february 18, 2020 - icici directcontent.icicidirect.com/mailimages/idirect_healthcheck_feb20.pdf ·...

TRANSCRIPT

ICIC

I S

ecurit

ies –

Retail E

quit

y R

esearch

Monthly

Sector U

pdate

February 19, 2020

Health Check

Domestic drives Q3; Aurobindo Unit IV receives VAI

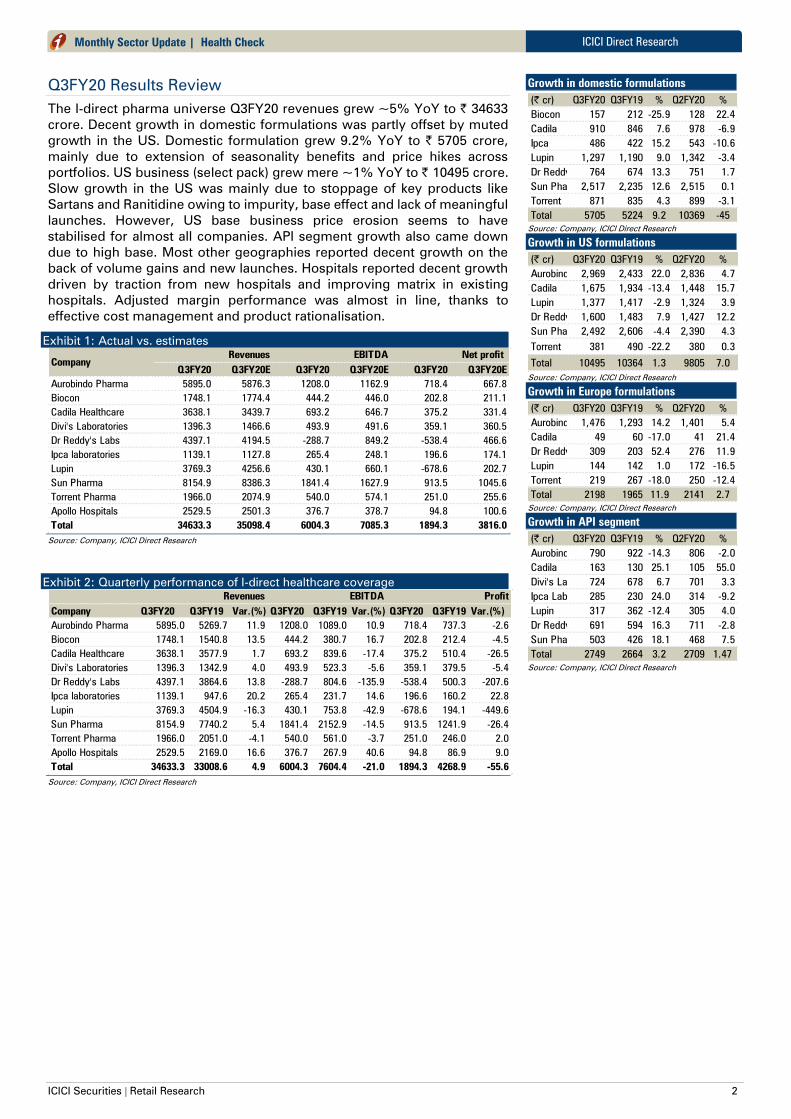

The I-direct pharma universe Q3FY20 revenues grew ~5% YoY to | 34633

crore. Decent growth in domestic formulations was partly offset by muted

growth in the US. Domestic formulations were mainly driven by extension

of seasonality benefit and price hikes across portfolios. US business (select

pack) grew mere ~1% YoY to | 10495 crore. Slow growth in the US was

mainly due to stoppage of key products like Sartans and Ranitidine, base

effect and lack of meaningful launches. However, US base business price

erosion seems to have stabilised for almost all companies. Hospitals

reported decent growth driven by traction from new hospitals and

improving matrix in existing hospitals. Adjusted sequential EBITDA margins

(ex-impairment charges) were same at 21%, though they contracted 189 bps

YoY due to higher base. Adjusted net profit (excluding impairment charges)

declined 6.1% YoY to | 4007 crore.

In a major positive for Aurobindo, the company’s general injectable

formulation facility (Unit IV) at Hyderabad received an establishment

inspection report (EIR) with voluntary action indicated (VAI) status from

USFDA despite 14 observations issued after the inspection in November

2019. This augurs well for the company, as it has 46 pending filings (~30%

of total pending filings) including 50-60% of pending injectables that are filed

from this plant. However, on the flip side, the company’s oral solids facility

(Unit VII) has received official action indicated (OAI) status from USFDA. Unit

VII contributes 20-30% to US revenues. The company had ~33 pending

USFDA approvals by end of Q3FY20 from this unit. The OAI status is in line

with our expectations and it is likely to face further remedial action.

Apollo Hospitals’ promoters have brought down their pledge position to

29.64% (down from 67.33% earlier) of the total 30.8% promoter holding

using proceeds from the Apollo Munich deal.

Dr Reddy’s has entered into an agreement to acquire part of Wockhardt’s

domestic branded business (62 products) including manufacturing facility at

Baddi, Himachal Pradesh for | 1850 crore. Revenues of the proposed acquire

business were | 377 crore in 9MFY20. The implied valuation comes to ~3.8x

annualised revenue.

The Indian pharmaceutical market (IPM) grew 7.6% to | 12078 crore in

January 2020. The growth was attributable to a price hike: 5.2%, new

product launches: 2.7% and volume decline of 0.3%. On a MAT basis, IPM

growth was 9.6% YoY to | 141224 crore.

Financials normalising but stock specific approach remains…

Domestic growth is likely to stabilise on an annual basis and is likely to grow

on the back of new launches and volume gain. The US generics narrative in

the last few quarters is reflecting some sort of normalcy on the back of

stability in the base business and new launches. However, regulatory

uncertainty is likely to remain an overhang on US-heavy companies.

Profitability is likely to improve as the management commentary continues

to suggest cost rationalisation and MR productivity. Improving operating

leverage is also likely to contribute to margin expansion. The companies are

also moderating their capex plans to focus on better RoCE. As per the

assertion from most of the managements, Coronavirus is not a concern

currently as inventory levels are covered till March for most APIs and key

starting materials (KSM). That said, if the supplies do not resume in March,

the industry is likely to start facing raw materials crunch from Q1FY21.

Overall, we continue to maintain a stock specific approach. India focused

players including MNCs, global CRAMs players and hospitals are our

preferred sub-segments for bargain hunting.

Stock Performance

Mcap

Company 1M 3M YTD 1Y 18-Feb

Sun Pharma.Inds. -12 -6 -8 -4 95851

Divi's Lab. 13 24 17 37 57295

Dr Reddy's Labs 7 19 13 27 53930

Torrent Pharma. 6 19 15 20 35828

Biocon 2 13 1 -2 35448

Cipla -10 -6 -10 -20 34797

Abbott 18 16 14 105 31536

Lupin -9 -7 -9 -10 31508

Aurobindo Pharma 0 15 7 -32 28529

Cadila Health. -3 9 3 -16 26843

Apollo Hospitals 6 22 19 53 23834

Pfizer 1 1 -3 41 18718

Ipca Labs. 9 16 18 66 16987

Sanofi 4 3 0 18 16170

Syngene Int. -2 -5 -5 3 12200

Alembic Pharma 7 17 12 18 12088

Natco Pharma 3 15 8 12 11689

Ajanta Pharma 14 33 33 34 11306

Fortis Health 6 5 13 11 11302

Glenmark Pharma. -15 -16 -12 -47 8639

Aster DM 6 12 6 11 8624

Jubilant Life -13 0 -8 -31 7884

Narayana Hrudayalaya-7 13 9 72 6867

FDC Ltd 6 26 16 61 4186

Indoco Remedies 22 69 30 44 2299

Hikal -7 5 4 -17 1467

Hester Bio -5 -4 5 9 1295

Shalby Ltd -5 -3 4 -27 1044

Healthcare Global 7 2 10 -41 1019

NGL Fine-Chem -10 1 1 5 266

Return (%)

Source: Bloomberg

Global indices performance

Company 1M 3M YTD 1Y 3Y 5Y

S&P 500 Pharm Index (US)-3 9 0 11 10 7

NASDAQ Biotechnology (US)0 10 2 10 8 3

S&P Pharmaceuticals (US)-1 21 2 13 4 -3

DJ Pharma and Biotech (US)-1 10 1 12 10 6

DJ STOXX Healthcare (EU)2 10 6 30 12 8

MSCI World Pharm & Biotech-1 9 2 17 11 6

NSE Pharma -3 4 1 -5 -8 -7

Return (%)

Source: Bloomberg

Research Analyst

Siddhant Khandekar

MItesh Shah, CFA

Sudarshan Agarwal

Siddhant Khandekar

ICICI Securities | Retail Research 2

ICICI Direct Research

Monthly Sector Update | Health Check

Q3FY20 Results Review

The I-direct pharma universe Q3FY20 revenues grew ~5% YoY to | 34633

crore. Decent growth in domestic formulations was partly offset by muted

growth in the US. Domestic formulation grew 9.2% YoY to | 5705 crore,

mainly due to extension of seasonality benefits and price hikes across

portfolios. US business (select pack) grew mere ~1% YoY to | 10495 crore.

Slow growth in the US was mainly due to stoppage of key products like

Sartans and Ranitidine owing to impurity, base effect and lack of meaningful

launches. However, US base business price erosion seems to have

stabilised for almost all companies. API segment growth also came down

due to high base. Most other geographies reported decent growth on the

back of volume gains and new launches. Hospitals reported decent growth

driven by traction from new hospitals and improving matrix in existing

hospitals. Adjusted margin performance was almost in line, thanks to

effective cost management and product rationalisation.

Exhibit 1: Actual vs. estimates

Q3FY20 Q3FY20E Q3FY20 Q3FY20E Q3FY20 Q3FY20E

Aurobindo Pharma 5895.0 5876.3 1208.0 1162.9 718.4 667.8

Biocon 1748.1 1774.4 444.2 446.0 202.8 211.1

Cadila Healthcare 3638.1 3439.7 693.2 646.7 375.2 331.4

Divi's Laboratories 1396.3 1466.6 493.9 491.6 359.1 360.5

Dr Reddy's Labs 4397.1 4194.5 -288.7 849.2 -538.4 466.6

Ipca laboratories 1139.1 1127.8 265.4 248.1 196.6 174.1

Lupin 3769.3 4256.6 430.1 660.1 -678.6 202.7

Sun Pharma 8154.9 8386.3 1841.4 1627.9 913.5 1045.6

Torrent Pharma 1966.0 2074.9 540.0 574.1 251.0 255.6

Apollo Hospitals 2529.5 2501.3 376.7 378.7 94.8 100.6

Total 34633.3 35098.4 6004.3 7085.3 1894.3 3816.0

Company

Revenues EBITDA Net profit

Source: Company, ICICI Direct Research

Exhibit 2: Quarterly performance of I-direct healthcare coverage

Company Q3FY20 Q3FY19 Var.(%) Q3FY20 Q3FY19 Var.(%) Q3FY20 Q3FY19 Var.(%)

Aurobindo Pharma 5895.0 5269.7 11.9 1208.0 1089.0 10.9 718.4 737.3 -2.6

Biocon 1748.1 1540.8 13.5 444.2 380.7 16.7 202.8 212.4 -4.5

Cadila Healthcare 3638.1 3577.9 1.7 693.2 839.6 -17.4 375.2 510.4 -26.5

Divi's Laboratories 1396.3 1342.9 4.0 493.9 523.3 -5.6 359.1 379.5 -5.4

Dr Reddy's Labs 4397.1 3864.6 13.8 -288.7 804.6 -135.9 -538.4 500.3 -207.6

Ipca laboratories 1139.1 947.6 20.2 265.4 231.7 14.6 196.6 160.2 22.8

Lupin 3769.3 4504.9 -16.3 430.1 753.8 -42.9 -678.6 194.1 -449.6

Sun Pharma 8154.9 7740.2 5.4 1841.4 2152.9 -14.5 913.5 1241.9 -26.4

Torrent Pharma 1966.0 2051.0 -4.1 540.0 561.0 -3.7 251.0 246.0 2.0

Apollo Hospitals 2529.5 2169.0 16.6 376.7 267.9 40.6 94.8 86.9 9.0

Total 34633.3 33008.6 4.9 6004.3 7604.4 -21.0 1894.3 4268.9 -55.6

Revenues EBITDA Profit

Source: Company, ICICI Direct Research

Growth in domestic formulations

(| cr) Q3FY20 Q3FY19 % Q2FY20 %

Biocon 157 212 -25.9 128 22.4

Cadila 910 846 7.6 978 -6.9

Ipca 486 422 15.2 543 -10.6

Lupin 1,297 1,190 9.0 1,342 -3.4

Dr Reddy's 764 674 13.3 751 1.7

Sun Pharma2,517 2,235 12.6 2,515 0.1

Torrent 871 835 4.3 899 -3.1

Total 5705 5224 9.2 10369 -45

Source: Company, ICICI Direct Research

Growth in US formulations

(| cr) Q3FY20 Q3FY19 % Q2FY20 %

Aurobindo 2,969 2,433 22.0 2,836 4.7

Cadila 1,675 1,934 -13.4 1,448 15.7

Lupin 1,377 1,417 -2.9 1,324 3.9

Dr Reddy's 1,600 1,483 7.9 1,427 12.2

Sun Pharma2,492 2,606 -4.4 2,390 4.3

Torrent 381 490 -22.2 380 0.3

Total 10495 10364 1.3 9805 7.0

Source: Company, ICICI Direct Research

Growth in Europe formulations

(| cr) Q3FY20 Q3FY19 % Q2FY20 %

Aurobindo 1,476 1,293 14.2 1,401 5.4

Cadila 49 60 -17.0 41 21.4

Dr Reddy's 309 203 52.4 276 11.9

Lupin 144 142 1.0 172 -16.5

Torrent 219 267 -18.0 250 -12.4

Total 2198 1965 11.9 2141 2.7

Source: Company, ICICI Direct Research

Growth in API segment

(| cr) Q3FY20 Q3FY19 % Q2FY20 %

Aurobindo 790 922 -14.3 806 -2.0

Cadila 163 130 25.1 105 55.0

Divi's Lab 724 678 6.7 701 3.3

Ipca Labs 285 230 24.0 314 -9.2

Lupin 317 362 -12.4 305 4.0

Dr Reddy's 691 594 16.3 711 -2.8

Sun Pharma 503 426 18.1 468 7.5

Total 2749 2664 3.2 2709 1.47

Source: Company, ICICI Direct Research

ICICI Securities | Retail Research 3

ICICI Direct Research

Monthly Sector Update | Health Check

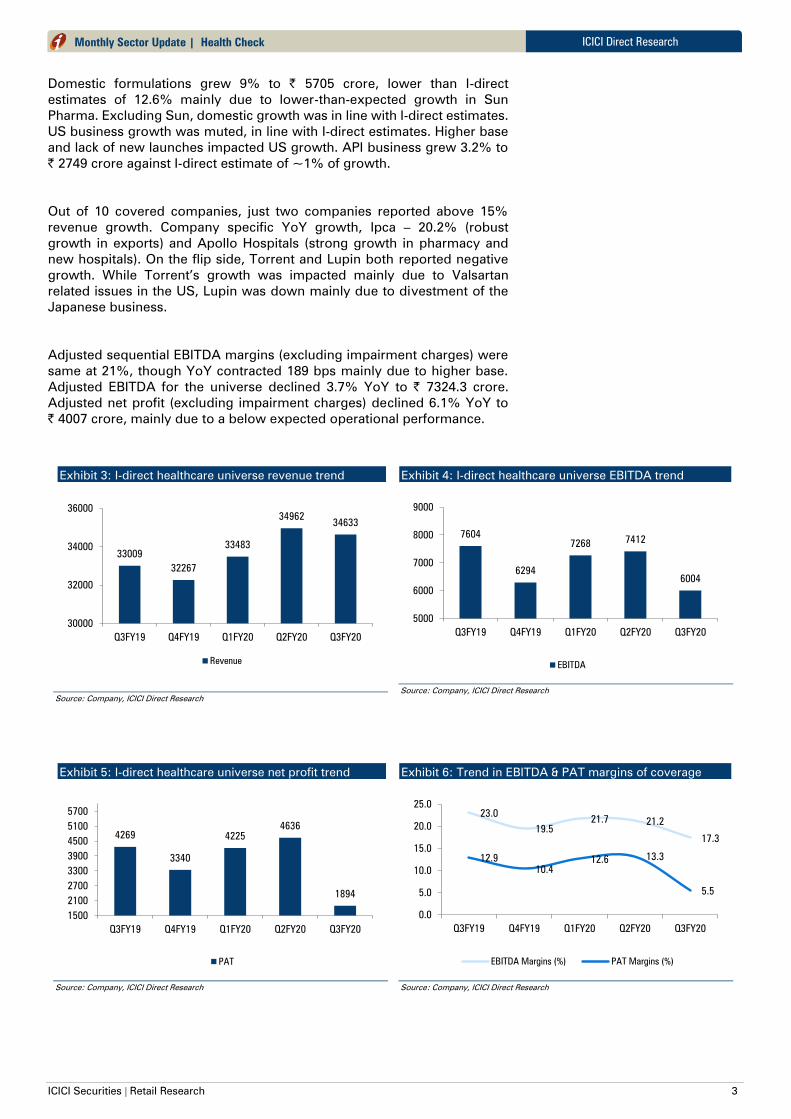

Domestic formulations grew 9% to | 5705 crore, lower than I-direct

estimates of 12.6% mainly due to lower-than-expected growth in Sun

Pharma. Excluding Sun, domestic growth was in line with I-direct estimates.

US business growth was muted, in line with I-direct estimates. Higher base

and lack of new launches impacted US growth. API business grew 3.2% to

| 2749 crore against I-direct estimate of ~1% of growth.

Out of 10 covered companies, just two companies reported above 15%

revenue growth. Company specific YoY growth, Ipca – 20.2% (robust

growth in exports) and Apollo Hospitals (strong growth in pharmacy and

new hospitals). On the flip side, Torrent and Lupin both reported negative

growth. While Torrent’s growth was impacted mainly due to Valsartan

related issues in the US, Lupin was down mainly due to divestment of the

Japanese business.

Adjusted sequential EBITDA margins (excluding impairment charges) were

same at 21%, though YoY contracted 189 bps mainly due to higher base.

Adjusted EBITDA for the universe declined 3.7% YoY to | 7324.3 crore.

Adjusted net profit (excluding impairment charges) declined 6.1% YoY to

| 4007 crore, mainly due to a below expected operational performance.

Exhibit 3: I-direct healthcare universe revenue trend

Source: Company, ICICI Direct Research

Exhibit 4: I-direct healthcare universe EBITDA trend

Source: Company, ICICI Direct Research

Exhibit 5: I-direct healthcare universe net profit trend

Source: Company, ICICI Direct Research

Exhibit 6: Trend in EBITDA & PAT margins of coverage

Source: Company, ICICI Direct Research

33009

32267

33483

3496234633

30000

32000

34000

36000

Q3FY19 Q4FY19 Q1FY20 Q2FY20 Q3FY20

Revenue

7604

6294

72687412

6004

5000

6000

7000

8000

9000

Q3FY19 Q4FY19 Q1FY20 Q2FY20 Q3FY20

EBITDA

4269

3340

4225

4636

1894

1500

2100

2700

3300

3900

4500

5100

5700

Q3FY19 Q4FY19 Q1FY20 Q2FY20 Q3FY20

PAT

23.0

19.5

21.7 21.2

17.3

12.9

10.4

12.613.3

5.5

0.0

5.0

10.0

15.0

20.0

25.0

Q3FY19 Q4FY19 Q1FY20 Q2FY20 Q3FY20

EBITDA Margins (%) PAT Margins (%)

ICICI Securities | Retail Research 4

ICICI Direct Research

Monthly Sector Update | Health Check

Exhibit 7: Deviation from estimates/change in Q3FY20 numbers

CompanyPrevious

Rating

Current

Rating

Deviation from

estimates

Remarks

Apollo Hospital Buy Buy In-LineStandalone operational results in line with I-direct estimates. However, net profit was

lower mainly due to higher-than-expected depreciation and interest cost

Aurobindo Pharma Hold Hold AboveRevenues in line with I-direct estimates while net profit was higher mainly due to a better

operational performance

Biocon Buy Hold In-LineResults almost in line with I-direct estimates on all fronts. Growth was mainly attributable

to increase in small molecules and biologics segment

Cadila Healthcare Hold Hold Above Results higher than I-direct estimates on all fronts

Divi's labs Hold Hold BelowRevenues below I-direct estimates due to lower-than-expected sales in custom synthesis

business while profitability was in line with I-direct estimates

Dr Reddy's Labs Hold Hold AboveResults (excluding one-off impairment charges) higher than I-direct estimates on all fronts

due to better-than-expected overall sales and operational performance

Ipca labs Buy Buy AboveRevenues in line with I-direct estimates while profitability was better due to a better

operational performance

Lupin Hold Hold BelowResults lower than I-direct estimates due to one-off impairment charges and divestment of

Kyowa (Japanese subsidiary)

Sun Pharma Hold Hold MixedRevenues in line with I-direct estimates while operational performance was better-than-

expected, profitability was lower due to higher tax and depreciation

Torrent Pharma Buy Hold BelowResults below I-direct estimates on operational front due to lower-than-expected growth in

domestic business. Net profit in line with our estimates due to higher other income

Source: ICICI Direct Research

ICICI Securities | Retail Research 5

ICICI Direct Research

Monthly Sector Update | Health Check

IPM grows 8% YoY in January, volume remains flat

The Indian pharmaceutical market (IPM) grew 7.6% YoY (8.8% in December

2019) to | 12078 crore in January 2020. The growth was attributable to price

hike: 5.2%, new product launches: 2.7%. While volumes declined 0.3%

(drop from December growth of 0.7%) and a drop from rolling average 12-

month growth of 1.8%).

Drugs under NLEM list grew 7.5% YoY while non-NLEM drugs grew 7.6%.

Among companies under I-direct coverage, nine (Dr Reddy’s, FDC, Torrent,

Pfizer, Glenmark, Sun Pharma, Natco, Cadila, Ipca) have outperformed

industry growth rate.

Therapy wise, 11 major therapies have registered faster than industry

growth. Notable among them with growth rates- stomatologicals: 13.5%,

blood related – 12.8%, cardiac – 10.5%, urology – 10.2%, respiratory: 9.7%,

anti-malarial: 9.7% and vaccines: 9.4%.

Domestic companies have grown at 8.6% YoY while MNC companies have

grown at 3.6%.

On a MAT basis, IPM growth was 9.6% YoY to | 141224 crore.

Exhibit 8: Domestic formulations - Growth trend

Source: ICICI Direct Research; AIOCD

Exhibit 9: Companies growth in domestic market in January 2020

Source: ICICI Direct Research, AIOCD

10.9

9.9

8.9

10.5

7.2

6.9

13.4

9.7

12.2

5.3

14.6

8.8

7.6

0.0

5.0

10.0

15.0

20.0

Jan-19

Feb-19

Mar-19

Apr-19

May-19

Jun-19

Jul-19

Aug-19

Sep-19

Oct-19

Nov-19

Dec-19

Jan-20

(%

)

Indian Pharma Market

5.4 5.6

-2.0 -1.9

13.8

5.0

20.4

11.0

-0.2

1.8

8.4

6.7

8.9

13.2

1.0

10.3

15.8

-5.0

0.0

5.0

10.0

15.0

20.0

25.0

Abbott

Aja

nta

Ale

mbic

Bio

con

Cadila

Cip

la

Dr R

eddys

Gle

nm

ark

GS

K P

harm

a

Indoco

Ipca L

abs

Lupin

Natco

Pfiz

er

Sanofi

Sun P

harm

a

Torrent

(%

)

Therapy wise performance (| crore)

Therapy Jan'20 Jan'19 %Dec'19 %

Cardiac 1611 1458 10.5 1545 4.3

Anti-Infectives 1571 1473 6.7 1620 -3.0

GI 1272 1209 5.3 1240 2.6

Anti Diabetic 1203 1127 6.7 1177 2.2

Respiratory 1031 940 9.7 1067 -3.4

Vitamins 987 915 7.8 997 -1.0

Derma 811 769 5.4 816 -0.7

Pain 791 743 6.5 802 -1.3

Neuro 749 691 8.4 727 3.1

Gynaecological 580 550 5.5 567 2.2

Anti-Neoplastics 255 239 6.8 253 0.6

Hormones 227 208 9.3 226 0.4

Ophthal 205 197 4.3 211 -3.0

Vaccines 196 180 9.4 196 0.4

Urology 160 145 10.2 161 -1.0

Blood Related 138 123 12.8 135 2.5

Others 118 102 15.8 114 3.6

Sex Stimulants 72 66 9.2 69 5.8

Stomatologicals 65 58 13.5 63 3.2

Anti Malarials 35 32 9.7 43 -16.7

Top brands in Indian pharma market (MAT;

| crore)

Source: ICICI Direct Research; AIOCD

Source: ICICI Direct Research; AIOCD

Acute vs. chronic vs. sub chronic

Source: ICICI Direct Research; AIOCD; As per AIOCD MAT Jan 2020

Acute

47%

Chronic

33%

Sub

Chronic

20%

Brand Company Therapy Jan'20YoY %

Mixtard Abbott Anti Diabetic 548 6.5

Glycomet GpUSV Anti Diabetic 493 7.1

Lantus Sanofi IndiaAnti Diabetic 489 4.3

Janumet MSD Anti Diabetic 479 11.1

Augmentin GSK Anti-Infectives448 19.6

Liv 52 Himalaya GI 406 5.0

Galvus Met Novartis Anti Diabetic 389 -13.6

Duphaston Abbott Hormones 387 12.2

Clavam Alkem Anti-Infectives377 11.0

Monocef Aristo Anti-Infectives368 22.9

ICICI Securities | Retail Research 6

ICICI Direct Research

Monthly Sector Update | Health Check

Exhibit 10: Domestic formulations – market share (MAT value January 2020)

Source: ICICI Direct Research, AIOCD

Exhibit 11: Acute vs. chronic vs. sub chronic (MAT value January 2020)

Source: ICICI Direct Research, AIOCD

8%

6%

5%4%

4%

3%

2% 2% 2% 2%

1%1%

1% 1% 1% 1%0%

0%

1%

2%

3%

4%

5%

6%

7%

8%

9%

Sun

Abbott

Cip

la

Cadila

Lupin

Torrent

Pfiz

er

Dr.

Reddys

Sanofi

Gle

nm

ark

Ipca

Ale

mbic

FD

C

Natco

Indoco

Aja

nta

Bio

con

39 40

57

3042

52

78

40

81

66

27

88

43

60

44 4127

54

3950

24

6145 28

9

42

527

57

1

52 17 5244

52

30

2210

199 13

2013 18 13

716 11

5

23

415

21 16

0

20

40

60

80

100

120

Abbott

Aja

nta

Ale

mbic

Bio

con

Cip

la

Dr.

Reddys

FD

C

Gle

nm

ark

Indoco

IPC

A

Lupin

Sun

Novartis

Pfiz

er*

Sanofi

Sun

Torrent

Cadila

%

Acute Chronic Sub Chronic

ICICI Securities | Retail Research 7

ICICI Direct Research

Monthly Sector Update | Health Check

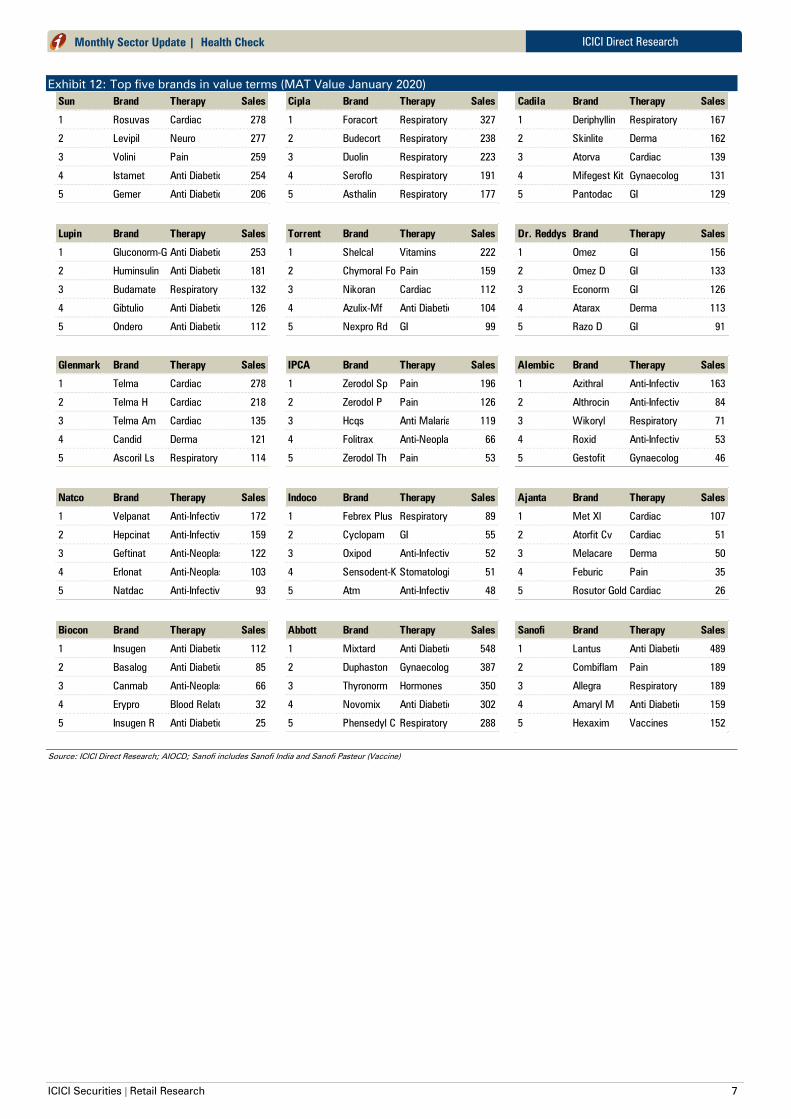

Exhibit 12: Top five brands in value terms (MAT Value January 2020)

Sun Brand Therapy Sales

1 Rosuvas Cardiac 278

2 Levipil Neuro 277

3 Volini Pain 259

4 Istamet Anti Diabetic 254

5 Gemer Anti Diabetic 206

Cipla Brand Therapy Sales

1 Foracort Respiratory 327

2 Budecort Respiratory 238

3 Duolin Respiratory 223

4 Seroflo Respiratory 191

5 Asthalin Respiratory 177

Cadila Brand Therapy Sales

1 Deriphyllin Respiratory 167

2 Skinlite Derma 162

3 Atorva Cardiac 139

4 Mifegest Kit Gynaecological 131

5 Pantodac GI 129

Lupin Brand Therapy Sales

1 Gluconorm-G Anti Diabetic 253

2 Huminsulin Anti Diabetic 181

3 Budamate Respiratory 132

4 Gibtulio Anti Diabetic 126

5 Ondero Anti Diabetic 112

Torrent Brand Therapy Sales

1 Shelcal Vitamins 222

2 Chymoral FortePain 159

3 Nikoran Cardiac 112

4 Azulix-Mf Anti Diabetic 104

5 Nexpro Rd GI 99

Dr. Reddys Brand Therapy Sales

1 Omez GI 156

2 Omez D GI 133

3 Econorm GI 126

4 Atarax Derma 113

5 Razo D GI 91

Glenmark Brand Therapy Sales

1 Telma Cardiac 278

2 Telma H Cardiac 218

3 Telma Am Cardiac 135

4 Candid Derma 121

5 Ascoril Ls Respiratory 114

IPCA Brand Therapy Sales

1 Zerodol Sp Pain 196

2 Zerodol P Pain 126

3 Hcqs Anti Malarials 119

4 Folitrax Anti-Neoplastics 66

5 Zerodol Th Pain 53

Alembic Brand Therapy Sales

1 Azithral Anti-Infectives 163

2 Althrocin Anti-Infectives 84

3 Wikoryl Respiratory 71

4 Roxid Anti-Infectives 53

5 Gestofit Gynaecological 46

Natco Brand Therapy Sales

1 Velpanat Anti-Infectives 172

2 Hepcinat Anti-Infectives 159

3 Geftinat Anti-Neoplastics 122

4 Erlonat Anti-Neoplastics 103

5 Natdac Anti-Infectives 93

Indoco Brand Therapy Sales

1 Febrex Plus Respiratory 89

2 Cyclopam GI 55

3 Oxipod Anti-Infectives 52

4 Sensodent-K Stomatologicals 51

5 Atm Anti-Infectives 48

Ajanta Brand Therapy Sales

1 Met Xl Cardiac 107

2 Atorfit Cv Cardiac 51

3 Melacare Derma 50

4 Feburic Pain 35

5 Rosutor Gold Cardiac 26

Biocon Brand Therapy Sales

1 Insugen Anti Diabetic 112

2 Basalog Anti Diabetic 85

3 Canmab Anti-Neoplastics 66

4 Erypro Blood Related 32

5 Insugen R Anti Diabetic 25

Abbott Brand Therapy Sales

1 Mixtard Anti Diabetic 548

2 Duphaston Gynaecological 387

3 Thyronorm Hormones 350

4 Novomix Anti Diabetic 302

5 Phensedyl Cough LinctusRespiratory 288

Sanofi Brand Therapy Sales

1 Lantus Anti Diabetic 489

2 Combiflam Pain 189

3 Allegra Respiratory 189

4 Amaryl M Anti Diabetic 159

5 Hexaxim Vaccines 152

Source: ICICI Direct Research; AIOCD; Sanofi includes Sanofi India and Sanofi Pasteur (Vaccine)

ICICI Securities | Retail Research 8

ICICI Direct Research

Monthly Sector Update | Health Check

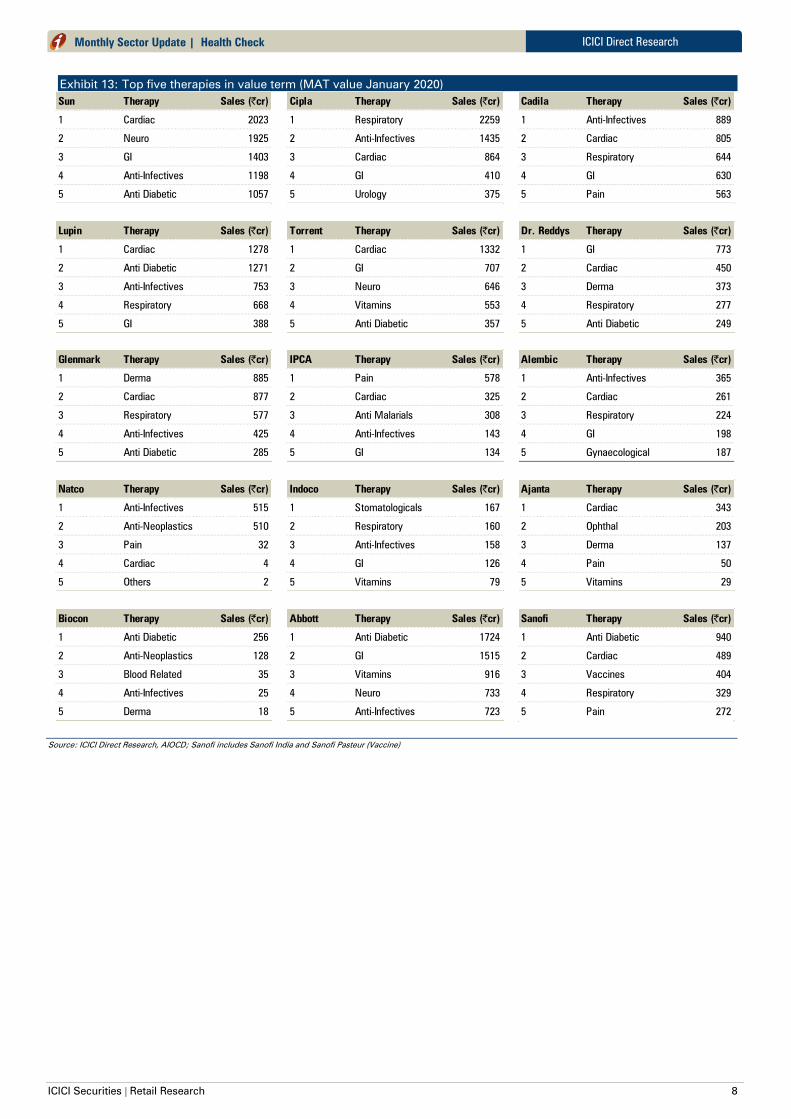

Exhibit 13: Top five therapies in value term (MAT value January 2020)

Sun Therapy Sales (|cr)

1 Cardiac 2023

2 Neuro 1925

3 GI 1403

4 Anti-Infectives 1198

5 Anti Diabetic 1057

Cipla Therapy Sales (|cr)

1 Respiratory 2259

2 Anti-Infectives 1435

3 Cardiac 864

4 GI 410

5 Urology 375

Cadila Therapy Sales (|cr)

1 Anti-Infectives 889

2 Cardiac 805

3 Respiratory 644

4 GI 630

5 Pain 563

Lupin Therapy Sales (|cr)

1 Cardiac 1278

2 Anti Diabetic 1271

3 Anti-Infectives 753

4 Respiratory 668

5 GI 388

Torrent Therapy Sales (|cr)

1 Cardiac 1332

2 GI 707

3 Neuro 646

4 Vitamins 553

5 Anti Diabetic 357

Dr. Reddys Therapy Sales (|cr)

1 GI 773

2 Cardiac 450

3 Derma 373

4 Respiratory 277

5 Anti Diabetic 249

Glenmark Therapy Sales (|cr)

1 Derma 885

2 Cardiac 877

3 Respiratory 577

4 Anti-Infectives 425

5 Anti Diabetic 285

IPCA Therapy Sales (|cr)

1 Pain 578

2 Cardiac 325

3 Anti Malarials 308

4 Anti-Infectives 143

5 GI 134

Alembic Therapy Sales (|cr)

1 Anti-Infectives 365

2 Cardiac 261

3 Respiratory 224

4 GI 198

5 Gynaecological 187

Natco Therapy Sales (|cr)

1 Anti-Infectives 515

2 Anti-Neoplastics 510

3 Pain 32

4 Cardiac 4

5 Others 2

Indoco Therapy Sales (|cr)

1 Stomatologicals 167

2 Respiratory 160

3 Anti-Infectives 158

4 GI 126

5 Vitamins 79

Ajanta Therapy Sales (|cr)

1 Cardiac 343

2 Ophthal 203

3 Derma 137

4 Pain 50

5 Vitamins 29

Biocon Therapy Sales (|cr)

1 Anti Diabetic 256

2 Anti-Neoplastics 128

3 Blood Related 35

4 Anti-Infectives 25

5 Derma 18

Abbott Therapy Sales (|cr)

1 Anti Diabetic 1724

2 GI 1515

3 Vitamins 916

4 Neuro 733

5 Anti-Infectives 723

Sanofi Therapy Sales (|cr)

1 Anti Diabetic 940

2 Cardiac 489

3 Vaccines 404

4 Respiratory 329

5 Pain 272

Source: ICICI Direct Research, AIOCD; Sanofi includes Sanofi India and Sanofi Pasteur (Vaccine)

ICICI Securities | Retail Research 9

ICICI Direct Research

Monthly Sector Update | Health Check

Monthly Sector News

Price hikes, new launches, recalls, approvals

Sun Pharma recalls testosterone hormone drug from US

Sun Pharma has issued a voluntary class-II recall of multiple batches of

testosterone cypionate for injection in the US. The drug, used to treat low

testosterone levels and in hormone therapy, was recalled due to deviations

from GMP norms at the Gujarat facility.

Sun Pharma recalls anti-migraine drug in US

Sun Pharma has also issued a voluntary class-II recall of 207,585 blisters and

384 bottles of its anti-migraine (Sumatriptan succinate) tablets in US due to

presence of impurities.

Sun Pharma launches Absorica LD in US

Sun Pharma has launched novel Absorica LD (isotretinoin) capsules in US

for the management of severe recalcitrant nodular acne in patients +12

years of age. The drug features company's micronisation technology, which

utilises micronised particles to optimise absorption at a 20% lower dose.

USFDA grants Rx-to-OTC conversion of gVoltaren gel

USFDA grants approval for an Rx-to-OTC (prescription to over the counter)

switch to GSK plc's arthritis pain drug, 'Voltaren' (diclofenac sodium) topical

gel. The switch implies that the drug will now be sold as non-

prescription/over the counter drug and will be unavailable through the

prescription route in US. Cipla has ~30% market share by value in gVoltaren

with US$27 million annual prescription (Rx) sales as per Bloomberg data.

Glenmark Europe recalls contrast agent in UK

As per media reports, Glenmark's Europe division is recalling specific

batches of Iohexol solution for injection 350 mg/1 ml and 300 mgl/1 ml as a

precautionary measure due to out of specification content issues. The recall

is being done at wholesaler and pharmacy level in UK.

Lawsuits, court rulings, settlements, regulatory issues

Aurobindo Unit IV receives EIR with VAI status from USFDA

The company’s general injectable formulation facility (Unit IV) at

Pashamylaram, Hyderabad has received establishment inspection report

(EIR) with voluntary action indicated (VAI) status from USFDA. The facility

had earlier received 14 observations after the inspection conducted by

USFDA in November 4-13, 2019.

This classification is a real positive surprise for the Street, including us and

augurs well for the company, as it has 46 pending filings (~30% of total

pending filings) including 50-60% of pending injectables that are filed from

this plant.

Lupin Vizag API facility receives five observations from USFDA

Lupin's API manufacturing facility at Visakhapatnam has received Form 483

with five observations on completion of the USFDA inspection conducted

from January 13-17, 2020.

Cipla's Patalganga facility receives USFDA EIR

Inspection of Cipla's Patalganga manufacturing facility has been closed with

receipt of establishment inspection report (EIR) from USFDA. The facility had

received four observations after the cGMP inspection (for both API &

Formulations) conducted from November 4-13, 2019.

Biocon’s oral solid dosage facility clears USFDA pre-approval inspection

Biocon’s oral solid dosage manufacturing facility in Bengaluru has received

no Form 483 observations after the USFDA pre-approval inspection

conducted from January 13-17, 2020.

ICICI Securities | Retail Research 10

ICICI Direct Research

Monthly Sector Update | Health Check

Alembic receives two observations from USFDA for its Gujarat API facility

Alembic Pharma’s API facility at Karkhadi, Gujarat received Form 483 with

two observations at the end of pre-approval inspection carried out by

USFDA from January 13-17, 2020.

Cipla's Goa facility receives OAI status from USFDA

USFDA has classified Cipla's Goa manufacturing facility as official action

indicated (OAI) for the inspection conducted from September 16-27, 2019

post which the unit had received 12 observations from USFDA. Post adverse

observations, OAI status is on expected lines. The impending negative

impact is likely to act as an overhang on the stock.

Cipla's Bangalore API facility receives four observations from USFDA

Cipla's API manufacturing facility at Bommasandra, Bangalore has received

Form 483 with four observations after the cGMP inspection conducted by

USFDA from January 20-24, 2020.

Lupin's three facilities at Pithampur complete UK MHRA's inspection

Lupin's manufacturing facilities(x3) at Pithampur complete UK Medicines

and Healthcare products Regulatory Agency’s (MHRA) inspection with one

major observation. As per the press release, no critical observations were

issued at the end of the inspection.

Biocon's Bangalore API facility receives five observations from USFDA

Biocon's API facility in Bengaluru has received Form 483 with five

observations after the USFDA pre-approval and GMP inspection conducted

from January 20-24, 2020.

Cipla's US facility receives EIR from USFDA

Cipla's InvaGen manufacturing facility in the US has received establishment

inspection report (EIR) from USFDA indicating closure of the inspection

conducted in December 2-6, 2019.

Dr Reddy's API Plant receives five observations after USFDA re-inspection

Dr Reddy's API Plant (CTO VI) at Srikakulam, Andhra Pradesh has received

Form 483 with five observations after the USFDA re-inspection completed

on January 28

Aurobindo's Unit VII receives OAI status from USFDA

Aurobindo's oral solids manufacturing facility (Unit VII) has received official

action indicated (OAI) status from USFDA. The USFDA had conducted cGMP

related inspection at this unit from September 19-27, 2019 post which the

company had received seven observations.

Unit VII is one of the largest and oldest plants for the company contributing

20-30% to US revenues. The company has ~33 pending USFDA approvals

(including 14 tentative approvals) by the end of Q2FY20 from this unit. The

OAI status is in line with our expectations and the company is likely to face

further remedial action from the USFDA like warning letter or in worst case

scenario an import alert. We await further action from USFDA. Until then, we

believe the stock is likely to remain under pressure.

Divi's Andhra Pradesh facility clears USFDA inspection

Divis Labs' manufacturing facility (Unit-II) at Village Chippada, Andhra

Pradesh has cleared USFDA inspection conducted in January 27-31, 2020

with no Form 483 observations.

Cadila gets DGCI approval for anti-diabetic drug in India

Cadila Healthcare has got approval for Saroglitazar Magnesium (Lipaglyn)

from Drug Controller General of India (DGCI) for treatment of type 2 diabetes

as an add-on therapy with Metformin.

ICICI Securities | Retail Research 11

ICICI Direct Research

Monthly Sector Update | Health Check

SC stays IHH open offer for Fortis

The Supreme Court has maintained its stay order on the takeover of Fortis

Healthcare by Malaysia's IHH Healthcare via open offer route. The court will

now hear the case on March 16.

NGT imposes | 5.7 crore penalty on Jubilant Life

As per media reports, the National Green Tribunal has imposed a penalty of

| 5.47 crore on Jubilant Life Sciences' distillery unit in Pune for discharging

effluents and causing damage to the environment.

Cadila's Ahmedabad SEZ facility clears USFDA inspection

Cadila Healthcare's (subsidiary Alidac Pharma) oncology injectables facility

at SEZ, Ahmedabad has cleared USFDA inspection with no Form 483

observations issued after the inspection conducted from January 27-

February 4, 2020.

Cadila receives EIR for Ahmedabad topical facility

Cadila's topical manufacturing facility at Ahmedabad has received

establishment inspection report (EIR) from USFDA indicating successful

closure of inspection. The facility had received no Form 483 observations

after the USFDA inspection conducted from December 16-20, 2019.

Lupin's Pithampur facility receives two observations from USFDA

Lupin's Pithampur (Unit-I) facility has received Form 483 with two

observations on completion of the USFDA inspection conducted from

February 3-11, 2020.

Dr Reddys’ Srikakulam formulations plant clears USFDA inspection

Dr Reddys' Unit-I SEZ formulations plant at Srikakulam, Andhra Pradesh has

cleared USFDA inspection with zero Form 483 observations.

Dr Reddys' Duvvada formulations plant receives VAI status from USFDA

Dr Reddys' formulations manufacturing facility (Vizag SEZ Plant 1 - FTO 7) at

Duvvada, Visakhapatnam has been classified as voluntary action indicated

(VAI) by USFDA. The facility had received eight Form 483 observations after

the USFDA inspection conducted earlier in August, 2019

Lupin's Aurangabad facility clears USFDA inspection

Lupin's Aurangabad facility has cleared USFDA inspection with no Form 483

observations. The inspection was conducted from February 10-14, 2020.

M&As, demergers, tie-ups and JVs

Sun Pharma, Rockwell medical ink pact for anaemia drug in India

Sun Pharma, Rockwell medical have signed a licensing agreement to

commercialise Rockwell's Triferic, a proprietary iron replacement and

haemoglobin maintenance drug, in India. As per the agreement, Sun will

exclusively develop and commercialise the drug indicated for treating

anaemia in haemodialysis patients while Rockwell will receive upfront and

milestone payments along with royalty on net sales.

Cadila licenses desidustat to CMS for China

Cadila Healthcare, China Medical System Holdings (CMS) have signed a

licensing agreement for Desidustat in Greater China. The drug, a novel oral

HlF-PH inhibitor, is indicated for treatment of anaemia in patients with

chronic kidney disease (CKD). Under terms of the agreement, CMS will

assume all development, registration & commercialisation responsibilities

for the drug while Cadila will receive initial upfront payment, milestone

payments and royalties on net sales.

Glenmark to divest its gynaecology business to True North

Glenmark's board has approved divestment of gynaecology business in

India & Nepal to Integrace Pvt Ltd (True North PE firm) for a cash

consideration of | 115 crore. The sale of this division, contributing less than

1% to company turnover, is expected to be completed by March 31, 2020.

ICICI Securities | Retail Research 12

ICICI Direct Research

Monthly Sector Update | Health Check

Ipca to acquire M/s. Noble Explochem Ltd

NCLT has approved Ipca Labs resolution plan for M/s Noble Explochem

under IBC. Under the plan, Noble will be merged with the company in

consideration of | 69 crore in cash towards settlement of all its liabilities.

Noble operations (manufacturing chemical explosives) have remained

closed since 2006, Ipca plans to employ Noble's assets to manufacture

chemicals, key starting materials and APls in the future.

Dr Reddys' subsidiary inks pact with Curis for oncology drug

Dr Reddys' subsidiary, Aurigene Discovery Technologies (Aurigene) has

signed an agreement with Curis Inc. for development and commercialisation

of CA-170 for treatment of patients with nonsquamous non-small cell lung

cancer (nsNSCLC). As per the terms of the agreement Aurigene will fund

and conduct a Phase 2b/3 randomised study evaluating CA-170 and acquire

rights to develop and commercialise CA-170 in Asia while Curis will be

entitled to royalty payments in Asia.

Cipla Medpro acquires right to market anti-psychotic drug in SA

Cipla's South African subsidiary Cipla Medpro has signed an agreement with

AstraZeneca (originator) and Luye Pharma (acquired rights) to secure

originator (Seroquel) and authorised generic brands (Truvalin) of an atypical

anti-psychotic drug, Quetiapine. The transaction allows Cipla Medpro to

market and distribute the drug in South Africa and neighbouring countries.

Dr Reddy to acquire part of Wockhardt's domestic branded business

Dr Reddy’s lab acquires Wockhardt’s part of domestic branded business

comprising of 62 products including manufacturing facility at Baddi,

Himachal Pradesh for a consideration of | 1850 crore. Revenues of the

proposed acquire business were | 377 crore in 9MFY20 (| 503 crore on

annualised basis). The implied valuation comes to ~3.8x annualised

revenue. This transaction is expected to be completed in May 2020 subject

to regulatory approvals.

We believe the deal value is in line with industry standard. Post this

acquisition, the domestic business contribution of Dr Reddy’s Lab in total

revenues is likely increase to 19-20% from 17% in 9MFY20.

Others

Syngene commissions phase-I of Hyderabad R&D facility

As per media reports, Biocon's contract research subsidiary, 'Syngene' has

commissioned first phase of its new Hyderabad R&D centre in Genome

valley. The 52000 sq ft facility will initially house ~150 scientists and will be

completely commissioned with 94000 sq ft and ~270 scientists by end of

year.

Apollo Hospitals introduces EMI card with Bajaj Finserv

Apollo Hospitals, Bajaj Finserv have introduced a co-branded health EMI

card to allow patients to convert their medical bills into no-cost EMIs that

can be repaid over a period of 12 months. The card offers EMI financing and

quick loan processing with minimal paperwork. The card would not only

help in medical emergencies but also serve patients without health

insurance or whose insurance limit is lower than treatment cost.

Apollo Hospitals brings down pledge to ~30% of promoter holding

Apollo Hospital’s promoters have brought down their pledge position to

29.64% (down from 67.33% earlier) of the total 30.8% promoter holding

using proceeds from the Apollo Munich deal.

Cadila launches research programme for COVID-19 vaccine

Cadila Healthcare has launched an accelerated research programme in India

and Europe to develop vaccine for novel coronavirus (COVID-19). The

company is working on two approaches, a DNA based vaccine and a live

attenuated recombinant measles virus vectored vaccine to combat COVID-

19.

ICICI Securities | Retail Research 13

ICICI Direct Research

Monthly Sector Update | Health Check

ANDA Approvals

Alembic Pharma has got USFDA approval for generic version of Covis

Pharma's Zanaflex (Tizanidine Hydrochloride) capsules, 2/4/6 mg in US. The

drug, used to treat and manage muscle spasms (spasticity), had an

estimated market size of ~US$ 28 million in US as per IQVIA MAT

September 2019.

Alembic Pharma has got tentative USFDA approval for the generic version

of Boehringer lngelheim's Jardiance (Empagliflozin) tablets, 10/25 mg in US.

The drug, used to improve glycaemic control in adults with type 2 diabetes,

had an estimated market size of ~US$3.4 billion as per IQVIA MAT

September 2019.

Alembic Pharma has got USFDA approval for generic version of Allergan's

Latisse (Bimatoprost) ophthalmic solution, 0.03% in US. The drug, indicated

to treat hypotrichosis (deficiency) of the eyelashes, had an estimated market

size of ~US$ 57 million in US as per IQVIA MAT September 2019.

Alembic Pharma has got USFDA approval for the generic version of AbbVie's

cholesterol drug 'Tricor' (Fenofibrate) tablets, 54/160 mg in US. The drug had

an estimated market size of ~US$100 million in US as per IQVIA MAT

September 2019.

Alembic Pharma has got USFDA approval for generic version of Actelion

Pharma's 'Tracleer' (Bosentan) tablets, 62.5/125 mg in US. The drug,

indicated for the treatment of pulmonary arterial hypertension(PAH), had an

estimated market size of ~US$ 68 million in US as per IQVIA MAT

September 2019.

Alembic Pharma has got USFDA approval for generic version of Pfizer's

antibiotic Zithromax (Azithromycin) tablet, 600 mg in the US. The drug had

an estimated market size of ~US$2 million in the US as per IQVIA MAT

September 2019.

Alembic Pharma (Aleor Derma, JV) has got USFDA approval for generic

version of Fougera Pharma's Temovate (Clobetasol Propionate, derma

therapy) cream, 0.05% in US. The drug had an estimated market size of

~US$ 57 million in US as per IQVIA MAT September 2019.

Alembic Pharma has got USFDA approval for generic version of Pfizer's

antibiotic Zithromax (Azithromycin) tablet, 250/500 mg in the US. The drug

had an estimated market size of ~US$129 million in the US as per IQVIA

MAT September 2019.

Aurobindo Pharma (Eugia Pharma, JV) has got USFDA approval for generic

version of Dava Pharma's autoimmune drug Rheumatrex (Methotrexate)

tablets, 2.5 mg in US. The drug, to be launched in March 2020, had an

estimated market size of ~US$98 million in the US as per IQVIA MAT

December 2019.

Lupin has received USFDA approval for the generic version of Sanofi-

Aventis’ Arava (Leflunomide) tablets, 10/20 mg. The drug, indicated for

treatment of rheumatoid arthritis, had an annual sales of ~US$44 million in

the US (IQVIA MAT December 2019). It will be manufactured at the

company's Pithampur facility.

Dr Reddy's has launched the generic equivalent of Alton Pharma's Syprine

(Trientine Hydrochloride) capsules, 250 mg in the US. The drug, indicated

for treatment of patients with Wilson's disease, had annual sales of ~US$94

million in the US (IMS MAT December 2019).

Cadila has received USFDA approval for the generic version of Vanos

(Fluocinonide) cream, 0.1% in US. The drug, used to treat a variety of skin

conditions (e.g. psoriasis, eczema, dermatitis, allergies, rash), will be

manufactured at the company's topical manufacturing facility in

Ahmedabad.

ICICI Securities | Retail Research 14

ICICI Direct Research

Monthly Sector Update | Health Check

Cadila Healthcare has got USFDA approval for the generic version of Canasa

(Mesalamine) suppository, 1000 mg for rectal use. The drug, used to treat

ulcerative proctitis (bowel disease), will be manufactured at the company's

Ahmedabad topical facility.

Lupin has received USFDA approval for the generic version of Novartis’

Moxeza (Moxifloxacin) ophthalmic solution, 0.5% in US. The drug, indicated

for treatment of conjunctivitis, had annual sales of ~US$10 million in the US

(IQVIA MAT December 2019). It will be manufactured at the company's

Pithampur facility.

Exhibit 14: One year forward PE

Source: ICICI Direct Research, Bloomberg

Exhibit 15: ICICI Direct coverage universe (Healthcare)

Company I-Direct CMP TP Rating M Cap

Code (|) (|) (| cr) FY19 FY20E FY21E FY22E FY19 FY20E FY21E FY22E FY19 FY20E FY21E FY22E FY19FY20EFY21EFY22E

Ajanta PharmaAJAPHA 1322 1,525 Buy 11533 43.5 53.0 63.4 76.2 30.4 24.9 20.8 17.3 21.8 24.1 23.2 23.9 17.1 18.0 18.6 19.1

Alembic PharmaALEMPHA 649 620 Hold 12235 31.4 44.3 26.6 31.0 20.6 14.6 24.4 20.9 19.6 21.6 13.4 14.9 21.8 24.9 13.3 13.8

Apollo HospitalsAPOHOS 1766 2,060 Buy 24570 17.0 24.5 41.6 69.8 104.1 72.2 42.4 25.3 8.8 10.9 14.3 17.6 7.1 9.1 12.9 18.5

Aurobindo PharmaAURPHA 589 630 Hold 34538 42.1 45.5 56.9 62.9 14.0 12.9 10.4 9.4 15.9 16.3 15.8 16.7 17.7 16.2 17.1 16.1

Biocon BIOCON 305 310 Hold 36654 6.2 7.5 10.3 15.7 49.2 40.5 29.6 19.5 10.9 12.9 15.1 19.4 12.2 12.3 14.7 18.6

Cadila HealthcareCADHEA 269 285 Hold 27544 18.1 13.3 15.6 19.0 14.9 20.3 17.2 14.1 13.0 10.1 11.1 12.6 17.8 12.1 12.8 13.9

Cipla CIPLA 441 490 Hold 35543 18.6 20.6 22.3 27.3 23.7 21.4 19.7 16.1 10.9 12.7 13.1 14.6 10.0 10.1 10.0 11.1

Divi's Lab DIVLAB 2169 1,990 Hold 57584 51.0 50.1 58.4 71.0 42.6 43.3 37.2 30.5 25.5 21.8 21.8 22.8 19.4 16.7 16.8 17.5

Dr Reddy's LabsDRREDD 3281 3,520 Hold 54501 114.8 107.5 148.2 175.9 28.6 30.5 22.1 18.7 11.1 8.6 14.1 16.8 13.6 11.5 14.0 14.6

Glenmark PharmaGLEPHA 316 340 Hold 8915 26.9 26.8 33.9 42.5 11.7 11.8 9.3 7.4 15.3 13.1 14.3 15.9 13.5 12.0 13.3 14.4

Hikal HIKCHE 121 160 Buy 1594 8.4 9.6 11.1 13.3 14.5 12.6 10.9 9.1 14.3 13.3 13.6 14.5 13.6 14.1 14.2 14.9

Ipca LaboratoriesIPCLAB 1372 1,560 Buy 17337 35.1 57.2 64.5 78.0 39.1 24.0 21.3 17.6 15.0 21.1 20.7 21.4 14.2 19.6 18.7 19.0

Indoco remediesINDREM 251 240 Hold 2313 -0.3 3.0 8.4 15.1 -797.6 85.0 29.9 16.6 1.0 4.6 9.3 15.3 -0.4 4.0 10.1 15.4

Lupin LUPIN 708 675 Hold 32054 16.5 -35.6 18.0 30.7 42.8 -19.9 39.3 23.1 9.4 8.6 7.8 12.2 5.4 -12.2 5.9 9.3

Narayana HrudalayaNARHRU 350 430 Buy 7150 2.9 7.2 9.8 13.3 120.5 48.9 35.8 26.3 7.7 12.0 13.9 16.5 5.5 12.2 14.5 16.7

Natco PharmaNATPHA 654 650 Hold 11907 34.9 26.9 24.6 23.4 18.7 24.3 26.6 27.9 21.3 14.6 12.7 11.3 18.5 12.6 10.4 9.1

Sun Pharma SUNPHA 406 460 Hold 97339 15.9 17.7 18.4 23.0 25.6 22.9 22.0 17.7 10.3 10.8 10.6 11.9 9.2 9.4 9.0 10.1

Syngene Int. SYNINT 306 360 Buy 12242 8.3 10.5 9.6 12.0 37.0 29.2 31.7 25.6 14.8 13.7 13.1 15.1 16.8 14.7 14.1 14.9

Torrent PharmaTORPHA 2199 2,020 Hold 37212 48.9 56.1 71.5 91.8 44.9 39.2 30.8 23.9 14.2 15.7 18.4 21.2 17.5 17.4 19.1 20.7

RoE (%)EPS (|) PE(x) RoCE (%)

Source: ICICI Direct Research, Bloomberg

0.0

10.0

20.0

30.0

40.0

Feb-17

Aug-17

Feb-18

Aug-18

Feb-19

Aug-19

Feb-20

x

NSE500 Index NSE Pharma

24% Premium

ICICI Securities | Retail Research 15

ICICI Direct Research

Monthly Sector Update | Health Check

RATING RATIONALE

ICICI Direct endeavours to provide objective opinions and recommendations. ICICI Direct assigns ratings to its

stocks according to their notional target price vs. current market price and then categorises them as Buy, Hold,

Reduce and Sell. The performance horizon is two years unless specified and the notional target price is defined as

the analysts' valuation for a stock

Buy: >15%;

Hold: -5% to 15%;

Reduce: -5% to -15%;

Sell: <-15%

Pankaj Pandey Head – Research [email protected]

ICICI Direct Research Desk,

ICICI Securities Limited,

1st Floor, Akruti Trade Centre,

Road No 7, MIDC,

Andheri (East)

Mumbai – 400 093

ICICI Securities | Retail Research 16

ICICI Direct Research

Monthly Sector Update | Health Check

ANALYST CERTIFICATION

We /I, Siddhant Khandekar, Inter CA, Mitesh Shah, CFA, Sudarshan Agarwal, PGDM (Finance) Research Analysts, authors and the names subscribed to this report, hereby certify that all of the views expressed

in this research report accurately reflect our views about the subject issuer(s) or securities. We also certify that no part of our compensation was, is, or will be directly or indirectly related to

the specific recommendation(s) or view(s) in this report. It is also confirmed that above mentioned Analysts of this report have not received any compensation from the companies mentioned

in the report in the preceding twelve months and do not serve as an officer, director or employee of the companies mentioned in the report.

Terms & conditions and other disclosures:

ICICI Securities Limited (ICICI Securities) is a full-service, integrated investment banking and is, inter alia, engaged in the business of stock brokering and distribution of financial products. ICICI

Securities Limited is a SEBI registered Research Analyst with SEBI Registration Number – INH000000990. ICICI Securities Limited SEBI Registration is INZ000183631 for stock broker. ICICI

Securities is a subsidiary of ICICI Bank which is India’s largest private sector bank and has its various subsidiaries engaged in businesses of housing finance, asset management, life insurance,

general insurance, venture capital fund management, etc. (“associates”), the details in respect of which are available on www.icicibank.com

ICICI Securities is one of the leading merchant bankers/ underwriters of securities and participate in virtually all securities trading markets in India. We and our associates might have investment

banking and other business relationship with a significant percentage of companies covered by our Investment Research Department. ICICI Securities generally prohibits its analysts, persons

reporting to analysts and their relatives from maintaining a financial interest in the securities or derivatives of any companies that the analysts cover.

Recommendation in reports based on technical and derivative analysis centre on studying charts of a stock's price movement, outstanding positions, trading volume etc as opposed to focusing

on a company's fundamentals and, as such, may not match with the recommendation in fundamental reports. Investors may visit icicidirect.com to view the Fundamental and Technical

Research Reports.

Our proprietary trading and investment businesses may make investment decisions that are inconsistent with the recommendations expressed herein.

ICICI Securities Limited has two independent equity research groups: Institutional Research and Retail Research. This report has been prepared by the Retail Research. The views and opinions

expressed in this document may or may not match or may be contrary with the views, estimates, rating, target price of the Institutional Research.

The information and opinions in this report have been prepared by ICICI Securities and are subject to change without any notice. The report and information contained herein is strictly

confidential and meant solely for the selected recipient and may not be altered in any way, transmitted to, copied or distributed, in part or in whole, to any other person or to the media or

reproduced in any form, without prior written consent of ICICI Securities. While we would endeavour to update the information herein on a reasonable basis, ICICI Securities is under no

obligation to update or keep the information current. Also, there may be regulatory, compliance or other reasons that may prevent ICICI Securities from doing so. Non-rated securities indicate

that rating on a particular security has been suspended temporarily and such suspension is in compliance with applicable regulations and/or ICICI Securities policies, in circumstances where

ICICI Securities might be acting in an advisory capacity to this company, or in certain other circumstances.

This report is based on information obtained from public sources and sources believed to be reliable, but no independent verification has been made nor is its accuracy or completeness

guaranteed. This report and information herein is solely for informational purpose and shall not be used or considered as an offer document or solicitation of offer to buy or sell or subscribe

for securities or other financial instruments. Though disseminated to all the customers simultaneously, not all customers may receive this report at the same time. ICICI Securities will not treat

recipients as customers by virtue of their receiving this report. Nothing in this report constitutes investment, legal, accounting and tax advice or a representation that any investment or strategy

is suitable or appropriate to your specific circumstances. The securities discussed and opinions expressed in this report may not be suitable for all investors, who must make their own

investment decisions, based on their own investment objectives, financial positions and needs of specific recipient. This may not be taken in substitution for the exercise of independent

judgment by any recipient. The recipient should independently evaluate the investment risks. The value and return on investment may vary because of changes in interest rates, foreign

exchange rates or any other reason. ICICI Securities accepts no liabilities whatsoever for any loss or damage of any kind arising out of the use of this report. Past performance is not necessarily

a guide to future performance. Investors are advised to see Risk Disclosure Document to understand the risks associated before investing in the securities markets. Actual results may differ

materially from those set forth in projections. Forward-looking statements are not predictions and may be subject to change without notice.

ICICI Securities or its associates might have managed or co-managed public offering of securities for the subject company or might have been mandated by the subject company for any other

assignment in the past twelve months.

ICICI Securities or its associates might have received any compensation from the companies mentioned in the report during the period preceding twelve months from the date of this report

for services in respect of managing or co-managing public offerings, corporate finance, investment banking or merchant banking, brokerage services or other advisory service in a merger or

specific transaction.

ICICI Securities encourages independence in research report preparation and strives to minimize conflict in preparation of research report. ICICI Securities or its associates or its analysts did

not receive any compensation or other benefits from the companies mentioned in the report or third party in connection with preparation of the research report. Accordingly, neither ICICI

Securities nor Research Analysts and their relatives have any material conflict of interest at the time of publication of this report.

Compensation of our Research Analysts is not based on any specific merchant banking, investment banking or brokerage service transactions.

ICICI Securities or its subsidiaries collectively or Research Analysts or their relatives do not own 1% or more of the equity securities of the Company mentioned in the report as of the last day

of the month preceding the publication of the research report.

Since associates of ICICI Securities are engaged in various financial service businesses, they might have financial interests or beneficial ownership in various companies including the subject

company/companies mentioned in this report.

ICICI Securities may have issued other reports that are inconsistent with and reach different conclusion from the information presented in this report.

Neither the Research Analysts nor ICICI Securities have been engaged in market making activity for the companies mentioned in the report.

We submit that no material disciplinary action has been taken on ICICI Securities by any Regulatory Authority impacting Equity Research Analysis activities.

This report is not directed or intended for distribution to, or use by, any person or entity who is a citizen or resident of or located in any locality, state, country or other jurisdiction, where such

distribution, publication, availability or use would be contrary to law, regulation or which would subject ICICI Securities and affiliates to any registration or licensing requirement within such

jurisdiction. The securities described herein may or may not be eligible for sale in all jurisdictions or to certain category of investors. Persons in whose possession this document may come

are required to inform themselves of and to observe such restriction.