fcf 9th edition chapter 16

DESCRIPTION

sdghdfhTRANSCRIPT

Chapter 16Problems 1-22

Input boxes in tanOutput boxes in yellowGiven data in blueCalculations in redAnswers in green

NOTE: Some functions used in these spreadsheets may require that the "Analysis ToolPak" or "Solver Add-in" be installed in Excel.To install these, click on "Tools|Add-Ins" and select "Analysis ToolPak" and "Solver Add-In."

To install these, click on "Tools|Add-Ins" and select "Analysis ToolPak"

Chapter 16Question 1

Input Area:

Market value $ 250,000 EBIT $ 28,000 Expansion-EBIT 30%Recession-EBIT 50%Debt issue $ 90,000 Interest rate 7%Shares outstanding 5,000

Output Area:

No debtEBIT $ 14,000 $ 28,000 $ 36,400 Interest $ - $ - $ - NI $ 14,000 $ 28,000 $ 36,400 EPS $ 2.80 $ 5.60 $ 7.28 Change EPS% -50.00% 0.00% 30.00%

With debtShare price = $ 50.00 Shares repurchased = 1,800.00

EBIT $ 14,000 $ 28,000 $ 36,400 Interest $ 6,300 ### $ 6,300 ### $ 6,300 NI $ 7,700 $ 21,700 $ 30,100 EPS $ 2.41 $ 6.78 $ 9.41 Change EPS% -64.52% 0.00% 38.71%

Chapter 16Question 2

Input Area:

Market value $ 250,000 EBIT $ 28,000 Expansion-EBIT 30%Recession-EBIT 50%Debt issue $ 90,000 Interest rate 7%Shares outstanding 5,000 Tax rate 35%

Output Area:

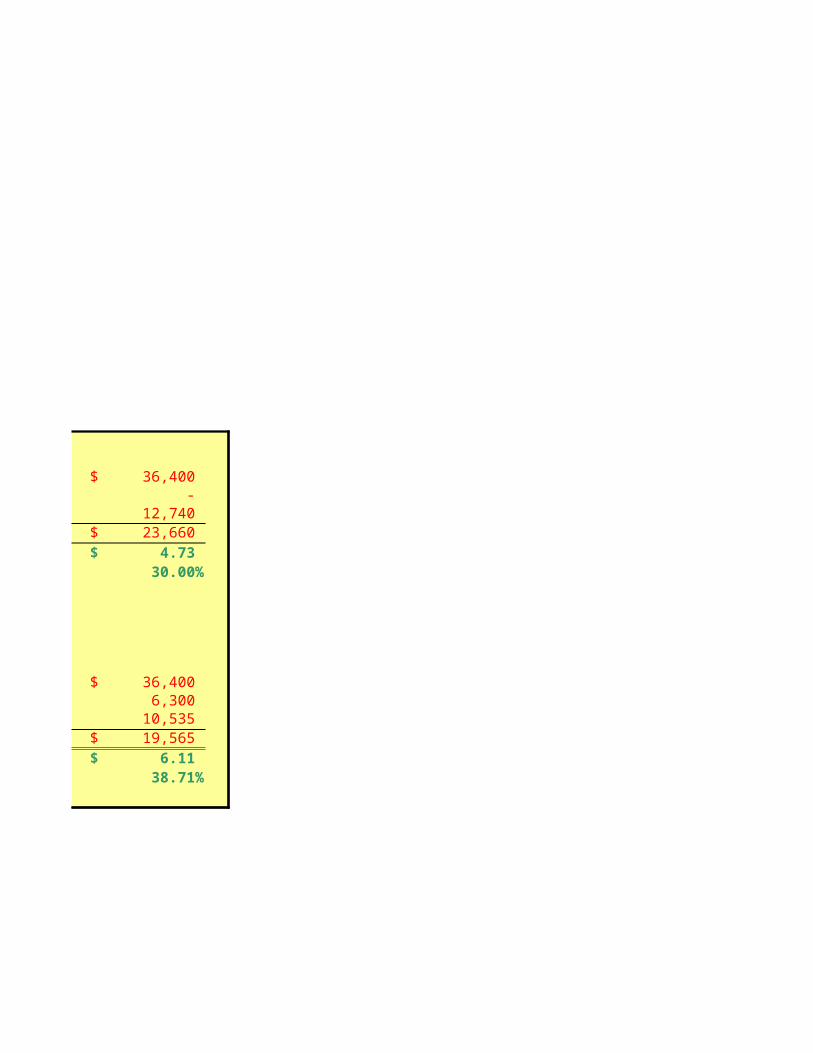

No debt with taxesEBIT $ 14,000 $ 28,000 $ 36,400 Interest - - - Taxes 4,900 9,800 12,740 NI $ 9,100 $ 18,200 $ 23,660 EPS $ 1.82 $ 3.64 $ 4.73 Change EPS% -50.00% 0.00% 30.00%

With debt and taxesShare price = $ 50.00 Shares repurchased = 1,800.00

EBIT $ 14,000 $ 28,000 $ 36,400 Interest 6,300 ### 6,300 ### 6,300 Taxes 2,695 7,595 10,535 NI $ 5,005 $ 14,105 $ 19,565 EPS $ 1.56 $ 4.41 $ 6.11 Change EPS% -64.52% 0.00% 38.71%

Chapter 16Question 3

Input Area:

No debtTE = MV = $ 250,000

With debtTE = $ 160,000

Output Area:

a. ROE 5.60% 11.20% 14.56%Change ROE% -50.00% 0.00% 30.00%

b. ROE 4.81% 13.56% 18.81%Change ROE % -64.52% 0.00% 38.71%

c. No debtNo debt, ROE 3.64% 7.28% 9.46%Change ROE % -50.00% 0.00% 30.00%

With debtWith debt, ROE 3.13% 8.82% 12.23%Change ROE % -64.52% 0.00% 38.71%

Chapter 16Question 4

Input Area:

Plan I:Shares outstanding 160,000

Plan II:Shares outstanding 80,000 Debt outstanding $ 2,800,000 Interest rate 8%

a. EBIT $ 350,000 b. EBIT $ 500,000

Output Area:

a. NI EPS Plan I $ 350,000 $ 2.19 Plan II $ 126,000 $ 1.58

b. Plan I $ 500,000 $ 3.13 Plan II $ 276,000 $ 3.45

c. Breakeven EBIT = $ 448,000.00

Chapter 16Question 5

Input Area:

Plan I:Shares outstanding 160,000

Plan II:Shares outstanding 80,000 Debt outstanding $ 2,800,000 Interest rate 8%

a. EBIT $ 350,000 b. EBIT $ 500,000

Output Area:

Price $ 35.00 V (I) $ 5,600,000.00 V (II) $ 5,600,000.00

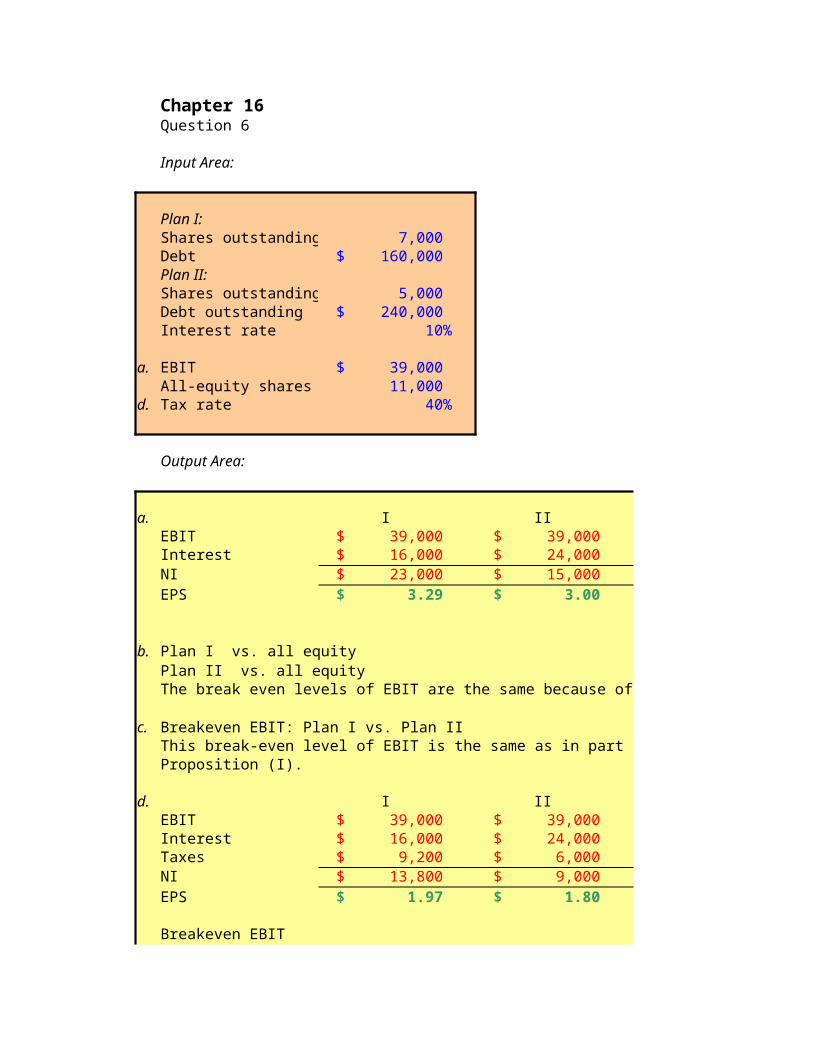

Chapter 16Question 6

Input Area:

Plan I:Shares outstanding 7,000 Debt $ 160,000 Plan II:Shares outstanding 5,000 Debt outstanding $ 240,000 Interest rate 10%

a. EBIT $ 39,000 All-equity shares 11,000

d. Tax rate 40%

Output Area:

a. I II All-Equity EBIT $ 39,000 $ 39,000 $ 39,000 Interest $ 16,000 $ 24,000 $ - NI $ 23,000 $ 15,000 $ 39,000 EPS $ 3.29 $ 3.00 $ 3.55

EBIT b. Plan I vs. all equity $ 44,000

Plan II vs. all equity $ 44,000 The break even levels of EBIT are the same because of M&M Proposition I.

c. Breakeven EBIT: Plan I vs. Plan II $ 44,000 This break-even level of EBIT is the same as in part (b) again, because of M&MProposition (I).

d. I II All-equity EBIT $ 39,000 $ 39,000 $ 39,000 Interest $ 16,000 $ 24,000 $ - Taxes $ 9,200 $ 6,000 $ 15,600 NI $ 13,800 $ 9,000 $ 23,400 EPS $ 1.97 $ 1.80 $ 2.13

Breakeven EBIT

Plan I vs. all-equity $ 44,000 Plan II vs. all-equity $ 44,000 PLanI vs. Plan II $ 44,000

The break-even levels of EBIT do not change because of additions of taxes reducesthe income of all three plans by the same percentage; therefore they do not changerelative to one another.

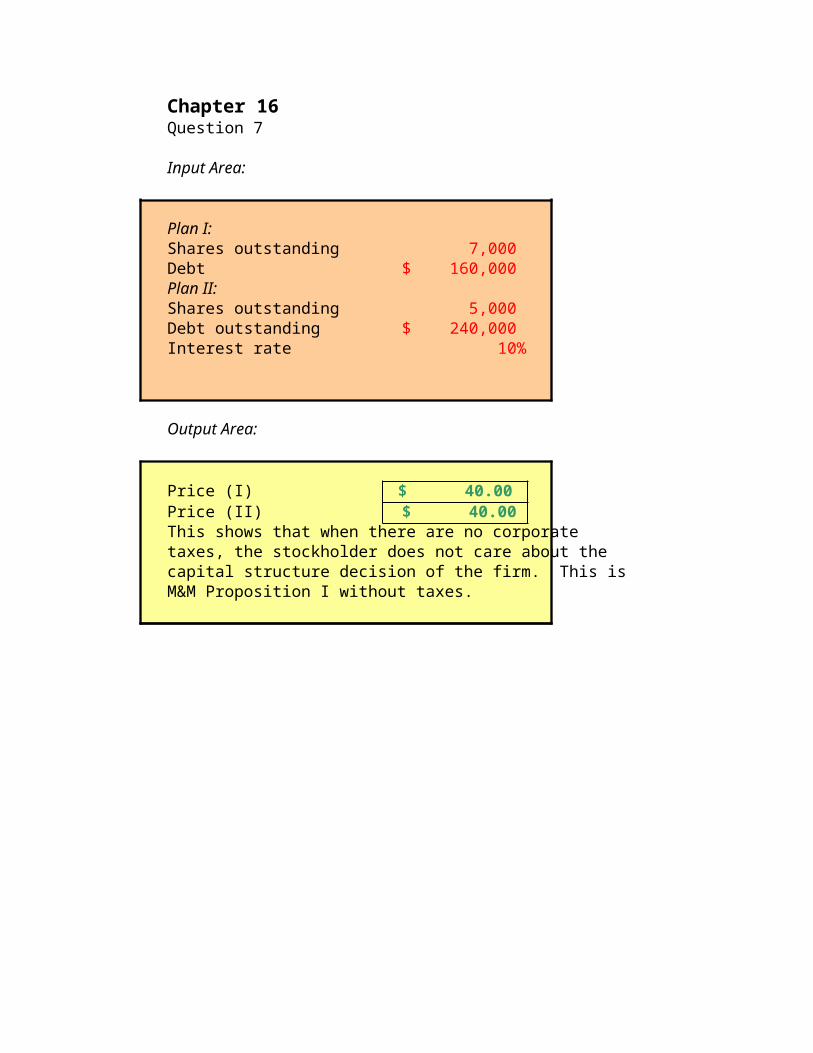

Chapter 16Question 7

Input Area:

Plan I:Shares outstanding 7,000 Debt $ 160,000 Plan II:Shares outstanding 5,000 Debt outstanding $ 240,000 Interest rate 10%

Output Area:

Price (I) $ 40.00 Price (II) $ 40.00 This shows that when there are no corporatetaxes, the stockholder does not care about thecapital structure decision of the firm. This isM&M Proposition I without taxes.

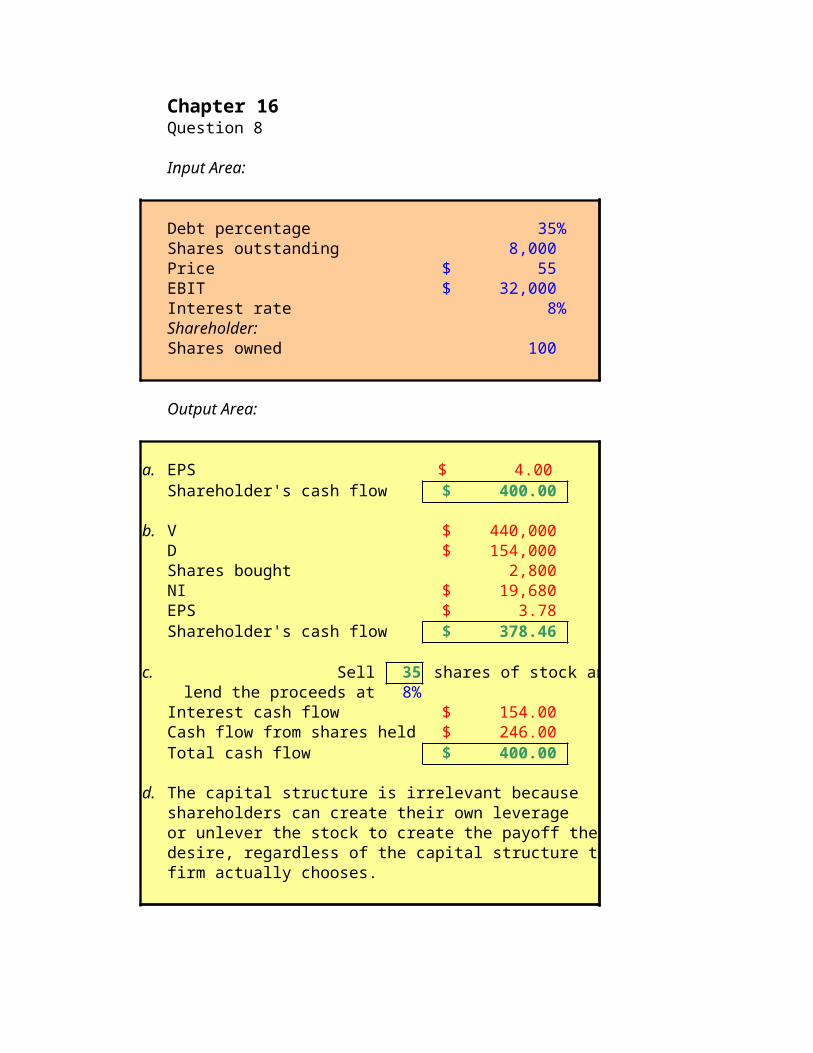

Chapter 16Question 8

Input Area:

Debt percentage 35%Shares outstanding 8,000 Price $ 55 EBIT $ 32,000 Interest rate 8%Shareholder:Shares owned 100

Output Area:

a. EPS $ 4.00 Shareholder's cash flow $ 400.00

b. V $ 440,000 D $ 154,000 Shares bought 2,800 NI $ 19,680 EPS $ 3.78 Shareholder's cash flow $ 378.46

c. Sell 35 shares of stock and lend the proceeds at 8%

Interest cash flow $ 154.00 Cash flow from shares held $ 246.00 Total cash flow $ 400.00

d. The capital structure is irrelevant because shareholders can create their own leverageor unlever the stock to create the payoff they desire, regardless of the capital structure the firm actually chooses.

Chapter 16Question 9

Input Area:

ABC:All-equity $ 600,000 XYZ:Stock value $ 300,000 Interest rate 8%

EBIT $ 80,000

Stockholder:Owns XYZ $ 30,000

Output Area:

a. EBIT $ 56,000 Stockholders CF $ 5,600 Return 18.67%

b. Sell all XYZ shares: nets $ 30,000 Borrow $ 30,000

at 8%Interest cash flow = $ (2,400.00)Use the proceeds from selling sharesand the borrowed funds to buy ABCshares:Stock cash flow (ABC) $ 8,000 Total cash flow $ 5,600 Rate 18.67%

c. 13.33%

18.67%

d. ABC: WACC 13.33%XYZ: WACC 13.33%When there are no corporate taxes, the costof cost of capital for the firm is unaffectedby the capital structure, this is M&M

ABC: RE

XYZ: RE

Proposition II without taxes.

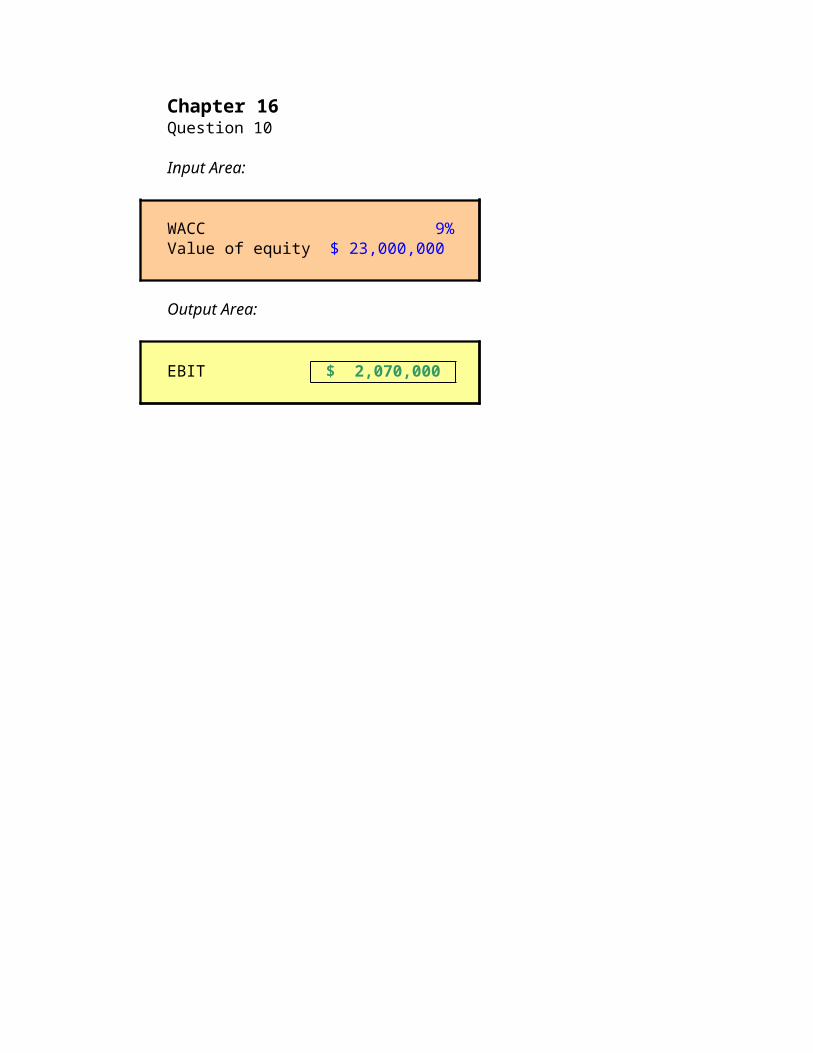

Chapter 16Question 10

Input Area:

WACC 9%Value of equity $ 23,000,000

Output Area:

EBIT $ 2,070,000

Chapter 16Question 11

Input Area:

WACC 9%Value of equity $ 23,000,000 Tax rate 35%

Output Area:

EBIT $ 3,184,615.38 WACC 9.00%Due to taxes, EBIT for an all-equityfirm would have to be higher for the firm to still be worth $ 23,000,000

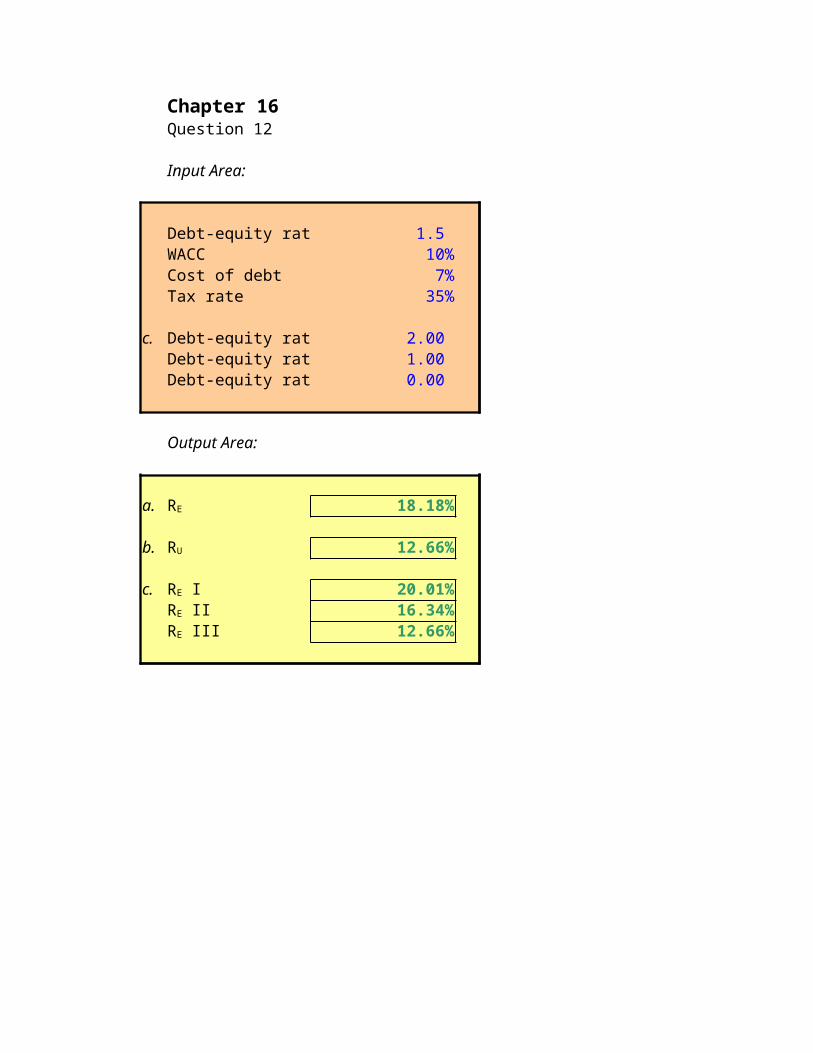

Chapter 16Question 12

Input Area:

Debt-equity ratio 1.5 WACC 10%Cost of debt 7%Tax rate 35%

c. Debt-equity ratio 2.00 Debt-equity ratio 1.00 Debt-equity ratio 0.00

Output Area:

a. 18.18%

b. 12.66%

c. 20.01%16.34%12.66%

RE

RU

RE IRE IIRE III

Chapter 16Question 13

Input Area:

Interest rate 8.20%WACC 11%Tax rate 35%

b. Convert to debt 25%c. Convert to debt 50%

Output Area:

a. All-equity financed 11.00%b. 11.61%c. 12.82%d. WACC(B) 10.04%

WACC(C) 9.08%

RE

RE

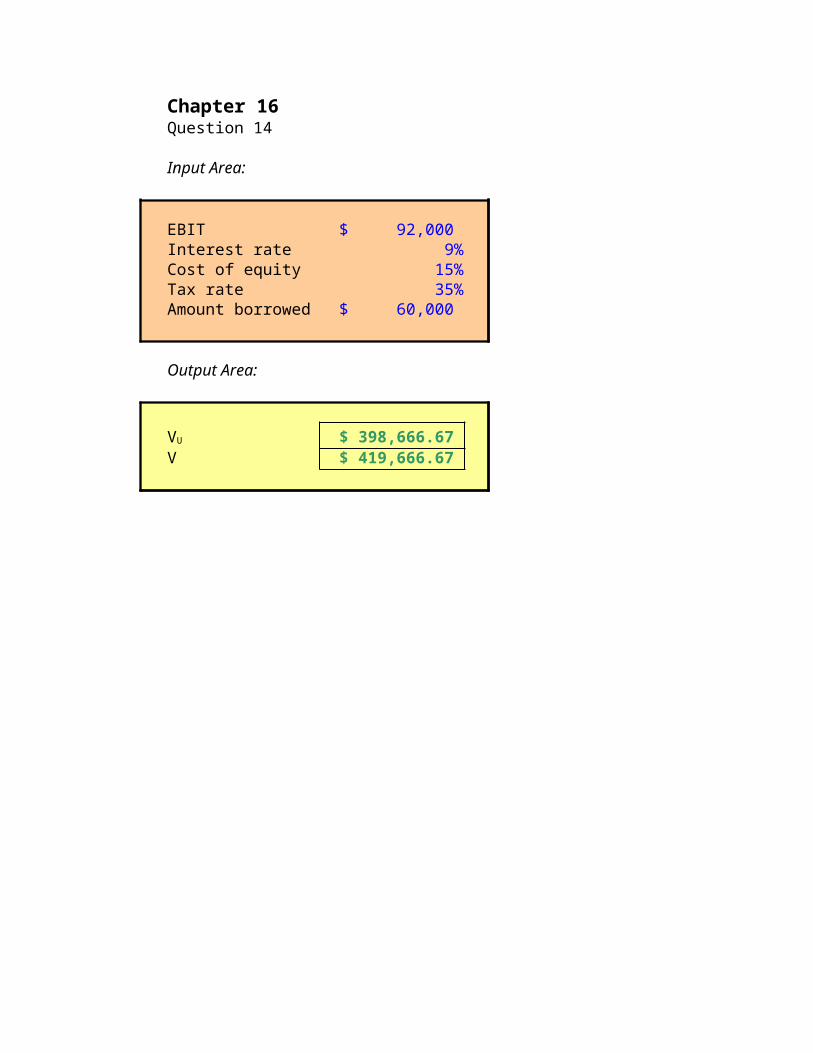

Chapter 16Question 14

Input Area:

EBIT $ 92,000 Interest rate 9%Cost of equity 15%Tax rate 35%Amount borrowed $ 60,000

Output Area:

$ 398,666.67 V $ 419,666.67 VU

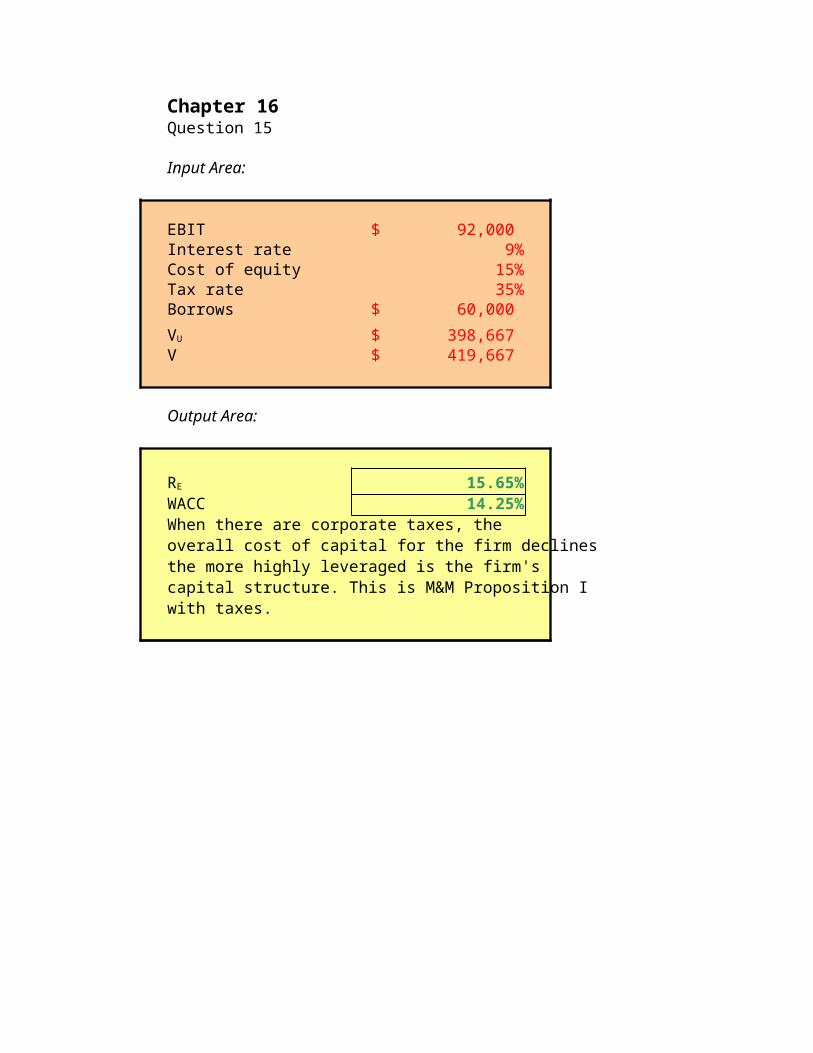

Chapter 16Question 15

Input Area:

EBIT $ 92,000 Interest rate 9%Cost of equity 15%Tax rate 35%Borrows $ 60,000

$ 398,667 V $ 419,667

Output Area:

15.65%WACC 14.25%When there are corporate taxes, the overall cost of capital for the firm declinesthe more highly leveraged is the firm's capital structure. This is M&M Proposition Iwith taxes.

VU

RE

Chapter 16Question 16

Input Area:

EBIT $ 64,000 Tax rate 35%Outstanding debt $ 95,000 Interest rate 8.50%Unlevered cost of capital 15.00%

Output Area:

$ 277,333.33

$ 310,583.33

Applying M&M Proposition I with taxes, the firmhas increased its value by issuing debt. As longas M&M Proposition I holds, that is, there are no bankruptcy costs and so forth, then the companyshould continue to increase its debt/equity ratioto maximze the value of the firm.

VU

VL

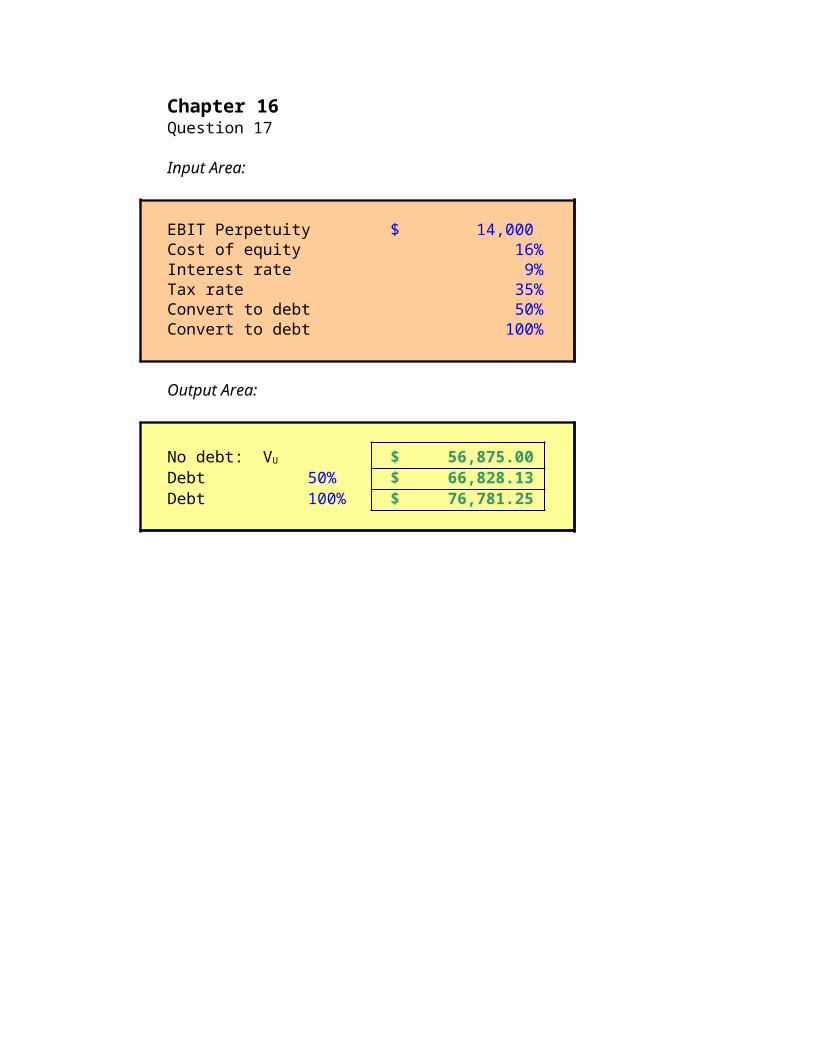

Chapter 16Question 17

Input Area:

EBIT Perpetuity $ 14,000 Cost of equity 16%Interest rate 9%Tax rate 35%Convert to debt 50%Convert to debt 100%

Output Area:

$ 56,875.00 Debt 50% $ 66,828.13 Debt 100% $ 76,781.25

No debt: VU

Chapter 16Question 18

Input Area:

VeblenProjected operating income $ 400,000 Year-end interest on debt $ - Market value of stock $ 2,500,000 Market value of debt $ -

Investor borrowing rate 6%Amount of equity to buy 5%

Output Area:

a. Investment in Knight $ 81,600 Investment in Veblen $ 125,000

Amount to borrow $ 43,400

Year-end cash flow from Knight $ 16,400

Year-end cash flow from Veblen $ 20,000 Interest payment $ 2,604 Net cash flow from Veblen investment $ 17,396

The cash flow from the investment in Veblenwill choose this strategy. This process will cause the value of stock to rise, and the value of KnightAny differences in the dollar returns to the two strategies will be eliminated, and the process will cease when the total market values of the two firms are equal.

Knight $ 400,000 $ 72,000 $ 1,632,000 $ 1,200,000

is higher. All investorsVeblento fall.

Any differences in the dollar returns to the two strategies will be eliminated, and the process will cease when the total market values of the two firms are equal.

Chapter 16Question 19

Output Area:

RE = RU + (RU - RD)(D/E)(1 - t)

WACC = (E/V)RE + (D/V)RD(1 - t) = (E/V)[RU + (RU - RD)(D/E)(1 - t)] + (D/V)RD(1 - t)

WACC = RU[(E/V) + (E/V)(D/E)(1 - t)] + RD(1 - t)[(D/V) - (E/V)(D/E)]

WACC = RU[(E/V) + (D/V)(1 - t)] = RU[{(E+D)/V} - t(D/V)] = RU[1 - t(D/V)]

)(D/E)(1 - t)] + (D/V)RD(1 - t)

[{(E+D)/V} - t(D/V)] = RU[1 - t(D/V)]

Chapter 16Question 20

Output Area:

RE = (EBIT - RDD)(1 - t)/E = [EBIT(1 - t)/E] - [RD(D/E)(1 - t)]

RE = RUVU/E - [RD(D/E)(1 - t)] = RU(VL - tD)/E - [RD(D/E)(1 - t)]

RE = RU(E + D - tD)/E - [RD(D/E)(1 - t)] = RU + (RU - RD)(D/E)(1 - t)

Chapter 16Question 21

Output Area:

M&M Proposition II, with RD = RF

RE = RA + (RA - RF)(D/E)

CAPM: RE = βE(RM - RF) + RF ; RA = βA(RM - RF) + RF

RE = βE(RM - RF) + RF = [1 + (D/E)][βA(RM - RF) + RF] - RF(D/E)

βE = βA[1 + D/E]

Chapter 16Question 22

1.00 Debt-equity ratio 0.00 Debt-equity ratio 1.00 Debt-equity ratio 5.00 Debt-equity ratio 20.00

Output Area:

Debt-equity ratio0.00 1.001.00 2.005.00 6.00

20.00 21.00

The equity risk to the shareholder is composed of both business and financial risk. Even if the assets of the firm are not very risky, the risk to the shareholder can still be large if the financial leverage is high. These higher levels of risk willbe reflected in the shareholder's required rate of return Re,which will increase with higher debt/equity ratios.

Asset β

βE = βA(1 + D/E)

β E