exploring trade dynamics between russia and turkey - denis varaksin - icis base oil london 2016

TRANSCRIPT

EXPLORING TRADE DYNAMICS

BETWEEN RUSSIA AND TURKEY

Denis Varaksin

Base Oils and Slack Wax Project Manager

DYM Resources GmbH

The 20th ICIS World Base Oils & Lubricants Conference

17-19 February 2016 London, UK

2

AgendaPresentation key points

Friends of FoesComplicated relationships between Russia

and Turkey, impact on base oils flows

DYM Resources GmbH

Niche oil products supplies

New Group II and III productionTaneco refinery startup review, running rates

and export routes

Russian market overviewRussian base oils capacities & closures

Export routes and dynamics

Modernisation plansRussian refineries modernisation plans and

impact on future base oils exports

N.Novgorod shut down impactConsequences of latest base oils unit closure,

refinery place in Russian base oil universe

CIS refinery reviewTurkembashi, Fergana, Baku and Naftan

refineries summary

3

Russia vs TurkeyMacroeconomics comparison of ex-friends

Turkey

• Population 78 mln

• GDP $722 bl

• GDP growth: + 4.2%

• Car sales: +26%

• Industrial growth: +4.4%

Russia

• Population: 146 mln

• GDP: $1236 bl

• GDP growth: -3.7% (decline)

• Car sales: -36% (decline)

• Industrial growth: -3.4% (decline)

Problem beginningTurkey took down Russian bomber Su-24,

that violated Turkey airspace for 17 seconds

according to Turkey.

Seventeen seconds awayPolitics impact on trade flows

2015

4

•Russia and Turkey had 12 wars, from 1568 to 1918 two countries were fighting each other for 69 years in total•Turkey is number one holiday destination for Russian tourists as well as big consumer of Russian Oil & Gas

AftermathRussia imposed sanctions against Turkish

companies working in Russia

Sanctions limited trading of fruits and vegetables (Turkey

accounted for 4% of Russian imports). Oil and gas trade was

not sanctioned, but some difficulties occurred for money

transfers and dealing with Turkish companies. Additional

sanctions may be imposed from both sides

2016

24 November

5

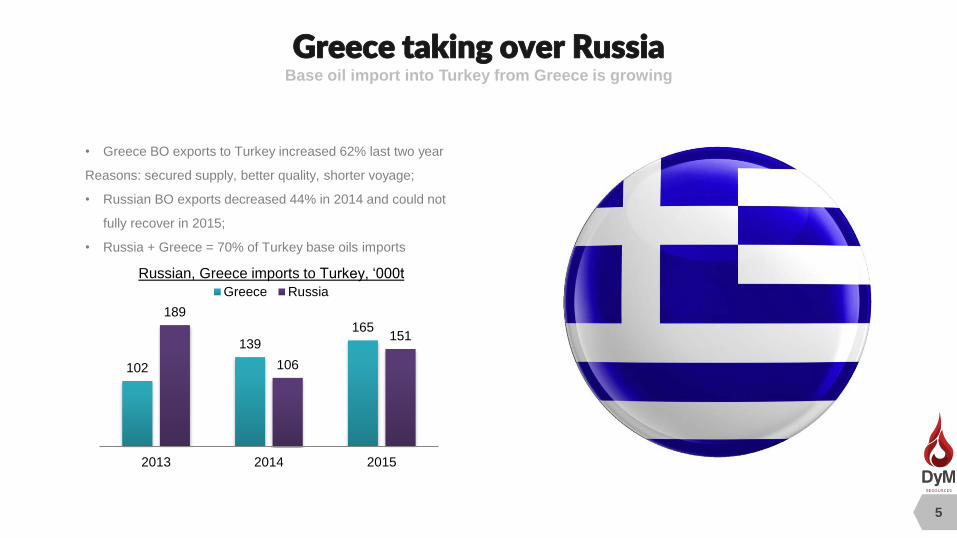

Greece taking over RussiaBase oil import into Turkey from Greece is growing

• Greece BO exports to Turkey increased 62% last two year

Reasons: secured supply, better quality, shorter voyage;

• Russian BO exports decreased 44% in 2014 and could not

fully recover in 2015;

• Russia + Greece = 70% of Turkey base oils imports

PERANCIS

SPANYOL

102

139

165189

106

151

2013 2014 2015

Russian, Greece imports to Turkey, ‘000t

Greece Russia

6

Russia & CIS base oils market recapLukoil is by far biggest base oil producer

Active producers

• Russia & CIS have 3mln tons per year capacity

• 90%+ is Group I mineral oils

• Since 2010 closed 1.1 mln t/yr BO units

• Plants located far from export outlets

Recent shutdowns

Producer Location Capacity, 000t/yr

Lukoil Volgograd 550

Lukoil Perm 440

Rosneft Novokuibyshevsk 350

Rosneft Angarsk 250

Rosneft/Gazprom Yaroslavl 250

Gazprom Omsk 240

Bashneft Ufa 220

Tatneft Nizhnekams 190

Uzbekneftegaz Fergana 200

Naftan Novopolotsk 195

Azerneftyag Baku 100

TRC Turkmenbashi 80

Location Date of closure Capacity, 000t/yr

Ryazan 2010 280

Orsk end of 2012 195

Kremenchug early 2012 370

N.Novgorod 2Q 2015 250

7

Russian base oils exports dynamicsRussian base oils export fell 13% in 2015

1,44

1,30

1,151,23

1,08

0,94

0,7

0,8

0,9

1

1,1

1,2

1,3

1,4

1,5

2010 2011 2012 2013 2014 2015

-13%

Key facts:

• Export dropped at highest pace since 2009

• Exports fell both by rail and river means of transport

• Volumes dropped 35% since 2010 despite rebound in 2013

• Russia is loosing presence in South-East Asia, India, UAE

Reasons:

• Lower demand from export markets

• Strong domestic demand due to import replacement

• Perm refinery faced production issues

• N.Novgorod base oil unit closure

-12%

+7%

-12%

-10%

8

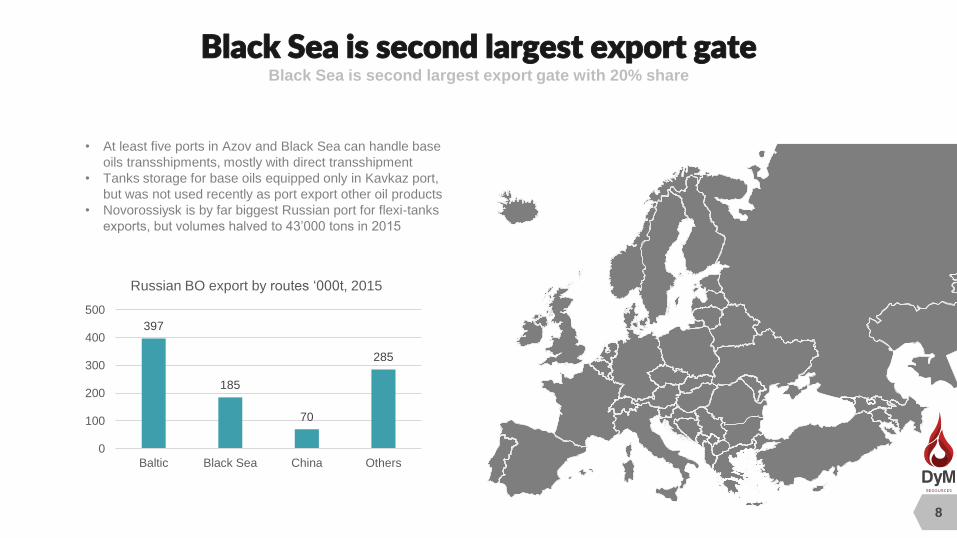

Black Sea is second largest export gateBlack Sea is second largest export gate with 20% share

• At least five ports in Azov and Black Sea can handle base

oils transshipments, mostly with direct transshipment

• Tanks storage for base oils equipped only in Kavkaz port,

but was not used recently as port export other oil products

• Novorossiysk is by far biggest Russian port for flexi-tanks

exports, but volumes halved to 43’000 tons in 2015

PERANCIS

SPANYOL

397

185

70

285

0

100

200

300

400

500

Baltic Black Sea China Others

Russian BO export by routes ‘000t, 2015

Russian BO export5 refineries controls 80% of BO export

9

GazpromActively decreasing

exports and focusing on

domestics finished lubes

market and CIS countries.

LukoilExport share decreased to

less than 50%, had to

change logistic scheme in

Back Sea due to sanctions

against Theodosia port, not

exporting through floating

storage

RosneftNovokuibyshevsk refinery exports

to CIS and Baltic. Angarsk

normally loads to China, but

was actively exporting to Baltic

Sea and Ukraine due to weak

China demand in 2015.

Volgograd35%

Novokuibyshevsk12%Omsk

11%

Perm11%

Angarsk11%

Yaroslavl4%

Ufa3%

Taneco0.5%

Others13%

Russian base oils export by refineries, 2015

10

Volgograd: Russian giant guarding Black Sea Biggest Russian base oils unit supplies to Turkey

• Volgograd 550’000 base oils unit is the biggest in Russia and CIS

• Refinery exports mainly SN 150, SN 500 and SN 900

• Only refinery in Russia exporting by river (Volgo-Don channel)

• Lukoil produces group III base oils in Volgograd (55’000t/yr

capacity, very high viscosity index, but has color)

Plant info

386

403

423

385

326

300

350

400

450

2011 2012 2013 2014 2015

Vogograd base oils export, '000t

Latvia16%

Romania6%

River30%Temryuk

13%

Eisk7%

Novo11%

Ukraine11%

Finland1%

Others5%

Volgograd export by destinations

11

Lukoil shuts 250’000t per year base oil unitVictim of low margins and high competition

Production and exports stopped in April 2015

Refinery accounted for 17% of Lukoil BO output

N.Novgorod loaded mainly light SN 150 grade

N.Novgorod refinery

139

89

94

72

15

‘00

0 t

70

0

140

2011 2012 2013 2014 2015

Svetly70%

Latvia8%

Belorussia

7%

Ukraine6%

Lithuania4%

Novo 3%Others2%

N.Novgorod was exported 70% though Lukoil’s

terminal in port Svetly (Kaliningrad region)

About 3% went to Novorossiisk port for flexi

containers export

12

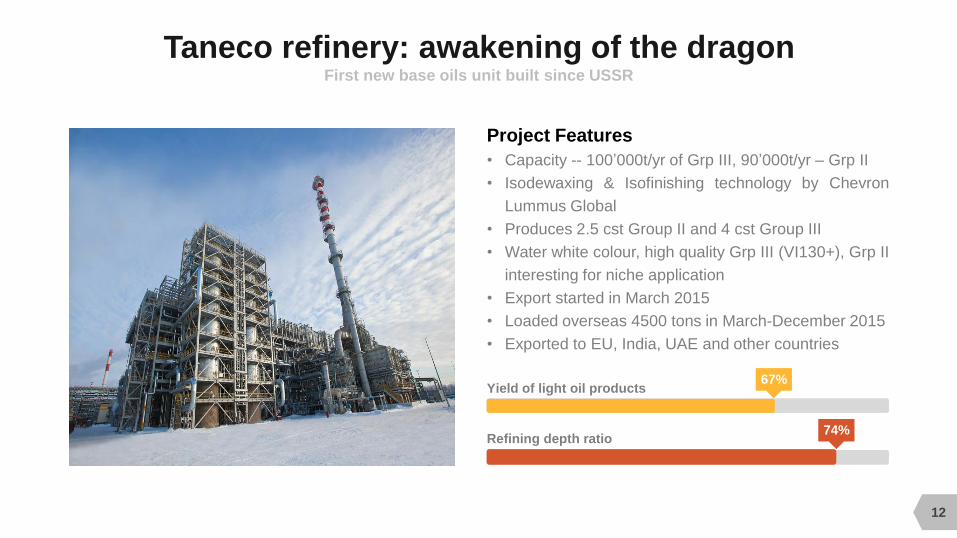

Taneco refinery: awakening of the dragonFirst new base oils unit built since USSR

• Capacity -- 100’000t/yr of Grp III, 90’000t/yr – Grp II

• Isodewaxing & Isofinishing technology by Chevron

Lummus Global

• Produces 2.5 cst Group II and 4 cst Group III

• Water white colour, high quality Grp III (VI130+), Grp II

interesting for niche application

• Export started in March 2015

• Loaded overseas 4500 tons in March-December 2015

• Exported to EU, India, UAE and other countries

Project Features

Yield of light oil products

Refining depth ratio

67%

74%

MODERNIZATION– WE WILL DO IT ONE DAY

13

Lukoil• Volgograd might be partly

convert to Group III by 2019,

• Perm scheduled to partly

partly to Grp II by 2021

Rosneft• Novokuibyyshevsk planned to

convert to Grp II/III by 2018

• Angarsk may add Group II

capacity by 2019/20

Gazprom• Yaroslavl* is undergoing

modernization to add Grp III

by 2017

• Omsk scheduled after 2021

BashneftBashneft at the moment has

no decided on its upgrading

program, most likely 3-5 years

production will be unchanged

*50% owned by Rosneft

14

Capacity to produce 80kt per year; average production of 2.5-3kt

of SN 180 and 2.5-3kt of SN 350 per month;

Group I+ product; almost Group II on new catalyst (VI above 100,

saturates 92+);

High Quality: bright color (0.5), low sulphur (below 0.03%), high

Viscosity Index;

Bulk cargo size from 1500mt to 3000mt, RTC parcels from 500

tons; exports to Iran, Central Asia and Black Sea;

Slack Wax production stopped in 2014, refinery is able to produce

up to 1500 tons of mixed slack wax per month;

3.7% tax for import into Turkey and Europe since Jan 2016;

Turkmenistan base oils :

hidden treasures

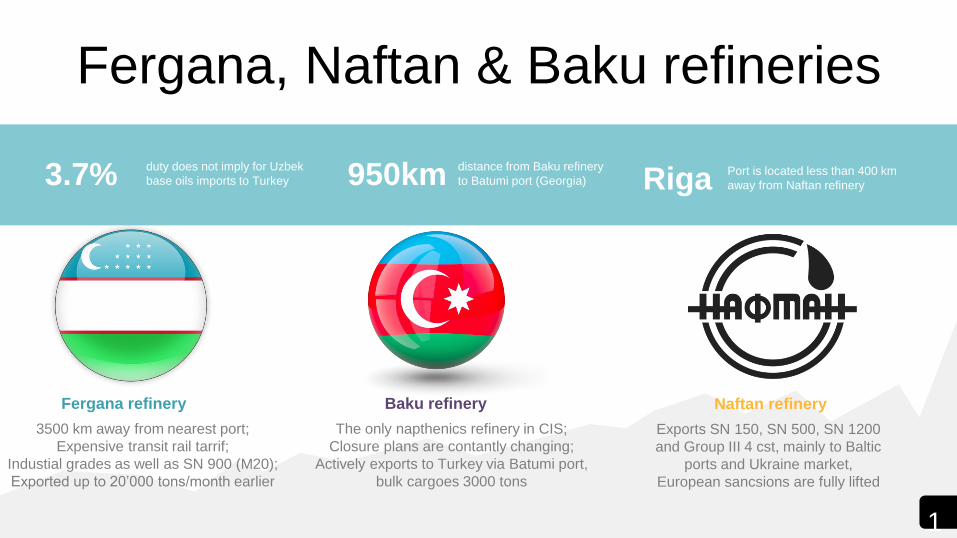

Fergana, Naftan & Baku refineries

3.7% duty does not imply for Uzbek

base oils imports to Turkey 950km distance from Baku refinery

to Batumi port (Georgia) Riga Port is located less than 400 km

away from Naftan refinery

Fergana refinery

3500 km away from nearest port;

Expensive transit rail tarrif;

Industial grades as well as SN 900 (M20);

Exported up to 20’000 tons/month earlier

Baku refinery

The only napthenics refinery in CIS;

Closure plans are contantly changing;

Actively exports to Turkey via Batumi port,

bulk cargoes 3000 tons

Naftan refinery

Exports SN 150, SN 500, SN 1200

and Group III 4 cst, mainly to Baltic

ports and Ukraine market,

European sancsions are fully lifted

1

5

16

DYM Resources GmbHNiche oil products supplies

Product rangeFocused on niche oil products: base oils

Group I, II and III; slack waxes;

petrochemicals; petroleum coke, etc.

Ideas to actions

LogisticsDoor to door services due to expertise with rail

tank cars, tanker loading, flexi and ISO tank

containers.

GeographyGeographic specialization: sourcing from

Russian Federation, CIS and Europe,

supplying globally.

Financing Financial flexibility to satisfy Producers and

support Buyers. Experienced with L/Cs, long-

term capital intense projects.

QualityHigh quality standards on all stages – from

product inspection at Producer’s plant up to

the unloading at Buyer’s facility.

LocationsHeadquarters in Berlin, Germany, although –

DYM team presence in Middle & Central Asia,

Central and Eastern Europe.

FEEL FREE TO

CONTACT US

THANKS FOR YOUR

Tel. +49 (176) 8601 5325

DYM Resources GmbH

Chorinerstr. 65, 10119 Berlin

ATTENTION!