exploration for and evaluation of mineral resources: ifrs 6 wiecek and young ifrs primer chapter 12

TRANSCRIPT

Exploration for and Evaluation of Mineral Resources: IFRS 6

Wiecek and Young

IFRS PrimerChapter 12

2

Exploration for and Evaluation of Mineral Resources Related standards IFRS 6 Current GAAP comparisons IFRS financial statement disclosures Looking ahead End-of-chapter practice

3

Related Standards

FAS 144 Accounting for the impairment or disposal of long-lived assets

FAS 69 Disclosures about oil and gas producing activities

FAS 25 Amendment of FASB Statement No. 19

FAS 19 Financial accounting by oil and gas producing companies

4

Related Standards

IAS 8 Accounting policies, changes in accounting estimates and errors

IAS 16 Property, plant and equipment IAS 36 Impairment of assets IAS 37 Provisions, contingent liabilities and

contingent assets IAS 38 Intangible assets

5

IFRS 6 - Overview

Objective and scope Recognition and measurement of exploration

and evaluation assets Impairment Disclosure

6

IFRS 6 – Objective and Scope

IFRS 6 is limited to the accounting for and reporting of costs associated only with the exploration and evaluation of mineral resources. These activities are defined as:

- the search for mineral resources…after the entity has obtained legal rights to explore in a specific area, and

- the determination of the technical feasibility and commercial viability of extracting the mineral resource.

7

IFRS 6 – Objective and Scope

IFRS 6 is an interim measure pending completion of a major project on extractive activities.

Permits continuation of accounting policies used prior to adoption of IFRS

Accounting policies may be inconsistent with IFRS Framework

8

IFRS 6 – Recognition and Measurement of Exploration and Evaluation Assets

Recognition:- Companies use a variety of methods to account

for exploration and evaluation activities, from expensing all related costs to fully capitalizing them

- Therefore, exploration and evaluation assets are defined in terms of the policy each company chooses

9

IFRS 6 – Recognition and Measurement of Exploration and Evaluation Assets

Exploration and evaluation assets are recognized at cost

Examples of costs that may be capitalized:

- Cost of exploration rights, geological studies, exploratory drilling and sampling, and evaluating technical and commercial viability of extraction

10

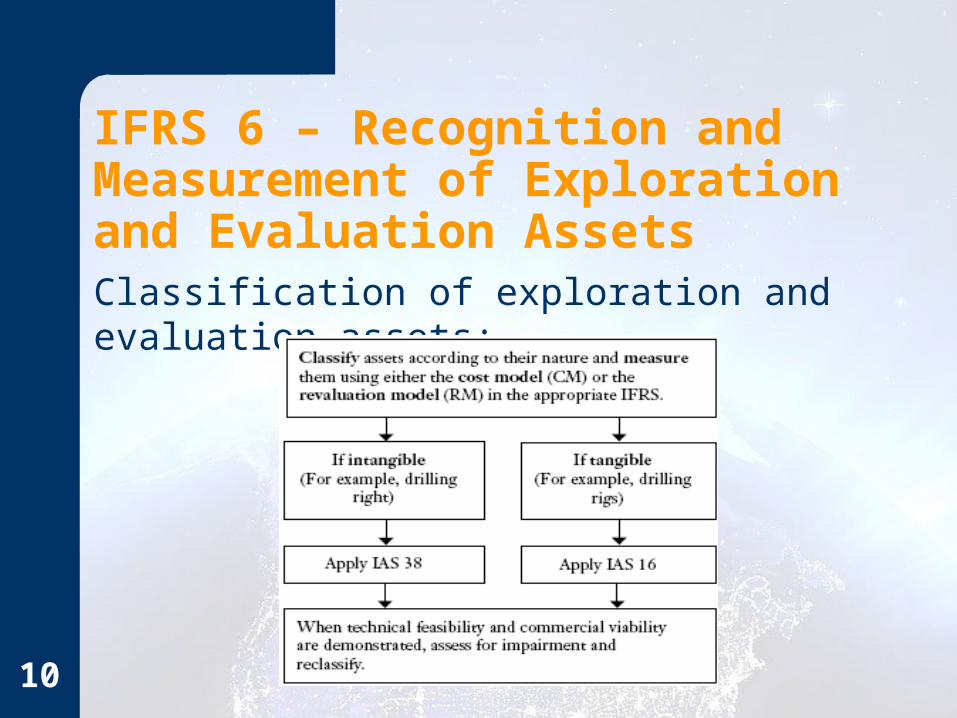

IFRS 6 – Recognition and Measurement of Exploration and Evaluation Assets

Classification of exploration and evaluation assets:

11

IFRS 6 - Impairment

Impaired? When facts and circumstances suggest that carrying amount > recoverable amount. Consider:

the right to explore expires and is not expected to be renewed no other substantial expenditures are planned for exploration or

evaluation in the area the entity decides to stop exploration and evaluation activities

because viable quantities have not been found in the area although development is likely, the costs capitalized as

exploration and evaluation assets exceed the amounts that are likely to be recovered

Impairment losses are taken to profit or loss – may be reversed

12

IFRS 6 - Disclosure

Disclosure objective: to identify and explain amounts recognized in the financial statements that result from exploration and evaluation activities

If classified as PP&E, use IAS 16 If classified as intangible asset, use IAS 38

13

IFRS 6 - Disclosure

Minimum disclosure:- Accounting policies for exploration and

evaluation expenditures and their capitalization as assets

- The amount of assets, liabilities, income, expense, and operating and investing cash flows from exploration and evaluation activities

14

Current GAAP Comparisons

Page 156 of 164 ofhttp://www.kpmg.co.uk/pubs/IFRScomparedtoU.S.GAAPAnOverview(2008).pdf

15

IFRS Financial Statement DisclosuresRoyal Dutch Shell plchttp://www-static.shell.com/static/investor/downloads/financial_information/reports/2007/2007_annual_report.pdf

Accounting policies – page 122 of 224Key accounting estimates – page 127 of 224Property, plant & equipment – pages 135-137

of 224

16

Looking Ahead

Comprehensive research project underway for approach to resolving issues unique to upstream extractive activities in mining and oil and gas industries

Discussion paper expected late 2009, with decision to proceed to be determined in late 2010

17

End-of-Chapter Practice

Copyright © 2010 John Wiley & Sons, Inc. All rights reserved. Reproduction or translation of this work beyond that permitted

by Access Copyright is unlawful. Requests for further information should be addressed to the Permissions

Department, John Wiley & Sons Inc., 111 River Street, Hoboken, NJ 07030-5774, (201) 748-6011, fax (201) 748-6008, website

http://www.wiley.com/go/permissions. The purchaser may make back-up copies for his or her own use only and not for

distribution or resale. The author and the publisher assume no responsibility for errors, omissions, or damages caused by the

use of these programs or from the use of the information contained herein.