expand - heritage oil · oml 30 lies onshore the niger delta in one of the most prolific oil...

TRANSCRIPT

E X PA N D

S T R A T E G I C R E P O R T2 0 1 3

E X PA N D

S T R A T E G I C R E P O R T2 0 1 3

P R O T E C T

C O R P O R a T E s O C i a l R E s P O n s i b i l i T y2 0 1 3

S T R U C T U R E

C o R p o R a T E g o v E R n a n C E2 0 1 3

e v o lv e

f i n a n c i a l s t a t e m e n t s2 0 1 3

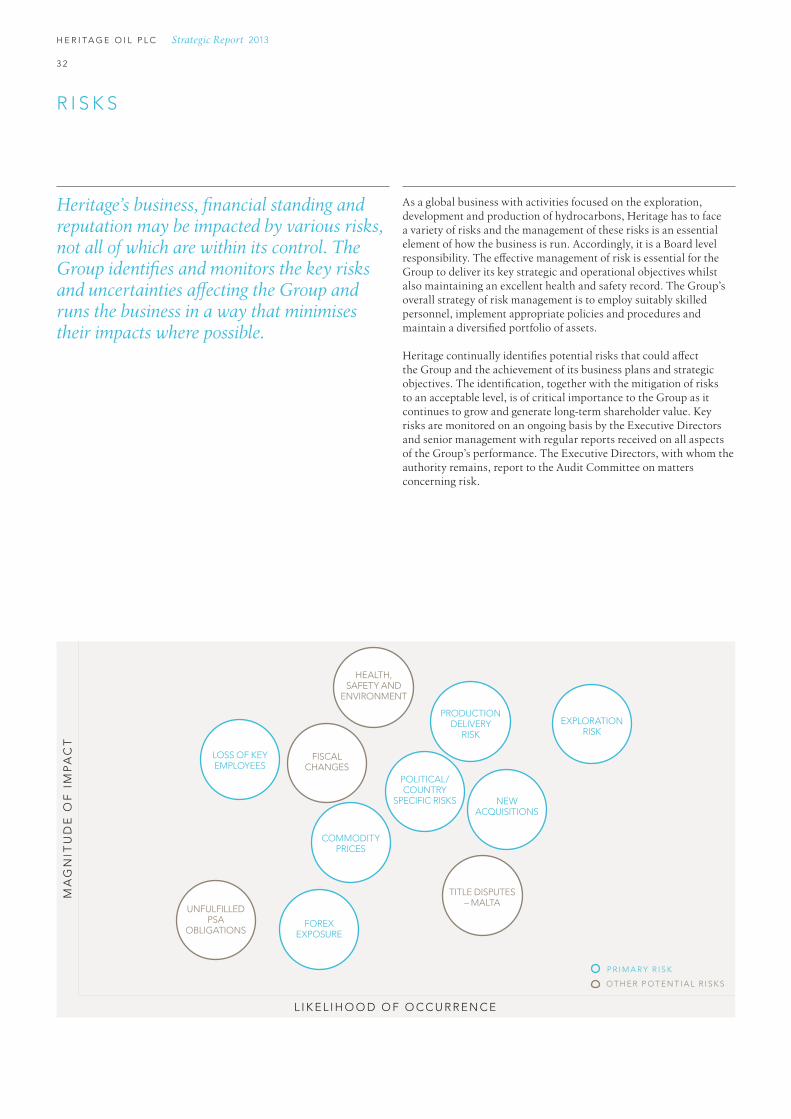

H E R I T A G E O I L P L C Strategic Report 2013

Heritage Oil Plc is an independent oil and gas exploration and production company with a Premium Listing on the London Stock Exchange (“LSE”) (symbol HOIL). The Company is a member of the FTSE 250 Index and has Exchangeable Shares listed on the Toronto Stock Exchange (“TSX”) (symbol HOC) and the LSE (symbol HOX).

Heritage is a versatile organisation, dedicated to creating and increasing shareholder value with a portfolio of quality assets managed by a highly experienced team with excellent technical, commercial and financial skills. The Company has producing assets in Nigeria and Russia and exploration assets in Tanzania, Papua New Guinea, Malta, Libya and Pakistan.

C O N T E N T S T H E H E R I TA G E O I L P L C A N N u A L R E P O R T A N D A C C O u N T S 2 0 1 3 C O N S I S T S O F F O u R D O C u M E N T S .

o v e r v i e wHighlights 2013 01Outlook 2014 01

a s s e t sAsset overview 02The Heritage business model 04

s t r a t e g yVision and strategic overview 06

s t r u c t u r eCorporate governance 08

p r o t e c tCorporate Social Responsibility 10

c H i e F e X e c u t i v e ’ s r e v i e w 12

o p e r a t i o n a l r e v i e wNigeria 16Russia 18Tanzania 19Papua New Guinea 20Malta 22Libya 23Pakistan 24Other developments 25

e v o l v eFinancial review 26Risks 32Strategic report glossary 35Advisers and financial calendar IBC

s t r a t e g i c r e p o r tThe Strategic Report provides an overview of Heritage, its processes and a Business Review.

c o r p o r a t e s o c i a l r e s p o n s i b i l i t yThe CSR Report provides detailed information concerning Heritage’s CSR strategy, policies, systems and performance.

c o r p o r a t e g o v e r n a n c eThe Corporate Governance Report provides detailed information on all aspects of Heritage’s corporate governance.

F i n a n c i a l s t a t e m e n t sThe Financial Statements Report provides detailed information on Heritage’s financial position.

H e r i t a g e O i l P l C

0 1

Strategic Report 2013

H i g H l i g H t s2 0 13

O u t l O O k 2 0 14

o p e r at i o n a l – Production from OML 30, Nigeria increased during the year and record gross

production since acquisition, of over 50,000 bopd has been achieved – Maintenance work over OML 30 is progressing as planned – 2013 average production from the interest in OML 30, Nigeria, net to Heritage of

8,919 bopd and net production from Russia of 577 bopd – Continued the work programme in Tanzania through processing of 2D seismic data

on Rukwa which has identified several prospects in the retained Rukwa South licence area. A geochemical survey of the Kyela licence has been completed and interpretation of the data is proceeding to schedule

– Expanded the exploration portfolio with the farm-in to four licences in Papua New Guinea (“PNG”); Petroleum Prospecting Licence 319 (“PPL 319”), Petroleum Retention Licence 13 (“PRL 13”), Petroleum Prospecting Licence 337 (“PPL 337”) and Petroleum Prospecting Licence 437 (“PPL 437”)

– Work programmes in PNG commenced with the acquisition and processing of seismic and evaluation of legacy datasets

F i n a n c i a l 1

– Total revenues, net to Heritage, for 2013 of $431.9 million – Profit after tax from continuing operations of $100.4 million, an increase of 104%

year-on-year – Operating cash flows of $235.3 million in 2013 compared to cash outflows of

$207.5 million in 2012 – Successfully completed the refinancing of the bridge loan facility with a five year

$550 million Senior Secured Revolving Reserves Based Lending Facility drawn by Shoreline Natural Resources Limited (“Shoreline”) in Nigeria

– Heritage cash at 31 December 2013 of $183.8 million

– Continued investment in OML 30 during 2014 including the installation of gas lift compressors, refurbishment of equipment, statutory inspection and testing of all pressure vessels and inspection of all wellheads and pipelines continue to support well optimisation and result in further increases in production

– Development drilling on OML 30 remains on track for commencing in the second half of the year

– As a result of an enforced shut-in at OML 30 during the first quarter of this year, total production, net to Heritage, for 2014 is estimated in the range of 14,500-18,000 bopd

– 2014 expected year end exit gross production rate from OML 30 between 65,000 and 70,000 bopd

– Exploration activity is set to increase with multi-well drilling campaigns planned for PNG and Tanzania

– Continue to look for further opportunities to create value – Intention to become a long-term sustainable dividend payer within the next

12 months

1 The Group has changed the accounting policy for the proportion of Shoreline it consolidates into its results and it now proportionally consolidates Shoreline’s financial results using 90% which is the eventual economic rights before completion of the partner’s option.

All dollars are US dollars unless otherwise stated.

H e r i t a g e O i l P l C

0 2

Strategic Report 2013

a s s e t O v e r v i e w

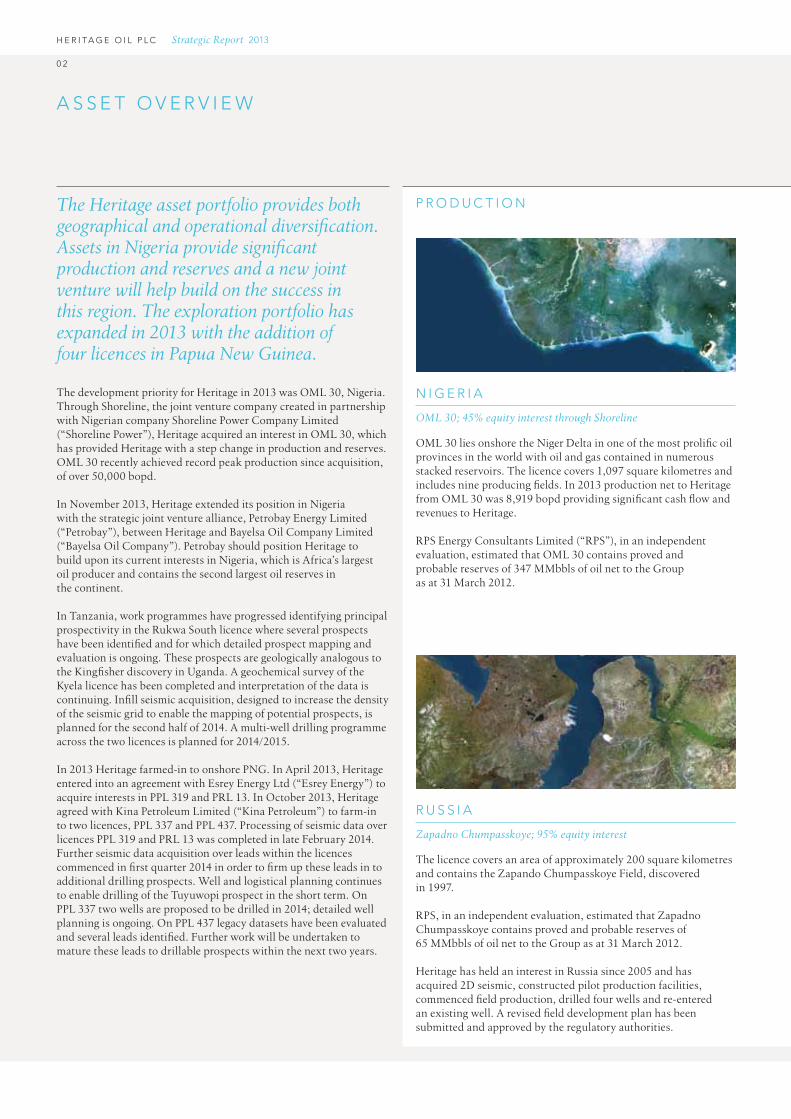

The development priority for Heritage in 2013 was OML 30, Nigeria. Through Shoreline, the joint venture company created in partnership with Nigerian company Shoreline Power Company Limited (“Shoreline Power”), Heritage acquired an interest in OML 30, which has provided Heritage with a step change in production and reserves. OML 30 recently achieved record peak production since acquisition, of over 50,000 bopd.

In November 2013, Heritage extended its position in Nigeria with the strategic joint venture alliance, Petrobay Energy Limited (“Petrobay”), between Heritage and Bayelsa Oil Company Limited (“Bayelsa Oil Company”). Petrobay should position Heritage to build upon its current interests in Nigeria, which is Africa’s largest oil producer and contains the second largest oil reserves in the continent.

In Tanzania, work programmes have progressed identifying principal prospectivity in the Rukwa South licence where several prospects have been identified and for which detailed prospect mapping and evaluation is ongoing. These prospects are geologically analogous to the Kingfisher discovery in Uganda. A geochemical survey of the Kyela licence has been completed and interpretation of the data is continuing. Infill seismic acquisition, designed to increase the density of the seismic grid to enable the mapping of potential prospects, is planned for the second half of 2014. A multi-well drilling programme across the two licences is planned for 2014/2015.

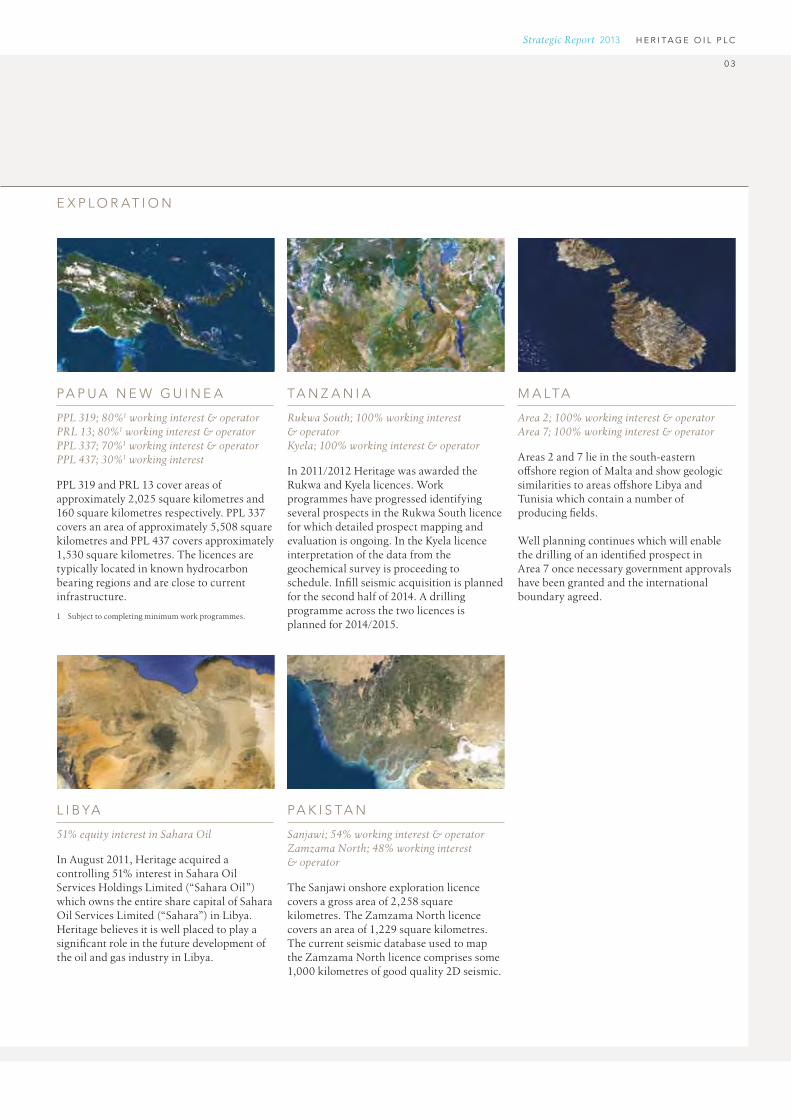

In 2013 Heritage farmed-in to onshore PNG. In April 2013, Heritage entered into an agreement with Esrey Energy Ltd (“Esrey Energy”) to acquire interests in PPL 319 and PRL 13. In October 2013, Heritage agreed with Kina Petroleum Limited (“Kina Petroleum”) to farm-in to two licences, PPL 337 and PPL 437. Processing of seismic data over licences PPL 319 and PRL 13 was completed in late February 2014. Further seismic data acquisition over leads within the licences commenced in first quarter 2014 in order to firm up these leads in to additional drilling prospects. Well and logistical planning continues to enable drilling of the Tuyuwopi prospect in the short term. On PPL 337 two wells are proposed to be drilled in 2014; detailed well planning is ongoing. On PPL 437 legacy datasets have been evaluated and several leads identified. Further work will be undertaken to mature these leads to drillable prospects within the next two years.

The Heritage asset portfolio provides both geographical and operational diversification. Assets in Nigeria provide significant production and reserves and a new joint venture will help build on the success in this region. The exploration portfolio has expanded in 2013 with the addition of four licences in Papua New Guinea.

N i g e r i a

OML 30; 45% equity interest through Shoreline

OML 30 lies onshore the Niger Delta in one of the most prolific oil provinces in the world with oil and gas contained in numerous stacked reservoirs. The licence covers 1,097 square kilometres and includes nine producing fields. In 2013 production net to Heritage from OML 30 was 8,919 bopd providing significant cash flow and revenues to Heritage.

RPS Energy Consultants Limited (“RPS”), in an independent evaluation, estimated that OML 30 contains proved and probable reserves of 347 MMbbls of oil net to the Group as at 31 March 2012.

r u s s i a

Zapadno Chumpasskoye; 95% equity interest

The licence covers an area of approximately 200 square kilometres and contains the Zapando Chumpasskoye Field, discovered in 1997.

RPS, in an independent evaluation, estimated that Zapadno Chumpasskoye contains proved and probable reserves of 65 MMbbls of oil net to the Group as at 31 March 2012.

Heritage has held an interest in Russia since 2005 and has acquired 2D seismic, constructed pilot production facilities, commenced field production, drilled four wells and re-entered an existing well. A revised field development plan has been submitted and approved by the regulatory authorities.

P r O d u c t i O N

H e r i t a g e O i l P l C

0 3

Strategic Report 2013

l i B Ya

51% equity interest in Sahara Oil

In August 2011, Heritage acquired a controlling 51% interest in Sahara Oil Services Holdings Limited (“Sahara Oil”) which owns the entire share capital of Sahara Oil Services Limited (“Sahara”) in Libya. Heritage believes it is well placed to play a significant role in the future development of the oil and gas industry in Libya.

Pa P u a N e w g u i N e a

PPL 319; 80%1 working interest & operator PRL 13; 80%1 working interest & operatorPPL 337; 70%1 working interest & operatorPPL 437; 30%1 working interest

PPL 319 and PRL 13 cover areas of approximately 2,025 square kilometres and 160 square kilometres respectively. PPL 337 covers an area of approximately 5,508 square kilometres and PPL 437 covers approximately 1,530 square kilometres. The licences are typically located in known hydrocarbon bearing regions and are close to current infrastructure.

1 Subject to completing minimum work programmes.

M a lta

Area 2; 100% working interest & operator Area 7; 100% working interest & operator

Areas 2 and 7 lie in the south-eastern offshore region of Malta and show geologic similarities to areas offshore Libya and Tunisia which contain a number of producing fields.

Well planning continues which will enable the drilling of an identified prospect in Area 7 once necessary government approvals have been granted and the international boundary agreed.

Pa k i s ta N

Sanjawi; 54% working interest & operatorZamzama North; 48% working interest & operator

The Sanjawi onshore exploration licence covers a gross area of 2,258 square kilometres. The Zamzama North licence covers an area of 1,229 square kilometres. The current seismic database used to map the Zamzama North licence comprises some 1,000 kilometres of good quality 2D seismic.

ta N Z a N i a

Rukwa South; 100% working interest & operator Kyela; 100% working interest & operator

In 2011/2012 Heritage was awarded the Rukwa and Kyela licences. Work programmes have progressed identifying several prospects in the Rukwa South licence for which detailed prospect mapping and evaluation is ongoing. In the Kyela licence interpretation of the data from the geochemical survey is proceeding to schedule. Infill seismic acquisition is planned for the second half of 2014. A drilling programme across the two licences is planned for 2014/2015.

e x P l O r at i O N

G O V E R N A N C E

R E G I O N A L K

NO

WL

ED

GE

+ C

ON

TA

CT

SC

OR

PO

RA

TE

SO

CI A

L R

ES P O

NS I B I L I T Y

E X P LOR AT ION

+ A

PP

RA

ISA

L

PR

OD

U C T I O N + D E V E L O P ME N

T

CA

PIT

AL

DI S

CI P

L INE

H e r i t a g e O i l P l C

0 4

Strategic Report 2013

t h e h e r i ta g e b u s i n e s s m o d e l

Heritage’s vision is to be a leading exploration and production company. The business model creates the foundation upon which the Company can achieve this.

The Company possesses certain key attributes, discussed overleaf, that provide it with a competitive advantage. Key Performance Indicators (“KPIs”) are used by the Company as one measure of performance and relate to both the underlying business model and the delivery of strategy. In addition, the Company actively monitors certain risks attached to the business model and strategy which are detailed on pages 32 to 34.

Heritage’s business model balances the exploration and appraisal process with cash generating production assets. This is supported through high standards of governance, regional knowledge and contacts and an effective Corporate Social Responsibility (“CSR”) policy framework.

H e r i t a g e O i l P l C

0 5

Strategic Report 2013

K e y per f o r m a n c e i n d i c ato r s co r e at t r i b u t e s

e x p l o r at i o n a n d a p p r a i s a lOur technical team is responsible for assessing new areas for exploration campaigns and ensuring that we have the ability to continually replenish our exploration portfolio. The team will identify core plays and prioritise exploration options across the portfolio. After reviewing the initial exploration programme, the team will propose an appraisal campaign to prove up the size of the discovery and deem whether it is commercial.

Further information on the current asset portfolio can be found in this report on pages 16 to 24.

p r o d u c t i o n a n d d e v e l o p m e n t Once the area has been proven, appraised and confirmed commercially viable, the development team is responsible for providing information to enable the Company to best achieve revenue generation and cash flow by producing the hydrocarbons. A strong regard for the environment and respect for local communities are important.

c a p i ta l d i s c i p l i n eAn appropriate capital structure balancing exploration and operational demands of the portfolio with financing requirements is required to ensure appropriate funding for long-term sustainable growth. This can include monetisation of assets or accessing capital markets and is an ongoing process to ensure efficient allocation of capital.

Further information can be found in the Financial Statements Report.

s u pp o r t e d by

g o v e r n a n c eHeritage seeks to achieve and maintain highest standards and best practice reporting in all areas of governance.

Further information can be found in the Corporate Governance Report.

r e g i o n a l K n o w l e d g e a n d c o n ta c t sRelationships with national and regional governments are a key focus within the business. These relationships provide the Company with the ability to assess risk and provide a competitive edge versus its peers.

Heritage uses a number of financial and operating KPIs that are closely aligned with the underlying business model and its strategy for delivering long-term sustainable growth. These are some of the indicators by which the Company monitors performance.

Several of these are linked to the primary business risks of the Company which are detailed on pages 32 to 34.

Lost Time Injury Frequency Rate (“LTIFR”) – Operationally a top priority is to keep people safe. This includes employees, contractors and local communities where we operate.

Staff turnover – Retaining quality staff is important to ensure delivery of the strategy.

Production from continuing operations – Production is key to revenue and cash generation and Heritage aims to achieve levels in line with annual budgeting and market guidance.

Reserves and contingent resources additions – The core business model involves replenishing the exploration portfolio, ensuring the continued growth of the Company and the potential production profile.

Average realised price – OML 30 Nigeria crude is priced using the Forcados benchmark, which trades at a premium to Brent. In Russia, the realised price improves, in part, as production increases due to better price negotiation and a wider customer base. Prices were not hedged during the year.

2013 2012 2011 2010

LTIFR1 0 0 0 0

Staff turnover2 2% 3% 2% 3%

Production +256% +296% +24% +65%

Reserves and contingent resources additions3 0% +564% +0% +42%

Average realised price4 +180% +8% +45% +26%

1 Lost Time Injury Frequency Rate per 10,000 hours worked. 2 Excludes staff members in Uganda who transferred with the sale of the Ugandan Assets in

2010 and excludes staff members in Kurdistan who transferred with the sale of an interest in the Miran Block in 2012.

3 Management estimates. 4 Realised price is a measure of the price achieved for output sold.

H e r i t a g e O i l P l C

0 6

Strategic Report 2013

E X PA N D

Heritage’s vision is to be a leading exploration and production company and the Company that generates long-term shareholder value.

V i s i o N A N D s t r At E g i c o V E r V i E w

V i s i o N A N D s t r At E g y K E y At t r ibu t E s o f h Er i tAgE

Heritage sets out to achieve its aim of sustainable long-term shareholder value through a strategy that focuses on:

– having a balanced portfolio of oil and gas exploration, development and production assets in a diversified range of countries;

– high-impact international plays with the potential to discover significant hydrocarbon reserves;

– generating cash flow through production; and – managing the portfolio effectively, which can include the

acquisition of value creating opportunities.

This is done against the background of:

– ensuring operations are safe and minimising Lost Time Injuries (“LTIs”) for staff and contractors;

– engagement with local communities who may be affected by our work;

– building successful long-term relationships with local governments, communities and stakeholders in the areas of operation; and

– high standards of corporate governance.

Heritage ensures this is done through:

– a diversified Board, which avoids “group think”; and – employing and retaining a world class team across all departments

of the Group.

Heritage has a unique background with which it can deliver on its strategy because of the following key attributes:

– demonstrated success of first mover advantage in territories such as Uganda and Kurdistan;

– proven track record of monetising assets with the current management team having raised c.$2 billion from asset sales;

– an appreciation of risk, both political and security; – management expertise with a team containing experience of

corporate finance, legal and industry specific skills; – technical expertise with senior members of the team having in

excess of 30 years’ industry experience; – a highly effective network of industry, political and institutional

relationships; – balanced portfolio of assets; and – strategic positioning of assets.

H e r i t a g e O i l P l C

0 7

Strategic Report 2013

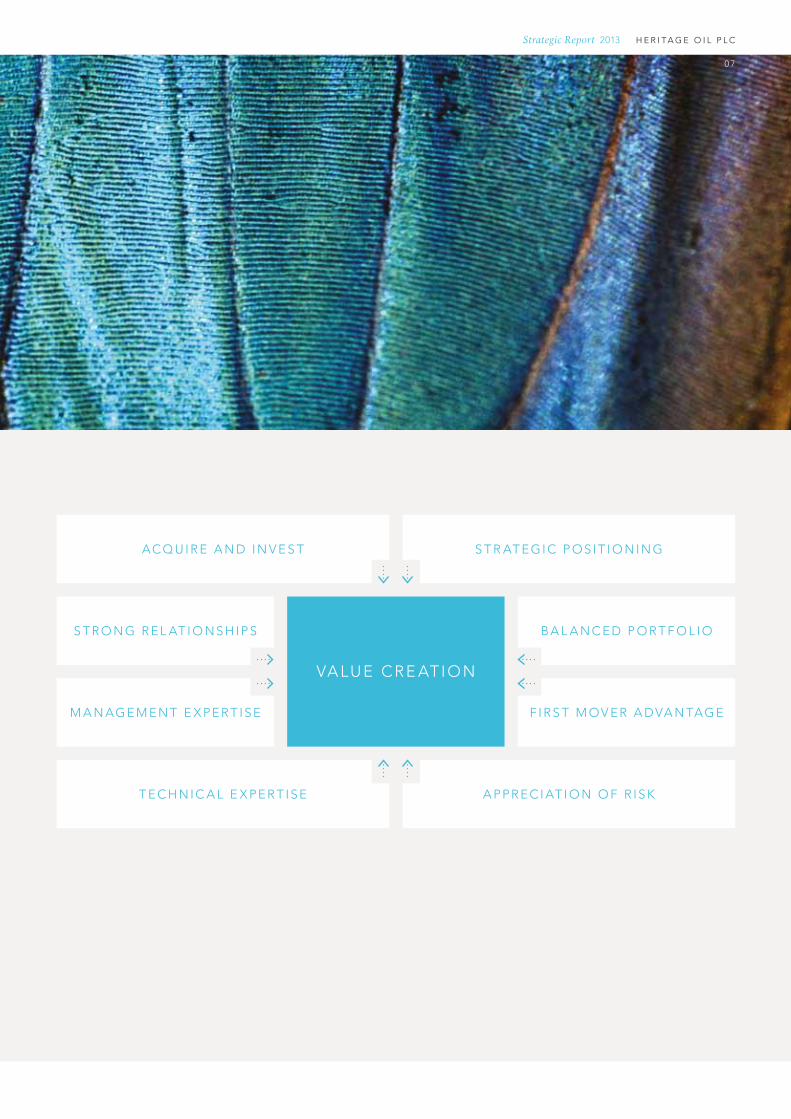

acq u i r e a n d i n V e s t s t r at eG i c p os i t i o n i n G

f i r s t m oV er a dVa n taG e

a ppr ec i at i o n o f r i s K

s t r o n G r el at i o n s h i p s

m a n aG em en t e x per t i s e

t ec h n i c a l e x per t i s e

b a l a n c e d p o r t f o l i o

Va lu e cre at i o n

H e r i t a g e O i l P l C

0 8

Strategic Report 2013

s t r u c t u r e

The Company aims to achieve best practice reporting on corporate governance.

c o r p o r at e G o V e r n a n c e

With a Premium Listing on the LSE and a member of the FTSE 250 Index, the Company is subject to the Financial Conduct Authority’s (“FCA”) Listing Rules and the requirement to explain how it has applied the main principles of the UK Corporate Governance Code (the “Code”).

h o w t h e b o a r d o p e r at e sThe Board delegates certain responsibilities to its committees in line with recommendations of the Code and to facilitate the achievement of business objectives of the Company. The Board is collectively responsible for the success of the Company and each Director must take decisions objectively in the interests of the Company. The Board’s principal role is to set strategy and the parameters within which the Group operates to further its objectives.

d e V e l o p m e n t s i n 2 0 1 3In the UK, last year saw significant changes in the reporting regime with new regulations on remuneration reporting and the introduction of the new Strategic Report which replaces the Business Review. Heritage continues to apply best practice principles in its reporting and has implemented changes to its reporting as a result. This includes new information provided in the Strategic Report on the breakdown of gender information of employees, information about the Group’s Human Rights Policy and information in the CSR Report on Greenhouse Gas (“GHG”) emissions.

l o o K i n G a h e a dWith the acquisition of our Nigerian operations and continued search for development opportunities in line with our strategy, it is important that we have robust risk management review processes in place. This will remain a focus for the forthcoming year. We will also implement actions identified from the Board evaluation exercise and those that may be necessary arising from changes to the Listing Rules concerning controlling shareholders. We will continue to review our narrative reporting to ensure it meets new developments and best practice.

The FCA is consulting on a number of measures designed to enhance protection for minority shareholders. As a Company with a controlling shareholder (a shareholder who owns 30% or more of the voting shares in a company), Heritage will be paying close attention to the new requirements. The new rules are expected to come into force mid-2014, although there will be transitional provisions to allow companies time to comply. We will monitor closely and put in place actions at the appropriate time.

We continue to support open and constructive dialogue with all shareholders on governance, strategy and executive remuneration and welcome any feedback.

H e r i t a g e O i l P l C

0 9

Strategic Report 2013

c o r p o r at e s t r u c t u r e

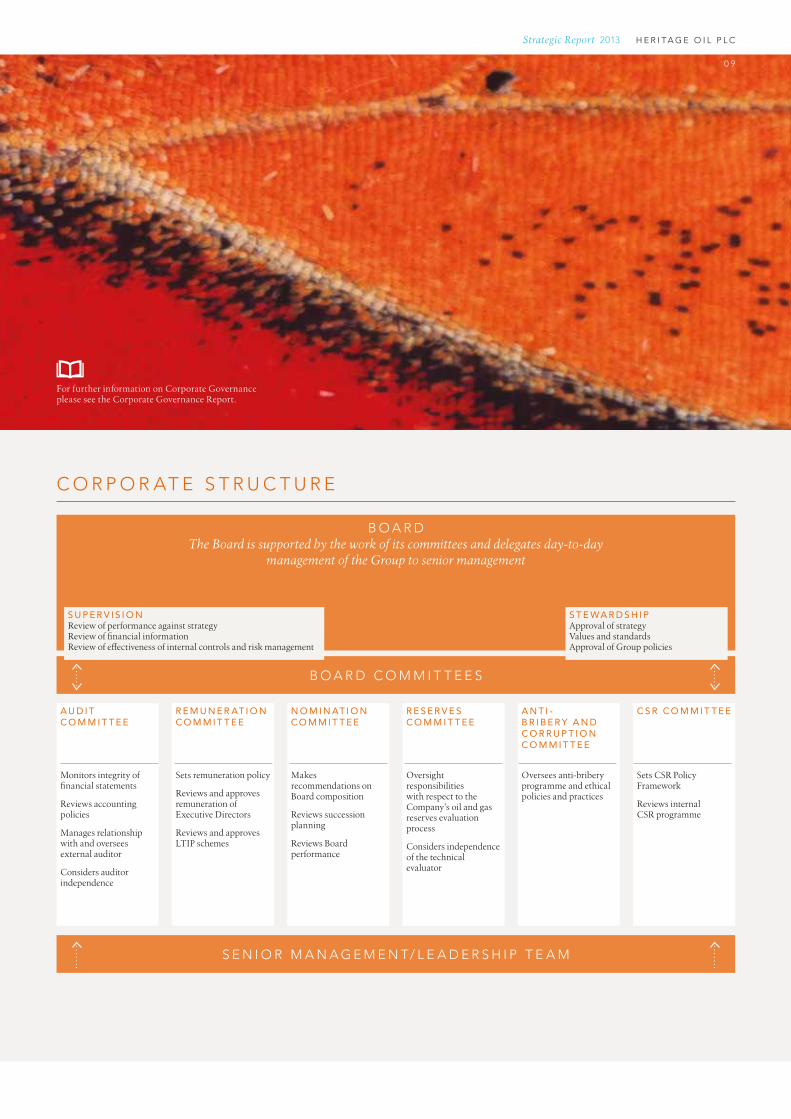

For further information on Corporate Governance please see the Corporate Governance Report.

S U P E R V I S I O NReview of performance against strategyReview of financial informationReview of effectiveness of internal controls and risk management

S T E WA R D S H I PApproval of strategyValues and standardsApproval of Group policies

b o a r dThe Board is supported by the work of its committees and delegates day-to-day

management of the Group to senior management

b o a r d c o m m i t t e e s

A U D I T C O M M I T T E E

R E M U N E R AT I O N C O M M I T T E E

N O M I N AT I O N C O M M I T T E E

R E S E R V E S C O M M I T T E E

A N T I -B R I B E R Y A N D C O R R U P T I O N C O M M I T T E E

C S R C O M M I T T E E

Monitors integrity of financial statements

Reviews accounting policies

Manages relationship with and oversees external auditor

Considers auditor independence

Sets remuneration policy

Reviews and approves remuneration of Executive Directors

Reviews and approves LTIP schemes

Makes recommendations on Board composition

Reviews succession planning

Reviews Board performance

Oversight responsibilities with respect to the Company’s oil and gas reserves evaluation process

Considers independence of the technical evaluator

Oversees anti-bribery programme and ethical policies and practices

Sets CSR Policy Framework

Reviews internal CSR programme

s e n i o r m a n a G e m e n t/ l e a d e r s h i p t e a m

H e r i t a g e O i l P l C

1 0

Strategic Report 2013

p r o t e c t

The business approach of Heritage is underpinned by CSR from the first stages of planning and being awarded a licence, through to exploration and production.

c o r p o r at e s o c i a l r e s p o n s i b i l i t y

V i s i o n a n d s t r at e G y

CSR encompasses the Company’s management of relationships with stakeholders; shareholders, employees, contractors, partners and the local communities in which we work. In addition, it includes the impact the Company has on society and the environment.

o u r c s r V i s i o n – to be a responsible and transparent business in all the areas in

which the Company operates, believing this is important to the operational aim of generating long-term growth for the Company;

– to create lasting legacies for local communities; – to operate to the highest international social, environmental

and safety standards; and – to maintain high standards of corporate governance.

c s r i n a c t i o nOur approach to CSR supports our business model and sets out essential core values that we believe make Heritage a good corporate citizen. The Company sets itself a high standard against which to measure itself and recognises the importance of being a partner of choice. Heritage aims to make a positive contribution in all areas where it operates.

G r e e n h o u s e G a s ( “ G h G ” ) e m i s s i o n s s tat e m e n tFrom 1 October 2013, all UK quoted companies are required to report on their greenhouse gas emissions as part of their annual Directors’ Report. As noted in previous reports, our primary activities in prior years have been in exploration, therefore we have not produced material amounts of GHG emissions and consequentially have not reported this information. However, with the acquisition of OML 30, Nigeria, we have formulated processes to secure all relevant information for reporting GHG emissions.

This assessment has been carried out in accordance with the World Business Council for Sustainable Development and World Resources Institute’s (WBCSD/WRI) Greenhouse Gas Protocol; a Corporate Accounting and Reporting Standard. This protocol is considered current best practice for corporate GHG emissions reporting.

2 0 1 3 G h G e m i s s i o n sTonnes of equivalent CO2 (tCO2e1)

Scope 1 1,949,067

Scope 2 4,115

Scope 3 266

Total 1,953,448

Intensity ratio 0.507 per bbl

1 Carbon dioxide equivalent or CO2e is a term for describing different greenhouse gases in a common unit. For any quantity and type of greenhouse gas, CO2e signifies the amount of CO2 which would have the equivalent global warming impact.

s e t p o l i c i e s

D e v i s e a n D m a i n ta i n s y s t e m s

m e a s u r e a n D m o n i t o r

p e r f o r m a n c e

c o m m u n i c at e a n D r e p o r t

t o s ta k e h o l D e r s

a p p ly s ta k e h o l D e r f e e D b ac k

o u r c s r s t r at e G y

H e r i t a g e O i l P l C

11

Strategic Report 2013

For further information on CSR please see the CSR Report.

o u r a r e a s o f i m pa c t a n d o p p o r t u n i t y

c o m m u n i t y a n d h u m a n r i G h t s m at t e r sWe support human rights, consistent with the stipulations contained within the United Nations Universal Declaration of Human Rights and remain committed to upholding these principles. We endeavour to ensure that these commitments extend to all of our supply chains and we work with our partners and contractors to ensure that they adhere to our contractual requirements.

It is important to the Company that relationships with neighbours and local communities are conducted sensitively and with mutual respect. These relationships recognise that active and enduring partnerships are a central and fundamental element of our business. We aim to promote the sharing of economic benefit created by our activities through the conduct of our community relationships.

G e n d e r d i s c l o s u r eHeritage operates in an environment with low representation of women at all levels of the industry. However, to address this Heritage operates equal opportunity policies in all its areas of activity and seeks to encourage the employment of women. Within Heritage women represent 32 of 143 (23%) total employees, 10 of 36 (27%) senior managers and 1 of 7 (14%) Board members.

d e V e l o p m e n t s i n 2 0 1 3 – approximately $5.3 million spent on CSR-related initiatives,

significantly higher than 2012; – no major environmental incidents, fines or sanctions across

all operations; – zero fatalities and LTIs across all operations; – zero breaches in business conduct policies; – employment of local people remains high across all operations; – secured all relevant information for reporting GHG emissions;

and – continued adoption of Heritage’s CSR policies and systems in

the Shoreline joint venture.

Heritage recognises specific responsibilities in each of six core areas of potential impact and opportunity, specific to the CSR aspects of our activities. Adherence to these CSR values are viewed as a key factor in securing the long-term operational success of the Company.

We aim to apply targets across our identified areas of impact and opportunity, to focus employees and enable the Company and stakeholders to monitor performance.

e n V i r o n m e n t a n d s u s ta i n a b i l i t yAim to make a positive contribution to global sustainability and to protect the environment.

h e a lt h a n d s a f e t yA core element of all activities and a natural priority.

e m p l o y e e sOur ability to create shareholder value is linked with our ability to recruit and retain high calibre staff.

c o m m u n i t y a n d h u m a n r i G h t s Active and enduring relationships are an essential and fundamental element of our business.

b u s i n e s s c o n d u c tWe maintain robust policies with respect to all matters concerning our business conduct.

c o r p o r at e G o V e r n a n c e As a company with a Premium Listing, Heritage maintains high corporate governance standards.

H e r i t a g e O i l P l C

1 2

Strategic Report 2013

R E C O R D B R E A K I N G Y E A R

C h I E f E x E C u t I v E ’ s R E v I E w

A N t h O N Y B u C K I N G h A mC h I E f E x E C u t I v E O f f I C E R

Our progress during 2013 resulted from increasing production in OML 30, where gross licence production exceeded 50,000 bopd in the first quarter of 2014, and on the exploration portfolio, the decision to enter PNG whilst continuing with our work programme in Tanzania. Our balanced portfolio includes significant producing fields and an enlarged exploration portfolio, a combination which provides both geographic and operational diversification.

We are delighted to report operations in Nigeria are progressing and production is increasing. The extensive maintenance backlog is declining and a programme of refurbishment and replacement is resulting in higher production. An extensive list of well optimisation activities continues to be refined. Over the course of this year work will continue to optimise existing wells and facilities to achieve further increases in production. Commencement of development drilling remains on track for the second half of the year.

In 2013 we started to build our exploration portfolio in onshore PNG by farming in to four licences. The exploration activities continue with seismic being acquired and multi-well drilling programmes in PNG and Tanzania planned for 2014/2015.

N I G E R I AO v E R v I E wOn 9 November 2012, Heritage announced that Shoreline, a special purpose private Nigerian company formed between a subsidiary of Heritage and a local Nigerian partner, Shoreline Power Company Limited (“Shoreline Power”), successfully completed the acquisition of a 45% interest in OML 30, together with a 45% interest in other assets under the joint operating agreement for OML 30, for a total cash consideration of $850 million, net of costs. Shoreline was structured with 55% of its equity interest held by Shoreline Power and the remaining 45% held by Heritage, through a wholly owned subsidiary. Under the arrangements Heritage’s economic interest was 97.5%.

2013 has been a remarkable year for Heritage with production increasing 256% and operating cash flows of $235 million. This step change has enabled the Company to continue building production in OML 30, a world class asset, and expand the exploration portfolio through obtaining additional exciting exploration opportunities.

H e r i t a g e O i l P l C

1 3

Strategic Report 2013

Gross production from OML 30 reached over 50,000 bopd, in the first quarter of 2014, in part from the benefit of continued maintenance and rehabilitation programmes. As a result of successful community relations engagement, production from the Uzere West Field recommenced in December 2013 after having been shut-in for over two years.

Production in the first quarter of this year, however, has been impacted as a result of a leak on the undersea tanker loading pipeline at the Forcados crude oil terminal. This stopped export shipments for approximately one month thereby forcing OML 30 to shut-in for a similar time once storage had reached capacity. The terminal resumed shipments in early April, and operations recommenced in OML 30. As a result of the enforced shut-in, 2014 production guidance from OML 30, net to Heritage, is now estimated in the range of 14,000 to 17,500 bopd, with an expected year end gross production exit rate from OML 30 between 65,000 and 70,000 bopd.

In 2013, average production from OML 30 net to Heritage was 8,919 bopd at an average realised price of $114.7/bbl for total net revenues of $423.2 million. Average quarterly production increased during the year with production in Q4 2013 averaging c.13,300 bopd net to Heritage, 63% higher than the average of c.8,150 bopd for the first nine months of 2013.

t h E A s s E tOML 30 lies onshore within the Niger Delta in one of the most prolific oil and gas provinces in the world. The licence covers 1,097 square kilometres and includes eight producing fields with oil and gas contained in numerous stacked reservoirs. The fields are deltaic shallow marine shelf sands at intermediate depth. The fields each contain up to 40 stacked reservoirs and the reservoirs are underlain by substantial aquifers that provide nearly infinite pressure support. The oil is good quality 30° API and typically sells at over 2% premium to Brent.

Since 1961 over 200 wells have been drilled on the licence and the strong aquifer support has enabled the majority of these to be producers. There is the potential to both stabilise and increase production in the near term through refurbishing infrastructure and restarting non-producing existing wells. Additionally, existing wells will be worked over to further increase production.

The licence benefits from infrastructure being in place with nine flow stations that have the capacity to handle 395,000 bpd thereby allowing for the projected production growth. The facilities have been robustly designed and constructed, and benefit from a standard design so equipment can easily be replaced if required.

w O R K P R O G R A m m EThe development of OML 30 remains the priority for the Company. All existing facilities have been reviewed to identify opportunities for improvement and maintenance. A number of comprehensive operational, engineering and community projects that commenced in 2013 are generating significant production increases.

Gas lift is the method of artificial lift within OML 30 and six of the eight fields have gas lift installed with plans to install gas lift in the remaining fields within the next two years. Work on the gas lift systems continues and the installation of new gas lift compressors procured in 2013 is nearing completion. A further five new gas compressors have been ordered to be installed later this year. In addition, replacement of gas lift engines for the existing compressors, installation of diesel generators and replacement of the instrument air compressors is in progress.

Wellhead maintenance has been completed on wells throughout the licence in preparation of flow line and gas line repairs. An extensive list of well optimisation activities continues to be refined. Over the course of this year work will continue aimed at further optimisation of the existing wells and facilities.

The drilling of new wells, planned to commence in the second half of 2014, should provide a significant increase to production with the longer term potential estimated at approximately 300,000 bopd gross.

t R A N s f O R C A D O s P I P E l I N EThe OML 30 acquisition included a 45% interest in the Trans Forcados Pipeline (“TFP”) that transports liquids from OML 30 to the Forcados Terminal. The 97 kilometre long pipeline is 26 inch in diameter and largely buried along most of its length. It has a capacity of 850,000 bpd. The TFP is used by several other operators and provides additional revenue for OML 30 through the tariffs charged. Maintenance and construction work was also undertaken on the TFP in 2013 to complete work that was initiated by the previous operator but delayed due to the prolonged sales process.

C O m m u N I t I E sIn Nigeria, engagement with local communities is fundamental to driving an improved performance from the licence and in generating shared wealth to all stakeholders. To this extent, a not for profit Non-Government Organisation (“NGO”), registered and working in Nigeria and West Africa for over 20 years, was engaged to work with the National Petroleum Development Company, the operator, and Shoreline to ensure a cohesive approach to community issues. Conclusions from extensive consultations with communities within the OML 30 licence area allowed Shoreline to gain an understanding of the fundamental issues of concern arising from activities in the area. This enabled Shoreline to engage accordingly in the interest of the impacted communities as well as helping to restore and build an environment such that all can benefit.

P E t R O B A Y E N E R G Y l I m I t E DIn November 2013, Heritage announced that a wholly owned subsidiary had entered into a joint venture agreement with Bayelsa Oil Company Limited (“Bayelsa Oil Company”), owned by the Bayelsa State government, and another Nigerian company to establish an indigenous Nigerian oil company called Petrobay Energy Limited (“Petrobay”). Heritage has a 45% equity interest in Petrobay which combines Bayelsa Oil Company’s indigenous support from state government and Heritage’s strong technical and financial capability. A number of upstream assets in the state of Bayelsa and the larger Niger Delta region have been identified and Petrobay will engage in both bilateral and competitive auction processes to acquire these assets. Petrobay will position Heritage to build upon its current interests in Nigeria, which is Africa’s largest oil producer and contains the second largest oil reserves on the continent.

H e r i t a g e O i l P l C

1 4

Strategic Report 2013

PA P u A N E w G u I N E AIn 2013 Heritage expanded its portfolio into onshore PNG through the farm-in to four licences. We look forward to developing and accelerating the work programme as this acreage provides the opportunity to discover large gas reserves at a time when regional gas demand is growing rapidly.

In April 2013, Heritage entered into an agreement with Esrey Energy Ltd (“Esrey Energy”) to acquire interests in PPL 319 and PRL 13. The work programme began with the acquisition of the first 62 kilometres of 2D seismic data over the Tuyuwopi structure in PPL 319. Processing of the new seismic data, combined with the reprocessing of c.300 kilometres of legacy seismic data over these licences was completed in late February 2014. Further seismic data acquisition over leads within the licences commenced in first quarter 2014 in order to firm up these leads into additional drillable prospects. Well and logistical planning continues to enable drilling of the Tuyuwopi prospect in the short term.

In October 2013, Heritage agreed with Kina Petroleum Limited (“Kina Petroleum”) to farm-in to two licences, PPL 337 and PPL 437. On PPL 337 two wells are proposed to be drilled this year; one located at the Raintree prospect where a Pliocene/Miocene age reef target is identified, and the second located on, or adjacent to, the Banam anticline where several Neogene age clastic targets have been identified. Detailed well planning is ongoing. PPL 337 has good road access and is close to potential local gas markets and the deep water port of Madang, which may be suitable for LNG export. On PPL 437 legacy datasets have been evaluated and several structural leads imaged. Further work will be undertaken to mature these leads to drillable prospects within the next two years.

tA N Z A N I AIn Tanzania, there is exciting potential in the Rukwa Rift Basin and Kyela licence which we believe share certain geological similarities with the hydrocarbon prolific Albert Basin of Uganda, where we were the pioneering oil company to undertake active exploration in nearly 60 years.

Reprocessing of the legacy seismic data in Rukwa was completed in 2012 and the acquisition of c.600 kilometres of 2D seismic data completed in March 2013. This data has been processed and initial interpretation completed with results indicating that the principal prospectivity lies in the Rukwa South area resulting in the Rukwa North licence being relinquished. Focused interpretation over the Rukwa South licence area has identified several prospects, for which detailed mapping and evaluation is ongoing.

A geochemical survey of the Kyela licence has been completed and interpretation of the data is continuing. Infill seismic acquisition, designed and positioned using all available data, will increase the density of the seismic grid and enhance the mapping of potential prospects. The survey is planned for the second half of 2014. A multi-well drilling programme across the two licences is planned for 2014/2015.

O t h E R A s s E t sR u s s I AProduction averaged 577 bopd for the year, a decrease of 5% year-on-year due to natural well decline and a temporary mechanical issue in 2013 that was resolved later in the year.

Based on positive results from the horizontal well (well 363) drilled in August 2011, a revised field development plan was submitted for Zapadno Chumpasskoye replacing vertical producers with horizontal wells. The change in well type should result in a 50% reduction in the number of production wells required to develop the field and a corresponding reduction in drilling expenditure of approximately $200 million. The development proposal was approved by regulatory authorities at the end of December 2012. Preparations continue for further development drilling in 2014/2015.

l I B YA A N D m A ltAHeritage is actively assisting government officials in both countries to move forward with discussions regarding the associated maritime boundary issues and hydrocarbon rights, ultimately to enable the exploration and development of Area 7 where a large prospect has been identified. Preparations are underway to enable the drilling of the prospect subject to necessary government approvals and the international boundary agreed.

C O R P O R At EN I G E R I A N tA x s tAt u sIn November 2013, Heritage announced that Shoreline had been in discussions with relevant government departments in Nigeria about its tax status. Post period-end the discussions concluded successfully and Shoreline received approval from relevant authorities in Nigeria of a waiver of petroleum profit tax between 2013 and 2017.

B O A R D C h A N G EWe were deeply saddened to report that Sir Michael Wilkes KCB, CBE, passed away in October 2013. He had been a Non-Executive Director of the Company since its listing in the UK in 2008. As well as being Senior Independent Director, Sir Michael was a member of the Audit Committee, Remuneration Committee, Nomination Committee and Anti-Bribery and Corruption Committee.

The Nomination Committee will seek to appoint a new Non-Executive Director in due course and there will be a review of Committee membership. Consideration will also be given for the appropriate candidate to fulfil the role of Senior Independent Director.

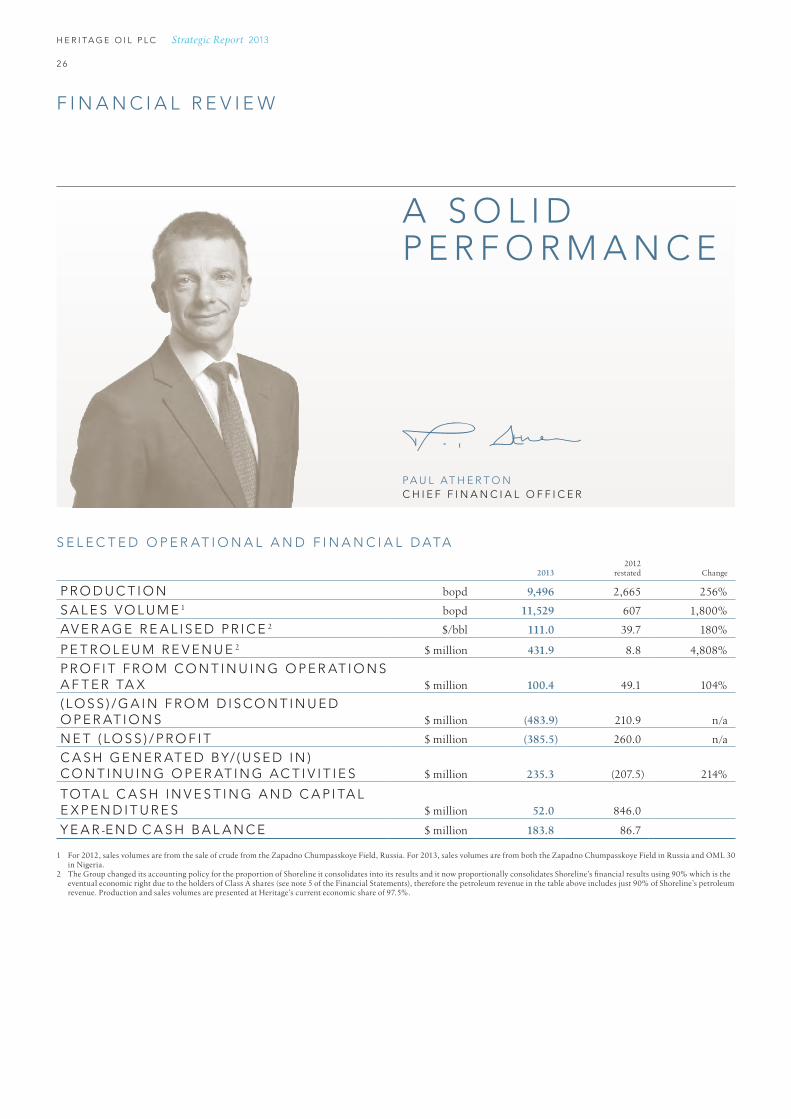

C A s hAs at 31 December 2013, Heritage had a cash position of $183.8 million, which is more than sufficient to cover planned work programmes. Heritage’s profit after tax from continuing operations in 2013 was $100.4 million, up 104% compared to $49.1 million in 2012.

R E f I N A N C I N GIn June 2013, Shoreline successfully completed the refinancing of its bridge loan facility. The new facility is a five year $550 million Senior Secured Revolving Reserves Based Lending Facility (the “RBL Facility”) which can be increased up to $600 million.

C h I E f E x E C u t I v E ’ s R E v I E w C O N t I N u E D

H e r i t a g e O i l P l C

1 5

Strategic Report 2013

The RBL Facility, which is secured at the Nigeria level, replaces the bridge loan executed as part of the acquisition of a 45% interest in the OML 30 licence and provides long-term financing to Shoreline to further develop the licence. The RBL Facility has been arranged on better terms and provides greater flexibility than the bridge loan.

s h O R E l I N E O P t I O NIn December 2012, Heritage announced that Shoreline Power had exercised its call option to acquire a 30% economic interest in Shoreline. Completion of the transaction is expected imminently, following which Heritage will have an effective working interest in OML 30 of 30.71%. On completion, Heritage will receive cash of $31.5 million and the balance will be provided by way of an interest bearing, secured loan from Heritage to Shoreline Power.

P E t R O f R O N t I E R C O R P.Heritage currently holds 19.98% of the outstanding common shares of PetroFrontier Corp (“PetroFrontier”) for investment purposes. PetroFrontier is listed on the TSX Venture Exchange and is focused on a high-impact drilling programme in Australia targeting billions of barrels of resources. The exploration drilling programme commenced in April 2014 with the Oz-Alpha 1 well. Michael Hibberd became a director of PetroFrontier in September 2013.

u G A N D AAs previously announced, a number of proceedings in connection with the sale of the Group’s interests in Blocks 1 and 3A in Uganda to Tullow remain ongoing. Heritage Oil & Gas Limited (“HOGL”) continues to challenge both the Uganda Revenue Authority (“URA”) in the Ugandan courts and, in accordance with the Production Sharing Agreements, the Ugandan government through international arbitration proceedings in London, which commenced in May 2011. The arbitration tribunal ruled in April 2013 that the determination of tax was outside its jurisdiction, but that there were two areas of HOGL’s claims which it will consider, in respect of contractual income tax stabilisation clause protection and breach of other contractual obligations.

That determination by the arbitral tribunal marked the end to the preliminary phase. The proceedings (which are ongoing) have now continued to deal with the merits phase of Heritage’s contractual claims against the Ugandan government and the underlying substantive Ugandan tax matters remain under appeal in the Ugandan courts.

In April 2011, Tullow made a payment to the URA of $313,447,500 and subsequently filed a claim in the High Court in England seeking compensation for alleged breach of contract, in part arising from the URA appointing Tullow as the agent for Heritage, responsible for the payment of the tax alleged owing by Heritage to the URA, and the refusal of HOGL and Heritage to cover Tullow’s payment. Heritage and HOGL filed their Defence and Counterclaim against Tullow.

The case was heard in the High Court in March 2013 and judgment received in June 2013. The Judge found in favour of Tullow and Heritage’s counterclaim was dismissed. Heritage was ordered to pay to Tullow $313,447,500 plus interest accrued on this amount and legal costs which have been paid. Heritage and HOGL made an application to the Court of Appeal for permission to appeal the judgment. Permission to appeal against the judgment was granted in September 2013. This appeal is expected to be heard in the Court of Appeal in May 2014.

C O R P O R At E s O C I A l R E s P O N s I B I l I t YWe continue to mature our approach to CSR and engagement with stakeholders towards achieving a shared future, which is a key element supporting our core business model. We have developed, and continue to review, a policy framework disclosing our essential core values. I am delighted to report that we continue to maintain a strong track record for health and safety which is fundamental in being viewed as a preferred partner.

Community relations are a key factor for success in our new Nigerian operations where there are over 90 communities living on the licence. Through Shoreline we are working with the communities within the OML 30 licence and are striving to improve their lives in the areas of health, education and environment. A comprehensive series of CSR programmes have already commenced in Nigeria.

During 2013, we spent a total of approximately $5.3 million on CSR-related activities with community programmes focused on areas where we were operationally more active. We are looking forward to having a positive contribution within our new areas of activity.

O u t l O O KThis year will see Nigeria remain the focus and continue increasing production and cash flow whilst concurrently progressing with exploration programmes in PNG and Tanzania, in order to generate value from the drill bit. Cash flow generation from OML 30 is now so robust that it is the intention of Heritage to become a long-term sustainable dividend payer commencing within the next 12 months.

As always, I am very grateful to our management team, employees and supportive Board for their dedication and contribution to the progress made by Heritage this past year. Finally, to our shareholders, thank you for your continued support and interest in Heritage.

A N t h O N Y B u C K I N G h A mC h I E f E x E C u t I v E O f f I C E R2 9 A P R I l 2 0 1 4

N I G E R I A

EriemuOweh

Olomoro-Oleh

Oroni

Osioka

Evwreni

Uzere West

O M L 3 0

Warri

Forcados

Escraros

Kokori

Afiesere

H e r i t a g e O i l P l C

1 6

Strategic Report 2013

o p e r at i o n a l r e v i e w

n i g e r i a

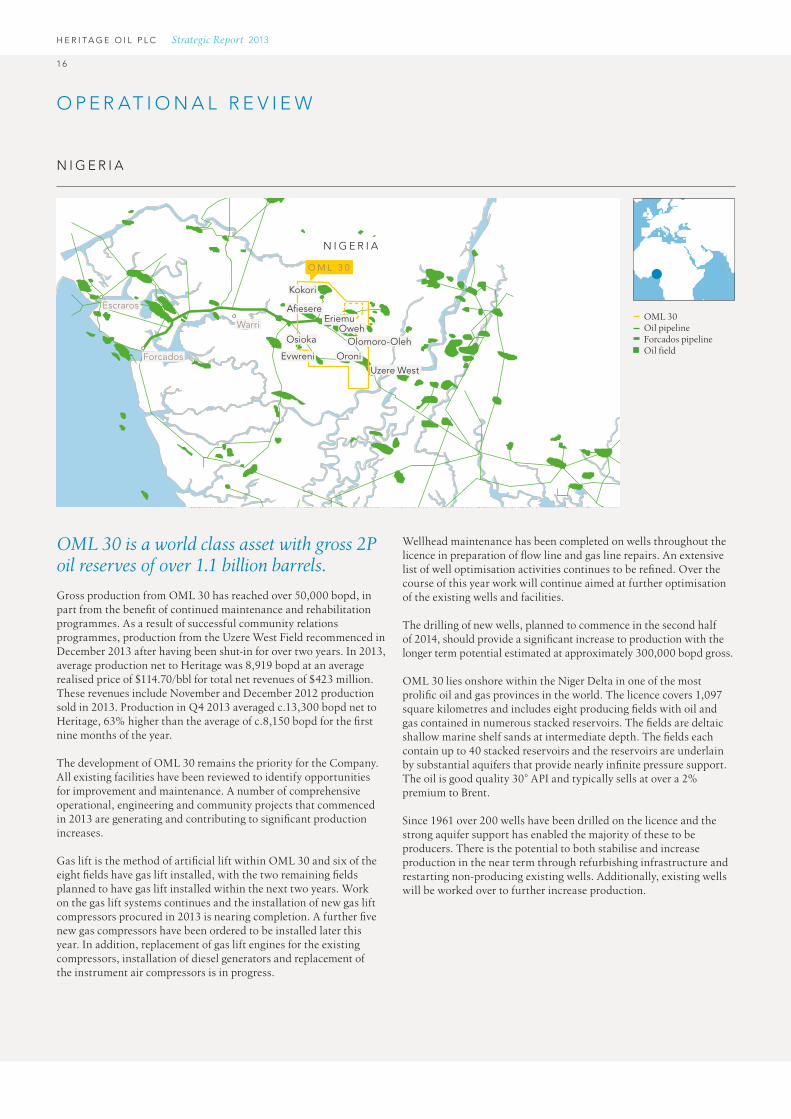

OML 30 is a world class asset with gross 2P oil reserves of over 1.1 billion barrels.

Gross production from OML 30 has reached over 50,000 bopd, in part from the benefit of continued maintenance and rehabilitation programmes. As a result of successful community relations programmes, production from the Uzere West Field recommenced in December 2013 after having been shut-in for over two years. In 2013, average production net to Heritage was 8,919 bopd at an average realised price of $114.70/bbl for total net revenues of $423 million. These revenues include November and December 2012 production sold in 2013. Production in Q4 2013 averaged c.13,300 bopd net to Heritage, 63% higher than the average of c.8,150 bopd for the first nine months of the year.

The development of OML 30 remains the priority for the Company. All existing facilities have been reviewed to identify opportunities for improvement and maintenance. A number of comprehensive operational, engineering and community projects that commenced in 2013 are generating and contributing to significant production increases.

Gas lift is the method of artificial lift within OML 30 and six of the eight fields have gas lift installed, with the two remaining fields planned to have gas lift installed within the next two years. Work on the gas lift systems continues and the installation of new gas lift compressors procured in 2013 is nearing completion. A further five new gas compressors have been ordered to be installed later this year. In addition, replacement of gas lift engines for the existing compressors, installation of diesel generators and replacement of the instrument air compressors is in progress.

Wellhead maintenance has been completed on wells throughout the licence in preparation of flow line and gas line repairs. An extensive list of well optimisation activities continues to be refined. Over the course of this year work will continue aimed at further optimisation of the existing wells and facilities.

The drilling of new wells, planned to commence in the second half of 2014, should provide a significant increase to production with the longer term potential estimated at approximately 300,000 bopd gross.

OML 30 lies onshore within the Niger Delta in one of the most prolific oil and gas provinces in the world. The licence covers 1,097 square kilometres and includes eight producing fields with oil and gas contained in numerous stacked reservoirs. The fields are deltaic shallow marine shelf sands at intermediate depth. The fields each contain up to 40 stacked reservoirs and the reservoirs are underlain by substantial aquifers that provide nearly infinite pressure support. The oil is good quality 30° API and typically sells at over a 2% premium to Brent.

Since 1961 over 200 wells have been drilled on the licence and the strong aquifer support has enabled the majority of these to be producers. There is the potential to both stabilise and increase production in the near term through refurbishing infrastructure and restarting non-producing existing wells. Additionally, existing wells will be worked over to further increase production.

OML 30 Oil pipeline Forcados pipeline Oil field

H e r i t a g e O i l P l C

1 7

Strategic Report 2013

The licence benefits from infrastructure being in place with nine flow stations that have the capacity to handle 395,000 bpd thereby allowing for the projected production growth. The facilities have been robustly designed and constructed, and benefit from a standard design so equipment can easily be replaced if required.

The OML 30 acquisition included a 45% interest in the segment of the TFP that transports liquids from OML 30 to the Forcados Terminal. The 97 kilometre long pipeline is 26 inch in diameter and largely buried along most of its length. It has a capacity of 850,000 bpd. The TFP is used by several other operators and provides additional revenue for OML 30 through the tariffs charged. Maintenance and construction work was also undertaken on the Trans Forcados Pipeline (“TFP”) to complete work that was initiated by the previous operator but delayed due to the prolonged sales process.

In Nigeria, engagement with local communities is fundamental to driving an improved performance from the licence and in generating shared wealth to all stakeholders. To this extent, a not for profit Non-Government Organisation (“NGO”), registered and working in Nigeria and West Africa for over 20 years, was engaged to work with the National Petroleum Development Company, the operator, and Shoreline to ensure a cohesive approach to community issues. Conclusions from extensive consultations with communities within the OML 30 licence area allowed Shoreline to gain an understanding of the fundamental issues of concern arising from activities in the area. This enabled Shoreline to engage accordingly in the interest of the impacted communities as well as helping to restore and build an environment such that all can benefit.

In December 2012, Heritage announced that Shoreline Power had exercised its call option to acquire a 30% economic interest in Shoreline. Completion of the transaction is expected imminently, following which Heritage will have an effective working interest in OML 30 of 30.71%. On completion, Heritage will receive cash of $31.5 million and the balance will be provided by way of an interest bearing, secured loan from Heritage to Shoreline Power.

In November 2013, Heritage announced that a wholly owned subsidiary has entered into a joint venture agreement with Bayelsa Oil Company, owned by the Bayelsa State government and another Nigerian company, to establish an indigenous Nigerian oil company called Petrobay. Heritage has a 45% equity interest in Petrobay which combines Bayelsa Oil Company’s indigenous support from state government and Heritage’s strong technical and financial capability.

A number of upstream assets in the state of Bayelsa and the larger Niger Delta region have been identified and Petrobay will engage in both bilateral and competitive auction processes to acquire these assets. Petrobay will look to enable Heritage to build upon its current interests in Nigeria, which is Africa’s largest oil producer and contains the second largest oil reserves in the continent.

Gross Remaining ReservesHeritage Group

Net Entitlement Reserves

o M l 3 0 – S u M M a r y o f r e S e r v e S 1 , 2

Gross ofRoyalty

(mmstb)

Net ofRoyalty

(mmstb)

Gross ofRoyalty

(mmstb)

Net ofRoyalty

(mmstb)

Proved Reserves (1P) 538 430 168 134

Proved & Probable Reserves (2P) 1,114 891 347 277

Proved & Probable & Possible Reserves (3P) 1,733 1,387 539 431

1 Post exercise of Shoreline Power option.2 As per RPS, as at 31 March 2012.

Z A PA D N OC H U M PA S S KOY EL I C E N C E

W E S T E R NS I B E R I A

H e r i t a g e O i l P l C

1 8

Strategic Report 2013

o p e r at i o n a l r e v i e w c o n t i n u e d

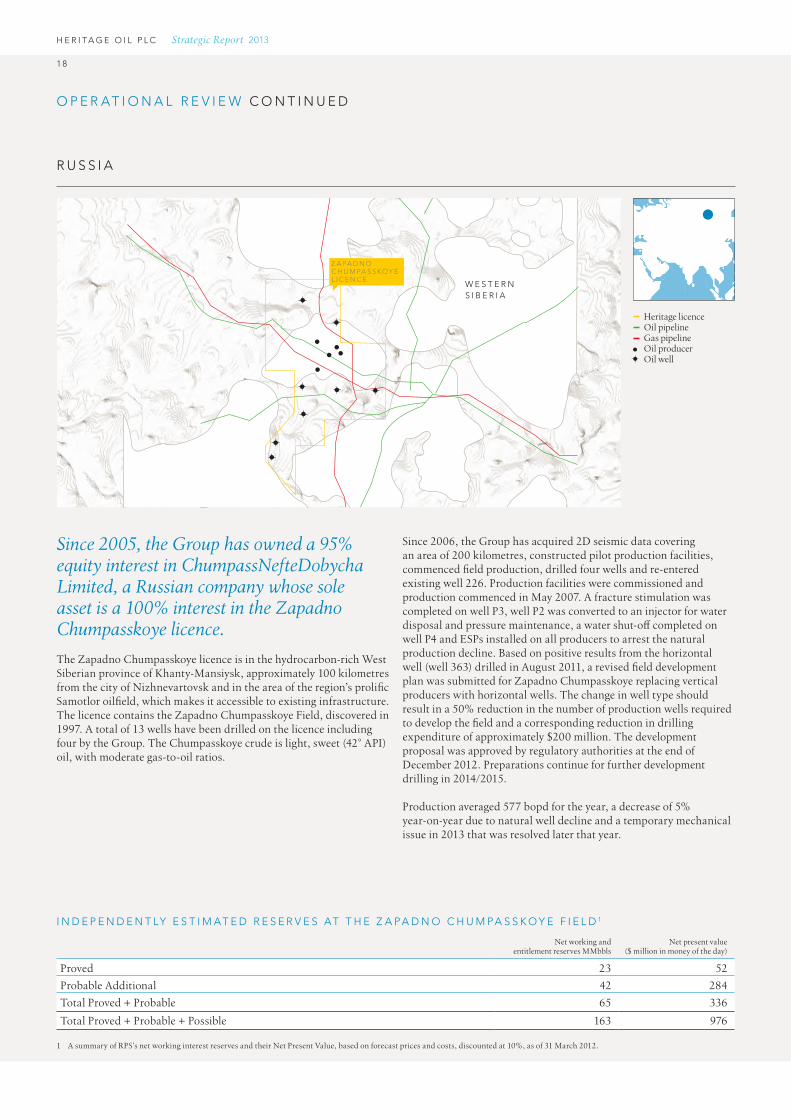

Since 2005, the Group has owned a 95% equity interest in ChumpassNefteDobycha Limited, a Russian company whose sole asset is a 100% interest in the Zapadno Chumpasskoye licence.

The Zapadno Chumpasskoye licence is in the hydrocarbon-rich West Siberian province of Khanty-Mansiysk, approximately 100 kilometres from the city of Nizhnevartovsk and in the area of the region’s prolific Samotlor oilfield, which makes it accessible to existing infrastructure. The licence contains the Zapadno Chumpasskoye Field, discovered in 1997. A total of 13 wells have been drilled on the licence including four by the Group. The Chumpasskoye crude is light, sweet (42° API) oil, with moderate gas-to-oil ratios.

Since 2006, the Group has acquired 2D seismic data covering an area of 200 kilometres, constructed pilot production facilities, commenced field production, drilled four wells and re-entered existing well 226. Production facilities were commissioned and production commenced in May 2007. A fracture stimulation was completed on well P3, well P2 was converted to an injector for water disposal and pressure maintenance, a water shut-off completed on well P4 and ESPs installed on all producers to arrest the natural production decline. Based on positive results from the horizontal well (well 363) drilled in August 2011, a revised field development plan was submitted for Zapadno Chumpasskoye replacing vertical producers with horizontal wells. The change in well type should result in a 50% reduction in the number of production wells required to develop the field and a corresponding reduction in drilling expenditure of approximately $200 million. The development proposal was approved by regulatory authorities at the end of December 2012. Preparations continue for further development drilling in 2014/2015.

Production averaged 577 bopd for the year, a decrease of 5% year-on-year due to natural well decline and a temporary mechanical issue in 2013 that was resolved later that year.

r u S S i a

i n d e p e n d e n t ly e S t i M at e d r e S e r v e S at t H e Z a pa d n o c H u M pa S S K o y e f i e l d 1

Net working andentitlement reserves MMbbls

Net present value($ million in money of the day)

Proved 23 52

Probable Additional 42 284

Total Proved + Probable 65 336

Total Proved + Probable + Possible 163 976

1 A summary of RPS’s net working interest reserves and their Net Present Value, based on forecast prices and costs, discounted at 10%, as of 31 March 2012.

Heritage licence Oil pipeline Gas pipeline

Oil producer Oil well

U N I T E D R E P U B L I C O F

T A N Z A N I A

Z A M B I A

K E N Y A

R U K W A S O U T H

K Y E L A

Mombasa

Dodoma

Ivuna-1Galula-1

Dar es Salaam

H e r i t a g e O i l P l C

1 9

Strategic Report 2013

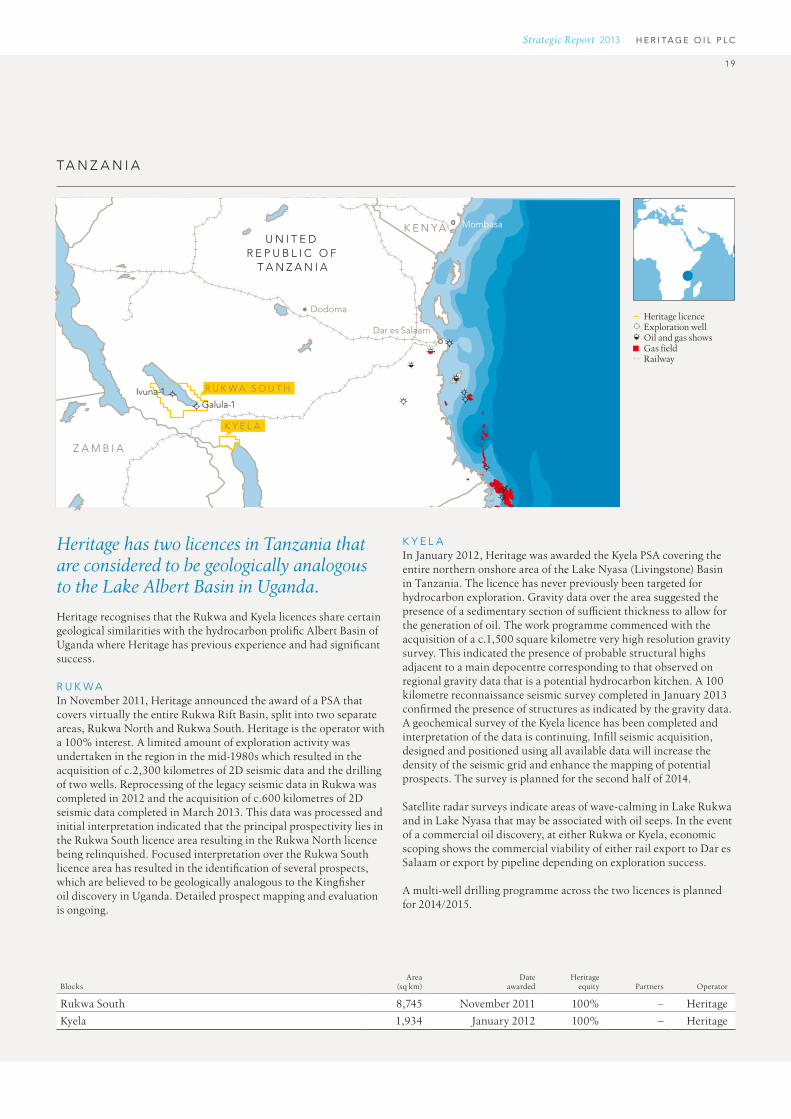

Heritage has two licences in Tanzania that are considered to be geologically analogous to the Lake Albert Basin in Uganda.

Heritage recognises that the Rukwa and Kyela licences share certain geological similarities with the hydrocarbon prolific Albert Basin of Uganda where Heritage has previous experience and had significant success.

r u K w aIn November 2011, Heritage announced the award of a PSA that covers virtually the entire Rukwa Rift Basin, split into two separate areas, Rukwa North and Rukwa South. Heritage is the operator with a 100% interest. A limited amount of exploration activity was undertaken in the region in the mid-1980s which resulted in the acquisition of c.2,300 kilometres of 2D seismic data and the drilling of two wells. Reprocessing of the legacy seismic data in Rukwa was completed in 2012 and the acquisition of c.600 kilometres of 2D seismic data completed in March 2013. This data was processed and initial interpretation indicated that the principal prospectivity lies in the Rukwa South licence area resulting in the Rukwa North licence being relinquished. Focused interpretation over the Rukwa South licence area has resulted in the identification of several prospects, which are believed to be geologically analogous to the Kingfisher oil discovery in Uganda. Detailed prospect mapping and evaluation is ongoing.

K y e l aIn January 2012, Heritage was awarded the Kyela PSA covering the entire northern onshore area of the Lake Nyasa (Livingstone) Basin in Tanzania. The licence has never previously been targeted for hydrocarbon exploration. Gravity data over the area suggested the presence of a sedimentary section of sufficient thickness to allow for the generation of oil. The work programme commenced with the acquisition of a c.1,500 square kilometre very high resolution gravity survey. This indicated the presence of probable structural highs adjacent to a main depocentre corresponding to that observed on regional gravity data that is a potential hydrocarbon kitchen. A 100 kilometre reconnaissance seismic survey completed in January 2013 confirmed the presence of structures as indicated by the gravity data. A geochemical survey of the Kyela licence has been completed and interpretation of the data is continuing. Infill seismic acquisition, designed and positioned using all available data will increase the density of the seismic grid and enhance the mapping of potential prospects. The survey is planned for the second half of 2014.

Satellite radar surveys indicate areas of wave-calming in Lake Rukwa and in Lake Nyasa that may be associated with oil seeps. In the event of a commercial oil discovery, at either Rukwa or Kyela, economic scoping shows the commercial viability of either rail export to Dar es Salaam or export by pipeline depending on exploration success.

A multi-well drilling programme across the two licences is planned for 2014/2015.

ta n Z a n i a

BlocksArea

(sq km)Date

awardedHeritage

equity Partners Operator

Rukwa South 8,745 November 2011 100% – Heritage

Kyela 1,934 January 2012 100% – Heritage

Heritage licence Exploration well Oil and gas shows Gas field Railway

P A P U AN E W G U I N E A

KeremaKumul Marine Terminal

Port Moresby

Madang

Popondetta

Lae

Daru

P P L 3 1 9

P R L 1 3

P P L 3 3 7

P P L 4 3 7

H e r i t a g e O i l P l C

2 0

Strategic Report 2013

pa p u a n e w g u i n e a

o p e r at i o n a l r e v i e w c o n t i n u e d

In 2013, Heritage expanded its portfolio into onshore Papua New Guinea (“PNG”) through the farm-in to four licences. This acreage provides the opportunity to discover large gas reserves at a time when regional gas demand is growing rapidly.

p p l 3 1 9 / p r l 1 3In April 2013, Heritage announced the farm-in to Petroleum PPL 319 and PRL 13. The contiguous licences are located onshore and have respective gross areas of approximately 2,025 and 160 square kilometres. Heritage has been appointed operator, and in return for earning an 80% working interest in both licences Heritage will fund the costs of seismic acquisition and drilling an exploration well. In addition, Heritage made a $4 million contribution to Esrey Energy Limited’s (formerly LNG Energy Limited) back costs on the licences.

The licences are located at the junction of the Papuan fold belt and the Miocene carbonate platform where there are producing fields and discoveries including the multi-TCF Triceratops and Elk/Antelope gas discoveries.

The licences benefit from being close to current and under-construction infrastructure with the Kutubu oil export pipeline and the PNG Liquefied Natural Gas pipeline crossing the acreage. The licences also benefit from the Kikori River which provides a link to the open sea, thereby providing additional transport options.

The work programme in 2013 began with the acquisition of the first 62 kilometres of 2D seismic data over the Tuyuwopi structure in PPL 319. Processing of the new seismic data, combined with the reprocessing of c.300 kilometres of legacy seismic data over these licences was completed in late February 2014. Further seismic data acquisition over leads within the licences has commenced in first quarter 2014, in order to firm up these leads as additional drilling prospects. Well and logistical planning continues to enable drilling of the Tuyuwopi prospect in the short term.

Heritage licence Oil field Gas field Oil pipeline Gas pipeline Oil pipeline proposed Gas pipeline proposed

H e r i t a g e O i l P l C

2 1

Strategic Report 2013

p p l 3 3 7In October 2013, Heritage announced the farm-in to PPL 337, which has a gross area of approximately 5,508 square kilometres. Heritage will earn a 70% working interest and operatorship, by funding the costs of drilling two shallow exploration wells. In addition, Heritage made a $500,000 contribution to Kina Petroleum’s back costs on the licence and in the event of a discovery, Heritage will carry Kina Petroleum’s costs of up to 100 kilometres of appraisal seismic data.

PPL 337 is located within the south-eastern part of the North New Guinea Basin, in the under explored Ramu Sub Basin. To date, three prospects and one advanced lead have been identified on the licence. A local depocentre has been identified in proximity to mapped prospects and the presence of gas seeps within the licence indicates an active petroleum system. These mapped prospects are in clastic and carbonate reef geological settings, with principal exploration targets at the large Banam anticline with an area of over 200 square kilometres and potential reef structures in the north of the licence respectively.

Legacy datasets, which include regional gravity and magnetic data, surface geological mapping, c.140 kilometres of 2D seismic acquired in 1997 and offset well data have been evaluated. Reprocessing of seismic data over the Banam anticline is ongoing.

Two wells are proposed to be drilled this year; one located at the Raintree prospect where a Pliocene/Miocene age reef target is identified, and the second located on or adjacent to the Banam anticline where several Neogene age clastic targets have been identified. The shallow nature of the targets identified makes the early drilling of wells the most cost effective method of assessing the potential within the licence. Detailed well planning to enable drilling of the two wells in 2014 is ongoing.

PPL 337 has good road access and is close to potential local gas markets and the deep water port of Madang, which may be suitable for LNG export.

p p l 4 3 7In October 2013, Heritage announced the farm-in to PPL 437 that has a gross area of approximately 1,530 square kilometres. Heritage will earn an initial 30% working interest, by carrying Kina Petroleum’s seismic acquisition costs for a minimum of 100 kilometres of data and make a $300,000 contribution towards Kina Petroleum’s back costs on the licence. During this phase Heritage will be the operator of the seismic work programme. Additionally, Heritage has an option to acquire a further 20% working interest from Kina Petroleum and operatorship of the licence by carrying Kina Petroleum through the drilling of an exploration well.

PPL 437 lies within a proven hydrocarbon system less than 20 kilometres north of the Elevala and Ketu c.1.0 TCF gas condensate fields and the recent Tingu-1 discovery well. Legacy datasets, which include regional gravity and magnetic data and surface geological mapping, in addition to c.250 kilometres of 2D seismic, have been evaluated. The identified prospectivity in the licence is within several structural leads imaged on this legacy seismic data which will be incorporated into this process with the aim of maturing these leads to drillable prospects within the next two years.

The licence is located close to an existing gas pipeline from PNG LNG’s gas fields to the LNG plant in Port Moresby and gas commercialisation options for the Elevala and Ketu fields include a mid-scale LNG project with a LNG plant to be located at Daru.

BlockArea

(sq km)Date

farm-inHeritage

equity1 Partners Operator

PPL 319 2,025 April 2013 80% Esrey Energy Heritage

PRL 13 160 April 2013 80% Esrey Energy Heritage

PPL 337 5,508 October 2013 70% Kina Petroleum Heritage

PPL 437 1,530 October 2013 30% Kina PetroleumCott Oil & Gas

Kina Petroleum

1 Heritage will earn its equity by funding minimum work programmes.

Tunis

Siracusa

Medina Bank-1

Sfax

Tripoli

T U N I S I A

L I B Y A

A R E A 2

A R E A 7

M A L T A

H e r i t a g e O i l P l C

2 2

Strategic Report 2013

The Group holds a PSC with the Maltese government for a 100% interest in Areas 2 and 7 in the south-eastern offshore region of Malta.

The Maltese licences cover almost 18,000 square kilometres and are situated approximately 80 kilometres (Area 2) and 140 kilometres (Area 7) offshore, in water depths of up to approximately 300 metres. The two Areas are close to, and geologically similar to, a number of producing fields offshore Libya, such as the Bouri field, and Tunisia.

With only one well previously drilled in Area 2, the Medina Bank-1 well in 1980 which did not reach its target, both licences are considered to be underexplored. Although drilled to a depth of 1,225 metres, the well failed to reach the deeper objective horizons, estimated to be between 1,500 and 4,500 metres.

The interpretation of seismic data in Heritage’s extensive dataset of approximately 5,000 kilometres of 2D seismic, has confirmed a highly attractive Lower Eocene carbonate reef play. Detailed prospect level mapping within Area 7 has identified a prospect with both Eocene and Cretaceous reef targets. These primary targets are recognised as major hydrocarbon producing zones in the central part of the Mediterranean.

In addition, the Company has recognised the presence of a south-to-north trending shelf margin on the eastern part of the blocks where a number of attractive reef prospects have been mapped.

Preparations are underway to enable the drilling of the prospect identified in Area 7 subject to relevant government approvals and the international boundary agreed.

BlocksArea

(sq km)Date

awardedHeritage

equity

Area 2 9,190 December 2007 100%

Area 7 8,778 December 2007 100%

M a lta

o p e r at i o n a l r e v i e w c o n t i n u e d

Heritage licence Exploration well Oil and gas shows Oil field Gas field

Tripoli

Sirte

Benghazi

A L G E R I A

N I G E R C H A D

E G Y P TL I B Y A

H e r i t a g e O i l P l C

2 3

Strategic Report 2013

l i b ya

In August 2011, Heritage acquired a controlling 51% interest in Sahara Oil which holds the necessary long-term permits and licences to provide oil field services in Libya.

Heritage has pursued its strategy of “first mover advantage” through pursuing participation in the restoration of the Libyan oil production sector which presents a dynamic and evolving environment.

Libya, which has the largest proven hydrocarbon reserves in Africa, is considered to be a highly attractive oil province due to the low cost of oil recovery, high quality oil which is generally sweet with API gravity ranging between 32–44º, proximity to European markets and well developed infrastructure.

A wholly owned subsidiary of Heritage acquired a 51% equity interest and control of Sahara Oil which owns the entire share capital of Sahara, a Libyan registered company providing services to the oil industry.

Sahara Oil was established in April 2009 and has been granted long-term licences to provide full oil field services in Libya, including the ability to drill onshore and offshore and hold both oil and gas licences. Our efforts have the aim of playing a key role in the substantial rehabilitation work needed to resume, maintain and increase Libya’s hydrocarbon production in line with National Oil Company (“NOC”) and Oil Ministry targets.

Heritage established a base in Benghazi in the first half of 2011, having been in discussions with senior members of the National Transitional Council, the legitimate and recognised government of Libya at the time, as well as with its Executive Committee, the NOC and certain subsidiaries. The dialogue with parties in country that would enable Heritage to participate in the rehabilitation of Libya’s hydrocarbons sector is ongoing.

Oil field Gas field Oil pipeline Gas pipeline

Quetta

PeshawarIslamabad

Lahore

S A N J A W I

Z A M Z A M A N O R T H

IR A N

A F G H A N I S T A N

I N D I A

P A K I S T A N

H e r i t a g e O i l P l C

2 4

Strategic Report 2013

pa K i S ta n

o p e r at i o n a l r e v i e w c o n t i n u e d

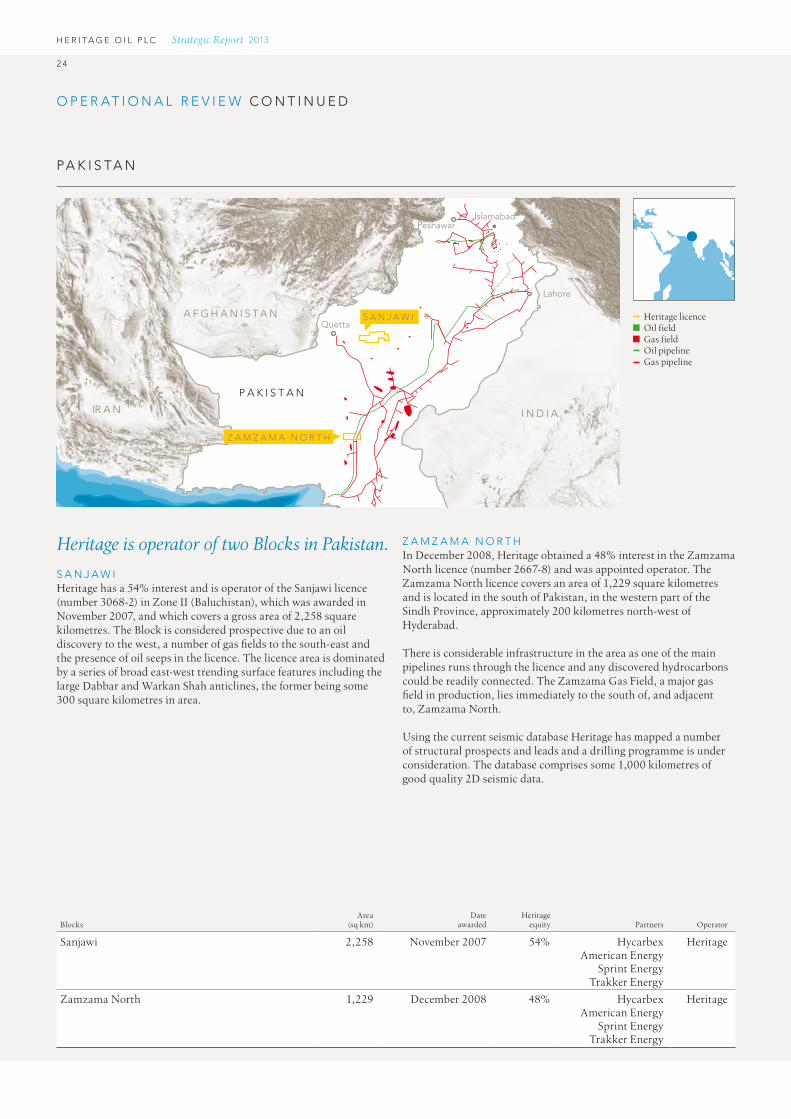

Heritage is operator of two Blocks in Pakistan.

S a n J a w iHeritage has a 54% interest and is operator of the Sanjawi licence (number 3068-2) in Zone II (Baluchistan), which was awarded in November 2007, and which covers a gross area of 2,258 square kilometres. The Block is considered prospective due to an oil discovery to the west, a number of gas fields to the south-east and the presence of oil seeps in the licence. The licence area is dominated by a series of broad east-west trending surface features including the large Dabbar and Warkan Shah anticlines, the former being some 300 square kilometres in area.

Z a M Z a M a n o r t HIn December 2008, Heritage obtained a 48% interest in the Zamzama North licence (number 2667-8) and was appointed operator. The Zamzama North licence covers an area of 1,229 square kilometres and is located in the south of Pakistan, in the western part of the Sindh Province, approximately 200 kilometres north-west of Hyderabad.

There is considerable infrastructure in the area as one of the main pipelines runs through the licence and any discovered hydrocarbons could be readily connected. The Zamzama Gas Field, a major gas field in production, lies immediately to the south of, and adjacent to, Zamzama North.

Using the current seismic database Heritage has mapped a number of structural prospects and leads and a drilling programme is under consideration. The database comprises some 1,000 kilometres of good quality 2D seismic data.

BlocksArea

(sq km)Date

awardedHeritage

equity Partners Operator

Sanjawi 2,258 November 2007 54% Hycarbex HeritageAmerican Energy

Sprint EnergyTrakker Energy

Zamzama North 1,229 December 2008 48% Hycarbex HeritageAmerican Energy

Sprint EnergyTrakker Energy

Heritage licence Oil field Gas field Oil pipeline Gas pipeline

H e r i t a g e O i l P l C

2 5

Strategic Report 2013

o t H e r d e v e l o p M e n t S

d i S p o S a l o f u g a n d a n a S S e t SAs previously announced, a number of proceedings in connection with the sale of the Group’s interests in Blocks 1 and 3A in Uganda to Tullow remain ongoing. Heritage Oil & Gas Limited (“HOGL”) continues to challenge both the Uganda Revenue Authority (“URA”) in the Ugandan courts and, in accordance with the Production Sharing Agreements, the Ugandan government through international arbitration proceedings in London, which commenced in May 2011. The arbitration tribunal ruled in April 2013 that the determination of tax was outside its jurisdiction, but that there were two areas of HOGL’s claims which it will consider, in respect of contractual income tax stabilisation clause protection and breach of other contractual obligations.

That determination by the arbitral tribunal marked the end to the preliminary phase. The proceedings (which are ongoing) have now continued to deal with the merits phase of Heritage’s contractual claims against the Ugandan government and the underlying substantive Ugandan tax matters remain under appeal in the Ugandan courts.