federal reserve's second monetary policy report, hearing before

TRANSCRIPT

FEBERAL RESERVE'S SECOND MONETARYPOLICY REPORT FOR 1982

HEARINGSBEFORE THE

COMMITTEE ONBANKING, HOUSING, AND URBAN AFFAIRS

UNITED STATES SENATENINETY-SEVENTH CONGRESS

SECOND SESSION

ON

OVERSIGHT ON THE MIDYEAR MONETARY POLICY REPORT TOCONGRESS PURSUANT TO THE FULL EMPLOYMENT AND BAL-

ANCED GROWTH ACT OF 1978

JULY 20, 21, AND 27, 1982

Printed for the use of the Committee on Banking, Housing, and Urban Affairs

[97-68]

U.S. GOVERNMENT PRINTING OFFICE

WASHINGTON: 1982

Digitized for FRASER http://fraser.stlouisfed.org/ Federal Reserve Bank of St. Louis

COMMITTEE ON BANKING, HOUSING, AND URBAN AFFAIRS

JAKE GARN, Utah, ChairmanJOHN TOWER, TexasJOHN HEINZ, PennsylvaniaWILLIAM L. ARMSTRONG, ColoradoRICHARD G. LUGAR, IndianaALFONSE M. D'AMATO, New YorkJOHN H. CHAFEE, Rhode IslandHARRISON "JACK" SCHMITT, New MexicoNICHOLAS F. BRADY, New Jersey

M. DANNY WALL, Staff DirectorROBERT W. RUSSELL, Minority Staff Director

W. LAMAR SMITH, Economist

DONALD W. RIEGLE, JR., MichiganWILLIAM PROXMIRE, WisconsinALAN CRANSTON, CaliforniaPAUL S. SARBANES, MarylandCHRISTOPHER J. DODD, ConnecticutALAN J. DIXON, IllinoisJIM SASSER, Tennessee

(H)

Digitized for FRASER http://fraser.stlouisfed.org/ Federal Reserve Bank of St. Louis

C O N T E N T S

TUESDAY, JULY 20, 1982

Pa«e

Opening statement of Chairman Garn 1Opening statements of:

Senator Riegle 2Senator Tower 'S3Senator Sasser 34Senator Schmitt 34

WITNESS

Paul A. Volcker, Chairman, Board o!' Governors of the Federal ReserveSystem 4

Monetary and credit targets 6Blend of monetary and fiscal policy 10Concluding' comments 11Midyear monetary policy report to Congress 14Answers to subsequent written questions of Senator Schmitt 79

Panel discussion:Congress blamed 35Failure to meet target growth 36Need for major change in policy mix 38Flight of money to short-term securities 41Effect of unregulated money market funds 42Turned the corner on inflation 44Ideas to change budget process 46Poor economy causes large lasting deficits 48Economic recovery predicted 49Constitutional amendment 50Impact of Government borrowing 53Huge short-term borrowing 53Administration supportive of present monetary policy 55Possibilities of lower interest rates 57Monetary policy counterproductive 58Amendment for national economic emergencies 60Small business bankruptcies 63Interest rates continue to rise 64Pressure on monetary policy 65Same debates and arguments 67Administration to stand pat on economic policy 70Fed response to sinking economy 72Record borrowing by the Treasury 74Cutting taxes 77Rash of farm foreclosures 78Investors sitting on short-term money 78

WEDNESDAY, JULY 21, 1982

WITNESSES

Murray L. Weidenbaum, Chairman, Council of Economic Advisers 83Prepared statement 85

Selecting a definition of money 85

Digitized for FRASER http://fraser.stlouisfed.org/ Federal Reserve Bank of St. Louis

IV

Murray L. Weidenbaum, Chairman, Council of Economic Advisers—Contin-ued

Prepared statement—Continued Pa»?pSetting and achieving monetary growth targets 89Variability of money growth 94Improved monetary control 98Conclusion 99Table 1—Composition of M, 87Figure 1—Income velocity of money 92

Panel discussion:Budget predictions constantly underestimated 100Serious economic conditions 102Difficult times are behind us 104Time is running out 104Recession bottomed out 106Trillion dollar debt 107Reduction of money supply 110Grant item veto power to the President 112Targeting interest rates 113Housing bill vetoed 125Bailout approach 116Characterizing Fed's monetary policy 118Discount rate lowered 119Foreign economic growth 122Frustration of politics 126Letter to Senator Sarbanes regarding the growth of money and its veloc-

ity in Germany and Japan compared to the United States 128Midcourse correction in economic policy 128

Donald E. Maude, Chief Financial Economist and Chairman, Interest RatePolicy Committee, Financial Economic Research Department, MerrillLynch, Pierce, Fenner & Smith, New York, N.Y 132

Prepared statement 133The setting 134Possible reconciliation 135Monthly changes in Mm 138M2 Growth 140Monetary policy conduct considerations 141Remarks 143Weekly credit market bulletins • 152Credit Market Digest 158

Serious contradictions 165M2 growing above targets 167Eliminate "base drift" 168

Leif H. Olsen, Chairman, Economic Policy Committee, Citibank, N.A., NewYork, N.Y 169

Prepared statement 170Panel discussion:

Contemporaneous reserve adjustment 176Federal deficits 177Balancing the budget 179Social security problem 181

TUESDAY, JULY 27, 1982

WITNESSES

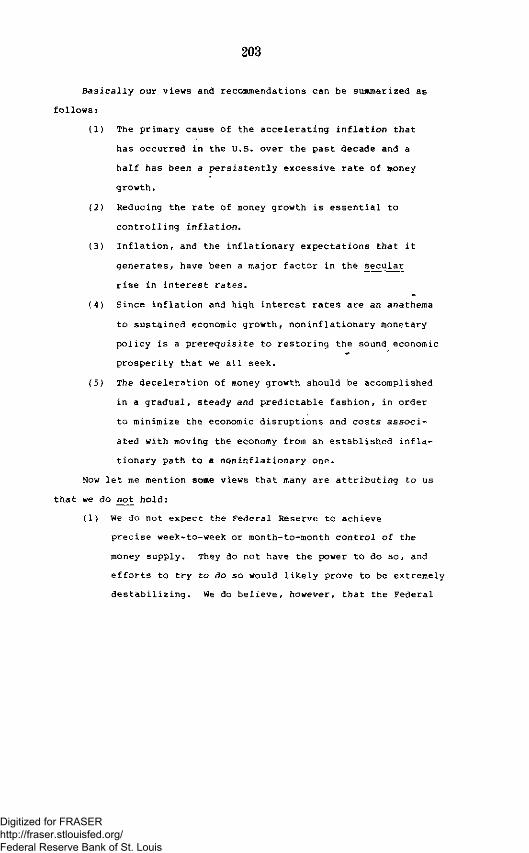

Beryl W. Sprinkel, Under Secretary of the Treasury for Monetary Affairs 183Views and recommendations 184Gradual deceleration of money growth 185Summary of study titled "The Effect of Volatile Money Growth on Inter-

est Rates and Economic Activity" 189Curb excessive Government spending 200Prepared statement 202

Summary 212Chart I—Growth in nominal GNP and adjusted monetary growth 214Chart II—Growth in Mi and the monetary base 215Chart III—Short-term monetary growth and short-term interest

rates 216

Digitized for FRASER http://fraser.stlouisfed.org/ Federal Reserve Bank of St. Louis

V

Beryl W. Sprinkel, Under Secretary of trie Treasury for Monetary Affairs—Continued Paw

Predicting monetary growth 217Federal Reserve targets 21!)Continuous deficit 219Good prospects for a recovery 222Subsequent additional statement on alternative ways to reduce interest

rates 224Steven M. Roberts, Director, Government Affairs, American Express Co 225

Monetary and fiscal policies 225Recommendations 226Prepared statement 227

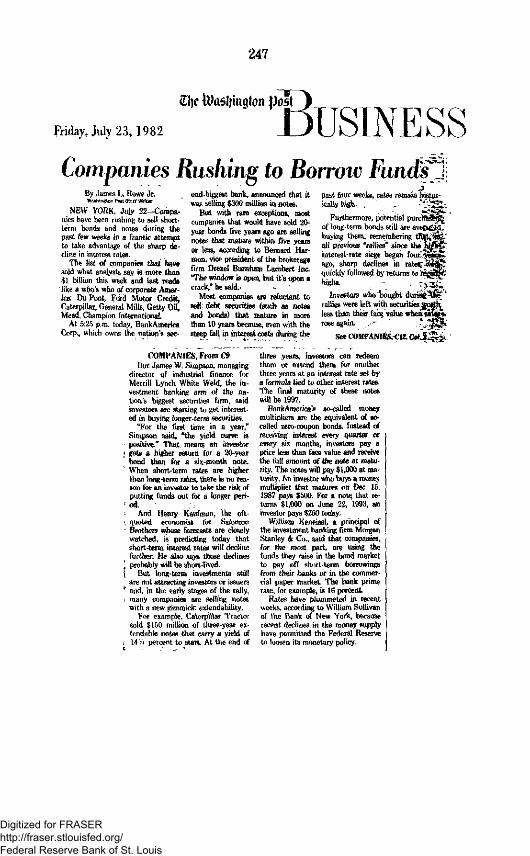

Newspaper article from the Washington Post entitled, "CompaniesRushing to Borrow Funds" 247

Testimony of Benjamin M. Friedman, professor of economics, Har-vard University, before the House Committee on Banking, Financeand Urban Affairs 248

Proposal for fiscal responsibility and lower interest rates 262Proposed joint resolution to reduce total Federal outlays as a share oi'

GNP 269Analysis of the proposed joint resolution 270

Controlling total net credit 271Comparing M, after 5 years 272Adjusting prime rates to cost of funds 273Problem controlling target for Mi 275Answers to subsequent written questions of Senator Riegle 278Reprint of paper by Alan Reynolds titled "The Trouble With Monetar-

ism" 282

ADDITIONAL MATERIAL RECEIVED FOR THE RECORD

Statement by Jack Carlson, vice president and chief economist, NationalAssociation of Realtors 306

Digitized for FRASER http://fraser.stlouisfed.org/ Federal Reserve Bank of St. Louis

Digitized for FRASER http://fraser.stlouisfed.org/ Federal Reserve Bank of St. Louis

FEDERAL RESERVE'S SECOND MONETARYPOLICY REPORT FOR 1982

TUESDAY, JULY 20, 1982

U.S. SENATE,COMMITTEE ON BANKING, HOUSING, AND URBAN AFFAIRS,

Washington, D.C.The committee met at 9:30 a.m. in room 5302 of the Dirksen

Senate Office Building, Senator Jake Garn (chairman of the com-mittee) presiding.

Present: Senators Garn, Tower, Lugar, Chafee, Schmitt, Brady,Riegle, Proxmire, Cranston, Sarbanes, Dixon, and Sasser.

The CHAIRMAN. The Banking Committee will come to order.Chairman Volcker, we are happy to have you with us this morn-

ing, to hear your report on monetary policy. I hope that we will beable to have a discussion with members of the Banking Committeethat avoids a lot of rhetoric, as we discuss the current condition ofthe U.S. economy, together with the appropriateness of recent pros-pective monetary policies.

To have a constructive discussion, we must not ignore the veryreal economic challenges that we face. Constructive discussion,however, will also require that we not ignore the equally real prog-ress that has been made since we began our efforts to slow infla-tion and curtail the government's growth rate—less than 19months ago.

Mr. Chairman, in the interest of time—we came to hear youtoday—and I would put the balance of my comments in the record,and turn to Senator Riegle for any comments that he might havebefore you begin, and then to Senator Dixon.

OPENING STATEMENT OF CHAIRMAN GARN

The CHAIRMAN. I hope that we will be able to avoid rhetoric thismorning as we discuss the current condition of the U.S. economytogether with the appropriateness of recent and prospective mone-tary policy. To have a constructive discussion, we must not ignorethe very real economic challenges we face. A constructive discus-sion, however, will also require that we will also require that wenot ignore the equally real progress that has been made since webegan our efforts to slow inflation and curtail government's growthrate less than 19 months ago.

Certainly, our greatest success has been in combatting what wasacknowledged to be our country's No. 1 economic problem whenRonald Reagan was elected President. During the 6 months priorto his inauguration, consumer prices rose at a 10.3-percent annual

(i)

Digitized for FRASER http://fraser.stlouisfed.org/ Federal Reserve Bank of St. Louis

rate. Over the last 6 months, consumer prices have risen at anannual rate of only 3.7 percent.

By holding firm to a commitment to gradually slow the mone-tary aggregates' growth rate, the Federal Reserve has played a cen-tral role in the successful fight against inflation.

With inflation down, our greatest current challenge is to hastena decline in interest rates so that the job-creating potential of oureconomy can be released.

Today I applaud the Federal Reserve's commitment to removingmoney-growth volatility as a contributor to high rates, as evidencedby your decision to try to use contemporaneous reserve accountingto improve your short-term control over the aggregates.

Nevertheless, I remain convinced that it is the Congress that isprimarily to blame for the failure of interest rates to decline asquickly as inflation. The first budget resolution which we recentlypassed calls for steadily declining Federal deficit in the yearsahead: $104 billion in fiscal year 1983; $84 billion in fiscal year1984; and $60 billion in fiscal year 1985.

But of the $281 billion in spending cuts that will be necessaryover the next 3 years to achieve these declining deficits, only $27billion—less than 10 percent—have been reconciled or enacted intolaw.

Is it any wonder that the financial markets have remained skep-tical—as evidenced by the stickiness of interest rates—of Congressability to make the budget cuts called for in the budget resolution?

Still, I began this statement with a call for a constructive discus-sion, one that acknowledges accomplishments as well as remainingproblems. In this spirit, we must acknowledge that an importantstart has been made toward lowering interest rates.

In the 4 years before Ronald Reagan began charting a new eco-nomic future, rates rose steadily. From an average of only 4.4 per-cent in December 1976, the yield on 3-month Treasury bills rose to:6.1 percent in December 1977; 9.1 percent in December 1978; 12.1percent in December 1979; and 15.7 percent in December 1980.

Yesterday that rate had come back down to just over 11 percent.Similarly, while the prime rate has not declined nearly enough, itis down substantially from the 21.5 percent Ronald Reagan inherit-ed.

From much of what you hear and read today, you might thinkrates were up—instead of down—from where they were 19 monthsago.

In conclusion, I again call for a discussion that does not fail toconfront problems head-on and also does not fail to give creditwhere credit is due.

OPENING STATEMENT OF SENATOR RIEGLESenator RIEGLE. Thank you, Mr. Chairman.Mr. Volcker, it's good to have you back before the committee

today.As I have had the chance to talk with leading financial and eco-

nomic people across the country, business people, labor people, andcitizens at the grassroots level, it's clear from everything I amhearing that the economy is in very, very serious trouble.

Digitized for FRASER http://fraser.stlouisfed.org/ Federal Reserve Bank of St. Louis

If I were to try to assess the bottom line, of what I'm hearingfrom this cross-section of opinion in the country, it is that the coun-try now, economically, seems to be on a disaster course, unlessmajor changes are made, unless the Federal deficits come down,and come down substantially, unless the interest rates come down,and come down substantially and stay down for a period of time;that unless these things are done, we are going to find ourselves ina situation where unemployment will go higher, the rate of bank-ruptcies—which is running at 550 firms a week—would likely gohigher.

We've got a number of interest rate-sensitive sectors of the econ-omy in terrible difficulty. Certainly the savings and loan industryis in that situation. Agriculture and farming are increasingly inthat situation. The auto industry is at less than 50 percent of ca-pacity operation. The steel industry is running at about 40 percentof capacity. The construction and the real estate industries are dev-astated.

The headline today, on the front of the business section of theWashington Post, indicates that housing starts declined 15.3 per-cent from May—and we're now facing the worst year for housingin the United States since World War II.

Capital investment plans have dropped off.If we consider all of this information, it shows that we are really

in extremely serious trouble. The question is: How are we going tochange this?

What is the Fed doing to change it?What are you saying in your conversations with the President?What is his response to you?Are we going to be able to get these rates down?Are they going to come down soon?Will they come down enough to make a difference?And if not, then what is our contingency plan?If we stay on this course and the damage and the destruction and

the hardship continue to accumulate, then the question is: How dowe propose to treat those problems, which are mounting every day,in every place that we look?

We have over 10.5 million people out of work in the country; andthat does not count another IVfe million that are no longer includedin the statistics because they have lost their unemployment bene-fits.

So, the situation is really at a desperate point. I'm going to bevery interested to hear both your assessment of the seriousness ofthe problem and how you feel that the Fed and the rest of us canchange these policies and improve the picture as it now appears.

The CHAIRMAN. Senator Brady, do you have any comments youwish to make?

Senator BRADY. No comments, thank you, Mr. Chairman.The CHAIRMAN. Senator Dixon.Senator DIXON. Mr. Chairman, I will make my statement after

the witness has concluded.The CHAIRMAN. Chairman Volcker, it is yours.

Digitized for FRASER http://fraser.stlouisfed.org/ Federal Reserve Bank of St. Louis

STATEMENT OF PAUL A. VOLCKER, CHAIRMAN, BOARD OFGOVERNORS OF THE FEDERAL RESERVE SYSTEM

Mr. VOLCKER. Mr. Chairman, I am pleased to have this opportu-nity once again to discuss monetary policy with you, within thecontext of recent and prospective economic developments.

As usual on these occasions, you have the Board of Governors'Humphrey-Hawkins report before you. This morning I want to en-large upon some aspects of that report and amplify as fully as I canmy thinking with respect to the period ahead.

In assessing the current economic situation, I believe the com-ments I made 5 months ago remain relevant. Without repeatingthat analysis in detail, I would emphasize that we stand at an im-portant crossroads for the economy and economic policy.

In these past 2 years, we have traveled a considerable waytoward reversing the inflationary trend of the previous decade ormore.

I would recall to you that, by the late 1970's, that trend hadshown every sign of feeding upon itself and tending to accelerate tothe point where it threatened to undermine the foundations of oureconomy. Dealing with inflation was accepted as a top national pri-ority, and, as events developed, that task fell almost entirely tomonetary policy.

In the best of circumstances, changing entrenched patterns of in-flationary behavior and expectations—in financial markets, in thepractices of business and financial institutions, and in labor negoti-ations—is a difficult and potentially painful process. Those, con-sciously or not, who have come to bet on rising prices and theready availability of relatively cheap credit to mask the risks ofrising costs, poor productivity, aggressive lending, or overextendedfinancial positions, have found themselves in a particularly diffi-cult position.

The pressures on financial markets and interest rates have beenaggravated by concern's over prospective huge volumes of Treasuryfinancing, and by the need of some businesses to borrow at a timeof a severe squeeze on profits. Lags in the adjustment of nominalwages and other costs to the prospects for sharply reduced inflationare perhaps inevitable, but have the effect of prolonging the pres-sure on profits—and indirectly on financial markets and employ-ment.

Remaining doubts and skepticism that public policy will carrythrough on the effort to restore stability also affect interest rates,perhaps most particularly in the longer term markets.

In fact, the evidence now seems to me strong that the inflation-ary tide has turned in a fundamental way. In stating that, I do notrely entirely on the exceptionally favorable consumer and producerprice data thus far this year, when the recorded rates of price in-crease, at annual rates, declined to SMj and 2V2 percent, respective-ly. That apparent improvement was magnified by some factorslikely to prove temporary, including, of course, the intensity of therecession; those price indexes are likely to appear somewhat lessfavorable in the second half of the year.

What seems to me more important for the longer run is that thetrend of underlying costs and nominal wages has begun to move

Digitized for FRASER http://fraser.stlouisfed.org/ Federal Reserve Bank of St. Louis

lower, and that trend should be sustainable as the economy recov-ers upward momentum. While less easy to identify—labor produc-tivity typically does poorly during periods of business decline—there are encouraging signs that both management and workersare giving more intense attention to the effort to improve produc-tivity. That effort should pay off in a period of business expansion,helping to hold down costs and encouraging a revival of profits, set-ting the stage for the sustained growth in real income we want.

I am acutely aware that these gains against inflation have beenachieved in a context of serious recession. Millions of workers areunemployed, many businesses are hard pressed to maintain profit-ability, and business bankruptcies are at a postwar high.

While it is true that some of the hardship can reasonably betraced to mistakes in management or personal judgment, includingpresumptions that inflation would continue, large areas of thecountry and sectors of the economy have been swept up in moregeneralized difficulty. Our financial system has great strength andresiliency, but particular points of strain have been evident.

Quite obviously, a successful program to deal with inflation, withproductivity, and with the other economic and social problems weface cannot be built on a crumbling foundation of continuing reces-sion. As you know, there have been some indications—most broadlyreflected in the rough stability of the real GNP in the second quar-ter and small increases in the leading indicators—that the down-ward adjustments may be drawing to a close. The tax reduction ef-fective July 1, higher social security payments, rising defensespending and orders, and the reductions in inventory alreadyachieved, all tend to support the generally held view among econo-mists that some recovery is likely in the second half of the year.

I am also conscious of the fact that the leveling off of the GNPhas masked continuing weakness in important sectors of the econo-my. In its early stages, the prospective recovery must be led largelyby consumer spending. But to be sustained over time, and to sup-port continuing growth in productivity and living standards, moreinvestment will be necessary.

At present, as you know, business investment is moving lower.House building has remained at depressed levels; despite somesmall gains in starts during the spring, the cyclical strengthnormal in that industry in the early stages of recovery is lacking.Exports have been adversely affected by the relative strength ofthe dollar in exchange markets.

I must also emphasize that the current problems of the Ameri-can economy have strong parallels abroad. Governments aroundthe world have faced, in greater or lesser degree, both inflationaryand fiscal problems. As they have come to grips with those prob-lems, growth has been slow or nonexistent, and the recessionarytendencies in various countries have fed back, one on another.

In sum, we are in a situation that obviously warrants concern,but also has great opportunities. Those opportunities lie in majorpart in achieving lasting progress—in pinning down and extendingwhat has already been achieved—toward price stability. In doingso, we will be laying the base for sustaining recovery over manyyears ahead, and for much lower interest rates, even as the econo-my grows.

Digitized for FRASER http://fraser.stlouisfed.org/ Federal Reserve Bank of St. Louis

6

Conversely, to fail in that task now, when so much headway hasbeen made, could only greatly complicate the problems of the econ-omy over time. I find it difficult to suggest when and how a credi-ble attack could be renewed on inflation should we neglect complet-ing the job now. Certainly the doubts and skepticism about our ca-pacity to deal with inflation—which now seems to be yielding—would be amplified, with unfortunate consequences for financialmarkets and ultimately for the economy.

I am certain that many of the questions, concerns, and dangersin your mind lie in the short run—and that those in good part re-volve around the pressures in financial markets. Can we look for-ward to lower interest rates to support the expansion in invest-ment and housing as the recovery takes hold? Is there, in fact,enough liquidity in the economy to support expansion—but not somuch that inflation is reignited? Will, in fact, the economy followthe recovery path so widely forecast in coming months?

These are the' questions that we in the Federal Reserve mustdeal with in setting monetary policy. As we approach these policydecisions, we are particularly conscious of the fact that monetarypolicy, however important, is only one instrument of economicpolicy. Success in reaching our common objective of a strong andprosperous economy depends upon more than appropriate mone-tary policies, and I will touch this morning on what seems to meappropriately complementary policies in the public and private sec-tors.

THE MONETARY TARGETS

Five months ago, in presenting our monetary and credit targetsfor 1982, I noted some unusual factors could be at work tending toincrease the desire of individuals and businesses to hold assets inthe relatively liquid forms encompassed in the various definitionsof money. Partly for that reason—and recognizing that the conven-tional base for the Mi target of the fourth quarter of 1981 was rela-tively low—I indicated that the Federal Open Market Committeecontemplated growth toward the upper ends of the specifiedranges. Given the bulge early in the year in Mi, the committee alsocontemplated that that particular measure of money might forsome months remain above a straight line projection of the target-ed range from the fourth quarter of 1981 to the fourth quarter of1982.

As events developed, Mi and M2 both remained somewhat abovestraight line paths until very recently. M3 and bank credit have re-mained generally within the indicated range, although close to theupper ends. See table I. Taking the latest full month of June, Migrew 5.6 percent from the base period and M2 9.4 percent, close tothe top of the ranges. To the second quarter as a whole, the growthwas higher, at 6.8 and 9.7 percent, respectively. Looked at on ayear-over-year basis, which appropriately tends to average throughvolatile monthly and quarterly figures, Mi during the first half of1982 averaged about 43A percent above the first half of 1981, afteraccounting for NOW account shifts early last year. On the samebasis, Mz and M3 grew by 9.7 and 10.5 percent, respectively, a rate

Digitized for FRASER http://fraser.stlouisfed.org/ Federal Reserve Bank of St. Louis

of growth distinctly faster than the nominal GNP over the sameinterval.

In conducting policy during this period, the committee was sensi-tive to indications that the desire of individuals and others for li-quidity was unusually high, apparently reflecting concerns and un-certainties about the business and financial situation. One reflec-tion of that may be found in unusually large declines in velocityover the period—that is, the ratio of measures of money to thegross national product. Mi velocity—particularly for periods asshort as 3 to 6 months—is historically volatile. A cyclical tendencyto slow, relative to its upward trend, during recessions is common.But an actual decline for two consecutive quarters, as happenedlate in 1981 and the first quarter of 1982, is rather unusual. Themagnitude of the decline during the first quarter was larger thanin any quarter of the entire postwar period. Moreover, declines invelocity of this magnitude and duration are often accompanied by,and are related to, reduced short-term interest rates. Those interestrate levels during the first half of 1982 were distinctly lower thanduring much of 1980 and 1981, but they rose above the levelsreached in the closing months of last year.

More direct evidence of the desire for liquidity or precautionarybalances affecting Mi can be found in the behavior of NOW ac-counts. As you know, NOW accounts are a relatively new instru-ment, and we have no experience of behavior over the course of afull business cycle. We do know that NOW accounts are essentiallyconfined to individuals, their turnover relative to demand accountsis relatively low, and, from the standpoint of the owner, they havesome of the characteristics of savings deposits, including a similar-ly low interest rate but easy access on demand. We also know thegreat bulk of the increase in Mi during the early part of the year—almost 90 percent of the rise from the fourth quarter of 1981 to thesecond quarter of 1982—was concentrated in NOW accounts, eventhough only about one-fifth of total Mi is held in that form. In con-trast to the steep downward trend in low-interest savings accountsin recent years, savings account holdings have stabilized or evenincreased in 1982, suggesting the importance of a high degree of li-quidity to many individuals in allocating their funds. A similartendency to hold more savings deposits has been observed in earlierrecessions.

I would add that the financial and liquidity positions of thehousehold sector of the economy, as measured by conventionalliquid asset and debt ratios, has improved during the recessionperiod. Relative to income, debt repayment burdens have declinedto the lowest level since 1976. Trends among business firms areclearly mixed. While many individual firms are under strong pres-sure, some rise in liquid asset holdings for the corporate sector as awhole appears to be developing. The gap between internal cashflow—that is, retained earnings and depreciation allowances—andspending for plant, equipment, and inventory has also been at ahistorically low level, suggesting that a portion of recent businesscredit demands is designed to bolster liquidity. But, for many yearsbusiness liquidity ratios have tended to decline, and balance sheetratios have reflected more dependence on short-term debt. In thatperspective, any recent gains in liquidity appear small.

Digitized for FRASER http://fraser.stlouisfed.org/ Federal Reserve Bank of St. Louis

In the light of the evidence of the desire to hold more NOW ac-counts and other liquid balances for precautionary rather thantransaction purposes during the months of recession, strong effortsto reduce further the growth rate of the monetary aggregates ap-peared inappropriate. Such an effort would have required morepressure on bank reserve positions—and presumably more pres-sures on the money markets and interest rates in the short run. Atthe same time, an unrestrained buildup of money and liquidityclearly would have been inconsistent with the effort to sustainprogress against inflation, both because liquidity demands couldshift quickly and because our policy intentions could easily havebeen misconstrued. Periods of velocity decline over a quarter ortwo are typically followed by periods of relatively rapid increase.Those increases tend to be particularly large during cyclical recov-eries. Indeed, velocity appears to have risen slightly during thesecond quarter, and the growth in NOW accounts has slowed.

Judgments on these seemingly technical considerations inevita-bly take on considerable importance in the target-setting processbecause the economic and financial consequences—including theconsequences for interest rates—of a particular Mi or M2 increaseare dependent on the demand for money. Over longer periods, acertain stability in velocity trends can be observed, but there is anoticeable cyclical pattern. Taking account of those normal histori-cal relationships, the various targets established at the beginningof the year were calculated to be consistent with economic recoveryin a context of declining inflation. That remains our judgmenttoday. Inflation has, in fact, receded more rapidly than anticipatedat the start of the year potentially leaving more room for realgrowth. On that basis, the targets established early in the year stillappeared broadly appropriate, and the Federal Open Market Com-mittee decided at its recent meeting not to change them at thistime.

However, the committee also felt, in the light of developmentsduring the first half, that growth around the top of those rangeswould be fully acceptable. Moreover—and I would emphasize this—growth somewhat above the targeted ranges would be tolerated fora time in circumstances in which it appeared that precautionary orliquidity motivations, during a period of economic uncertainty andturbulence, were leading to stronger than anticipated demands formoney.

We will look to a variety of factors in reaching that judgment,including such technical factors as the behavior of different compo-nents in the money supply, the growth of credit, the behavior ofbanking and financial markets, and, more broadly, the behavior ofvelocity and interest rates.

I believe it is timely for me to add that, in these circumstances,the Federal Reserve should not be expected to respond, and doesnot plan to respond, strongly to various bulges—or for that mattervalleys—in monetary growth that seem likely to be temporary. Aswe have emphasized in the past, the data are subject to a good dealof statistical noise in any circumstances, and at times when de-

Digitized for FRASER http://fraser.stlouisfed.org/ Federal Reserve Bank of St. Louis

9

mands for money and liquidity may be exceptionally volatile, morethan usual caution is necessary in responding to blips.1

We, of course, have a concrete instance at hand of a relativelylarge—and widely anticipated—jump in Mi in the first week ofJuly—possibly influenced to some degree by larger social securitypayments just before a long weekend. Following as it did a succes-sion of money supply declines, that increase brought the mostrecent level for Mi barely above the June average, and it is not ofconcern to us.

It is in this context, and in view of recent declines in short-termmarket interest rates, that the Federal Reserve yesterday reducedthe basic discount rate from 12 to \\l/z percent.

In looking ahead to 1983, the Open Market Committee agreedthat a decision at this time would—even more obviously thanusual—need to be reviewed at the start of the year in light of allthe evidence as to the behavior of velocity or money and liquiditydemand during the current year. Apart from the cyclical influencesnow at work, the possibility will need to be evaluated of a morelasting change in the trend of velocity.

The persistent rise in velocity during the past 20 years has beenaccompanied by rising inflation and interest rates—both factorsthat encourage economization of cash balances. In addition, techno-logical change in banking—spurred in considerable part by theavailability of computers—has made it technically feasible to domore and more business on a proportionately smaller cash base.With incentives strong to minimize holdings of cash balances thatbear no or low interest rates, and given the technical feasibility todo so, turnover of demand deposits has reached an annual rate ofmore than 300, quadruple the rate 10 years ago. Technologicalchange is continuing, and changes in regulation and bank practicesare likely to permit still more economization of Mi-type balances.However, lower rates of interest and inflation should moderate in-centives to exploit that technology fully. In those conditions, veloc-ity growth could slow, or conceivably at some point stop;

To conclude that the trend has, in fact, changed would clearly bepremature, but it is a matter we will want to evaluate carefully astime passes. For now, the committee felt that the existing targetsshould be tentatively retained for next year. Since we expect to bearound the top end of the ranges this year, those tentative targetswould, of course, be fully consistent with somewhat slower growthin the monetary aggregates in 1983. Such a target would be appro-priate on the assumption of a more or less normal, cyclical rise invelocity. With inflation declining, the tentative targets wouldappear consistent with, and should support, continuing recovery ata moderate pace.

1 In that connection, a number of observers have noted that the first month of a calendarquarter—most noticeably in January and April—sometimes shows an extraordinarily large in-crease in M,—amplified by the common practice of multiplying the actual change by 12 to showan annual rate. Those bulges, more typically than not, are partially washed out by slower thannormal growth the following month. The standard seasonal adjustment techniques we use tosmooth out monthly money supply variations—indeed, any standard techniques—may, in fact,be incapable of keeping up with rapidly changing patterns of financial behavior, as they affectseasonal patterns. A note attached to this statement sets forth some work in process developingnew seasonal adjustment techniques.

Digitized for FRASER http://fraser.stlouisfed.org/ Federal Reserve Bank of St. Louis

10

BLEND OF MONETARY AND FISCAL POLICY

The Congress, in adopting a budget resolution contemplating cutsin expenditures and some new revenues, also called upon the Fed-eral Reserve to "reevaluate its monetary targets in order to assurethat they are fully complementary to a new and more restrainedfiscal policy." I can report that members of the committee wel-comed the determination of the Congress to achieve greater fiscalrestraint, and I want particularly to recognize the leadership ofmembers of the Budget Committees and others in achieving thatresult. In most difficult circumstances, progress is being madetoward reducing the huge potential gap between receipts and ex-penditures. But I would be less than candid if I did not also reporta strong sense that considerably more remains to be done to bringthe deficit under control as the economy expands. The fiscal situa-tion, as we appraise it, continues to carry the implicit threat ofcrowding out business investment and housing as the economygrows—a process that would involve interest rates substantiallyhigher than would otherwise be the case. For the more immediatefuture, we recognized that the need remains to convert the inten-tions expressed in the budget resolution into concrete legislativeaction.

In commenting on the budget, I would distinguish sharply be-tween the cyclical and structural deficit—that is, the portion of thedeficit reflecting an imbalance between receipts and expenditureseven in a satisfactorily growing economy with declining inflation.To the extent the deficit turns out to be larger than contemplatedentirely because of a shortfall in economic growth, that add onwould not be a source of so much concern. But the hard fact re-mains that, if the objectives of the budget resolution are fullyreached, the deficit would be about as large in fiscal 1983 as thisyear, even as the economy expands at a rate of 4 to 5 percent ayear and inflation—and thus inflation-generated revenues—re-mains higher than members of the Open Market Committee nowexpect.

In considering the question posed by the budget resolution, theOpen Market Committee felt that full success in the budgetaryeffort should itself be a factor contributing to lower interest ratesand reduced strains in financial markets. It would thus assist im-portantly in the common effort to reduce inflationary pressures inthe context of a growing economy. By relieving concern aboutfuture financing volume and inflationary expectations, I believe, asa practial matter, a credibly firmer budget posture might permit adegree of greater flexibility in the actual short-term execution ofmonetary policy without arousing inflationary fears. Specifically,market anxiety that shortrun increases in the Ms might presagecontinuing monetization of the debt could be ameliorated. But anygains in these respects will, of course, be dependent on firmness inimplementing the intentions set forth in the resolution and on en-couraging confidence among borrowers and investors that theeffort will be sustained and reinforced in coming years.

Taking account of all these considerations, the committee did notfeel that the budgetary effort, important as it is, would in itself ap-propriately justify still greater growth in the monetary aggregates

Digitized for FRASER http://fraser.stlouisfed.org/ Federal Reserve Bank of St. Louis

11over time than I have anticipated. Indeed, excessive monetarygrowth—and perceptions thereof—would undercut any benefitsfrom the budgetary effort with respect to inflationary expectations.We believe fiscal restraint should be viewed more as an importantcomplement to appropriately disciplined monetary policy than as asubstitute.

CONCLUDING COMMENTS

In an ideal world, less exclusive reliance on monetary policy todeal with inflation would no doubt have eased the strains and highinterest rates that plague the economy and financial marketstoday. To the extent the fiscal process can now be brought morefully to bear on the problem, the better off we will be—the moreassurance we will have that interest rates will decline and keep de-clining during the period of recovery, and that we will be able tosupport the increases in investment and housing essential tohealthy, sustained recovery. Efforts in the private sector—to in-crease productivity, to reduce costs, and to avoid inflationary andjob-threatening wage increases—are also vital, even though theconnection between the actions of individual firms and workersand the performance of the economy may not always be self-evi-dent to the decisionmakers. We know progress is being made inthese areas, and more progress will hasten full and strong expan-sion.

But we also know that we do not live in an ideal world. There isstrong resistance to changing patterns of behavior and expectationsingrained over years of inflation. The slower the progress on thebudget, the more industry and labor build in cost increases in anti-cipationg of inflation or Government acts to protect markets orimpede competition, the more highly speculative financing is un-dertaken, the greater the threat that available supplies of moneyand credit will be exhausted in financing rising prices instead ofnew jobs and growth. Those in vulnerable, competitive positionsare most likely to feel the impact first and hardest, but unfortu-nately the difficulties spread over the economic landscape.

The hard fact remains that we cannot escape those dilemmas bya decision to give up the fight on inflation—by declaring the battlewon before it is. Such an approach would be transparently clear—not just to you and me— but to the investors, the businessmen, andthe workers, who would, once again, find their suspicions con-firmed that they had better prepare to live with inflation and tryto keep ahead of it. The reactions in financial markets and othersectors of the economy would, in the end, aggravate our problems,not eliminate them. It would strike me as the cruelest blow of allto the millions who have felt the pain of recession directly to sug-gest, in effect, it was all in vain.

I recognize months of recession and high interest rates have con-tributed to a sense of uncertainty. Businesses have postponed in-vestment plans. Financial pressures have exposed lax practices andstretched balance-sheet positions in some institutions—financial aswell as nonfinancial. The earnings position of the thrift industryremains poor.

Digitized for FRASER http://fraser.stlouisfed.org/ Federal Reserve Bank of St. Louis

12

But none of those problems can be dealt with successfully byreinflation or by a lack of individual discipline. It is precisely thatenvironment that contributed so much to the current difficulties.

In contrast, we are now seeing new attitudes of cost containmentand productivity growth—and ultimately our industry will be in amore robust competitive position. Millions are benefiting from lessrapid price increases—or acutally lower prices—at their shoppingcenters and elsewhere. Consumer spending appears to be movingahead and inventory reductions help set the stage for productionincreases.

Those are developments that should help recovery get firmly un-derway. The process of disinflation has enough momentum to besustained during the early stages of recovery—and that success canbreed further success as concerns about inflation recede. As recov-ery starts, the cash flow of business should improve. And, moreconfidence should encourage greater willingness among investorsto purchase longer debt maturities. Those factors should, in turn,work toward reducing interest rates, and sustaining them at lowerlevels, encouraging in turn the revival of investment and housingwe want.

I have indicated the Federal Reserve is sensitive to the specialliquidity pressures that could develop during the current period ofuncertainty.

Moreover, the basic solidity of our financial system is back-stopped by a strong structure of governmental institutions precise-ly designed to cope with the secondary effects of isolated failures.The recent problems related largely to the speculative activities ofa few highly leveraged firms can and will be contained. And overtime, an appropriate sense of prudence in taking risks will serve uswell.

We have been through—we are in—a trying period. But toomuch has been accomplished not to move ahead and complete thejob of laying the groundwork for a much stronger economy. As welook forward, not just to the next few months but to long years, therewards will be great: In renewed stability, in growth, and inhigher employment and standards of living.

That vision will not be accomplished by monetary policy alone.But we mean to do our part.[Additional material received from the Federal Reserve Board

follows:]

TABLE I.—TARGETED AND ACTUAL GROWTH OF MONEY AND BANK CREDIT[Percent changes, at seasonally adjusted annual rates]

Actual growth

Digitized for FRASER http://fraser.stlouisfed.org/ Federal Reserve Bank of St. Louis

13

APPENDIX—ALTERNATIVE SEASONAL ADJUSTMENT PROCEDURE

For some time the Federal Reserve has been investigating ways to improve itsprocedures for seasonal adjustment, particularly as they apply to the monetary ag-gregates. In June of last year, a group of prominent outside experts, asked by theBoard to examine seasonal adjustment techniques, submitted their recommenda-tions.1 The committee suggested, among other things, that the Board's staff developseasonal factor estimates from a model-based procedure as an alternative to thewidely used X-ll technique that provides the basis for the current seasonal adjust-ment procedure,^ and release the results.

The Board staff has been developing a procedure using statistical models tailoredto each individual series.n The table on the last page compares monthly and quar-terly average growth rates for the current Mi series with those of an alternativeseries from the model-based approach.

Differences in seasonal adjustment techniques do not change the trend in mone-tary growth, but, as may be seen in the table, they do alter month-to-month growthrates owing to differing estimates of the distribution over time of the seasonal com-ponent in money behavior. Shortrun money growth is variable under both the alter-native and current techniques of seasonal adjustment, illustrating the inherently-large "noise" component of the series. However, the redistribution of the seasonalcomponent under the alternative technique does on average tend to moderatemonth-to-rnonth changes somewhat.

The Board will continue to publish seasonally adjusted estimates for Mi on bothcurrent and alternative bases at least until the annual review of seasonal factors in1988. A detailed description of the alternative method will be available shortly.

GROWTH RATES OF M, USING CURRENT1 AND ALTERNATIVE2 SEASONAL ADJUSTMENTPROCEDURES

1981

1982

' See Committee of Experts on Seasonal Adjustment Techniques, Seasonal Adjustment of theMonetary Aggregates (Board of Governors of the Federal Reserve System, October 1981).

2 The current seasonal adjustment technique has most recently been summarized in the de-scription to the mimeograph release of historical money stock data dated March 1982. Detaileddescriptions of the X-ll program and variants can be obtained from technical paper No. 15 ofthe U.S. Department of Commerce (revised February I9B7i and from the report to the Boardcited in footnote 1.

-1 The model-based seasonal adjustment procedures currently under review by the Board staffuse methods based on the well-developed theory of statistical regression and time series model-ing. These approaches allow development of seasonal factors that are more sensitive than thecurrent Factors to unique characteristics of each series, including, for example, fixed and evolv-ing seasonal patterns, trading day effects, within-month seasonal variations, holiday effects, out-lier adjustments, special events adjustments (such as the 1980 credit controls experience), andserially correlated noise components.

Digitized for FRASER http://fraser.stlouisfed.org/ Federal Reserve Bank of St. Louis

14

GROWTH RATES OF Mi USING CURRENT' AND ALTERNATIVEa SEASONAL ADJUSTMENTPROCEDURES—Continued

[Monthly ai'e'iige percenl annual ra tes ]

June . . 16

BOARD OF GOVERNORS OF THE FEDERAL RESERVE SYSTEM—MIDYEAR MONETARY POLICYREPORT TO CONGRESS PURSUANT TO THE FULL EMPLOYMENT AND BALANCEDGROWTH ACT OF 1978

BOARD OF GOVERNORS OF THEFEDERAL RESERVE SYSTEM,

Washington. D.C., July JO, W8J.The PRESIDENT OF THE SENATE,The SPEAKER OF THE HOUSE OF REPRESENTATIVES,Washington. D.C.

The Board of Governors is pleased to submit its Midyear Monetary Policy Reportto the Congress pursuant to the Full Employment and Balanced Growth Act of 1978.

Sincerely,PAUL A. VOLCKER, Chairman.

SECTION l: THE PERFORMANCE OF THE ECONOMY IN THE FIRST HALF OF 1982

The contraction in economic activity that began in mid-1981 continued into thefirst half of 1982, although at a diminished pace. Declines in production and employ-ment slowed, while sales of automobiles improved. Real GNP fell at a 4 percentannual rate between the third quarter of 1981 and the first quarter of 1982. Withoutput declining, the margin of unused plant capacity widened and the unemploy-ment rate rose to a postwar record.

By mid-1982, however, the recession seemed to be drawing to a close. Inventorypositions had improved substantially, homebuilding was beginning to revive, andconsumer spending appeared to be rising. Nonetheless, there were signs of increasedweakness in business investment. Although final demands apparently fell duringthe second quarter, the rate of inventory liquidation slowed, and on balance, realGNP apparently changed little. If, in fact, this spring or early summer is deter-mined to have been the cyclical trough, both the depth and duration of the declinein activity will have been about the same as in other postwar recessions.

The progress in reducing inflation that began during 1981 continued in the firsthalf of 1982. The greatest improvement was in prices of food and energy—whichbenefited from favorable supply conditions—but increases in price measures that ex-clude these volatile items also have slowed markedly. Moreover, increases in em-ployment costs, which carry forward the momentum of inflation, have diminishedconsiderably. Not only have wage increases eased for union workers in hardpressedindustries as a result of contract concessions, but wage and fringe benefit increasesalso have slowed for non-union and white-collar workers in a broad range of indus-tries. In addition there has been increasing use of negotiated work-rule changes as

Digitized for FRASER http://fraser.stlouisfed.org/ Federal Reserve Bank of St. Louis

15

well as other efforts by business to enhance productivity and trim costs. At thesame time, purchasing power has been rising; real compensation per hour increased1 percent during 1981 and rose at about a 3 percent annual rate over the first halfof 1982.

Digitized for FRASER http://fraser.stlouisfed.org/ Federal Reserve Bank of St. Louis

16

Industrial ProductionIndex, 1967= 100

150

140

130

1978 1980 1982

Real GNP

1972 Dollars

Change from end of previous period, annual rale, percent

nr

1978HI H2 HI

1980 1982

Gross Business Product PricesChange (com end ol previous period, annual rate, percent

Fixed-weighted Index

1978

Note Dala lor 19S2 H1 are partially estimated by the FRB

H1 H2 Ml1980 1982

Digitized for FRASER http://fraser.stlouisfed.org/ Federal Reserve Bank of St. Louis

17

Interest ratesAs the recession developed in the autumn of 1981, short-term interest rates moved

down substantially. However, part of this decline was retraced at the turn of theyear as the demand for money bulged and reserve positions tightened. After themiddle of the first quarter, short-term rates fluctuated but generally trended down-ward, as money—particularly the narrow measure, Mi—grew slowly on average andthe weakness in economic activity continued. In mid-July, short-term rates were dis-tinctly below the peak levels reached in 1980 and 1981. Nonetheless, short-termrates were still quite high relative to the rate of inflation.

Long-term interest rates also remained high during the first half of 1982. In part,this reflected doubts by market participants that the improved price performancewould be sustained over the longer run. This skepticism was related to the fact that,during the past two decades, episodes of reduced inflation have been short-lived, fol-lowed by reacceleration to even faster rates of price increase. High long-term ratesalso have been fostered by the prospect of huge deficits in the federal budget evenas the economy recovers. Fears of deepening deficits have affected expectations offuture credit market pressures, and perhaps also have sustained inflation expecta-tions. The resolution on the 1983 fiscal year budget that was adopted by the Con-gress represents a beginning effort to deal with the prospect of widening deficits;and the passage of implementing legislation should work in the direction of reduc-ing market pressures on interest rates.

Digitized for FRASER http://fraser.stlouisfed.org/ Federal Reserve Bank of St. Louis

18

Interest RatesPercent

— 6

1978 1980 1982

Funds Raised by Private Nonfinancial SectorsSeasonally adjusted, annual rate, billions of dollars

300

200

1980 1982

Federal Government BorrowingSeasonally ad|usted, annual rate, billions of dollars

Combined Deficit Financed by the Public

120

80

40

1978 1980

Note Data for 19B2 H1 are partially estimated by the FHB

1982

Digitized for FRASER http://fraser.stlouisfed.org/ Federal Reserve Bank of St. Louis

19

Domestic credit flowsAggregate credit flows to private non-financial borrowers increased somewhat in

the first half of 1982 from the reduced pace in the second half of 1981, according tovery preliminary estimates. Business borrowing rose while households reduced fur-ther their use of credit. Borrowing by the federal government increased sharply inlate 1981, after the 5 percent cut in personal income tax rates, and remained nearthe new higher level during the first half of 1982 on a seasonally adjusted basis.Reflecting uncertainties about the future economic and financial environment, bothlenders and borrowers have shown a strong preference for short-term instruments.

Much of the slackening in credit flows to nonfinancial sectors in the last part of1981 was accounted for by households, particularly by household mortgage borrow-ing. Since then, mortgage credit flows have picked up slightly. The advance was en-couraged in part by the gradual decline in mortgage rates from the peaks of lastfall. In addition, households have made widespread use of adjustable-rate mortgagesand "creative" financing techniques—including relatively short-term loans made bysellers at below-market interest rates and builder "buy-downs." About two-fifths ofall conventional mortgage loans closed recently were adjustable-rate instruments,and nearly three-fourths of existing home transactions reportedly involved somesort of creative financing.

Business borrowing dropped sharply during the last quarter of 1981, primarily re-flecting reduced inventory financing needs. However, credit use by nonfinancial cor-porations rose significantly in the first half of 1982, despite a further drop in capitalexpenditures. The high level of bond rates has discouraged corporations from issu-ing long-term debt, and a relatively large share of business borrowing this year hasbeen accomplished in short-term markets—at banks and through sales of commer-cial paper. The persistently large volume of business borrowing suggests an accumu-lation of liquid assets as well as an intensification of financial pressures on at leastsome firms. Signs of corporate stress continue to mount, including increasing num-bers of dividend reductions or suspensions, a rising fraction of business loans atcommercial banks with interest or principal past due, and relatively frequent down-gradings of credit ratings.

After raising a record volume of funds in U.S. credit markets in 1981, the federalgovernment continued to borrow at an extraordinary pace during the first half of1982, as receipts (national income and product accounts basis) fell while expendi-tures continued to rise. Owing to the second phase of the tax cut that went intoeffect on July 1 and the effects on tax revenues of the recession and reduced infla-tion, federal credit demands will expand further in the period ahead.

ConsumptionPersonal consumption expenditures (adjusted for inflation) fell sharply in the

fourth quarter of 1981, but turned up early in 1982 and apparently strengthenedfurther during the second quarter. The weakness in consumer outlays during thefourth quarter was concentrated in the auto sector, as total sales fell to an annualrate of 7.4 million units—the lowest quarterly figure in more than a decade—andsales of domestic models plummeted to a 5.1 million unit rate.

Digitized for FRASER http://fraser.stlouisfed.org/ Federal Reserve Bank of St. Louis

20

Real Income and ConsumptionChange Irom end ol previous period, annual rate, percent

[T|] Real Disposable Personal Income

P~] Real Personal Consumption Expenditures

1978HI H2 M1

1980 1982

Real Business Fixed InvestmentChange from end of previous period, annual rate, percent

Producers' Durable Equipment

Structures' 20

10

1978

Total Private Housing Starts

H1 H2 H11980 1982

Millions ot units

2.0

1.5

1.0

1978 1980

Note; Data for 1 962 HI are partially estimated by trie FAB

1982

Digitized for FRASER http://fraser.stlouisfed.org/ Federal Reserve Bank of St. Louis

21

Price rebates and other sales promotion programs during the early months of1982 provided a fillip to auto demand, and sales climbed to an 8.1 million unit rate.Auto markets remained firm into the spring, boosted in part by various purchaseincentives. But as has generally occurred when major promotions have ended, autopurchases fell sharply in June. Outside the auto sector, retail sales at most types ofstores were up significantly for the second quarter as a whole. Even purchases atfurniture and appliance outlets, which had been on a downtrend since last autumn,increased during the spring.

Real after-tax income has continued to edge up, despite the sharp drop in outputduring the recession. The advance reflects not only typical cyclical increases intransfer payments but also the reduction in personal income tax rates on October 1.Households initially saved a sizable proportion of the tax cut, boosting the personalsaving rate from SVi percent in mid-1981—about equal to the average of the late1970s and early 1980s—to 6,1 percent in the fourth quarter of 1981. During early1982, however, consumers increased spending, partly to take advantage of pricemarkdowns for autos and apparel, and the saving rate fell.Business investment

As typically occurs during a recession, the contraction in business fixed invest-ment has lagged behind the decline in overall activity. Indeed, even though realGNP dropped substantially during the first quarter of 1982, real spending for fixedbusiness capital actually rose a bit. An especially buoyant element of the invest-ment sector has been outlays for nonfarm buildings—most notably, commercialoffice buildings, for which appropriations and contracts often are set a year or morein advance.

In contrast to investment in structures, business spending for new equipmentshowed little advance during 1981 and weakened considerably in the first half of1982. Excluding business purchases of new cars, which also were buoyed by rebateprograms, real investment in producers' durable equipment fell at a 2 percentannual rate in the first quarter. The decline evidently accelerated in the secondquarter. In April and May, shipments of nondefense capital goods, which accountfor about 80 percent of the spending on producers' durable equipment, averagednearly 3 percent below the first-quarter level in nominal terms. Moreover, sales ofheavy trucks dropped during the second quarter to a level more than 20 percentbelow the already depressed first-quarter average.

Businesses liquidated inventories at a rapid rate during late 1981 and in the firsthalf of 1982. The adjustment of stocks followed a sizable buildup during the summerand autumn of last year that accompanied the contraction of sales. The most promi-nent inventory overhang by the end of 1981 was in the automobile sector as salesfell precipitously. However, with a combination of production cutbacks and salespromotions, the days' supply of unsold cars on dealers lots had improved consider-ably by spring.

Manufacturers and non-auto retailers also found their inventories rising rapidlylast autumn. Since then, manufacturers as a whole have liquidated the accumula-tion that occurred during 1981, although some problem areas still exist—particular-ly in primary metals. Stocks held by non-auto retailers have been brought downfrom their cyclical peak, but they remain above pre-recession levels.Residential construction

Housing activity thus far in 1982 has picked up somewhat from the depressedlevel in late 1981. Housing starts during the first five months of 1982 were up 10percent on average from the fourth quarter of 1981, The improvement in homebuild-ing has been supported by strong underlying demand for housing services in mostmarkets and by the continued adaptation of real estate market participants to non-traditional financing techniques that facilitate transactions.

The turnaround in housing activity has not occurred in all areas of the country.In the south, home sales increased sharply in the first part of 1982, and housingstarts rose 25 percent from the fourth quarter of 1981. In contrast, housing startsdeclined further, on average, during the first five months of 1982 in both the westand the industrial north central states.Government

Federal government purchases of goods and services, measured in constant dol-lars, declined over the first half of 1982. The decrease occurred entirely in the non-defense area, primarily reflecting a sharp drop in the rate of inventory accumula-tion by the Commodity Credit Corporation during the spring quarter. Purchases bythe Commodity Credit Corporation had reached record levels during the previoustwo quarters owing to last summer's large harvests and weak farm prices. Other

Digitized for FRASER http://fraser.stlouisfed.org/ Federal Reserve Bank of St. Louis

22

nondefense outlays fell slightly over the first half of the year as a result of cuts inemployment and other expenditures under many programs. Real defense spendingapparently rose over the First half of the year, and the backlog of unfilled ordersgrew further. The federal deficit on a national income and product account basiswidened from $100 billion at the end of 1981 to about $130 billion during the springof this year. Much of this increase in the deficit reflects the effects of the recessionon federal expenditures and receipts.

At the state and local goverment level, real purchases of goods and services fellfurther over the first half of 1982 after having declined 2 percent during 1981. Mostof the weakness this year has been in construction outlays as employment levelshave stabilized after large reductions in the federally funded CETA program led tosizable layoffs last year. The declines in state and local government activity in partreflect fiscal strains associated with the withdrawal of federal support for many ac-tivities and the effects of cyclically sluggish income growth on tax receipts. Becauseof the serious revenue problems, several states have increased sales taxes and excisetaxes on gasoline and alcohol.

International payments and tradeThe weighted-average value of the dollar, after declining about 10 percent from

its peak last August, began to strengthen sharply again around the beginning of theyear and since then has appreciated nearly 15 percent on balance. The appreciationof the dollar has been associated to a considerable extent with the declining infla-tion rate in the United States and the rise in dollar interest rates relative to yieldson assets denominated in foreign currencies..

Digitized for FRASER http://fraser.stlouisfed.org/ Federal Reserve Bank of St. Louis

23

Foreign Exchange Value of the U.S. DollarIndex, March 1973 = 100

— 110

— 100

— 90

— 80

1978 1980

Current Account Balance

T982

Annual rate, billions o( dollars

10

20

1978 1980

Note Dala for 1982 H1 are partially estimalea Oy the FRB

1982

Digitized for FRASER http://fraser.stlouisfed.org/ Federal Reserve Bank of St. Louis

24

Reflecting the effects of the strengthening dollar, as well as the slowing of eco-nomic growth abroad, real exports of goods and services have been decreasing sincethe beginning of 1981. The volume of imports other than oil, which rose fairly stead-ily throughout last year, dropped sharply in the first half of 1982, owing to theweakness of aggregate demand—especially for inventories—in the United States. Inaddition, both the volume and price of imported oil fell during the first half of theyear. The current account, which was in surplus for 1981 as a whole, recorded an-other surplus in the first half of this year as the value of imports fell more than thevalue of exports.

Labor marketsEmployment has declined by nearly IVa million since the peak reached in mid-

1981. As usually happens during a cyclical contraction, the largest job losses havebeen in durable goods manufacturing industries—such as autos, steel, and machin-ery—as well as at construction sites. The job losses in manufacturing and construc-tion during this recession follow a limited recovery from the 1980 recession; as aresult, employment levels in these industries are more than 10 percent below their1979 highs. In addition, declines in aggregate demand have tempered the pace ofhiring at service industries and trade establishments over the past year. As oftenhappens near a business cycle trough, employment fell faster than output in early1982 and labor productivity showed a small advance after declining sharply duringthe last half of 1981.

Since mid-1981 there has been a 21/* percentage point rise in the overall unem-ployment rate to a postwar record high of 9 Vz percent. The effects of the recessionhave been most severe in the durable goods and construction industries, and theburden of rising unemployment has been relatively heavy on adult men, who tendto be more concentrated in these industries. At the same time, joblessness amongyoung and inexperienced workers remains extremely high; hardest hit have beenblack male teenagers who experienced an unemployment rate of nearly 60 percentin June 1982.

Reflecting the persistent slack in labor markets, most indicators of labor supplyalso show a significant weakening. For example, the number of discouraged work-ers—that is, persons who report that they want work but are not looking for jobsbecause they believe they cannot find any—has increased by nearly half a millionover the past year, continuing an upward trend that began before the 1980 reces-sion. In addition, the labor force participation rate—the proportion of the working-age population that is employed or actively seeking jobs—has been essentially flatfor the last two years after rising about one-half percentage point annually between1975 and 1979.

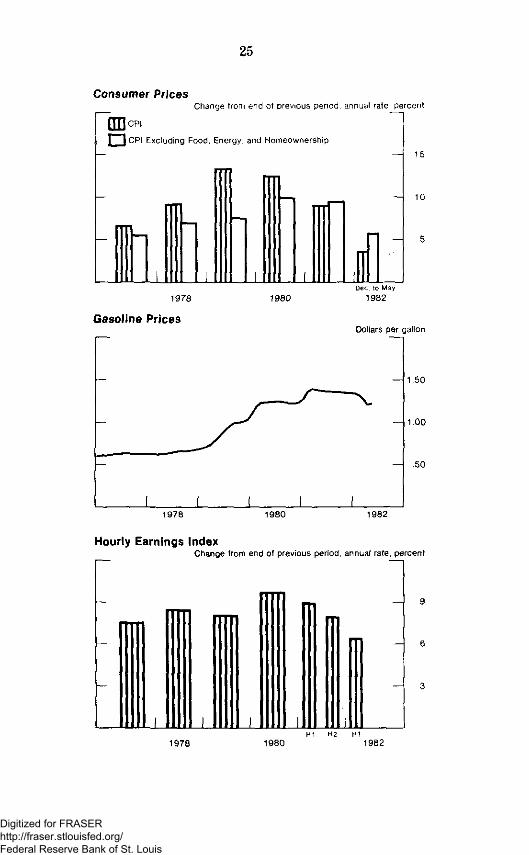

Prices and labor costsA slowing in the pace of inflation, which was evident during 1981, continued

through the first half of this year. During the first five months of 1982 (the latestdata available), the consumer price index increased at an annual rate of 3.5 percent,sharply lower than the 8.9 percent rise during 1981. Much of the improvement wasin energy and food prices as well as in the volatile CPI measure of homeownershipcosts. But even excluding these items, the annual rate of increase in consumerprices has slowed to 5Va percent this year compared with a 9J/2 percent rise lastyear. The moderation of price increases also was evident at the producer level.Prices of capital equipment have increased at a 4V4 percent annual rate thus farthis year—well below the 9'A percent pace of 1981. In addition, the decline in rawmaterials prices, which occurred throughout last year, has continued in the firsthalf of 1982.

Digitized for FRASER http://fraser.stlouisfed.org/ Federal Reserve Bank of St. Louis

25

Consumer PricesChange from end Of previous period, annual rate, percenl

Excluding Food, Energy, and Horneownership

15

10

1976

Gasoline Prices

1930

Dec to May1982

Dollars per gallon

1.50

1.00

.50

1978 1980 1982

Hourly Earnings IndexChange from end of previous period, annual rate, percent

1978H1 H2 H1

1980 1982

Digitized for FRASER http://fraser.stlouisfed.org/ Federal Reserve Bank of St. Louis

Gasoline prices at the retail level, which had remained virtually flat over thesecond half of 1981, fell substantially during the first four months of 1982. Slackdomestic demand and an overhang of stocks on world petroleum markets precipitat-ed the decline in prices. However, gasoline prices began to rise again in May in re-flection of rising consumption, reduced stocks, and lower production schedules bymajor crude oil suppliers.

The rate of increase in employment costs decelerated considerably during the firsthalf of 1982. The index of average hourly earnings, a measure of wage trends forproduction and nonsupervisory personnel, rose at a ti'/4 percent annual rate over thefirst half of this year, compared with an increase of 8'A percent during 1981. Part ofthe slowing was due to early negotiation of expiring contracts and renegotiation ofexisting contracts in a number of major industries. These wage concessions are ex-pected to relieve cost pressures and to enhance the competitive position of firms inthese industries. Increases in fringe benefits, which generally have risen faster thanwages over the years, also are being scaled back. Because wage demands, not tomention direct escalator provisions, are responsive to price performance, the prog-ress made in reducing the rate of inflation should contribute to further moderationin labor cost pressures.

SECTION 2: THE GKOWTH OF MONEY AND CREDIT IN THE FIRST HALF OF 1982

The annual targets for the monetary aggregates announced in February werechosen to be consistent with continued restraint on the growth of money and creditin order to exert sustained downward pressure on inllation. At the same time, thesetargets were expected to result in sufficient money growth to support an upturn ineconomic activity. Measured from the fourth quarter of 1981 to the fourth quarterof 1982, the growth ranges for the aggregates adopted by the Federal Open MarketCommittee (FOMCl were as follows: for M>, 2Va to f>Va percent; for M2, ti to 9 per-cent; and for M;i, fi'/a to 9'/a percent. The corresponding range specified by theFOMC for bank credit was 6 to 9 percent.l

When the FOMC was deliberating on its annual targets in February, the Commit-tee was aware that Mi already had risen well above its average level in the fourthquarter of 1981, In light of the financial and economic backdrop against which thebulge in Mi had occurred, the Committee believed it likely that there had been anupsurge in the public's demand Cor liquidity. It also seemed probable that thisstrengthening of money demand would unwind in the months ahead. Thus, underthese circumstances and given the relatively low base for the M! range for 1982, itdid not appear appropriate to seek an abrupt return to the annual target range, andthe FOMC indicated its willingness to permit Mi to remain above the range for awhile. At the same time, the FOMC agreed that the expansion in M, for the year asa whole might appropriately be in the upper part of its range, particularly if availa-ble evidence suggested the persistence of unusual desires for liquidity that had to beaccommodated to avoid undue financial stringency.

In setting the annual target for Ma, the FOMC indicated that Mj growth for theyear as a whole probably would be in the upper part of its annual range and mightslightly exceed the upper limit. The Committee anticipated that demands for theassets included in M2 might be enhanced by new tax incentives such as the broad-ened eligibility for IRA/Keogh accounts, or by further deregulation of deposit rates.The Committee expected that M5 growth again would be influenced importantly bythe pattern of business financing and, in particular, by the degree to which borrow-ing would be focused in markets for short-term credit.

As anticipated—and consistent with the FOMC's short-run targets—the surge inM, growth in December and January was followed by appreciably slower growth.After January, M, increased at an annual rate of only 1'4 percent on average, andthe level of Mi in June was only slightly above the upper end of the Committee'sannual growth range. From the fourth quarter of 1981 to June, Mi increased at a5.6 percent annual rate. M2 growth so far this year also has run a bit above theFOMC's annual range; from the fourth quarter of 1981 through June, M^ increasedon average at a 9.4 percent annual rate. From a somewhat longer perspective,Mi has increased at a 4.7 percent annual rate, measuring growth from the first halfof 1981 to the first half of 1982 and abstracting from the shift into NOW accounts in11*81; and M2 has grown at. a 9.7 percent annual rate on a half-year over half-yearbasis.

1 Because of the authorization of international banking facil i t ies iIBF's) on Dec. .'!, 11181. thebank credit data starting in December litHl are not comparable with earlier data. The target forbank credit was put in terms of annual ized growth measured from the average of December1!)81 and January !f)S2 to the average level in the fourth quarter of 1982 so that the shift ofassets to IBF's that occurred at the tu rn of the year would not have a major impact on thepattern of growth.

Digitized for FRASER http://fraser.stlouisfed.org/ Federal Reserve Bank of St. Louis

27

Ranges and Actual Monetary Growth

M1Billions ot dollars

Range adopted by FOMC for1981 04 to 1982 Q4

450

Annual Rates of Growth

1981 Q4 to June5.6 Percent

1981 04 to 1982 Q26.8 Percent

1981 H1 to 1962 H14 7 Percent'

1981 1982

M2

Range adopted by FOMC lor1981 Q4 to 1982 Q4

l p-LL.

Billions of dollars

I960

1900

185O

1800

Annual Rates of Growth

1981 04 to June9.4 Percent

1981 Q4 to 1982 O29.7 Percent

1981 H1 to 1962 H19.7 Percent

1981 1982

Digitized for FRASER http://fraser.stlouisfed.org/ Federal Reserve Bank of St. Louis

28

Although Mi growth has been moderate on balance thus far this year, thatgrowth has considerably exceeded the pace of increase in nominal GNP. Indeed, thefirst-quarter decline in the income velocity of Mi—that is, GNP divided by M,—wasextraordinarily sharp. Similarly, the velocity of the broader aggregates has been un-usually weak. Given the persistence of high interest rates, this pattern of velocitybehavior suggests a heightened demand for M, and M? over the first half.

The unusual demand for Mt has been focused on its NOW account component.Following the nationwide authorization of NOW accounts at the beginning of 1981,the growth of such deposits surged. When the aggregate targets were reviewed thispast February, a variety of evidence indicated that the major shift from convention-al checking and savings accounts into NOW accounts was over; in particular, therate at which new accounts were being opened had dropped off considerably. As aresult of that shift, however, NOW accounts and other interest-bearing checkabledeposits had grown to account for almost 20 percent of M, by the beginning of 1982.Subsequently, it has become increasingly apparent that Mi is more sensitive tochanges in the public's desire to hold highly liquid assets.

Mi is intended to be a measure of money balances held primarily for transactionpurposes. However, in contrast to the other major components of Mi—currency andconventional checking accounts—NOW accounts also have some characteristics oftraditional savings accounts. Apparently reflecting precautionary motives to a con-siderable degree, NOW accounts and other interest-bearing checkable deposits grewsurprisingly rapidly in the fourth quarter of last year and the first quarter of thisyear. Although growth in this component has slowed recently, its growth from thefourth quarter of last year to June has been 80 percent at an annual rate. The othercomponents of M, increased at an annual rate of less than 1 percent over this sameperiod.

Looking at the components of M3 not also included in M,, the so-called nontran-saction components, these items grew at a 10% percent annual rate from the fourthquarter to June. General purpose and broker/dealer money market mutual fundswere an especially strong component of M2, increasing at almost a 30 percentannual rate this year. Compared with last year, however, when the assets of suchmoney funds more than doubled, this year's increase represents a sharp decelera-tion.

Perhaps the most surprising development affecting M2 has been the behavior ofconventional savings deposits. After declining in each of the past four years—falling16 percent last year—savings deposits have increased at about a 4 percent annualrate thus far this year. This turnaround in savings deposit flows, taken togetherwith the strong increase in NOW accounts and the still substantial growth inmoney funds, suggests that stronger preferences to hold safe and highly liquid fi-nancial assets in the current recessionary environment are bolstering the demandfor M2 as well as M,.

Digitized for FRASER http://fraser.stlouisfed.org/ Federal Reserve Bank of St. Louis

29

Ranges and Actual Monetary Growth

dollars

2300

— 2200

Annual Rates of Growth

'981 O4 to June9.7 Percent

1981 O4 to 1982 Q29.8 Percent

1981 H1 to 1982 H110 5 Percent

1982

Bank Credit

Range adopted by FOMC torDec 1981-Jan 1982 to 1982 Q4

Billions of dollars

Annual Rates ot Growth

1982

Digitized for FRASER http://fraser.stlouisfed.org/ Federal Reserve Bank of St. Louis

30

M3 increased at a 9.7 annual rate from the fourth quarter of 1981 to June, justabove the upper end of the FOMC's annual growth target. Early in the year, M3growth was relatively moderate as a strong rise in large denomination CDs wasoffset by declines in term RPs and in money market mutual, funds restricted to in-stitutional investors. During the second quarter, however, M3 showed a larger in-crease; the weakness in its term RP and money fund components subsided andheavy issuance of large CDs continued. With growth of "core deposits" relativelyweak on average, commercial banks borrowed heavily in the form of large CDs tofund the increase in their loans and investments.