Data source: IMF (2010, Appendix II); selected countries listed for each regime, see also Table 23.1

Figure 8.9 US dollar: effective exchange rates, 1973-2011

a. US effective exchange rates, broad

0

100

200

300

400

1972 1980 1988 1996 2004 2012

real

nominal

b. US effective exchange rates, major

0

50

100

150

200

1972 1980 1988 1996 2004 2012

real

nominal

Data source: www.federalreserve.gov

Figure 8.9 US dollar: effective exchange rates, 1973-2011

c. US real effective exchange rates, major and broad

65

75

85

95

105

115

125

1972 1980 1988 1996 2004 2012

major currencies

broad currencies

March 1985 February 2002

Data source: www.federalreserve.gov

Figure 8.10 Out-of-sample exchange rate forecasting

Out of sample forecasting

0

5

10

15

20$

/DM

1-m

$/D

M 6

-m

$/D

M 1

2-m

$/Y

en

1-m

$/Y

en

6-m

$/Y

en

12

-m

$/£

1-m

$/£

6-m

$/£

12

-mcurrency pair and duration (months)

root

mea

n sq

uare

d er

ror

of f

orec

ast

Random walk

Monetary

Dornbusch

Portfolio

Data source: Meese and Rogoff (1983)

Figure 8.11 Canada; interest rates and inflation rate (CPI), 1970 – 2011

Canada; inflation and nominal and real interest rate, 1970-2011

-4

0

4

8

12

16

20

24

1970 1980 1990 2000 2010

nominal interest rate

real interest rate

inflation rate

Data source: IFS; bank rate (end of period) and cpi (% change), monthly data

Figure 8.12 UK; interest rates and term structure, 1980-2011

UK; 3 month and 6 month interest rates and term structure

0

10

20

1980 1985 1990 1995 2000 2005 2010

-1

0

13 months

6 months

term structure(right-hand scale)

Data source: IFS; 3 and 6 month Paris Interbank Offer rate

Arbitrage and interest parity

• Fisher equation:

r = i - π

• Covered interest parity (Fig. 8.13)

Equilibrium condition:

[F(1+iUS)/E]L = [(1+iEU)]L

F/E = (1+iEU)/(1+iUS)

Figure 8.13 Two investment options

L euro to invest

exchange L euro for L/S dollar

receive (1+iEU)L euroinvest L in European bonds

invest L/S in American bonds receive (1+iUS)(L/S) dollar

exchange (1+iUS)(L/S) dollar for F(1+iUS )(L/S) euro

compare revenueL euro to invest

exchange L euro for L/Edollar

receive (1+iEU)L euroinvest L in European bonds

invest L/E in American bonds receive (1+iUS)(L/E)dollar

exchange (1+iUS)(L/E)dollar for F(1+iUS )(L/E)euro

compare revenue

(BOX 8.4) Figure 8.14 Australia – USA: 12-month covered interest parity

Australia-USA; 12 months covered interest parity

-0.03

0

0.03

0.06

0.09

-0.03 0 0.03 0.06 0.09

12 month forward - spot rate

inte

rest

rat

e di

ffer

entia

l

Data source: IFS; shown interest rates are interbank offered rates, 1986-2005

Interest parity, transaction costs, exchange rates, and capital mobility

• rhome = rforeign + risk + TC

A simple version of uncovered interest parity (UIP) condition:

• rhome = rforeign + dE ; TC = 0, risk = dE

Given rforeign ,UIP indicates that in a world of high degree of capital mobility, the domesticinterest rate can differ from the foreign interest rate only if the exchange rate is not fixed.