fa.morganstanley.com methodology and asset allocation 59 - 62 key asset class risk considerations 63...

TRANSCRIPT

John and Jane Smith

January 04, 2016

LifeView® Financial Goal Analysis

Prepared by:

John Advisor, CFP®Financial AdvisorSAMPLE

Table Of Contents

IMPORTANT DISCLOSURE INFORMATION 1 - 4

Summary of Goals and Resources

Personal Information and Summary of Financial Goals 5 - 6

Net Worth Summary - All Resources 7

Net Worth Detail - All Resources 8 - 9

Resources Summary 10 - 11

Current Portfolio Allocation 12 - 13

Target Band 14

Results

What If Worksheet 15 - 20

Worksheet Detail - Combined Details 21 - 26

Worksheet Detail - Health Care Expense Schedule 27 - 29

Worksheet Detail - Retirement Distribution Cash Flow Chart 30 - 38

Worksheet Detail - Inside the Numbers Final Result 39

Worksheet Detail - Bear Market Test 40

Worksheet Detail - Special Asset Test 41

Worksheet Detail - Portfolio Probability Matrix 42

Worksheet Detail - Allocation Comparison 43 - 44

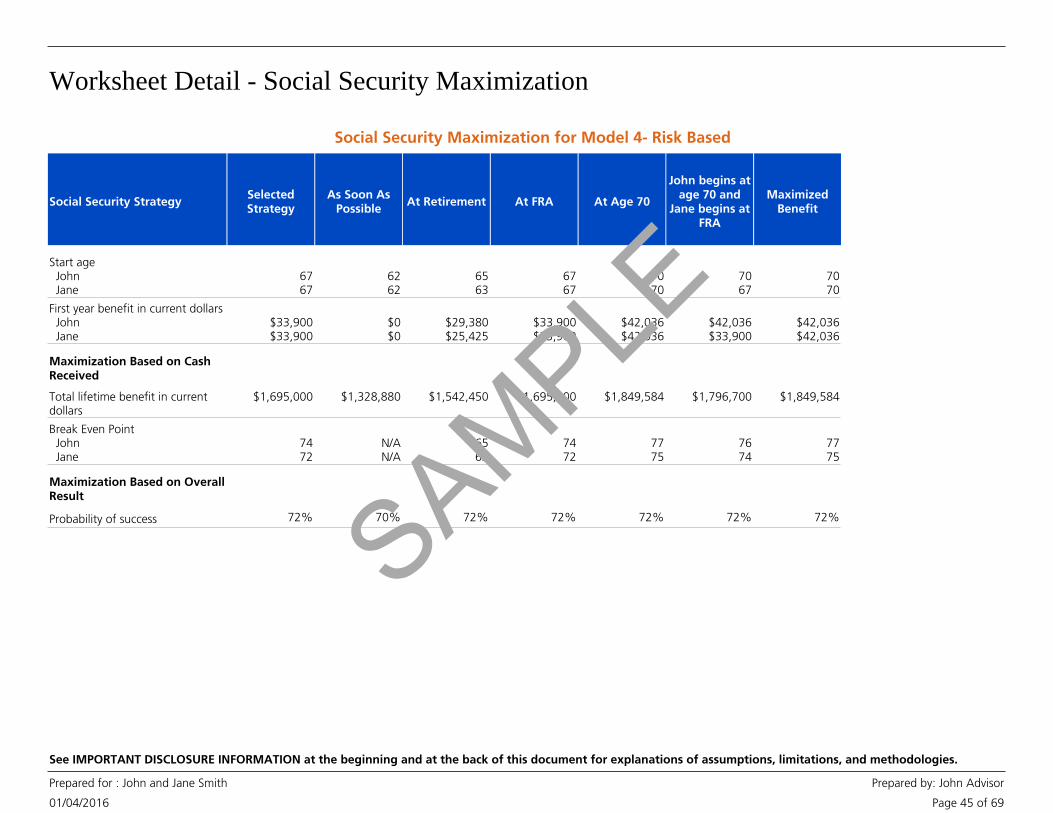

Worksheet Detail - Social Security Maximization 45 - 46

Employer Stock Plans

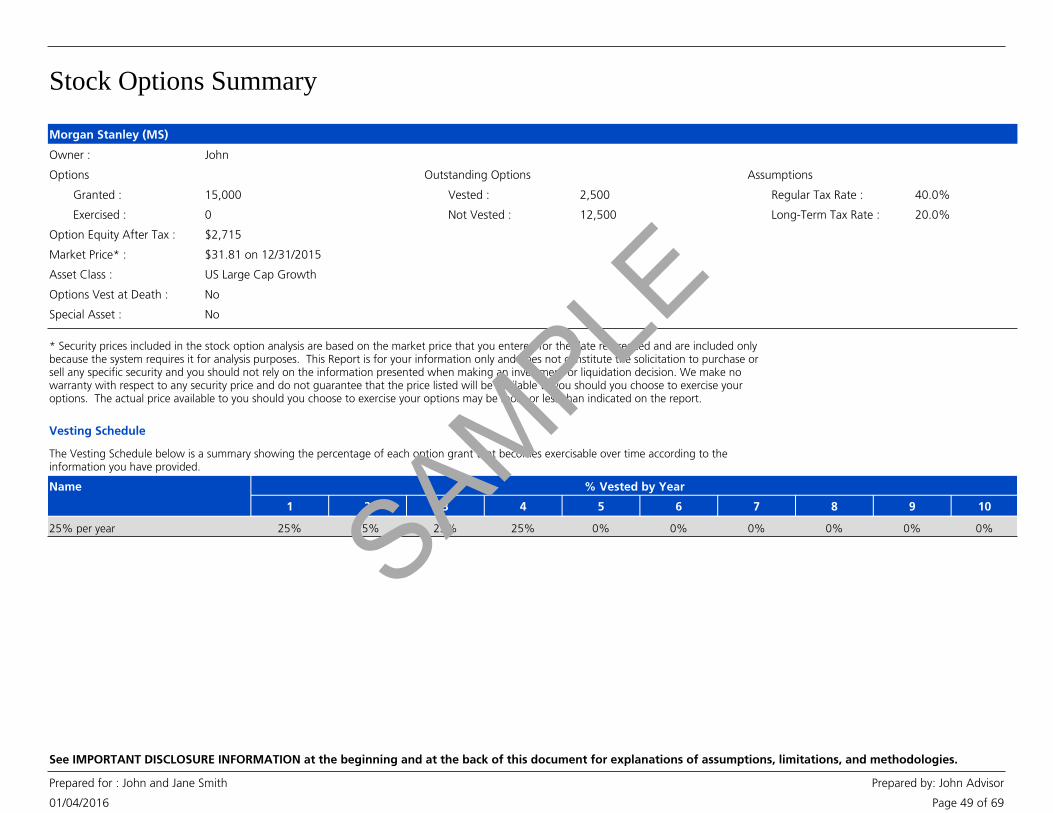

Stock Options 47 - 48

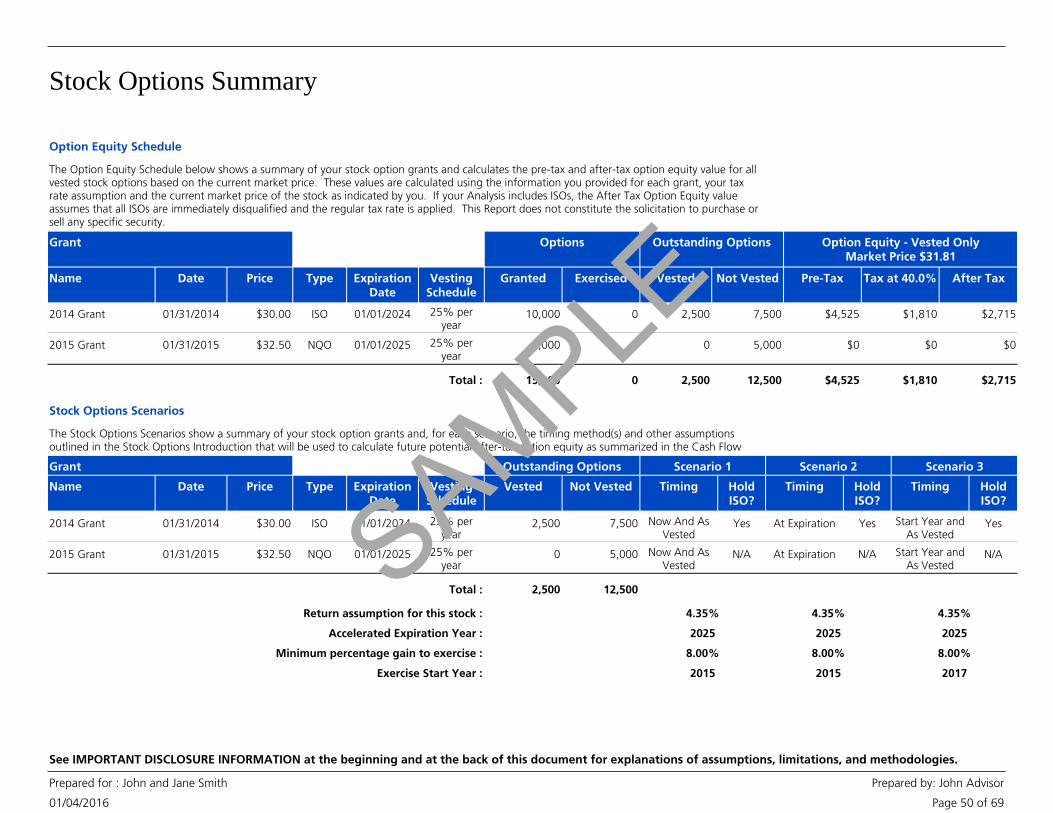

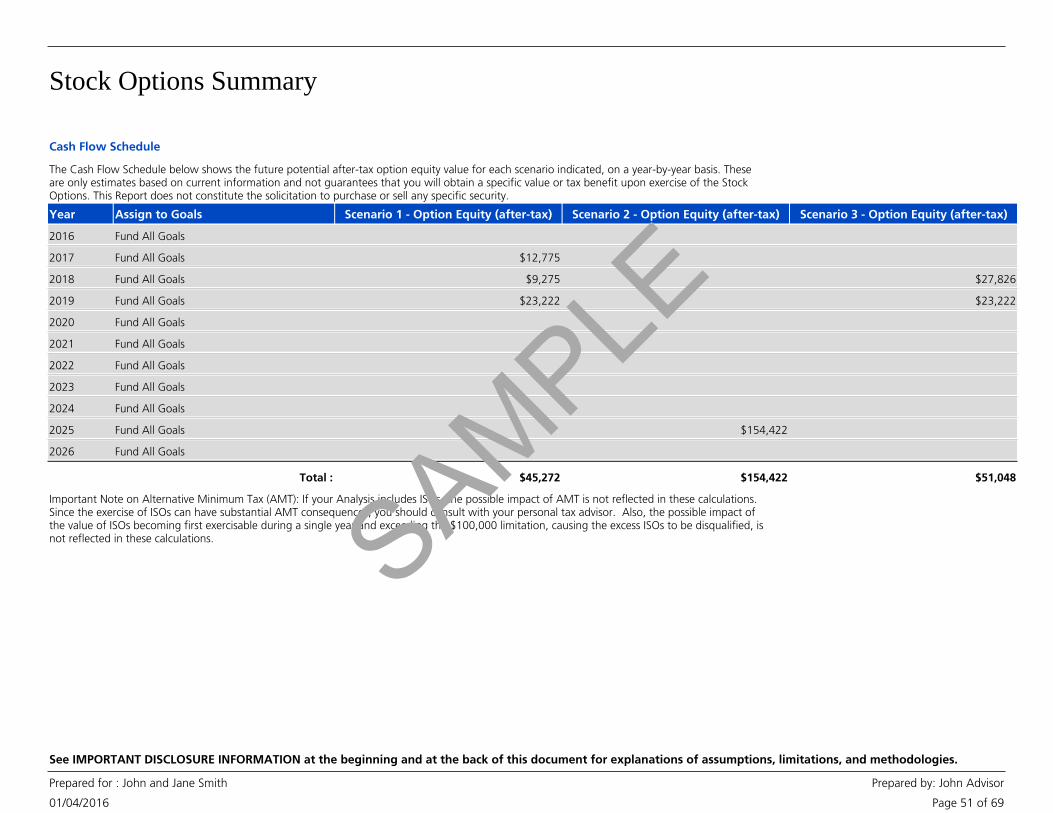

Stock Options Summary 49 - 51

Appendix

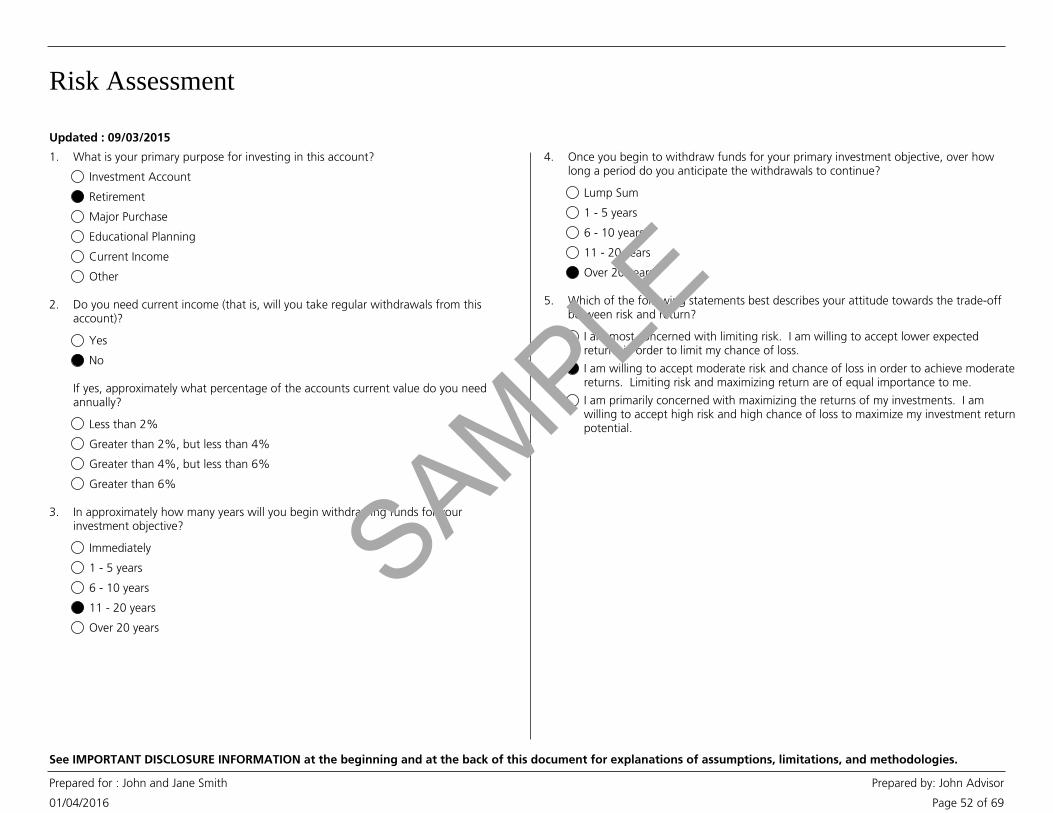

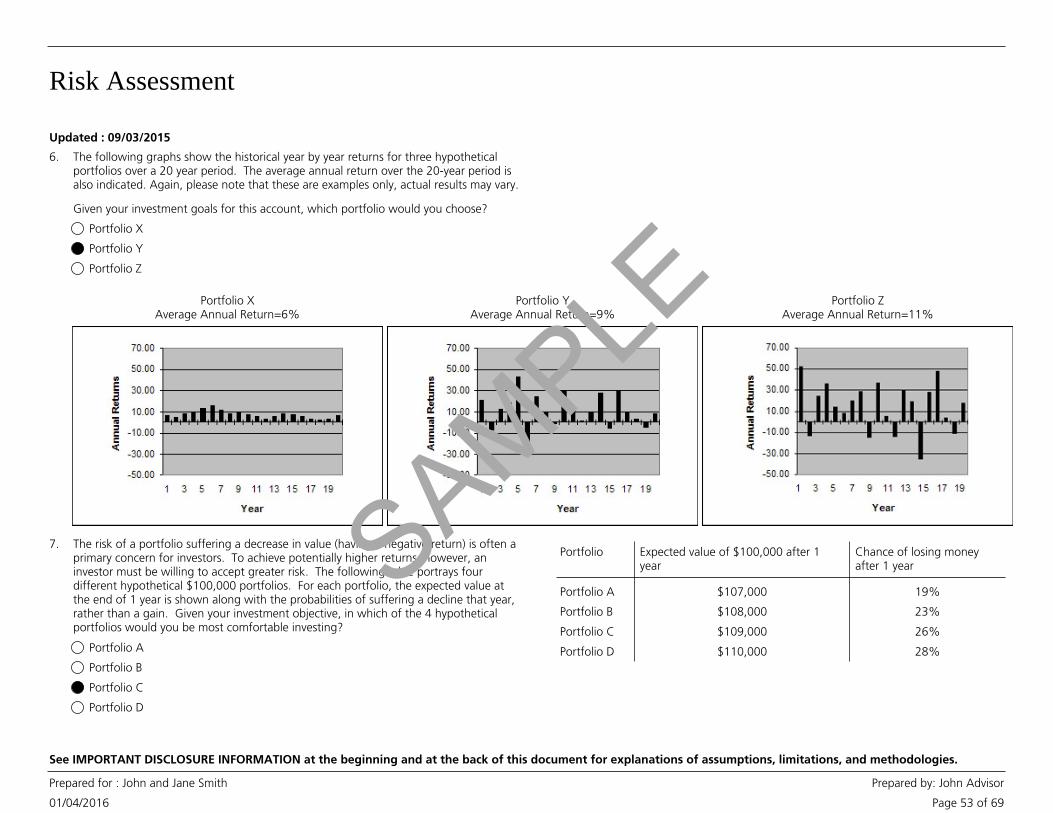

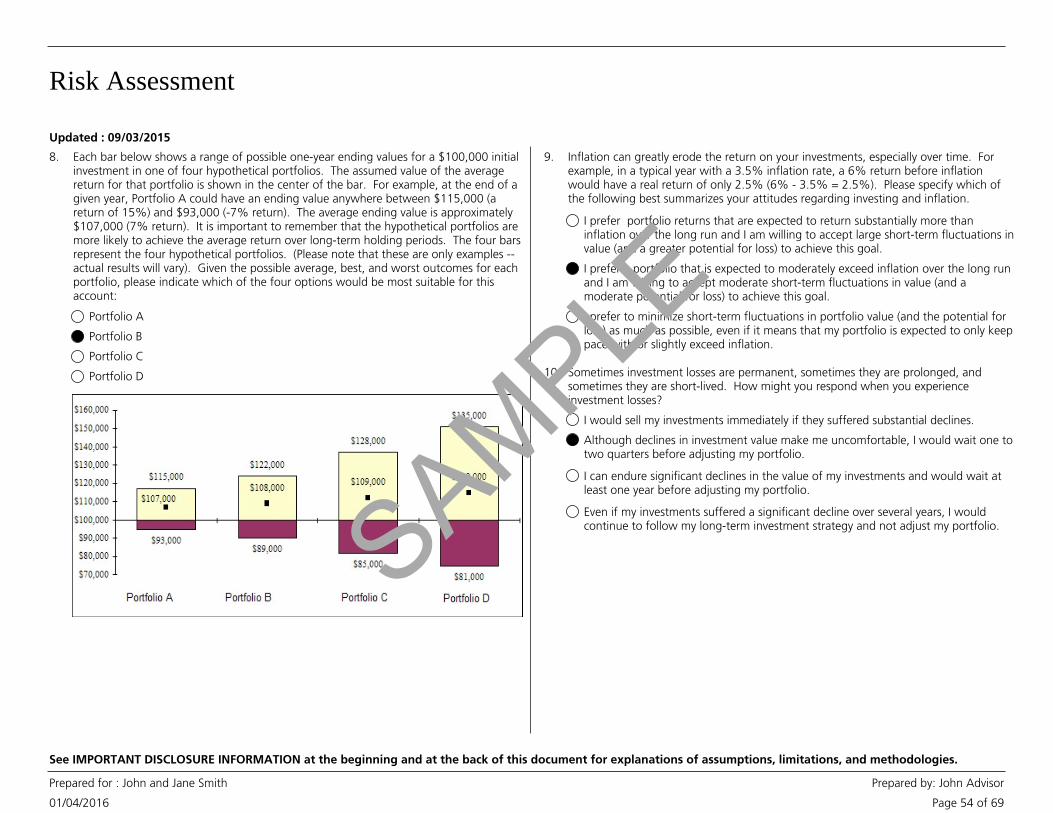

Risk Assessment 52 - 54

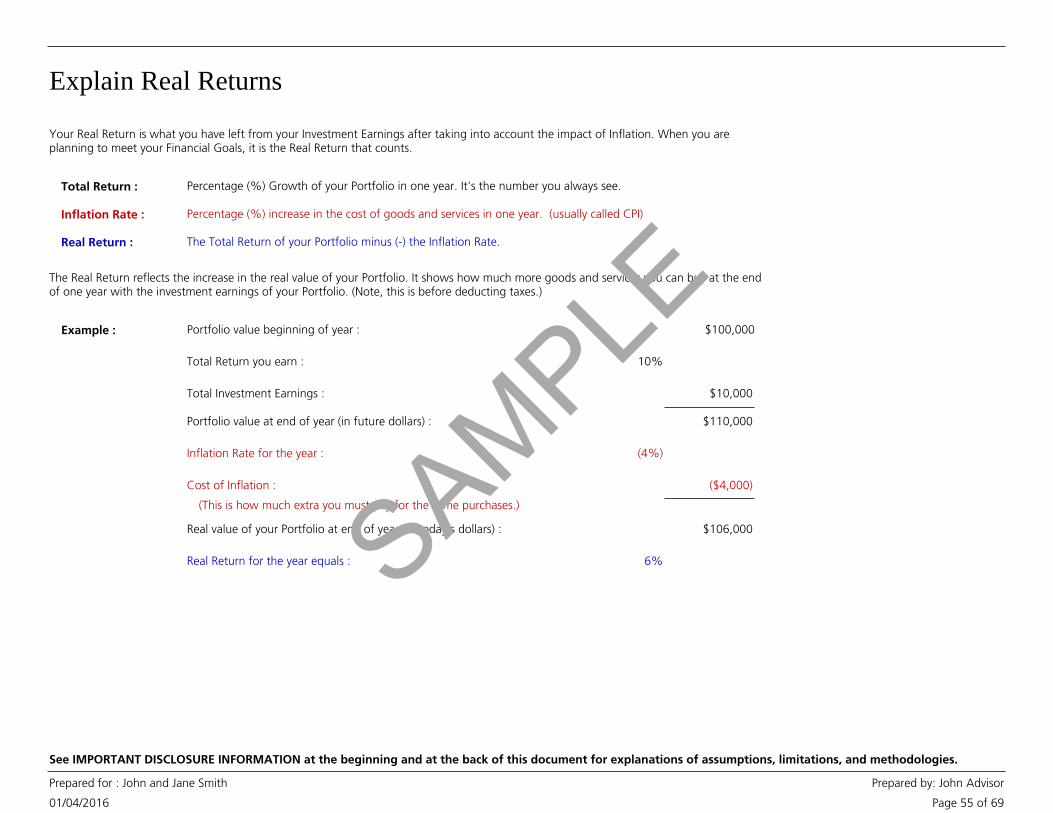

Explain Real Returns 55

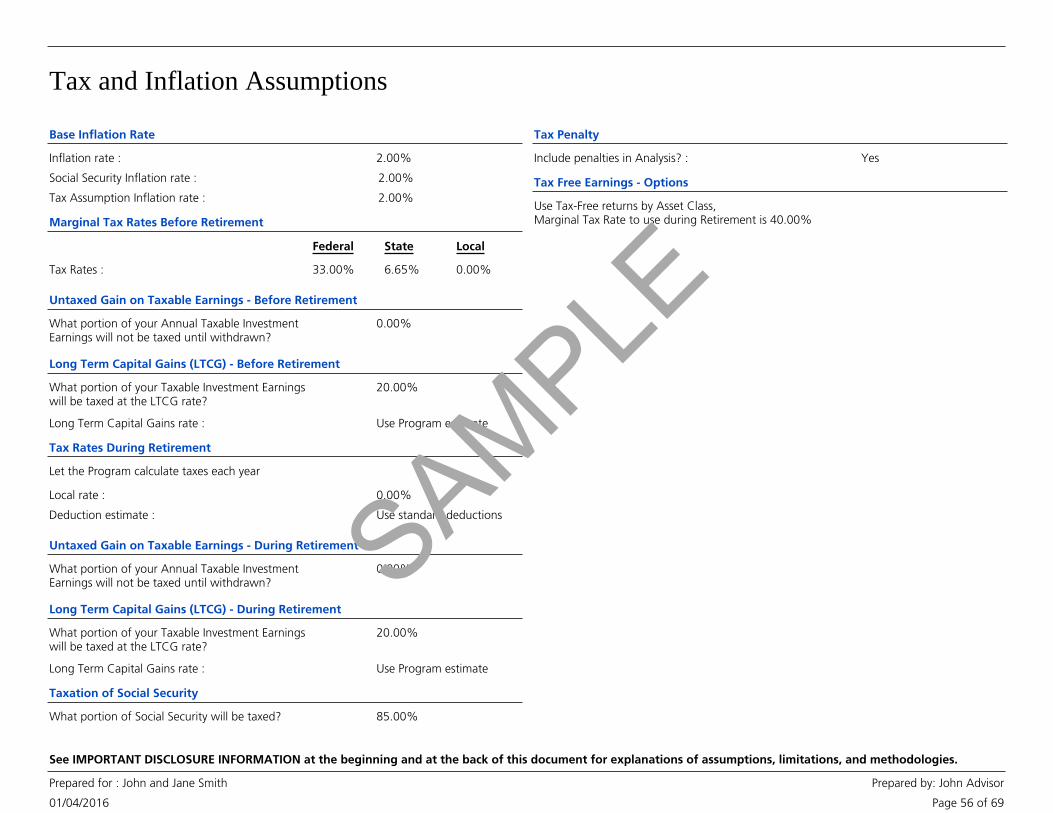

Tax and Inflation Assumptions 56

IMPORTANT DISCLOSURE INFORMATION 57 - 58

Return Methodology and Asset Allocation 59 - 62

Key Asset Class Risk Considerations 63 - 64

Glossary of Terms 65 - 69

SAMPLE

IMPORTANT DISCLOSURE INFORMATION

01/04/2016

Prepared for : John and Jane Smith Prepared by: John Advisor

Page 1 of 69

Information that you provided about your assets, financial goals, and personal situation arekey assumptions for the calculations and projections in this Report. Please review all theinformation thoroughly to ensure that it is correct and complete. In particular, please reviewthe Report sections titled "Personal Information and Summary of Financial Goals", CurrentPortfolio Allocation", and "Tax and Inflation Assumptions" to verify the accuracy of theseassumptions. If any of the assumptions are incorrect, you should notify your FinancialAdvisor. Even small changes in assumptions can have a substantial impact on the resultsshown in this Report. The information provided by you should be reviewed periodically andupdated when either the information or your circumstances change. Morgan Stanley has noresponsibility and is under no obligation to monitor or update this Report in the futureunless expressly engaged by you to do so at that time.

Information Provided by You

Every individual’s financial circumstances, needs and risk tolerances are different. ThisLifeView® Financial Goal Analysis (the "Report") is based on the information you providedto us, the assumptions you have asked us to make and the other assumptions indicatedherein as of the date of the Report. It is not an official account statement. The purpose oftaking the time to organize your financial life is to gain better control of your financialfuture. This Report should be considered a working document that can assist you with thisobjective. You should carefully review the information and suggestions found in this Reportand then decide on future steps.

Asset Allocation Information

LifeView Goal Analysis Assumptions and Limitations

LifeView Goal Analysis is powered by MoneyGuidePro®

IMPORTANT: The projections or other information generated by LifeView® GoalAnalysis regarding the likelihood of various investment outcomes (including anyassumed rates of return) are hypothetical in nature, do not reflect actualinvestment results, and are not guarantees of future results.

Any asset allocation information presented herein, which may take into account your assetsin one or more Employee Retirement Income Security Act of 1974, as amended("ERISA")-covered employee benefit plans and/or one or more individual retirementaccounts, is for general asset allocation education and information purposes only, andshould not be viewed as fiduciary investment advice or specific recommendations withrespect to any particular investment or asset allocation mix under the Investment AdvisersAct of 1940 as amended, ERISA, the Internal Revenue Code or any other applicable law. Inapplying any particular asset allocation model to your individual circumstances, you shouldconsider your other assets, income and investments, in addition to any interest(s) you mayhave in ERISA-covered employee benefit plans or individual retirement accounts. Thus, it isvery important for you to insure that you review this Report to make sure that it includes allof your assets, income and investments.

Assumptions and Limitations

LifeView Goal Analysis offers several methods of calculating results, each of which providesone outcome from a wide range of possible outcomes. LifeView Goal Analysis does notpurport to recommend or implement an investment strategy. Financial forecasts, rates ofreturn, risk, inflation, and other assumptions may be used as the basis for illustrations inLifeView Goal Analysis. They should not be considered a guarantee of future performanceor a guarantee of achieving overall financial objectives. All results use simplifying estimatesand assumptions that are not tailored to your specific circumstances. No Report has theability to accurately predict the future, eliminate risk or guarantee investment results. Asinvestment returns, inflation, taxes, and other economic conditions vary from the LifeViewGoal Analysis assumptions, your actual results will vary (perhaps significantly) from thosepresented in this Report.

The assumed return rates in LifeView Goal Analysis are not reflective of any specificinvestment and do not include any fees or expenses that may be incurred by investing inspecific products. The actual returns of a specific investment may be more or less than thereturns used in LifeView Goal Analysis. The return assumptions are based on historic rates ofreturn of securities indices which serve as proxies for the broad asset classes. It is notpossible to directly invest in an index. Moreover, different forecasts may choose differentindices as a proxy for the same asset class, thus influencing the return of the asset class.LifeView Goal Analysis results may vary with each use and over time.

SAMPLE

IMPORTANT DISCLOSURE INFORMATION

01/04/2016

Prepared for : John and Jane Smith Prepared by: John Advisor

Page 2 of 69

Morgan Stanley cannot give any assurances that any estimates, assumptions orother aspects of the analyses will prove correct. They are subject to actual knownand unknown risks, uncertainties and other factors that could cause actual resultsto differ materially from those shown.

These analyses speak only as of the date of this Report. Morgan Stanley expresslydisclaims any obligation or undertaking to update or revise any statement or otherinformation contained herein to reflect any change in past results, futureexpectations or circumstances upon which that statement or other information isbased.

Rate of Return Methodology

The analysis contained in the Report is conducted using the Morgan Stanley WealthManagement Global Investment Committee’s Secular Return Estimates (“GIC Estimate”).GIC Estimate approved returns are generated based on proprietary formulas which includestudying historical return averages of the broad market indices and making strategicadjustments for more recent market conditions and other factors deemed relevant by theforecaster. The Return Methodology and Asset Allocation sections include a description ofthe return methodology that has been used to prepare this Report. The methodology shouldbe carefully considered in evaluating the results presented to you.

LifeView Goal Analysis is powered by MoneyGuidePro®

The return assumptions used in this Report are estimates based on average annual returnsfor the index used as a proxy for each asset class. The portfolio returns are calculated byweighting individual return assumptions for each asset class according to your portfolioallocation. During the preparation of these analyses, your Morgan Stanley Financial Advisormay have refined the asset allocation strategy to develop a strategy which optimizes thepotential returns that could be achieved with the appropriate level of risk that you would bewilling to assume. Asset classes not included may have characteristics similar or superior tothose being analyzed.

Hypothetical performance results have inherent limitations. There are frequently largedifferences between hypothetical and actual performance results subsequently achieved byany particular asset allocation or trading strategy. Hypothetical performance results do notrepresent actual trading and are generally designed with the benefit of hindsight. Theycannot account for all factors associated with risk, including the impact of financial risk inactual trading or the ability to withstand losses or to adhere to a particular trading strategyin the face of trading losses. There are numerous other factors related to the markets ingeneral or to the implementation of any specific trading strategy that cannot be fullyaccounted for in the preparation of hypothetical performance results and all of which canadversely affect actual trading results.

Monte Carlo simulations are used to show how variations in rates of return each year canaffect your results. A Monte Carlo simulation calculates the results of your Plan by runningit many times, each time using a different sequence of returns. Some sequences of returnswill give you better results, and some will give you worse results. These multiple trialsprovide a range of possible results, some successful (you would have met all your goals) andsome unsuccessful (you would not have met all your goals). The percentage of trials thatwere successful is shown as the probability that your Plan, with all its underlyingassumptions, could be successful. In LifeView Goal Analysis, this is the Probability ofSuccess. Analogously, the percentage of trials that were unsuccessful is shown as theProbability of Failure. The Results Using Monte Carlo Simulations indicate the likelihoodthat an event may occur as well as the likelihood that it may not occur. In analyzing thisinformation, please note that the analysis does not take into account actual marketconditions, which may severely affect the outcome of your goals over the long-term.

Results Using Monte Carlo Simulations

SAMPLE

IMPORTANT DISCLOSURE INFORMATION

01/04/2016

Prepared for : John and Jane Smith Prepared by: John Advisor

Page 3 of 69

IMPORTANT NOTES AND DISCLOSURES FROM MORGAN STANLEY

Morgan Stanley provides its existing and prospective brokerage customers with a number offinancial tools that produce certain reports to assist customers in managing their wealth andassets. These tools generate reports that include this Report. This Report is generated byusing a computer software program developed by MoneyGuidePro, a third party softwareprovider. Results may vary with each use of the software and over time. Enhancementsand changes to the software may be made in the future. Morgan Stanley is not responsiblefor the accuracy of the assumptions made in the Report, or the calculations in the analyses.Future Reports may contain information capabilities and other content that is moreexpansive or otherwise different from the content of this Report.

This Report creates a brokerage relationship among you, your Financial Advisor and MorganStanley. You should understand the differences between a brokerage and advisoryrelationship. When providing you brokerage services, our legal obligations to you aregoverned by the Securities Act of 1933, the Securities Exchange Act of 1934, the rules ofself-regulatory organizations such as the Financial Industry Regulatory Authority (FINRA),and state securities laws, where applicable. When providing you advisory services, our legalobligations to you are governed by the Investment Advisers Act and applicable statesecurities laws. These latter advisory obligations govern our conduct and disclosurerequirements, creating a legal standard which is referred to as a “fiduciary” duty to you.Please ask your Financial Advisor questions to make sure you understand your rights and ourobligations to you, including the extent of our obligations to disclose conflicts of interestand to act in your best interest. For additional answers to questions about the differencesbetween our advisory and brokerage services, please visit our web site athttp://www.morganstanley.com/ourcommitment/ or contact us at 866-866-7426.

Morgan Stanley is both a registered broker-dealer and investment adviser and its FinancialAdvisors act in dual capacities as broker-dealer and investment advisory representatives.Many Morgan Stanley Financial Advisors may use the designation Certified Financial Planneror "CFP," a certification mark owned by the Certified Financial Planner Board of Standards,Inc. Each of these Financial Advisors also is licensed to act as a broker-dealer representativeon behalf of Morgan Stanley. When any of these Financial Advisors assists clients byproviding them a LifeView® Financial Plan, he/she is doing so as a CFP and investmentadvisory representative of Morgan Stanley. However, in providing other services tocustomers, such as assisting customers in implementing a Financial Plan once it has beendelivered, providing financial tools/reports to customers, or effecting transactions for thecustomer's brokerage account, the Financial Advisor carrying a CFP designation is onlyacting as a broker-dealer representative unless the Financial Advisor and client have enteredinto a written agreement that creates an investment advisory relationship.

This Report is not a financial plan. A financial plan generally seeks to address a widespectrum of your long-term financial needs, and can include recommendations aboutinsurance, savings, tax and estate planning, and investments, taking into consideration yourgoals and situation, including anticipated retirement or other employee benefits. MorganStanley will only prepare a financial plan at your specific request using Morgan Stanleyapproved financial planning software where you will enter into a written agreement with aFinancial Advisor, such as Morgan Stanley LifeView® Advisor. If you would like to have afinancial plan prepared for you, please consult with your Financial Advisor.

This Report does not constitute an offer to buy, sell, or recommend any particularinvestment or asset, nor does it recommend that you engage in any particular investment,manager or trading strategy. It reflects only allocations among broad asset classes. Allinvestments have risks. The decisions as to when and how to invest are solely yourresponsibility.

By providing you this Report, neither Morgan Stanley nor your Financial Advisorare acting as a fiduciary for purposes of the Investment Advisers Act of 1940, asamended (the “Investment Advisers Act”), ERISA or section 4975 of the Code withrespect to any ERISA-covered employee benefit plan or any individual retirementaccount in either the planning, execution or provision of this analysis. Unlessotherwise provided in a written agreement between you and Morgan Stanley,Morgan Stanley, its affiliates and their respective employees, agents andrepresentatives, including your Financial Advisor, (a) do not have discretionaryauthority or control with respect to the assets in any ERISA-covered employeebenefit plan or any individual retirement account included in this Report, (b) willnot be deemed an "investment manager" as defined under ERISA, or otherwisehave the authority or responsibility to act as a "fiduciary" (as defined under ERISA,the Investment Advisers Act or other applicable law) with respect to such assets,and (c) will not provide "investment advice," as defined by ERISA and/or section4975 of the Internal Revenue Code, as amended, with respect to such assets.

Please keep in mind that Morgan Stanley is not a tax or legal advisor and this Report doesnot constitute tax, legal or accounting advice. You should discuss any tax and legalinformation outlined in this document with your accounting, tax and legal advisors prior totaking action. Your Morgan Stanley Financial Advisor can work with you and these advisorsto answer your questions and, if you choose, help you implement the options you decideupon. There is no requirement, however, that you implement any strategies at all. Inaddition, you are not obligated to implement any options shown in this Report or tootherwise conduct business through Morgan Stanley or its affiliates.

Timing for implementing, monitoring and adjusting your strategies is a critical element inachieving your financial objectives. You are responsible for implementing, monitoring andperiodically reviewing and adjusting your investment strategies.

SAMPLE

IMPORTANT DISCLOSURE INFORMATION

01/04/2016

Prepared for : John and Jane Smith Prepared by: John Advisor

Page 4 of 69

IMPORTANT NOTES AND DISCLOSURES FROM MORGAN STANLEY (continued)

Powered by MoneyGuidePro® and MoneyGuidePro® are marks of PIEtech, Inc.

By accepting delivery of this Report, you are deemed to acknowledge and agree that:

1) you have reviewed and accept the information contained within this Report andunderstand the disclaimers, assumptions and methods included with it;

2) you believe that all information provided by you is complete and accurate to the best ofyour knowledge;

3) you recognize that all investments have risks; that performance and attainment offinancial objectives are not guaranteed; and that all estimates and assumed data, includingreturns, are included only for general education and do not represent a forecast of futureevents or results;

4) you understand that this Report was generated using a brokerage tool, is not a financialplan and created a brokerage (not advisory) relationship among you, your Financial Advisorand Morgan Stanley that governed the preparation of this Report and ended upon receiptof this Report;

6) you understand that Morgan Stanley is not a legal or tax advisor and that this Reportdoes not constitute tax, legal, or accounting advice.

© 2012 Morgan Stanley Smith Barney LLC. Member SIPC.

5) you understand that Morgan Stanley and your Financial Advisor are not fiduciaries underERISA or the Internal Revenue Code with respect to this Report or your use or our use (onyour behalf) of the software which generated this Report, or your IRA and retirement planaccounts unless otherwise provided in a written agreement between you and MorganStanley. The information in this Report is provided to you on the understanding that, forpurposes of ERISA and the Code, it is intended to be educational material, will not form aprimary basis for any investment decision made by you or on your behalf, and will not beviewed for ERISA or Code purposes as fiduciary investment advice or specificrecommendations with respect to asset allocation or any particular investment, and that(unless otherwise provided in a written agreement) you remain solely responsible for yourassets and all investment decisions with respect to your assets; andSAMPLE

Summary of Goals and Resources

SAMPLE

Personal Information and Summary of Financial Goals

01/04/2016

Prepared for : John and Jane Smith Prepared by: John Advisor

Page 5 of 69

See IMPORTANT DISCLOSURE INFORMATION at the beginning and at the back of this document for explanations of assumptions, limitations, and methodologies.

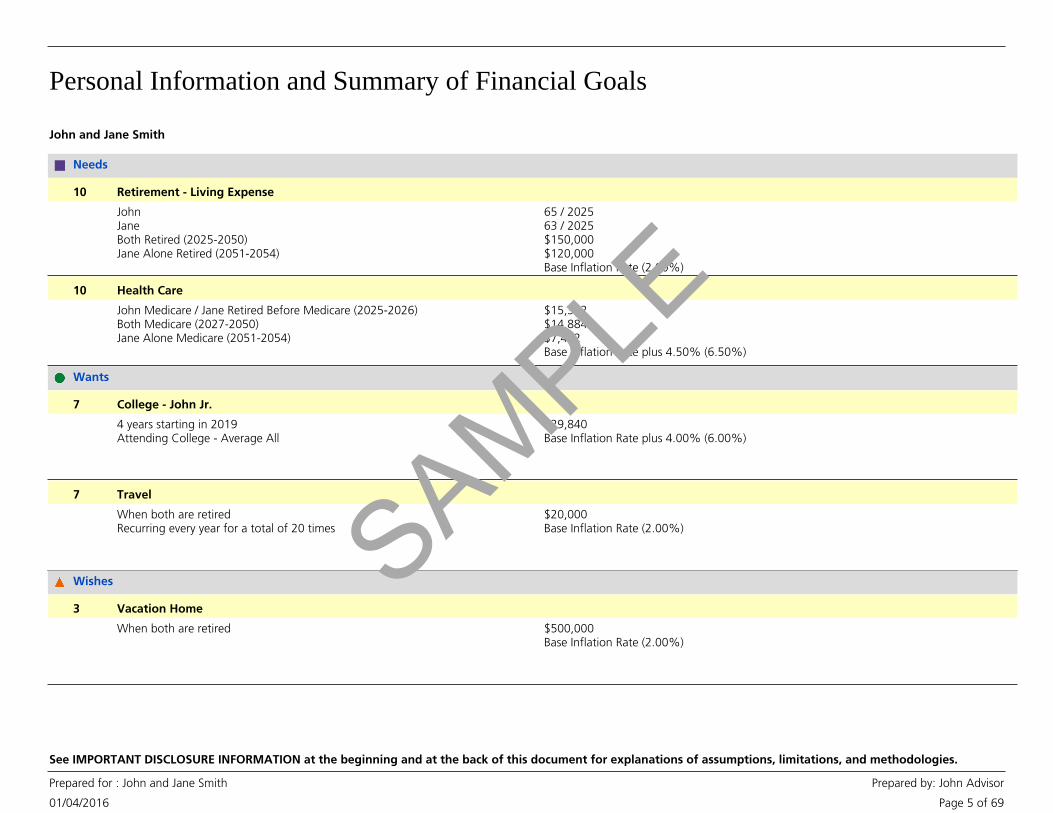

John and Jane Smith

Needs

Retirement - Living Expense10

JohnJaneBoth Retired (2025-2050)Jane Alone Retired (2051-2054)

65 / 202563 / 2025$150,000$120,000Base Inflation Rate (2.00%)

Health Care10

John Medicare / Jane Retired Before Medicare (2025-2026)Both Medicare (2027-2050)Jane Alone Medicare (2051-2054)

$15,302$14,884$7,442Base Inflation Rate plus 4.50% (6.50%)

Wants

College - John Jr.7

4 years starting in 2019Attending College - Average All

$29,840Base Inflation Rate plus 4.00% (6.00%)

Travel7

When both are retiredRecurring every year for a total of 20 times

$20,000Base Inflation Rate (2.00%)

Wishes

Vacation Home3

When both are retired $500,000Base Inflation Rate (2.00%)

SAMPLE

Personal Information and Summary of Financial Goals

01/04/2016

Prepared for : John and Jane Smith Prepared by: John Advisor

Page 6 of 69

See IMPORTANT DISCLOSURE INFORMATION at the beginning and at the back of this document for explanations of assumptions, limitations, and methodologies.

Personal Information

John

Male - born 05/22/1960, age 55

Jane

Female - born 08/07/1962, age 53

Married, US Citizens living in NY

Employed - $150,000

Employed - $150,000

• This section lists the Personal and Financial Goal information you provided, which willbe used to create your Report. It is important that it is accurate and complete.

Participant Name Date of Birth Age Relationship

John Jr. 02/01/2001 14 Child

SAMPLE

Net Worth Summary - All Resources

01/04/2016

Prepared for : John and Jane Smith Prepared by: John Advisor

Page 7 of 69

See IMPORTANT DISCLOSURE INFORMATION at the beginning and at the back of this document for explanations of assumptions, limitations, and methodologies.

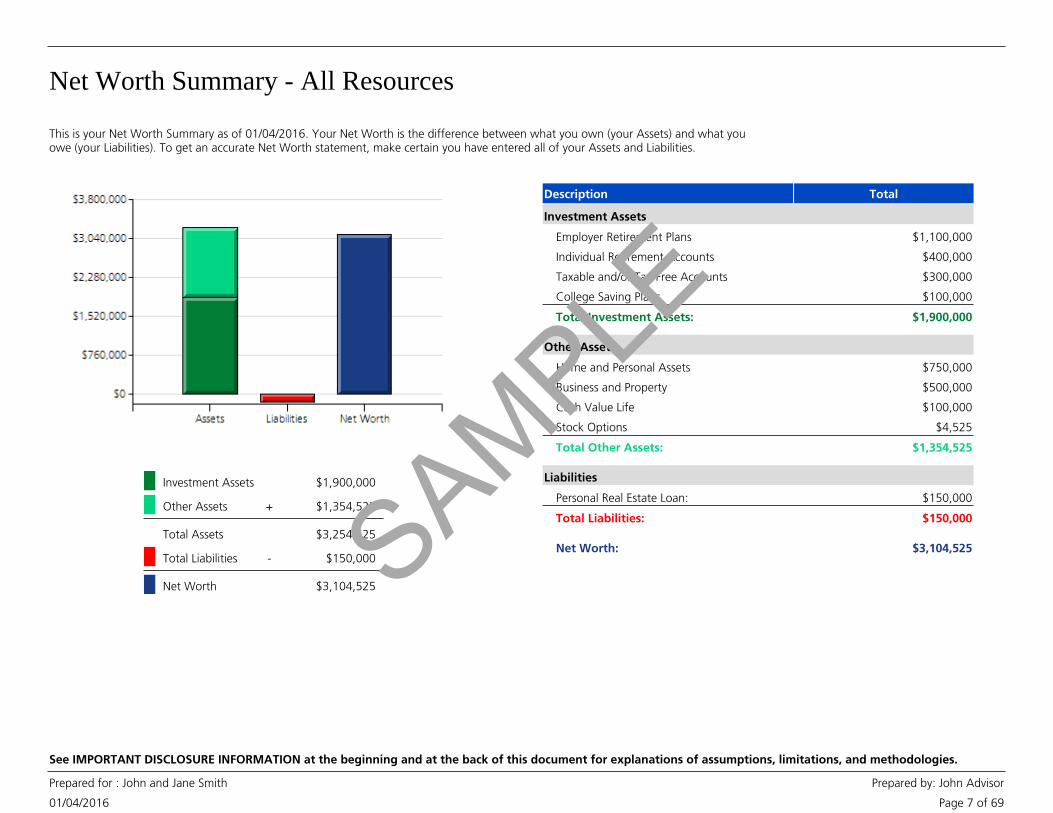

This is your Net Worth Summary as of 01/04/2016. Your Net Worth is the difference between what you own (your Assets) and what youowe (your Liabilities). To get an accurate Net Worth statement, make certain you have entered all of your Assets and Liabilities.

+ $1,354,525Other Assets

Investment Assets $1,900,000

Total Liabilities $150,000

Net Worth $3,104,525

$3,254,525Total Assets

-

Description Total

Investment Assets

Employer Retirement Plans $1,100,000

Individual Retirement Accounts $400,000

Taxable and/or Tax-Free Accounts $300,000

College Saving Plans $100,000

Total Investment Assets: $1,900,000

Other Assets

Home and Personal Assets $750,000

Business and Property $500,000

Cash Value Life $100,000

Stock Options $4,525

Total Other Assets: $1,354,525

Liabilities

Personal Real Estate Loan: $150,000

Total Liabilities: $150,000

Net Worth: $3,104,525SAMPLE

Net Worth Detail - All Resources

01/04/2016

Prepared for : John and Jane Smith Prepared by: John Advisor

Page 8 of 69

See IMPORTANT DISCLOSURE INFORMATION at the beginning and at the back of this document for explanations of assumptions, limitations, and methodologies.

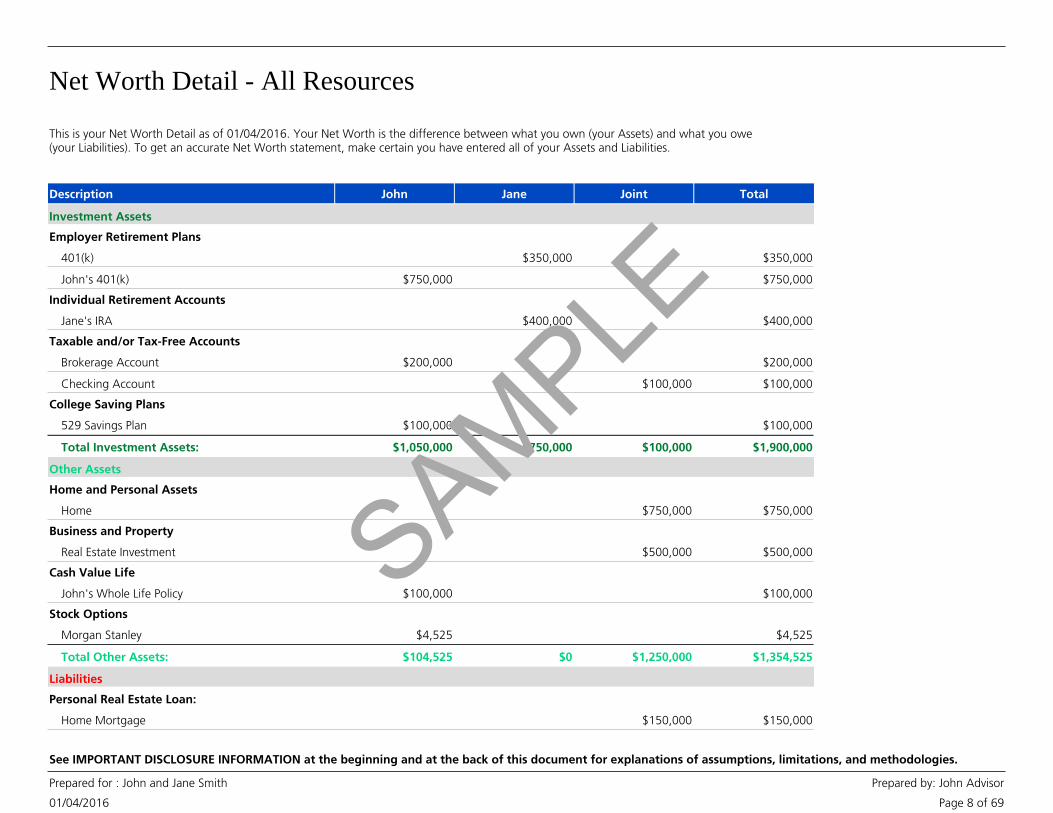

This is your Net Worth Detail as of 01/04/2016. Your Net Worth is the difference between what you own (your Assets) and what you owe(your Liabilities). To get an accurate Net Worth statement, make certain you have entered all of your Assets and Liabilities.

Description TotalJointJaneJohn

Investment Assets

Employer Retirement Plans

401(k) $350,000$350,000

John's 401(k) $750,000$750,000

Individual Retirement Accounts

Jane's IRA $400,000$400,000

Taxable and/or Tax-Free Accounts

Brokerage Account $200,000$200,000

Checking Account $100,000$100,000

College Saving Plans

529 Savings Plan $100,000$100,000

Total Investment Assets: $1,900,000$1,050,000 $750,000 $100,000

Other Assets

Home and Personal Assets

Home $750,000$750,000

Business and Property

Real Estate Investment $500,000$500,000

Cash Value Life

John's Whole Life Policy $100,000$100,000

Stock Options

Morgan Stanley $4,525$4,525

Total Other Assets: $1,354,525$104,525 $0 $1,250,000

Liabilities

Personal Real Estate Loan:

Home Mortgage $150,000$150,000

SAMPLE

Net Worth Detail - All Resources

01/04/2016

Prepared for : John and Jane Smith Prepared by: John Advisor

Page 9 of 69

See IMPORTANT DISCLOSURE INFORMATION at the beginning and at the back of this document for explanations of assumptions, limitations, and methodologies.

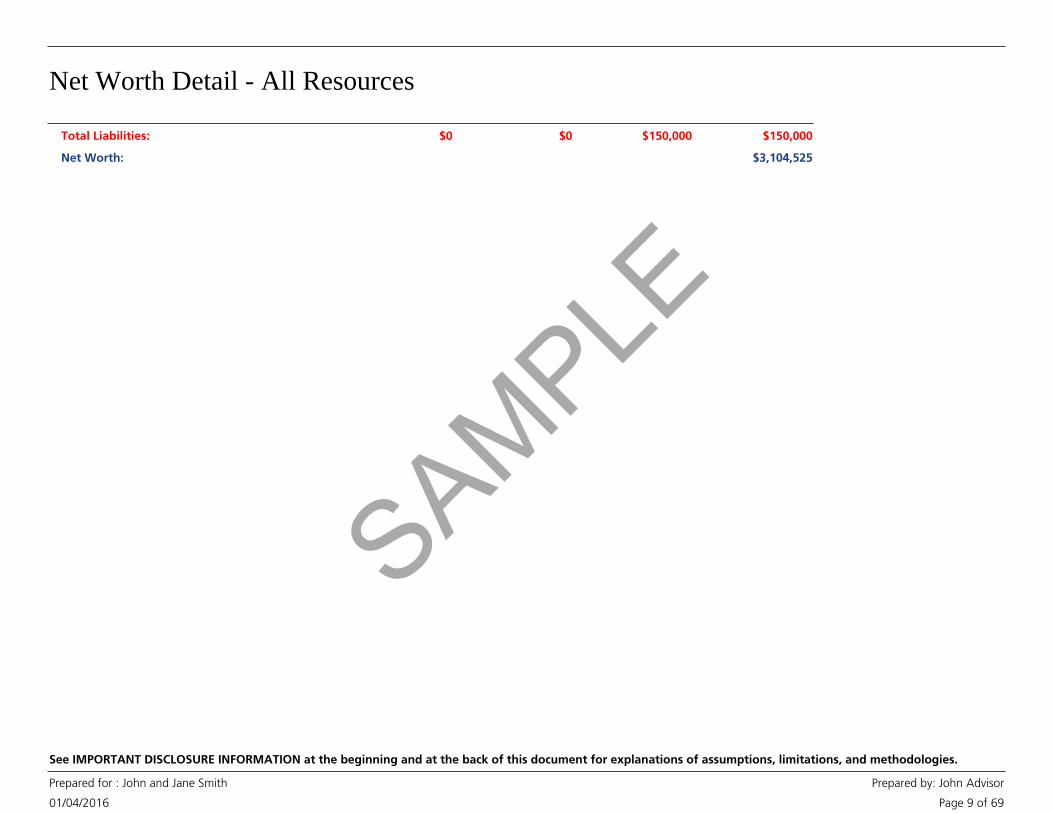

Total Liabilities: $150,000$0 $0 $150,000

Net Worth: $3,104,525

SAMPLE

Resources Summary

01/04/2016

Prepared for : John and Jane Smith Prepared by: John Advisor

Page 10 of 69

See IMPORTANT DISCLOSURE INFORMATION at the beginning and at the back of this document for explanations of assumptions, limitations, and methodologies.

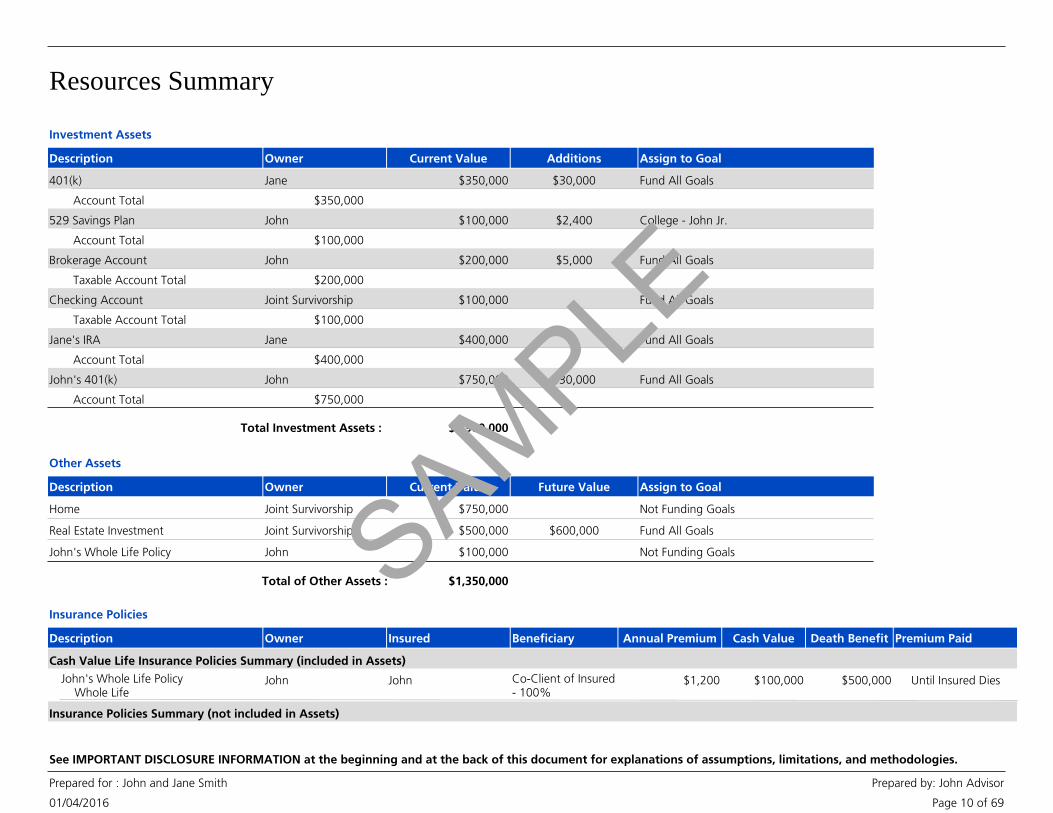

Description Owner Current Value Additions Assign to Goal

Investment Assets

Jane401(k) $350,000 $30,000 Fund All Goals

$350,000Account Total

John529 Savings Plan $100,000 $2,400 College - John Jr.

$100,000Account Total

JohnBrokerage Account $200,000 $5,000 Fund All Goals

$200,000Taxable Account Total

Joint SurvivorshipChecking Account $100,000 Fund All Goals

$100,000Taxable Account Total

JaneJane's IRA $400,000 Fund All Goals

$400,000Account Total

JohnJohn's 401(k) $750,000 $30,000 Fund All Goals

$750,000Account Total

$1,900,000Total Investment Assets :

Description Owner Current Value Future Value Assign to Goal

Other Assets

Home Joint Survivorship $750,000 Not Funding Goals

Real Estate Investment Joint Survivorship $500,000 $600,000 Fund All Goals

John's Whole Life Policy John $100,000 Not Funding Goals

$1,350,000Total of Other Assets :

Annual Premium Cash ValueDescription Owner BeneficiaryInsured Death Benefit Premium Paid

Insurance Policies

Cash Value Life Insurance Policies Summary (included in Assets)

$1,200 $100,000John's Whole Life Policy Whole Life

John Co-Client of Insured- 100%

John $500,000 Until Insured Dies

Insurance Policies Summary (not included in Assets)

SAMPLE

Resources Summary

01/04/2016

Prepared for : John and Jane Smith Prepared by: John Advisor

Page 11 of 69

See IMPORTANT DISCLOSURE INFORMATION at the beginning and at the back of this document for explanations of assumptions, limitations, and methodologies.

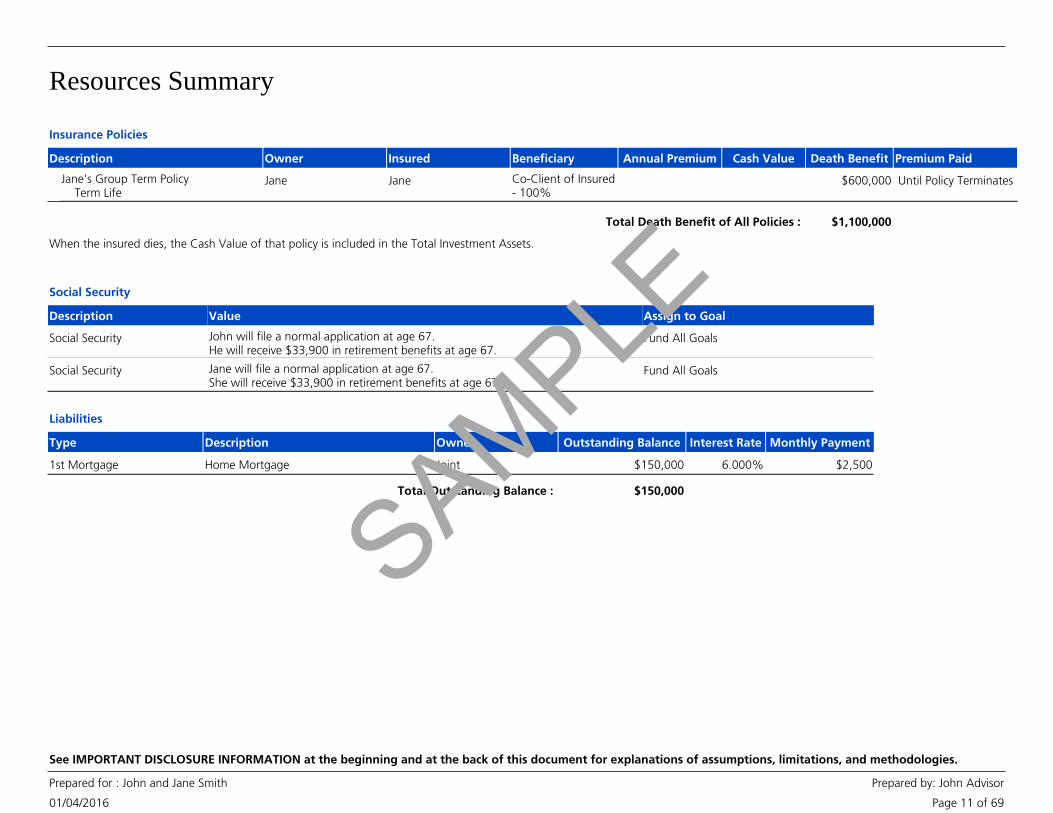

Annual Premium Cash ValueDescription Owner BeneficiaryInsured Death Benefit Premium Paid

Insurance Policies

Jane's Group Term Policy Term Life

Jane Co-Client of Insured- 100%

Jane $600,000 Until Policy Terminates

$1,100,000Total Death Benefit of All Policies :

When the insured dies, the Cash Value of that policy is included in the Total Investment Assets.

Social Security

Description Value Assign to Goal

Social Security John will file a normal application at age 67.He will receive $33,900 in retirement benefits at age 67.

Fund All Goals

Social Security Jane will file a normal application at age 67.She will receive $33,900 in retirement benefits at age 67.

Fund All Goals

Type Outstanding Balance Monthly PaymentDescription Interest RateOwner

Liabilities

1st Mortgage Home Mortgage $150,000 $2,5006.000%Joint

$150,000Total Outstanding Balance :

SAMPLE

Current Portfolio Allocation

01/04/2016

Prepared for : John and Jane Smith Prepared by: John Advisor

Page 12 of 69

See IMPORTANT DISCLOSURE INFORMATION at the beginning and at the back of this document for explanations of assumptions, limitations, and methodologies.

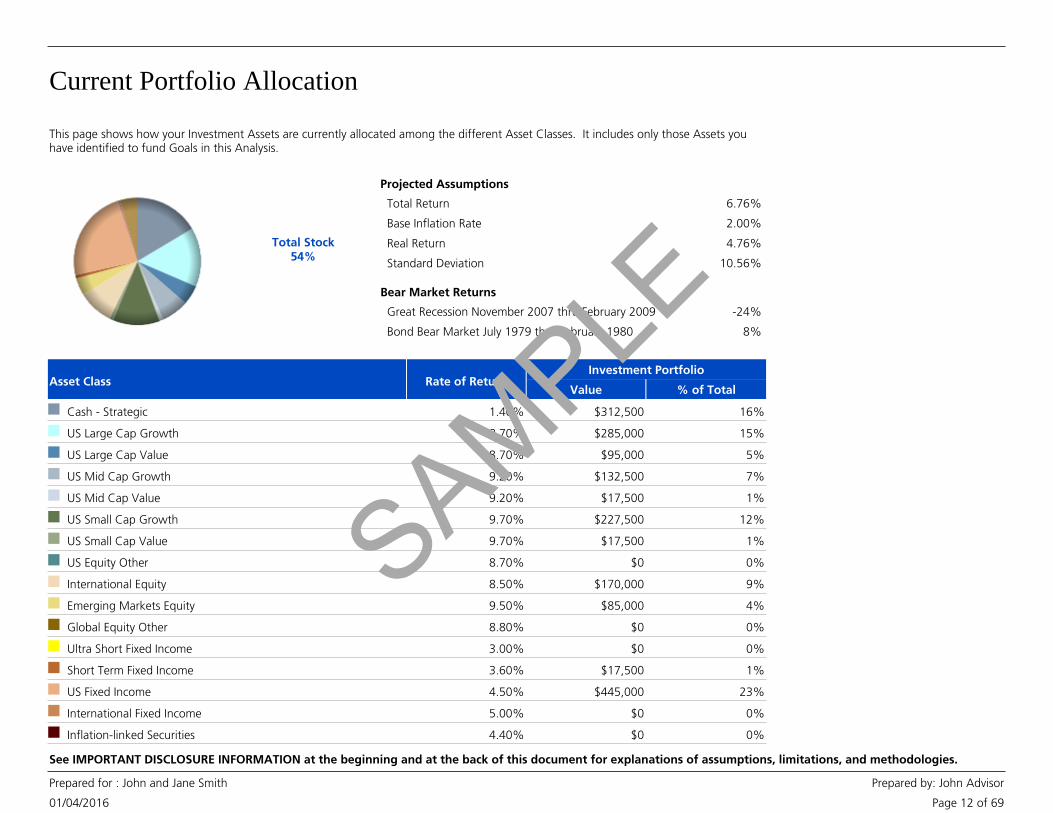

Total Stock54%

This page shows how your Investment Assets are currently allocated among the different Asset Classes. It includes only those Assets youhave identified to fund Goals in this Analysis.

Projected Assumptions

Total Return 6.76%

Base Inflation Rate 2.00%

Real Return 4.76%

Standard Deviation 10.56%

Bear Market Returns

Great Recession November 2007 thru February 2009 -24%

Bond Bear Market July 1979 thru February 1980 8%

Asset Class Rate of ReturnValue % of Total

Investment Portfolio

16%$312,5001.40%Cash - Strategic

15%$285,0008.70%US Large Cap Growth

5%$95,0008.70%US Large Cap Value

7%$132,5009.20%US Mid Cap Growth

1%$17,5009.20%US Mid Cap Value

12%$227,5009.70%US Small Cap Growth

1%$17,5009.70%US Small Cap Value

0%$08.70%US Equity Other

9%$170,0008.50%International Equity

4%$85,0009.50%Emerging Markets Equity

0%$08.80%Global Equity Other

0%$03.00%Ultra Short Fixed Income

1%$17,5003.60%Short Term Fixed Income

23%$445,0004.50%US Fixed Income

0%$05.00%International Fixed Income

0%$04.40%Inflation-linked Securities

SAMPLE

Current Portfolio Allocation

01/04/2016

Prepared for : John and Jane Smith Prepared by: John Advisor

Page 13 of 69

See IMPORTANT DISCLOSURE INFORMATION at the beginning and at the back of this document for explanations of assumptions, limitations, and methodologies.

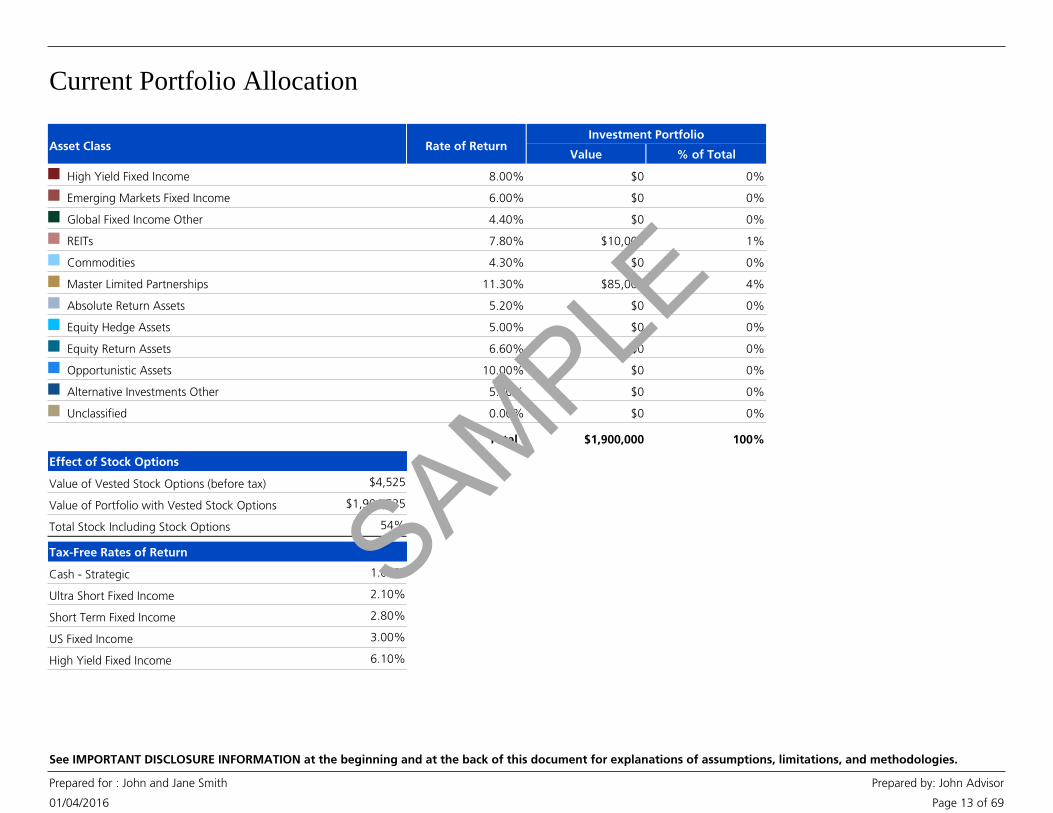

Asset Class Rate of ReturnValue % of Total

Investment Portfolio

0%$08.00%High Yield Fixed Income

0%$06.00%Emerging Markets Fixed Income

0%$04.40%Global Fixed Income Other

1%$10,0007.80%REITs

0%$04.30%Commodities

4%$85,00011.30%Master Limited Partnerships

0%$05.20%Absolute Return Assets

0%$05.00%Equity Hedge Assets

0%$06.60%Equity Return Assets

0%$010.00%Opportunistic Assets

0%$05.80%Alternative Investments Other

0%$00.00%Unclassified

Total : 100%$1,900,000

Effect of Stock Options

Value of Vested Stock Options (before tax) $4,525

Value of Portfolio with Vested Stock Options $1,904,525

Total Stock Including Stock Options 54%

Tax-Free Rates of Return

1.00%Cash - Strategic

2.10%Ultra Short Fixed Income

2.80%Short Term Fixed Income

3.00%US Fixed Income

6.10%High Yield Fixed Income

SAMPLE

Target Band

01/04/2016

Prepared for : John and Jane Smith Prepared by: John Advisor

Page 14 of 69

See IMPORTANT DISCLOSURE INFORMATION at the beginning and at the back of this document for explanations of assumptions, limitations, and methodologies.

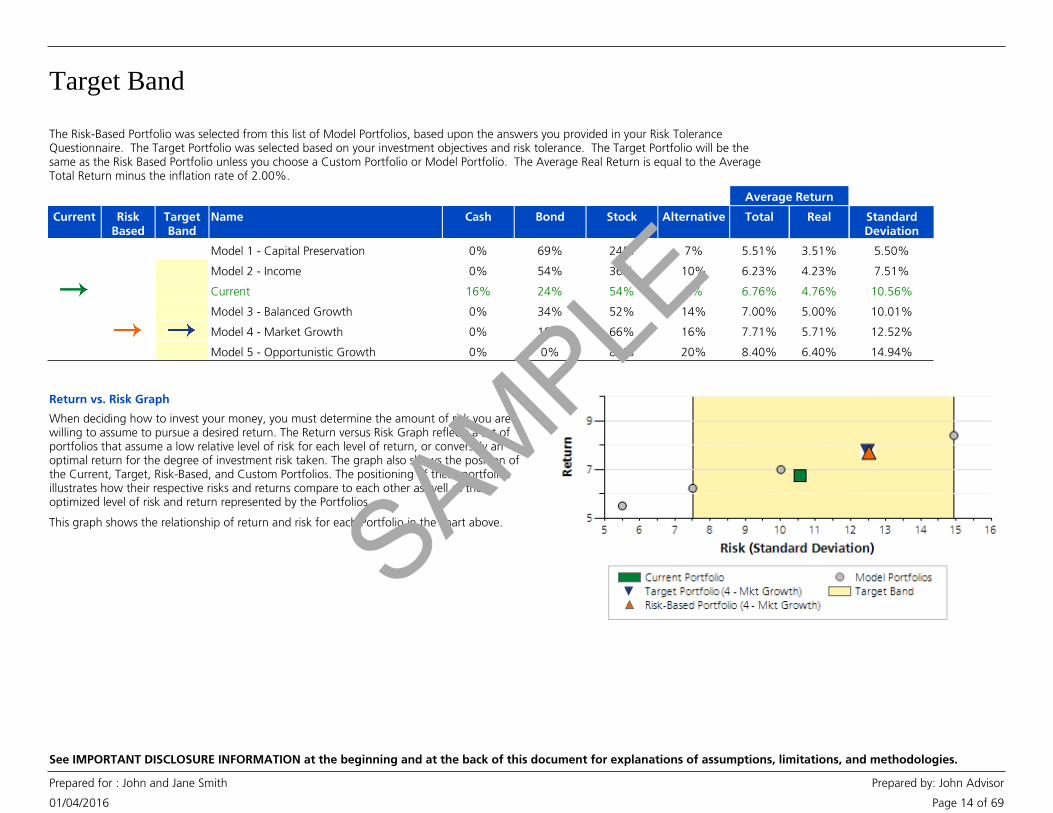

The Risk-Based Portfolio was selected from this list of Model Portfolios, based upon the answers you provided in your Risk ToleranceQuestionnaire. The Target Portfolio was selected based on your investment objectives and risk tolerance. The Target Portfolio will be thesame as the Risk Based Portfolio unless you choose a Custom Portfolio or Model Portfolio. The Average Real Return is equal to the AverageTotal Return minus the inflation rate of 2.00%.

RiskBased

TargetBand

Name TotalStock RealCurrent

Average Return

StandardDeviation

BondCash Alternative

Model 1 - Capital Preservation 5.51%24% 3.51% 5.50%69%0% 7%

Model 2 - Income 6.23%36% 4.23% 7.51%54%0% 10%

Current 6.76%54% 4.76% 10.56%24%16% 5%

Model 3 - Balanced Growth 7.00%52% 5.00% 10.01%34%0% 14%

Model 4 - Market Growth 7.71%66% 5.71% 12.52%18%0% 16%

Model 5 - Opportunistic Growth 8.40%80% 6.40% 14.94%0%0% 20%

Return vs. Risk Graph

This graph shows the relationship of return and risk for each Portfolio in the chart above.

When deciding how to invest your money, you must determine the amount of risk you arewilling to assume to pursue a desired return. The Return versus Risk Graph reflects a set ofportfolios that assume a low relative level of risk for each level of return, or conversely anoptimal return for the degree of investment risk taken. The graph also shows the position ofthe Current, Target, Risk-Based, and Custom Portfolios. The positioning of these portfoliosillustrates how their respective risks and returns compare to each other as well as theoptimized level of risk and return represented by the Portfolios.

SAMPLE

Results

SAMPLE

What If Worksheet

01/04/2016

Prepared for : John and Jane Smith Prepared by: John Advisor

Page 15 of 69

See IMPORTANT DISCLOSURE INFORMATION at the beginning and at the back of this document for explanations of assumptions, limitations, and methodologies.

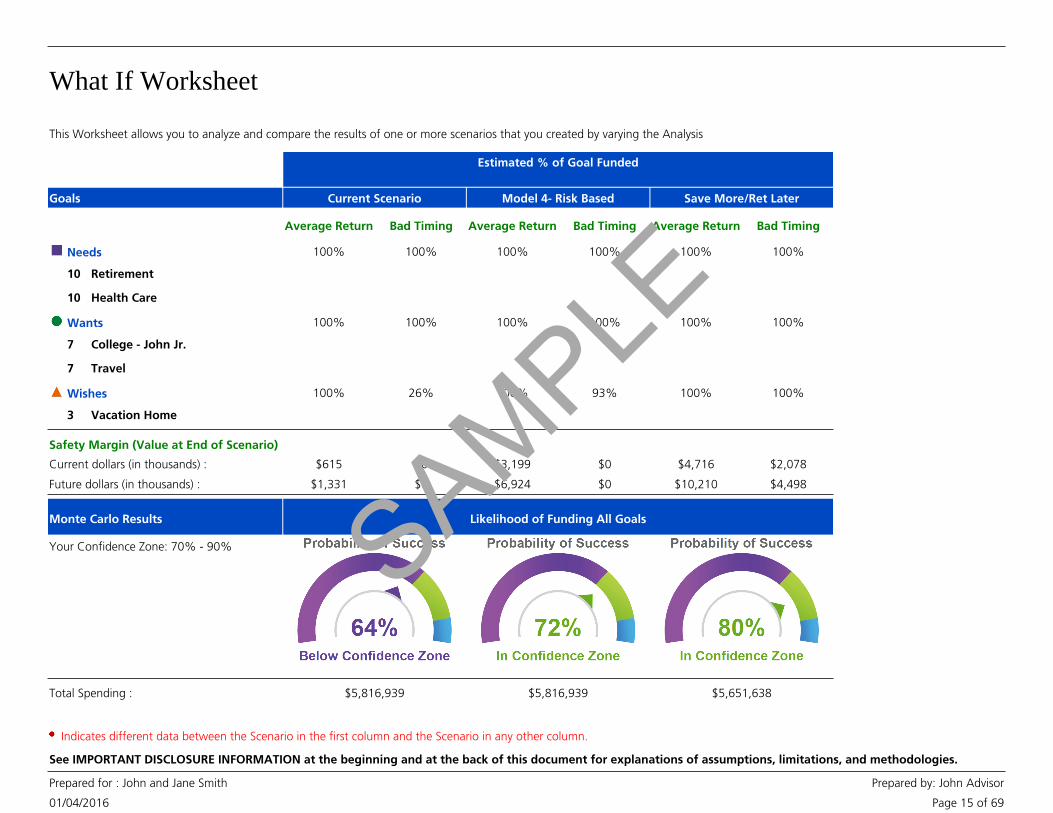

This Worksheet allows you to analyze and compare the results of one or more scenarios that you created by varying the Analysisassumptions.

Goals

Estimated % of Goal Funded

Current Scenario Model 4- Risk Based Save More/Ret Later

Average Return Bad Timing Average Return Bad Timing Average Return Bad Timing

Needs 100% 100% 100% 100% 100% 100%

10 Retirement

10 Health Care

Wants 100% 100% 100% 100% 100% 100%

7 College - John Jr.

7 Travel

Wishes 100% 26% 100% 93% 100% 100%

3 Vacation Home

$615

$1,331

Current dollars (in thousands) :

Future dollars (in thousands) :

$3,199

$6,924

Safety Margin (Value at End of Scenario)

$4,716

$10,210

$0

$0

$0

$0

$2,078

$4,498

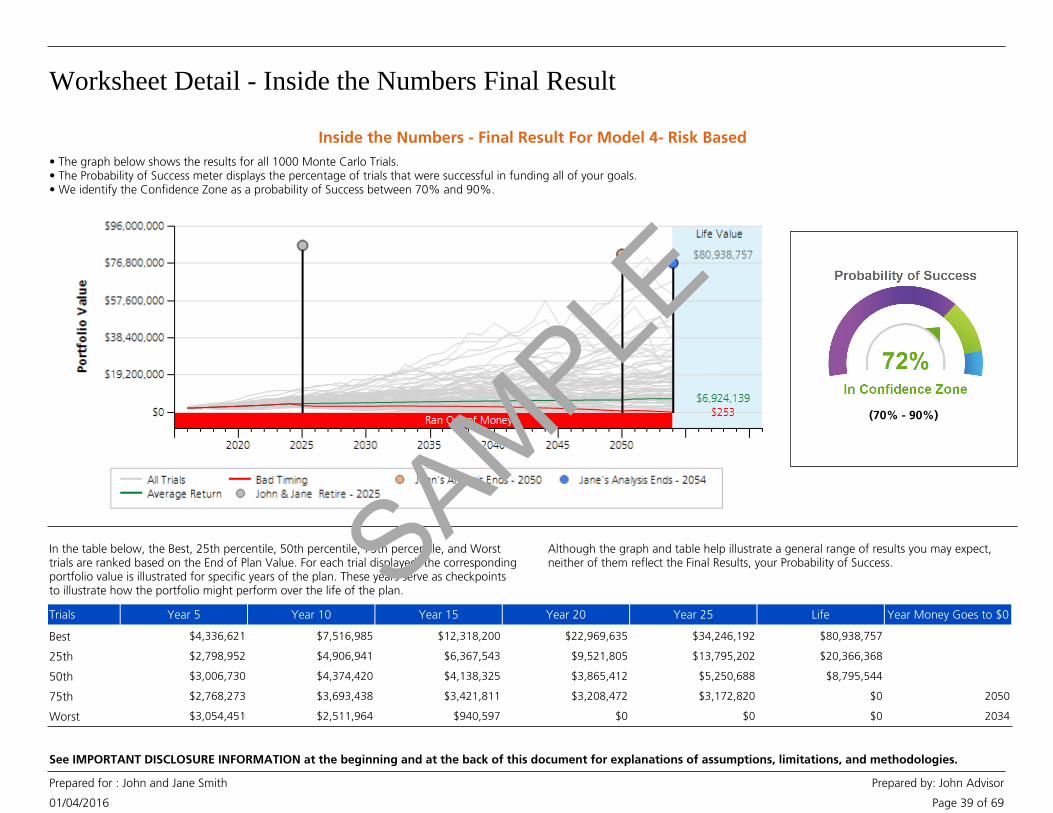

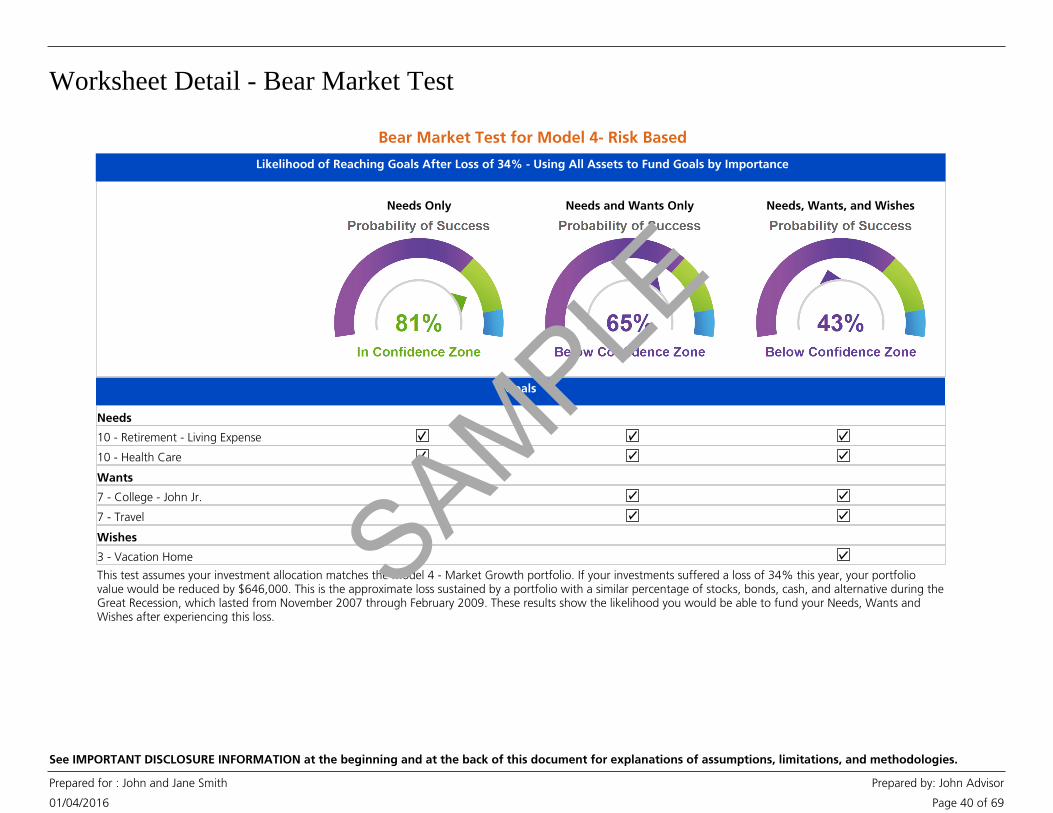

Your Confidence Zone: 70% - 90%

Likelihood of Funding All GoalsMonte Carlo Results

Total Spending : $5,816,939 $5,816,939 $5,651,638

Indicates different data between the Scenario in the first column and the Scenario in any other column.

SAMPLE

What If Worksheet

01/04/2016

Prepared for : John and Jane Smith Prepared by: John Advisor

Page 16 of 69

See IMPORTANT DISCLOSURE INFORMATION at the beginning and at the back of this document for explanations of assumptions, limitations, and methodologies.

Key Assumptions Current Scenario Model 4- Risk Based Save More/Ret Later

Stress Tests

Method(s) Bad Timing Program Estimate Years of bad returns: 2025: -14.35% 2026: -3.80%

Bad Timing Program Estimate Years of bad returns: 2025: -17.34% 2026: -4.81%

Bad Timing Program Estimate Years of bad returns: 2026: -17.34% 2027: -4.81%

False 0

Funding Order

Assets - Ignore Earmarks No No No False 1

Retirement Income - Ignore Earmarks No No No False 1

Hypothetical Average Rate of Return

Before Retirement : Current 4 - Mkt Growth 4 - Mkt Growth False 1

Total Return : 6.76% 7.71% 7.71% False 1

Standard Deviation : 10.56% 12.52% 12.52% False 1

Total Return Adjustment : 0.00% 0.00% 0.00% False 1

Adjusted Real Return : 4.76% 5.71% 5.71% False 1

After Retirement : Current 4 - Mkt Growth 4 - Mkt Growth False 1

Total Return : 6.76% 7.71% 7.71% False 1

Standard Deviation : 10.56% 12.52% 12.52% False 1

Total Return Adjustment : 0.00% 0.00% 0.00% False 1

Adjusted Real Return : 4.76% 5.71% 5.71% False 1

Base inflation rate : 2.00% 2.00% 2.00% False 1

Tax-Free Options

Before Retirement True 1

Reallocate a portion of bonds to tax-free: No No No False 1

Percent of bond allocation to treat as tax-free: 0.00% 0.00% 0.00% False 1

After Retirement True 1

Reallocate a portion of bonds to tax-free: No No No False 1

Percent of bond allocation to treat as tax-free: 0.00% 0.00% 0.00% False 1

Indicates different data between the Scenario in the first column and the Scenario in any other column.

SAMPLE

What If Worksheet

01/04/2016

Prepared for : John and Jane Smith Prepared by: John Advisor

Page 17 of 69

See IMPORTANT DISCLOSURE INFORMATION at the beginning and at the back of this document for explanations of assumptions, limitations, and methodologies.

Key Assumptions Current Scenario Model 4- Risk Based Save More/Ret Later

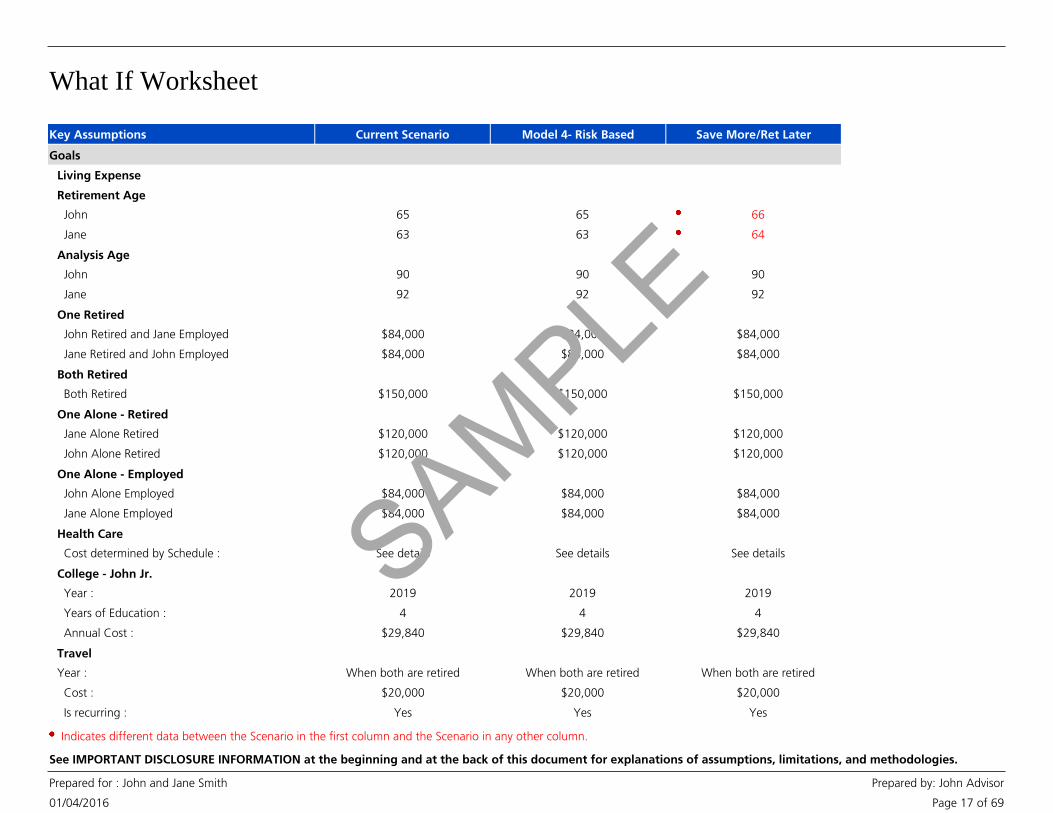

Goals

Living Expense True 1

Retirement Age True 1

John 65 65 66 False 1

Jane 63 63 64 False 1

Analysis Age True 1

John 90 90 90 False 1

Jane 92 92 92 False 1

One Retired True 1

John Retired and Jane Employed $84,000 $84,000 $84,000 False 1

Jane Retired and John Employed $84,000 $84,000 $84,000 False 1

Both Retired True 1

Both Retired $150,000 $150,000 $150,000 False 1

One Alone - Retired True 1

Jane Alone Retired $120,000 $120,000 $120,000 False 1

John Alone Retired $120,000 $120,000 $120,000 False 1

One Alone - Employed True 1

John Alone Employed $84,000 $84,000 $84,000 False 1

Jane Alone Employed $84,000 $84,000 $84,000 False 1

Health Care True 1

Cost determined by Schedule : See details See details See details False 1

College - John Jr. True 1

Year : 2019 2019 2019 False 1

Years of Education : 4 4 4 False 1

Annual Cost : $29,840 $29,840 $29,840 False 1

Travel True 1

Year : When both are retired When both are retired When both are retired False 1

Cost : $20,000 $20,000 $20,000 False 1

Is recurring : Yes Yes Yes False 1

Indicates different data between the Scenario in the first column and the Scenario in any other column.

SAMPLE

What If Worksheet

01/04/2016

Prepared for : John and Jane Smith Prepared by: John Advisor

Page 18 of 69

See IMPORTANT DISCLOSURE INFORMATION at the beginning and at the back of this document for explanations of assumptions, limitations, and methodologies.

Key Assumptions Current Scenario Model 4- Risk Based Save More/Ret Later

Goals

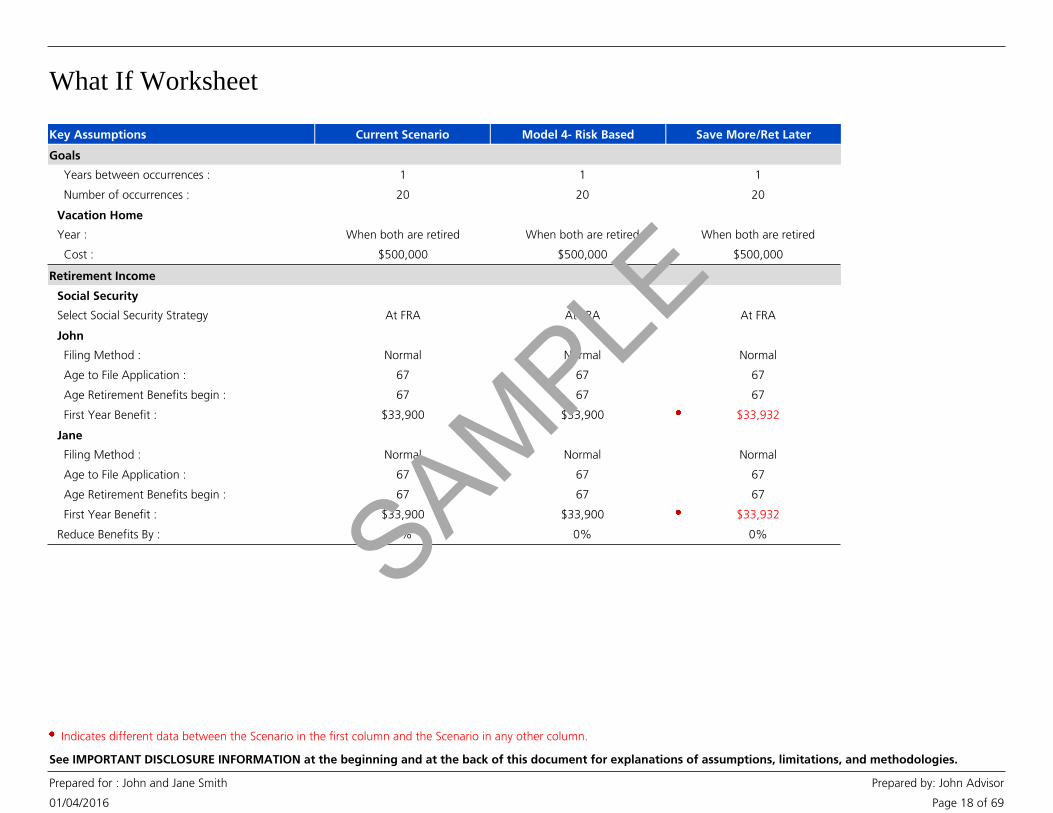

Years between occurrences : 1 1 1 False 1

Number of occurrences : 20 20 20 False 1

Vacation Home True 1

Year : When both are retired When both are retired When both are retired False 1

Cost : $500,000 $500,000 $500,000 False 1

Retirement Income

Social Security True 1

Select Social Security Strategy At FRA At FRA At FRA False 1

John True 1

Filing Method : Normal Normal Normal False 1

Age to File Application : 67 67 67 False 1

Age Retirement Benefits begin : 67 67 67 False 1

First Year Benefit : $33,900 $33,900 $33,932 False 1

Jane True 1

Filing Method : Normal Normal Normal False 1

Age to File Application : 67 67 67 False 1

Age Retirement Benefits begin : 67 67 67 False 1

First Year Benefit : $33,900 $33,900 $33,932 False 1

Reduce Benefits By : 0% 0% 0% False 1

Indicates different data between the Scenario in the first column and the Scenario in any other column.

SAMPLE

What If Worksheet

01/04/2016

Prepared for : John and Jane Smith Prepared by: John Advisor

Page 19 of 69

See IMPORTANT DISCLOSURE INFORMATION at the beginning and at the back of this document for explanations of assumptions, limitations, and methodologies.

Key Assumptions Current Scenario Model 4- Risk Based Save More/Ret Later

Asset Additions

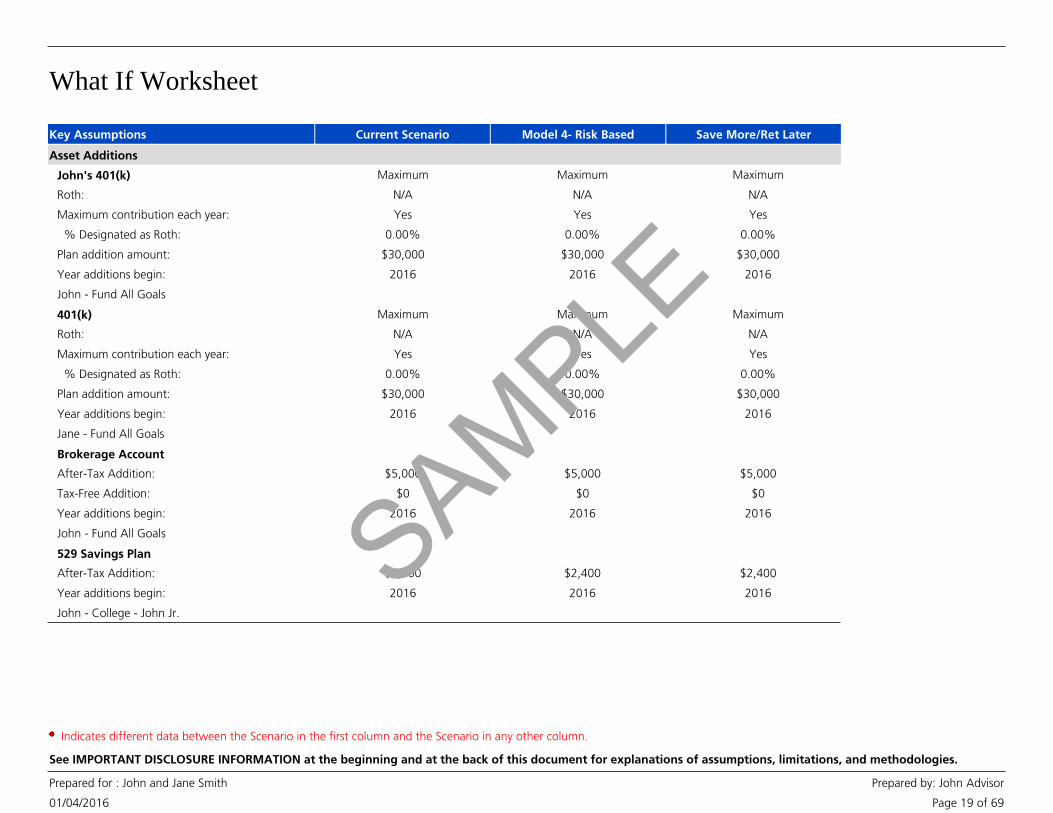

John's 401(k) Maximum Maximum Maximum True 1

Roth: N/A N/A N/A False 1

Maximum contribution each year: Yes Yes Yes False 1

% Designated as Roth: 0.00% 0.00% 0.00% False 1

Plan addition amount: $30,000 $30,000 $30,000 False 1

Year additions begin: 2016 2016 2016 False 1

John - Fund All Goals False 1

401(k) Maximum Maximum Maximum True 1

Roth: N/A N/A N/A False 1

Maximum contribution each year: Yes Yes Yes False 1

% Designated as Roth: 0.00% 0.00% 0.00% False 1

Plan addition amount: $30,000 $30,000 $30,000 False 1

Year additions begin: 2016 2016 2016 False 1

Jane - Fund All Goals False 1

Brokerage Account True 1

After-Tax Addition: $5,000 $5,000 $5,000 False 1

Tax-Free Addition: $0 $0 $0 False 1

Year additions begin: 2016 2016 2016 False 1

John - Fund All Goals False 1

529 Savings Plan True 1

After-Tax Addition: $2,400 $2,400 $2,400 False 1

Year additions begin: 2016 2016 2016 False 1

John - College - John Jr. False 1

Indicates different data between the Scenario in the first column and the Scenario in any other column.

SAMPLE

What If Worksheet

01/04/2016

Prepared for : John and Jane Smith Prepared by: John Advisor

Page 20 of 69

See IMPORTANT DISCLOSURE INFORMATION at the beginning and at the back of this document for explanations of assumptions, limitations, and methodologies.

Key Assumptions Current Scenario Model 4- Risk Based Save More/Ret Later

Extra Savings by Tax Category

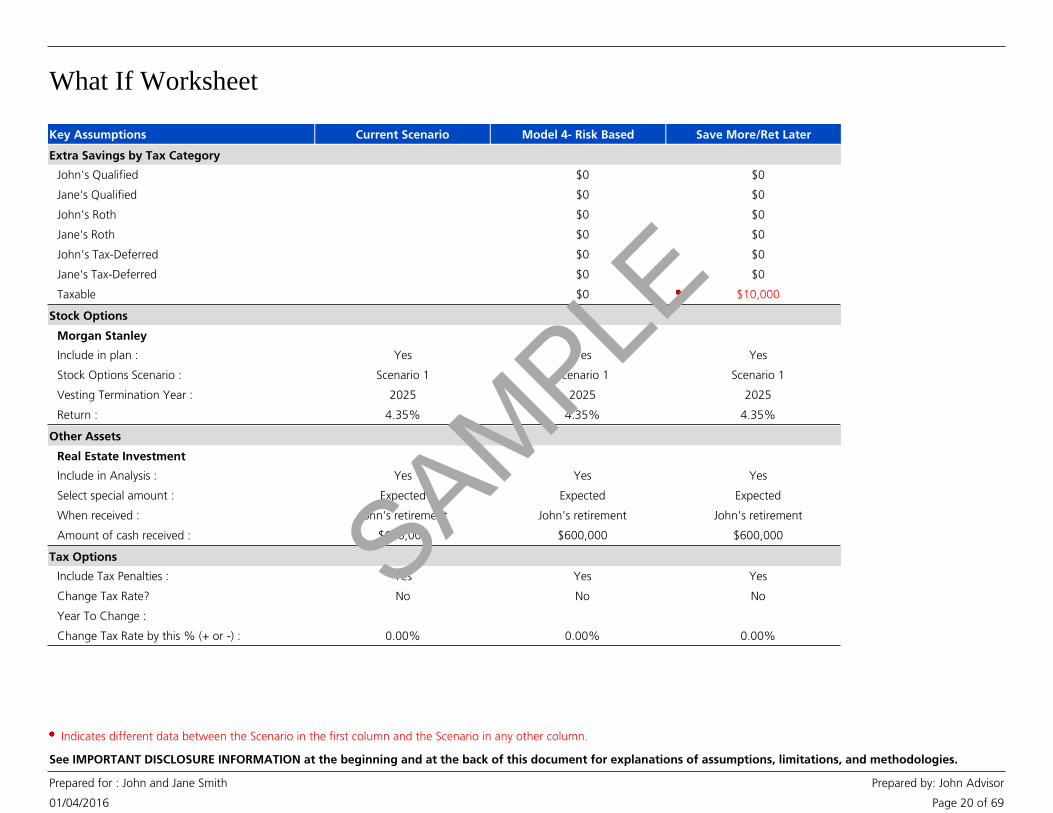

John's Qualified $0 $0 False 1

Jane's Qualified $0 $0 False 1

John's Roth $0 $0 False 1

Jane's Roth $0 $0 False 1

John's Tax-Deferred $0 $0 False 1

Jane's Tax-Deferred $0 $0 False 1

Taxable $0 $10,000 False 1

Stock Options

Morgan Stanley True 1

Include in plan : Yes Yes Yes False 1

Stock Options Scenario : Scenario 1 Scenario 1 Scenario 1 False 1

Vesting Termination Year : 2025 2025 2025 False 1

Return : 4.35% 4.35% 4.35% False 1

Other Assets

Real Estate Investment True 1

Include in Analysis : Yes Yes Yes False 1

Select special amount : Expected Expected Expected False 1

When received : John's retirement John's retirement John's retirement False 1

Amount of cash received : $600,000 $600,000 $600,000 False 1

Tax Options

Include Tax Penalties : Yes Yes Yes False 1

Change Tax Rate? No No No False 1

Year To Change : False 1

Change Tax Rate by this % (+ or -) : 0.00% 0.00% 0.00% False 1

Indicates different data between the Scenario in the first column and the Scenario in any other column.

SAMPLE

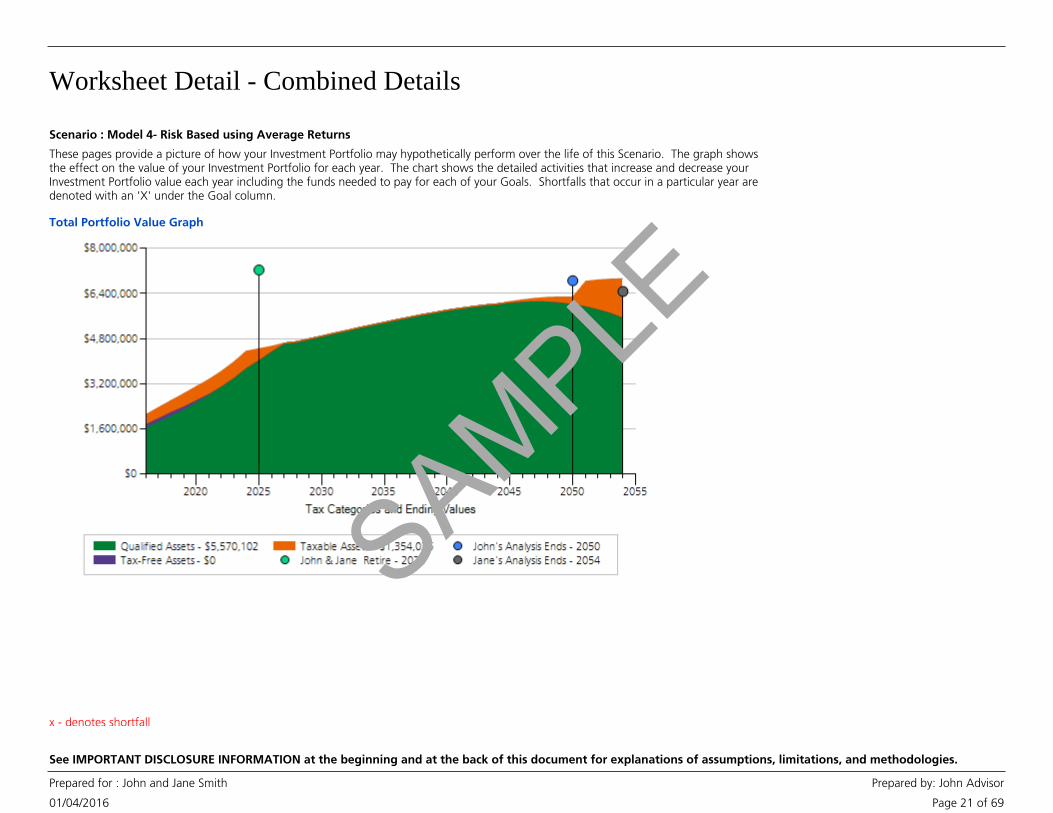

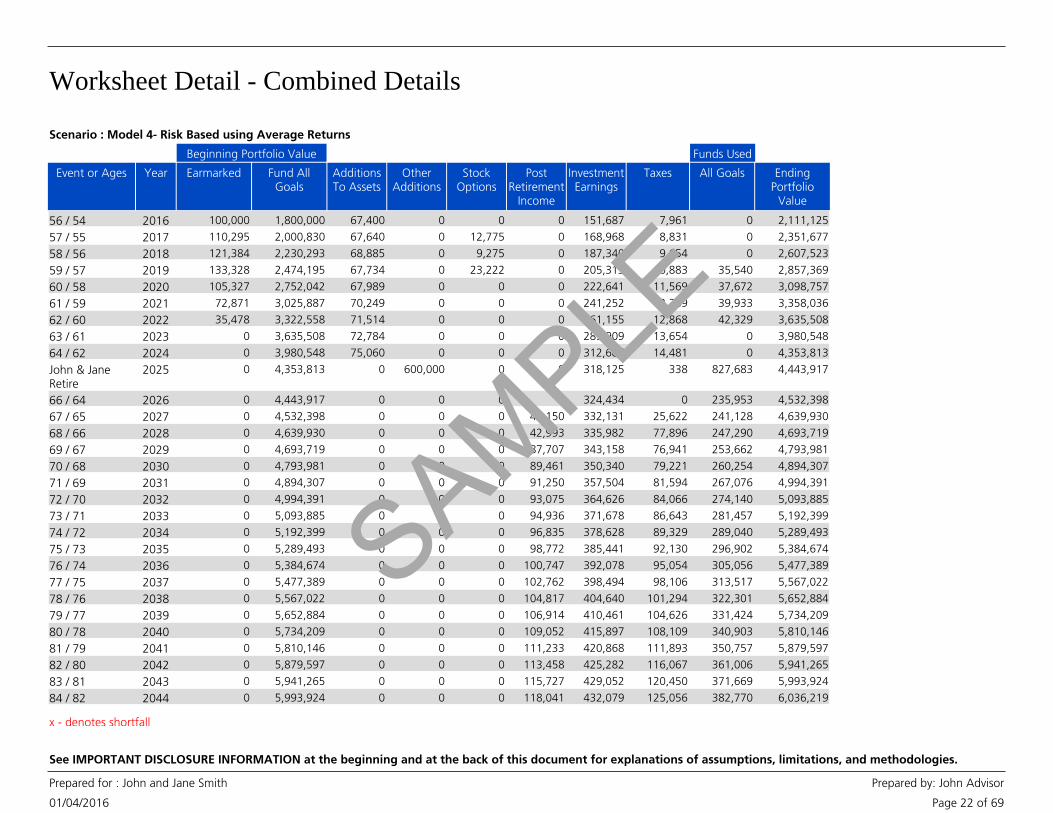

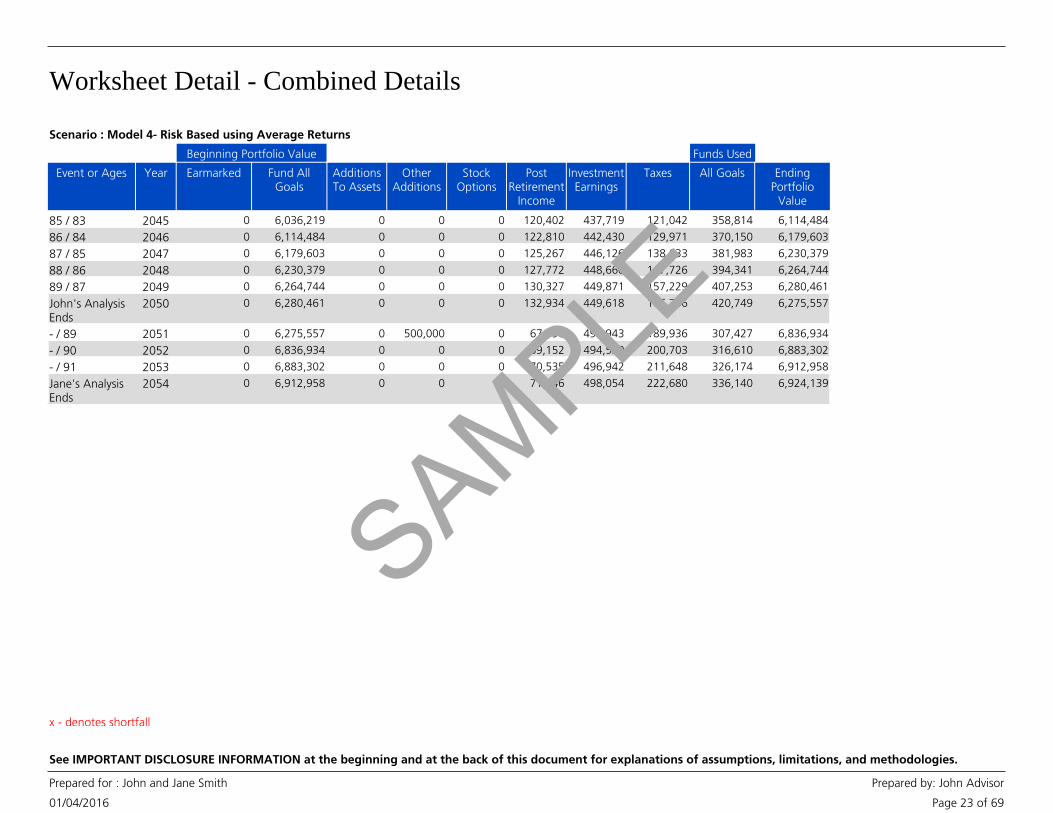

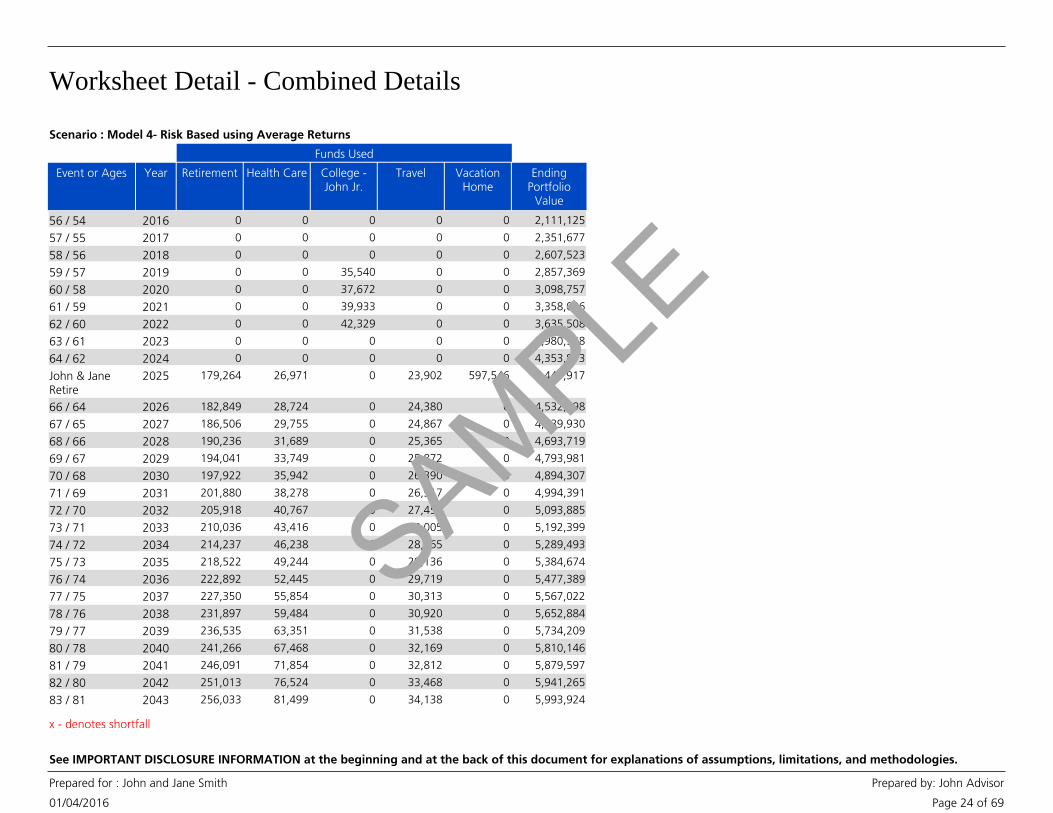

Worksheet Detail - Combined Details

01/04/2016

Prepared for : John and Jane Smith Prepared by: John Advisor

Page 21 of 69

See IMPORTANT DISCLOSURE INFORMATION at the beginning and at the back of this document for explanations of assumptions, limitations, and methodologies.

Total Portfolio Value Graph

These pages provide a picture of how your Investment Portfolio may hypothetically perform over the life of this Scenario. The graph showsthe effect on the value of your Investment Portfolio for each year. The chart shows the detailed activities that increase and decrease yourInvestment Portfolio value each year including the funds needed to pay for each of your Goals. Shortfalls that occur in a particular year aredenoted with an 'X' under the Goal column.

Scenario : Model 4- Risk Based using Average Returns

x - denotes shortfall

SAMPLE

Worksheet Detail - Combined Details

01/04/2016

Prepared for : John and Jane Smith Prepared by: John Advisor

Page 22 of 69

See IMPORTANT DISCLOSURE INFORMATION at the beginning and at the back of this document for explanations of assumptions, limitations, and methodologies.

Event or Ages Year

Beginning Portfolio Value

Earmarked Fund AllGoals

AdditionsTo Assets

OtherAdditions

StockOptions

PostRetirement

Income

InvestmentEarnings

Taxes

Funds Used

All Goals EndingPortfolio

Value

56 / 54 2016 100,000 1,800,000 67,400 0 0 0 151,687 7,961 0 2,111,125

57 / 55 2017 110,295 2,000,830 67,640 0 12,775 0 168,968 8,831 0 2,351,677

58 / 56 2018 121,384 2,230,293 68,885 0 9,275 0 187,340 9,654 0 2,607,523

59 / 57 2019 133,328 2,474,195 67,734 0 23,222 0 205,313 10,883 35,540 2,857,369

60 / 58 2020 105,327 2,752,042 67,989 0 0 0 222,641 11,569 37,672 3,098,757

61 / 59 2021 72,871 3,025,887 70,249 0 0 0 241,252 12,289 39,933 3,358,036

62 / 60 2022 35,478 3,322,558 71,514 0 0 0 261,155 12,868 42,329 3,635,508

63 / 61 2023 0 3,635,508 72,784 0 0 0 285,909 13,654 0 3,980,548

64 / 62 2024 0 3,980,548 75,060 0 0 0 312,687 14,481 0 4,353,813

John & JaneRetire

2025 0 4,353,813 0 600,000 0 0 318,125 338 827,683 4,443,917

66 / 64 2026 0 4,443,917 0 0 0 0 324,434 0 235,953 4,532,398

67 / 65 2027 0 4,532,398 0 0 0 42,150 332,131 25,622 241,128 4,639,930

68 / 66 2028 0 4,639,930 0 0 0 42,993 335,982 77,896 247,290 4,693,719

69 / 67 2029 0 4,693,719 0 0 0 87,707 343,158 76,941 253,662 4,793,981

70 / 68 2030 0 4,793,981 0 0 0 89,461 350,340 79,221 260,254 4,894,307

71 / 69 2031 0 4,894,307 0 0 0 91,250 357,504 81,594 267,076 4,994,391

72 / 70 2032 0 4,994,391 0 0 0 93,075 364,626 84,066 274,140 5,093,885

73 / 71 2033 0 5,093,885 0 0 0 94,936 371,678 86,643 281,457 5,192,399

74 / 72 2034 0 5,192,399 0 0 0 96,835 378,628 89,329 289,040 5,289,493

75 / 73 2035 0 5,289,493 0 0 0 98,772 385,441 92,130 296,902 5,384,674

76 / 74 2036 0 5,384,674 0 0 0 100,747 392,078 95,054 305,056 5,477,389

77 / 75 2037 0 5,477,389 0 0 0 102,762 398,494 98,106 313,517 5,567,022

78 / 76 2038 0 5,567,022 0 0 0 104,817 404,640 101,294 322,301 5,652,884

79 / 77 2039 0 5,652,884 0 0 0 106,914 410,461 104,626 331,424 5,734,209

80 / 78 2040 0 5,734,209 0 0 0 109,052 415,897 108,109 340,903 5,810,146

81 / 79 2041 0 5,810,146 0 0 0 111,233 420,868 111,893 350,757 5,879,597

82 / 80 2042 0 5,879,597 0 0 0 113,458 425,282 116,067 361,006 5,941,265

83 / 81 2043 0 5,941,265 0 0 0 115,727 429,052 120,450 371,669 5,993,924

84 / 82 2044 0 5,993,924 0 0 0 118,041 432,079 125,056 382,770 6,036,219

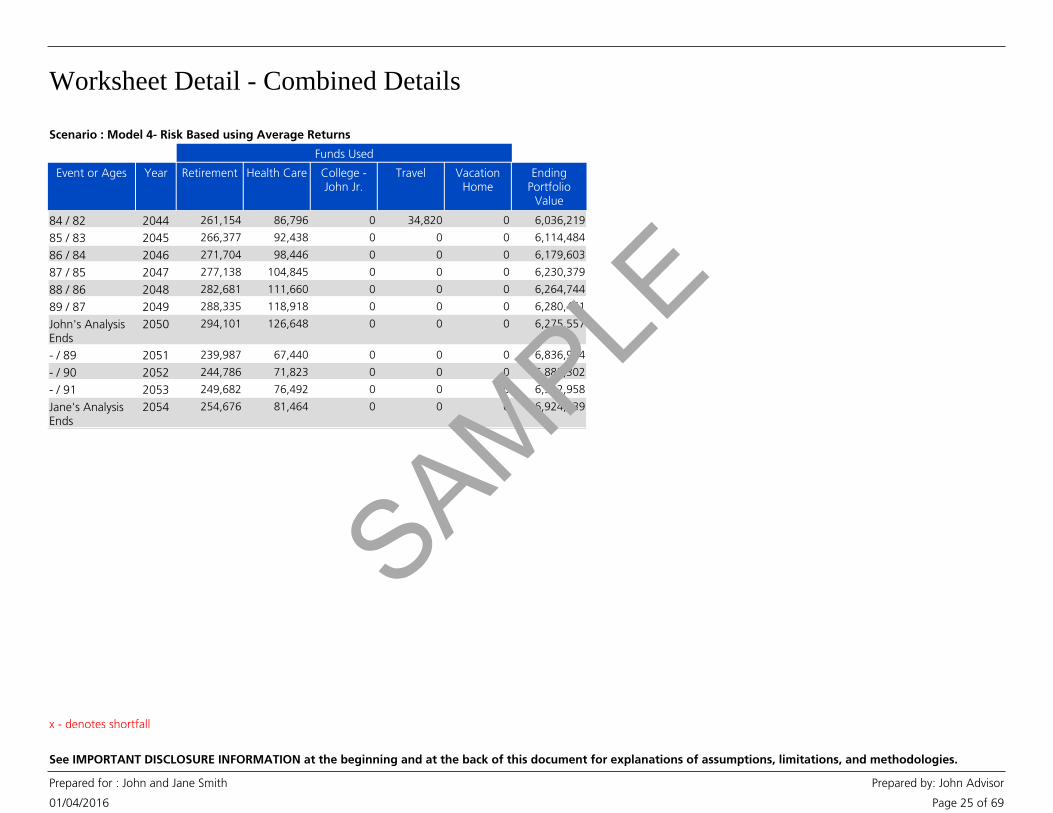

Scenario : Model 4- Risk Based using Average Returns

x - denotes shortfall

SAMPLE

Worksheet Detail - Combined Details

01/04/2016

Prepared for : John and Jane Smith Prepared by: John Advisor

Page 23 of 69

See IMPORTANT DISCLOSURE INFORMATION at the beginning and at the back of this document for explanations of assumptions, limitations, and methodologies.

Event or Ages Year

Beginning Portfolio Value

Earmarked Fund AllGoals

AdditionsTo Assets

OtherAdditions

StockOptions

PostRetirement

Income

InvestmentEarnings

Taxes

Funds Used

All Goals EndingPortfolio

Value

85 / 83 2045 0 6,036,219 0 0 0 120,402 437,719 121,042 358,814 6,114,484

86 / 84 2046 0 6,114,484 0 0 0 122,810 442,430 129,971 370,150 6,179,603

87 / 85 2047 0 6,179,603 0 0 0 125,267 446,126 138,633 381,983 6,230,379

88 / 86 2048 0 6,230,379 0 0 0 127,772 448,660 147,726 394,341 6,264,744

89 / 87 2049 0 6,264,744 0 0 0 130,327 449,871 157,229 407,253 6,280,461

John's AnalysisEnds

2050 0 6,280,461 0 0 0 132,934 449,618 166,706 420,749 6,275,557

- / 89 2051 0 6,275,557 0 500,000 0 67,796 490,943 189,936 307,427 6,836,934

- / 90 2052 0 6,836,934 0 0 0 69,152 494,530 200,703 316,610 6,883,302

- / 91 2053 0 6,883,302 0 0 0 70,535 496,942 211,648 326,174 6,912,958

Jane's AnalysisEnds

2054 0 6,912,958 0 0 0 71,946 498,054 222,680 336,140 6,924,139

Scenario : Model 4- Risk Based using Average Returns

x - denotes shortfall

SAMPLE

Worksheet Detail - Combined Details

01/04/2016

Prepared for : John and Jane Smith Prepared by: John Advisor

Page 24 of 69

See IMPORTANT DISCLOSURE INFORMATION at the beginning and at the back of this document for explanations of assumptions, limitations, and methodologies.

Scenario : Model 4- Risk Based using Average Returns

Event or Ages Year

Funds Used

Retirement Health Care College -John Jr.

Travel VacationHome

EndingPortfolio

Value

56 / 54 2016 0 0 0 0 0 2,111,125

57 / 55 2017 0 0 0 0 0 2,351,677

58 / 56 2018 0 0 0 0 0 2,607,523

59 / 57 2019 0 0 35,540 0 0 2,857,369

60 / 58 2020 0 0 37,672 0 0 3,098,757

61 / 59 2021 0 0 39,933 0 0 3,358,036

62 / 60 2022 0 0 42,329 0 0 3,635,508

63 / 61 2023 0 0 0 0 0 3,980,548

64 / 62 2024 0 0 0 0 0 4,353,813

John & JaneRetire

2025 179,264 26,971 0 23,902 597,546 4,443,917

66 / 64 2026 182,849 28,724 0 24,380 0 4,532,398

67 / 65 2027 186,506 29,755 0 24,867 0 4,639,930

68 / 66 2028 190,236 31,689 0 25,365 0 4,693,719

69 / 67 2029 194,041 33,749 0 25,872 0 4,793,981

70 / 68 2030 197,922 35,942 0 26,390 0 4,894,307

71 / 69 2031 201,880 38,278 0 26,917 0 4,994,391

72 / 70 2032 205,918 40,767 0 27,456 0 5,093,885

73 / 71 2033 210,036 43,416 0 28,005 0 5,192,399

74 / 72 2034 214,237 46,238 0 28,565 0 5,289,493

75 / 73 2035 218,522 49,244 0 29,136 0 5,384,674

76 / 74 2036 222,892 52,445 0 29,719 0 5,477,389

77 / 75 2037 227,350 55,854 0 30,313 0 5,567,022

78 / 76 2038 231,897 59,484 0 30,920 0 5,652,884

79 / 77 2039 236,535 63,351 0 31,538 0 5,734,209

80 / 78 2040 241,266 67,468 0 32,169 0 5,810,146

81 / 79 2041 246,091 71,854 0 32,812 0 5,879,597

82 / 80 2042 251,013 76,524 0 33,468 0 5,941,265

83 / 81 2043 256,033 81,499 0 34,138 0 5,993,924

x - denotes shortfall

SAMPLE

Worksheet Detail - Combined Details

01/04/2016

Prepared for : John and Jane Smith Prepared by: John Advisor

Page 25 of 69

See IMPORTANT DISCLOSURE INFORMATION at the beginning and at the back of this document for explanations of assumptions, limitations, and methodologies.

Scenario : Model 4- Risk Based using Average Returns

Event or Ages Year

Funds Used

Retirement Health Care College -John Jr.

Travel VacationHome

EndingPortfolio

Value

84 / 82 2044 261,154 86,796 0 34,820 0 6,036,219

85 / 83 2045 266,377 92,438 0 0 0 6,114,484

86 / 84 2046 271,704 98,446 0 0 0 6,179,603

87 / 85 2047 277,138 104,845 0 0 0 6,230,379

88 / 86 2048 282,681 111,660 0 0 0 6,264,744

89 / 87 2049 288,335 118,918 0 0 0 6,280,461

John's AnalysisEnds

2050 294,101 126,648 0 0 0 6,275,557

- / 89 2051 239,987 67,440 0 0 0 6,836,934

- / 90 2052 244,786 71,823 0 0 0 6,883,302

- / 91 2053 249,682 76,492 0 0 0 6,912,958

Jane's AnalysisEnds

2054 254,676 81,464 0 0 0 6,924,139

x - denotes shortfall

SAMPLE

Worksheet Detail - Combined Details

01/04/2016

Prepared for : John and Jane Smith Prepared by: John Advisor

Page 26 of 69

See IMPORTANT DISCLOSURE INFORMATION at the beginning and at the back of this document for explanations of assumptions, limitations, and methodologies.

Notes

• IMPORTANT: The projections or other information generated by this tool regarding thelikelihood of various investment outcomes are hypothetical in nature, do not reflect actualinvestment results, and are not guarantees of future results.

• Results may vary with use and over time.

• The return assumptions used are estimates based on average annual returns for the indexused as a proxy for each asset class. The portfolio returns were calculated by weightingindividual return assumptions for each asset class according to the portfolio allocationselected by you or your Financial Advisor. The portfolio returns may have also been modifiedby your Financial Advisor to reflect the outcome of a different return by conducting a TotalReturn Adjustment or selecting a Custom Portfolio. For a explanation of the methodologyused to calculate returns, please review the Important Disclosure Information and ReturnMethodology sections.

• The return assumptions in this tool are not reflective of any specific product and do notinclude any fees or expenses that may be incurred by investing in specific products. Theactual returns of a specific product may be more or less than the returns used in this tool.

• No investment strategy or allocation can eliminate risk or guarantee investment results.

• Additions and withdrawals occur at the beginning of the year.

• Other Additions come from items entered in the Other Assets section and any applicableproceeds from insurance policies.

• Stock Options and Restricted Stock values are after-tax and based on the Exercise Scenarioselected.

• Strategy Income is based on the particulars of the Goal Strategies selected. StrategyIncome from immediate annuities and 72(t) distributions is pre-tax. Strategy Income fromNet Unrealized Appreciation (NUA) is after-tax.

• Post Retirement Income includes the following: Social Security, pension, annuity, rentalproperty, royalty, alimony, part-time employment, trust, and any other retirement income asentered in the Scenario.

• For married clients, if either Social Security Program Estimate or Use This Amount andEvaluate Annually is selected for a participant, the Program defaults to the greater of theselected benefit or the age-adjusted spousal benefit based on the other participant’sbenefit. The spousal benefit is not applicable to domestic partners.

• Investment Earnings are calculated on all assets after any withdrawals for 'Goal Expense','Taxes on Withdrawals' and 'Tax Penalties' are subtracted.

• The taxes column is a sum of (1) taxes on retirement income, (2) taxes on strategy income,(3) taxes on withdrawals from qualified assets for Required Minimum Distributions, (4) taxeson withdrawals from taxable assets' untaxed gain used to fund Goals in that year, (5) taxeson withdrawals from tax-deferred or qualified assets used to fund Goals in that year, and (6)taxes on the investment earnings of taxable assets. Tax rates used are detailed in the Taxand Inflation Options page. (Please note, the Taxes column does not include any taxesowed from the exercise of Stock Options or the vesting of Restricted Stock.)

• Tax Penalties can occur when Qualified and Tax-Deferred Assets are used prior to age59½. If there is a value in this column, it illustrates that you are using your assets in thisScenario in a manner that may incur tax penalties. Generally, it is better to avoid taxpenalties whenever possible.

• These calculations do not incorporate penalties associated with use of 529 Planwithdrawals for non-qualified expenses.

• Funds for each Goal Expense are used first from Earmarked Assets. If sufficient funds arenot available from Earmarked Assets, Fund All Goals Assets will be used to fund theremaining portion of the Goal Expense, if available in that year.

• All funds needed for a Goal must be available in the year the Goal occurs. Funds fromEarmarked Assets that become available after the Goal year(s) have passed are not includedin the funding of that Goal, and accumulate until the end of the Scenario.

• For married clients, ownership of qualified assets is assumed to roll over to the survivingco-client at the death of the original owner. For domestic partners, qualified assets areassumed to be transferred as a non-spousal inheritance to the surviving co-client at thedeath of the original owner. In both cases, the Program assumes the surviving co-clientinherits all remaining assets of the original owner.

x - denotes shortfall

SAMPLE

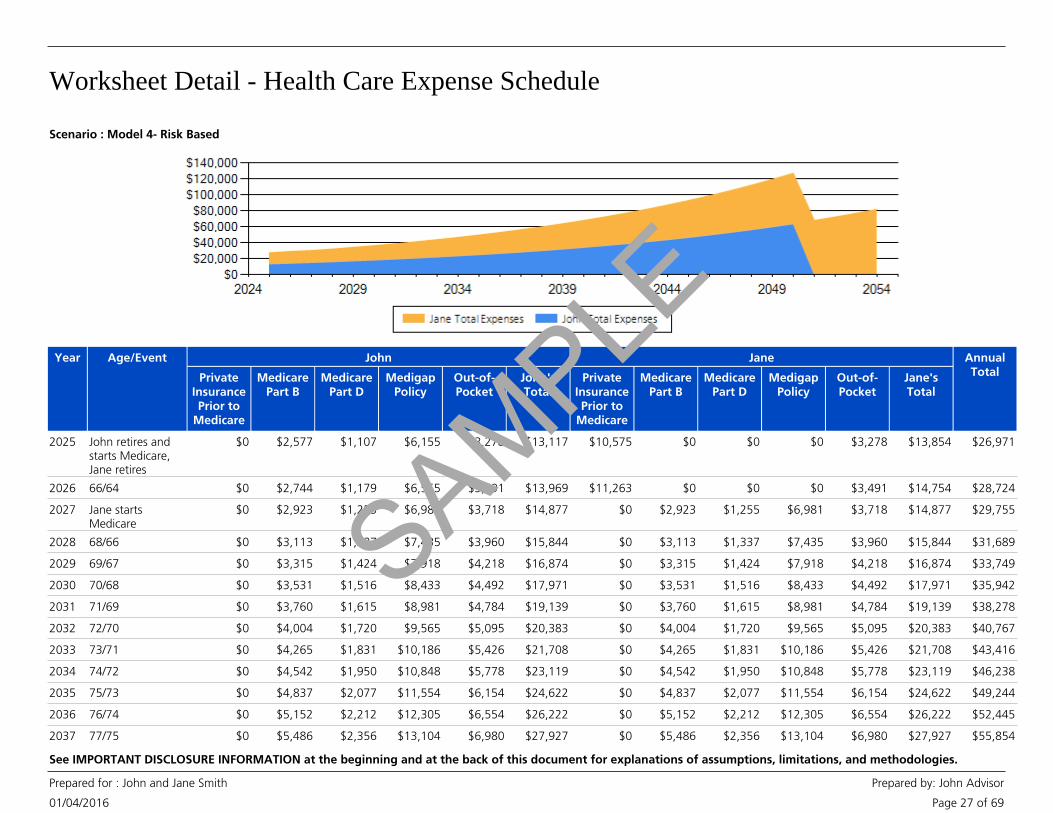

Worksheet Detail - Health Care Expense Schedule

01/04/2016

Prepared for : John and Jane Smith Prepared by: John Advisor

Page 27 of 69

See IMPORTANT DISCLOSURE INFORMATION at the beginning and at the back of this document for explanations of assumptions, limitations, and methodologies.

Year Age/Event John

PrivateInsurancePrior to

Medicare

MedicarePart B

MedicarePart D

MedigapPolicy

Out-of-Pocket

John'sTotal

Jane

PrivateInsurancePrior to

Medicare

MedicarePart B

MedicarePart D

MedigapPolicy

Out-of-Pocket

Jane'sTotal

AnnualTotal

2025 John retires andstarts Medicare,Jane retires

$0 $2,577 $1,107 $6,155 $3,278 $13,117 $10,575 $0 $0 $0 $3,278 $13,854 $26,971

2026 66/64 $0 $2,744 $1,179 $6,555 $3,491 $13,969 $11,263 $0 $0 $0 $3,491 $14,754 $28,724

2027 Jane startsMedicare

$0 $2,923 $1,255 $6,981 $3,718 $14,877 $0 $2,923 $1,255 $6,981 $3,718 $14,877 $29,755

2028 68/66 $0 $3,113 $1,337 $7,435 $3,960 $15,844 $0 $3,113 $1,337 $7,435 $3,960 $15,844 $31,689

2029 69/67 $0 $3,315 $1,424 $7,918 $4,218 $16,874 $0 $3,315 $1,424 $7,918 $4,218 $16,874 $33,749

2030 70/68 $0 $3,531 $1,516 $8,433 $4,492 $17,971 $0 $3,531 $1,516 $8,433 $4,492 $17,971 $35,942

2031 71/69 $0 $3,760 $1,615 $8,981 $4,784 $19,139 $0 $3,760 $1,615 $8,981 $4,784 $19,139 $38,278

2032 72/70 $0 $4,004 $1,720 $9,565 $5,095 $20,383 $0 $4,004 $1,720 $9,565 $5,095 $20,383 $40,767

2033 73/71 $0 $4,265 $1,831 $10,186 $5,426 $21,708 $0 $4,265 $1,831 $10,186 $5,426 $21,708 $43,416

2034 74/72 $0 $4,542 $1,950 $10,848 $5,778 $23,119 $0 $4,542 $1,950 $10,848 $5,778 $23,119 $46,238

2035 75/73 $0 $4,837 $2,077 $11,554 $6,154 $24,622 $0 $4,837 $2,077 $11,554 $6,154 $24,622 $49,244

2036 76/74 $0 $5,152 $2,212 $12,305 $6,554 $26,222 $0 $5,152 $2,212 $12,305 $6,554 $26,222 $52,445

2037 77/75 $0 $5,486 $2,356 $13,104 $6,980 $27,927 $0 $5,486 $2,356 $13,104 $6,980 $27,927 $55,854

Scenario : Model 4- Risk Based

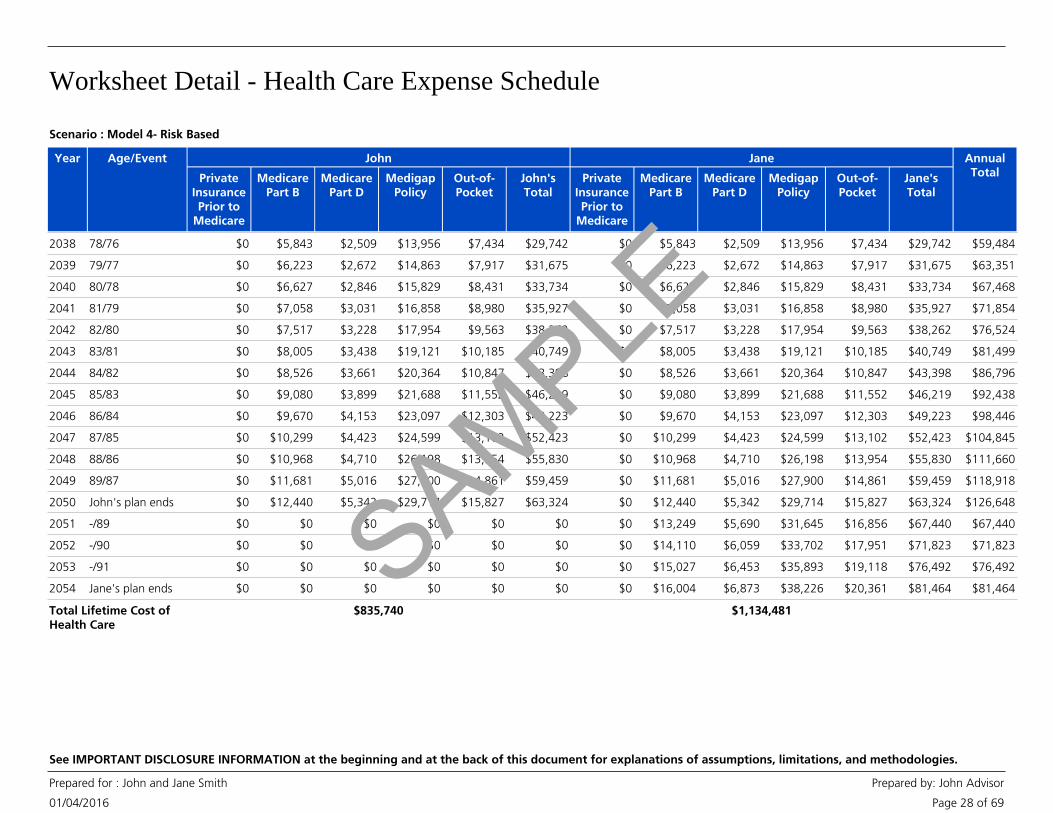

SAMPLE

Worksheet Detail - Health Care Expense Schedule

01/04/2016

Prepared for : John and Jane Smith Prepared by: John Advisor

Page 28 of 69

See IMPORTANT DISCLOSURE INFORMATION at the beginning and at the back of this document for explanations of assumptions, limitations, and methodologies.

Year Age/Event John

PrivateInsurancePrior to

Medicare

MedicarePart B

MedicarePart D

MedigapPolicy

Out-of-Pocket

John'sTotal

Jane

PrivateInsurancePrior to

Medicare

MedicarePart B

MedicarePart D

MedigapPolicy

Out-of-Pocket

Jane'sTotal

AnnualTotal

2038 78/76 $0 $5,843 $2,509 $13,956 $7,434 $29,742 $0 $5,843 $2,509 $13,956 $7,434 $29,742 $59,484

2039 79/77 $0 $6,223 $2,672 $14,863 $7,917 $31,675 $0 $6,223 $2,672 $14,863 $7,917 $31,675 $63,351

2040 80/78 $0 $6,627 $2,846 $15,829 $8,431 $33,734 $0 $6,627 $2,846 $15,829 $8,431 $33,734 $67,468

2041 81/79 $0 $7,058 $3,031 $16,858 $8,980 $35,927 $0 $7,058 $3,031 $16,858 $8,980 $35,927 $71,854

2042 82/80 $0 $7,517 $3,228 $17,954 $9,563 $38,262 $0 $7,517 $3,228 $17,954 $9,563 $38,262 $76,524

2043 83/81 $0 $8,005 $3,438 $19,121 $10,185 $40,749 $0 $8,005 $3,438 $19,121 $10,185 $40,749 $81,499

2044 84/82 $0 $8,526 $3,661 $20,364 $10,847 $43,398 $0 $8,526 $3,661 $20,364 $10,847 $43,398 $86,796

2045 85/83 $0 $9,080 $3,899 $21,688 $11,552 $46,219 $0 $9,080 $3,899 $21,688 $11,552 $46,219 $92,438

2046 86/84 $0 $9,670 $4,153 $23,097 $12,303 $49,223 $0 $9,670 $4,153 $23,097 $12,303 $49,223 $98,446

2047 87/85 $0 $10,299 $4,423 $24,599 $13,102 $52,423 $0 $10,299 $4,423 $24,599 $13,102 $52,423 $104,845

2048 88/86 $0 $10,968 $4,710 $26,198 $13,954 $55,830 $0 $10,968 $4,710 $26,198 $13,954 $55,830 $111,660

2049 89/87 $0 $11,681 $5,016 $27,900 $14,861 $59,459 $0 $11,681 $5,016 $27,900 $14,861 $59,459 $118,918

2050 John's plan ends $0 $12,440 $5,342 $29,714 $15,827 $63,324 $0 $12,440 $5,342 $29,714 $15,827 $63,324 $126,648

2051 -/89 $0 $0 $0 $0 $0 $0 $0 $13,249 $5,690 $31,645 $16,856 $67,440 $67,440

2052 -/90 $0 $0 $0 $0 $0 $0 $0 $14,110 $6,059 $33,702 $17,951 $71,823 $71,823

2053 -/91 $0 $0 $0 $0 $0 $0 $0 $15,027 $6,453 $35,893 $19,118 $76,492 $76,492

2054 Jane's plan ends $0 $0 $0 $0 $0 $0 $0 $16,004 $6,873 $38,226 $20,361 $81,464 $81,464

$835,740 $1,134,481Total Lifetime Cost ofHealth Care

Scenario : Model 4- Risk Based

SAMPLE

Worksheet Detail - Health Care Expense Schedule

01/04/2016

Prepared for : John and Jane Smith Prepared by: John Advisor

Page 29 of 69

See IMPORTANT DISCLOSURE INFORMATION at the beginning and at the back of this document for explanations of assumptions, limitations, and methodologies.

Scenario : Model 4- Risk Based

• Program assumptions:

• The scenario assumes that client and co-client will each use a combination of Medicare PartA (Hospital Insurance), Part B (Medical Insurance), Part D (Prescription Drug Insurance),Medigap insurance , and Out-of Pocket expenses. The program uses initial default values thatmay have been adjusted based on your preferences and information provided by you.

Notes

• The scenario assumes that client and co-client each qualify to receive Medicare Part A at nocharge and therefore it is not reflected in the Health Care Expense schedule.

• Estimates for private insurance prior to retirement are based on the information youprovided.

• Medicare and Medigap costs begin at the later of age 65, your retirement age, or thecurrent year.

• All costs are in future dollars.

• Costs associated with Long Term Care needs are not addressed by this goal. A separate LTCgoal can be created.

• General Information regarding Medicare:

• Part B premiums are uniform nationally and are increased for those with a higher ModifiedAdjusted Gross Income.

• Part D coverage is optional. Premiums are increased for those with a higher ModifiedAdjusted Gross Income, differ from state to state, and vary based on the specific plan andlevel of benefit selected.

• Medigap coverage is optional and policies (Plans A-N) are issued by private insurers.

• Clients may incur out-of-pocket healthcare expenses, for costs not covered by Medicarebenefits and Medigap insurance.

• If clients retire before age 65, they may choose to purchase private health insurance or toself-insure. Costs and coverage for private health insurance varies greatly.

SAMPLE

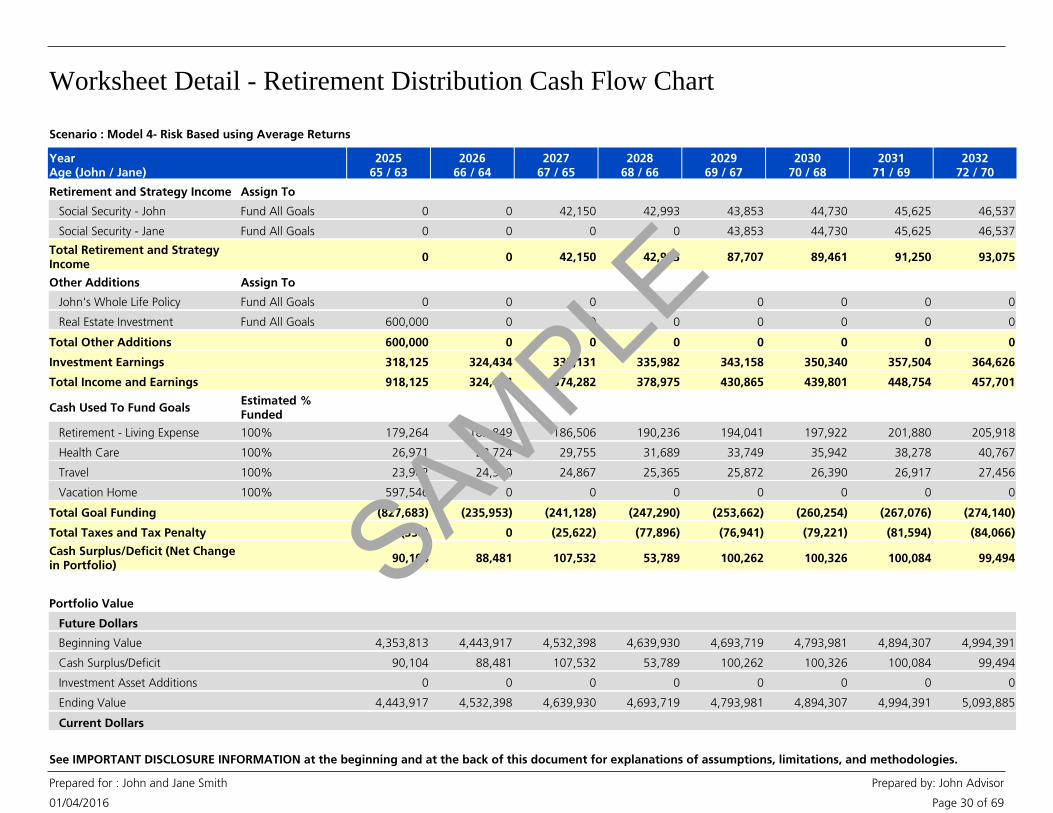

Worksheet Detail - Retirement Distribution Cash Flow Chart

01/04/2016

Prepared for : John and Jane Smith Prepared by: John Advisor

Page 30 of 69

See IMPORTANT DISCLOSURE INFORMATION at the beginning and at the back of this document for explanations of assumptions, limitations, and methodologies.

202565 / 63

202666 / 64

202767 / 65

202868 / 66

202969 / 67

203070 / 68

203171 / 69

203272 / 70

YearAge (John / Jane)

Retirement and Strategy Income Assign To

Social Security - John 0Fund All Goals 0 42,150 42,993 43,853 44,730 45,625 46,537

Social Security - Jane 0Fund All Goals 0 0 0 43,853 44,730 45,625 46,537

Total Retirement and StrategyIncome

0 0 42,150 42,993 87,707 89,461 91,250 93,075

Other Additions Assign To

John's Whole Life Policy 0Fund All Goals 0 0 0 0 0 0 0

Real Estate Investment 600,000Fund All Goals 0 0 0 0 0 0 0

Total Other Additions 600,000 0 0 0 0 0 0 0

Investment Earnings 318,125 324,434 332,131 335,982 343,158 350,340 357,504 364,626

Total Income and Earnings 918,125 324,434 374,282 378,975 430,865 439,801 448,754 457,701

Cash Used To Fund GoalsEstimated %Funded

Retirement - Living Expense 179,264100% 182,849 186,506 190,236 194,041 197,922 201,880 205,918

Health Care 26,971100% 28,724 29,755 31,689 33,749 35,942 38,278 40,767

Travel 23,902100% 24,380 24,867 25,365 25,872 26,390 26,917 27,456

Vacation Home 597,546100% 0 0 0 0 0 0 0

Total Goal Funding (827,683) (235,953) (241,128) (247,290) (253,662) (260,254) (267,076) (274,140)

Total Taxes and Tax Penalty (338) 0 (25,622) (77,896) (76,941) (79,221) (81,594) (84,066)

Cash Surplus/Deficit (Net Changein Portfolio)

90,104 88,481 107,532 53,789 100,262 100,326 100,084 99,494

Portfolio Value

Future Dollars

Beginning Value 4,353,813 4,443,917 4,532,398 4,639,930 4,693,719 4,793,981 4,894,307 4,994,391

Cash Surplus/Deficit 90,104 88,481 107,532 53,789 100,262 100,326 100,084 99,494

Investment Asset Additions 0 0 0 0 0 0 0 0

Ending Value 4,443,917 4,532,398 4,639,930 4,693,719 4,793,981 4,894,307 4,994,391 5,093,885

Current Dollars

Scenario : Model 4- Risk Based using Average Returns

SAMPLE

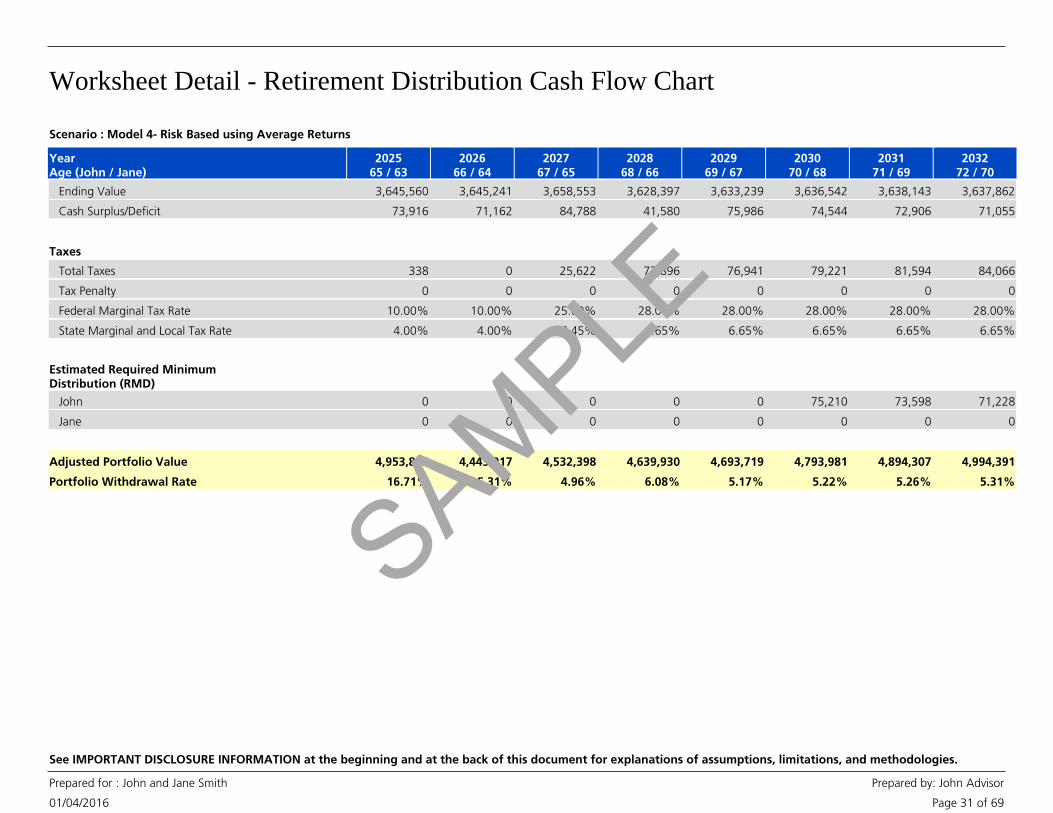

Worksheet Detail - Retirement Distribution Cash Flow Chart

01/04/2016

Prepared for : John and Jane Smith Prepared by: John Advisor

Page 31 of 69

See IMPORTANT DISCLOSURE INFORMATION at the beginning and at the back of this document for explanations of assumptions, limitations, and methodologies.

202565 / 63

202666 / 64

202767 / 65

202868 / 66

202969 / 67

203070 / 68

203171 / 69

203272 / 70

YearAge (John / Jane)

Ending Value 3,645,560 3,645,241 3,658,553 3,628,397 3,633,239 3,636,542 3,638,143 3,637,862

Cash Surplus/Deficit 73,916 71,162 84,788 41,580 75,986 74,544 72,906 71,055

Taxes

Total Taxes 338 0 25,622 77,896 76,941 79,221 81,594 84,066

Tax Penalty 0 0 0 0 0 0 0 0

Federal Marginal Tax Rate 10.00% 10.00% 25.00% 28.00% 28.00% 28.00% 28.00% 28.00%

State Marginal and Local Tax Rate 4.00% 4.00% 6.45% 6.65% 6.65% 6.65% 6.65% 6.65%

Estimated Required MinimumDistribution (RMD)

John 0 0 0 0 0 75,210 73,598 71,228

Jane 0 0 0 0 0 0 0 0

Adjusted Portfolio Value 4,953,813 4,443,917 4,532,398 4,639,930 4,693,719 4,793,981 4,894,307 4,994,391

Portfolio Withdrawal Rate 16.71% 5.31% 4.96% 6.08% 5.17% 5.22% 5.26% 5.31%

Scenario : Model 4- Risk Based using Average Returns

SAMPLE

Worksheet Detail - Retirement Distribution Cash Flow Chart

01/04/2016

Prepared for : John and Jane Smith Prepared by: John Advisor

Page 32 of 69

See IMPORTANT DISCLOSURE INFORMATION at the beginning and at the back of this document for explanations of assumptions, limitations, and methodologies.

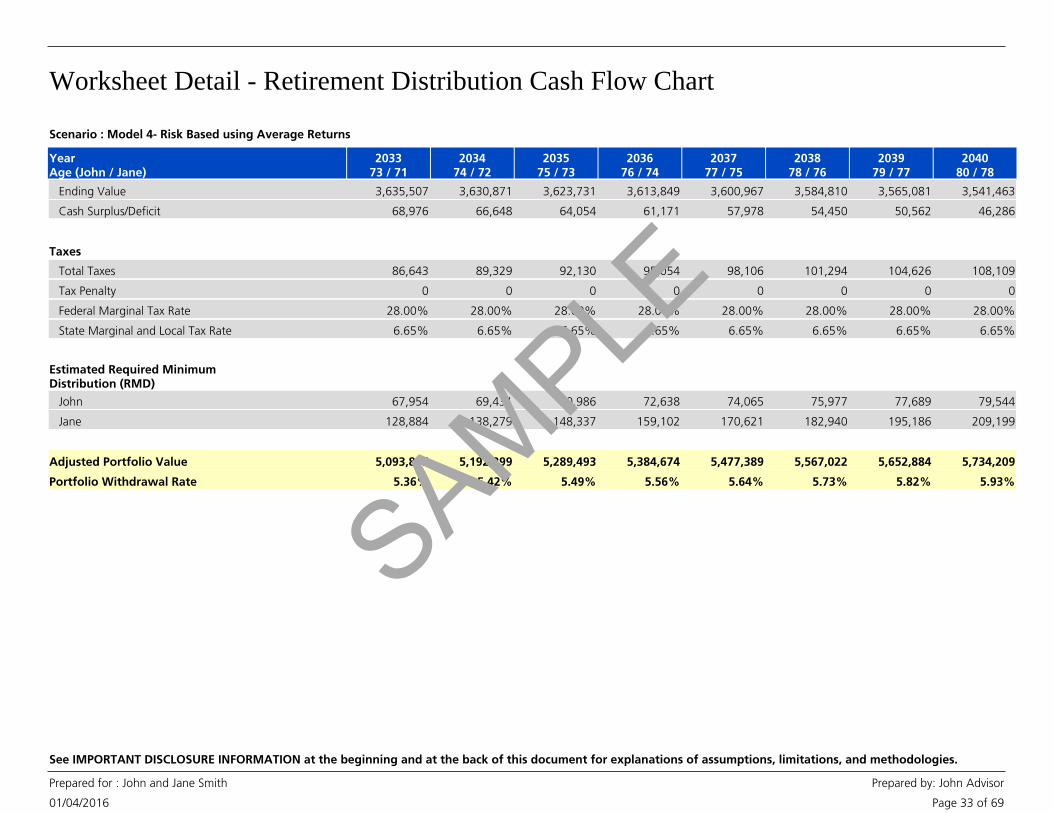

203373 / 71

203474 / 72

203575 / 73

203676 / 74

203777 / 75

203878 / 76

203979 / 77

204080 / 78

YearAge (John / Jane)

Retirement and Strategy Income Assign To

Social Security - John 47,468Fund All Goals 48,418 49,386 50,374 51,381 52,409 53,457 54,526

Social Security - Jane 47,468Fund All Goals 48,418 49,386 50,374 51,381 52,409 53,457 54,526

Total Retirement and StrategyIncome

94,936 96,835 98,772 100,747 102,762 104,817 106,914 109,052

Other Additions Assign To

John's Whole Life Policy 0Fund All Goals 0 0 0 0 0 0 0

Real Estate Investment 0Fund All Goals 0 0 0 0 0 0 0

Total Other Additions 0 0 0 0 0 0 0 0

Investment Earnings 371,678 378,628 385,441 392,078 398,494 404,640 410,461 415,897

Total Income and Earnings 466,614 475,463 484,213 492,825 501,256 509,457 517,375 524,949

Cash Used To Fund GoalsEstimated %Funded

Retirement - Living Expense 210,036100% 214,237 218,522 222,892 227,350 231,897 236,535 241,266

Health Care 43,416100% 46,238 49,244 52,445 55,854 59,484 63,351 67,468

Travel 28,005100% 28,565 29,136 29,719 30,313 30,920 31,538 32,169

Vacation Home 0100% 0 0 0 0 0 0 0

Total Goal Funding (281,457) (289,040) (296,902) (305,056) (313,517) (322,301) (331,424) (340,903)

Total Taxes and Tax Penalty (86,643) (89,329) (92,130) (95,054) (98,106) (101,294) (104,626) (108,109)

Cash Surplus/Deficit (Net Changein Portfolio)

98,514 97,094 95,181 92,715 89,633 85,862 81,325 75,937

Portfolio Value

Future Dollars

Beginning Value 5,093,885 5,192,399 5,289,493 5,384,674 5,477,389 5,567,022 5,652,884 5,734,209

Cash Surplus/Deficit 98,514 97,094 95,181 92,715 89,633 85,862 81,325 75,937

Investment Asset Additions 0 0 0 0 0 0 0 0

Ending Value 5,192,399 5,289,493 5,384,674 5,477,389 5,567,022 5,652,884 5,734,209 5,810,146

Current Dollars

Scenario : Model 4- Risk Based using Average Returns

SAMPLE

Worksheet Detail - Retirement Distribution Cash Flow Chart

01/04/2016

Prepared for : John and Jane Smith Prepared by: John Advisor

Page 33 of 69

See IMPORTANT DISCLOSURE INFORMATION at the beginning and at the back of this document for explanations of assumptions, limitations, and methodologies.

203373 / 71

203474 / 72

203575 / 73

203676 / 74

203777 / 75

203878 / 76

203979 / 77

204080 / 78

YearAge (John / Jane)

Ending Value 3,635,507 3,630,871 3,623,731 3,613,849 3,600,967 3,584,810 3,565,081 3,541,463

Cash Surplus/Deficit 68,976 66,648 64,054 61,171 57,978 54,450 50,562 46,286

Taxes

Total Taxes 86,643 89,329 92,130 95,054 98,106 101,294 104,626 108,109

Tax Penalty 0 0 0 0 0 0 0 0

Federal Marginal Tax Rate 28.00% 28.00% 28.00% 28.00% 28.00% 28.00% 28.00% 28.00%

State Marginal and Local Tax Rate 6.65% 6.65% 6.65% 6.65% 6.65% 6.65% 6.65% 6.65%

Estimated Required MinimumDistribution (RMD)

John 67,954 69,431 70,986 72,638 74,065 75,977 77,689 79,544

Jane 128,884 138,279 148,337 159,102 170,621 182,940 195,186 209,199

Adjusted Portfolio Value 5,093,885 5,192,399 5,289,493 5,384,674 5,477,389 5,567,022 5,652,884 5,734,209

Portfolio Withdrawal Rate 5.36% 5.42% 5.49% 5.56% 5.64% 5.73% 5.82% 5.93%

Scenario : Model 4- Risk Based using Average Returns

SAMPLE

Worksheet Detail - Retirement Distribution Cash Flow Chart

01/04/2016

Prepared for : John and Jane Smith Prepared by: John Advisor

Page 34 of 69

See IMPORTANT DISCLOSURE INFORMATION at the beginning and at the back of this document for explanations of assumptions, limitations, and methodologies.

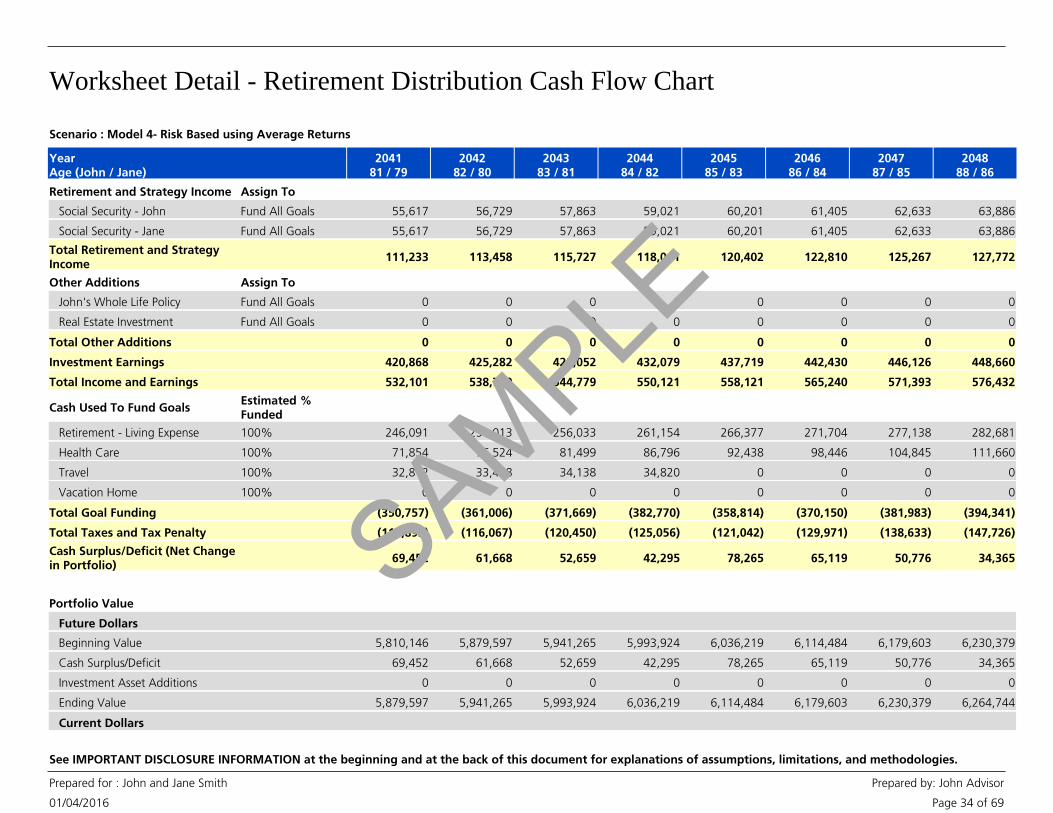

204181 / 79

204282 / 80

204383 / 81

204484 / 82

204585 / 83

204686 / 84

204787 / 85

204888 / 86

YearAge (John / Jane)

Retirement and Strategy Income Assign To

Social Security - John 55,617Fund All Goals 56,729 57,863 59,021 60,201 61,405 62,633 63,886

Social Security - Jane 55,617Fund All Goals 56,729 57,863 59,021 60,201 61,405 62,633 63,886

Total Retirement and StrategyIncome

111,233 113,458 115,727 118,041 120,402 122,810 125,267 127,772

Other Additions Assign To

John's Whole Life Policy 0Fund All Goals 0 0 0 0 0 0 0

Real Estate Investment 0Fund All Goals 0 0 0 0 0 0 0

Total Other Additions 0 0 0 0 0 0 0 0

Investment Earnings 420,868 425,282 429,052 432,079 437,719 442,430 446,126 448,660

Total Income and Earnings 532,101 538,740 544,779 550,121 558,121 565,240 571,393 576,432

Cash Used To Fund GoalsEstimated %Funded

Retirement - Living Expense 246,091100% 251,013 256,033 261,154 266,377 271,704 277,138 282,681

Health Care 71,854100% 76,524 81,499 86,796 92,438 98,446 104,845 111,660

Travel 32,812100% 33,468 34,138 34,820 0 0 0 0

Vacation Home 0100% 0 0 0 0 0 0 0

Total Goal Funding (350,757) (361,006) (371,669) (382,770) (358,814) (370,150) (381,983) (394,341)

Total Taxes and Tax Penalty (111,893) (116,067) (120,450) (125,056) (121,042) (129,971) (138,633) (147,726)

Cash Surplus/Deficit (Net Changein Portfolio)

69,452 61,668 52,659 42,295 78,265 65,119 50,776 34,365

Portfolio Value

Future Dollars

Beginning Value 5,810,146 5,879,597 5,941,265 5,993,924 6,036,219 6,114,484 6,179,603 6,230,379

Cash Surplus/Deficit 69,452 61,668 52,659 42,295 78,265 65,119 50,776 34,365

Investment Asset Additions 0 0 0 0 0 0 0 0

Ending Value 5,879,597 5,941,265 5,993,924 6,036,219 6,114,484 6,179,603 6,230,379 6,264,744

Current Dollars

Scenario : Model 4- Risk Based using Average Returns

SAMPLE

Worksheet Detail - Retirement Distribution Cash Flow Chart

01/04/2016

Prepared for : John and Jane Smith Prepared by: John Advisor

Page 35 of 69

See IMPORTANT DISCLOSURE INFORMATION at the beginning and at the back of this document for explanations of assumptions, limitations, and methodologies.

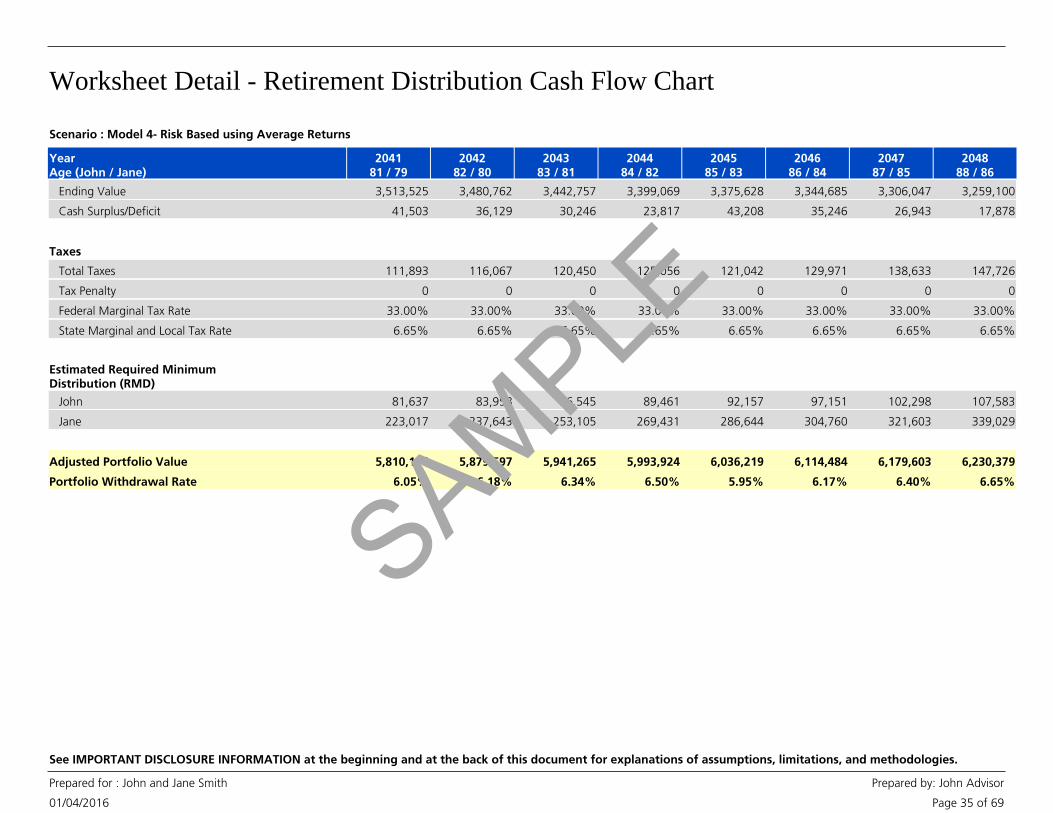

204181 / 79

204282 / 80

204383 / 81

204484 / 82

204585 / 83

204686 / 84

204787 / 85

204888 / 86

YearAge (John / Jane)

Ending Value 3,513,525 3,480,762 3,442,757 3,399,069 3,375,628 3,344,685 3,306,047 3,259,100

Cash Surplus/Deficit 41,503 36,129 30,246 23,817 43,208 35,246 26,943 17,878

Taxes

Total Taxes 111,893 116,067 120,450 125,056 121,042 129,971 138,633 147,726

Tax Penalty 0 0 0 0 0 0 0 0

Federal Marginal Tax Rate 33.00% 33.00% 33.00% 33.00% 33.00% 33.00% 33.00% 33.00%

State Marginal and Local Tax Rate 6.65% 6.65% 6.65% 6.65% 6.65% 6.65% 6.65% 6.65%

Estimated Required MinimumDistribution (RMD)

John 81,637 83,958 86,545 89,461 92,157 97,151 102,298 107,583

Jane 223,017 237,643 253,105 269,431 286,644 304,760 321,603 339,029

Adjusted Portfolio Value 5,810,146 5,879,597 5,941,265 5,993,924 6,036,219 6,114,484 6,179,603 6,230,379

Portfolio Withdrawal Rate 6.05% 6.18% 6.34% 6.50% 5.95% 6.17% 6.40% 6.65%

Scenario : Model 4- Risk Based using Average Returns

SAMPLE

Worksheet Detail - Retirement Distribution Cash Flow Chart

01/04/2016

Prepared for : John and Jane Smith Prepared by: John Advisor

Page 36 of 69

See IMPORTANT DISCLOSURE INFORMATION at the beginning and at the back of this document for explanations of assumptions, limitations, and methodologies.

204989 / 87

205090 / 88

2051- / 89

2052- / 90

2053- / 91

2054- / 92

YearAge (John / Jane)

Retirement and Strategy Income Assign To

Social Security - John 65,164Fund All Goals 66,467 0 0 0 0

Social Security - Jane 65,164Fund All Goals 66,467 67,796 69,152 70,535 71,946

Total Retirement and StrategyIncome

130,327 132,934 67,796 69,152 70,535 71,946

Other Additions Assign To

John's Whole Life Policy 0Fund All Goals 0 500,000 0 0 0

Real Estate Investment 0Fund All Goals 0 0 0 0 0

Total Other Additions 0 0 500,000 0 0 0

Investment Earnings 449,871 449,618 490,943 494,530 496,942 498,054

Total Income and Earnings 580,199 582,552 1,058,739 563,682 567,478 570,000

Cash Used To Fund GoalsEstimated %Funded

Retirement - Living Expense 288,335100% 294,101 239,987 244,786 249,682 254,676

Health Care 118,918100% 126,648 67,440 71,823 76,492 81,464

Travel 0100% 0 0 0 0 0

Vacation Home 0100% 0 0 0 0 0

Total Goal Funding (407,253) (420,749) (307,427) (316,610) (326,174) (336,140)

Total Taxes and Tax Penalty (157,229) (166,706) (189,936) (200,703) (211,648) (222,680)

Cash Surplus/Deficit (Net Changein Portfolio)

15,717 (4,903) 561,376 46,369 29,656 11,181

Portfolio Value

Future Dollars

Beginning Value 6,264,744 6,280,461 6,275,557 6,836,934 6,883,302 6,912,958

Cash Surplus/Deficit 15,717 (4,903) 561,376 46,369 29,656 11,181

Investment Asset Additions 0 0 0 0 0 0

Ending Value 6,280,461 6,275,557 6,836,934 6,883,302 6,912,958 6,924,139

Current Dollars

Scenario : Model 4- Risk Based using Average Returns

SAMPLE

Worksheet Detail - Retirement Distribution Cash Flow Chart

01/04/2016

Prepared for : John and Jane Smith Prepared by: John Advisor

Page 37 of 69

See IMPORTANT DISCLOSURE INFORMATION at the beginning and at the back of this document for explanations of assumptions, limitations, and methodologies.

204989 / 87

205090 / 88

2051- / 89

2052- / 90

2053- / 91

2054- / 92

YearAge (John / Jane)

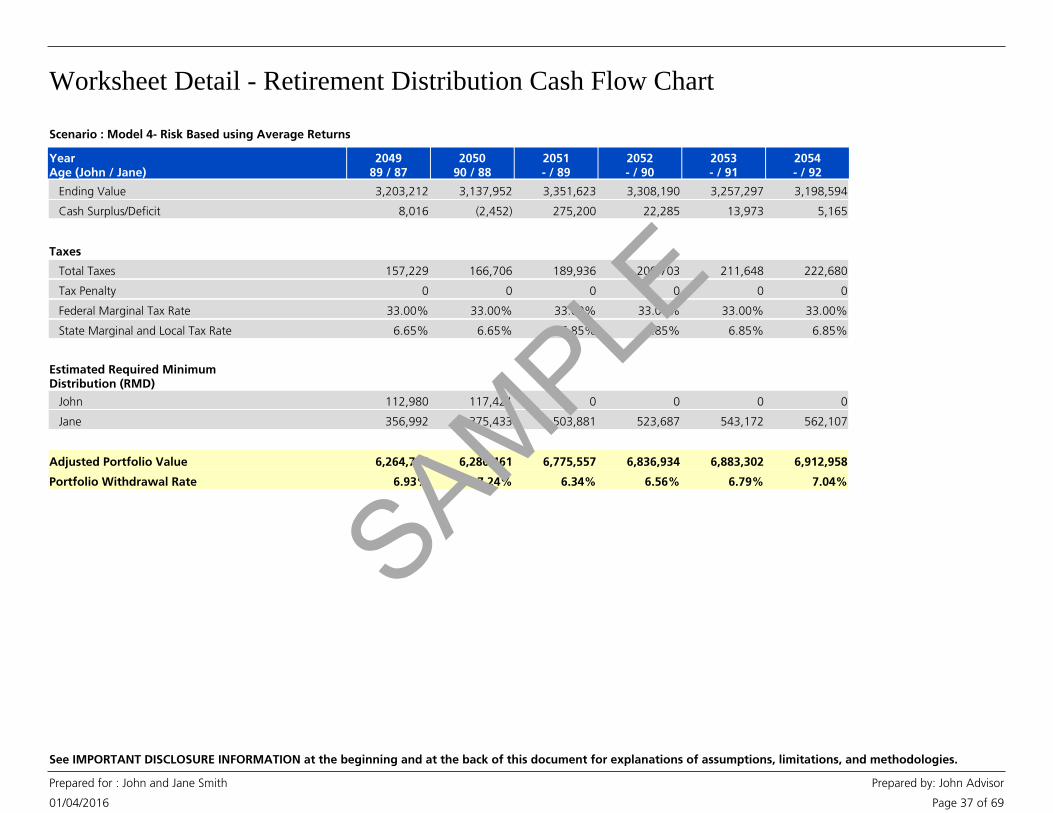

Ending Value 3,203,212 3,137,952 3,351,623 3,308,190 3,257,297 3,198,594

Cash Surplus/Deficit 8,016 (2,452) 275,200 22,285 13,973 5,165

Taxes

Total Taxes 157,229 166,706 189,936 200,703 211,648 222,680

Tax Penalty 0 0 0 0 0 0

Federal Marginal Tax Rate 33.00% 33.00% 33.00% 33.00% 33.00% 33.00%

State Marginal and Local Tax Rate 6.65% 6.65% 6.85% 6.85% 6.85% 6.85%

Estimated Required MinimumDistribution (RMD)

John 112,980 117,421 0 0 0 0

Jane 356,992 375,433 503,881 523,687 543,172 562,107

Adjusted Portfolio Value 6,264,744 6,280,461 6,775,557 6,836,934 6,883,302 6,912,958

Portfolio Withdrawal Rate 6.93% 7.24% 6.34% 6.56% 6.79% 7.04%

Scenario : Model 4- Risk Based using Average Returns

SAMPLE

Worksheet Detail - Retirement Distribution Cash Flow Chart

01/04/2016

Prepared for : John and Jane Smith Prepared by: John Advisor

Page 38 of 69

See IMPORTANT DISCLOSURE INFORMATION at the beginning and at the back of this document for explanations of assumptions, limitations, and methodologies.

Scenario : Model 4- Risk Based using Average Returns

• For married clients, if either Social Security Program Estimate or Use This Amount andEvaluate Annually is selected for a participant, the Program defaults to the greater of theselected benefit or the age-adjusted spousal benefit based on the other participant’sbenefit. The spousal benefit is not applicable to domestic partners.

• The Income section includes Retirement Income, Strategy Income, Stock Options,Restricted Stock, Other Assets, proceeds from Insurance Policies, and any remaining assetvalue after 72(t) distributions have been completed.

• Retirement Income includes the following: Social Security, pension, annuity, rentalproperty, royalty, alimony, part-time employment, trust, and any other retirement income asentered in the Scenario.

• Additions and withdrawals occur at the beginning of the year.

• Results may vary with use and over time.

• IMPORTANT: The projections or other information generated by this tool regarding thelikelihood of various investment outcomes are hypothetical in nature, do not reflect actualinvestment results, and are not guarantees of future results.

• The return assumptions used are estimates based on average annual returns for the indexused as a proxy for each asset class. The portfolio returns were calculated by weightingindividual return assumptions for each asset class according to the portfolio allocationselected by you or your Financial Advisor. The portfolio returns may have also been modifiedby your Financial Advisor to reflect the outcome of a different return by conducting a TotalReturn Adjustment or selecting a Custom Portfolio. For a explanation of the methodologyused to calculate returns, please review the Important Disclosure Information and ReturnMethodology sections.

• The return assumptions in this tool are not reflective of any specific product and do notinclude any fees or expenses that may be incurred by investing in specific products. Theactual returns of a specific product may be more or less than the returns used in this tool.

• No investment strategy or allocation can eliminate risk or guarantee investment results.

• The values shown for income and investment earnings are estimates based on theassumptions included in this report, such as rates of return, inflation rate, asset values, assetadditions, tax rates, income sources and amounts, and goal expenses. Any changes inassumptions will also change these values.

• Strategy Income is based on the particulars of the Goal Strategies selected. StrategyIncome from immediate annuities and 72(t) distributions is pre-tax. Strategy Income fromNet Unrealized Appreciation (NUA) is after-tax.

Notes