executing our tap agenda - siemens · december 2007 october 2010 q3 conference call april 2008 ......

TRANSCRIPT

Copyright © Siemens AG 2008. All rights reserved.

Executing Our TAP Agenda

Peter Löscher, President and CEO

JPMorgan 6th Annual Pan-European Capital Goods & Aerospace CEO Conference London, June 12th, 2008

Page 2 June 12th, 2008 Copyright © Siemens AG 2008. All rights reserved.JPMorgan 6th European Capital Goods Conference

This document contains forward-looking statements and information – that is, statements related to future, not past, events. These statements may be identified by words such as “expects,” “looks forward to,” “anticipates,” “intends,” “plans,” “believes,” “seeks,”“estimates,” “will,” “project” or words of similar meaning. Such statements are based on our current expectations and certain assumptions, and are, therefore, subject to certain risks and uncertainties. A variety of factors, many of which are beyond Siemens’control, affect our operations, performance, business strategy and results and could cause the actual results, performance or achievements of Siemens to be materially different from any future results, performance or achievements that may be expressed orimplied by such forward-looking statements. For us, particular uncertainties arise, among others, from changes in general economic and business conditions (including margin developments in major business areas); the challenges of integrating major acquisitions and implementing joint ventures and other significant portfolio measures; changes in currency exchange rates and interest rates;introduction of competing products or technologies by other companies; lack of acceptance of new products or services by customers targeted by Siemens; changes in business strategy; the outcome of pending investigations and legal proceedings, especially the corruption investigation we are currently subject to in Germany, the United States and elsewhere; the potential impact of such investigations and proceedings on our ongoing business including our relationships with governments and other customers;the potential impact of such matters on our financial statements; as well as various other factors. More detailed information about certain of these factors is contained throughout this report and in our other filings with the SEC, which are available on the Siemens website, www.siemens.com, and on the SEC's website, www.sec.gov. Should one or more of these risks or uncertainties materialize, or should underlying assumptions prove incorrect, actual results may vary materially from those described in the relevant forward-looking statement as expected, anticipated, intended, planned, believed, sought, estimated or projected. Siemens does not intend or assume any obligation to update or revise these forward-looking statements in light of developments which differ from those anticipated.

EBITDA (adjusted), Return on capital employed, Free cash flow, Cash conversion and Net debt are Non-GAAP financial measures.A reconciliation of these amounts to the most directly comparable IFRS financial measures is available on our Investor Relationswebsite under www.siemens.com/ir, Financial Publications, Quarterly Reports. 'Group profit from operations' is reconciled to 'Income before income taxes' of Operations under 'Reconciliation to financial statements' in the table 'Segment Information'.

Safe Harbour Statement

Page 3 June 12th, 2008 Copyright © Siemens AG 2008. All rights reserved.JPMorgan 6th European Capital Goods Conference

Attractive markets with tailwind from MEGATRENDS

Focused on three Sectors with strong end markets

1) Combined revenues of businesses 2) Combined revenues of businesses including €1.4 bn Dade Behring pro-forma

High BUSINESS QUALITY in #1 or #2 positions

EnergyBusinesses from

Power GenerationPower Transmission & Distribution

IndustryBusinesses from

Automation & DrivesIndustrial Solutions & ServicesTransportation SystemsBuilding TechnologiesOsram

HealthcareBusinesses from

Medical Solutions

Three SECTORS

Sie

men

s IT

Sol

utio

ns a

nd S

ervi

ces

Sie

men

s Fi

nanc

ial S

ervi

ces

Cross-sectoral

~€20bn1)

~€40bn1)

~€11bn2)Regional shift ofeconomic gravity

Growing demand forsafety and security

Increasing mobility

Growing demand forhealth- and elder care

Growing need forenvironmental care

Increasing scarcity ofnatural resources

Mega-trends

DemographicChange

Urbanization

Page 4 June 12th, 2008 Copyright © Siemens AG 2008. All rights reserved.JPMorgan 6th European Capital Goods Conference

Priorities are clearly defined

Main Topics

Portfolio priorities

Leadership structure

Capital allocation

Target margins

SG&A reduction

Equity culture

Our Principles …

IncreaseTRANSPARENCY

EnforceACCOUNTABILITY

DrivePERFORMANCE

New structureas of Jan 081)

Clear focus on organic growth

Continued com-mitment to SBB2)

First outlinein Q3 2008

Implementation ongoing4)

New targets for2010 defined3)

1) see page 6 for new Sector setup2) see page 22 for execution of € 2 bn first tranche of share buyback3) see page 17 for new target margins on Sector and Division levels4) see pages 11-13 and 18-19 for details on SG&A cost reduction

Page 5 June 12th, 2008 Copyright © Siemens AG 2008. All rights reserved.JPMorgan 6th European Capital Goods Conference

Organic growth is clear portfolio priority

Organic Growth

Exploit global growth opportunities1)

Exploit potential from past acquisitions (> EUR 20 billion over last 5 years)

Earnings conversion2)

1

Three sectors: Energy, Industry and Healthcare3)

Less complex, more competitive4)

Streamlining2

Value creation

Strict financial hurdle rates

M&A deal book

Selectiveinvestment3

Sector CFO namedDivision CEO and CFO namedDecember 2007

New organization approvedManaging Board incl. Sector CEO approved

November 2007Supervisory Board

Share buyback completedCapital structure target achievedSG&A project completedTarget margins achieved

October 2010

Streamlining Other Operations completedOctober 2009

New management compensation scheme in place October 2008

Start pro forma reporting in new structureOutline new management compensation schemeGuidance on EPS range for 2009

July 2008Q3 conference call

Update on SG&A project April 2008 Q2 analyst conference

New target margins for Energy and Industry SectorTarget margins for Divisions

January 2008 AGM

Milestones (deliverables)Reporting dates

Sector CFO namedDivision CEO and CFO namedDecember 2007

New organization approvedManaging Board incl. Sector CEO approved

November 2007Supervisory Board

Share buyback completedCapital structure target achievedSG&A project completedTarget margins achieved

October 2010

Streamlining Other Operations completedOctober 2009

New management compensation scheme in place October 2008

Start pro forma reporting in new structureOutline new management compensation schemeGuidance on EPS range for 2009

July 2008Q3 conference call

Update on SG&A project April 2008 Q2 analyst conference

New target margins for Energy and Industry SectorTarget margins for Divisions

January 2008 AGM

Milestones (deliverables)Reporting dates

1) see page 7 and 8 for strong order growth in Q2 20082) see page 9 for strong earnings conversion of key value drivers in Q2 20083) see page 6 for new Sector setup4) see page 12 for new regional cluster setup

Page 6 June 12th, 2008 Copyright © Siemens AG 2008. All rights reserved.JPMorgan 6th European Capital Goods Conference

1) not reported externally because of cross-divisional service character 2) 7/11 for shareholder representatives 3) no members of former Group boards

New organizational setup in place –leadership, governance and people

Clear chain of

commandand

escalation path

Sector CFO namedDivision CEO and CFO namedDecember 2007

New organization approvedManaging Board incl. Sector CEO approved

November 2007Supervisory Board

Share buyback completedCapital structure target achievedSG&A project completedTarget margins achieved

October 2010

Streamlining Other Operations completedOctober 2009

New management compensation scheme in place October 2008

Start pro forma reporting in new structureOutline new management compensation schemeGuidance on EPS range for 2009

July 2008Q3 conference call

Update on SG&A project April 2008 Q2 analyst conference

New target margins for Energy and Industry SectorTarget margins for Divisions

January 2008 AGM

Milestones (deliverables)Reporting dates

Sector CFO namedDivision CEO and CFO namedDecember 2007

New organization approvedManaging Board incl. Sector CEO approved

November 2007Supervisory Board

Share buyback completedCapital structure target achievedSG&A project completedTarget margins achieved

October 2010

Streamlining Other Operations completedOctober 2009

New management compensation scheme in place October 2008

Start pro forma reporting in new structureOutline new management compensation schemeGuidance on EPS range for 2009

July 2008Q3 conference call

Update on SG&A project April 2008 Q2 analyst conference

New target margins for Energy and Industry SectorTarget margins for Divisions

January 2008 AGM

Milestones (deliverables)Reporting dates

Supervisory Board 11/20 new 2)

Industry Energy

Osram Service Rotating Equipment 1)

Industry Solutions Power Transmission

Mobility Power Distribution

Healthcare

Industry Automation Fossil Power Generation Imaging & IT

Drive Technologies Renewable Energy Workflow & Solutions

Building Technologies Oil & Gas Diagnostics

6/15 Division CEO new 3)

Global Function HeadsFinance and ControllingLegal and ComplianceHuman ResourcesTechnology

6/8 new

Managing BoardChief Executive Officer

IndustryCEO

EnergyCEO

HealthcareCEO

Page 7 June 12th, 2008 Copyright © Siemens AG 2008. All rights reserved.JPMorgan 6th European Capital Goods Conference

Q2 2008 – key figures and financial highlights

Adjusted1)nominal

% Change

2%

15%

-38%

-67%

-56%

-32%

1%

12%

1,623 m2,619 mFree Cash Flow (Cont. Op.)

412 m1,259 mNet income (''all-in'')

565 m1,286 mIncome from Cont. Op.

1,203 m1,781 mGroup profit from Operations

18,001 m

20,850 m

Q2 2007

18,094 mSales (Cont. Op.)

23,371 m

Q2 2008

New orders (Cont. Op.)

1) Adjusted for portfolio and currency translation effects

Very strong y-o-y organic order growth1) of 15% across all regions

No slowdown for market leader A&D

Group Profit from Operations affected by € 857m project charges, but: very good underlying margins

Income from Continuing Operations affected by increased expenses for compliance investigations and costs related to Siemens transformation programs

Page 8 June 12th, 2008 Copyright © Siemens AG 2008. All rights reserved.JPMorgan 6th European Capital Goods Conference

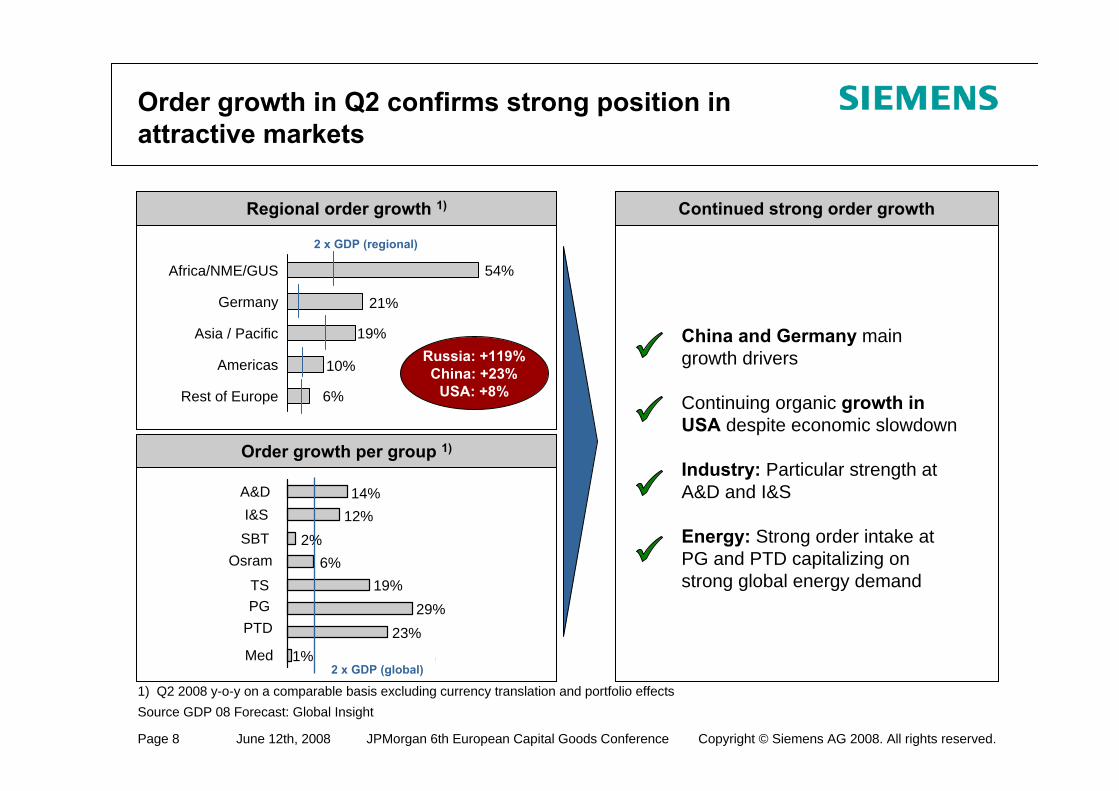

Order growth per group 1)

Regional order growth 1)

1) Q2 2008 y-o-y on a comparable basis excluding currency translation and portfolio effectsSource GDP 08 Forecast: Global Insight

14%

SBTI&S

Med

Osram

A&D

TSPG

PTD

12%2%

6%19%

29%23%

1%2 x GDP (global)

54%Africa/NME/GUS

21%Germany

19%Asia / Pacific

10%Americas

6%Rest of Europe

2 x GDP (regional)

Continued strong order growth

China and Germany main growth drivers

Continuing organic growth in USA despite economic slowdown

Industry: Particular strength at A&D and I&S

Energy: Strong order intake at PG and PTD capitalizing on strong global energy demand

Order growth in Q2 confirms strong position in attractive markets

Russia: +119%China: +23%

USA: +8%

Page 9 June 12th, 2008 Copyright © Siemens AG 2008. All rights reserved.JPMorgan 6th European Capital Goods Conference

Key value drivers show strong earnings conversion

A&D Med PTD

14.2%

14.4%

Q2 2007

16.7%

Q2 2008

+310 bp

17.5%

13.4%

15.3%

Q2 2007 Q2 2008

16.3%

+100 bp

12.5%

8.1%

Q2 2007

11.6%

Q2 2008

+350 bp

PPA - € 35mOTC - € 2m

PPA - € 50mOTC - € 52m

Margin improvement driven by economies of scale as a result of high capacity utilization

Increasing underlying profitability despite challenges

in market conditions

Favorable product mix and economies of scale associated

with higher revenue

PPA - € 37mOTC - € 9m

PPA - € 10m

As reported Adjusted for PPA, one time costs (OTC)

Page 10 June 12th, 2008 Copyright © Siemens AG 2008. All rights reserved.JPMorgan 6th European Capital Goods Conference

Our innovative solutions address key customer needs

Unifying Product Planningand Production

Shortening engineering processFaster time to market by up to 50%

Gas turbine SGT5-8000HFast start-up capability & operational flexibilityHigh reliability and availability In combined cycle duty efficiencyof over 60%

Siemens Gas Turbine –Unmatched Efficiency

Lowest life cycle costsReduced investment costs/kW

MAGNETOM EssenzaCompletely produced in ChinaComplete range of clinical applicationsCertified for worldwide delivery

World’s first high end –low cost MR scanner

Significantly lower price :< $1mAddressing new market segment-

smaller community hospitals

Digital design / Digital factoryIntegrated plant engineering(Simatic Automation Designer)Virtual commissioningCollaborative Data Management(Worldwide implementation of Teamcenter Platform, e.g. at VW)

Page 11 June 12th, 2008 Copyright © Siemens AG 2008. All rights reserved.JPMorgan 6th European Capital Goods Conference

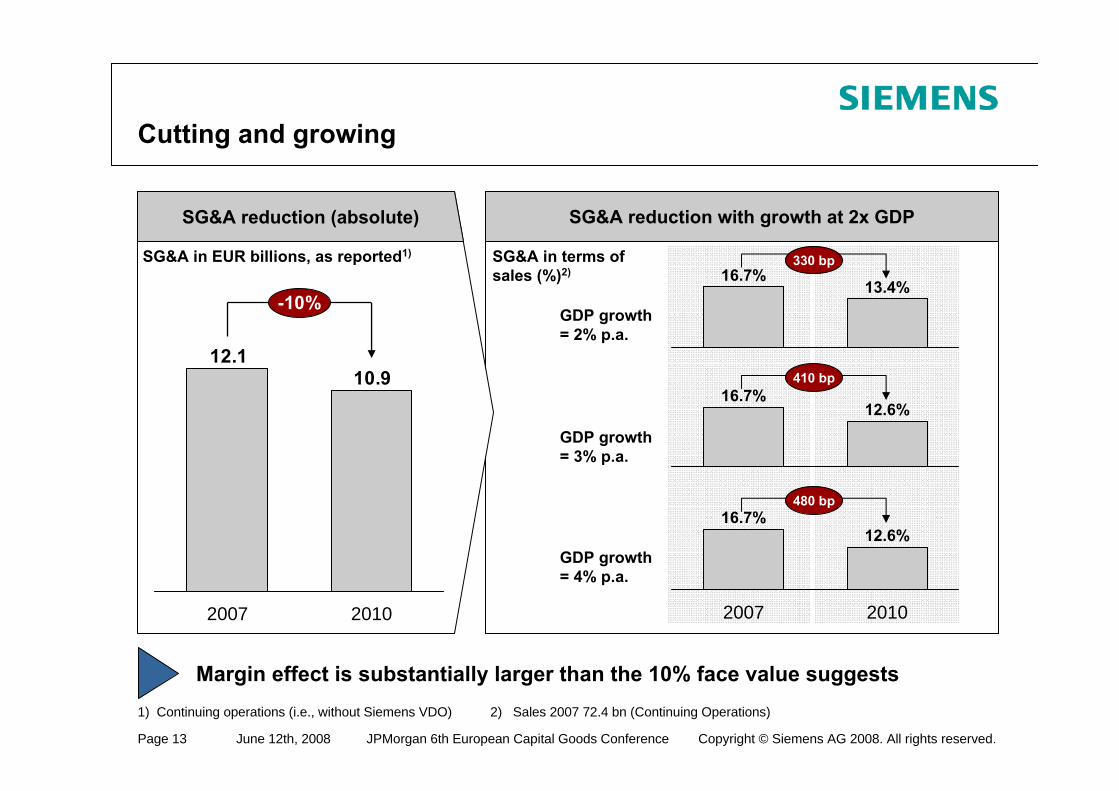

SG&A cost reduction

€ bn, as reported1)

Main drivers

Eliminating duplicate functions on all levels by new accountability principles

Reducing number of legal entities and reporting units

Cutting overhead by new Sector setup2) and Regional clusters

Driving cost efficiency through streamlined go-to-market

Target breakdown

-6%

-22%

SG&A cost reduction plan for € 1.2 bn in place

11.9

FY 06

~8.9

~3.2

12.1

FY 07

10.9

G&A

Sales &Marketing

FY 10

∼2.5

∼8.4

-10%

1) Continuing operations (i.e., without Siemens VDO) 2) see page 19 for new Sector setup

Sector CFO namedDivision CEO and CFO namedDecember 2007

New organization approvedManaging Board incl. Sector CEO approved

November 2007Supervisory Board

Share buyback completedCapital structure target achievedSG&A project completedTarget margins achieved

October 2010

Streamlining Other Operations completedOctober 2009

New management compensation scheme in place October 2008

Start pro forma reporting in new structureOutline new management compensation schemeGuidance on EPS range for 2009

July 2008Q3 conference call

Update on SG&A project April 2008 Q2 analyst conference

New target margins for Energy and Industry SectorTarget margins for Divisions

January 2008 AGM

Milestones (deliverables)Reporting dates

Sector CFO namedDivision CEO and CFO namedDecember 2007

New organization approvedManaging Board incl. Sector CEO approved

November 2007Supervisory Board

Share buyback completedCapital structure target achievedSG&A project completedTarget margins achieved

October 2010

Streamlining Other Operations completedOctober 2009

New management compensation scheme in place October 2008

Start pro forma reporting in new structureOutline new management compensation schemeGuidance on EPS range for 2009

July 2008Q3 conference call

Update on SG&A project April 2008 Q2 analyst conference

New target margins for Energy and Industry SectorTarget margins for Divisions

January 2008 AGM

Milestones (deliverables)Reporting dates

Page 12 June 12th, 2008 Copyright © Siemens AG 2008. All rights reserved.JPMorgan 6th European Capital Goods Conference

Regional clusters: more transparent, faster and closer to the customers

Increased sales efficiency across countries Bundling of central functions within clustersOptimized span of control for Sectors and Regions

~190 Countries ~70 Regional Companies

20 Clusters

Sector CFO namedDivision CEO and CFO namedDecember 2007

New organization approvedManaging Board incl. Sector CEO approved

November 2007Supervisory Board

Share buyback completedCapital structure target achievedSG&A project completedTarget margins achieved

October 2010

Streamlining Other Operations completedOctober 2009

New management compensation scheme in place October 2008

Start pro forma reporting in new structureOutline new management compensation schemeGuidance on EPS range for 2009

July 2008Q3 conference call

Update on SG&A project April 2008 Q2 analyst conference

New target margins for Energy and Industry SectorTarget margins for Divisions

January 2008 AGM

Milestones (deliverables)Reporting dates

Sector CFO namedDivision CEO and CFO namedDecember 2007

New organization approvedManaging Board incl. Sector CEO approved

November 2007Supervisory Board

Share buyback completedCapital structure target achievedSG&A project completedTarget margins achieved

October 2010

Streamlining Other Operations completedOctober 2009

New management compensation scheme in place October 2008

Start pro forma reporting in new structureOutline new management compensation schemeGuidance on EPS range for 2009

July 2008Q3 conference call

Update on SG&A project April 2008 Q2 analyst conference

New target margins for Energy and Industry SectorTarget margins for Divisions

January 2008 AGM

Milestones (deliverables)Reporting dates

Expected benefits

Page 13 June 12th, 2008 Copyright © Siemens AG 2008. All rights reserved.JPMorgan 6th European Capital Goods Conference

SG&A reduction with growth at 2x GDPSG&A reduction (absolute)

GDP growth = 3% p.a.

GDP growth = 4% p.a.

GDP growth = 2% p.a.

330 bp

410 bp

480 bp

SG&A in EUR billions, as reported1) SG&A in terms of sales (%)2)

Cutting and growing

10.912.1

2007

-10%

2010

16.7%12.6%

16.7%

2007

12.6%

2010

13.4%16.7%

2) Sales 2007 72.4 bn (Continuing Operations)

Margin effect is substantially larger than the 10% face value suggests1) Continuing operations (i.e., without Siemens VDO)

Page 14 June 12th, 2008 Copyright © Siemens AG 2008. All rights reserved.JPMorgan 6th European Capital Goods Conference

Outlook 2008

Organic revenue growth for the fiscal year will be twice the rate of GDP growth

Group Profit from Operations will match prior year’s level

Income from Continuing Operations will match prior year’s level

This outlook excludes earnings impacts that may arise from legal and regulatory matters, which are not yet quantifiable, and from measures that may be taken as part of Siemens’ transformation programs, including SG&A reduction. Within discontinued operations, divestment of the enterprise networking business is expected to result in a substantial loss.

Page 15 June 12th, 2008 Copyright © Siemens AG 2008. All rights reserved.JPMorgan 6th European Capital Goods Conference

TAP – consistent execution against plan

Sector CFO namedDivision CEO and CFO namedDecember 2007

New organization approvedManaging Board incl. Sector CEO approved

November 2007Supervisory Board

Share buyback completedCapital structure target achievedSG&A project completedTarget margins achieved

October 2010

Streamlining Other Operations completedOctober 2009

New management compensation scheme in place October 2008

Start pro forma reporting in new structureOutline new management compensation schemeGuidance on EPS range for 2009

July 2008Q3 conference call

Update on SG&A project April 2008 Q2 analyst conference

New target margins for Energy and Industry SectorTarget margins for Divisions

January 2008 AGM

Milestones (deliverables)Reporting dates

Page 16 June 12th, 2008 Copyright © Siemens AG 2008. All rights reserved.JPMorgan 6th European Capital Goods Conference

Backup

Page 17 June 12th, 2008 Copyright © Siemens AG 2008. All rights reserved.JPMorgan 6th European Capital Goods Conference

Profitability targets close the gap to best competitors

1) Best possible comparison with Groups of former organization (blurred due to selective movement of businesses)

16-19%Diagnostics

12-16%Renewable Energy10-14% PG

5-7% I&S10-14%Oil & Gas

7-10% PTD10-14%Power Transmission

11-15%Power Distribution

13-15% Med

14-17%Imaging & ITHealthcare14-17% Workflow & Solutions

Fossil Power Generation

Osram

Mobility

Industry Solutions

Building Technologies

Drive Technologies

Industry Automation

Division

10-14% PG11-15%

Energy11-15%

10-12% Osram10-12%

11-14%

5-7% TS5-7%

5-7% I&S5-7%

7-9% SBT7-10%

11-16%12-15% A&D

12-17%

Industry 9-13%

Main competitorsTarget margin of former Group 1)ChangeNew 2010

target marginSector

16-19%Diagnostics

12-16%Renewable Energy10-14% PG

5-7% I&S10-14%Oil & Gas

7-10% PTD10-14%Power Transmission

11-15%Power Distribution

13-15% Med

14-17%Imaging & ITHealthcare14-17% Workflow & Solutions

Fossil Power Generation

Osram

Mobility

Industry Solutions

Building Technologies

Drive Technologies

Industry Automation

Division

10-14% PG11-15%

Energy11-15%

10-12% Osram10-12%

11-14%

5-7% TS5-7%

5-7% I&S5-7%

7-9% SBT7-10%

11-16%12-15% A&D

12-17%

Industry 9-13%

Main competitorsTarget margin of former Group 1)ChangeNew 2010

target marginSector

Sector CFO namedDivision CEO and CFO namedDecember 2007

New organization approvedManaging Board incl. Sector CEO approved

November 2007Supervisory Board

Share buyback completedCapital structure target achievedSG&A project completedTarget margins achieved

October 2010

Streamlining Other Operations completedOctober 2009

New management compensation scheme in place October 2008

Start pro forma reporting in new structureOutline new management compensation schemeGuidance on EPS range for 2009

July 2008Q3 conference call

Update on SG&A project April 2008 Q2 analyst conference

New target margins for Energy and Industry SectorTarget margins for Divisions

January 2008 AGM

Milestones (deliverables)Reporting dates

Sector CFO namedDivision CEO and CFO namedDecember 2007

New organization approvedManaging Board incl. Sector CEO approved

November 2007Supervisory Board

Share buyback completedCapital structure target achievedSG&A project completedTarget margins achieved

October 2010

Streamlining Other Operations completedOctober 2009

New management compensation scheme in place October 2008

Start pro forma reporting in new structureOutline new management compensation schemeGuidance on EPS range for 2009

July 2008Q3 conference call

Update on SG&A project April 2008 Q2 analyst conference

New target margins for Energy and Industry SectorTarget margins for Divisions

January 2008 AGM

Milestones (deliverables)Reporting dates

Page 18 June 12th, 2008 Copyright © Siemens AG 2008. All rights reserved.JPMorgan 6th European Capital Goods Conference

Key G&A improvement areas and levers identified

∼3.2Baseline FY 2007

Leverage newsector organization

Leverage new regionalcluster organization

Operate with clearaccountability

Ensure effective cor-porate governance

Capture synergies ofscale by appropriate

pooling

Ensure operational excellence

Target FY 2010 ∼2.5

Reductionby 22%

Key improvement areas

Consolidation of headquarter central functions from 8 Groups into 3 Sectors(e.g., in accounting, controlling, communication)

Bundling of infrastructure from ~ 70 regional companies into 20 regional clusters to exploit cost synergies (e.g., in accounting, controlling, IT)

No institutionalized 2nd opinionReduction of profit center structures from 900 to 500No corporate-driven performance controlling for regionsReduction of consultant support

Streamlining Corporate headquarters to governance activities resulting in cost reduction Reduction of number of corporate programs and initiatives by > 50%Reduction in number of legal entities from 1,800 to < 1,000Centralizing of auditing

Bundling of shared services to double Siemens-internal service coverageConsolidation of real-estate management into a single entity

Optimize fragmented and oversized IT services by infrastructure standardizationand application consolidationIntroduction of rolling forecast replacing bottom-up planning

Reported G&A cost, € bn

Page 19 June 12th, 2008 Copyright © Siemens AG 2008. All rights reserved.JPMorgan 6th European Capital Goods Conference

Levers for sales cost reduction and efficiency gains

FY 2007

Optimizationof infrastructure

Optimizationof back office

Front end

FY 2010 ∼8.4

∼8.9

Reductionby 6%

Key improvement areas

Bundling of infrastructure in Clusters Integration of legal entitiesStreamlining of sales mgt. structures Discontinuation of major IT projectsBundling of shared services to double service coverage

Centralization of sales back office (e.g. offer preparation, technical consulting,…) in 20 Clusters (instead of 70 countries) or across ClustersInterface optimization between HQ-Regions, no duplicate functionsReduction of HQ back office functions Removal of cross-Divisional coordination functions in vertical markets

Efficiency increase

Growth related increase

Sales efficiency:Standardization of planning, logistics, pricing, CRM processes across Clusters and selected DivisionsFocused market approach (selection of market segments) Leverage e-Business

Go-to-market / sales channels:Redefining sales representation in smaller countriesRestructuring of sales officesStronger orientation towards verticals like automotive, F&BLeverage channel management with partners Joint wholesale approachLeverage cross-Divisional sales

Reported sales cost, € bn

Page 20 June 12th, 2008 Copyright © Siemens AG 2008. All rights reserved.JPMorgan 6th European Capital Goods Conference

Growth

Update on Fit42010 comprehensive target system

Cash conversion Capital structureAdj. industrial net debt / EBITDA

Capital efficiency

1 – growth rate

>2x GDP ROCE 14 - 16%

0.8x – 1.0x

Cash

ProfitabilityGrowth

Capitalstructure

1) FY 2007 adjusted for VDO proceeds € 11.4 bn and Dade Behring purchase price € 5.2 bn

4%

10%10%

FY 2006 FY 2007 Q2 2008 YTD

9.6%

FY 2006

12.7%

FY 2007

8.6%

Q2 2008 YTD

Q2 2008 YTD

0.040.37

0.76 1)

FY 2006 FY 2007FY 2006 FY 2007

0.86

Q2 2008 YTD

0.69

1.73

Page 21 June 12th, 2008 Copyright © Siemens AG 2008. All rights reserved.JPMorgan 6th European Capital Goods Conference

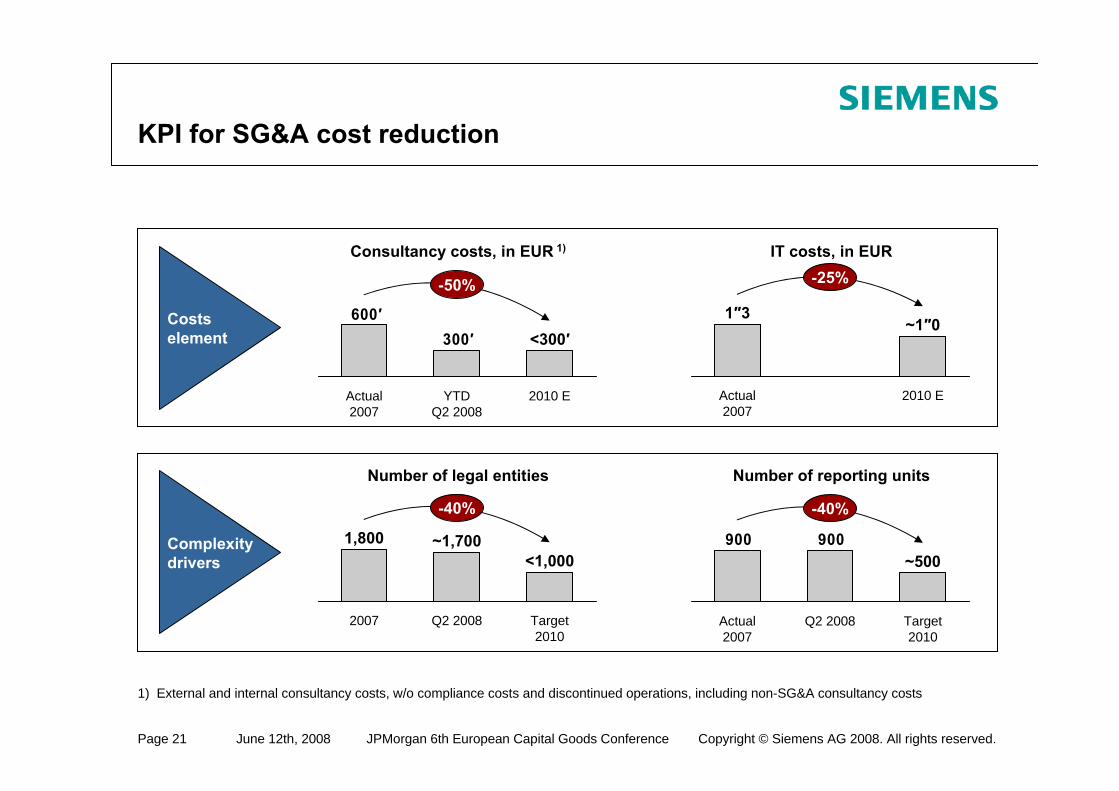

KPI for SG&A cost reduction

1) External and internal consultancy costs, w/o compliance costs and discontinued operations, including non-SG&A consultancy costs

Costs element

Complexitydrivers

Consultancy costs, in EUR 1) IT costs, in EUR

Number of legal entities Number of reporting units

300′600′

<300′

-50%

2010 EYTD Q2 2008

Actual2007

Actual2007

-25%

1″3

2010 E

~1″0

900900

Q2 2008

-40%

Target2010

Actual2007

~5001,800

2007

~1,700

Q2 2008

<1,000

Target2010

-40%

Page 22 June 12th, 2008 Copyright © Siemens AG 2008. All rights reserved.JPMorgan 6th European Capital Goods Conference

€ 2 bn share buyback tranche successfully executed

Number of sharesoutstanding

Share price and daily repurchase volume28 Jan – 8 April

We are fully committed to the share buyback program and will provide continuing updates of next steps

0

200.000

400.000

600.000

800.000

1.000.000

28-Jan-08

5-Feb-08

13-Feb-08

21-Feb-08

29-Feb-08

10-Mar-08

18-Mar-08

28-Mar-08

7-Apr-08

Volu

me

50

60

70

80

90

100

Share Price (€)

Repurchased Vo lume Gro ss Repurchased P rice

914.2m

01 Jan 08

24.9m

889.3m

08 Apr 08

(2.7% of sharesoutstanding)

Sector CFO namedDivision CEO and CFO namedDecember 2007

New organization approvedManaging Board incl. Sector CEO approved

November 2007Supervisory Board

Share buyback completedCapital structure target achievedSG&A project completedTarget margins achieved

October 2010

Streamlining Other Operations completedOctober 2009

New management compensation scheme in place October 2008

Start pro forma reporting in new structureOutline new management compensation schemeGuidance on EPS range for 2009

July 2008Q3 conference call

Update on SG&A project April 2008 Q2 analyst conference

New target margins for Energy and Industry SectorTarget margins for Divisions

January 2008 AGM

Milestones (deliverables)Reporting dates

Sector CFO namedDivision CEO and CFO namedDecember 2007

New organization approvedManaging Board incl. Sector CEO approved

November 2007Supervisory Board

Share buyback completedCapital structure target achievedSG&A project completedTarget margins achieved

October 2010

Streamlining Other Operations completedOctober 2009

New management compensation scheme in place October 2008

Start pro forma reporting in new structureOutline new management compensation schemeGuidance on EPS range for 2009

July 2008Q3 conference call

Update on SG&A project April 2008 Q2 analyst conference

New target margins for Energy and Industry SectorTarget margins for Divisions

January 2008 AGM

Milestones (deliverables)Reporting dates

Page 23 June 12th, 2008 Copyright © Siemens AG 2008. All rights reserved.JPMorgan 6th European Capital Goods Conference

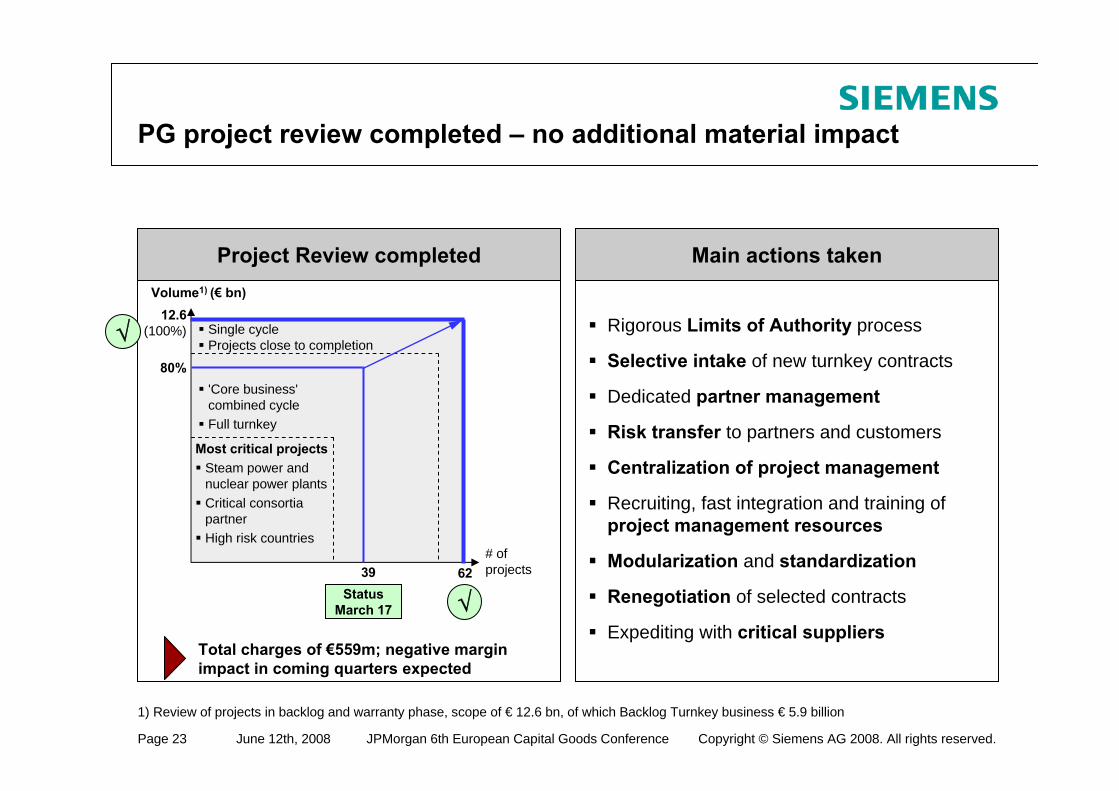

PG project review completed – no additional material impact

Project Review completed Main actions taken

Rigorous Limits of Authority process

Selective intake of new turnkey contracts

Dedicated partner management

Risk transfer to partners and customers

Centralization of project management

Recruiting, fast integration and training of project management resources

Modularization and standardization

Renegotiation of selected contracts

Expediting with critical suppliers

# of projects

Most critical projectsSteam power and nuclear power plantsCritical consortia partnerHigh risk countries

12.6(100%)

80%

Volume1) (€ bn)

'Core business' combined cycleFull turnkey

Single cycle Projects close to completion

62Status

March 17

39

√

Total charges of €559m; negative margin impact in coming quarters expected

√

1) Review of projects in backlog and warranty phase, scope of € 12.6 bn, of which Backlog Turnkey business € 5.9 billion

Page 24 June 12th, 2008 Copyright © Siemens AG 2008. All rights reserved.JPMorgan 6th European Capital Goods Conference

Business mix will drive higher Fossil PG margins

Backlog in Fossil

29%

Turnkey

71%

Products & Service

€ 22.5 bn08/03/31

Order intake in Fossil

30%

Turnkey

70%

Products & Service

€ 4.2 bnQ2 2008

Turning turnkey backlog into sales

Business mix will change

1,5 2,2 1,8

3,0

1,3

>2010

5.9

4Q 07 Turned into

revenue

New order intake

6.6

2Q 08 2H 08 2009 2010

0,5

Backlog in € bn

Order intake (%)

39% 34% 33%

61%

100%

2007

66%

100%

2010E

67%

100%

Long termtarget

Turnkey

Products& Service

New orders in 07-08 more profitable than older projects

Challenges from Olkiluoto - project <50% completed

Fossil PG Margin of 7-9% in 2009

Fossil's 2010 target of 11-15% confirmed

Page 25 June 12th, 2008 Copyright © Siemens AG 2008. All rights reserved.JPMorgan 6th European Capital Goods Conference

Financial Calendar

July

June

June 2008 Post Q2 roadshows with CEO and CFO in New York and Boston (June 9-10), London (June 12), Frankfurt (June 13)

June 4, 2008Deutsche Bank German & Austrian Corporate Conference – Joe Kaeser, CFO

June 12, 2008JPMorgan Pan-European CEO Conference – Peter Löscher, CEO

August/September No events planned so far

June 30 – July 1, 2008Capital Market Days of Sector Energy – Munich, Germany

July 30, 2008Q3 Financial report and conference call

Page 26 June 12th, 2008 Copyright © Siemens AG 2008. All rights reserved.JPMorgan 6th European Capital Goods Conference

Reconciliation and Definitions for Non-GAAP Measures (I)

Group profit from Operations is reconciled to Income before income taxes of Operations under Reconciliation to financial statements on thetable Segment Information. See our Financial Publications at our Investor Relations website under www.siemens.com/ir.

Earnings before interest and taxes (EBIT) (adjusted) is Income from continuing operations before income taxes less Financial income (expense), net and Income (loss) from investments accounted for using the equity method, net.

Earnings before interest, taxes, depreciation and amortization (EBITDA) (adjusted) is EBIT before Depreciation and Amortization, definedas amortization and impairments of intangible assets depreciation and impairments of property, plant and equipment.

Group profit is reconciled to EBIT and EBITDA on the table Segment Information Analysis (II). See our Financial Publications at our Investor Relations website under www.siemens.com/ir.

Return on Capital Employed (ROCE) is a measure of how capital invested in the Company or the Group yields competitive returns. For the Company, ROCE is calculated as Net income (before interest) divided by average Capital employed (CE). Net income (before interest) is defined as Net income excluding Other interest income (expense), net and excluding taxes on Other interest income (expense), net. Taxes on Other interest income (expense), net are calculated in simplified form by applying the current tax rate which can be derived from the Consolidated Statements of Income, to Other interest income (expense), net. CE is defined as Total equity plus Long-term debt plus Short-term debt and current maturities of long-term debt minus Cash and cash equivalents. Because Siemens reports discontinued operations, Siemens also calculates ROCE on a continuing operations basis, using Income from continuing operations rather than Net income. For purposes of this calculation, CE is adjusted by the net figure for Assets classified as held for disposal included in discontinued operations less Liabilities associated with assets classified as held for disposal included in discontinued operations.For the Operations Groups, ROCE is calculated as Group profit divided by average Net capital employed (NCE). Group profit for the Operations Groups is principally defined as earnings before financing interest, certain pension costs and income taxes. Group profit excludes various categories of items which are not allocated to the Groups since the Managing Board does not regard such items as indicative of the Groups’performance. NCE for the Operations Groups is defined as total assets less tax assets, provisions and non-interest bearing liabilities other than tax liabilities.Average (Net) Capital employed for the fiscal year is calculated as a 'five-point average' obtained by averaging the (Net) Capital employed at the beginning of the first quarter plus the final figures for all four quarters of the fiscal year. For the calculation of the average during for the quarters, see below:

Page 27 June 12th, 2008 Copyright © Siemens AG 2008. All rights reserved.JPMorgan 6th European Capital Goods Conference

Reconciliation and Definitions for Non-GAAP Measures (II)

• NCE for Operations Groups

Our cash target is based on the Cash Conversion Rate (CCR), which serves as a target indicator for the Company’s or the Group’s cash flow. For the Company, CCR is defined as the ratio of Free cash flow to Net income, where Free cash flow equals the Net cash provided by (used in) operating activities less Additions to intangible assets and property, plant and equipment. Because Siemens reports discontinued operations, this measure is also shown on a continuing operations basis, using Income from continuing operations, Net cash provided by (used in) operating activities – continuing operations and Additions to intangible assets and property, plant and equipment for continuing operations for the calculation. For the Groups, CCR is defined as Free cash flow divided by Group profit.

All values needed for the calculation of ROCE and CCR can be obtained from the Consolidated Financial Statements and Notes to Consolidated Financial Statements.Group profit, Net capital employed and Free cash flow for the Company and the Groups can be found on the table Segment information. Our Consolidated Financial Statements are available on our Investor Relations website under www.siemens.com/ir.

Siemens ties a portion of its executive incentive compensation to achieving economic value added (EVA) targets. EVA measures the profitability of a business (using Group profit for the Operating Groups and Income before income taxes for the Financing and Real estate businesses as a base) against the additional cost of capital used to run a business (using NCE for the Operating Groups and risk-adjusted equity for the Financing and Real estate businesses as a base). A positive EVA indicates that a business has earned more than its cost of capital, and is therefore defined as value-creating. A negative EVA indicates that a business is earning less than its cost of capital and is therefore defined as value-destroying. Other organizations that use EVA may define and calculate EVA differently.

Average calculation for CE*:

4 Point average: (CE ending Q4 Prior year + CE ending Q1 + CE ending Q2 + CE ending Q3) / 4Q3

3 Point average: (CE ending Q4 Prior year + CE ending Q1 + CE ending Q2) / 3Q2

2 Point average: (CE ending Q4 Prior year + CE ending Q1) / 2Q1Year-to-Date

2 Point average: (CE ending Q3 + CE ending Q4) / 2Q4

2 Point average: (CE ending Q2 + CE ending Q3) / 2Q3

2 Point average: (CE ending Q1 + CE ending Q2) / 2Q2

2 Point average: (CE ending Q4 Prior year + CE ending Q1) / 2Q1Quarter-to-Date

Page 28 June 12th, 2008 Copyright © Siemens AG 2008. All rights reserved.JPMorgan 6th European Capital Goods Conference

Reconciliation and Definitions for Non-GAAP Measures (III)

Our capital structure target is based on an Adjusted industrial net debt divided by EBITDA (adjusted). For the calculation of Adjusted industrial net debt, we subtract from Net debt (defined as Long-term debt plus Short-term debt and current maturities of long-term debt less Cash and cash equivalents less Available-for-sale financial assets) (1) SFS debt excluding SFS internally purchased receivables and (2) 50% of the nominal amount of our hybrid bond; and add/subtract (3) Funded status of Pension benefits, (4) Funded status of Other post-employment benefits; andadd (5) Credit guarantees. The components of Net debt are available on our Consolidated Balance Sheets, SFS debt less internally purchased receivables is available in our Management Discussion & Analysis under Capital Resources and Requirements. The Funded status of our principle pension plans and Other post-employment benefits, the amount of credit guarantees and the nominal amount of our Hybrid bond is available in the Notes to our Consolidated Financial Statements.

To measure Siemens’ achievement of the goal to grow at twice the rate of global GDP, we use GDP on real basis (i.e. excluding inflationand currency translation effects) with data provided by Global Insight Inc. and compare those growth rates with growth rates of our revenue(under IFRS). In accordance with IFRS, our revenue numbers are not adjusted by inflation and currency translation effects.

Return on equity (ROE) margin for SFS was calculated as SFS’ Income before income taxes divided by the allocated equity for SFS.Allocated equity for SFS for the financial year 2007 is €1.041 billion. The allocated equity for SFS is determined and influenced by the respective credit ratings of the rating agencies and by the expected size and quality of its portfolio of leasing and factoring assets and equity investments and is determined annually. This allocation is designed to cover the risks of the underlying business and is in line with common credit risk management standards in banking. The actual risk profile of the SFS portfolio is monitored and controlled monthly and is evaluated against the allocated equity.

Group profit from Operations, EBIT (adjusted), EBITDA (adjusted), ROCE, CCR, EVA and Adjusted industrial net debt are or may be Non-GAAP financial measures as defined in relevant rules of the U.S. Securities and Exchange Commission. Our management takes these measures,among others, into account in its management of our business, and for this reason we believe that investors may find it useful to consider these measures in their evaluation of our performance. None of Group profit from Operations, EBIT (adjusted), EBITDA (adjusted), ROCE and EVA should be viewed in isolation as an alternative to IFRS net income for purposes of evaluating our results of operations; CCR should not be viewed in isolation as an alternative to measures reported in our IFRS cash flow statement for purposes of evaluating our cash flows; and Adjusted industrial net debt should not be viewed in isolation as an alternative to liabilities reported in our IFRS balance sheet for purposes of evaluating our financial condition.

Page 29 June 12th, 2008 Copyright © Siemens AG 2008. All rights reserved.JPMorgan 6th European Capital Goods Conference

Siemens Investor Relations Team

Webpage: http://www.siemens.com/investorrelations

e-mail: [email protected]

Telephone: +49-89-636-32474

Fax: +49-89-636-32830

Michael Sen +49-89-636-33780

Gerald Brady +1-408-492-4439

Florian Flossmann +49-89-636-34095

Sabine Groß +49-89-636-35755

Dr. Martin Meyer +49-89-636-33693

Christof Schwab +49-89-636-32677

Dr. Gerd Venzl +49-89-636-44144