fannie mae matrices & guidelines - lenderselect...

TRANSCRIPT

LSMG Fannie Mae Matrices & Guidelines Page 1 of 37 Revised 06/17/2016

FANNIE MAE MATRICES & GUIDELINES

LSMG Fannie Mae Matrices & Guidelines Page 2 of 37 Revised 06/17/2016

Fannie Mae Matrices & Guidelines ........................................................ 1

LSMG Fannie Mae Purchase Matrix and Guidelines ............................ 5 Qualifying Matrix ............................................................................................................................................ 5 Primary Residence .......................................................................................................................................... 5 Second Home3 ................................................................................................................................................ 5 Investment Property3 ..................................................................................................................................... 5 HomeReady Mortgage .................................................................................................................................... 5

Borrower Income Eligibility .........................................................................................................................................6 Borrower Income Flexibilities .....................................................................................................................................6 Area Median Income ....................................................................................................................................................7 Mortgage Insurance (MI) Coverage and Financed MI ..............................................................................................7 Pricing ...........................................................................................................................................................................7 Homeownership Education ........................................................................................................................................7 Underwriting – Boarder Income and Rental Income ................................................................................................9 What’s the difference between boarder income and rental income? .......................................................................9 Non-Borrower Household Income Feature: ............................................................................................................10 Requirements and Underwriting ..............................................................................................................................10 Underwriting – Non-Occupant Borrowers ...............................................................................................................10 What’s the difference between a non-occupant borrower and a non-borrower household member? ...............10 Example: Cash-on-Hand ...........................................................................................................................................11 HomeReady Summary ...............................................................................................................................................11

Home Possible Advantage Mortgage1 ......................................................................................................... 12 Acceptable Funds for Down Payment, Closing Costs & Reserves ............................................................ 13 Earnest Money Deposit ................................................................................................................................ 13 Maximum Allowable Contributions from Interested Parties ................................................................... 13 Additional Requirements ............................................................................................................................. 14

Fannie Mae Refinance Matrix ............................................................... 15 Qualifying Matrix .......................................................................................................................................... 15 Cash-Out Refinance...................................................................................................................................... 15 No Cash-Out Refinance................................................................................................................................ 15 Conforming Loan Limits .............................................................................................................................. 15 Primary Residence ........................................................................................................................................ 16 Second Home13 ............................................................................................................................................. 16 Investment Property13 .................................................................................................................................. 16

Fannie Mae Guidelines .......................................................................... 17 Appraisals ...................................................................................................................................................... 17 Bankruptcy .................................................................................................................................................... 17 Condominiums - Full Review (New Construction Only) .......................................................................... 17

Declarations (Recorded) ............................................................................................................................................17 Articles of Incorporation ............................................................................................................................................17 Bylaws (Recorded) ......................................................................................................................................................17 Plat Map (Recorded) ..................................................................................................................................................17 Hazard Insurance (Master Policy) .............................................................................................................................17 Condo Association Budget for the Current Year (From HOA) ................................................................................17 Condo Questionnaire (Completed by HOA) ............................................................................................................18

Condominiums - Limited Review ............................................................................................................... 18 Limited Review Process for Detached Condo Units ................................................................................................18

LSMG Fannie Mae Matrices & Guidelines Page 3 of 37 Revised 06/17/2016

Projects Eligible for Limited Review (Attached Condos) .........................................................................................19 Projects Ineligible for Limited Review ......................................................................................................................19

Condominiums – Established Projects ....................................................................................................... 19 Condominiums – Hazard Insurance ........................................................................................................... 19

Two – Four Unit Condo Projects ...............................................................................................................................19 Condominiums - Ineligible Project Types (Streamline and Full Review) ............................................... 20

Ineligible Project Types ..............................................................................................................................................20 Eligible Borrowers ......................................................................................................................................... 21 Escrow Waivers ............................................................................................................................................. 21 Exceptions ..................................................................................................................................................... 22 Financed Properties (Maximum Number): Fannie Mae ........................................................................... 22

More Than Four Financed Properties (Including Second Homes or 1-4 Unit Investment Properties) ..............22 Reserve Requirements ...............................................................................................................................................22

FINANCED PROPERTIES (Maximum Number): FREDDIE MAC ............................................................. 23 Foreclosure .................................................................................................................................................... 23 Gift of Equity ................................................................................................................................................. 23

Acceptable Donors .....................................................................................................................................................23 Gift Funds ...................................................................................................................................................... 23

Acceptable Donors .....................................................................................................................................................23 Income ........................................................................................................................................................... 24

Alimony or Child Support ..........................................................................................................................................24 Base Pay (Salary and Hourly) .....................................................................................................................................25 Base Income Calculation Guidelines ........................................................................................................................25 Bonus and Overtime ..................................................................................................................................................26 Capital Gains Income .................................................................................................................................................26 Commission Income ..................................................................................................................................................26 Employment Offers or Contracts ..............................................................................................................................26 Long-Term Disability Income ...................................................................................................................................27 Military Income ..........................................................................................................................................................27 Rental Income from Property Other Than the Subject Property ............................................................................27 Rental Income from Previous Principal Residence .................................................................................................27 Retirement and Pension Income ..............................................................................................................................27 Seasonal Income ........................................................................................................................................................27 Secondary Employment Income ...............................................................................................................................28 Self-Employment ........................................................................................................................................................28 Social Security Income ...............................................................................................................................................28 Tip Income ..................................................................................................................................................................28 Unemployment Benefits ............................................................................................................................................28 VA Benefits Income ....................................................................................................................................................28

Conventional Self-Employment Matrix ...................................................................................................... 29 Positive vs. Negative Self-Employment ....................................................................................................................29 If Self-Employment Income is Counted in Order to Qualify, the Following is Required: .....................................29 If Self-Employment Income is Stated, but NOT Used to Qualify, the Following is Required for LP Only: ..........29 If using 2014 Income to Qualify, One of the Following is Required: ......................................................................29 Miscellaneous .............................................................................................................................................................29

Interested Party Contributions .................................................................................................................... 30 Installment Loans ......................................................................................................................................... 30

Ten Payments or Less Remaining .............................................................................................................................30 Cash-Out Refinances .................................................................................................................................... 30

Eligible Cash-Out Transactions .................................................................................................................................30 Ineligible Cash-Out Transactions .............................................................................................................................30 Acceptable Uses ..........................................................................................................................................................30

Limited Cash-Out Refinances (Rate and Term) ......................................................................................... 31 Eligible Limited Cash-Out Transactions (Rate and Term .......................................................................................31 Ineligible Limited Cash-Out Transactions (Rate and Term) ...................................................................................31

LSMG Fannie Mae Matrices & Guidelines Page 4 of 37 Revised 06/17/2016

Maximum Number of Financed Properties: Fannie Mae ......................................................................... 31 More Than Four Financed Properties (Including Second Homes or 1-4 Unit Investment Properties) ..............31 Reserve Requirements ...............................................................................................................................................32

MAXIMUM NUMBER OF FINANCED PROPERTIES: FREDDIE MAC ..................................................... 32 Non-Arm's Length Transactions ................................................................................................................. 32 Open Accounts .............................................................................................................................................. 33

Open 30 Day Charge Accounts ..................................................................................................................................33 Properties Listed For Sale............................................................................................................................. 33 Property Types - Eligible .............................................................................................................................. 33

One – Four Unit Properties ........................................................................................................................................33 Requirements for Factory-Built Housing other than Manufactured Housing ......................................................33 Property Location .......................................................................................................................................................33 Mixed-Use Properties ................................................................................................................................................34 Appraisal Requirements for Mixed-Use Properties .................................................................................................34 Multiple Parcels ..........................................................................................................................................................34

Property Types – Ineligible .......................................................................................................................... 34 Refinance to Buy-Out an Owner’s Interest ................................................................................................. 35 Refer with Caution Loans ............................................................................................................................. 35 Repair Escrows .............................................................................................................................................. 35 Reserves ......................................................................................................................................................... 35

Liquid Financial Reserves ..........................................................................................................................................35 Acceptable Sources of Reserves .................................................................................................................................36 Unacceptable Sources of Reserves ............................................................................................................................36

Seasoning Requirements ............................................................................................................................. 36 Second Homes .............................................................................................................................................. 36 Short Sale (Pre-Foreclosure Sale) ................................................................................................................ 36 Student Loans ............................................................................................................................................... 36 Vacating a Primary Residence Reserve Requirement ................................................................................ 37

LSMG Fannie Mae Matrices & Guidelines Page 5 of 37 Revised 06/17/2016

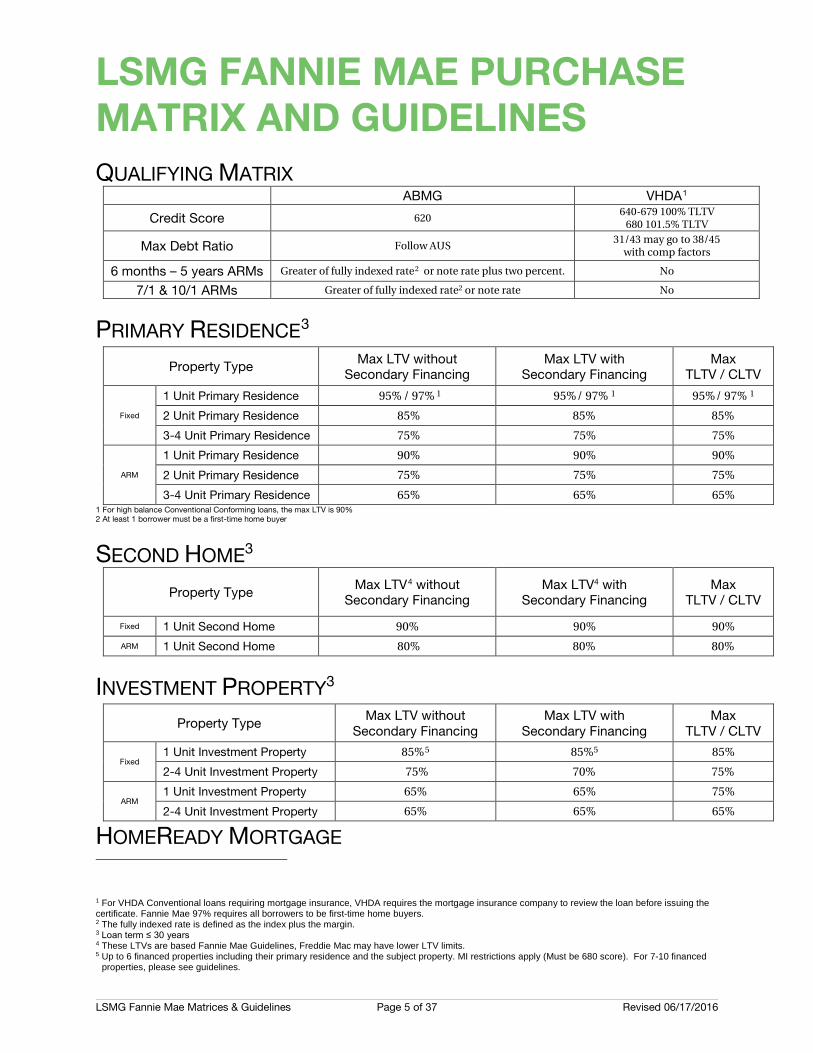

LSMG FANNIE MAE PURCHASE MATRIX AND GUIDELINES

QUALIFYING MATRIX ABMG VHDA1

Credit Score 620 640-679 100% TLTV 680 101.5% TLTV

Max Debt Ratio Follow AUS 31/43 may go to 38/45 with comp factors

6 months – 5 years ARMs Greater of fully indexed rate2 or note rate plus two percent. No

7/1 & 10/1 ARMs Greater of fully indexed rate2 or note rate No

PRIMARY RESIDENCE3 Property Type Max LTV without

Secondary Financing Max LTV with

Secondary Financing Max

TLTV / CLTV

Fixed

1 Unit Primary Residence 95% / 97% 1 95%/ 97% 1 95%/ 97% 1 2 Unit Primary Residence 85% 85% 85% 3-4 Unit Primary Residence 75% 75% 75%

ARM

1 Unit Primary Residence 90% 90% 90% 2 Unit Primary Residence 75% 75% 75% 3-4 Unit Primary Residence 65% 65% 65%

1 For high balance Conventional Conforming loans, the max LTV is 90% 2 At least 1 borrower must be a first-time home buyer

SECOND HOME3

Property Type Max LTV4 without

Secondary Financing Max LTV4 with

Secondary Financing Max

TLTV / CLTV

Fixed 1 Unit Second Home 90% 90% 90% ARM 1 Unit Second Home 80% 80% 80%

INVESTMENT PROPERTY3

Property Type Max LTV without

Secondary Financing Max LTV with

Secondary Financing Max

TLTV / CLTV

Fixed 1 Unit Investment Property 85%5 85%5 85% 2-4 Unit Investment Property 75% 70% 75%

ARM 1 Unit Investment Property 65% 65% 75% 2-4 Unit Investment Property 65% 65% 65%

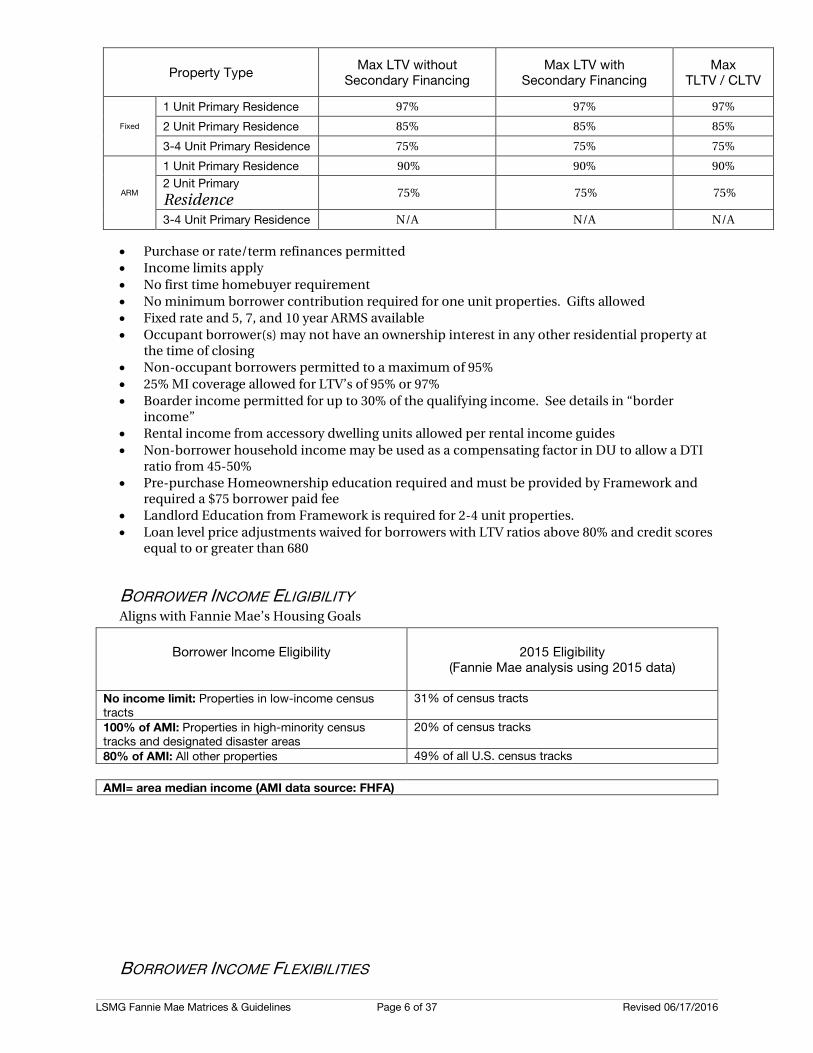

HOMEREADY MORTGAGE

1 For VHDA Conventional loans requiring mortgage insurance, VHDA requires the mortgage insurance company to review the loan before issuing the certificate. Fannie Mae 97% requires all borrowers to be first-time home buyers. 2 The fully indexed rate is defined as the index plus the margin. 3 Loan term ≤ 30 years 4 These LTVs are based Fannie Mae Guidelines, Freddie Mac may have lower LTV limits. 5 Up to 6 financed properties including their primary residence and the subject property. MI restrictions apply (Must be 680 score). For 7-10 financed

properties, please see guidelines.

LSMG Fannie Mae Matrices & Guidelines Page 6 of 37 Revised 06/17/2016

Property Type Max LTV without

Secondary Financing Max LTV with

Secondary Financing Max

TLTV / CLTV

Fixed

1 Unit Primary Residence 97% 97% 97% 2 Unit Primary Residence 85% 85% 85% 3-4 Unit Primary Residence 75% 75% 75%

ARM

1 Unit Primary Residence 90% 90% 90% 2 Unit Primary

Residence 75% 75% 75%

3-4 Unit Primary Residence N/A N/A N/A

• Purchase or rate/term refinances permitted • Income limits apply • No first time homebuyer requirement • No minimum borrower contribution required for one unit properties. Gifts allowed • Fixed rate and 5, 7, and 10 year ARMS available • Occupant borrower(s) may not have an ownership interest in any other residential property at

the time of closing • Non-occupant borrowers permitted to a maximum of 95% • 25% MI coverage allowed for LTV’s of 95% or 97% • Boarder income permitted for up to 30% of the qualifying income. See details in “border

income” • Rental income from accessory dwelling units allowed per rental income guides • Non-borrower household income may be used as a compensating factor in DU to allow a DTI

ratio from 45-50% • Pre-purchase Homeownership education required and must be provided by Framework and

required a $75 borrower paid fee • Landlord Education from Framework is required for 2-4 unit properties. • Loan level price adjustments waived for borrowers with LTV ratios above 80% and credit scores

equal to or greater than 680

BORROWER INCOME ELIGIBILITY Aligns with Fannie Mae’s Housing Goals

BORROWER INCOME FLEXIBILITIES

Borrower Income Eligibility

2015 Eligibility

(Fannie Mae analysis using 2015 data)

No income limit: Properties in low-income census tracts

31% of census tracts

100% of AMI: Properties in high-minority census tracks and designated disaster areas

20% of census tracks

80% of AMI: All other properties 49% of all U.S. census tracks AMI= area median income (AMI data source: FHFA)

LSMG Fannie Mae Matrices & Guidelines Page 7 of 37 Revised 06/17/2016

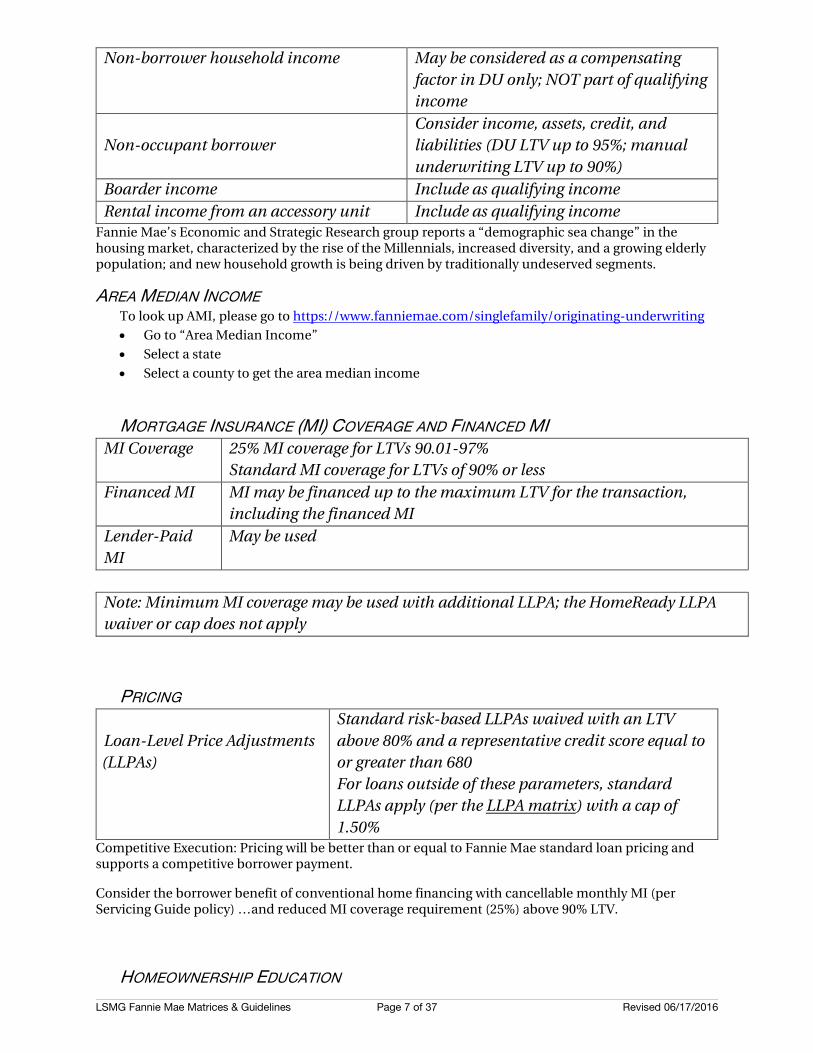

Non-borrower household income May be considered as a compensating factor in DU only; NOT part of qualifying income

Non-occupant borrower

Consider income, assets, credit, and liabilities (DU LTV up to 95%; manual underwriting LTV up to 90%)

Boarder income Include as qualifying income Rental income from an accessory unit Include as qualifying income

Fannie Mae’s Economic and Strategic Research group reports a “demographic sea change” in the housing market, characterized by the rise of the Millennials, increased diversity, and a growing elderly population; and new household growth is being driven by traditionally undeserved segments.

AREA MEDIAN INCOME To look up AMI, please go to https://www.fanniemae.com/singlefamily/originating-underwriting • Go to “Area Median Income” • Select a state • Select a county to get the area median income

MORTGAGE INSURANCE (MI) COVERAGE AND FINANCED MI MI Coverage 25% MI coverage for LTVs 90.01-97%

Standard MI coverage for LTVs of 90% or less Financed MI MI may be financed up to the maximum LTV for the transaction,

including the financed MI Lender-Paid MI

May be used

Note: Minimum MI coverage may be used with additional LLPA; the HomeReady LLPA waiver or cap does not apply

PRICING Loan-Level Price Adjustments (LLPAs)

Standard risk-based LLPAs waived with an LTV above 80% and a representative credit score equal to or greater than 680 For loans outside of these parameters, standard LLPAs apply (per the LLPA matrix) with a cap of 1.50%

Competitive Execution: Pricing will be better than or equal to Fannie Mae standard loan pricing and supports a competitive borrower payment.

Consider the borrower benefit of conventional home financing with cancellable monthly MI (per Servicing Guide policy) …and reduced MI coverage requirement (25%) above 90% LTV.

HOMEOWNERSHIP EDUCATION

LSMG Fannie Mae Matrices & Guidelines Page 8 of 37 Revised 06/17/2016

1-Unit 2- to 4-Unit Pre-Purchase Homeownership Education

• Homeownership education required prior to note date for at least on borrower on all transactions (purchase and LCOR).

• Must be provided through Framework (https://homeready.frameworkhomeownership.org), an online program approved by Fannie Mae. Some exceptions apply.

• $75 fee paid by the borrower to Framework for a simple, accessible online program with email support 7 days a week.

• Lenders may choose to provide a credit against closing costs.

• Homeownership education certificate must be retained in the mortgage file.

• Although one-on-one counseling is optional for HomeReady, Framework will offer borrowers a referral to a HUD-approved counseling agency for additional assistance, if requested by the borrower.

Special Borrower Considerations

• Online education may not be appropriate for all potential home buyers. The presence of disability, lack of Internet access, and other issues may indicate that a consumer is better served through other education modes (e.g., in-person classroom education, telephone conference call, etc.)

• ONLY in these situations, consumers should be directed to Framework’s toll-free customer service line (855-659-2267), from which they can be directed to a HUD-approved counseling agency that can meet their needs.

• The counseling agency that handles the referral must provide a certificate of completion, and the lender must retain a copy of the certificate in the loan file.

Post-Purchase Support To support sustainability, borrowers will have access to post-purchase homeownership support for the life of the loan through Framework’s homeownership advisor service.

LSMG Fannie Mae Matrices & Guidelines Page 9 of 37 Revised 06/17/2016

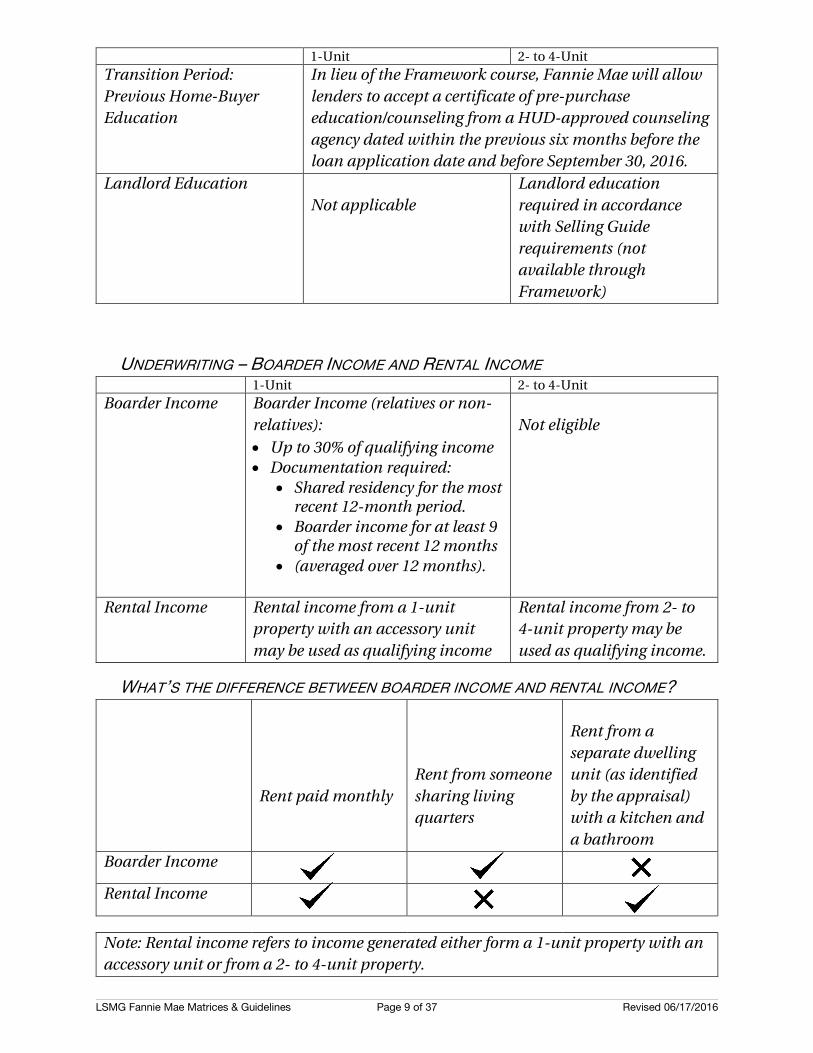

1-Unit 2- to 4-Unit Transition Period: Previous Home-Buyer Education

In lieu of the Framework course, Fannie Mae will allow lenders to accept a certificate of pre-purchase education/counseling from a HUD-approved counseling agency dated within the previous six months before the loan application date and before September 30, 2016.

Landlord Education Not applicable

Landlord education required in accordance with Selling Guide requirements (not available through Framework)

UNDERWRITING – BOARDER INCOME AND RENTAL INCOME 1-Unit 2- to 4-Unit Boarder Income Boarder Income (relatives or non-

relatives): • Up to 30% of qualifying income • Documentation required:

• Shared residency for the most recent 12-month period.

• Boarder income for at least 9 of the most recent 12 months

• (averaged over 12 months).

Not eligible

Rental Income Rental income from a 1-unit property with an accessory unit may be used as qualifying income

Rental income from 2- to 4-unit property may be used as qualifying income.

WHAT’S THE DIFFERENCE BETWEEN BOARDER INCOME AND RENTAL INCOME?

Rent paid monthly

Rent from someone sharing living quarters

Rent from a separate dwelling unit (as identified by the appraisal) with a kitchen and a bathroom

Boarder Income

Rental Income

Note: Rental income refers to income generated either form a 1-unit property with an accessory unit or from a 2- to 4-unit property.

LSMG Fannie Mae Matrices & Guidelines Page 10 of 37 Revised 06/17/2016

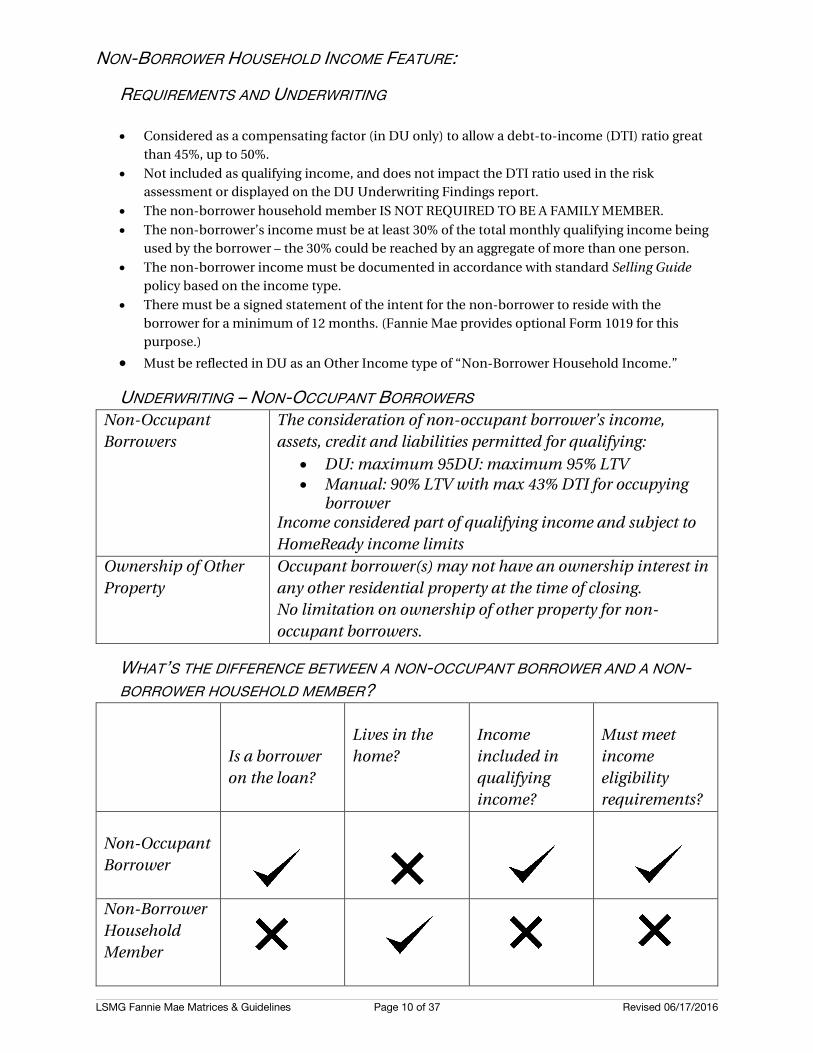

NON-BORROWER HOUSEHOLD INCOME FEATURE:

REQUIREMENTS AND UNDERWRITING

• Considered as a compensating factor (in DU only) to allow a debt-to-income (DTI) ratio great than 45%, up to 50%.

• Not included as qualifying income, and does not impact the DTI ratio used in the risk assessment or displayed on the DU Underwriting Findings report.

• The non-borrower household member IS NOT REQUIRED TO BE A FAMILY MEMBER. • The non-borrower’s income must be at least 30% of the total monthly qualifying income being

used by the borrower – the 30% could be reached by an aggregate of more than one person. • The non-borrower income must be documented in accordance with standard Selling Guide

policy based on the income type. • There must be a signed statement of the intent for the non-borrower to reside with the

borrower for a minimum of 12 months. (Fannie Mae provides optional Form 1019 for this purpose.)

• Must be reflected in DU as an Other Income type of “Non-Borrower Household Income.”

UNDERWRITING – NON-OCCUPANT BORROWERS Non-Occupant Borrowers

The consideration of non-occupant borrower’s income, assets, credit and liabilities permitted for qualifying:

• DU: maximum 95DU: maximum 95% LTV • Manual: 90% LTV with max 43% DTI for occupying

borrower Income considered part of qualifying income and subject to HomeReady income limits

Ownership of Other Property

Occupant borrower(s) may not have an ownership interest in any other residential property at the time of closing. No limitation on ownership of other property for non-occupant borrowers.

WHAT’S THE DIFFERENCE BETWEEN A NON-OCCUPANT BORROWER AND A NON-BORROWER HOUSEHOLD MEMBER?

Is a borrower on the loan?

Lives in the home?

Income included in qualifying income?

Must meet income eligibility requirements?

Non-Occupant Borrower

Non-Borrower Household Member

LSMG Fannie Mae Matrices & Guidelines Page 11 of 37 Revised 06/17/2016

EXAMPLE: CASH-ON-HAND A borrower who does not have a bank account wants to use money he has saved (cash-on-hand) for his down payment to purchase a 1-unit home.

• This is acceptable if the borrower customarily uses cash for expenses. • In addition, the lender must

- Verify that the amount of funds saved is consistent with the borrower’s previous payment practices

- Confirm that the funds are in a financial institution account or an acceptable escrow account (at the time of application, or no less than 30 days prior to closing)

- Obtain a written statement from the borrower that discloses the source of funds and states that the funds have been borrowed

- Determine that the borrower’s credit report and other verifications indicate limited or no use of credit and limited or depository relationship between the borrower and a financial institution.

HOMEREADY SUMMARY Redesigned/enhances affordable lending product with a new name

Borrower eligibility • Aligned with Fannie Mae’s regulatory housing

goals (includes underserved census tracts and minority, disaster areas)

• DU will identify borrower eligibility for all loans submitted to DU

Pricing – improved and simplified • Standard risk-based pricing waived for LTVs

>80% with a credit score >=680 • Competitive borrower payment • Execution always better than or equal to FNM

standard pricing Homeownership education • Mandatory pre-purchase homeownership

education via online Framework course • Access to post-purchase homeownership

advisors

New features • Eligibility

• FTHB and Non-FTHN to 97% LTV (DU only) • Manufactured Housing to 95% (DU only) • HomeStyle Renovation to 95% (requires

lender approval) Underwriting/income flexibility

• Household income as a compensating factor for DTI > 45% to 50% (DU only)

• Non-occupant borrower income • Rental income from accessory units (1-unit

property) • Boarder income documentation flexibility

LSMG Fannie Mae Matrices & Guidelines Page 12 of 37 Revised 06/17/2016

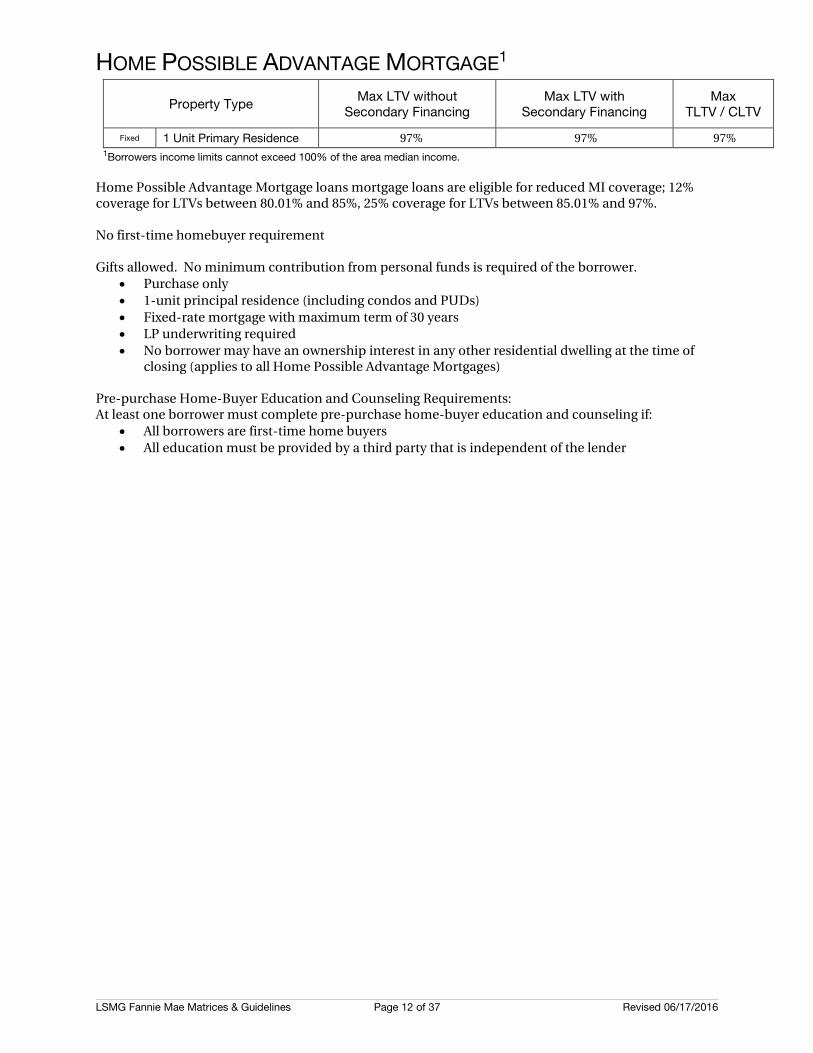

HOME POSSIBLE ADVANTAGE MORTGAGE1

Property Type Max LTV without

Secondary Financing Max LTV with

Secondary Financing Max

TLTV / CLTV

Fixed 1 Unit Primary Residence 97% 97% 97% 1Borrowers income limits cannot exceed 100% of the area median income. Home Possible Advantage Mortgage loans mortgage loans are eligible for reduced MI coverage; 12% coverage for LTVs between 80.01% and 85%, 25% coverage for LTVs between 85.01% and 97%. No first-time homebuyer requirement Gifts allowed. No minimum contribution from personal funds is required of the borrower.

• Purchase only • 1-unit principal residence (including condos and PUDs) • Fixed-rate mortgage with maximum term of 30 years • LP underwriting required • No borrower may have an ownership interest in any other residential dwelling at the time of

closing (applies to all Home Possible Advantage Mortgages)

Pre-purchase Home-Buyer Education and Counseling Requirements: At least one borrower must complete pre-purchase home-buyer education and counseling if:

• All borrowers are first-time home buyers • All education must be provided by a third party that is independent of the lender

LSMG Fannie Mae Matrices & Guidelines Page 13 of 37 Revised 06/17/2016

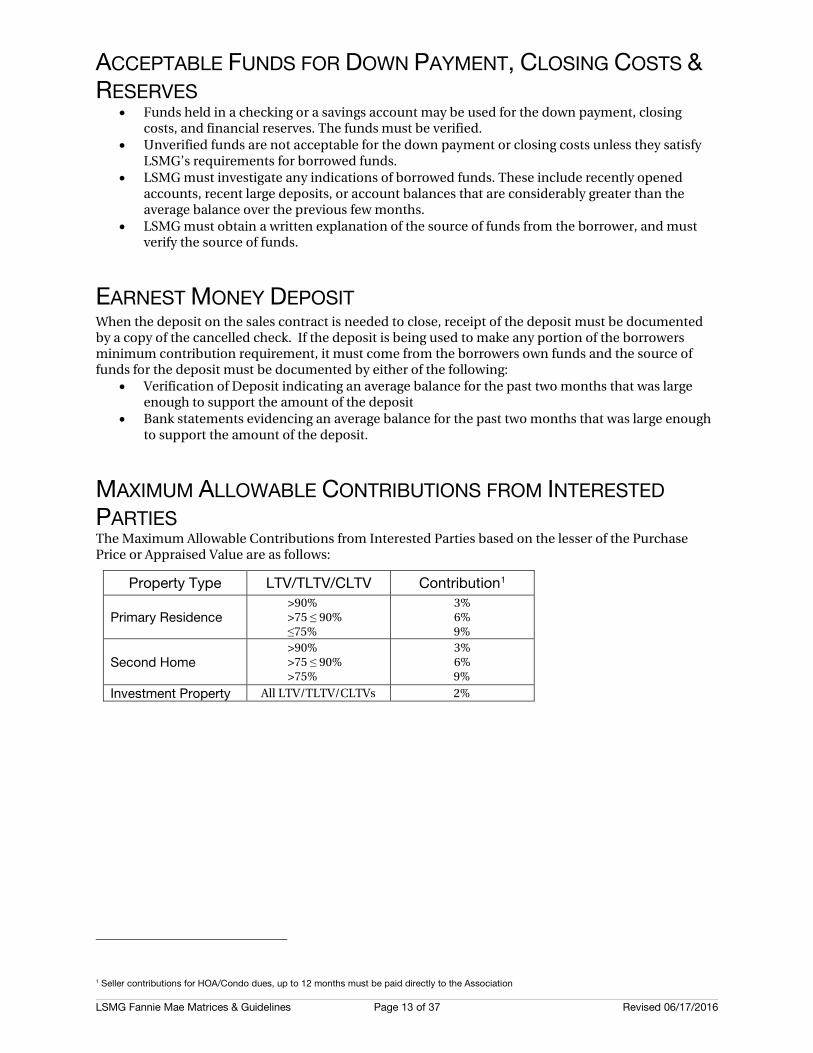

ACCEPTABLE FUNDS FOR DOWN PAYMENT, CLOSING COSTS & RESERVES

• Funds held in a checking or a savings account may be used for the down payment, closing costs, and financial reserves. The funds must be verified.

• Unverified funds are not acceptable for the down payment or closing costs unless they satisfy LSMG’s requirements for borrowed funds.

• LSMG must investigate any indications of borrowed funds. These include recently opened accounts, recent large deposits, or account balances that are considerably greater than the average balance over the previous few months.

• LSMG must obtain a written explanation of the source of funds from the borrower, and must verify the source of funds.

EARNEST MONEY DEPOSIT When the deposit on the sales contract is needed to close, receipt of the deposit must be documented by a copy of the cancelled check. If the deposit is being used to make any portion of the borrowers minimum contribution requirement, it must come from the borrowers own funds and the source of funds for the deposit must be documented by either of the following:

• Verification of Deposit indicating an average balance for the past two months that was large enough to support the amount of the deposit

• Bank statements evidencing an average balance for the past two months that was large enough to support the amount of the deposit.

MAXIMUM ALLOWABLE CONTRIBUTIONS FROM INTERESTED PARTIES The Maximum Allowable Contributions from Interested Parties based on the lesser of the Purchase Price or Appraised Value are as follows:

Property Type LTV/TLTV/CLTV Contribution1

Primary Residence >90% >75 ≤ 90% ≤75%

3% 6%

9%

Second Home >90% >75 ≤ 90% >75%

3% 6% 9%

Investment Property All LTV/TLTV/CLTVs 2%

1 Seller contributions for HOA/Condo dues, up to 12 months must be paid directly to the Association

LSMG Fannie Mae Matrices & Guidelines Page 14 of 37 Revised 06/17/2016

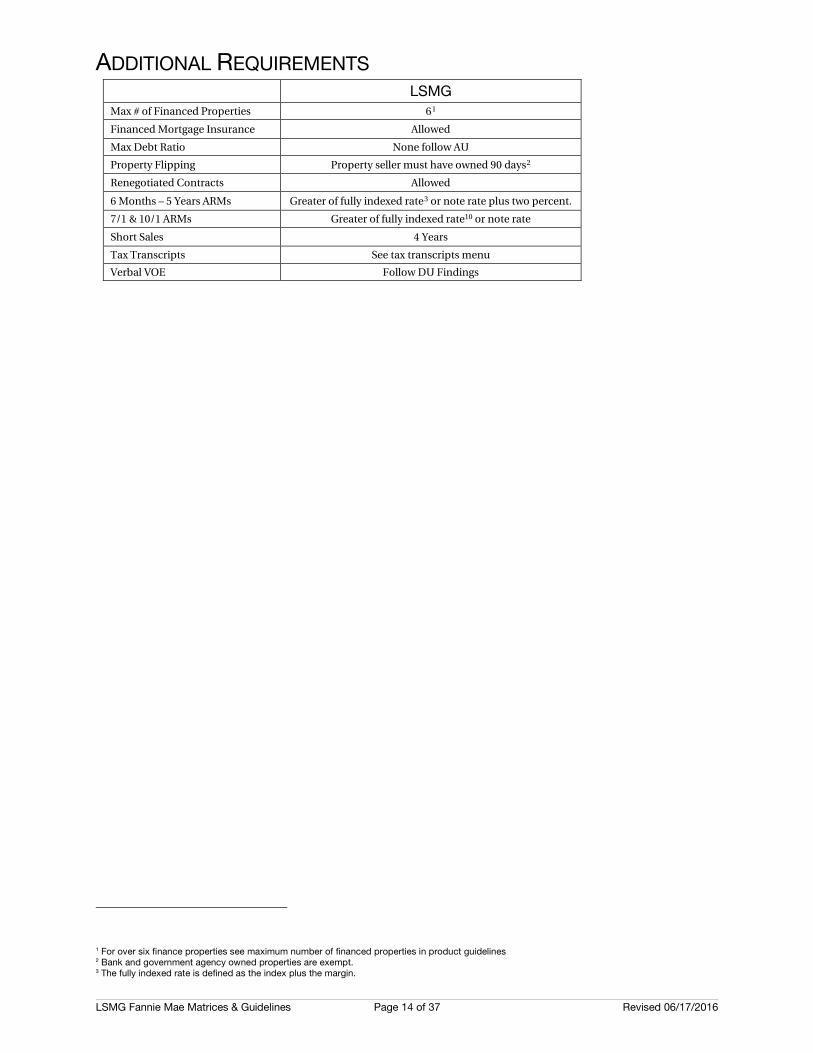

ADDITIONAL REQUIREMENTS LSMG

Max # of Financed Properties 61 Financed Mortgage Insurance Allowed Max Debt Ratio None follow AU Property Flipping Property seller must have owned 90 days2 Renegotiated Contracts Allowed 6 Months – 5 Years ARMs Greater of fully indexed rate3 or note rate plus two percent. 7/1 & 10/1 ARMs Greater of fully indexed rate10 or note rate Short Sales 4 Years Tax Transcripts See tax transcripts menu Verbal VOE Follow DU Findings

1 For over six finance properties see maximum number of financed properties in product guidelines 2 Bank and government agency owned properties are exempt.

3 The fully indexed rate is defined as the index plus the margin.

LSMG Fannie Mae Matrices & Guidelines Page 15 of 37 Revised 06/17/2016

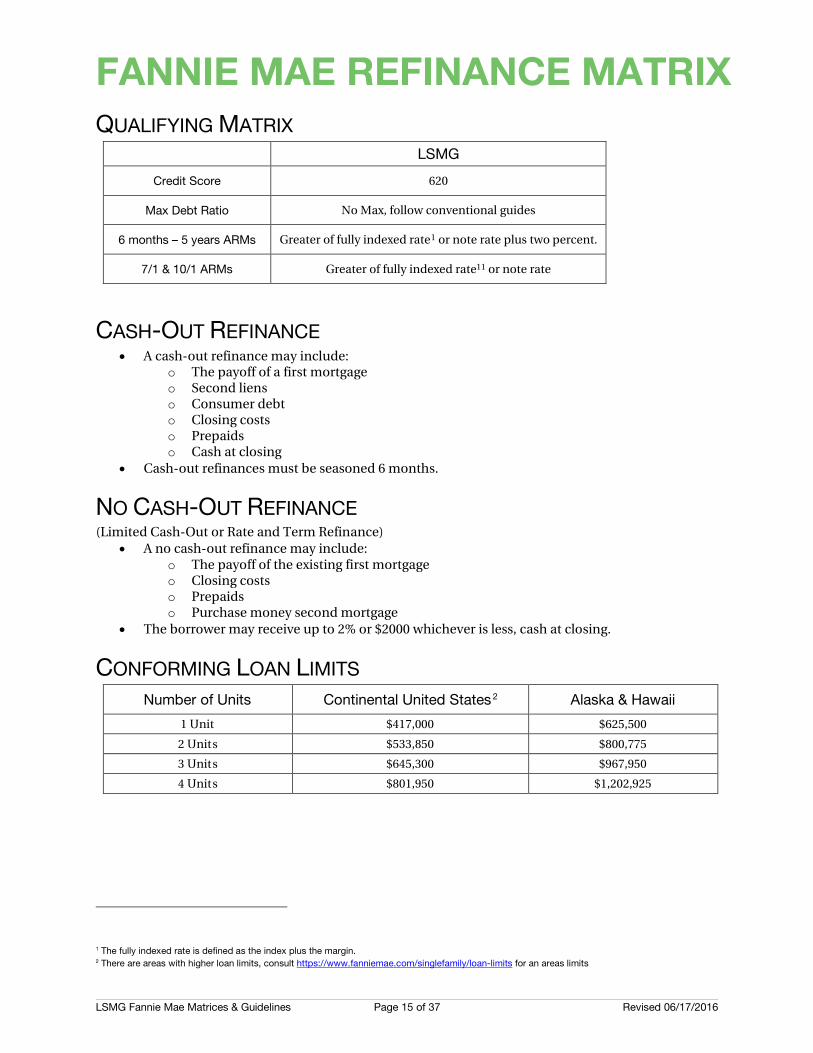

FANNIE MAE REFINANCE MATRIX

QUALIFYING MATRIX LSMG

Credit Score 620

Max Debt Ratio No Max, follow conventional guides

6 months – 5 years ARMs Greater of fully indexed rate1 or note rate plus two percent.

7/1 & 10/1 ARMs Greater of fully indexed rate11 or note rate

CASH-OUT REFINANCE • A cash-out refinance may include:

o The payoff of a first mortgage o Second liens o Consumer debt o Closing costs o Prepaids o Cash at closing

• Cash-out refinances must be seasoned 6 months.

NO CASH-OUT REFINANCE (Limited Cash-Out or Rate and Term Refinance)

• A no cash-out refinance may include: o The payoff of the existing first mortgage o Closing costs o Prepaids o Purchase money second mortgage

• The borrower may receive up to 2% or $2000 whichever is less, cash at closing.

CONFORMING LOAN LIMITS Number of Units Continental United States2 Alaska & Hawaii

1 Unit $417,000 $625,500 2 Units $533,850 $800,775 3 Units $645,300 $967,950 4 Units $801,950 $1,202,925

1 The fully indexed rate is defined as the index plus the margin. 2 There are areas with higher loan limits, consult https://www.fanniemae.com/singlefamily/loan-limits for an areas limits

LSMG Fannie Mae Matrices & Guidelines Page 16 of 37 Revised 06/17/2016

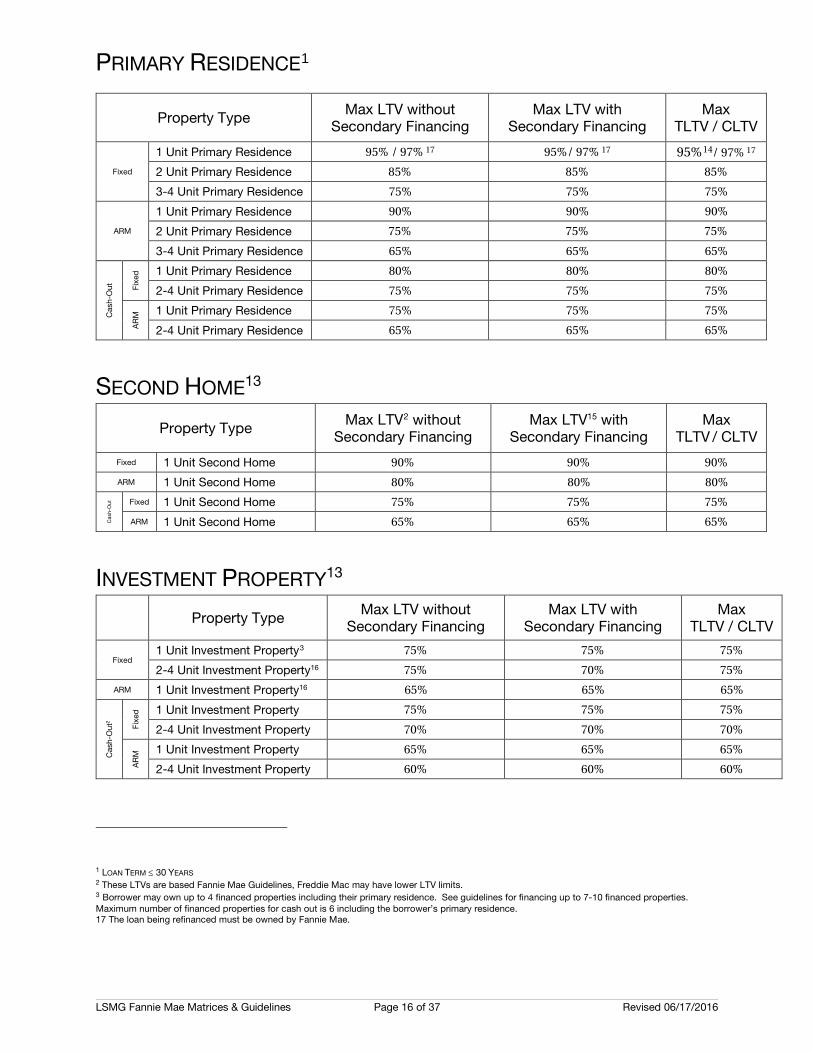

PRIMARY RESIDENCE1

Property Type Max LTV without Secondary Financing

Max LTV with Secondary Financing

Max TLTV / CLTV

Fixed

1 Unit Primary Residence 95% / 97% 17 95%/ 97% 17 95%14/ 97% 17

2 Unit Primary Residence 85% 85% 85% 3-4 Unit Primary Residence 75% 75% 75%

ARM

1 Unit Primary Residence 90% 90% 90% 2 Unit Primary Residence 75% 75% 75% 3-4 Unit Primary Residence 65% 65% 65%

Cas

h-O

ut

Fixe

d 1 Unit Primary Residence 80% 80% 80% 2-4 Unit Primary Residence 75% 75% 75%

AR

M 1 Unit Primary Residence 75% 75% 75%

2-4 Unit Primary Residence 65% 65% 65%

SECOND HOME13

Property Type Max LTV2 without Secondary Financing

Max LTV15 with Secondary Financing

Max TLTV / CLTV

Fixed 1 Unit Second Home 90% 90% 90% ARM 1 Unit Second Home 80% 80% 80%

Cas

h-O

ut Fixed 1 Unit Second Home 75% 75% 75%

ARM 1 Unit Second Home 65% 65% 65%

INVESTMENT PROPERTY13

Property Type Max LTV without

Secondary Financing Max LTV with

Secondary Financing Max

TLTV / CLTV

Fixed 1 Unit Investment Property3 75% 75% 75% 2-4 Unit Investment Property16 75% 70% 75%

ARM 1 Unit Investment Property16 65% 65% 65%

Cas

h-O

ut2

Fixe

d 1 Unit Investment Property 75% 75% 75% 2-4 Unit Investment Property 70% 70% 70%

AR

M 1 Unit Investment Property 65% 65% 65%

2-4 Unit Investment Property 60% 60% 60%

1 LOAN TERM ≤ 30 YEARS 2 These LTVs are based Fannie Mae Guidelines, Freddie Mac may have lower LTV limits. 3 Borrower may own up to 4 financed properties including their primary residence. See guidelines for financing up to 7-10 financed properties.

Maximum number of financed properties for cash out is 6 including the borrower’s primary residence. 17 The loan being refinanced must be owned by Fannie Mae.

LSMG Fannie Mae Matrices & Guidelines Page 17 of 37 Revised 06/17/2016

FANNIE MAE GUIDELINES APPRAISALS

• Conventional appraisals cannot be more than four months old to the date of closing. • An appraisal must be ordered through LSMG’s Appraisal Department. • The appraiser must be on LSMG’s Approved Appraiser List. • If a transfer appraisal is requested restrictions may apply, Contact the Appraisal Department for

procedures. • A recertification of value is acceptable if the recertification is ordered before the appraisal

expires.

BANKRUPTCY Approvals are available four years from dismissal date or 2 years from discharge date, and must receive an Automated Underwriting Accept.

CONDOMINIUMS - FULL REVIEW (NEW CONSTRUCTION ONLY) The underwriter will run the loan through Condo Project Manager. Project approval is good for 6 months and may be used for multiple borrowers. Project approval is not specific to each loan transaction. In order for the condo to be warranted, the following items must be obtained:

DECLARATIONS (RECORDED) The declarations must be recorded. The underwriter will review the documents to determine how many units were built or planned for. They will compare the number listed on the declarations to the number that was provided on the Condo Questionnaire. Should these figures differ; the underwriter will request any amendments to the declarations so that they match the Condo Questionnaire.

ARTICLES OF INCORPORATION

BYLAWS (RECORDED) The bylaws also must be recorded. These bylaws are the restrictions for the condo. The underwriter will verify there are no restrictions that prohibit our first lien on the property.

PLAT MAP (RECORDED) A plat map shows the entire subdivision (when it was proposed). The underwriter verifies this information matches the number of properties as stated in the declarations and questionnaire.

HAZARD INSURANCE (MASTER POLICY) The master policy must be provided to determine the complex has a minimum of one million dollars of general liability and the property has building replacement coverage. If there are more than 21 units in the condo, the underwriter must verify we have enough fidelity coverage (Crime Coverage). The policy must cover at least three months condo dues multiplied by the number of units in the project (See two to four unit condo projects for requirements).

CONDO ASSOCIATION BUDGET FOR THE CURRENT YEAR (FROM HOA)

LSMG Fannie Mae Matrices & Guidelines Page 18 of 37 Revised 06/17/2016

LSMG must have the most current year’s budget for the condo association. The underwriter must determine the condo association has enough reserves. A minimum of ten percent of the total dues must be a line item in the budget.

CONDO QUESTIONNAIRE (COMPLETED BY HOA) The underwriter determines that no more than 15% of the owners are delinquent for more than 60 days. The underwriter also determines: owner occupancy vs renters, if the condo is in litigation, and if more than one person owns ten percent of the units. At least 50% of the total units in the subject’s legal phase must have been conveyed to purchasers of primary residences. The occupancy/renter ratio is negotiable and is solely determined by Condo Project Manager. All other items mentioned negatively impact the approval of the condo and will result in a decline. *NOTE: New Condominiums in Florida are not eligible for full review.

CONDOMINIUMS - LIMITED REVIEW A limited review for a condo allows LSMG to streamline the condo approval process. A limited review eliminates the need to review the owner occupancy requirements as established by LSMG. In order to qualify for a limited review the Desktop Underwriter feedback must allow for a limited review and the project must meet the following:

Occupancy Type Maximum LTV/CLTV/HCLTV Maximum LTV/CLTV/HCLTV for Established Condos in Florida

Principal Residence ≤ 90% ≤ 75% Second Home ≤ 75% ≤ 70% Investment Property Not Allowed Not Allowed

LIMITED REVIEW PROCESS FOR DETACHED CONDO UNITS When LSMG performs a Limited Review for a mortgage secured by a detached unit in a condo project, we warrant that the following eligibility criteria have been met:

• The mortgage is secured by a single detached unit in a condo project. • The mortgage is not secured by a manufactured home. • The project is not an ineligible project. (See Ineligible Projects Section) • The condo unit is occupied as the owner’s principal residence or second home, whether the

loan is manually underwritten or submitted to Desktop Underwriter. • The condo unit is an investment property and the loan was submitted to Desktop

Underwriter. • The appraiser commented on, and reflected in the appraisal report, any effect that buyer

resistance to the condo form of ownership has on the market value of the individual unit. • If the condo project is new, the appraiser used as a comparable sale at least one detached

condo unit, which may be located either in a competing project or in the subject project, if the condo unit is offered by a builder other than the one that built the subject unit.

• The mortgage title insurance policy satisfies Fannie Mae’s special title insurance requirements for units in condo projects.

• The property is covered by either: o The type of hazard and flood insurance coverage required for single-family

detached dwellings, if the condo unit consists of the entire structure as well as the site and air space.

- OR - o The project’s master hazard and flood insurance policies, if the condo unit consists

only of the air space for the unit and the improvements and site are considered to be common areas or limited common areas.

• Fidelity Coverage (employee dishonesty) is not required.

LSMG Fannie Mae Matrices & Guidelines Page 19 of 37 Revised 06/17/2016

PROJECTS ELIGIBLE FOR LIMITED REVIEW (ATTACHED CONDOS) The Limited Review process enables LSMG to deliver individual loans secured by units in a project based on loan-level characteristics, if applicable.

A project must meet the following requirements to be eligible for a Limited Review:

• The project is not an ineligible project (see below) • The project does not consist of manufactured homes

• The project must be an established project (at least 90% of the total units in the project have been conveyed to the unit purchasers)

• The project is 100% complete, including all units and common elements • The project is not subject to additional phasing or annexation • Control of the homeowners’ association has been turned over to the unit owners

• The project is covered by insurance in accordance with LSMG’s hazard insurance requirements

PROJECTS INELIGIBLE FOR LIMITED REVIEW • Mortgages secured by attached units in new condo projects, whether they are manually

underwritten or submitted to Desktop Underwriter. • Mortgages secured by attached condo units that are investment properties.

CONDOMINIUMS – ESTABLISHED PROJECTS If the condominium does not qualify for Limited Review, the project must be certified through Fannie Mae’s Cond Project Manager. Items needed for a Full Review are:

• Association Budget • Master Insurance Policy • Condominium Questionnaire

The master policy must be provided to determine the complex has a minimum of one million dollars of general liability and the property has building replacement coverage. If there are more than 21 units in the condo, the underwriter must verify we have enough fidelity coverage (Crime Coverage). The policy must cover at least three months condo dues multiplied by the number of units in the project (See two to four unit condo projects for requirements).

LSMG must have the most current year’s budget for the condo association. The underwriter must determine the condo association has enough reserves. A minimum of ten percent of the total dues must be a line item in the budget.

The underwriter determines that no more than 15% of the owners are delinquent for more than 60 days. The underwriter also determines: owner occupancy vs renters, if the condo is in litigation, and if more than one person owns ten percent of the units. At least 50% of the total units in the subject’s legal phase must have been conveyed to purchasers of primary residences. The occupancy/renter ratio is negotiable and is solely determined by Condo Project Manager. All other items mentioned negatively impact the approval of the condo and will result in a decline. *NOTE: New Condominiums in Florida are not eligible for full review.

CONDOMINIUMS – HAZARD INSURANCE

TWO – FOUR UNIT CONDO PROJECTS • Must have $1,000,000.00 in general liability coverage in a master policy covering both units. The

policy must be in the name of the association. • HO3 condo insurance policy is required.

LSMG Fannie Mae Matrices & Guidelines Page 20 of 37 Revised 06/17/2016

• Master Flood Policy covering both units. • At least one unit must be sold as a Principal Residence. The borrower cannot own both units.

CONDOMINIUMS - INELIGIBLE PROJECT TYPES (Streamline and Full

Review) LSMG will not fund mortgages that are secured by units in certain types of PUD, condos, or cooperative projects, regardless of the characteristics of the unit mortgage.

INELIGIBLE PROJECT TYPES • Projects that are managed and operated as a hotel or motel, even though the units are

individually owned • Hotel or motel conversions (or conversions of other similar transient properties) • Projects with names that include the word “hotel” or “motel” • Projects that include registration services and offer rentals of units on a daily basis • Projects that restrict the owner’s ability to occupy the unit • Projects with mandatory rental pooling agreements that require unit owners to either rent their

units or give a management firm control over the occupancy of the units. Note: These formal agreements between the developer, homeowners’ association, and/or the individual unit owners, obligate the unit owner to rent the property on a seasonal, monthly, weekly, or daily basis. In many cases, the agreements include blackout dates, continuous occupancy limitations, and other such use restrictions. In return, the unit owner receives a share of the revenue generated from the rental of the unit.

• Projects with non-incidental business operations owned or operated by the homeowners’ association such as, but not limited to, a restaurant, a spa, a health club, etc.

• Investment securities (i.e. projects that have documents on file with the Securities and Exchange Commission, or projects where unit ownership is characterized or promoted as an investment opportunity)

• Common interest apartments or community apartment projects are projects or buildings that are owned by several owners as tenants-in-common or by a homeowners’ association in which individuals have an undivided interest in a residential apartment building and land, and have the right of exclusive occupancy of a specific apartment in the building

• Timeshare or segmented ownership projects • Houseboat projects • New projects where the seller is offering sale/financing structures in excess of LSMG’s eligibility

policies for individual mortgage loans. These excessive structures include, but are not limited to: builder/developer contributions, sales concessions, HOA or principal and interest payment abatements, and/or contributions not disclosed on the HUD-1 Settlement Statement.

• Projects where more than 25% of the total space is used for nonresidential purposes • Projects where a single entity (the same individual, investor group, partnership, or corporation)

owns more than ten percent of the total units in the project. • Multi-dwelling unit condos or co-op projects that permit an owner to hold title (or stock

ownership and the accompanying occupancy rights) to more than one dwelling unit, with ownership of all of his or her owned units (or shares) evidenced by a single deed and financed by a single mortgage (or share loan)

• Condo or co-op projects that represent a legal, but non-conforming, use of the land, if zoning regulations prohibit rebuilding the improvements to current density in the event of their partial or full destruction

• A tax-sheltered syndicate’s leasing to a co-op or “leasing” co-op projects that involve the leasing of the land and the improvements to the co-op corporation, even if the co-op corporation owns part of the building

• Co-op projects that are subject to leasehold estates • Limited equity co-op projects in which the co-op corporation places a limit on the amount of

return that can be received when stock or shares are sold • Co-op projects with units that are subject to resale restrictions or located on land owned by

community land trusts

LSMG Fannie Mae Matrices & Guidelines Page 21 of 37 Revised 06/17/2016

• Co-op projects in which the developer or sponsor has an ownership interest or other rights in the project real estate or facilities other than the interest or rights it has in relation to unsold units

• Any project (condo, co-op, or PUD) for which the homeowners’ association or co-op corporation is named as a party to pending litigation, or for which the project sponsor or developer is named as a party to pending litigation that relates to the safety, structural soundness, habitability, or functional use of the project. Note: Projects for which LSMG determines that pending litigation involves minor matters are not considered ineligible projects, provided the lender concludes that the pending litigation has no impact on the safety, structural soundness, habitability, or functional use of the project. The following are defined to be minor matters:

o Non-monetary litigation involving neighbor disputes or rights of quiet enjoyment; o Litigation for which the claimed amount is known, the insurance carrier has agreed to

provide the defense, and the amount is covered by the association's or co-op corporation's insurance; - OR -

o The homeowners' association or co-op corporation is named as the plaintiff in a foreclosure action, or as a plaintiff in an action for past due homeowners' association assessments.

• If LSMG is aware of pending litigation and is unable to determine whether the litigation may be deemed a minor matter, you may contact the underwriter to determine whether LSMG will accept mortgages secured by units in the project.

ELIGIBLE BORROWERS Two occupying borrowers, one with a credit score and one with no score, are eligible for conventional financing if the AUS findings come back as “Accept”. Pricing will be determined on the one borrower’s score.

ESCROW WAIVERS • LSMG requires an LTV of 80% or less for the borrower(s) to be eligible for an escrow waiver and

is subject to a price adjustment. • LSMG advocates the establishment of an escrow account for the payment of taxes and

insurance, particularly for borrowers with blemished credit histories or first-time homeowners. • LSMG may waive escrow account requirements for an individual first mortgage, provided the

standard escrow provision remains in the mortgage loan legal documents. LSMG cannot waive an escrow account for certain refinance transactions or for the payment of premiums for borrower-purchased mortgage insurance if applicable.

• When the requirement for an escrow account is waived, LSMG will retain rights to enforce the requirement in appropriate circumstances.

• When LSMG permits escrow waivers, subject to the mortgage documents and applicable law, the LSMG’s written policies must provide that the waiver not be based solely on the LTV ratio of a loan, but also on whether the borrower has the financial ability to handle the lump-sum payments of taxes, insurance, and other items described above.

• LSMG may have a written policy governing the circumstances under which escrow accounts may be waived. If an escrow account is not established, LSMG will provide borrowers with a timely, clearly written disclosure that advises them of the implications of not establishing an escrow account. The disclosure must:

o Inform borrowers of any applicable fees associated with the waiver of escrows; o Advise borrowers that in most cases they may contact their servicer to set up an escrow

account if they decide to do so even after the closing of their mortgage loan; o Advise borrowers that they are responsible for personally and directly paying the non-

escrowed items, in addition to paying the mortgage loan payment; and o Explain the consequences of a failure to pay non-escrowed items, including the

requirement for LSMG to place of insurance and the potentially higher cost, including any potential commission payments to LSMG and/or reduced coverage for borrowers under lender-placed insurance.

LSMG Fannie Mae Matrices & Guidelines Page 22 of 37 Revised 06/17/2016

EXCEPTIONS Please submit requests for exceptions to the guidelines to the exception screen in Byte. The following are LSMG Conventional Loan Guidelines that commonly receive exceptions.

• The property was previously listed for sale in the last six months is ineligible for Cash / Out Refinance. An exception may be granted with up to 70% LTV.

• Employment contracts require paystub within seven days after closing. Additional days may be granted.

• Borrowers with 5-10 financed properties with a maximum of 70% LTV. An exception of up to 75% LTV may be granted.

• The seller must be on the Title for 90 days. An exception of less than 90 days may be granted. • The waiting period for a foreclosure is seven years. A shorter waiting period, with a minimum

of five years, may be granted. • If a home has been listed for sale in the last six months it may be eligible for normal loan to

value limits if it can be verified that the property has been taken off the market prior to the refinance application.

FINANCED PROPERTIES (MAXIMUM NUMBER): FANNIE MAE

MORE THAN SIX FINANCED PROPERTIES1 (INCLUDING SECOND HOMES OR 1-4

UNIT INVESTMENT PROPERTIES) When purchasing or refinancing a Second Home or Investment Property, the borrower may own or be obligated on up to ten financed properties (including the Primary residence), provided the borrower meets the following criteria: • A minimum credit score of 720 is required for 7-10 properties only • Desktop Underwriter only • Purchase or Rate and Term Refinances: MAX 70% LTV/CLTV • Cash-out refinance transactions are not permitted for 7-10 properties only • No history of bankruptcy or foreclosure within the past seven years • No late mortgage payments (30 days or greater) within the past twelve months • Regardless of Desktop Underwriter findings, rental income on the subject Investment Property

must be fully documented, and rental income that is being used to qualify the borrower(s) from other retained properties must be supported by two years of tax returns

• The borrower(s) must complete and sign Form 4506-T (Request for Transcript of Tax Return) and the transcript(s) must be obtained from the IRS to validate the accuracy of the tax returns provided by the borrower(s)

RESERVE REQUIREMENTS If the borrower owns other financed properties, additional reserves must be calculated and documented for financed properties other than the subject property and the borrower’s principal residence. The other financed properties reserves amount must be determined by applying a specific percentage to the outstanding unpaid principal balance (UPB) for mortgage and HELOCs on these other financed properties. The percentages are based on the number of financed properties:

o 2% of the UPB if the borrower has one to four financed properties, o 4% of the UPB if the borrower has five to six financed properties, or o 6% of the UPB if the borrower has seven to ten financed properties (DU only).

1 Including Second Homes or 1-4 Unit Investment Properties

LSMG Fannie Mae Matrices & Guidelines Page 23 of 37 Revised 06/17/2016

The UPB calculation does not include the mortgages and HELOCs that are on the subject property, the borrower’s principal residence, properties that are sold or pending sale, and accounts that will be paid by closing (or omitted in DU on the online loan application). Note: DU will also include in the UPB calculation open mortgages and HELOCs on the credit report that are not disclosed on the online loan application.

FINANCED PROPERTIES (MAXIMUM NUMBER): FREDDIE MAC In analyzing other real estate financed by a borrower who is applying for a mortgage for a second home or investment property, the number of allowable other properties for which the borrower is financially obligated is six. The borrower no longer needs to have a two year history of managing investment properties, and that he/she maintain six months of rent loss insurance in order to use income from an investment property for qualifying purposes. These changes are effective for settlement dates on or after October 26, 2015. Properties #5 and #6 are eligible for the same LTV limits as properties #1 - #4.

FORECLOSURE A seven year waiting period is required and is measured from the completion date of the foreclosure action as reported on the credit report or other foreclosure documents provided by the borrower.

GIFT OF EQUITY A gift of equity refers to a gift provided by the seller of a property to the buyer. The gift represents a portion of the seller’s equity in the property, and is transferred to the buyer as a credit in the transaction. A gift of equity is permitted for principal residence and second home purchase transactions. The acceptable donor and minimum borrower contribution requirements for gifts also apply to gifts of equity. The following two documents must be retained in the loan file:

• A signed gift letter • The HUD-1 Settlement Statement listing the gift of equity

ACCEPTABLE DONORS A gift can be provided by: • A relative which is defined as the borrower’s spouse, child, or other dependent, or by any other

individual who is related to the borrower by blood, marriage, adoption, or legal guardianship • A fiancé, fiancée, or domestic partner.

The donor may not be, or have any affiliation with, the builder, the developer, the real estate agent, or any other interested party to the transaction.

GIFT FUNDS A borrower of a mortgage loan secured by a principal residence may use funds received as a personal gift from an acceptable donor. Gift funds may fund all or part of the down payment, closing costs, or financial reserves subject to the minimum borrower contribution requirements. Borrowers using less than five percent of their own funds are required to have a minimum 660 credit score and no greater than a 50% payment shock1. Gifts are not allowed on an investment property.

ACCEPTABLE DONORS A gift can be provided by:

1 Borrowers with no current housing expense will be considered on a case by case basis to evaluate the payment shock.

LSMG Fannie Mae Matrices & Guidelines Page 24 of 37 Revised 06/17/2016

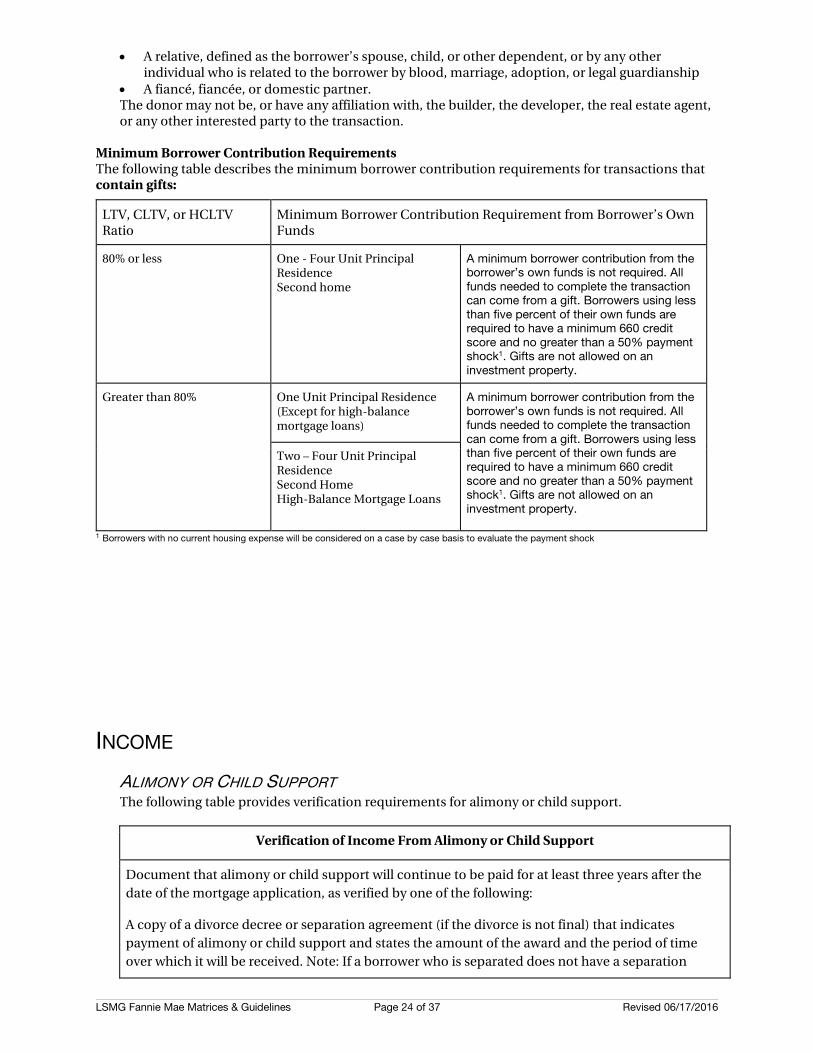

• A relative, defined as the borrower’s spouse, child, or other dependent, or by any other individual who is related to the borrower by blood, marriage, adoption, or legal guardianship

• A fiancé, fiancée, or domestic partner. The donor may not be, or have any affiliation with, the builder, the developer, the real estate agent, or any other interested party to the transaction.

Minimum Borrower Contribution Requirements The following table describes the minimum borrower contribution requirements for transactions that contain gifts:

LTV, CLTV, or HCLTV Ratio

Minimum Borrower Contribution Requirement from Borrower’s Own Funds

80% or less One - Four Unit Principal Residence Second home

A minimum borrower contribution from the borrower’s own funds is not required. All funds needed to complete the transaction can come from a gift. Borrowers using less than five percent of their own funds are required to have a minimum 660 credit score and no greater than a 50% payment shock1. Gifts are not allowed on an investment property.

Greater than 80% One Unit Principal Residence (Except for high-balance mortgage loans)

A minimum borrower contribution from the borrower’s own funds is not required. All funds needed to complete the transaction can come from a gift. Borrowers using less than five percent of their own funds are required to have a minimum 660 credit score and no greater than a 50% payment shock1. Gifts are not allowed on an investment property.

Two – Four Unit Principal Residence Second Home High-Balance Mortgage Loans

1 Borrowers with no current housing expense will be considered on a case by case basis to evaluate the payment shock

INCOME

ALIMONY OR CHILD SUPPORT The following table provides verification requirements for alimony or child support.

Verification of Income From Alimony or Child Support

Document that alimony or child support will continue to be paid for at least three years after the date of the mortgage application, as verified by one of the following:

A copy of a divorce decree or separation agreement (if the divorce is not final) that indicates payment of alimony or child support and states the amount of the award and the period of time over which it will be received. Note: If a borrower who is separated does not have a separation

LSMG Fannie Mae Matrices & Guidelines Page 25 of 37 Revised 06/17/2016

agreement that specifies alimony or child support payments, the lender should not consider any proposed or voluntary payments as income.

• Any other type of written legal agreement or court decree describing the payment terms for the alimony or child support.

• Documentation that verifies any applicable state law that mandates alimony, child support, or separate maintenance payments, which must specify the conditions under which the payments must be made.

Check for limitations on the continuance of the payments, such as the age of the children for whom the support is being paid or the duration over which alimony is required to be paid.

Document no less than six months of the borrower’s most recent regular receipt of the full payment with copies of bank statements.

Review the payment history to determine its suitability as stable qualifying income. To be considered stable income, full, regular, and timely payments must have been received for six months or longer. Income received for less than six months is considered unstable and may not be used to qualify the borrower for the mortgage. In addition, if full or partial payments are made on an inconsistent or sporadic basis, the income is not acceptable for the purpose of qualifying the borrower.

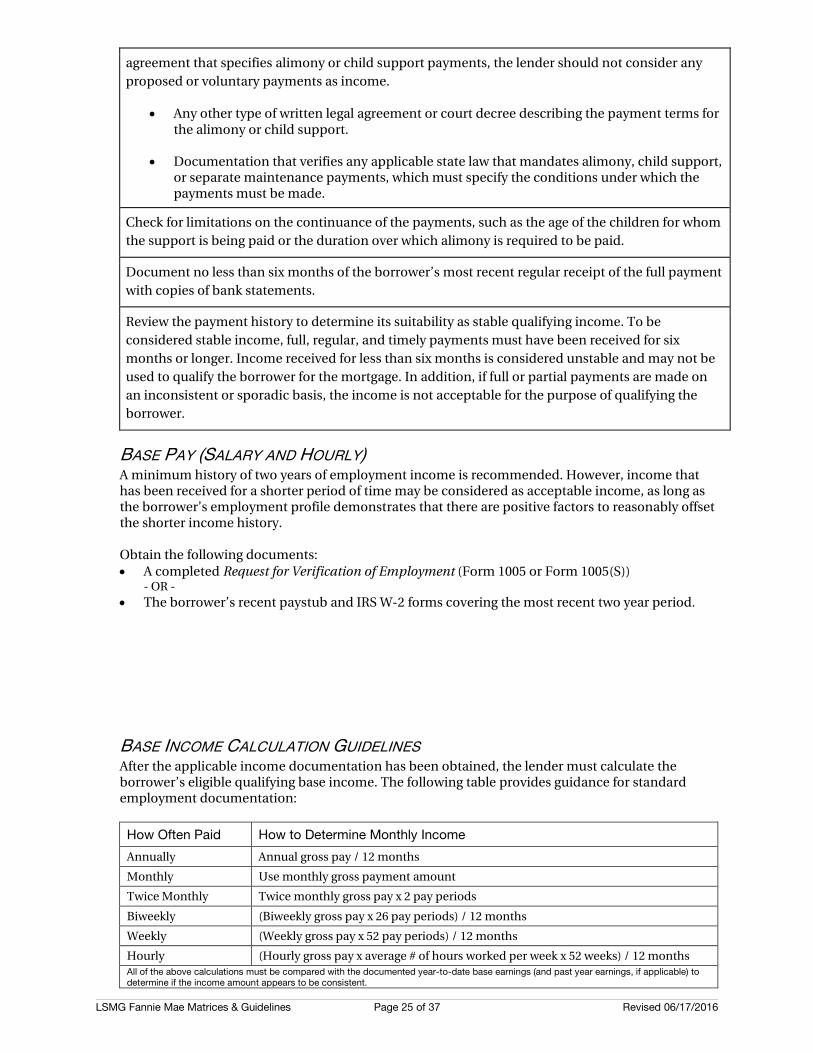

BASE PAY (SALARY AND HOURLY) A minimum history of two years of employment income is recommended. However, income that has been received for a shorter period of time may be considered as acceptable income, as long as the borrower’s employment profile demonstrates that there are positive factors to reasonably offset the shorter income history. Obtain the following documents: • A completed Request for Verification of Employment (Form 1005 or Form 1005(S))

- OR - • The borrower’s recent paystub and IRS W-2 forms covering the most recent two year period.

BASE INCOME CALCULATION GUIDELINES After the applicable income documentation has been obtained, the lender must calculate the borrower’s eligible qualifying base income. The following table provides guidance for standard employment documentation:

How Often Paid How to Determine Monthly Income

Annually Annual gross pay / 12 months Monthly Use monthly gross payment amount Twice Monthly Twice monthly gross pay x 2 pay periods Biweekly (Biweekly gross pay x 26 pay periods) / 12 months Weekly (Weekly gross pay x 52 pay periods) / 12 months Hourly (Hourly gross pay x average # of hours worked per week x 52 weeks) / 12 months All of the above calculations must be compared with the documented year-to-date base earnings (and past year earnings, if applicable) to determine if the income amount appears to be consistent.

LSMG Fannie Mae Matrices & Guidelines Page 26 of 37 Revised 06/17/2016

BONUS AND OVERTIME Borrowers relying on overtime or bonus income for qualifying purposes must have a history of no less than 12 months to be considered stable.

Obtain the following documents: • A completed Form 1005 or Form 1005(S), or the borrower’s recent paystub and IRS W-2 forms

covering the most recent two year period. • If the borrower has recently changed positions with his or her employer, determine the effect of

the change on the borrower’s eligibility and opportunity to receive bonus or overtime pay in the future.

• If a borrower who has historically been employed on a part-time basis indicates that he or she will now be working full-time, obtain written confirmation from the borrower’s employer.

• A verbal VOE is required from each employer.

CAPITAL GAINS INCOME • LSMG will document a two-year history of capital gains income by obtaining copies of the

borrower’s signed federal income tax returns that were filed with the IRS for the past two years, including IRS Form 1040, Schedule D.

• LSMG will develop an average income from the last two- years and use the averaged amount as part of the borrower’s qualifying income as long as the borrower provides evidence that he or she owns additional property or assets that can be sold if extra income is needed to make future mortgage loan payments. Note: Capital losses identified on IRS Form 1040, Schedule D, do not have to be considered when calculating income or liabilities, even if the losses are recurring.

COMMISSION INCOME A minimum history of 2 years of commission income is recommended; however, commission income that has been received for 12 to 24 months may be considered as acceptable income, as long as there are positive factors to reasonably offset the shorter income history.

If the commission income represents less that 25% of the borrower's total annual employment income, obtain the following documents: • A completed Request for Verification of Employment (Form 1005 or Form 1005(S))

- OR - • The borrower’s recent paystub and IRS W-2 forms covering the most recent two year period. • If commission income represents 25% or more of the borrower’s total annual employment

income, obtain the following documents: • Copies of the borrower’s signed federal income tax returns that were filed with the IRS for the

past two years; and either o A completed Form 1005 or Form 1005(S)

- OR - o The borrower’s recent paystub and IRS W-2 forms covering the most recent two-year

period.

If tax returns are obtained, any non-reimbursed business expenses must be subtracted from the gross commission income.

EMPLOYMENT OFFERS OR CONTRACTS • LSMG must document the borrower’s income and employment history • LSMG must obtain the borrower’s offer or signed contract with no contingencies for future

employment and anticipated income. • The borrower must begin employment before the loan closes. LSMG must obtain a paystub

from the borrower that includes sufficient information to support the income used to qualify

LSMG Fannie Mae Matrices & Guidelines Page 27 of 37 Revised 06/17/2016

the borrower within seven days after closing.

LONG-TERM DISABILITY INCOME A copy of the borrower’s disability policy or benefits statement from the benefits payer (insurance company, employer, or other qualified disinterested party) must be obtained to determine: • The borrower’s current eligibility for the disability benefits. • The amount and frequency of the disability payments. • If there is a contractually established termination or modification date.

Generally, long-term disability will not have a defined expiration date and must be expected to continue. The requirement for re-evaluation of benefits is not considered a defined expiration date. If a borrower is currently receiving short-term disability payments that will decrease to a lesser amount within the next three years because they are being converted to long-term benefits, the amount of the long-term benefits must be used as income to qualify the borrower.

MILITARY INCOME • Military personnel may be entitled to different types of pay in addition to their base pay. Flight

or hazard pay, rations, clothing allowance, quarters’ allowance, and proficiency pay are acceptable sources of stable income, as long as the lender can establish that the particular source of income will continue to be received in the future.

• Income paid to military reservists while they are satisfying their reserve obligations also is acceptable if it satisfies the same stability and continuity tests applied to secondary employment.

RENTAL INCOME FROM PROPERTY OTHER THAN THE SUBJECT PROPERTY When the borrower owns property, other than the subject property, that is rented, the lender must document the monthly gross (and net) rental income with the borrower’s most recent signed federal income tax return that includes Schedule E. Copies of the current lease agreement(s) may be substituted if the borrower can document a qualifying exception.

RENTAL INCOME FROM PREVIOUS PRINCIPAL RESIDENCE To be able to count rental income from a previous principal residence the following items are required: • A copy of the lease that covers a minimum of twelve months. • Reserve requirements above must be met

RETIREMENT AND PENSION INCOME Document regular and continued receipt of the income, as verified by one of the following: • Letters regular from the organizations providing the income • Copies of retirement award letters. • Copies of signed federal income tax returns. • IRS W-2 or 1099 forms.

- OR - • Copies of the borrower’s two most recent bank statements.

If retirement income is paid in the form of a monthly distribution from a 401(k), IRA, or Keogh retirement account, determine whether the income is expected to continue for at least three years after the date of the mortgage application. In addition; • The borrower must have unrestricted access without penalty to the accounts;

- AND - • If the assets are in the form of stocks, bonds, or mutual funds, 70% of the value (remaining after

any applicable costs for the subject transaction) must be used to determine the number of distributions remaining to account for the volatile nature of these assets

SEASONAL INCOME

LSMG Fannie Mae Matrices & Guidelines Page 28 of 37 Revised 06/17/2016

• Verify that the borrower has worked in the same job (or the same line of seasonal work) for the past two years.

• Confirm with the borrower’s employer that there is a reasonable expectation that the borrower will be rehired for the next season.

• For seasonal unemployment compensation, verify that it is appropriately documented, clearly associated with seasonal layoffs, expected to recur, and reported on the borrower’s signed federal income tax returns. Otherwise, unemployment compensation cannot be used to qualify the borrower.

SECONDARY EMPLOYMENT INCOME • Verification of a minimum history of two years of uninterrupted secondary employment

income is recommended. However, income that has been received for a shorter period of time (no less than 12 months) may be considered as acceptable income, as long as there are positive factors to reasonably offset the shorter income history.

• A borrower may have a history that includes different employers, which is acceptable as long as income has been consistently received.

SELF-EMPLOYMENT See Self-Employment Matrix

SOCIAL SECURITY INCOME Document regular receipt of payments, as verified by one of the following: • A copy of the Social Security Administration’s award letter • Copies of signed federal income tax returns • Social Security Benefit Statement (Form SSA-1099)

- OR - • Copies of the borrower’s recent bank statements Social Security income for retirement or long-term disability will not have a defined expiration date and must be expected to continue. However, if the Social Security benefits are not for retirement or long-term disability, LSMG must confirm that the remaining term is at least three years from the date of the mortgage application. An example of evidence of continuance would be third- party documentation from a doctor.

TIP INCOME Obtain the following documents: • A completed Request for Verification of Employment (Form 1005 or Form 1005(S))

- OR - • The borrower’s recent paystub and IRS W-2 forms covering the most recent two year period.

Tip income may be used to qualify the borrower if the lender verifies that the borrower has received it for the last two years. The lender must determine the amount of tip income that may be considered in qualifying the borrower.

Tip income must be entered in DU in the Other Monthly Income section of the loan application as “Other Types of Income” and verified according to these requirements.

UNEMPLOYMENT BENEFITS • Document that the borrower has received the payments consistently for at least two years by

obtaining copies of signed federal income tax returns. • Unemployment compensation cannot be used to qualify the borrower unless it is clearly

associated with seasonal employment that is reported on the borrower’s signed federal income tax returns. Verify that the seasonal income is likely to continue.

VA BENEFITS INCOME • Document the borrower’s receipt of VA benefits with a letter or distribution form from the VA.

LSMG Fannie Mae Matrices & Guidelines Page 29 of 37 Revised 06/17/2016