expatriate taxation inbound and outbound deputation - mr... · expatriate taxation inbound and...

TRANSCRIPT

Expatriate Taxation

Inbound and Outbound Deputation

Workshop on Taxation of Foreign Remittances

C. A. Gupta

20 December 2013

©2013 Deloitte Haskins & Sells

Contents

• Basis of income tax charge

• Key provisions - ITA

• Key provisions - DTAA

• Tax rate

• Grossing up

• Specific Issues

• Taxation of Stock Awards

• Case Studies

©2013 Deloitte Haskins & Sells

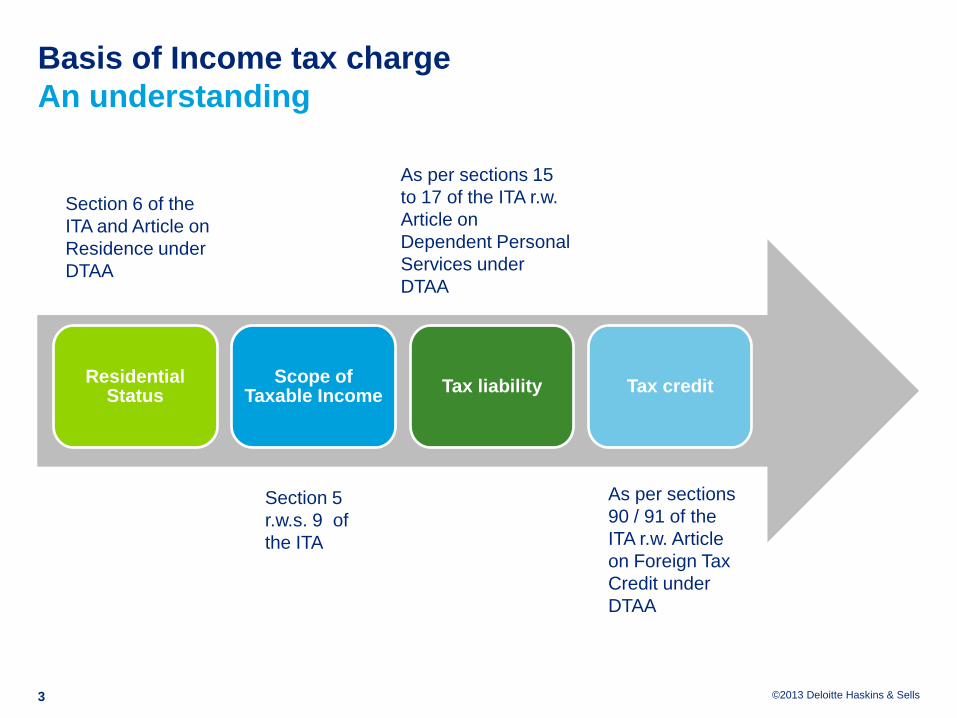

Basis of Income tax charge

An understanding

Residential Status

Scope of Taxable Income

Tax liability Tax credit

3

Section 6 of the

ITA and Article on

Residence under

DTAA

Section 5

r.w.s. 9 of

the ITA

As per sections 15

to 17 of the ITA r.w.

Article on

Dependent Personal

Services under

DTAA

As per sections

90 / 91 of the

ITA r.w. Article

on Foreign Tax

Credit under

DTAA

©2013 Deloitte Haskins & Sells

Key provisions - ITA

©2013 Deloitte Haskins & Sells

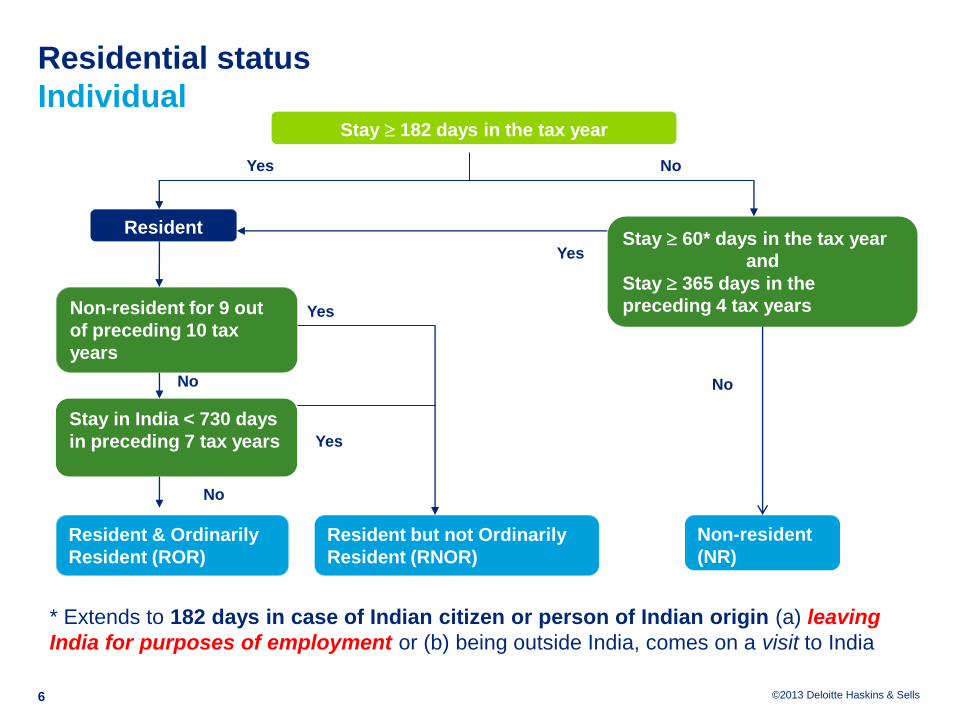

Residential status (Section 6 of ITA)

Individual

• Depends upon the number of days stay in India.

• The residential status of individual taxpayer can be categorized as:

• Resident and ordinarily resident (“ROR”)

• Resident but not ordinarily resident (“RNOR”)

• Non-resident (“NR”)

5

Tax year in India is from April to March

©2013 Deloitte Haskins & Sells

Residential status

Individual

6

Yes No

Yes

No

Yes

No

Yes

No

Stay 182 days in the tax year

Stay 60* days in the tax year

and

Stay 365 days in the

preceding 4 tax years Non-resident for 9 out

of preceding 10 tax

years

Resident & Ordinarily

Resident (ROR)

Resident but not Ordinarily

Resident (RNOR)

Non-resident

(NR)

Resident

Stay in India < 730 days

in preceding 7 tax years

* Extends to 182 days in case of Indian citizen or person of Indian origin (a) leaving

India for purposes of employment or (b) being outside India, comes on a visit to India

©2013 Deloitte Haskins & Sells

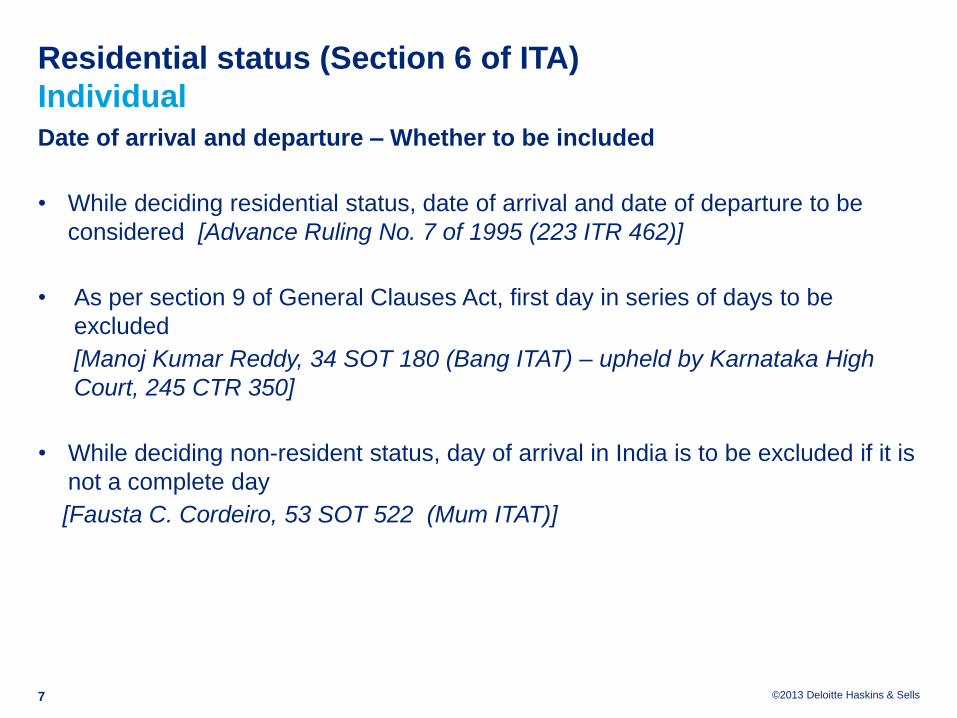

Residential status (Section 6 of ITA)

Individual

Date of arrival and departure – Whether to be included

• While deciding residential status, date of arrival and date of departure to be

considered [Advance Ruling No. 7 of 1995 (223 ITR 462)]

• As per section 9 of General Clauses Act, first day in series of days to be

excluded

[Manoj Kumar Reddy, 34 SOT 180 (Bang ITAT) – upheld by Karnataka High

Court, 245 CTR 350]

• While deciding non-resident status, day of arrival in India is to be excluded if it is

not a complete day

[Fausta C. Cordeiro, 53 SOT 522 (Mum ITAT)]

7

©2013 Deloitte Haskins & Sells

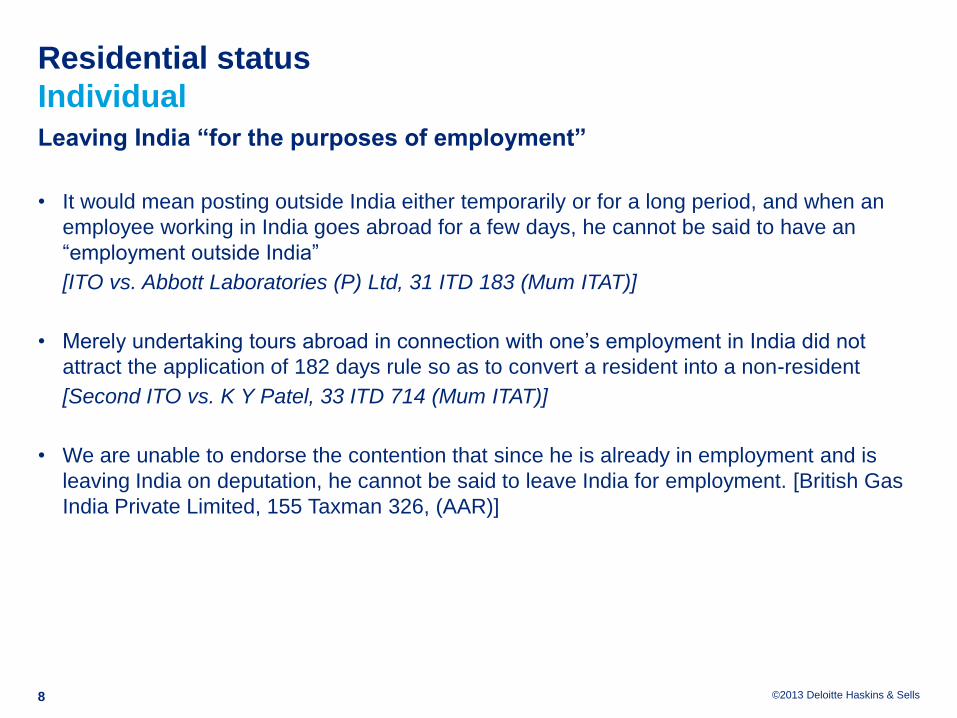

Residential status

Individual

Leaving India “for the purposes of employment”

• It would mean posting outside India either temporarily or for a long period, and when an

employee working in India goes abroad for a few days, he cannot be said to have an

“employment outside India”

[ITO vs. Abbott Laboratories (P) Ltd, 31 ITD 183 (Mum ITAT)]

• Merely undertaking tours abroad in connection with one’s employment in India did not

attract the application of 182 days rule so as to convert a resident into a non-resident

[Second ITO vs. K Y Patel, 33 ITD 714 (Mum ITAT)]

• We are unable to endorse the contention that since he is already in employment and is

leaving India on deputation, he cannot be said to leave India for employment. [British Gas

India Private Limited, 155 Taxman 326, (AAR)]

8

©2013 Deloitte Haskins & Sells

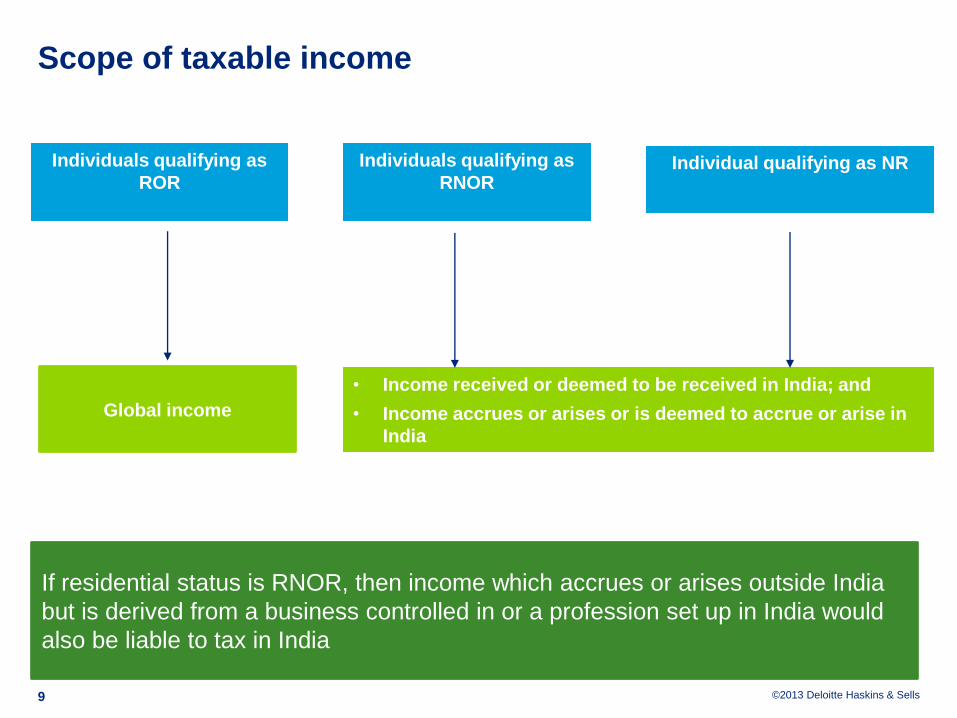

Individual qualifying as NR

Scope of taxable income

9

Individuals qualifying as

ROR

Individuals qualifying as

RNOR

• Income received or deemed to be received in India; and

• Income accrues or arises or is deemed to accrue or arise in

India

Global income

If residential status is RNOR, then income which accrues or arises outside India

but is derived from a business controlled in or a profession set up in India would

also be liable to tax in India

©2013 Deloitte Haskins & Sells

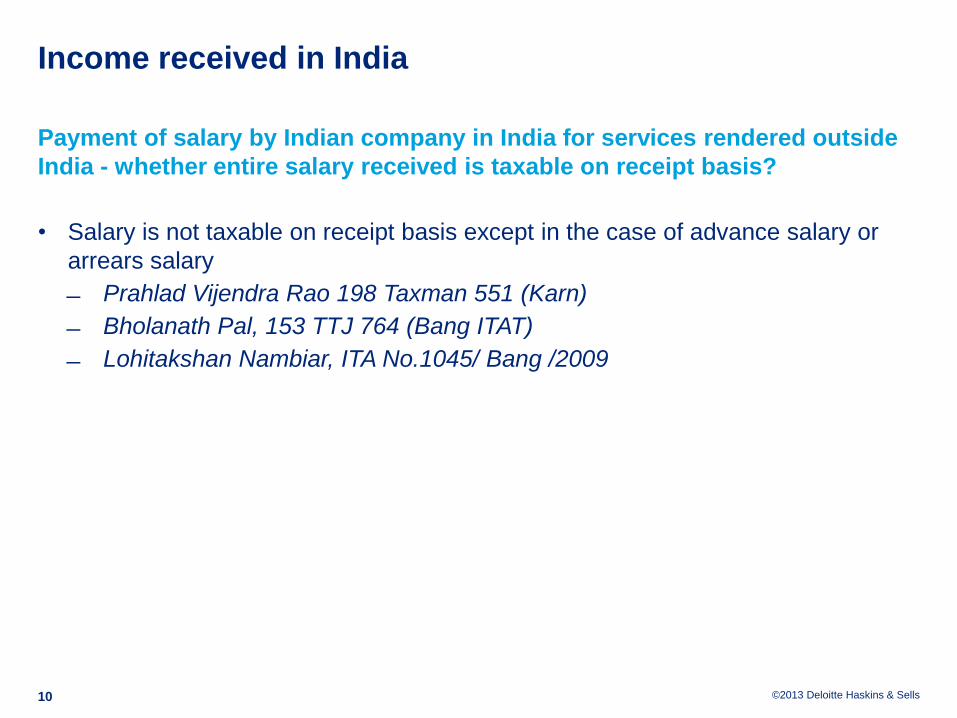

Income received in India

Payment of salary by Indian company in India for services rendered outside

India - whether entire salary received is taxable on receipt basis?

• Salary is not taxable on receipt basis except in the case of advance salary or

arrears salary

Prahlad Vijendra Rao 198 Taxman 551 (Karn)

Bholanath Pal, 153 TTJ 764 (Bang ITAT)

Lohitakshan Nambiar, ITA No.1045/ Bang /2009

10

©2013 Deloitte Haskins & Sells

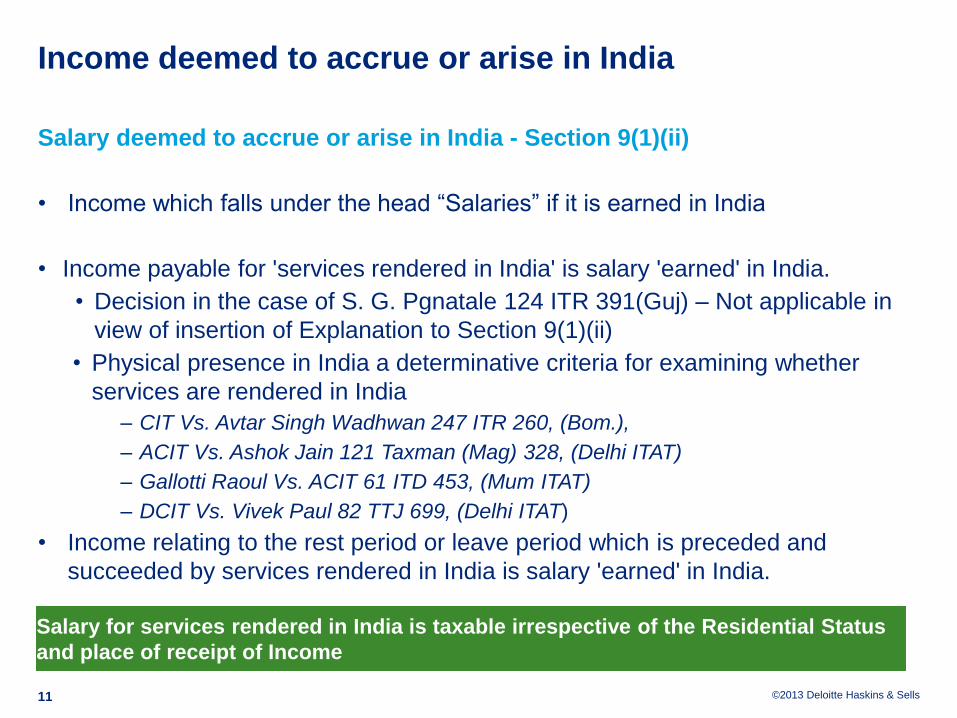

Income deemed to accrue or arise in India

Salary deemed to accrue or arise in India - Section 9(1)(ii)

• Income which falls under the head “Salaries” if it is earned in India

• Income payable for 'services rendered in India' is salary 'earned' in India.

• Decision in the case of S. G. Pgnatale 124 ITR 391(Guj) – Not applicable in

view of insertion of Explanation to Section 9(1)(ii)

• Physical presence in India a determinative criteria for examining whether

services are rendered in India

‒ CIT Vs. Avtar Singh Wadhwan 247 ITR 260, (Bom.),

‒ ACIT Vs. Ashok Jain 121 Taxman (Mag) 328, (Delhi ITAT)

‒ Gallotti Raoul Vs. ACIT 61 ITD 453, (Mum ITAT)

‒ DCIT Vs. Vivek Paul 82 TTJ 699, (Delhi ITAT)

• Income relating to the rest period or leave period which is preceded and

succeeded by services rendered in India is salary 'earned' in India.

11

Salary for services rendered in India is taxable irrespective of the Residential Status

and place of receipt of Income

©2013 Deloitte Haskins & Sells

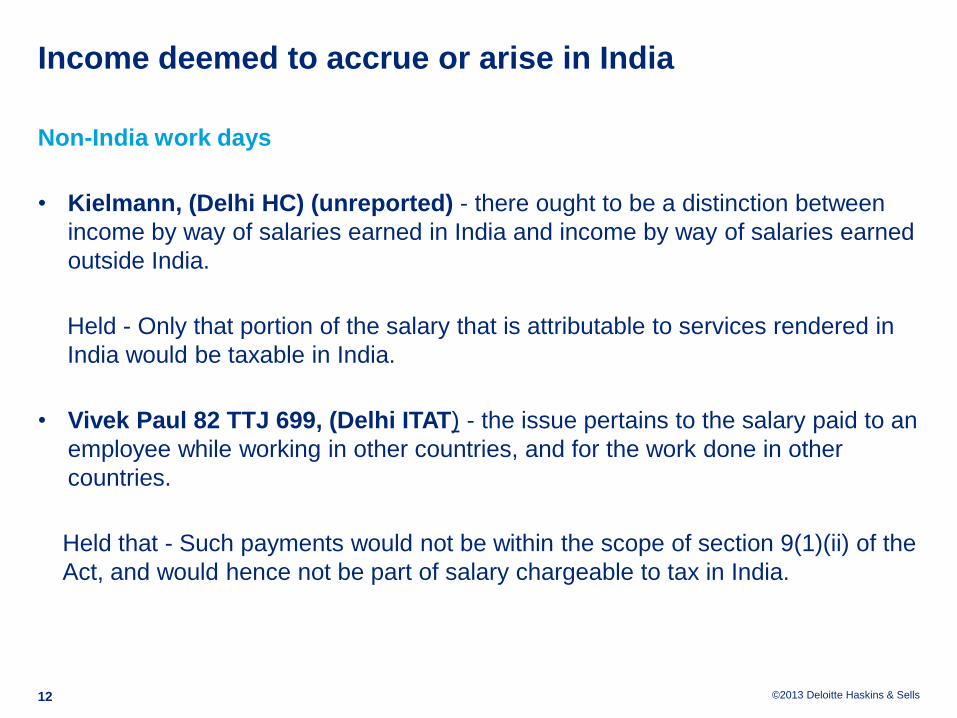

Income deemed to accrue or arise in India

Non-India work days

• Kielmann, (Delhi HC) (unreported) - there ought to be a distinction between

income by way of salaries earned in India and income by way of salaries earned

outside India.

Held - Only that portion of the salary that is attributable to services rendered in

India would be taxable in India.

• Vivek Paul 82 TTJ 699, (Delhi ITAT) - the issue pertains to the salary paid to an

employee while working in other countries, and for the work done in other

countries.

Held that - Such payments would not be within the scope of section 9(1)(ii) of the

Act, and would hence not be part of salary chargeable to tax in India.

12

©2013 Deloitte Haskins & Sells

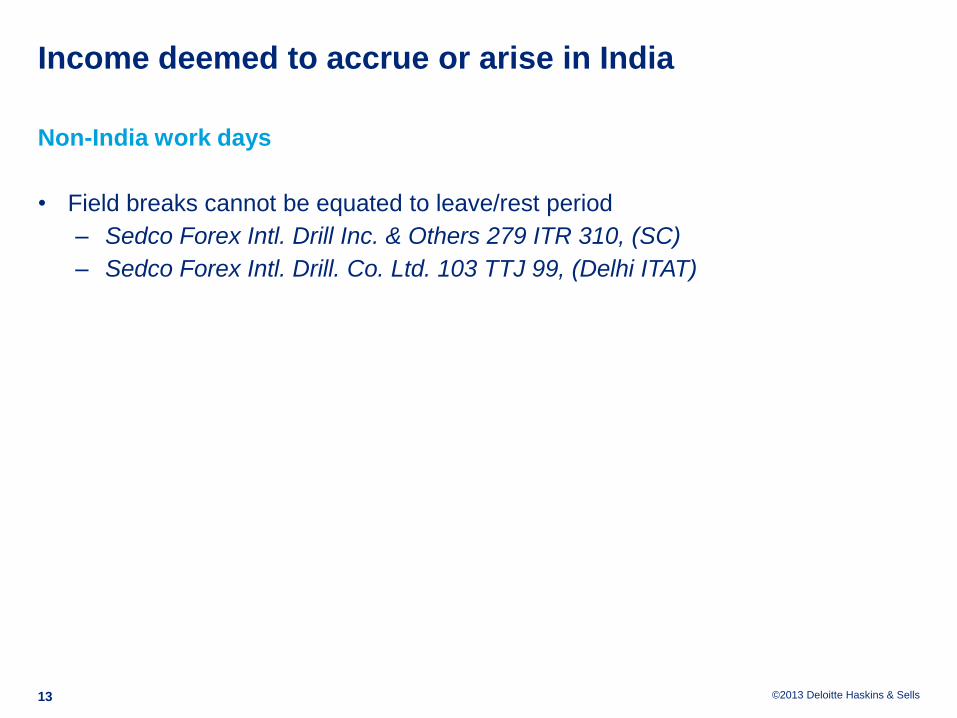

Income deemed to accrue or arise in India

Non-India work days

• Field breaks cannot be equated to leave/rest period

‒ Sedco Forex Intl. Drill Inc. & Others 279 ITR 310, (SC)

‒ Sedco Forex Intl. Drill. Co. Ltd. 103 TTJ 99, (Delhi ITAT)

13

©2013 Deloitte Haskins & Sells

Income from Salary (Sections 15 & 17)

Salary – taxable on receipt or due basis whichever is earlier

Perquisites – Part of ‘salary’ & taxed in the hands of the employee such as

• Accommodation

• Amenities like servant, gardener, etc.

• Free Food

• Car Benefit

• Gifts

• Stock Options

• Other benefits by way of ESOPs, contribution to an approved superannuation

fund in excess of Rs.100,000 and any other prescribed benefit or amenity to be

taxed as perquisites in the hands of employees.

Profit in lieu of salary – taxed as salary

14

©2013 Deloitte Haskins & Sells

Relevant exemptions

Short stay

90 Day rule – Section 10(6)(vi)

Conditions

• Employee is a foreign citizen employed by a foreign enterprise

• Foreign entity is not engaged in trade / business in India

• Stay in India ≤ 90 days in a tax year

• Remuneration is not liable to be deducted from employer's income chargeable

to tax in India

Exempt Amount

• Remuneration received as employee of foreign enterprise for services rendered

during stay in India

15

©2013 Deloitte Haskins & Sells

Relevant exemptions

Non-monetary perquisite

Section 10(10CC)

• Income in the nature of a perquisite not provided for by way of monetary

payment

• Tax paid by the employer on behalf of the employee at the option of the

employer

• Perquisite exempt in the hand of employee

As per section 40(a)(v) of the ITA, the tax actually paid by the employer under

section 10(10CC) is not eligible for deduction in the hands of the employer

16

©2013 Deloitte Haskins & Sells

Double Taxation Avoidance

Agreement

©2013 Deloitte Haskins & Sells

Double Tax Avoidance Agreement – Section 90 of the ITA

Residence

• Applicability – Resident of either of the Contracting States. In case of dual

residency, tie-breaker rule is applied to determine residency

• Tie breaker Rule:

‒ Availability of permanent home

‒ Center of vital interests

‒ Habitual abode

‒ Nationality

Taxability – Article on Dependent Personal Services and Pension

Elimination of Double Taxation

• Two methods of eliminating double taxation in case of individual:

‒ Dependent personal service (Exemption method)

‒ Foreign tax credit (Credit method)

18

©2013 Deloitte Haskins & Sells

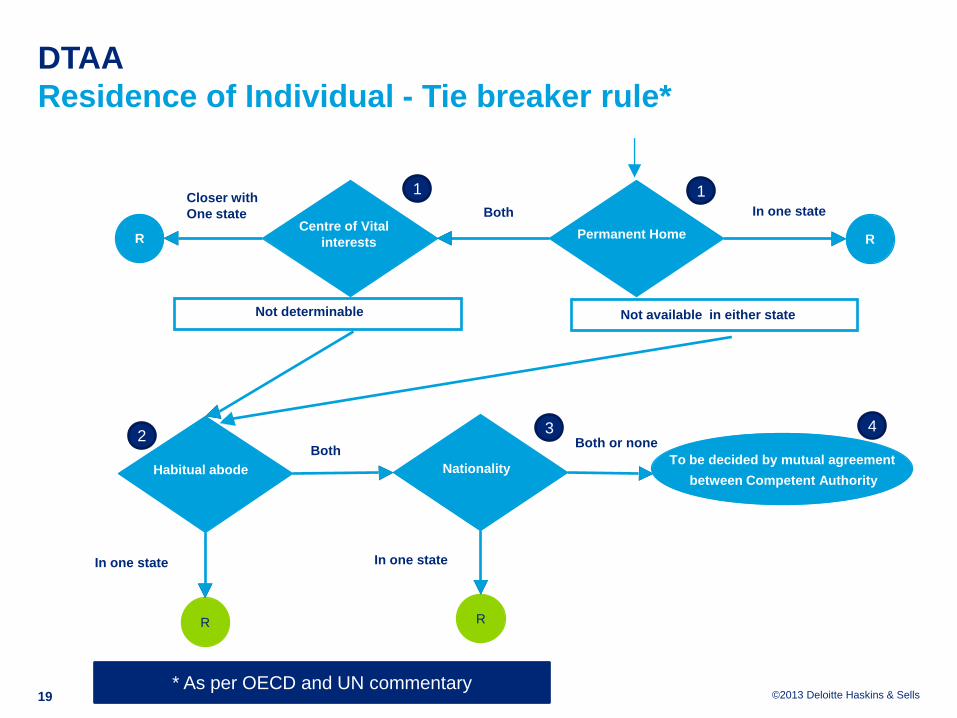

DTAA

Residence of Individual - Tie breaker rule*

19

Centre of Vital

interests Permanent Home

Both

R

Closer with

One state

Not determinable

R

In one state

Nationality Habitual abode *

R

In one state

Both

R

In one state

Both or none

To be decided by mutual agreement

between Competent Authority

Not available in either state

1 1

2 3 4

* As per OECD and UN commentary

©2013 Deloitte Haskins & Sells

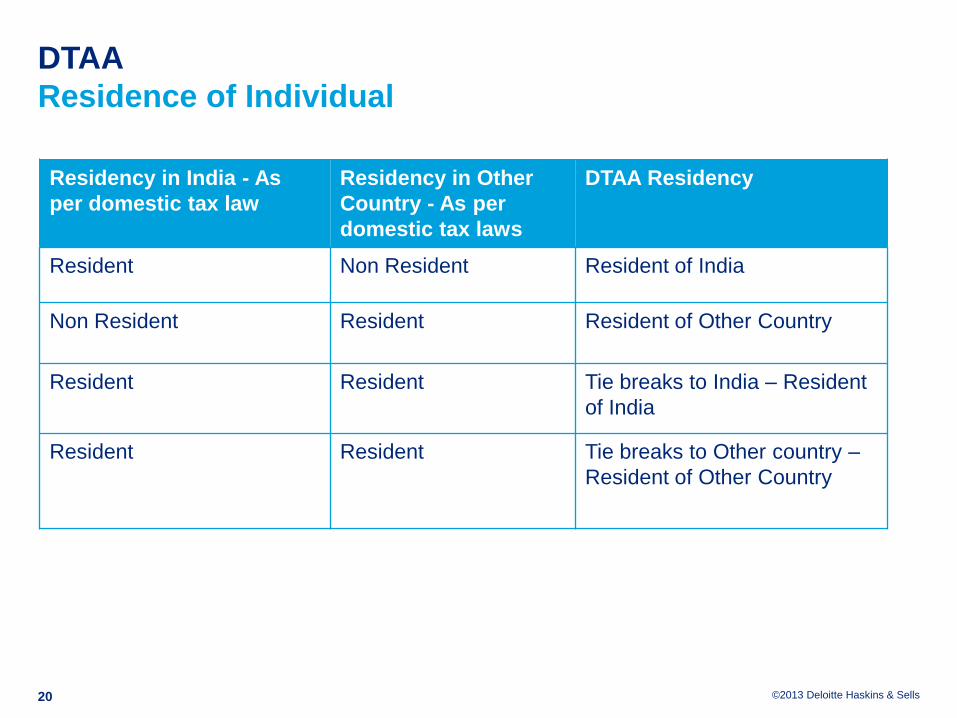

DTAA

Residence of Individual

20

Residency in India - As

per domestic tax law

Residency in Other

Country - As per

domestic tax laws

DTAA Residency

Resident Non Resident Resident of India

Non Resident Resident Resident of Other Country

Resident Resident Tie breaks to India – Resident

of India

Resident Resident Tie breaks to Other country –

Resident of Other Country

©2013 Deloitte Haskins & Sells

DTAA

Residence of Individual

Some practical issues

• Different tax year followed by host and home country – Split residency

• Permanent Home in both countries – Whether house in spouse name could be

construed a permanent home of the taxpayer for treaty purposes

• Center of vital interests and habitual abode – Subjective evaluation

• Determination of residence to be settled by the Competent authorities by mutual

agreement – may be time consuming

21

©2013 Deloitte Haskins & Sells

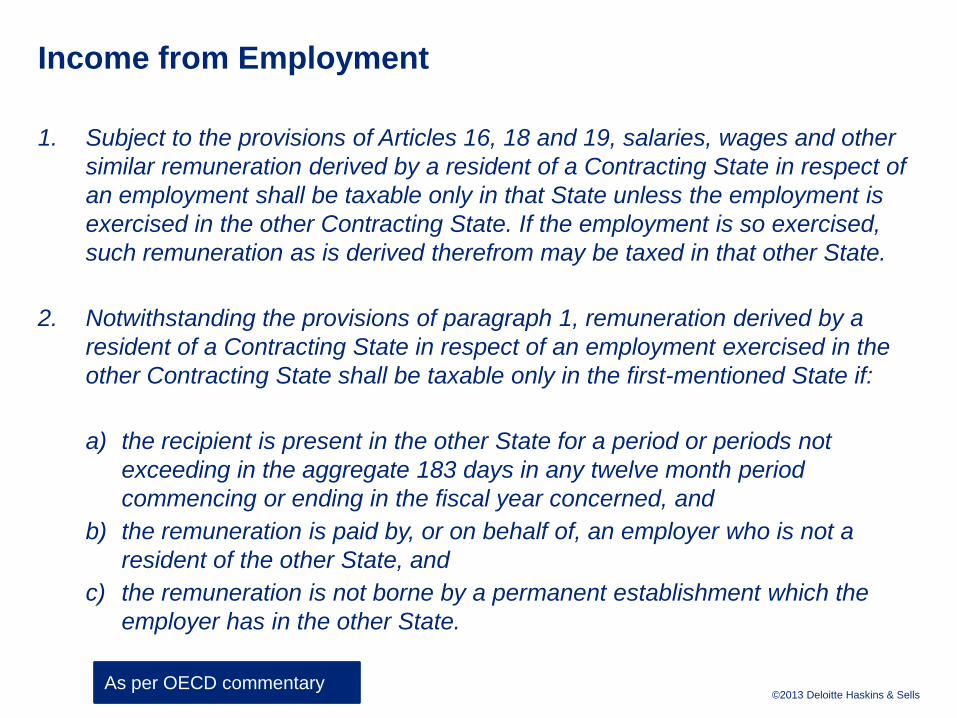

Income from Employment

1. Subject to the provisions of Articles 16, 18 and 19, salaries, wages and other

similar remuneration derived by a resident of a Contracting State in respect of

an employment shall be taxable only in that State unless the employment is

exercised in the other Contracting State. If the employment is so exercised,

such remuneration as is derived therefrom may be taxed in that other State.

2. Notwithstanding the provisions of paragraph 1, remuneration derived by a

resident of a Contracting State in respect of an employment exercised in the

other Contracting State shall be taxable only in the first-mentioned State if:

a) the recipient is present in the other State for a period or periods not

exceeding in the aggregate 183 days in any twelve month period

commencing or ending in the fiscal year concerned, and

b) the remuneration is paid by, or on behalf of, an employer who is not a

resident of the other State, and

c) the remuneration is not borne by a permanent establishment which the

employer has in the other State.

As per OECD commentary

©2013 Deloitte Haskins & Sells

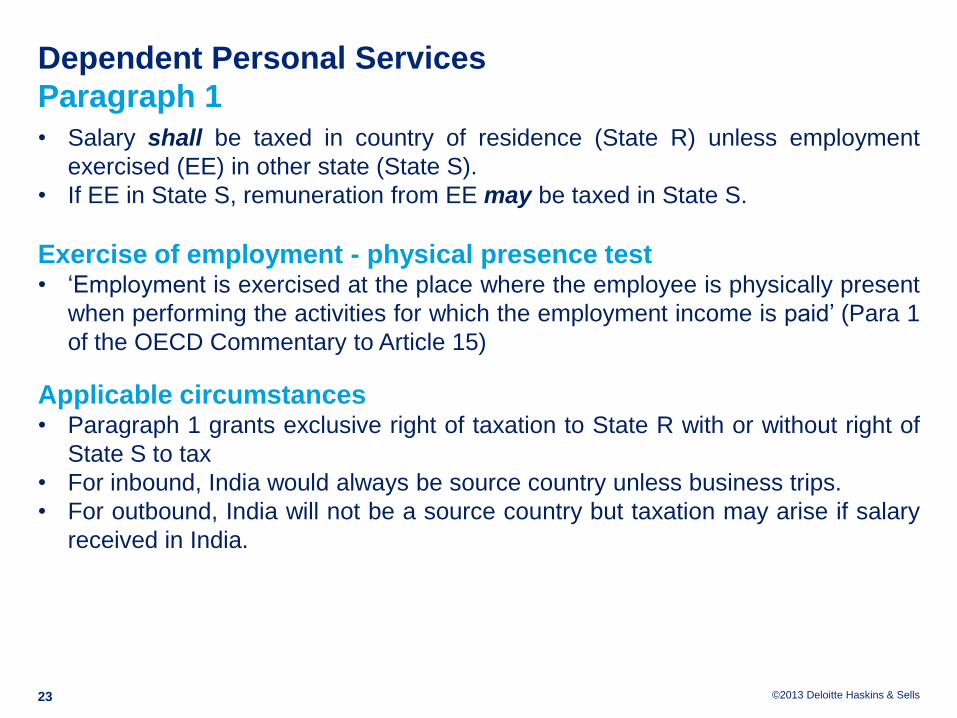

Dependent Personal Services

Paragraph 1

• Salary shall be taxed in country of residence (State R) unless employment

exercised (EE) in other state (State S).

• If EE in State S, remuneration from EE may be taxed in State S.

Exercise of employment - physical presence test • ‘Employment is exercised at the place where the employee is physically present

when performing the activities for which the employment income is paid’ (Para 1

of the OECD Commentary to Article 15)

Applicable circumstances • Paragraph 1 grants exclusive right of taxation to State R with or without right of

State S to tax

• For inbound, India would always be source country unless business trips.

• For outbound, India will not be a source country but taxation may arise if salary

received in India.

23

©2013 Deloitte Haskins & Sells

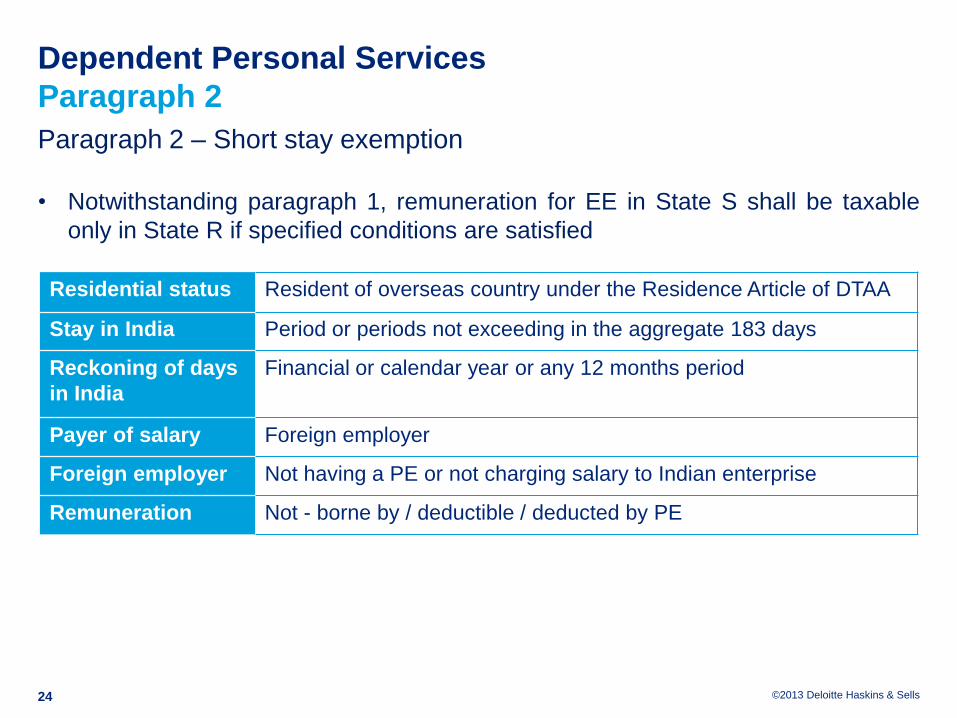

Dependent Personal Services

Paragraph 2

Paragraph 2 – Short stay exemption

• Notwithstanding paragraph 1, remuneration for EE in State S shall be taxable

only in State R if specified conditions are satisfied

Residential status Resident of overseas country under the Residence Article of DTAA

Stay in India Period or periods not exceeding in the aggregate 183 days

Reckoning of days

in India

Financial or calendar year or any 12 months period

Payer of salary Foreign employer

Foreign employer Not having a PE or not charging salary to Indian enterprise

Remuneration Not - borne by / deductible / deducted by PE

24

©2013 Deloitte Haskins & Sells

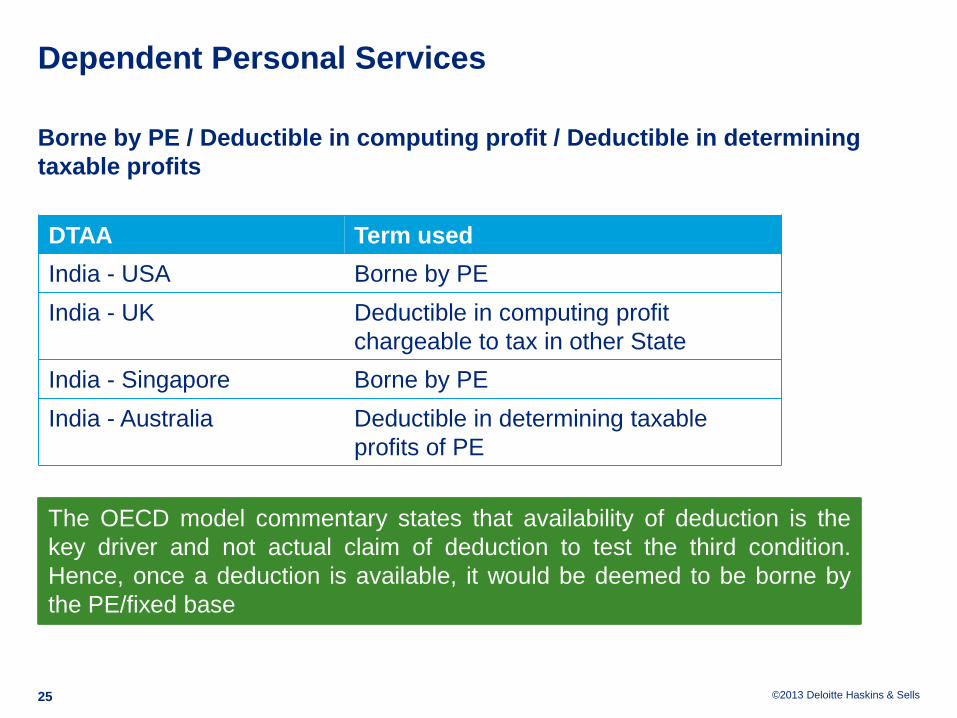

Dependent Personal Services

Borne by PE / Deductible in computing profit / Deductible in determining

taxable profits

25

DTAA Term used

India - USA Borne by PE

India - UK Deductible in computing profit

chargeable to tax in other State

India - Singapore Borne by PE

India - Australia Deductible in determining taxable

profits of PE

The OECD model commentary states that availability of deduction is the

key driver and not actual claim of deduction to test the third condition.

Hence, once a deduction is available, it would be deemed to be borne by

the PE/fixed base

©2013 Deloitte Haskins & Sells

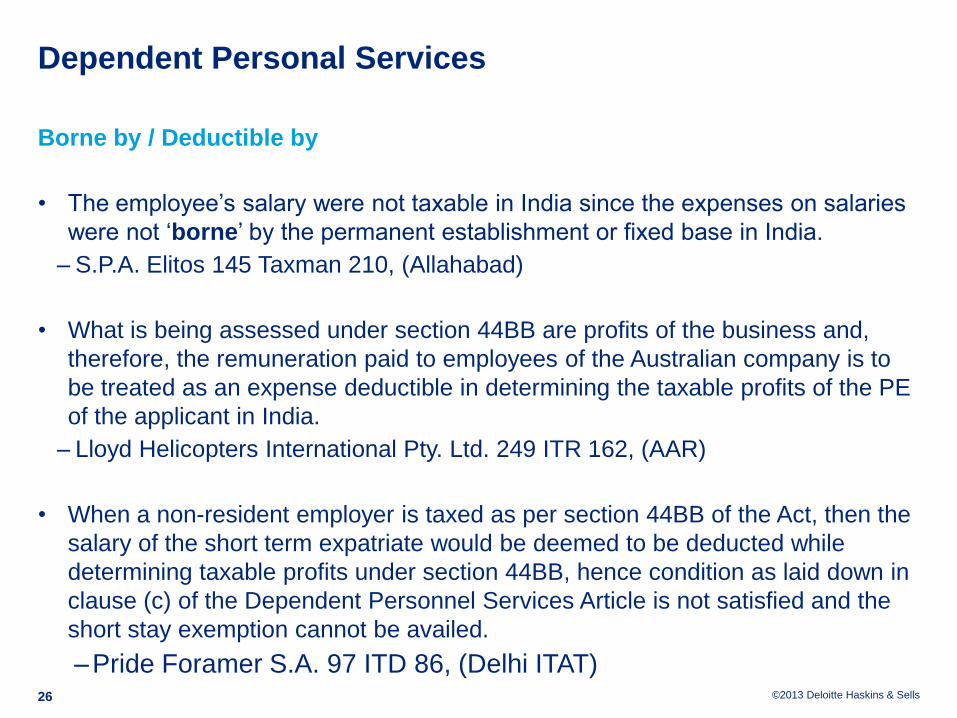

Dependent Personal Services

Borne by / Deductible by

• The employee’s salary were not taxable in India since the expenses on salaries

were not ‘borne’ by the permanent establishment or fixed base in India.

‒ S.P.A. Elitos 145 Taxman 210, (Allahabad)

• What is being assessed under section 44BB are profits of the business and,

therefore, the remuneration paid to employees of the Australian company is to

be treated as an expense deductible in determining the taxable profits of the PE

of the applicant in India.

‒ Lloyd Helicopters International Pty. Ltd. 249 ITR 162, (AAR)

• When a non-resident employer is taxed as per section 44BB of the Act, then the

salary of the short term expatriate would be deemed to be deducted while

determining taxable profits under section 44BB, hence condition as laid down in

clause (c) of the Dependent Personnel Services Article is not satisfied and the

short stay exemption cannot be availed.

‒Pride Foramer S.A. 97 ITD 86, (Delhi ITAT)

26

©2013 Deloitte Haskins & Sells

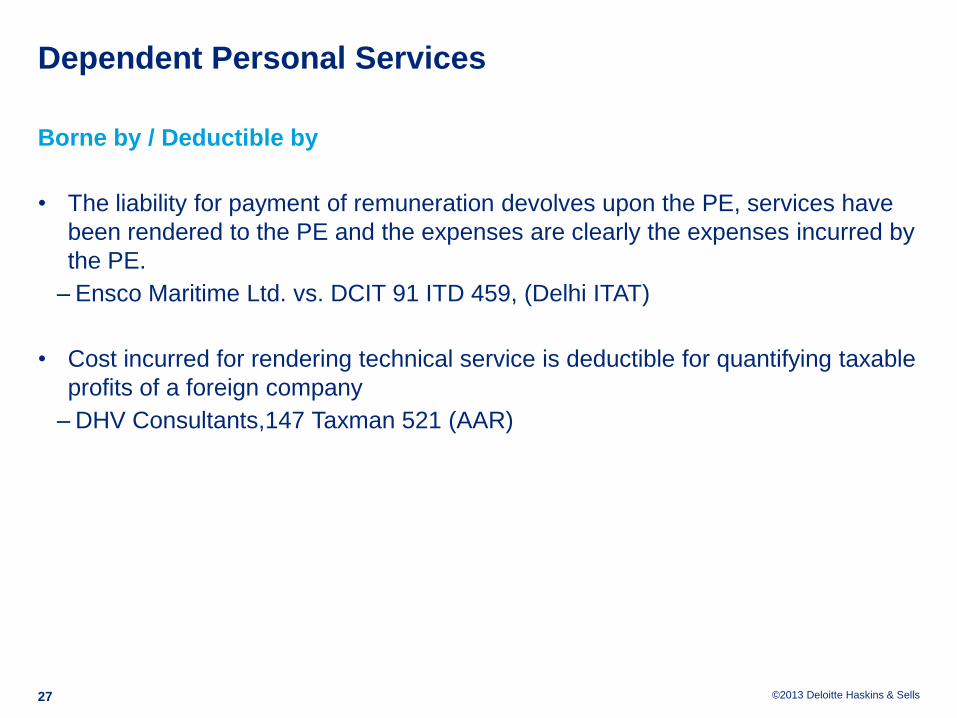

Dependent Personal Services

Borne by / Deductible by

• The liability for payment of remuneration devolves upon the PE, services have

been rendered to the PE and the expenses are clearly the expenses incurred by

the PE.

‒ Ensco Maritime Ltd. vs. DCIT 91 ITD 459, (Delhi ITAT)

• Cost incurred for rendering technical service is deductible for quantifying taxable

profits of a foreign company

‒ DHV Consultants,147 Taxman 521 (AAR)

27

©2013 Deloitte Haskins & Sells

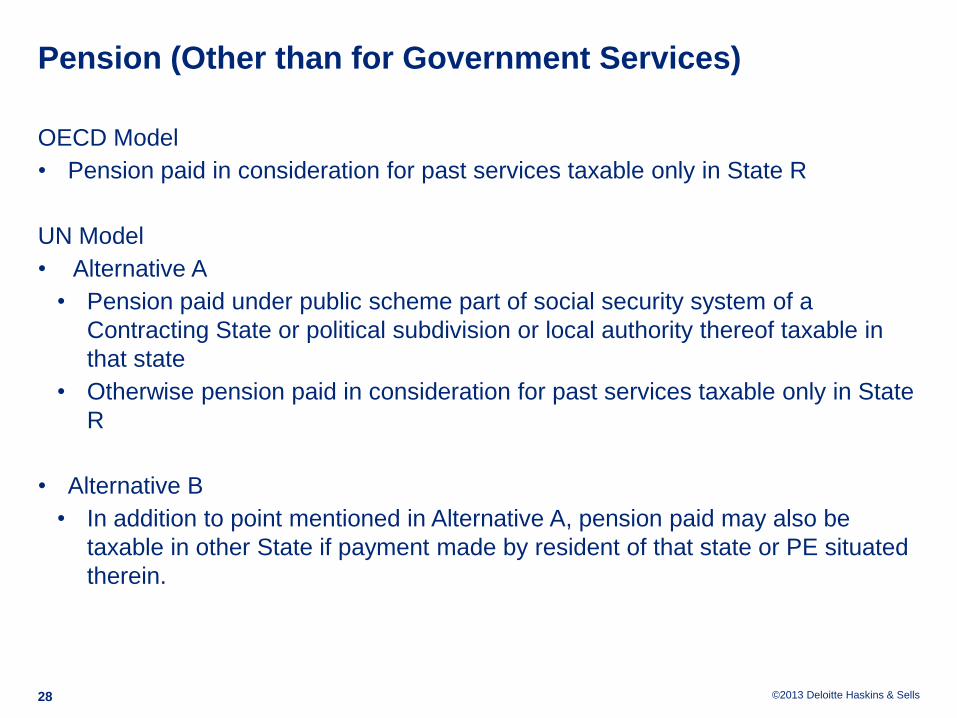

Pension (Other than for Government Services)

OECD Model

• Pension paid in consideration for past services taxable only in State R

UN Model

• Alternative A

• Pension paid under public scheme part of social security system of a

Contracting State or political subdivision or local authority thereof taxable in

that state

• Otherwise pension paid in consideration for past services taxable only in State

R

• Alternative B

• In addition to point mentioned in Alternative A, pension paid may also be

taxable in other State if payment made by resident of that state or PE situated

therein.

28

©2013 Deloitte Haskins & Sells

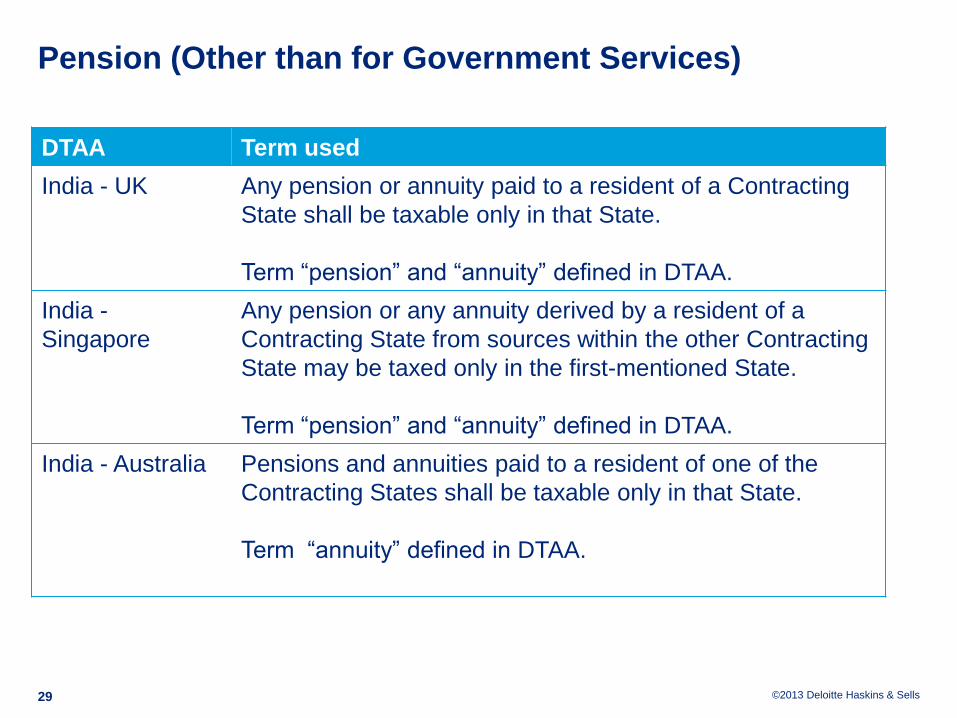

Pension (Other than for Government Services)

DTAA Term used

India - UK Any pension or annuity paid to a resident of a Contracting

State shall be taxable only in that State.

Term “pension” and “annuity” defined in DTAA.

India -

Singapore

Any pension or any annuity derived by a resident of a

Contracting State from sources within the other Contracting

State may be taxed only in the first-mentioned State.

Term “pension” and “annuity” defined in DTAA.

India - Australia Pensions and annuities paid to a resident of one of the

Contracting States shall be taxable only in that State.

Term “annuity” defined in DTAA.

29

©2013 Deloitte Haskins & Sells

Pension (Other than for Government Services)

India- US tax treaty

• Paragraph 1 provides that private pensions and any annuities derived by a

resident of a Contracting State from sources within the other Contracting State

are taxable only in the State of residence of the recipient.

• Paragraph 2 provides a different rule for social security benefits and other public

pensions paid by a Contracting State to a resident of the other Contracting State

or a citizen of the United States. Such payments are taxable only in the

Contracting State that pays them.

• Term “pension” and “annuity” defined in DTAA.

30

©2013 Deloitte Haskins & Sells

Foreign Tax Credit

• In order to provide relief from double taxation, India has entered into DTAA with

various countries.

• DTAA resolves double taxation through exemption mechanism and/or credit

mechanism.

‒ Eg : If ‘A’ is a tax resident of India, as per the DTAA between India and other

country, say USA, the taxes paid in USA may be claimed as credit against taxes

payable in India.

• The amount of credit of foreign tax shall not exceed the Indian income-tax

payable in respect of income which is taxed outside India

31

©2013 Deloitte Haskins & Sells

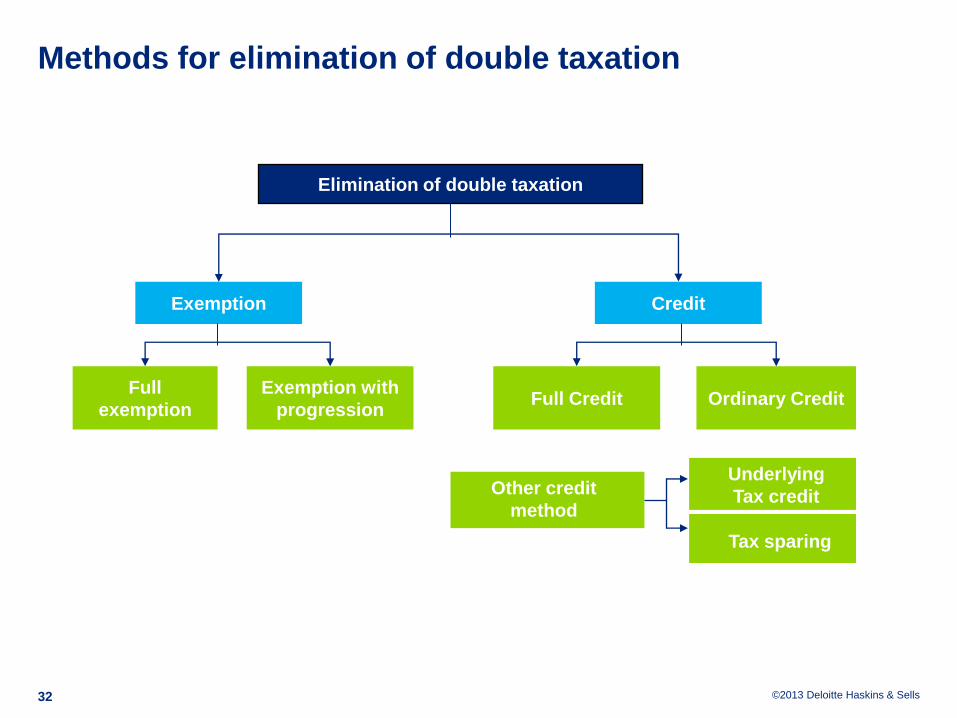

Methods for elimination of double taxation

32

Elimination of double taxation

Exemption Credit

Exemption with

progression Ordinary Credit Full Credit

Full

exemption

Other credit

method

Underlying

Tax credit

Tax sparing

©2013 Deloitte Haskins & Sells

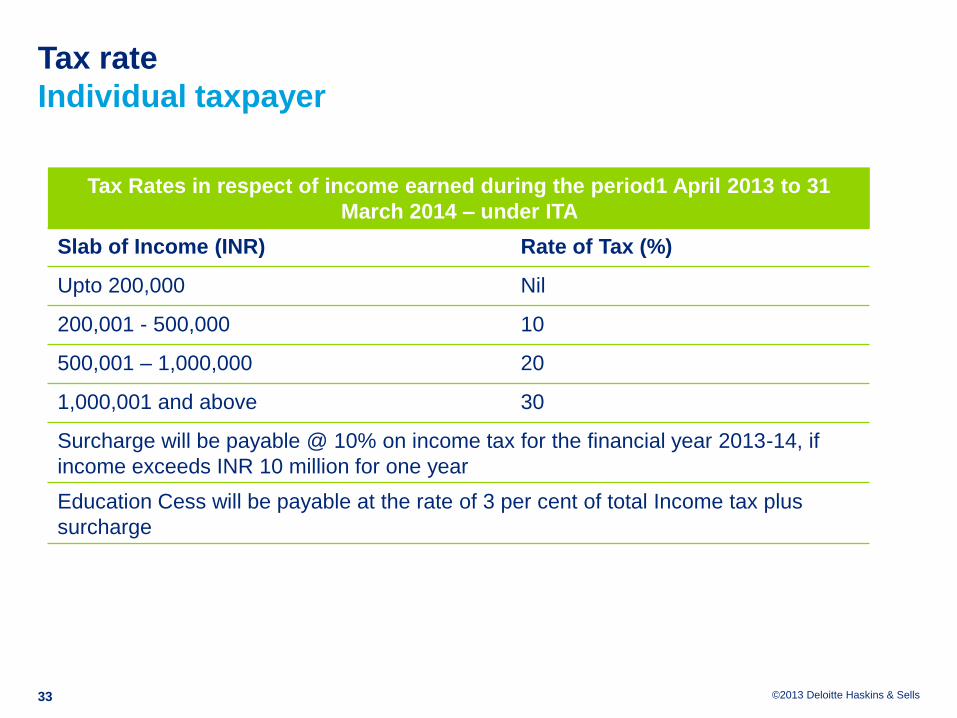

Tax rate

Individual taxpayer

33

Tax Rates in respect of income earned during the period1 April 2013 to 31

March 2014 – under ITA

Slab of Income (INR) Rate of Tax (%)

Upto 200,000 Nil

200,001 - 500,000 10

500,001 – 1,000,000 20

1,000,001 and above 30

Surcharge will be payable @ 10% on income tax for the financial year 2013-14, if

income exceeds INR 10 million for one year

Education Cess will be payable at the rate of 3 per cent of total Income tax plus

surcharge

©2013 Deloitte Haskins & Sells

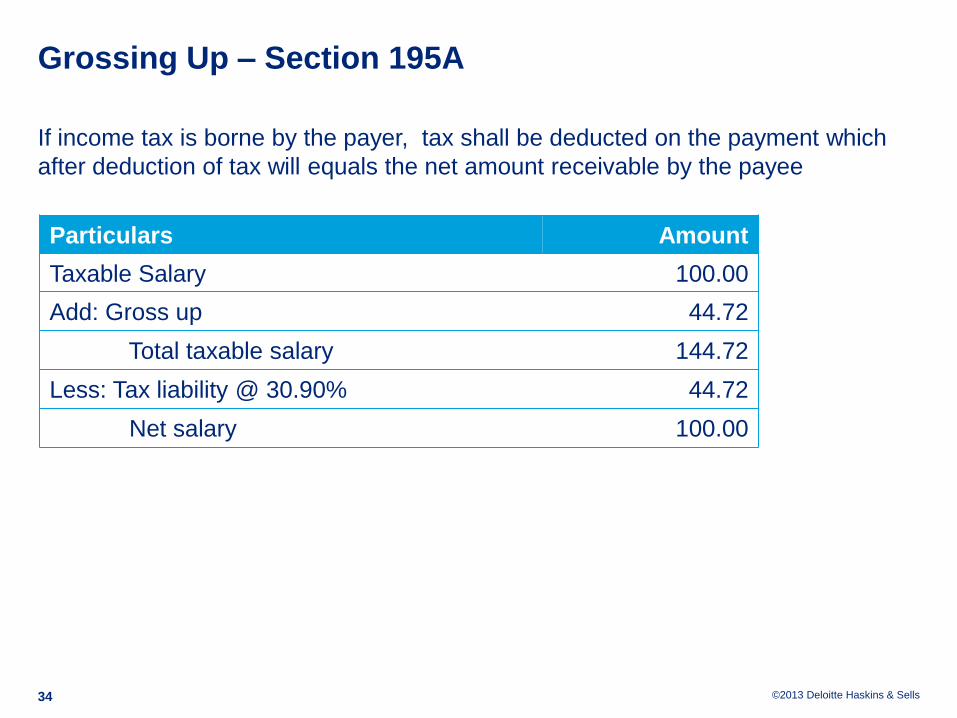

Grossing Up – Section 195A

If income tax is borne by the payer, tax shall be deducted on the payment which

after deduction of tax will equals the net amount receivable by the payee

34

Particulars Amount

Taxable Salary 100.00

Add: Gross up 44.72

Total taxable salary 144.72

Less: Tax liability @ 30.90% 44.72

Net salary 100.00

©2013 Deloitte Haskins & Sells

Specific Issues

©2013 Deloitte Haskins & Sells

Inbound

©2013 Deloitte Haskins & Sells

Tax equalization and hypothetical taxes

Concept

Principle

• Employee should be tax neutral on the employer-sourced income while taking

up an international assignment

Application

• Hypothetical tax is the estimated amount of income tax which the expatriate

would have paid in his home country if he would have continued working in his

home country.

• Companies ensure that an assignee neither suffers nor unduly benefits as a

consequence of differences in tax laws and rates between the employee’s Home

country and Host country.

• The hypothetical tax calculated is reduced from the salary of the employee and

only the net salary is considered as the salary payable to the employee

• At the end of the year, a reconciliation is made between hypo tax and actual tax

in home country.

• The tax liability of the employee in the Host country as well as Home country is

borne by the employer

37

©2013 Deloitte Haskins & Sells

Deductibility of Hypothetical tax (Hypo Tax)

• Tax borne by employee (hypo tax) not be included in employee's income

• Case laws:

‒ Yoshio Kubo & Ors. (ITA 441/2003 and connected cases dated 31 July

2013)

‒ Jaydev Raja, (2012) 211 Taxmann 188, (Bom)

‒ Anand Kumar Dutta v. JCIT (ITA No. 943/Del/2005)

‒ Roy Marshall v. ACIT (OSD) [2008] ITA No.2038/ Mum/ 06

38

©2013 Deloitte Haskins & Sells

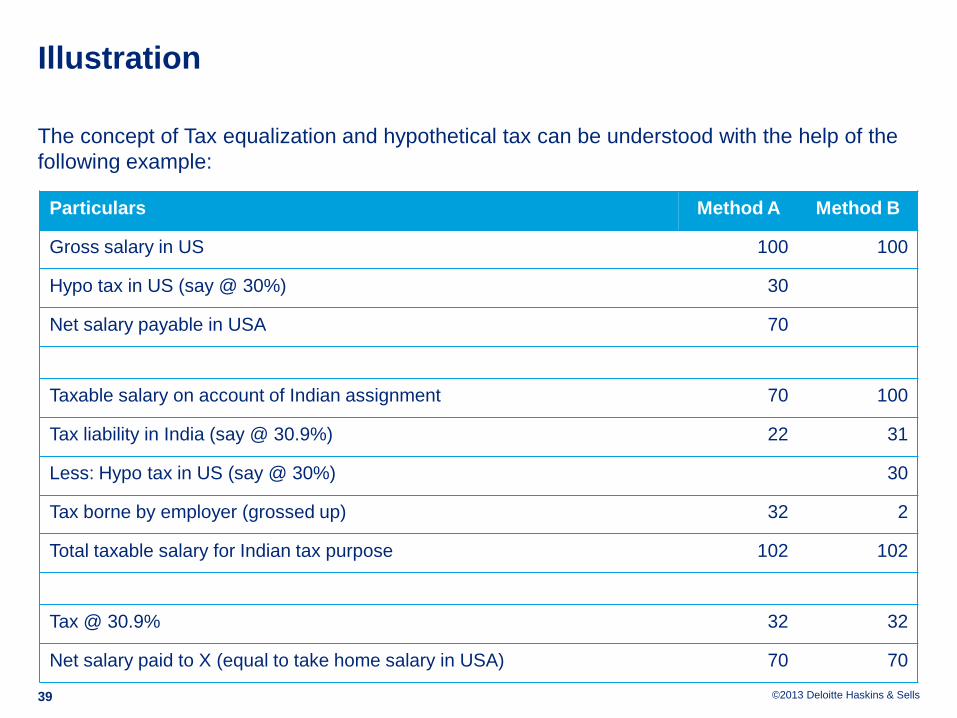

Illustration

The concept of Tax equalization and hypothetical tax can be understood with the help of the

following example:

39

Particulars Method A Method B

Gross salary in US 100 100

Hypo tax in US (say @ 30%) 30

Net salary payable in USA 70

Taxable salary on account of Indian assignment 70 100

Tax liability in India (say @ 30.9%) 22 31

Less: Hypo tax in US (say @ 30%) 30

Tax borne by employer (grossed up) 32 2

Total taxable salary for Indian tax purpose 102 102

Tax @ 30.9% 32 32

Net salary paid to X (equal to take home salary in USA) 70 70

©2013 Deloitte Haskins & Sells

Tax on “non monetary” perquisites [Section 10(10CC)]

Issues

• Tax under tax equalisation scheme : is it entitled to exemption ?

• What constitutes monetary and non monetary perquisites?

‒ Based on judicial precedents:

• Any payment made to outside parties directly by the employer may be classified as

a non-monetary perquisite.

• Any payment which is in the nature of direct payment to the employee by the

employer may be classified as a monetary payment.

• Tax liability borne by employer – Whether eligible for section 10(10CC) benefit?

‒ Based on judicial precedents

‒ Tax liability borne by employer in the nature of non-monetary perquisite eligible for

section 10(10CC) benefit

‒ As eligible for section 10(10CC) benefit, subject to single grossing up

Yoshio Kubo – 2013 – Delhi High Court – ITA 441/2003

Sedco Forex International Drilling Inc - Uttarkhand High Court (_____)

Delhi Special Bench decision of RBF Rig Corporation v/s Asst CIT (2008) 297 ITR (AT) (Del) (SB)

40

©2013 Deloitte Haskins & Sells

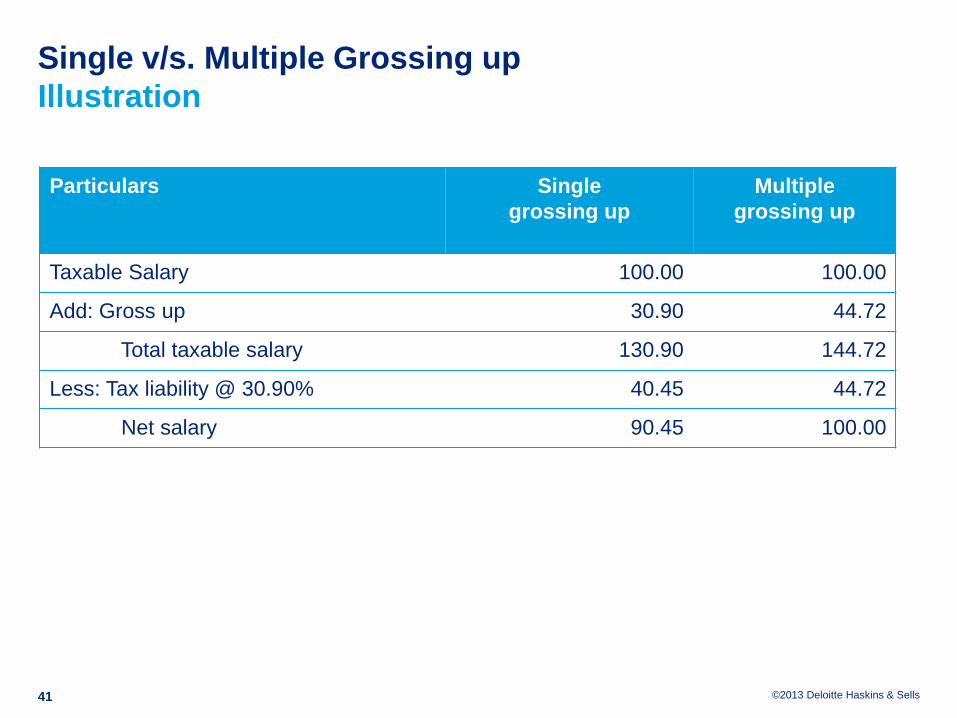

Single v/s. Multiple Grossing up

Illustration

Particulars Single

grossing up

Multiple

grossing up

Taxable Salary 100.00 100.00

Add: Gross up 30.90 44.72

Total taxable salary 130.90 144.72

Less: Tax liability @ 30.90% 40.45 44.72

Net salary 90.45 100.00

41

©2013 Deloitte Haskins & Sells

Contribution towards mandatory social security schemes

/ plans

Issue

• Whether contribution towards mandatory social security schemes / plans are

deductible while computing the taxable salary?

• “Contribution towards such scheme was treated as diversion of income by

overriding title and portion of salary represented by above contributions never

accrued to the expatriate.”

‒ Gallotti Raoul Vs. ACIT 61 ITD 453 (Mum ITAT)

To be examined on a case to case basis

42

©2013 Deloitte Haskins & Sells

Some other issues

• Taxation of per – diem

• Multiple country responsibility

• Premium paid towards personal accident insurance

• Employer’s contribution to Overseas Pension

• Requirement to file India tax return – treaty benefit claimed

43

©2013 Deloitte Haskins & Sells

Outbound

©2013 Deloitte Haskins & Sells

Some issues

• Liable to tax v. subject to tax

• Withholding tax obligation

• Outbound – salary received in India

• Foreign Tax Credit

• Taxation of per-diem

• ROR - received in India

• ROR - received outside India

• Withholding tax obligation

45

©2013 Deloitte Haskins & Sells

Taxation of Stock Awards

©2013 Deloitte Haskins & Sells

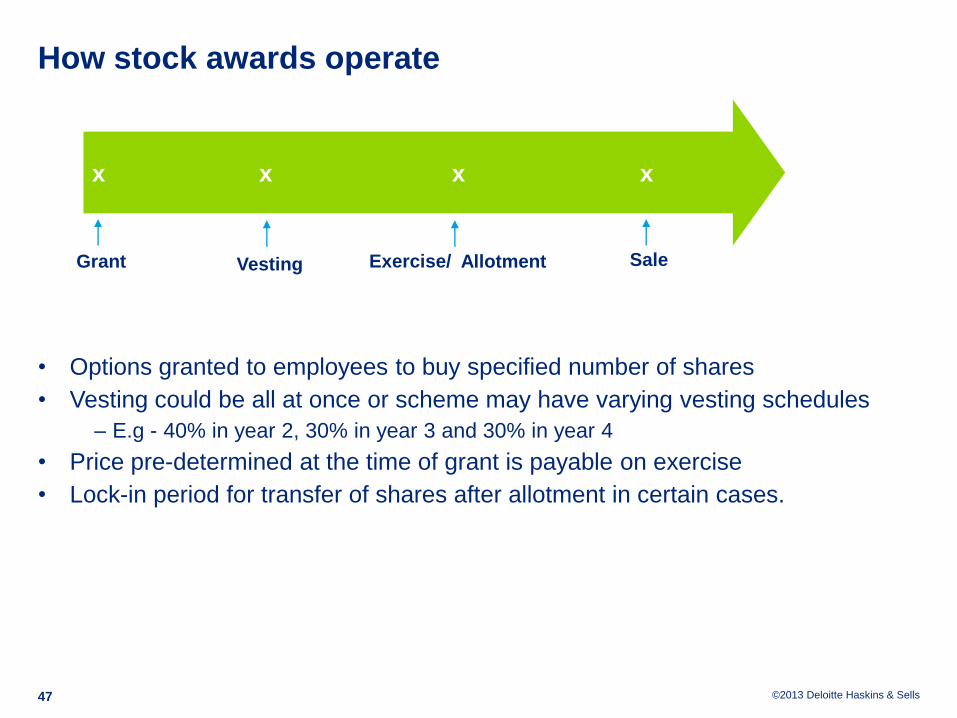

How stock awards operate

• Options granted to employees to buy specified number of shares

• Vesting could be all at once or scheme may have varying vesting schedules

‒ E.g - 40% in year 2, 30% in year 3 and 30% in year 4

• Price pre-determined at the time of grant is payable on exercise

• Lock-in period for transfer of shares after allotment in certain cases.

47

x x x x

Grant Vesting Exercise/ Allotment Sale

©2013 Deloitte Haskins & Sells

Forms of stock awards

48

Employee Stock Option Plan (ESOP)

• Options granted to employees to buy

specified number of shares at a pre-

determined price after the vesting period

• On exercise of option, shares will be

allotted to the employees

Employee Share Purchase Plan (ESPP)

• Employee granted a right to acquire shares

• On exercise of right, employee will receive

shares

• Generally, exercise price to be lower than

market price

Stock Appreciation Rights (SAR)/ Phantom

• SAR - an incentive based on the financial

performance of the company.

• Shares are not allotted

• Cash awards are provided to the

employees based on the increase in the

value of shares over the specific period

Restricted Stock Units (RSUs)

• Employee to satisfy certain conditions to be

eligible for vesting

• Upon vesting, employee receives shares

©2013 Deloitte Haskins & Sells

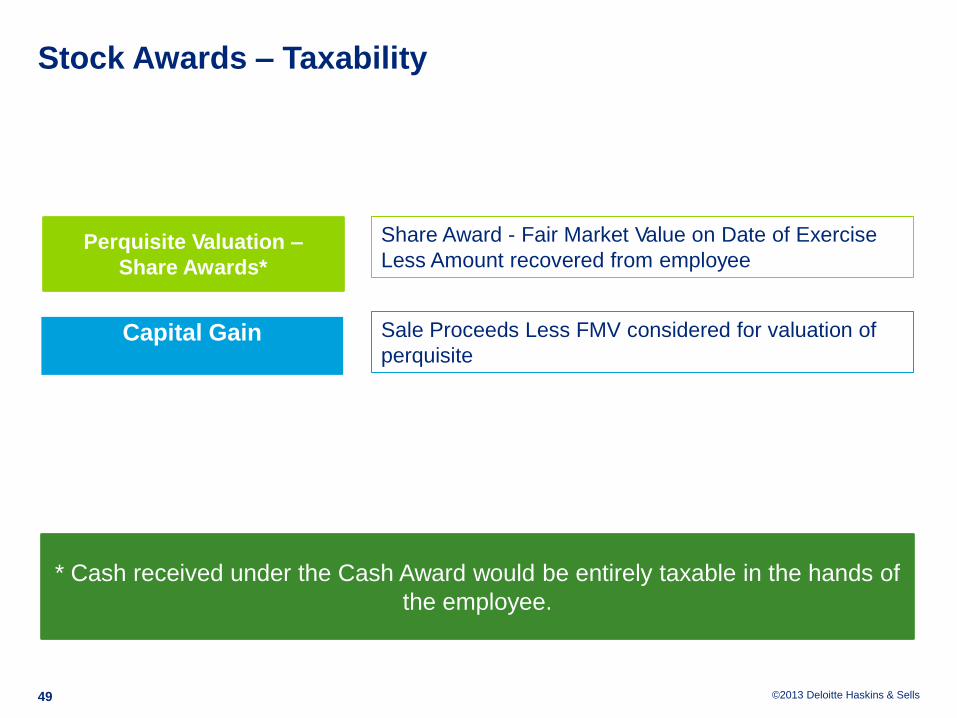

Stock Awards – Taxability

49

Capital Gain

* Cash received under the Cash Award would be entirely taxable in the hands of

the employee.

Perquisite Valuation –

Share Awards*

Share Award - Fair Market Value on Date of Exercise

Less Amount recovered from employee

Sale Proceeds Less FMV considered for valuation of

perquisite

©2013 Deloitte Haskins & Sells

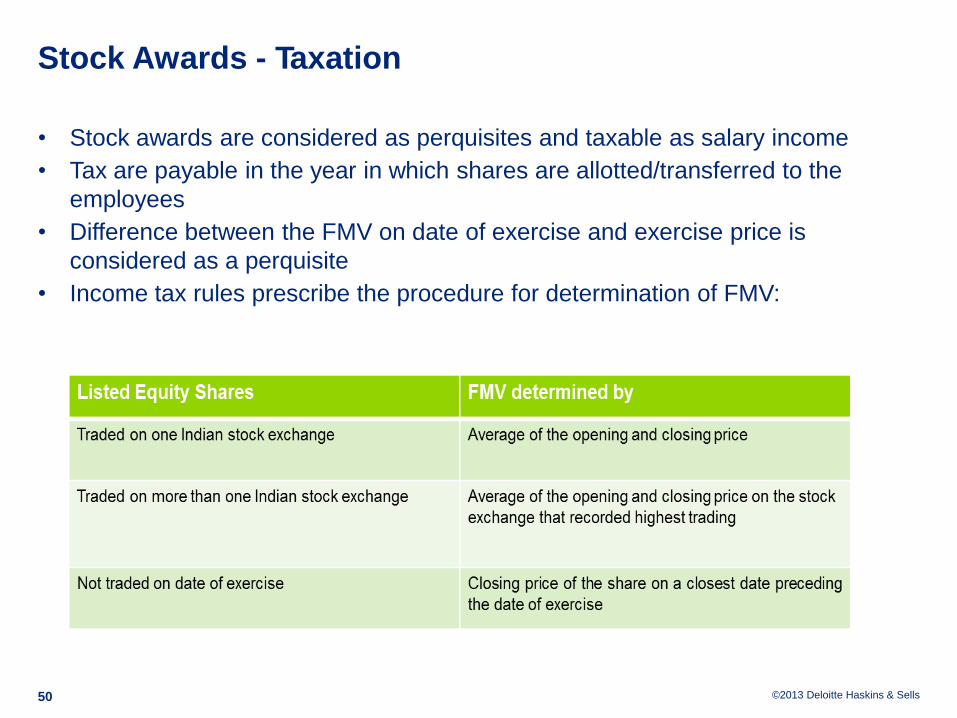

Stock Awards - Taxation

• Stock awards are considered as perquisites and taxable as salary income

• Tax are payable in the year in which shares are allotted/transferred to the

employees

• Difference between the FMV on date of exercise and exercise price is

considered as a perquisite

• Income tax rules prescribe the procedure for determination of FMV:

50

©2013 Deloitte Haskins & Sells

Important points in Stock Awards taxation

• Equity shares not listed on Indian stock exchange or any other securities listed

or not-listed on Indian stock exchange or listed outside India

- Category-I merchant banker to determine FMV:

• On date of exercise; or

• Any date not more than 180 days preceding the date of exercise

• Onus is on employer to deduct tax in the year in which stocks are allotted to the

employees

51

©2013 Deloitte Haskins & Sells

Key Issues

• No specific guidelines/clarifications in respect of sourcing of the perquisite ie

whether it should be taxable :

‒ from date of grant to date of vesting

‒ from date of grant to date of exercise

‒ or entire amount should be taxable

• Employees who are Resident and Ordinarily Resident (ROR) are taxed in India

on global income – in this case is sourcing allowed?

52

The Delhi Tribunal in the case of ACIT vs. Robert Arthur Keltz held that only proportionate amount of

stock option benefit relating to the period of services rendered in India during the grant period would be

taxable in India (Reliance was placed on OECD commentary and Circular 9 of 2007)

ACIT v. Robert Arthur Keltz, ITA No.3452/ Del/ 2011 dated 24 May 2013

©2013 Deloitte Haskins & Sells

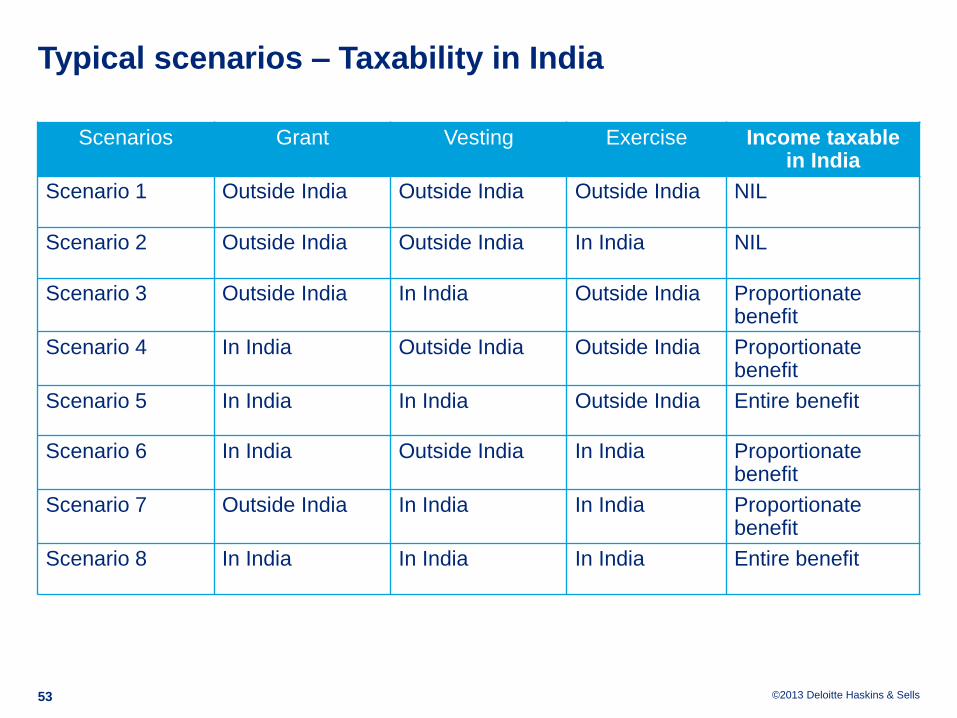

Typical scenarios – Taxability in India

Scenarios Grant Vesting Exercise Income taxable in India

Scenario 1 Outside India Outside India Outside India NIL

Scenario 2 Outside India Outside India In India NIL

Scenario 3 Outside India In India Outside India Proportionate benefit

Scenario 4 In India Outside India Outside India Proportionate benefit

Scenario 5 In India In India Outside India Entire benefit

Scenario 6 In India Outside India In India Proportionate benefit

Scenario 7 Outside India In India In India Proportionate benefit

Scenario 8 In India In India In India Entire benefit

53

©2013 Deloitte Haskins & Sells

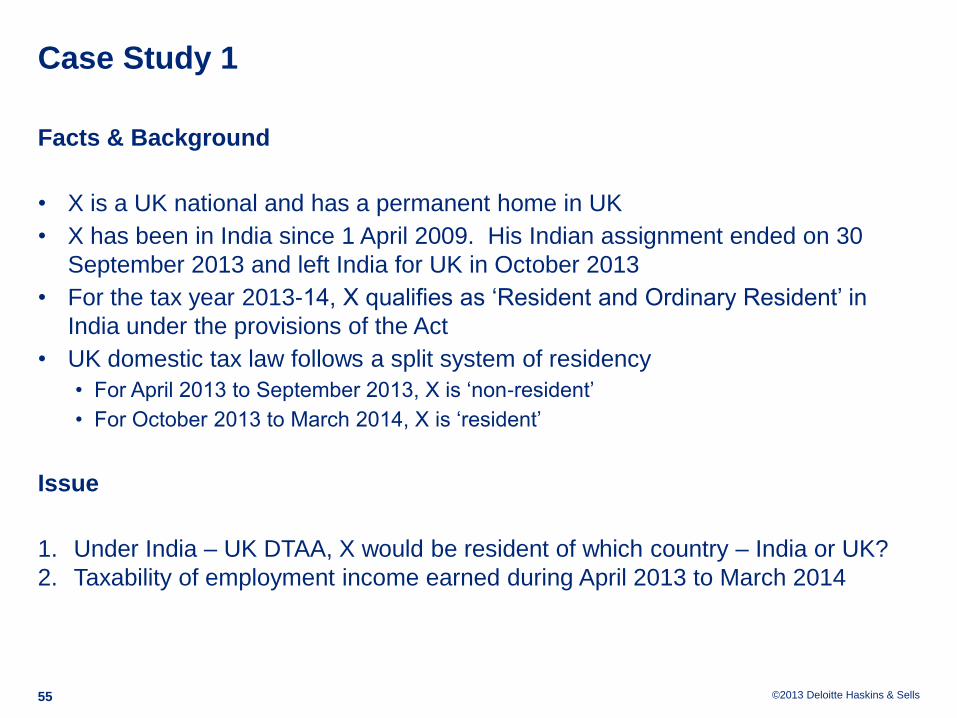

Case Study 1

©2013 Deloitte Haskins & Sells

Case Study 1

Facts & Background

• X is a UK national and has a permanent home in UK

• X has been in India since 1 April 2009. His Indian assignment ended on 30

September 2013 and left India for UK in October 2013

• For the tax year 2013-14, X qualifies as ‘Resident and Ordinary Resident’ in

India under the provisions of the Act

• UK domestic tax law follows a split system of residency

• For April 2013 to September 2013, X is ‘non-resident’

• For October 2013 to March 2014, X is ‘resident’

Issue

1. Under India – UK DTAA, X would be resident of which country – India or UK?

2. Taxability of employment income earned during April 2013 to March 2014

55

©2013 Deloitte Haskins & Sells

Case Study 2

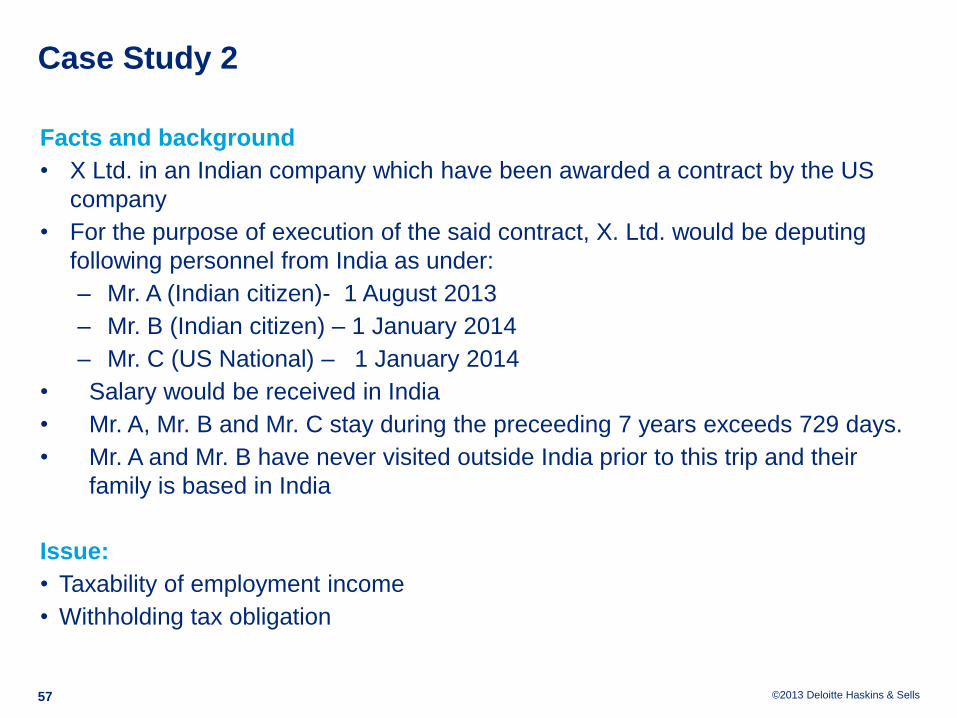

©2013 Deloitte Haskins & Sells

Case Study 2

Facts and background

• X Ltd. in an Indian company which have been awarded a contract by the US

company

• For the purpose of execution of the said contract, X. Ltd. would be deputing

following personnel from India as under:

‒ Mr. A (Indian citizen)- 1 August 2013

‒ Mr. B (Indian citizen) – 1 January 2014

‒ Mr. C (US National) – 1 January 2014

• Salary would be received in India

• Mr. A, Mr. B and Mr. C stay during the preceeding 7 years exceeds 729 days.

• Mr. A and Mr. B have never visited outside India prior to this trip and their

family is based in India

Issue:

• Taxability of employment income

• Withholding tax obligation

57

©2013 Deloitte Haskins & Sells

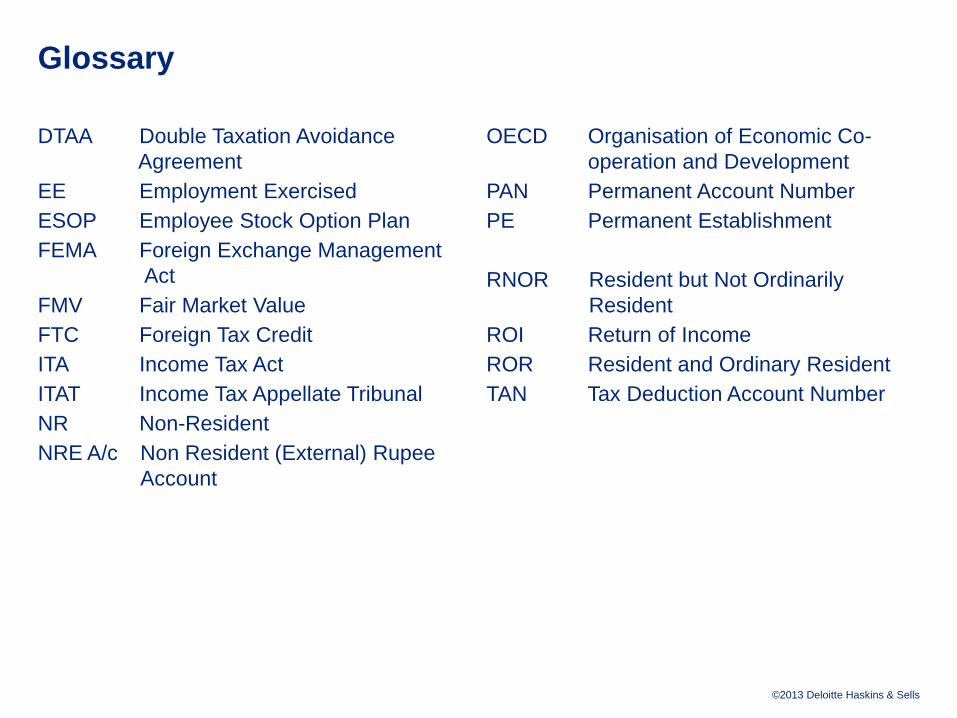

Glossary

DTAA Double Taxation Avoidance

Agreement

EE Employment Exercised

ESOP Employee Stock Option Plan

FEMA Foreign Exchange Management

Act

FMV Fair Market Value

FTC Foreign Tax Credit

ITA Income Tax Act

ITAT Income Tax Appellate Tribunal

NR Non-Resident

NRE A/c Non Resident (External) Rupee

Account

OECD Organisation of Economic Co-

operation and Development

PAN Permanent Account Number

PE Permanent Establishment

RNOR Resident but Not Ordinarily

Resident

ROI Return of Income

ROR Resident and Ordinary Resident

TAN Tax Deduction Account Number

This material and the information contained herein prepared by Deloitte Haskins & Sells (DHS) is intended to provide general information on a particular subject or

subjects and is not an exhaustive treatment of such subject(s). None of DHS, Deloitte Touche Tohmatsu Limited, its member firms, or their related entities

(collectively, the “Deloitte Network”) is, by means of this material, rendering professional advice or services. The information is not intended to be relied upon as

the sole basis for any decision which may affect you or your business. Before making any decision or taking any action that might affect your personal finances or

business, you should consult a qualified professional adviser.

No entity in the Deloitte Network shall be responsible for any loss whatsoever sustained by any person who relies on this material.

©2013 Deloitte Haskins & Sells