explore your employee benefts - standardwe believe in protecting what matters abc company, inc....

TRANSCRIPT

Explore Your Employee Benefts We believe in protecting what matters

ABC Company, Inc.

Standard Insurance Company ABC COMPANY®

1

ABC Company, Inc.

Group Policy #000000

Act Now to Help Protect What You Care About

When you buy insurance through work, you get

competitive group rates. And it’s convenient, with premiums deducted right

from your paycheck.

Having a lot of beneft choices is great — but can be confusing! You may be wondering … which ones are the best for me and my family?

Think of insurance as a fnancial safety net that can help protect you when life doesn’t go as planned. Each beneft that ABC Company, Inc. offers can play a role in helping you achieve fnancial security.

Enrolling in coverage now is an easy way to help make sure you and your loved ones have the protection you need. Use this guide to explore your group insurance options from Standard Insurance Company (The Standard). The forms you need are also right here.

Explore your beneft options with ABC Company, Inc.

• Additional Life insurance

• Additional Accidental Death and

Dismemberment

• Short Term Disability insurance

• Long Term Disability insurance

Benefts You Can Add at Group Rates

• Basic Life insurance

• Accidental Death and Dismemberment insurance

• Dependents Life insurance

Your Employer-Paid Benefts

The Standard 1 Welcome Letter

Protect Your Family From the Unexpected An accident, serious illness or hospital stay can be a big drain on your fnances. Even with medical insurance, deductibles and copays can pile up. The insurance below pays a beneft directly to you — instead of your doctors. So, you can use the money for anything you choose — from medical costs to rent, gas and groceries.

Accident insurance can help keep your fnances on track when an accident happens. It pays a beneft directly to you, not to medical providers. Another plus, your group insurance rate won’t increase as you get older.

Critical Illness insurance helps you manage expenses during a serious illness, such as a heart attack, stroke or cancer. It pays a lump-sum beneft directly to you upon diagnosis with a covered illness. You can use the

ENROLL SOON

Enrollment begins January 1, 2019 and ends January 15, 2019.

ATTEND YOUR GROUP MEETING ON:

• January 2, 2019, 3pm, Atrium

• January 10, 2019, 3pm, Atrium

2

money to pay bills while you or a family member recover.

Hospital Indemnity insurance can help you take care of the out-of-pocket costs of a stay in the hospital. It pays you a fat beneft regardless of any medical coverage you have.

Protect Your Health Dental insurance from The Standard helps you and your family take care of your smiles and your health. You can choose your own dentist. Visit standard.com/dental to fnd an in-network dentist in your area.

Vision insurance includes coverage for eye exams and helps pay for contact lenses and glasses. Visit standard.com/vision to find an in-network vision specialist.

Protect Your Loved Ones Life insurance helps take care of your family if something happens to you. It can help your loved ones get through a difficult time and pay for important things, like a home or college plans.

Accidental Death and Dismemberment (AD&D) insurance helps protect your family’s fnances if an accident causes death or a severe physical loss. It pays a beneft in addition to any life insurance you have. That can help pay for a funeral or ongoing special care.

Protect Your Paycheck Disability insurance can replace part of your paycheck if you can’t work because of an illness, injury or pregnancy. The beneft payments can help with bills that continue even when you can’t work — like your rent

Enroll online at www.standard.com

Contact your employee benefts representative if you have questions about submitting forms.

or mortgage.

Short term disability insurance can help pay the bills if you become disabled and can’t work for a short period of time.

Long term disability insurance helps replace part of your paycheck if you experience a disability that lasts for months or even years.

Ready to apply? You’ll fnd the forms right here. Once you review your options, the next step is to apply using the forms at the end of this guide. Remember to turn them in before your enrollment 000000 period ends! SI 20444 (3/19)

The Standard 2 Welcome Letter

We Believe

WE’RE AT OUR BEST WHEN YOU NEED US THE MOST The heart of our business is helping you navigate life’s challenges. Whether you have lost a loved one, are recovering from a disabling event or are planning for the future, we’re there for you with exceptional customer service and support. We consistently step up to meet your needs — focusing our time, energy and expertise —to make work and life a little bit easier for you.

3

Standard Insurance Company ABC Company, Inc. Group Policy #000000 Effective Date Month, Day, Year

GROUP BASIC LIFE AND ACCIDENTAL DEATH AND DISMEMBERMENT INSURANCE

Group Basic Life insurance from Standard Insurance Company helps provide fnancial protection by promising to pay a beneft in the event of an eligible member’s , or his or her dependent’s, covered death. Basic Accidental Death and Dismemberment (AD&D) insurance may provide an additional amount in the event of a covered death or dismemberment as a result of an accident.

The cost of this insurance is paid by ABC Company, Inc.

Eligibility

Defnition of a Member You are a member if you are an active employee of ABC Company, Inc. and regularly working at least 00 hours each week. You are not a member if you are a temporary or seasonal employee, a full-time member of the armed forces, a leased employee or an independent contractor.

Class Defnition Class 1 All full-time salaried members Class 2 All other members

Eligibility Waiting Period If you are already a member on the date the group policy is effective, you are eligible on that date. If you become a member after the group policy effective date, you are eligible on the frst day of the month that follows or coincides with 00 days as a member.

Your dependents will need to provide acceptable evidence of good health if you elect coverage after initially becoming eligible.

Benefts

Your Basic Life coverage amount is 0 times your annual earnings to a maximum of $000,000. Acceptable evidence of good health may be required to become insured for the amount of coverage in excess of $000,000.

Basic Life Coverage Amount

The Standard 14 Group Basic Life and AD&D Insurance

Benefts Continued

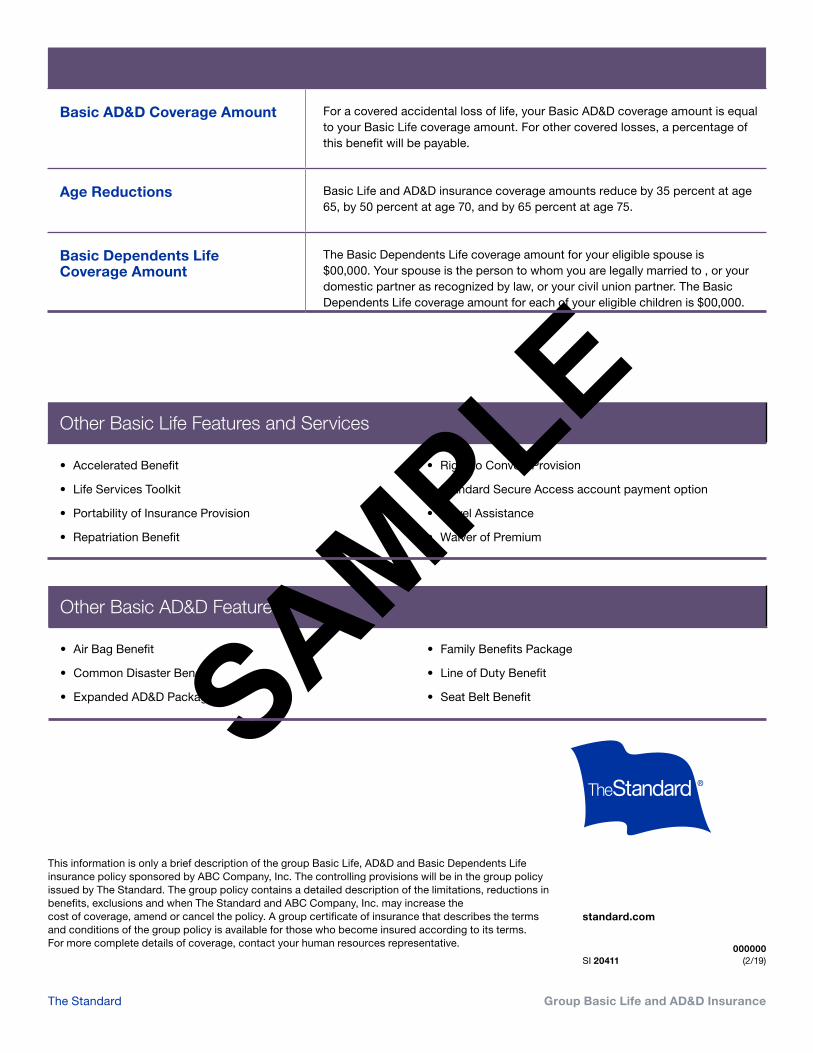

Basic AD&D Coverage Amount For a covered accidental loss of life, your Basic AD&D coverage amount is equal to your Basic Life coverage amount. For other covered losses, a percentage of this beneft will be payable.

Age Reductions Basic Life and AD&D insurance coverage amounts reduce by 35 percent at age 65, by 50 percent at age 70, and by 65 percent at age 75.

Basic Dependents Life Coverage Amount

The Basic Dependents Life coverage amount for your eligible spouse is $00,000. Your spouse is the person to whom you are legally married to , or your domestic partner as recognized by law, or your civil union partner. The Basic Dependents Life coverage amount for each of your eligible children is $00,000.

Other Basic Life Features and Services

• Accelerated Beneft

• Life Services Toolkit

• Portability of Insurance Provision

• Repatriation Beneft

• Right to Convert Provision

• Standard Secure Access account payment option

• Travel Assistance

• Waiver of Premium

Other Basic AD&D Features

• Air Bag Beneft

• Common Disaster Beneft

• Expanded AD&D Package

• Family Benefts Package

• Line of Duty Beneft

• Seat Belt Beneft

This information is only a brief description of the group Basic Life, AD&D and Basic Dependents Life insurance policy sponsored by ABC Company, Inc. The controlling provisions will be in the group policy issued by The Standard. The group policy contains a detailed description of the limitations, reductions in benefts, exclusions and when The Standard and ABC Company, Inc. may increase the cost of coverage, amend or cancel the policy. A group certifcate of insurance that describes the terms and conditions of the group policy is available for those who become insured according to its terms. For more complete details of coverage, contact your human resources representative.

Standard Insurance Company 1100 SW Sixth Avenue Portland OR 97204

standard.com

000000 SI 20411 (2/19)

The Standard 25 Group Basic Life and AD&D Insurance

We Believe in

A CULTURE OF CARING The remarkable individuals who fnd their way to The Standard are united by their compassion and a genuine desire to help. And it doesn’t stop there. Our employees volunteer their time to community partners across the country. Our culture of caring places a high value on giving back and the difference that makes to our customers and local communities.

6

’

0 -111 II 1

A L®

Standard Insurance Company ABC Company, Inc. Group Policy #000000

GROUP ADDITIONAL LIFE AND AD&D INSURANCE

We can help provide for your family when you can’t.

Life insurance helps protect the people who depend on your income by paying them an amount of money specified in the policy if you die.

AD&D insurance pays an amount of money specified in the policy if a covered accident results in your death or a severe physical loss, such as a hand, a foot or your eyesight.

Life and AD&D insurance is an easy, responsible way to help your loved ones during a difficult time — and into the future.

What’s at stake. A death or serious accident might

Additional Life

leave your family facing expenses they couldn t cover without your income. That could include extra costs for medical care or a funeral.

Group Additional Life and Accidental Death and Dismemberment (AD&D) insurance can help protect your family’s finances if something happens to you. This coverage can help provide financial support and stability to your family if you pass away or have a serious accident.

and AD&D insurance can help make things easier for the people you care about.

You’re covered under Basic Life insurance if you take no action, provided you meet the eligibility requirements. But if Basic Life insurance doesn’t meet your needs, you can apply for additional coverage. Plan now to help your family cover future expenses like:

Tuition Child Care Housing Daily Living Costs Expenses

The Standard 18 Group Additional Life and AD&D Insurance

Life Insurance

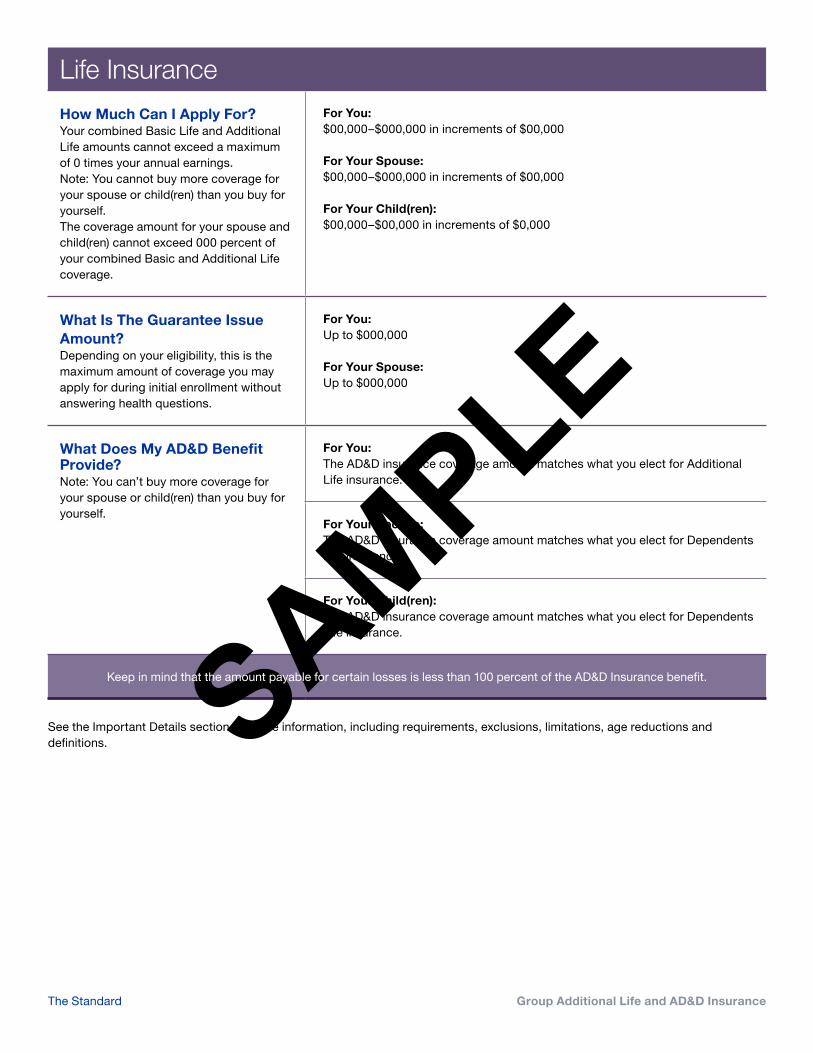

How Much Can I Apply For? For You:

Your combined Basic Life and Additional $00,000–$000,000 in increments of $00,000

Life amounts cannot exceed a maximum of 0 times your annual earnings. For Your Spouse:

Note: You cannot buy more coverage for $00,000–$000,000 in increments of $00,000

your spouse or child(ren) than you buy for yourself. For Your Child(ren):

The coverage amount for your spouse and $00,000–$00,000 in increments of $0,000

child(ren) cannot exceed 000 percent of your combined Basic and Additional Life coverage.

What Is The Guarantee Issue Amount? Depending on your eligibility, this is the maximum amount of coverage you may apply for during initial enrollment without answering health questions.

For You: Up to $000,000

For Your Spouse: Up to $000,000

What Does My AD&D Benefit Provide? Note: You can’t buy more coverage for your spouse or child(ren) than you buy for yourself.

For You: The AD&D insurance coverage amount matches what you elect for Additional Life insurance.

For Your Spouse: The AD&D insurance coverage amount matches what you elect for Dependents Life insurance.

For Your Child(ren): The AD&D insurance coverage amount matches what you elect for Dependents Life insurance.

Keep in mind that the amount payable for certain losses is less than 100 percent of the AD&D Insurance benefit.

See the Important Details section for more information, including requirements, exclusions, limitations, age reductions and definitions.

The Standard 29 Group Additional Life and AD&D Insurance

@

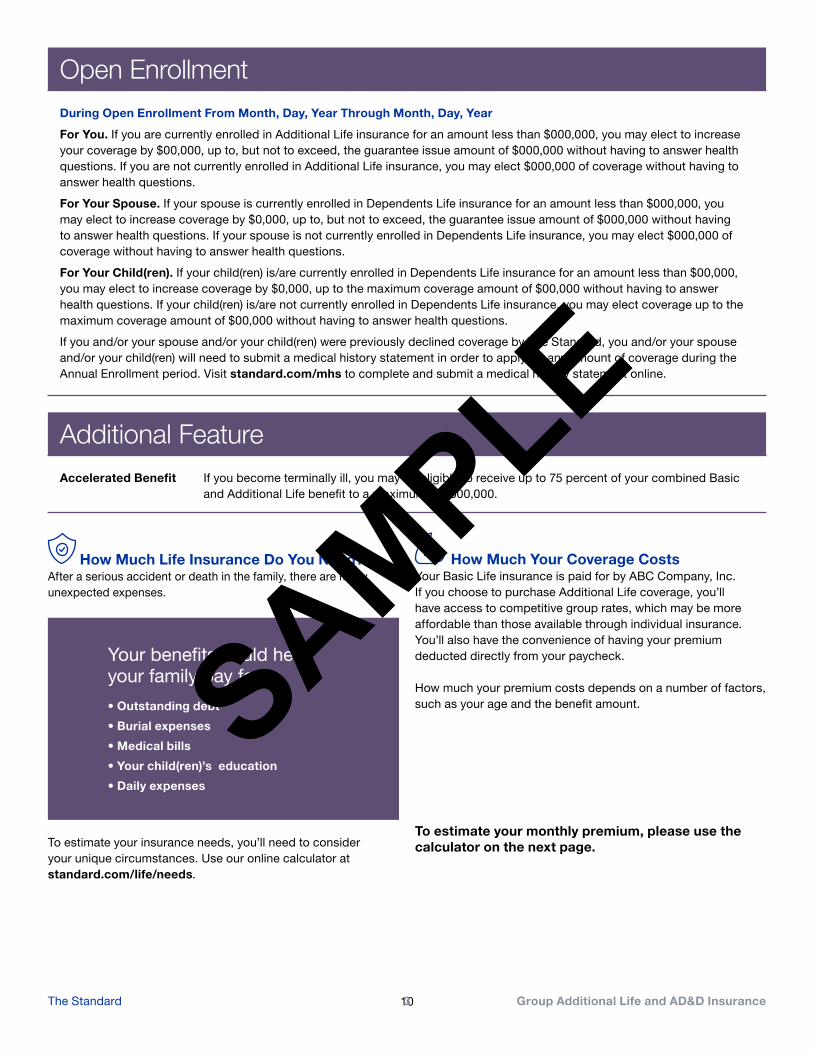

Open Enrollment During Open Enrollment From Month, Day, Year Through Month, Day, Year

For You. If you are currently enrolled in Additional Life insurance for an amount less than $000,000, you may elect to increase your coverage by $00,000, up to, but not to exceed, the guarantee issue amount of $000,000 without having to answer health questions. If you are not currently enrolled in Additional Life insurance, you may elect $000,000 of coverage without having to answer health questions.

For Your Spouse. If your spouse is currently enrolled in Dependents Life insurance for an amount less than $000,000, you may elect to increase coverage by $0,000, up to, but not to exceed, the guarantee issue amount of $000,000 without having to answer health questions. If your spouse is not currently enrolled in Dependents Life insurance, you may elect $000,000 of coverage without having to answer health questions.

For Your Child(ren). If your child(ren) is/are currently enrolled in Dependents Life insurance for an amount less than $00,000, you may elect to increase coverage by $0,000, up to the maximum coverage amount of $00,000 without having to answer health questions. If your child(ren) is/are not currently enrolled in Dependents Life insurance, you may elect coverage up to the maximum coverage amount of $00,000 without having to answer health questions.

If you and/or your spouse and/or your child(ren) were previously declined coverage by The Standard, you and/or your spouse and/or your child(ren) will need to submit a medical history statement in order to apply for any amount of coverage during the Annual Enrollment period. Visit standard.com/mhs to complete and submit a medical history statement online.

Additional Feature Accelerated Benefit If you become terminally ill, you may be eligible to receive up to 75 percent of your combined Basic

and Additional Life benefit to a maximum of $500,000.

How Much Your Coverage Costs Your Basic Life insurance is paid for by ABC Company, Inc. If you choose to purchase Additional Life coverage, you’ll have access to competitive group rates, which may be more affordable than those available through individual insurance. You’ll also have the convenience of having your premium deducted directly from your paycheck.

How much your premium costs depends on a number of factors, such as your age and the benefit amount.

How Much Life Insurance Do You Need? After a serious accident or death in the family, there are many unexpected expenses.

Your benefits could help your family pay for:

• Outstanding debt

• Burial expenses

• Medical bills

• Your child(ren)’s education

• Daily expenses

To estimate your monthly premium, please use the To estimate your insurance needs, you’ll need to consider calculator on the next page. your unique circumstances. Use our online calculator at standard.com/life/needs.

The Standard 103 Group Additional Life and AD&D Insurance

Use this formula to calculate your premium payment:

÷ 1000 = x = --->

Enter the amount of coverage Enter your rate from This amount is an To get a sense of your semimonthly you are requesting (see benefit the rate table. estimate of how premium, take your monthly premium, amounts on page 2). much you would multiply by 12 months, and divide by 24

pay each month. pay periods. This is your semimonthly premium.

If you buy coverage for your spouse, your monthly rate is shown in the following table. Use the same formula to calculate the premium that you used for yourself, but use your spouse’s age and your spouse’s rate.

If you buy Dependents Life with AD&D coverage for your child(ren), your monthly rate is $0.00 per $0,000 for $00,000, no matter how many children you’re covering. Your monthly AD&D rate of $0.00 per $1,000 of AD&D benefit is included.

Age (as of January 1)

Your Rate* (Per $1,000 of

Total Coverage)

Your Spouse s Rate** (Per $1,000 of

Total Coverage)

<30 $0.00 $0.00

30–34 $0.00 $0.00

35–39 $0.00 $0.00

40–44 $0.00 $0.00

45–49 $0.00 $0.00

50–54 $0.00 $0.00

55–59 $0.00 $0.00

60–64 $0.00 $0.00

65–69 $0.00 $0.00

70–74 $0.00 $0.00

75+ $0.00 $0.00

*Includes a monthly AD&D rate of $0.00 per $1,000 of AD&D benefit

**Includes a monthly AD&D rate of $0.00 per $1,000 of AD&D benefit for your spouse.

’

The Standard 114 Group Additional Life and AD&D Insurance

Important Details Here’s where you’ll find the nitty-gritty details about the plan.

Life and AD&D Insurance Eligibility Requirements A minimum number of eligible employees must apply and qualify for the proposed plan before coverage can become effective. If this requirement is not met, this plan will not become effective. To be eligible for coverage, you must be:

• Insured for Basic Life insurance through The Standard

• An active employee of ABC Company, Inc. regularly

working at least 00 hours per week

• Class 1

• Class 2

Temporary and seasonal employees, full-time members of the armed forces, leased employees and independent contractors are not eligible.

If you buy Additional Life and AD&D insurance for yourself, you may also buy Life and AD&D coverage for your eligible child(ren) and/or spouse. This is called Dependents Life and AD&D insurance.

You can choose to cover your spouse, meaning a person to whom you are legally married, or your domestic partner as recognized by law, or your civil union partner.

You may also choose to cover your child. Child means your unmarried child from live birth through age 20 (through age 24 if a registered student in full-time attendance at an accredited educational institution). Please note:

• Your child cannot be insured by more than one employee.

• Your spouse or child(ren) must not be a full-time member(s) of

the armed forces.

• You cannot be insured as both an individual and a dependent.

Medical Underwriting Approval for Life Coverage Required for:

• Coverage amounts higher than the guarantee issue

amount

• All late applications (applying 00 days after becoming

eligible)

• Requests for coverage increases

• Reinstatements

• Employees eligible but not insured under the prior life

insurance plan

Visit standard.com/mhs to submit a medical history statement online.

Note: If your family status changes, you may have the ability to apply for coverage or increase your coverage for a limited time without having to submit a medical history statement. Please see your human resources representative or plan administrator

Coverage Effective Date for Life Coverage To become insured, you must:

• Meet the eligibility requirements listed in the previous

sections,

• Serve an eligibility waiting period,*

• Receive medical underwriting approval (if applicable),

• Apply for coverage and agree to pay premium, and

• Be actively at work (able to perform all normal duties of

your job) on the day before the insurance is scheduled

to be effective.

*The eligibility waiting period varies; contact your human

resources representative for details.

If you are not actively at work on the day before the scheduled effective date of your insurance , including any Dependents Life insurance coverages, your insurance will not become effective until the day after you complete one full day of active work as an eligible employee. You may have a different effective date for Life coverage below and above the guarantee issue amount. Contact your human resources representative or plan administrator for further information about the applicable coverage effective date for your insurance, including Dependents Life insurance.

Life and AD&D Age Reductions Under this plan, your coverage amount reduces to 65 percent at age 65, to 50 percent at age 70 and to 35 percent at age 75. Your spouse’s coverage amount reduces by your spouse’s age as follows: to 65 percent at age 65, to 50 percent at age 70 and to 35 percent at age 75. If you or your spouse are age 65 or over, ask your human resources representative or plan administrator for the amount of coverage available.

The Standard 125 Group Additional Life and AD&D Insurance

-

-

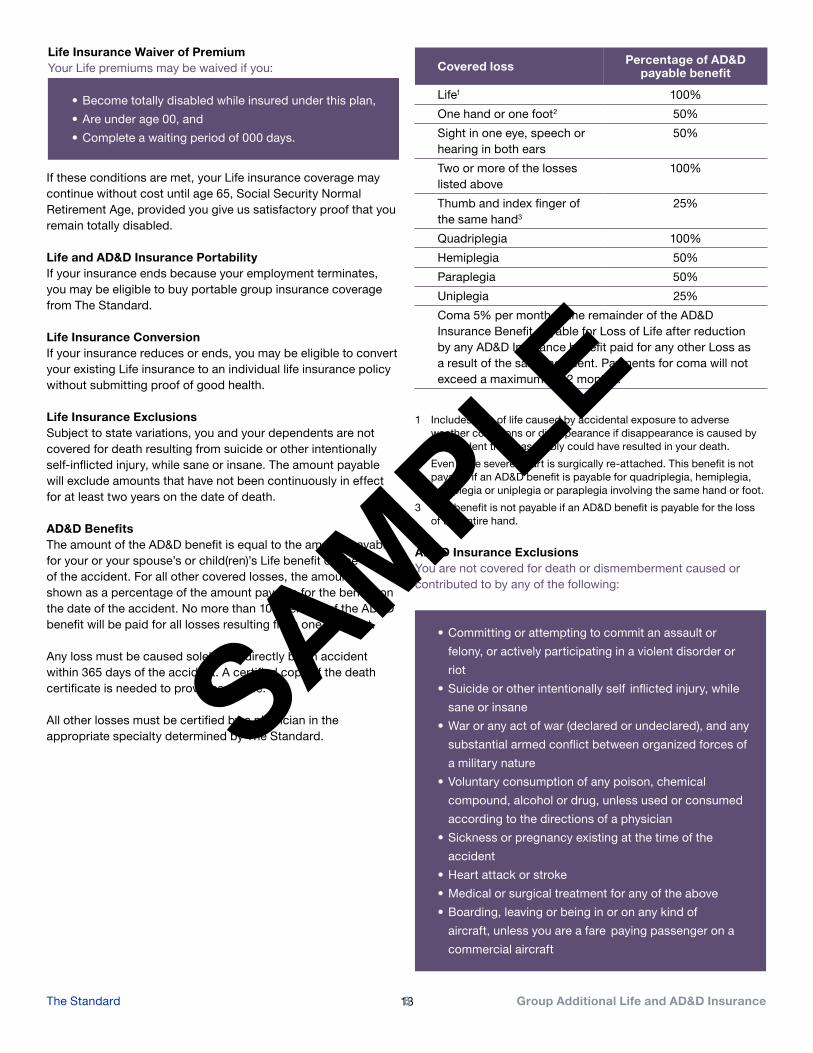

Life Insurance Waiver of Premium Your Life premiums may be waived if you:

• Become totally disabled while insured under this plan,

• Are under age 00, and

• Complete a waiting period of 000 days.

If these conditions are met, your Life insurance coverage may continue without cost until age 65, Social Security Normal Retirement Age, provided you give us satisfactory proof that you remain totally disabled.

Life and AD&D Insurance Portability If your insurance ends because your employment terminates, you may be eligible to buy portable group insurance coverage from The Standard.

Life Insurance Conversion If your insurance reduces or ends, you may be eligible to convert your existing Life insurance to an individual life insurance policy without submitting proof of good health.

Life Insurance Exclusions Subject to state variations, you and your dependents are not covered for death resulting from suicide or other intentionally self-inflicted injury, while sane or insane. The amount payable will exclude amounts that have not been continuously in effect for at least two years on the date of death.

AD&D Benefits The amount of the AD&D benefit is equal to the amount payable for your or your spouse’s or child(ren)’s Life benefit on the date of the accident. For all other covered losses, the amount is shown as a percentage of the amount payable for the benefit on the date of the accident. No more than 100 percent of the AD&D benefit will be paid for all losses resulting from one accident.

Any loss must be caused solely and directly by an accident within 365 days of the accident. A certified copy of the death certificate is needed to prove loss of life.

All other losses must be certified by a physician in the appropriate specialty determined by The Standard.

Covered loss Percentage of AD&D payable benefit

Life1 100%

One hand or one foot2 50%

Sight in one eye, speech or 50% hearing in both ears

Two or more of the losses 100% listed above

Thumb and index finger of 25% the same hand3

Quadriplegia 100%

Hemiplegia 50%

Paraplegia 50%

Uniplegia 25%

Coma 5% per month of the remainder of the AD&D Insurance Benefit payable for Loss of Life after reduction by any AD&D Insurance benefit paid for any other Loss as a result of the same accident. Payments for coma will not exceed a maximum of 12 months.

1 Includes loss of life caused by accidental exposure to adverse weather conditions or disappearance if disappearance is caused by an accident that reasonably could have resulted in your death.

2 Even if the severed part is surgically re-attached. This benefit is not payable if an AD&D benefit is payable for quadriplegia, hemiplegia, paraplegia or uniplegia or paraplegia involving the same hand or foot.

3 This benefit is not payable if an AD&D benefit is payable for the loss of the entire hand.

AD&D Insurance Exclusions You are not covered for death or dismemberment caused or contributed to by any of the following:

• Committing or attempting to commit an assault or

felony, or actively participating in a violent disorder or

riot

• Suicide or other intentionally self inflicted injury, while

sane or insane

• War or any act of war (declared or undeclared), and any

substantial armed conflict between organized forces of

a military nature

• Voluntary consumption of any poison, chemical

compound, alcohol or drug, unless used or consumed

according to the directions of a physician

• Sickness or pregnancy existing at the time of the

accident

• Heart attack or stroke

• Medical or surgical treatment for any of the above

• Boarding, leaving or being in or on any kind of

aircraft, unless you are a fare paying passenger on a

commercial aircraft

The Standard 136 Group Additional Life and AD&D Insurance

2

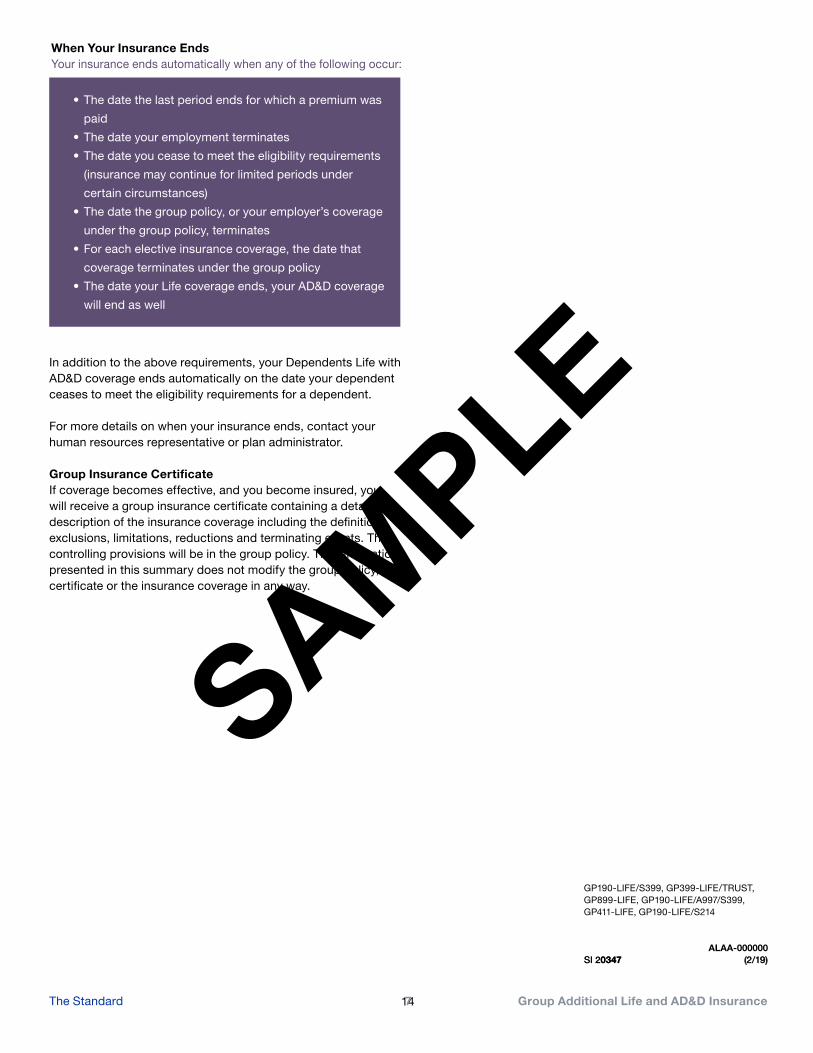

When Your Insurance Ends Your insurance ends automatically when any of the following occur:

• The date the last period ends for which a premium was

paid

• The date your employment terminates

• The date you cease to meet the eligibility requirements

(insurance may continue for limited periods under

certain circumstances)

• The date the group policy, or your employer’s coverage

under the group policy, terminates

• For each elective insurance coverage, the date that

coverage terminates under the group policy

• The date your Life coverage ends, your AD&D coverage

will end as well

In addition to the above requirements, your Dependents Life with AD&D coverage ends automatically on the date your dependent ceases to meet the eligibility requirements for a dependent.

For more details on when your insurance ends, contact your human resources representative or plan administrator.

Group Insurance Certificate If coverage becomes effective, and you become insured, you will receive a group insurance certificate containing a detailed description of the insurance coverage including the definitions, exclusions, limitations, reductions and terminating events. The controlling provisions will be in the group policy. The information presented in this summary does not modify the group policy, certificate or the insurance coverage in any way.

Standard Insurance Company 1100 SW Sixth Avenue Portland OR 97204

GP190-LIFE/S399, GP399-LIFE/TRUST, GP899-LIFE, GP190-LIFE/A997/S399, GP411-LIFE, GP190-LIFE/S214

000000 ALAAALAA-000000

SISI 203470347 (2/19)(2/19)

The Standard 147 Group Additional Life and AD&D Insurance

We Believe

YOU MATTER You’re the reason we’re here. Your fnancial well-being and peace of mind matter because you matter. Not because they serve our bottom line. We believe you deserve to live and work feeling confdent in tomorrow. We challenge ourselves to go above and beyond to serve you every day. Not as a number or a policy — but as a person.

15

’

’

A L©

Standard Insurance Company ABC Company, Inc. Group Policy #000000

GROUP SHORT TERM DISABILITY INSURANCE

expenses:

Protect your income if you’re out on leave.

Short Term Disability insurance can help pay benefits if you become disabled and can t work for a short amount of time.

This coverage replaces a portion of your income when you can t work because of a qualifying disability, including injury, physical disease, pregnancy or mental disorder

You may receive weekly benefits that replace a specified percentage of your eligible earnings. Benefits begin

Disability

after the short benefit waiting period explained below.

You may also receive help returning to work if you need accommodations.

Your health insurance helps pay medical bills. Short Term Disability insurance pays you. It can replace part of your paycheck if you can’t work due to a qualifying disability.

insurance helps protect your income if you’re unable to work.

Even if you’re healthy now, it’s important to protect yourself and the people who count on your income. If you can’t work, Short Term Disability insurance may help you pay for ongoing

Car Housing Groceries Child Care Insurance Costs

The Standard 161 Group Short Term Disability Insurance

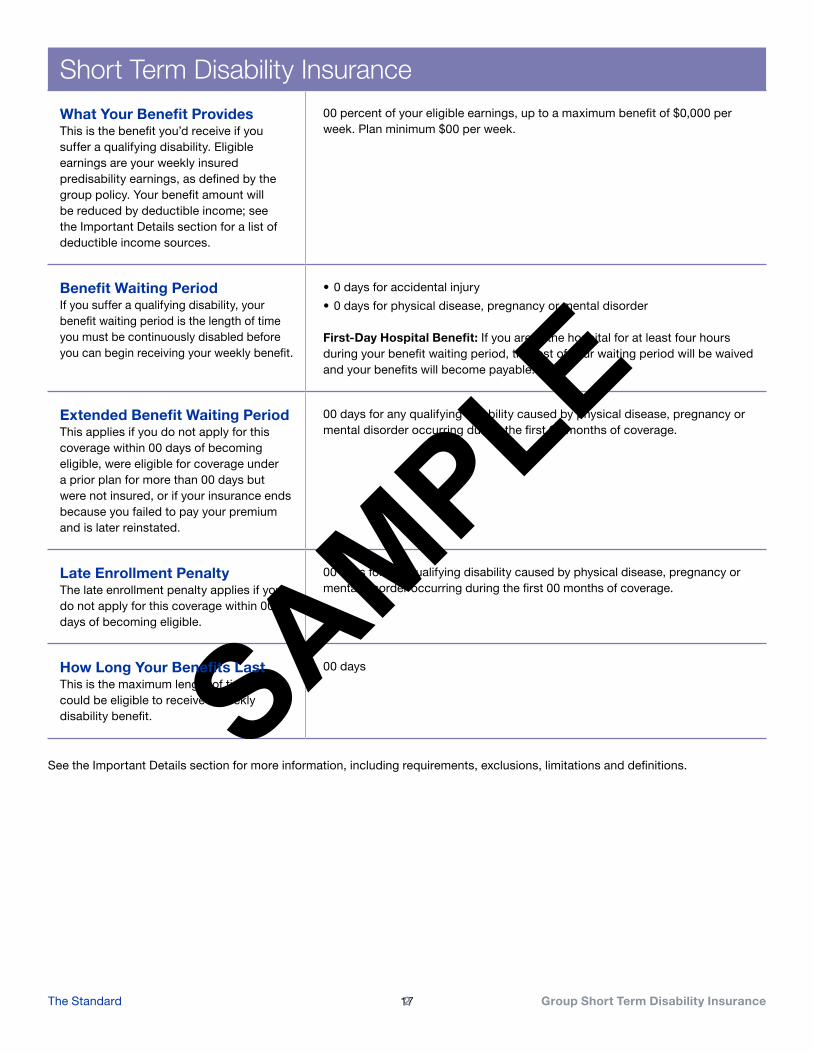

Short Term Disability Insurance

What Your Benefit Provides 00 percent of your eligible earnings, up to a maximum benefit of $0,000 per

This is the benefit you’d receive if you week. Plan minimum $00 per week.

suffer a qualifying disability. Eligible earnings are your weekly insured predisability earnings, as defined by the group policy. Your benefit amount will be reduced by deductible income; see the Important Details section for a list of deductible income sources.

Benefit Waiting Period • 0 days for accidental injury

If you suffer a qualifying disability, your • 0 days for physical disease, pregnancy or mental disorder benefit waiting period is the length of time you must be continuously disabled before First-Day Hospital Benefit: If you are in the hospital for at least four hours you can begin receiving your weekly benefit. during your benefit waiting period, the rest of your waiting period will be waived

and your benefits will become payable.

Extended Benefit Waiting Period This applies if you do not apply for this coverage within 00 days of becoming eligible, were eligible for coverage under a prior plan for more than 00 days but were not insured, or if your insurance ends because you failed to pay your premium and is later reinstated.

00 days for any qualifying disability caused by physical disease, pregnancy or mental disorder occurring during the first 00 months of coverage.

Late Enrollment Penalty 00 days for any qualifying disability caused by physical disease, pregnancy or

The late enrollment penalty applies if you do not apply for this coverage within 00 days of becoming eligible.

mental disorder occurring during the first 00 months of coverage.

How Long Your Benefits Last This is the maximum length of time you could be eligible to receive a weekly disability benefit.

00 days

See the Important Details section for more information, including requirements, exclusions, limitations and definitions.

The Standard 172 Group Short Term Disability Insurance

®

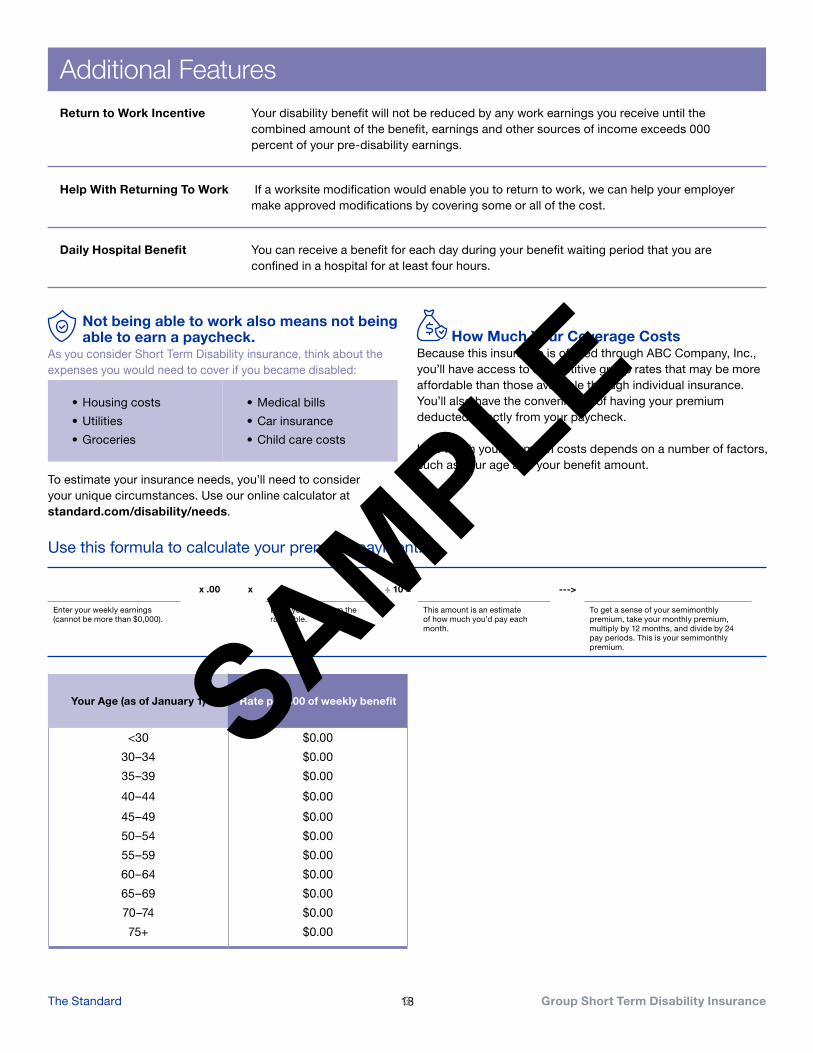

Additional Features Return to Work Incentive Your disability benefit will not be reduced by any work earnings you receive until the

combined amount of the benefit, earnings and other sources of income exceeds 000 percent of your pre-disability earnings.

Help With Returning To Work If a worksite modification would enable you to return to work, we can help your employer make approved modifications by covering some or all of the cost.

Daily Hospital Benefit You can receive a benefit for each day during your benefit waiting period that you are confined in a hospital for at least four hours.

Not being able to work also means not being able to earn a paycheck.

As you consider Short Term Disability insurance, think about the expenses you would need to cover if you became disabled:

• Housing costs

• Utilities

• Groceries

• Medical bills

• Car insurance

• Child care costs

To estimate your insurance needs, you’ll need to consider your unique circumstances. Use our online calculator at standard.com/disability/needs.

How Much Your Coverage Costs Because this insurance is offered through ABC Company, Inc., you’ll have access to competitive group rates that may be more affordable than those available through individual insurance. You’ll also have the convenience of having your premium deducted directly from your paycheck.

How much your premium costs depends on a number of factors, such as your age and your benefit amount.

x .00 x ÷ 10 = --->

Enter your weekly earnings (cannot be more than $0,000).

Enter your rate from the rate table.

This amount is an estimate of how much you’d pay each month.

To get a sense of your semimonthly premium, take your monthly premium, multiply by 12 months, and divide by 24 pay periods. This is your semimonthly premium.

Your Age (as of January 1) Rate per $00 of weekly benefit

<30 $0.00

30–34 $0.00

Use this formula to calculate your premium payment:

35–39

40–44

45–49

50–54

55–59

60–64

65–69

70–74

75+

$0.00

$0.00

$0.00

$0.00

$0.00

$0.00

$0.00

$0.00

$0.00

The Standard 183 Group Short Term Disability Insurance

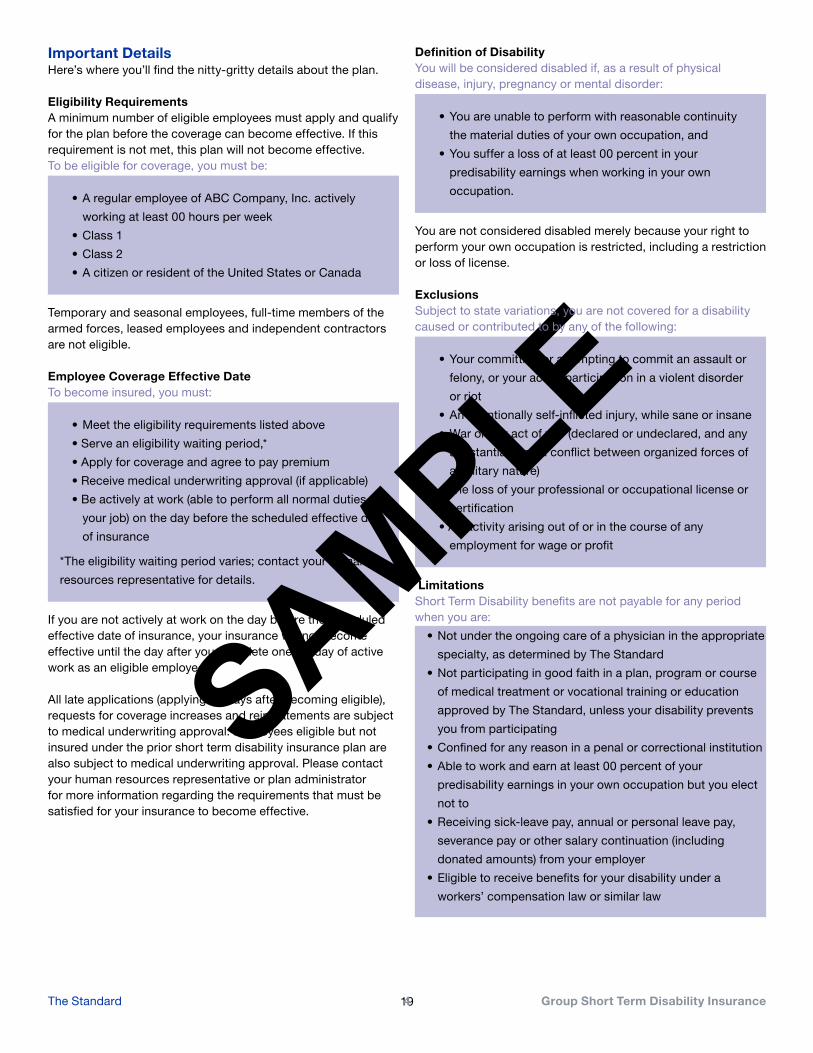

Important Details Here’s where you’ll find the nitty-gritty details about the plan.

Eligibility Requirements A minimum number of eligible employees must apply and qualify for the plan before the coverage can become effective. If this requirement is not met, this plan will not become effective. To be eligible for coverage, you must be:

• A regular employee of ABC Company, Inc. actively

working at least 00 hours per week

• Class 1

• Class 2

• A citizen or resident of the United States or Canada

Temporary and seasonal employees, full-time members of the armed forces, leased employees and independent contractors are not eligible.

Employee Coverage Effective Date To become insured, you must:

• Meet the eligibility requirements listed above

• Serve an eligibility waiting period,*

• Apply for coverage and agree to pay premium

• Receive medical underwriting approval (if applicable)

• Be actively at work (able to perform all normal duties of

your job) on the day before the scheduled effective date

of insurance

*The eligibility waiting period varies; contact your human

resources representative for details.

If you are not actively at work on the day before the scheduled effective date of insurance, your insurance will not become effective until the day after you complete one full day of active work as an eligible employee.

All late applications (applying 00 days after becoming eligible), requests for coverage increases and reinstatements are subject to medical underwriting approval. Employees eligible but not insured under the prior short term disability insurance plan are also subject to medical underwriting approval. Please contact your human resources representative or plan administrator for more information regarding the requirements that must be satisfied for your insurance to become effective.

Definition of Disability You will be considered disabled if, as a result of physical disease, injury, pregnancy or mental disorder:

• You are unable to perform with reasonable continuity

the material duties of your own occupation, and

• You suffer a loss of at least 00 percent in your

predisability earnings when working in your own

occupation.

You are not considered disabled merely because your right to perform your own occupation is restricted, including a restriction or loss of license.

Exclusions Subject to state variations, you are not covered for a disability caused or contributed to by any of the following:

• Your committing or attempting to commit an assault or

felony, or your active participation in a violent disorder

or riot

• An intentionally self-inflicted injury, while sane or insane

• War or any act of war (declared or undeclared, and any

substantial armed conflict between organized forces of

a military nature)

• The loss of your professional or occupational license or

certification

• An activity arising out of or in the course of any

employment for wage or profit

Limitations Short Term Disability benefits are not payable for any period when you are:

• Not under the ongoing care of a physician in the appropriate

specialty, as determined by The Standard

• Not participating in good faith in a plan, program or course

of medical treatment or vocational training or education

approved by The Standard, unless your disability prevents

you from participating

• Confined for any reason in a penal or correctional institution

• Able to work and earn at least 00 percent of your

predisability earnings in your own occupation but you elect

not to

• Receiving sick-leave pay, annual or personal leave pay,

severance pay or other salary continuation (including

donated amounts) from your employer

• Eligible to receive benefits for your disability under a

workers’ compensation law or similar law

The Standard 194 Group Short Term Disability Insurance

When Your Benefits End Your Short Term Disability benefits end automatically on the date any of the following occur:

• You are no longer disabled

• Your maximum benefit period ends

• Long term disability benefits become payable to you

under a long term disability plan

• Benefits become payable under any other disability

insurance plan which you become insured through

employment during a period of temporary recovery

• You fail to provide proof of continued disability and

entitlement to benefits

When Your Insurance Ends Your insurance ends automatically when any of the following occur:

• The date the last period ends for which a premium was

paid

• The date your employment terminates

• The date the group policy (or your employer’s coverage

under the group policy) terminates

• The date you cease to meet the eligibility requirements

(insurance may continue for limited periods under

certain circumstances)

• The date ABC Company, Inc. ends participation in the

• You pass away

Deductible Income Your benefits will be reduced if you have deductible income, which is income you receive or are eligible to receive while receiving Short Term Disability benefits. Deductible income includes:

• Sick pay, annual or personal leave pay, severance pay

or other forms of salary continuation (including donated

amounts) paid that exceeds 00 percent of your indexed

predisability earnings when added to your Short Term

Disability benefit

• Amounts under any workers’ compensation law or

similar law

• Amounts under unemployment compensation law

• Amounts because of your disability from any other

group insurance

• Any disability or retirement benefits received or you are

eligible to receive from your employer’s retirement plan

• Amounts under any state disability income benefit law

or similar law

• Earnings from work activity while you are disabled, plus

the earnings you could receive if you work as much as

your disability allows

• Earnings or compensation included in your predisability

earnings which you receive or are eligible to receive

while Short Term Disability benefits are payable

group policy

Group Insurance Certificate If coverage becomes effective, and you become insured, you will receive a group insurance certificate containing a detailed description of the insurance coverage, including the definitions, exclusions, limitations, reductions and terminating events. The controlling provisions will be in the group policy. The information presented in this summary does not modify the group policy, certificate or the insurance coverage in any way.

• Amounts due from or on behalf of a third party because

of your disability, whether by judgment, settlement or

other method

• Any amount you receive by compromise, settlement or

other method as a result of a claim for any of the above

GP399-STD, GP899-STD, GP309-STD, GP209-STD, GP399/ASSOC, GP399-STD/TRUST

000000 SI 20359 (2/19)

The Standard 520 Group Short Term Disability Insurance

We Believe in

A BETTER TOMORROW Our beliefs don’t stop at our walls. We believe in helping our communities grow stronger — so the world can be brighter for all of us.

21

’

~ L®

Standard Insurance Company ABC Company, Inc. Group Policy #000000

GROUP LONG TERM DISABILITY INSURANCE

isability.

Long Term Disability insurance helps protect your income if you can’t work and don’t get your regular paycheck.

Long Term Disability insurance can help pay the bills if you become disabled and can t work for an extended period. That could be a few months or several years. This coverage helps replace part of your paycheck. That can help you protect your lifestyle and savings.

You can get help returning to work when you’re ready. This Long Term Disability coverage includes incentives and assistance to help you get back to work. The Standard may also help pay the costs of modifying your workplace to accommodate your needs.

Long Term Disability insurance can help protect your income if you can’t work due to a qualifying disability. It can also help you get back to work when you’re ready. Whether you’re out for a few months or years, this benefit can help you protect your income — and those who depend on it.

One in four 20-year-olds will become disabled before reaching age 67. And one in 10 Americans

Protect your income while coping with a long-lasting d

live with severe disability.* Long-term disabilities can be caused by accidents but also by illnesses such as cancer and heart disease. How many paychecks could you miss? Long Term Disability insurance can help you maintain your lifestyle and pay for things like:

Housing Groceries Car Insurance College Tuition Costs

*Source: Basic Facts, U.S. Social Security Administration, June 2018

The Standard 221 Group Long Term Disability Insurance

Features ltiona

Long Term Disability Insurance

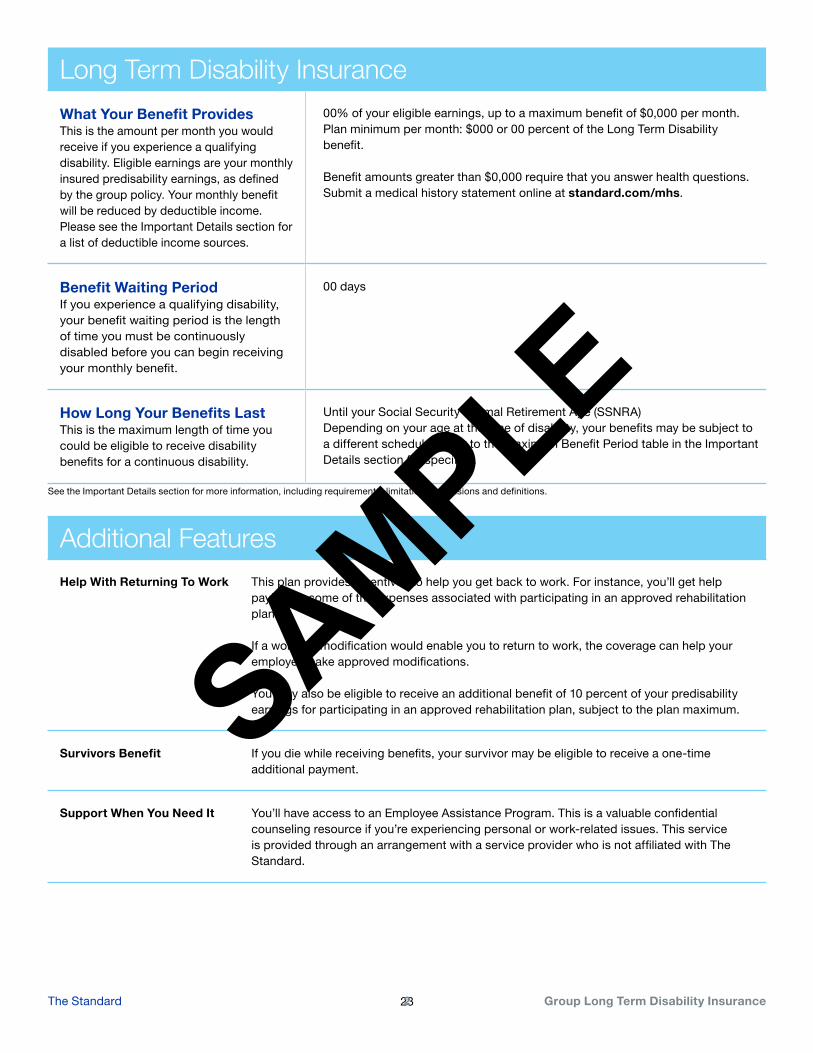

What Your Benefit Provides This is the amount per month you would receive if you experience a qualifying disability. Eligible earnings are your monthly insured predisability earnings, as defined by the group policy. Your monthly benefit will be reduced by deductible income. Please see the Important Details section for a list of deductible income sources.

00% of your eligible earnings, up to a maximum benefit of $0,000 per month. Plan minimum per month: $000 or 00 percent of the Long Term Disability benefit.

Benefit amounts greater than $0,000 require that you answer health questions. Submit a medical history statement online at standard.com/mhs.

Benefit Waiting Period If you experience a qualifying disability, your benefit waiting period is the length of time you must be continuously disabled before you can begin receiving your monthly benefit.

00 days

How Long Your Benefits Last Until your Social Security Normal Retirement Age (SSNRA)

This is the maximum length of time you Depending on your age at the time of disability, your benefits may be subject to

could be eligible to receive disability a different schedule. Refer to the Maximum Benefit Period table in the Important

benefits for a continuous disability. Details section for specifics.

See the Important Details section for more information, including requirements, limitations, exclusions and definitions.

AddiHelp With Returning To Work This plan provides incentives to help you get back to work. For instance, you’ll get help

paying for some of the expenses associated with participating in an approved rehabilitation plan.

If a worksite modification would enable you to return to work, the coverage can help your employer make approved modifications.

You may also be eligible to receive an additional benefit of 10 percent of your predisability earnings for participating in an approved rehabilitation plan, subject to the plan maximum.

Survivors Benefit If you die while receiving benefits, your survivor may be eligible to receive a one-time additional payment.

Support When You Need It You’ll have access to an Employee Assistance Program. This is a valuable confidential counseling resource if you’re experiencing personal or work-related issues. This service is provided through an arrangement with a service provider who is not affiliated with The Standard.

The Standard 232 Group Long Term Disability Insurance

Additional Features Continued

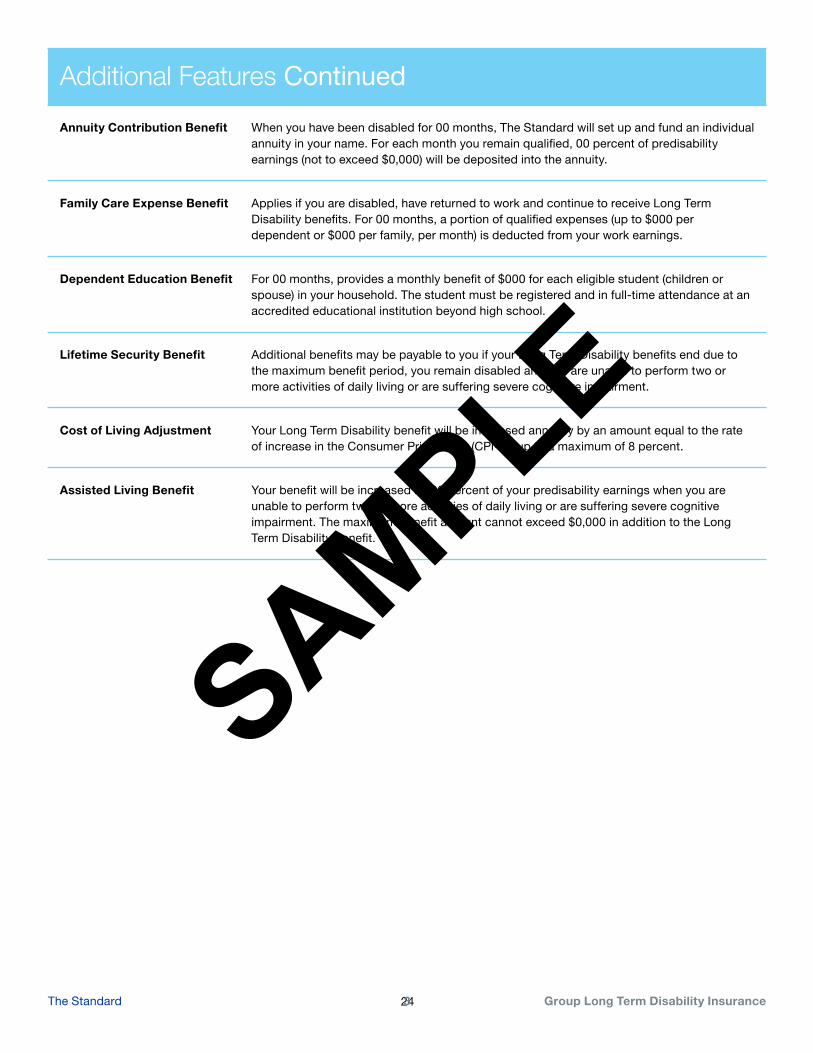

Annuity Contribution Benefit When you have been disabled for 00 months, The Standard will set up and fund an individual annuity in your name. For each month you remain qualified, 00 percent of predisability earnings (not to exceed $0,000) will be deposited into the annuity.

Family Care Expense Benefit Applies if you are disabled, have returned to work and continue to receive Long Term Disability benefits. For 00 months, a portion of qualified expenses (up to $000 per dependent or $000 per family, per month) is deducted from your work earnings.

Dependent Education Benefit For 00 months, provides a monthly benefit of $000 for each eligible student (children or spouse) in your household. The student must be registered and in full-time attendance at an accredited educational institution beyond high school.

Lifetime Security Benefit Additional benefits may be payable to you if your Long Term Disability benefits end due to the maximum benefit period, you remain disabled and you are unable to perform two or more activities of daily living or are suffering severe cognitive impairment.

Cost of Living Adjustment Your Long Term Disability benefit will be increased annually by an amount equal to the rate of increase in the Consumer Price Index (CPI-W) up to a maximum of 8 percent.

Assisted Living Benefit Your benefit will be increased by 00 percent of your predisability earnings when you are unable to perform two or more activities of daily living or are suffering severe cognitive impairment. The maximum benefit amount cannot exceed $0,000 in addition to the Long Term Disability benefit.

The Standard 243 Group Long Term Disability Insurance

As you consider Long Term Disability insurance, evaluate what makes sense for you.

Getting by without a paycheck isn’t easy, especially for an extended period of time. Make sure you have enough financial protection to help you cover your housing costs, utilities and other bills.

To estimate your insurance needs, you’ll need to consider your unique circumstances. Use our online calculator at standard.com/disability/needs.

How Much Your Coverage Costs Because this insurance is offered through Company Name, you’ll have access to competitive group rates that may be more affordable than those available through individual insurance. You’ll also have the convenience of having your premium deducted directly from your paycheck.

How much your premium costs depends on a number of factors, such as your age and benefit amount.

Use this formula to calculate your premium payment:

x ÷ 100 = --->

Enter your monthly earnings (cannot be more than $0,000).

Enter your rate from the rate table.

This amount is an estimate of how much you’d pay each month

To get a sense of your semimonthly premium, take your monthly premium, multiply by 12 months, and divide by 24 pay periods. This is your semimonthly premium

Your Age (as of January 1)

<30

30–34

35–39

40–44

45–49

50–54

55–59

60–64

65–69

70–74

75+

Rate %

0.00

0.00

0.00

0.00

0.00

0.00

0.00

0.00

0.00

0.00

0.00

The Standard 254 Group Long Term Disability Insurance

Important Details Definition of Disability

Temporary and seasonal employees, full-time members of the armed forces, leased employees and independent contractors are not eligible.

Employee Coverage Effective Date To become insured you must:

• Meet the eligibility requirements listed above

• Serve an eligibility waiting period,*

• Apply for coverage and agree to pay premiums

• Receive medical underwriting approval (if applicable)

• Be actively at work (able to perform all normal duties of

your job) on the day before the scheduled effective date

of insurance

*The eligibility waiting period varies; contact your human

resources representative for details.

If you are not actively at work on the day before the scheduled effective date of insurance, your insurance will not become effective until the day after you complete one full day of active work as an eligible employee.

All late applications (applying 00 days after becoming eligible), requests for coverage increases (including requests to insure predisability earnings that are greater than the last amount for which evidence of insurability was required), amounts over the guarantee issue amount and reinstatements are subject

or loss of license.

Maximum Benefit Period If you become disabled before age 62, Long Term Disability benefits may continue during disability until age 65 or to the Social Security Normal Retirement Age (SSNRA) or 3 years, 6 months, whichever is longer. If you become disabled at age 62 or older, the benefit duration is determined by the age when disability begins:

Age Maximum Benefit Period

62 3 years, 6 months

63 3 years

64 2 years, 6 months

65 2 years

66 1 year, 9 months

67 1 year, 6 months

68 1 year, 3 months

69 1 year

Here’s where you’ll find the nitty-gritty details about the plan.

Eligibility Requirements A minimum number of eligible employees must apply and qualify for the proposed plan before coverage can become effective. If this requirement is not met, this plan will not become effective. To be eligible for coverage, you must be:

• A regular employee of ABC Company, Inc. actively

working at least 00 hours per week

• Class 1

• Class 2

• A citizen or resident of the United States or Canada

to medical underwriting approval. Employees eligible but not insured under the prior long term disability insurance plan are also subject to medical underwriting approval. Please contact your human resources representative or plan administrator for more information regarding the requirements that must be satisfied for your insurance to become effective.

For the benefit waiting period and to the end of the maximum benefit period that Long Term Disability benefits are payable, you will be considered disabled if, as a result of physical disease, injury, pregnancy or mental disorder:

• You are unable to perform with reasonable continuity

the material duties of your own occupation, and or

• You suffer a loss of at least 00 percent of your

predisability earnings when working in your own

occupation.

You are not considered disabled merely because your right to perform your own occupation is restricted, including a restriction

The Standard 265 Group Long Term Disability Insurance

-

-

treatment of a preexisting condition unless on the date

you become disabled, you have been continuously

insured under the group policy for the exclusion period

and you have been actively at work for at least one full

day after the end of the exclusion period

A preexisting condition is a mental or physical condition whether or not diagnosed or misdiagnosed during the 00-day period just

• For which you or a reasonably prudent person would

have consulted a physician or other licensed medical

professional; received medical treatment, services or

advice; undergone diagnostic procedures, including

self administered procedures; or taken prescribed

• Which, as a result of any medical examination, including

routine examination, was discovered or suspected

Treatment-Free Period: If you are treatment free for 00 consecutive months during the exclusion period, any remaining

predisability earnings, but you elect not to work.

In addition, the length of time you can receive Long Term Disability payments will be limited if:

• You reside outside of the United States or Canada

• Your disability is caused or contributed to by mental

disorders or substance abuse.

• Your disability is caused or contributed to by mental

disorders, substance abuse or the environment,

chronic fatigue conditions, chronic pain conditions,

carpal tunnel or repetitive motion syndrome,

temporomandibular joint disorder or craniomandibular

joint disorder.

When Your Benefits End Your Long Term Disability benefits end automatically on the date any of the following occur:

• You are no longer disabled

• You maximum benefit period ends

• Benefits become payable under any other disability

insurance plan under which you become insured through

employment during a period of temporary recovery

• You fail to provide proof of continued disability and

entitlement to benefits

Exclusions Subject to state variations, you are not covered for a disability caused or contributed to by any of the following:

• Your committing or attempting to commit an assault or

felony, or your active participation in a violent disorder

or riot

• An intentionally self inflicted injury, while sane or insane

• War or any act of war (declared or undeclared, and any

substantial armed conflict between organized forces of

a military nature)

• The loss of your professional or occupational license

or certification

• A preexisting condition or the medical or surgical

Preexisting Condition Provision

before your insurance becomes effective:

drugs or medications

exclusion period will not apply Exclusion Period: 00 months

Limitations Long Term Disability benefits are not payable for any period when you are:

• Not under the ongoing care of a physician in the

appropriate specialty, as determined by The Standard

• Not participating in good faith in a plan, program or

course of medical treatment or vocational training or

education approved by The Standard, unless your

disability prevents you from participating

• Confined for any reason in a penal or correctional

institution

• Able to work during the 00 month own occupation

period and earn at least 00 percent of your indexed

• You pass away

The Standard 276 Group Long Term Disability Insurance

Deductible Income When Your Insurance Ends Your benefits will be reduced if you have deductible income, which Your insurance ends automatically when any of the following occur: is income you receive or are eligible to receive while receiving Long Term Disability benefits. Deductible income includes:

• Sick pay, annual or personal leave pay, severance

pay or other forms of salary continuation (including

donated amounts) paid that exceeds 100 percent of

your indexed predisability earnings when added to your

Long Term Disability benefit

• Benefits under any workers’ compensation law or

similar law

• Amounts under unemployment compensation law

• Social Security disability or retirement benefits,

group insurance

similar law

your disability allows

other method

including benefits for your spouse and children

• Amounts because of your disability from any other

• Any retirement or disability benefits you received

from your employer’s retirement plan which are not

attributable to your contributions

• Benefits under any state disability income benefit law or

• Earnings from work activity while you are disabled, plus

the earnings you could receive if you work as much as

• Earnings or compensation included in your predisability

earnings which you receive or are eligible to receive

while Long Term Disability benefits are payable

• Amounts due from or on behalf of a third party because

of your disability, whether by judgment, settlement or

• Any amount you receive by compromise, settlement or

other method as a result of a claim for any of the above

Conversion You may have the option to obtain Long Term Disability conversion insurance after the termination of your insurance with Company Name, if you meet the requirements defined by the group policy.

Group Insurance Certificate If coverage becomes effective, and you become insured, you will receive a group insurance certificate containing a detailed description of the insurance coverage, including the definitions, exclusions, limitations, reductions and terminating events. The controlling provisions will be in the group policy. The information present in this summary does not modify the group policy, certificate or the insurance coverage in any way.

• The date the last period ends for which a premium

was paid

• The date your employment terminates

• The date the group policy terminates

• The date you cease to meet the eligibility requirements

(insurance may continue for limited periods under

certain circumstances)

• The date Company Name ends participation in the

group policy

GP399-LTD/TRUST, GP899-LTD, GP209-LTD, GP608-LTD, GP190-LTD/ASSOC/S399, GP190-LTD/TRUST/S399, GP491-LTD/TRUST/S399

000000 SI 20351 (2/19)

The Standard 728 Group Long Term Disability Insurance

We Believe in

DOING THE RIGHT THING We take pride in purpose, and we’ve built more than a century-long reputation on it. We know that our actions — how we administer claims and manage our business — affect people’s lives. We take that responsibility seriously.

29

Life Services Toolkit Resources and Tools to Help You and Your Benefciary Meet Life’s Challenges

Group Life insurance through your employer gives you assurance that your family will receive some fnancial assistance in the event of a death. But coverage under a group Life policy from Standard Insurance Company (The Standard) does more than help protect your family from fnancial hardship after a loss. We have partnered with Morneau Shepell to offer a lineup of additional services that can make a difference now and in the future.

Online tools and services can help you create a will, make advance funeral plans and put your fnances in order. After a loss, benefciaries can consult experts by phone or in person, and obtain other helpful information online.

The Life Services Toolkit is automatically available to those insured under a group Life insurance policy from The Standard. Recipients of an Accelerated Beneft can access services for 12 months after the date of payment.

Services to Help You Now Visit the Life Services Toolkit website at standard.com/mytoolkit (enter username “assurance”) for information and tools to help you make important life decisions.

Estate Planning Assistance: Online tools walk you through the steps to prepare a will and create other documents, such as living wills, powers of attorney and health care agent forms.

Financial Planning: Consult online services to help you manage debt, calculate mortgage and loan payments, and take care of other fnancial matters with confdence.

Health and Wellness: Timely articles about nutrition, stress management and wellness help employees and their families lead healthy lives.

Identity Theft Prevention: Check the website for ways to thwart identity thieves and resolve issues if identity theft occurs.

Funeral Arrangements: Use the website to calculate funeral costs, fnd funeral-related services and make decisions about funeral arrangements in advance.

If you are a recipient of an Accelerated Beneft1, you may access the services for benefciaries outlined on the next page.

Standard Insurance Company 1100 SW Sixth Avenue Portland, OR 97204

standard.com 1 An Accelerated Beneft allows a covered individual who becomes terminally ill to receive a portion of the Life insurance proceeds while living, if all other eligibility requirements are met.

Life Services Toolkit EE 30 SI 20587 (3/19)

Services for Your Benefciary Life insurance benefciaries2 can access services for 12 months after the date of death. Recipients of an Accelerated Beneft can access services for 12 months after the date of payment.

These supportive services can help your benefciary cope after a loss:

• Grief Support: Clinicians with master’s degrees are on call to provide confdential grief sessions by phone or in person. Benefciaries are eligible for up to six face-to-face sessions and unlimited phone contact.

Benefciaries can participate in phone consultations or in-person meetings with trained grief counselors.

• Legal Services: Benefciaries can obtain legal assistance from experienced attorneys. They can:

- Schedule an initial 30-minute offce and a telephone consultation with a network attorney. Benefciaries who wish to retain a participating attorney after the initial consultation receive a 25 percent rate reduction from the attorney’s normal hourly or fxed fee rates.

- Obtain an estate-planning package that consists of a simple will, a living will, a health care agent form and a durable power of attorney.

• Financial Assistance: Benefciaries have unlimited phone access to fnancial counselors who can help with issues such as budgeting strategies, and credit and debt management, including hour-long sessions on topics requiring more in-depth discussion.

• Support Services: During an emotional time, benefciaries can receive help planning a funeral or memorial service. Work-life advisors can guide them to resources to help manage household repairs and chores; fnd child care and elder care providers; or organize a move or relocation.

• Online Resources: Benefciaries can easily access additional services and features on the Life Services Toolkit website for benefciaries, including online resources to calculate funeral costs, fnd funeral-related services and make decisions about funeral arrangements.

For benefciary services, visit standard.com/mytoolkit (User name = support) or call the phone assistance line at 800.378.5742.

2 The Life Services Toolkit is not available to Life insurance benefciaries who are minors or to non-individual entities such as trusts, estates or charities.

The Standard is a marketing name for StanCorp Financial Group, Inc. and subsidiaries. Insurance products are offered by Standard Insurance Company of Portland, Oregon in all states except New York. Product features and availability vary by state and are solely the responsibility of Standard Insurance Company.

The Life Services Toolkit is provided through an arrangement with Morneau Shepell and is not affliated with The Standard. Morneau Shepell is solely responsible for providing and administering the included service. This service is not an insurance product.

31

~ 121 ~ ~

~ ~ LI f§) JG

r------- Q,,_ : --------~ 7

A Helping Hand When You Need It Rely on the support, guidance and resources of your Employee Assistance Program.

There are times in life when you might need a little help coping or fguring out what to do. Take advantage of the Employee Assistance Program1

(EAP) which includes WorkLife Services and is available to you and your family in connection with your group insurance from Standard Insurance

Online Resources Visit workhealthlife.com/Standard6 to explore a wealth of information online, including videos, guides, articles, webinars, resources, self-assessments and calculators.

Company (The Standard). It’s confdential — information will be released only with your permission or as required by law.

Connection to Resources, Support and Guidance You, your dependents (including children to age 26)2 and all household members can contact master’s-degreed clinicians 24/7 by phone, online, live chat, email and text. There’s even a mobile EAP app. Receive referrals to support groups, a network counselor, community resources or your health plan. If necessary, you’ll be connected to emergency services.

Your program includes up to six face-to-face assessment and counseling sessions per issue. EAP services can help with:

Depression, grief, loss and emotional well-being

Family, marital and other relationship issues

Life improvement and goal-setting

Addictions such as alcohol and drug abuse

Stress or anxiety with work or family

Financial and legal concerns

Identity theft and fraud resolution

Online will preparation

WorkLife Services WorkLife Services are provided in connection with the Employee Assistance Program. They can save you hours of research time by providing referrals for important needs like education, adoption, travel, daily living and care for your pet, child or elderly loved one.

1 The EAP service is provided through an arrangement with Morneau Shepell, which is not affliated with The Standard. Morneau Shepell is solely responsible for providing and administering the included service. EAP is not an insurance product and is provided to groups of 10–2,499 lives. This service is only available while insured under The Standard’s group policy.

2 Individual EAP counseling sessions are available to eligible participants 16 years and older; family sessions are available for eligible members 12 years and older, and their parent or guardian. Children under the age of 12 will not receive individual counseling sessions.

The Standard is a marketing name for StanCorp Financial Group, Inc. and subsidiaries. Insurance products are offered by Standard Insurance Company of Portland, Oregon in all states except New York. Product features and availability vary by state and are solely the responsibility of Standard Insurance Company.

Contact EAP

877.851.1631 TDD: 800.327.1833 24 hours a day, seven days a week

workhealthlife.com/Standard6

NOTE: It’s a violation of your company’s 32contract to share this information with individuals

who are not eligible for this service.

With EAP, assistance is immediate, personal and available when you need it.

Standard Insurance Company 1100 SW Sixth Avenue Portland, OR 97204

standard.com

Employee Assistance Program-6 SI 20585 (3/19)

[!]

dib @

~ ~ ll1ll

m

r----------------~--------------------~ I I I I I I I

offers aid before and during your trip, including:

Passport, visa, weather and currency exchange information, health hazards advice and inoculation requirements

Emergency ticket, credit card and passport replacement, funds transfer and missing baggage

Help replacing prescription medication or lost corrective lenses and advancing funds for emergency medical payment

Emergency evacuation to the nearest adequate medical facility and medically necessary repatriation to the employee’s home, including repatriation of remains2

Connection to medical care providers, interpreter services, a local attorney, consular offce or bail bond services

Return travel companion if travel is disrupted due to emergency transportation services or return dependent children if left unattended due to prolonged hospitalization2

Logistical arrangements for ground transportation, housing and/or evacuation in the event of political unrest and social instability

The Standard is a marketing name for StanCorp Financial Group, Inc. and subsidiaries. Insurance products are offered by Standard Insurance Company of Portland, Oregon in all states except New York. Product features and availability vary by state and are solely the responsibility of Standard Insurance Company.

+1.240.330.1380 Everywhere else

standard.com/travel

1 Travel Assistance is provided by Generali Global Assistance. Generali Global Assistance (GGA) is the marketing name used by GMMI, Inc. for their services, which is not affliated with The Standard. Travel Assistance is subject to the terms and conditions, including exclusions and limitations of the Travel Assistance Program Description. GGA is solely responsible for providing and administering the included service. Travel Assistance is not an insurance product. This service is only available while insured under The Standard’s group policy.

2 Must be arranged by Generali Global Assistance. The Combined Single Limit (CSL) for these services is $1 million. One service or combination of the services may exceed the CSL. The insured is responsible for payment of any expenses that exceed the CSL.

Travel Assistance Explore the World with Confdence

Things can happen on the road. Passports get stolen or lost. Unforeseen events or circumstances derail travel plans. Medical problems surface at the most inconvenient times. Travel Assistance can help you navigate these issues and more at any time of the day or night. You and your spouse are covered with Travel Assistance1 — and so are kids through age 25 — with your group insurance from Standard Insurance Company (The Standard).

Security That Travels with You Travel Assistance is available when you travel more than 100 miles from home or internationally for up to 180 days for business or pleasure. It

Travel Assistance is available if you travel more than 100 miles from home or in a foreign country.

Travel Risk Intelligence Portal Contact standard.com/travel 866.455.9188: United States,

Canada, Puerto Rico, U.S. Virgin For frst time activation, use the Islands and Bermuda following information:

Group ID: D2STD +1.240.330.1380: Everywhere else Activation Code: 181002 [email protected]

In all cases, the medical professionals, medical facilities or legal counsel suggested by Generali Global Assistance (GGA) to provide services to Participants are not employees or agents of The Standard or GGA, and the fnal decision to utilize any such medical professional, medical facility, or legal counsel is the Participant’s choice alone. The Standard and GGA are not responsible and shall not be liable for any wrongful act or omission of any transportation provider, healthcare professional or legal 34 counsel who is not an employee of The Standard or GGA, as applicable. Generali Global Assistance is the marketing name for GMMI, Inc.

Contact Travel Assistance

866.455.9188 United States, Canada, Puerto Rico, U.S. Virgin Islands and Bermuda

Standard Insurance Company 1100 SW Sixth Avenue Portland, OR 97204

standard.com

Travel Assistance EE SI 20584 (3/19)

□

□

□

□

□ □ □

□

□

□

□ □

□ □ □

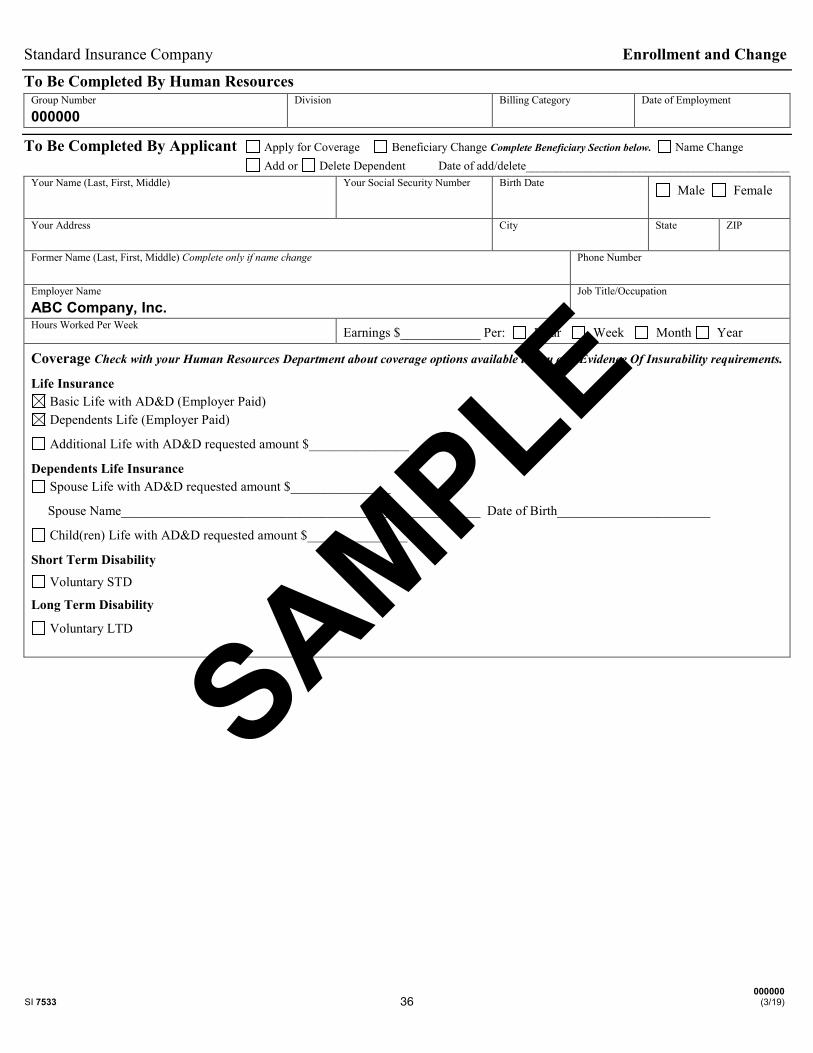

Standard Insurance Company Enrollment and Change

To Be Completed By Human Resources Group Number

000000 Division Billing Category Date of Employment

To Be Completed By Applicant Apply for Coverage Beneficiary Change Complete Beneficiary Section below. Name Change Add or Delete Dependent Date of add/delete____________________________________________

Your Name (Last, First, Middle) Your Social Security Number Birth Date Male Female

Your Address City State ZIP

Former Name (Last, First, Middle) Complete only if name change Phone Number

Employer Name

ABC Company, Inc. Job Title/Occupation

Hours Worked Per Week Earnings $____________ Per: Hour Week Month Year

Coverage Check with your Human Resources Department about coverage options available to you and Evidence Of Insurability requirements.

Life Insurance Basic Life with AD&D (Employer Paid) Dependents Life (Employer Paid)

Additional Life with AD&D requested amount $_______________

Dependents Life Insurance Spouse Life with AD&D requested amount $_______________

Spouse Name______________________________________________________ Date of Birth_______________________

Child(ren) Life with AD&D requested amount $_______________

Short Term Disability

Voluntary STD

Long Term Disability

Voluntary LTD

000000 SI 7533 36 (3/19)

I'\.

/A '/ ~ V/

~ ',.

/ "~ /

/t ) ~

~ " '- :::::... "-....' ...... >

~~v

~

~

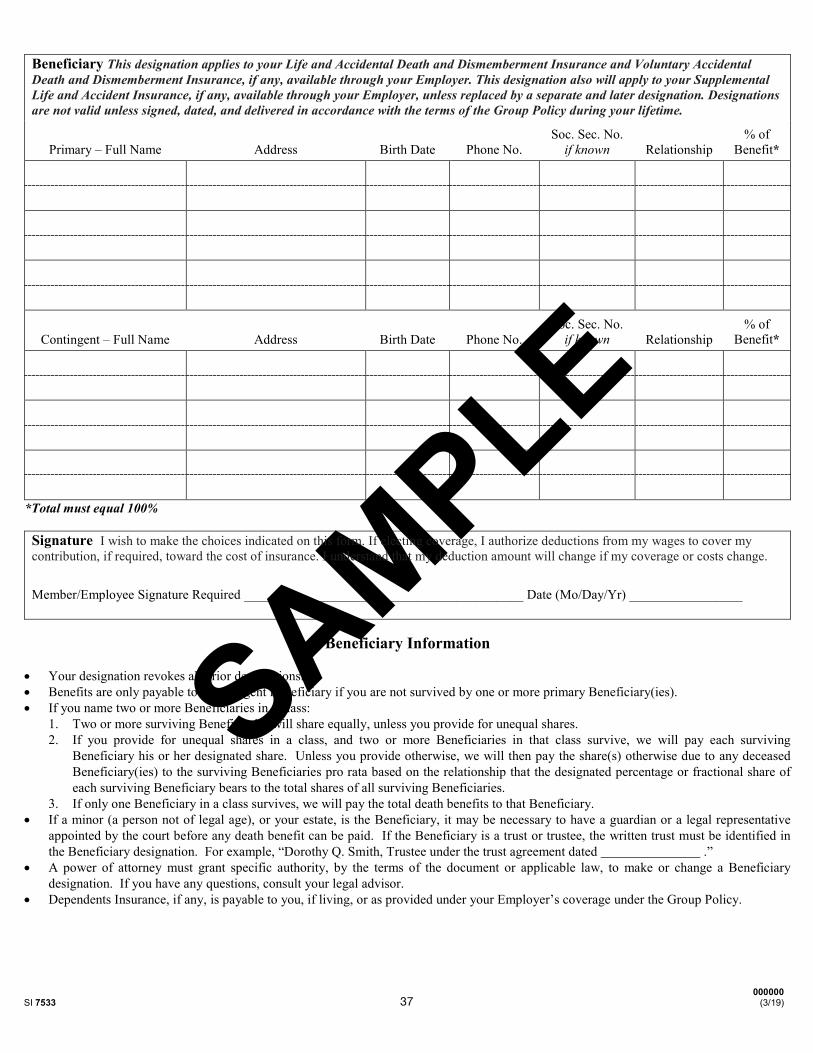

Beneficiary This designation applies to your Life and Accidental Death and Dismemberment Insurance and Voluntary Accidental Death and Dismemberment Insurance, if any, available through your Employer. This designation also will apply to your Supplemental Life and Accident Insurance, if any, available through your Employer, unless replaced by a separate and later designation. Designations are not valid unless signed, dated, and delivered in accordance with the terms of the Group Policy during your lifetime.

Soc. Sec. No. % of Primary – Full Name Address Birth Date Phone No. if known Relationship Benefit*

Soc. Sec. No. % of Contingent – Full Name Address Birth Date Phone No. if known Relationship Benefit*

*Total must equal 100%

Signature I wish to make the choices indicated on this form. If electing coverage, I authorize deductions from my wages to cover my contribution, if required, toward the cost of insurance. I understand that my deduction amount will change if my coverage or costs change.

Member/Employee Signature Required __________________________________________ Date (Mo/Day/Yr) _________________

Beneficiary Information

• Your designation revokes all prior designations. • Benefits are only payable to a contingent Beneficiary if you are not survived by one or more primary Beneficiary(ies). • If you name two or more Beneficiaries in a class:

1. Two or more surviving Beneficiaries will share equally, unless you provide for unequal shares. 2. If you provide for unequal shares in a class, and two or more Beneficiaries in that class survive, we will pay each surviving

Beneficiary his or her designated share. Unless you provide otherwise, we will then pay the share(s) otherwise due to any deceased Beneficiary(ies) to the surviving Beneficiaries pro rata based on the relationship that the designated percentage or fractional share of each surviving Beneficiary bears to the total shares of all surviving Beneficiaries.

3. If only one Beneficiary in a class survives, we will pay the total death benefits to that Beneficiary. • If a minor (a person not of legal age), or your estate, is the Beneficiary, it may be necessary to have a guardian or a legal representative

appointed by the court before any death benefit can be paid. If the Beneficiary is a trust or trustee, the written trust must be identified in the Beneficiary designation. For example, “Dorothy Q. Smith, Trustee under the trust agreement dated .”

• A power of attorney must grant specific authority, by the terms of the document or applicable law, to make or change a Beneficiary designation. If you have any questions, consult your legal advisor.

• Dependents Insurance, if any, is payable to you, if living, or as provided under your Employer’s coverage under the Group Policy.

000000 SI 7533 37 (3/19)

Standard Insurance Company

For more than 100 years, we have been dedicated to our core purpose: to help people achieve fnancial well-being and peace of mind. We have earned a national reputation for quality products and superior service by always striving to do what is right for our customers.

Headquartered in Portland, Oregon, The Standard is a nationally recognized provider of group Disability, Life, Dental and Vision insurance and Individual Disability insurance. We provide insurance to more than 24,800 groups, covering over 8 million employees nationwide.* Our frst group policy, written in 1951 and still in force today, stands as a testament to our commitment to building long-term relationships.

To learn more about products from The Standard, contact your human resources department or visit us at standard.com.

Standard Insurance Company 1100 SW Sixth Avenue Portland, OR 97204

Enrollment Booklet 000000-A

SI 20564 (3/19)