experience and change – consumer perspectives on respite services and the ndis national respite...

TRANSCRIPT

Experience and Change – consumer perspectives on respite services and the NDIS

National Respite and Community Care Conference 2014

Friday, 24th October 2014Cain Beckett, Director PwC

Why am I here?

I lead PwC’s disability assignments for Government’s and service providers nationally.

Chair of the NSW Disability Council advising the Minister for Aging and Disability Services

Started the Attitude Foundation with Graeme Innes AM just recently

10+ years as a board-member of Cerebral Palsy Alliance

• I am a customer!

2

3

A consumer view of the NDIS

1. What does the NDIS mean for your customers?

2. Perspectives on change and further ahead on the journey.

3. Questions

PwC 4

What does the NDIS mean for your customers?

PwC

NDIS: customer-led care under a national insurance model representing 1% of Australia’s GDP.

5 5

PwC

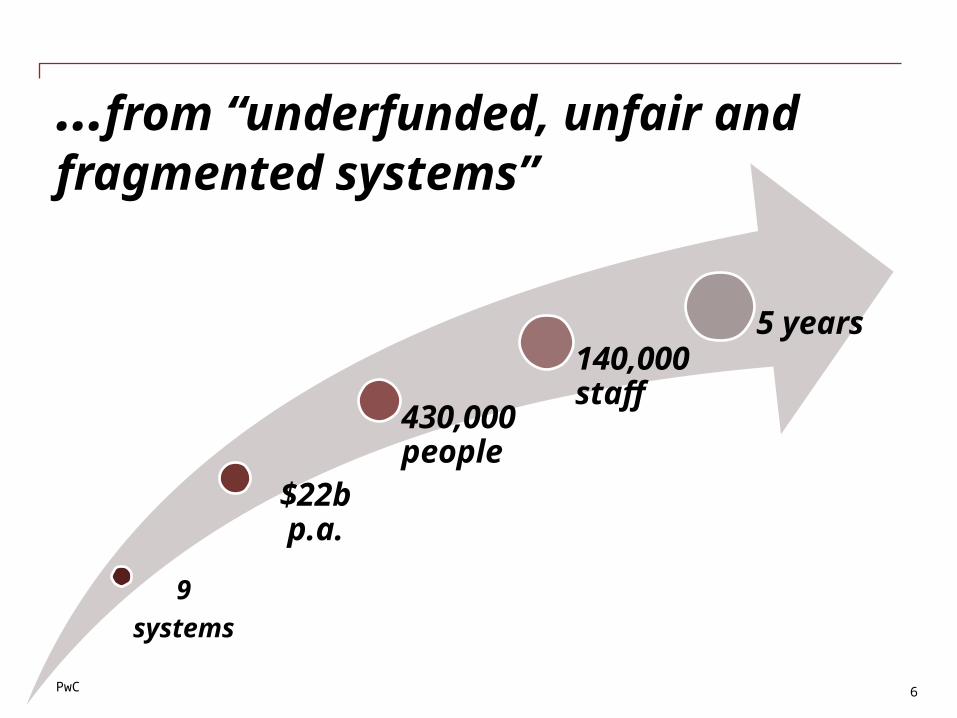

…from “underfunded, unfair and fragmented systems”

6

9systems

$22b p.a.

430,000 people

140,000 staff

5 years

6

PwC 7

Someone somewhere in Government no longer decides how many times a person with a disability can have a shower each week!

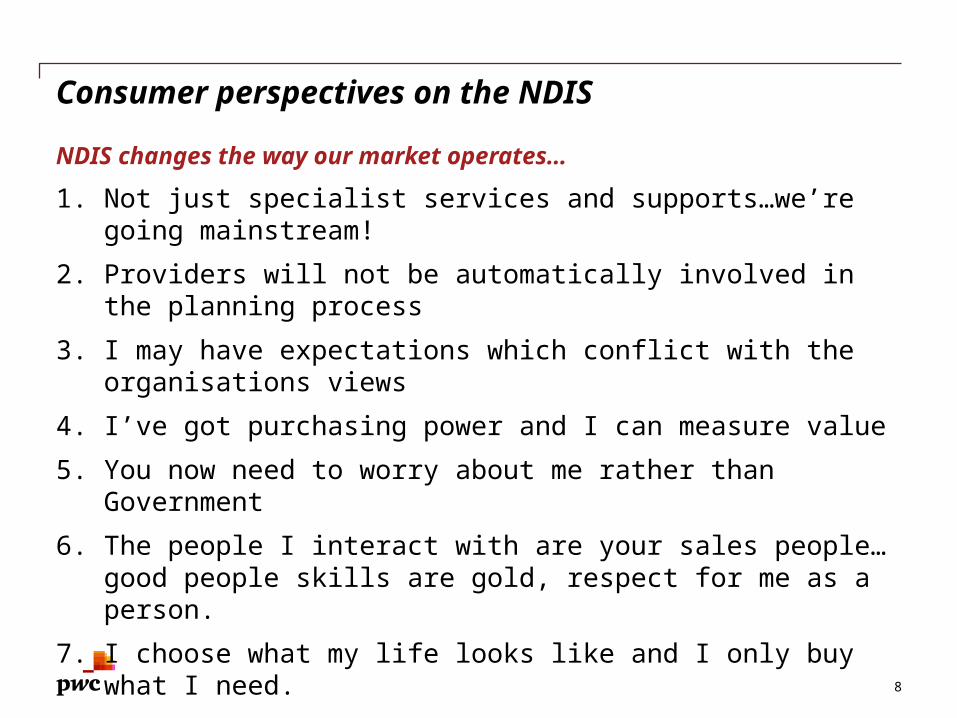

Consumer perspectives on the NDIS

NDIS changes the way our market operates…

1. Not just specialist services and supports…we’re going mainstream!

2. Providers will not be automatically involved in the planning process

3. I may have expectations which conflict with the organisations views

4. I’ve got purchasing power and I can measure value

5. You now need to worry about me rather than Government

6. The people I interact with are your sales people…good people skills are gold, respect for me as a person.

7. I choose what my life looks like and I only buy what I need.

8. I don’t care about your costs, or whether you make a profit 8

Its about the person so NDIS doesn’t call it respite

9

0

2,000,000

4,000,000

6,000,000

8,000,000

10,000,000

12,000,000

14,000,000NDIS expenditure - Q4 COAG report

PwC 10

Perspectives on NDIS change

In an attractive market, there will be new entrantsApproximate breakdown of likely NDIS spending in 2017-18

Source: Table 16.20 2011 Productivity Commission report

$1b

cvcv

cv

Est. annual spend on aids, appliances and home modification …roughly the same as the market for tea and coffee.

11

12

The NDIS policy approach is the cheapest option

Existing

GDP linked

ST2

NDIS

Source: PwC 2011, Disability Expectations : http://www.pwc.com.au/industry/government/assets/disability-in-australia.pdf

3. For governments the “do nothing option” is somewhere between $9bn - $30bn more costly.

13

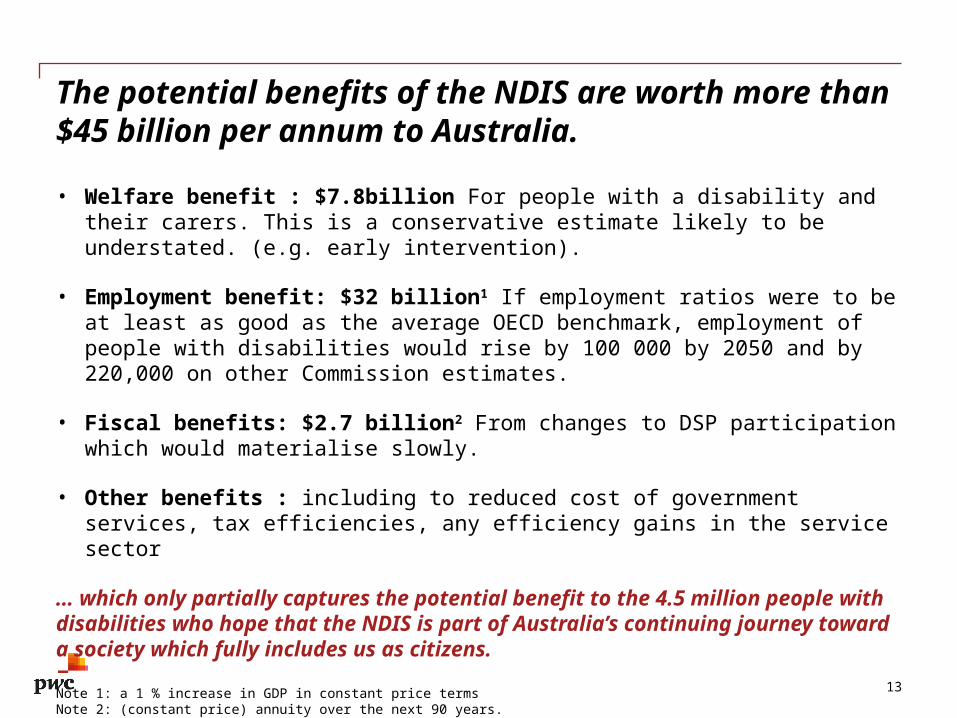

The potential benefits of the NDIS are worth more than $45 billion per annum to Australia.

• Welfare benefit : $7.8billion For people with a disability and their carers. This is a conservative estimate likely to be understated. (e.g. early intervention).

• Employment benefit: $32 billion1 If employment ratios were to be at least as good as the average OECD benchmark, employment of people with disabilities would rise by 100 000 by 2050 and by 220,000 on other Commission estimates.

• Fiscal benefits: $2.7 billion2 From changes to DSP participation which would materialise slowly.

• Other benefits : including to reduced cost of government services, tax efficiencies, any efficiency gains in the service sector

… which only partially captures the potential benefit to the 4.5 million people with disabilities who hope that the NDIS is part of Australia’s continuing journey toward a society which fully includes us as citizens.

Note 1: a 1 % increase in GDP in constant price termsNote 2: (constant price) annuity over the next 90 years.

14

Outside the trial sites the wave hasn’t hit yet, but is only 12-18 months away..

2013-14 2014-15 2016-17 2017-18 2018-190

100000

200000

300000

400000

500000

Per yearCummulative

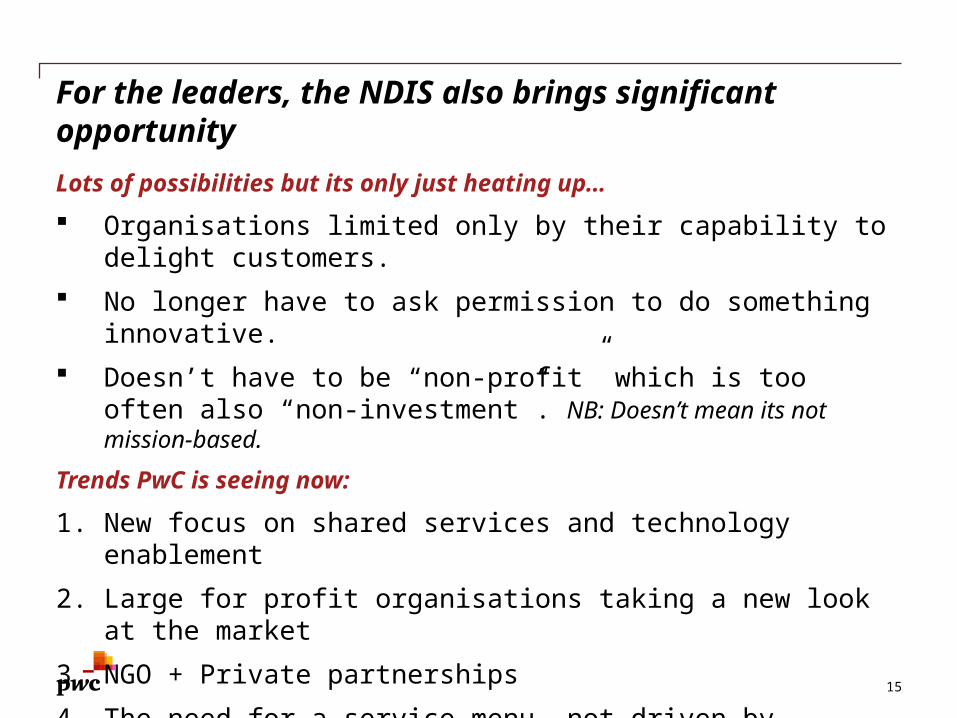

For the leaders, the NDIS also brings significant opportunity

Lots of possibilities but its only just heating up…

Organisations limited only by their capability to delight customers.

No longer have to ask permission to do something innovative.

Doesn’t have to be “non-profit” which is too often also “non-investment”. NB: Doesn’t mean its not mission-based.

Trends PwC is seeing now:

1. New focus on shared services and technology enablement

2. Large for profit organisations taking a new look at the market

3. NGO + Private partnerships

4. The need for a service menu, not driven by government.

5. Mergers and new business operating models15

Contact

© 2013 PricewaterhouseCoopers. All rights reserved.PwC refers to the Australian member firm, and may sometimes refer to the PwC network.Each member firm is a separate legal entity. Please see www.pwc.com/structure for further details.

Liability limited by a scheme approved under Professional Standards LegislationThis content is for general information purposes only, and should not be used as a substitute for consultation with professional advisors.

Cain Beckett , [email protected]: +61 (2) 8266 1854

PwC 17

Questions?