ey life sciences sector update asia-pacific and japan | april 2016

TRANSCRIPT

EY Life Sciences Sector UpdateAsia-Pacific and Japan

April 2016

2 | EY Life Sciences Sector Update Asia-Pacific and Japan | April 2016

Contents

04 a insi s Asia-Pacific and Japan

12 Featured articles 12 To combat pricing challenges, biopharmas need

new models 14 Optimizing supply chain effectiveness in Asia

with trade analytics

18 Mergers and acquisitions (M&A)

22 Financing and IPOs

28 Appendix 28 EY thought leadership 30 Contacts

3EY Life Sciences Sector Update Asia-Pacific and Japan | April 2016 |

T o o u r c lie n t s a n d f rie n d s :

c fi s di i n EY Life Sciences Sector Update Asia-Pacific and Japan.

During the past year we have had the pleasure of spending considerable time connecting with clients and companies throughout Asia. Feedback about our annual reports, Beyond borders and Pulse of the industry, is very positive. But it’s also clear the community is hungry for more detailed analysis of how these life sciences trends play out in the dynamic Asian market.

a d n n a in Asia-Pacific i n is apid c an J s staying abreast of sector developments can be tough. We understand the need for frequent in-depth analysis presented in an easy-to-digest format. We hope the EY Life Sciences Sector Update fi s n ds n is iss add ss a di s a a topics you’ve signaled are of interest. The information is presented in an easy-to-read format, and we hope this report strikes the right balance between “detailed analysis” and “digestible content.”

fi s s c i n d c n M ark et insig h ts, highlights a number of sector trends and provides brief yet informative updates on various regulatory and legislative trends for a number of key markets in Asia. Our M erg ers and acq u isitions and F inancing and I P O s sections provide helpful summaries of recent global and local trends via charts and short captions.

In addition, we’re also very excited to include two featured articles, both written sp cifica is p ica i n

fi s a ic a d s ad Ana s i ci nc s n ic in examines the implications of ongoing concerns about high drug prices. In addition to outlining the pressures many pharmas face, Ellen discusses how stakeholders in Asia are addressing the issue.

s c nd a ic c a d s a ad ad Ana ics a c nc and s Asia-Pacific i ci nc s a ad ic n in s c pani s can s da a ana ics ac i si nifican s pp c ain n fi s and in in

a and Asian a p ac c a s in financ a and p a i ns we strongly urge you to read this article and think about how it may apply to your organization.

p n is fi s iss find is a pda and c a n di i a i a i ns and can n a i s ia i i ci nc s ai c n s a c i ica as c n in fin is p

to improve its overall value.

R ick F onte P atrick F l och elAsia-Pacific i ci nc s a ad a P a ac ica c ad

4 | EY Life Sciences Sector Update Asia-Pacific and Japan | April 2016

Market insights: Asia-Pacific and Japan

I n t h is e d it io n , w e h ig h lig h t k e y s e c t o r, re g u la t o ry a n d le g is la t iv e t re n d s f o r t h e f o llo w in g m a rk e t s :

AS E AN• Malaysia

• Indonesia

• Vietnam

• Thailand

• in ap

Au s t ra lia

C h in a

I n d ia

J a pa n

S o u t h K o re a

5EY Life Sciences Sector Update Asia-Pacific and Japan | April 2016 |

K e y h ig h lig h t s• India and China have introduced initiatives to strengthen

domestic manufacturing. The Indian government has prioritized a “Make in India” campaign aimed at bulk drugs and medical devices. In China, biopharma and advanced medical devices have been positioned as the priority sectors under the government’s Made in China 2025 plan. Meanwhile, 12 countries, including Japan,

a a sia in ap and i na a si n d ans-Pacific Pa n s ip is pac i p i p p potential of these countries by reducing import barriers.

• The government bodies continue to promote local innovation, primarily through increased funding support. For example, the Australian government has recently ann nc d p ans in s i i n in a i dica research fund to help commercialize breakthrough discoveries. Japan has also undertaken several measures to boost innovative research. This includes a special premium for innovative drugs and setting up funding a nci s a p in p a ac ica s and medical devices.

• Curbing health care expenditures, in particular drug prices, is another pivotal area for many nations in the Asia-Pacific i n ina and ndia a isi d their pricing policies to impose stricter controls. Japan, meanwhile, has been the most aggressive in its reforms, announcing its decision to impose direct price controls on “high-selling” drugs. At the same time, the country has set ambitious targets for increasing generic drug utilization. Other geographies such as India and China have revisited their pricing policies to impose stricter controls.

• a is an a a c s in is region. China, India and Japan have undertaken reforms designed to maintain quality and safety standards while streamlining drug approvals.

• Identifying new growth opportunities is another theme. sp cific s a ad p d is i d p nd n n

given market, but across the region, executives in Asia-Pacific a p i n in i n p s i sci nc s businesses. These include medical marijuana (Australia),

a a -c ifi d d s a a a sia n in pharmacies (India), stem-cell therapy (Indonesia) and

i si i a s a

AS E AN M a la y s ia : F o c u s o n in c re a s in g t h e e x po rt c a pa b ilit ie s o f t h e in d u s t ry

The signing of the Trans-Pacific Partnership (TPP) has put Malaysia in sp i ca a is a i n i s inn a c pani s an additional period of data exclusivity for patented products when there are regulatory delays. This statute has angered patient advocates in Malaysia who believe the law will delay access to affordable generics. The government, meanwhile, argues it can use compulsory licensing to make sure patients have access to needed medicines.

inc i d c s ad a i s PP s d n fi p s both drugs and medical devices.1 In particular, the pact will encourage the l ocal produ ction of m edical dev ices, especially higher-value technologies. Malaysia, striving to become the regional export hub for medtech, has recently approved 11 medical technology projects with an in s n an i i n 2

i a a a sia a s an s c a ad in h al al dru g m anu factu ring . As of August 2015, the country had nearly

a a -c ifi d p a ac ica an ac s 3 However, lack of formal guidelines is acting as an impediment for the players operating in is fi d 4

Important recent reg u l atory sh ifts include new medtech guidelines related to mandatory incident reporting, device labeling and harmonization with foreign regulatory assessments. In addition, the

inis a is s d in ficac d s fi s ic ns d accin d n an fi s n a ia 5, 6

I n d o n e s ia : C o pin g w it h t h e in c re a s e d d e m a n d t h ro u g h d o m e s t ic m a n u f a c t u rin g

Indonesia’s universal health care plan has spurred demand for pharmaceuticals and medical devices. However, the shortage of locally manufactured drugs, along with rising import costs, hampers the progress of this plan.7 Consequently, the government is planning to introduce economic stimulus packages to streng th en dom estic produ ction, especially of raw materials. In addition, the government is contemplating relaxing foreign ownership laws.8 Meanwhile, domestic companies in Indonesia continue to boost their manufacturing capacity to keep pace with the increasing demand.

Building a sustainable health system has become a priority as the country implements its universal health care programs. To rein in escal ating costs, the government has proposed a co-payment initiative that will allow the private insurers to supplement the universal health care policy.9

The Indonesian government intends to participate in the T P P .10 As in Malaysia, Indonesia’s pro-TPP stance has resulted in protests about possible delayed access to generics.

On the innovation front, Indonesia is making progress in stem - cel l research s and anc ns i i ini ia p c inica ia for allogeneic stem cells (cells that come from another person) for treatment of osteoarthritis sometime later in 2016.11

a insi s Asia-Pacific and Japan

6 | EY Life Sciences Sector Update Asia-Pacific and Japan | April 2016

V ie t n a m : E m ph a s is o n im m u n iz a t io n a m id in c re a s in g q u a lit y c o n c e rn s

Vietnam has stepped up its efforts to strengthen its ex tended prog ram on im m u niz ation, which expands pediatric coverage and enhances quality of inoculations.12 This is expected to offer greater opportunities to both foreign and domestic manufacturers with high-quality vaccines.

On the reg u l atory front, the ministry of health has launched an online drug registration service to ease administrative procedures, while tightening drug quality standards.13, 14 In addition, the government is developing a draft decree to more strictly manage medical devices.15

T h a ila n d : M o v in g t o w a rd d ire c t pric e c o n t ro ls a n d t a c k lin g t h e g ro w in g pro t e s t s o n T P P

The country is attempting to fix nonuniform pharmaceutical pricing in public and private hospitals.16 One solution for this includes the government’s proposal to include drug pricing within the approval framework for patented drugs, introduced as part of Thailand’s drugs bill. This will require innovator companies to submit their pricing structures as part of the registration process. In another move, Thailand’s Internal Trade Department, Public Health Ministry and the Food and Drug Administration (FDA) have mandated the display of drug prices on the packaging to stop private hospitals from overcharging patients. These moves are being strongly opposed

a i s pa i s inc din p i ica fi s p i a spi a s and multinational pharma companies. These bodies argue that the different cost structures of private and public hospitals justify the differential pricing and that bureaucracy may increase if pricing details are included in the approval process.17

From an intellectual property aspect, Thailand’s signing of the T P P is worrying a large faction of the local industry and consumer groups. The clause of “data exclusivity” (DE) after patent protection is the biggest challenge that the local industry has cited. DE will allow the innovator companies to extend its exclusivity period and thus hamper the growth of local generics players and result in increased drug prices.18 It may also limit the country’s ability to issue compulsory licenses.19

In the b iotech indu stry , the focus is on developing hubs in the country. Currently, a panel of members is creating a national strategy for biotech and to attract investments into the sector.20

S in g a po re : P ro v id in g f u n d in g s u ppo rt t o n u rt u re n o v e l s t a rt - u ps

in ap is c s d n b ol stering its R & D ex pertise. One of the key areas here is indigenous drug development of novel biologics. Working

i ni si in ap s A nc ci nc c n and s a c A A as disc d i s fi s c inica candida ETC-159, an anti-cancer agent.21 in ap is a s inc asin ndin

ans a i na dicin ia a i na s a c nda i n in ap n n as a ca d i i n

n fi a s ad anc acad ic s a c in c cia setting.22 Most of the funds will go to collaborative laboratories that conduct research; funds will also be used to train scientists.23

in ap as a s ad a in s n s sp its domestic medtech industry.24 EDBI, the corporate investment a in ap c n ic p n a d as in s d an undisclosed sum in Massachusetts-based life science tools company

apid ic i s s s n an ini ia i n accelerator JFDI has partnered with Germany’s Medical Innovations Incubator to augment medical technology start-ups. Both of these initiatives are expected to result in technology transfer and job-c a i n pp ni i s in in ap

in ap is a s in s in in di i a a pp ni i s as joined forces with Philips to jointly invest in digital health companies that are working on population health management tools for the Asian market.25 Meanwhile, the pan-Asian insurance group AIA and Japan s c i d nica in a a d a n in ap -based incubator for digital health companies.26

a insi s Asia-Pacific and Japan

7EY Life Sciences Sector Update Asia-Pacific and Japan | April 2016 |

Au s t ra lia R e f o rm s t o f u e l in d u s t ry g ro w t h a n d im pro v e a c c e s s ib ilit y a ppe a r t o b e t h e g o v e rn m e n t ’ s n e a r- t e rm a g e n d a .

After several rounds of negotiations over 10 years, the Trans-Pacific P artnersh ip ( T P P ) as fina i d in c s a is s a preferential trade zone among 12 member countries: Australia, Brunei, Canada, Chile, Japan, Malaysia, Mexico, New Zealand, Peru,

in ap and i na 27 The trade pact is a victory for the A s a ian n n as i s s fi - a pa n p c i n term for biologics, with a provision for extending this period.28 At the same time, the deal paves the way for increasing exports. Note that changes in import tariffs used to protect the interests of the local companies might negatively impact the domestic industry.29

Australia is taking strides to improve its R & D env ironm ent. The na i n as id n ifi d i c n as a p n ia opportunity. The government has recently announced plans to invest

i i n in a i dica s a c nd p c cia i breakthrough discoveries.30 The Biomedical Translation Fund is

p c d c p a i na in i i a p i a in s s a s p a dica s a c cia isa i n nd

i i n 31

To improve patient access to medicines, the Australian government as a a d i i n in s sidi s h epatitis C dru g s such

as a di i ad a ni i ad a in a is - s i and Ibavyr (Pendopharm).32 As a result of these subsidies, which are

c i a c a n c s s c d a s A s A s pa i n s c n s

P a ac ica n fi s c P 33, 34 To create budget to cover the hepatitis C medicines, the federal government has removed

n np sc ip i n d s P a ac ica n fi s c a step that is forecasted to save roughly half a billion Australian d a s n fi a s 35

M edical m arij u ana is also emerging as a new opportunity for Australian life sciences companies. In October 2015, the federal government lifted its ban on growing cannabis for medical purposes and is currently amending its Narcotics Drugs Act.36 The government also plans to establish a body for regulating cultivation and importation of the drug.37 ic ia is s c fi s s a to legalize marijuana cultivation, with other states also expected to follow this path.

a insi s Asia-Pacific and Japan

8 | EY Life Sciences Sector Update Asia-Pacific and Japan | April 2016

C h in aT h e C h in e s e lif e s c ie n c e s in d u s t ry is in t h e m id d le o f m a j o r h e a lt h c a re re f o rm s . S t re a m lin in g t h e re g u la t o ry e n v iro n m e n t , im pro v in g q u a lit y , c u rb in g h e a lt h c a re c o s t s a n d b o o s t in g t h e d o m e s t ic in d u s t ry a re t h e k e y d riv e rs o f t h e s e re f o rm s .

The China Food and Drug Administration (CFDA) has instituted several initiatives designed to expedite the drug approval process. The integral aspects of the reforms include:

• i p i in app a c inica ia s

• Allowing simultaneous country clinical studies by multinational corporations

• Expanding the fast-track approval to many new categories of drugs (e.g., pediatric/geriatric drugs, drugs treating China-prevalent diseases and internationally innovative drugs)

These efforts are designed to reduce the drug approval time frame from 6–8 years to 2–3 years. By 2016, the CFDA aims to eliminate the current backlog of 18,000 drug applications.38

I m prov ing th e q u al ity of its products is another goal of CFDA. Manufacturers bear greater responsibility for submitting review applications and must verify clinical trial data. Violations carry strict penalties, including a potential three-year delay in a drug application.39 Generics that meet international standards will also be prioritized.40

P ricing reform s are another priority in China as the government aims to reduce overall health care costs. Provincial tenders now occur annually, and the CFDA’s role is limited to monitoring — not setting — prices.41 These changes create an opportunity for pharma to interact directly with hospitals, empowering local health systems to negotiate pricing.42

At the local level, provincial governments are working to redu ce th e contrib u tion of dru g sal es to h ospital s’ rev enu e. As part of this initiative, they have already implemented a zero markup policy on drug sales for the hospitals in 100 major cities.43 These reforms separate drug prescription and dispensation while increasing medical service fees to compensate for lost drug sales.

These reforms are designed to promote th e dom estic indu stry . The government is encouraging local innovation by launching a three-year pilot program, the Marketing Authorization Holder (MAH) system, across 10 provinces.44 nd A a d s ic ins i i ns and s a c p s nn in s na i na i can a s fi drugs for approval. Apart from MAH, the government has deemed biopharmaceutical and medical device manufacturing as high priority products for its “Made in China 2025” initiative.45 To further boost the domestic industry, authorities are also offering incentives for hospitals to use domestically produced medical devices.46

Apart from these reforms, increasing h eal th insu rance cov erag e continues to be a priority in China. In August 2015, the country released guidelines on full implementation of critical illness insurance. Through its expansion, the government aims to improve affordability by reducing the out-of-pocket ratio from 34% in 2014 to less than 30% by the end of 2017.47

a insi s Asia-Pacific and Japan

9EY Life Sciences Sector Update Asia-Pacific and Japan | April 2016 |

I n d iaAn in c re a s in g f o c u s o n “ M a k e in I n d ia ” a n d g ro w t h o f o n lin e s a le s a re s h a pin g t h e d y n a m ic s o f t h e in d u s t ry .

With the Make in India campaign, the country aims to streng th en its dom estic capab il ities of m anu factu ring of active pharmaceutical ingredients (APIs) and medical devices. After convening a task force,

a c i ndia c a d s ai d a p in API manufacturing, simplifying foreign investment, awarding tax

n fi s and s in ind s -acad ia a i ns ips 48

n d c n n n is i din i s fi s d dica d industrial park in Andhra Pradesh. In a separate effort, the Department of Industrial Policy and Promotion and the Ministry

c p ais a as i i n in di c i n investment for medical devices. To streamline device creation and approval, the government has also prioritized creating medtech-sp cific a i ns 49

As India puts reforms in place to encourage manufacturing capabilities, it is also focused on enh ancing th e credib il ity of its ex ported produ cts. For instance, it has created a trace-and-track system for exported drug formulations.50 All drugs manufactured by non-small-scale industry will need to adhere to this system by 1 April 2016. To strengthen quality control, India’s Central Drugs

anda d n ani a i n p ans s p a n a s in a a and i d fic s in a s a s ns p p

implementation of regulations.51 is a s c i in addi i na drug inspectors to perform quality checks. On the post-market front, the government is setting up new adverse drug reaction monitoring centers under the Pharmacovigilance Program of India (launched in early 2015).52

I m prov ing affordab il ity continues to be a key requirement in India. The country is extending the pricing controls used for pharmaceuticals to imported medical devices such as cardiac stents, pacemakers and implants.53 The central government also plans to expand the Jan Aushadhi program, which provides unbranded generic versions of 439 life-saving medicines and 250 medical devices at lower prices through Jan Aushadhi stores.54 It has also formed a public-private task force to ensure universal access to quality health care by 2030.55

On the b iotech front, the government has released its National i c n p n a s a is ndia

as a d-c ass i - an ac in and is isin i s biosimilar guidelines.56, 57

A s in oth er cou ntries, sy stem s to sim pl ify th e reg u l atory approv al process are al so u nderw ay as in d c d an - na d system to speed drug approval applications and improve clinical trial monitoring.58 The union health ministry has abolished conducting repeat preclinical or toxicity studies on animals if similar data from another country have been submitted.59

The rise of onl ine m edicine sal es is yet another area garnering a lot of attention. While the government is developing guidelines to regulate this new segment, the industry associations (e.g., the All India Organization of Chemists and Druggists and the Indian Medical Association) are not happy with this growing trend. A formal regulatory framework that protects the rights of stakeholders and guides online pharmacy sales is urgently needed.

a insi s Asia-Pacific and Japan

10 | EY Life Sciences Sector Update Asia-Pacific and Japan | April 2016

J a pa nP ro po s e d pric in g c o n t ro ls f o r “ h ig h - s e llin g ” d ru g s h a u n t in t e rn a t io n a l d ru g m a k e rs . Am b it io u s g e n e ric t a rg e t s s e t b y t h e g o v e rn m e n t a re s t irrin g u p t h e m a rk e t .

To rein in h eal th care spending , the Japanese government has undertaken several measures aimed at reducing drug prices. The most recent one is a controversial rule to reduce prices of “high-selling” drugs. As part of the rule, if a product’s annual sales are in the range of ¥100 billion–¥150 billion and its actual sales are at least 1.5 times projected sales, it will face a price cut of up to 25%. If the drug generates sales of over ¥150 billion and stands at 1.3 times its sales outlook, then it will face a price cut of 50%. Industry bodies have expressed strong opposition to this decision, terming it arbitrary, unreasonable and counter to the government’s agenda of promoting innovation. This rule will most certainly affect prices of the next-generation hepatitis C medicines, which have had strong launches in Japan.60

At the same time, the government aims to increase the volume of generics prescribed from 54.7% of all medicines to 80% by 2020.61 Achieving this target will come at the expense of the long-listed (off-pa n and d d s ic a si nifican pa sin ss mix of several pharmaceutical companies in Japan. The pressure on the long-listed drugs will have several implications for Japanese pharma companies.

idsi and s a c pani s i si nifican p s Japanese market will obviously be more affected than the larger Japanese companies that have a better international mix. R epl enish ing th e R & D pipel ines will become a key priority to offset the losses from long-listed drugs. To bolster pipelines, M&A is expected to increase among domestic Japanese pharmas. This scale will also be important, as companies face pressure to globalize to reduce their dependence on in-country drug sales. Increased generics

i i a i n i a s a a ifica i ns d dis i s ic anticipate increased inventory and transaction costs as a result of increases in both the number of suppliers and products carried. As Japanese distributors deal with this new dynamic, identifying new

sin ss d s and ain ainin p fi a i i i a p i i

Although the government is keeping a tight leash on drug prices, it is investing to im prov e th e reg u l atory infrastru ctu re. The Pharmaceuticals and Medical Devices Agency (PMDA) is building large databases to collect and analyze clinical data and real-world medical data, for development of more effective post-marketing safety measures. To meet these requirements, pharmaceutical companies will need to make some adjustments in their IT systems. For example, the drugmakers will need to submit clinical data required

a in a i a i n in inica a a n c an anda ds Consortium format. The PMDA is also looking to invest ¥132 million to recruit 13 new full-time PMDA employees to increase the agency’s regulatory and safety review capabilities.62

B ol stering innov ation is also a key priority for the government. It as s a is d A nc dica s a c and p n A a Japan s si n s a i na ns i s a

and s a i na ns i a s a c 63 The new agency will support and fund new product development in both the pharma and medical devices sectors. The AMED will receive budgetary funding of ¥126.5 billion in FY16 (up 1.3% from ¥124.8 billion in FY15).64

inis a a and a as a nc d a in form of a private panel for the health minister to promote health care start-ups in the country. The government has also decided to continue with the innovation premium for innovative drugs that satisfy certain conditions.

a insi s Asia-Pacific and Japan

11EY Life Sciences Sector Update Asia-Pacific and Japan | April 2016 |

S o u t h K o re aB u ild in g b io s im ila rs a n d R & D c a pa b ilit ie s a re t h e k e y s h o rt - t e rm g ro w t h d riv e rs o f t h e in d u s t ry .

a is acin c b iosim il ars capital of th e w orl d and aim s to h av e 2 2 % of g l ob al b iosim il ar m ark et sh are b y 2 0 2 0 . n pa ic a c pani s i n and a s n i pis a changing the face of the global biosimilars market.65 nd d a s n

i pis c n n app a fi s n i si i a n pa i a s as i si i a si ns icad c p in

an s and i a in a s a s d p n 66 Depending on s n i a s a s n i pis p ans ais p

i i n ia a is in n c an s in 67 Celltrion a s n a n d p an a s si a a icad

i si i a in i d d and Ad inis a i n

i c n i s in i n inn a i n is a p p i i a inis ci nc and P annin

as ann nc d i s p ans in s i i n in i c sector over the next three years.68 is inc d s p idin financia marketing and business development support to 10 home-grown

biotech and medical device companies. To develop R & D ex pertise, d s ic i p a as a p d d ais i p ndi 10%–20% in 2016. Many companies hope to follow the example set by Hanmi Pharmaceuticals, which in 2015 signed six licensing deals and c a a i p c s inc din a i i n dia s d a i

an fi 69, 70

sid i si i a s an p a as c n in opportunities in new arenas. One area generating much focus is halal-c ifi d d an ac in a a -d si na d p d c s a ad using ingredients and manufacturing processes that adhere to Islamic dietary law. Ildong Pharmaceutical is one of the leading players in this n fi d c in fi s an p a a c pan ain a a c ifica i n a s i d a i n 71

12 | EY Life Sciences Sector Update Asia-Pacific and Japan | April 2016

Featured article: To combat pricing challenges, biopharmas need new modelsByEllenLicking,EYLeadAnalyst

The debate about drug pricing has reached a fever pitch. As populations age and the incidence of chronic disease continues to rise, governments, private payers, health systems and patients around the globe are searching for solutions to make health care spending sustainable.

The economic drivers that guide the pricing of televisions, mobile phones or clothing don’t apply to the pricing of drugs. There are multiple reasons for this, including market exclusivities and a disconnect between the economic buyer (the payer) and the end user (the patient). But the primary reason for high drug prices is the structure of the current system, which relies on unit-based pricing, a methodology that is too one-dimensional for the current needs of the marketplace. This structure has resulted in incentives that encourage biopharma companies to make pricing decisions that are driven by what is possible rather than what is rational.

As a result, biopharma companies have taken the following approach when charging for their drugs: establish a public, unit-based list price for the product and then negotiate, on a market-by-market basis,specific,undiscloseddiscountsorrebatesbasedonin-countryregulations and health technology assessment (HTA) criteria. This approachhashadtwobenefits:1)itissimpletoimplement;2)itpreservespricingflexibility,especiallyinmarketsthatusereferencepricing.

A model under threatIn the past, this lack of pricing transparency worked to manufacturers’ advantage. However, in today’s environment, where the list prices of drugs are high and publicly available, the public doesn’t discriminate between the perceived cost of a medicine and the amount actually spent. Moreover, the heterogeneity of drug costs globally — for instance, certain cancer drugs can cost half as much in Europe as in theUS—reinforcesperceptionsthatpricingpracticesare“unfair,”fueling the industry’s negative reputation.

Biopharma’s historical pricing model is now under threat. One reason: the temporal misalignment between when drug costs occur and when theirbenefitsarerealizedcomplicatesdrugpricingdecisions.Withveryfewexceptions,thebenefitsassociatedwithatherapywon’tbe measurable until many years in the future. However, companies muststillberewardedforthedifficultandriskyworkofinnovation,requiring high up-front price tags for many specialty products. Resource-constrainedpayers,meanwhile,needdrugutilizationpolicies that are consistent with tight annual budget cycles.

Hit hard by their own budget constraints, payers are therefore adopting new restrictions that limit the use of newly launched products. As multiple drugs with similar indications and clinical impactcompeteforshareintherapeuticbattlefieldssuchasoncologyordiabetes,itcanbedifficulttodifferentiatenewerentrantsfromexistingplayers.Afloodofbiosimilarscreatesadditionaldownwardprice pressure in categories that have historically enjoyed pricing flexibility.

In this environment, steep discounts and aggressive rebating strategies to establish market access have become the norm in competitive markets. The more comparable the drugs — or the greater the number of competitors in a particular market — the greater the likelihood payers will act aggressively to rein in drug costs.

We’veseenitalready,especiallyintheAsia-Pacificregion,wherecurbing health care expenditures is a priority for many nations. Both China and India have revisited their drug pricing policies to impose stricter controls. Japan, meanwhile, has been the most aggressive in its reforms, announcing it will impose direct price controls on “high-selling” drugs and change incentives to bolster generic use. Industry groups have already expressed strong opposition to the direct price controls,callingthem“arbitrary”andinconflictwiththeJapanesegovernment’s agenda to promote innovation. One class of drugs most likely to be affected by the policy shift: the next-generation hepatitis C medicines, which have had strong launches in Japan.

13EY Life Sciences Sector Update Asia-Pacific and Japan | April 2016 |

The hepatitis C medicines have also been a lightning rod for pricing d a s in ca a app n d n A i s i i a Pa an a na i i ad ci nc s a - a pa i is i ns a di and Harvoni, was approved in 2014. Net prices of the Gilead products dropped as the biotech sought deals that would keep the products on payers’ formularies.

V al u e is in th e ey e of th e b eh ol derGone are the days when the primary buyer of a drug was the individual physician. In the current cost-constrained environment, pa s n n p i a a c in nc prioritizing budgetary certainty and the development of evidence-based protocols that enable the delivery of the highest value of care to the greatest number of people. Although patients and caregivers continue to place a high priority on advancements that improve quality of life, the current environment means such innovations may result in nice-to-have, not need-to-have products, depending on how much they cost.

s s i a s a d s a p d c ficac and sa But as with improvements in quality of life, these attributes are now n c ssa n s fici n s d i s a n ac d European health systems have emerged as drivers of acceptability around the globe:

• i nifican di n ia i n c pa d s anda d ca

• a i i id n i s s n s p p a i n s i n fi

• a - d c s

• p- n a da i i dicin

• a c s a ca s s

• i i d ac i c s sa in s

One of the critical challenges in developing balanced pricing strategies s s di c ac a is n sin d fini i n product value. Even in Europe, where HTA bodies evaluate clinical and c s - c i n ss id nc is n s anda d d fini i n health care value. Not only do the value formulas vary from country to country, but how those formulas are implemented within a given

a a n c nsis n n in a ni sa i p in a is n di fic sinc is a a n a i n in

pa c ni and i is p i ica nacc p a s c s -effectiveness measures to arbitrate drug prices.

n Asia-Pacific an i dispa a na i na p ici s an a of high-priced innovator products will differ from market to market. n A s a ia ins anc a p d c s a i a s in nc d the number of years it has been on the national formulary. This is one mechanism Australia is using to limit the annual price increases associated with branded pharmaceuticals in other parts of the world.

s dispa a d fini i ns a a c a d a sin ss opportunity: the development of third-party tools that compare the

ficac sid c s and c s s di n p d c s i s a phenomenon, these value frameworks can’t be ignored; by developing an alternative pricing assessment, these frameworks provide credible pricing alternatives that manufacturers must address head on when trying to justify a product’s value.

N ew pricing m odel s neededIntuitively, biopharma companies realize that their pricing strategies

s a in acc n a ca s a d s d fin product value. Executives also understand that the current status quo can’t continue forever. Yet, too often, companies still assemble pricing plans that rely on outdated methodologies and fail to account for the downstream consequences the decision may have on the deployment of care.

What is needed is a more systematic approach that optimizes pricing i i i ac ss di n a s p d c i s d

To work, this approach must be grounded in an honest assessment of how other stakeholders, including the payers, value the medicine’s different features. Moreover, companies must acknowledge that

ca s c s c ns ain s infini s c s s pp acc ss innovation no longer exist. Thus, biopharmaceutical companies will be able to design smarter commercial strategies that lead to greater value creation only if they integrate their customers’ value drivers into their pricing decisions at the outset.

n is c n d fini i n pa i a s s i in forward, the payer may be a traditional insurer — either the government or a private organization. But it could also be a physician

p a is a is financia i s p sc i in d cisi ns n an individual patient. Indeed, in an era when the industry has moved to ai in dicin s indi id a s n ds as d n sp cific n ic

environmental information, these new pricing approaches, if applied smartly, will allow companies to design pricing arrangements that are tailored to the individual needs of the payer in question.

14 | EY Life Sciences Sector Update Asia-Pacific and Japan | April 2016

Effective trade policies and capabilities are critical for enabling companiestoaccessmarketsquickly,effectivelyandcostefficientlywhile at the same time maintaining compliance with a myriad of regulatory, customs and indirect tax requirements. Those companies withbest-in-classtradecapabilitiesoftenenjoyasignificantcompetitive advantage compared to their peers. Historically, however, many companies operating in Asia have struggled to achieve desired levels of trade effectiveness and performance or, at the very least, have been unable to identify and capitalize on available opportunities tosignificantlyreducecostandmitigateriskintheirsupplychains.This inability to identify and capitalize on such opportunities is often present even at companies with highly effective trade capabilities. That’s because the limitations are often attributable to factors outside thecontrolandvisibilityofthecompany’sinternaltradeandfinancefunctions. For many companies operating in Asia, such limitations have related principally to regional complexity and supply chain visibility.

The high degree of operating complexity encountered throughout Asiaisonereasonit’smoredifficulttoachievedesiredlevelsoftrade effectiveness in this region. Unlike in Western markets, there isn’t the same degree of harmonization for regulatory processes, customs procedures and indirect tax requirements. These different requirements, coupled with often restrictive trade barriers, increase the complexity and risk of doing business in Asia. That complexity and risk is also heightened by a lack of standardization in accepted local business practices and ways of working. In such an environment, it is easier to misstep, elevating the level of business risk. In addition, it is oftenmoredifficulttoidentifyandquantifyareasofthepotentiallysignificantopportunity.

Supplychainvisibility—orlackthereof—isanotherreasonwhyachievingtradeeffectivenessinAsiaissochallenging.Lackofaccess to accurate and comprehensive trade data prevents many companiesfrombeingabletoaccuratelydefine,visualizeandanalyzetheir import and export transactions. As a result, many companies have to make decisions based on what they believe is happening

rather than what is actually happening. Unfortunately, there can be significantgapsbetweenthesetwostates.Historically,suchgapshaveresultedprincipallyinlostopportunity.Intoday’shighlyfluidand evolving regulatory and tax environment, however, such gaps arebecomingmorelikelytoresultincostlybusinessrisks.Suchrisksinclude potential underpayment of customs duties and indirect taxes, exposuretounderpaymentpenalties,financialstatementerrorsandreputational risk.

The good news is that processes and tools are now available to help companies overcome these historical challenges. Within the last six toeightmonths,significantinnovationhasbeenmadeinapproachesfor obtaining accurate and comprehensive trade data. This access to data, combined with advancements in trade analytics tools and methodologies (i.e., “trade analytics”), is enabling companies to quicklyachievesignificantimprovementsintheirtradeeffectiveness.Suchimprovementshaveresultedinsubstantialprospectiveandretrospectivecostsavings,tradeflowefficiencies,andopportunitiesto proactively identify and mitigate areas of potential controversy and exposure.

... the customs broker creates a new and unique data set that now resides outsideofthecompany’sERPsystems.

Barriers to trade effectivenessOneofthemostsignificantbarriersthatcompaniesencounterwhenattempting to drive trade effectiveness is poor supply chain visibility (i.e.,aninabilitytoaccuratelydefine,visualizeandanalyzetheirimport and export transactions). This inability results in large part from a lack of access to accurate and comprehensive trade data. Without access to this data, companies are much less likely to be in a position to identify and capitalize on available opportunities to reduce

Featured article: Optimizing supply chain effectiveness in Asia with trade analytics ByMarcBunch,GlobalLeader,EYTradeAnalytics, andRickFonte,Asia-PacificLifeSciencesTaxLeader

15EY Life Sciences Sector Update Asia-Pacific and Japan | April 2016 |

costs,mitigateriskand/orenhancetradeflowefficiency.Thislackofdata access and its implications are often not well understood by key stakeholders within a number of organizations. Yet understanding the origins of the problem and the limitations it creates is critical to fully appreciating why internal trade functions are currently so constrained, and why accessing and analyzing this data can unlock substantialbenefits.

Eachtimegoodscrossaborder,companiesmustfileacustomsentry, usually electronically. The data on the customs entry is legally required to be presented at an invoice line item level and can be in excessof100fieldsperimport/exportline.Tocompletetheentry,the company’s customs broker must combine several sources of data,includingimporter/exporterEnterpriseResourcePlanning(ERP)transactionaldatareceivedfromthecompany,customsbrokerdeterminations(e.g.,harmonized-systemclassificationdeterminations, customs valuation adjustments), shipping data and source/destination data. In the process, the customs broker creates a new and unique data set that now resides outside of the company’s ERPsystems.Itisthisuniquedatathatissubmittedelectronicallyto the customs authority, but not to the company. Unfortunately, no other single source of data provides the information needed to derive meaningfulinsightsandachievetruetradeeffectiveness.ERPdataisinsufficientlydetailed,andthedataattributesthatareavailablearenot in a single location; thus, substantial effort is required to collate informationthatisnotfitforpurpose.Meanwhile,otherdatasources,including data from shipping or logistics systems, are too narrowly focused.

Inadditiontocreatingasignificantbarriertoachievingtradeeffectiveness, companies’ lack of ready access to this data puts them at greater risk during audit, as they are less able to proactively defend theirpositions.Keepinmind,athird-partybrokersubmitsdatatothe appropriate government agency on behalf of the company. That scenario results in data asymmetry: the government has full access to the data, but the company, which is legally responsible for the information, does not. This situation increases the company’s risk as the government agencies auditing the company’s customs, indirect taxes and direct taxes are increasingly more likely to have better information and knowledge about the company’s transactions than the company does.

The evolution of trade analytics capabilitiesSignificantadvancementshaverecentlybeenmadeintradeanalytics capabilities, and the traditional barriers to achieving trade effectiveness no longer exist. First, data access is no longer an issue. Electronic customs declarations are now required in virtually every country, and it is now possible to access this unique data set. During thelast12months,well-definedprocessesforrequesting,andsuccessfully obtaining, such data directly from customs authorities or customs brokers’ entry systems have been established for virtually everycountryinAsia.Suchdatacannowbedirectlyandquicklyobtained with virtually no involvement from company personnel. By directly accessing this data from external sources, not only can companies now access the complete set of trade data they need to perform meaningful analyses (i.e., the company’s importer/exporter ERPtransactionaldatacombinedwiththecustomsbroker’sdata)buttheycanalsoavoidthecomplexitiesandfrustrationsofinternalERPdata extraction, inaccuracy and data cleansing.

Second,significantadvancementsindataanalyticsmeanthathighlyintuitive and robust analytical tools are now available. As previously noted, the data on the customs entry is legally required to be presented at an invoice line item level; thus, even one year of trade data represents an unmanageable volume of data. Given the amount of data to be analyzed, advanced analytics are required to convert such information into actionable insights.

Finally,everycompany’ssupplychains,tradeflowsandproductsarevery different, as are their business and trade priorities, objectives, challenges and opportunities. Data access and analytics tools capable of processing and analyzing trade data are of minimal value unless combined with processes and customized tests designed to identify actionableinsightsandopportunitiesspecifictoeachcompany.Just as every available analytical test may not be relevant for every company,norwilleveryavailabletestnecessarilybesufficient.Consequently, a static analytical tool or engine that simply produces predetermined test results without taking into consideration each company’s unique needs will more often than not fail to identify theinsightsofgreatestpotentialbenefit.Onlybycombiningtheright data, technology and process can a company truly optimize its trade effectiveness. Proven processes, including a rapidly expanding inventoryofcustomizedanalyticstestsdevelopedspecificallyfortrade, are now available.

Based on recent developments in trade analytics processes, data can now be obtained and analyses performed for any country in the world.

The power of trade analyticsTrade analytics can inform and support companies on a wide range of supply chain, customs and tax decisions and opportunities in Asia, ranging from macro-strategic to micro-operational. One of the key benefitsofaneffectivetradeanalyticsofferingisthatitrequiresno effort for companies to obtain the transactional-level trade data theyneedtoaccuratelydefineandvisualizetheirimportandexporttransactions,bothphysicalandfinancial,andforbothcurrentandprior periods. Most companies have never had this level of visibility or insight — they have instead relied on what they believe is happening.

Trade analytics offerings utilize advanced data analytics and processes to analyze and model this unique data set, enabling them to identify potentially substantial prospective and retrospective cost savings,tradeflowefficienciesandopportunitiesforriskmitigation.Based on recent developments in trade analytics processes, data can now be obtained and analyses performed for any country in the world. The results are delivered in easy-to-read dashboards that clearlypresentandsummarizethecompany’scurrentstateprofile,gaps and business opportunities. This makes it easy for companies to identify and prioritize potential investment areas and next steps (see exhibits 1 and 2 on the following page for two sample screenshots of analyses performed for customs duty).

16 | EY Life Sciences Sector Update Asia-Pacific and Japan | April 2016

Featured article

Ex h ib it 1 : Graphical summary of origin of imports, customs duties paid, effective duty rates and trends over time as starting point for identifying areas of potential opportunity

Ex h ib it 2 : Ana sis c n ad s ad A n A pp ni is a ai a as n n c ai d inc din an ifica i n p n ia n fi

17EY Life Sciences Sector Update Asia-Pacific and Japan | April 2016 |

Featured article

Scalable process, actionable insights and benefits ad ana ics p c ss is i sca a a din c pani s si nifican a i d d fin i p i i i s and a as c s pani s

a i i i a a ad app ac and s ass ss s s a a ai a ana ica s s can a s a d c sin c s n sp cific s s a in a as i a c i ica i sin ss s and c a a in n

d p n n ana ica s s pani s a s a i i i s a in s a and pi in p c ss n a i i d n s c countries, or analyzing data for an entire region or regions. In our experience, based on results from more than 100 recent engagements and

p s an c s i d ana ica s s s c n id n ifi d insi s and n fi s a can ac i d through trade analytics include:

s sa in s and i p n s s pp c ain fici nc s in su ppl ier rational iz ation and consol idation, including:

• d n ifica i n i ns c n i s su ppl ier cl u sters are present and thus there is an opportunity to resource goods purchased from both low-cost and high-cost countries

• d n ifica i n ins anc s si nifican s sa ds are being imported from suppliers in multiple countries, enabling companies to neg otiate m ore com petitiv e pricing and consolidate suppliers

• d n ifica i n ins anc s ds a in s c d an unusually high number of suppliers, and thus, al ternate sou rcing strateg ies a n ficia

Proactive development and implementation of controv ersy m anag em ent and risk m itig ation strategies and overall improvements to internal control s p n id n ifica i n a i s p in and p a i na inconsistencies or errors, including:

• d n ifica i n H S coding inconsistency resulting in the nonpayment or underpayment of customs duties

• is a i in financia and p sica ad s id n i ins anc s where the company’s actual transactions are inconsistent with the company’s tax operating m odel s and transfer pricing strategies

• Utilization of m u l tipl e and inconsistent incoterm s, in general, as well as with respect to the same supplier, resulting from weaknesses in internal controls, internal and external compliance issues, and failures by customs brokers to declare the correct incoterms

Scenario m odel ing nd s and financia i pac and sc pin considerations for strategic supply chain decisions, including the evaluation of bonded facility implementation, distribution center location analysis, and government trade programs such as inward and outward processing regimes

C u stom s du ty and G ST / V A T / J C T refunds and prospective savings resulting from:

• d n ifica i n and c c i n H arm oniz ed Sy stem ( H S) coding inconsistencies that lead to customs duty over- or underpayments, inc din sa ds a n c assifi d sin di n codes

• Payments or overpayments of customs duty on importations from free trade ag reem ent countries

• R esou rcing of im portations where the same goods are being imported from both countries with and without preferential customs duty rates

• d n ifica i n pp ni i s cu stom s du ty draw b ack s where exported goods incorporate both dutiable and non-dutiable imported goods or components

• c nci ia i n im port V A T / G ST / J C T paid c di s a n in AJ fi in s id n i iss d c di s

Finished pharmaceutical products and certain chemical intermediates are often not subject to customs duties under the World Trade Organization Agreement on Trade in Pharmaceuticals, as part of the zero-for-zero initiative. However, in several Asian countries, duty continues to apply, particularly for those new products not yet updated on the zero-for-zero list. In addition, materials and packaging used for research and development, manufacturing and clinical trials are frequently dutiable and must be considered.

Cost savings and improvements to supply chain operations resulting from correcting compliance and operational errors and inefficiencies, including:

• d n ifica i n incoterm noncom pl iance and double payment of shipping costs to both supplier and shipper

• d n ifica i n s inc c inv oice cu rrency and/or use of multiple currencies by a single supplier, resulting in violations of company policy, failures by customs brokers to declare the correct currency, and possibly over- or underpayments of customs duties

• C u stom s b rok er rational iz ation allowing companies to decrease the number of parties declaring information to various governments on their behalf and, thus, reduce the risk of unintended reporting errors and noncompliance

• Assessment of cu stom s b rok er perform ance, ranging from clearance times to error rates, to identify areas for operational improvement and cost savings, including decreasing the time required for goods to clear customs, thus reducing demurrage and storage fees

• Assessment of business decisions regarding sh ipping m eth ods utilized s a s ai and s c d cisi ns a s c s fici n

• Preparatory work and process improvement to increase likelihood of success in seeking A u th oriz ed Econom ic O perator status

The appropriate/reasonable way to develop a true appreciation for the advantages trade analytics can provide an organization is to see a demonstration of EY’s Global Trade Analytics offering. For more information, or to arrange for a demonstration, please contact Marc

nc a ad ad Ana ics a a c nc c

18 | EY Life Sciences Sector Update Asia-Pacific and Japan | April 2016

Mergers and acquisitions (M&A)

M e rg e rs a n d a c q u is it io n s ( M & A) — g lo b a lTotal deal value in life sciences reached

i i n in a inc as the prior year and a new record. In addition to nearly 2,000 total announced deals, life sciences was third in overall industry deal value in 2015, trailing only technology and consumer products and retail.

Global M&A activity in life sciences reached new heights in 2015

Source: ThomsonOne

0

400

800

1,200

1,600

2,000

100

200

300

400

500

0

Global M&A activity in life sciences reached new heights in 2015

Deal volumeDeal value (US$billion)

US$

b

Num

ber

of d

eals

2011 2012 2013 2014 2015

19EY Life Sciences Sector Update Asia-Pacific and Japan | April 2016 |

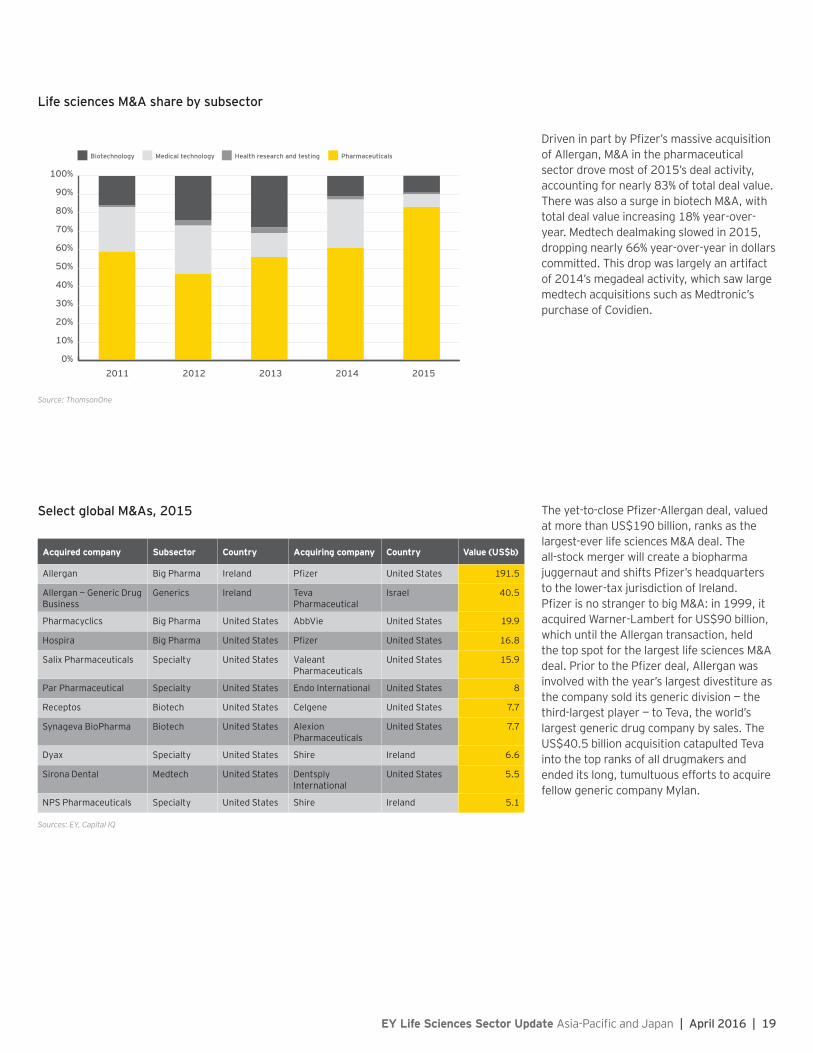

i n in pa Pfi s assi ac isi i n of Allergan, M&A in the pharmaceutical sector drove most of 2015’s deal activity, accounting for nearly 83% of total deal value. There was also a surge in biotech M&A, with total deal value increasing 18% year-over-year. Medtech dealmaking slowed in 2015, dropping nearly 66% year-over-year in dollars committed. This drop was largely an artifact of 2014’s megadeal activity, which saw large medtech acquisitions such as Medtronic’s purchase of Covidien.

Life sciences M&A share by subsectorLife Sciences M&A share by sub-sector

Biotechnology Medical technology Health research and testing Pharmaceuticals

2011 2012 2013 2014 20150%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

Source: ThomsonOne

Sources: EY, Capital IQ

A cq u ired com pany Su b sector C ou ntry A cq u iring com pany C ou ntry V al u e ( US$ b )

Allergan Big Pharma Ireland Pfizer ni d a s 191.5

Allergan — Generic Drug Business

Generics Ireland Teva Pharmaceutical

Israel 40.5

Pharmacyclics Big Pharma ni d a s AbbVie ni d a s 19.9

Hospira Big Pharma ni d a s Pfizer ni d a s 16.8

a i P a ac ica s p cia ni d a s Valeant Pharmaceuticals

ni d a s 15.9

Par Pharmaceutical p cia ni d a s Endo International ni d a s 8

c p s Biotech ni d a s Celgene ni d a s 7.7

na a i P a a Biotech ni d a s Alexion Pharmaceuticals

ni d a s 7.7

Dyax p cia ni d a s i Ireland 6.6

i na n a Medtech ni d a s Dentsply International

ni d a s 5.5

P P a ac ica s p cia ni d a s i Ireland 5.1

- -c s Pfi -A an d a a d a an i i n an s as largest-ever life sciences M&A deal. The all-stock merger will create a biopharma

na and s i s Pfi s ad a s to the lower-tax jurisdiction of Ireland. Pfi is n s an i A in i ac i d a n - a i i n which until the Allergan transaction, held the top spot for the largest life sciences M&A d a P i Pfi d a A an as involved with the year’s largest divestiture as the company sold its generic division — the third-largest player — to Teva, the world’s largest generic drug company by sales. The

i i n ac isi i n ca ap d a into the top ranks of all drugmakers and ended its long, tumultuous efforts to acquire fellow generic company Mylan.

Select global M&As, 2015

Mergers and acquisitions (M&A) — Asia-Pacific and Japan

Sources: EY, Capital IQ

The values of Asia-Pacific M&As have skyrocketed

Deal volumeDeal values (US$b)

US$

b

Num

ber

of M

&A

s

2011 2012 2013 2014 20150

10

20

30

40

50

60

0

100

200

300

400

500

600

Mergers and acquisitions

20 | EY Life Sciences Sector Update Asia-Pacific and Japan | April 2016

a a Asia-Pacific and Japan A ac d i i n in a

jump of 83% from the previous year and a whopping 380% increase since 2011. With the total value of global life sciences M&A

ac in i i n in Asia-Pacific and Japan A a s a actually tripled the global growth rates since

n - i d a i sci nc s A cc s i in Asia-Pacific

a a d a si s i i n a s i n n -fi si a d a s

Asia-Pacific and Japan M&As

Sources: EY, Capital IQ

Asia-Pacific M&As by sub-sector, 2015

Medical technology PharmaceuticalsBiotechnology

US$

b

2011 2012 2013 2014 2015

0

10

20

30

40

50

60

Asia-Pacific i n as i n ss d a si nifican p ic in A in i sciences subsectors: biotechnology, medical technology and pharmaceuticals. Most of the focus is on buying pharmaceutical companies; 61% of 2015’s regional deal total

i i n as a i d p a a M&A. Meanwhile, values for biotech deals have increased the most (up 540%) since 2011, followed by medtech M&A (up 356%).

As ia - P a c if ic a n d J a pa n M & As b y s u b s e c t o r

Source: EY, Capital IQ

Asia-Pacific M&As by country, 2015

Total M&A value Total number of M&As

US$

b

All others Australia India South Korea Japan China

Num

ber

of M

&A

s

350

280

210

140

70

0

45

36

27

18

9

0

Mergers and acquisitions

21EY Life Sciences Sector Update Asia-Pacific and Japan | April 2016 |

Mainland China dominated M&A in 2015. Chinese-based life sciences companies acc n d i i n a Asia-Pacific A a Japan and

a i d a dis an s c nd i of M&A value, followed by Australia with 3%. A Asia-Pacific c n i s acc n d less than 1.5% of the industry’s M&A total.

Of the 532 M&A deals that had announced terms, more than 60% were of companies domiciled in China, and an astonishing 96% of those deals transpired between Chinese buyers and sellers. In fact, only 12% of all Asia-Pacific A d a s in d c pani s in different countries. Despite the tremendous

p sp c s i in Asia-Pacific c pani s sp n ss an i i n in total to acquire 10 companies in the region. None of them were based in China.

Asia-Pacific and Japan M&As by country, 2015

In 2015, there were 11 M&A deals worth an i i n and an i i n s

deals, 22 targeted Chinese companies. In fact, China was responsible for 9 of the 10 largest deals in 2015, including the top two, which involved investor groups taking public companies private.

In the case of WuXi PharmaTech, a buyout group consisting of its management team acquired the company at an 11% premium and stopped its trading on the New York

c c an An - is d company, Mindray Medical, is currently being targeted by investors aiming to take the imaging and diagnostic company private.

A cq u ired com pany Su b sector C ou ntry A cq u iring com pany C ou ntry D eal v al u e ( US$ b ) Statu s

WuXi PharmaTech ic s China Investor Group China 2.9 Completed

Mindray Medical Medical Technology

China Investor Group China 2.5 Pending

Beijing Jialin Pharma

Pharmaceutical China Xinjiang Tianshan Wool Tex

China 1.6 Pending

Hubei Biocause Pharmaceutical

Pharmaceutical China Investor Group China 1.6 Pending

aan i ic n Pharmaceutical

Pharmaceutical China Jiangsu Jiujiujiu Tech China 1.6 Completed

Mudanjiang Youbo Pharmaceutical

Biotech China Jiuzhitang China 1.5 Completed

Guangzhou Baiyunshan Pharmaceutical

Pharmaceutical China Investor Group China 1.5 Pending

ai n Pharmaceutical

Pharmaceutical China Furen Pharmaceutical China 1.4 Pending

Changchun an s n i

Biotech China ian n an HuangHai Machinery

China 1.1 Completed

Boditech Med Inc Biotech a

p cia P p s Acquisition Company

a

1.0 Completed

Select Asia-Pacific M&As, 2015

Financing: Excerpts from Beyond Borders 2016, EY’s global biotechnology report

22 | EY Life Sciences Sector Update Asia-Pacific and Japan | April 2016

Forthesecondyearinarow,thebiotechnologysector’sfinancingtotalreachedunprecedentedheights.Intotal,biotechcompaniesraisednearlyUS$71billionin2015,easilysurpassingtherecord-settingUS$56billionamassedtheyearprior.Fuelingthisbest-everfinancialpicturewererecordcapitalraisesinthreecategories:follow-onpublicfinancingrounds(US$21.8billion),debt(US$32.1billion)andventurecapital(US$11.8billion).Itwasalsoanotherstellaryearforinitialpublicofferings,withmorethanUS$5.2billionraisedinIPOs,thethird-highesttotalon record.

Whetherlargeorsmall,publicorprivate,biotechcompaniesacrosstheindustryhavebeenabletotakeadvantageofthefree-flowingcapitaloverthepasttwoyears.Duringthisperiod,biotechshavefilled(orrefilled)theircofferswithcashtodrivefutureresearchanddevelopmentand business development agendas.

Financing and IPOs

23EY Life Sciences Sector Update Asia-Pacific and Japan | April 2016 |

Innovation capital in the US and Europe surpassed US$40 billion in 2015

Sources: EY, Capital IQ and VentureSource.nn a i n capi a is a n capi a ais d c pani s i n s ss an i i n

0

10

20

30

40

50

60

70

80

Innovation capital in the US and Europe surpassed US$40 billion in 2015Innovation capital Capital raised by commercial leaders

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015

US$

b

n and p inn a i n capi a cas ais d c pani s i n s ss an i i n ac d i s i s - a in c s in a i i n is a inc d d a n P and - n d a s a as as a s a in s a d

in s a d in s i ad n A n and i n c ns i d as a i i i n ais d s c s commercial leaders.

Financing and IPOs

24 | EY Life Sciences Sector Update Asia-Pacific and Japan | April 2016

Sources: EY, Capital IQ and VentureSource.

US and European early stage venture investment reached unprecedented heights

US and European early stage venture investment reached unprecedented heightsCapital raised Capital raised by commercial leaders

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015

Cap

ital

rai

sed

(US$

b)

Num

ber

of d

eals

0

1

2

3

4

0

50

100

150

200

250

n a s a n nds ac d a n i - a a in a s s d and i s A financin s ais d a c in d i i n a s a n c d s n P a ac ica s ic ais d a s - i c s d in s n n i p d in i i n in n n s a s n nd a n p i n - nc s a -

p n c ais d i i n in a i s A financin a as p s a s - n nd As a s financin n c as a d a i i n

Financing and IPOs

25EY Life Sciences Sector Update Asia-Pacific and Japan | April 2016 |

A d p- in P s in fina a a si na innin nd is a s n a d ss P a fares in the coming months, it is worth remembering that 78 biotechs went public in 2015, compared with 95 (the all-time record) in 2014.

i c s ais d i i n in s d in s ind s s i d- i s P a a a P d a a as c pa a s i i n s i i n p P a n s an s in i i n and Adap i n in

p i i n s P ac i i cc d in i c s ais d a as i i n and ais d a as million.

acc ss in-d p insi s and da a financin a ic in Beyond borders 2016 p as isi i a i ns s p sp c i s n i sciences, at ey.com/vitalsigns.

Sources: EY, Capital IQ and VentureSource.

US and European biotechnology IPOs by year

US and European biotechnology IPOs by yearCapital raised Number of deals

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015

Cap

ital

rai

sed

in IP

Os

(US$

b)

Num

ber

of d

eals

0

1

2

3

4

5

6

7

8

0

20

40

60

80

100100

0

Asia-Pacific and Japan IPOs

Financing and IPOs

26 | EY Life Sciences Sector Update Asia-Pacific and Japan | April 2016

i P ind in and p showed signs of closing in 2015, it was

n id p n in Asia-Pacific i - Asia-Pacific- ad a d c pani s ais d

i i n in an inc as over the previous year, and just shy of the

i i n ais d in and p p d a s P a in

ina s i i c c pani s a n d s a n capi a

billion), directly followed by pharmaceuticals i i n and dica c n

i i n

Chinese life sciences companies dominated Asia-Pacific P a i p ic

in s an i i n roughly 70% of all capital raised in the region. Of the 17 companies that raised more than

i i n a as d in ain and ina a finis d a dis an s c nd

i P s i i n i Australia and Japan each had six IPOs.

Asia-Pacific IPOs by subsector

Sources: EY, Capital IQ

Asia-Pacific IPOs by sub-sector, 2015

Medical technologyBiotechnology Pharmaceuticals

US$

b

2011 2012 2013 2014 2015

0

1

2

3

4

5

Life sciences IPOs in Asia-Pacific and Japan, 2015

3

3.5

2.5

2

1.5

1

.5

0

35

30

25

20

15

10

5

0

Life Sciences IPOs in Asia-Pacific, 2015

Number of IPOs closedTotal IPO value

US$

b

Num

ber

of IP

Os

China South Korea India Japan Singapore Australia New Zealand

Financing and IPOs

27EY Life Sciences Sector Update Asia-Pacific and Japan | April 2016 |

Just two years after being taken private ina s P i a i i

became 2015’s largest life sciences IPO. is is i s s c nd P as c pan i ina n p ic n asda

exchange in 2007. The producer of drugs to treat bleeding disorders brought in an i p ssi i i n n a s n times its original IPO — and attracted ins i i na in s s s c as ac c and

in ap s s i n a nd i c p i n A i ci nc s

P an million went public on a domestic exchange.

A is a in ap - is d p c inica genetic medicine company — with primary operations based out of Cambridge, MA,

A c s d n ad ancin s p nucleic acid therapeutics.

Top Asia-Pacific and Japan IPOs, 2015

C om pany C ou ntry Su b sector A m ou nt raised ( US$ m ) Ex ch ang e

i China Biotech 711 n n

an ai a ai i ica Technology

China Biotech 305 n n

Heilongjiang ZBD Pharmaceutical China Pharma 246 an ai

ic an a i c n China Medtech 223 n n

A a a i s India Pharma 203 Mumbai

i in ci nc n Pharmaceutical

China Biotech 186 n n

YiChang HEC ChangJiang Pharmaceutical

China Pharma 174 n n

Caregen a Pharma 154 A

d n n a p i i d China Medtech 135 n n

n P a ac ica a Pharma 129

Ningbo Medicalsystem Biotechnology

China Biotech 126 n n

i nc P a ac ica p China Pharma 123 an ai

an i Japan Biotech 108 Tokyo

P a a s a c P d c s a Biotech 107 A

A i ci nc s in ap Pharma 102 Nasdaq

n d an n Pharmaceuticals

China Pharma 100 n n

an P - i i - n in in Company

China Pharma 100 an ai

28 | EY Life Sciences Sector Update Asia-Pacific and Japan | April 2016

Appendix

E Y t h o u g h t le a d e rs h ip EY perspective on life sciencesThe following is a sample of recent life sciences-related thought leadership produced by EY. Please visit ey.com/vitalsigns for EY’s full library of industry insights and reports.

Beyond borders 2016 g l ob al b iotech nol og y report s c nd a in a i c n s c s financin a ac d

np c d n d i s i c n c pani s ais d n a i i n in asi s passin c d-s in i i n a ass d a p i in is s - financia pic c d capi a ais s in ca i s - n p ic financin nds d and n capi a as a s an s a a ini ia p ic in s i an i i n raised in IPOs, the third-highest total on record.

F inancing narrativ e

B ey ond b orders 2 0 1 6B o u n t if u l h a rv e s t le a v e s b io t e c h w e ll pre pa re d f o r w in t e r

Life Sciences Global Corporate Divestment Study EY’s Global Corporate Divestment Study c s s n ss ns c p a s can a n p i a i fi s i p in p i i s divestment execution. The study is based on interviews with 900 global C-suite executives and 100 PE executives, plus external market data.

29EY Life Sciences Sector Update Asia-Pacific and Japan | April 2016 |

Protecting information at life sciences companiesHow to safeguard the assets that matter most: as the life sciences sector continues to become more data-driven, cyberthreats and breaches of data systems are becoming an increasingchallenge.Recentincidentsinvolvingthelossofprotectedhealthinformationandsensitive information at pharmacies, health systems, providers and payers have shown that attackscontinuetobecomemoresophisticated.Theseattacksalsosignificantlyimpactanorganization’s bottom line, brand and reputation.

Pulse of the Industry medical technology report 2015 In EY’s 8th annual Pulse of the Industry medical technology report, we review the noteworthy financialperformance,deal-makingandfinancingtrendsthatsurfacedinthelast12monthsand discuss the future implications of these trends.

EY’s Life Sciences Tax capabilities: Asia-Pacific and Japan EYiscontinuingtomakesignificantinvestmentsinthelifesciencessectorinAsia-PacificandJapan. Within Tax, such investments have included the further development of an extensive life sciences tax infrastructure and tax leadership team comprised of designated tax sector leadersandspecialtypracticeresourcesattheArea,Regionandmemberfirmlevels.TheseresourcesserveasthebackboneofEY’sbroaderAsia-PacificandJapanLifeSciencestaxnetwork, as well as designated single points of contact and coordination for EY account teams and client personnel.

Adapt or fail: changing models in global medtech As published in MedTech Strategist,Parthenon-EY’sDanShoenholzandKeyuriShahoutlinestrategies medical device companies can use to succeed in a new health care landscape or risk being overcome by change.

Firepower index and growth gap report 2016Deal tectonics: at the fault line of growth goals and competitive pressures, mergers and acquisitions (M&A) in the biopharmaceutical industry skyrocketed in 2015, with the value of 2015announceddealstotalingmorethanUS$300billion,anewrecordfortheindustry.Asthe specialty pharmaceutical sector sees its ability to pursue large acquisitions evaporate, long-promisedorganicgrowthfrombigpharmanewdruglauncheshasfinallyarrived.Butarenewedfocusonvalue-basedpricing,staunchcompetitionacrosskeytherapeuticbattlefieldsand consolidating payer clout may weaken the industry’s ability to reach revenue targets for both new and legacy therapeutics.

Contacts

R ick F onteAsia-Pacific i ci nc s a ad

in apic a d n s c

+65 6309 8105

H u g o W al k insh awAsia-Pacific i ci nc s Ad is

n adin ap

a ins a s c+ 65 6309 8098

B ernard N gAsia-Pacific i ci nc s

ansac i ns adan aina d- n cn c

+86 21 2228 2005

P atrick F l och ela P a ac ica c ad

Tokyoc -p c s inni n p

+81 3 3503 1542

L if e S c ie n c e s s e c t o r le a d e rs

3 0 | EY Life Sciences Sector Update Asia-Pacific and Japan | April 2016

Hironao [email protected]+81 3 3503 1566

Japan

Greater China

South Korea

ASEAN

Oceania

Titus Bongart [email protected]+86 21 2228 2884

Felix [email protected]+86 21 2228 2586

Jon Junyoung [email protected]+82 2 3787 6378

Sabine DettwilerASEANLifeSciencesLeaderSingaporesabine.dettwiler@sg.ey.com+65 9028 5228

Gamini [email protected]+61 2 9248 4702

31EY Life Sciences Sector Update Asia-Pacific and Japan | April 2016 |

L if e S c ie n c e s s e rv ic e lin e le a d e rs

i sci nc s c n ac s

C h ina ( M ainl and)

Felix Fei Assurance an ai i i cn c +86 21 2228 2586

Titus Bongart a - ad an ai i s n a cn c +86 21 2228 2884

Vickie Tan a - ad an ai ic i an cn c +86 21 2228 2648

Edward Chang Ad is - ad an ai d a d c an cn c +86 10 5815 2321

A n Ad is - ad an ai s a n cn c +86 21 2228 8888

Bernard Ng Transactions an ai na d- n cn c +86 21 2228 2005

H ong K ong /M acau

Cary Wu Assurance n n ca c +85 2 2849 9122

a ina n Tax n n a ina n c +85 2 2849 9175

Edward Chang Ad is - ad an ai d a d c an cn c +86 10 5815 2321

Judy Tsang Transactions n n d san c +85 2 2846 9016

T aiw an in Ass anc - ad Taipei in c +886 2 2757 8888

in Ass anc - ad Hsinchu in c +886 3 688 6000

Ann n Tax Taipei ann s n c +886 2 2757 8888

Jon Huang Advisory Taipei n an c +886 2 2757 8888

Audry Ho Transactions Taipei a d c +886 2 2757 8888

A u stral ia Gamini Martinus Assurance dn a ini a in s a c +61 2 9248 4702

Denise Brotherton Tax Melbourne d nis n a c +61 3 9288 8758

Milan Milosevic Advisory dn i an i s ic a c +61 2 9248 5028

Jason Wrigley Transactions dn as n i a c +61 2 9248 5303

N ew Z eal and Jon Hooper Assurance Auckland n p n c +64 9 300 8124

Aa n in a Tax Auckland aa n in a n c +64 9 300 7059

Sou th K orea Jon Junyoung Huh Assurance n- n n c +82 2 3787 6378

Ja i Tax a -c i c +82 2 3770 0961

n i i Advisory n -si i c +82 2 3787 6600

an Transactions -s an c +82 2 3770 0907

Oceania

S o u t h K o re a

3 2 | EY Life Sciences Sector Update Asia-Pacific and Japan | April 2016

G re a t e r C h in a

i sci nc s c n ac s

J apan Hironao Yazaki Assurance Tokyo a a i- n s inni n p +81 3 3503 1566

J na an a - i a - ad Tokyo na an s a -s i p c +81 3 3506 2426

a s id an na i a - ad Tokyo a s id an na i p c +81 3 3506 1364

as i ada Advisory Tokyo sada - s s inni n p +81 70 2161 0714

Takayuki Ooka Transactions Tokyo a a i a p c +81 3 4582 6422

J a pa n

3 3EY Life Sciences Sector Update Asia-Pacific and Japan | April 2016 |

Sing apore/B ru nei

an Assurance in ap s an s c +65 6309 8238

i n i Tax in ap si - n si s c +65 6309 8807

a in i Advisory in ap sa in d i s c +65 9028 5228

Abhay Bangi Transactions in ap a a an i s c +65 6309 6151

I ndonesia P a Assurance Jakarta p s a id c +62 21 5289 4012

Peter Ng Tax Jakarta p n id c +62 21 5289 5228

a in i Advisory in ap sa in d i s c +65 9028 5228

is i Transactions Jakarta c is p i id c +6221 5289 5000

T h ail and/M y anm ar

ai n n a Assurance Bangkok sai n in a c +662 264 9090

an n Tax Bangkok s -san n c +662 264 9090

a in i Advisory in ap sa in d i s c +65 9028 5228

Abhay Bangi Transactions in ap a a an i s c +65 6309 6151

P h il ippines/G u am

Ana a ad Assurance Makati City ana a c ad p c +63 2 894 8354

Czarina “Bing” Miranda Tax Makati City c a ina i anda p c +63 2 894 8304

Joseph Ian Canlas Advisory Makati City s p ian can as p c +63 2 8910307

Abhay Bangi Transactions in ap a a an i s c +65 6309 6151

M al ay sia Yoon Hoong Hoh Assurance a a p n- n c +6 03 7495 8608

Janice Wong Tax a a p anic n c +6 03 7495 8223

a in i Advisory in ap sa in d i s c +65 9028 5228

Abhay Bangi Transactions in ap a a an i s c +65 6309 6151

V ietnam /C am b odia/ Laos

Ernest Yoong Assurance Hoh Chi Minh City n s n n c +84 8 3824 8210

Thinh X Than Tax Hoh Chi Minh City in an an n c +84 8 3824 8360

a in i Advisory in ap sa in d i s c +65 9028 5228

Abhay Bangi Transactions in ap a a an i s c +65 6309 6151

AS E AN

34 | EY Life Sciences Sector Update Asia-Pacific and Japan | April 2016