extraordinary shareholders’ meeting - unicredit · extraordinary shareholders’ meeting ......

TRANSCRIPT

EExxttrraaoorrddiinnaarryy SShhaarreehhoollddeerrss’’ MMeeeettiinngg

JJuullyy 2277 22000055

IInnffoorrmmaattiivvee SShheeeett aaccccoorrddiinngg ttoo aarrtt..7700 ooff CCoonnssoobb RReessoolluuttiioonn 1111997711//9999

AAnnnneexx 11

ILLUSTRATIVE

REPORT

OF THE DIRECTORS

Capital increase in accordance with article 2441, paragraph four, of the civil code, up to a maximum amount of € 2.343.642.931,00, corresponding to up to 4.687.285.862 ordinary shares, to be paid by contribution of Bayerische Hypo-und Vereinsbank A.G. (“HVB”), Bank Austria Creditanstalt A.G. (“Bank Austria”) and Bank BPH S.A. (“BPH”) shares, with consequent amendment of the first paragraph of article 5 of the Company’s By-Laws.

Dear Shareholders,

This extraordinary shareholders meeting has been convened to resolve upon a proposal to increase the Company’s capital to be paid in by contribution in kind of: (i) HVB’s ordinary bearer and registered preference shares; (ii) Bank Austria’s ordinary bearer and registered preference shares; (iii) BPH’s ordinary bearer shares, and on the consequent amendments to the Company’s By-Laws.

The capital increase is finalised to the implementation of the envisaged combination between the UniCredit Group and the HVB Group, whose main principles are set out in an agreement (“Business Combination Agreement” or “BCA”) whereby UniCredit and HVB have agreed upon the terms of the aforementioned offers, the organizational and business model of the new Group, its governance and the lines for the definition of the future structure of the Group.

The aforementioned agreement contemplates, firstly, the acquisition of control of the HVB Group through the launching by UniCredit of: (i) a public exchange offer to acquire up to 100% of the share capital of HVB and (ii) two voluntary offers to acquire up to 100% of the shares of Bank Austria and BPH – in which HVB and Bank Austria hold a stake of 77,5% and 71,0% respectively. Taking into account the shares already held by HVB and Bank Austria in their respective subsidiaries, the proposed capital increase would be authorised to acquire - should the offers on Bank Austria and BPH be completely successful - a direct holding amounting to 22,5% of the share capital of Bank Austria and to 29,0% of the share capital of BPH.

You will find below an illustration of the rationale underlying our proposal and of the significant advantages that – upon completion of the aforementioned offers – would derive to the Company by the envisaged combination, which would lead to the creation of a Banking Group among the three first European players in the Eurozone.

1. RATIONALE AND MAIN ELEMENTS OF THE TRANSACTION

In the past decade, UniCredit showed a significant ability to create value, by generating, since the year of its privatisation (1993), a constant growth of per-share profits, which

2

increased at a yearly rate of 33%, from the equivalent of € 0,02 per share in 1994 to € 0,34 per share in 2004.

To achieve such goals, the UniCredit Group was capable of leveraging both on external – through mergers and acquisitions – and on organic growth.

In particular, as far as the external growth is concerned, the UniCredit Group has achieved excellent results in restructuring various companies acquired in Italy and abroad. It should be noted in this connection that, since the year of its acquisition (1999), Bank Pekao reduced its cost/income from 69% to 55%, with a corresponding growth of the per-share price of 143%1. Since 2001, Pioneer reduced its cost/income from 78% to 51%. Moreover, from 1994 to 2004, the overall Group reduced its cost/income from 86% to 57%, also due to the integration of the regional banks following implementation of the S3 Project.

Capitalising on the S3 Project, which led to a strong focus on client segments, the UniCredit Group developed its capabilities for organic growth. Actually, between 2002 and the first quarter of 2005, the market share for lending in Italy increased from 9,9% to 10,9%, while, in 2004, 99.000 new retail clients were acquired, net of operational reclassifications. Between 2002 and the first quarter of 2005, the share of managed assets from extra-Group networks increased of 50%, from € 38 billion to € 57 billion.

Thanks to such track-record, UniCredit shares steadily rank among the most profitable securities in the Italian market, with a dividend yield of 5,3%. However, failing further growth opportunities, there is the risk that UniCredit shares could be perceived in the market as a high-yield bond, with a high yearly coupon but with limited prospects for price growth.

Against this background, the opportunities to create value which can generate positive effects on UniCredit shares’ prices in the mid-term do not seem to leave out of consideration external growth strategies. Additionally, it should be pointed out that the possibilities to implement such a strategy are limited, in light of the scarcity of available opportunities. Furthermore, any research for possible targets must take account of certain restraints: firstly, any transaction shall ensure both the preservation of dividends in the short term and growth in the following years; indeed, growth in the medium-long term cannot be detrimental to shareholders in the short term. Secondly, the transaction must give scope to create entities with increased strategic opportunities: increased geographical diversification; economies of scale in production businesses; further consolidation opportunities. Finally, each transaction must be justified by a clear equity story, within which UniCredit may take advantage of its restructuring skills and UniCredit together with the target may create a new entity with excellence features, thereby generating signficant synergies.

In light of the foregoing, the business combination with the HVB Group appears as the most interesting opportunity available at the moment. Indeed, there is no space in Italy for middle-sized or big transactions, but only for selected growth opportunities in specific businesses (if any). In other western Europe markets, notwithstanding the ostensible flurry of possible initiatives, a little number of transactions has been carried out. In such a scenario, due to its size, UniCredit could not easily propose itself in the role of the combination leader. Moreover, UniCredit’s growth initiatives continue both in Central Eastern Europe (“CEE”) – where such opportunities are at this stage limited and onerous – and in other markets (e.g. China), but cannot deliver a “strategic leap” to the Group.

1 On the basis of the price as of 2 June 2005 relative to the purchase price.

3

The combination between the UniCredit Group the HVB Group would lead to the creation of a banking group among the three first European players in the Eurozone, with aggregate clients volumes amounting to approximately € 800 billion. The contribution by the HVB Group to the newly created entity would be significant both in terms of volumes and of banking revenues, amounting respectively to 64% and 47% of the combined Group, while its contribution in terms of profitability would amount approximately to 28%. The new group would also benefit from increased business diversification in geographic terms, where Italy would only account for 30% of lending activities, as well as in terms of clients segments, with a more balanced mix between retail and corporate.

Finally, the combined Group would acquire an excellent positioning in the main European markets, becoming the second Italian banking group, the second in Germany and the first in Austria, by far the first banking group in the CEE, where, in particular, it would be leader in Poland, Croatia and Bulgaria, with a presence in all other markets including Hungary, Russia and Serbia, target markets for UniCredit where we do not have a presence yet.

The combined Group would also have a selected presence outside Europe.

2. THE HVB GROUP – RECENT HISTORY AND FEATURES

2.1 RECENT HYSTORY. The HVB recent history starts in 1998, the year of the merger between Bayerische Vereinsbank (founded in 1869) and Bayerische Hypotheken-und Wechsel Bank (founded in 1835). In that year the Group, that already had a widespread presence, mainly in corporate segments, in CEE markets (Bulgaria, Czech Republic, Hungary, Slovakia, Baltic Countries), further expanded also due to the acquisition of the Polish bank Przemysolowo-Handlowy S.A. (BPH). In 1999, HVB expanded its presence in the Russian market, increasing to 40% its participation in International Moscow Bank.

In 2000, HVB acquired Bank Austria Creditanstalt, thus becoming the third European group in terms of size. Through the acquisition of Bank Austria, that already controlled the Polish bank PBK (merged into BPH thereafter) and other banks in the Czech Republic, Slovakia, Hungary, Slovenia, Croatia, Romania, Ukraine and Russia, the HVB Group significantly increased its presence in CEE markets. In 2001, HVB and Bank Austria started the combination of the respective banking subsidiaries in those markets, under the coordination of Bank Austria, except for the banks in the ex Soviet Union.

In 2002, the Group effected a major internal reorganisation whereby it was structured in two macro-regional divisions - Germany and Austria/CEE – and in two global divisions– Corporates & Markets and Real Estate Workout, subsequently renamed RER. At the same time, the Group continued to grow in CEE through the acquisition (from UniCredit) of Splitska banka in Croatia and Bank Biochim in Bulgaria, and the setting up of HVB Bosnia Herzegovina in Bosnia Herzegovina.

In 2003, in the wake of a difficult macroeconomic environment that affected the operational performance and the quality of the assets (in particular the real estate loan portfolio), HVB started a rationalisation of its activities with a view to increasing its capital ratios. To this end it: (i) disposed of its consumer credit company Norisbank in Germany and the private banks Bank von Ernst and Baankhaus Bethmann Maffei, in Switzerland and Germany respectively; (ii) transferred its commercial real estate loan portfolio to a newco, Hypo Real Estate, that was subsequently listed; (iii) started the IPO of Bank Austria, already 100% controlled at the time. Furthermore, the organisational structure of the group was again changed by creating three macro-divisions: Germany, Austria & CEE and Corporate & Markets.

4

The Group rationalization continued in 2004, through the disposal of existing holdings (in Allianz, B&B and the power company E.ON, with shareholding in Munich Re reduced to its current 10%). In March 2004, to further strengthen its capital base, HVB increased its capital with pre-emptive rights in an overall amount of €3 billion. In Germany, HVB incorporated its subsidiary bank Vereins und-Westbank, headquartered in Hamburg. The Group further expanded in the CEE by acquiring Hebros Bank in Bulgaria and Eksimbanka in Serbia, along with acquiring a majority share in International Moscow Bank.

In January 2005, HBV announced an extraordinary adjustment of its real estate loan portfolio totalling €2.5 billion, and started a restructuring plan (“PRO”), intended to achieve, upon implementation, cost synergies for €280 million. Following recent adjustments, asset quality appears to be in line with its German competitors: the Group resumed growth, also owing to a business restructuring plan in Germany which generated positive results during first quarter 2005, with profits of approximately €340 million. As far as its expansion in the CEE is concerned, the HVB Group recently finalized a transaction in Romania aimed at the merger of HVB Bank Romania and a private bank, Banca Tirac, thereby creating the fourth leading bank in Romania based on total assets.

2.2 KEY DATA. HVB, whose head office is in Munich, is currently the ninth largest banking group in Europe in terms of total assets and the second largest in Germany. As at 31 December 2004, HVB had total consolidated assets equal to € 467 billion, loans to clients of € 275 billion, deposits by clients for an amount of € 144 billion, approximately 10 million clients and a network of 2,036 branches in Germany, Austria and the CEE. The overall intermediation margin for 2004 exceeds € 9 billion, whereas the operational result is more than € 3 billion.

The group mianly focuses on retail and corporate clients in Germany, Austria and the CEE and operates through the following business lines:

− Germany: divided into 3 sub-segments: retail clients, corporate clients and real estate;

− Austria & CEE: divided into 3 sub-segments: retail clients, corporate clients and CEE;

− Corporates & Markets: (including large corporate clients and structured finance);

− RER (Real Estate Restructuring): which includes a credit portfolio under restructuring and has incorporated the previous division of Real Estate Workout (residential loans) created after the 1998 merger.

As at 10 June 2005, HVB had a market capitalization of approximately € 15.0 billion. Munich Re is the major shareholder with a share of 18.4% of the voting capital, despite having diluted its previous holding (of 25.6%) by not taking part to the capital increase of approximately € 3 billion carried out by HVB in March 2004. There are no controlling shareholders.

HVB is the controlling shareholder of Bank Austria. Since the listing of 22.5% of Bank Austria on the Vienna Stock Exchange in July 2003, HVB owns 77.5% of its capital. At the time of their combination, HVB and Bank Austria entered into agreements defining Bank Austria’s role within the Group (“Regions Bank Agreement”), whose main contents

5

- together with their incidence on the transaction submitted to your approval - are illustrated below.

As of 31 December 2004, Bank Austria had total consolidated assets of € 147 billion, net credits to clients of € 78 billion and net assets of € 7 billion, increasing relative to the previous year by 7%, 8% and 8% respectively. It closed the 2004 financial year with a consolidated intermediation margin of € 3.5 billion and consolidated profits of € 0.6 billion, with a ROE of 10% and a cost/income ratio of 65%. As far as the quality of assets is concerned, the level of Bank Austria’s overdue credits appears stable compared to the end of 2004, with overdue credits equal to 4% of gross credits.

Bank Austria controls 71.0% of the Polish bank BPH. As at 31 December 2004, BPH had total consolidated assets of € 13 billion, credits to clients of € 7 billion and net assets of € 1.5 billion (data in PLN converted at the exchange rate of 4.08 PLN/€ at the end of 2004), increased, relative to the previous year, by 11%, 10% and 12% respectively. BPH closed the 2004 financial year with an intermediation margin of € 639 million and consolidated profits of € 174 million (data in PLN converted at the average exchange rate for the year 2004 of 4.53 PLN/€), with ROE of 14% and a cost/income ratio of 54%. As far as the quality of assets is concerned, the level of BPH’s overdue credits appears stable compared to the end of 2004, with overdue credits of € 0.7 billion equal to 8% of gross credits.

2.3 MARKET POSITIONING. HVB is the second largest German bank in terms of total assets, with an average national market share equal to 5% at the end of 2004, strongly rooted in the region of Bavaria, one of Germany’s richest regions (18% of the German GDP and per capita GDP equal to 128% of the EU15 average), where it controls a 15% market share. In Germany it operates through around 700 branches, of which 57% in Bavaria with a national average market share of 5%, and has 4 million clients.

The German banking sector is characterised by a three “pillar” structure: the commercial banks, the public banks (which include Landesbanken and Sparkassen) and the cooperative banks. The market is highly fragmented: the 3 biggest banks, including HVB, have an overall market share of around 15-20%, with predominance of public banks and cooperative banks, which are not necessarily oriented to maximizing profits. HVB’s main competitors at national level are Commerzbank, Deutsche Bank and Dresdner Bank, and at regional level the public banks and cooperative banks.

HVB operates on the Austrian market through Bank Austria: created in 1997 following the merger of Bank Austria and Creditanstalt, Bank Austria is the biggest Austrian bank with a national average market share of 18% in terms of total assets, 20% in terms of loans to clients and 14% in deposits by clients. It operates in Austria through around 400 branches and has 1.8 million clients.

The Austrian banking market is characterized by the presence of three different types of credit institutions: saving banks, commercial banks and cooperative banks. In this context, a limited number of banks of significant size (the 5 leading banks, including Bank Austria, increased their overall market share through mergers and acquisitions from 45%, in the mid-nineties, to approximately 55-60% nowadays) operate side by side with a large number of smaller banks, principally saving banks and cooperative banks. The main Austrian banks (Bank Austria, Erste Bank, Raiffeisen Bank) are characterized by a strong positioning in the CEE. Bank Austria’s main competitors are: Erste Bank, 3-Banken Gruppe (in which Bank Austria holds a minority stake) and Investkredit Bank.

6

As far as the CEE markets are concerned, HVB operates in those countries mainly through companies controlled by Bank Austria, which has a sub-holding role in financial activities in Austria and Eastern Europe. With total assets of approximately € 35 billion, around 900 branches and 4.5 million clients, HVB is the second largest banking group in the CEE after UniCredit. The group is present in 11 countries: Croatia (5th in terms of total assets, with a market share of 8%, based on 2004 data), Bulgaria (4th with 10%), Poland (3rd with 8%), Bosnia (4th with 8%), Slovakia (5th with 5%), Czech Republic (4th with 6%), Serbia (5th with 6%), Romania (8th with 5%), Hungary (7th with 5%), Slovenia (7th with 5%) and Russia (around 1%).

With total assets of PLN 59 billion (€ 13 billion) at the end of 2004, BPH is the third largest Polish banking group. Public participation in the Polish banking sector has decreased strongly in the past 10 years and PKO BP (partially privatised in 2004) and BGZ remain the only banks currently controlled by the State. The number of banking institutions has gradually decreased over the past few years following a large number of merger and acquisition transactions. The sector is characterised by the high participation of foreign financial institutions (8 of the 10 biggest Polish banks are in fact in foreign hands). Compared with other CEE economies, Poland is characterized by a lower degree of concentration, with the 5 leading banks having around a 50% market share in terms of total assets. BPH’s main competitors are PKO BP, Bank Pekao, Bank Handlowy, ING Bank, BRE Bank and BZW BK.

2.4 FINANCIAL STRUCTURE. As of 31 March 2005, following an adjustment of non performing loans for an amount of € 2.5 billion in January, HVB has a core capital of € 15.4 billion, regulatory capital of € 27.2 billion and total risk weighted assets of around €264 billion, corresponding to a Tier I ratio of 6.4% and to a Total Capital Ratio of 10.2%.

2.5 PERFORMANCE. IN 2004 HVB recorded a consolidated operating result of € 1,389 million, slightly lower than the original target of € 1,400-1,700 million, but higher than the consensus estimate of around € 1.2 billion.

These results, higher than estimated, are mainly due to particularly high operating profits. Yet, the contribution of extraordinary items was also significant; these were mainly represented by: (i) non recurrent interest in the amount of around € 157 million; (ii) income deriving from the sale of holdings; and (iii) a reduction in operating expenses due to the postponement of IT projects and the deferment of retirement expenses and other extraordinary costs.

In spite of the good operating results, HVB recorded a consolidated loss of € 2,278 million in 2004, after extraordinary adjustments on loans in the amount of € 2.5 billion (vs. a loss of € 2,442 million in 2003).

With the adjustments on loans of € 2.5 million announced on 21 January 2005, HVB significantly improved the quality of its assets, bringing the coverage ratio of non performing loans from 44.5% at the end of 2003 to 55.5% at the end of 2004, whereas the flow of overdue loans at the level of HVB A.G. appears to have benefited from a significant slowdown (€ 1,149 million in the second half -year 2004 compared to € 1,847 million in the first half year).

As at 31 March 2005, HVB reported consolidated operating results of € 871 million, representing an increase of 11.8% compared to the first quarter of 2004 (€ 779 million), with a target for the entire 2005 financial year of € 3,324 million. These results are due

7

both to the growth in earnings (+9.2% of the interest margin due to an improvement in margins; +8.0% of net commissions and profits from financial operations by 21.5% compared to the first quarter of 2004) and to cost efficiency (growth contained within 3.8%, in line with the 2005 target). Based on the annualised data of the first quarter of 2005, the net interest margin on total credits is of 1.7%, the intermediation margin on total credits is equal to 3.0% and the cost/income ratio equal to 65%. HVB closed the first quarter of 2005 with consolidated profits of € 336 million, equal to around € 1.3 billion in annualised terms, compared to a loss of € 2.7 billion at the end of 2004 and profits of € 56 million in the first quarter of 2005, equivalent to a ROE of 11.6%.

As far as the quality of the assets is concerned, the level of HVB’s non performing loans, excluding the RER division, appears stable if compared to the end of 2004 (€ 12.8 billion overdue at the end of 2004), with non performing loans of € 12.9 billion, equal to 3.4% of the credit exposure.

3. CORPORATE STRUCTURE OF THE TARGET BANKS

3.1 HVB. HVB’s share capital is equal to € 2,252,097,420 and is represented by 750,699,140 shares without per-share nominal value, subdivided in two categories: ordinary (bearer) and preference. There are 736,145,540 ordinary shares, with an overall nominal value equal to € 2,208,436,620. There are 14,553,600 preference shares, with an overall nominal value equal to € 43,660,800. Registered shares generally do not carry voting rights but guarantee the right to receive a preference dividend, equal to the ordinary dividend plus € 0.064 per share. The preference element of € 0.064 per share must be paid to the holders of preference shares in priority over the payment of ordinary dividends. In the event that the aforementioned preference element is not paid for two consecutive financial years, including any arrears, holders of preferred shares acquire a voting right until payment of outstanding dividends. Since the preferential element was not paid by HVB in 2002 and 2003 financial years, the preference shares currently carry voting rights.

HVB’s share capital (including the preference shares) is held by a variety of institutional and retail investors. In addition to the major shareholder - Munich Re – other significant shareholders are the Bavarian Foundation Bayerische Landesstiftung, which holds 2% represented solely by preference shares, and the asset management company Capital Group, which holds 5% of the capital. Based on the information supplied by HVB, the remaining 75% of the capital is divided among other strategic investors (5%), other institutional investors (55%) and retail investors (15%). The ordinary shares are listed on the Frankfurt Stock Exchange and on several other local German stock exchanges, on the Vienna Stock Exchange, the Zurich Stock Exchange and the Paris Stock Exchange. An ADR program is traded “over-the-counter” in the U.S. All the preference shares are held by Bayerische Landesstiftung and are not listed.

3.2 BANK AUSTRIA. Bank Austria’s capital amounts to € 1,068,920,749.80, represented by 147,031,740 shares without per-share nominal value, subdivided in two categories: ordinary and preference shares. There are 147,021,640 ordinary shares, and 10,100 preference shares. Special rights attach to the preference shares: in particular, it is requested that these shares be represented at the general meeting to resolve on certain matters which affect the existence and the governance structure of Bank Austria, as will be better illustrated below. 77.5% of the ordinary shares are held by HVB, with the remaining 22.5% held by institutional and retail investors. The ordinary shares are listed

8

on the Vienna and Warsaw Stock Exchanges. The preference shares are held by Anteilsverwaltung-Zentralsparkasse (“AVZ”), the Foundation of the city of Vienna, and the Work Council Fund (“WCF”), the Fund of Bank Austria’s employees.

3.3 BPH. BPH’s capital amounts to PLN 143,581,150 represented by 28,716,230 ordinary shares with a nominal value of PLN 5.0 each. 71.0% of the shares are held by Bank Austria, with the remaining 29.0% held by institutional and retail investors. The shares are listed on the Warsaw and London Stock Exchanges under a GDR program.

4. THE OFFERS

As anticipated, the Business Combination Agreement entered into by UniCredit and HVB sets out the terms of the envisaged combination, the organisational and business model of the new Group, its governance and the criteria for the definition of the future Group structure. Considering that the main contents of the agreement - and, hence, of the transaction - will be illustrated below, we would like to underline in the first place that, in order to implement the transaction in consideration, UniCredit intends to launch three public offers to acquire, either directly and indirectly, up to 100% of the share capital of HVB, Bank Austria and BPH.

4.1 PUBLIC OFFER FOR HVB. UniCredit intends to launch a voluntary exchange offer to acquire up to 100% of the share capital of HVB, represented by ordinary and preference shares. The proposed exchange ratio would be 5.00 newly-issued UniCredit shares – issued following the capital increase to be subscribed for by contribution in kind submitted to your approval today - for each HVB share, determined on the basis of the valuations of the 2 companies by applying the valuation methods detailed below. Considering the price of UniCredit on 10 June 2005 (Euro 4.095), this exchange ratio represents an implicit premium of 8.3% over HVB shares’ average price during the three-month period immediately preceding the announcement of the transaction, while the premium on the price of HVB as of 10 June 2005 would be 2.3%. On the basis of the UniCredit price on 25 May 2005 - the day before the start of significant market speculation - (Euro 4.2375), this exchange ratio implies an implicit premium of 13.5% on the average price of HVB in the three months preceding the same date, while the premium on the price of HVB as of the same date would be 10.4%.

As anticipated, in order to maximise the success of the exchange offer for the HVB shares, UniCredit has undertaken to list its ordinary shares - with effect from completion of the offer - on the Frankfurt Stock Exchange.

4.2 PUBLIC OFFER FOR BANK AUSTRIA. The acquisition of control by UniCredit over HVB would entail the acquisition of (indirect) control over Bank Austria. This, under local laws, requires the launching of a mandatory take-over bid, necessarily contemplating a cash consideration.

To avoid any impact on capital structure deriving therefrom, we would launch, as a preventive measure, a voluntary public offer simultaneously with the HVB offer, over 100% of the shares of Bank Austria: the pre-emptive voluntary offer could, in fact, be launched by offering UniCredit shares as payment, provided that a cash alternative is also offered, leaving to the addresse of the offer the option to choose the form of payment. It should be noted that HVB could not adhere to the offer, neither the one contemplating an exchange offer (since this would be in breach of the prohibition contemplated by article 2357-quater read in conjunction with article 2359-quinquies of the Italian civil code), nor the cash offer since HVB has given an undertaking to that

9

effect in the BCA; consequently, upon completion of the offer, UniCredit would directly hold up to a maximum of 22.5% of the share capital of Bank Austria.

The ratio of the exchange offer should take into account the premium paid to the HVB (parent company) shareholders in the valuation of the controlling interest in Bank Austria, in order to comply with the principle of equality of treatment of shareholders in said company. The structure of the offer has been informally submitted to the local supervisory authority - the Take-over Commission - which, while accepting the principle of parallel (“paper”/”cash”), preemptive offers, was not able to confirm, at that time, whether the cash offer was enough to comply with the take-over law. It should be mentioned, however, that the Take-over Commission will issue an opinion on the Offer following the formal submission of the offer document, on which it shall issue a statement, taking also into account the price component of the offer, following receipt of opinions issued thereon by one expert appointed by UniCredit and another appointed by the target company (Bank Austria).

The proposed exchange ratio - calculated on the basis of the methods detailed below - would be 19.92 newly-issued UniCredit shares for each Bank Austria share and, on the basis of the UniCredit shares’ price as at 10 June 2005, would represent an implicit premium of 8.3% on the average Bank Austria price, in the 3 months prior to the announcement, while being in line with the Bank Austria price on 10 June 2005 (+ 0.1%). On the basis of the UniCredit price on 25 May 2005, before market speculation, this exchange ratio would represent an implicit premium of 13.6% on the average Bank Austria price, in the 3 months prior to the same date, while the premium on the Bank Austria price on the same date would be 12.1%.

The cash price offered, however, would be Euro 70.04 per share, equal to the average price over the 6 months prior to 27 May 2005 (the last working day before the joint UniCredit/HVB announcement of 30 May). This price represents the lower limit required for mandatory offers.

The difference between the cash offer and the value implicit in the exchange offer (on the basis of the UniCredit price on 10 June 2005) would be 16.3%.

We would like to inform you that, on the basis of the foregoing, should those who adhere to the Bank Austria offer (who will be the minority shareholders only, given HVB’s undertaking not to adhere) opt in part to receive a cash consideration, the aggregate disbursement by UniCredit would amount approximately to Euro 2.3 billion.

4.3 PUBLIC OFFER FOR BPH. The acquisition of control over Bank Austria by UniCredit would entail (indirect) acquisition of control over BPH, triggering the requirement to launch a mandatory offer in cash. In line with the considerations already made with regard to Bank Austria, we are envisaging to launch as a preventive measure a voluntary offer simultaneously with the HVB and Bank Austria offers, for 100% of BPH shares. The offer might be launched by offering UniCredit shares in payment, provided that a cash alternative will be guaranteed, leaving to the subscribers the option to receive any form of payment. The exchange ratio proposed for the voluntary exchange offer would be 33.13 newly-issued UniCredit shares for each BPH share, which, on the basis of the UniCredit price on 10 June 2005 and the PLN/Euro exchange rate, at the same date, of 4.03, would represent an implicit premium of 9.8% on the average BPH price in the 6 months prior to the announcement (the lower price limit established under Polish law for take-over offers), while there would be a discount on the BPH price on 10 June 2005 of 2.6%. On the basis of the UniCredit price and the PLN/Euro

10

exchange rate on 25 May 2005, before market speculation, this exchange ratio would represent an implicit premium of 19.7% on the average BPH price in the 6 months prior to the same date, while the premium on the BPH price on the same date would be 21.6%.

The payment for the cash offer, however, would be equal to the average price during the 6 months prior to the date of the announcement (as defined under Polish law), which price would represent the lower limit required for mandatory offers. Should the Polish authorities assume that the announcement of 12 June represents the end of the reference period for the price calculation, such price would be Euro 123.58 per share.

The offer would be launched for 100% of the share capital of BPH, provided that HVB committed to use its best efforts to procure that Bank Austria will not tender its shares in the offer; in such case, potential subscribers would be represented by the minority shareholders only and, consequently, at the end of the offer, UniCredit could directly acquire up to 29.0% of the BPH share capital. Should those who adhere to the offer opt to receive a cash consideration, the aggregate disbursement for UniCredit, would be approximately Euro 1.0 billion, subject to the requirement on UniCredit to issue, in any event, a letter of guarantee for 100% of the counter value of the cash offer (in order to account for the possibility, albeit remote, of Bank Austria tendering its shares).

The difference between the payment for cash and the value implicit in the exchange offer (on the basis of the UniCredit price on 10 June 2005) would be 9.8%.

Finally, it should be pointed out that listing of UniCredit shares on the Warsaw Stock Exchange is a condition to enable local investors to hold UniCredit shares. Consequently, UniCredit has also undertaken to list its ordinary shares on that Stock Exchange.

4.4 DAB BANK A.G. (“DAB”) AND KOEHLER & KRENZER FASHION A.G. As permitted under current German laws, UniCredit would apply for an exemption from the launching of a mandatory offer for DAB, a listed company, 76.4% of which is held by HVB (market value of Euro 451 million on 2 June 2005) and for Koehler and Krenzer Fashion A.G., a listed company, 49% of which is held by HVB (market value Euro 28 million on 2 June 2005), in light of the relatively negligible size of the aforementioned companies.

4.5 TECHNICAL ELEMENTS. UniCredit has given instructions to the transfer agent to manage the operational aspects of the offers. Should the offers prove successful, the transfer agent will be responsible to exchange the shares tendered in exchange of the newly-issued UniCredit shares, in case of exchange offers, or against cash, in case of cash offers. In addition, the agent will be responsible for the following activities: managing the accounts in which the tendered shares and in which the newly-issued UniCredit shares will be deposited; the accounting of the tendered shares and the notices to the Stock Exchanges and to the public of the acceptance levels.

With regard to the Bank Austria and BPH offers, the transfer agent will also be responsible for managing the share fractions.

4.6 OFFER CONDITIONS. Inter alia, the offers described above would be conditional upon the issuance of the necessary regulatory approvals by the competent Banking Supervisory and Stock Exchanges Authorities. It should be noted in this connection, that the Bank of Italy has already granted authorisation to the combination in pursuance of current legislative and regulatory provisions; similarly, the minutes of

11

today’s resolution on the capital increase and consequent amendments to the By-Laws, shall be submitted to the aforementioned Authority, pursuant to art. 56 of Legislative Decree 385/93.

Completion of the HVB offer would, in addition, be subject to the following conditions:

§ attainment of a minimum acceptance level of at least 65% of the HVB share capital. UniCredit intends, however, to reserve the right to accept the shares received, even in the event that they do not reach the aforementioned minimum level;

§ authorisation by the competent antitrust authorities for completion of the transaction. The transaction would be examined by the antitrust authority of the European Union, which could refer it back to the competent national authorities, and by the national authorities of the non-EU countries involved.

The effectiveness of the Bank Austria offer would also be conditional upon the successful completion of the HVB offer.

As far as the BPH offer is concerned, in accordance with local laws it cannot be conditional upon the outcome of the HVB offer; specific provisions have, therefore, been inserted in the BCA to the effect that, should such offer be unsuccessful, UniCredit and HVB will negotiate ways and conditions to enable UniCredit to monetize its holding in BPH, acquired on completion of the offer launched in Poland.

4.7 SUPPORT TO THE HVB OFFER. Given the friendly nature of the proposed combination, on the date of its announcement, the HVB management board expressed a favourable opinion on the transaction; furthermore, the management board has undertaken to recommend the offer for the HVB shares to its shareholders (within two weeks of the publication of the relevant document and in compliance with current local provisions) and to use its best efforts to ensuring that the supervisory board does the same. Likewise, within the limits of the administrative bodies’ fiduciary duties under local laws, the management board has undertaken, under the same terms, not to take any steps which could prevent the success of the offers launched by UniCredit nor to solicit any competing offers.

4.8 TIMELINE OF THE OFFERS. On the basis of the provisions of German take-over rules, and considering that the terms of the combination have been announced to the market on 12 June, it is expected that the HVB offer period would start on 23 August 2005 and end on 6 October 2005, with a possible two-week extension in case the minimum acceptance level is attained. Given the different provisions of law in force in Austria, UniCredit will have to submit the offer document to the competent authorities for approval, within 40 working days as of the first joint UniCredit/HVB announcement (30 May 2005) - which was required by the same Austrian authority - and, on the basis of the expected timing for granting the authorisation - estimated in approximately 2 weeks - launch the Bank Austria offer, presumably during the second week of August. Finally, the expected timing for the BPH offer will have to be discussed with the Polish authorities.

4.9 PLACES OF THE OFFERS. The HVB, Bank Austria and BPH offers would be addressed to all shareholders, excluding, however, USA, Canadian, Japanese and Australian residents; it is proposed, however, to apply to BaFin for authorisation to extend the HVB offer to qualified institutional investors (Q.I.B.s) in the USA. The HVB offer

12

would be launched only in Germany, the Bank Austria offer would be launched only in Austria, while the BPH offer would be launched in Poland only.

4.10 LISTING OF THE UNICREDIT SHARES. In order to maximise the success of the exchange offer for the HVB shares, making it more attractive to local investors, UniCredit has, under the terms of the BCA, undertaken to list its ordinary shares on the Frankfurt Stock Exchange upon completion of the offer.

In this connection, it should be noted that the Frankfurt Stock Exchange is divided into three markets, namely (i) the Official Market, (ii) the Regulated Market and (iii) the Unofficial Regulated Market. The three markets mainly differ in terms of initial admission requirements (e.g. minimum expected market capitalisation, minimum free float). These requirements are more restrictive in the case of the Official and Regulated Markets and less restrictive in that of the Unofficial Regulated Market. Furthermore, within the Official and Regulated Markets there are two separate segments: the so-called “Prime Standard” and the so-called “General Standard”. Once listed on one of the two, Official or Regulated, markets, a company automatically acquires the right to be listed on the “General Standard” segment, while admission to the “Prime Standard” segment may be obtained upon specific application to the authorities. The two segments differ in terms of reporting obligations to the market post admission (e.g. frequency of publication of financial data, frequency of meetings with financial analysts). Such obligations are more restrictive in the case of the “Prime Standard” and less so in the case of the “General Standard”. Therefore, companies listed on the “Prime Standard” of regulated markets typically address themselves to an international investor base and may be included in the major indices (e.g. DAX).

In accordance with the BCA, UniCredit has undertaken to obtain listing on the Official Market, without, however, assuming any specific undertaking with regard to the specific quotation segment (“Prime Standard” or “General Standard”) since admission to the “Prime Standard” must be decided upon by the relevant authorities. It should be noted, however, that, irrespective of the market segment, inclusion in the major indices (e.g. DAX) is reserved exclusively to companies having their registered office in Germany and, therefore, UniCredit could not, in any event, be included in one of the indices.

Furthermore, with regard to the BPH offer, it should be noted that as a precondition to enable local investors to hold UniCredit shares, UniCredit should also be listed on the Warsaw Stock Exchange. Consequently, UniCredit has also undertaken to list its ordinary shares on the Warsaw Stock Exchange. Finally, it is worth noting that, in the absence of an analogous requirement on the Austrian market, it is not contemplated to list the UniCredit shares on the Vienna Stock Exchange.

5. DETERMINATION OF THE VALUE OF UNICREDIT, HVB, BANK AUSTRIA AND BPH - THE EXCHANGE RATIOS

UniCredit internally carried out valuations on the capital of UniCredit and of the target banks based on of the most recent financial statements (31 December 2004 and 31 March 2005). The most suitable exchange ratios have been identified on the basis of the results obtained by using the various valuation methods selected. These exchange ratios have been confirmed by the advisors instructed to issue a fairness opinion.

13

For the purposes of the transaction under consideration, the economic value of both UniCredit and of the target companies was estimated on a standalone basis and without taking into account the possible effects which could derive from the wider industrial project. The values resulting from the various valuation methods must, therefore, be understood as aimed only at determining an exchange ratio deemed appropriate for the purposes of the aforementioned offers. Among the many valuation methods, widely accepted and applied to companies operating in the financial sector, the following main methods were selected:

- the Discounted Dividend Model (“DDM”) method

- the “Market Multiples” method

- the “Value Map” method

- the “Stock Exchange Quotations” method

Unlike UniCredit and HVB, in the case of Bank Austria and BPH, since it was impossible to verify the estimated projections on the basis of the analysts’ and advisers’ forecasts with the management of the respective companies, it was decided not to use the DDM method in view of the lack of consistent available data and the consequent lack of comparability with the application of the same method to UniCredit. Therefore, the remaining methods were used for the evaluation concerning Bank Austria and BPH.

Furthermore, considering that all banks being valued are listed, the value per share of the companies has been verified by comparing it with the analysts’ “Target Price” consensus on the pre-speculation share price. The market data included in all valuation methods are up-dated to 10 June 2005.

It should be pointed out that the value of UniCredit shares referred to below for each valuation method only refers to UniCredit ordinary shares. The aggregate value of UniCredit includes both the value of the ordinary shares and the value of the saving shares and UniCredit saving shares have different market values compared to ordinary shares (the average value over the last 6 months exceeded by 7.1% the value of ordinary shares). In light of these circumstances, it was deemed appropriate to weight the number of savings shares, calculating the number of “ordinary shares equivalent” to the savings shares on the basis of the different price between the two classes of shares. On the basis of the average trading values in the last 6 months, the number of “ordinary equivalent shares” amounts to 23,247,718, and therefore the total number of ordinary UniCredit shares has been raised from 6,333,373,477 to 6,356,621,195 for the purposes of the compared valuation. For valuation purposes, HVB’s and Bank Austria’s preference shares have been treated as ordinary shares from an economic point of view. Therefore, the value per share of HVB and Bank Austria has been calculated by dividing total values by the total number of the ordinary and saving shares, i.e. 750,699,140 shares in the case of HVB and 147,031,740 shares in that of Bank Austria.

As detailed below, it should be noticed that the range of exchange ratios determined in accordance with each valuation method was defined by identifying:

- as a minimum exchange ratio, the ratio between the min imum value per share of the target company and the maximum value per UniCredit share;

- as a maximum exchange ratio, the ratio between the maximum value per share of the target company and the minimum value per UniCredit share.

14

5.1 DUE DILIGENCE. In accordance with the BCA, UniCredit and HVB have reciprocally completed a limited due diligence exercise with a view to asses the accuracy of the valuations undertaken, with particular reference to the quality of the assets. The due diligence findings did not alter the opinion as to the validity of the strategic project and did not require any review of the valuations carried out.

5.2 THE RELATIVE EVALUATION OF UNICREDIT

The DDM Method

The financial method selected is based on a variant of the Discounted Cash Flow (DCF) method, namely the Discounted Dividend Model. This method involves the construction of a financial model based on the definition of expected profits through the construction of a Profit & Loss Account and a Balance Sheet over a 5-year period of the company to be valued. The estimates resulted in a projected increase of profits at a compounded annual growth rate of 10.6% over the period 2004-2009.

In particular, the DDM method estimates the value of the bank on the basis of maximum monetary flows which are directly attributable to the shareholders, taking into account minimum target capital ratios (6% Core Tier 1 Ratio).

Profit & Loss Account and Balance Sheet projections were estimated on the basis of 2004 accounts figures and the prospective development over the three-year period 2005-2007 indicated in the Group Plan; while in the case of subsequent years, up to 2009, growth forecasts were developed by taking into account, among other things, the Group’s business mix and the geographic operational area. The long-term profit growth rate “g” (i.e. beyond 2009) was set at 2%; the discount rate (cost of equity) was determined, on the basis of the Capital Asset Pricing Model theory, within a range of 9.10-9.55%

Market Multiples Method

The Market Multiples method assumes that the value of a bank is determined by taking as a reference the trading multiples of credit institutions whose characteristics are similar to those which are the subject of valuation (comparables). This method is based on parameters considered appropriate and more directly comparable between the banks in the selected sample. In order to find the most comparable parameter among the various companies to be valued, the net profit was selected resulting in the calculation of the P/E ratio (Price/Earning: price divided by the prospective net profit as at 2006). The P/E multiple, to be applied to the relevant net profit of the company to be valued, is universally accepted as a valuation parameter to analyse financial companies in general, and banks in particular.

The UniCredit comparables sample was selected on the basis of the principal Italian and international banking groups deemed to be comparable in terms of business mix, size, organisational structure, considering also the growing globalisation of markets as well as the significant portion of business conducted by the Group in foreign markets. Consequently, the sample includes the following banks: Banca Intesa, SanPaolo IMI, Montepaschi, Société Générale, Santander, BBVA, SEB and Danske.

The parameters used in the case of UniCredit are derived from the projection included in the Group Plan 2005-2007 drawn up by the management. In the case of the parameter used for the sample, the consensus of the financial analysts reported by FactSet was adopted. With reference to the time-scale for monitoring the share prices for the comparables, the figure

15

used was the average of the prices recorded at four different time periods: last day, 1 month, 3 months and 6 months before 10th June 2005.

The extremes of the valuation range obtained using the Market Multiples method were determined by the minimum and maximum results of the valuations from application of the P/E 2006 multiple on the basis of the above-mentioned time periods.

The Value Map method

The Value Map method values the economic capital of a bank on the basis of the statistical correlation between the prospective profitability (expected Return on Equity - ROE) and the existing ratio between market capitalisation and book value (expected P/BV).

Also in this case, as in the method described above, as far as the parameter for UniCredit are concerned, the Group Plan 2005-2007 was used, while in the case of the sample, the consensus of the financial analysts reported by FactSet was adopted. Furthermore, also in this case, with reference to the time period for monitoring the share prices for the comparables, the figure used was the average of the prices recorded at four different time periods: last day, 1 month, 3 months and 6 months before 10 June 2005.

The Value Map was developed by comparing the correlation between the P/BV 2005 and the ROE 2006, in order to value UniCredit prospective profitability in relation to the expected for the sample. Therefore, the extremes of the valuation range obtained using the Value Map method were determined by the minimum and maximum results of the valuations from application of the P/BV 2005/ROE 2006 multiple on the basis of the above-mentioned time periods.

A summary of the results of the application of the valuation methods used is given in the following tables:

UniCredit valuation 100% (Euro millions)

UniCredit valuation per share (Euros)

MIN MAX MIN MAX DDM 32,158 34,144 5.06 5.37 Market Multiples 29,294 30,428 4.61 4.79 Value Map 29,587 30,388 4.65 4.78 Market averages Last day 25,961 4.08 1 month 27,082 4.26 3 months 27,981 4.40 6 months 27,610 4.34 Last day before speculation 26,865 4.23 1 month before speculation 27,952 4.40 3 months before speculation 28,333 4.46 6 months before speculation 27,647 4.35 Analysts’ consensus 29,754 32,886 4.68 5.17

5.3 THE RELATIVE VALUATION OF HVB

The DDM method

16

For the application of this method the expected growth of HVB up to 2009 was estimated. The long-term growth rate “g” of net profits (beyond 2009) was quantified at 2%, while the cost of equity was determined in a range of 8.88-9.78%.

The Market Multiples method

In applying the Market Multiples method for the valuation of HVB the same assumptions were used as described earlier in the case of UniCredit. However, since the principal element which ensures the efficacy of the Market Multiples method consists of the affinity between the evaluated banks and those used for the definition of the multiples, given the diversity between UniCredit and HVB, it was considered appropriate to use comparative samples which were partially different in relation to UniCredit and took account of the differences in size and operations.

The comparables sample used in the case of HVB was selected in the context of a group of German and European banks which were comparable on the basis of performance, profitability, efficiency and relative size, within the domestic market, having characteristics as similar as possible to those of HVB and includes: Commerzbank, Postbank, Hypo Real Estate, Banca Intesa, Société Générale, Nordea and FSPA.

Unlike the UniCredit valuation, the parameters used in the case of HVB derive from internal estimates drawn up in collaboration with the advisors and verified in relation to the financial analysts’ projections and in conjunction with the HVB management, while the financial analysts’ consensus reported by FactSet was used for the sample.

The extremes of the valuation range obtained using the Market Multiples method were determined by the minimum and maximum figure of the valuations resulting from application of the P/E 2006 multiple on the basis of the time periods of the last day, 1 month, 3 months and 6 months before 10 June 2005.

The Value Map method

The assumptions described in the case of UniCredit were also used when applying the Value Map method, except that they were applied to the sample adopted for HVB in the context of the Market Multiples method. Therefore, the extremes of the valuation range obtained using the Value Map method were determined by the minimum and maximum results of the valuations from application of the P/BV 2005/ROE 2006 multiple on the basis of the time periods of the last day, 1 month, 3 months and 6 months before 10th June 2005.

A summary of the results of the application of the valuation methods used is given in the following tables:

UniCredit valuation

100% (Euro millions) HVB valuation 100%

(Euro)

MIN MAX MIN MAX

DDM 32,158 34,144 15,564 17,826 Market Multiples 29,294 30,428 14,757 15,408 Value Map 29,587 30,388 15,389 16,685 Market averages Last day 25,961 15,029 1 month 27,082 14,702 3 months 27,981 14,187

17

6 months 27,610 13,622 Last day before speculation 26,865 14,406 1 month before speculation 27,952 14,133 3 months before speculation 28,333 14,005 6 months before speculation 27,647 13,407 Analysts’ consensus 29,754 32,886 14,156 15,646

UniCredit valuation

per share (Euros) HVB valuation per

share (Euros) Exchange ratio

MIN MAX MIN MAX MIN MAX

DDM 5.06 5.37 20.73 23.75 3.86 4.69 Market Multiples 4.61 4.79 19.66 20.52 4.11 4.45 Value Map 4.65 4.78 20.50 22.23 4.29 4.78 Market averages Last day 4.08 20.02 4.90 1 month 4.26 19.58 4.60 3 months 4.40 18.90 4.29 6 months 4.34 18.15 4.18

Last day before speculation 4.23 19.19 4.54 1 month before speculation 4.40 18.83 4.28 3 months before speculation 4.46 18.66 4.19 6 months before speculation 4.35 17.86 4.11

Analysts’ consensus 4.68 5.17 18.86 20.84 3.65 4.45

Conclusions

In the light of the ranges of standalone exchange ratios, the exchange ratio based on the average UniCredit and HVB 3-month market prices (4.29 UniCredit shares for each HVB share) appears to be representative of the distribution of exchange ratios obtained by applying the different methodologies.

Given such an exchange ratio, it was considered appropriate to apply a premium (16.9% or 16.6% post dilution as a result of the recently implemented increases in capital) since the transaction envisages the acquisition of a controlling interest. Such premium, justified, from a strategic and economic standpoint, by the possibility of creating synergies resulting from the transaction, has led to an exchange ratio for the offer of 5.00 UniCredit shares for each HVB share.

5.4 RELATIVE VALUATION OF BANK AUSTRIA

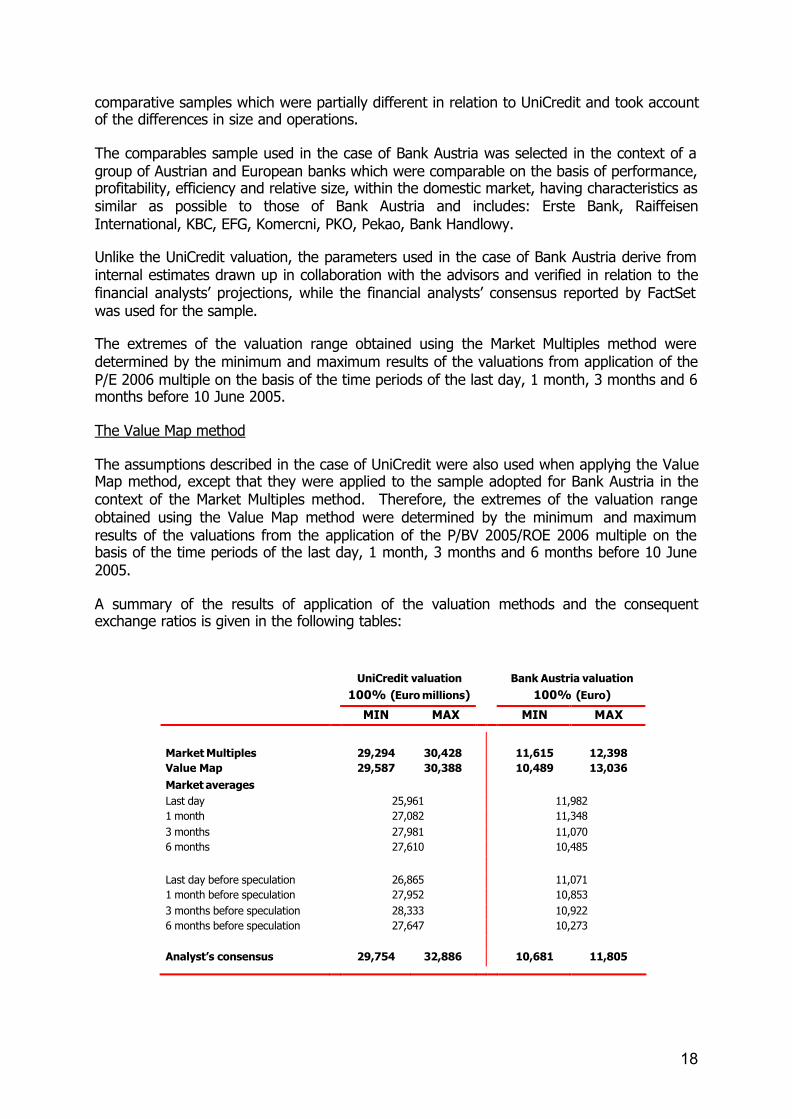

The Market Multiples method

In applying the Market Multiples method for the valuation of Bank Austria the same assumptions were used as described earlier in the case of UniCredit. However, since the principal element which ensures the efficacy of the Market Multiples method consists of the affinity between the evaluated banks and those used for the definition of the multiples, given the diversity between UniCredit and Bank Austria, it was considered appropriate to use

18

comparative samples which were partially different in relation to UniCredit and took account of the differences in size and operations.

The comparables sample used in the case of Bank Austria was selected in the context of a group of Austrian and European banks which were comparable on the basis of performance, profitability, efficiency and relative size, within the domestic market, having characteristics as similar as possible to those of Bank Austria and includes: Erste Bank, Raiffeisen International, KBC, EFG, Komercni, PKO, Pekao, Bank Handlowy.

Unlike the UniCredit valuation, the parameters used in the case of Bank Austria derive from internal estimates drawn up in collaboration with the advisors and verified in relation to the financial analysts’ projections, while the financial analysts’ consensus reported by FactSet was used for the sample.

The extremes of the valuation range obtained using the Market Multiples method were determined by the minimum and maximum results of the valuations from application of the P/E 2006 multiple on the basis of the time periods of the last day, 1 month, 3 months and 6 months before 10 June 2005.

The Value Map method

The assumptions described in the case of UniCredit were also used when applying the Value Map method, except that they were applied to the sample adopted for Bank Austria in the context of the Market Multiples method. Therefore, the extremes of the valuation range obtained using the Value Map method were determined by the minimum and maximum results of the valuations from the application of the P/BV 2005/ROE 2006 multiple on the basis of the time periods of the last day, 1 month, 3 months and 6 months before 10 June 2005.

A summary of the results of application of the valuation methods and the consequent exchange ratios is given in the following tables:

UniCredit valuation 100% (Euro millions)

Bank Austria valuation 100% (Euro)

MIN MAX MIN MAX

Market Multiples 29,294 30,428 11,615 12,398 Value Map 29,587 30,388 10,489 13,036

Market averages Last day 25,961 11,982 1 month 27,082 11,348 3 months 27,981 11,070 6 months 27,610 10,485

Last day before speculation 26,865 11,071 1 month before speculation 27,952 10,853 3 months before speculation 28,333 10,922 6 months before speculation 27,647 10,273 Analyst’s consensus 29,754 32,886 10,681 11,805

19

UniCredit valuation per share (Euro)

Bank Austria valuation per share

(Euro)

Exchange Ratio

MIN MAX MIN MAX MIN MAX Market Multiples 4.61 4.79 79.00 84.32 16.50 18.30 Value Map 4.65 4.78 71.34 88.66 14.92 19.05 Market averages Last day 4.08 81.49 19.95 1 month 4.26 77.18 18.12 3 months 4.40 75.29 17.10 6 months 4.34 71.31 16.42 Last day before speculation 4.23 75.29 17.82 1 month before speculation 4.40 73.81 16.79 3 months before speculation 4.46 74.28 16.67 6 months before speculation 4.35 69.87 16.07 Analysts' Consensus 4.68 5.17 72.64 80.29 14.04 17.15

Conclusions

In order to guarantee equal treatment for Bank Austria minority shareholders with respect to HVB, the same premium applied to the HVB offer (16.9% or 16.6% after dilution due to the impact of recently implemented capital increases) was applied to the exchange ratio based on the three month average market prices of UniCredit and Bank Austria (17.10 UniCredit shares per each Bank Austria share), which appears to be representative of the distribution of exchange ratios determined by applying the various methodologies. The application of such premium, which is justified by the existence of synergies directly attributable to Bank Austria as a result of the transaction, has led to identifying an exchange ratio for the offer of 19.92 UniCredit shares for each Bank Austria share.

5.5 THE RELATED VALUATION OF BPH

The Market Multiples method

In applying the Market Multiples method for the valuation of BPH, the same assumptions were used as described earlier in the case of UniCredit. However, since the principal element which ensures the efficacy of the Market Multiples method consists of the affinity between the evaluated banks and those used for the definition of the multiples, given the diversity between UniCredit and BPH, it was considered appropriate to use comparative samples which were partially different in relation to UniCredit and took account of the differences in size and operations.

The comparables sample used for BPH was selected from a group of Polish and European banks which are comparable on the basis of performance, profitability, efficiency, and relative size within the domestic market, having characteristics as similar as possible to those of BPH, and includes: PKO, Bank Pekao, Bank Zachodni, and Bank Handlowy.

Unlike the UniCredit valuation, the parameters used in the case of BPH derive from internal estimates drawn up in collaboration with the advisors and verified in relation to

20

the financial analysts’ projections, while the financial analysts’ consensus reported by FactSet was used for the sample.

The extremes of the valuation range obtained using the Market Multiples method were determined by the minimum and maximum results of the valuations from application of the P/E 2006 multiple on the basis of the time periods of the last day, 1 month, 3 months and 6 months before 10 June 2005.

The Value Map method

The assumptions described in the case of UniCredit were also used when applying the Value Map method, except that they were applied to the sample adopted for BPH in the context of the Market Multiples method. Therefore, the extremes of the valuation range obtained using the Value Map method were determined by the minimum and maximum results of the valuations from the application of the P/BV 2005/ROE 2006 multiple on the basis of the time periods of the last day, 1 month, 3 months and 6 months before 10 June 2005.

A summary of the results of the application of the valuation methods and the resulting exchange ratios are set forth in the following tables:

UniCredit 100% Valuation (Euro mln)

BPH 100% Valuation (Euro mln)

MIN MAX MIN MAX

Market Multiples 29,294 30,428 3,614 3,870 Value Map 29,587 30,388 3,654 3,837 Market averages Last day 25,961 4,004 1 month 27,082 3,644 3 months 27,981 3,545 6 months 27,610 3,552 Last day before speculation 26,865 3,369 1 month before speculation 27,952 3,361 3 months before speculation 28,333 3,447 6 months before speculation 27,647 3,424 Analysts' Consensus 29,754 32,886 3,248 3,590

UniCredit valuation per share (Euro)

BPH valuation per share (Euro)

Exchange Ratio

MIN MAX MIN MAX MIN MAX

Market Multiples 4.61 4.79 125.86 134.78 26.29 29.25 Value Map 4.65 4.78 127.26 133.61 26.62 28.70 Market averages Last day 4.08 139.44 34.14 1 month 4.26 126.90 29.79 3 months 4.40 123.46 28.05 6 months 4.34 123.70 28.48

21

Last day before speculation 4.23 117.32 27.76 1 month before speculation 4.40 117.05 26.62 3 months before speculation 4.46 120.03 26.93 6 months before speculation 4.35 119.25 27.42 Analysts' Consensus 4.68 5.17 113.11 125.01 21.86 26.71

Conclusions

In order to guarantee equal treatment for BPH minority shareholders with respect to HVB, the same premium applied to the HVB offer (16.9% or 16.6% after dilution due to the impact of recently implemented capital increases) was applied to the exchange ratio based on the six month average market prices of UniCredit and BPH (28.48 UniCredit shares per each BPH share), which appears to be representative of the distribution of exchange ratios determined by applying the various methodologies. The application of such premium, which is justified by the existence of synergies directly attributable to BPH as a result of the transaction, has led to identifying an exchange ratio for the offer of 33.13 UniCredit shares for each BPH share.

5.6 TOTAL COUNTERVALUE OF THE OFFERS. On the basis of market prices as of 10 June 2005 and the €/PLN exchange rate on the same date, and assuming complete success for the exchange offers with respect to HVB, Bank Austria, and BPH, and assuming furthermore that the Bank Austria and BPH shares held by HVB and Bank Austria, respectively, are not tendered, the total countervalue would be € 19.2 billion.

5.7 EVALUATION PURSUANT TO ARTICLE 2343 OF THE CIVIL CODE, REPORT ON THE ISSUE PRICE PURSUANT TO ARTICLE 2441 OF THE CIVIL CODE AND ARTICLE 158 OF LEGISLATIVE DECREE 58/98. The audit firm issued an opinion as to the appropriateness of the exchange ratios determined hereinabove, in compliance with Article 2441 of the civil code and Article 158, paragraph one, of Legislative Decree 58/1998.

The expert appointed by the Genoa Court in compliance with Article 2343 of the civil code at the request of UniCredit, on the other hand, has prepared his own sworn statement regarding the shares to be transferred that are the subject of the offers.

Both documents were deposited at the UniCredit’s registered office and the market management company, together with the information document prepared in compliance with Article 70 of the Issuers Regulation adopted by CONSOB with Resolution no. 11971/99, as amended.

6. UNICREDIT CAPITAL INCREASE

On the basis of the foregoing, the capital increase that is the subject matter of our proposal must be in such an amount as to enable the exchange of the shares tendered with regard to the HVB, Bank Austria and BPH offers, on the basis of the aforementioned exchange ratios without, however, including the Bank Austria shares held by HVB and the BPH shares held by Bank Austria, which cannot in any case be exchanged for UniCredit shares.

Therefore, the proposal that we are submitting to you refers to an overall maximum increase in capital stock of € 2,343,642,931.00 by issuing up to 4,687,285,862 ordinary shares with regular dividend rights, under the terms set forth in the following schedule:

22

Total N° of shares

N° shares to be exchanged

Exchange Ratio

Maximum N° UniCredit shares to be issued

HVB 750,699,140 750,699,140 5.00 3,753,495,700 Bank Austria 147,031,740 33,041,840 19.92 658,193,453 BPH 28,716,230 8,318,645 33.13 275,596,709 Total 4,687,285,862

The total price of the issue would be determined on the basis of the consideration for the acquisition of HVB and the minority stakes in Bank Austria and BPH, calculated on the basis of the exchange ratios multiplied by the UniCredit share price as of 10 June 2005. The total price of the proposed capital increase issue would therefore be € 19,194,435,604.89, which represents the valuation attributed to the transaction by the market. Given the maximum number of UniCredit shares to be issued – which, as indicated hereinabove, is 4,687,285,862 - the unit price of the issue would be € 4.095, € 0.50 of which is the nominal value and € 3.595 the share premium.

Finally, we would like to inform you that, as of the date this Report, UniCredit's fully subscribed and paid-in capital was € 3,169,025,381.50, divided into 6,338,050,763 shares with a value of € 0.50 each, 6,316,344,211 of which are ordinary shares and 21,706,552 of which are saving shares. Moreover, on 2 May 2005 UniCredit’s extraordinary shareholders meeting resolved upon a capital increase of up to € 22,490, by issuing a maximum of 44,980 ordinary shares for the merger of Banca dell’Umbria 1462 and Cassa di Risparmio Carpi, that we expect to be effective on 1 July 2005.

In addition, on 12 June 2005, the UniCredit Board of Directors decided upon a free capital increase, in compliance with articles 2349 and 2443 of the Civil Code, in the total amount of € 8,492,143, by issuing 16,984,286 ordinary shares to be allocated to all Group employees in implementation of the incentives plan adopted last year. Because it is estimated that this capital increase shall be effective on the date of the illustration of this proposal to the shareholders meeting, on that date the subscribed and paid-in UniCredit capital shall amount to € 3,177,540,014.50, divided into 6,355,080,029 shares with a value of € 0.50 each, 6,333,373,477 of which are common shares and 21,706,552 are saving shares.

7. IMPACTS ON THE UNICREDIT SHAREHOLDER BASE AND ON SHAREHOLDER AGREEMENTS (IF ANY) UNDER ARTICLE 122 OF LEGISLATIVE DECREE 58/98

In light of the foregoing, the issuance of UniCredit ordinary shares for the exchange offers illustrated in this Report would entail a dilution of the holdings held by current UniCredit shareholders of approximately 42.5%.

The shareholder structure of the holding, in the event of full acceptance of the exchange offers and assuming that Munich Re sells 50% of its holding on the market, would change as indicated in the following table:

23

Market 74.1%

Bayerische Landesstiftung

0.7%

AVZ 1.5%

Capital Group 1.7%

Munich Re 3.1%

Aviva 1.5%

Allianz 2.8%

Fondazione Cassamarca 1.2% Fondazione Carimonte 4.0% Fondazione Cariverona

4.3%

Fondazione CRT 5.0%

We are not aware of any shareholder agreement relating to UniCredit shares, with the exception of the shareholders’ agreement entered into by the Credit Institution Management Personnel Union Organizations "Uniosind" and "Sinfub", which have as members – according to the information available to UniCredit – 394 shareholders who are employees of the UniCredito Italiano Group who hold a total of 903,134 ordinary shares in the Company, which represents 0.014% of the ordinary capital, for which the members have not communicated any consequences deriving from the capital increase.

8. ORGANIZATIONAL MODEL OF THE GROUP RESULTING FROM THE COMBINATION – STRUCTURE OF THE GROUP TO BE IMPLEMENTED

8.1 ORGANIZATIONAL MODEL OF THE GROUP RESULTING FROM THE COMBINATION. As anticipated, the BCA sets out, inter alia, the organizational model for the new Group, which contemplates a divisionalised structure focused on customer segments, and the creation of common product factories. The focus on customer segments would facilitate the integration of operations in the various markets, thereby enabling the creation of significant synergies, especially in global businesses (asset management, investment banking, private banking, corporate).

In the past, the UniCredit and the HVB Groups displayed distinctive expertise in the retail, private and asset management and operations segments and in the corporate and investment banking segments, which provides the prospect of strong complementarity in the management and operation of the combined Group. It has therefore been agreed with the HVB management that the combined Group shall be based upon the following divisions:

- Retail;

- Private Banking and Asset Management;

- Corporate/SMEs;

- Multinationals/Investment Banking;

24

- Global Banking Services;

- Central Eastern Europe.

To favour integration and the generation of synergies among the various Divisions, the new Group would maintain a clear separation between distribution activities - allocated to commercial banking institutions - and the product factories, responsible for product development of specialized services to be distributed through the Group banking own networks and third parties’ networks. The product factories could either be in the form of separate legal entities or of organizational units.

In addition, the new Group's ability to meet the potentially different requirements of clients in the major markets where it has a presence (Italy, Germany, Austria), particularly in the retail segment, would be ensured by the continued presence of separate banking institutions in individual markets. The three Italian banks in the segment would therefore be joined by a German bank and an Austrian bank, preserving the multinational character of the group and promoting institutional relationships as well as relationships with regulatory authorities in the individual countries. It is expected that increased future intra-Group integration would enable to align the legal structure of the banks in Germany and Austria with the organizational structure by segment, by "exporting" the S3 Project.

The Global Banking Services Division would retain responsibility for improving the cost structure and internal processes of the combined Group, by providing services to the other divisions in the area of human resources, IT services, organization, back-office, transaction services (payment settlement), intra-group property management. The role of the Global Banking Services division would therefore be key to the integration of the new Group and the generation of some of the synergies identified.

Given the different degree of development of the relevant markets, the CEE division would retain its own independence from other Group divisions. Such division would be responsible for management of activities in all CEE markets where the Group has a presence, including Russia, the Baltic countries and Turkey, as well as for further expansion of the Group in the region. The banks operating in the various countries in the region would nevertheless continue in the process of divitionalising their activities on the basis of customer segments, so as to ensure uniform management of operations on a regional basis and enable the generation of synergies among the various markets. As the larger and more advanced markets, such as Poland, come closer to the standards of markets which are historically part of the European Union, it is anticipated that the operations in such markets will be transferred to the respons ibility of segment divisions.

With the establishment of the new UniCredit Group, the holding company would be responsible for management of operations of significant size in numerous markets, including those with different features. To ensure a uniform management of operations, a reorganization of the activities of the holding company staff - on the basis of a limited number reporting lines to the Managing Director - is envisaged. The management structure to be implemented would be based on the "professional family" concept, which provides a direct reporting relationship among corresponding organizational functions belonging to the various companies in the Group.

8.2 GROUP STRUCTURE TO BE IMPLEMENTED. In the event that the HVB, Bank Austria, and BPH offers are successful, the structure of the combined Group immediately after completion of the offer would be relatively complex, entailing an indirect chain of control on the

25

business activities of HVB. UniCredit would in fact assume direct control of HVB, which in turn would control Bank Austria, which would control the CEE banks. Various companies controlled by UniCredit, HVB, and Bank Austria would perform product factories functions in the various markets. In order to ensure an efficient structure for the new Group, we believe that the main banking institutions of the Group should be directly controlled by UniCredit. The "target" structure of the Group therefore provides that UniCredit will directly retain direct control, not only of HVB, but also of Bank Austria as well as the product factories. With regard to asset management activities, the current operations of HVB and Bank Austria should be controlled by PGAM. Banks in the CEE should also be directly controlled by UniCredit and combined into a single company in the respective markets. If tax and capital efficient, it is envisaged that a sub-holding company controlled by UniCredit will be established, which will retain control on CEE activities.

9. GROUP GOVERNANCE

To further illustrate the main elements of the agreed combination between UniCredit and HVB, the principles for the governance of the Group set out under the BCA are described below.

9.1 STRUCTURE AND COMPOSITION OF BOARD OF DIRECTORS OF UNICREDIT. Firstly, a new Board of Directors will appointed, so that eight HVB nominees indicated in the BCA will become Board members, representing one third of the members of the Board of Directors. To this end, we are proposing in the context of today's shareholders meeting an amendment to the By-Laws of the company to provide for a maximum number of 24 members of the Board of Directors. It was agreed in the BCA that, on the date of the approval of this proposal by the shareholder meeting, the current UniCredit directors would resign, conditional upon and with effect as of the completion of HVB offer.

Finally, the aforementioned appointment of all the members of the Board of Directors for a three year term will be proposed in the context of an ordinary shareholders meeting that the Board of Directors is required to convene immediately upon completion of the HVB offer.

In the context of a Board meeting to be held immediately upon its renewal the Board will appoint Mr. Dieter Rampl as Chairman of UniCredit. In line with UniCredit’s structure and consistent with the instructions by the Regulatory Authority, the Chairman would have a non-executive role, and, within that framework, he would specifically be entitled to:

- propose to the shareholders meeting – or to the Board of Directors, in case of co-optation – a candidate director should the number of directors be increased or in case of early termination (for whatever reason) of one of the directors designated by HVB, so that for the entire term of the agreement the aforementioned one-third representation will be assured;

- propose one third of the directors for a second term;