february 22, 2001 alaskan pipeline meeting agenda introduction to enron & el paso assessing the...

TRANSCRIPT

February 22, 2001

Alaskan Pipeline Meeting

Agenda

Introduction to Enron & El Paso

Assessing the Alaskan Gas Impact

Enron & El Paso Value Added

Enron Overview

$74 Billion Corporation headquartered in Houston, Texas

Largest Wholesale Marketer of Natural Gas

Largest Wholesale Marketer of Electricity

Owner/Operator of Major US Natural Gas Pipelines

Northern Natural Gas

TransWestern Pipeline

Northern Border (operator/partial owner)

Florida Gas Transmission (operator/partial owner)

Bridgeline Holdings (partial owner)

Owner/Operator of Electric Generation Worldwide6000 MW in US

5400 MW internationally

Enron Interstate Pipelines

Transwestern

Northern Natural

Northern Border

Florida Gas

El Paso/Coastal Overview

Merger received FTC approval January 29, 2001

$50+ Billion Corporation headquartered in Houston, Texas

Largest U.S. Owner/Operator of Major InterstatesTennessee Gas Pipeline

ANR

El Paso Natural Gas

SONAT

Colorado Interstate

Florida Gas Transmission (partial owner)

Portland (partial owner)

Great Lakes (partial owner)

Alliance (partial owner)

Largest US Storage Owner/Operator

Second largest US Gas Wholesale Marketer

Current El Paso Interstate Pipelines

El PasoCoastal

Combined Enron and El PasoInterstate Pipelines

El PasoCoastalEnronEnron/El Paso

Enron & El Paso Combined Presence

Over 95,000 miles of pipe in U.S.

27 Bcf/d interstate transport

39 Bcf/d gas marketed in U.S.

10,700 MW of U.S. electric generation

757 MM MWhs marketed

615 Bcf of storage working gas

11 Bcf/d storage deliverability

Assessing the Alaskan Gas Impact

Current Forecasts

Big Bang Growth Case

Impact of Alaska Gas Arriving in 2010

Impact of Alaska Gas Arriving in 2007

2010 Demand Forecasts

(Tcf) GRI NPC Gov't* WEFA

US (incl exports to Mexico) 29.5 29.4 28.8 28.3

Canada 3.3 3.5 4.3 3.7

"North America" 32.8 32.9 33.1 32.0

Bcfd 89.9 90.1 90.7 87.7

* EIA's AEO 2001 and NEB's Supply/Demand to 2025

(Tcf) GRI NPC Gov't* WEFA

US (incl exports to Mexico) 29.5 29.4 28.8 28.3

Canada 3.3 3.5 4.3 3.7

"North America" 32.8 32.9 33.1 32.0

Bcfd 89.9 90.1 90.7 87.7

* EIA's AEO 2001 and NEB's Supply/Demand to 2025

Volatility in Forecasts

Forecasts for 2010

27.5

28.0

28.5

29.0

29.5

30.0

1997 1998 1999 2000 2001

Forecast Year

Tcf

EIA

GRI

U.S. Only

Forecasts for 2010

27.5

28.0

28.5

29.0

29.5

30.0

1997 1998 1999 2000 2001

Forecast Year

Tcf

EIA

GRI

U.S. Only

Forecasts for Electric Gen Growing

3400

3500

3600

3700

3800

3900

4000

4100

4200

4300

1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009

Forecast Year

Mil

lio

ns

of

MW

h

1991 1992

1993 1994

1995 1996

1997 1998

1999 2000

2001

U.S. Only

3400

3500

3600

3700

3800

3900

4000

4100

4200

4300

1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009

Forecast Year

Mil

lio

ns

of

MW

h

1991 1992

1993 1994

1995 1996

1997 1998

1999 2000

2001

U.S. Only

Source: NERC Load & Resource Reports

Big Bang Growth Case

EEA Model used as Base StructureEngine for GRI and Other Forecasts

1998 Base Data

North American PerspectiveUpdated Projections of Canadian Demand

Net Mexico Demand

Exogenous ModificationsLNG, Sable Island

Alaskan Supply

Unconstrained Supply

Big Bang Growth Case

23.2

26.5

9.9

7.20.1

29.2

32.8

24.2

9.61.0

1998 Growth 2010

Mexico

L, P & F

Electric

Industrial

R&C

96.8

66.9

6.3 / 1.9%

14.3 / 8.1%

.9 / >100%

Growth/CAGR29.9 / 3.0%

6.0 / 1.6%

2.4 / 2.5%

Bcfd

23.2

26.5

9.9

7.20.1

29.2

32.8

24.2

9.61.0

1998 Growth 2010

Mexico

L, P & F

Electric

Industrial

R&C

96.8

66.9

6.3 / 1.9%

14.3 / 8.1%

.9 / >100%

Growth/CAGR29.9 / 3.0%

6.0 / 1.6%

2.4 / 2.5%

Bcfd

U.S. GDP grows at 2.5% per year

North American electric demand grows at 1.9% per year

Industrial production grows at 3% per year

Canadian GDP grows at 3% per year through 2005,

then slows to 2% per year thereafter

Canadian Tar Sands production’s demand for gas grows to 1 Bcfd

by 2010

RACC declines to $22.58/bbl by end of 2002 and

grows at 1.5% per year (nominal) thereafter

Background Assumptions

Major Predictions

Coal generation capacity flat

Exports to Mexico grow to 1.0 Bcfd by 2005 and

remain flat thereafter

LNG imports exceed 3.5 Bcfd by 2010

Sable Island production up to 2 Bcfd by 2010

Major Projections

Gas grows at 3% per yearAlaska gas increases demand by 2.6 Bcfd (excluding LP&F impact)

Nominal prices at Henry Hub peak at $4.35 during the forecast period

$4.99

$3.65

$4.46

$3.60 $3.48

$2.76

$4.18 $4.28

$4.53

$5.18

$4.66

$2.00

$2.50

$3.00

$3.50

$4.00

$4.50

$5.00

$5.50

2001 2002 2003 2004 2005 2006 2007 2008 2009 2010

Henry Hub Chicago AECO-C

$4.99

$3.65

$4.46

$3.60 $3.48

$2.76

$4.18 $4.28

$4.53

$5.18

$4.66

$2.00

$2.50

$3.00

$3.50

$4.00

$4.50

$5.00

$5.50

2001 2002 2003 2004 2005 2006 2007 2008 2009 2010

Henry Hub Chicago AECO-C

Big Bang Demand Case

Tcf Bcfd

GRI 2000 Baseline 32.8 89.9

+ Exports to Mexico 0.1 0.4

+ Electric Growth 0.2 0.5

+ Canadian Demand 1.2 3.2

Big Bang Demand 34.3 93.9

+ Fuel Switching 0.9 2.6

+ Lease, Plant & Fuel 0.1 0.3

Big Bang Demand w/ Alaska 35.3 96.8

Tcf Bcfd

GRI 2000 Baseline 32.8 89.9

+ Exports to Mexico 0.1 0.4

+ Electric Growth 0.2 0.5

+ Canadian Demand 1.2 3.2

Big Bang Demand 34.3 93.9

+ Fuel Switching 0.9 2.6

+ Lease, Plant & Fuel 0.1 0.3

Big Bang Demand w/ Alaska 35.3 96.8

Mexico

2.7% AAGR in demand for natural

gas from 1991 to 1997

Total gas demand forecasted to

grow 5.3 Bcfd by 2008Annual growth rate exceeding 9%

Electric Sector expected to grow at a

rate exceeding 20% – 2.5 Bcfd 0

1000

2000

3000

4000

5000

6000

7000

8000

9000

10000

19

99

20

00

20

01

20

02

20

03

20

04

20

05

20

06

20

07

20

08

MMCFD

Residential and Transport

Industrial

Electric Sector

Oil and Petrochemical

0

1000

2000

3000

4000

5000

6000

7000

8000

9000

10000

19

99

20

00

20

01

20

02

20

03

20

04

20

05

20

06

20

07

20

08

MMCFD

Residential and Transport

Industrial

Electric Sector

Oil and Petrochemical

Source: Natural Gas Market Perspective 1999-2008, Ministry of Energy.

Race between gas infrastructure investment and electric

generation

Production estimated grow at 7%

rate1998 Production = 1.26 Tcf or 3.5 Bcfd

Over 78% located in southern regions

Mexico Will Continue toRely on Natural Gas Imports

Source: Natural Gas Market Perspective 1998-2007 & 1999-2008, Ministry of Energy.

Balance (supply less demand)M

MC

FD

Balance with investment Balance without investment

500

0

500

1000

1500

2000

2500

3000

3500

20

02

20

03

20

04

20

05

20

06

20

07

20

08

19

99

20

00

20

01

Mexico’s demand for U.S. gas modeled to grow to 1 Bcfd by

2005 and remain flat thereafter

U.S & Canadian ElectricLoad Growth

4,000

4,200

4,400

4,600

4,800

5,000

5,200

5,400

5,600

5,800

1999 2010

TWh

4,000

5,800

4,900

4,200

4,000

4,200

4,400

4,600

4,800

5,000

5,200

5,400

5,600

5,800

1999 2010

TWh

4,000

5,800

4,900

4,200

4,9339.0 / 24.7

3.9 / 10.7

Big BangTcf / Bcfd

Load Growth per NERC 2000 ES&D; Reliability Assessment

Base Projection 1.9% / yr

Upper Band 3.4% / y

r

Lower Band .4% / yr

Canadian Natural Gas Demandby 2010

Total Canadian demand in 1999 was 8.0 Bcfd

NEB forecasts consumption in 2010 at 4.3 Tcf or

11.8 BcfdAnnual GDP growth of 3% through 2005, decelerating to 2%

thereafter

40% of growth occurs in eastern provinces

(Ontario, Quebec and Maritimes)

Oil Sands production now estimated by NEB to

require 1 Bcfd of natural gas by 2010.6 Bcfd included in NEB June ’99 forecast

Sources: Statistics Canada websiteNEB, Canadian Energy, Supply & Demand to 2025; June 1999NEB, Canada’s Oil Sands; October 2000

Demand Response

29.2

32.6

21.9

9.3

1.0

29.2

32.8

24.2

9.61.0

2010 w/o Alaska Gas Demand Response 2010 w/ Alaska Gas

Mexico

L, P & F

Electric

Industrial

R&C

96.893.9

.3

2.3

.3

2.9

29.2

32.6

21.9

9.3

1.0

29.2

32.8

24.2

9.61.0

2010 w/o Alaska Gas Demand Response 2010 w/ Alaska Gas

Mexico

L, P & F

Electric

Industrial

R&C

96.893.9

.3

2.3

.3

2.9

Big Bang Supply in 2010

GRI Big

Bang

Lower 48 67.4 61.7

Alaska 1.8 5.5

WCSB 19.9 22.3

Eastern Canada 0.7 2.2

LNG 0.4 3.5

Storage, Balancing (0.3) 1.5

Big Bang Supply 90.0 96.7

BCFD

GRI Big

Bang

Lower 48 67.4 61.7

Alaska 1.8 5.5

WCSB 19.9 22.3

Eastern Canada 0.7 2.2

LNG 0.4 3.5

Storage, Balancing (0.3) 1.5

Big Bang Supply 90.0 96.7

BCFD

LNG

700 Tcf of Stranded Gas

Estimated worldwide LNG export capability in 2010 up to 12 Tcf

/ yr

LNG landed cost in U.S. $3.00 to $3.50 / MMBtu

U.S. LNG receiving terminals’ sendout capacityCurrent/ w/ Economically Big

Service Initial Expandable BangDate Capacity Capacity Flow

Distrigas Active 450 740 600

Cove Point Early 2002 1000 1800 1200

Elba Island Early 2002 540 790 600

CMS Trunkline Active 700 1200 800

Baja California 2005 700 700 350

Bahamas, Seattle, N Carolina . . . ???

LNG imports in 2010 will exceed 3.5 Bcfd

Sable Island

Sable Island production will reach 2.2 Bcfd by 2010

.2

.4.2.4

.2

.6

.2

.6

.2

.2

.7

.4

.2

.7

.8

1.0

2.2

0.0

0.5

1.0

1.5

2.0

2.5

Bcfd

2001 2002 2003 2004 2005 2006 2007 2010

Domestic Export Panuke

Ziff Energy Big Bang Case

.2

.4.2.4

.2

.6

.2

.6

.2

.2

.7

.4

.2

.7

.8

1.0

2.2

0.0

0.5

1.0

1.5

2.0

2.5

Bcfd

2001 2002 2003 2004 2005 2006 2007 2010

Domestic Export Panuke

Ziff Energy Big Bang Case

Snapshot of 35 Tcf

World in 2010

Excludes Lease, Plant & Fuel

Major Demand Growth (1998-2010)

8.212.4

4.2

Northeast

5.17.2

2.1

California

6.09.3

3.3

Canada

8.512.1

3.6

Midwest

3.66.7

3.1

Southeast

3.75.5

1.7

Central

14.517.1

2.6

WSC

59.786.3

26.6

Legend (Bcfd)

19

98

20

10

66.895.9

29.1

Legend (Bcfd)

19

98

20

10

Supply Response (1998 – 2010)

14.220.2

5.2

GOM

1.25.5 4.3

Alaska

12.815.6

2.9

Tx/La

16.6

22.3

5.8

WCSB

0.0 2.2 2.2

Maritimes

3.27.7

4.5

Rockies

0.23.2 3.0

LNG

0.0 0.4 0.4

LNG

Bcfd

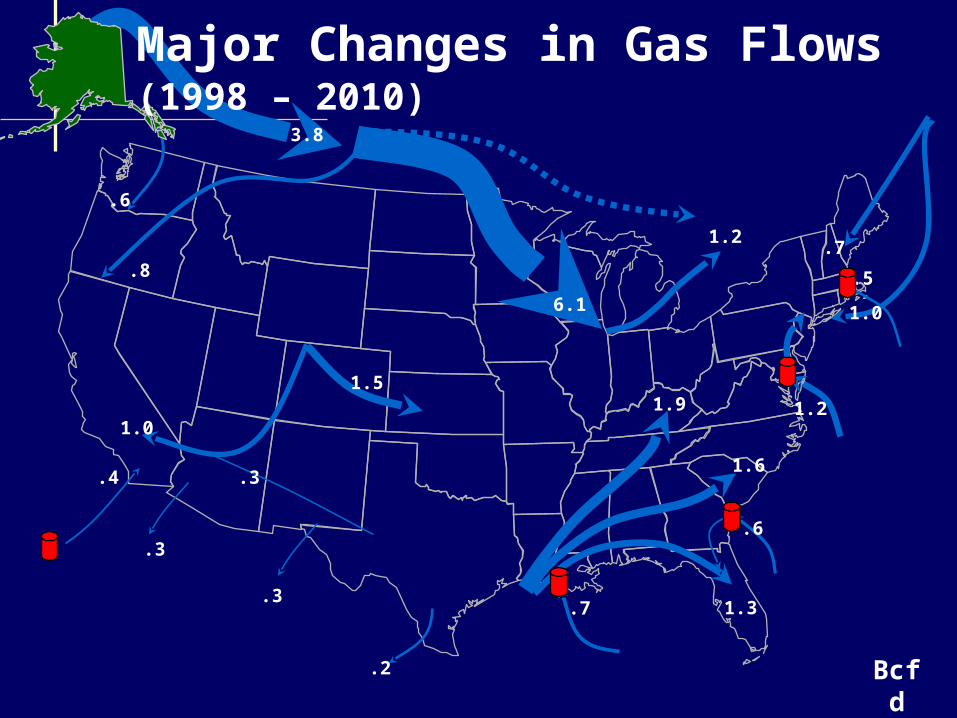

Major Changes in Gas Flows(1998 – 2010)

3.8

6.1

1.0

1.3

.7

1.0

1.6

1.9 1.2

.2

.3

1.2

1.5

.4

.7

.6

.8 .5

.6

.3

.3

Pipeline Infrastructure Required to Move 35 Tcf

4.0

1.1

1.3

.4

1.1

.8

1.2

.3

.5

1.0

1.1

.6

.5

.5

Offshore connections

.9

* Alliance capacity shown wet

.9

5.7 *

9.0

.9

1.5 * .7

.2

.7

2.5

NoCal3.35

AECO-C2.76

Chicago3.65

Henry3.65

Opal3.16

Gas PricesBasis

New York4.57

Gas Prices & Basis(35 Tcf in 2010 – Nominal $)

.49

.59 .89

.00.92

2009 2010 2009 2010

AECO-C 3.48 2.76 2.73 2.11

Chicago 4.66 3.65 3.65 2.79

Henry Hub 4.28 3.65 3.35 2.79

Nominal 1999$

2009 2010 2009 2010

AECO-C 3.48 2.76 2.73 2.11

Chicago 4.66 3.65 3.65 2.79

Henry Hub 4.28 3.65 3.35 2.79

Nominal 1999$

1.81

Impact of Alaskan Gas in 2010:35 Tcf Market

2.9 Bcfd Demand Response

$1.00 Temporary Depression in Chicago

Price

More Infrastructure Needed from Western

Canada to California and to Chicago1.8 Bcf to California

4.2 Bcf to Chicago

Impact of Alaskan Gas in 2007:33 Tcf Market

2.9 Bcfd Demand Response

Demand at 35 Tcf by 2010

$1.00 Temporary Depression in Chicago

Price

Recovers by 2010

More Infrastructure Needed from Western Canada

to California and to Chicago

1.3 Bcf to California

4.2 Bcf to Chicago

NoCal3.14

AECO-C2.73

Chicago3.26

Henry3.23

Opal2.41

New York5.08

Gas Prices & Basis(33 Tcf in 2007 – Nominal $)

.85

.41 .53

.031.85

2.35

Gas PricesBasis

2006 2007 2008 2010

AECO-C 3.42 2.73 2.90 3.45

Chicago 4.26 3.26 3.41 4.15

Henry Hub 3.94 3.23 3.40 4.15

2006 2007 2008 2010

AECO-C 3.42 2.73 2.90 3.45

Chicago 4.26 3.26 3.41 4.15

Henry Hub 3.94 3.23 3.40 4.15

Summary

Demand Will Follow Supply

Adequate Netback to Alaska

Significant “B to C” Infrastructure Needed

AECO Hub is Gateway to East / West Optionality

New York via TransCanada

Chicago via Alliance, Northern Border

California via PGT

Continuous Market Intelligence Critical Given

Dynamic Markets

El Paso and Enron

Value Added

Why are we Interested?

Strategic Focus on the North

Development of New Gas Supply

Increase clean BTU supplies to N. America

Allow market growth

Improve utilization of existing pipeline grid

Opportunities for New Investment

Significant N. American Pipeline Project

A Core Competency – “It’s What We Do For A

Living!”

How Can We Add Value?

U.S. Political/Regulatory Expertise

FERC

Environmental Agencies

Governmental Players

Successful Market Players

Trading/Marketing/Risk Management

Consumers - Power Plants (~13,000 MW/~2.2 Bcfd)

Enron currently owns 6000 MW in US

Market Access

Involved in all major U.S. markets

Excellent relationships with consumers

Owner of significant import capacity

How Can We Add Value?

EPC Expertise

Physical Operating Capability

Recognized “Best in Class”

Existing Infrastructure

Economies of Scale

Widely Respected “Industry Innovators”

Source of Equity

Management Commitment

Conclusions

Demand Will Be There IF Confidence in

Supply Maintained

Pricing Levels in 2007 – 2010 Appear to

Support Alaskan Gas

El Paso & Enron Can Supply Considerable

Pipeline & Market Expertise