explicit option pricing formula for a mean-reverting asset in

TRANSCRIPT

Explicit Option Pricing Formula

for a Mean-Reverting Asset in

Energy Markets

Anatoliy SwishchukMathematical & Computational

Finance LabDept of Math & Stat, University

of Calgary, Calgary, AB, CanadaQMF 2007 Conference

Sydney, AustraliaDecember 12-15, 2007

This research is supported by MITACS and NSERC

Outline

• Mean-Reverting Models (MRM): Deterministic vs. Stochastic

• MRM in Finance Markets: Variances or Volatilities (Not Asset Prices)

• MRM in Energy Markets: Asset Prices

• Change of Time Method (CTM)

• Mean-Reverting Model (MRM)

• Option Pricing Formula

• Drawback of One-Factor Models

• Future Work

Motivations for the Work

• Paper: Javaheri, Wilmott and Haug (2002)

”GARCH and Volatility Swaps”, Wilmott

Magazine, Jan Issue (they applied PDE

approach to find a volatility swap for MRM and

asked about the possible option pricing formula

• Paper: Bos, Ware and Pavlov (2002) “On a

Semi-Spectral Method for Pricing an Option on a

Mean-Reverting Asset”, Quantit. Finance J.

(PDE approach, semi-spectral method to

calculate numerically the solution)

Wilmott, Javaheri & Haug (2002)

Model

• Wilmott, Javaheri & Haug (GARCH and Volatility Swaps, Wilmott Magazine, 2002)-volatility swap for

-continuous-time GARCH(1,1) model

M. Yor’s Results

• M. Yor On some exponential functions of

Brownian motion, Adv. In Applied Probab., v. 24,

No. 3, (1992), 509-531-started the research for

the integral of an exponential Brownian motion

• H. Matsumoto, M. Yor Exponential Functionals

of Brownian motion, I: Probability laws at fixed

time, Probability Surveys, v. 2 (2005), 312-347-

there is still no closed form probability density

function, while the best result is a function with a

double integral.

Mean-Reversion Effect

• Guitar String Analogy: if we pluck the guitar string, the string will revert to its place of equilibrium

• To measure how quickly this reversion back to the equilibrium location would happen we had to pluck the string

• Similarly, the only way to measure mean reversion is when the variances of asset prices in financial markets and asset prices in energy markets get plucked away from their non-event levels and we observe them go back to more or less the levels they started from

The Mean-Reverting Deterministic Process

Mean-Reverting Plot (a=4.6,L=2.5)

Meaning of Mean-Reverting Parameter

• The greater the mean-reverting parameter

value, a, the greater is the pull back to the

equilibrium level

• For a daily variable change, the change in time,

dt, in annualized terms is given by 1/365

• If a=365, the mean reversion would act so

quickly as to bring the variable back to its

equilibrium within a single day

• The value of 365/a gives us an idea of how

quickly the variable takes to get back to the

equilibrium-in days

Mean-Reverting Stochastic Process

Mean-Reverting Models in Financial

Markets

• Stock (asset) Prices follow

geometric Brownian motion

• The Variance of Stock Price

follows Mean-Reverting Models

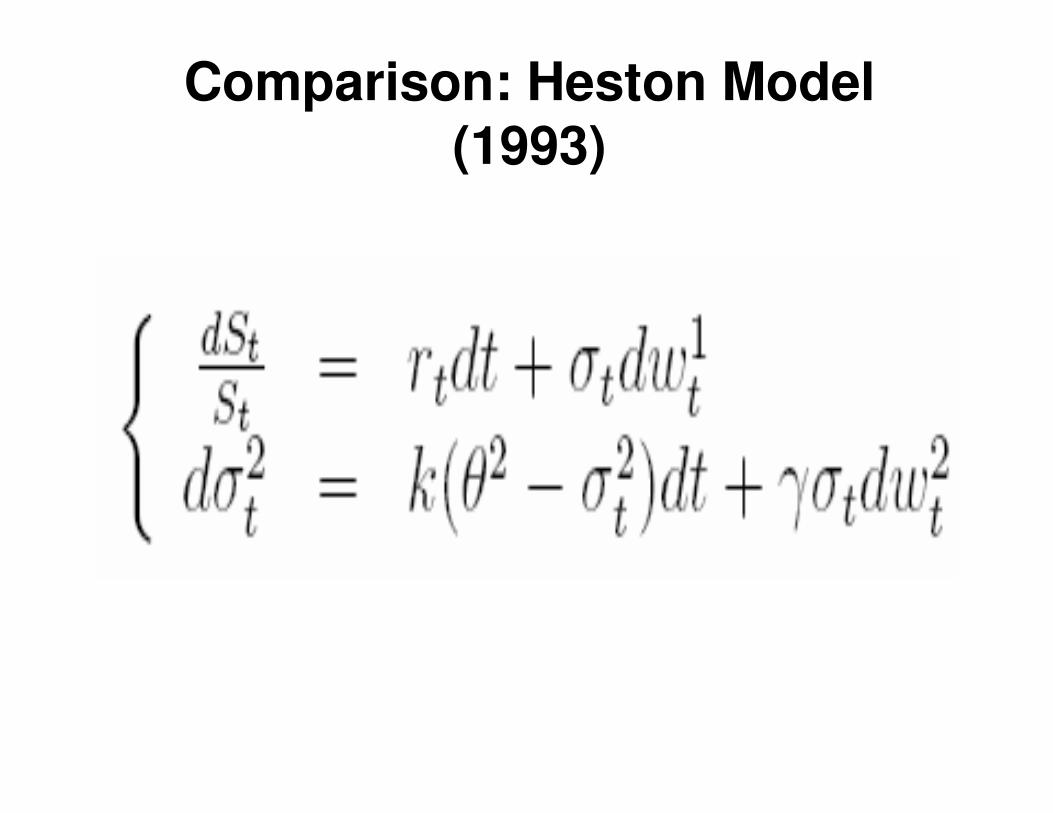

• Example: Heston Model

Mean-Reverting Models in

Energy Markets

• Asset Prices follow Mean-Reverting Stochastic Processes

• Example: Continuous-Time GARCH Model (or Pilipovic One-Factor Model)

Mean-Reverting Models in Energy

Markets

Change of Time: Definition and Examples

• Change of Time-change time from t to a non-negative process T(t) with non-decreasing sample paths

• Example1 (Subordinator): X(t) and T(t)>0 are some processes, then X(T(t)) is subordinated to X(t); T(t) is change of time

• Example 2 (Time-Changed Brownian Motion): M(t)=B(T(t)), B(t)-Brownian motion

• Example 3 (Product Process):

Time-Changed Brownian Motion by Bochner

• Bochner (1949) (‘Diffusion Equation and Stochastic Process’, Proc. N.A.S. USA, v. 35)-introduced the notion of change of time (CT) (time-changed Brownian motion)

• Bochner (1955) (‘Harmonic Analysis and the Theory of Probability’, UCLA Press, 176)-further development of CT

Change of Time: First Intro into Financial Economics

• Clark (1973) (‘A

‘Subordinated Stochastic

Process Model with Fixed Variance for Speculative

Prices’, Econometrica, 41, 135-156)-introduced

Bochner’s (1949) time-

changed Brownian motion into financial

economics:

• He wrote down a model for the log-price M as

M(t)=B(T(t)),

• where B(t) is Brownian

motion, T(t) is time-

change (B and T are independent)

Change of Time: Short History. I.

• Feller (1966) (‘An Introduction to Probability

Theory’, vol. II, NY: Wiley)-introduced subordinated

processes X(T(t)) with Markov process X(t) and T(t) as a process with independent increments (i.e., Poisson

process); T(t) was called randomized operational time

• Johnson (1979) (‘Option Pricing When the

Variance Rate is Changing’, working paper, UCLA)-introduced time-changed SVM in continuous time

• Johnson & Shanno (1987) (‘Option Pricing

When the Variance is Changing’, J. of Finan. & Quantit.

Analysis, 22, 143-151)-studied the pricing of options

using time-changing SVM

Change of Time: Short History. II.

• Ikeda & Watanabe (1981) (‘SDEs and Diffusion Processes’, North-Holland Publ. Co)-introduced and studied CTM for the solution of SDEs

• Barndorff-Nielsen, Nicolato & Shephard (2003) (‘Some recent development in stochastic volatility modelling’)-review and put in context some of their recent work on stochastic volatility (SV) modelling, including the relationship between subordination and SV (random time-chronometer)

• Carr, Geman, Madan & Yor (2003) (‘SV for Levy Processes’, mathematical Finance, vol.13)-used subordinated processes to construct SV for Levy Processes (T(t)-business time)

CT and Embedding Problem

• Embedding Problem was first terated by Skorokhod(1965)-sum of any sequence of i.r.v. with mean zero and

finite variation could be embedded in Brownian motion

(BM) using stopping time

• Dambis (1965) and Dubis and Schwartz (1965)-every

continuous martingale could be time-changed BM

• Huff (1969)-every processes of pathwise bounded

variation could be embedded in BM

• Monroe (1972)-every right continuous martingale could

be embedded in a BM

• Monroe (1978)-local martingale can be embedded in BM

Change of Time:

Simplest (Martingale) Case

Change of Time:

Ito Integral’s Case

Change of Time: SDE’s Case

Geometric Brownian Motion SVM

Change of Time Method

Connection between phi_t and phi_t^(-1)

Solution for GBM Equation

Using Change of Time

Explicit Expression for

Mean-Reverting SV Model

Solution of MRM by CTM

Explicit Expression for

Explicit Expression for

Comparison: Solution of GBM & MRM

-GBM

-MRM

Explicit Expression for S(t)

where

Properties of

Properties of

Properties of eta(t)

Properties of Eta(t). II.

Mean Value of MRM S(t)

Dependence of ES(t) on T

Dependence of ES(t) on S_0 and T

Variance for S(t)

Dependence of Variance of S(t) on S_0 and T

Dependence of Volatility of S(t) on S_0 and T

European Call Option for MRM.I.

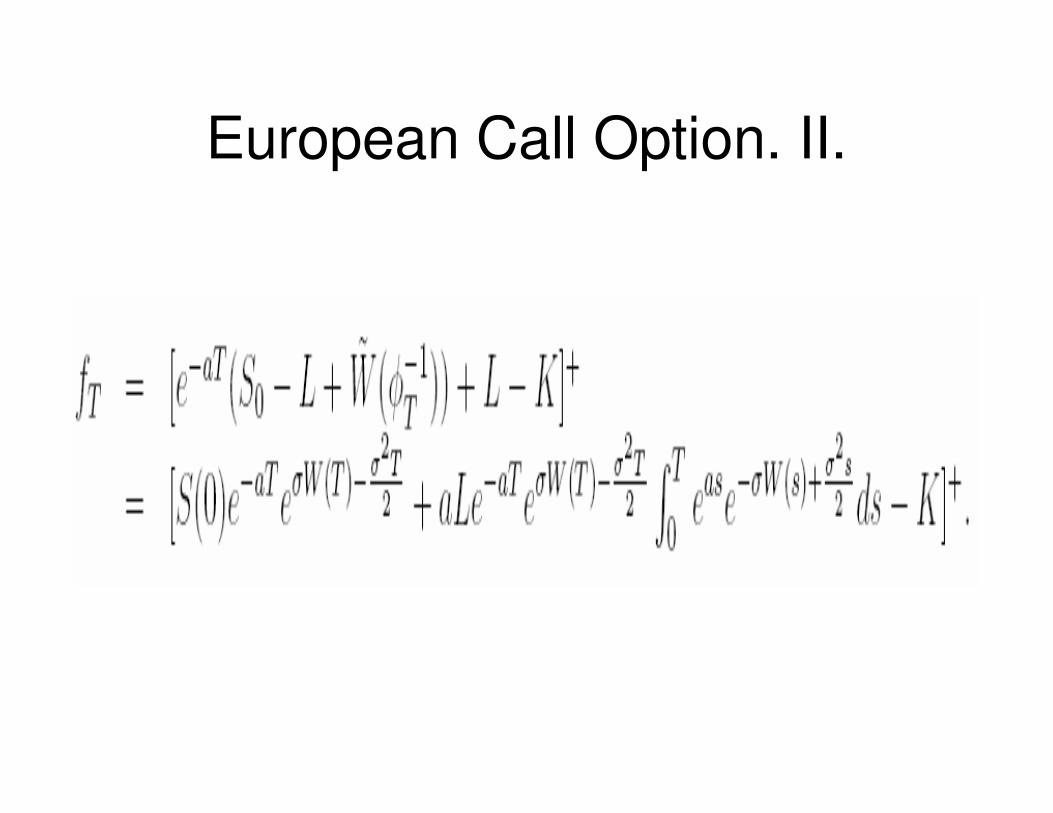

European Call Option. II.

Expression for C_T in the case of

MRM

C_T=BS(T)+A(T)

Expression for C_T=BS(T)+A(T).II.

Expression for BS(T)

Expression for y_0 for MRM

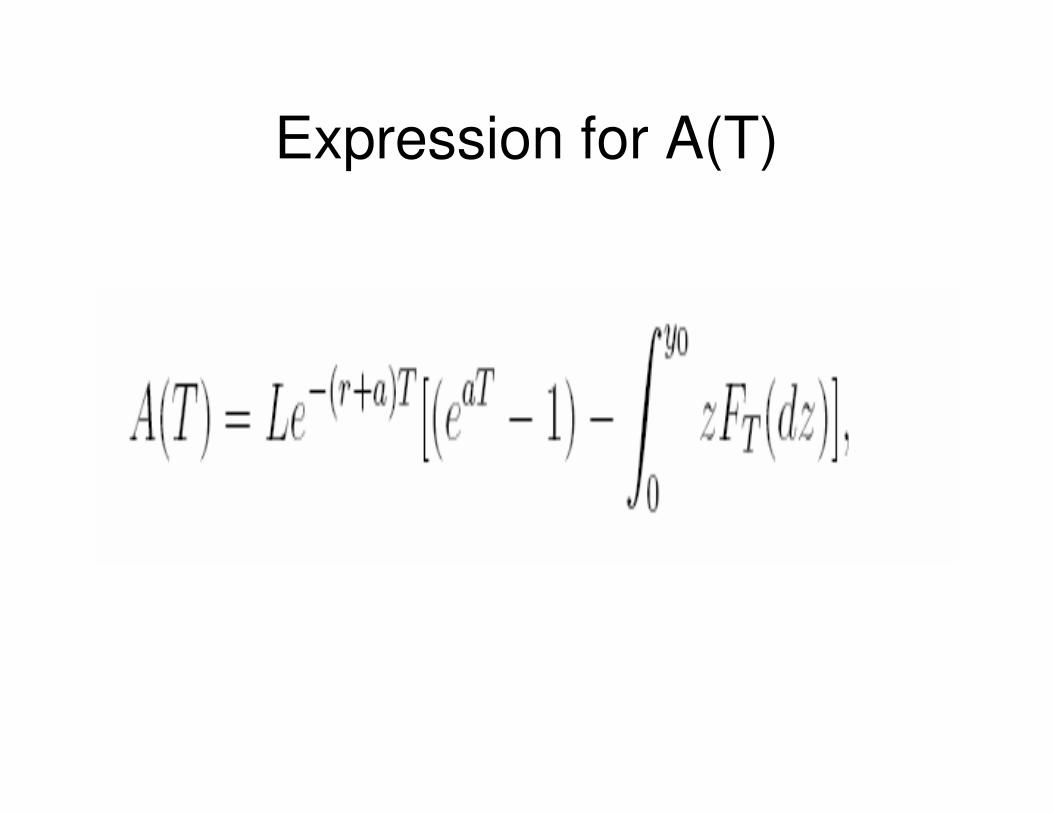

Expression for A(T).I.

Moment generating) function of

Eta(T)

Expression for A(T)

European Call Option for MRM

(Explicit Formula)

European Call Option for MRM in Risk-Neutral

World

Dependence of C_T on T

Comparison of Three Solutions

• Heston Model

• Mean-Reverting Model

• Black-Scholes Model

Comparison: Heston Model

(1993)

Explicit Solution for CIR Process: CTM

Comparison: Solutions to the Three

Models

-GBM

-MRM

-Heston model

Summary

-martingale

-martingale

-sum of two martingales

1.

2.

3.

GBM Model

Mean-Reverting Model

Heston Model

Problem

-explicit expression ?

We know all the moments at this moment, though

To calculate an option price for Heston model, for example

Drawback of One-Factor Mean-

Reverting Models

• The long-term mean L remains fixed over time: needs to be recalibrated on a continuous basis in order to ensure that the resulting curves are marked to market

• The biggest drawback is in option pricing: results in a model-implied volatility term structure that has the volatilities going to zero as expiration time increases (spot volatilities have to be increased to non-intuitive levels so that the long term options do not lose all the volatility value-as in the marketplace they certainly do not)

Future Work

• Change of Time

Method for Two-

Factor

Continuous-Time

GARCH Model

The End

Thank You for Your

Attention and Time!

http://wwww.math.ucalgary.ca/~aswish/