federal fiscal compliance 101 texas education agency (tea)

TRANSCRIPT

Federal Fiscal Compliance 101

Texas Education Agency (TEA)

Major Federal Fiscal Compliance and Reporting Requirements

CEIS and MOE Voluntary Reduction Reporting

FFATA Reporting

Indirect Cost Rates

Title I, Part A Comparability

NCLB LEA MOE

IDEA-B LEA MOE

Special Education SSA Configuration Changes

Corrective Actions

Reports, Notifications and Submissions

GFFC Reports and Data Collections

TEAL/TEASE Application TEA Federal Compliance Determinations LEA responses to Federal Compliance

Determinations

Ensure appropriate LEA staff have access!

Reports, Notifications and Submissions

Grants and Federal Program Compliance (GAFPC) listervSign up for GAFPC at: http://miller.tea.state.tx.us/list/

Ensure appropriate LEA staff are subscribed to GAFPC!

CEIS and MOE Voluntary Reduction Reporting

Requirement

Report on applicable CEIS Set-Aside amounts, students served, and MOE Voluntary Reduction taken by LEA’s.

CEIS and MOE Voluntary Reduction Reporting

Common Errors to Avoid

CEIS Set-Aside amounts > 15%

MOE Voluntary Reduction > 50%

Combined, the CEIS Set-Aside and MOE Voluntary Reduction may not exceed lower of the two

CEIS and MOE Voluntary Reduction Reporting

Common Errors to Avoid (Continued)

CEIS Set-Aside yet no CEIS Students Served

CEIS Students Served yet no CEIS Set-Aside

Special Education Consolidated Grant Application is not amended for CEIS Set-Aside changes

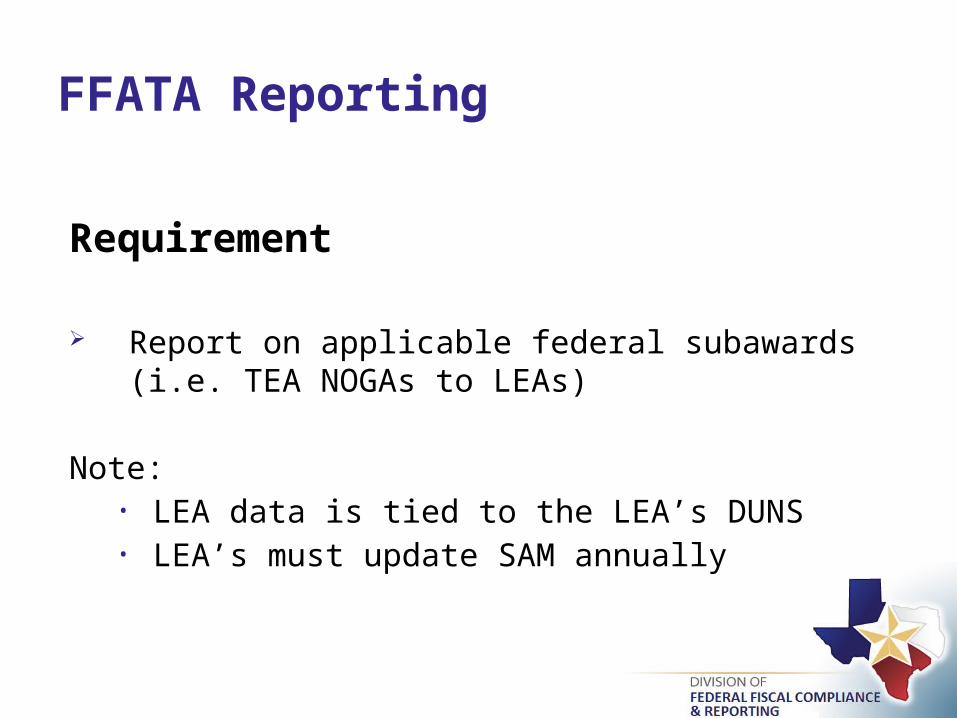

FFATA Reporting

Requirement

Report on applicable federal subawards (i.e. TEA NOGAs to LEAs)

Note:• LEA data is tied to the LEA’s DUNS• LEA’s must update SAM annually

FFATA Reporting

Common Errors to Avoid

Incorrect 9-digit zip code for the physical address in SAM

Outdated address or business contact information in AskTED

Incorrect DUNS on file at TEA

Indirect Cost Rates

Request Rate Via Annual Submission

ISDs – Exhibit J-2 of AFR (electronic submission)

Open-enrollment Charter – eGrant Special Collection SC5010

ESCs/Other Governmental Agencies – Indirect Cost Rate Proposal submitted directly to TEA

LEA may apply its Indirect Cost Rate if allowable by the grant

The indirect cost rate cap may be less than the LEA’s approved Indirect Cost Rate

Administrative caps may limit the amount of indirect costs recovered

Application of Indirect Cost Rates

Application of Indirect Cost Rates

Common Errors to Avoid

The indirect cost recovery is calculated when the LEA submits the final expenditure report

If the LEA has requested reimbursement in excess of the allowable indirect costs on its periodic expenditure reports, a refund due will be generated

Title I, Part A Comparability

Requirement

LEAs required to annually submit Comparability Computation Form and Comparability Assurance Document using GFFC Reports and Data Collections

Submissions due November 12th

Title I, Part A Comparability

Common Errors to Avoid

Misclassification of Campus (either Title/Skipped or Non-Title)

Not reporting EE and/or PK campuses in Elementary Grade-span group

Not demonstrating compliance with one test for all grade-span groupings tested

Title I, Part A Comparability

Common Errors to Avoid (Continued)

Subdividing Grade-span into High/Low enrollment and not meeting Significant Difference of Enrollment criteria

Uploading Comparability Computation Form as a PDF rather than Excel as required

Uploading Comparability Assurance Document without Superintendent Signature as required

NCLB LEA MOE

Requirement

Determine LEA compliance with NCLB Maintenance of Effort (MOE)

Applies to LEAs receiving federal funds under covered NCLB (ESEA) programs

NCLB LEA MOE

Common Misconceptions

MYTH: Similar to IDEA-B LEA MOE, there are federal statutory exceptions to NCLB LEA MOE.

TRUTH: There are no federal statutory exceptions.

MYTH: TEA has authority to waive penalty for noncompliance.

TRUTH: Only USDE has authority to waive penalty.

NCLB LEA MOE

Common Misconceptions

MYTH: Receipt of USDE waiver constitutes compliance with requirement.

TRUTH: Final Determinations DO NOT change; only the penalty is waived.

MYTH: Penalty only impacts only Title I, Part A. TRUTH: Noncompliance impacts all covered programs.

IDEA-B LEA Eligibility

Requirement

LEA must certify it has budgeted in the current year an amount greater than or equal to the amount required to meet the MOE requirement.

Applies to LEAs receiving federal funds under an IDEA-B formula grant

Special Education Consolidated Grant Application

Schedule BS6006 - Fiscal Compliance Requirements

Part 1: LEA MOE Eligibility

Part 2: CEIS Set-Aside and MOE Voluntary Reduction Amount

IDEA-B LEA MOE

Requirement

Determine LEA compliance with IDEA-B Maintenance of Effort (MOE)

Applies to LEAs receiving federal funds under an IDEA-B formula grant

IDEA-B LEA MOE

2014 Updates to IDEA-B LEA MOE Handbook

SHARS Medicaid Cost Share is not included in the IDEA-B LEA MOE calculation

Exceptionally Costly Program is defined as amount greater than the average per-pupil (as defined in Section 9101 of ESEA)

IDEA-B LEA MOE

Fiscal Agents and Member Districts

TEA has no authority to resolve SSA disputes

Member Districts must contact their Fiscal Agent for amounts reported on their behalf

State Reconsideration for Significant PEIMS Errors

Special Education Shared Services Arrangement (SSA) Configuration Changes

Requirement

LEA must notify TEA of configuration changes annually by February 1st

LEA must submit the new SSA Contracts annually by June 1st

Requirement

LEA may owe a refund to TEA from a federal finding in an audit

LEA may have required corrective actions from a federal finding in an audit

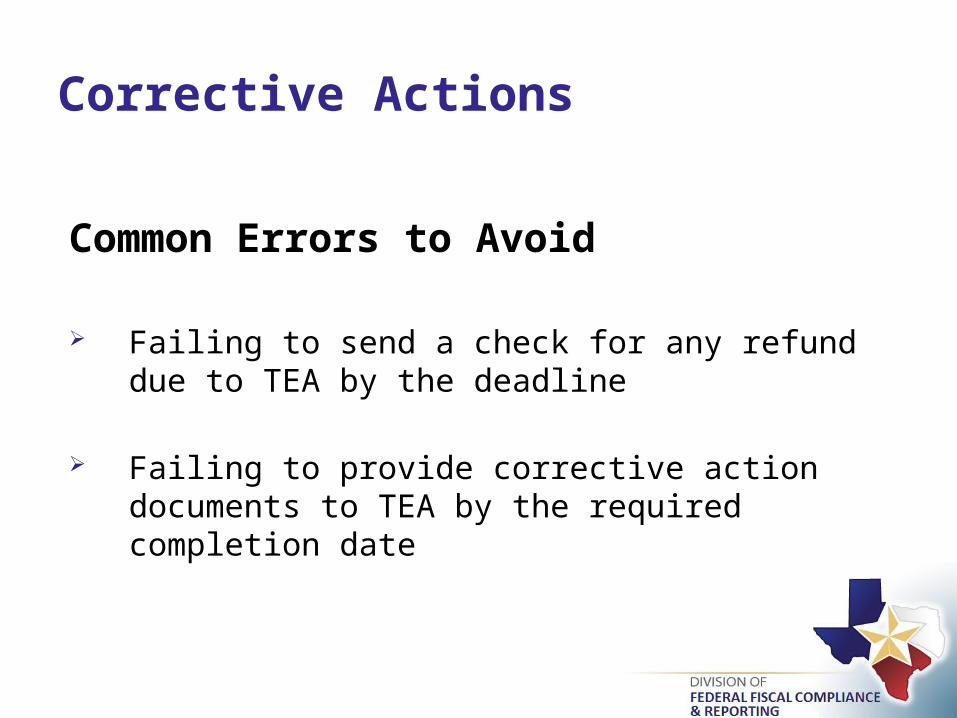

Corrective Actions

Corrective Actions

Common Errors to Avoid

Failing to send a check for any refund due to TEA by the deadline

Failing to provide corrective action documents to TEA by the required completion date

Visit the FFCR website:http://

www.tea.state.tx.us/index4.aspx?id=2147505847

For questions, please send an email to:

Additional Questions?