feasibility study: economic feasibility technical feasibility operational feasibility organizational...

TRANSCRIPT

Feasibility Study:• Economic feasibility• Technical feasibility• Operational feasibility• Organizational feasibility• Legal feasibility• Schedule feasibility

Feasibility Analysis:

“Once is not enough”

(Creeping Commitment approach)

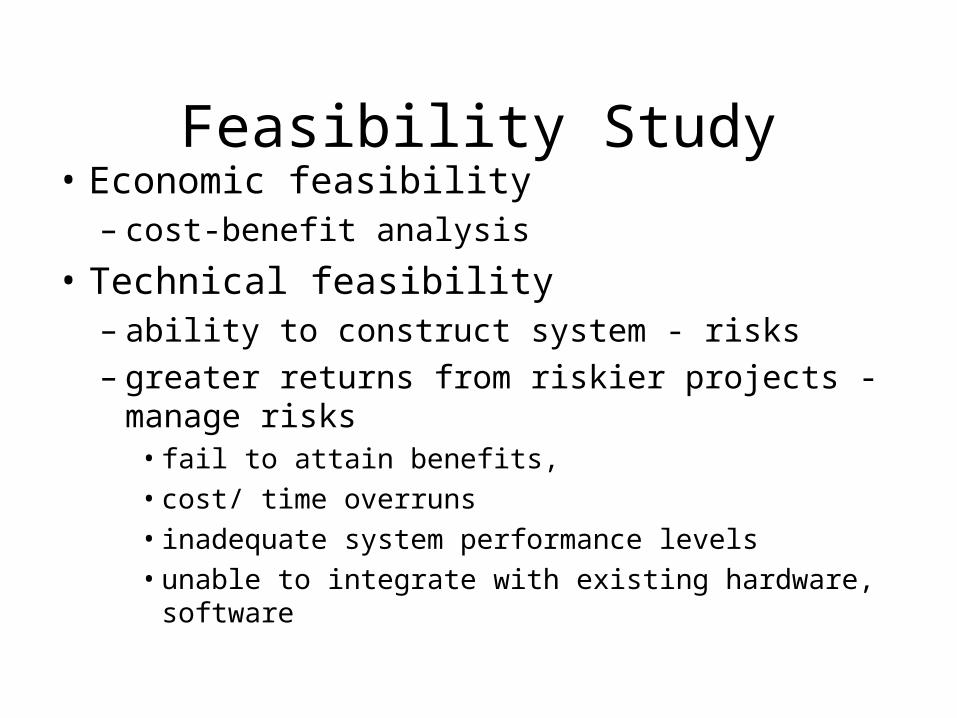

Feasibility Study• Economic feasibility

– cost-benefit analysis

• Technical feasibility– ability to construct system - risks– greater returns from riskier projects - manage risks

• fail to attain benefits,

• cost/ time overruns

• inadequate system performance levels

• unable to integrate with existing hardware, software

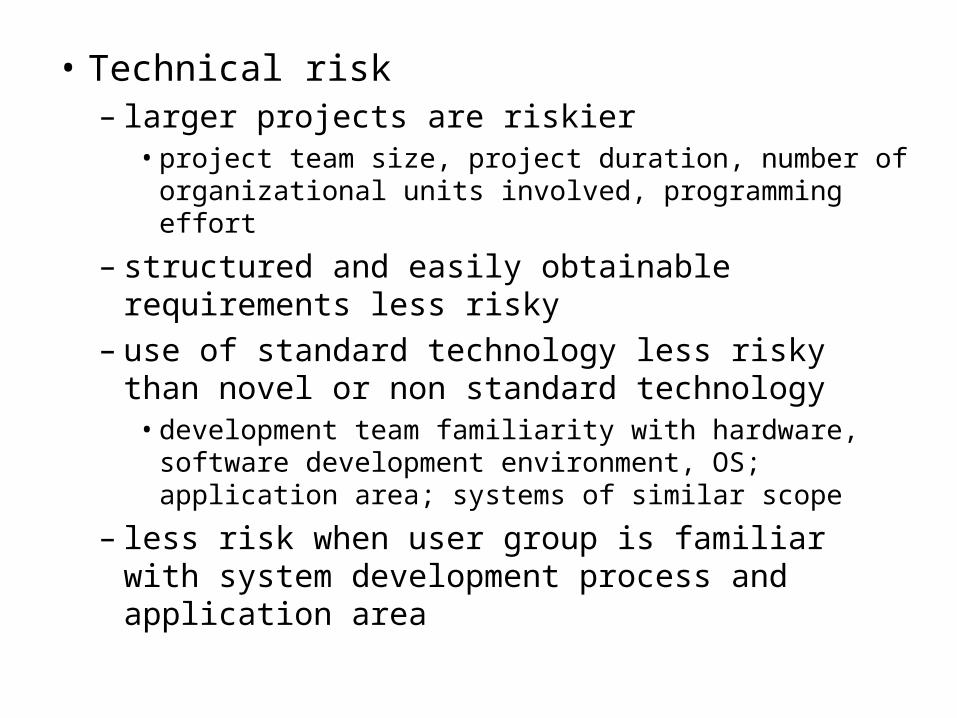

• Technical risk– larger projects are riskier

• project team size, project duration, number of organizational units involved, programming effort

– structured and easily obtainable requirements less risky

– use of standard technology less risky than novel or non standard technology

• development team familiarity with hardware, software development environment, OS; application area; systems of similar scope

– less risk when user group is familiar with system development process and application area

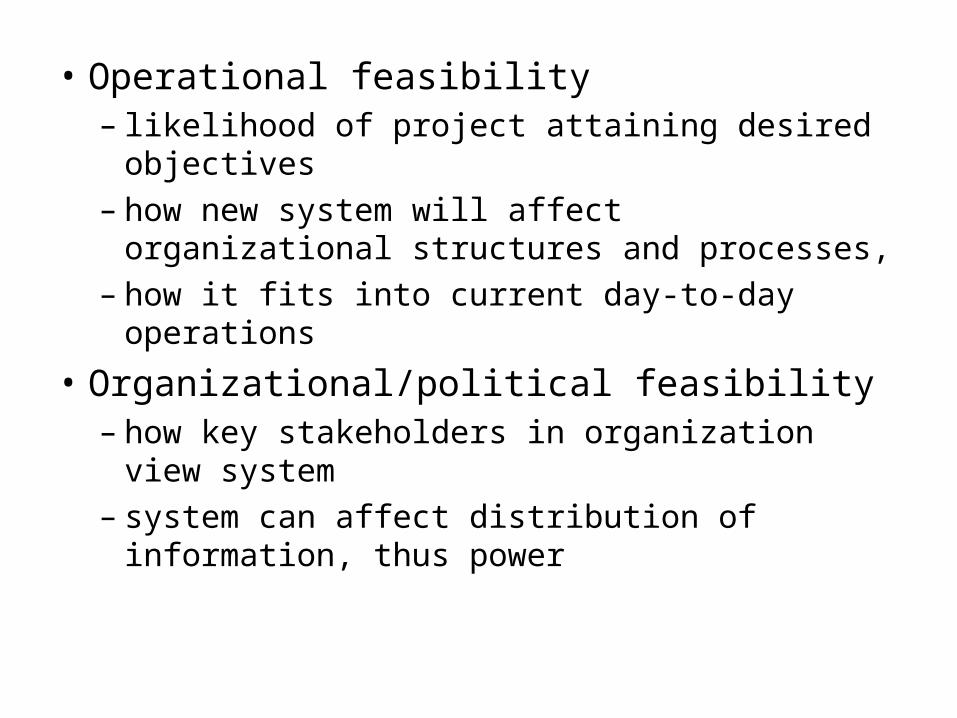

• Operational feasibility– likelihood of project attaining desired objectives– how new system will affect organizational

structures and processes, – how it fits into current day-to-day operations

• Organizational/political feasibility– how key stakeholders in organization view system– system can affect distribution of information, thus

power

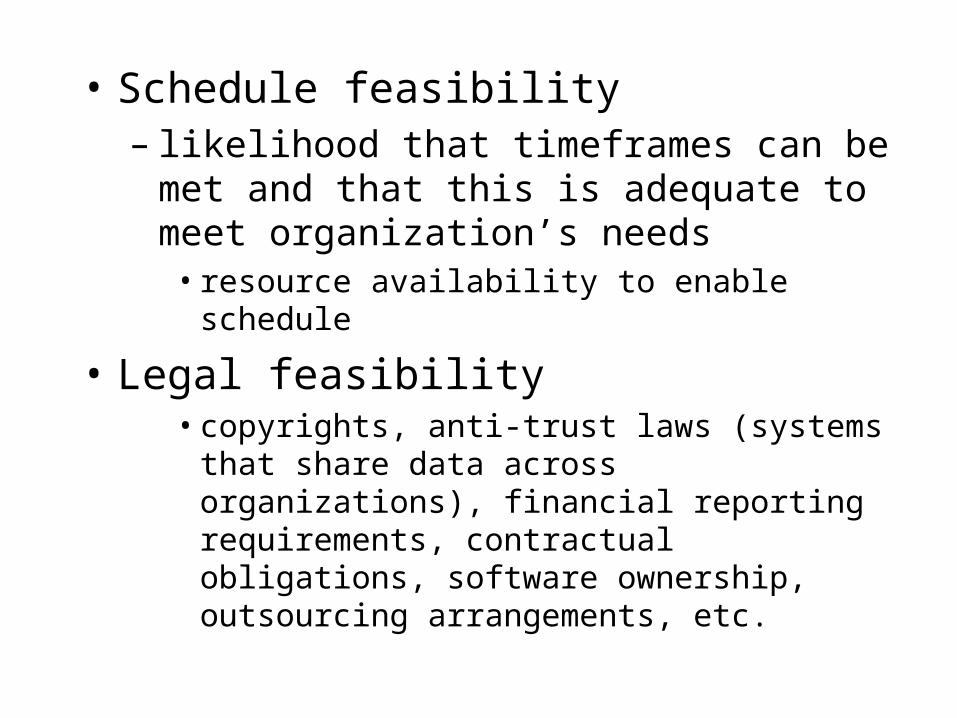

• Schedule feasibility– likelihood that timeframes can be met and that

this is adequate to meet organization’s needs• resource availability to enable schedule

• Legal feasibility• copyrights, anti-trust laws (systems that share data

across organizations), financial reporting requirements, contractual obligations, software ownership, outsourcing arrangements, etc.

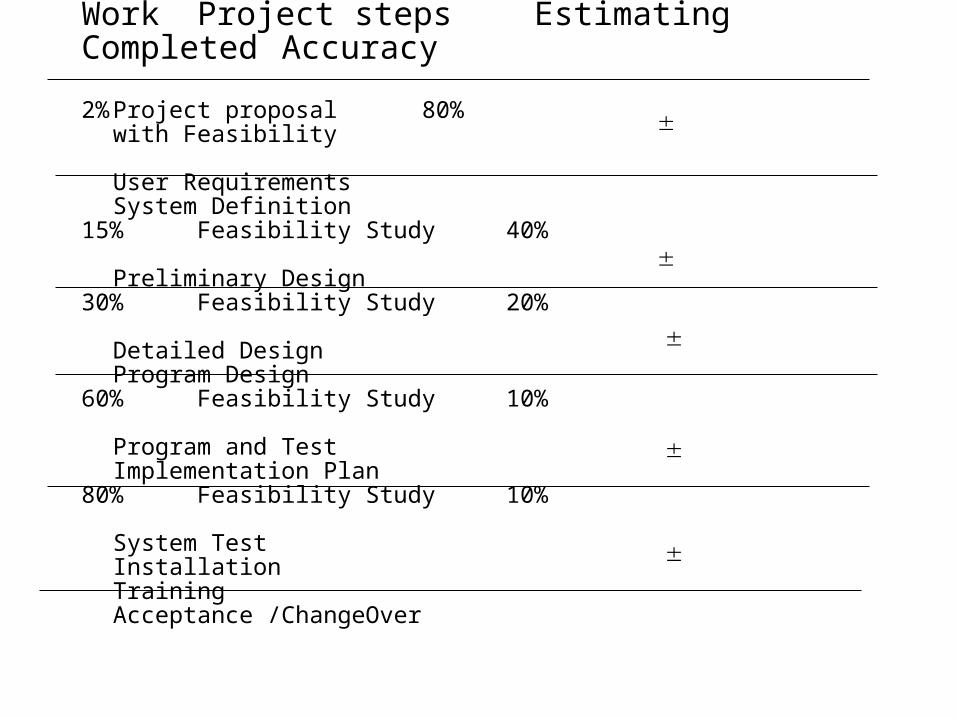

Work Project steps EstimatingCompleted Accuracy

2% Project proposal 80%with Feasibility

User RequirementsSystem Definition

15% Feasibility Study 40%

Preliminary Design30% Feasibility Study 20%

Detailed DesignProgram Design

60% Feasibility Study 10%

Program and TestImplementation Plan

80% Feasibility Study 10%

System TestInstallationTrainingAcceptance /ChangeOver

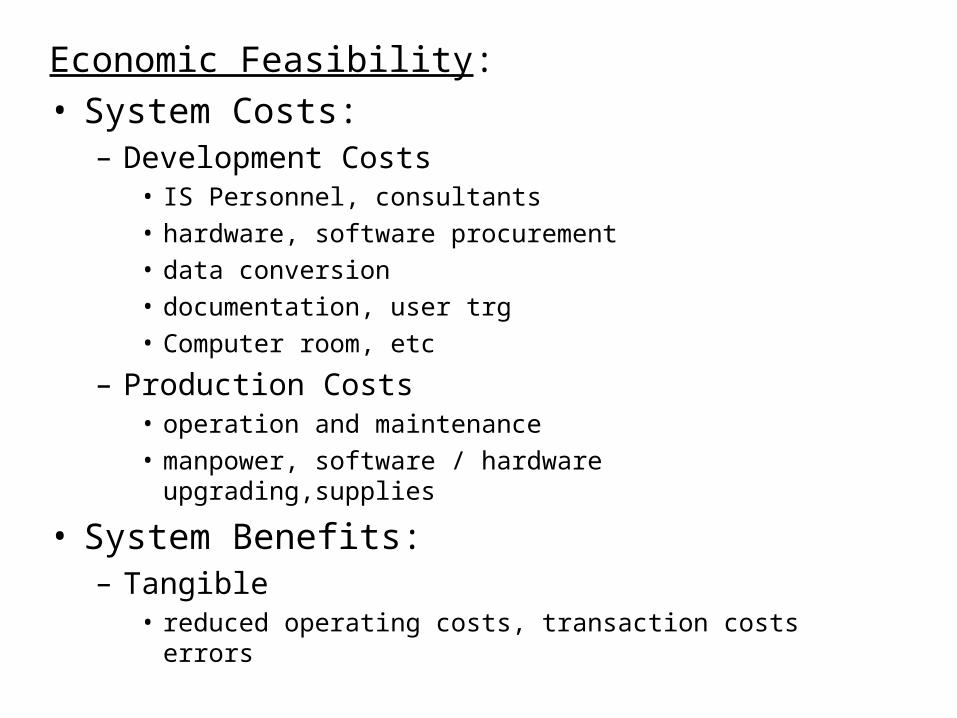

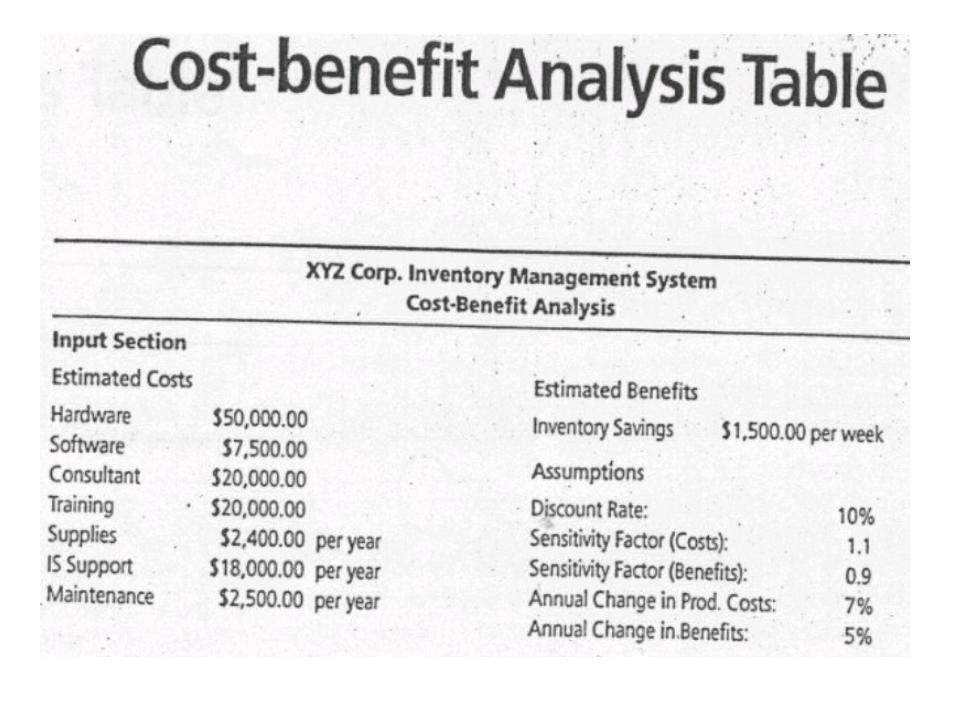

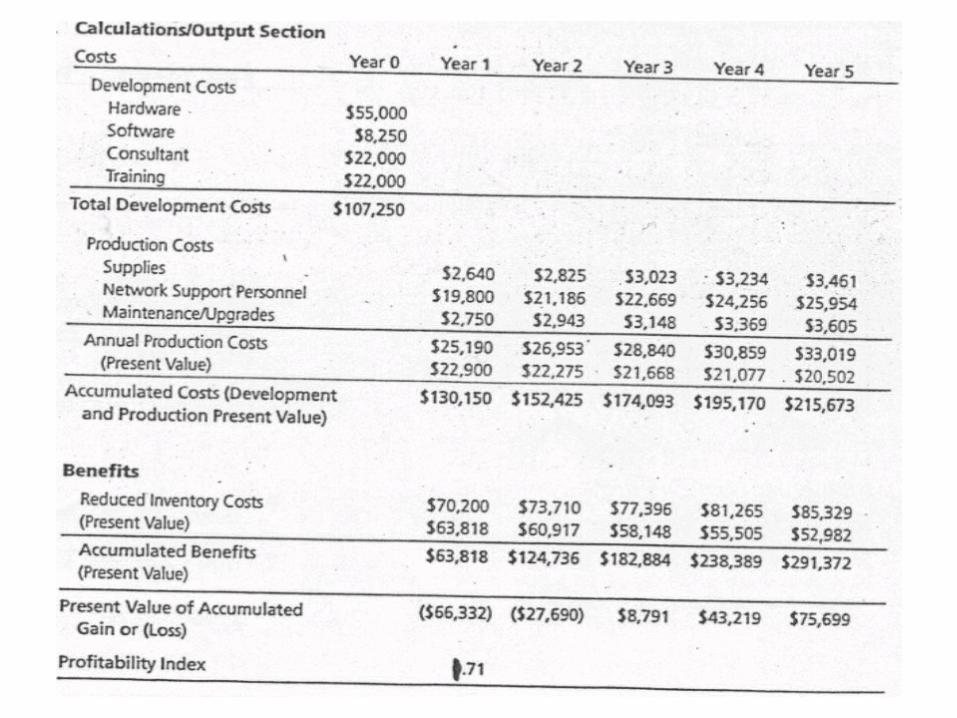

Economic Feasibility:• System Costs:

– Development Costs• IS Personnel, consultants• hardware, software procurement• data conversion• documentation, user trg• Computer room, etc

– Production Costs• operation and maintenance• manpower, software / hardware upgrading,supplies

• System Benefits:– Tangible

• reduced operating costs, transaction costs errors

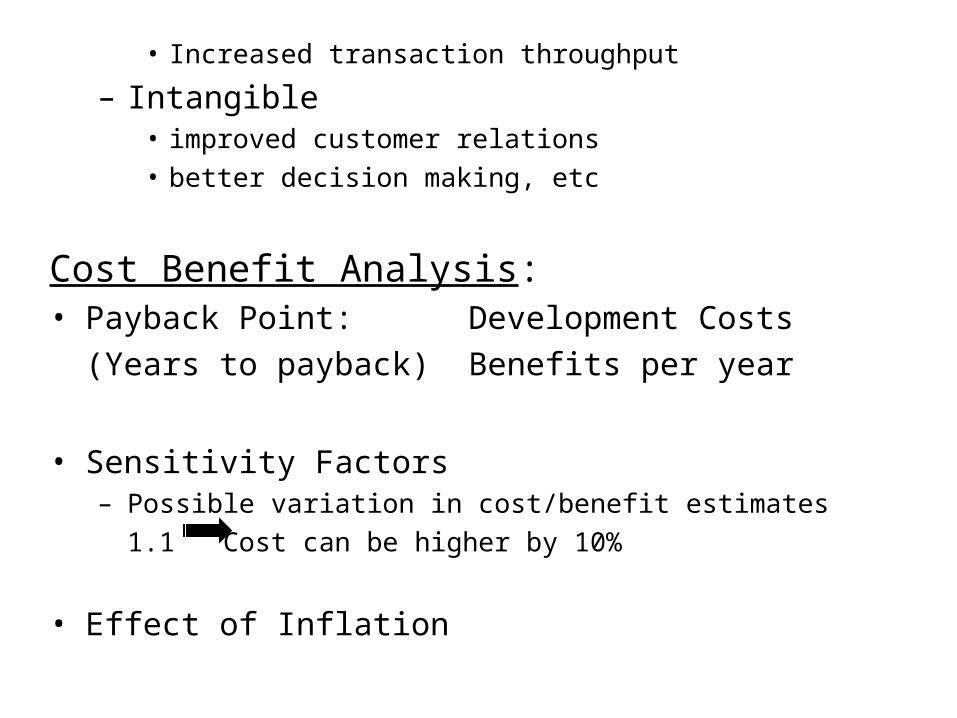

• Increased transaction throughput

– Intangible• improved customer relations• better decision making, etc

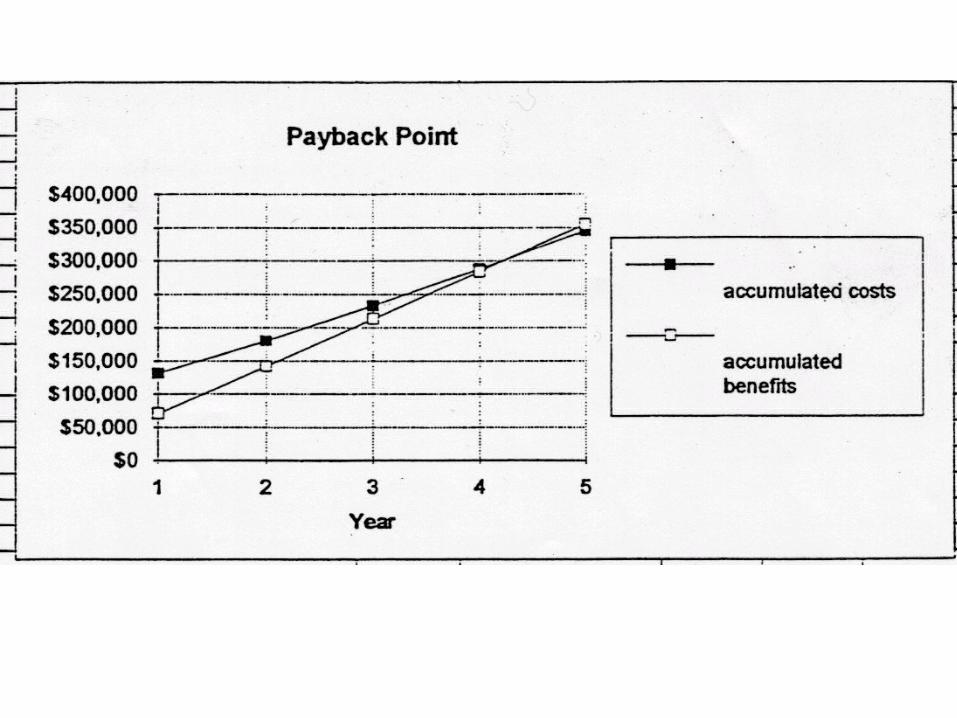

Cost Benefit Analysis:• Payback Point: Development Costs

(Years to payback) Benefits per year

• Sensitivity Factors– Possible variation in cost/benefit estimates

1.1 Cost can be higher by 10%

• Effect of Inflation

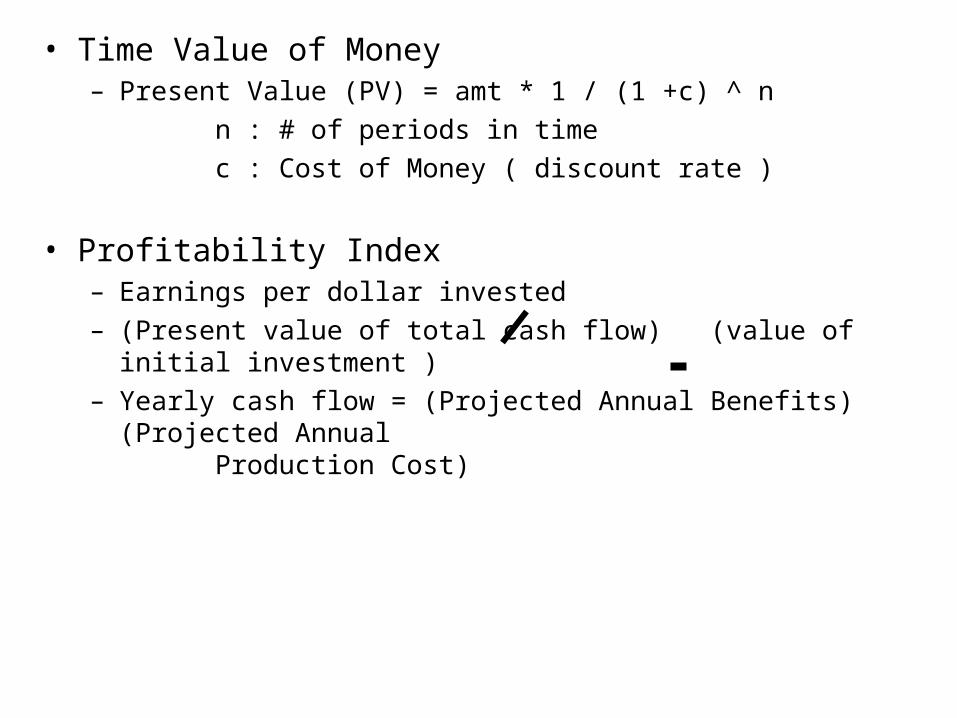

• Time Value of Money– Present Value (PV) = amt * 1 / (1 +c) ^ n

n : # of periods in time

c : Cost of Money ( discount rate )

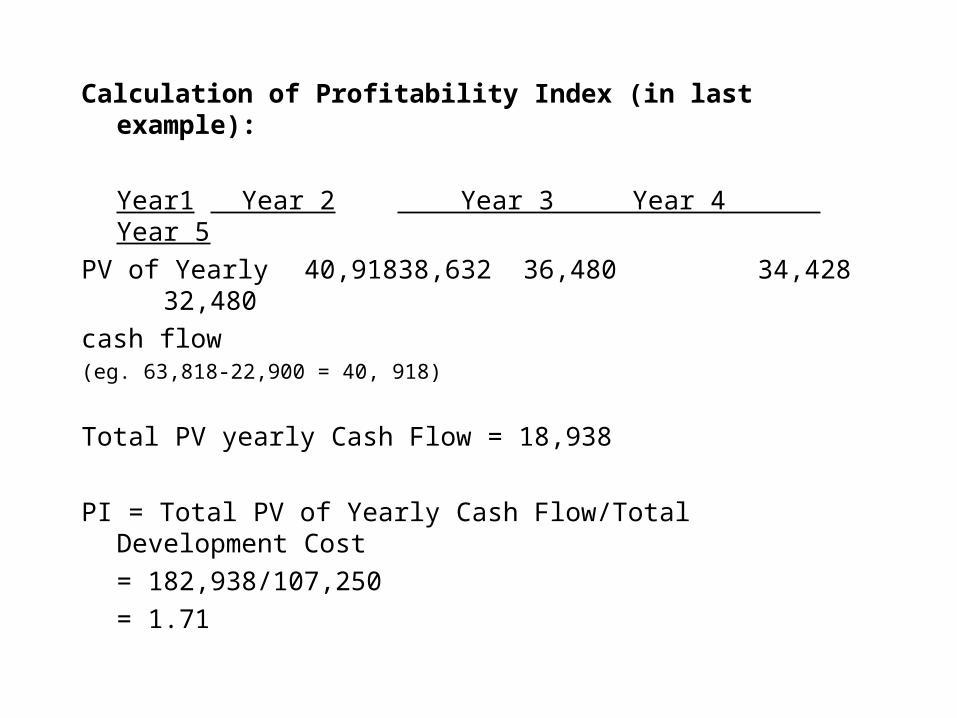

• Profitability Index– Earnings per dollar invested– (Present value of total cash flow) (value of initial investment )– Yearly cash flow = (Projected Annual Benefits) (Projected Annual

Production Cost)

Calculation of Profitability Index (in last example):

Year1 Year 2 Year 3 Year 4 Year 5

PV of Yearly 40,918 38,632 36,480 34,428 32,480

cash flow(eg. 63,818-22,900 = 40, 918)

Total PV yearly Cash Flow = 18,938

PI = Total PV of Yearly Cash Flow/Total Development Cost

= 182,938/107,250

= 1.71

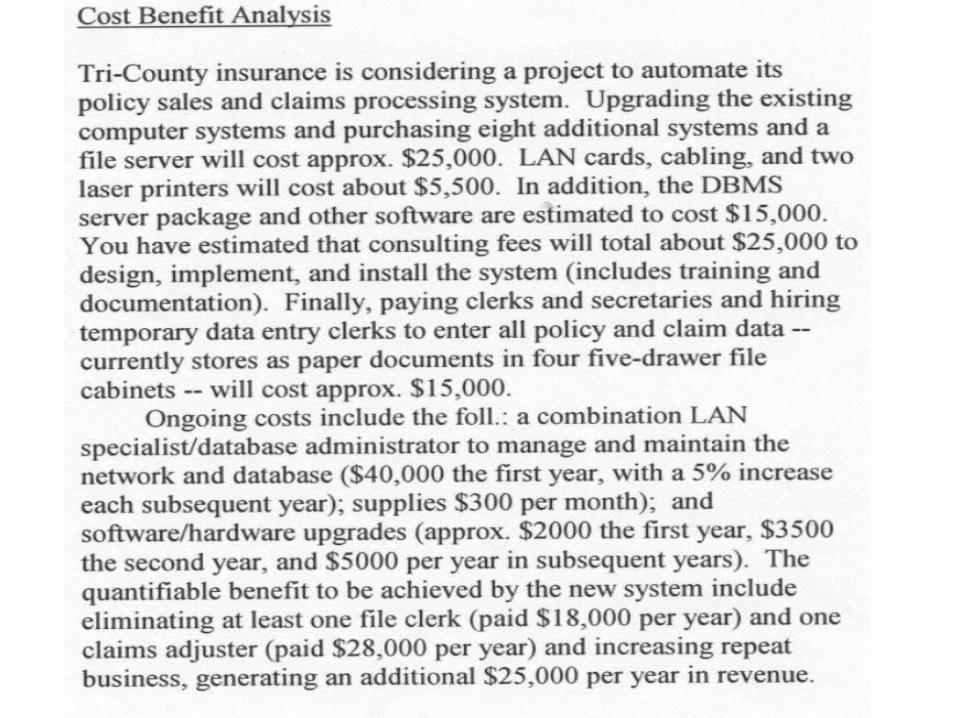

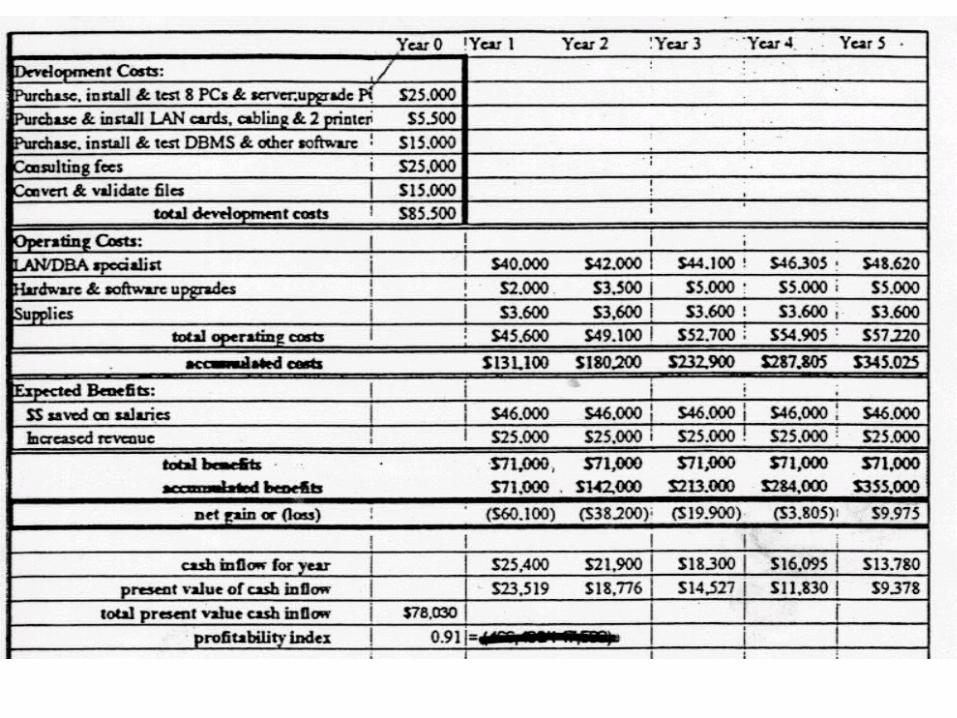

• Example of Cost Benefit analysis for Tri-County Insurance

Note that this example does not consider sensitivity factors or inflation. The discount rate used for calculations is 8%.

Calculations in this example are done a little differently than in the earlier example – Present values are calculated for the cash-flows here, whereas in the last example the PVs were calculated for the costs and benefits separately.