exporters’ database - biaabiaa.com.au/resources/library/korea-exporters-v1.pdf · gyeonggi-do,...

TRANSCRIPT

ICOMIA EXPORTERS’ DATABASE

K O R E A

Edition 1 September 2011

1 Edition 1 – Sep 2011

ICOMIA EXPORTERS’ DATABASE

KOREA

CONTENTS

Boat Builders.............................................................................................................................................................. 2 Marinas ...................................................................................................................................................................... 4 Distributors handling imports into Korea ................................................................................................................... 5 Market Summary ....................................................................................................................................................... 7 Market Entry .............................................................................................................................................................. 7

Disclaimer While ICOMIA has tried to ensure the information contained in this file is accurate, we are dependent on independent sources and therefore cannot guarantee it. If you become aware of any inaccuracies you are encouraged to inform us at [email protected] to allow us to make corrections.

2 Edition 1 – Sep 2011

Boat Builders

Company Name What they are building Ownership details (e.g. Joint Venture)

Contact

Dongnam Leisure Boat Co., Ltd. Manufacturer of Dongnam Tank boats (inflatable)

Wholly Korean owned company

219-3 Choeup-Dong, Jin-Gu, Busan, Korea Jinseo Yang +82 51 817 7075 +82 10 2337 7959 [email protected] www.114boatcom

GHI Yachts

Manufacturing fibreglass composite powerboats from 13m to superyachts to 73m also power catamarans and sailing boats. GHI Yachts blends composite technology, state of the art steel and aluminium constructions with the world’s top designers, consultants and suppliers from the USA and Europe

Wholly Korean owned company

1697-5, Nanchun-ri, Sanho-eup, Yeongam-gun, Jeonnam, Korea Sengwook Moon +82 61 464 0900 +82 61 464 0790 (fax) +82 10 4735 9984 (mobile) [email protected] www.ghiyachts.com

Global Exclusive Lifestyle Ltd ( UK )

Known also as G.E.L. Korean Limited Soon to begin production of Fusion catamarans in Korea

James Stewart Kim Chairman +82 10 9263 2568 [email protected]

Hyundai Yachts Co, Ltd Manufacturer of Asan 45 62 82 fibreglass luxury yachts

Wholly Korean owned company

178-14 Seoguni, Paltanmeon, Hwaseong, Gyeonggi-Do, Korea (South) 445914 Ji Yeon, Lee +82 31 8059 6637 +82 31 8059 6638 [email protected] www.hdyachts.com

3 Edition 1 – Sep 2011

Company Name What they are building Ownership details (e.g. Joint Venture)

Contact

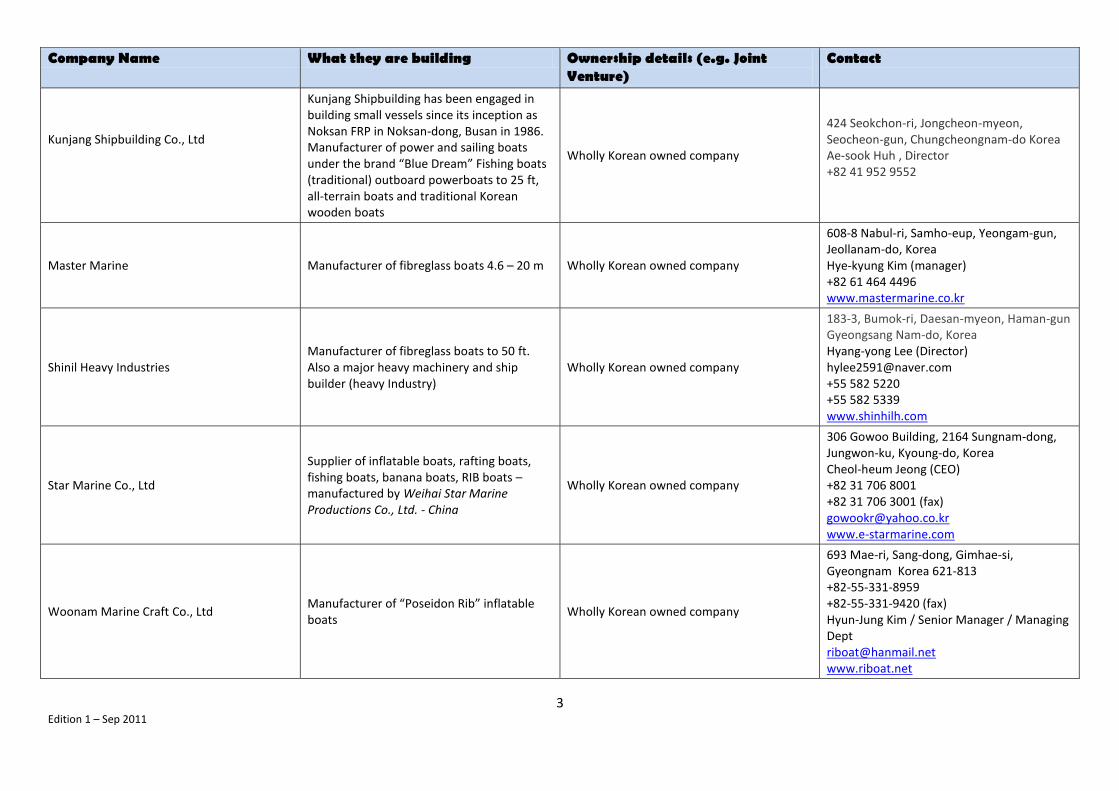

Kunjang Shipbuilding Co., Ltd

Kunjang Shipbuilding has been engaged in building small vessels since its inception as Noksan FRP in Noksan-dong, Busan in 1986. Manufacturer of power and sailing boats under the brand “Blue Dream” Fishing boats (traditional) outboard powerboats to 25 ft, all-terrain boats and traditional Korean wooden boats

Wholly Korean owned company

424 Seokchon-ri, Jongcheon-myeon, Seocheon-gun, Chungcheongnam-do Korea Ae-sook Huh , Director +82 41 952 9552

Master Marine Manufacturer of fibreglass boats 4.6 – 20 m Wholly Korean owned company

608-8 Nabul-ri, Samho-eup, Yeongam-gun, Jeollanam-do, Korea Hye-kyung Kim (manager) +82 61 464 4496 www.mastermarine.co.kr

Shinil Heavy Industries Manufacturer of fibreglass boats to 50 ft. Also a major heavy machinery and ship builder (heavy Industry)

Wholly Korean owned company

183-3, Bumok-ri, Daesan-myeon, Haman-gun Gyeongsang Nam-do, Korea Hyang-yong Lee (Director) [email protected] +55 582 5220 +55 582 5339 www.shinhilh.com

Star Marine Co., Ltd

Supplier of inflatable boats, rafting boats, fishing boats, banana boats, RIB boats – manufactured by Weihai Star Marine Productions Co., Ltd. - China

Wholly Korean owned company

306 Gowoo Building, 2164 Sungnam-dong, Jungwon-ku, Kyoung-do, Korea Cheol-heum Jeong (CEO) +82 31 706 8001 +82 31 706 3001 (fax) [email protected] www.e-starmarine.com

Woonam Marine Craft Co., Ltd Manufacturer of “Poseidon Rib” inflatable boats

Wholly Korean owned company

693 Mae-ri, Sang-dong, Gimhae-si, Gyeongnam Korea 621-813 +82-55-331-8959 +82-55-331-9420 (fax) Hyun-Jung Kim / Senior Manager / Managing Dept [email protected] www.riboat.net

4 Edition 1 – Sep 2011

Company Name What they are building Ownership details (e.g. Joint Venture)

Contact

Woosung I.B. Co., Ltd Manufacturer and exporter of “Walker Bay” and Zebec inflatable boats and life jackets, kayaks and on-water amusement craft

Wholly Korean owned company

331-10, Hyosung-Dong Gyeyang-Gu Incheon Korea Walter Kim Sales Manager +82 32 5558001 +82 32 5558003 (fax) [email protected] www.zebec.co.kr

Y & C Yacht & Creation Corp

First boat under construction at present – full details are not available however it is planned to have the boat completed and launched in time for the Korean boat shows in 2011 At time of compilation the website, although correct, was not operating.

Wholly Korean owned company

Jerome Lee President +82 11 9515 0954 [email protected] www.top7yacht.com

Marinas

Project Developer Details Contact

Baegunpo Marina Near 895-3 Yongho-dong, Nam-gu

Busan Metropolitan City Nam-gu District Office

112,400m² (land 35,150, sea area 77,250) 300 berths 73 dry (land) 227 on water Project cost A$30.79 million – 2010 – 2019 Seeking investors -

Lee, Jong Cheol Mayor of Nam-Gu, Busan +82 51 607 4002 [email protected]

Wangsan Marina (Near Incheon International Airport

Korean Air

Full service 300 berth marina and yacht club being specifically designed for the 17

th Asian Games

Yachting in 2014. The marina is being designed by AC Martin (USA) budget is US$150million construction to start in 2012 and be completed by end of 2013.

Mr Woojin Jeon, Team Head, Facility Maintenance and Operation, Korean Air +82 2 2656 7418 [email protected]

5 Edition 1 – Sep 2011

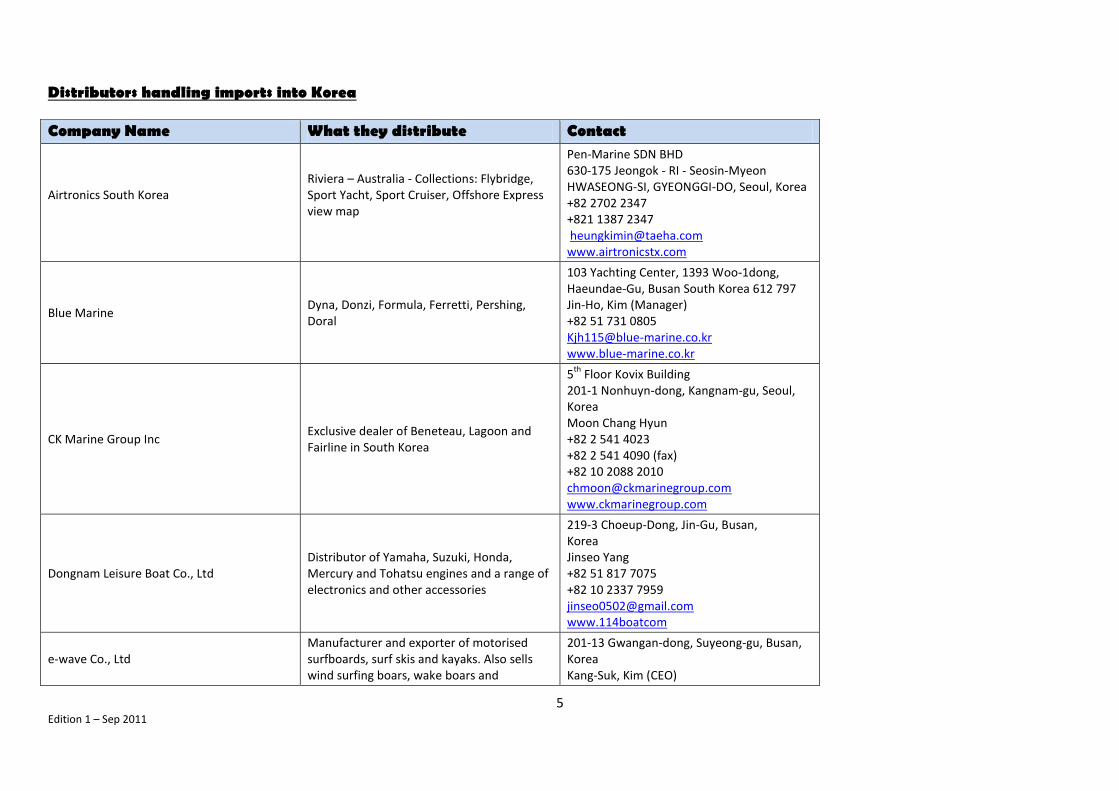

Distributors handling imports into Korea

Company Name What they distribute Contact

Airtronics South Korea

Riviera – Australia - Collections: Flybridge, Sport Yacht, Sport Cruiser, Offshore Express view map

Pen-Marine SDN BHD 630-175 Jeongok - RI - Seosin-Myeon HWASEONG-SI, GYEONGGI-DO, Seoul, Korea +82 2702 2347 +821 1387 2347 [email protected] www.airtronicstx.com

Blue Marine Dyna, Donzi, Formula, Ferretti, Pershing, Doral

103 Yachting Center, 1393 Woo-1dong, Haeundae-Gu, Busan South Korea 612 797 Jin-Ho, Kim (Manager) +82 51 731 0805 [email protected] www.blue-marine.co.kr

CK Marine Group Inc Exclusive dealer of Beneteau, Lagoon and Fairline in South Korea

5th

Floor Kovix Building 201-1 Nonhuyn-dong, Kangnam-gu, Seoul, Korea Moon Chang Hyun +82 2 541 4023 +82 2 541 4090 (fax) +82 10 2088 2010 [email protected] www.ckmarinegroup.com

Dongnam Leisure Boat Co., Ltd Distributor of Yamaha, Suzuki, Honda, Mercury and Tohatsu engines and a range of electronics and other accessories

219-3 Choeup-Dong, Jin-Gu, Busan, Korea Jinseo Yang +82 51 817 7075 +82 10 2337 7959 [email protected] www.114boatcom

e-wave Co., Ltd Manufacturer and exporter of motorised surfboards, surf skis and kayaks. Also sells wind surfing boars, wake boars and

201-13 Gwangan-dong, Suyeong-gu, Busan, Korea Kang-Suk, Kim (CEO)

6 Edition 1 – Sep 2011

Company Name What they distribute Contact associated equipment +82 51 622 9999

+82 51 755 0707 [email protected] www.blue-wave.co.kr

Global Exclusive Lifestyle Ltd ( UK )

Known also as G.E.L. Korean Limited Agent/representative/distributor of Fusion catamarans (France) and Gemini catamarans (USA).

James Stewart Kim Chairman +82 10 9263 2568 [email protected] www.gelkorea.co.kr

Hyundai Yachts Co, Ltd Maritimo - Australia

178-14 Seoguni, Paltanmeon, Hwaseong, Gyeonggi-Do, Korea (South) 445914 Ji Yeon, Lee +82 31 8059 6637 +82 31 8059 6638 [email protected] www.hdyachts.com

Komarine Co., Ltd

Tournament brand boats – manufactured in Australia Korean distributor for Wiggins (USA) marina forklifts

109 – 45, Il, Sin-Dong, Bupyeong-Gu, Incheon City, Korea 403110 Ji-Yeon, Kim +82 32 503 4609 [email protected] www.komarine.kr

Korea Marine Leisure Co., Ltd Importer distributor Yamaha outboard motors, pwc, a range of wake boards and accessories

887-7, Hadan-2Dong, Saha-Ku, Busan, Korea Soo Jong Lee +82 51 206 8373 +82 51 204 6819 (fax) [email protected] www.yamahamarine.co.kr

Power Marine Co., Ltd Agents / distributors of Princess, Grand Banks, Sunreef Yachts, Fountain Mercury Powerboats and RTM canoes and kayaks

Yachting Center 4-4, 1393 Woo 1-Dong, Haeundae-Gu, Busan, South Korea Kwang Soo, Jung +82 51 731 4000 +82 51 741 4332 [email protected] www.powermarine.co.kr

7 Edition 1 – Sep 2011

Market Summary

Recreational boating is slowly but surely forming a culture in South Korea thanks to the persistent “getting people on water” activities of the Korea International Boat Show, Yacht & Boat

Korea, sailing schools, provincial and central government’s efforts to establish this lifestyle choice. Whilst sales at the 2011 events were nothing spectacular – interest and enthusiasm

continues to grow and the industry maintains commitment for betterment and expansion. Foreign investment in recreational and associated boating infrastructure is rising, eg the opening

of the marina on the Hann River, however until there are more marinas established around the Southern coastline growth will remain constant but slow.

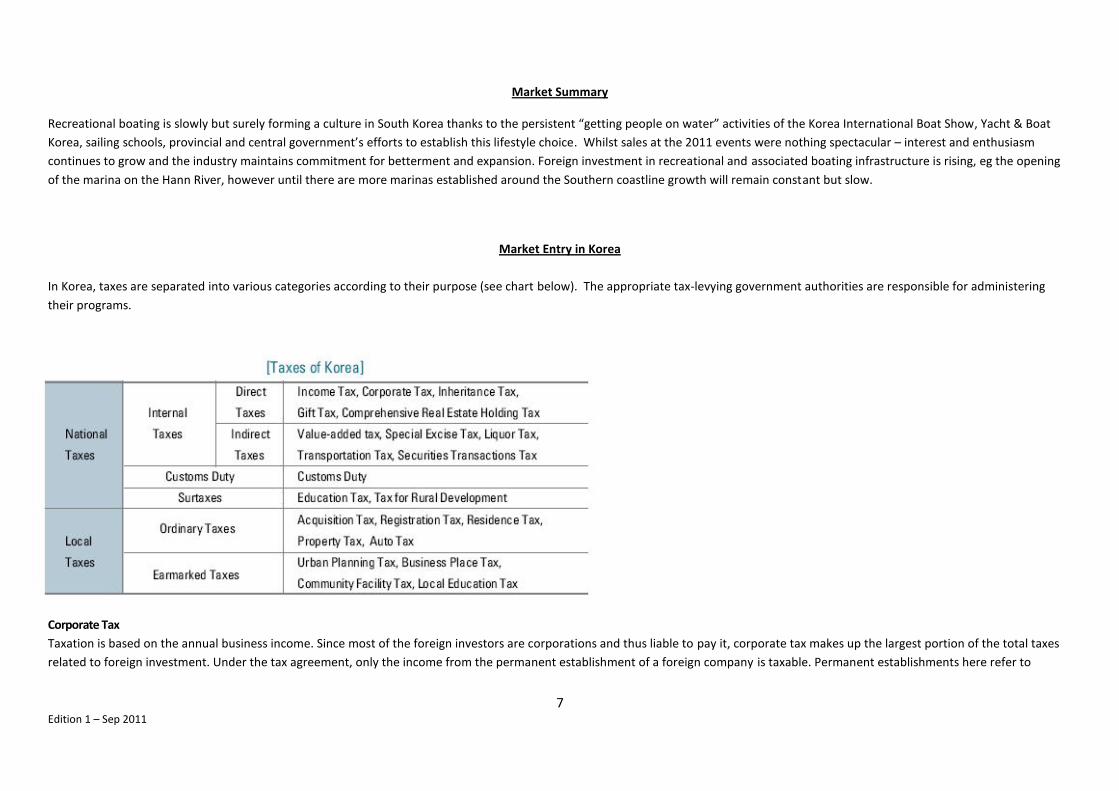

Market Entry in Korea

In Korea, taxes are separated into various categories according to their purpose (see chart below). The appropriate tax-levying government authorities are responsible for administering

their programs.

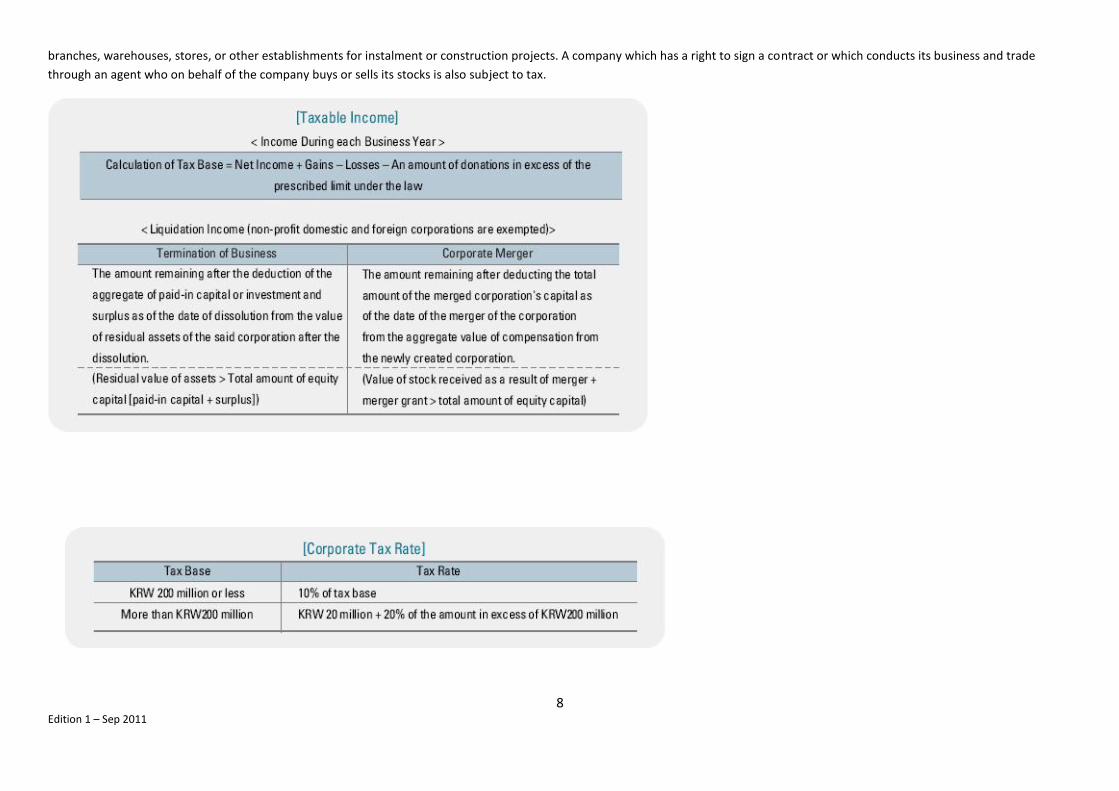

Corporate Tax

Taxation is based on the annual business income. Since most of the foreign investors are corporations and thus liable to pay it, corporate tax makes up the largest portion of the total taxes

related to foreign investment. Under the tax agreement, only the income from the permanent establishment of a foreign company is taxable. Permanent establishments here refer to

8 Edition 1 – Sep 2011

branches, warehouses, stores, or other establishments for instalment or construction projects. A company which has a right to sign a contract or which conducts its business and trade

through an agent who on behalf of the company buys or sells its stocks is also subject to tax.

9 Edition 1 – Sep 2011

Registration Tax

A Registration tax is levied when registering particulars concerning acquisition, transfer, alteration, or lapse of property rights or other titles in the official registry book. It should be paid

before business registration and the tax rate is as follows. Registration tax rates for corporations moving into the Overpopulation Control Zone from a Non- Overpopulation Control Zone

shall be levied three times the rates given above. However, for the following lines of business whose need to be at such a location is justified, heavy taxation shall not be applied.

10 Edition 1 – Sep 2011

11 Edition 1 – Sep 2011

Customs Duties

Tariff Assessment

All goods being imported from foreign countries into Korea must have their customs duties prepaid. Customs duties are calculated by multiplying the tax base of the tariff by the tariff rate.

The tariff tax base is either the value of the imported goods or the quantity. The tariff rate is provided on the tariff rate table by group of items. As the tax rate applies to each HS Number

(Harmonized System Number) corresponding to an item or a group of items, the tariff is affected by the decision on which value should be regarded as the taxable value or how the taxable

value is decided.

If the value is the tax base of the tariff, it is an “ad valorem duty” and if the quantity is tax based, it is called a “specific commercial duty.” The value, which is the tax base of the ad valorem

duty, is called the “taxable value.” Korean customs valuations on taxable values reflect the relevant provisions of the WTO Valuation Agreement. (For more information, visit

www.customs.go.kr)

Taxable Value

Taxable values on imported goods are assessed by various methods. The valuation method, which decides taxable value by transaction value, is called the first method. However, for cases

other than sales, the transaction value cannot be used as the base for taxable value. In these cases, the taxable value is determined by reviewing the following methods successively.

Customs Duties Refund

A customs duties refund refers to a situation where the Korean government returns certain customs duties to the customs duties payers under specific conditions. It is part of the export

support system that aims to enhance the international price competitiveness of Korean export goods. Under the system the Korean government returns to the exporters or the

manufacturers of export goods the customs duties they paid when they imported raw material for export goods.

12 Edition 1 – Sep 2011

How Foreigners Advance into Korea

Type Act Note

1 Local Corporation Foreign Investment Promotion Act Recognized as a foreign investment

2 Private Business

3 Branch Foreign Exchange Transactions Act Categorized as a domestic branch of the foreign corporation

4 Office

Comparison of a Foreign-Invested Company and a Domestic Branch

A Foreign-Invested Company under the Foreign Investment Promotion Act

Establishment of a local corporation in Korea by a foreign national or a foreign corporation is regulated by the Foreign Investment Promotion Act and the Commercial Act. A foreigner shall

invest not less than 100 million won for the local corporation concerned to be recognized as foreign investment under the Foreign Investment Promotion Act.

Private business established by a foreigner with the investment of not less than 100 million won is also recognized as foreign investment under the Foreign Investment Promotion Act.

Domestic Branch of a Non-resident (a foreign company, etc.) under the Foreign Exchange Transactions Act

A 'branch' operates business that generates profits in Korea, and is not recognized as foreign direct investment.

13 Edition 1 – Sep 2011

An 'office' does not carry out business that generates profits in Korea, but instead undertakes a non-sales function such as market research, R&D etc. An 'office' is granted a distinct number,

equivalent to business registration, at a jurisdictional tax office in Korea without the need for registration, which is different from a 'branch.'

<Comparison of a Foreign-Invested Company and a Domestic Branch>

Category Foreign-Invested Company Domestic Branch of a Foreign Company

Act Foreign Investment Promotion Act Foreign Exchange Transactions Act

Corporation Type Domestic corporation Foreign corporation

Identity Foreign investors and foreign-invested companies are of separate entities (independent accounting & settlement)

Headquarters and branches are of a single entity (the same accounting & settlement)

Delegated agency to process report and grant permission

Invest KOREA (KOTRA) or headquarters of a foreign exchange bank Branches of a foreign exchange bank (report), the Ministry of Strategy and Finance (permission of financial business etc.)

Minimum (Maximum) Investment Amount

100 million won or more per case, no upper limit No limit in investment amount

Scope of Tax Obligations Tax obligations for all domestic and overseas income Corporate tax rate: 10% for 200 million won or less, 22% for over KRW 200 million

Tax obligations for income from domestic sources only Corporate tax rate: 10% for 200 million won or less, 22% for over 200 million won In some cases, branch tax shall be paid.

Types of a Foreign Company's Domestic Branch

There are two types of domestic branches: a branch and a liaison office. A branch undertakes sales activities in Korea to generate profits. Meanwhile, a liaison office does not conduct sales activities to create profits, but instead carries out non-sales functions such as business contacts, market research, R&D, etc. Liaison offices can carry out quality control, market surveys, advertisements, and other incidental and supportive roles. However, they are limited in their scope of activities, since they are not allowed to sell products directly, or to stock inventory for sale on behalf of the headquarters.

14 Edition 1 – Sep 2011

Procedures to Establish a Foreign Company's Domestic Branch

Branch Establishment Report In order for a foreign company to establish a domestic branch, report shall be made to the head of a designated foreign exchange bank.

Required Documents

Report form of the establishment of a foreign company's domestic branch

Article of association (Notarization of the location of the headquarters is required)

Corporation: Article of association of headquarters

Private business: Financial statements, which have been audited by a certified public accountant

Letter of appointment for the head of a domestic branch, or a minute of the headquarters' board of directors on the matter

Power of attorney where the establishment of a domestic branch is commissioned to another person (Notarization of the location of the headquarters is required)

A certified copy of registration or operation permission of headquarters (Notarization of the location of the headquarters is required when a copy is submitted)

Both a branch and an office shall make a report to the Minister of Strategy and Finance in any of the following cases:

Financial businesses other than banking business, including fund loans, brokering and arranging overseas finance, cards, instalment financing, etc.

Businesses related to securities and insurances

Businesses, which are not permitted under the Foreign Investment Promotion Act or other laws

Businesses that are against Korea's morals and customs

15 Edition 1 – Sep 2011

Branch Establishment Registration

Under the Commercial Act, the establishment and registration of a business office is required, where a foreign company carries out business in Korea. An office under the Foreign Exchange Transactions Act is not allowed to conduct sales activities but information exchange, etc. Therefore, only branches can be registered as a business office.

Closure of Branch and Retrieval of Liquidation Funds

A report to the head of the designated foreign exchange bank has to be made, where a person who has acquired the establishment permission etc. under relevant regulations intends to close the domestic branch; liquidate assets, he/she has held in Korea; and retrieve the fund from liquidation. In such cases, the amount of retrieved funds shall not exceed the sum of funds brought in for the operation of the domestic office, retained earnings and other reserves of the domestic branch. (Losses are deducted.)

Required Documents for Retrieval of Funds

Application form: Apply under the name of liquidator when assigning the applicant

Statement of reasons for application

Liquidation report, which has been audited by a certified public accountant (including balance sheet and income statement on the date of closure and the date when liquidation is completed)

Certificate of the full payment of taxes (national & local tax)

Specifications of funds brought in for operations, retained earnings and other reserves

Certificate of bank balance (It shall be identical to the amount that can be remitted in the liquidation report)

Certified copy of liquidation completion registration (for a sales operation branch)

In cases where a certified copy of liquidation completion registration cannot be submitted, the following documents shall be submitted:

Certificate of fact for closure report (issued by a jurisdictional tax office)

Documents certifying the appointment of a liquidator

Documents certifying the fact for peremptory notice for bonds (copy of newspaper notice)

Certificate of whether there are payments in arrears to Korean workers (issued by the head of a jurisdictional labour office)

Original report form of the closure of a foreign company's domestic branch