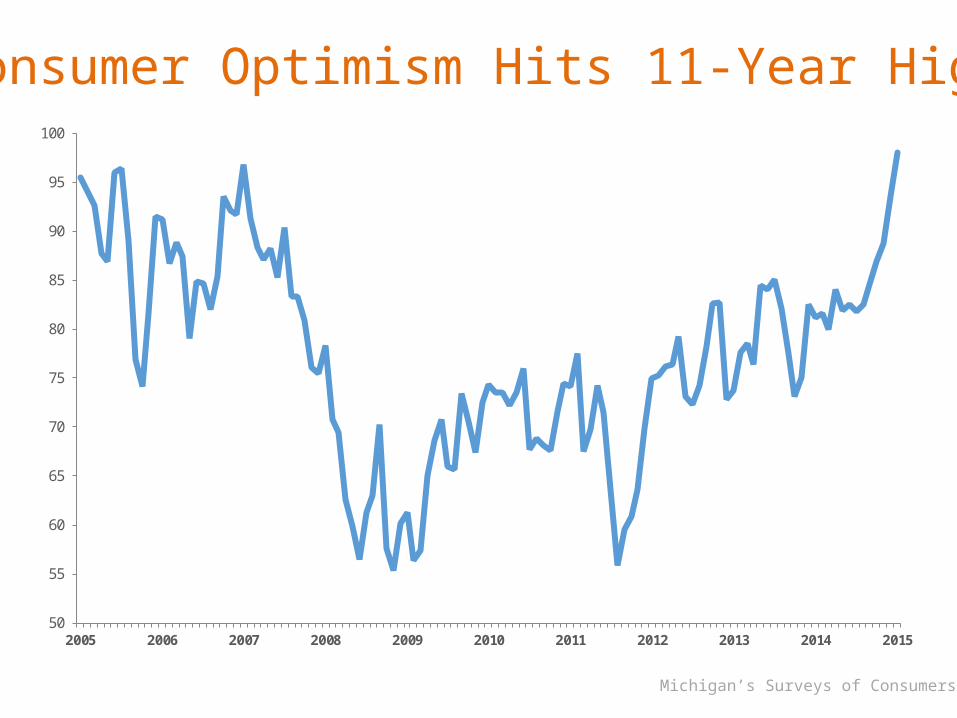

february 2015. michigan’s surveys of consumers consumer optimism hits 11-year high

TRANSCRIPT

FEBRUARY 2015

50

55

60

65

70

75

80

85

90

95

100

2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015

Michigan’s Surveys of Consumers

Consumer Optimism Hits 11-Year High

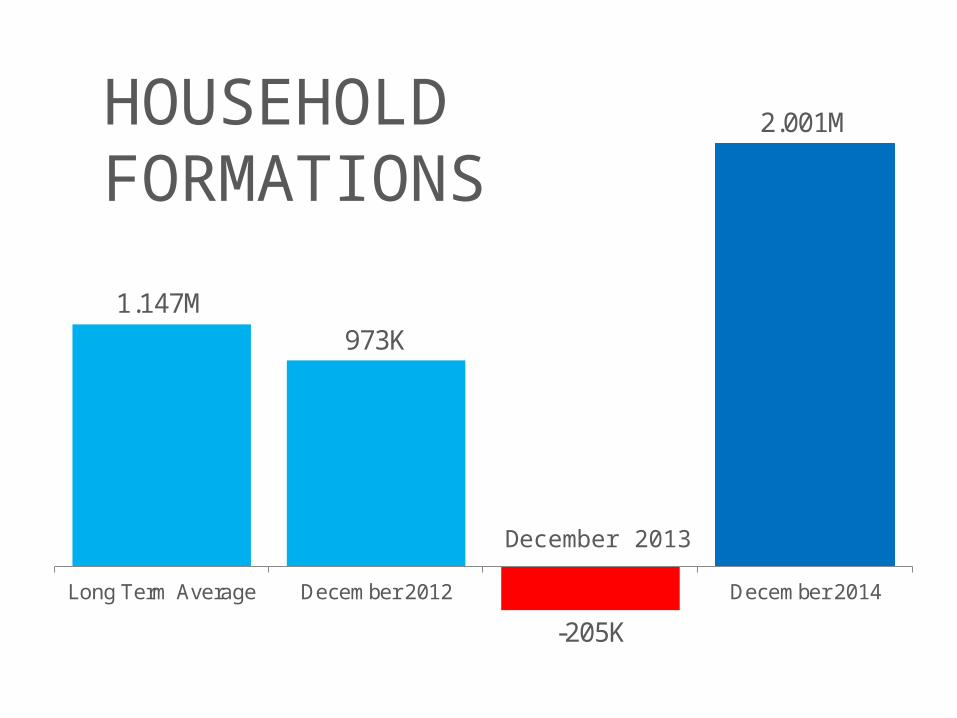

1.147M973K

-205K

2.001M

Long Term Average December 2012 December 2013 December 2014

December 2013

HOUSEHOLD FORMATIONS

NAR

$83 $990

$4,800

$9,000

$18,000

Initial Month 1 Year 5 Years 10 Years 30 Years

Savings on Reduced FHA Mortgage Insurance PremiumsBased on a mortgage of $200,000

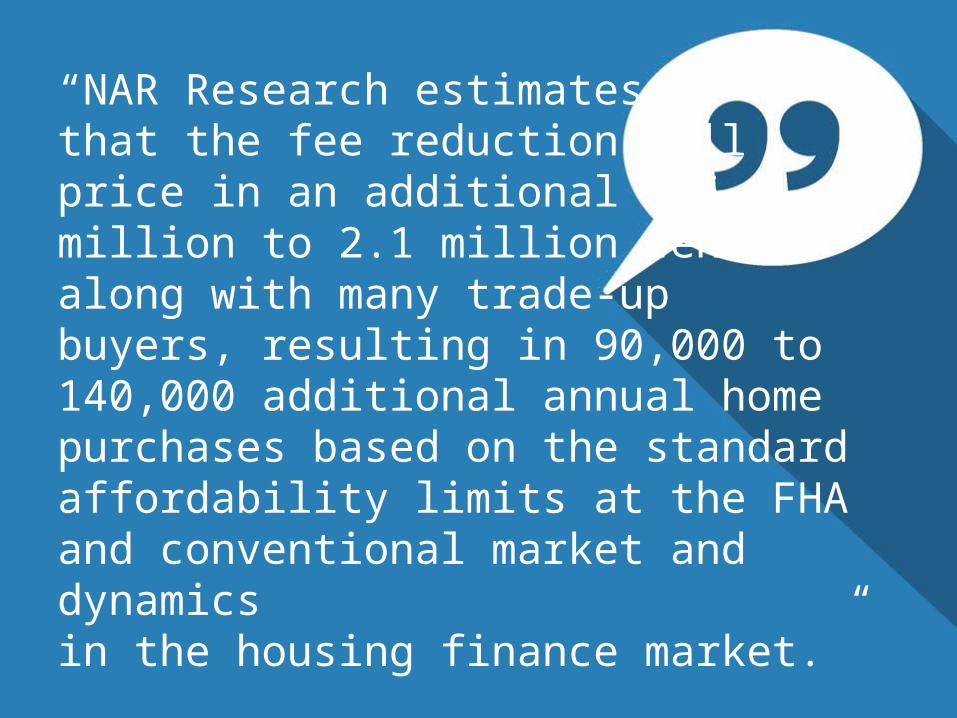

“NAR Research estimates that the fee reduction will price in an additional 1.6 million to 2.1 million renters along with many trade-up buyers, resulting in 90,000 to 140,000 additional annual home purchases based on the standard affordability limits at the FHA and conventional market and dynamicsin the housing finance market.”

April2013

May June July Aug Sept Oct Nov Dec Jan2014

Feb March April May June July Aug Sept Oct Nov Dec

Mortgage Credit Availability

31%

47%58%

Age 18-24 Age 25-34 Age 35-44

Renters Planning on Buying a Home

Freddie Mac

in the next 3 years by age group

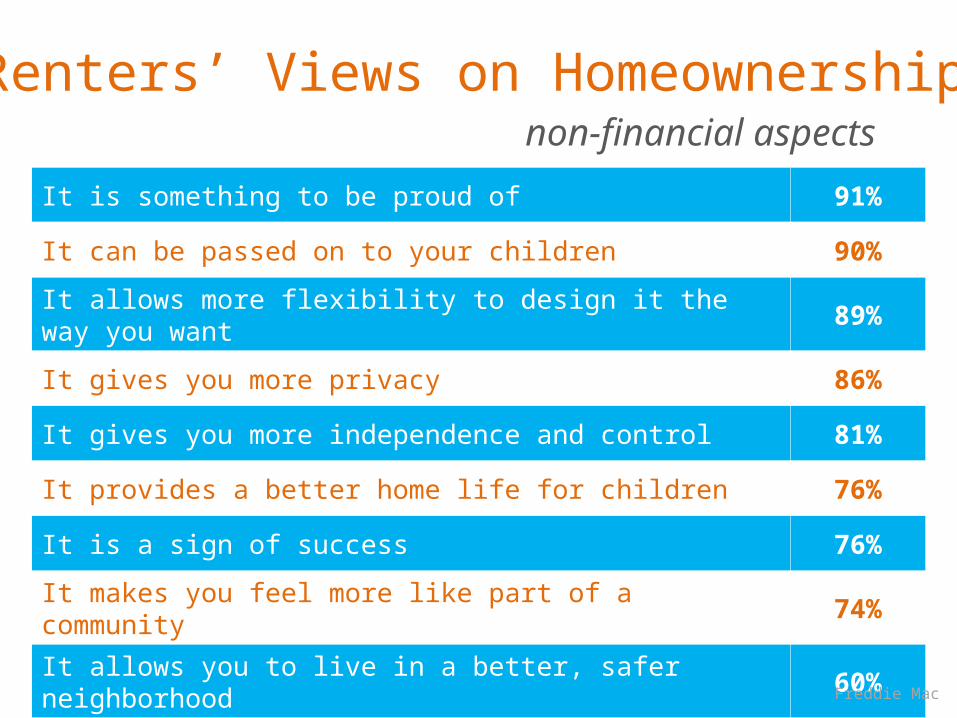

Renters’ Views on Homeownership

Freddie Mac

86%

Homeownership provides protection

against rent increases

80%

Homeownership is an investment opportunity that

builds long-term wealth

77%

Homeownership provides stability and/or

financial security

financial aspects

It is something to be proud of 91%

It can be passed on to your children 90%

It allows more flexibility to design it the way you want 89%

It gives you more privacy 86%

It gives you more independence and control 81%

It provides a better home life for children 76%

It is a sign of success 76%

It makes you feel more like part of a community 74%

It allows you to live in a better, safer neighborhood 60%

Freddie Mac

Renters’ Views on Homeownershipnon-financial aspects

#1 Reasons Renters Won’t Buy

Freddie Mac

44%

62% 58%

Age 18-24 Age 25-34 Age 35-44

Impact on “Willingness to Pay”

5%

40%

A 2% Change in Mortgage Rate Change in Down Payment

The impact on a renter’s “willingness to pay” when buying a house.

Federal Reserve Bank of New York

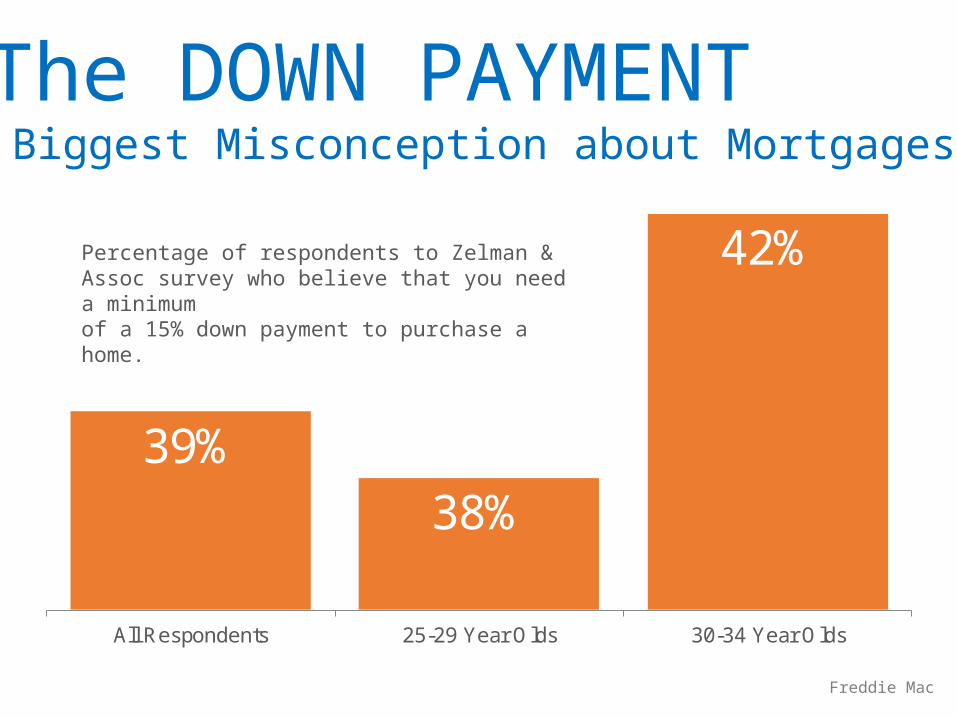

The DOWN PAYMENT Biggest Misconception about Mortgages

39%38%

42%

All Respondents 25-29 Year Olds 30-34 Year Olds

Percentage of respondents to Zelman & Assoc survey who believe that you need a minimum of a 15% down payment to purchase a home.

Freddie Mac

“It’s not that Millennials and other potential homebuyers aren’t qualified in terms of

their credit scores or in how much they have saved for

their down payment.

It’s that they think they’re not qualified or they think that they don’t have a big enough down payment.”

Housing Wire commenting on a study by Nomura

Julián Castro, Secretary for HUD

“A home is often a primary source of wealth in a family…

Having a home is generational way to pass that wealth on. We want people responsible enough to own a home to have that opportunity.”

A Second CHALLENGEA Second CHALLENGE

Lawrence Yun, NAR’s Chief Economist

“The total inventory of homes available for sale fell for the first time in 16 months…

Months supply is already low at 4.4 months.

More inventories are needed, not less. Or else, home prices could re-accelerate.”

-25%

-20%

-15%

-10%

-5%

0%

5%

10%

Jan Feb March April May June July Aug Sept Oct Nov Dec Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec

% -24% -20.8 -16.8 -14% -13% -7.6% -5% -6.2% 1.8% 0.9% 5.0% 1.6% 7.3% 5.3% 3.2% 6.5% 6% 5.5% 5.8% 4.5% 6% 5.2% 5% -0.50

NAR 1/2015

Year-over-Year Inventory Levels

4

5

6

7

8

9

10

11

2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014

Historically, number of years home sellers lived in their homes

Pent Up Seller Demand

Pent Up Seller Demand

Equity Share by State Q3 2014

July 2013 August September October November December January2014

February March Apr il May June July August September October November December

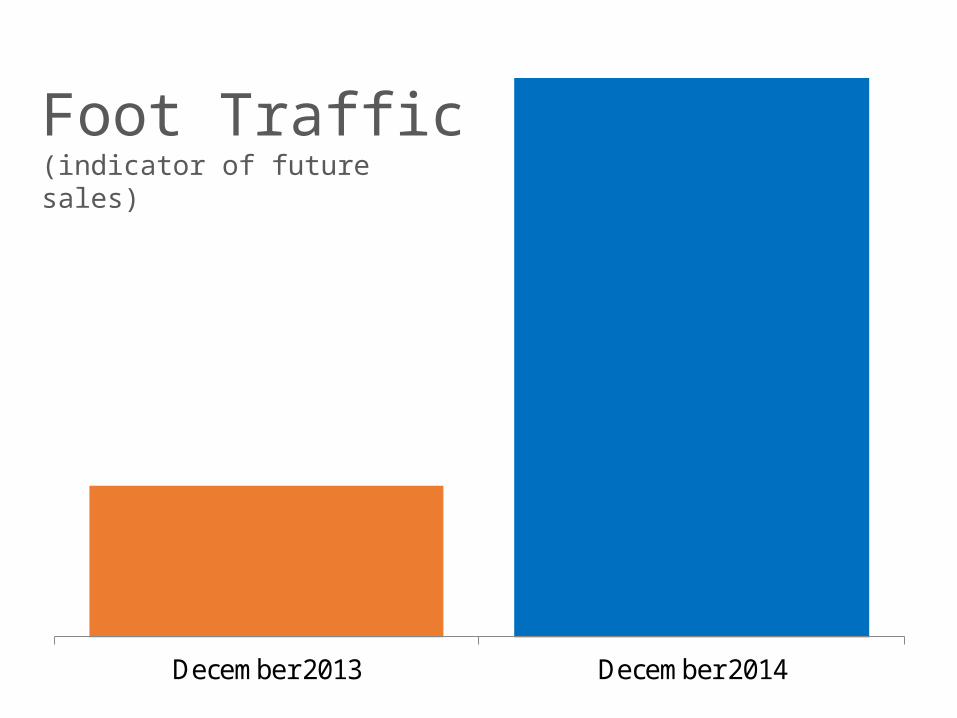

Foot Traffic (indicator of future sales)

December 2013 December 2014

Foot Traffic (indicator of future sales)

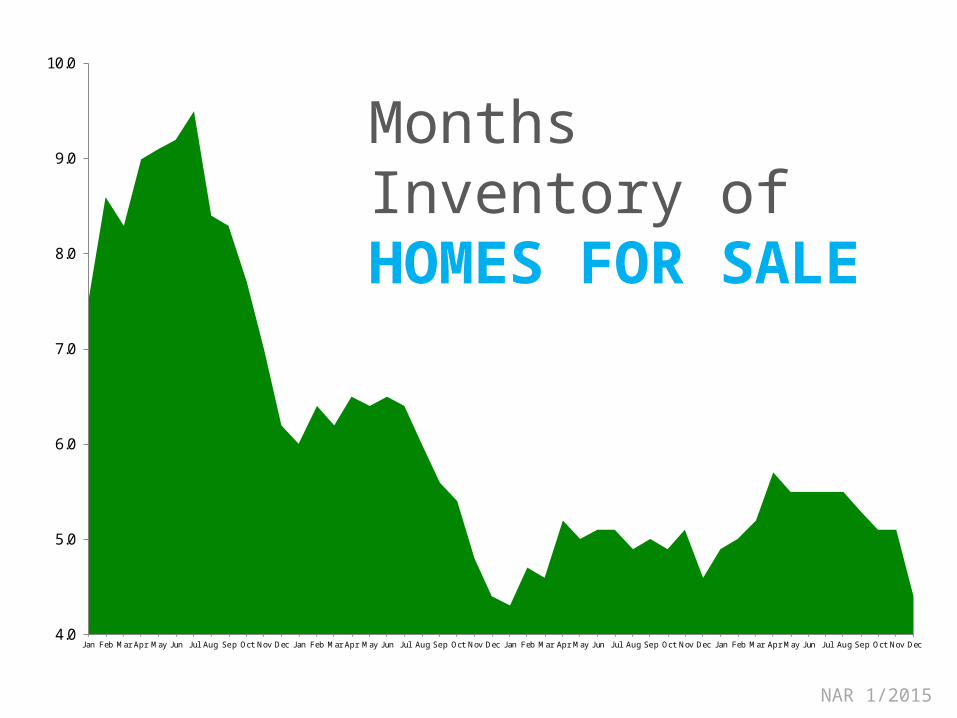

5.7

5.5 5.5 5.5 5.5

5.3

5.1 5.1

4.4

Apr May Jun Jul Aug Sep Oct Nov Dec

Months Inventory of HOMES FOR SALE

NAR 1/2015

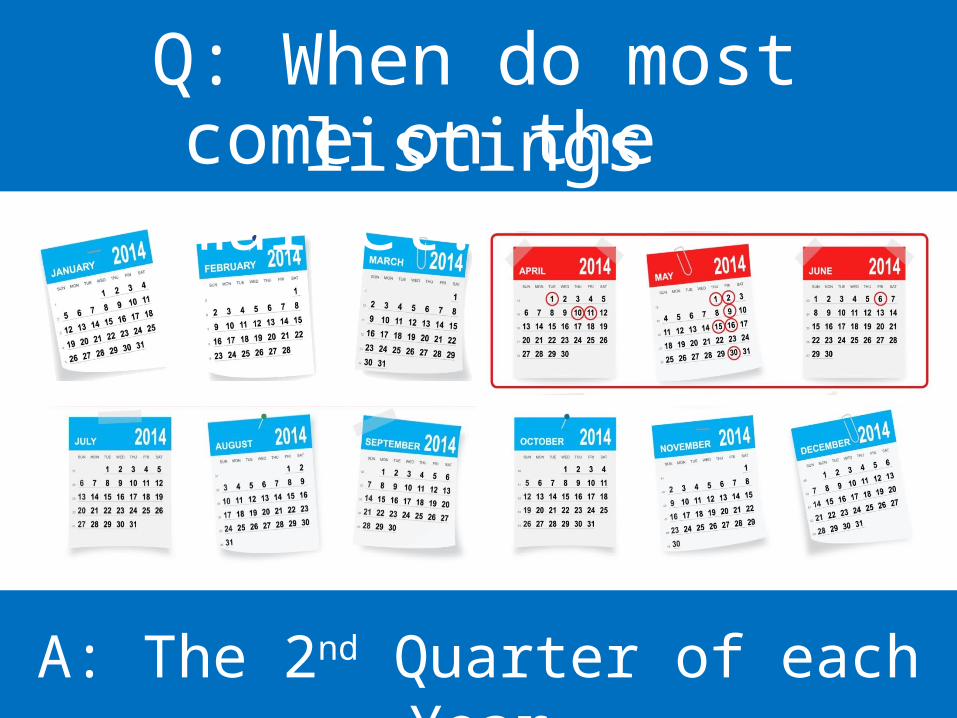

Q: When do most listingscome on the market?

A: The 2nd Quarter of each Year

1.88 1.901.96

2.23 2.252.29

2.35

Jan Feb Mar Apr May Jun Jul

2014 Available Inventoryin millions

-4.4%

8.9%

16% 15.7%

10.4%

5.2%

$0-100K $100-250K $250-500K $500-750K $750K-1M $1M+

% -4.4% 8.9% 16.0% 15.7% 10.4% 5.2%

% Change in Sales from last year

by Price Range

4,000,000

4,500,000

5,000,000

5,500,000

Jan2012

Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec Jan2013

Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec Jan2014

Feb Mar Apr May Jun July Aug Sept Oct Nov Dec

NAR 1/2015

EXISTING Home Sales

90

95

100

105

110

Jan Feb MarApr May Jun Jul Aug Sep Oct Nov Dec Jan Feb Mar Apr May Jun Jul AugSep Oct Nov Dec Jan Feb Mar Apr May Jun Jul AugSep Oct Nov Dec

100 = Historically Healthy Level

NAR 1/2015

PENDING Home Sales

3.2

3.4

3.6

3.8

4

4.2

4.4

4.6

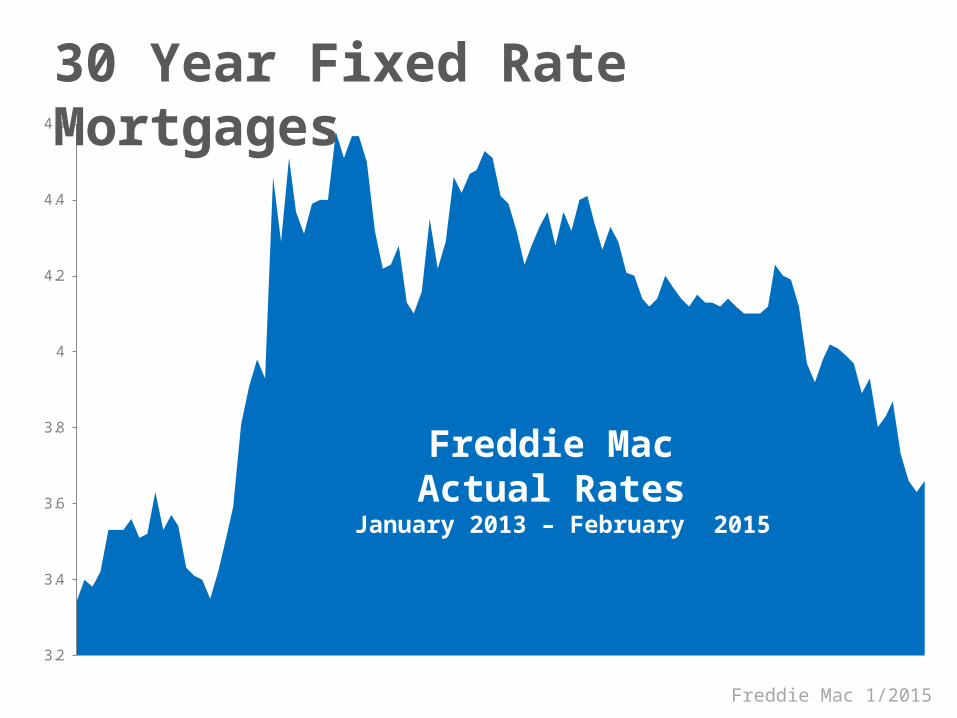

Freddie Mac 1/2015

Freddie Mac Actual Rates

January 2013 – February 2015

30 Year Fixed Rate Mortgages

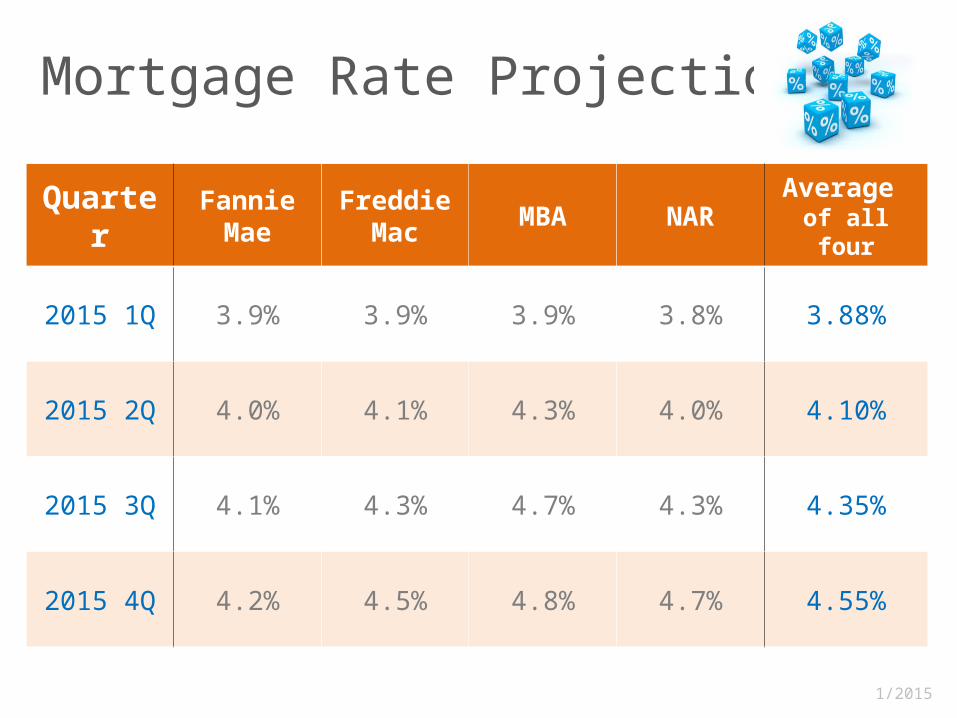

QuarterFannie

MaeFreddie

MacMBA NAR Average

of all four

2015 1Q 3.9% 3.9% 3.9% 3.8% 3.88%

2015 2Q 4.0% 4.1% 4.3% 4.0% 4.10%

2015 3Q 4.1% 4.3% 4.7% 4.3% 4.35%

2015 4Q 4.2% 4.5% 4.8% 4.7% 4.55%

Mortgage Rate Projections

1/2015

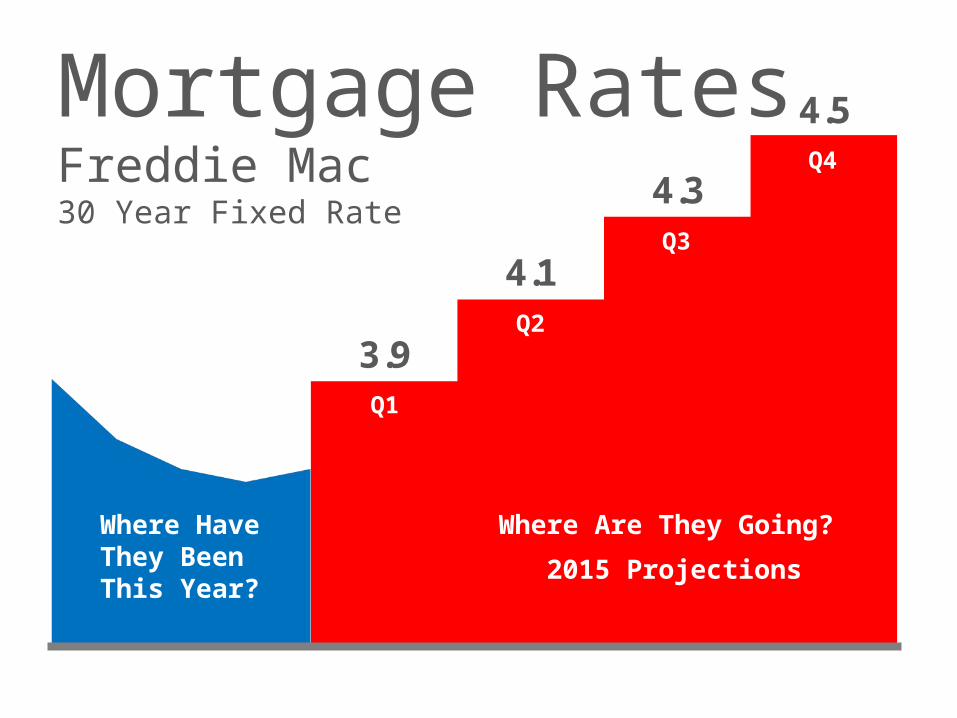

3.9

4.1

4.3

4.5

Where Are They Going?

2015 Projections

Q1

Q2

Q3

Q4

Where Have They Been This Year?

Mortgage RatesFreddie Mac 30 Year Fixed Rate

4.0

5.0

6.0

7.0

8.0

9.0

10.0

Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec

Months Inventory of HOMES FOR SALE

NAR 1/2015

4.0

4.5

5.0

5.5

6.0

Jan'13

Feb Mar Apr May Jun Jul Aug Sept Oct Nov Dec Jan'14

Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec

Months Inventory of HOMES FOR SALE

NAR 1/2015

4.6

4.95.0

5.2

5.7

5.5 5.5 5.5 5.5

5.3

5.1 5.1

4.4

4.0

4.5

5.0

5.5

6.0

Dec Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec

Months Inventory of HOMES FOR SALE

NAR 1/2015

0.0%

2.0%

4.0%

6.0%

8.0%

10.0%

12.0%

14.0%

June 2012 January 2013 January 2014 November

S&P Case Shiller 1/2015

Year-Over-Year

PRICECHANGES

Case Shiller

13.2%12.9%

12.4%

10.8%

9.3%

8.1%

6.7%

5.6%

4.8%4.5% 4.3%

Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov

S&P Case Shiller 1/2015

Year-Over-Year PRICE CHANGES

Case Shiller

S&P Case-Shiller Home Price Indices

S&P Case Shiller 1/2015

Jan2012

Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec Jan2013

Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec Jan2014

Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec

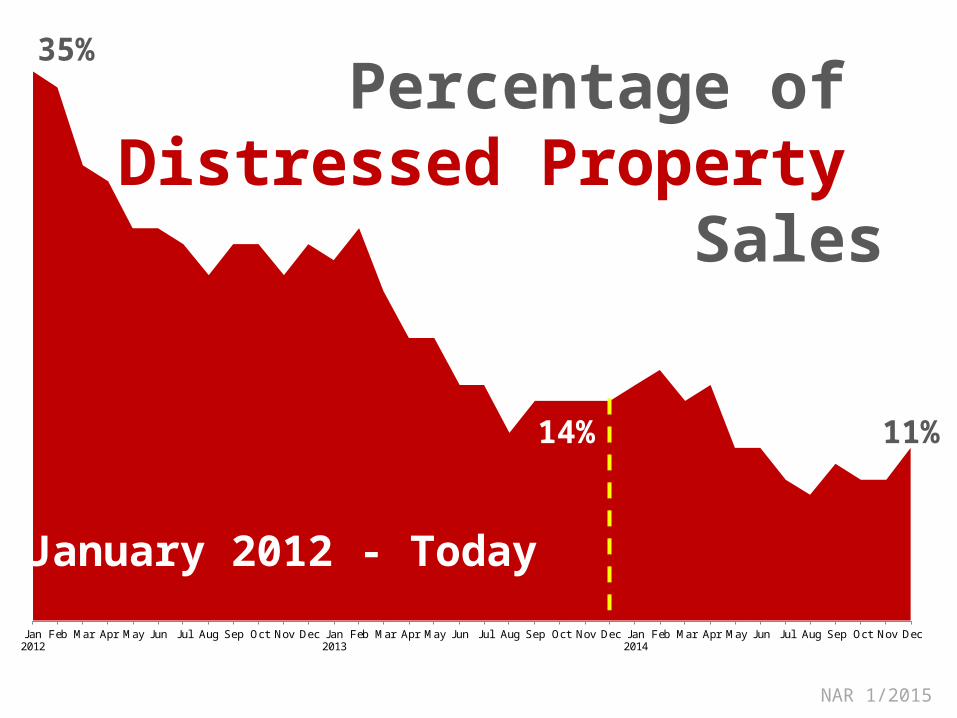

Percentage of Distressed Property

Sales

35%

11%14%

NAR 1/2015

January 2012 - Today

KEEPINGCURRENTMATTERS.COM

Slide Slide Title Link

4 Consumer Optimism http://www.sca.isr.umich.edu/tables.html

5 Household Formations https://ycharts.com/indicators/us_household_formation

6 FHA Savings http://economistsoutlook.blogs.realtor.org/2015/01/08/fha-lowers-pricing-to-reflect-less-risk/

7 NAR Quote http://economistsoutlook.blogs.realtor.org/2015/01/08/fha-lowers-pricing-to-reflect-less-risk/

8 Mortgage Credit Availability http://www.mba.org/ResearchandForecasts/MCAI.htm

9-12

Renters Planning on Buying, Views on Homeownership (financial & non financial), #1 Reason Won’t Buy

http://www.freddiemac.com/multifamily/pdf/mf_renter_profile.pdf

13 Impact on ‘Willingness To Pay’ http://www.newyorkfed.org/research/staff_reports/sr702.pdf

14 Down Payment Misconception http://www.freddiemac.com/news/blog/christina_boyle/20140616_mortgage_down_payments.html

15 Housing Wire Quote http://www.housingwire.com/blogs/1-rewired/post/30441-nomura-fear-is-keeping-demand-pent-up

16, 54 Julián Castro Quote http://portal.hud.gov/hudportal/HUD?src=/press/speeches_remarks_statements/2015/Statement_011315

18 Lawrence Yun Quote http://economistsoutlook.blogs.realtor.org/2015/01/26/shrinking-inventory/#sf7126105

19 Year-over-Year Inventory www.realtor.org

Resources

KEEPINGCURRENTMATTERS.COM

Slide Slide Title Link

20 Pent Up Seller Demand http://economistsoutlook.blogs.realtor.org/2015/01/28/pent-up-sellers/#sf7158951

21 Equity Share by State http://www.corelogic.com/about-us/researchtrends/equity-report.aspx

22-23, 24 Foot Traffic, Months Inventory www.realtor.org

25-26 Listings Come to Market 2014http://economistsoutlook.blogs.realtor.org/2015/01/14/ehs-in-2014-by-the-numbers-part-3-popular-listing-dates/ http://www.realtor.org/topics/existing-home-sales/data

28, 29, 30Sales by Price Range, Existing Home Sales, Pending Home Sales

www.realtor.org

31, 3330-Year Fixed Rate, Mortgage Rate Freddie Mac 2015

http://www.freddiemac.com/pmmshttp://www.freddiemac.com/finance/ehforecast.html

32 Mortgage Rate Projections

http://www.fanniemae.com/resources/file/research/emma/pdf/Housing_Forecast_012215.pdfhttp://www.freddiemac.com/finance/pdf/january_2015_public_outlook.pdfhttp://www.mortgagebankers.org/files/Bulletin/InternalResource/90432_.pdfhttp://www.realtor.org

34-36 Months Inventory for Sale http://www.realtor.org/

37, 38, 39 Case Shiller YOY & HPI http://us.spindices.com/index-family/real-estate/sp-case-shiller

40 % of Distressed Properties http://www.realtor.org/

52 NAR Membership http://www.realtor.org/membership/historic-report

53 Seth Godin Quote http://sethgodin.typepad.com/seths_blog/2015/01/you-are-what-you-share.html

Resources

JOIN THE KCM MEMBERS FACEBOOK GROUP

facebook.com/groups/kcmmembers

2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014

NAR Membership in thousands

NAR

"The culture we will live in next month is a direct result of what people like us share today. The things we share and don't share determine what happens next."

Seth Godin

"Homeownership is still the cornerstone of the American Dream — a fact you can see in the lives of everyday folks. It’s a source of pride. It’s a source of wealth, providing both a nest and a nest egg.

And it strengthens communities and fuels growth in the overall economy."

Julián Castro, Secretary for HUD

FEBRUARY 2015